NARUC Natural Gas Committee New York City July 17, 2007 David Sweet – Executive Director World Alliance for Decentralized Energy (WADE) Edinburgh, Washington, Edmonton, Beijing

NARUC Natural Gas Committee New York City July 17, 2007 David Sweet – Executive Director World Alliance for Decentralized Energy (WADE) Edinburgh, Washington,

Jan 02, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

NARUC Natural Gas Committee

New York CityJuly 17, 2007

David Sweet – Executive DirectorWorld Alliance for Decentralized Energy (WADE)

Edinburgh, Washington, Edmonton, Beijing

2

LNG supply - who knows what the future will bring?

3

Doomsday Scenario

“The world will soon start to run out of conventionally produced oil. If we manage somehow to overcome that shock by shifting the burden to coal and natural gas, the two other primary fossil fuels, life may go on more or less as it has been – until we start to run out of all fossil fuels by the end of this century… Even if human life does go on, civilization as we know it will not survive, unless we can find a way to live without fossil fuels.”

Out of Gas, by David Goodstein

4

A Contrarian Voice “The raw fuels are not running out. The

faster we extract and burn them, the faster we find still more.”

“The cost of energy as we use it has less and less to do with the cost of fuel.”

“The more efficient our technology, the more energy we consume.”

“The competitive advantage in manufacturing is now swinging decisively back toward the United States.”

The Bottomless Well, by Peter Huber and Mark Mills

5

The Oracle on LNG

“If North American natural gas markets are to function with the flexibility exhibited by oil, unlimited access to the vast world reserves of gas is required.”

Alan Greenspan, June 2003

6

Source: BG, ALNG, CMS, University o f Houston (IELE)

LNG Value Chain

7

LNG

Source: WADE based on BP Statistical Review of World Energy2007

2007 Proven World Natural Gas Reserves by Region (181 Trillion Cubic Meters)

8%

8%

41%

35%

4%

4% North America

South America

Europe & Eurasia

Middle East

Africa

Asia Pacific

8

9

LNGU.S. Natural Gas Production, Consumption, and Net Imports, 1960-2030

0

5

10

15

20

25

30

1960 1970 1980 1990 2000 2010 2020 2030

(Tri

llio

n c

ub

ic f

eet)

Consumption

Production

16%

21%

Source: WADE based on EIA World Energy Outlook 2007

10

LNG

Source: WADE based on 2004 Cedigaz data

Global and Projected Natural Gas Liquefaction Capacity

0

20

40

60

80

100

120

140

160

1960 1970 1980 1990 2000 2010

num

ber

of

pla

nts

0

50

100

150

200

250

300

350

400

450

tota

l capacity (

mill

ion t

/year)

cumulative # plants

cumulative # plants (projected)

cumulative capacity

cumulative capacity (projected)

11

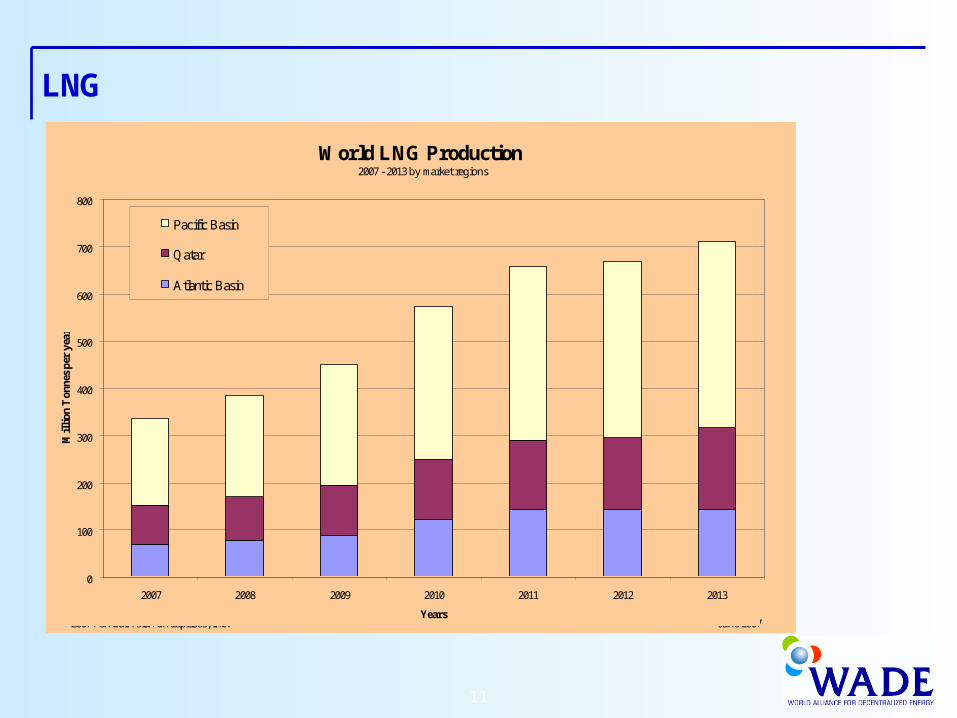

LNG

World LNG Production

0

100

200

300

400

500

600

700

800

2007 2008 2009 2010 2011 2012 2013

Years

Mil

lion

Ton

nes

per

year

Pacific Basin

Qatar

Atlantic Basin

2007 - 2013 by market regions

©2007 Pan EurAsian Enterprises, Inc. June 2007

12

LNG

Source: WADE based on 2004 Cedigaz data

Gas Liquefaction Capacity by Region (2004)

51%

19%

22%

1%

7%

Asia- Oceania

Middle East

Africa

North America

Latin America

13

LNG

Source: WADE based on 2004 Cedigaz data

Projected Gas Liquefaction Capacity by Region (2015)

29%

32%

26%

4%

8%1%

Asia- Oceania

Middle East

Africa

North America

Latin America

Europe

14

LNG

US LNG Imports by Country, 1992-2006 (Billion cubic feet)

0

100

200

300

400

500

600

700

1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Egypt

Nigeria

Trinidad and Tobago

Others

Algeria

15

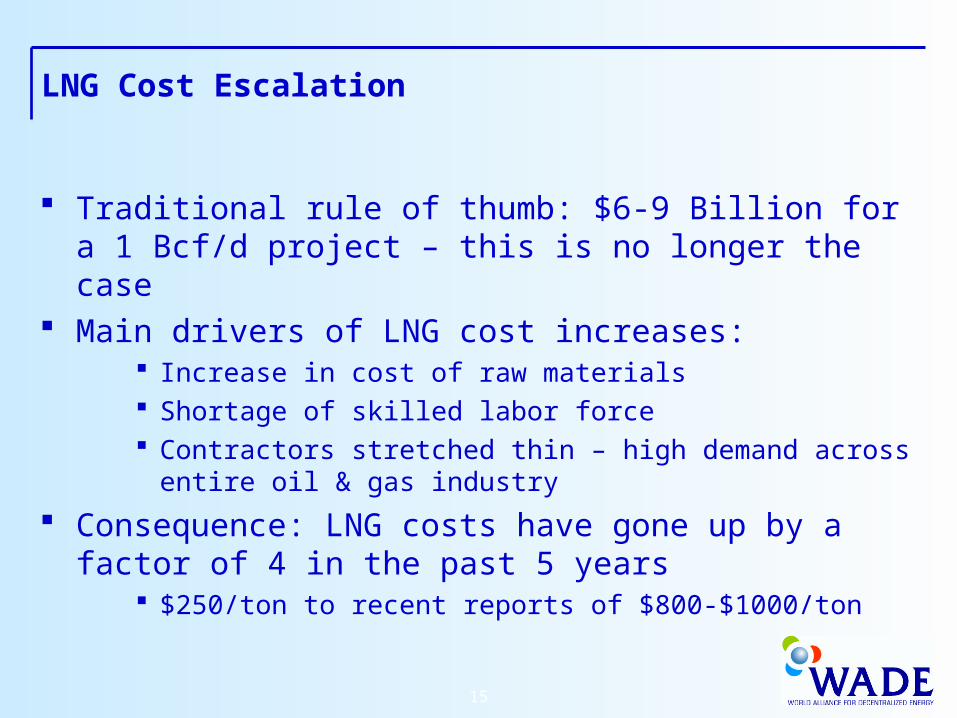

LNG Cost Escalation

Traditional rule of thumb: $6-9 Billion for a 1 Bcf/d project – this is no longer the case

Main drivers of LNG cost increases: Increase in cost of raw materials Shortage of skilled labor force Contractors stretched thin – high demand across entire

oil & gas industry

Consequence: LNG costs have gone up by a factor of 4 in the past 5 years

$250/ton to recent reports of $800-$1000/ton

16

LNG Cost Escalation

1.00

1.25

1.50

1.75

2.00

2.25

2.50

J an-03 J ul-03 J an-04 J ul-04 J an-05 J ul-05 J an-06

Carbon Steel

Stainless Steel

Nickel

Aluminum

Copper

Nickel

Aluminium

Carbon Steel hot-rolled plate

Copper

Raw materials price increases 2003-06(1-Jan-2003 = 1.0)

Sources: MEPS, LME

304 Stainless hot-rolled plate

1.00

1.25

1.50

1.75

2.00

2.25

2.50

J an-03 J ul-03 J an-04 J ul-04 J an-05 J ul-05 J an-06

Carbon Steel

Stainless Steel

Nickel

Aluminum

Copper

Nickel

Aluminium

Carbon Steel hot-rolled plate

Copper

Raw materials price increases 2003-06(1-Jan-2003 = 1.0)

Sources: MEPS, LME

304 Stainless hot-rolled plate

Source: Poten & Partners

17

LNG Drivers – Energy Price Escalation

Source: WADE based on EIA World Energy Outlook 2007

World Oil Price, 1980-2030 (2005 $US/barrel)

$0

$20

$40

$60

$80

$100

$120

1980 1990 2000 2010 2020 2030

History Projections

High Price

Reference Scenario

Low Price

18

LNG Drivers - NIMBY, BANANA and NOPE

19

LNG Drivers - Climate Change

20

LNG is a Long Term Play

LNG infrastructure will not be built on short-term contracts – long term is the anchor but spot is growing

LNG value chain is a capital intensive investment that requires a sharing of project risks over the asset life

LNG will continue to be a growing component of the supply portfolio

21

NARUC/IOGCC Report on Long Term Contracts (10/85)

State regulators should take a more active role encouraging long-term gas supply, transportation, storage plans

State regulators should minimize second guessing and taking a short-term perspective when evaluating long-term contracts

State regulators should recognize the special features of certain infrastructure projects, specifically … LNG projects, will require substantial revenue guarantees

22

Conclusions

The future can change quickly Global LNG supply is expanding rapidly – for now Costs will continue to escalate Energy price increases and climate change will

drive supply additions Spot trade will grow but long term contracts will

remain the foundation of LNG market Long term investments need long term contracts

Related Documents