Municipal Finance Overview City Council Meeting Tuesday, January 21, 2020

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Municipal Finance Overview

City Council MeetingTuesday, January 21, 2020

Introducing Finance!!• Goals of this Presentation

• Educate Councilors about how municipal finance works• Provide brief history of revenues, expenditures, capital investment

and property tax burden• Demonstrate the City’s Financial Transparency Center and other

information resources to help you stay up to date on the City’s finances

• Provide insight into how Accounting, Assessing, Purchasing and Treasury work together with the CFO’s office to manage Framingham’s finances

Operating Budget Development & Approval Process

Divisions develop FY budget requests &

submit to CFO

CFO Office develops FY revenue

estimates assembles global budget and target bottom line

Mayor and Division Heads review assembled data; Mayor makes final

decisions on budget message, policy goals

and data.

Mayor Submits Budget Package to

City Council no later than 60 days before the start of

the FY

City Council receive budget

package and refers to Finance

Subcommittee

Finance subcommittee

holds public hearing on

budget

Finance subcommittee may

amend budget; recommend to

Council w/in 21 days

Full council has 21 days to act on budget; approve;

send back to Mayor

Mayor may sign or veto

any changes

Capital Improvement Plan & Capital Inventory

Prepare

• Divisions Update Capital Improvement Plans • Divisions prioritize next FY requests and submit next FY and five forward years to CFO Office• Divisions update and submit Capital Inventory to CFO Office• CFO Office assembles combined inventories in Council determined format

Finalize

• CFO Office assembles all plans/evaluates upcoming year based on multi-criteria evaluation tool; impact on debt service and management capacity

• Review with Divisions/Departments, COO; Mayor final imprimatur on CI Plan• Review Capital Inventory with Mayor for final approval

Submit• Submit Capital Improvement Plan to City council; refers to Finance Subcommittee• Submit Capital Inventory to City Council; refers to Finance subcommittee

General Fund Revenue Sources

• Property Taxes: Largest Revenue Source• Real estate – residential and commercial• Personal Property – business equipment used for the operation of

a business

• State Aid: revenue sharing from the State• Education Aid: Chapter 70 aid and Charter School Reimbursement• Unrestricted General Government Aid• Reimbursement for tax exemptions and veterans benefits

General Fund Revenue Sources

• Local Receipts – local charges for services• Motor vehicle excise tax• Local room and meals taxes• Building permits• Fees for services

• Other Financing Sources• Indirect Charges – overhead for water and sewer departments

transferred from Enterprise Fund• Free Cash – ending fund balance from prior fiscal year

Largest Revenue Source: Property Taxes

State Aid, a % of Total

74.8 73.769 67.3 65.8 67.1 67.1 66.8

14.9 16.2 18.7 1… 20.6 19.8 21.4 21.9

0

20

40

60

80

100

FY2010 FY2011 FY2012 FY2013 FY2014 FY2015 FY2016 FY2017 FY2018 FY2019 FY2020

Taxes State Aid Local Receipts Enterprise Indirect Free Cash Misc

Property taxes, a % of Total

How Does Proposition 2 ½ Work?• First 2 ½ limit – Annual Property Tax levy – Levy Limit

• Increase the prior year total levy by a maximum of 2.5%• Add taxes from new development – called New Growth

FY18 Total Levy Plus 2.5% Add NG Total Tax Levy FY19

$188,453,913 $193,165,261 $3,074,494 $196,239,755

How Does Prop 2 ½ Work?• Tax levy ceiling – the second 2 ½

• Limits total the city can levy tax to 2.5% of Equalized Valuation (EQV) or assessed value

• Which means the ability to tax is dependent upon the total value of the taxable property in a municipality

• Prop 2 ½ passed in 1980, after 37 years some communities have maxed out their taxing capacity

• The importance of wisely managing development cannot be understated

• Development and redevelopment impacts the city’s ability to generate revenue to provide services

0

50000000

100000000

150000000

200000000

250000000

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

Total Tax Levy Tax Levy CeilingOverride

Override

Recession

Recession

Housing bubble

Industrial Growth

Tax levy history

What is an override? A debt exclusion?• A debt exclusion means we add the cost of borrowing for this project

on top of the regular tax levy for the life of the borrowing term (20 years)

• The cost of borrowing means the annual payment to pay off the loan, like a mortgage – we call the debt service

• A debt exclusions is a type of override, but it differs from an operating override in that it goes away once the loan has been satisfied.

• An operating override, often just called an override, carries on forever

• Both of these actions require a city-wide ballot vote in order to be added

196,355,067

261,112,924

120,000,000

170,000,000

220,000,000

270,000,000

320,000,000

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Maximum Levy Limit

Total Tax Levy

Levy Ceiling

Levy Ceiling, Max Levy Limit, Actual Levy, FY10-25 (proj)

2.5% levy per year FY21-25

Excess capacity

What does Excess Capacity Mean to Taxpayers?

FY19 Tax Levy $191,224,338

FY19 Property Value $8,993,348,365

FY19 Single Rate $21.26

FY19 Tax Levy $191,224,338

FY19 Property Value $9,787,816,255

FY19 Single Rate $19.54

Tax Levy, Tax Rate, Property Value & Tax Burden• Tax rate is a function of Tax levy divided by total value

• If value goes up the tax rate goes down• If value goes down the tax rate goes up

We have a split rate, so we shift tax burden from residential to commercial taxpayers, which means we don’t have one tax rate

Tax Levy, Tax Rate, Property Value & Tax Burden

Property Type as % of Total% of Tax Levy paid by Property Type

If we had a single tax rate the average residential taxpayer would pay $1,600 more in property taxes

61%

28%

6%5%Residential

Commercial

Industrial

Personal Property

77%

17%

3% 3%Residential

Commercial

Industrial

Personal Property

? Questions on Taxes ?

On to State Aid…..

Second Largest Revenue Source: State Aid• Chapter 70 Education Aid – How does it work?

• State sets a Foundation Budget by formula – FY19 is $107.2M• State determines minimum city contribution using two factors:

community income and equalized value – FY19 is $60.5 million• Difference between these two numbers is Education Aid (Ch.70) –

FY19 is $46.6M (Governors proposal) [FY20 $50.96 million]• The House and Senate then rework the Governor’s proposal

• Political ‘reallocating’ usually happens

• FY19 Foundation budget formula includes an increased cost factor for employee health insurance

0

20

40

60

80

100

120

140

160

180M

illio

ns

Foundation Budget C70 Aid Required NSS Actual NSS

Chapter 70 Profile thru FY19 (DESE)

$54MTotal District Spending

Foundation Budget

Ch 70 Aid

Required Net School Spending

$163M

Additional State Aid Types

• Unrestricted General Government Aid [FY20: $10.56 million]

• Charter School Reimbursement Aid [FY20: $536,578]

• PILOT payment for certain State owned land [FY20: $465,122]

• Reimbursement for a portion of Ch 115 Veterans benefits [$277,904]

• Reimbursement of certain property tax exemptions [ $196,125 ]

? Questions on State Aid ?

On to Spending…..

16.1%

4.4%

7.6%

1.1%

60.8%

3.1%

1.4% 1.7% 2.6% 1.2%

Public Safety, Health & Inspections

General Gov't - Mayor, City Council,City Clerk, Elections, HR, Tech SvcsPublic Works

Business & Economic Development

Framingham School Dept

Keefe Tech Assessment

Financial Management

Library Services

Parks & Recreation

Financial Reserves

FY20 Cost of Services as a Percent of Total Budget

Expenditures FY20 Voted Municipal Departments $66,797,797 Framingham School District $138,484,986 Keefe Technical Assessmnt $9,170,250 Group Health Insurance $30,993,694

Other Insurances $5,563,617Retirement $16,513,289OPEB Trust $0Debt Service $14,600,280Stabilization/Reserves $1,368,209EDIC/Traffic & Diability Commi $26,000Non Appropriations $10,237,262

Total Expenditures $293,755,385Expenditure Growth Rate 3.2%

FY20 Voted General Fund Budget

4.11% or $5.5M increase

Combined Municipal Departments: 2.9% increase

Keefe Tech Assessment: 2% increase

Group Insurance: 1.7% increase

Retirement: $1M from free cash to forward fund liability

Debt Service: decrease of 2%

State assessments: 4.5% increase; overlay 8% reduction

FY20 Voted Water and Sewer Budgets

$5,466,901, 23%

$8,419,638, 35%

$8,441,595, 35%

$1,776,388, 7%

Total City Operations MWRA Assessments Debt Service Indirect Overhead Charges

Water Dept Budget $24,104,522

$4,853,425, 16%

$13,704,216, 44%

$11,036,574, 35%

$1,645,850, 5%

Total City Operations MWRA Assessments Debt Service Indirect Overhead Charges

Sewer Dept Budget$31,240,065

? Questions on Spending?

On to Financial Data/Transparency…..

Where to Find Framingham Financial Data?• Go to the Finance Division webpage and click on Budget Central• Or simply search “budget central” in the search field on the main

page• Has budget and financial reports from 2008 through 2020

OR• Go to the

• Two options for financial data: “ClearGov” infographics and “Open Data Framingham”

TRANSPARENCY CENTERReview budgets, open data information and how Framingham compares to other similar communities.

Framingham Financial Transparency Center

Clear Gov Infographics based data with benchmarking capability

Open Data Framingham allows you to access standard reports or download data datadirectly to analyze yourself

? Questions on Financial Transparency ?

ON TO ASSESSING!!

Thank You

Managing Framingham’s Finances

Tax AssessmentBy: William G. Naser, MAA Chief Assessor

September 2019

Managing Framingham’s FinancesAssessing function overview

Assessors value real and personal property which is a major source of revenue for most communities, as value is converted to tax. In addition, this department levies excise tax on motor vehicles and boats. Another value function is in the role of special assessments and betterments levied on properties receiving an enhancement of value due to property improvement.

Land Residential Commercial/Industrial Personal Motor Vehicle

Managing Framingham’s FinancesAssessing function overview(con’t)

Other Assessing duties: Calculate annual community’s new growth (additional value) as part of the proposition 2 ½

calculation. Analyze and determine values for all real and personal property: 21,052 accounts and over 10 billion

in property value Follow guidelines and standards to receive state value approval annually for all real and personal

property Present annual tax rate options for Mayor/City Council choice of community tax burden Review value appeals submitted by taxpayers; local Board grants or denies appeal Defend values at Appellate Tax Board hearings Commit Real & Personal Property tax amounts to the Tax Collector, for billing and collection

New Growth Appellate Tax Board

Managing Framingham’s FinancesValue function – Residential (77% of Framingham value)

Residential single family homes are valued by reviewing sales that occur during the assessment period. Sales are reviewed and qualified as market transactions (as opposed to non-qualified sales, such as family sales, bankruptcy, other). First, complete a physical inspection of sale properties Second, adjust building components based on inspection (bath count,

conditions,etc.) Third, perform mass appraisal analysis; take sale ratios and adjust properties

(not all adjustments are the same, depends on property type…for example if colonial types are selling at a higher ratio than cape styles, colonials would adjust higher than capes; say capes went up by 3% and colonials by 5%) Goal is to value property at full value as of assessment date.

Managing Framingham’s FinancesValue function - Residential

Valuing Methods: Market or Sales method – uses open market sales to arrive a value range for

property groups

Cost method – uses land value, plus building cost, and cost information to arrive at a value range for property groups

City of Framingham uses a blended approach with residential improved properties, using components of each of these methods. The use of highly sophisticated software aids us in the ability to analyze and produce values that meet or exceed Department of Revenue requirements annually.

SALES BLD MATERIALS

Managing Framingham’s FinancesValue function – Commercial/Industrial (20%)/Personal (3%)

Valuing Methods: Commercial & Industrial Income method – uses capitalized income to arrive a value

range for property groups (and uses Cost method as a secondary approach to value)

Personal (business) Cost method – uses asset listings; original cost less yearly

depreciation to arrive a value for property type(s)DIRECT CAPITALIZATION TAXABLE ASSETS

V=I/RValue = Income/Rate

Managing Framingham’s FinancesConverting Value to Tax

STEP 1 – Complete city valuation of all property, receive state value approval

STEP 2 – Receive Tax Levy amount (tax money) to be raised through real and personal property

STEP 3 – Prepare tax burden scenarios and local tax options for City Council decisions

Managing Framingham’s FinancesAmount to operate City of Framingham/ Source of Funds

Amount to run city, one year: $345,900,000 EXPENSERevenue sources: State funds (cherry sheets) $61,520,000 Local receipts (motor vehicle, investments, etc.) $73,957,000 NON-TAX REVENUE

Free cash and other $15,423,000Total Receipts/Revenue Sources $150,900,000

TOTAL TO BE RAISED (city expenses total): $345,900,000Minus Cash available (all revenues) ($150,900,000)

So ‘gap’ amount is the money needed from Real and personal property taxes….called the LEVY AMOUNT $195,000,000

Managing Framingham’s FinancesConverting Value to Tax/Tax Rates VALUE TAX Dollars

Estimated Levy (amount to be raised thru taxes): $195,000,000Estimated Taxable Value (real and personal): $10,303,000,000 Single Tax Rate: $195,000,000/10,303,000,000 = $18.93/1000 in value

CIP SHIFT RES FACTOR RESIDENTIAL OS COMMERCIAL INDUSTRIALPERSONAL PROPERTY

RES SHARE PERCENTAGE

CIP SHARE PERCENTAGE

1.66 0.8140 15.41 0.00 31.42 31.42 31.42 63.50 36.49611.67 0.8112 15.35 0.00 31.61 31.61 31.61 63.28 36.71601.68 0.8084 15.30 0.00 31.80 31.80 31.80 63.06 36.93581.69 0.8055 15.25 0.00 31.98 31.98 31.98 62.84 37.15571.70 0.8027 15.19 0.00 32.17 32.17 32.17 62.62 37.37551.71 0.7999 15.14 0.00 32.36 32.36 32.36 62.40 37.59541.72 0.7971 15.09 0.00 32.55 32.55 32.55 62.18 37.81531.73 0.7943 15.03 0.00 32.74 32.74 32.74 61.96 38.03511.74 0.7915 14.98 0.00 32.93 32.93 32.93 61.75 38.25501.75 0.7886 14.93 0.00 33.12 33.12 33.12 61.53 38.4748

1.00 100.00 18.93 0.00 18.93 18.93 18.93 77.1970 22.8030

Estimated Tax Rates (DOR approves tax rates)

Managing Framingham’s FinancesConverting Value to Tax/Tax Rates/ Average Single Family

CIP Shift Factor

RESIDENTIAL RATE

AVERAGE SINGLE FAMILY VALUE - FY2020

FY20 Tax Amount

1.66 15.41$ 438,310 $6,754 1.67 15.35$ 438,310 $6,728 1.68 15.30$ 438,310 $6,706 1.69 15.25$ 438,310 $6,684 1.70 15.19$ 438,310 $6,658 1.71 15.14$ 438,310 $6,636 1.72 15.09$ 438,310 $6,614 1.73 15.03$ 438,310 $6,588 1.74 14.98$ 438,310 $6,566 1.75 14.93$ 438,310 $6,544

1.00 $18.93 438,310 $8,297

Estimated RE Tax - Average SF Dwelling using factors from 1.66 -1.75

Managing Framingham’s FinancesAssessing – Tax Deferral and Tax Exemptions

The Assessing department offers 2 types of tax relief for qualified taxpayers owning residential property. EXEMPTIONS are yearly adjustments made to the taxpayers tax

amount (non-repayment).There are veteran and non-veteran exemption programs.

• The DEFERRAL program is a yearly delay in payment of taxes. Qualified taxpayers can delay tax payments with 4% annual interest.

EXEMPTION PROGRAM types NUMBER OF APPROVALS TAX DOLLARS ABATED7 292 298,615$

DEFERRAL PROGRAM NUMBER OF APPROVALSTAX DOLLARS to be

recovered

9 9 41,809$

Managing Framingham’s FinancesAssessing Department Summary

The Assessing department is a value based. All year long, values are being refined and adjusted. The conclusion of the work, is state tax rate approval usually in November each year.• A bill file with all the values and new tax rate for the tax year is created, and sent to

the Tax Collector, and then real and personal property bills are mailed.• The goal is to value each property fairly and proportionately to other similar

properties.• The revenue created from tax assessment is typically about 65% of the tax dollars

needed to operate the community.• We are a department of 7 people who are charged with a significant responsibility to

all taxpayers in the community. • We are happy to review and go over individual assessments in our office. And we

appreciate the cooperation we receive from other departments and all taxpayers in Framingham.

Managing Framingham’s Finances

Thank you !

?s on Assessing?

ON TO ACCOUNTING!!

Managing Framingham’s Finances

AccountingBy: Richard G. Howarth, Jr

September 19, 2019

Managing Framingham’s FinancesThe Role of Accounting Officer

The Role of the Accounting Officer is defined by Statue and includes the responsibilities of approving all Bills and Payrolls for payment, maintaining the books in accordance with the Uniform Massachusetts Accounting System (UMAS) and Generally Accepted Accounting Principles (GAAP), as well as providing reports for regulators, independent Auditors and the Public and Notification if appropriations are exceeded.

Managing Framingham’s FinancesAccounting function overview(con’t)

Accounting Functions: Approval of BillsMaintaining Books of Account and Financial

Records Notifications; and Reports

Managing Framingham’s Finances Approval of bills

Approval of bills: G.L.c. 41 S. 52 & G.L.c.41 S.56• examine requisite oaths & approval for the payment of bills &

Payrolls• inspect departmental accounts & approve their payment by

TreasurerExamination of Bills & Payrolls

• Charges are correct;• Goods, materials or services charged for were ordered;• Goods and materials were delivered; and• Services were actually rendered to or for the City.

Managing Framingham’s FinancesApproval of bills(con’t)

• withhold payment if it is considered fraudulent, unlawful or excessive;

• file with the Treasurer a statement outlining the reason(s) for the withholding; and

• draw a warrant upon the treasury for payment, if all is in order, and process

Managing Framingham’s FinancesBooks of Account & Financial Records

Uniform Massachusetts Accounting System (UMAS)

A uniform accounting system established by the Director of Accounts in the Department of Revenue for local governmental entities.

To prepare • Balance Sheet• Schedule A

Managing Framingham’s FinancesBooks of Account & Financial Records(con’t)

Books include General Journal, General Ledger and Subsidiary Ledgers

Amount of each specific appropriation; Amounts & purposes of expenditures; Receipts from each source of Income; Amount of assessment Levied; and Abatements made.

Additional items• Contracts & Surety Bonds• Detailed Record of Debt

Managing Framingham’s FinancesNotifications

Notifications• May notify person to whom money is due.(stops interest

accruing)• Statement of Payments Amount; “Departmental

Turnover” • Notification of Receipts• Notice of Condition Appropriation• Notification of Debt Not Provided For to Assessors

Managing Framingham’s FinancesMunicipal Reporting

Department of Revenue-Division of Local Services• Balance Sheet

Cash Reconciliation ReportOutstanding ReceivablesStatement of IndebtednessSnow & Ice Data Sheet

• Schedule A• Tax Recap

Managing Framingham’s FinancesMunicipal Reporting (con’t)

Financial Reports• Financial Statements• Single Audit• OPEB

Managing Framingham’s Finances

Thank you !

?s on Accounting?

On to Treasurer!

Tax CollectionCarolyn Lyons, Treasurer/Collector

Managing Framingham’s Finances

Managing Framingham’s Finances

Treasurer’s OverviewOnce the Assessor commits the Real & Personal Property for billing and collection, this office creates the quarterly bills and prepares them with the City’s vendor who then prints and mails all the quarterly bills.

The Treasurer’s Office collects all forms of payments that are made to the City. The bulk of the payments we collect are Real Estate Tax, Personal Property Tax, Excise Tax, Parking tickets and Water and Sewer bills. But we also collect and reconcile all payments that are made in every department in the City.

Managing Framingham’s Finances

Payment methodsPayments can be made in our office online at the City’s websitemail or lockbox

Payments are also made to our office by mortgage companies and tax services

Managing Framingham’s Finances

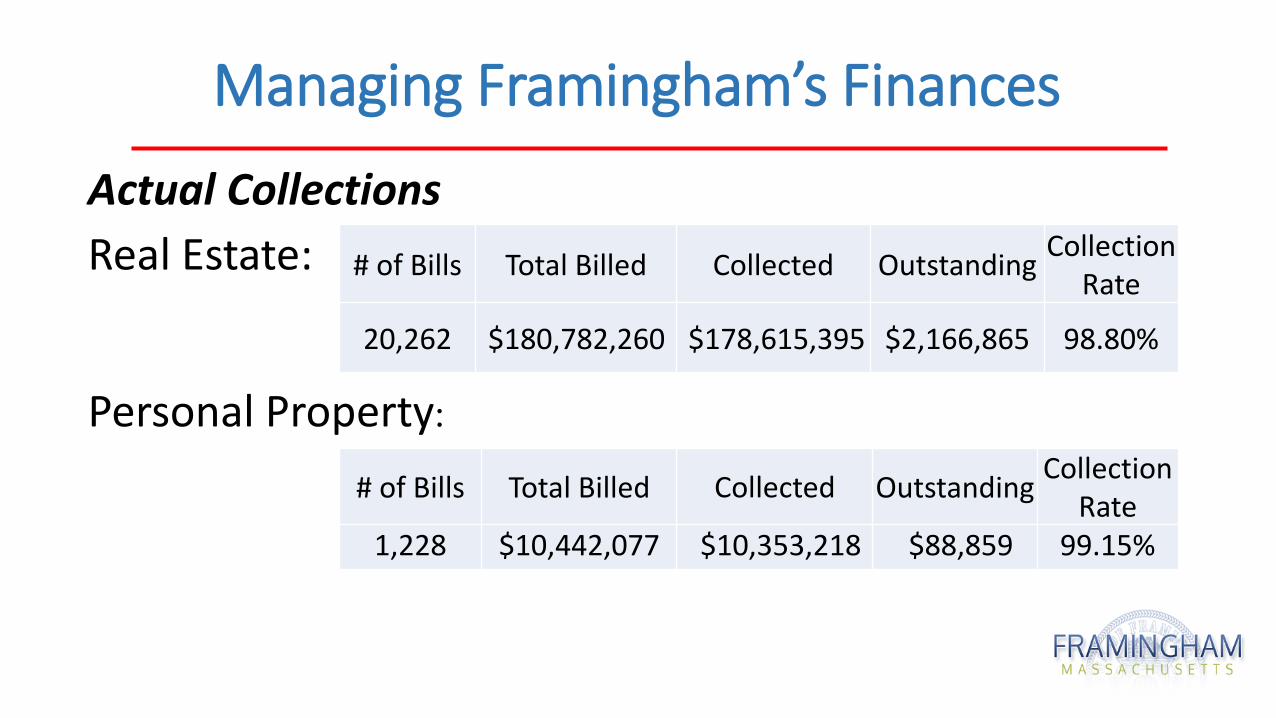

Actual CollectionsReal Estate:

Personal Property:

# of Bills Total Billed Collected Outstanding Collection Rate

20,262 $180,782,260 $178,615,395 $2,166,865 98.80%

# of Bills Total Billed Collected Outstanding Collection Rate

1,228 $10,442,077 $10,353,218 $88,859 99.15%

Managing Framingham’s FinancesWater and Sewer bills

# of Bills Total Billed CollectedOutstanding

liened to Real Estate

Collection Rate

73,495 $45,211,316 $43,959,686 $1,251,629 98%

Managing Framingham’s Finances

Excise tax:

Parking tickets:

# of Bills Total Billed Collected Outstanding Collection Rate

58,294 $8,520,000 $6,910,505 $1,608,494 88.50%

# of Bills Total Billed Collected Outstanding Collection Rate

3,684 $78,825 $53,520 $25,305 75.00%

Managing Framingham’s FinancesTax Title

All Real Estate accounts that go unpaid by the end of a fiscal year will be subject to having their account advertised in the newspaper and if still unpaid after the advertising a will then lien placed on their property with the Middlesex Registry of Deeds.

• A demand letter called a Notice of Advertising is sent to the homeowner. With 30 days to pay.

• If unpaid after the 30 days the homeowner is advertised in the newspaper and after 14 days after the advertisement the lien process will begin if the account is still unpaid. The Treasurer has 60 days to record the lien with the Registry of Deeds.

There have been instances where we offer a payment plan to residents once the account is in Tax Title, this signed agreement would be for no more than 5 years and with a payment of 25% of the balance prior to the agreement being approved.

• On a average we put about 100 accounts into Tax Title with an average outstanding total of $520K per year

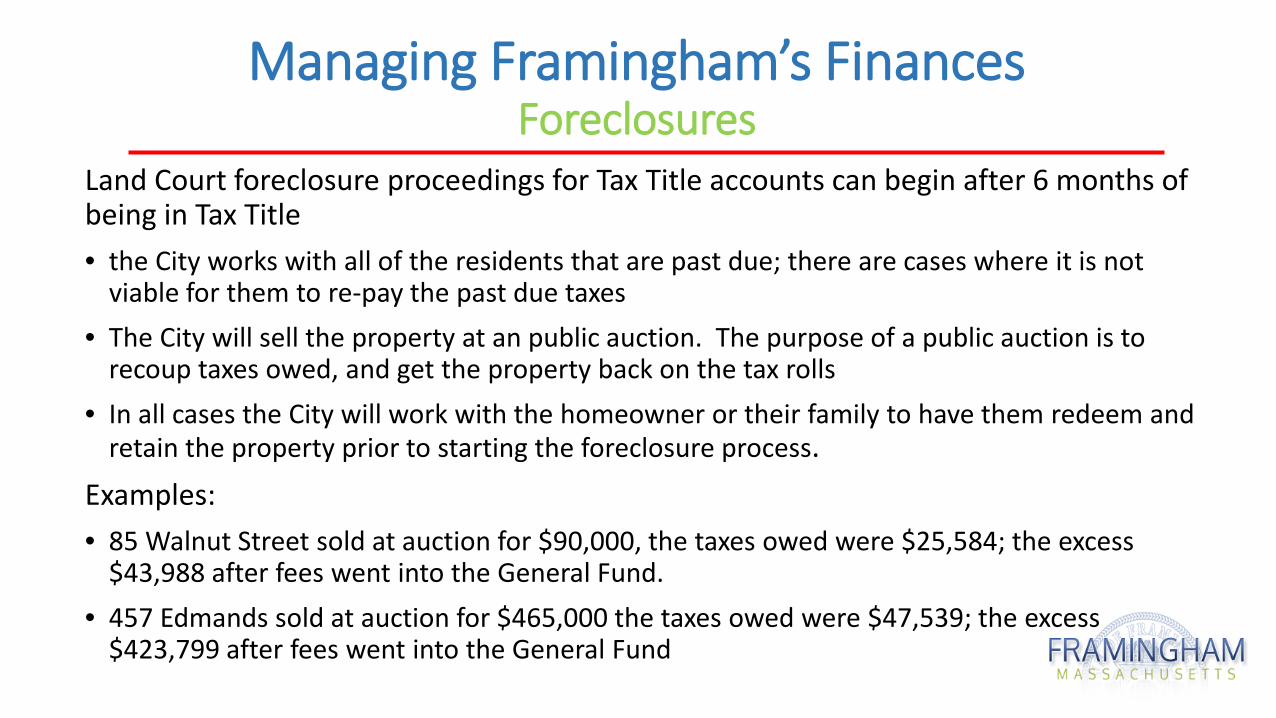

Managing Framingham’s FinancesForeclosures

Land Court foreclosure proceedings for Tax Title accounts can begin after 6 months of being in Tax Title • the City works with all of the residents that are past due; there are cases where it is not

viable for them to re-pay the past due taxes • The City will sell the property at an public auction. The purpose of a public auction is to

recoup taxes owed, and get the property back on the tax rolls• In all cases the City will work with the homeowner or their family to have them redeem and

retain the property prior to starting the foreclosure process. Examples:• 85 Walnut Street sold at auction for $90,000, the taxes owed were $25,584; the excess

$43,988 after fees went into the General Fund.• 457 Edmands sold at auction for $465,000 the taxes owed were $47,539; the excess

$423,799 after fees went into the General Fund

Managing Framingham’s FinancesThe Elderly and Disabled Taxation Fund is a program whereby taxpayers donate money to aid in defraying Real Estate taxes for the elderly and disabled. There are minimum yearly requirements to approved to receive the aid. • Must own and occupy property and must be a Framingham resident for a

minimum of 5 years.• Must be 60 years of age for a single person and if married one person must

be 60 years old.• Single person income cannot exceed $30,000 and total estate cannot

exceed $100,000.• Married couple income cannot exceed $40,000. and total estate cannot

exceed $200,00• Disabled resident must have SSDI or private disability insurance. Income

and Estate requirements as stated above.

Managing Framingham’s Finances

The Committee consists of the Chairman of the Board of Assessors, the Treasurer/Collector and three residents.

The applications are located in the Treasurer’s Office and are filed annually between January 1st and March 15th.

In 2019, we received $5,135 in donations and were able to give 13 applicants that applied and were approved $395 to go towards their taxes.

Managing Framingham’s FinancesOther Treasurer Duties:• This office works with the CFO and Accountant to borrow (bond) twice a year, in

June and in December. The City borrows for water/sewer projects, equipment for all departments, fire station, school roof, etc. This office is responsible for paying all of the bond bills received on a monthly basis.

• The Treasurer’s Office is responsible for reconciling all of the cities bank accounts. We have 80-90 bank accounts with a daily average of $125-$150K, depending on the time of the year. We work with the Accountant to ensure we balance to the General Ledger.

• This department also transfer funds weekly to fund payroll, vendor checks• The department also prints and mails all Accounts Payable checks, Payroll checks

for the city.

Managing Framingham’s FinancesWe have 7 employees who work hard at giving the best customer service to all of our residents and non residents.

We are always willing to help and review any issues you have with any of your bills or payments that are made to our office.

We are also grateful for all of the support we receive from the Assessors, Accounting, CFO and all the departments in the City.

Thank You?questions?

On to Purchasing!

Framingham Government Academy

Thursday September 19, 2019

Purchasing Department

Who are we - Staff• Chief Procurement Officer• Procurement Administrator• Part-time Administrative Assistant• Handle all purchasing functions for city and school departments • DPW Capital Unit conducts bids for Public Works Capital Projects

• Assistant Director of Public Works

• Procurement Administrator for Public Works

Purchasing DepartmentWhat we do – Procurement 101

• Ensure all purchases are made in strict compliance of procurement laws and regulations of the Commonwealth and city

• Apply best practices for procurement as recommended by Massachusetts Inspector General and Massachusetts Association of Public Procurement Officials

• Work closely with stakeholders throughout city and school departments• Maximize the value of available funding for goods and services• Contract with responsive and responsible vendors• Conduct auctions of surplus goods and equipment• Conduct audits for contract compliance and administration goals

Education Ensures Successful Bids & ContractsMassachusetts Inspector General provides a curriculum to obtain Massachusetts Public Procurement Officials Certification (MCPPO)

• Educate public purchasing officials to operate effectively, promote excellence in public procurement and help private sector employees understand state and local bidding requirements

• For public officials including anyone with responsibly for public procurement, contracting for public works and building projects, contract management or oversight or auditing in Massachusetts

• Procurement officials and staff, superintendents, school business officials and staff, public works director and staff, housing authority officials, architects and engineers performing public work, auditors, department heads, contracting officers and staff

• Teaches participants about procurement, contracting and ethics laws• Provides practical recommendations to assist public officials in implementing

best practices in their own jurisdictions

Education Ensures Successful Bids & ContractsOfficials throughout the city hold MCPPO certification or have attended classes toward future certification

Asst. CFO/Chief Procurement Officer Procurement Administrator School Executive Director of Finance & Operations Operations Manager Capital Projects & Facilities Management Chief Engineer Department of Public Works Assistant Director of Public Works Public Works Capital Procurement Administrator School Capital Projects CoordinatorDeputy Director Parks, Recreation & Cultural Affairs

Education Ensures Successful Bids & ContractsOfficials throughout the city hold MCPPO certification or have attended classes towards future certification

Deputy Director Public WorksAssistant Director of Highway & SanitationAssProgram Administrator SanitationProgram Administrator HighwayAssistant Director of Admin & Ops DPWWater Supervisor

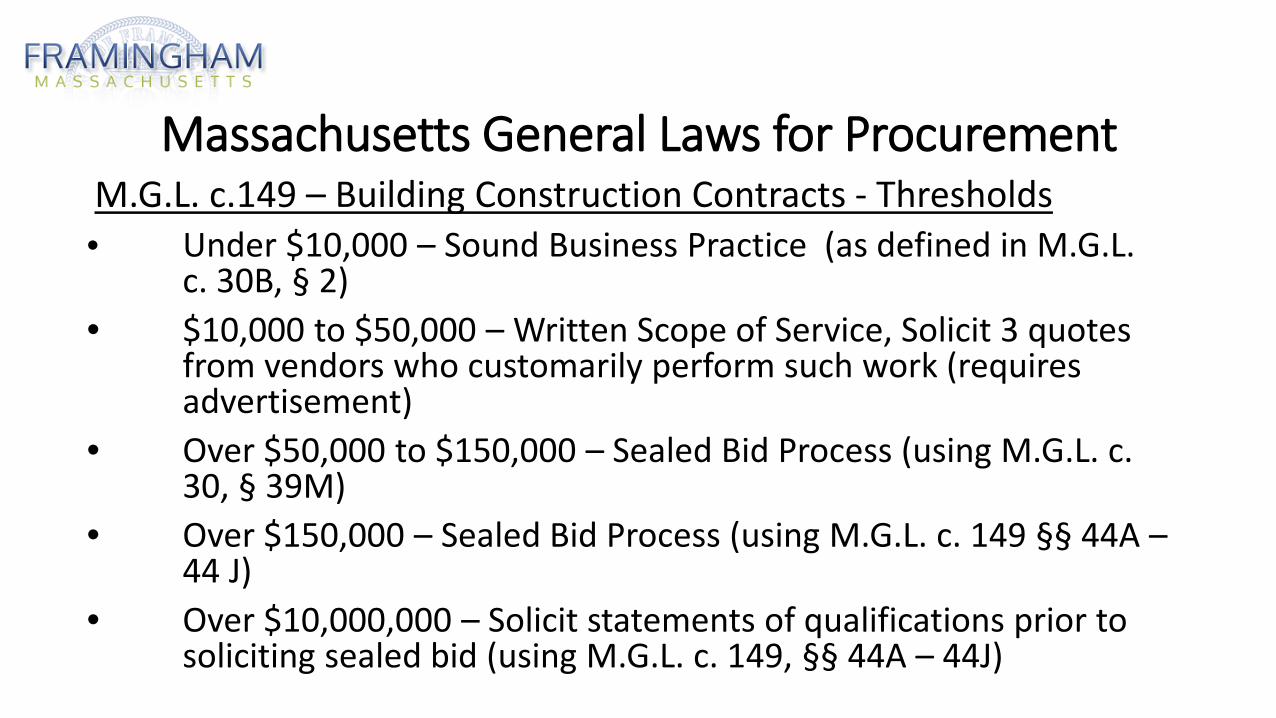

Massachusetts General Laws for ProcurementMost recent updates issued by the state occurred July 2018M.G.L. c.149 – Building Construction ContractsM.G.L. c.30, § 39M, or M.G.L. c. 30B, § 5 – Public Works (Non-Building) Construction Contracts (with labor)M.G.L. c.30, § 39M, or M.G.L. c. 30B, § 5 – Construction Materials Procurement (without labor)M.G.L. c. 7c, §§ 44-58 – Design Services for Public Building ProjectsM.G.L. c. 30B (Uniform Procurement Act) – Procurement of Supplies and Services

Massachusetts General Laws for ProcurementM.G.L. c.149 – Building Construction Contracts - Thresholds• Under $10,000 – Sound Business Practice (as defined in M.G.L.

c. 30B, § 2)• $10,000 to $50,000 – Written Scope of Service, Solicit 3 quotes

from vendors who customarily perform such work (requires advertisement)

• Over $50,000 to $150,000 – Sealed Bid Process (using M.G.L. c. 30, § 39M)

• Over $150,000 – Sealed Bid Process (using M.G.L. c. 149 §§ 44A –44 J)

• Over $10,000,000 – Solicit statements of qualifications prior to soliciting sealed bid (using M.G.L. c. 149, §§ 44A – 44J)

Massachusetts General Laws for ProcurementM.G.L. c.149 – Building Construction Contracts

McAuliffe Library

Massachusetts General Laws for ProcurementM.G.L. c.149 – Building Construction Contracts

Fire Station 2

Massachusetts General Laws for ProcurementM.G.L. c.149 – Building Construction Contracts

Village Hall Renovation

Massachusetts General Laws for ProcurementM.G.L. c.149 – Building Construction Contracts

Fuller Middle School

Massachusetts General Laws for ProcurementM.G.L. c. 30, § 39M, or M.G.L. c. 30B, § 5 – Public Works (Non-Building) Construction Contracts (With Labor) - Thresholds

• Under $10,000 – (M.G.L. c. 30, § 39M) Sound Business practice (as defined in M.G.L. c. 30B, § 2)

• $10,000 to $50,000 – (M.G.L. c. 30, § 39M) Written Scope of Service, Solicit 3 quotes from vendors who customarily perform such work (requires advertisement)

• $50,000 or less – (M.G.L. c. 30B § 5 Option) Sealed Bids • Over $50,000 (M.G.L. c. 30, § 39M) Sealed Bids

Massachusetts General Laws for ProcurementM.G.L. c.30, § 39M, or M.G.L. c. 30B, § 5 – Public Works (Non-Building) Construction Contracts (with labor)Central St./Edgell Rd. Utility Improvements North Concord Roadway Improvements

Massachusetts General Laws for ProcurementM.G.L. c.30, § 39M, or M.G.L. c. 30B, § 5 – Public Works (Non-Building) Construction Contracts (with labor)

Salem End Road Bridge Sewer Pump Station Replacements

Massachusetts General Laws for ProcurementM.G.L. c. 30, § 39M, or M.G.L. c. 30B, § 5 – Construction Materials Procurement (Without Labor) - Thresholds

• Under $10,000 – (M.G.L. c. 30, § 39M) Sound Business practice (as defined in M.G.L. c. 30B, § 2)

• $10,000 to $50,000 – (M.G.L. c. 30, § 39M) Written Scope of Service, Solicit 3 quotes from vendors who customarily perform such work (requires advertisement)

• Over $50,000 (M.G.L. c. 30, § 39M) Sealed Bids • Any Amount (M.G.L. c. 30B, § 5 Option) Sealed Bids

Massachusetts General Laws for Procurement

M.G.L. c.30, § 39M, or M.G.L. c. 30B, § 5 – Construction Materials Procurement (without labor)

Sand Loam Stone

Massachusetts General Laws for Procurement

M.G.L. c.30, § 39M, or M.G.L. c. 30B, § 5 – Construction Materials Procurement (without labor)

Water Pipes Sewer/Drainage Pipes Fire Hydrants

Massachusetts General Laws for ProcurementM.G.L. c. 7C, §§ 44-58 Design Services for Public Building Project - Thresholds

• Estimated Design Fee (EDF) less than $30,000 or Estimated Construction Cost (ECC) less than $300,000 – Recommendation (not required) to solicit qualifications and prices from at least three designers

• Estimated Design Fee (EDF) of $30,000 or more AND Estimated Construction Cost (ECC) of $300,000 or more – Qualifications based selection process. Jurisdiction must set the design fee ORset a not-to exceed fee limit and negotiate the fee with the top-ranked designer within the fee limit

Massachusetts General Laws for ProcurementM.G.L. c. 7c, §§ 44-58 – Design Services for Public Building Projects

Lexington Street Library Entrance

Massachusetts General Laws for ProcurementM.G.L. c. 30 - Procurement of Supplies and Services -Thresholds

• Under $10,000 – Sound Business Practice (Defined as ensuring the receipt of favorable prices by periodically soliciting price lists or quotes)

• $10,000 to $50,000 –Written Scope of Service, Solicit 3 quotes from vendors who customarily provide the supply or service

• Over $50,000 - Sealed Bids or Proposals

Massachusetts General Laws for ProcurementM.G.L. c. 30B – Procurement of Supplies and Services

School Food/Groceries School Bus Transportation

Massachusetts General Laws for ProcurementM.G.L. c. 30B – Procurement of Supplies and Services

Photocopiers (Lease) Office Supplies

Massachusetts General Laws for ProcurementM.G.L. c. 30B – Procurement of Supplies and Services

Fire Trucks Ambulance Services

Massachusetts General Laws for ProcurementM.G.L. c. 30B – Procurement of Supplies and Services

Police Cruisers Tractors/Equipment

Procurement & Bidding Process

Departments develop scope of work and

specifications in cooperation with staff

and/or consultants

CPO Office reviews documentation and

develops Invitation for Bid (IFB) in

cooperation with department and City

Solicitor

Bidding Calendar is developed and advertised according to Mass General

Laws for procurement

Bids received in accordance with

calendar deadlines are opened in a

public bid opening

Department and

procurement staff review

bids

Department assess bids

and recommends award to CPO

CPO reviews recommendation for

award to ensure compliance

Contract is awarded to the responsive and

responsible bidder

Contract is routed for signature

Procurement ResourcesCooperative/Collaborative Purchasing Programs

• Chapter 30B, § 22 allows local jurisdictions to purchase supplies from contracts that have been procured by an in-state or out-of-state political subdivision, unit of a political subdivision, or a federal or state agency

• As long as the contract is open to local jurisdictions and was procured in a manner that constitutes full and open competition

• Allows local jurisdiction to purchase from such contracts without conducting its own procurement process

• Only goods – not services • Requires performing due diligence to determine compliance

Procurement ResourcesCooperative/Collaborative Purchasing Programs

Massachusetts Statewide Contracts through Operational Service Division (OSD)

16 Categories of Contracts - Energy, Technology, Office/Educational Supplies, Tradespersons, Vehicles, Public Safety Equipment

U.S. General Services Administration (GSA)Fleet Vehicles & Equipment, Technology, Furniture, Office Supplies/Equipment

Massachusetts Higher Education Consortium (MHEC)Lab Equipment, Appliances, Furniture, Books, Software/Technology,Custodial Cleaning Equipment & Supplies, Multimedia

Number of Contracts Awarded FY2016 – FY2019 (75 unit price, on call or revenue contracts FY19)

111102

120

140

73 71

122116

125 122 121

68

FY2016 FY2017 FY2018 FY2019

City School DPW

Value of Contracts Awarded FY2016 – FY2019 (does not include unit price or on-call contracts)

$6,525,280$11,352,627 $11,895,407

$8,730,453$6,959,723

$32,968,667

$3,796,484

$94,818,458

$16,514,326$19,691,308 $19,775,213

$16,076,938

FY2016 FY2017 FY2018 FY2019

Town/City School DPW

Surplus Supplies & Auctions• Chapter 30B – applies to the disposal of any supply

with resale or salvage value• Supplies Valued Over $10,000 – solicitation for sealed

bid, public auction or use of an established market• Swaps – jurisdictions may swap with internal

departments (police to school), other local governments within the Commonwealth, or with state or federal government agencies (exempt from 30B)

• Value – legitimate sources must be used for determining value of surplus items (Kelly’s Blue Book)

• Bids/Auctions – Procurement department advertises bids or arranges for auction

• Bid Requirement – All bids must be accompanied by a signed non-collusion form

• Award – CPO determines rule for award (highest bid from a responsible bidder)

Real Property - Acquisitions

• Value – advertising required with a cost of $35,000 or greater• Definition – real property is defined as property consisting of land, buildings, crops or

other resources still attached to or within the land or improvements to fixtures permanently attached to the land or a structure on it

• Interests – include leases, mortgages, preservation restrictions, easement and profits à prendre (the right to remove gravel or ledge from land)

• Exemptions – eminent domain takings, rental of residential property to qualified tenants (housing authority), redemption or auction of tax title property

Chapter 30B – applies to the purchase, sale or lease/rental of real property

Real Property - Dispositions

• 30B – advertising and soliciting for proposals required with a cost of $35,000 or greater• Definition – real property is defined as property consisting of land, buildings, crops or

other resources still attached to or within the land or improvements to fixtures permanently attached to the land or a structure on it

• Value – determine value, may you use appraisal or municipal assessment• Leases – value determined by calculating the fair market value of the lease over the

entire contract term• Emergencies – may shorten or waive advertising period (endanger the health or safety

or people or their property)

Any disposition of real property, regardless of value, must be declared property available for disposition. Property disposed at less than fair market value must be posted in Central Register with explanation difference in price (value vs. sale)

Contract Compliance & Administration• Valid Bid – effective bidding specification• Strong Contract – procurement team and legal review • Contract oversight and monitoring – OPM, vendor, city

staff, stakeholders • Ongoing Communication – achieve procurement goals

and eliminate and/or minimize change orders • Documentation – avoid legal problems and mitigate

risk• Dispute Resolution – record keeping and

documentation critical (vendor is not your friend –DOCUMENT!!!)

• Financials – current and ongoing financial management throughout life of contract until closeout

Preventing Fraud, Waste & Abuse • Guidance – Office of Inspector General, Attorney

General, City Solicitor, CPO• Certification – bidders must complete non-collusion

form• Communication – bidders may only communicate

questions regarding bids to procurement staff• Bids – all bids received by procurement office and

remain sealed until public bid opening• Documentation – all bids are opened and reviewed by

procurement official and witnessed by staff• Awards – recommendation for awards reviewed by

CPO• Compliance – CPO reviews recommendation for award

for compliance with bidding laws, bid requirements and financial thresholds

Preventing Fraud, Waste & Abuse Separation of Duties• Contract – signed by vendor, department head, CPO, city

solicitor, city accountant, Mayor• Requisition – department enters requisition in MUNIS and

attaches completed contract• Purchase Order – requisition is reviewed and approved by

department, CFO, accounting and converted to PO• Vendor – department authorizes vendor to begin work

once PO is completed• Payments – invoices received from vendor are reviewed by

department and submitted for payment against PO• A/P Process – accounting reviews invoices for payment and

reviews contract for compliance• Warrant – accounting submits final A/P warrant to Mayor

for approval • Checks – treasurer issues payment to vendor

Preventing Fraud, Waste & Abuse Contract Administration & Auditing

• Independent Audit – annual audit includes review of randomly selected procurement processes and contracts to ensure compliance with M.G.L.’s

• Internal Audit – financial analyst in CFO’s office performs audit of procurement processes and associated contract to ensure compliance with M.G.L.’s and that invoices and payments are made in accordance with contract specifications and proper documentation is complete

• Audit findings shared with CFO, CPO, procurement staff, departmental staff

• Information used to improve as needed

City of Framingham – Purchasing Department Bidshttps://www.framinghamma.gov/bids.aspx

Office of the Inspector General – Procurement Bulletinshttps://www.mass.gov/lists/oig-procurement-bulletins

Department of Labor Standards (DLS) – Prevailing Wage Information https://www.mass.gov/prevailing-wage-program

Division of Capital Asset Management and Maintenance (DCAMM)https://www.mass.gov/orgs/division-of-capital-asset-management-and-maintenance

Information & Resources

United States Department of Labor – Occupational Safety and Health Administrationhttps://www.osha.gov/

Massachusetts Attorney General’s Office – Bid Protest Decision Lookuphttp://www.bpd.ago.state.ma.us/Default.aspx?sectionYear=0&year=2019

Massachusetts School Building Authority – Fuller Middle Schoolhttp://www.massschoolbuildings.org/node/40100

Learn about CM at-riskhttps://www.mass.gov/service-details/learn-about-cm-at-risk

Information & Resources

Thank you for your time!!!

? Questions?

Related Documents