Introduction Page 1 of 70

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Introduction

Page 1 of 70

1.1 INTRODUCTION

Generally by the word “Bank” we can easily understand thatthe financial institution deals with money. But there aredifferent types of banks such as; Central Banks, CommercialBanks, Saving Banks, Investment banks, Industrial Banks, Co-operative Banks etc. But when we use the term “Bank” withoutany prefix, or qualification, it refers to the ‘commercialbanks’. Commercial banks are the primary contributors to theeconomy of a country.

we can say Commercial banks are a profit-making institutionthat holds the deposits of individual & business in checking& savings accounts and then uses these funds to make loans.Both general public and the government are dependent on theservices of banks as the financial intermediary. As, banksare profit–earning concern; they collect deposit at thelowest possible cost and provided loans and advances athigher cost. The differences between two are the profit forthe bank.

Banking sector is expanding its hand in different financialevents every day. At the same time the banking process isbecoming faster, easier and the banking area is becomingwider. As the demand for better service increase day by day,they are coming with different innovative ideas & products.In order to survive in the competitive field of the bankingsector, all banking organizations are looking for betterservice opportunities to provide their fellow clients. As a

Page 2 of 70

result, it has become essential for every person to have someidea on the bank and banking procedure.

1.2 Objective of the study

There are some objectives for preparing this report . It is aprocess of integrating the practical experience. The specificobjectives of this study are as following:

To analyze the service procedure of Mutual Trust Bank Limited.

To know the banking operation.

To know the area of import finance

To know the area of export finance

To know the area of remittance

To know the position of the bank

To gather the practical experience

1.3 Scope of the study

The main aim of MTBL is to serve their customers Therefore, they operate three divisions and foreign exchange division isone of them. And I have worked in this department for last three month for gathering practical experience .

1.4 Methodology of the study

For smooth and accurate study every one has to follow some rules & regulations. The study input were collected from two sources

Page 3 of 70

1.4.1 Primary sources of data

o Face to face conversation with the bank officers & staffs

o Informal conversation with the clients

1.4.2 Secondary sources of data

o Annual report of MTBL

o Prospectus of MTBL

o Credit Policy of MTBL

o Different papers of MTBL

o Unpublished data

1.5 Limitations Of the Study

The main limitation here is as an internee I could not shareall the information every time for the organization internalsecurity. There are some other limitations these limitationsare as follows:

The duration of my internship Program was only threemonths. But this allocated time is not enough for acomplete and fruitful study.

The Bank was a busy one having heavy rush of people,whom officers need to deal with. So allocation of time

Page 4 of 70

for an internee is very much difficult for the officersof the bank.

I was not assigned for a specific task in each day. SoI was not able to understand banking activities deeply.

Bank is a sophisticate business sector. So bank do notinterested to provide me confidential data. As a resultin my report there is a confidential data limitation.

Page 5 of 70

PROFILE OF ORGANIZATION

Page 6 of 70

2.1 OVERVIEW OF MUTUAL TRUST BANK

Mutual Trust Bank Ltd. started its commercial operation fromOctober 1999 as a scheduled bank obtaining license fromBangladesh Bank under Bank Company Act 1991. It’s a 3rd

generation private commercial bank in Bangladesh. MercantileBank Ltd., EXIM Bank Ltd., Bank Asia Ltd., One Bank Ltd.,First Security Bank Ltd., Premier Bank Ltd., Standard BankLtd. got license in the year 1999. Mutual Trust Bank Ltd.Along with these banks are un-officially known as 3rd

generation private commercial bank.

On the other hand National Bank Ltd., IFIC Bank Ltd., The City Bank Ltd., AB Bank Ltd., United Commercial Bank Ltd etc.are known as 1st generation private commercial bank and DhakaBank Ltd., Prime Bank Ltd., South East Bank Ltd., Dutch-Bangla Bank Ltd etc are 2nd generation bank in terms of theirlaunching year.

The bank has issued 3,000,000 No of shares to the public adsponsors group. The directors and share holders

Page 7 of 70

simultaneously trying to develop the Bank day by day. By thegrace of Almighty Allah this bank has passes away a long pathof tremendous activities and Colourful achievement.

2.2 Corporate Vision

To establish Mutual Trust Bank as a Role Model in the BankingSector of Bangladesh. To meet the needs of Customers, Providefulfilment for People and create shareholder value.

Vision of MTBL is to always service to achieve superiorfinancial performance, be considered a leading IslamicBank by reputation and performance.

To establish and maintain the modern Banking techniques,to ensure soundness and development of the financialsystem based on Mutual principles and to become thestrong and efficient organization with highly motivatedprofessionals working for the benefit of peoples, basedupon accountability, transparency and integrity in orderto ensure the stability of financial systems.

MTBL will try to encourage savings in the form of directinvestment.

MTBL will also try to try encourage investmentparticularly in projects, which are more likely to leadto higher employment.

2.3 Corporate Mission

To constantly seek to better serve Customers.

Be pro-active in fulfilling Social Responsibilities

To enabled by cutting-edge technology.

Page 8 of 70

Working environment to be supportive of Teamwork,

enabling the Employees to perform to the very best oftheir abilities.

2.4 Values

Commitment

Shareholders-Create sustainable economic value for ourshareholders by utilizing an honest and efficientbusiness methodology.

Community- Committed to serve the society throughemployment creation, support community projects and be aresponsible corporate citizen.

Customers- render state-of-the-art service to ourcustomers, offering diversified products and aspiring tofulfil their banking needs to the best of our abilities.

Employees-Be reliant on the inherent merit of theemployees and honour our relationships as a tribute tobe a part of this renowned financial institution.

Accountability-As a bank we are judged solely by thesuccessful execution of our commitments, we expect andembrace that form of judgement .

Agility-We can see things from different perspectiveswe are open to change and not bounded by how we havedone things in past .

Trust-We value mutual trust, which encompassestransparent and candid communications among all parties.

Page 9 of 70

2.5 Corporate Governance

Corporate governance is a fundamental part of the culture andbusiness practice of MTB and remains the cornerstone ofrunning business operation in MTB, which is directed andcontrolled by the board of directors who are responsible forensuring that the management maintains a system of internalcontrol to provide assurance of effective and efficientoperations, internal financial controls and compliance withlaws and regulations.

2.6 Board of Directors of MTBL

2.6.1 Profile of the Directors

The Board of Directors of Mutual Trust Bank Ltd. generallyconsists of experts from the following four areas:

1. Advisers: Persons representing this group must be wellversed in the modern credit operation and SME loan, law andjurisprudence.

2. Banker: There must be a member who is fully conversantwith banking law and practices and has practicalexperiences in Banking business including foreign trade.

3. Economist : A member from this group need not necessarilybe an experienced economist to start with. But if he is anexperienced Economist it is an added advantage. What isimportant is that he must be really proficient in moderneconomies with an in depth study of the community, which abank is going to solve. He must have up to date knowledgein the development of the contemporary world.

4. Lawyer: A member representing this group should be asuccessful practitioner lawyer. He must be proficient in

Page 10 of 70

commercial law including company law. In consultation withthe Management and Economist members of the council, heshould be able to draft such innovating contracts, whichwill have the sanction of Management and a banking law ofthe land.

2.7 Function of MTBL

The functions of MTBL are divided into three sections theseare:1) General Banking. 2) Foreign Exchange.3) Investment.Under these three sections MTBL do their services. Each ofthis section serves vario2.7.1 General Banking

us services for satisfying their clients.General department performs the majority functions of a bank.It is the core department of any bank. The activities ofgeneral banking of MTBL are mainly divided into the followingcategories:

Mobilization of deposits Receipts and payment of cash. Handling transfer transaction. Operations of clearing house Maintenance of accounts with Bangladesh bank and other

bank. Collection of cheque and bill. Issue and payment of Demand Draft, telegraphic transfer

and Executing customers standing instructions. Maintenance of safe deposit lockers. Maintenance of internal accounts of the bank.

2.7.2. Foreign Exchange

Foreign Exchange Business plays a vital role in providingsubstantial revenue in the bank income pool. Like all modern

Page 11 of 70

Banks MTBL operates in the area of the foreign Exchangebusiness MTBL performs the following tasks:

a) Opening letter of credit (LC) against commission forimporting industrial, agricultural and otherpermissible items under CCI& C’S Import policy.

b) Opening letter of credit on the principle ofpromotion of export & import business in our country.

c) Post Financing in import under Cash LC / DeferredLC.

d) Financing to export on interest payment basis agt.Packing credit.

e) Handling Inward and outward remittance.

2.7.3 Investment Operation

Investment operation is the vital operation which earngreater share of total revenue. Well planned and appropriateinvestment policy frame work is a pre-requisite for achievingthe goal of the Bank i.e. implementation.

Optimum utilization of invest table fund. Profitability of the investments. Safety and security of the investments. Investment at minimum possible risk Liquidity of investments. Conform to central bank’s investment restrictions /

priority. Performance to short term investments Performance to the investment for small amount / size. Satisfactory return on investments

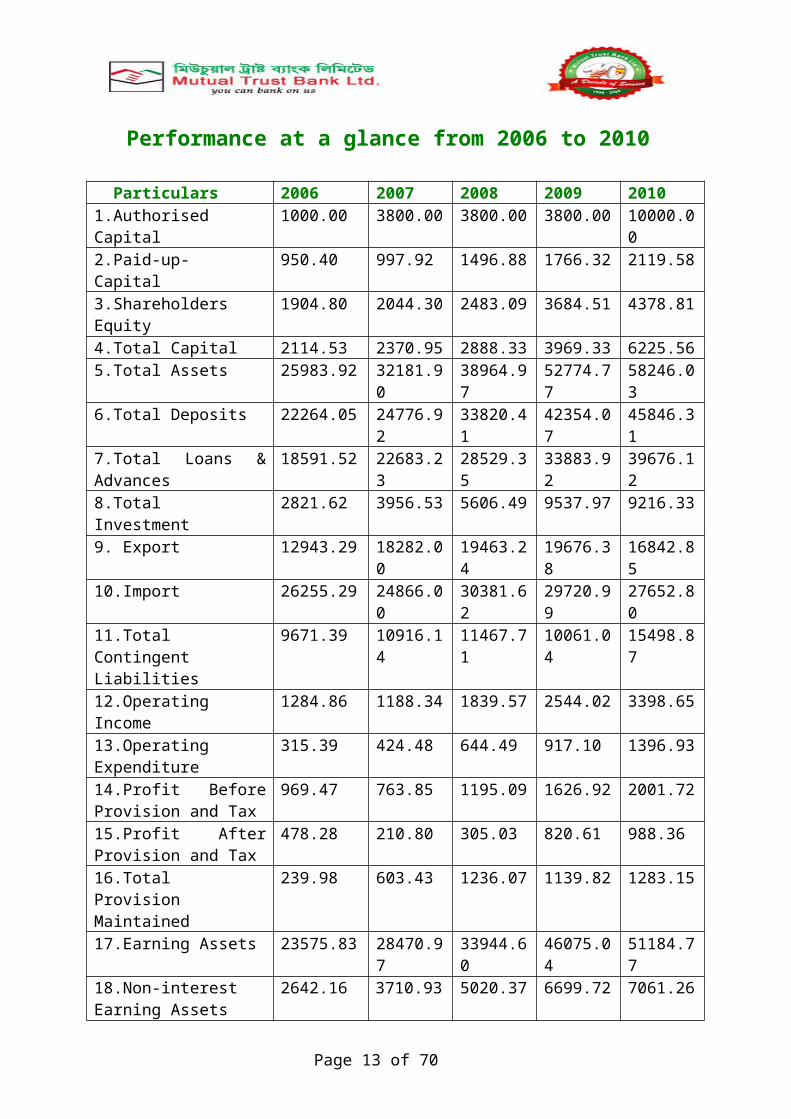

2.7.4 Five Years at a Glance

Mutual Trust Banks Performance Given Below

Page 12 of 70

Performance at a glance from 2006 to 2010

Particulars 2006 2007 2008 2009 20101.AuthorisedCapital

1000.00 3800.00 3800.00 3800.00 10000.00

2.Paid-up-Capital

950.40 997.92 1496.88 1766.32 2119.58

3.ShareholdersEquity

1904.80 2044.30 2483.09 3684.51 4378.81

4.Total Capital 2114.53 2370.95 2888.33 3969.33 6225.565.Total Assets 25983.92 32181.9

038964.97

52774.77

58246.03

6.Total Deposits 22264.05 24776.92

33820.41

42354.07

45846.31

7.Total Loans &Advances

18591.52 22683.23

28529.35

33883.92

39676.12

8.TotalInvestment

2821.62 3956.53 5606.49 9537.97 9216.33

9. Export 12943.29 18282.00

19463.24

19676.38

16842.85

10.Import 26255.29 24866.00

30381.62

29720.99

27652.80

11.TotalContingentLiabilities

9671.39 10916.14

11467.71

10061.04

15498.87

12.OperatingIncome

1284.86 1188.34 1839.57 2544.02 3398.65

13.OperatingExpenditure

315.39 424.48 644.49 917.10 1396.93

14.Profit BeforeProvision and Tax

969.47 763.85 1195.09 1626.92 2001.72

15.Profit AfterProvision and Tax

478.28 210.80 305.03 820.61 988.36

16.TotalProvisionMaintained

239.98 603.43 1236.07 1139.82 1283.15

17.Earning Assets 23575.83 28470.97

33944.60

46075.04

51184.77

18.Non-interestEarning Assets

2642.16 3710.93 5020.37 6699.72 7061.26

Page 13 of 70

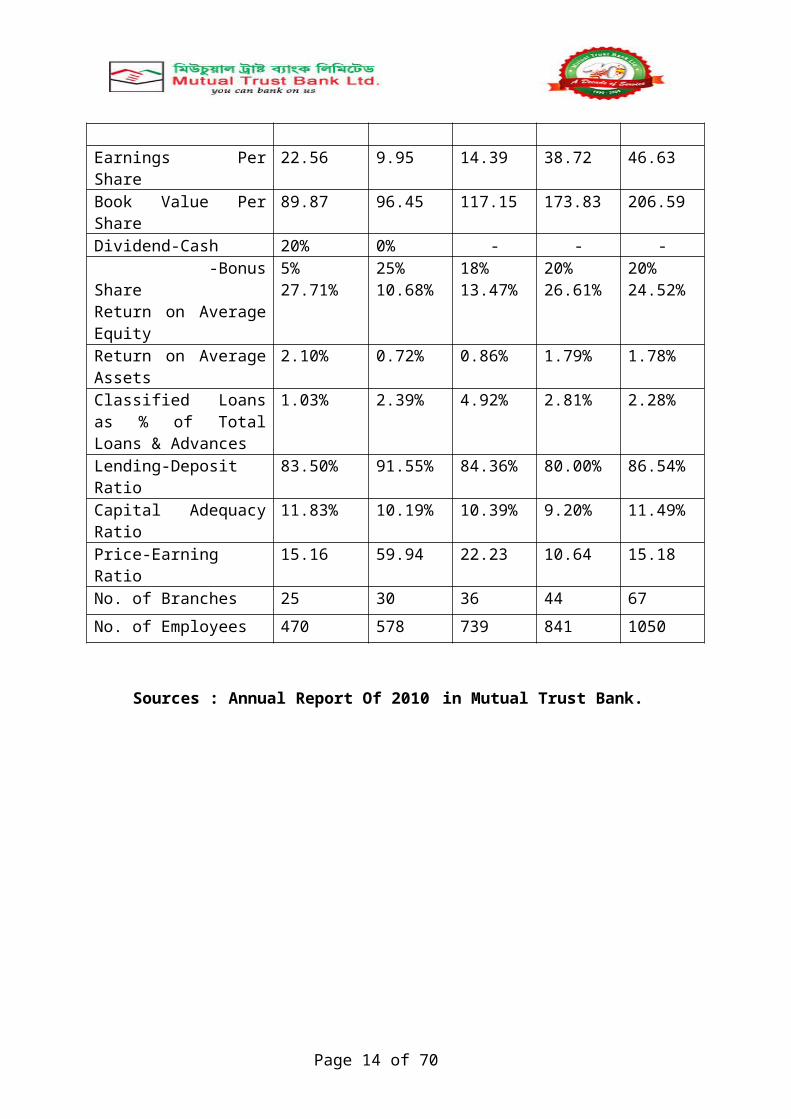

Earnings PerShare

22.56 9.95 14.39 38.72 46.63

Book Value PerShare

89.87 96.45 117.15 173.83 206.59

Dividend-Cash 20% 0% - - - -BonusShare Return on AverageEquity

5%27.71%

25%10.68%

18%13.47%

20%26.61%

20%24.52%

Return on AverageAssets

2.10% 0.72% 0.86% 1.79% 1.78%

Classified Loansas % of TotalLoans & Advances

1.03% 2.39% 4.92% 2.81% 2.28%

Lending-DepositRatio

83.50% 91.55% 84.36% 80.00% 86.54%

Capital AdequacyRatio

11.83% 10.19% 10.39% 9.20% 11.49%

Price-EarningRatio

15.16 59.94 22.23 10.64 15.18

No. of Branches 25 30 36 44 67No. of Employees 470 578 739 841 1050

Sources : Annual Report Of 2010 in Mutual Trust Bank.

Page 14 of 70

Page 15 of 70

FOREIGN EXCHANGE

Page 16 of 70

Foreign Exchange Division

3.1.1 Meaning of Foreign Exchange

Foreign Exchange means exchange foreign currency between twocountries. If we consider ‘Foreign Exchange’ as a subject,then it means all kind of transactions related to foreigncurrency. In other wards foreign exchange deals with foreignfinancial transactions.H.E. Evitt defined “Foreign Exchange” as the means andmethods by which rights to wealth expressed in terms of thecurrency of one country are converted into rights to wealthin terms of the currency of another country.

3.1.2 Necessity of Foreign Exchange

No country is self-sufficient in this world. Every one ismore or less dependent on another, for goods or services.Say, Bangladesh has cheap manpower whereas Saudi Arabia hascheap petroleum. So Bangladesh is dependent on Saudi Arabiafor petroleum and Saudi Arabia is dependent on Bangladesh forcheap manpower. People of one country are going to anothercountry for Education, Medical Service etc. One-countryexport Agricultural commodities, another country exportsIndustrial products, all these transactions needs ForeignCurrency & are related to Foreign Exchange.

3.1.3 Function of Foreign Exchange

The Bank actions as a media for the system of foreignexchange policy. For this reason, the employee who is relatedof the bank to foreign exchange, especially foreign businessshould have knowledge of these following functions: Rate of exchange works. How the rate of exchange works. Premium and discount.

Page 17 of 70

Risk of exchange rate. Causes of exchange rate. Exchange control. Convertibility. Exchange position. Intervention money. Foreign exchange transaction. Foreign exchange trading. Export and import letter of credit. Non-commercial letter of credit.

3.1.4 Activities of Foreign Exchange

There are three kinds of foreign exchange transactions: Import. Export. Remittance.

3.1.5 Regulations for foreign exchange

Foreign exchange transactions are being controlled by thefollowing rules & regulations:

Foreign Exchange Regulation (FER) Act, 1947 in the BritishIndia provides the legal basis for regulating certainpayments, dealings in foreign exchange and securities and theimport and export of currency and bullion. This Act was firstadapted in Pakistan and then, in Bangladesh

Authorised Dealers in foreign exchange are required to bringthe foreign exchange regulations to the notice of theircustomers in their day-to-day dealings and to ensurecompliance with the regulations by such customers. Theauthorized dealers should report to the Bangladesh Bank anyattempt, direct or indirect, of evasion of the provisions ofthe Act, or any rules, orders or directions issued thereunder.

Page 18 of 70

Basic regulations under the FER Act are issued by theGovernment as well as by the Bangladesh Bank in the form ofNotifications which are published in the Bangladesh Gazette.

The authorized dealers must maintain adequate and properrecords of all foreign exchange transactions and furnish suchparticulars in the prescribed returns for submission to theBangladesh Bank. They should continue to preserve the recordsfor a reasonable period for ready reference as also forinspection, if necessary, by Bangladesh Bank's officials.

3.1.6 Responsibilities of Foreign Exchange

This division is responsible for monitoring and supervisingthe foreign exchange dealings of the bank. It performs thefollowing functions:

Making guidelines and frameworks for foreign dealingscomplying the rules of Bangladesh Bank

Circulating instructions of Bangladesh Bank Maintaining correspondence with foreign banks and

exchange houses with which it has exchange arrangement Maintaining NOSTRO accounts with banks in abroad Fixing and sending foreign exchange rates to Authorized

Dealer (AD) 3.1.7 Foreign Trade

Foreign trade can be easily defined as a business activity,which crosses national boundaries. These may be betweenparties or government ones. Trade among nations is a commonoccurrence and normally benefits both the exporter andimporter.

Page 19 of 70

Foreign trade can usually be justified on the principle ofcomparative advantage. According to this economic principle,it is economically profitable for the country to specializein the production of that commodity in which the producercountry has the grater comparative advantage and to allowthe other country to produce that commodity in which it hasthe lesser comparative advantage. It includes the spectrumof goods, services, investment, technology transfer etc.

The banks, which provide such transactions, are referred toas rendering international banking operations. Internationaltrade demands a flow of goods from seller to buyer and ofpayment from buyer to seller. And this flow of goods andpayment are done through Letter of Credit.

3.1.8 Letter of credit

Letter of credit (L/C) can be defined as a “Credit Contract”whereby the buyer’s bank is committed (on behalf of thebuyer) to place an agreed amount of money at the seller’sdisposal under some agreed conditions. Since the agreedconditions include, amongst other things, the presentationof some specified documents, the letter of credit is calledDocumentary Letter of Credit.

Is to make a payment to or to the order of a thirdparty(the beneficiary) or is to accept and pay bills ofexchange(Drafts)drawn by the beneficiary, or

Authorizes another bank to effect such payment or toaccept and pay such bills of exchange (Drafts)

Authorizes another bank to negotiate against stipulateddocuments provide that terms and conditions arecomplied with.

3.1.9 Types of Documentary Credit

Documentary Credits may be either:

Page 20 of 70

(a) Revocable credit(b) Irrevocable credit(c) Revolving credit(d) Transferable credit(e) Back-to-Back credit

(a) Revocable credit

A revocable credit is a credit that can be amended or cancelled by the issuing bank at any time without prior notice to the seller.

(b) Irrevocable credit

An irrevocable credit constitutes a definite undertaking ofthe issuing bank (since it can not be amended or cancelledwithout the agreement of all parties thereto), provided thatthe stipulated documents are presented and the terms andconditions are satisfied by the seller. This sort of creditis always preferred to revocable letter of credit.

(c)Revolving Credit:

The revolving credit is one that provides for restoring thecredit to the original amount after it has been utilized.

(d) Transferable Credit:A transferable credit is one that can be transferred by theoriginal beneficiary in full or in part to one or moresubsequent beneficiaries such credit can be transferred onceonly unless otherwise specified.

(e) Back-to-Back Credit:

The back-to-back credit is a new credit opened on the basisof an original credit in favor of another beneficiary.

3.1.10. Parties to a letter of Credit:The parties are:

The Issuing Bank,

Page 21 of 70

The Confirming Bank, if any, and

The Beneficiary.

Other parties that facilitate the Documentary Creditare:

The Applicant, The Advising Bank, The Nominated Paying/ Accepting Bank, and The Transferring Bank, if any.

Issuing Bank – It is the bank which opens/issues a L/C onbehalf of the importer.Confirming Bank – It is the bank, which adds its confirmationto the credit and it done at the request of issuingbank. Confirming bank may or may not be advising bank.Beneficiary Bank –Beneficiary is the party in whose favor theL\C is established.Applicant – Applicant is the person who request the openingbank to open a L\C. He is also known as importer\buyer.

Advising / Notifying Bank – is the bank through whichthe L/C is advised to the exporters. This bank isactually situated in exporters country. It may alsoassume the role of confirming and /or negotiating bankdepending upon the condition of the credit.

Negotiating Bank – is the bank, which negotiates thebill and pays the amount of the beneficiary. Theadvising bank and the negotiating bank may or may not bethe same. Sometimes it can also be confirming bank.

Paying / Accepting Bank – is the bank on which the billwill be drawn (as per condition of the credit). Usuallyit is the issuing bank.

Page 22 of 70

Reimbursing bank – is the bank, which would reimburse

the negotiating bank after getting payment –instructions from issuing bank.

3.1.11.Some Important Documents of L\C

(a) Forwarding

Forwarding is the letter given by the advising bank to theissuing bank. Several copies are sent to the issuingbank. All copies including original should be kept in thebank.

(b) Bill of Exchange

According to the section 05, Negotiable Instruments (NI) Act-1881, A “bill of exchange” is an instrument in writingcontaining an unconditional order signed by the maker,directing a certain person to pay [on demand or at fixed ordeterminable future time] a certain sum of money only to orto the order of a certain person or to the bearer of the instrument. It may be either at sight orcertain day sight. At sight means making payment wheneverdocuments will reach in the issuing bank.

(c) Invoice

Invoice is the price list along with quantities. Severalcopies of invoice are give. Two copies should be given tothe client and the other copies should be kept in the bank.If there is only one copy, then its photocopy should be keptin the bank and the original copy should be given to the client. If anyoriginal invoice contains the custom’s seal, then it cannotbe given to the client.

(d) Bill of Lading

Page 23 of 70

Bill of Lading is the bill given by shipping company to theclient. Only one copy of Bill of Lading should be given tothe client and the remaining copy should be kept in the bank.

(e) Packing List Packing list is the letter describing the number of packetsand there size. If there are several copies, then two copiesshould be given to the client and the remaining should bekept in the bank. But if there is only one copy, then thephotocopy should be kept in the bank and the original copyshould be given to the client.

(f) Certificate of Origin

Certificate of origin is a document describing the producingcountry of the goods. One copy of the certificate of originshould be given to the client and the remaining copy shouldbe kept in the bank. But if there is only one copy, then thephotocopy should be kept in the bank and the original shouldbe given to the client.

(g) Shipment Advice

The copy mentioning the name of the insurance company should be given to the client and the remaining copies should be kept in the bank. But if only one copy is given, then the photocopy should be kept in the bank and the original copy should be given to the bank.

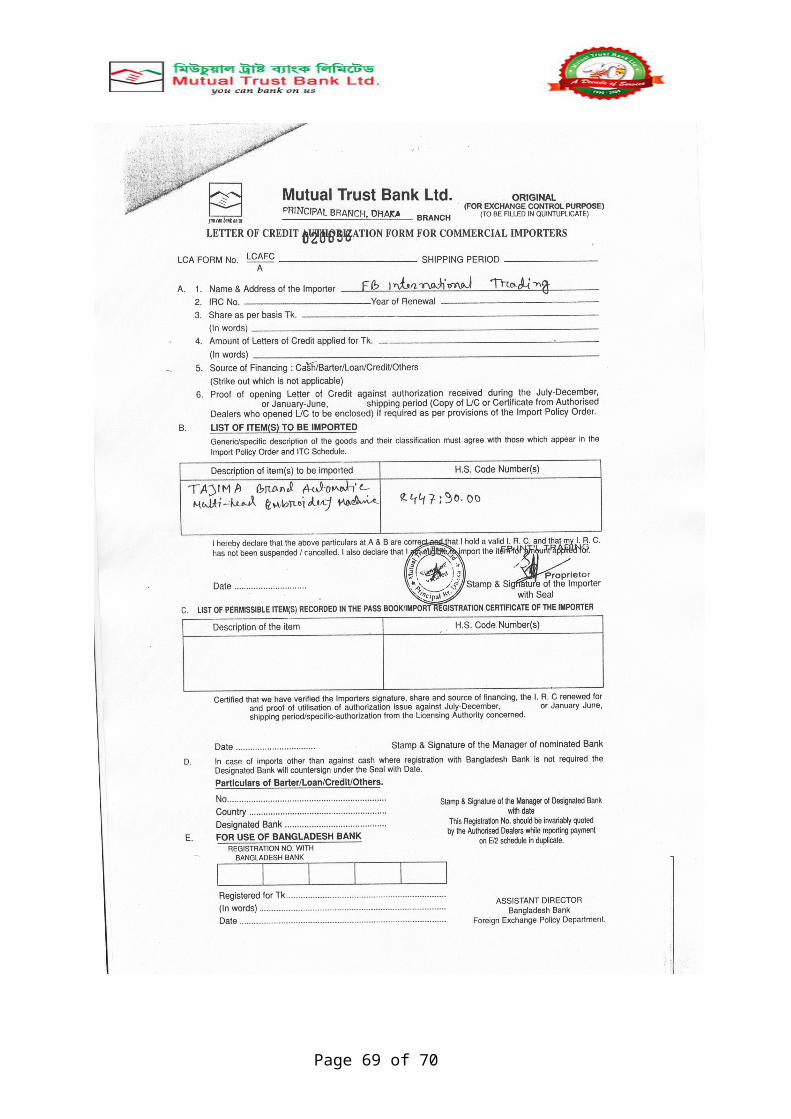

3.1.12.Documents Required for open L\C

The importer after receiving the preformed invoice from theexporter, by applying for the issue of a documentary credit,the importer request his bank to make a promise of payment tothe supplier. Obviously, the bank will only agree to thisrequest if it can rely on reimbursement by the applicant. Theapplicant must therefore have adequate funds in the bankaccount or a credit line sufficient to cover the requiredamount. Banks deal in documents and not in goods. Once the

Page 24 of 70

bank has issued the credits its obligation to pay isconditional on the presentation of the stipulated documentswith in the prescribed time limit. The importer should submitthe following documents for opening L/C:

Valid Import Registration Certificate

(commercial/industrial). Tax Identification Number Certificate (TIN) Membership Certificate of a recognized Trade Association

as per IPO. A declaration, in triplicate, that the importer has paid

income-tax or submitted income tax returns for the yearpreceding year.

Pro-forma Invoice or Indent duly accepted by the

importer. Insurance Cover Notice with money paid receipt covering

value goods to the imported. L/C Application form duly signed by the importer. Letter of Credit authorization Form (LCAF) commercial

or industrial as the case may be duly signed by theimporter and incorporation new ITC number of at least 6digits under the Harmonized system as given in theimport Trade Control schedule 1998.

IMP Form duly signed by the importer

3.1.13. FORM – IMPThis form is prepared for maintaining account of the money,which goes out side the country for the purpose of payment.This form is required by Bangladesh Bank. It is anapplication for permission under 4/5 of the Foreign ExchangeRegulation Act, 1947 to purchase foreign currency for thepayment of import. 3.1.14. Copies of IMP - FORMIMP – FORM has four copies:

1. Original copy for Bangladesh Bank.

Page 25 of 70

2. Duplicate copy for authorized dealers. It is issued for

processing Exchange Control Copy of bill of entry orcertified invoice.

3. Triplicate copy for authorized dealers’ record.4. Quadruplicate copy for submission to the bank in case

of imports where documents are retired.

Following documents are sent with FORM-IMP:a) Letter of Credit Authorization Form,b) One copy of invoice,c) Indent copy / proforma invoice.

The following information is included in the FORM-IMP:i. Name and address of the authorized dealer,ii. Amount of foreign currency in words and figures,iii. Names and address of the beneficiary,

iv. L/C Authorization Form number and date,v. Registration number of L/C Authorization Form with

Bangladesh Bank, andvi. Description of the goods.

3.2 Import

3.2.1 Definition

Imports of goods into Bangladesh is regulated by the ministryof commerce and industry in terms of the Import and Export(Control) Act, 1950, with import policy orders issued by annually, and Public Notices issued fromtime to time by the office of the Chief Controller of Importand Export (CCI & E). Through the process of import somevital but which are inadequate in our country products areimported to meet the local needs of the people.

3.2.2 Import MechanismTo import, a person should be competent to be an ‘importer’.According to Import and Export (Control) Act, 1950, theofficer of Chief Controller of Import and Export provides theregistration (IRC) to the importer. After obtaining this, the

Page 26 of 70

person has to secure a letter of credit authorization (LCA)from Bangladesh Bank. And then a person becomes a qualifiedimporter. He requests or instructs the opening bank to openan L/C. 3.2.3 Import Procedures

An importer is required to have the following to importthrough MTBL

i. Applicant has to apply for opening L/C by aprescribed form.

ii. Applicant has to submit the Letter of Indent orLetter of Proforma Invoice.

iii. Applicant has to submit IRC (Indentors RegistrationCertificate). It is a certificate being renewedevery year. This certificate is necessary if thecontract is made between the buyers and the agentsof the sellers. IRC is of two types – COM and IND.COM is given for commerce purpose and IND is givenfor industrial purpose.

iv. Applicant has to submit LCAF (Letter of CreditAuthorization Form).

v. Applicant has to submit insurance document.

vi. Applicant has to prepare FORM-IMP.

vii. Recently, there has been made a provision to give acertificate named TIN (Tax Payers IdentificationNumber). Taxation department issues thiscertificate.

viii. Then after proper scrutiny bank will open anL/C.

While opening L/C, importer must keep certain percentage ofthe document value in the bank as margin.

3.2.4 Accounting Treatment For Opening L/C

For opening L/C, importer will apply to the issuing bank. Inthat case, importer is called applicant or opener. After

Page 27 of 70

opening an L/C bank will create a contingent liability. Inthat case, the accounting posting will be the following:

Customers LiabilityDr.

Contingent Liability Cr.

Generally L/C is opened against some margin.

While paying the money by the issuing bank, issuing bank willreverse the above entry and the entry will be

Contingent Liability Dr. Customers Liability Cr.

Then the issuing bank will give another entry---

Payment Against Document (PAD) Dr. Prime General Account Cr. Exchange Gain

Cr.

PAD will debit because the bank will pay the money againstsome documents. MTBL General Account is a miscellaneousaccount. It will be credited because by this entry MTBLcreates a liability. He has to pay the money to the advisingbank. And the gain made by the transaction is shown atExchange Gain Account.

All these entries are made after receiving some documentsfrom the exporters. The above procedure is called Lodging.After giving the above entry, MTBL will inform the clientsfor collecting the documents from the bank. Importers willpay the due to the bank and collects the documents. In thatcase, the entry will be --- Party Account Dr. PAD Account Cr.

Page 28 of 70

After opening the L/C, MTBL (issuing bank) must receive thedocuments for any other proceedings. These documents are ---

i. Bill of Lading, ii. Invoice,iii. Packing List,iv. Country of Origin.

3.2.5 Import Policy3.2.5 Import Policy

At the beginning of each financial year, the Chief Controllerof Imports and Exports announces the Import policy coveringvarious aspects of imports in the coming year. The mainpoints covered by the Import Policy are the following:

Items eligible for imports during the shipping period. Items importable against – Cash foreign Exchange, Foreign

aid and barter, Wages Earners Scheme. The Procedure for induction of new comers into the import

trade. The procedure for imports by industrial consumers and

commercial importers and for import under Wages Earnersscheme.

Procedure for formation of groups. The procedure for submission of application for Repeat

License. The dates for opening Letter of Credit, and shipment and

the rules for revalidation of the License/LCA .

3.2.6 Licensing for Imports3.2.6 Licensing for Imports:

Most imports into Bangladesh require a license from thelicensing authority. In recent years, however, the task of

Page 29 of 70

licensing has increasingly been delegated to the commercialbanks. Beginning from the shipping period 1983-84, thecommercial banks have been entrusted with the responsibilityof licensing imports in both industrial and commercialsectors. Licensing is done by the commercial banks by meansof a specially designed form known as Letter of CreditAuthorization or simply LCA. The following documents arerequired to be submitted by the importer to his banker:

o LCA form properly filled in and signed.o L\C application.o Purchase contract in the shape of an indent or

pro-forma invoice.o Insurance cover note.o Membership certificate from a Chamber of

Commerce and Industry or registered TradeAssociation.

3.2.7 Verification and Lodgment of Document by the opening3.2.7 Verification and Lodgment of Document by the openingBankBank

On receipt of the shipping documents from the negotiatingbank, the L/C opening bank should carefully examine these toensure that they confirm to the terms of the credit; inparticular, the following are the main points that should belooked into:

The documents have been negotiated within the stipulateddates.

The amount drawn dose not exceeds the amount authorized inthe credit.

The bill of exchange is drawn in the manner stipulated inthe credit; the amount is written in figures and words andcorresponds to that of the invoice, and properly endorsed.

The merchandise in properly invoiced in the name of theopener of the credit i.e. the buyer or the importer withfull description of the merchandise indicating, whereapplicable, the unit price. The invoice is signed andbears Bangladesh Bank’s Registration number.

Page 30 of 70

The Bill of Lading is clean, shipped ‘on board’ showing

freight prepaid and endorsed to the order of the issuingbank.

The certificate of origin given by the supplier is inconformity with that mentioned in the credit.

Other documents like weight list, packing list, pre-shipment inspection certificate etc. have been receivedand are in accordance with the terms of the credit.

3.2.8 Applicant of the client to open the L/C3.2.8 Applicant of the client to open the L/C

The client will approach to open the L/C in Bank’s prescribedform duly stamped & signed along with the following paper &documents.

Indent/Proforma invoice. Insurance cover note with money receipt. LCAF duly felled in & signed. Membership certificate from chamber of commerce/Trade

Association. Tax payment certificate/declaration. IMP & TM form signed by the importer. Charge documents. IRC pass book, Trade license, Membership certificate & VAT

registration certificate in case of new client. Export L/C in case of Back-to-Back L/C.

3.2.9 Importer points to prepare an L/C

To prepare an L/C the Ads should take care on the followingpoints:L/C Number, Place & Date of issue, Date & Place of expiry,Shipment date, Presentation period, Applicant, Beneficiary,Advising Bank Account, Part-shipment & Transshipment,Availability, Port of Shipment, & Port of destination, Tenureof the Draft, Documents required, Payment, UCP, Bill oflading, Bill of Exchange, Pre-shipment Inspection, Datacontent, Special Conditions, Authenticity of the credit.

3.2.10 Lodgment of Import Documents3.2.10 Lodgment of Import Documents

Page 31 of 70

If import documents found in order, it to be made entry inthe bill register and necessary voucher to be passed, puttingBill number on the documents, this process is called Lodgmentof the bill. The word ‘Lodgment’ means temporary stay. Sincethe documents, stay at this stage for a temporary period i.e.up to retirement of the documents, the process is calledLodgment, Bank must lodge the documents immediate after receipt of the same, not exceeding 7 bankingdays, following the day of receipt of the documents.

3.2.11 Procedures of Lodgment3.2.11 Procedures of Lodgment

Bill register: Bank wills entry the documents in the billregister. Bill register must include date of Lodgment,Bill No., Bill of Exchange No, Amount, and Name of theNegotiation Bank, B/L no & date, merchandise, retirementdate & other particulars.

Application of rate: Foreign Currency would be convertedat B.C selling rate ruling on the date of Lodgment.

Exchange Control Form: IMP & Tm form must be filed in andsigned by the importer at the time of Lodgment.

Endorsement of LCAF: LCA form must be endorsed showingutilization of shipment.

Noting on the File: Utilized amount showing bill no to benoted on the printed format of L/C file.

3.2.12 Retirement of the Documents

The process of collecting documents from bank by the importeris called retirement of the documents. The importer givesnecessary instructions to the bank for retirement of theimport bills or for the disposal of the shipping documents toclear the imported goods from the customs authority. Theimporter may instruct the bank to retire the documents by

Page 32 of 70

debiting his current account with the bank or by creatingLoan Against Trust Receipt (LTR). Following steps are takenwhile retiring the documents –

Calculation of interest. Calculation of other charges. Passing vouchers. Entry in the register. Endorsement in the Bill of Lading And other transport

documents and in the Bill of Exchange.

3.3 Export

3.3.1 Definition Creation of wealth in any country depends on the expansion ofproduction and increasing participation in internationaltrade. By increasing production in the export sector we canimprove the employment level of such a highly populatedcountry like Bangladesh. Bangladesh exports a large quantityof goods and services to foreign households. Readymadetextile garments (both knitted and woven), Jute, Jute-made products, frozen shrimps, tea are the main goods that Bangladeshi exporters export to foreign countries.

Garments sector is the largest sector that exports the lion share of the country's export. Bangladesh exports most of itsreadymade garments products to U.S.A and European Community (EC) countries. Bangladesh exports about 40% of its readymadegarments products to U.S.A. Most of the exporters who export through MTBL are readymade garments exporters. They open export L/Cs here to export their goods, which they open against the import L/Cs opened by their foreign importers.Export L/C operation is just reverse of the import L/Coperation. For exporting goods by the local exporter, bankmay act as advising banks and collecting bank (negotiablebank) for the exporter.

3.3.2 Export PolicyExport policies formulated by the Ministry of Commerce, GOB provide the overall guideline and incentives for promotion of

Page 33 of 70

exports in Bangladesh. Export policies also set out commodity-wise annual target. It has been decided to formulate these policies to cover a five-year period to make them contemporaneous with the five-year plans and to provide the policy regime.The export-oriented private sector, through theirrepresentative bodies and chambers are consulted in theformulation of export policies and are also represented inthe various export promotion bodies set up by the government.

3.3.3 Export Incentives Financial Incentives

Restructuring of Export Credit Guarantee Scheme; Convertibility of Taka in current account; Exporters can deposit 40% of FOB value of their

export earnings in own accounts in dollar and poundsterling;

Export Development Fund; Expansion of export credit period from 180 days to

270 days; 50% tax rebate on export earnings; Bonded warehouse facilities to 100% export oriented

firms; Duty free import of capital equipment for 100%

export oriented firms;

A. General Incentives National Export Trophy to successful exporters; Training course on external trade; Arrangement of international trade fairs,

commodity-based exhibitions in the country andparticipation in foreign trade fairs;

B. Other Incentives

Page 34 of 70

Assistance in improvement of quality and packaging

of exportable items; Simplification of export procedures;

3.3.4 Export ProceduresThe import and export trade in our country are regulated bythe Import and Export (Control) Act, 1950.Under the exportpolicy of Bangladesh the exporter has to get valid Exportregistration Certificate (ERC) from Chief Controller ofImport & Export (CCI&E). The ERC is required to renew everyyear. The ERC number is to incorporate on EXP forms and otherpapers connected with exports. (a) Registration of Exporters For obtaining ERC, intending Bangladeshi exporters arerequired to apply to the controller/ Joint Controller/ DeputyController/ Assistant Controller of Imports and Exports,Dhaka/ Chittagong/ Rajshahi/ Mymensingh/ Sylhet/ Comilla/Barishal/ Rangpur in the prescribed form along with thefollowing documents:

Nationality and Assets Certificate; Memorandum and Article of Association and

Certificate of Incorporation in case of LimitedCompany;

Bank Certificate; Income Tax Certificate; Trade License etc.

(b) Securing the OrderAfter getting ERC Certificate the exporter may proceed tosecure the export order. He can do this by contacting thebuyers directly or through agent.In this purpose the exporter may get help from:

License Officer; Buyer’s Local Agent; Export Promoting Organization; Bangladesh Mission Abroad; Chamber of Commerce (local & foreign)

Page 35 of 70

Trade Fair etc.

(c) Signing the ContractAfter communicating buyer, exporter has to get contracted(writing or oral) for exporting exportable items fromBangladesh detailing commodity, quantity, price, shipment,insurance and marks, inspection and arbitration etc.

(d) Receiving Letter of CreditAfter getting contract for sale, exporter should ask thebuyer for Letter of Credit (L/C) clearly stating terms andconditions of export and payment.The following are the main points to be looked into forreceiving/ collecting export proceeds by means of DocumentaryCredit:

(1) The terms of the L/C are in conformity with thoseof the contract;

(2) The L/C is an irrevocable one, preferably confirmedby the advising bank;

(3) The L/C allows sufficient time for shipment andnegotiation.

Terms and conditions should be stated in the contract clearlyin case of other mode of payment:

Cash in advance; Open account; Collection basis (Documentary/ Clean)

(e) Procuring the materials After making the deal and on having the L/C opened in hisfavor, the next step for the exporter is to set about thetask of procuring or manufacturing the contractedmerchandise.(f) Shipment of goods Then the exporter should take the preparation for exportarrangement for delivery of goods as per L/C and then prepareand submit shipping documents for Payment/ Acceptance/Negotiation in due time.

Page 36 of 70

Documents for shipment:

EXP form, ERC (valid), L/C copy, Customer Duty Certificate, Shipping Instruction, Transport Documents, Insurance Documents, Invoice, Other Documents, Bills of Exchange (if required) Certificate of Origin, Inspection Certificate, Quality Control Certificate,

(g)Final StepSubmission of the documents to the Bank for negotiation.3.3.5 Export FinancingFinancing exports constitutes an important part of a bank’sactivities. Exporters require financial services at fourdifferent stages of their export operation. During each ofthese phases exporters need different types of financialassistance depending on the nature of the export contract.

Pre-shipment credit Post-shipment credit

Pre-shipment creditPre-shipment credit, as the name suggests, is given tofinance the activities of an exporter prior to the actualshipment of the goods for export. The purpose of such creditis to meet working capital needs starting from the point ofpurchasing of raw materials to final shipment of goods forexport to foreign country. Before allowing such credit tothe exporters the bank takes into consideration about thecredit worthiness, export performance of the exporters,together with all other necessary information required forsanctioning the credit in accordance with the existing rules

Page 37 of 70

and regulations. Pre-shipment credit is given for thefollowing purposes:

Cash for local procurement and meeting relatedexpenses.

Procuring and processing of goods for export. Packing and transporting of goods for export. Payment of insurance premium. Inspection fees. Freight charges etc.

An exporter can obtain credit facilities against lien on theirrevocable, confirmed and unrestricted export letter of credit in form of the followings:

a) Export cash credit (Hypothecation)b) Export cash credit (Pledge)c) Export cash credit against trust receipt.d) Packing credit.e) Back to back letter of credit.f) Credit against Red-clause letter of credit.

(a) Export cash credit (Hypothecation)Under this arrangement, a credit is sanctioned againsthypothecation of the raw materials or finished goodsintended for export. Such facility is allowed to the firstclass exporters. As the bank has got no security in thiscase, except charge documents and lien on exports L/C orcontract, bank normally insists on the exporter infurnishing collateral security. The letter of hypothecationcreates a charge against merchandise in favour of the bank.But neither the ownership nor the possession is passed toit.

(b) Export cash Credit (Pledge)Such Credit facility is allowed against pledge of exportablegoods or raw materials. In this case cash credit facilitiesare extended against pledge of goods to be stored in the godown under bank’s control by signing letter of pledge andother pledge documents. The exporter surrenders the physical

Page 38 of 70

possession of the goods under banks effective control assecurity for payment of bank dues. In the event of failureof the exporter to honour his commitment, the bank can sellthe pledged merchandise for recovery the advance.

(c) Export Cash Credit Against Trust ReceiptIn this case, credit limit is sanctioned against trustreceipt (TR). Here also unlike pledge, the 3xportable goodsremain in the custody of the exporter. He is required toexecute a stamped export trust receipt in favour of thebank, he holds wherein a declaration is made that goodspurchas4ed with financial assistance of bank in trust forthe bank. This type of credit is granted when the exporterwants to utilize the credit for processing, packing andrendering the goods in exportable condition and when itseems that exportable goods cannot be taken into bank’scustody. This facility is allowed only to the first classparty and collateral security is generally obtained in thiscase.

(d) Packing CreditPacking Credit is essentially a short-term advance grantedby a Bank to an exporter for assisting him to buy, process,manufacture, and pack and ships the goods. Generally formovement of goods from the hinterland areas to the ports ofshipment the Banks provide interim facilities by way ofPacking Credit. This type of credit is sanctioned for the transitionalperiod starting from dispatch of goods till the negotiationof the export documents. Practically except for singletransaction, most of the pre-shipment credits are allowed inthe form of limits duly sanctioned by Bank in favour ofregular exporters for a particular period.

Charge Documents for Packing Credit

Page 39 of 70

Banker should obtain the following charge documents duly stamped prior to disbursement:

I) Demand Promissory Note ii) Letter of Arrangement iii) Letter of Lien of Packing Credit (On special

adhesive stamp)iv) Letter of Disbursement v) Packing Credit Letter

(e) Back to Back Letter of Credit (BTB)Bangladesh is a developing country. After receiving orderfrom the importer, very frequently exporters face problemsof scarcity of raw material. Because some raw materials arenot available in the country. These have to be collectedfrom abroad. In that case, exporter gives lien of export L/Cto bank as security and opens an L/C against it forimporting raw materials.

Sometimes there is provision in the export L/C that theimporter can use the certain portion of the export L/Camount for importing accessories that are necessary for themaking of the product. Only in that case, BTB is opened.

(f) Advance against Red-clause Letter of CreditUnder Red clause letter of credit, the opening bankauthorizes the Advising Bank/Negotiating Bank to makeadvance to the beneficiary prior to shipment to enable himto procure and store the exportable goods in anticipation ofhis effecting the shipment and submitting a bill under theL/C. as the clause containing such authority is printed inred ink, the L/C is called Red clause and Green clauserespectively. Though it is not prohibited, yet very rare inBangladesh.

Post Shipment Credit

Page 40 of 70

This type of credit refers to the credit facilities extendedto the exporters by the banks after shipment of the goodsagainst export documents. Necessity for such credit arisesas the exporter cannot afford to wait for a long time forwithout paying manufacturers/suppliers. Before extendingsuch credit, it is necessary on the part of banks to lookinto carefully the financial soundness of exporters andbuyers as well as other relevant documents connected withthe export in accordance with the rules and regulations inforce. Banks in our country extend post shipment credit tothe exporters through:

a) Negotiation of documents under L/C;b) Foreign Documentary Bill Purchase (FDBP):c) Advances against Export Bills surrendered for

collection;

(a) Negotiation of documents under L/CThe exporter presents the relative documents to thenegotiating bank after the shipment of the goods. A slightdeviation of the documents from those specified in the L/Cmay rise an excuse to the issuing bank to refuse thereimbursement of the payment already made by the negotiatingbank. So the negotiating bank must be careful, prompt,systematic and indifferent while scrutinizing the documentsrelating to the export.

(b) Foreign Documentary Bill Purchase (FDBP)Sometimes the client submits the bill of export to bank forcollection and payment of the BTB L/C. In that case, bankpurchases the bill and collects the money from the exporter.MTBL subtracts the amount of bill from BTB and gives therest amount to the client in cash or by crediting hisaccount or by the pay order.

Date Reference number (FDBP) Name of the drawee

Page 41 of 70

Name of the collecting bank Conversion rate Bill amount both in figure & in Taka. Export form number Export L/C number

(c) Advances against Export Bills surrendered for collection Banks generally accept bills for collection of proceeds when they are not drawn under an L/C or when the documents, even though drawn against an L/C contain some discrepancies.Bills drawn under L/C, without any discrepancy in the documents, are generally negotiated by the bank and the exporter gets the money from the bank immediately. However, if the bill is not eligible for negotiation, the exporter may obtain advance from the bank against the security of export bill.

3.3.6 Export Documents Checking

General verification: L\ C restricted or not. Exporter submitted documents before expiry dateof the credit. Shortage of documents etc. Particular verification: Each and every document should be verified with theL/C. Cross verification:

Verified one documents to another

After proper examination or checking of a described Exportdocument banker may find following discrepancies:

GENERAL: Late shipment Late presentation L/C expired L/C over-drawn Partial shipment or transshipment beyond L/C terms.

Page 42 of 70

BILL OF EXCHANGE (B/E) Amount of B/E differ with Invoice. Not drawn on L/C issuing Bank. Not signed Tenor of B/E not identical with L/C. Full set not submitted.

COMMERCIAL INVOICE(C/I): Not issued by the Beneficiary. Not signed by the Beneficiary. Not made out in the name of the Applicant Description, Price, quantity, sales terms of

the goods not corresponds to the Credit. Not marked one fold as Original. Shipping Mark differs with B/L & Packing

List.

PACKING LIST: Not market one fold as Original. Not signed by the Beneficiary. Shipping marks differ with B/L.

BILL OF LADING / AIRWAY BILL ETC (TRANSPORT DOCUMENTS)

Full set of B/L not submitted. “Shipped on Board”, “Freight Prepaid” or “Freight

Collect” etc. notations are not marked on theB/L.

B/L not indicate the name and the capacity of the partyi.e. carrier or master, on whose behalf the agent issigning the B/L.

Shipped on Board Notation not showing name of Pre-carriage vessel/intended vessel.

Shipped on Board Notation not showing port of loadingand vessel name (In case B/L indicates a place ofreceipt or taking in charge different from the port ofloading).

Short Form B/L Charter party B/L

Page 43 of 70

Description of goods in B/L not agree with that of

Invoice, B/E & P/L Alterations in B/L not authenticated. Loaded on Deck. B/L bearing clauses or notations expressly declaring

defective condition of the goods and/or the packages.

OTHERS N.N. Documents not forwarded to buyers or forwarded

beyond L/C terms. Inadequate number of Invoice, Packing List, B/L & Others

submitted. Short shipment Certificate not submitted.

While checking the export documents following things must be taken in consideration. L/C terms Each and every clause in the L/C must be compliedwith meticulously and ensure the following:

That the documents are not state; That the documents are negotiated within the L/C

validity, That the documents value does not exceeds the L/C

value.

(i) Draft/Bill of Exchange Draft is to examine as under

Draft must be dated It must be made out in the name of the beneficiary’s bank

or to be endorsed to the bank. The signature of the drawer must be verified by the

negotiating bank. Amount must be tallied with the Invoice amount. It must be marked as drawn under L/C No……Dated…..Issued

by………..Bank.

(ii) Invoice It is to be scrutinized to ensure the following The Invoice is addressed to the Importer

Page 44 of 70

The full description of merchandise must be given in the

invoice strictly as per L/C. The price, quality, quantity, etc. must be as per L/C. The Invoice must be language in the language of L/C. No other charges are permissible in the Invoice beyond

the stipulation on the L/C. The amount of draft and Invoice must be same and within

the L/C value. If L/C calls for consular invoice, then the beneficiary’s

invoice is not sufficient. Number of Invoice will be submitted as per L/C. The shipping mark and number of packing list shown in the

B/L must be identical with those given in the Invoice andother documents.

The Invoice value must not be less than the valuedeclared in EXP Forms.

Invoice amount must be correct on the basis of price,quantity as per L/C.

Invoice amount, indicate sale terms/ Incoterms VIZ FOB,CFR, CIF etc.

(iii) Other documents

Beneficiary statement, VISA/Export License issued by EPB,Certificate of Origin, Weight Certificate, PhytosaitaryCertificate, Packing List, Inspection Certificate.Certificate of analysis, quality certificate, MCD dulysigned and any other documents required by L/C each of thesecertificates/documents conform to the goods invoice and arerelevant to L/C.

Negotiating Bank will check the above documents whether itis as per L/C or not. If Negotiating Bank finds everythingin order or as per export L/C, bank will negotiate thedocument and will disburse the generated fund as per Banksnorms. If the Negotiating Bank finds any discrepancies inthe documents, they will send the documents on collection orthey can negotiate under reserve by the request of theexporter or they can seek permission/Negotiation authorityfrom issuing Bank to allow Negotiating Bank to Negotiate the

Page 45 of 70

documents despite the discrepancies. L/C issuing Bank willinform the matter to buyer, if the buyer accepts thediscrepancies mentioned by Negotiating Bank, issuing bankwill authorize the Negotiating bank to negotiate thediscrepant documents.

3.4 Remittance

3.4.1 Definition Remittance represents transfer of fund from one place toanother through official channel.

3.4.2 Foreign RemittanceForeign remittance means remittance of foreign currenciesfrom one place/persons to another place/person. In broadsense, foreign remittance includes all sale and purchase offoreign currencies on account of Import, Export, Travel andother purposes. However, specifically foreign remittancemeans sale & purchase of foreign currencies for the purposesother than export and import. As such, All foreign remittance transactions are grouped into twobroad categories- Outward remittance & Inward remittance.

3.4.3 Outward RemittanceThe term “ Outward remittances” include not only remittancei.e. sale of foreign currency by TT. MT, Drafts, Traveler’scheques but also includes payment against imports into Bangladesh & Local currency credited to Non-resident Taka Accounts of Foreign Banks or Convertible TakaAccount. A. Private Remittance

1. Family remittance facilityForeign Nationals working in Bangladesh with approval of theGovernment may remit through an Authorized Dealer 50% of

Page 46 of 70

Salary and 100% of leave salary as also actual savings and admissible person benefits. No prior approval of Bank is necessary for such remittance.

2. Remittance of Membership fees/registration fees etc.Authorized Dealer may remit without prior approval ofBangladesh Bank, membership fees of Foreign professional andscientific institutions and fees for applicationregistration, admission, examination (TOEFL, SAT etc.) inconnection with admission into foreign educationalinstitutions on the basis of written application supportedby demand notice/letter of the concerned institution.

3. EducationPrior permission of Bangladesh Bank is not required forreleasing foreign exchange in favor/on behalf of Bangladeshstudents studying abroad or willing to proceeds abroad forstudies.

4. Remittance of Consular FeesConsular fees collected by foreign embassies in Bangladesh Taka and deposited in a Taka Account maintained with an AD solely for this purpose may be remitted abroad without priorapproval of Bangladesh Bank.

5. Remittance of evaluation feeAuthorized Dealers without prior approval of Bangladesh Bankmay remit evaluation fee on behalf of Bangladeshis desiringimmigration to foreign countries for getting educationalcertificates of the person concerned evaluated by a foreigninstitution. A demand note of the foreign immigrationauthority is required for this purpose.

6. TravelPrivate travel quota entitlement of Bangladesh Nationals isset at US$3000/- per year for visit to countries other thanSAARC member countries and Myanmar, Quota for SAARC membercountries and Myanmar is US$1000/- for travel by air andUS$500/-for travel by overland route. Fore minors (Below 12

Page 47 of 70

year in age) the applicable quota will be half the amountallowable to adults.

7. Health & MedicalAuthorized Dealers without prior approval of Bangladesh Bankmay release foreign exchange up to US$10,000/- for medicaltreatment abroad on the basis of the recommendation of themedical Board set up the Head Directorate and the costestimate of the foreign medical institution.

8. Seminars & workshops Without prior approval of Bangladesh Bank AD may releaseUS$200/- per diem and US$250/- per diem to the privatesector participants for attending seminars, conferences andworkshops organized by recognized International bodies inSAARC member countries or Myanmar and in other countriesrespectively for the actual period of theseminar/workshop/conference to be held on this basis ofinvitation letters received in the names of the applicationor their employer institutional.

9. Foreign Nationals

i) The Authorized Dealers may issue foreign currency TCs toforeign nationals without any limit and foreign currencynotes up to US$300/- or equivalent per person againstsurrender of equivalents amounts in foreign currencies. TheTCs

and foreign currency notes should however, be delivered onlyon production of ticket for a destination outside Bangladeshand the amount issued should be endorsed on the relativepassports.

ii) Authorized Dealers may allow recon version of unspentTaka funds of foreign tourists into foreign exchange onproduction of the encashment certificate of foreigncurrency. Recon version shall be allowed by the same AD withwhich the

Page 48 of 70

foreign currency was encased earlier. AD should retain theoriginal encashment certificate and relative FMJ forms whererecon version exceeds US$5000/-.

10. Remittance for HajjAuthorized Dealers may release foreign exchange to theintending pilgrims for performing Hajj as perinstructions/circulars to be issued by the Bangladesh Bankeach year.

11. Other Private remittanceApplications for remittances by private individuals forpurposes other than those mentioned above should beforwarded to Bangladesh Bank for consideration & approvalafter assessing the benefits of the purpose of remittance onthe basis of documentary evidence submitted by theapplicant.

B. Official & Business Travel

1. Official VisitFor official or semi officials visits abroad by theofficials of govt., Autonomous/Semi-autonomous institutionsetc., Authorized Dealers may release foreign exchange as perentitlements fixed by the Ministry of Finance from time to

time, In such cases, the applicant for foreign exchangeshall be required to submit the sanction letter and thecompetent authority’s Order/Notification/Circularauthorizing the travel.

2. Business Travel for New ExportersUp to US$6,000/- or equivalent may be issued by an ADwithout prior approval of Bangladesh Bank to a new exporterfor business travel abroad, against recommendation letterfrom Export Promotion requirement beyond US$6000/- is

Page 49 of 70

accommodated by Bangladesh Bank upon written request throughan AD with supporting documents.

3. Business Travel Quota for Importers and Non-exportingproducersI) Subject to annual upper limit of US$5000/- importers areentitled to a business travel quota @ 1% of their importssettled during the previous financial year.

ii) Subject to annual upper limit of US$5000/- non exportingproducers for the local markets are entitled to a businesstravel quota @1% of their turnover of the proceedingfinancial year as declared in their tax returns.

4. Exporters’ Retention QuotaMerchandise exporters may retain up to 50% of realized FOBvalue of their exports in foreign currency accounts.However, for exports of goods having accounts. However, forexports of goods having high import content (such asreadymade garments, products including naphtha, furnace oilbitumen, electronic goods etc.,) the retention quota is 7.5%of the repatriated FOB value.

C. Commercial Remittances

1.Opening of branches or subsidiary companies abroadRemittance of up to US$30,000/- or equivalent per annum maybe released by the Authorized Dealers without prior approvalof Bangladesh Bank to meet current

expenses of offices/branches opened abroad by resident inBangladesh or Commercial/Industrial concern incorporated inBangladesh.Such remittance may only be made in the names of concernedoffices/subsidiary companies abroad subject top examinationof following papers:-

Page 50 of 70

I) Approval letter of the competent authority of the countryconcerned for opening the office in that country copy ofreport submitted to Bangladesh banks, as per prescribedformat, within one month of opening of foreignbranches/subsidiaries.

Before effecting remittances for subsequent years theAuthorized Dealers shall verify the renewed lease agreement(if applicable and shall satisfy itself about the actualnecessity of remitting funds by examining the actual and/orestimated incomes and expenses of the offices/subsidiariesabroad as revealed from the its audited accounts and theother papers/vouchers.

2. Remittance by shipping companies airlines & courierserviceForeign Shipping Companies, airlines and courier servicecompanies may send, through an AD, funds collected inBangladesh towards freight and passage after adjustment oflocal cost & Taxes, if any without prior approval ofBangladesh Bank.

3. Remittance of Royalty and technical feesNo prior permission is required for remitting royalty,technical know-how or technical assistance fees, operationalservices fees, marketing commission etc., if the total feesand other expenses connected with technology transfer do notexceed. a) 6% of the cost of imported machinery in case ofnew projects. b) 6% of the previous year’s sales as declared in theincome tax returns of the ongoing concerns.

4. Remittance on account of training & consultancyIndustrial enterprises producing for local market may remitthrough Authorized Dealers up to 1% of their annual sales asdeclared in their previous years’ tax return for the purposeof training and consultancy services as per relevant

Page 51 of 70

contract with the foreign trainer/consultant, without priorapproval of Bangladesh Bank.

5. Remittance of profits of foreign firms/branchesAuthorized Dealers may without prior Bangladesh Bankapproval remit abroad the post tax profits of branches offoreign firms and companies including foreign banks & otherfinancial institutions subject to submission of relevantdocuments/information along with the application.

6. Remittance of Dividend Prior permission of Bangladesh Bank is not required for- i) Remittance of dividend income to non-residentshareholders on receipt of application in the prescribeform the companies concerned.ii) Remittance of dividend declared out of previous years’accumulated reserves.

7. Subscriptions to foreign media servicesOn application from the local newspapers, Authorized Dealersmay remit foreign exchange towards cost of subscription ofnews items, features, articles of foreign news agenciessubject to submission of (I) contracts entered into between the applicant and theforeign news agency and (ii) NOC of the Ministry ofInformation.

8. Costs/ for Reuter monitorsAuthorized Dealers may remit abroad costs/fees on account oftheir own subscription to foreign media services such asReuter monitor service, without prior approval of BangladeshBank.

9.Advertisement of Bangladeshi Products in mass media abroadPrior permission of Bangladesh is not required by theAuthorized Dealers for remittance of charges foradvertisement of Bangladeshi commodities in mass mediaabroad subject to submission of Invoice from the concernedforeign mass media along with the applications of the

Page 52 of 70

remitter. The applicant will have to submit copy of theadvertisement to the Ad within one month of this issuance.

10. Bank ChargesThe Authorized Dealers may affect remittances towardssettlement of dues to foreign banks of bank charges, cost ofcables and other incidental charges arising in their normalcourse of the business without prior approval of BangladeshBank.

3.4.4 Travelers ChequesTravelers Cheque (TC) is an instrument for a specific amountof widely accepted foreign currencies, issued in favor ofTravelers/Visitors to carry foreign exchange for meetingtheir expenses in abroad. Travelers cheque may be indifferent currencies, such as US$, Pound Starling, JapaneseYen, Saudi Real, Canadian Dollar, French Frances, GermanMarks, Swiss Frances, etc.

3.4.5 Procedure of Travelers Cheques

a) Insure that the intending traveler is a client of theAuthorized Dealer (AD) Bank or is sufficiently well knownto the AD Bank.

b) The intending travelers must come to the Bank with thefollowing documents to have the T.C. Valid Passport. Confirmed Valid Air Ticket.

c) Verification of the Passport & Air Ticket regardingvalidity, Illegibility, status etc. of the same.

d) Filling up the T/M form by the purchaser and signing onthat T/M.

e) Realization of required fund.f) Fill up the purchase Agreement Form (PAF) regarding the

name, address etc.of the purchaser, T.C series no. Date ofissue, amount etc, and give endorsement on the passport.

g) Be sure that purchaser signed all cheques in the upperleft side of the cheque, only one person may sign anycheque.

Page 53 of 70

h) Use original P.A.F. for settlement and retain duplicatefor records.

i) Two sets of Photographs of Passport and Air Ticket to beobtained.

3.4.6 Inward remittanceThe term” Inward Remittance” includes not only purchase ofForeign Currency by TT, MT, Drafts etc. but also purchasesof bills, purchases of Traveller’s cheques.

Purposes of Inward Remittances Family Maintenance Indenting Commission Recruiting Agents Commission Realization of Export Proceeds Donation

3.4.7 Purchase of Currency Notes, Travelers cheques, Draftsetc.

Following General observations are required in addition tocommon judgment/intelligent /vigilance of the dealingofficers: -

i) Currency notes to be checked very carefully so as toavoid risk of purchasing counter Notes.ii) While purchasing Travelers cheque signature of theholder to be obtained on the TC/s in front of the Bankofficials and should be verified with the signature of theholder already given at the time of issuance of T.Cs, iii) Drafts should not be purchased under any circumstancesunless the holder is a regular/valued customer of the bank.Indemnity Bond to be obtained for revering the amount paidin advance to the holder in case of dishonor of theinstrument.iv) Private cheque should not be purchased under anycircumstance without prior approval of Head Office.

3.4.8 Dealing In Foreign Currency Notes & Coins

Page 54 of 70

Only Authorized Dealers and Authorized Money Changer arepermitted to deal in foreign currency notes & coinsAuthorized Dealers and Money Changers may freely buy foreigncurrency from incoming passengers regardless of nationalityand regardless of whether or not a declaration on form FMJis produced at the time of encashment. If this form isproduced, the amount encased should be endorsed on it.

The Authorized Dealers may also purchase foreign currencynotes, coins and other travel instruments freely fromAuthorized Money changers without production of Form FMJ.

3.4.9 Disposal of Foreign Currency notes./Coins & others byIncoming passengers

Incoming passengers may bring in any amount of foreignexchange with declaration FMC at the time of arrival. Nodeclaration is necessary for amounts up to US$5000/- for non residents, the entire amount brought inwith declaration or up to US$5000/- brought in withoutdeclaration may be freely taken out at the time of departureor may deposit the amount in F.C Account subject tosubmission of form FMJ for excess of US$5000.- orequivalent. An incoming person, who is ordinarily residentin Bangladesh i. May retain foreign exchange up to US$5000/- or

equivalent brought in without declaration or ii. Take-out the same freely at the time of departure form

Bangladesh without endorsement in passport and air ticket

iii. Deposit the amount in RFCD account of the person concerned.

3.4.10 Mode Of Inward Remittances

A) Telegraphic Transfer (TT)This is an instruction for transfer of money by Telegram,Cable or telex from a bank in one country to another Bank indifferent center. This is an instruction form the Importers

Page 55 of 70

Bank to the exporters Bank. The TT charge is realized by usfrom the partly as per Bank circular

B) Mail Transfer (M.T)This transfer is the order to pay cash to a 3rd party. ThisTransfer is sent by mail & the charge must be realized as perBank circular.

C) Drafts & ChequeA draft is pay order issued by one Bank to another Bank orits branch.

3.5 Statement Return on Foreign Exchange Department

The statement and return of foreign exchange department aregiven below:

* Daily Statement of L/C opening position and foreigncurrency position.

* Weekly statement of onion, garlic spices etc.

* Fortnightly statement of IRC renewal to CCI&E.

* Fortnightly statement of LCAF copy to CCI&E.

* Performance report of foreign Exchange Business.

* Statement of FBN (Regular).

* Statement of foreign Exchange Income Analysis.

* Statement of Outstanding Export Bills.

* Statement of Commodity wise.

* Statement of outstanding commitment.

Page 56 of 70

* Statement of Inward Remittance.

* Statement of Bangladesh bank return.

* Statement of Customer liability.

* Statement of AID, Loan, Grant for L/C..

Page 57 of 70

Findings & Recommendation

4.1 FINDINGS

Page 58 of 70

Mutual Trust Bank is one of the most potential Banks in thebanking sector. It has a large portfolio with huge assets tomeet up its liabilities and the management of this bank isequipped with the expert bankers and managers in all level ofmanagement. So it is not an easy job to find out thedrawbacks of this branch. I would rather feel like producingmy personal opinion about the ongoing practices in PrincipalBranch.

4.1.1 Problems that I foundThough Mutual Trust Bank is a leading bank in our country .Even there are some problems in banking system these are asfollows: Delivery of LCAF form IRC register does not maintain Lack of modern software Lack of credit Bill of entry does not match in time Letter of credit does not maintained properly More time for making PAD register.

4.2 RecommendationsFor the improvement of the service the following measuresshould be taken:

Delivery of LCAF formDelivery of LCAF form for the party does not maintain inthe import department which is maintained by the exportdepartment. But all of the bank maintain this form inImport Department. In that case, sometimes customer facesvarious problems.

IRC Register Does Not Maintain IRC (Import Register Certificate) does not maintainproperly Sometimes officers are busy and they does notmaintain their register.

Lack Of Modern SoftwareLack of modern software in payment against document. Toprepare PAD register.

Page 59 of 70

Lack Of CreditLack of Credit is issued by doc print .where as anotherbank use SAM(SWIFT ALIENCE MASSENGER)

Bill Of Entry Does not Match in Time

Bill of Entry does not match in time for that reason auditorscompliance for the importer. For Checking importdocument does not maintain any software do it manually.

Letter of Credit Does not Maintained ProperlyProposal of the LC does not check all the time properly .Where sometimes import form and proforma invoice are notavailable. Which makes problem for issuing IMP to theBangladesh Bank.

More Time For Making Pad RegisteredThere are always shortages of application forms, brochures, etc. in the branch The Boucher of the payment against document maintain manually which consume more timefor making PAD.

Page 60 of 70

Page 61 of 70

CONCLUSION

5.1 Conclusion

Since the banking service especially the private Banks aredoing an outstanding business, so it is clear that the modernpeople are more concerned about securing their valuableassets and get high-quality and timely services. For thisreason lot of new commercial bank has been established inlast few years and these banks have made this banking sectorvery competitive .Now banks have to organize their operationand do their operations according to the need of the market.

Page 62 of 70

Banking sectors no more depends on a traditional method ofbanking. In this competitive world this sector has trenchedits wings wide enough to cover any kind of financial servicesanywhere in this world. The major task for banks, to survivein this competitive environment is by managing its assets andliabilities in an efficient way.

The employees of Mutual Trust Bank are very efficient;everyone knows their work very well and can performefficiently to produce the best output. The bank has plans toopen more branches to expand their network.

They are also playing a significant role in the import andexport of Bangladesh. Especially Mutual Trust Bank has moreimport business than its rivals. If this bank can concentrateon import business, it will give the opportunity to circulatethe profit more rapidly than other sources. If the Bank canreduce the difference between imports financing to exportfinancing, bank can make more profit and gain achievement.

With the current performance of the Bank and with littleimprovement here and there will certainly make Mutual TrustBank one of the best Private Bank in Bangladesh in the nearfuture.

Page 63 of 70

Bibliography

Article

Annual report 2010 of Mutual Trust Bank Ltd. Training Materials

Interneto www.bangladeshbank.org o www.google.corn o www.mutualtrustbank.com.

Page 64 of 70

Appendix-1

Page 65 of 70

Page 66 of 70

Page 67 of 70

Appendix-2

Page 68 of 70

Page 69 of 70

Page 70 of 70

Related Documents