N O R T H E R N T R U S T G L O B A L E C O N O M I C R E S E A R C H Paul L. Kasriel, Chief Economist PH: 312.444.4145 [email protected] October 2009 © 2006 Northern Trust Corporation northerntrust.com The Shoals of Depression Have Been Avoided, but Strong Headwinds Remain

N O R T H E R N T R U S T G L O B A L E C O N O M I C R E S E A R C H Paul L. Kasriel, Chief Economist PH: 312.444.4145 [email protected] October 2009 © 2006.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

N O R T H E R N T R U S T G L O B A L E C O N O M I C R E S E A R C H

Paul L. Kasriel, Chief EconomistPH: [email protected]

October 2009

© 2006 Northern Trust Corporation northerntrust.com

The Shoals of Depression Have Been Avoided, but Strong Headwinds Remain

2 Northern Trust Global Economic Research

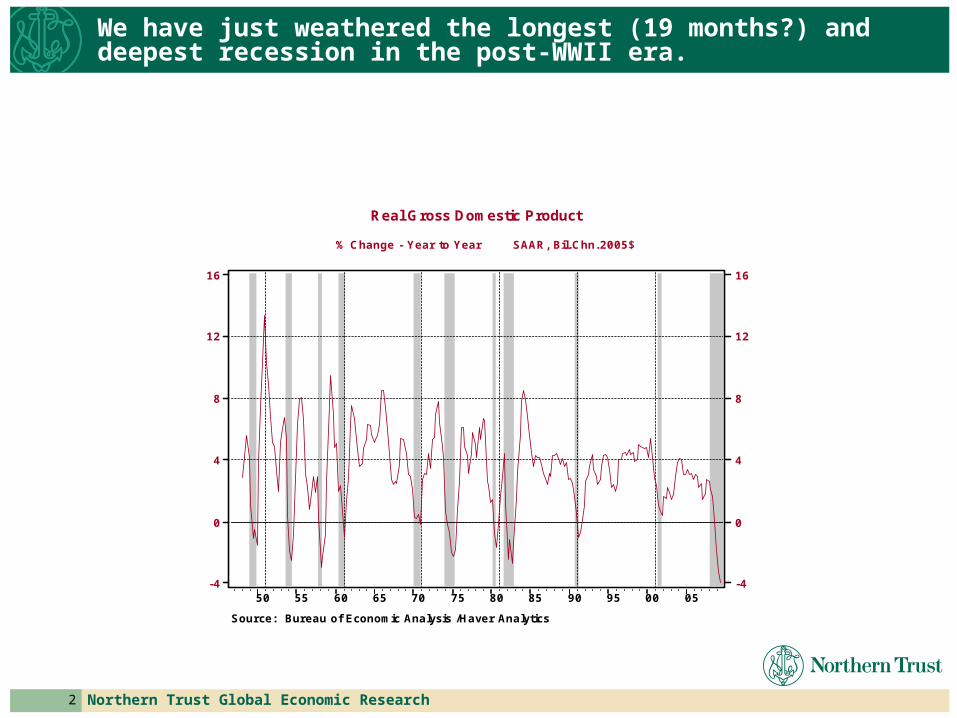

We have just weathered the longest (19 months?) and deepest recession in the post-WWII era.

Real Gross Domestic Product

% Change - Year to Year SAAR, Bil. Chn. 2005$

050095908580757065605550

Source: Bureau of Economic Analysis /Haver Analytics

16

12

8

4

0

-4

16

12

8

4

0

-4

3 Northern Trust Global Economic Research

In August, the ISM-Mfg. Composite Index popped above 50 for the first time since January 2008.

ISM Manufacturing: PMI Composite Index

SA, 50+=Increasing

SEPAUGJULJUN09

MAYAPRMARFEBJANDECNOVOCT

Source: Institute for Supply Management /Haver Analytics

56

52

48

44

40

36

32

56

52

48

44

40

36

32

4 Northern Trust Global Economic Research

The behavior of the ISM-Mfg. Index suggests that the recession ended in July 2009.

ISM Manufacturing: PMI Composite Index

SA, 50+=Increasing

050095908580757065605550

Source: Institute for Supply Management /Haver Analytics

80

70

60

50

40

30

20

80

70

60

50

40

30

20

It is not that any one sector is soaring …

…rather a number of sectors have either stopped descending or are descending at a much slower rate.

6 Northern Trust Global Economic Research

Thanks to the sharp decline in home prices and the low level of mortgage rates, house purchases are now much more affordable.

Composite Housing Affordability Index

Median Inc=Qualifying Inc=100

05009590858075

Source: National Association of Realtors /Haver Analytics

180

160

140

120

100

80

60

180

160

140

120

100

80

60

7 Northern Trust Global Economic Research

High housing affordability and the $8K first-time-homebuyer tax credit have resulted in increases in home sales in four of the past five months.

Home Sales: Sum of New and Existing

SAAR, Thous

0908070605040302

Source: Haver Analytics

9000

8250

7500

6750

6000

5250

4500

9000

8250

7500

6750

6000

5250

4500

8 Northern Trust Global Economic Research

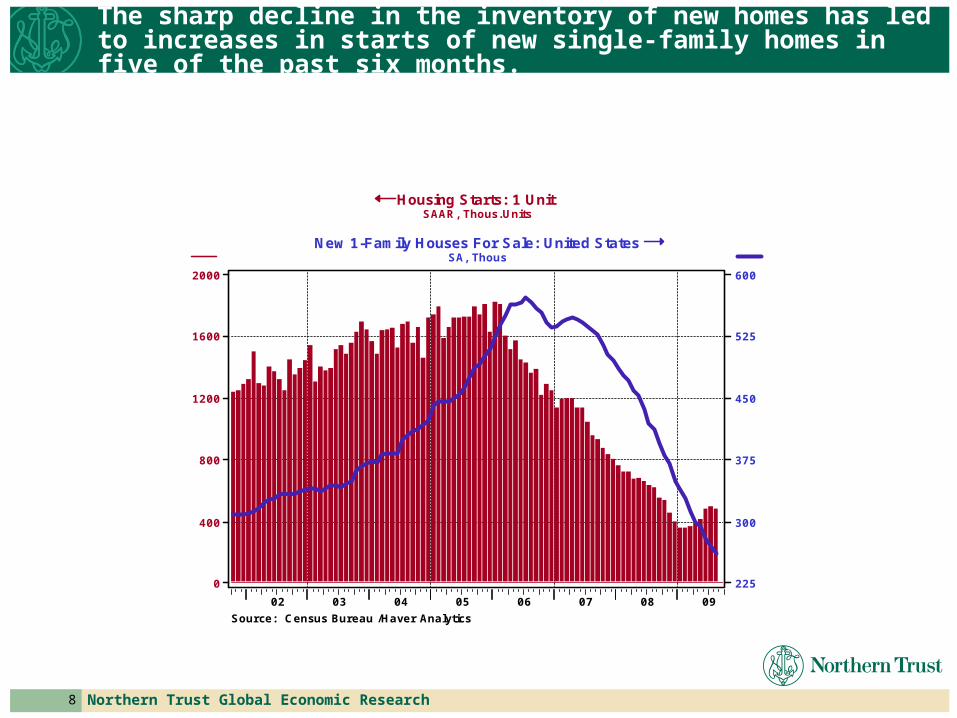

The sharp decline in the inventory of new homes has led to increases in starts of new single-family homes in five of the past six months.

Housing Starts: 1 UnitSAAR, Thous. Units

New 1-Family Houses For Sale: United StatesSA, Thous

0908070605040302

Source: Census Bureau /Haver Analytics

2000

1600

1200

800

400

0

600

525

450

375

300

225

9 Northern Trust Global Economic Research

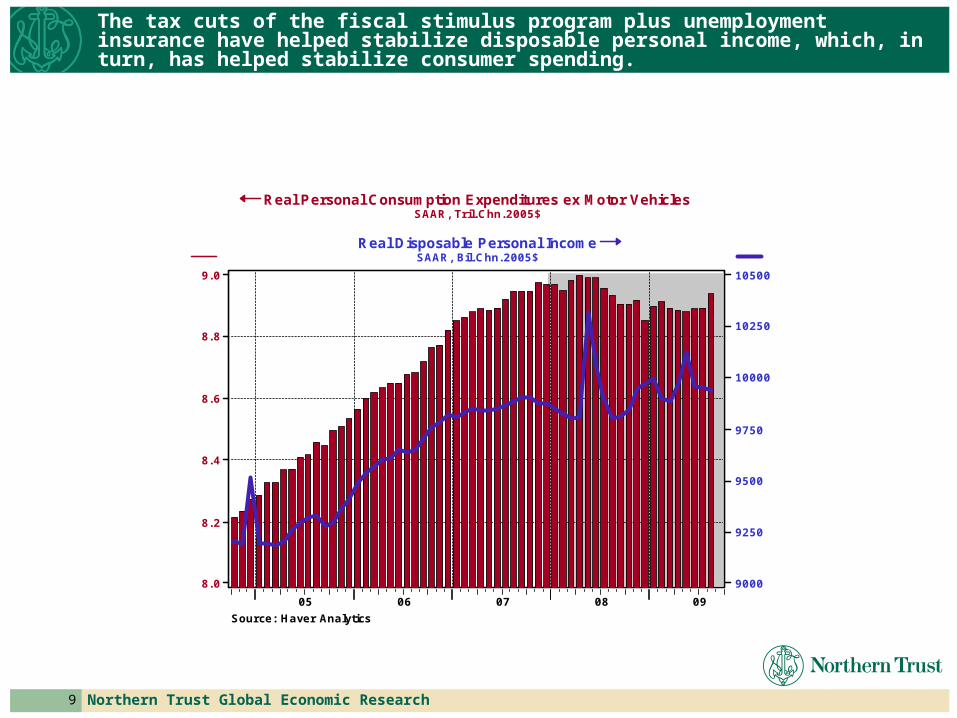

The tax cuts of the fiscal stimulus program plus unemployment insurance have helped stabilize disposable personal income, which, in turn, has helped stabilize consumer spending.

Real Personal Consumption Expenditures ex Motor VehiclesSAAR, Tr il. Chn. 2005$

Real Disposable Personal IncomeSAAR, Bil. Chn. 2005$

0908070605

Source: Haver Analytics

9. 0

8. 8

8. 6

8. 4

8. 2

8. 0

10500

10250

10000

9750

9500

9250

9000

10 Northern Trust Global Economic Research

Car and truck sales appeared to have bottomed even before “cash-for-clunkers.” There is natural replacement demand given that some of us are still driving 1995 Subarus!

Total Light Vehicle Retail Sales {Imported+Domestic}

SAAR, Mil. Units

09080706

Source: Autodata Corporation /Haver Analytics

18

16

14

12

10

8

18

16

14

12

10

8

11 Northern Trust Global Economic Research

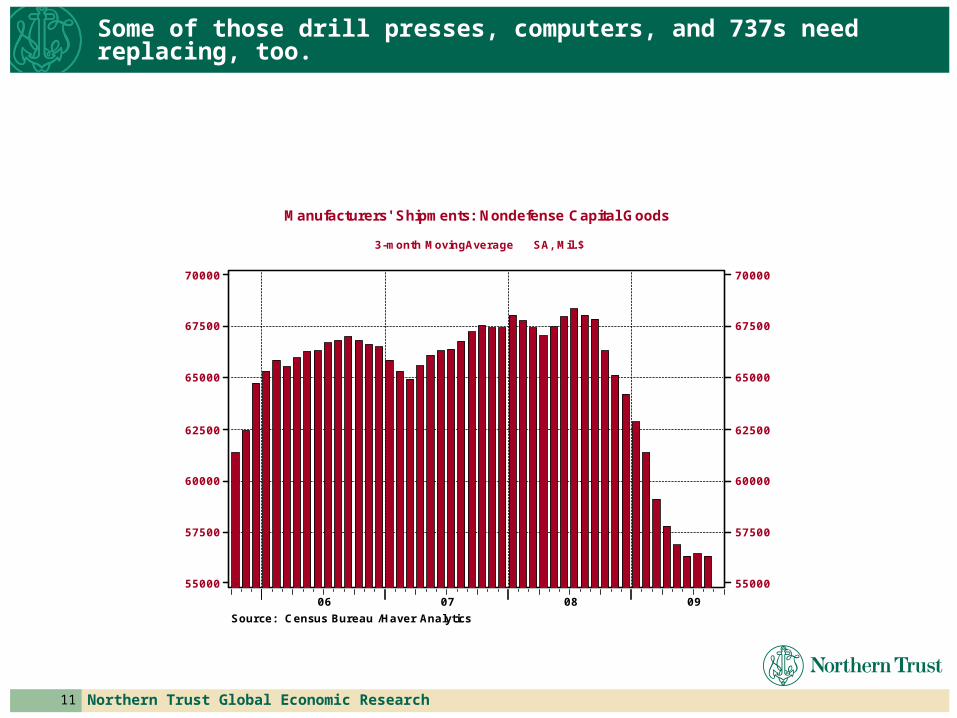

Some of those drill presses, computers, and 737s need replacing, too.

Manufacturers' Shipments: Nondefense Capital Goods

3-month MovingAverage SA, Mil. $

09080706

Source: Census Bureau /Haver Analytics

70000

67500

65000

62500

60000

57500

55000

70000

67500

65000

62500

60000

57500

55000

12 Northern Trust Global Economic Research

Economic activity is improving in the developed economies …

Euro Area16: Gross Domestic Product % Change - Annual Rate SA/WDA, Mil. Chn. 00. Euros

Japan: Gross Domestic Product % Change - Annual Rate SAAR, Bil. Chn. 2000. Yen

09080706

Sources: Eurostat, CAO /Haver

8

4

0

-4

-8

-12

-16

8

4

0

-4

-8

-12

-16

13 Northern Trust Global Economic Research

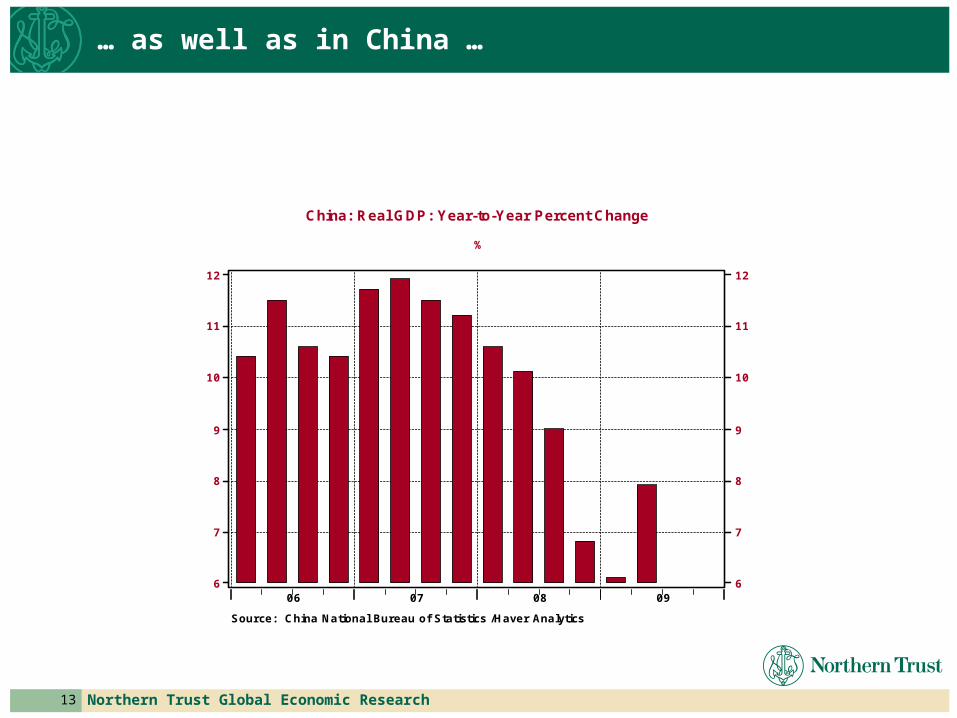

… as well as in China …

China: Real GDP: Year-to-Year Percent Change

%

09080706

Source: China National Bureau of Statistics /Haver Analytics

12

11

10

9

8

7

6

12

11

10

9

8

7

6

14 Northern Trust Global Economic Research

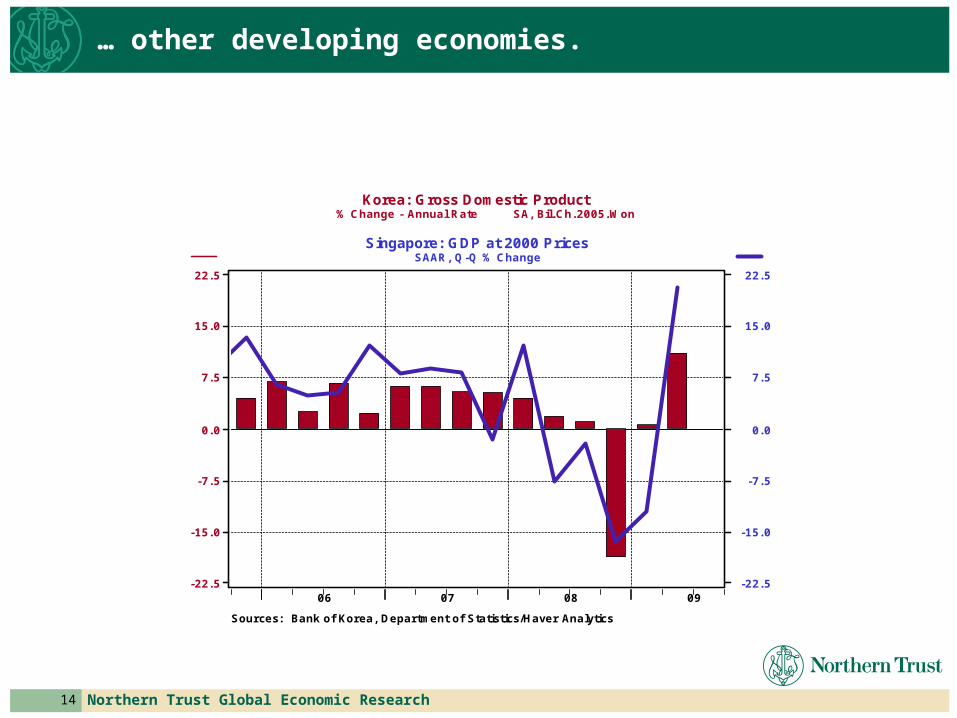

… other developing economies.

Korea: Gross Domestic Product % Change - Annual Rate SA, Bil. Ch. 2005. Won

Singapore: GDP at 2000 PricesSAAR, Q-Q % Change

09080706

Sources: Bank of Korea, Department of Statistics/Haver Analytics

22. 5

15. 0

7. 5

0. 0

-7. 5

-15. 0

-22. 5

22. 5

15. 0

7. 5

0. 0

-7. 5

-15. 0

-22. 5

15 Northern Trust Global Economic Research

The economic recovery underway in the rest of the world is boosting U.S. exports.

Exports, f.a.s.

SA, Mil. Chn. 2005$

090807Source: Bureau of the Census /Haver Analytics

105000

100000

95000

90000

85000

80000

75000

105000

100000

95000

90000

85000

80000

75000

16 Northern Trust Global Economic Research

State & local government infrastructure spending in Q2 grew at its fastest rate since 2001 due to the “Build America Bonds” program authorized by the fiscal stimulus program.

Real State & Local Govt Gross Investment

% Change - Annual Rate SAAR, Bil. Chn. 2005$

090807060504030201

Source: Bureau of Economic Analysis /Haver Analytics

30

20

10

0

-10

-20

-30

30

20

10

0

-10

-20

-30

17 Northern Trust Global Economic Research

Speaking of the stimulus program, for the most part, the federal spending portion of it has yet to kick in.

Real Federal Nondefense Gross Investment

% Change - Annual Rate SAAR, Bil. Chn. 2005$

0908

Source: Bureau of Economic Analysis /Haver Analytics

60

40

20

0

-20

-40

60

40

20

0

-20

-40

18 Northern Trust Global Economic Research

After the largest inventory liquidation in the post-WWII era, some businesses will have to begin restocking because their shelves are bare.

Change in Business Inventories as % of Final Sales of Domestic Product

SAAR, Chn. 2005$

050095908580757065605550

Source: Haver Analytics

2. 25

1. 50

0. 75

0. 00

-0. 75

-1. 50

2. 25

1. 50

0. 75

0. 00

-0. 75

-1. 50

19 Northern Trust Global Economic Research

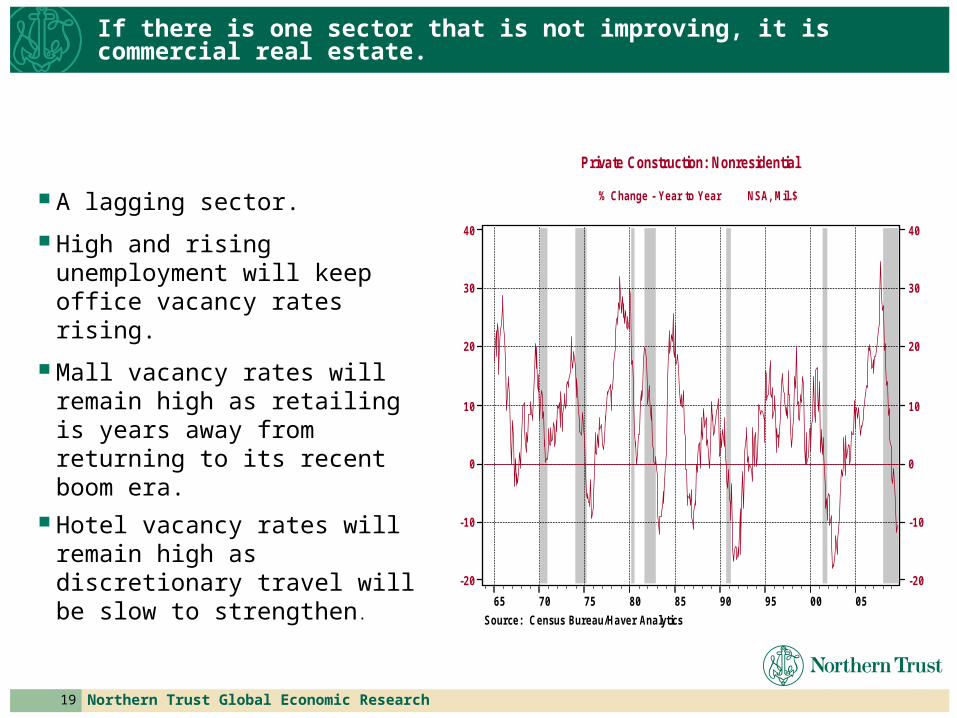

If there is one sector that is not improving, it is commercial real estate.

A lagging sector.

High and rising unemployment will keep office vacancy rates rising.

Mall vacancy rates will remain high as retailing is years away from returning to its recent boom era.

Hotel vacancy rates will remain high as discretionary travel will be slow to strengthen.

Private Construction: Nonresidential

% Change - Year to Year NSA, Mil. $

050095908580757065

Source: Census Bureau/Haver Analytics

40

30

20

10

0

-10

-20

40

30

20

10

0

-10

-20

20 Northern Trust Global Economic Research

This is likely to be another jobless recovery.

Growth will be too slow to quickly re-employ laid-off workers let alone employ new labor-market entrants.

The near-record low workweek means that production can be increased by extending the hours worked by current staff rather than having to hire additional employees.

There is going to be structural unemployment.

All Employees: Total Nonfarm Difference - Per iod to Per iod SA, Thous

Civilian Unemployment Rate: 16 yr +SA, %

05009590

Source: Bureau of Labor Statistics /Haver Analytics

750

500

250

0

-250

-500

-750

10

8

6

4

2

Financial market conditions are improving

22 Northern Trust Global Economic Research

After Lehman collapsed, the interbank loan market froze up. This market now is thawing as evidenced by the decline in Libor interest rates and the decline in discount-window borrowing from the Fed.

Interest Rate Spread: 3-Month Libor minus Fed Discount Rate percentage points

Reserve Bank Credit: Primary Credit to Depository InstitutionsAvg, Mil. $

0908Source: Haver Analytics

3. 00

2. 25

1. 50

0. 75

0. 00

-0. 75

120000

100000

80000

60000

40000

20000

0

23 Northern Trust Global Economic Research

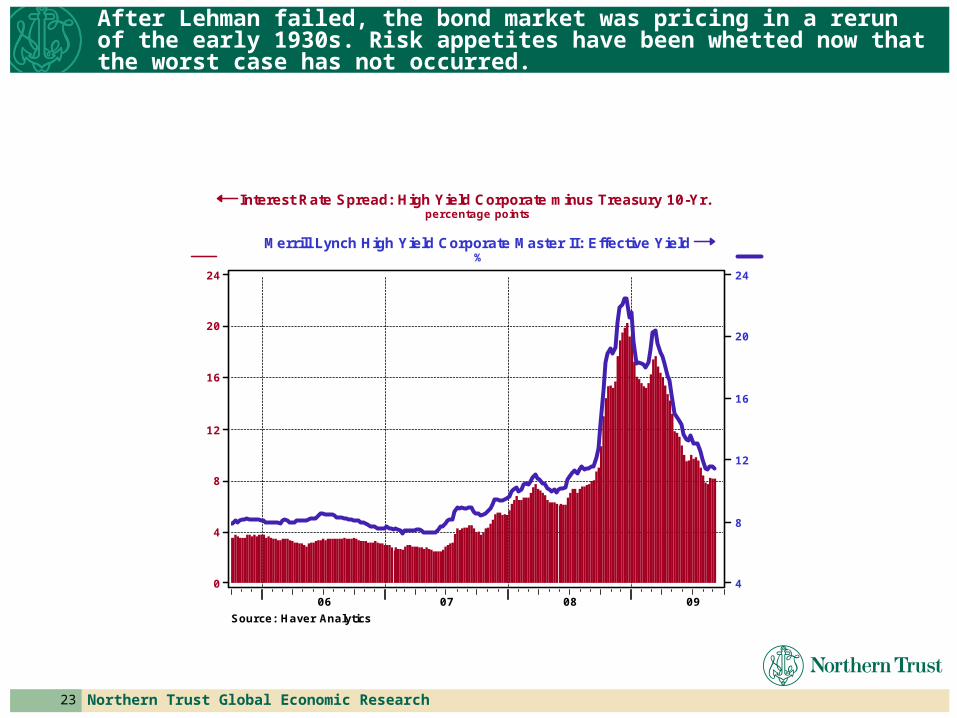

After Lehman failed, the bond market was pricing in a rerun of the early 1930s. Risk appetites have been whetted now that the worst case has not occurred.

Interest Rate Spread: High Yield Corporate minus Treasury 10-Yr.percentage points

Merrill Lynch High Yield Corporate Master II: Effective Yield%

09080706

Source: Haver Analytics

24

20

16

12

8

4

0

24

20

16

12

8

4

24 Northern Trust Global Economic Research

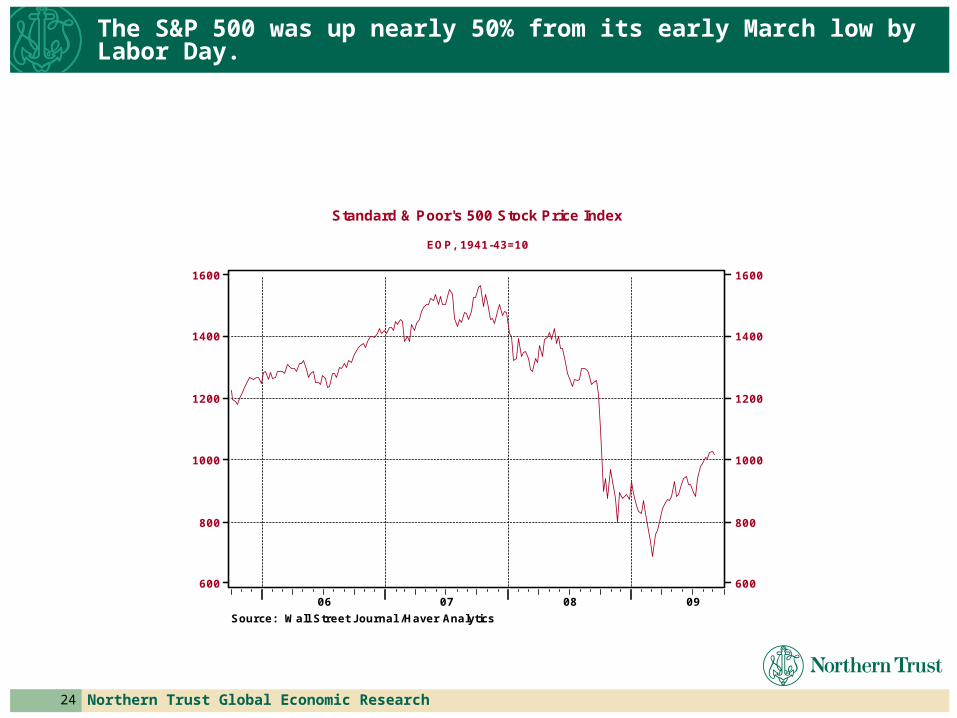

The S&P 500 was up nearly 50% from its early March low by Labor Day.

Standard & Poor's 500 Stock Price Index

EOP, 1941-43=10

09080706

Source: Wall Street Journal /Haver Analytics

1600

1400

1200

1000

800

600

1600

1400

1200

1000

800

600

The economy still faces strong headwinds

26 Northern Trust Global Economic Research

Commercial banks have experienced extremely high loan charge-off and delinquency rates.

Loan Charge-Off Rate: All Insured Commercial BanksSAAR,%

Loan Delinquency Rate: All Insured Commercial BanksSA,%

0500959085

Source: Federal Reserve Board /Haver Analytics

8

6

4

2

0

8

6

4

2

0

27 Northern Trust Global Economic Research

As a result, there has been an unprecedented decline in net lending by the private financial system.

Private Financial Sector Net Lending

SAAR, Bil. $

0500959085807570656055

Source: Haver Analytics

4000

3000

2000

1000

0

-1000

-2000

4000

3000

2000

1000

0

-1000

-2000

Financial institutions have acquired much-needed capital through the TARP program and new equity issuance in the market. But with a wave of commercial mortgage defaults expected, some institutions could become undercapitalized again.

Until financial institutions are confident of their longer-run capital adequacy, they will be unable and/or reluctant to create new credit, which will restrain the pace of the economic recovery.

It will take households some time to recover from their “overindulgence” in the past expansion.

30 Northern Trust Global Economic Research

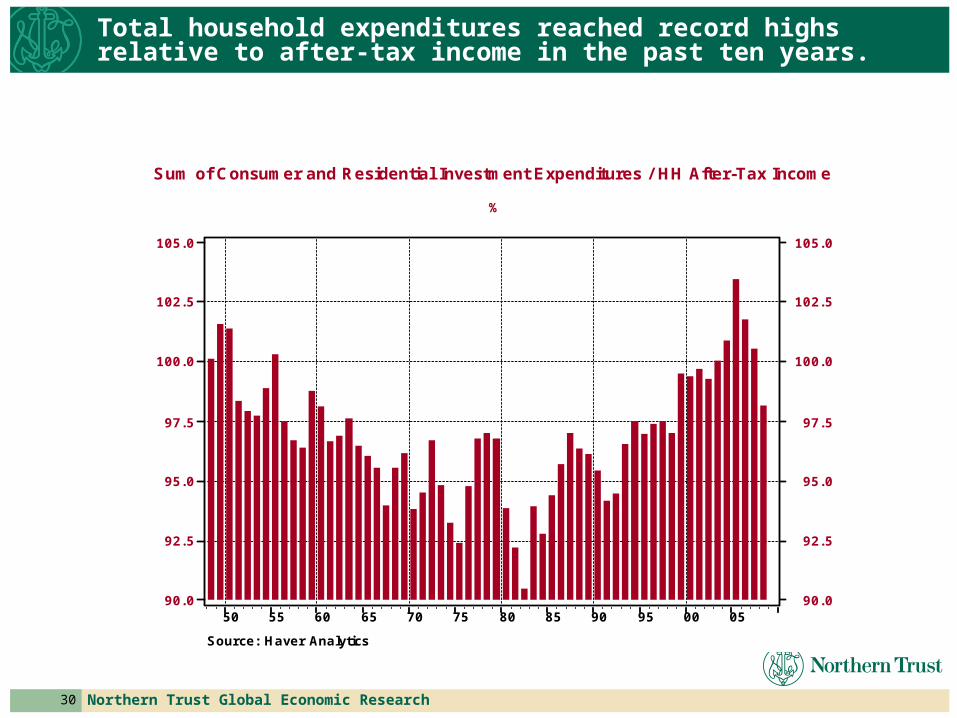

Total household expenditures reached record highs relative to after-tax income in the past ten years.

Sum of Consumer and Residential Investment Expenditures / HH After-Tax Income

%

050095908580757065605550

Source: Haver Analytics

105. 0

102. 5

100. 0

97. 5

95. 0

92. 5

90. 0

105. 0

102. 5

100. 0

97. 5

95. 0

92. 5

90. 0

31 Northern Trust Global Economic Research

In order to fund their increased spending, households stepped up their borrowing, largely against the equity in their houses, to record levels relative to their after-tax incomes.

Households: Borrowing as a % of After-Tax Income

0500959085807570656055

Source: Haver Analytics

16

12

8

4

0

-4

16

12

8

4

0

-4

32 Northern Trust Global Economic Research

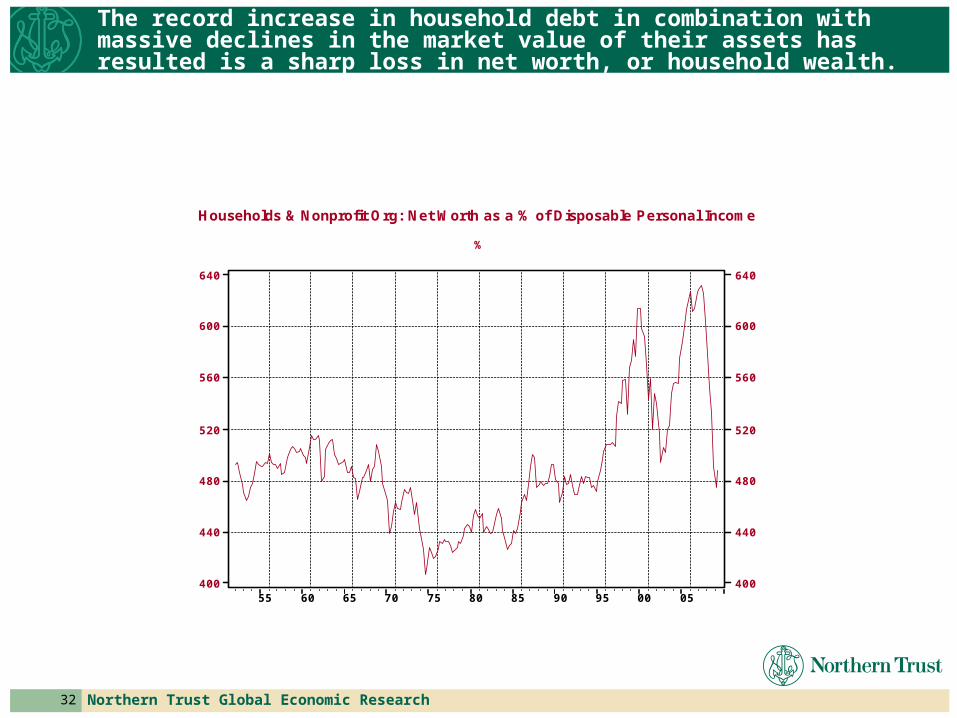

The record increase in household debt in combination with massive declines in the market value of their assets has resulted is a sharp loss in net worth, or household wealth.

Households & Nonprofit Org: Net Worth as a % of Disposable Personal Income

%

0500959085807570656055

640

600

560

520

480

440

400

640

600

560

520

480

440

400

33 Northern Trust Global Economic Research

Households are likely to rebuild their wealth through the purchases of stocks and bonds rather than the purchases of McMansions, SUVs and plasma TVs. All else the same, this would impart downward pressure on interest rates.

Households: Net Acquisition of Financial AssetsSAAR, Bil. $

Households & Nonprofit Orgs: Capital ExpendituresSAAR, Bil. $

0500959085807570656055

Source: Federal Reserve Board /Haver Analytics

2000

1600

1200

800

400

0

2000

1600

1200

800

400

0

Is the federal deficit a headwind?

35 Northern Trust Global Economic Research

Not right now. Although Treasury borrowing has soared in recent quarters, there has been an unprecedented net paydown of nonfederal debt.

Federal Government: Liabilities: Credit Market InstrumentsSAAR, Bil$

Nonfederal Sectors: Liabilities: Credit Market InstrumentsSAAR, Bil. $

0500959085807570656055

Sources: Federal Reserve Board, Haver Analytics

2500

2000

1500

1000

500

0

-500

2500

2000

1500

1000

500

0

-500

36 Northern Trust Global Economic Research

Thus, the pace of total nonfinancial sector borrowing has slowed, which has helped keep Treasury yields at relatively low levels.

Domestic Nonfinancial-Sector Borrowing as a % of GDP 4-qtr MovingAverage

Long-Term Treasury Composite, Over 10 Years% p. a.

0500959085807570656055

Source: Haver Analytics

24

20

16

12

8

4

0

24

20

16

12

8

4

0

37 Northern Trust Global Economic Research

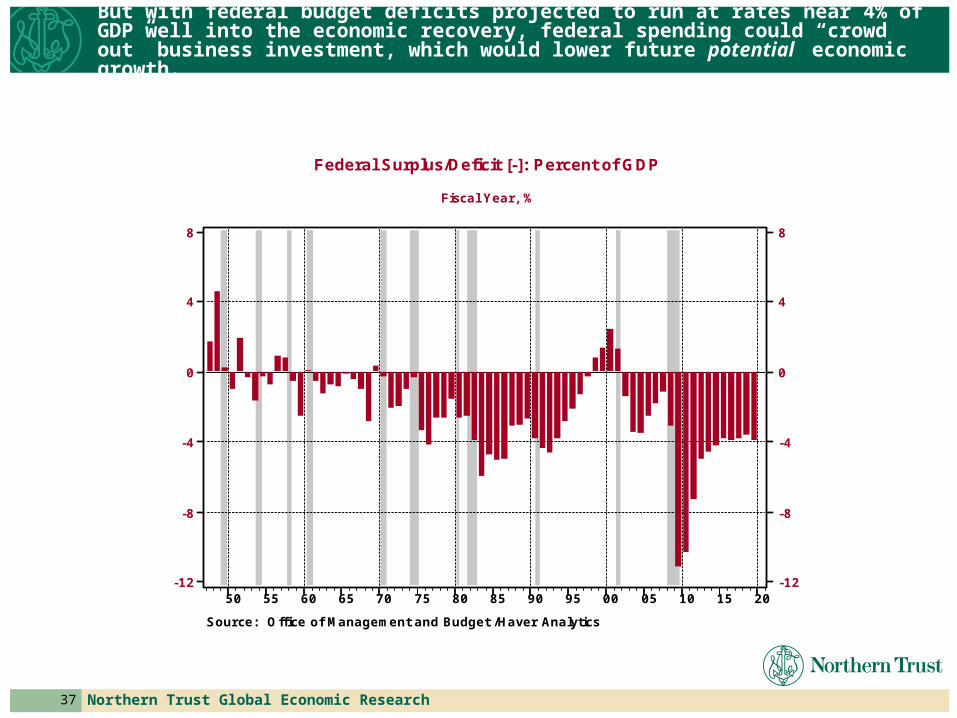

But with federal budget deficits projected to run at rates near 4% of GDP well into the economic recovery, federal spending could “crowd out” business investment, which would lower future potential economic growth.

Federal Surplus/Deficit [-]: Percent of GDP

Fiscal Year , %

201510050095908580757065605550

Source: Office of Management and Budget /Haver Analytics

8

4

0

-4

-8

-12

8

4

0

-4

-8

-12

Will the headwinds prevail, pushing the economy back into recession?

39 Northern Trust Global Economic Research

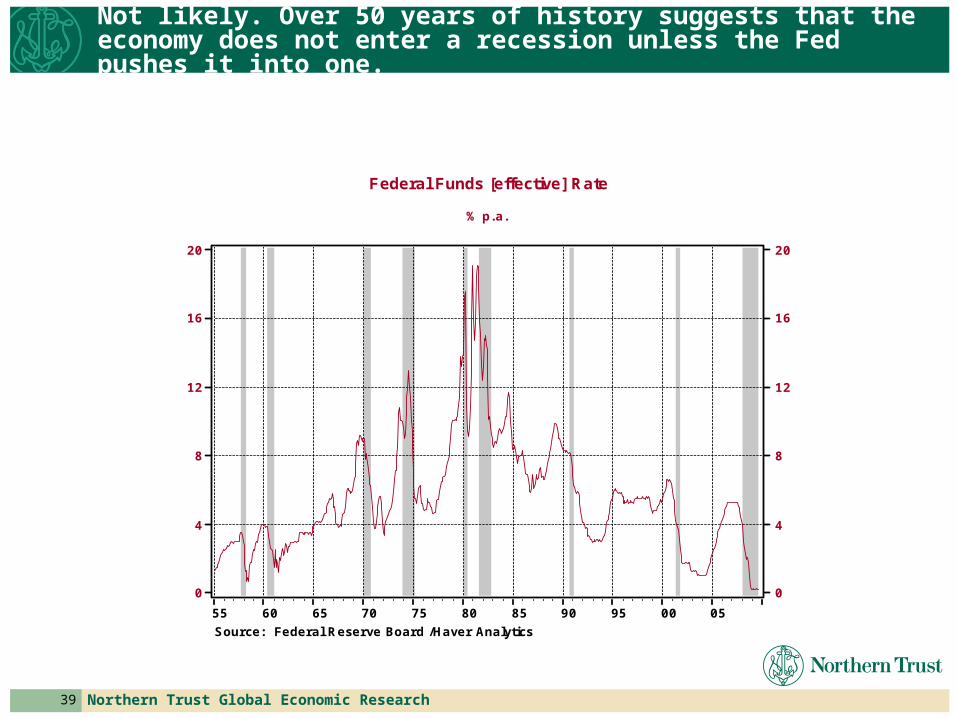

Not likely. Over 50 years of history suggests that the economy does not enter a recession unless the Fed pushes it into one.

Federal Funds [effective] Rate

% p. a.

0500959085807570656055

Source: Federal Reserve Board /Haver Analytics

20

16

12

8

4

0

20

16

12

8

4

0

What about inflation? Won’t all the credit the Fed has created in recent years guarantee rapid inflation?

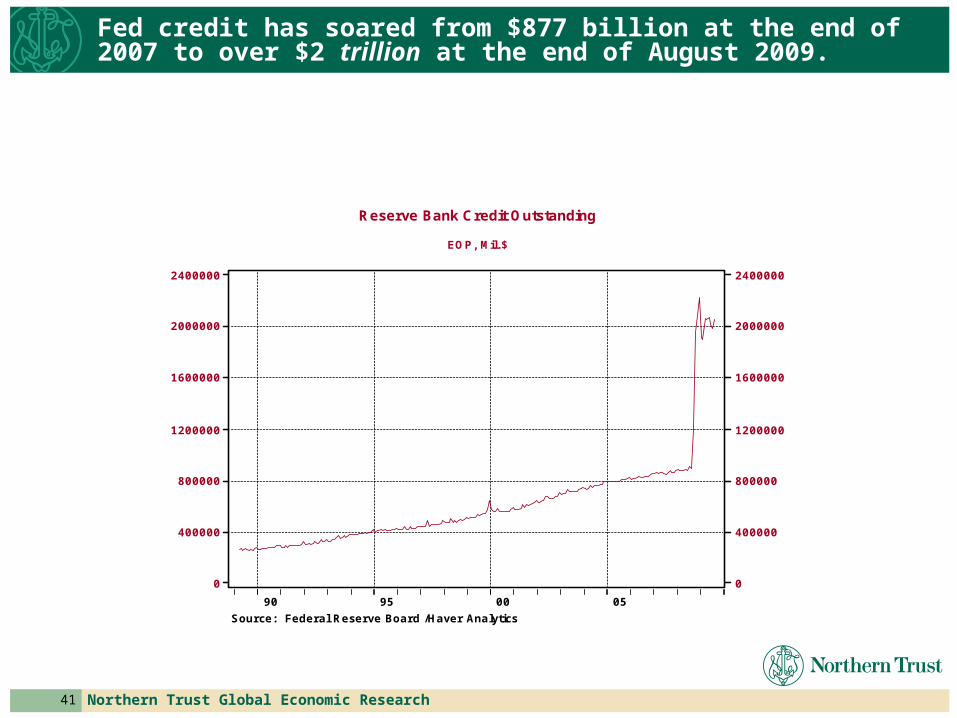

41 Northern Trust Global Economic Research

Fed credit has soared from $877 billion at the end of 2007 to over $2 trillion at the end of August 2009.

Reserve Bank Credit Outstanding

EOP, Mil. $

05009590

Source: Federal Reserve Board /Haver Analytics

2400000

2000000

1600000

1200000

800000

400000

0

2400000

2000000

1600000

1200000

800000

400000

0

42 Northern Trust Global Economic Research

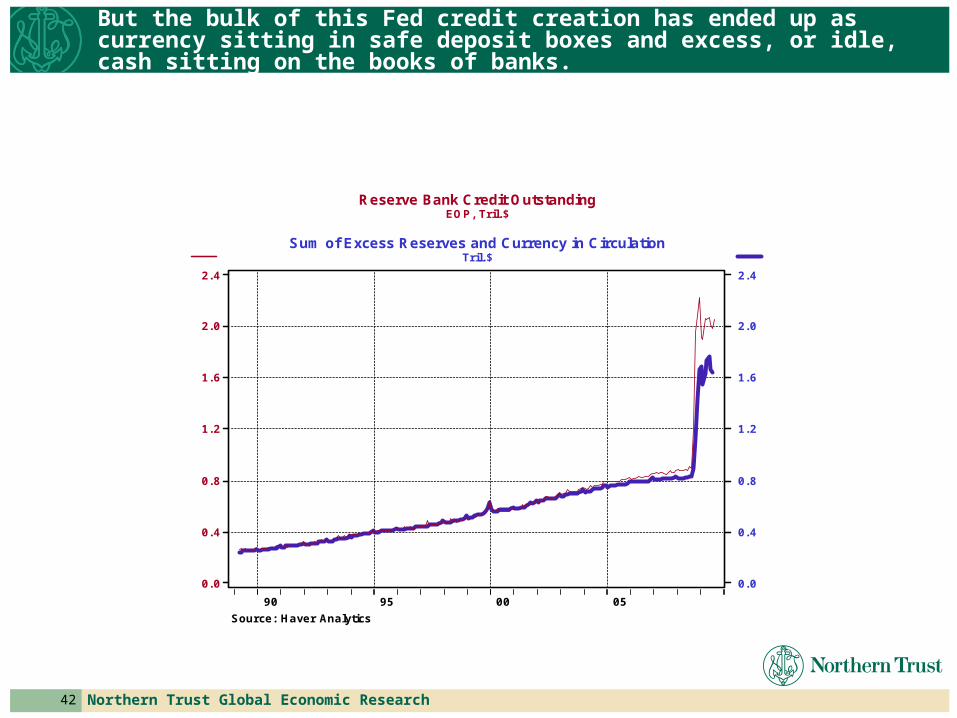

But the bulk of this Fed credit creation has ended up as currency sitting in safe deposit boxes and excess, or idle, cash sitting on the books of banks.

Reserve Bank Credit OutstandingEOP, Tr il. $

Sum of Excess Reserves and Currency in CirculationTril. $

05009590

Source: Haver Analytics

2. 4

2. 0

1. 6

1. 2

0. 8

0. 4

0. 0

2. 4

2. 0

1. 6

1. 2

0. 8

0. 4

0. 0

43 Northern Trust Global Economic Research

Although growth in the broad measure of money supply skyrocketed right after the Lehman failure, it has fallen back to Earth in recent months.

Money Stock: M2

6-month %Change-ann SA, Bil. $

0908070605040302010099989796

Source: Federal Reserve Board /Haver Analytics

16

12

8

4

0

16

12

8

4

0

44 Northern Trust Global Economic Research

To summarize:

The recovery has commenced.

Balance sheet repair by financial institutions and households will restrain the pace of the recovery through 2010.

Because the recovery will be muted initially, the unemployment rate is likely to continue rising through the first half of 2010, perhaps peaking out at a level over 10-1/2%.

The sharp increase in Fed credit is not currently inflationary, but has the potential to be if the Fed does not neutralize this credit at the appropriate time.

The earliest the Fed is likely to begin “neutralizing” the credit it has created is midyear 2010 and then, only tentatively.

Related Documents

![R G O PN O R F K Q O R F G L O G O N O ] T F R O N ^ F R S ...](https://static.cupdf.com/doc/110x72/617aae25fb20c8678c4c479e/r-g-o-pn-o-r-f-k-q-o-r-f-g-l-o-g-o-n-o-t-f-r-o-n-f-r-s-.jpg)