NATIONAL GRID Market Evolution in Ireland APEX 2004 Annual Conference Ann Scully Manager, Market Operations ESB National Grid

NATIONAL GRID Market Evolution in Ireland APEX 2004 Annual Conference Ann Scully Manager, Market Operations ESB National Grid.

Dec 23, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

NATIONAL GRID

Market Evolution in Ireland

APEX 2004 Annual Conference

Ann Scully

Manager, Market OperationsESB National Grid

NATIONAL GRID

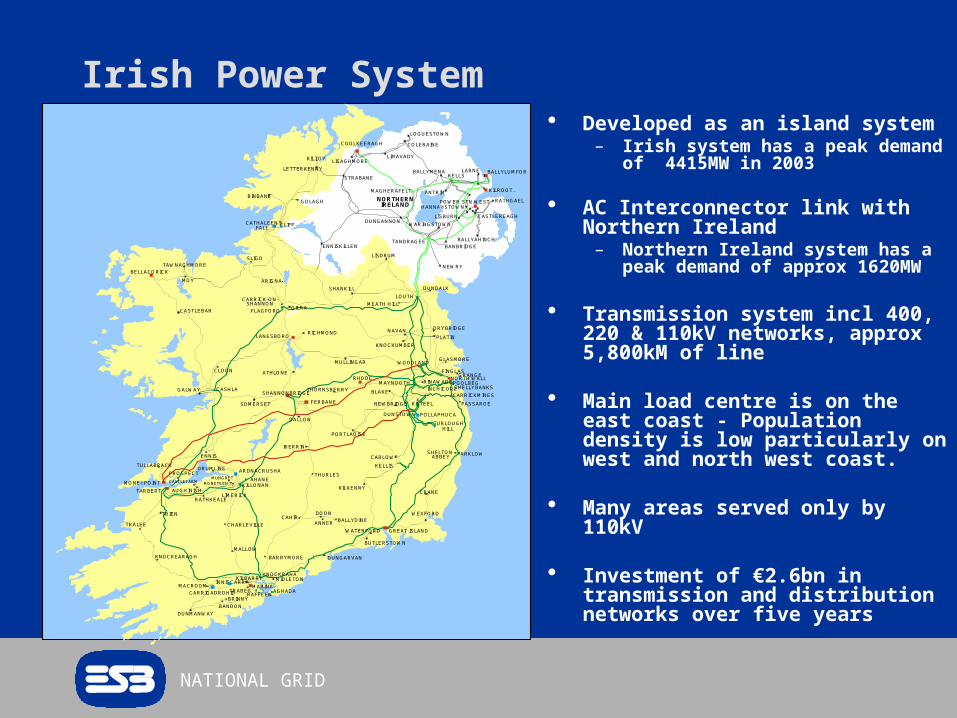

Irish Power System Developed as an island system

– Irish system has a peak demand of 4415MW in 2003

AC Interconnector link with Northern Ireland

– Northern Ireland system has a peak demand of approx 1620MW

Transmission system incl 400, 220 & 110kV networks, approx 5,800kM of line

Main load centre is on the east coast - Population density is low particularly on west and north west coast.

Many areas served only by 110kV

Investment of €2.6bn in transmission and distribution networks over five years

NORTHERNIRELAND

TARBERT

DUNMANWAY

RAFFEEN

CARRICK-ON-SHANNON

TURLOUGHHILL

CARRICKMINES

FASSAROE

MOY

TAWNAGHMORE

CAHIR

CLOON

GILRA

BLAKE

WOODLAND

MUNGRET

LIMERICK

BUTLERSTOWN

WATERFORD

FLAGFORD

GALWAY

GRANGEFINGLAS

INCHICORE

NORTH WALLPOOLBEGSHELLYBANKS

MAYNOOTH

CARLOWSHELTON

ABBEY

DUNSTOWN

KILTEELNEWBRIDGE

ANNER

BANDON

MACROOM

CARRIGADROHID

KILBARRYINNISCARRA

TRABEGMARINA

TRALEE

MONETEEN

RATHKEALE

CASTLEFARM

AUGHINISH

DRUMLINE

ENNIS

MONEYPOINT

TULLABRACK

DALLOW

PORTLAOISE

KILKENNY

IKERRIN

KILTOY

LETTERKENNY

STRABANE

BELLACORICK

LOUTH

SHANKILL

NAVAN

KNOCKUMBER

MULLINGAR

ATHLONE

LANESBORO

KNOCKRAHA

RINAWADE

CATHALEEN'SFALL

ENNISKILLEN

CLIFF

SLIGO

DUNGARVAN

CASTLEBAR

RICHMONDPLATIN

GLASMORE

ARKLOW

CRANE

WEXFORD

THURLES

DOONBALLYDINE

GREAT ISLAND

BARRYMORE

MALLOW

KNOCKEARAGH

KILLONAN

BRINNY

TANDRAGEE

LISDRUM

DUNDALK

FERBANE

SHANNONBRIDGECASHLA

MIDLETON

CHARLEVILLE

POLLAPHUCA

AHANE

DRYBRIDGE

RHODE

PROSPECT

TRIEN

AGHADA

ARDNACRUSHA

SOMERSET

BINBANE

ARIGNA

GOLAGH

MEATH HILL

THORNSBERRY

KELLIS

BANBRIDGE

NEWRY

BALLYAHINCH

WARINGSTOWN

MAGHERAFELT

DUNGANNON

ANTRIM

LOGUESTOWN

COLERAINE

LIMAVADY

COOLKEERAGH

LISAGHMORE

BALLYMENAKELLS

LARNE BALLYLUMFOR

KILROOT.

RATHGAEL

CASTLEREAGH

POWER STN WESTHANNAHSTOWN

LISBURN

NATIONAL GRID

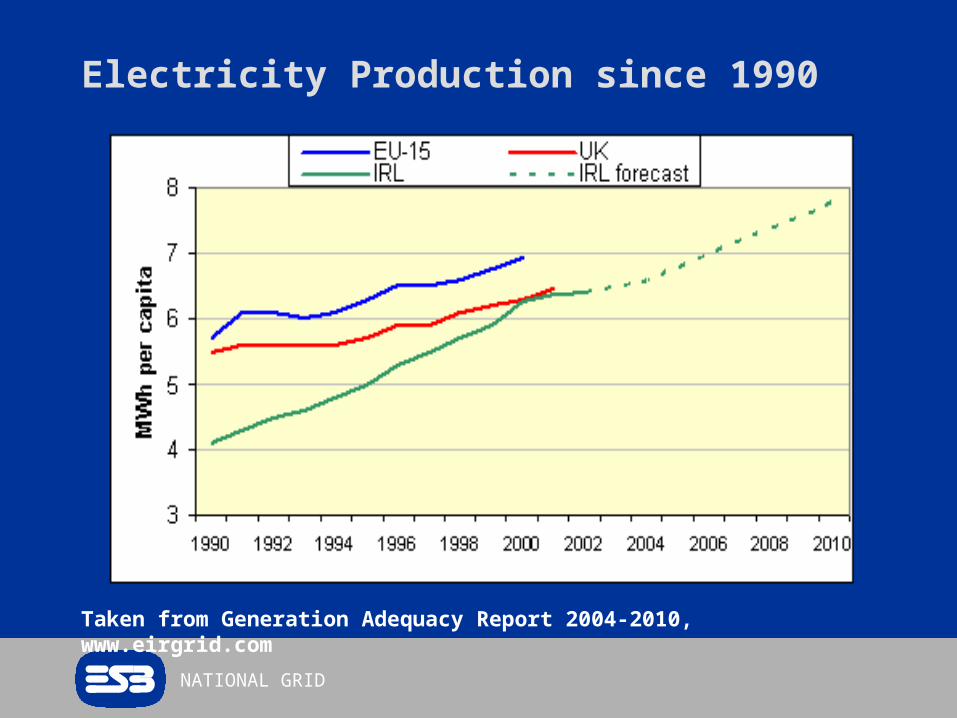

Electricity Production since 1990

Taken from Generation Adequacy Report 2004-2010, www.eirgrid.com

NATIONAL GRID

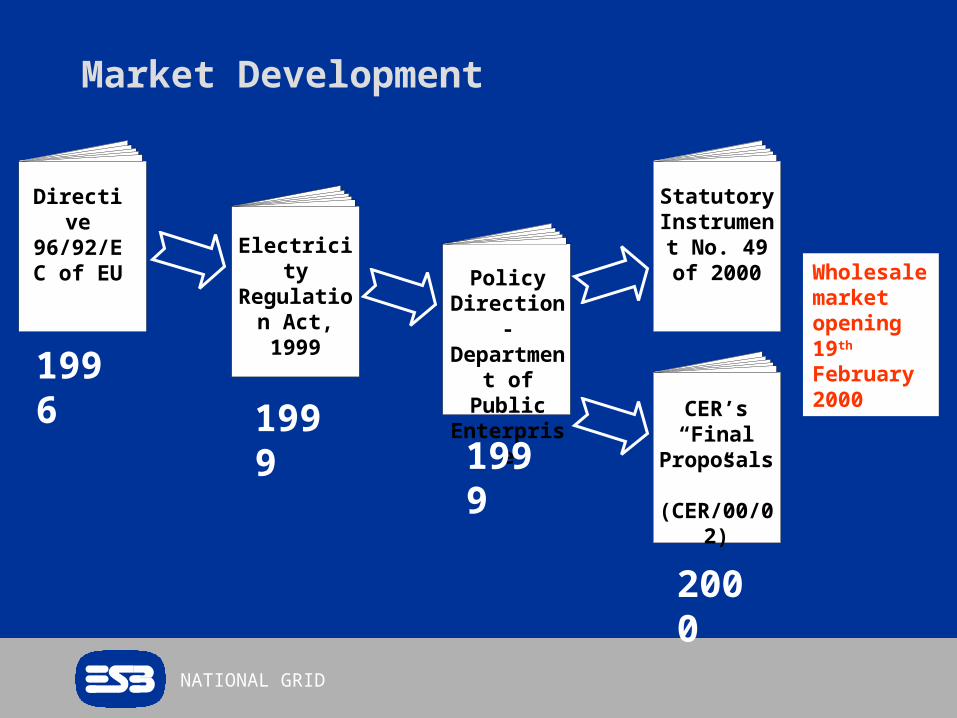

Market Development

Policy Direction -

Department of Public

EnterpriseCER’s “Final

Proposals” (CER/00/02)

Statutory Instrument No. 49 of

2000

Directive 96/92/EC

of EU Electricity Regulation Act, 1999

1996

19991999

2000

Wholesale market opening 19th February 2000

NATIONAL GRID

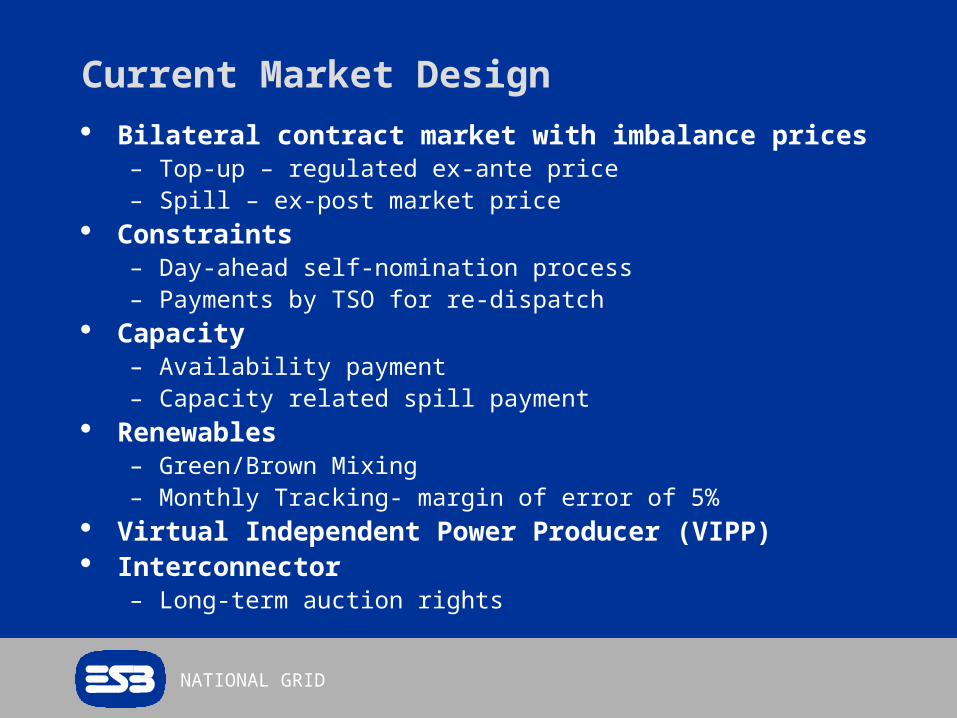

Current Market Design

Bilateral contract market with imbalance prices– Top-up – regulated ex-ante price – Spill – ex-post market price

Constraints– Day-ahead self-nomination process– Payments by TSO for re-dispatch

Capacity – Availability payment– Capacity related spill payment

Renewables– Green/Brown Mixing– Monthly Tracking- margin of error of 5%

Virtual Independent Power Producer (VIPP) Interconnector

– Long-term auction rights

NATIONAL GRID

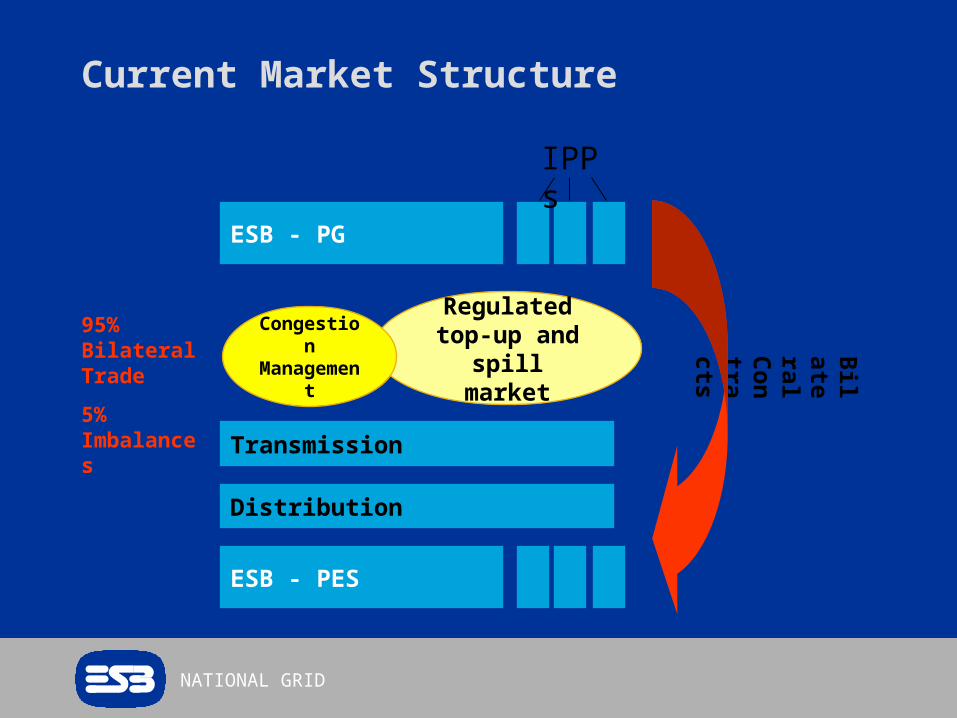

Current Market Structure

ESB - PES

Distribution

ESB - PG

Transmission

Regulated top-up and spill

market

Congestion Managemen

t

Bila

teral C

on

tracts

95% Bilateral Trade

5% Imbalances

IPPs

NATIONAL GRID

New Participants

0

1

2

3

4

5

6

7

8

9

1999 2000 2001 2002 2003 2004

Number of Suppliers joining market Number of Generators joining market

2000- 28% of market open

2002- 40% of market open

2004- 56% of market open

Full retail opening on 19th February 2005

NATIONAL GRID

Price Setting for Apr-June 2004

679

542 538

468

353

249 245

190165

145 13499 83 78 65 62 58 57 51 43 30 27

5 20

100

200

300

400

500

600

700

TB3 MP3 AD1 PB3 MP2 PBC PB2 MP1 MRT GI3 AT1 AT4 PB1 NW5 AP5 AT2 GI2 NW4 HNC ED1 DB1 TP1 GI1 None

99% of time spill price is set by single player

NATIONAL GRID

Increases in Wind Capacity

0100200300400500600700800900

10001

99

2

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Year

MW

NATIONAL GRID

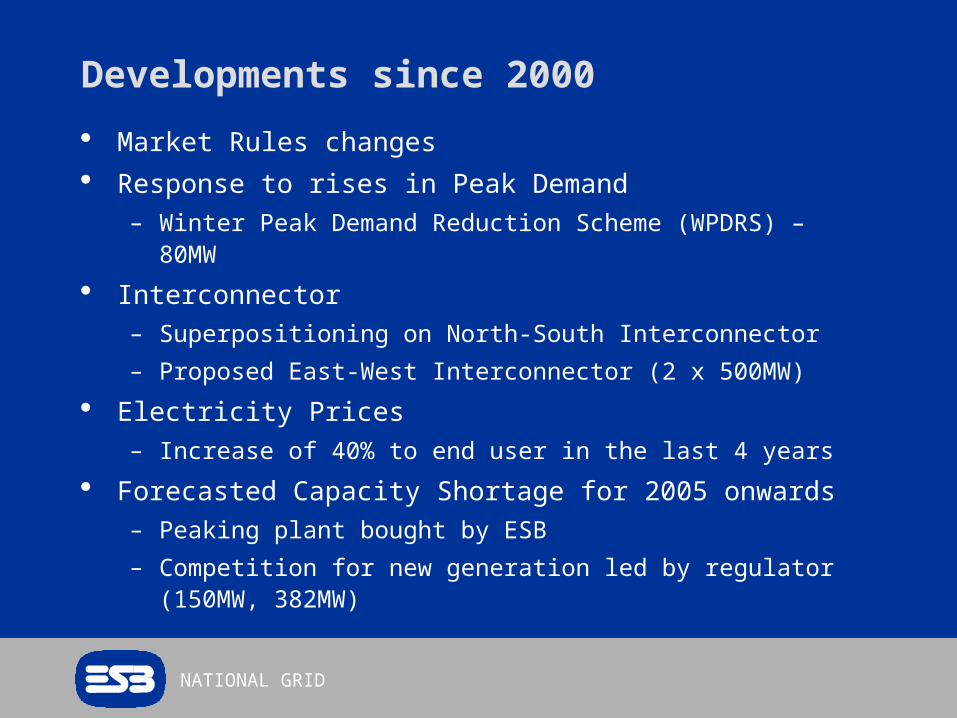

Developments since 2000

Market Rules changes

Response to rises in Peak Demand– Winter Peak Demand Reduction Scheme (WPDRS) – 80MW

Interconnector– Superpositioning on North-South Interconnector

– Proposed East-West Interconnector (2 x 500MW)

Electricity Prices– Increase of 40% to end user in the last 4 years

Forecasted Capacity Shortage for 2005 onwards– Peaking plant bought by ESB

– Competition for new generation led by regulator (150MW, 382MW)

NATIONAL GRID

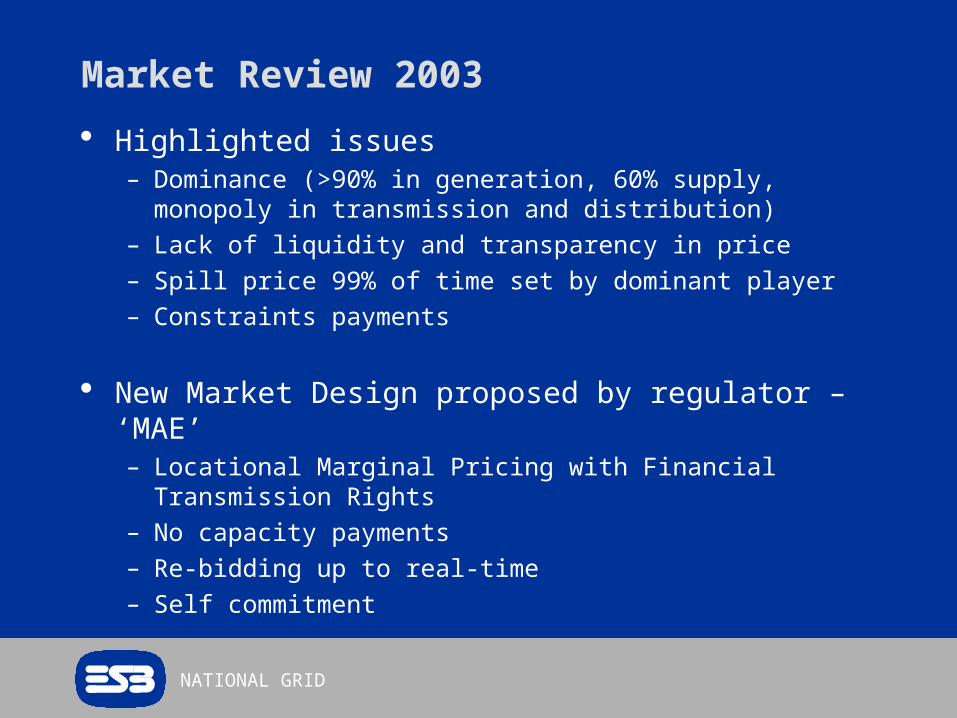

Market Review 2003

Highlighted issues– Dominance (>90% in generation, 60% supply, monopoly in

transmission and distribution)– Lack of liquidity and transparency in price– Spill price 99% of time set by dominant player– Constraints payments

New Market Design proposed by regulator – ‘MAE’– Locational Marginal Pricing with Financial Transmission

Rights– No capacity payments– Re-bidding up to real-time– Self commitment

NATIONAL GRID

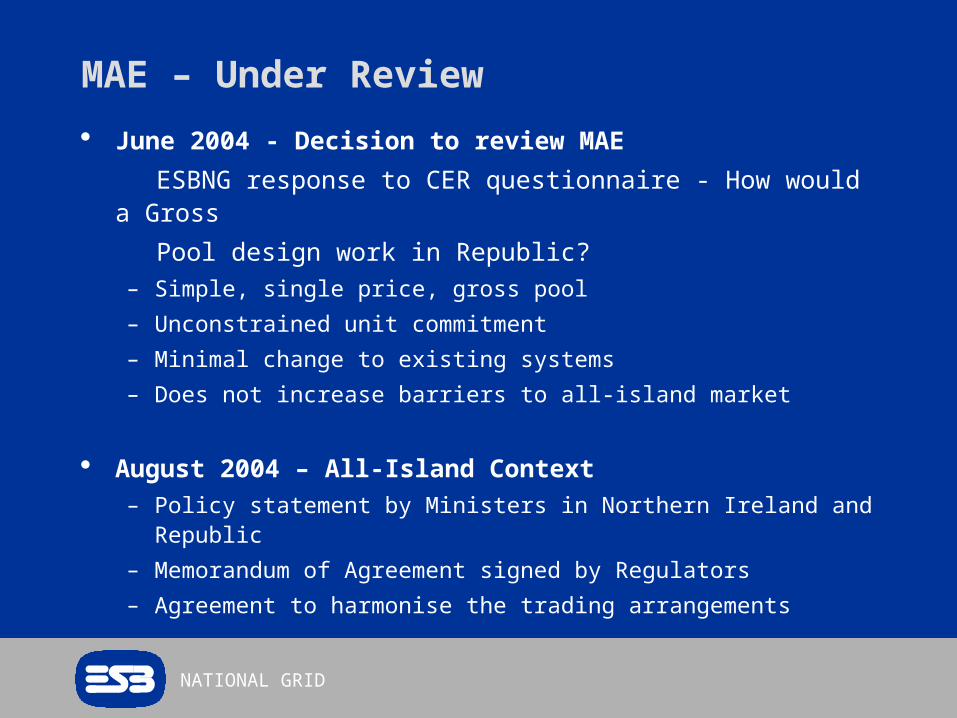

MAE – Under Review

June 2004 - Decision to review MAE

ESBNG response to CER questionnaire - How would a Gross

Pool design work in Republic? – Simple, single price, gross pool

– Unconstrained unit commitment

– Minimal change to existing systems

– Does not increase barriers to all-island market

August 2004 – All-Island Context– Policy statement by Ministers in Northern Ireland and Republic

– Memorandum of Agreement signed by Regulators

– Agreement to harmonise the trading arrangements

NATIONAL GRID

All-Island Energy Market

Joint consultation process on All Island Framework

ESBNG response:

– Development programme should:

– Include feasible timetable with key interim goals

– Contain a workable and efficient project implementation structure

Key priorities:

– Harmonise trading arrangements

– Connection policy & transmission tariffs

An all-island market should provide for a competitive, sustainable and reliable markets in electricity and natural gas on the Island of Ireland at minimum cost necessary.

All-Island Energy Development Framework, 21 June 2004

NATIONAL GRID

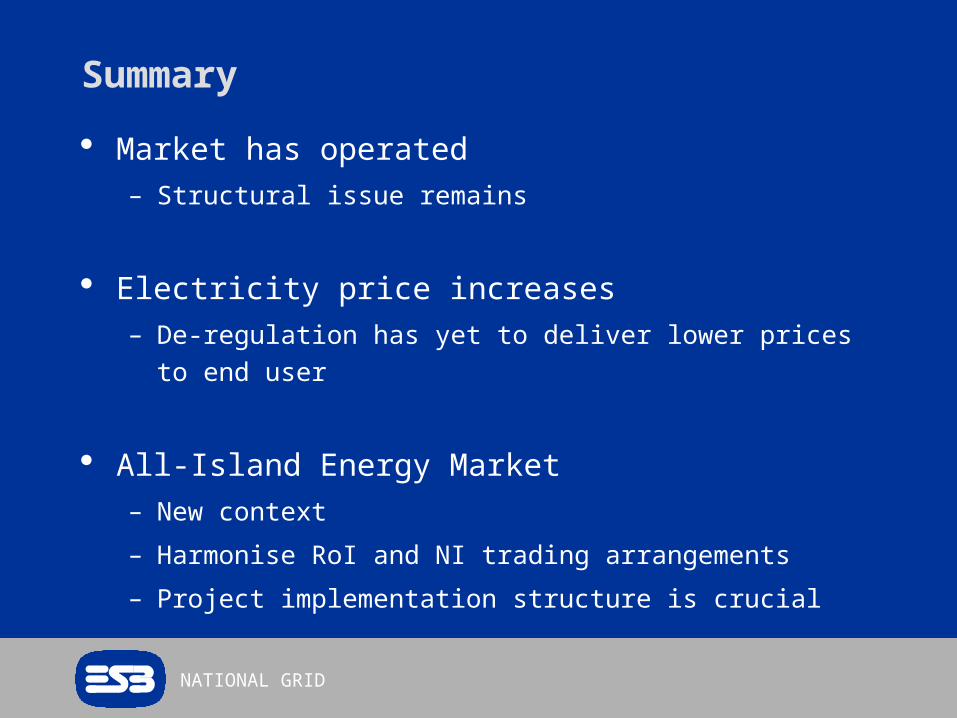

Summary

Market has operated– Structural issue remains

Electricity price increases – De-regulation has yet to deliver lower prices to end user

All-Island Energy Market – New context

– Harmonise RoI and NI trading arrangements

– Project implementation structure is crucial

NATIONAL GRID

New Capacity since 2000

0

100

200

300

400

500

600

700

800

MW

2000 2001 2002 2003 2004 to date

Brown Green CHP

NATIONAL GRID

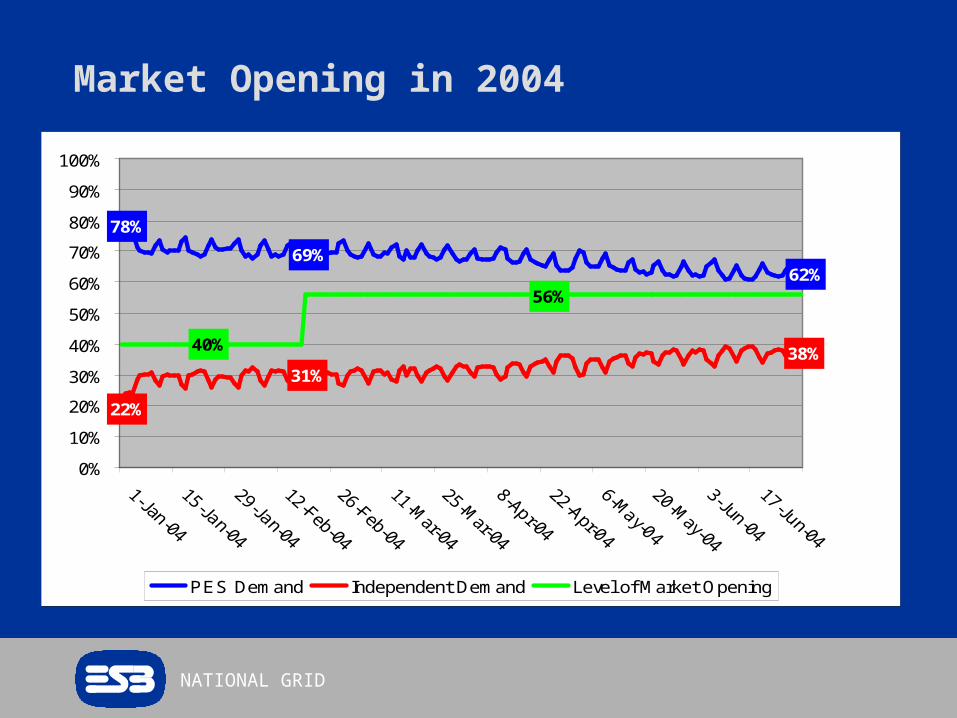

Market Opening in 2004

69%62%

78%

31%

22%

38%40%

56%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

PES Demand Independent Demand Level of Market Opening

NATIONAL GRID

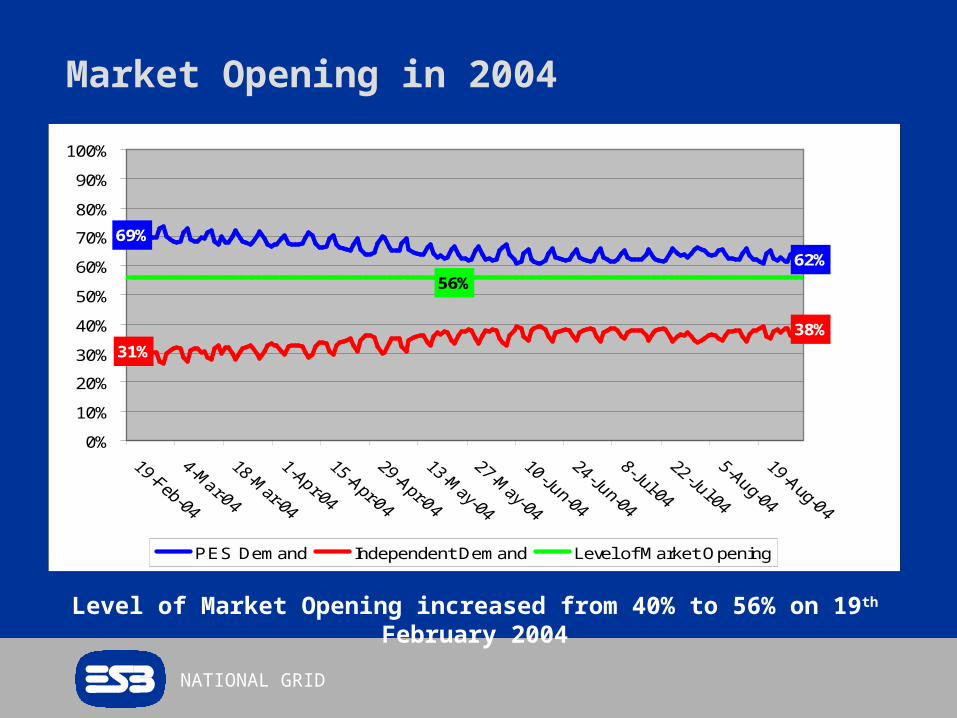

Market Opening in 2004

Level of Market Opening increased from 40% to 56% on 19th February 2004

69%

62%

31%38%

56%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

PES Demand Independent Demand Level of Market Opening

Related Documents

![[Smart Grid Market Research] Brazil: The Smart Grid Network, Zpryme Smart Grid Insights, October 2011](https://static.cupdf.com/doc/110x72/577d20871a28ab4e1e931ff6/smart-grid-market-research-brazil-the-smart-grid-network-zpryme-smart-grid.jpg)