ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ARE LOCATED IN APPENDIX A. Yuanta does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. Share price performance relative to VN Market cap USD 341.51 mn 6M avg. daily turnover USD 1.17 mn Outstanding shares 285.27 mn Free float 61.61% FINI ownership 48.29% Major shareholders 29.86% Net Debt / Equity 0.10x 2020 P/B (x) 1.63x FOL Room 1.71% Financial outlook (VND bn) Year to Dec 2018A 2019E 2020 Guidance Sales 3,480 2,546 1,520 Op. profit 1,012 641 122 Net profit* 709 893 764 EPS (VND) 2,967 3,435 2,671 EPS chg (%) -6% 16% -22% P/B (X) 1.3 1.3 ROE (%) 20% 18% Div. yield (%) 1.22% 1.80% 1.7% *Net profit attributable to shareholders (PATMI minus employee welfare contribution). Sources: NLG, Bloomberg, Yuanta Vietnam Nam Long Investment Corp (NLG VN) Unlock upside potential by new projects NLG has only fulfilled 26% of 2020 PAT guidance in 9M20. However, the company expects to reach this target in 4Q20 by delivering completed units (i.e., Waterpoint and Novia) and transferring shares in its subsidiaries (i.e., a 35% stake in the Waterfront project and 100% stake in the Paragon Dai Phuoc project). High presales value fortifies future earnings. 9M20 presales value was VND3.3bn, increasing 23% YoY. Three projects (i.e., Mizuki, Akari, and Southgate) should be the main contributors to NLG’s earnings in upcoming years. So far, the company has sold 1,751 Akari units (for sales of VND3,785bn and 94% of the first phase's units) and 976 Soughgate units (VND3,762bn of revenue and 57% of the first phase's units). Additionally, the 760-unit Mizuki highrise project will be launched in 4Q20 and 63 lowrise units will be launched in 2021, which should contribute to 2022 earnings. Unlocking new projects in 2021. The commencement date of three new projects (i.e., Waterfront, Hai Phong, and Can Tho) were postponed due to ongoing administrative issues. However, the company still expects the first phase of three new projects to officially launch next year. Also, two new projects with size area above 50ha in the east of HCMC are likely to be acquired in 2021, which could be a catalyst for NLG’s share price amid the shortage of HCMC landbank. Our view: The attractiveness of Mizuki and Akari projects is beyond dispute given HCMC’s shortage of housing supply, and especially supply of mid-end housing. Although demand for the Southgate project is likely tepid, NLG has implemented a solid sales strategy (e.g., by carefully controlling the number of units launched, types of housing, and intervals between tranch launches) to maintain a certain level of "heat" for the project. We believe this explains NLG's share price increase of 15.7% YTD and its stronger recovery of 67.4% since the pandemic-driven trough. The potential for NLG’s new projects (e.g., NLG Can Tho, NLG Hai Phong, and new landbank) is unclear. We believe the market is concerned about the determinants of internal rate of return at these projects, including launch schedules, average selling prices, and take-up rates. Therefore, any signal of a successful launch from these new projects could unlock further upside for NLG’s share price. After changing some of our assumptions, new our per-share fair value estimate for NLG is VND30,500, which offers 7.6% expected 12-month TSR. We thus downgrade our recommendation to Hold-Outperform from the previous BUY. (10) (5) - 5 10 15 20 15,000 18,000 21,000 24,000 27,000 30,000 NLG NLG vs. VNIndex (RHS) VND ppt Company Update Vietnam: Property 1 December 2020 NLG VN HOLD – Outperform TP upside +5.9% Close 30 Nov 2020 Price VND 28,800 12M Target VND 30,500 Previous Target VND 29,700 Change +2.7% What’s new? ► NLG fulfilled just 26% of its 2020 PAT guidance during 9M20. ► But its high presales value fortifies future earnings. 9M20 presales value was VND3.3bn, increasing 23% YoY. ► NLG should be able to unlock upside potential from its new projects in 2021, including Waterfront, NLG Hai Phong, and Can Tho. Our view ► The attractiveness of the Mizuki and Akari projects is beyond dispute given the shortage of housing supply in HCMC, especially mid-end housing. ► NLG has implemented a reasonable sales strategy for the Southgate project despite likely tepid demand. ► The potential of new projects (e.g., NLG Can Tho, NLG Hai Phong, and new landbank) is unclear. ► As such, we downgrade our recommendation to HOLD-Outperform from the previous BUY. Company profile: Nam Long Investment Corporation is a real estate developer that is primarily focused on affordable and mid-end housing. Its main markets are Ho Chi Minh City and neighboring provinces such as Long An and Dong Nai. The firm has also been expanding its operating areas (for example, to Hai Phong). NLG’s landbank is currently 650ha. Tam Nguyen +84 28 3622 6868 ext 3815 [email protected] Bloomberg code: YUTA

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ANALYST CERTIFICATION AND IMPORTANT DISCLOSURES ARE LOCATED

IN APPENDIX A. Yuanta does and seeks to do business with companies covered in its research

reports. As a result, investors should be aware that the firm may have a

conflict of interest that could affect the objectivity of this report. Investors

should consider this report as only a single factor in making their investment

decision.

Share price performance relative to VN

Market cap USD 341.51 mn

6M avg. daily turnover USD 1.17 mn

Outstanding shares 285.27 mn

Free float 61.61%

FINI ownership 48.29%

Major shareholders 29.86%

Net Debt / Equity 0.10x

2020 P/B (x) 1.63x

FOL Room 1.71%

Financial outlook (VND bn)

Year to Dec 2018A 2019E 2020

Guidance

Sales 3,480 2,546 1,520

Op. profit 1,012 641 122

Net profit* 709 893 764

EPS (VND) 2,967 3,435 2,671

EPS chg (%) -6% 16% -22%

P/B (X) 1.3 1.3

ROE (%) 20% 18%

Div. yield (%) 1.22% 1.80% 1.7%

*Net profit attributable to shareholders (PATMI minus

employee welfare contribution).

Sources: NLG, Bloomberg, Yuanta Vietnam

Nam Long Investment Corp (NLG VN) Unlock upside potential by new projects

NLG has only fulfilled 26% of 2020 PAT guidance in 9M20. However, the company expects to

reach this target in 4Q20 by delivering completed units (i.e., Waterpoint and Novia) and

transferring shares in its subsidiaries (i.e., a 35% stake in the Waterfront project and 100%

stake in the Paragon Dai Phuoc project).

High presales value fortifies future earnings. 9M20 presales value was VND3.3bn, increasing

23% YoY. Three projects (i.e., Mizuki, Akari, and Southgate) should be the main contributors to

NLG’s earnings in upcoming years. So far, the company has sold 1,751 Akari units (for sales of

VND3,785bn and 94% of the first phase's units) and 976 Soughgate units (VND3,762bn of

revenue and 57% of the first phase's units). Additionally, the 760-unit Mizuki highrise project

will be launched in 4Q20 and 63 lowrise units will be launched in 2021, which should

contribute to 2022 earnings.

Unlocking new projects in 2021. The commencement date of three new projects (i.e.,

Waterfront, Hai Phong, and Can Tho) were postponed due to ongoing administrative issues.

However, the company still expects the first phase of three new projects to officially launch

next year. Also, two new projects with size area above 50ha in the east of HCMC are likely to

be acquired in 2021, which could be a catalyst for NLG’s share price amid the shortage of

HCMC landbank.

Our view: The attractiveness of Mizuki and Akari projects is beyond dispute given HCMC’s

shortage of housing supply, and especially supply of mid-end housing. Although demand for

the Southgate project is likely tepid, NLG has implemented a solid sales strategy (e.g., by

carefully controlling the number of units launched, types of housing, and intervals between

tranch launches) to maintain a certain level of "heat" for the project. We believe this explains

NLG's share price increase of 15.7% YTD and its stronger recovery of 67.4% since the

pandemic-driven trough.

The potential for NLG’s new projects (e.g., NLG Can Tho, NLG Hai Phong, and new landbank) is

unclear. We believe the market is concerned about the determinants of internal rate of return

at these projects, including launch schedules, average selling prices, and take-up rates.

Therefore, any signal of a successful launch from these new projects could unlock further

upside for NLG’s share price. After changing some of our assumptions, new our per-share fair

value estimate for NLG is VND30,500, which offers 7.6% expected 12-month TSR. We thus

downgrade our recommendation to Hold-Outperform from the previous BUY.

(10)

(5)

-

5

10

15

20

15,000

18,000

21,000

24,000

27,000

30,000NLG

NLG vs. VNIndex (RHS)VND ppt

Company Update

Vietnam: Property 1 December 2020

NLG VN

HOLD – Outperform

TP upside +5.9%

Close 30 Nov 2020

Price VND 28,800

12M Target VND 30,500

Previous Target VND 29,700

Change +2.7%

What’s new?

► NLG fulfilled just 26% of its 2020 PAT

guidance during 9M20.

► But its high presales value fortifies future

earnings. 9M20 presales value was

VND3.3bn, increasing 23% YoY.

► NLG should be able to unlock upside

potential from its new projects in 2021,

including Waterfront, NLG Hai Phong, and

Can Tho.

Our view

► The attractiveness of the Mizuki and Akari projects is

beyond dispute given the shortage of housing supply

in HCMC, especially mid-end housing.

► NLG has implemented a reasonable sales strategy for

the Southgate project despite likely tepid demand.

► The potential of new projects (e.g., NLG Can Tho,

NLG Hai Phong, and new landbank) is unclear.

► As such, we downgrade our recommendation to

HOLD-Outperform from the previous BUY.

Company profile: Nam Long Investment Corporation is a real estate developer that is primarily focused on affordable and mid-end housing. Its main

markets are Ho Chi Minh City and neighboring provinces such as Long An and Dong Nai. The firm has also been expanding its operating areas (for

example, to Hai Phong). NLG’s landbank is currently 650ha.

Tam Nguyen

+84 28 3622 6868 ext 3815

Bloomberg code: YUTA

1 December 2020 Page 2 of 10

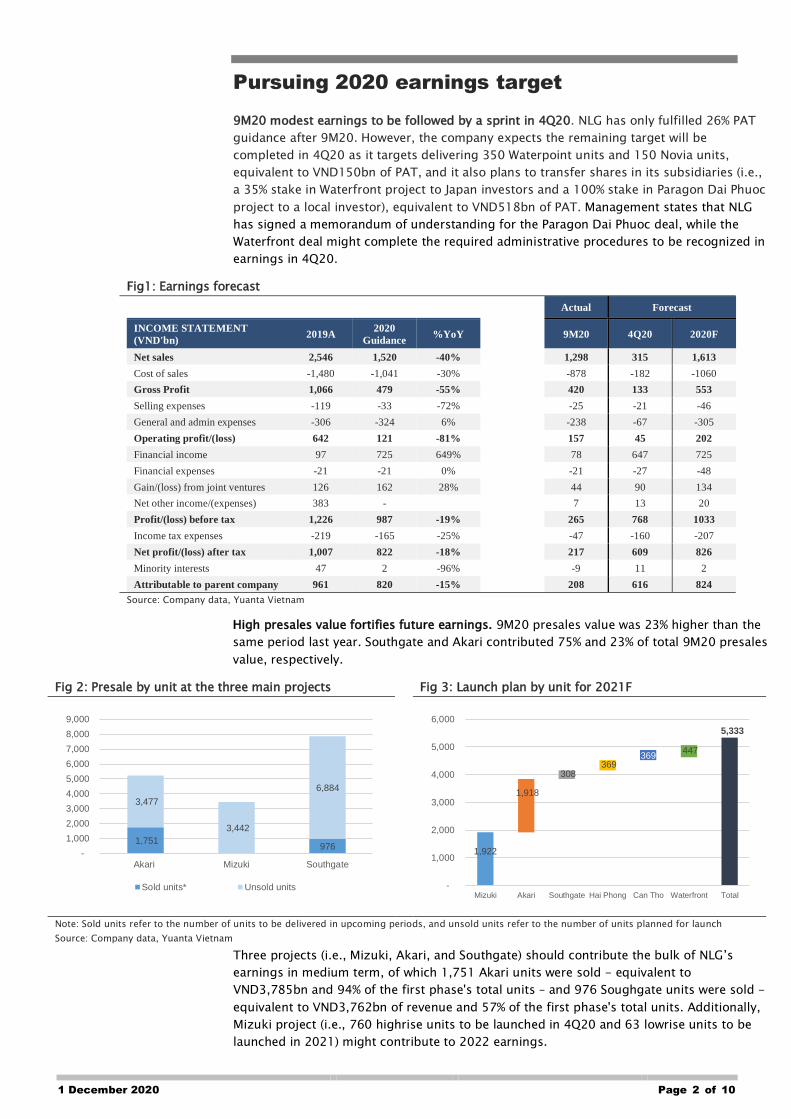

Pursuing 2020 earnings target

9M20 modest earnings to be followed by a sprint in 4Q20. NLG has only fulfilled 26% PAT

guidance after 9M20. However, the company expects the remaining target will be

completed in 4Q20 as it targets delivering 350 Waterpoint units and 150 Novia units,

equivalent to VND150bn of PAT, and it also plans to transfer shares in its subsidiaries (i.e.,

a 35% stake in Waterfront project to Japan investors and a 100% stake in Paragon Dai Phuoc

project to a local investor), equivalent to VND518bn of PAT. Management states that NLG

has signed a memorandum of understanding for the Paragon Dai Phuoc deal, while the

Waterfront deal might complete the required administrative procedures to be recognized in

earnings in 4Q20.

Fig1: Earnings forecast

Actual Forecast

INCOME STATEMENT

(VND'bn) 2019A

2020

Guidance %YoY 9M20 4Q20 2020F

Net sales 2,546 1,520 -40% 1,298 315 1,613

Cost of sales -1,480 -1,041 -30% -878 -182 -1060

Gross Profit 1,066 479 -55% 420 133 553

Selling expenses -119 -33 -72% -25 -21 -46

General and admin expenses -306 -324 6% -238 -67 -305

Operating profit/(loss) 642 121 -81% 157 45 202

Financial income 97 725 649% 78 647 725

Financial expenses -21 -21 0% -21 -27 -48

Gain/(loss) from joint ventures 126 162 28% 44 90 134

Net other income/(expenses) 383 - 7 13 20

Profit/(loss) before tax 1,226 987 -19% 265 768 1033

Income tax expenses -219 -165 -25% -47 -160 -207

Net profit/(loss) after tax 1,007 822 -18% 217 609 826

Minority interests 47 2 -96% -9 11 2

Attributable to parent company 961 820 -15% 208 616 824

Source: Company data, Yuanta Vietnam

High presales value fortifies future earnings. 9M20 presales value was 23% higher than the

same period last year. Southgate and Akari contributed 75% and 23% of total 9M20 presales

value, respectively.

Fig 2: Presale by unit at the three main projects Fig 3: Launch plan by unit for 2021F

Note: Sold units refer to the number of units to be delivered in upcoming periods, and unsold units refer to the number of units planned for launch

Source: Company data, Yuanta Vietnam

Three projects (i.e., Mizuki, Akari, and Southgate) should contribute the bulk of NLG’s

earnings in medium term, of which 1,751 Akari units were sold - equivalent to

VND3,785bn and 94% of the first phase's total units – and 976 Soughgate units were sold -

equivalent to VND3,762bn of revenue and 57% of the first phase's total units. Additionally,

Mizuki project (i.e., 760 highrise units to be launched in 4Q20 and 63 lowrise units to be

launched in 2021) might contribute to 2022 earnings.

1,751 976

3,477

3,442

6,884

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Akari Mizuki Southgate

Sold units* Unsold units

1,922

5,333

1,918

308 369

369 447

-

1,000

2,000

3,000

4,000

5,000

6,000

Mizuki Akari Southgate Hai Phong Can Tho Waterfront Total

1 December 2020 Page 3 of 10

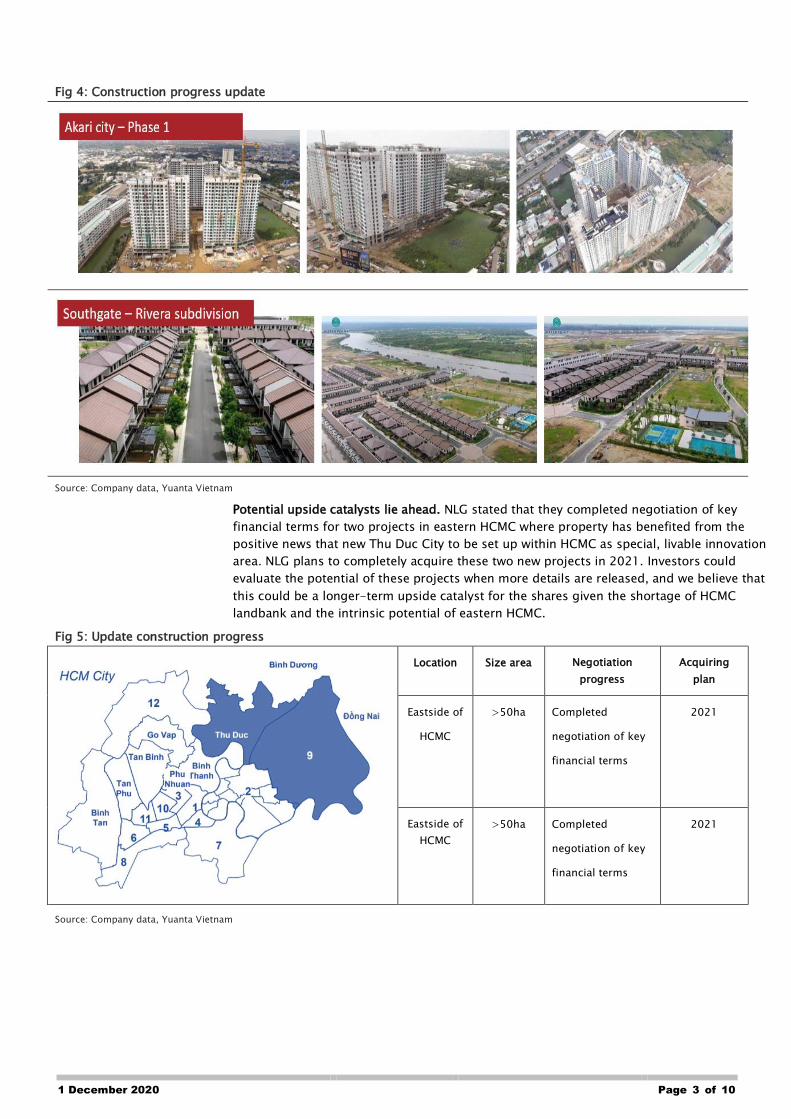

Fig 4: Construction progress update

Source: Company data, Yuanta Vietnam

Potential upside catalysts lie ahead. NLG stated that they completed negotiation of key

financial terms for two projects in eastern HCMC where property has benefited from the

positive news that new Thu Duc City to be set up within HCMC as special, livable innovation

area. NLG plans to completely acquire these two new projects in 2021. Investors could

evaluate the potential of these projects when more details are released, and we believe that

this could be a longer-term upside catalyst for the shares given the shortage of HCMC

landbank and the intrinsic potential of eastern HCMC.

Fig 5: Update construction progress

Location Size area Negotiation

progress

Acquiring

plan

Eastside of

HCMC

>50ha Completed

negotiation of key

financial terms

2021

Eastside of

HCMC

>50ha Completed

negotiation of key

financial terms

2021

Source: Company data, Yuanta Vietnam

1 December 2020 Page 4 of 10

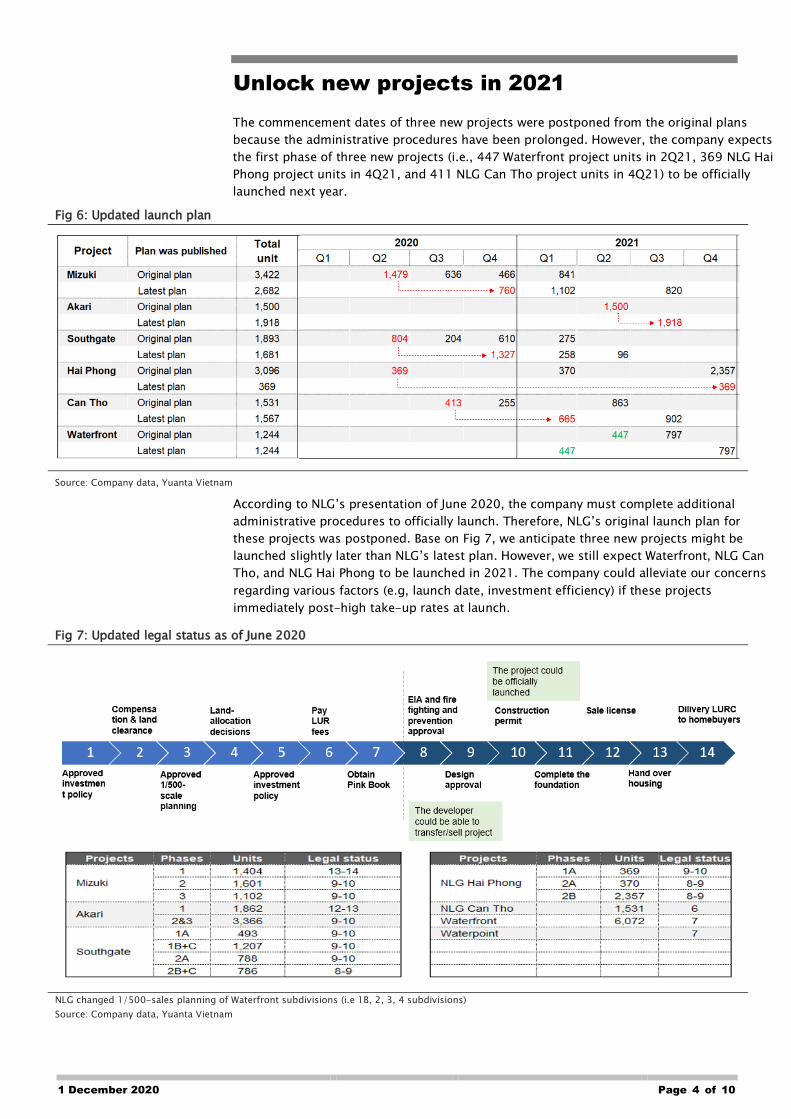

Unlock new projects in 2021

The commencement dates of three new projects were postponed from the original plans

because the administrative procedures have been prolonged. However, the company expects

the first phase of three new projects (i.e., 447 Waterfront project units in 2Q21, 369 NLG Hai

Phong project units in 4Q21, and 411 NLG Can Tho project units in 4Q21) to be officially

launched next year.

Fig 6: Updated launch plan

Source: Company data, Yuanta Vietnam

According to NLG’s presentation of June 2020, the company must complete additional

administrative procedures to officially launch. Therefore, NLG’s original launch plan for

these projects was postponed. Base on Fig 7, we anticipate three new projects might be

launched slightly later than NLG’s latest plan. However, we still expect Waterfront, NLG Can

Tho, and NLG Hai Phong to be launched in 2021. The company could alleviate our concerns

regarding various factors (e.g, launch date, investment efficiency) if these projects

immediately post-high take-up rates at launch.

Fig 7: Updated legal status as of June 2020

NLG changed 1/500-sales planning of Waterfront subdivisions (i.e 1B, 2, 3, 4 subdivisions)

Source: Company data, Yuanta Vietnam

1 December 2020 Page 5 of 10

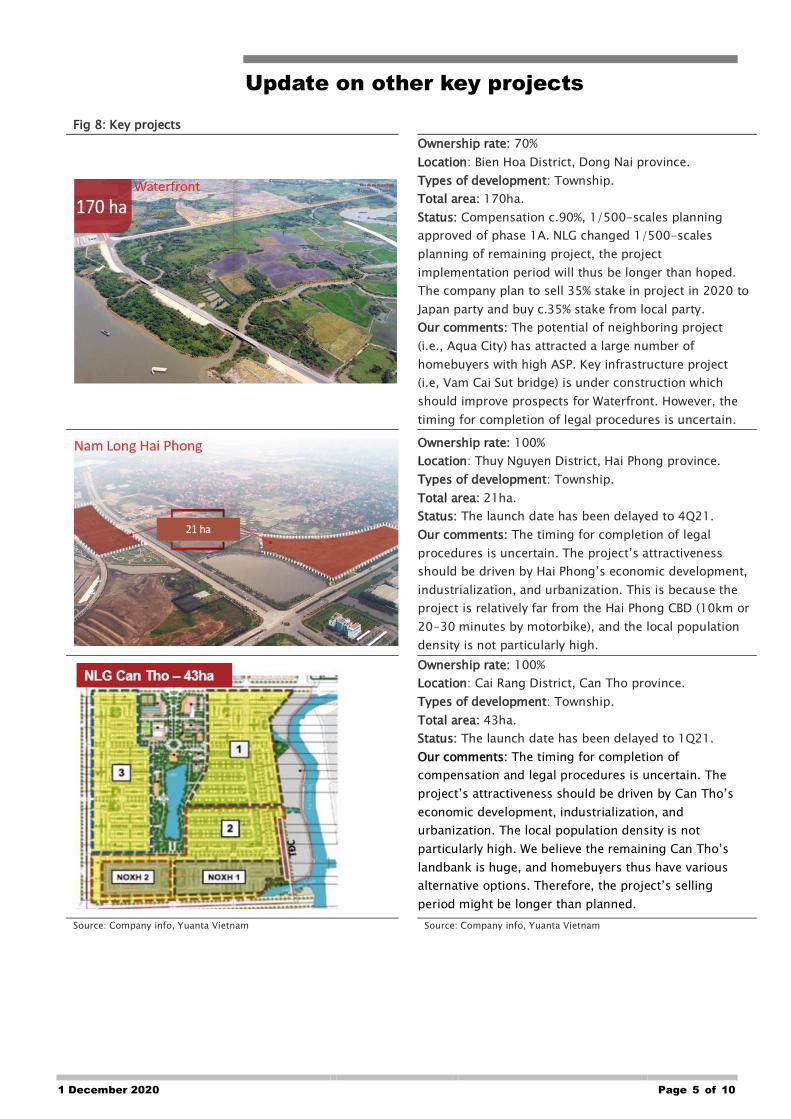

Update on other key projects

Fig 8: Key projects

Ownership rate: 70%

Location: Bien Hoa District, Dong Nai province.

Types of development: Township.

Total area: 170ha.

Status: Compensation c.90%, 1/500-scales planning

approved of phase 1A. NLG changed 1/500-scales

planning of remaining project, the project

implementation period will thus be longer than hoped.

The company plan to sell 35% stake in project in 2020 to

Japan party and buy c.35% stake from local party.

Our comments: The potential of neighboring project

(i.e., Aqua City) has attracted a large number of

homebuyers with high ASP. Key infrastructure project

(i.e, Vam Cai Sut bridge) is under construction which

should improve prospects for Waterfront. However, the

timing for completion of legal procedures is uncertain.

Ownership rate: 100%

Location: Thuy Nguyen District, Hai Phong province.

Types of development: Township.

Total area: 21ha.

Status: The launch date has been delayed to 4Q21.

Our comments: The timing for completion of legal

procedures is uncertain. The project’s attractiveness

should be driven by Hai Phong’s economic development,

industrialization, and urbanization. This is because the

project is relatively far from the Hai Phong CBD (10km or

20-30 minutes by motorbike), and the local population

density is not particularly high.

Ownership rate: 100%

Location: Cai Rang District, Can Tho province.

Types of development: Township.

Total area: 43ha.

Status: The launch date has been delayed to 1Q21.

Our comments: The timing for completion of

compensation and legal procedures is uncertain. The

project’s attractiveness should be driven by Can Tho’s

economic development, industrialization, and

urbanization. The local population density is not

particularly high. We believe the remaining Can Tho’s

landbank is huge, and homebuyers thus have various

alternative options. Therefore, the project’s selling

period might be longer than planned.

Source: Company info, Yuanta Vietnam Source: Company info, Yuanta Vietnam

1 December 2020 Page 6 of 10

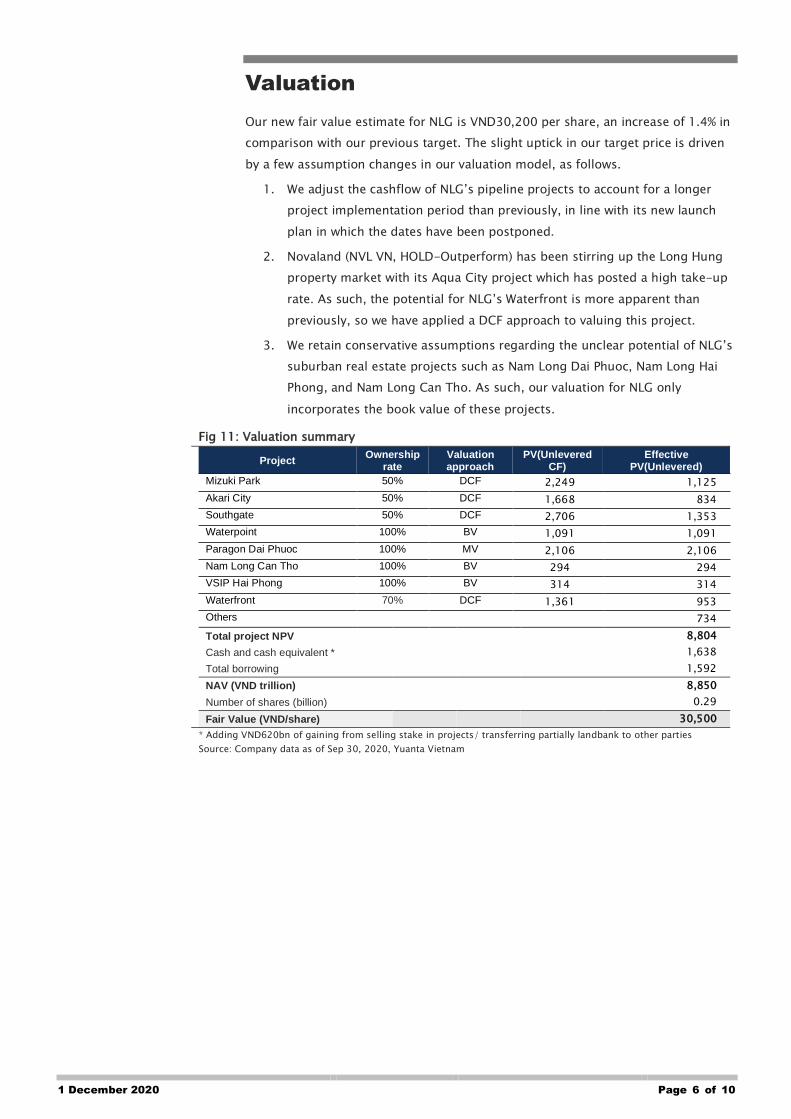

Valuation

Our new fair value estimate for NLG is VND30,200 per share, an increase of 1.4% in

comparison with our previous target. The slight uptick in our target price is driven

by a few assumption changes in our valuation model, as follows.

1. We adjust the cashflow of NLG’s pipeline projects to account for a longer

project implementation period than previously, in line with its new launch

plan in which the dates have been postponed.

2. Novaland (NVL VN, HOLD-Outperform) has been stirring up the Long Hung

property market with its Aqua City project which has posted a high take-up

rate. As such, the potential for NLG’s Waterfront is more apparent than

previously, so we have applied a DCF approach to valuing this project.

3. We retain conservative assumptions regarding the unclear potential of NLG’s

suburban real estate projects such as Nam Long Dai Phuoc, Nam Long Hai

Phong, and Nam Long Can Tho. As such, our valuation for NLG only

incorporates the book value of these projects.

Fig 11: Valuation summary

Project Ownership

rate Valuation approach

PV(Unlevered CF)

Effective PV(Unlevered)

Mizuki Park 50% DCF 2,249 1,125

Akari City 50% DCF 1,668 834

Southgate 50% DCF 2,706 1,353

Waterpoint 100% BV 1,091 1,091

Paragon Dai Phuoc 100% MV 2,106 2,106

Nam Long Can Tho 100% BV 294 294

VSIP Hai Phong 100% BV 314 314

Waterfront 70% DCF 1,361 953

Others

734

Total project NPV

8,804

Cash and cash equivalent *

1,638

Total borrowing

1,592

NAV (VND trillion)

8,850

Number of shares (billion)

0.29

Fair Value (VND/share)

30,500

* Adding VND620bn of gaining from selling stake in projects/ transferring partially landbank to other parties

Source: Company data as of Sep 30, 2020, Yuanta Vietnam

1 December 2020 Page 7 of 10

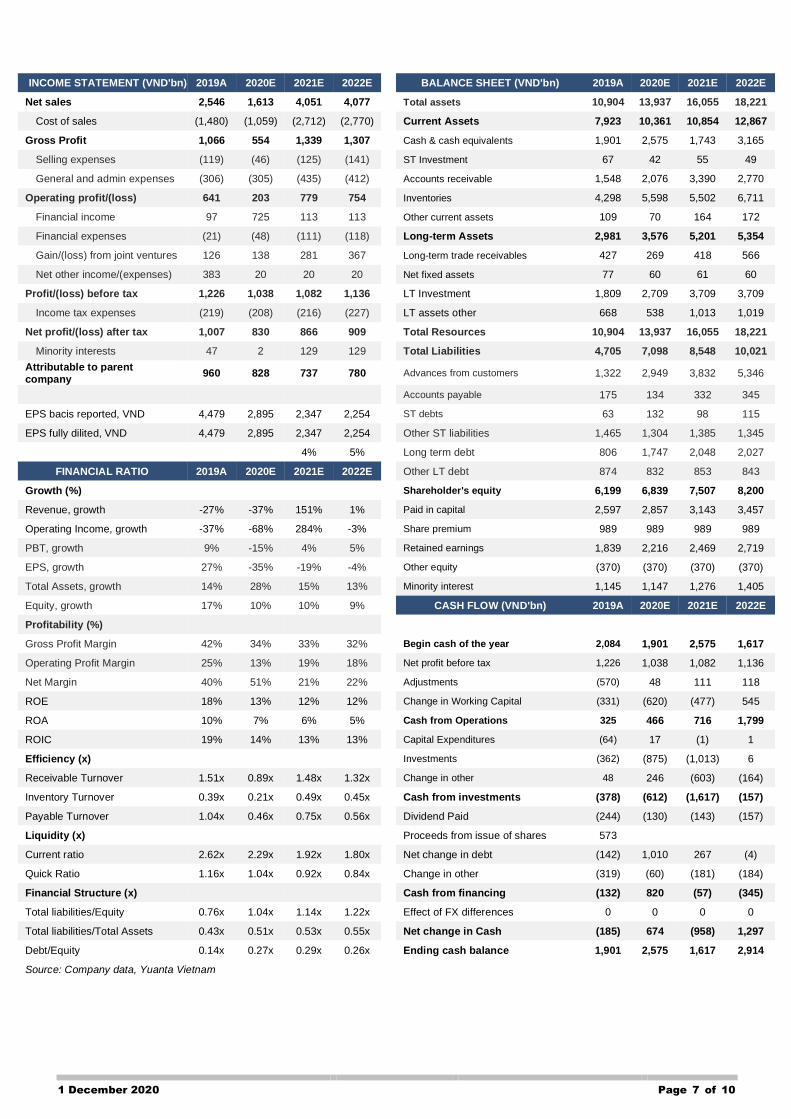

INCOME STATEMENT (VND'bn) 2019A 2020E 2021E 2022E BALANCE SHEET (VND'bn) 2019A 2020E 2021E 2022E

Net sales 2,546 1,613 4,051 4,077 Total assets 10,904 13,937 16,055 18,221

Cost of sales (1,480) (1,059) (2,712) (2,770) Current Assets 7,923 10,361 10,854 12,867

Gross Profit 1,066 554 1,339 1,307 Cash & cash equivalents 1,901 2,575 1,743 3,165

Selling expenses (119) (46) (125) (141) ST Investment 67 42 55 49

General and admin expenses (306) (305) (435) (412) Accounts receivable 1,548 2,076 3,390 2,770

Operating profit/(loss) 641 203 779 754 Inventories 4,298 5,598 5,502 6,711

Financial income 97 725 113 113 Other current assets 109 70 164 172

Financial expenses (21) (48) (111) (118) Long-term Assets 2,981 3,576 5,201 5,354

Gain/(loss) from joint ventures 126 138 281 367 Long-term trade receivables 427 269 418 566

Net other income/(expenses) 383 20 20 20 Net fixed assets 77 60 61 60

Profit/(loss) before tax 1,226 1,038 1,082 1,136 LT Investment 1,809 2,709 3,709 3,709

Income tax expenses (219) (208) (216) (227) LT assets other 668 538 1,013 1,019

Net profit/(loss) after tax 1,007 830 866 909 Total Resources 10,904 13,937 16,055 18,221

Minority interests 47 2 129 129 Total Liabilities 4,705 7,098 8,548 10,021

Attributable to parent company

960 828 737 780 Advances from customers 1,322 2,949 3,832 5,346

Accounts payable 175 134 332 345

EPS bacis reported, VND 4,479 2,895 2,347 2,254 ST debts 63 132 98 115

EPS fully dilited, VND 4,479 2,895 2,347 2,254 Other ST liabilities 1,465 1,304 1,385 1,345

4% 5% Long term debt 806 1,747 2,048 2,027

FINANCIAL RATIO 2019A 2020E 2021E 2022E Other LT debt 874 832 853 843

Growth (%) Shareholder's equity 6,199 6,839 7,507 8,200

Revenue, growth -27% -37% 151% 1% Paid in capital 2,597 2,857 3,143 3,457

Operating Income, growth -37% -68% 284% -3% Share premium 989 989 989 989

PBT, growth 9% -15% 4% 5% Retained earnings 1,839 2,216 2,469 2,719

EPS, growth 27% -35% -19% -4% Other equity (370) (370) (370) (370)

Total Assets, growth 14% 28% 15% 13% Minority interest 1,145 1,147 1,276 1,405

Equity, growth 17% 10% 10% 9% CASH FLOW (VND'bn) 2019A 2020E 2021E 2022E

Profitability (%)

Gross Profit Margin 42% 34% 33% 32% Begin cash of the year 2,084 1,901 2,575 1,617

Operating Profit Margin 25% 13% 19% 18% Net profit before tax 1,226 1,038 1,082 1,136

Net Margin 40% 51% 21% 22% Adjustments (570) 48 111 118

ROE 18% 13% 12% 12% Change in Working Capital (331) (620) (477) 545

ROA 10% 7% 6% 5% Cash from Operations 325 466 716 1,799

ROIC 19% 14% 13% 13% Capital Expenditures (64) 17 (1) 1

Efficiency (x) Investments (362) (875) (1,013) 6

Receivable Turnover 1.51x 0.89x 1.48x 1.32x Change in other 48 246 (603) (164)

Inventory Turnover 0.39x 0.21x 0.49x 0.45x Cash from investments (378) (612) (1,617) (157)

Payable Turnover 1.04x 0.46x 0.75x 0.56x Dividend Paid (244) (130) (143) (157)

Liquidity (x) Proceeds from issue of shares 573

Current ratio 2.62x 2.29x 1.92x 1.80x Net change in debt (142) 1,010 267 (4)

Quick Ratio 1.16x 1.04x 0.92x 0.84x Change in other (319) (60) (181) (184)

Financial Structure (x) Cash from financing (132) 820 (57) (345)

Total liabilities/Equity 0.76x 1.04x 1.14x 1.22x Effect of FX differences 0 0 0 0

Total liabilities/Total Assets 0.43x 0.51x 0.53x 0.55x Net change in Cash (185) 674 (958) 1,297

Debt/Equity 0.14x 0.27x 0.29x 0.26x Ending cash balance 1,901 2,575 1,617 2,914

Source: Company data, Yuanta Vietnam

Appendix A: Important Disclosures

Analyst Certification

Each research analyst primarily responsible for the content of this research report, in whole or in part, certifies that with respect to

each security or issuer that the analyst covered in this report: (1) all of the views expressed accurately reflect his or her personal

views about those securities or issuers; and (2) no part of his or her compensation was, is, or will be, directly or indirect ly, related

to the specific recommendations or views expressed by that research analyst in the research report.

Ratings Definitions

BUY: We have a positive outlook on the stock based on our expected absolute or relative return over the investment period. Our

thesis is based on our analysis of the company’s outlook, financial performance, catalysts, valuation and risk profile. We

recommend investors add to their position.

HOLD-Outperform: In our view, the stock’s fundamentals are relatively more attractive than peers at the current price. Our thesis is

based on our analysis of the company’s outlook, financial performance, catalysts, valuation and risk profile.

HOLD-Underperform: In our view, the stock’s fundamentals are relatively less attractive than peers at the current price. Our thesis

is based on our analysis of the company’s outlook, financial performance, catalysts, valuation and risk profile.

SELL: We have a negative outlook on the stock based on our expected absolute or relative return over the investment period. Our

thesis is based on our analysis of the company’s outlook, financial performance, catalysts, valuation and risk profile. We

recommend investors reduce their position.

Under Review: We actively follow the company, although our estimates, rating and target price are under review.

Restricted: The rating and target price have been suspended temporarily to comply with applicable regulations and/or Yuanta policies.

Note: Yuanta research coverage with a Target Price is based on an investment period of 12 months. Greater China Discovery Series

coverage does not have a formal 12 month Target Price and the recommendation is based on an investment period specified by the

analyst in the report.

Global Disclaimer

© 2020 Yuanta. All rights reserved. The information in this report has been compiled from sources we believe to be reliable, but we

do not hold ourselves responsible for its completeness or accuracy. It is not an offer to sell or solicitation of an offer to buy any

securities. All opinions and estimates included in this report constitute our judgment as of this date and are subject to change

without notice.

This report provides general information only. Neither the information nor any opinion expressed herein constitutes an offer or

invitation to make an offer to buy or sell securities or other investments. This material is prepared for general circulation to clients

and is not intended to provide tailored investment advice and does not take into account the individual financial situation and

objectives of any specific person who may receive this report. Investors should seek financial advice regarding the appropriateness

of investing in any securities, investments or investment strategies discussed or recommended in this report. The information

contained in this report has been compiled from sources believed to be reliable but no representation or warranty, express or implied,

is made as to its accuracy, completeness or correctness. This report is not (and should not be construed as) a solicitation to act as

securities broker or dealer in any jurisdiction by any person or company that is not legally permitted to carry on such business in

that jurisdiction.

Yuanta research is distributed in the United States only to Major U.S. Institutional Investors (as defined in Rule 15a-6 under the

Securities Exchange Act of 1934, as amended and SEC staff interpretations thereof). All transactions by a US person in the securities

mentioned in this report must be effected through a registered broker-dealer under Section 15 of the Securities Exchange Act of

1934, as amended. Yuanta research is distributed in Taiwan by Yuanta Securities Investment Consulting. Yuanta research is

distributed in Hong Kong by Yuanta Securities (Hong Kong) Co. Limited, which is licensed in Hong Kong by the Securities and Futures

Commission for regulated activities, including Type 4 regulated activity (advising on securities). In Hong Kong, this research report

may not be redistributed, retransmitted or disclosed, in whole or in part or and any form or manner, without the express written

consent of Yuanta Securities (Hong Kong) Co. Limited.

Taiwan persons wishing to obtain further information on any of the securities mentioned in this publication should contact:

Attn: Research

Yuanta Securities Investment Consulting

4F, 225,

Section 3 Nanking East Road, Taipei 104

Taiwan

Hong Kong persons wishing to obtain further information on any of the securities mentioned in this publication should contact:

Attn: Research

Yuanta Securities (Hong Kong) Co. Ltd

23/F, Tower 1, Admiralty Centre

18 Harcourt Road,

Hong Kong

Korean persons wishing to obtain further information on any of the securities mentioned in this publication should contact:

Head Office

Yuanta Securities Building

Euljiro 76 Jung-gu

Seoul, Korea 100-845

Tel: +822 3770 3454

Indonesia persons wishing to obtain further information on any of the securities mentioned in this publication should contact :

Attn: Research

PT YUANTA SECURITIES INDONESIA

(A member of the Yuanta Group)

Equity Tower, 10th Floor Unit EFGH

SCBD Lot 9

Jl. Jend. Sudirman Kav. 52-53

Tel: (6221) – 5153608 (General)

Thailand persons wishing to obtain further information on any of the securities mentioned in this publication should contact:

Research department

Yuanta Securities (Thailand)

127 Gaysorn Tower, 16th floor

Ratchadamri Road, Pathumwan

Bangkok 10330

Vietnam persons wishing to obtain further information on any of the securities mentioned in this publication should contact:

Research department

Yuanta Securities (Vietnam)

4th Floor, Saigon Centre

Tower 1, 65 Le Loi Boulevard,

Ben Nghe Ward, District 1,

HCMC, Vietnam

YUANTA SECURITIES NETWORK

YUANTA SECURITIES VIETNAM OFFICE

Head office: 4th Floor, Saigon Centre, Tower 1, 65 Le Loi Boulevard, Ben Nghe Ward, District 1, HCMC, Vietnam

Institutional Research

Matthew Smith, CFA

Head of Research

Tel: +84 28 3622 6868 (ext. 3874)

Binh Truong

Deputy Head of Research (O&G, Energy)

Tel: +84 28 3622 6868 (3845)

Tam Nguyen

Analyst (Property)

Tel: +84 28 3622 6868 (ext. 3874)

Tram Nguyen

Assistant Analyst

Tel: +84 28 3622 6868 (ext. 3845)

Tanh Tran

Analyst (Banks)

Tel: +84 28 3622 6868 (3874)

Institutional Sales

Huy Nguyen

Head of Institutional sales

Tel: +84 28 3622 6868 (3808)

Duyen Nguyen

Sales Trader

Tel: +84 28 3622 6868 (ext. 3890)

Related Documents