Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

June 1997 • Volume 34 • Number 2

n FINANCESDevelopmentFINANCIAL FLOWS TO AFRICA3 How Can Sub-Saharan Africa Attract More Private Capital Inflows?

Amar Bhattacharya, Peter J. Montief, and Sunii Snarma

7 Financial Liberalization in Africa and AsiaHow PHI and Mahmood Pradhan

RURAL ENERGY

11 Tackling the Rural Energy Problem in Developing CountriesDouglas F. Barnes, Robert van der P/as, and Willem Floor

GUEST ARTICLE 16 Japan's Economy Needs Structural Change

ALSO IN THIS ISSUE 22 Growth and the Environment: Allies or Foes?Vinod Thomas and Tamara Belt

25 The Reform of Wholesale Payment SystemsDavid Folkerts-Landau, Peter Garber, and Dirk Scj&toaker

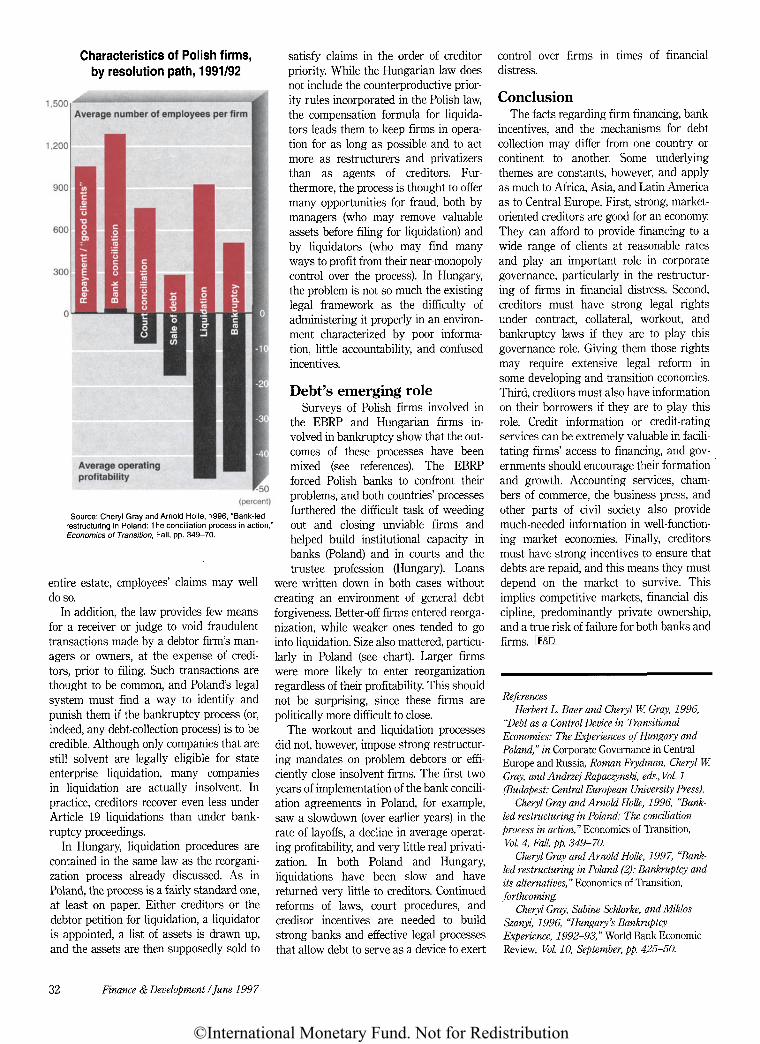

29 Creditors' Crucial Role in Corporate GovernanceCheryl W. Gray

33 Interest Rales: An Approach to LiberalizationHassanali Meriran and Bernard Laurens

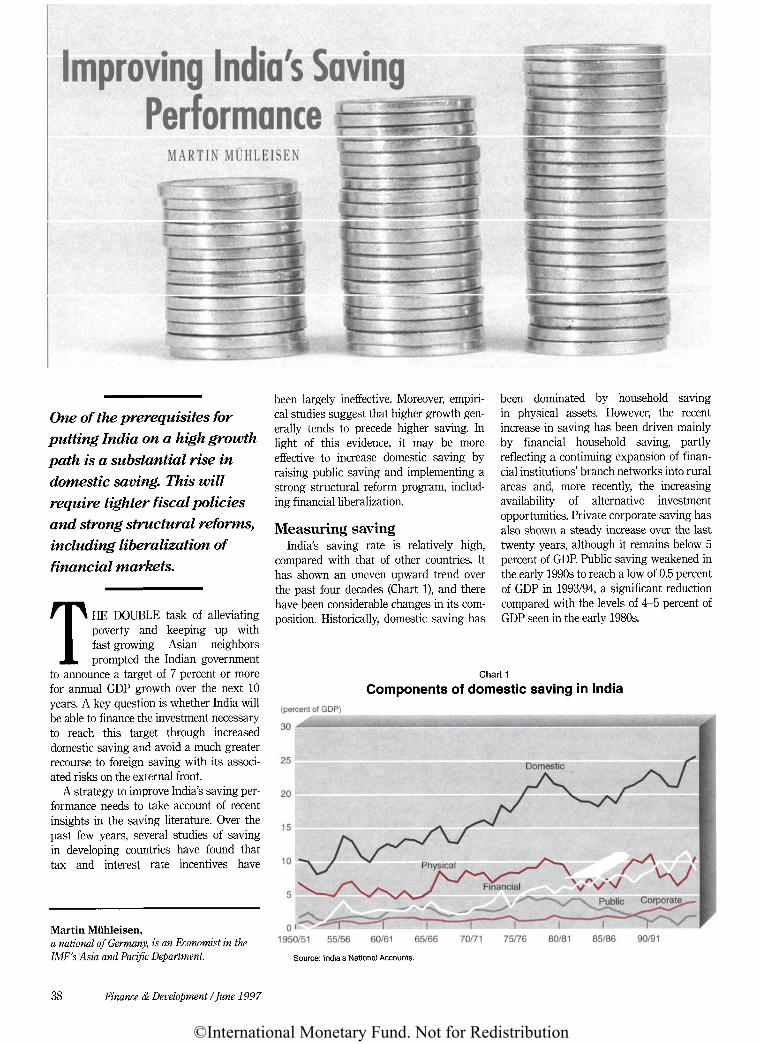

38 Improving India's Sating Performance

42 Islamic Financial Systems Zamir Iqbal

Maritn muhleisen

Takatoshi Ito

©International Monetary Fund. Not for Redistribution

A QUARTERLY PUBLICATION OF THE INTERNATIONAL MONETARY FUND AND THE WORLD BANK

DEPARTMENTS2 Letter from the Editor

20 World Economy in TransitionBias in the US Consumer Price Index: WhyIt Could Be Important Paul A. Armknechtand Paula R. De Masi

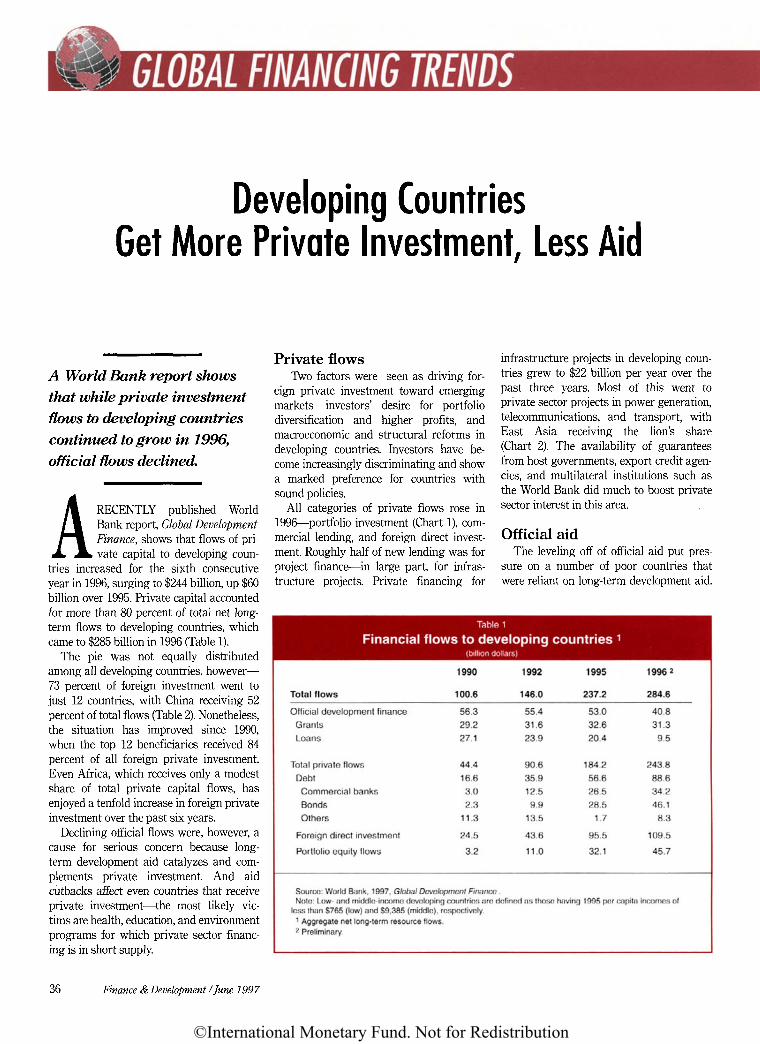

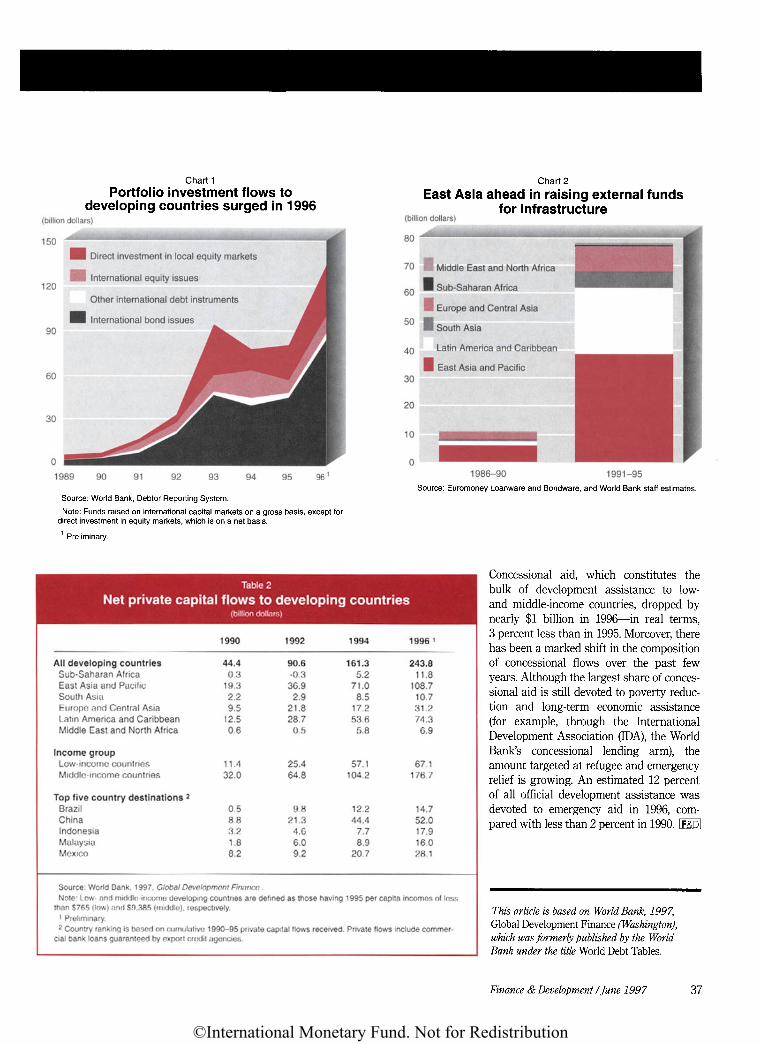

36 Global Financing TrendsDeveloping Countries Get More PrivateInvestment, Less Aid

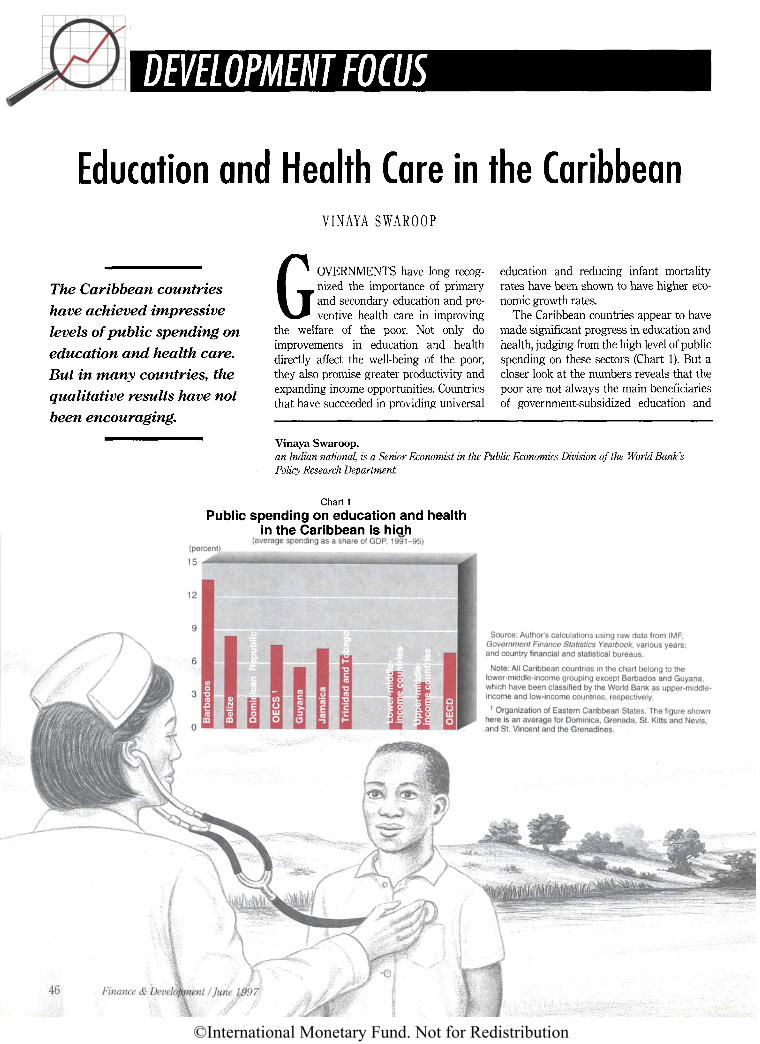

46 Development FocusEducation and Health Care in theCaribbean Vinaya Swaroop

55 Readers' Comments

BOOKS49 The Banking Panics of the Great Depression by Elmus Wicker

James M. Boughton

49 The Foreign Aid Business: Economic Assistance and Development Co-operationby Kunibert Rafter and H.W. Singer

David Dollar

51 The Clash of Civilizations and the Remaking of World Order by Samuel P. HuntingtonKe-young Chu

52 Fifty Years of Bretton Woods Twins (IMF and World Bank) by S.L.N. SimhaMargaret Garritsen de Vrles

52 Institutions lor Environmental Aid: Pitfalls and Promise, edited by Robert 0. Keohaneand Marc A. Levy

David Freestone

53 Central Banking in Developing Countries by Anand ChandavarkarManuel Guitian

54 Against the Tide: An Intellectual History of Free Trade by Douglas A. IrwinJ.M. Finger

© 1997 by the International Monetary Fund and the International Bank for Reconstruction andDevelopment/The World Bank. All rights reserved. Requests for permission to reproduce articlesshould be sent to the Editor. Finance & Development will normally give permission promptly, andwithout asking a fee, when the intended reproduction is for noncommercial purposes.

FINANCEDevelopment is published quarterlyin English, Arabic, Chinese, French,German, Portuguese, and Spanishby the International Monetary Fundand the International Bank forReconstruction and Development,Washington, DC 20431, USA.

Opinions expressed in articles andother materials are those of theauthors; they do not necessarily reflectIMF or World Bank policy.

Claire LiuksilaEDITOR-IN-CHIEF

Asimina CaminisSENIOR EDITORPaul GleasonASSISTANT EDITOR

Luisa MacdonaldART EDITORJune LavinEDITORIAL ASSISTANT

Jessie HamiltonADMINISTRATIVE ASSISTANT

ADVISORS TO THE EDITOR

Adrienne CheastyWilliam EasterlyEmmanuel JimenezNaheed KirmaniAnne McGuirkGobind NankaniLant PritchettPeter J. QuirkOrlando RoncesvallesGarry ScninasiMarcelo Selowsky

Periodicals-class postage is paid atWashington, DC and at additionalmailing offices. The English edition isprinted at Lancaster Press, Lancaster,PA. Postmaster: please send change ofaddress to:

Finance & Development700 19th Street NWWashington, DC 20431 USATelephone: (202) 623-8300Fax Number: (202) 623-4738E-mail: [email protected] site:http://www.worldbank.org/fanddEnglish edition ISSN 0015-1947

©International Monetary Fund. Not for Redistribution

LETTER FROM THE EDITOR

GOVERNMENT UNDER THE SPOTLIGHT

World Development Report 1997The State in a Changing World

World BankPublications

Government is in the spotlight in this twentieth annual edition of the WorldDevelopment Report. This year the World Bank's flagship publication isdevoted to the role and effectiveness of the state, a topic that ranks high on theagenda in developing and industrial countries alike. The Report looks at whatthe state should do, how it should do it, and how it can do it better in a rapidlychanging world.

June 1997.354 pages.English editions:Paperback: Stock no. 61114-F (ISBN0-19-521114-6). $25.95.Hardcover: Stock no. 61115-F (ISBN 0-19-521115-4). $49.95.Translations forthcoming in paperback.

Published for the World Bank by Oxford University Press.

Visit our Website: http://www.worldbank.org

For IS customers, contact The World Bank, P.O. Box 7247-8619. Philadelphia, PA 19170-8619. Phone: (703) 661-1580, Fax: (703) 661-1501. Shipping and handling: US$5.00. Airmaildelivery outside the US is US$13.00 for one item plus US$6.00 for each additional item.Payment by US$ check drawn on a US bank payable to the World Bank or by VISA, MasterCard,or American Express. Customers outside the US, please contact your World Bank distributor.

1265

WW w hile many developing countries elsewhere are enjoying rapid growth, fueled in significant part by inflows of private for-

eign capital, many sub-Saharan African countries are stuck in low gear. As official capital flows dwindle in a climate of aid fatigueand budget pressures in industrial countries, sub-Saharan Africa's political leaders increasingly agree that the region's prospectshinge on its more thorough integration into the global economy. But how can this be accomplished? The lead articles in this issuediscuss two specific areas in which sub-Saharan African countries might usefully undertake reforms.

The article by Amar Bhattacharya, Peter Montiel, and Sunil Sharma notes that although the recent surge in international privatecapital flows to developing countries has largely bypassed sub-Saharan Africa, some countries in the region have received consider-ably more than others. It examines the reasons for their differing success and suggests ways in which the sub-Saharan Africancountries might attract more foreign private capital.

Since financial liberalization is now widely recognized as a crucial element in countries' economic development, developing coun-tries have become increasingly interested in how they can successfully bring it about. In their article, Huw Fill and MahmoodPradhan examine the experiences of Asian and sub-Saharan African countries in liberalizing their financial systems. They notethat Asian countries' liberalization efforts generally have been more successful and highlight some lessons from the Asian experi-ence that might be applied to countries in sub-Saharan Africa.

Over the past five years, the economic situation in much of sub-Saharan Africa has improved. An increasing number of countrieshave persevered with adjustment and structural reform, and their efforts are beginning to bear fruit. Still, the road to sustainableeconomic growth in the region as a whole will be neither short nor easy. But, as the authors of these articles observe, sub-SaharanAfrican countries can derive substantial benefits if they make determined efforts to reform their economies.

Claire Liuksila

Editor-in-Chief

'.- i'in<nii'( A- I h T t ' l t i / / / ! / ! i t l ' l i u i t t(.t(.>i

©International Monetary Fund. Not for Redistribution

International private capitalhas largely bypassed sub-Saharan Africa. But this factmasks significant differencesamong countries. Whataccounts for these differences,and what actions can sub-Saharan countries take toattract more private capital?

O

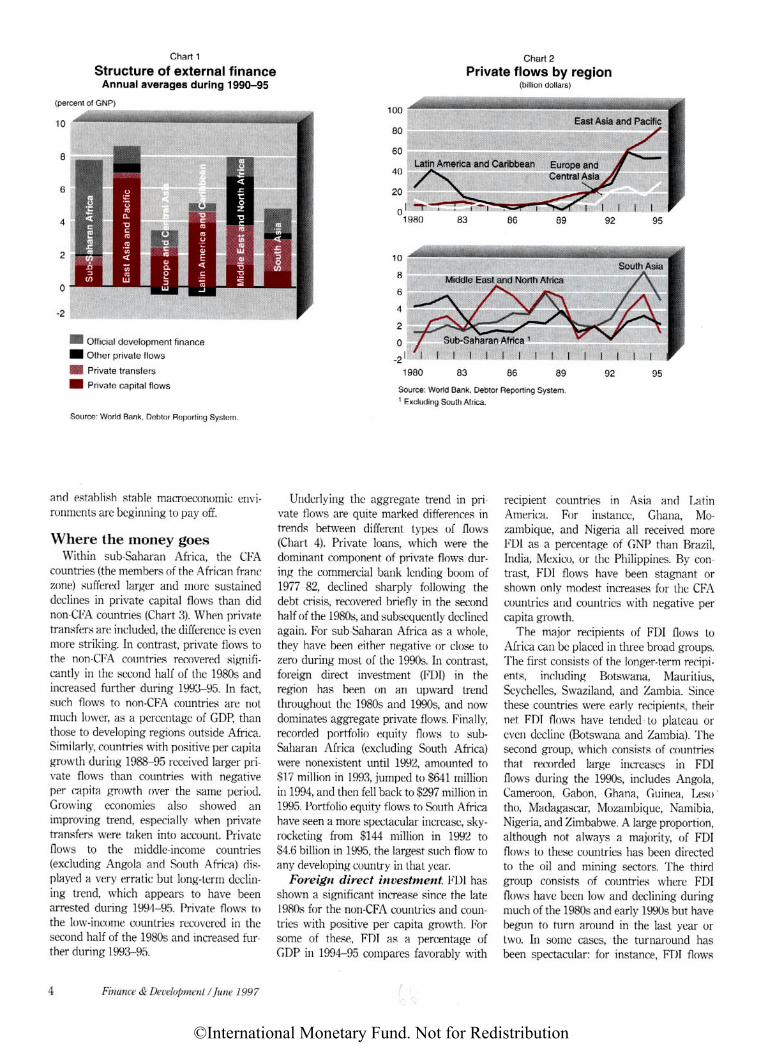

FFICIAL FINANCE accounts fora higher proportion of externalfinancial flows to sub-SaharanAfrica than to any other devel-

oping region (Chart 1). Despite the sharpincrease in official finance to Europe andCentral Asia in the 1990s, sub-SaharanAfrica continues to account for thelargest—and, indeed, a growing—share

Amar Bhattacharya,an Indian national, is an Economic Adviser inthe World Bank's International EconomicsDepartment.

of official development finance; during1990-95, the latter region received 26 per-cent of total official development financeprovided to all developing countries. Al-most 95 percent of this was made availableon either highly concessional or grantterms.

In contrast, the share of long-term pri-vate capital—defined as the sum of privateloans (bank loans plus bond finance), port-folio equity flows, and foreign direct invest-ment—flowing to sub-Saharan Africa islower, as a percentage of GNP, than that ofall other developing regions except SouthAsia. Private transfers and other privateflows (including returning flight capital)play a relatively important role in sub-Saharan Africa, as they do in such otherregions as South Asia and the Middle Eastand North Africa. Nonetheless, adding inthese flows does not change the picture; infact, total private flows (including unre-quited transfers) to sub-Saharan Africa arelower, as a percentage of GNP, than for allother developing regions.

Along with Latin America, sub-SaharanAfrica saw the sharpest decline in privateflows in the aftermath of the debt crisis(Chart 2). Private flows to sub-SaharanAfrica began to recover in the second halfof the 1980s, but, in contrast to the experi-ence of most other developing regions, theydeclined again in the early 1990s beforerecovering modestly during 1993-95. Formost years during 1982-95, annual long-term private capital flows have been lessthan half the peak of $5.5 billion reached in1982.

Why has sub-Saharan Africa been leftout? A survey of commercial banks, invest-ment banks, and mutual fund managersconducted by the authors reveals thatinvestors perceive the risks to be higherthere than in other regions and face greaterimpediments to identifying and exploitingprofitable opportunities in sub-SaharanAfrica than elsewhere. Despite these handi-caps, some countries in the region areattracting private capital flows. Theirefforts to adopt outward-looking policies

Peter J. Montiel,a US national, is Professor of Economics atWilliams Cottege.

Sunil Sharma,an Indian national, is a Senior Economist in theEmerging Markets Studies Division of the IMF'sResearch Department.

Finance & Development /June 1997 3

How Can Sub-Saharan Africa Attract MorePrivate Capital Inflows?

AMAR BHATTACHARYA, PETER J. MONTIEL, AND SUNIL SHARMA

©International Monetary Fund. Not for Redistribution

©International Monetary Fund. Not for Redistribution

ChartsPrivate flows to sub-Saharan Africa 1

(percent of GDP)

Chart 4

Composition of private flows tosub-Saharan Africa 1

Source: Amar Bhattacharya, Peter J. Montiel, and Sunil Sharma, 1996, "Private CapitalFlows to Sub-Saharan Africa: An Overview of Trends and Determinants," unpublished,World Bank and International Monetary Fund (Washington).

1 Excluding Angola and South Africa.

Source: World Bank, Debtor Reporting System.1 Excluding South Africa.

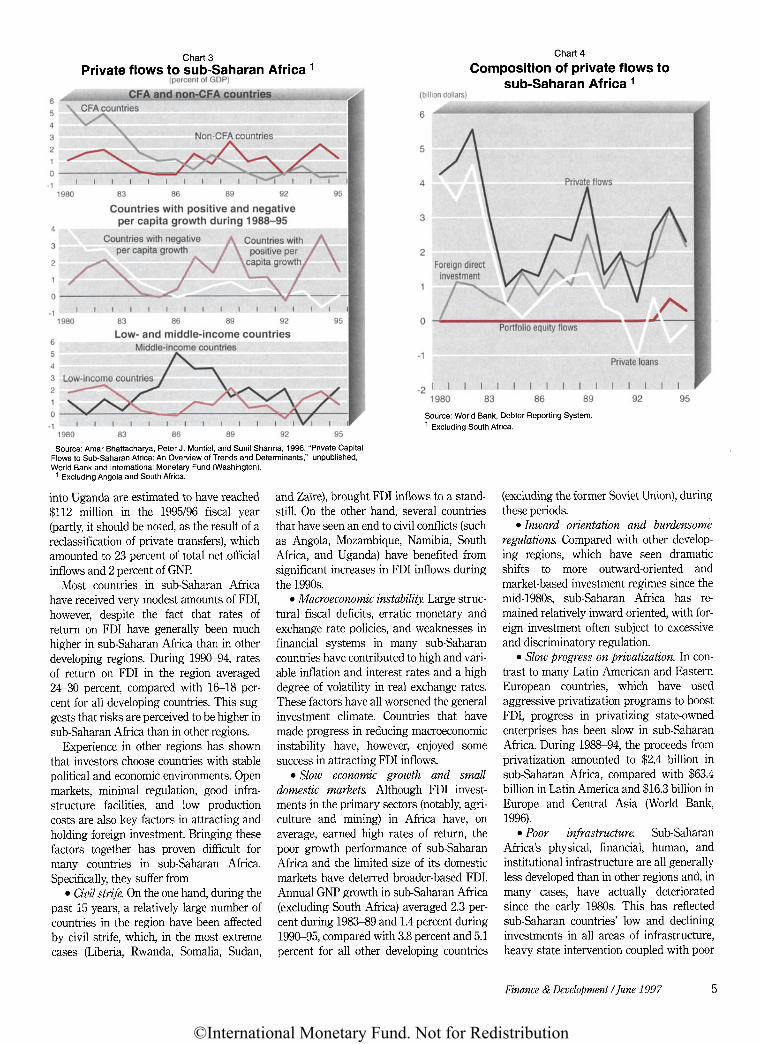

into Uganda are estimated to have reached$112 million in the 1995/96 fiscal year(partly, it should be noted, as the result of areclassification of private transfers), whichamounted to 23 percent of total net officialinflows and 2 percent of GNP.

Most countries in sub-Saharan Africahave received very modest amounts of FDI,however, despite the fact that rates ofreturn on FDI have generally been muchhigher in sub-Saharan Africa than in otherdeveloping regions. During 1990-94, ratesof return on FDI in the region averaged24-30 percent, compared with 16-18 per-cent for all developing countries. This sug-gests that risks are perceived to be higher insub-Saharan Africa than in other regions.

Experience in other regions has shownthat investors choose countries with stablepolitical and economic environments. Openmarkets, minimal regulation, good infra-structure facilities, and low productioncosts are also key factors in attracting andholding foreign investment. Bringing thesefactors together has proven difficult formany countries in sub-Saharan Africa.Specifically, they suffer from

• Civil strife. On the one hand, during thepast 15 years, a relatively large number ofcountries in the region have been affectedby civil strife, which, in the most extremecases (Liberia, Rwanda, Somalia, Sudan,

and Zaire), brought FDI inflows to a stand-still. On the other hand, several countriesthat have seen an end to civil conflicts (suchas Angola, Mozambique, Namibia, SouthAfrica, and Uganda) have benefited fromsignificant increases in FDI inflows duringthe 1990s.

• Macroeconomk instability. Large struc-tural fiscal deficits, erratic monetary andexchange rate policies, and weaknesses infinancial systems in many sub-Saharancountries have contributed to high and vari-able inflation and interest rates and a highdegree of volatility in real exchange rates.These factors have all worsened the generalinvestment climate. Countries that havemade progress in reducing macroeconomicinstability have, however, enjoyed somesuccess in attracting FDI inflows.

• Slow economic growth and smalldomestic markets. Although FDI invest-ments in the primary sectors (notably, agri-culture and mining) in Africa have, onaverage, earned high rates of return, thepoor growth performance of sub-SaharanAfrica and the limited size of its domesticmarkets have deterred broader-based FDI.Annual GNP growth in sub-Saharan Africa(excluding South Africa) averaged 2.3 per-cent during 1983-89 and 1.4 percent during1990-95, compared with 3.8 percent and 5.1percent for all other developing countries

(excluding the former Soviet Union), duringthese periods.

• Inward orientation and burdensomeregulations. Compared with other develop-ing regions, which have seen dramaticshifts to more outward-oriented andmarket-based investment regimes since themid-1980s, sub-Saharan Africa has re-mained relatively inward-oriented, with for-eign investment often subject to excessiveand discriminatory regulation.

• Slow progress on privatization. In con-trast to many Latin American and EasternEuropean countries, which have usedaggressive privatization programs to boostFDI, progress in privatizing state-ownedenterprises has been slow in sub-SaharanAfrica. During 1988-94, the proceeds fromprivatization amounted to $2.4 billion insub-Saharan Africa, compared with $63.4billion in Latin America and $16.3 billion inEurope and Central Asia (World Bank,1996).

• Poor infrastructure. Sub-SaharanAfrica's physical, financial, human, andinstitutional infrastructure are all generallyless developed than in other regions and, inmany cases, have actually deterioratedsince the early 1980s. This has reflectedsub-Saharan countries' low and declininginvestments in all areas of infrastructure,heavy state intervention coupled with poor

Finance & Development /June 1997 5

©International Monetary Fund. Not for Redistribution

implementation capacity, and limited suc-cess thus far in expanding private provi-sion of basic infrastructure.

• High wage and production costs. As aresult of the macroeconomic and micro-economic factors listed above and, in somecases, countries' labor market policies,wage costs in the region tend to be highrelative to productivity levels. Overallcosts of production are also generallyhigher than elsewhere—for example,almost double those prevailing in low-income Asian countries.

Private loans. Private loans have beenon a declining trend for all country groupsin sub-Saharan Africa. Unlike other devel-oping regions where commercial bankloans have shown a sharp turnaround inthe 1990s, such lending to most sub-Saharan countries has remained negativeor at very low levels. In part, this hasoccurred because most African countrieshave not yet restored their access to finan-cial markets. In contrast to other regions,where creditworthiness ratings have showna marked improvement in the 1990s, credit-worthiness ratings for sub-SaharanAfrican countries have remained muchlower, on average, and are only just begin-ning to improve. The main factors believedto have contributed to sub-Saharan coun-tries' generally low levels of creditworthi-ness are high political risk, weak growthand export performance, macroeconomicinstability, and high levels of indebtedness.Low levels of commercial bank borrowingalso reflect decisions made by many coun-tries to restrict such borrowing, especiallyfor general budgetary support.

Portfolio equity Hows, Althoughportfolio investment into sub-SaharanAfrica (with the notable exception of SouthAfrica) is still extremely small comparedwith flows into other emerging markets,there are encouraging signs of growinginvestor interest. Since 1994, more than 12Africa-oriented funds have been set up witha total size of more than $1 billion. Initially,the focus of these funds was primarily theSouth African market, but the base hasbeen broadening to encompass a growing(though still limited) number of otherAfrican countries, including Botswana,Cote d'lvoire, Ghana, Kenya, Mauritius,Zambia, and Zimbabwe. This growing poolof portfolio investment is already perceivedto bring important benefits including liq-uidity, incentives for privatization, andpressure for policy reforms and improve-ment of the financial infrastructure.

Investors, looking ahead, expressguarded optimism about making portfolio

6 Finance & Development /June 1997

investments in Africa. In sharp contrast tothe situation only a few years ago, virtuallyall stock markets on the continent have nowbeen opened up to foreign investment, andin many countries there has been a shiftaway from state-centered ideologies. Anumber of factors are, however, still seen asconstraining portfolio investment: inves-tors view political instability and weakmacroeconomic fundamentals as the mostimportant impediments.

Many structural weaknesses are alsoviewed as inhibiting investment. A reduc-tion in the transaction costs of doing busi-ness will be critical. The setting up of anefficient securities trading and settlementsystem and the presence of internationalcustodians are important elements of thefinancial infrastructure that is needed toattract foreign investors. Corruption in thepublic sector, including the judiciary, iscited by many investors as not only increas-ing transaction costs but also acting as adeterrent in its own right.

The supply of assets is still very limited,and, in addition to the public companiesalready listed on stock exchanges, the num-ber of private firms listed needs to beincreased. In some cases, privatization ofpublic assets offers the best avenue forincreasing the supply of assets in the econ-omy and attracting foreign investors. Whilefcireign investment can play a valuable roleiri stimulating capital markets in Africa, thegrowth and stability of these markets willrequire the development of a healthy baseof domestic investors. Pension reform andthe promotion of mutual funds couldencourage domestic investment in fledglingstock markets. Over the longer term, defi-ciencies in human capital, infrastructure,and institutions need to be addressed ifmore African countries are to attract thegrowing pool of portfolio investment.

The futureAid fatigue and fiscal pressures in the

industrial countries have made it more diffi-cult for developing countries to attract offi-cial capital flows. In such an environment,sub-Saharan Africa has no recourse but totap private foreign capital to raise produc-tivity levels necessary for sustainedincreases in living standards. With manyAsian and Latin American countries grow-ing rapidly and far ahead of most Africancountries in terms of putting in place thefinancial infrastructure needed to effi-ciently absorb foreign capital, most Africancountries will have to undertake speedypolicy and structural reform to attract pri-vate flows. Market discipline is likely to be

severe in the initial stages, and countriesthat backtrack on reform will find theiraccess to international capital limited andwhat is available to them will be providedon costlier terms.

At the micro level, sub-Saharan countrieswill need to take concerted action on manyfronts:

• improve infrastructure;• strengthen banking systems;• develop capital markets by accelerat-

ing the pace of privatization and broaden-ing the domestic investor base;

• formulate an appropriate regulatoryframework and a more liberal investmentregime;

• introduce competitive labor marketpolicies while creating and maintaininginstitutions for upgrading human capital;and

• reform the judiciary system and con-tain corruption.

It needs emphasizing that a piecemealapproach, even one including tax holidaysand other investment incentives, is unlikelyto sway investor decisions and attract inter-national resources on a sustainable basis.

While microeconomic factors are difficultto quantify, the macroeconomic factorsused in the empirical analysis we havecarried out (Bhattacharya, Montiel, andSharma, 1996) yielded clear-cut conclu-sions. In sub-Saharan Africa, economiccharacteristics like output growth, open-ness, relative stability of real effectiveexchange rates, low external debt, and highinvestment rates have encouraged privatecapital flows. The first three of these havebeen crucial for drawing in FBI and the lasttwo factors, coupled with output growth,have been particularly important forobtaining foreign private loans. IF&DI

Suggestions for further reading:Amar Bhattacharya, Peter J. Montiel, and

Sunil Sharma, 1996, "Private Capital Flows toSub-Saharan Africa: An Overview of Trendsand Determinants," unpublished, World Bankand International Monetary Fund(Washington).

Louis Kasekende, Damoni Kitabire, andMatthew Martin, 1996, "Capital Inflows andMacroeconomic Policy in Sub-Saharan Africa,"Jerome Levy Economics Institute, Bard College,Working Paper No. 158.

Peter J. Montiel, 1995, "Financial Policiesand Economic Growth: Theory, Evidence andCountry Specific Experience from Sub-SaharanAfrica," Special Paper No. 8, African EconomicResearch Consortium (AERC).

World Bank, 1996, World Debt Tables(Washington).

©International Monetary Fund. Not for Redistribution

ylsfaw countries have gener-ally been more successful thanAfrican countries in liberaliz-ing their financial systems.Why have their outcomes dif-fered? Asia's experience withliberalization offers some use-ful lessons for Africa.

B OTH ECONOMIC theory and

practical experience suggest thatfinancial liberalization can stimu-late economic development. Until

the 1980s, extensive government interven-tion was the norm in the financial marketsof developing countries. Ceilings wereimposed on bank interest rates; credit wasallocated by administrative decision ratherthan market criteria; and inflows of foreign

capital were strictly controlled. Over thelast twenty years, however, many develop-ing countries—persuaded by both the theo-retical arguments made in support ofliberalization and the experience of manyof the rapidly growing countries—havebegun to liberalize their financial marketsby abolishing these types of controls.

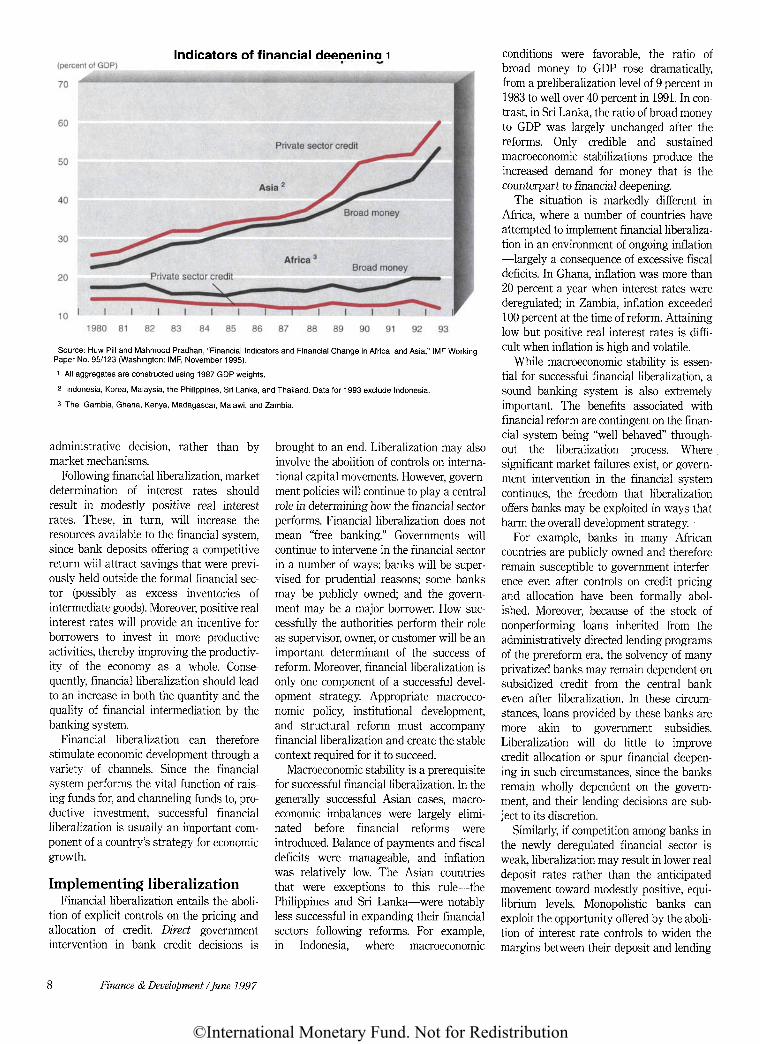

The results of financial liberalizationappear quite different for Asia and Africa.If one uses the ratio of broad money (cashplus deposits in the commercial bankingsystem) to national income as a measure offinancial deepening and the success ofreform, liberalization appears to have beenmuch more successful in Asia (see chart).However, this simple comparison can bemisleading. Financial reform was imple-mented much earlier in most Asian coun-tries than in Africa; for example, Malaysialiberalized interest rates in 1978. In con-trast, even the earliest African liberalizers(The Gambia and Ghana) began to intro-duce reform only in the late 1980s.Moreover, financial development is only

one part of a broader process of economicdevelopment, of which it is both a causeand a consequence. The generally moresuccessful economic performance of Asianeconomies over the last two decades hasunderpinned and enlarged the benefits offinancial sector reforms.

Nevertheless, the Asian experience offerssome important lessons for Africa.Comparison of the experiences of the twocontinents suggests that if financialreforms are to succeed, they must be imple-mented in an appropriate macroeconomic,financial, and institutional environment.

Benefits of liberalizationIn most developing countries, the bank-

ing sector dominates the financial systemand securities markets are not well devel-oped. Restrictions on bank behaviorimposed by the government often result innegative real interest rates and an excessdemand for credit, requiring banks toration their lending. Consequently, credit isallocated to favored sectors and firms by

Huw Pill,a UK national, was a visiting scholar in the IMF's Research Departmentwhen undertaking the research on which this artick is based and is cur-rently an Assistant Professor in Harvard University's Graduate School ofBusiness Administration.

Mahmood Pradhan,a UK national, is a Senior Economist in the IMF's Asia and PacificDepartment.

Finance & Development /June 1997 7

ipclfliberalizap'tn Africa and Asia .--z

• fUW PILL AND MAHMOOD PRADrlAN '%|

OTH ECONOMICTHERY AND

©International Monetary Fund. Not for Redistribution

Indicators of financial deepening 1

Source: Huw Pill and Mahmood Pradhan, "Financial Indicators and Financial Change in Africa and Asia," IMF WorkingPaper No. 95/123 (Washington: IMF, November 1995).

1 All aggregates are constructed using 1987 GDP weights.

2 Indonesia, Korea, Malaysia, the Philippines, Sri Lanka, and Thailand. Data for 1993 exclude Indonesia.

3 The Gambia, Ghana, Kenya, Madagascar, Malawi, and Zambia.

administrative decision, rather than bymarket mechanisms.

Following financial liberalization, marketdetermination of interest rates shouldresult in modestly positive real interestrates. These, in turn, will increase theresources available to the financial system,since bank deposits offering a competitivereturn will attract savings that were previ-ously held outside the formal financial sec-tor (possibly as excess inventories ofintermediate goods). Moreover, positive realinterest rates will provide an incentive forborrowers to invest in more productiveactivities, thereby improving the productiv-ity of the economy as a whole. Conse-quently, financial liberalization should leadto an increase in both the quantity and thequality of financial intermediation by thebanking system.

Financial liberalization can thereforestimulate economic development through avariety of channels. Since the financialsystem performs the vital function of rais-ing funds for, and channeling funds to, pro-ductive investment, successful financialliberalization is usually an important com-ponent of a country's strategy for economicgrowth.

Implementing liberalizationFinancial liberalization entails the aboli-

tion of explicit controls on the pricing andallocation of credit. Direct governmentintervention in bank credit decisions is

8 Finance & Development I June. 1997

brought to an end. Liberalization may alsoinvolve the abolition of controls on interna-tional capital movements. However, govern-ment policies will continue to play a centralrole in determining how the financial sectorperforms. Financial liberalization does notmean "free banking." Governments willcontinue to intervene in the financial sectorin a number of ways: banks will be super-vised for prudential reasons; some banksmay be publicly owned; and the govern-ment may be a major borrower. How suc-cessfully the authorities perform their roleas supervisor, owner, or customer will be animportant determinant of the success ofreform. Moreover, financial liberalization isonly one component of a successful devel-opment strategy. Appropriate macroeco-nomic policy, institutional development,and structural reform must accompanyfinancial liberalization and create the stablecontext required for it to succeed.

Macroeconomic stability is a prerequisitefor successful financial liberalization. In thegenerally successful Asian cases, macro-economic imbalances were largely elimi-nated before financial reforms wereintroduced. Balance of payments and fiscaldeficits were manageable, and inflationwas relatively low. The Asian countriesthat were exceptions to this rule—thePhilippines and Sri Lanka—were notablyless successful in expanding their financialsectors following reforms. For example,in Indonesia, where macroeconomic

conditions were favorable, the ratio ofbroad money to GDP rose dramatically,from a preliberalization level of 9 percent in1983 to well over 40 percent in 1991. In con-trast, in Sri Lanka, the ratio of broad moneyto GDP was largely unchanged after thereforms. Only credible and sustainedmacroeconomic stabilizations produce theincreased demand for money that is thecounterpart to financial deepening.

The situation is markedly different inAfrica, where a number of countries haveattempted to implement financial liberaliza-tion in an environment of ongoing inflation—largely a consequence of excessive fiscaldeficits. In Ghana, inflation was more than20 percent a year when interest rates werederegulated; in Zambia, inflation exceeded100 percent at the time of reform. Attaininglow but positive real interest rates is diffi-cult when inflation is high and volatile.

While macroeconomic stability is essen-tial for successful financial liberalization, asound banking system is also extremelyimportant. The benefits associated withfinancial reform are contingent on the finan-cial system being "well behaved" through-out the liberalization process. Wheresignificant market failures exist, or govern-ment intervention in the financial systemcontinues, the freedom that liberalizationoffers banks may be exploited in ways thatharm the overall development strategy. •

For example, banks in many Africancountries are publicly owned and thereforeremain susceptible to government interfer-ence even after controls on credit pricingand allocation have been formally abol-ished. Moreover, because of the stock ofnonperforming loans inherited from theadministratively directed lending programsof the prereform era, the solvency of manyprivatized banks may remain dependent onsubsidized credit from the central bankeven after liberalization. In these circum-stances, loans provided by these banks aremore akin to government subsidies.Liberalization will do little to improvecredit allocation or spur financial deepen-ing in such circumstances, since the banksremain wholly dependent on the govern-ment, and their lending decisions are sub-ject to its discretion.

Similarly, if competition among banks inthe newly deregulated financial sector isweak, liberalization may result in lower realdeposit rates rather than the anticipatedmovement toward modestly positive, equi-librium levels. Monopolistic banks canexploit the opportunity offered by the aboli-tion of interest rate controls to widen themargins between their deposit and lending

Finance & Development /June 1997

©International Monetary Fund. Not for Redistribution

rates to increase profits. In those Africancountries where this has happened—Kenya, Madagascar, and Malawi in oursample—liberalization has resulted in littlefinancial deepening, since the attractive-ness of bank deposits to domestic savershas, if anything, been reduced.

When financial deregulation is imple-mented—and especially where nonperform-ing loans are inherited from the prereformera—interest rate liberalization should beaccompanied by structural reforms, includ-ing restructuring bank balance sheets toremove bad debt, privatizing publiclyowned banks, and introducing measures topromote competition in the banking sector.The implementation of concurrentstructural reforms in several Asiancountries explains an importantpart of their greater success com-pared with reform efforts in Africa.

Of course, deregulation also cre-ates opportunities for banks tomake poor lending decisions. If,prior to reform, banks have notmade loans based on market crite-ria, their ability to manage creditevaluation and allocation is likely tohave either atrophied or never beendeveloped. Moreover, the process offinancial liberalization itself will introducenew uncertainties into the economic sys-tem. Newly liberalized banks may thereforebe prone to making poor lending decisions.Strengthening the management and riskevaluation capabilities of bank managers ina newly liberalized environment should bean integral part of the restructuring pro-cess. This is likely to require governmentaction. For example, the government mayrelax restrictions on foreign ownership ofdomestic banks so that foreign "best prac-tice" managerial and credit assessmenttechniques can be introduced.

Systemic risk also needs to be managedmore carefully in a deregulated financialsector. Paradoxically, the need for effectiveprudential supervision of financial institu-tions may be greater in a liberal environ-ment than under a government-controlledregime of financial repression. The exis-tence of controls on bank behavior priorto reform may make the financial sectorstable, albeit at considerable expensein economic efficiency. Deregulation willundermine this controls-based stability andtherefore necessitate much greater empha-sis on prudential supervision. If bankschoose to use the new freedoms implied byliberalization to exploit potential marketfailures, the effects on macroeconomic andfinancial stability can be catastrophic.

Financial liberalization cannot be imple-mented in a vacuum. Macroeconomic stabil-ity prior to reform is essential. Butpolicymakers also need to strengthen insti-tutional development in the financial sys-tem before liberalization is introduced. Ifthe legal, accounting, management, andsupervisory infrastructures of the financialsector are weak, then deregulation alone isunlikely to generate the expected benefitsand, in fact, highly destabilizing forces maybe unleashed. Accompanying structuralmeasures are therefore vital. This ismost apparent in Africa, where economicinstitutions remain underdeveloped andhighly fragile. Even in the more successful

"If financial reforms are tosucceed, they must be imple-

mented in an appropriatemacroeconomic, financial,

and institutionalenvironment."

Asian cases, there is considerable scope forimprovement. The large number of non-performing loans on many Asian banks'balance sheets is testament to the dif-ficulty of implementing effective bankingsupervision as liberalization proceeds,even in relatively benign macroeconomicenvironments.

Measuring resultsConventionally, the success of financial

liberalization has been assessed using twocriteria: the extent of financial deepeningand the evolution of real interest ratestoward plausible equilibrium levels. Indeed,these criteria have been used in this article.These two measures, however, suffer fromcertain drawbacks that may obscure someof the important differences between theAfrican and Asian experiences with finan-cial reform.

Abstracting from institutional details, itis clear that reform occurs in several stages.Typically, domestic financial liberalization—the abolition of controls on interest ratesand credit allocation—precedes interna-tional financial liberalization—the elimina-tion of capital controls and restrictions onthe convertibility of domestic currency intoforeign exchange. Conventional measuresof the success of financial reform focus ondomestic deregulation, although in many

cases international liberalization is at leastas important.

For example, if abolishing capital con-trols on the balance of payments results ingreater integration of domestic and inter-national financial markets, arbitrage pres-sures may keep the domestic real interestrate close to world levels. Therefore, wheredomestic real interest rates are initiallyabove world rates owing to a shortage ofdomestic savings, international financialliberalization that offers domestic firmsaccess to international capital may lower,rather than raise, real interest rates.

Similar concerns affect financial deepen-ing. Prior to international financial liberal-

ization, broad money offers a goodindication of the banking system'sscope for credit expansion, sincedomestic bank deposits are themain source of finance for banklending. When capital controls areabolished, however, capital inflows—in the form of deposits madeby foreign residents in domesticbanks—add to the funds bankshave available for credit expansionbut do not increase broad money(since they are excluded from it bydefinition). Money-based measures

of financial deepening may therefore bemisleading when capital inflows are impor-tant (see chart).

Capital flows are not the only reasonwhy money and credit-based measures offinancial deepening may diverge, however.In general, government borrowing from thebanking system will, for a given level ofbroad money, reduce the amount of creditavailable to the domestic private sector. Ifprivate sector activity is more productivethan government expenditure, then thiscrowding out of private borrowing mayhave strong negative repercussions for eco-nomic performance that would not, how-ever, be reflected in the conventionalmeasure of financial deepening.

The chart suggests that several financialliberalizations undertaken in Africa sincethe late 1980s—before fiscal deficits wereeliminated—have been adversely affectedin this way. In the absence of well-developed government securities markets,deficits were financed largely by govern-ment borrowing from banks. Consequently,these countries' apparent success in achiev-ing financial deepening (as indicated bychanges in the conventional money-basedmeasure) during the early 1990s is beliedby what private sector credit measuresshow. Since theory suggests that credit islikely to be more important for economic

Finance & Development /June 1997 9

©International Monetary Fund. Not for Redistribution

Financial liberalization in Indonesia and Kenya

IndonesiaForeign exchange controls were eliminated in Indonesia in 1971, partlyat the urging of the IMF but also because these controls reduced theefficiency of international trade and payments, and were extremely dif-ficult to enforce given Indonesia's proximity to an open internationalfinancial center in Singapore. However, extensive controls on thedomestic financial system remained in place until 1983. Only then wereinterest rates liberalized and controls on credit allocation relaxed.Prudential supervision was strengthened in 1984, after the initial liber-alization of the banking system. Similarly, after relaxing controls on theentry of new banks and easing restrictions on the extension of bankbranches in 1988-89, stricter prudential regulations were introduced bythe centra] bank to constrain the explosion of bank credit that followedderegulatioa

Indonesia's experience is therefore characterized by the implementa-tion of several large reforms, each followed by retrenchment and con-solidation. Although problems have emerged because institutionaldevelopment, especially in the area of prudential supervision, hastended to lag behind deregulation measures, the overall success ofreform has been considerable. Real interest rates have been positivesince 1983, and financial deepening has been extensive. Privatelyowned banks now constitute a much larger proportion of the bankingsector, as the relative importance of publicly owned banks has declined,and securities markets, especially the Jakarta Stock Exchange, have

become more important. Although there have been occasional set-backs, and institutional weaknesses in the accounting and legal sys-tems remain, overall the financial liberalization strategy pursued inIndonesia has been supportive of wider economic development.

KenyaFinancial liberalization in Kenya is much more recent. Ceilings on banklending rates were not removed until July 1991. The central bank con-tinued to announce guidelines for the sectoral composition of bankcredit expansion, although these were not strictly enforced after inter-est rate liberalization. International financial liberalization is even morerecent. Offshore borrowing by domestic residents has been permittedonly since early 1994, and portfolio capital inflows from abroad wererestricted until January 1995. Supporting structural and institutionalreforms have yet to be fully implemented. Many banks remain publiclyowned and competition among them is limited.

Deregulation of interest rates in this monopolistic environment per-mitted banks to widen their margins such that real interest rates onbank deposits fell substantially. Partly in consequence, financial deep-ening has been modest, especially when measured by the ratio of pri-vate sector credit to national income. Although it is too early toevaluate the success of financial liberalization, the lack of accompany-ing institutional and structural reforms suggests that financial sectorreforms will provide only modest benefits to the overall Kenyan devel-opment strategy'.

development than the supply of broadmoney, these findings help to explain whythe initial results of the African experienceswith financial liberalization are generallyregarded as disappointing, despite someprogress on the usual financial deepeningmeasure. In Asia, where fiscal deficits werereduced prior to financial reform, bothmoney and credit measures indicatethat significant financial deepening hasoccurred and the beneficial impacts ofreform on countries' real economies havebeen greater.

As liberalization proceeds, banks ceaseto dominate the entire financial system.Securities markets emerge and become anincreasingly important source of funds formany firms. This process is quite advancedin many Asian countries. As alternativesources of external funds become availableto domestic firms, neither broad money norbank credit will be an adequate comprehen-sive indicator of either the success of reformor its likely impact on real economic perfor-mance, because they do not include thefinancial flows that occur outside banks'balance sheets. In Asia, equity and bondmarkets now play an important role infinancing domestic firms' investment pro-jects, and the conventional measures offinancial deepening will not capture theireffects. In such circumstances, broader

measures of credit, which encompass newissues on the securities markets, are betterindicators of the success of financial reform.

Lessons for liberalizersFinancial liberalization is an extremely

important component of a successful devel-opment strategy. If financial deregulation isimplemented in isolation, it is unlikely topromote growth and may, in fact, impedeeconomic development. The importance ofachieving macroeconomic stability prior toreform is well known, yet structural reformand institutional development in the finan-cial sector, especially prudential financialsupervision, are equally essential as liberal-ization proceeds.

Liberalization has been implemented in anumber of African and Asian countries.Reforms in Asia were introduced both ear-lier and in more favorable macroeconomicenvironments. Although the creation ofeffective supervisory institutions remains achallenge in some countries, the Asianexperience has been very successful over-all. In comparison, financial liberalizationin Africa, where reforms were introducedmore recently, has yielded modest results,although some of the benefits have yetto accrue. Nevertheless, concerns remain.The environment in Africa is far lessfavorable—considerable macroeconomic

imbalances persist and institutional devel-opment is not well advanced. The Asianexperience offers some important lessonsfor Africa in both respects.

Measuring the results of reform isextremely important if policy is to be welldesigned and implemented. The effects ofliberalization itself may distort the infer-ences drawn from conventional measures offinancial deepening about the success ofreform. Consequently, a wide range ofperformance indicators should be moni-tored by policymakers. This is especiallyimportant in Africa, where conventionalmeasures may exaggerate the success ofcountries' reform programs in their earlystages and thereby obscure underlyingproblems—notably, fiscal imbalances—that will require attention if financial reformis to be successful in the medium term. If&Dl

This article is based on the authors' paper,"Financial Indicators and Financial Change inAfrica and Asia," IMF Working PaperNo. 95/123 (Washington: IMF, November1995).Reference

Ronald!. McKinnon, 1993, The Order ofEconomic Liberalization: Financial Control inthe Transition to a Market Economy, second ed.(Baltimore, Maryland: Johns Hopkins UniversityPress).

10 Finance & Development I'June 1997

©International Monetary Fund. Not for Redistribution

Tackling the Rural EnergyProblem in

\ Developing CountriesD O I J G L A 5 F . B A K N E S , 8 0 H K K T V A N D E R P L A S .

A N D \ \ LI.BM F L O O R

Many people in the developingworld lack access to energysources such us oil, gas, andelectricity, and slill depend onbiomass. The problems of sup-plying them with modern fuelsappear daunting, but practi-cal and financially sustain-able solutions exist.

E NERGY MARKETS do not func-tion efficiently in many developingcountries, particularly in ruralareas, where nearly 2 billion peo-

ple do not have electricity or access to modern fuels such as oil and gas. The problemis likely lu worsen in coming decades. Thepopulation of the developing world is

Douglas F. Barnes*.a US national, is an Etiergv Planner until tlieI'ower Dewlupmt'nl. Efftdency aiiif HouseholdFuels Division uftlie World flank's Finance andPrivate Stctor Development Virp Presidency

expected i" mnvu-e by 3.billion Ov.er tin-next torn1 vc;irs, mid ylttrgy, Oematld p'.-rr.-ipim w i l l j i iuvv lapidlyvAsCOunrries' ecu-[nimic develfipmem proceeds, Llltii pelcapita nm-mnpnon < > i " commercial energyimTeascs. rVi kapiw c»nsHnipnab of onii-mrif ia l entity ir. Mv Unittd Stales. I'mexamplr, is fit) liiut'ri l i i g l i c r t l i un in Atnni.40 limes higher than IF South Asia. 1.1lime-; higher rlrin in f{a>i Asia, and 6 linic-r-hipher than in Latin America^

Inadequate energy markeS threalt'ii lodampen economic growth, ijotiblu develdpment, and keep living Ji|andards low.Allhuugh grid electrificMm IK the tradi-tional means of providingHiablc electricitysupplies, coiincclion to dapnt gnds v$\ heloo expensive to be cost-.efftrrive for manyrui^al areas. Fortimateljfterc ai'e a numberof promising altcrnjfts for increasinj;energy supplies evetv»very remote areas,ranging from more Spdcnl use of tradi-tional fuels lo advai«3 technologie.s basedon renewable energjfwces.

Kubcrl MIII (Ifi'ffcis.a Uuli'li natiiiiinl.fllii l-jierfy ilanner icillt llu-Puuvr Developtnaf, Kffiaency anil HouseholdI-'ini-, !>it/-:i"ii i'ftit< W>>r!Aiiui;}:.'< FiiMim mill^f;Private Sector KflafimeaKiec Pre.iidt'icy

W ' *The current situationKHoi';-- -ii;ice 197U tn incrrasr ckilricily

-;uppHep sr developing counlues have been•vivarkHi)l\ successful Bee table). Btitbccaitst i > ! \njpulntHjn firowth, the numberdt" liousi-hdlfl-: wirhou' i-!i'i-i:ui!.\ in -n i ll-'ir^ft and ::• r\cn ^niwirii; in ••nine i v i ; i < > n ^Oin'-tbL'd ')' all eiit-rgj' cunsnmed in diudevetopiiijT wor!4 ciniifo hum biomass. Inaddition !'i Ui-ing their primary M H I I T C ofcnedfe biomass als< i provides many peoplein tl»ipvel()ping%orl^fcith a livelihood.In Afrii'ii alum;, theprnductmn anri m;irkel-ing ofcfood fuels (rSfKvood;mdcliarcoiil) isa SSfeillion business tliat employs morethan 400,000 people.

Wood and nihcr trathlioiial kiflv- ,^icii t^dung H-IVI- numerous diwidvaniage^.. !mw-evtr. Tliej are f^UK effic«t than otherenergy soiinv-;; S kf t^ra in <ii wm.d. furex.'implf. generate:- oniy "ne tenth ut rhcliRat jiclded by a kil"irnm trf Hiiuidpetroieum gas d.IJ(i\ Miwver, burningthese types oi" [\n-l? in an enclosed, pxir lv

Willem Flour.Dutch nati">-i :f a Seititifnrrgt' Flmiu'r

:'->th the Ann r lAwhpnienffficit'tKyTmJHfimttttMI'tii-if. Itti-ifiiii! n/ tltt l\'i<t!i!Rattl;':i-:nance. an<; I'nratf Nr,'.^ Dtrrli>j>i>iti:! Vii,I'irsidsii£\

Finance .<. /)<•/; hptm-at •'jtoirW/ I I

©International Monetary Fund. Not for Redistribution

North Africa and the Middle EastLatin America and the CaribbeanSub-Saharan AfricaSouth AsiaEast Asia and the PacificAll developing countries

Total served (in millions)

1970

65

67

28

39

51

52

320

1990

8182

3853

82

76

1,100

1970

14

15

412

25

18

340

1990

35

40

825

45

33

820

ventilated space presents a major healthhazard. According to some estimates,smoke contributes to acute respiratoryinfections that affect 4 million infants andchildren a year. Studies have shown thatnonsmoking women in India and Nepalwho have cooked on biomass stoves formany years have a higher-than-normal inci-dence of chronic respiratory disease. Theuse of wood fuels has also taken a serioustoll on the environment in many regions,leading to deforestation, soil erosion, andreduced soil fertility. Deforestation, in turn,has forced many poor people to resort toeven less efficient sources of energy, such ascrop residues and dung—materials thatcould otherwise have been used for fertil-izer. Finally, many children and adults indeveloping countries must spend up to sev-eral hours per day gathering fuel; thisleaves them less time for schooling and pro-ductive activities and thus perpetuatespoverty.

Moving up the energy ladderIn poor countries with annual per capita

incomes of $300 or less, at least 90 percentof the population depends on wood anddung for cooking. But people move up the"energy ladder" as their incomes grow,eventually switching to electricity for light-ing and fossil fuels for cooking; in agricul-ture and industry, diesel engines andelectricity replace manual and animalpower. The transition to modern fuels isusually complete by the time annual percapita incomes reach $1,000-$1,500. Withtechnological progress and reductions inthe costs of modern fuels, the income levelat which people make the transition candecline significantly. For example, a transi-tion that took nearly 70 years in the United

States (1850-1920) took only 30 years inKorea (1950-80). But such transitions willnot happen overnight. Even in East Asiaand the Pacific, a region that has experi-enced rapid economic growth and signifi-cant increases in the supply of commercialenergy, biomass still accounts for 33 per-cent of energy supplies and its use isexpected to decrease by only 50 percentover the next 15-25 years.

What are the options?Because biomass use will continue

throughout the developing world for sometime to come, energy policies must supportways to use wood fuels more efficiently andsustainably, while creating the necessaryconditions for supplying modern fuels tothose who lack them.

Farm forestry and local forestmanagement. Farm forestry—plantingtrees, shrubs, and grasses on farmlandsand between crops—and forest manage-ment have long played an important role inalleviating wood shortages in China, India,and many other countries. Because farmersoutnumber foresters in most countries byseveral thousand to one, involving them inplanting trees and shrubs can dramaticallyaccelerate afforestation. And the incentiveto participate in farm forestry programs isstrong: wood fetches a high price in someurban markets, and trees and shrubs cansupply farmers with fodder, building mate-rials, green mulch, fruit, and other byprod-ucts that may be as valuable as thefirewood itself.

Experience suggests that effective man-agement of existing forest resourcesdepends on letting local people take respon-sibility for forests or woodlands. Some suc-cessful participatory effects have now been

pioneered in several countries. In these pro-grams, farmers get to sell all the woodextracted from local woodlands; however,they must participate in a resource-man-agement program developed in collabora-tion with the national forestry department.

Improved charcoal efficiency.Charcoal represents an intermediate rungon the energy ladder, between wood andkerosene or LPG. It burns without smoke ordangerous flames and requires only a sim-ple stove whose heat output is relativelyeasy to control. However, local charcoal pro-ducers often use inefficient charcoalingkilns that consume more wood than neces-sary. Kilns based on traditional designs butthat are more energy efficient have beendeveloped in collaboration with end usersin Madagascar, Rwanda, and Thailand andsuccessfully disseminated through exten-sion programs and training. Programs pro-moting technical innovation have beenmost successful when accompanied by theforest-management programs describedabove, which give villagers custody of localforest resources.

Efficient use of biomass. One way toimprove wood fuel use is for governmentsto encourage the private sector to developand market improved stoves in rural areasby supporting stove design and testing,and conducting publicity campaigns andtraining programs. Relatively simple andinexpensive stoves—for example, withimproved chimneys—can reduce theamount of fuel needed for cooking by asmuch as 30 percent, yield substantialhealth benefits, and free women and chil-dren from hours of gathering firewood.Experience has shown, however, that suchprograms need to be targeted. For example,the successful Chinese National ImprovedStove Program, the largest ever undertaken(120 million stoves have been installed inrural households), was concentrated onareas with the greatest shortages of woodfor fuel.

Although fuels from biomass are gener-ally much less efficient for cooking thanmodern fuels, biogas derived fromdigesters of dung and farm residues is anexception. Both China and India have donemuch to develop biogas and encourage itsuse. However, only farmers who raise live-stock can easily acquire biogas; it is thus acost-effective option for less than 10 percentof most rural populations.

Rural electrification. Rural demandfor electricity comes mainly from house-holds that use electricity for lighting andfrom farms, agro-industries, and small com-mercial and manufacturing establishments,

12 Finance & Development /June 1997

Source: World Bank project and sector reports, and surveys of electricity statistics by the World Bank's regionalstaff in Asia and Latin America.

Note: Figures are estimates.

BljM?niWsTiTfMMfifnB*TsiSr>lLs*K*jiiinTH^TfBt*T^MH<iHii ^^^B^ ^ ^ ^ ^ • V^ Mra ffli ^ ^QQ^ ^ ^ ^ ^ ^ ^ I

(PERCENT OF POPULATION)

uRBAB rURAL

©International Monetary Fund. Not for Redistribution

which use electricity for productive pur-poses such as irrigation pumping, watersupplies, crop processing, refrigeration, andmotive power. Most rural electrificationprograms have focused on connecting ruralareas to national or local grids (see box).However, grid-supplied electricity is not thelowest cost alternative under all conditions.

For example, technologies involvingwind power, solar thermal power (sunlightused to heat air or water), photovoltaic (PV)cells (which produce electricity directlyfrom sunlight), and small-scale hydropowermerit more attention from policymakers.They are often an ideal way to get energyto rural areas and have significantenvironmental advantages relative tofossil fuels. Solar power is a particu-larly attractive option for countrieswith abundant sunlight and a poorlydeveloped rural grid electrificationsystem.

The costs associated with thesetechnologies, once prohibitive, havedecreased significantly over the pastdecade. Today, PV systems supplyelectricity economically to rural areasthroughout the developing world forlighting in homes and schools, domesticappliances, refrigeration in health clinics,village water pumps, telephones, and streetlighting.

Rural energy policiesEvidence suggests that people are will-

ing to spend a significant portion of theirincomes on higher quality energy thatimproves their quality of life and enablesthem to be more productive. Governmentshave an important role to play in creatingconditions that provide consumers withmore energy choices and encourage innova-tion and investment in new technologies.Prices should be liberalized to reflect costs,and regulatory policies need to encouragecompetition and level the playing field forall types of energy markets, whether theyare served by public utilities, private firms,or community enterprises. For example"off-grid" power companies and coopera-tives are often totally excluded by electric-ity regulations from serving people, andpolicies that artificially hold down pricessometimes provide little incentive for suchlocal initiatives to get started.

Pricing and market reforms. Ingeneral, energy subsidies (prevalent indeveloping countries) should be avoided.Subsidies undermine incentives both forconsumers to make least-cost choices andfor investors to develop alternative energyforms, and more often disproportionately

benefit higher-income households, whichuse more energy than poor households. Insome cases, subsidized fuels never evenreach the poor. In Ecuador, for example,kerosene for cooking and lighting was sub-sidized until recently, but retailers preferredto sell the kerosene for use in vehicles,which was more lucrative than selling it tothe poor. Electricity subsidies are a particu-lar problem. They have left many utilitieseconomically crippled, unable to financethe extension of services to rural areas.Moreover, they distort the market, encour-age consumers to buy grid-suppliedelectricity, and discourage the development

"Subsidies undermine incen-tives both for consumers to

make least-cost choices andfor investors to develop alter-native energy forms, and...disproportionately benefit

higher-income households."

of decentralized, off-grid companies.Universal pricing (charging the same pricescountrywide), a common practice, also cre-ates disincentives for electric utilities toserve rural markets, where costs tend to behigher.

Even when subsidies do benefit the poor,they may represent an unsustainable finan-cial burden on the state. Market liberaliza-tion is usually a far more effective strategy.In Hyderabad, India, for example, only therichest 10 percent of households used LPGin 1980. Middle-class households usedkerosene because they could not obtainLPG, a more efficient fuel. There was nokerosene for the poor because the limitedamounts available for public distributionwere bought by middle-class households.As a result, the poor had to use wood,which was even more expensive thankerosene. When the Indian government lib-eralized energy markets and relaxedrestrictions on the production and importof LPG, more middle-class householdsswitched to LPG. Supplies of kerosene werethen more plentiful and more available tothe poor. Now more than 60 percent ofhouseholds in the city use LPG.

One subsidy that can be justified is a life-line rate for grid electricity. Most poorpeople use very little electricity and needonly the most basic service. Thus, the appli-cation of lower tariffs for consumption ofsmall amounts of electricity provides a

direct benefit for the poor and usually doesnot represent a significant financial drainon the distribution company. Any financiallosses can be recovered by chargingslightly higher prices to large-volume cus-tomers, who usually have higher incomes.

Alleviating problems with firstcosts. In developing countries, the firstcosts associated with getting access to mod-ern sources of energy are often prohibitivelyhigh for the rural poor, who are also usuallyunable to obtain credit. The fees for beingconnected to an electricity grid can rangebetween $20 and $1,000; a solar home sys-tem costs between $500 and $1,000.

Installing a microgrid can cost a com-munity tens of thousands of dollars.

There are two ways of dealingwith the high initial costs of ruralenergy services—lowering systemcosts through design innovationsand giving rural consumers access tocredit.

Many distribution companiesdesign systems with the capacity todeliver between 3 and 7 kilowatts ofservice and that require heavierwires, larger transformers, and gen-

erally more expensive distribution systemscomponents. The entire system design canbe lightened to provide service at less cost.Similarly, the standard household PV sys-tem promoted by many development agen-cies provides about 50 watts of power, butrecent evidence from Kenya shows that peo-ple there are purchasing more affordable PVsystems that provide only about 12 watts.

Many practical options exist for provid-ing affordable credit for rural energy. Forexample, electricity companies could allowcustomers to pay access charges overseveral years. In a recent project inIndonesia, banks are advancing credit toconsumers for the purchase of householdPV systems. Some nongovernmental orga-nizations (NGOs) in Nepal and Peru aremaking credit available for the installationof microgrid systems based on micro-hydroelectric systems.

Emphasizing participation andinstitutional development. Local par-ticipation is crucial for the success of ruralenergy policies. Cooperatives, NGOs, andcommunity organizations can be highlyeffective vehicles for supporting the deliv-ery of energy services and managingresources.

Participatory efforts must be properlydesigned, however. The first attempts topromote community biogas systems in theIndian village of Pura failed because theywere aimed at getting villagers to use

Finance & Development /June 1997 13

©International Monetary Fund. Not for Redistribution

Options for rural electrificationBetween 1970 and 1990, nearly 1.3 billion people, 500 million ofdiem in rural areas, were newly supplied with electricity fromnational grids. But the population in some developing regionsgrew faster than electricity supplies. The number of people insub-Saharan Africa with electricity increased by only 18 millionbetween 1970 and 1990, while the total population grew by 118million. Similarly, in South Asia, 140 million people gainedaccess to electricity during the same period, but, because of pop-ulation growth, the number of people without service grew bymore than 100 million.

Surveys of rural energy use show that many people spendsignificant sums on candles, kerosene, and batteries for lightingtheir homes. Many rural people in Bolivia, for example,spend $4-$5 per month on candles.Switching to electricity and usingjust one 40-watt bulb or a 20-wattincandescent lamp would cost a fewdollars more per month but wouldprovide 25 to 75 times more lightthan a candle.

regions with the necessary resources. The costs per kWh of elec-tricity generated by micro-hydropower can be as low as 20-30cents, depending on the site; 90 cents for PV panels; and 40-90cents for small wind sets. Electricity for local distribution canalso be generated from such fuels as biogas or biomass.

Micro-hydropower can be one of the cheapest options for pro-viding electricity to rural areas too remote to be connected to agrid Much care needs to be given to selecting the site for amicro-hydro project, however, given possible variations instream flows during the year and from river to river, and theircosts can vary significantly, depending on the terrain. In moun-tainous countries like Nepal, for example, transportation ofequipment and materials can account for as much as 25 percent

of total project costs.

"Grid supplies areusually the cheapestoption in areas withhigh load densities,as well as in areasnear the grid. Butconnecting small,

isolated villages to agrid can be expensive.

The choicesMany people without electricity

in rural areas are therefore willingto pay to get it. Grid supplies areusually the cheapest option in areaswith high load densities, as well asin areas near the grid. But connect-ing small, isolated villages to a gridcan be expensive because of the nec-essary investment in transmissionlines, poles, transformers, and otherinfrastructure. In some instances, other options—includingdiesel generators, renewable energy (solar energy, micro-hydropower, wind, and small biomass-fired generators), and"hybrids" combining several of these—are more cost-effective.

Grid electrification. The high initial costs of grid electri-fication can be reduced considerably if design standards suit-able for areas with less demand are used. Most rural consumersneed from 0.2 kilowatts to 0.5 kilowatts, much less than the typ-ical minimum service connection ratings in developing coun-tries' utilities. The costs of installation and wiring provided byutilities are also high, but these can be lowered by simplifyingwiring codes and using load limiters (circuit breakers) to encour-age lower levels of consumption. Other cost-cutting strategiesinclude using cheaper utility poles and involving local people inconstruction and maintenance.

Micro-grids supplied by diesel generators. De-centralized, isolated distribution systems have been common inremote population centers for many decades—in most develop-ing countries, they predate the establishment of grids. The costsof such systems typically range between 20 and 60 cents perkilowatt hour (kWh). However, diesel generators can be hard tomaintain and expensive to operate because of their remote loca-tions and the costs of spare parts and fuel.

Renewable energy sources. Energy from solar, wind,and micro-hydropower schemes is an attractive option in

Successful approachesCountries that have succeeded in

making grid electricity service avail-able to rural people have done sothrough strong public leadershipand highly strengthened financialsupport. There are many ways topay for rural expansion withoutdestroying the financial viability ofthe electricity industry.

In Thailand, the public distribu-tion system serving areas outside ofBangkok—the Provincial ElectricityAuthority—was successful inexpanding grid electrification. Itdealt with the problems of lowerloads in rural areas by extending

service first to the highest-load villages, developing low-costconnection techniques, and promoting load development. Costswere reduced through standardization of systems design andprovision of a financially sustainable lifeline tariff for meetingthe minimal requirements of the poorest consumers.

In Costa Rica, rural cooperatives were able to establish arural grid in the early 1960s with long-term capital from the USAgency for International Development and the Inter-AmericanDevelopment Bank.

A regulatory regime requiring distribution companies toexpand service to a blend of high- and low-income householdswithin an assigned territory while requiring full-cost recoveryfor the system as a whole, is a possibility. There are also exam-ples of communities, innovative private companies, coopera-tives, and individuals that are successfully distributingelectricity through minigrids without subsidies. However, otherpotential innovations have often been thwarted by regulationsand policies that prohibit private enterprises other than thenational utility from selling electricity and by the absence oftraining and technical support. Another policy that discouragesprivate sector participation in rural electrification is uniformcountrywide pricing, which effectively makes small local gridsfinancially unsustainable.

14I'~tiM>n'i- £ !>i vc.lopment /Jitm- 1997

©International Monetary Fund. Not for Redistribution

biogas for cooking instead of wood. Butsince wood is abundant and easy to collectin Pura, people had no incentive to switch.When the villagers revealed their desire forclean and reliable water supplies, the com-munity established a system that producedbiogas for fueling a five-horsepower dieselgenerator. Electricity from the generatorwas supplied to households through amicro-grid and used to power a deep tube-well pump. Each household participatingin the program received a tap providingclean water in front of its house.

Identification of the appropriate socialunit to work with is also crucial. SeveralWorld Bank-financed community woodlotand forestry projects in the late 1970s andthe 1980s had disappointing resultsbecause communities had been mistakenlyviewed as units of social organizationwhen, in reality, the interests of subgroupswithin those communities frequentlyclashed. And insufficient attention wasgiven to other complicating factors: com-munity land was limited and the tenure ofcommon lands uncertain; the influence of

local authorities was uneven; and distribu-tional arrangements for the products werecontested.

Creating enabling conditions.Investments in rural energy may falterbecause of economic conditions. For exam-ple, in rapidly developing agriculturalregions, electricity helps to raise theproductivity of local agro-industrial andcommercial activities by supplying motivepower, refrigeration, lighting, and processheating. Increased earnings from agricul-ture and local industry and commerce thenlead, in turn, to greater household demandfor electricity. However, when developmentefforts fail because of, say, poor croppricing, flawed marketing policies, andinadequate roads, programs to improveelectricity supplies are also likely tolanguish.

ConclusionHelping people in rural areas gain access

to energy is a great challenge, but themeans available for realizing this goal haveexpanded considerably in recent years. As

renewable energy systems come down incost, they are becoming an increasinglyattractive way to provide electricity to ruralareas. The costs of grid electrificationschemes can also be reduced to make elec-tricity more affordable to a broader spec-trum of rural people, and new, off-gridrural companies and cooperatives canemerge if competition is promoted, barriersto entry are reduced, and the pricing play-ing field is leveled. Moreover, continued useof biomass need not deplete the environ-ment, thanks to farm-forestry and forest-management programs that involvefarmers. Concerted efforts by governments,policymakers, the private sector, andNGOs, coupled with significant local partic-ipation, can lead to impressive results. IF&DI

This article is based on Rural Energy andDevelopment: Improving Energy Supplies forTwo Billion People, a study published by theWorld Bank in 1996 in the Development inPractice series (Washington).

Keep up with the world economyWhat are the prospects for economic growth and inflation in the advancedeconomies, developing countries, and countries in transition?How are the forces of globalization, including increased trade and capitalflows, affecting the world economy? What are the effects on wages andunemployment in the industrial countries? How are these trends influencingthe tendency of per capita income levels in developing countries to convergetoward those of advanced economies?What policies would lead to the best outcomes?The answers may surprise you.

The World Economic Outlook, May 1997A Survey by the Staff of the International Monetary FundAnnexes, boxes, charts, and an extensive statistical appendix supplement the text.ISSN 0256-6877.

Available in English, French, Spanish, and Arabic.$35.00 (academic rate: $24.00). (paper)

TO ORDER, PLEASE WRITE OR CALL:International Monetary Fund • Publication Services • Box FD-297 •70019th Street, N.W. • Washington, DC 20431 U.S.A.Telephone (202) 623-7430 •Telefax: (202) 623-7201 • E-mail: [email protected] • Internet: http://www.imf.orgAll orders must be prepaid. American Express, MasterCard, and VISA credit cards accepted.

Finance & Development /June 1997 15

©International Monetary Fund. Not for Redistribution

GUEST ARTICLE

Japan's Economy Needs Structural ChangeT A K A T O S H I I T O

Japan's economic miracleappears to be waning. Struc-tural changes are needed toput the economy on a reason-ably high growth path onceagain.

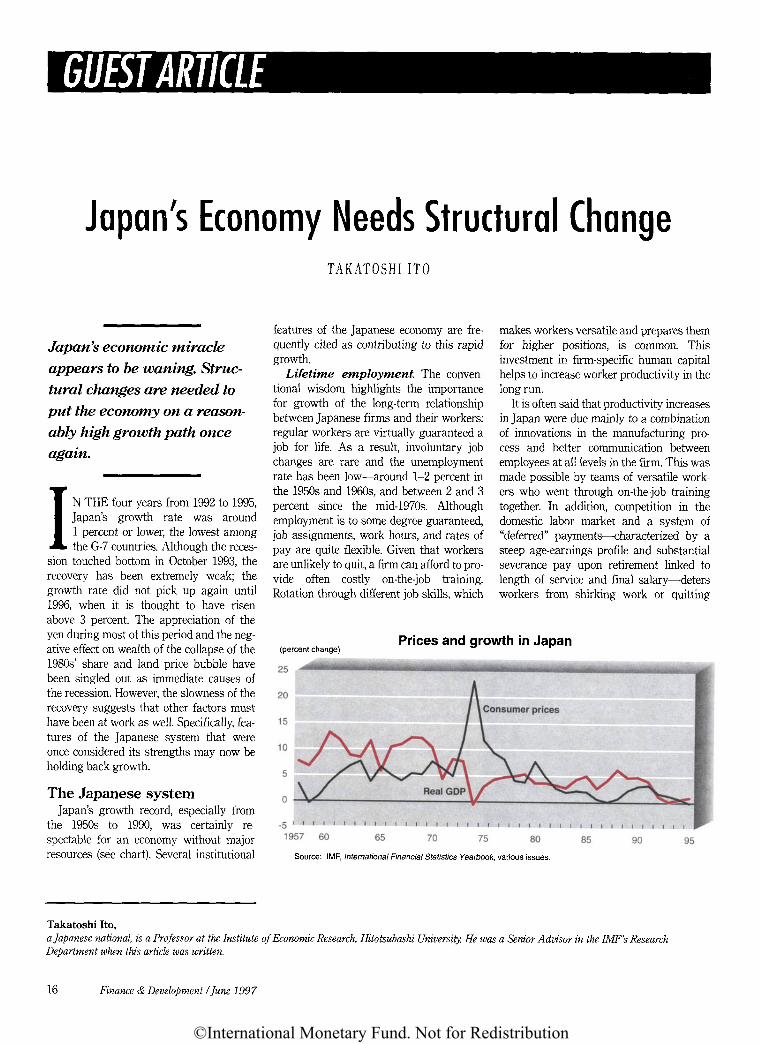

I N THE four years from 1992 to 1995,Japan's growth rate was around1 percent or lower, the lowest amongthe G-7 countries. Although the reces-

sion touched bottom in October 1993, therecovery has been extremely weak; thegrowth rate did not pick up again until1996, when it is thought to have risenabove 3 percent. The appreciation of theyen during most of this period and the neg-ative effect on wealth of the collapse of the1980s' share and land price bubble havebeen singled out as immediate causes ofthe recession. However, the slowness of therecovery suggests that other factors musthave been at work as well. Specifically, fea-tures of the Japanese system that wereonce considered its strengths may now beholding back growth.

The Japanese systemJapan's growth record, especially from

the 1950s to 1990, was certainly re-spectable for an economy without majorresources (see chart). Several institutional

features of the Japanese economy are fre-quently cited as contributing to this rapidgrowth.

Lifetime employment. The conven-tional wisdom highlights the importancefor growth of the long-term relationshipbetween Japanese firms and their workers:regular workers are virtually guaranteed ajob for life. As a result, involuntary jobchanges are rare and the unemploymentrate has been low—around 1-2 percent inthe 1950s and 1960s, and between 2 and 3percent since the mid-1970s. Althoughemployment is to some degree guaranteed,job assignments, work hours, and rates ofpay are quite flexible. Given that workersare unlikely to quit, a firm can afford to pro-vide often costly on-the-job training.Rotation through different job skills, which

makes workers versatile and prepares themfor higher positions, is common. Thisinvestment in firm-specific human capitalhelps to increase worker productivity in thelong run.

It is often said that productivity increasesin Japan were due mainly to a combinationof innovations in the manufacturing pro-cess and better communication betweenemployees at all levels in the firm. This wasmade possible by teams of versatile work-ers who went through on-the-job trainingtogether. In addition, competition in thedomestic labor market and a system of"deferred" payments—characterized by asteep age-earnings profile and substantialseverance pay upon retirement linked tolength of service and final salary—detersworkers from shirking work or quitting

(percent changePrices and growth in Japan

Takatoshi Ito,a Japanese national, is a Professor at the Institute of Economic Research, Hitotsubashi University. He was a Senior Advisor in the IMF's ResearchDepartment when this article was written.

16 Finance & Development /June 1997

Source: IMF, International Financial Statistics Yearbook, various issues.

©International Monetary Fund. Not for Redistribution

altogether. Thus, lifetime employment issupported by a system of implicit contracts.Moreover, it is self-sustaining: lifetimeemployment contributes to the growth of afirm, and growth makes it possible for thefirm to maintain lifetime employment.

The system works especially well in anexpansionary environment, since the rela-tively large pool of "underpaid" youngerworkers makes possible more "deferred"payments to retiring workers. When theorganizational hierarchy of a corporationgrows, more management positions are cre-ated, and therefore "deferred" paymentsincrease. Thus, lifetime employment canalso be seen as a type of pay-as-you-gocompany pension scheme.

The main bank system. Stronglong-term relationships betweenbanks and firms are often cited as asource of strength in the Japaneseeconomy. Typically, a firm develops arelationship with a particular bankand relies on its financial support overthe long term. The bank not only pro-vides loans to, but also holds sharesin, the firm. In return, the firm usesthe bank for major transactions fromwhich the bank earns profits. A bankthat has this type of primary relation-ship with a firm is called a main bank.

The main bank acts as an agent forinvestors and lenders to the firm,examining the viability of investmentprojects and monitoring the perfor-mance of management. Individualstockholders do not monitor manage-ment efforts, and Japanese institu-tional investors have not exercised thekind of monitoring power, such aspressing for higher dividends, thatinvestors have in the United States, forexample. Because a main bank takes along-term view, a firm's managementis able to embark on long-term investmentprojects with committed funding.

Keiretsu. In addition to the strong rela-tionship between banks and firms, theJapanese economy is characterized by long-term relationships between businesses inthe form of keiretsu, or enterprise groups.There are horizontal keiretsu (acrossdifferent industries) and vertical keiretsu(between a manufacturer and its suppliers,or its wholesale distributors, dealers, andretailers).

Conventional wisdom on the significanceof the keiretsu to the Japanese economy issimilar to that for the main banks; theymonitor the performance of management.Since group firms hold each other's shares,they are effectively safe from hostile

takeovers. Management can therefore con-centrate on long-term investment projects,rather than on dressing up quarterly earn-ings reports. Conversely, if the managementof a company has failed, the group firmscan collectively decide to replace those whoare responsible.

Industrial policy. Despite the popularimage of interventionist government, publicexpenditure as a percentage of GDP inJapan has been relatively small comparedwith other industrial countries. Never-theless, public policy has been used topromote growth in a variety of ways.During the 1950s and 1960s, the govern-ment targeted certain industries as sunrise

Takatoshi Ito

industries, providing them with variousadvantages to stimulate their expansion.They were given low-interest loans throughgovernment financial institutions andreceived hard-to-obtain foreign exchangeallocations. The government also restrictedentry to markets that were consideredimportant and crowded, and some marketswere segmented to limit competition.

One influential but controversial inter-pretation of the industrial policy of thisperiod goes as follows. When a chosen sun-rise industry was in its infancy, the gov-ernment protected the domestic marketthrough quotas and high tariffs, butallowed domestic firms to compete withinthe captive market. Japanese firms eitherlicensed foreign technology or reverse engi-neered foreign products to catch up. As the