DECLARATION DECLARATION This is to declare that I have carried out this project work myself in part fulfillment of the …………………………..Program of SCDL. The work is original, has not been copied from anywhere else and has not been submitted to any other University/Institute for an award of any degree / diploma. Date: Signature: Place: Name:

Mutual Fund

Dec 21, 2015

mba project on mutual fund- 50 pages

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

DECLARATIONDECLARATION

This is to declare that I have carried out this project work myself in part fulfillment of the

…………………………..Program of SCDL. The work is original, has not been copied from

anywhere else and has not been submitted to any other University/Institute for an award of any

degree / diploma.

Date:

Signature:

Place:

Name:

CONTENTS SR NO.

Declaration 1

Executive Summary 2Chapter-1 Introduction 4

1.What is mutual fund

2.Concept of mutual fund

3.Advantages and disadvantage of mutual fund

4.Histroy of indian mutual fund

5.Categories of mutual fund

a.based on their structure

b.based on investment objective

6.Pros and cons of investing in mutual funds

7.Mutual funds in india

8.Major players of mutual fund in india

9.Guidelines of sebi for mutual funds

5-28

Chapter-2 Data analysis & interpretation 29-33Chapter-3 Fund Expense 34-37Chapter-4 Objective and Scope 38-40Chapter-5 Research Methodology 41-42Chapter-6 Conclusion and Rational 43-45 Chapter-7 Suggestions & Recommendations & Bibliography 46-50

EXECUTIVE SUMMARY

In few years Mutual Fund has emerged as a tool for ensuring one’s financial wellbeing. Mutual Funds have not only contributed to the India growth story but have also helped families tap into the success of Indian Industry. As information and awareness is rising more and more people are enjoying the benefits of investing in mutual funds.

The main reason the number of retail mutual fund investors remains small is that nine in ten people with incomes in India do not know that mutual funds exist. But once people are aware of mutual fund investment opportunities, the number who decide to invest in mutual funds increases to as many as one in five people.

This Project gave me a great learning experience and will help to know about the investors’ Preferences in Mutual Fund means Are they prefer any particular Asset Management Company (AMC), Which type of Product they prefer, Which Option (Growth or Dividend) they prefer.

Mutual fund and its various aspects, the company profile, objectives of the study, Research Methodology. one can have a brief knowledge about mutual fund and its basis through the project.

Chapter-1

Introduction

INTRODUCTION TO MUTUAL FUND AND ITS VARIOUS ASPECTS.

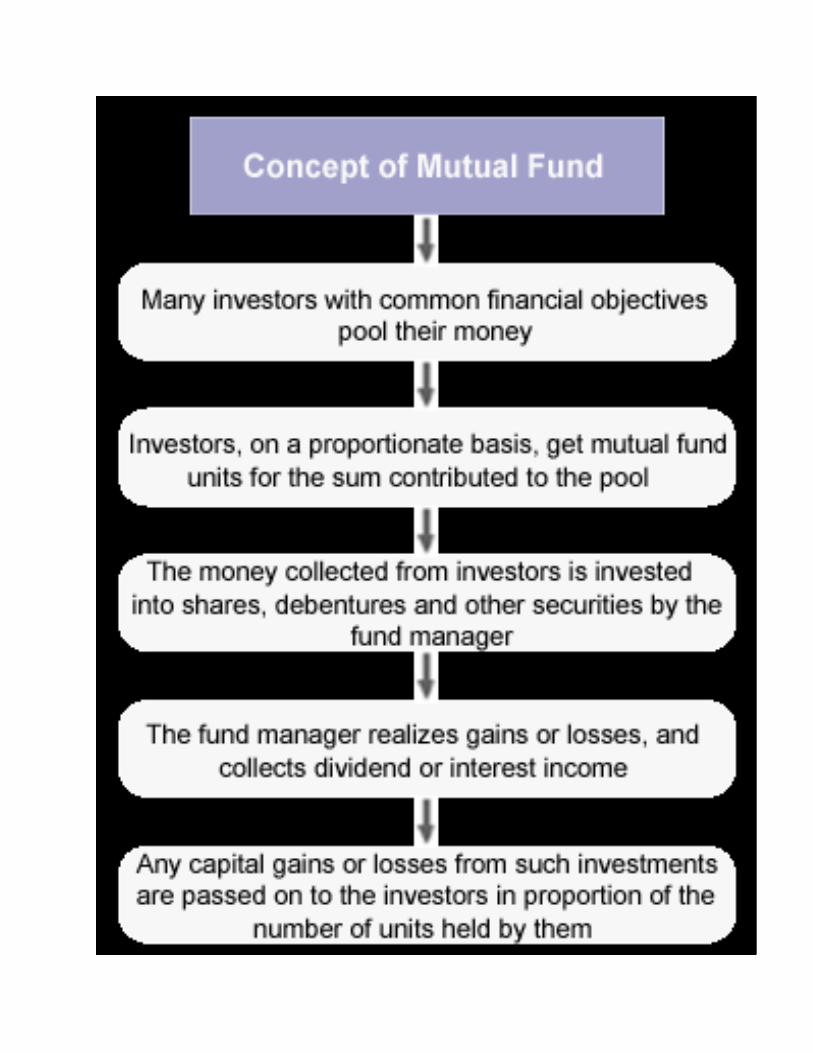

Mutual fund is a trust that pools the savings of a number of investors who share acommon financial goal. This pool of money is invested in accordance with a statedobjective. The joint ownership of the fund is thus “Mutual”, i.e. the fund belongs to all investors. The money thus collected is then invested in capital market instruments such as shares, debentures and other securities. The income earned through these investments and the capital appreciations realized are shared by its unit holders in proportion the number of units owned by them. Thus a Mutual Fund is the most suitable investment for the common man as it offers an opportunity to invest in a diversified, professionally managed basket of securities at a relatively low cost. A Mutual Fund is an investment tool that allows small investors access to a well diversified portfolio of equities, bonds and other securities. Each shareholder participates in the gain or loss of the fund. Units are issued and can be redeemed as needed. The fund’s Net Asset value (NAV) is determined each day.

Investments in securities are spread across a wide cross-section of industries andsectors and thus the risk is reduced. Diversification reduces the risk because all stocks may not move in the same direction in the same proportion at the same time. Mutual fund issues units to the investors in accordance with quantum of money invested by them. Investors of mutual funds are known as unit holders.

When an investor subscribes for the units of a mutual fund, he becomes part owner of the assets of the fund in the same proportion as his contribution amount put up with the corpus (the total amount of the fund). Mutual Fund investor is also known as a mutual fund shareholder or a unit holder.Any change in the value of the investments made into capital market instruments (such as shares, debentures etc) is reflected in the Net Asset Value (NAV) of the scheme. NAV is defined as the market value of the Mutual Fund scheme's assets net of its liabilities. NAV of a scheme is calculated by dividing the market value of scheme's assets by the total number of units issued to the investors

The Duties & Functions of Fund Managers

When individuals and institutions invest in a fund, they actually invest in the fund's manager. He is responsible for managing the fund's investments and ensuring that the fund's strategy is aligned with its goals. He is also responsible for the overall operation of the fund, from customer service to risk management. Therefore, investors should consider fund managers a key factor in their selection of a fund.

Reporting-

Fund managers must ensure their funds' reporting requirements are met. Funds are designed with different strategies and objectives and have different risks, policies and expenses. These details are important to clients and regulators and should be clearly outlined in a prospectus. Fund managers are responsible for ensuring that prospectuses and other documents are completed, filed and distributed as regulations require

.

Compliance-

Fund managers must also ensure their funds operate in accordance with regulations outlined by authorities, such as the Securities and Exchange Commission. Regulations can cover aspects of the fund's business from getting clients to handling redemptions. For example, HedgeCo explains that hedge funds are not allowed to use general solicitation or general advertisement to attract new clients. If questions, concerns or problems arise, a fund manager may have to answer to the fund's directors, investors or even regulators and legislators.

Growth and Performance-

People turn to funds because they want growth. Fund managers can only deliver it by putting clients' money to work, so they have to decide where to invest. Their choices are shaped not only by the rules and regulations applicable to the fund, but also by clients' expectations. Fund managers are judged by how well their fund performs. At a minimum, they need to deliver growth that exceeds interest rates and the rate of inflation to justify the risks of investing.

Wealth Protection-

Fund managers have a responsibility to protect investors' money. Prudent investors are aware that funds must take some risks to deliver growth but they do not expect reckless behavior. Therefore, fund managers' choices to buy or sell assets are preceded by a lot of research and due diligence, which can involve investigating companies or assets, attending industry events and employing risk management techniques to assess investments. Fund managers also address risk by ensuring asset portfolios are sufficiently diversified.

The Ways You Actually Make Money from Owning Mutual Funds

How you start making money when you invest in a mutual fund depends upon the type of fund

you own. If you own a stock fund, you already learned in Making Money from Investing in

Stocks that the biggest sources of potential profit are an increase in the stock price (capital gains)

or cash dividends paid to you for your pro-rata share of the company's distributed profits. If the

fund instead focused on investing in bonds, you are making money through interest income. If

the fund specializes in investing in real estate, you might be making money from rents, property

appreciation and profits from business operations, such as vending machines in an office

building.

The Three Keys to Making Money Through Mutual Fund Investing

There are three major keys to making money through mutual fund investing. These are:

1. Keep expenses low. The number one consideration when it comes to making money from

mutual funds is keeping your costs low. This is the reason so many financial advisers tell their

clients to invest in low cost index funds. These are often referred to as "dumb money"

because they have no portfolio manager. Instead, they hold a basket of stocks with similar

characteristics, such as those belong to an index like the Dow Jones Industrial Average. Why

is that important? Because saving even 1% over an investing lifetime can lead to enormous

wealth. If an 18 year old saved $5,000 per year, the difference between a 7% return and an 8%

return over 50 years is $836,206. That is real money by anyone's standards!

2. Give yourself plenty of time to compound your wealth. The longer you money stays invested,

the more time you have to capture the power of compound interest.

3. Don't invest in anything you don't understand. The first rule of making money, as Warren

Buffett has often quipped, is to never lose money. The second rule is to see rule #1. You

should know exactly what each of your mutual funds owns and why you are invested in it.

How A Mutual Fund Works?

A fund sponsor - generally a financial intermediary like sbi, icici organizes a mutual fund as a corporation; however, it is not an operating company with employees and a physical place of business in the traditional sense. A fund is a "virtual" company, which is typically externally managed. It relies on third parties or service providers, either fund sponsor affiliates or independent contractors, to manage the fund's portfolio and carry out other operational and administrative activities.

The fund sponsor raises money from the investing public, who become fund shareholders. It then invests the proceeds in securities (stocks, bonds and money market instruments) related to the fund's investment objective. The fund provides shareholders with professional investment management, diversification, liquidity and investing convenience. For these services, the fund sponsor charges fees and incurs expenses for operating the fund, all of which are charged proportionately against a shareholder's assets in the fund.

The most prevalent and well-known type of mutual fund operates on an open-ended basis. This means that it continually issues (sells) shares on demand to new investors and existing shareholders who are buying. It redeems (buys back) shares from shareholders who are selling.

Mutual fund shares are bought and sold on the basis of a fund's net asset value (NAV). Unlike a stock price, which changes constantly according to the forces of supply and demand, NAV is determined by the daily closing value of the underlying securities in a fund's portfolio (total net assets) on a per share basis.

Definitions of key terms.

Net asset value

A fund's net asset value (NAV) equals the current market value of a fund's holdings minus the fund's

liabilities (sometimes referred to as "net assets"). It is usually expressed as a per-share amount,

computed by dividing net assets by the number of fund shares outstanding. Funds must compute

their net asset value according to the rules set forth in their prospectuses. Funds compute their NAV

at the end of each day that the New York Stock Exchange is open, though some funds compute

NAVs more than once daily.

Valuing the securities held in a fund's portfolio is often the most difficult part of calculating net asset

value. The fund's board typically oversees security valuation.

Expense ratio

The expense ratio allows investors to compare expenses across funds. The expense ratio equals

the 12b-1 fee plus the management fee plus the other fund expenses divided by average daily net

assets. The expense ratio is sometimes referred to as the total expense ratio (TER).

Average annual total return

The SEC requires that mutual funds report the average annual compounded rates of return for one-,

five-and ten-periods using the following formula:[14]

P(1+T)n = ERV

Where:

P = a hypothetical initial payment of $1,000

T = average annual total return

n = number of years

ERV = ending redeemable value of a hypothetical $1,000 payment made at the beginning of the one-, five-, or ten-year periods at the end of the one-, five-, or ten-year periods (or fractional portion)

Turnover

Turnover is a measure of the volume of a fund's securities trading. It is expressed as a percentage of

average market value of the portfolio's long-term securities. Turnover is the lesser of a fund's

purchases or sales during a given year divided by average long-term securities market value for the

same period. If the period is less than a year, turnover is generally annualized.

The Advantages:

Diversification: A single mutual fund can hold securities from hundreds or

even thousands of issuers. This diversification considerably reduces the risk

of a serious monetary loss due to problems in a particular company or

industry.

Affordability: You can begin buying units or shares with a relatively small

amount of money (e.g., 500 for the initial purchase). Some mutual funds also

permits you to buy more units on a regular basis with even smaller

installments (e.g., 50 per month).

Professional Management: Many investors do not have the time or

expertise to manage their personal investments every day, to efficiently

reinvest interest or dividend income, or to investigate the thousands of

securities available in the financial markets. Mutual funds are managed by

professionals who are experienced in investing money and who have the

education, skills and resources to research diverse investment opportunities.

Liquidity: Units or shares in a mutual fund can be bought and sold any

business day (that the market is open), thus, providing investors with easy

access to their money.

Flexibility: Many mutual fund companies manage several different funds

(e.g., money market, fixed-income, growth, balanced, sector, index and

global funds) and allow you to switch between these funds at little or no

charge. This enables you to change your portfolio balance as and when your

personal needs, financial goals or market conditions change.

The Disadvantages:

When you invest in a mutual fund you place your money in the hands of a

professional manager. The return on your investment depends heavily on

that manager’s skill and judgment.

Research has shown that few portfolio managers are able to out-perform the

market. Check the fund manager’s track record over a period of time when

selecting a fund.

Fees for fund management services and various administrative and sales

costs can reduce the return on your investment. These are charged, in almost

all cases, whether the fund performs well or not.

Redeeming your mutual fund investment in the short-term could

significantly impact your return due to sales commissions and redemption

fees.

HISTORY OF THE INDIAN MUTUAL FUND INDUSTRY

The mutual fund industry in India started in 1963 with the formation of Unit Trust of India, at the initiative of the Government of India and Reserve Bank. Though the growth was slow, but it accelerated from the year 1987 when non-UTI players entered the Industry. In the past decade, Indian mutual fund industry had seen a dramatic improvement, both qualities wise as well as quantity wise. Before, the monopoly of the market had seen an ending phase; the Assets Under Management (AUM) was Rs67 billion. The private sector entry to the fund family raised the Aum to Rs. 470 billion in March 1993 and till April 2004; it reached the height if Rs. 1540 billion.The Mutual Fund Industry is obviously growing at a tremendous space with the mutual fund industry can be broadly put into four phases according to the development ofthesector. Each phase is briefly described as under.

First Phase – 1964-87

Unit Trust of India (UTI) was established on 1963 by an Act of Parliament by theReserve Bank of India and functioned under the Regulatory and administrative control of the Reserve Bank of India. In 1978 UTI was de-linked from the RBI and the Industrial Development Bank of India (IDBI) took over the regulatory andadministrative control in place of RBI. The first scheme launched by UTI was UnitScheme 1964. At the end of 1988 UTI had Rs.6,700crores of assets undermanagement.

Second Phase – 1987-1993 (Entry of Public Sector Funds)

1987 marked the entry of non- UTI, public sector mutual funds set up by public sector banks and Life Insurance Corporation of India (LIC) and General InsuranceCorporation of India (GIC). SBI Mutual Fund was the first non- UTI Mutual Fundestablished in June 1987 followed by Can bank Mutual Fund (Dec 87), Punjab National Bank Mutual Fund (Aug 89), Indian Bank Mutual Fund (Nov 89), Bank of India (Jun90), Bank of Baroda Mutual Fund (Oct 92). LIC established its mutual fund in June1989 while GIC had set up its mutual fund in December 1990.At the end of 1993, the mutual fund industry had assets under management of Rs.47,004crores.

Third Phase – 1993-2003 (Entry of Private Sector Funds)

1993 was the year in which the first Mutual Fund Regulations came into being, under which all mutual funds, except UTI were to be registered and governed. The erstwhile Kothari Pioneer (now merged with Franklin Templeton) was the first private sector mutual fund registered in July 1993.

The 1993 SEBI (Mutual Fund) Regulations were substituted by a more comprehensive and revised Mutual Fund Regulations in 1996. The industry now functions under the SEBI (Mutual Fund) Regulations 1996. As at the end of January 2003, there were 33 mutual funds with total assets of Rs. 1,21,805crores.

Fourth Phase – since February 2003

In February 2003, following the repeal of the Unit Trust of India Act 1963 UTI wasbifurcated into two separate entities. One is the Specified Undertaking of the Unit Trust of India with assets under management of Rs.29,835crores as at the end of January 2003, representing broadly, the assets of US 64 scheme, assured return and certain other schemes.

The second is the UTI Mutual Fund Ltd, sponsored by SBI, PNB, BOB and LIC. It is registered with SEBI and functions under the Mutual Fund Regulations. Consolidation and growth. As at the end of September, 2004, there were 29 funds, which manage assets of Rs.153108 crores under 421 schemes.

CATEGORIES OF MUTUAL FUND

Mutual funds can be classified as follow :

Based on their structure

· Open-ended funds : Investors can buy and sell the units from the fund, at any point of time.

· Close-ended funds : These funds raise money from investors only once. Therefore,after the offer period, fresh investments can not be made into the fund. If the fund is listed on a stocks exchange the units can be traded like stocks (E.g., Morgan Stanley Growth Fund). Recently, most of the New Fund Offers of close-ended funds provided liquidity window on a periodic basis such as monthly or weekly. Redemption of units can be made during specified intervals. Therefore, such funds have relatively low liquidity.

Based on their investment objective:

Equity funds: These funds invest in equities and equity related instruments. Withfluctuating share prices, such funds show volatile performance, even losses. However, short term fluctuations in the market, generally smoothens out in the long term, thereby offering higher returns at relatively lower volatility. At the same time, such funds can yield great capital appreciation as, historically, equities have outperformed all asset classes in the long term. Hence, investment in equity funds should be considered for a period of at least 3-5 years. It can be further classified as:

i) Index funds- In this case a key stock market index, like BSE Sensex or Nifty istracked. Their portfolio mirrors the benchmark index both in terms of composition and individual stock weightages.

ii) Equity diversified funds- 100% of the capital is invested in equities spreadingacross different sectors and stocks.

iii|) Dividend yield funds- it is similar to the equity diversified funds except that theyinvest in companies offering high dividend yields.

iv) Thematic funds- Invest 100% of the assets in sectors which are related throughsome theme.e.g. -An infrastructure fund invests in power, construction, cements sectors etc.

v) Sector funds- Invest 100% of the capital in a specific sector. e.g. - A banking sector fund will invest in banking stocks.

vi) ELSS- Equity Linked Saving Scheme provides tax benefit to the investors.

Balanced fund: Their investment portfolio includes both debt and equity. As a result, on the risk-return ladder, they fall between equity and debt funds. Balanced funds are the ideal mutual funds vehicle for investors who prefer spreading their risk across various instruments.Following are balanced funds classes:

i) Debt-oriented funds -Investment below 65% in equities.

ii) Equity-oriented funds -Invest at least 65% in equities, remaining in debt.

Debt fund:They invest only in debt instruments, and are a good option for investor savers to idea of taking risk associated with equities. Therefore, they invest exclusively in fixed-income instruments like bonds, debentures,

Government of India securities;and money market instruments such as certificates of deposit (CD), commercial paper(CP) and call money. Put your money into any of these debt funds depending on your investment horizon and needs.

i) Liquid funds- These funds invest 100% in money market instruments, a largeportion being invested in call money market.

ii) Gilt funds ST- They invest 100% of their portfolio in government securities of andT-bills.

iii) Floating rate funds - Invest in short-term debt papers. Floaters invest in debtinstruments which have variable coupon rate.

iv) Arbitrage fund- They generate income through arbitrage opportunities due to mispricing between cash market and derivatives market. Funds are allocated to equities,derivatives and money markets. Higher proportion (around 75%) is put in moneymarkets, in the absence of arbitrage opportunities.

v) Gilt funds LT- They invest 100% of their portfolio in long-term governmentsecurities.

vi) Income funds LT- Typically, such funds invest a major portion of the portfolio in long-term debt papers.

vii) MIPs- Monthly Income Plans have an exposure of 70%-90% to debt and anexposure of 10%-30% to equities.

viii) FMPs- fixed monthly plans invest in debt papers whose maturity is in line withthat of the fund.

Pros & cons of investing in mutual funds:

For investments in mutual fund, one must keep in mind about the Pros and cons of investments in mutual fund.

Advantages of Investing Mutual Funds:

1. Professional Management - The basic advantage of funds is that, they are professional managed,by well qualified professional. Investors purchase funds because they do not have the time or the expertise to manage their own portfolio. A mutual fund is considered to be relatively less expensiveway to make and monitor their investments.

2. Diversification - Purchasing units in a mutual fund instead of buying individual stocks or bonds,the investors risk is spread out and minimized up to certain extent. The idea behind diversification is to invest in a large number of assets so that a loss in any particular investment is minimized by gainsin others.

3. Economies of Scale - Mutual fund buy and sell large amounts of securities at a time, thus help to reducing transaction costs, and help to bring down the average cost of the unit for their investors.

4. Liquidity - Just like an individual stock, mutual fund also allows investors to liquidate their holdings as and when they want.

5. Simplicity - Investments in mutual fund is considered to be easy, compare to other available in the market, and the minimum investment is small. Most AMC also have automatic purchase plans whereby as little as Rs. 2000, where SIP start with just Rs.50 per month basis.

Disadvantages of Investing Mutual Funds:

1. Professional Management- Some funds doesn’t perform in neither the market, as their management is not dynamic enough to explore the available opportunity in the market, thus many investors debate over whether or not the so-called professionals are any better than mutual fund or investor himself, for picking up stocks.

2. Costs – The biggest source of AMC income, is generally from the entry & exit load which they charge from an investors, at the time of purchase. The mutual fund industries are thus charging extra cost under layers of jargon.

3. Dilution - Because funds have small holdings across different companies, high returns from a few investments often don't make much difference on the overall return. Dilution is also the result of afund getting too big. When money pours into funds that have had strong success, the manager often has trouble finding a good investment for all the new money.

4. Taxes - when making decisions about your money, fund managers don't consider your personal tax situation. For example, when a fund manager sells a security, a capital-gain tax is triggered, which how profitable the individual is from the sale. It might have been more advantageous for the individual to defer the capital gains liability.

Mutual Funds Industry in India

The origin of mutual fund industry in India is with the introduction of the concept of mutual fund by UTI in the year 1963. Though the growth was slow, but it accelerated from the year 1987 when non-UTI players entered the industry.

In the past decade, Indian mutual fund industry had seen a dramatic improvements, both quality wise as well as quantity wise. Before, the monopoly of the market had seen an ending phase, the Assets Under Management (AUM) was Rs. 67bn. The private sector entry to the fund family rose the AUMRs. 470 in in March 1993 and till April 2004, it reached the height of 1,540 bn.

Putting the AUM of the Indian Mutual Funds Industry into comparison, the total of it is less than the deposits of SBI alone, constitute less than 11% of the total deposits held by the Indian banking industry.

The main reason of its poor growth is that the mutual fund industry in India is new in the country.Large sections of Indian investors are yet to be intellectuated with the concept. Hence, it is the primeresponsibility of all mutual fund companies, to market the product correctly abreast of selling.

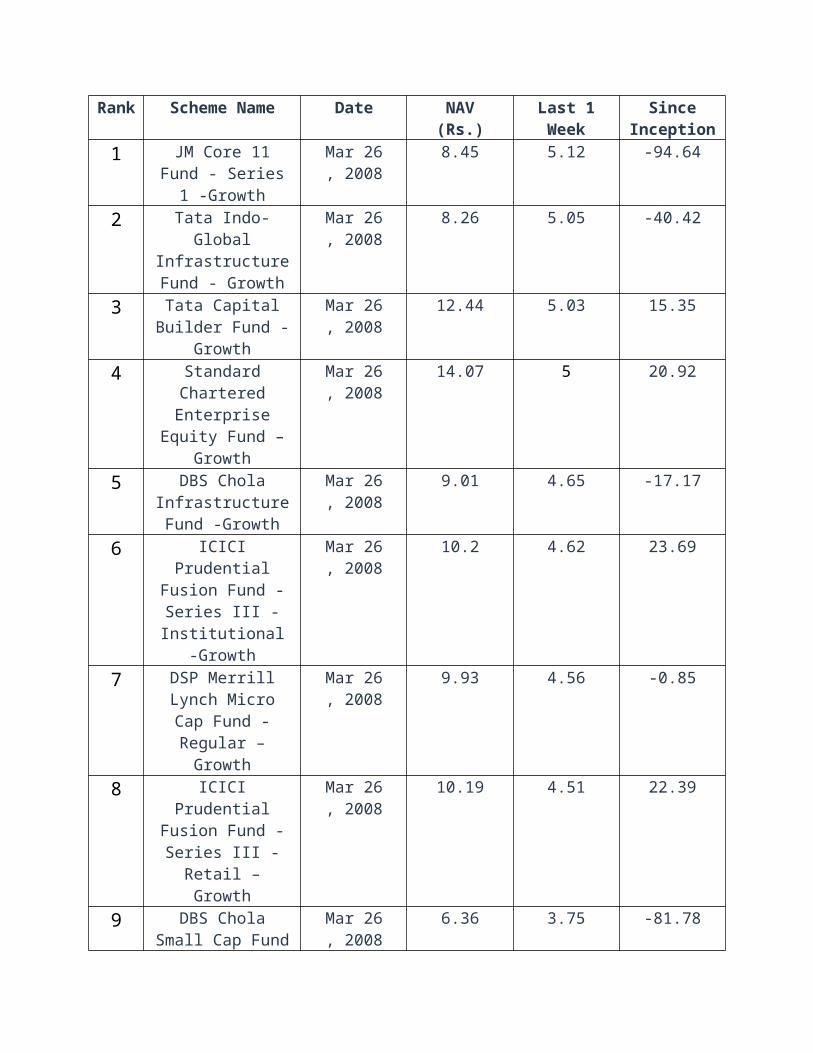

The major players in the Indian Mutual Fund Industry are:

Ran Scheme Name Date NAV Last 1 Since

k (Rs.) Week Inception1 JM Core 11 Fund -

Series 1 -GrowthMar 26, 2008

8.45 5.12 -94.64

2 Tata Indo-Global InfrastructureFund - Growth

Mar 26, 2008

8.26 5.05 -40.42

3 Tata Capital Builder Fund -Growth

Mar 26, 2008

12.44 5.03 15.35

4 Standard Chartered Enterprise Equity Fund – Growth

Mar 26, 2008

14.07 5 20.92

5 DBS Chola Infrastructure Fund

-Growth

Mar 26, 2008

9.01 4.65 -17.17

6 ICICI Prudential Fusion Fund -

Series III - Institutional -Growth

Mar 26, 2008

10.2 4.62 23.69

7 DSP Merrill Lynch Micro Cap Fund - Regular – Growth

Mar 26, 2008

9.93 4.56 -0.85

8 ICICI Prudential Fusion Fund -

Series III - Retail – Growth

Mar 26, 2008

10.19 4.51 22.39

9 DBS Chola Small Cap Fund -Growth

Mar 26, 2008

6.36 3.75 -81.78

10 Principal Personal Taxsaver

Mar 26, 2008

124.66 3.44 29.97

11 Benchmark Split Capital Fund -

Plan A - Preferred Units

Mar 26, 2008

141.51 3.14 13.71

12 ICICI Prudential FMP – Series 33 - Plan A – Growth

Mar 26, 2008

9.89 2.91 -7.88

13 Tata SIP Fund - Series I -Growth

Mar 26, 2008

10.25 2.38 2.39

14 Sahara R.E.A.L Fund – Growth

Mar 25, 2008

7.64 1.86 -49.52

15 Tata SIP Fund - Series II - Growth

Mar 26, 2008

9.93 1.58 -0.94

Guidelines of the SEBI for Mutual Fund Companies :

To protect the interest of the investors, SEBI formulates policies and regulates the mutual funds. It notified regulations in 1993 (fully revised in 1996) and issues guidelines from time to time.SEBI approved Asset Management Company (AMC) manages the funds by making investments in various types of securities. Custodian, registered with SEBI, holds the securities of various schemes of the fund in its custodyAccording to SEBI Regulations, two thirds of the directors of Trustee Company or board of trustees must be independent.The Association of Mutual Funds in India (AMFI) reassures the investors in units of mutualfunds that the mutual funds function within the strict regulatory framework. Its objective is to increase public awareness of the mutual fund industry. AMFI also is engaged in upgrading professional standards and in promoting best industry practices in diverse areas such asvaluation, disclosure, transparency etc

Performance measures

Equity funds: the performance of equity funds can be measured on the basis of: NAVGrowth, Total Return; Total Return with Reinvestment at NAV, Annualized Returns and Distributions, Computing Total Return (Per Share Income and Expenses, Per Share Capital Changes, Ratios, Shares Outstanding), the Expense Ratio, Portfolio Turnover Rate, Fund Size,Transaction Costs, Cash Flow, Leverage.

Debt fund: likewise the performance of debt funds can be measured on the basis of: Peer Group Comparisons, The Income Ratio, Industry Exposures and Concentrations, NPAs,besides NAV Growth, Total Return and Expense Ratio.

Liquid funds: the performance of the highly volatile liquid funds can be measured on thebasis of: Fund Yield, besides NAV Growth, Total Return and Expense Ratio.

Concept of benchmarking for performance evaluation:

Every fund sets its benchmark according to its investment objective. The funds performance is measured in comparison with the benchmark. If the fund generates a greater return than the benchmark then it is said that the fund has outperformed benchmark , if it is equal to benchmark then the correlation between them is exactly 1. And if in case the return is lower than the benchmark then the fund is said to be underperformed.

Chapter – 2

Data Analysis

&

Interpretation

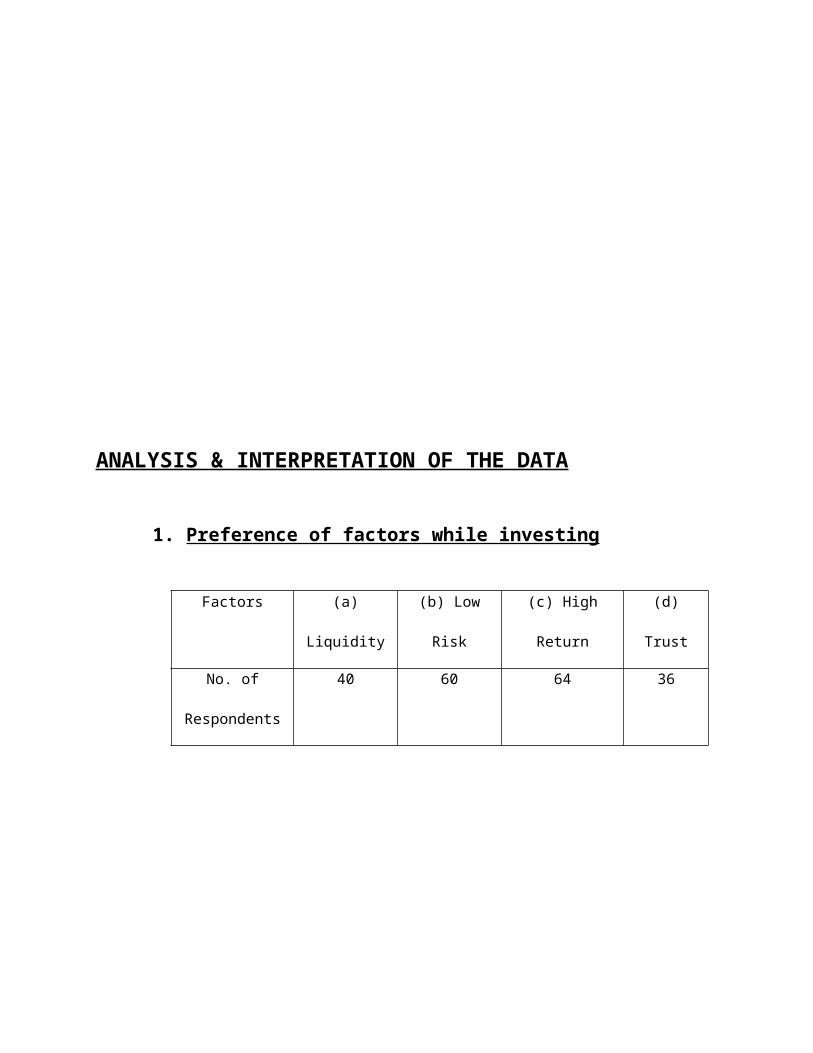

ANALYSIS & INTERPRETATION OF THE DATA

1. Preference of factors while investing

Factors (a) Liquidity (b) Low Risk (c) High Return (d) Trust

No. of

Respondents

40 60 64 36

20%

30%32%

18%

Liquidity Low Risk High Return Trust

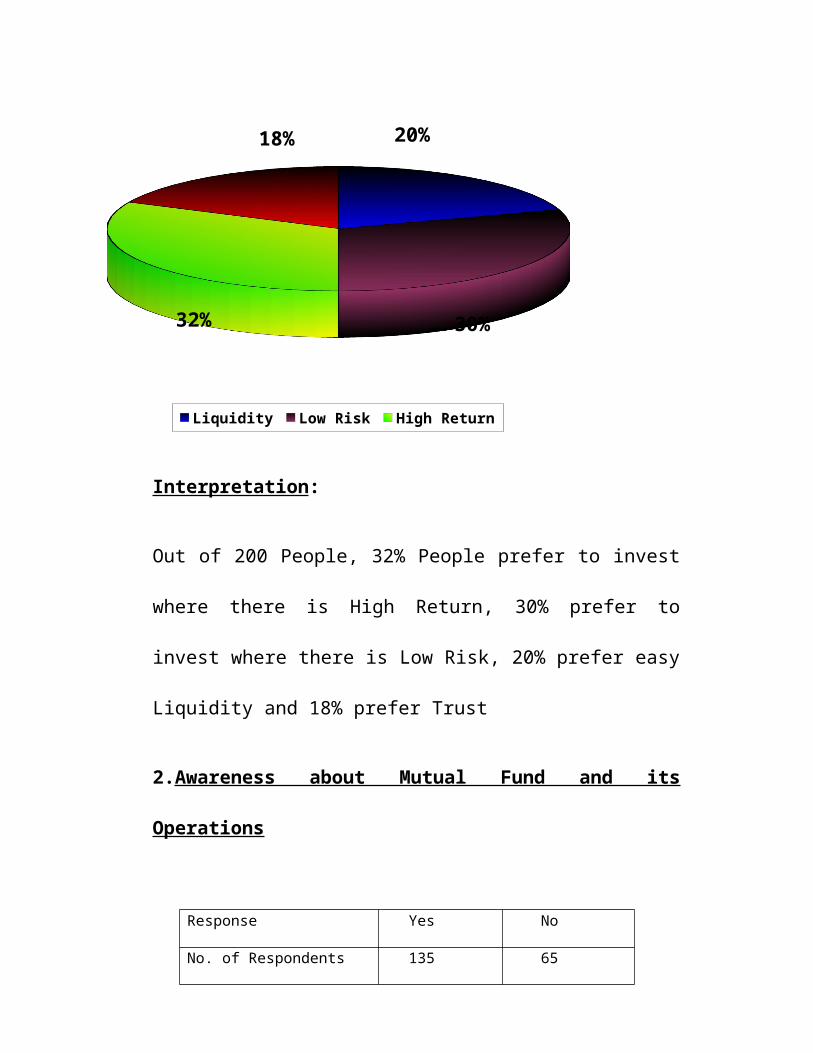

Interpretation:

Out of 200 People, 32% People prefer to invest where there is High

Return, 30% prefer to invest where there is Low Risk, 20% prefer easy

Liquidity and 18% prefer Trust

2.Awareness about Mutual Fund and its Operations

68%

33%

Yes No

Interpretation:

From the above chart it is inferred that 67% People are aware of Mutual Fund and its operations and 33% are not aware of Mutual Fund and its operations.

Response Yes No

No. of Respondents 135 65

3.Source of information for customers about Mutual Fund

Source of information No. of Respondents

Advertisement 18

Peer Group 25

Bank 30

Financial Advisors 62

Advertisement Peer Group Bank Financial Advisors0

10203040506070

18 25 30

62

Source of Information

No.

of R

espo

nden

ts

Interpretation:

From the above chart it can be inferred that the Financial Advisor is the most

important source of information about Mutual Fund. Out of 135 Respondents,

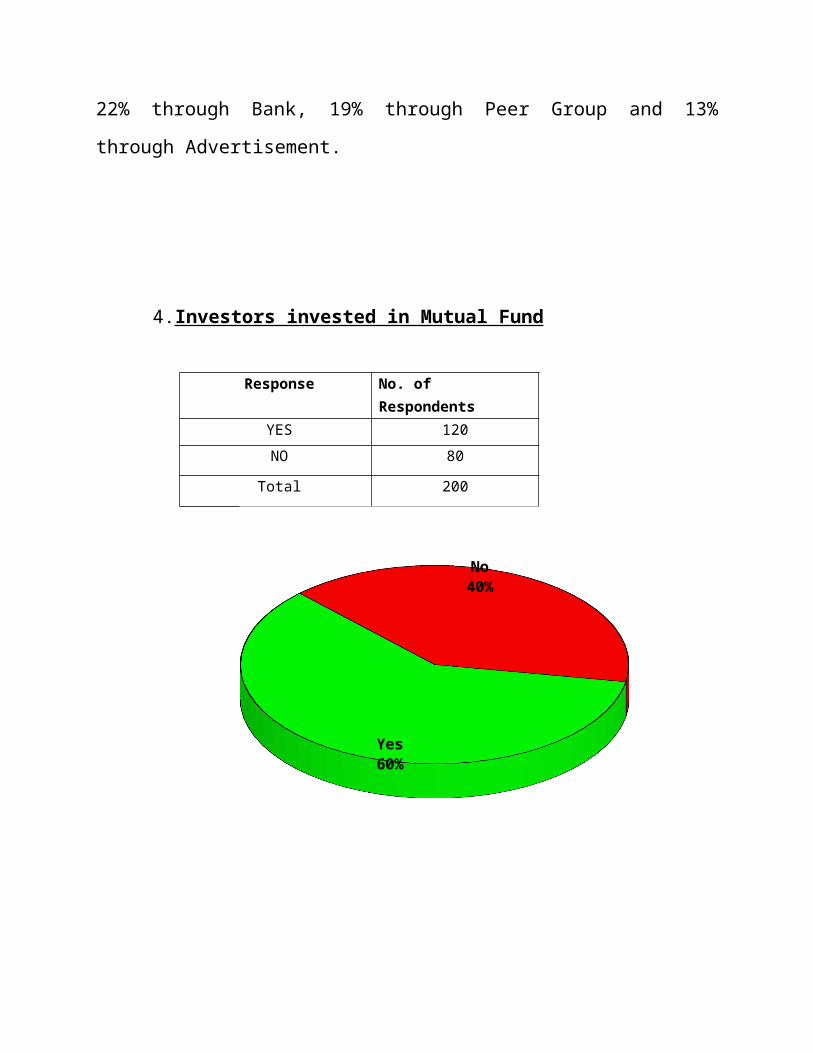

46% know about Mutual fund Through Financial Advisor, 22% through Bank, 19%

through Peer Group and 13% through Advertisement.

4.Investors invested in Mutual Fund

Response No. of Respondents

YES 120

NO 80

Total 200

Yes60%

No40%

Interpretation:

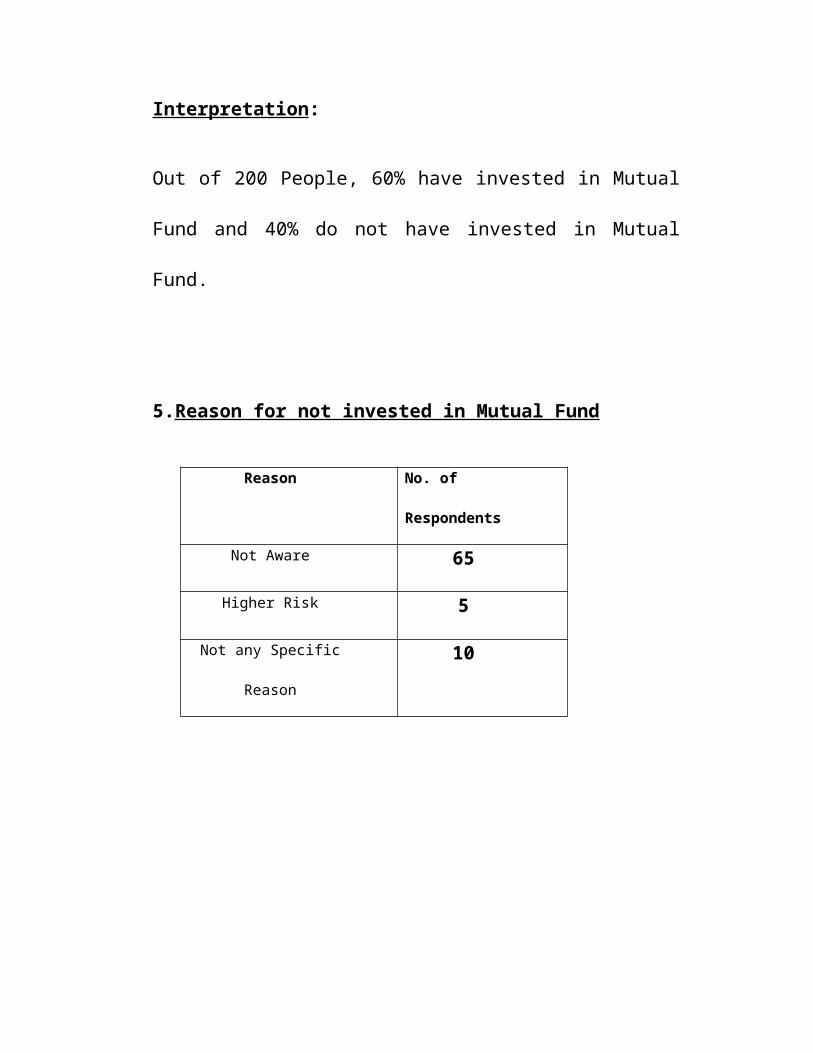

Out of 200 People, 60% have invested in Mutual Fund and 40% do

not have invested in Mutual Fund.

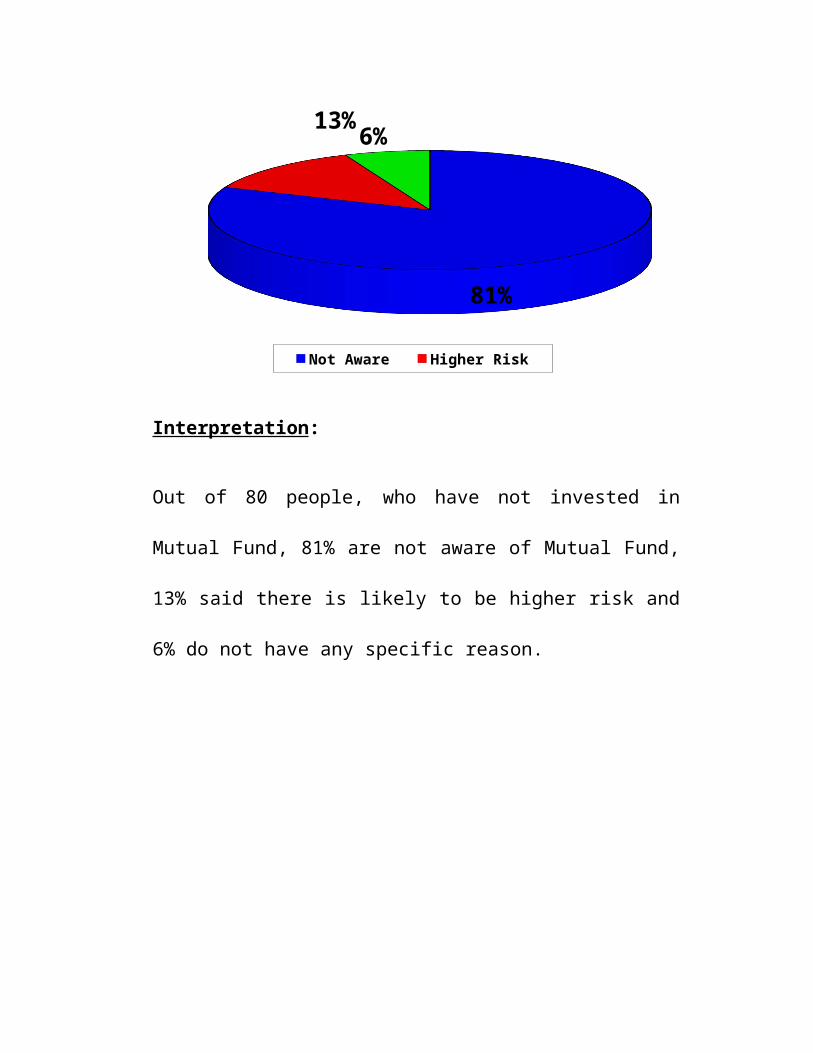

5.Reason for not invested in Mutual Fund

Reason No. of Respondents

Not Aware 65

Higher Risk 5

Not any Specific Reason 10

81%

13%6%

Not Aware Higher Risk Not Any

Interpretation:

Out of 80 people, who have not invested in Mutual Fund, 81% are not

aware of Mutual Fund, 13% said there is likely to be higher risk and

6% do not have any specific reason.

Chapter – 3

FUND EXPENSES

Expenses

Investors in a mutual fund pay the fund's expenses. These expenses fall into five categories:

management fee, distribution charges (sales loads and 12b-1 fees), the management fee,

securities transaction fees, shareholder transaction fees and fund services charges. Some of these

expenses reduce the value of an investor's account; others are paid by the fund and reduce net

asset value.

Recurring fees and expenses—specifically the 12b-1 fee, the management fee and other fund

expenses—are included in a fund's total expense ratio (TER), often referred to simply the

"expense ratio". Because all funds must compute an expense ratio using the same method,

investors may compare costs across funds.

There is considerable controversy about the level of mutual fund expenses.

Management fee

The management fee is paid to the management company or sponsor that organizes the fund,

provides the portfolio management or investment advisory services and normally lends its brand

to the fund. The fund manager may also provide other administrative services. The management

fee often has breakpoints, which means that it declines as assets (in either the specific fund or in

the fund family as a whole) increase. The management fee is paid by the fund and is included in

the expense ratio.

The fund's board reviews the management fee annually. Fund shareholders must vote on any

proposed increase, but the fund manager or sponsor can agree to waive some or all of the

management fee in order to lower the fund's expense ratio.

Distribution charges

Distribution charges pay for marketing, distribution of the fund's shares as well as services to

investors. There are three types of distribution charges:

Front-end load or sales charge. A front-end load or sales charge is a commission paid to

a broker by a mutual fund when shares are purchased. It is expressed as a percentage of the

total amount invested or the "public offering price", which equals the net asset value plus the

front-end load per share. The front-end load often declines as the amount invested increases,

through breakpoints. The front-end load is paid by the shareholder; it is deducted from the

amount invested.

Back-end load. Some funds have a back-end load, which is paid by the investor when shares

are redeemed. If the back-end load declines the longer the investor holds shares, it is called a

contingent deferred sales charges (CDSC). Like the front-end load, the back-end load is paid

by the shareholder; it is deducted from the redemption proceeds.

12b-1 fees. Some funds charge an annual fee to compensate the distributor of fund shares for

providing ongoing services to fund shareholders. This fee is called a 12b-1 fee, after the SEC

rule authorizing it. The 12b-1 fee is paid by the fund and reduces net asset value.

A no-load fund does not charge a front-end load or back-end load under any circumstances and

does not charge a 12b-1 fee greater than 0.25% of fund assets.

Securities transaction fees

A mutual fund pays expenses related to buying or selling the securities in its portfolio. These

expenses may includebrokerage commissions. Securities transaction fees increase the cost basis

of investments purchased and reduce the proceeds from their sale. They do not flow through a

fund's income statement and are not included in its expense ratio. The amount of securities

transaction fees paid by a fund is normally positively correlated with its trading volume or

"turnover".

Shareholder transaction fees

Shareholders may be required to pay fees for certain transactions. For example, a fund may

charge a flat fee for maintaining an individual retirement account for an investor. Some funds

charge redemption fees when an investor sells fund shares shortly after buying them (usually

defined as within 30, 60 or 90 days of purchase); redemption fees are computed as a percentage

of the sale amount. Shareholder transaction fees are not part of the expense ratio.

Fund services charges

A mutual fund may pay for other services including:

Board of directors or trustees fees and expenses

Custody fee: paid to a custodian bank for holding the fund's portfolio in safekeeping and

collecting income owed on the securities

Fund administration fee: for overseeing all administrative affairs such as preparing financial

statements and shareholder reports, SEC filings, monitoring compliance, computing total

returns and other performance information, preparing/filing tax returns and all expenses of

maintaining compliance with state blue sky laws

Fund accounting fee: for performing investment or securities accounting services and

computing the net asset value.

Professional services fees: legal and auditing fees

Registration fees: paid to the SEC and state securities regulators

Shareholder communications expenses: printing and mailing required documents to

shareholders such as shareholder reports and prospectuses

Transfer agent service fees and expenses: for keeping shareholder records, providing

statements and tax forms to investors and providing telephone, internet and or other investor

support and servicing

Other/miscellaneous fees

Controversy

Critics of the fund industry argue that fund expenses are too high. They believe that the market

for mutual funds is not competitive and that there are many hidden fees, so that it is difficult for

investors to reduce the fees that they pay. They argue that the most effective way for investors to

raise the returns they earn from mutual funds is to invest in funds with low expense ratios.

Fund managers counter that fees are determined by a highly competitive market and, therefore,

reflect the value that investors attribute to the service provided. They also note that fees are

clearly disclosed.

Chapter – 4

Objectives and scope

OBJECTIVES OF THE STUDY

1. To find out the Preferences of the investors for Asset

Management Company.

2. To know the Preferences for the portfolios.

3. To know why one has invested or not invested in SBI Mutual fund

4. To find out the most preferred channel.

5. To find out what should do to boost Mutual Fund Industry.

Scope of the study

A big boom has been witnessed in Mutual Fund Industry in resent

times. A large number of new players have entered the market and

trying to gain market share in this rapidly improving market.

Chapter – 5

Research Methodology

RESEARCH METHODOLOGY

Research is a process through which we attempt to achieve systematically and

with the support of data the answer to a question, the resolution of a problem,

or a greater understanding of a phenomenon. This process, which is

frequently called research methodology.

This report is based on primary as well secondary data, however primary data

collection was given more importance since it is overhearing factor in attitude

studies. One of the most important users of research methodology is that it

helps in identifying the problem, collecting, analyzing the required

information data and providing an alternative solution to the problem .It also

helps in collecting the vital information that is required by the top

management to assist them for the better decision making both day to day

decision and critical ones.

Data sources:

Research is totally based on primary data. Secondary data can be used only for

the reference. Research has been done by primary data collection, and

primary data has been collected by interacting with various people. The

secondary data has been collected through various journals and websites.

Chapter – 6

Conclusion &Rationale

CONCLUSION

Running a successful Mutual Fund requires complete understanding of the

peculiarities of the Indian Stock Market and also the psyche of the small

investors. This study has made an attempt to understand the financial

behavior of Mutual Fund investors in connection with the preferences of

Brand (AMC), Products, Channels etc. I observed that many of people

have fear of Mutual Fund. They think their money will not be secure in

Mutual Fund. They need the knowledge of Mutual Fund and its related

terms. Many of people do not have invested in mutual fund due to lack of

awareness although they have money to invest. As the awareness and

income is growing the number of mutual fund investors are also growing.

“Brand” plays important role for the investment. People invest in those

Companies where they have faith or they are well known with them like-

Reliance, UTI, SBIMF, ICICI Prudential etc.

Distribution channels are also important for the investment in mutual

fund. Financial Advisors are the most preferred channel for the investment

in mutual fund. They can change investors’ mind from one investment

option to others. Many of investors directly invest their money through

AMC because they do not have to pay entry load. Only those people invest

directly who know well about mutual fund and its operations and those

have time.

RATIONALE

- A mutual fund portfolio can offer diversification across stocks (a diversified

equity fund invests in various stocks) and asset classes ( a balanced

fund/monthly income plan invests in both equities an debt instruments).

- This rationale is fundamentally flawed. Despite being in the midst of a

seemingly endless rally, mutual fund can offer investors many advantaged and

continue to be the retail investor’s best bet.

- Investing in equities is a rather complex process. It entails studying, tracking

and understanding factors like the economy – both domestic and global,

interest rates, the political and legal environment among others.

- Secondly, a mutual fund investors offers investors the benefits of

diversification. Any financial planner worth his salt will vouch for the

importance of holding a well-diversified portfolio.

Chapter – 7

Suggestions &Recommendations &

Bibliography

SUGGESTIONS AND RECOMMENDATIONS

The most vital problem spotted is of ignorance. Investors should be made

aware of the benefits. Nobody will invest until and unless he is fully

convinced. Investors should be made to realize that ignorance is no longer

bliss and what they are losing by not investing.

Mutual funds offer a lot of benefit which no other single option could offer.

But most of the people are not even aware of what actually a mutual fund

is? They only see it as just another investment option. So the advisors

should try to change their mindsets. The advisors should target for more

and more young investors. Young investors as well as persons at the height

of their career would like to go for advisors due to lack of expertise and

time.

Mutual Fund Company needs to give the training of the Individual

Financial Advisors about the Fund/Scheme and its objective, because they

are the main source to influence the investors.

Before making any investment Financial Advisors should first enquire

about the risk tolerance of the investors/customers, their need and time

(how long they want to invest). By considering these three things they can

take the customers into consideration.

Younger people will be a key new customer group into the future, so

making greater efforts with younger customers who show some interest

in investing should pay off.

To succeed however, advisors must provide sound advice and high

quality.

BIBLIOGRAPHY

NEWS PAPERS

OUTLOOK MONEY

TELEVISION CHANNEL (CNBC AAWAJ)

MUTUAL FUND HAND BOOK

FACT SHEET AND STATEMENT

WWW.SBIMF.COM

WWW.MONEYCONTROL.COM

WWW.AMFIINDIA.COM

WWW.ONLINERESEARCHONLINE.COM

WWW. MUTUALFUNDSINDIA.COM

“MUTUAL FUND”

PROJECT REPORT BY

MS. PRIYA CHANDRA THUWAL

REGISTRATION NUMBER-201326250

SYMBIOSIS CENTRE FOR DISTANCE LEARNING (SCDL) Symbiosis Bhavan, 1065-B Gokhale Cross Road,

Model Colony, Pune-411016 Website: www.scdl.net

2013-2015

Related Documents