Munib Faiz Khan 1 Islamic Banking System vs. Conventional Banking System

Munib Faiz Khan1 Islamic Banking System vs. Conventional Banking System.

Dec 19, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Munib Faiz Khan 1

Islamic Banking System

vs. Conventional Banking

System

Munib Faiz Khan 2

Presented By

Munib Faiz Khan

M.B.A (b) Mor. 2nd

Semester

Munib Faiz Khan 3

What is Conventional Banking?

More you have, the more you can get.If you have little ornothing, you get nothing.Conventional banking is based on collateral

Munib Faiz Khan 4

Principles of Conventional Banking

Manmade PrinciplesDebtor-creditor relationship Interest

Munib Faiz Khan 5

Services and Products offered by Conventional Banks

Banks are in business to earn a profitProtect customer’s money’s purchasing

powerBanks are regulatedLoansSavings Accounts

Munib Faiz Khan 6

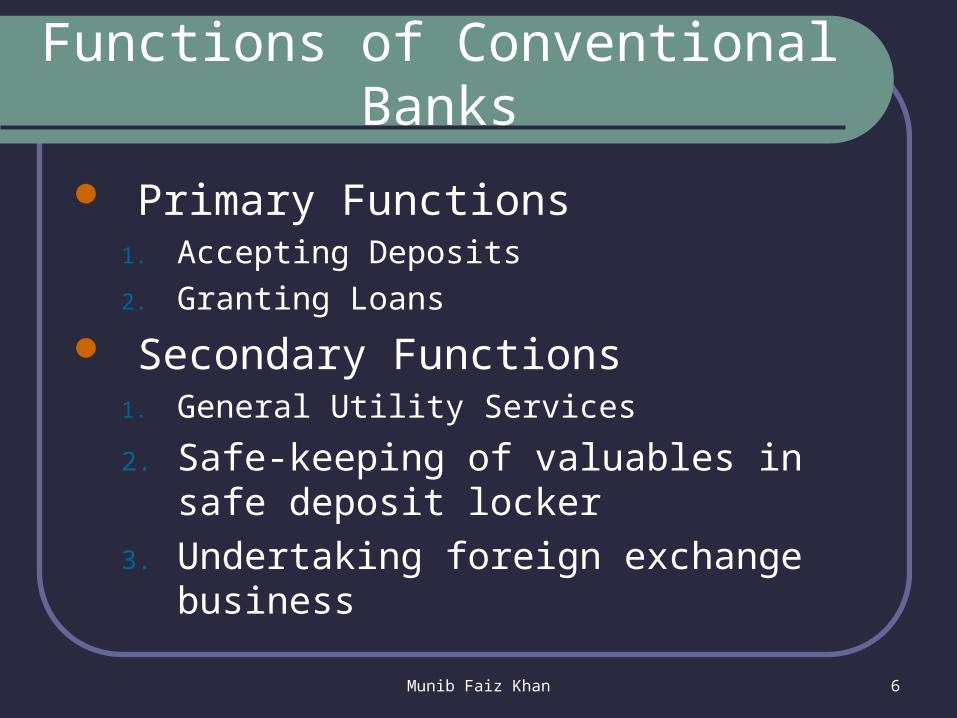

Functions of Conventional Banks

Primary Functions1. Accepting Deposits

2. Granting Loans

Secondary Functions1. General Utility Services

2. Safe-keeping of valuables in safe deposit locker

3. Undertaking foreign exchange business

Munib Faiz Khan 7

Factors which may attract customers

Better products and servicesFinancial position of banksLatest facilitiesInterest on depositsStrong global imageReputation and economic benefits

Munib Faiz Khan 8

Different conventional Banks working in Pakistan

MCBABLUBLBank AlfalahStandard CharteredNBP

Munib Faiz Khan 9

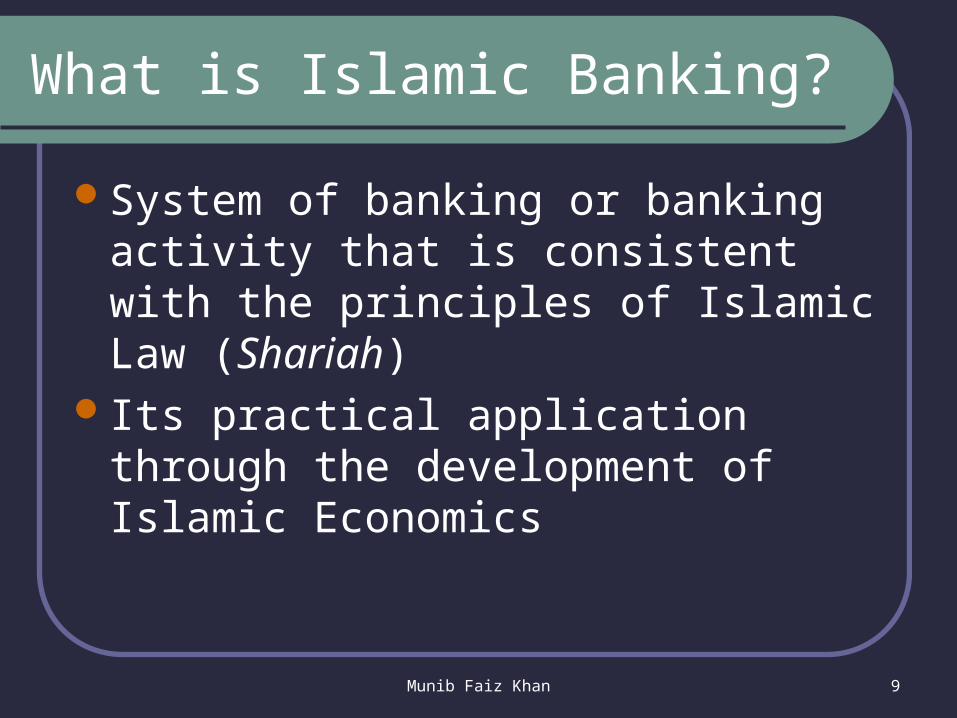

What is Islamic Banking?

System of banking or banking activity that is consistent with the principles of Islamic Law (Shariah)

Its practical application through the development of Islamic Economics

Munib Faiz Khan 10

Islamic Economic System

Primary Objectives of Islamic Economic System

Equal Distribution of MoneySocial Justice

Munib Faiz Khan 11

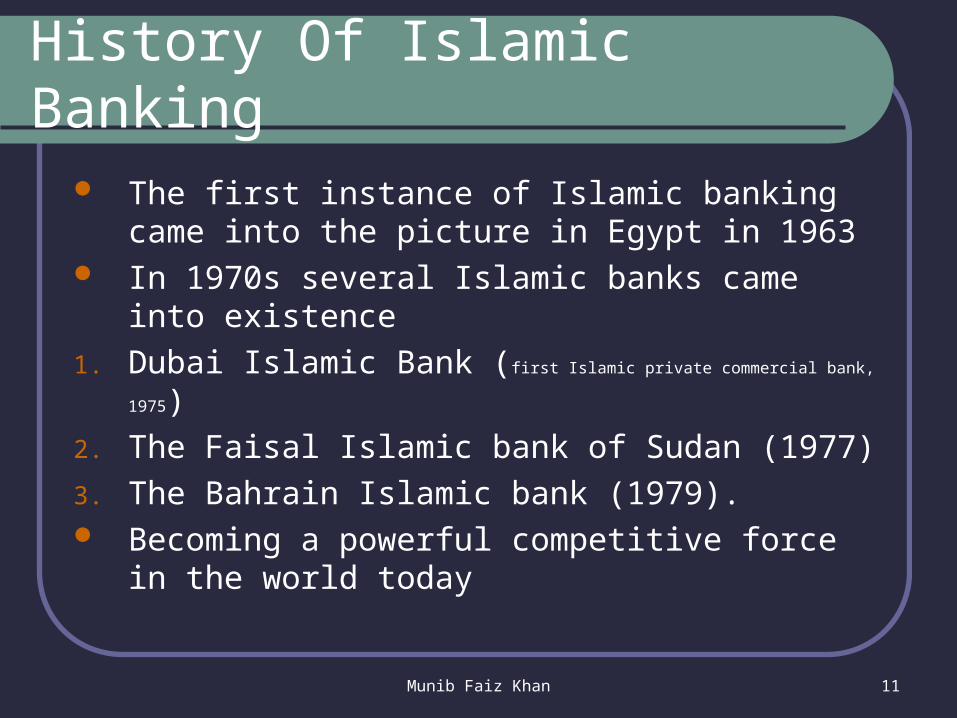

History Of Islamic Banking

The first instance of Islamic banking came into the picture in Egypt in 1963

In 1970s several Islamic banks came into existence

1. Dubai Islamic Bank (first Islamic private commercial bank, 1975)

2. The Faisal Islamic bank of Sudan (1977)

3. The Bahrain Islamic bank (1979). Becoming a powerful competitive force in the

world today

Munib Faiz Khan 12

Principles Of Islamic Banking

Shariah laws and values that comprehensively guide individuals’ in (ritual and non-ritual) life.

Dealings with haram (unlawful) services and commodities, such as gambling, liquors, etc. are prohibited.

Contracts should be based upon profit and risk sharing; and in the forms of buyer

1. Seller (Murabaha), 2. Lessor – leasee (Ijarah),3. Partnership (Musharakah), 4. Debtor – Creditor (qard hasan) relationship.

Munib Faiz Khan 13

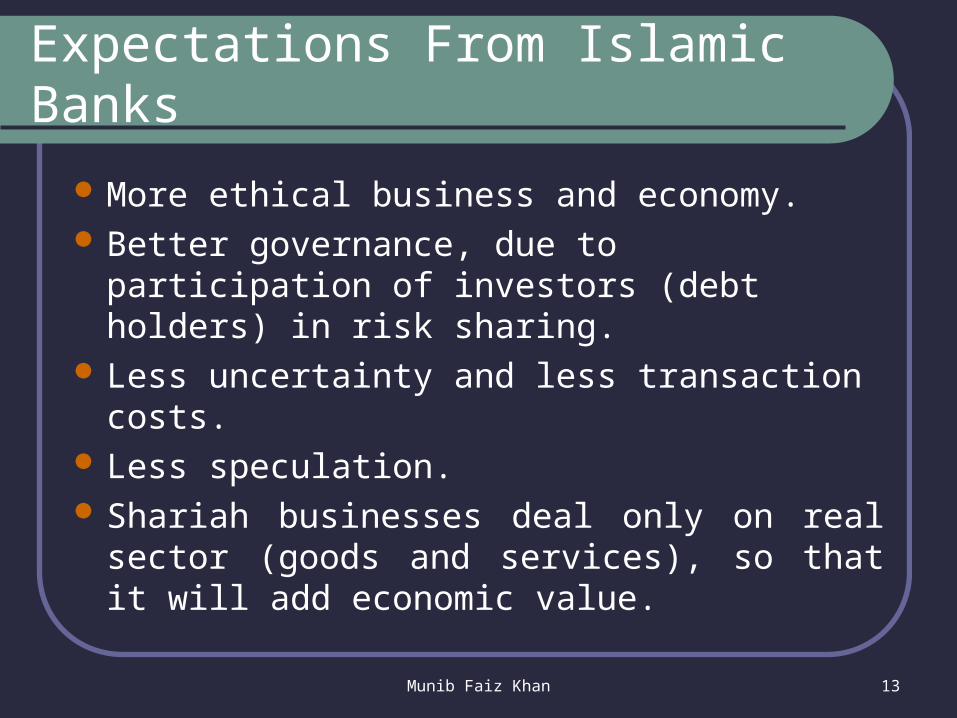

Expectations From Islamic Banks

More ethical business and economy. Better governance, due to participation of

investors (debt holders) in risk sharing. Less uncertainty and less transaction costs. Less speculation. Shariah businesses deal only on real sector

(goods and services), so that it will add economic value.

Munib Faiz Khan 14

Different Islamic Banks Working In Pak

Meezan BankBank Islami Pakistan LimitedDubai Islamic Bank Limited PakistanDawood Islamic Bank LimitedEmirates Global Islamic bank Limited

Munib Faiz Khan 15

Factors Which May Customers in Islamic Banking

Interest free loanFinancial position of bankIslamic teaching and ShariahKnowledge on Islam and religious

environment in the cityFinancial position of bankEconomic benefits and better facilities.

Munib Faiz Khan 16

Services & Products of I.B

Currently available Islamic Banking Products and services are

Partnership based modes of financing Musharakah Finance, Mudarabah Finance, Trade based modes of financing Murabahah Finance, Salam finance Rental based modes of financing Ijarah Finance, Diminishing Musharaka

Finance

Munib Faiz Khan 17

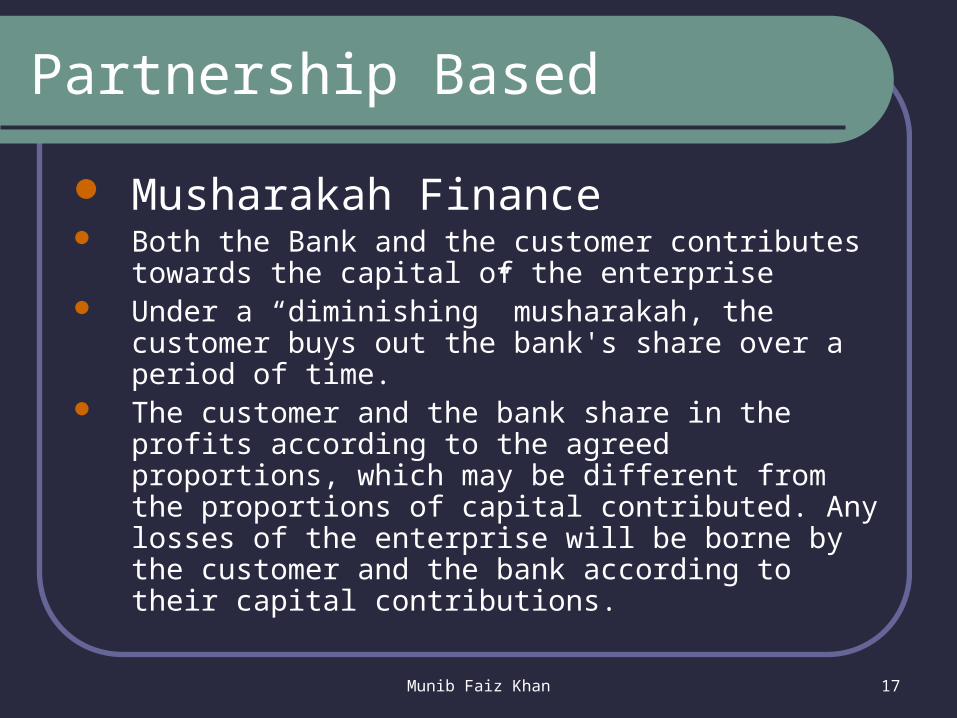

Partnership Based

Musharakah Finance Both the Bank and the customer contributes towards

the capital of the enterprise Under a “diminishing” musharakah, the customer

buys out the bank's share over a period of time. The customer and the bank share in the profits

according to the agreed proportions, which may be different from the proportions of capital contributed. Any losses of the enterprise will be borne by the customer and the bank according to their capital contributions.

Munib Faiz Khan 18

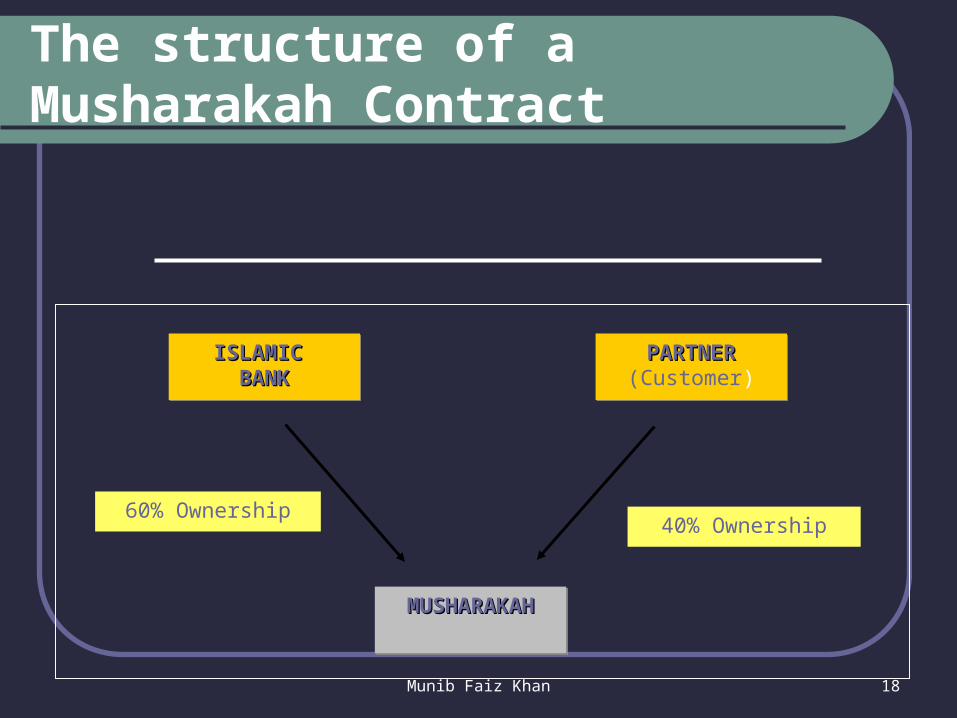

ISLAMIC ISLAMIC BANKBANK

ISLAMIC ISLAMIC BANKBANK

PARTNERPARTNER(Customer)PARTNERPARTNER(Customer)

MUSHARAKAHMUSHARAKAHMUSHARAKAHMUSHARAKAH

60% Ownership40% Ownership

The structure of a Musharakah Contract

Munib Faiz Khan 19

Partnership Based

Mudarbah The bank provides to the customer (mudarib) all the capital to

fund a specified enterprise The customer contributes only entrepreneurship. The customer is responsible for the day to day management of

the enterprise and is entitled to deduct its management fee(mudarib fee) from the enterprise's profits.

The mudarib fee could be a fixed fee (to cover management expenses) and a percentage of the profits or a combination of the two. A classical mudarib fee is based on a percentage of the profits only.

The balance of the profit of the enterprise is payable to the bank If the enterprise makes a loss, the bank (as the fund provider or

Rabbul Mal) has to bear all the losses unless the loss has resulted from negligence on the part of the mudarib.

Munib Faiz Khan 20

Trade Based

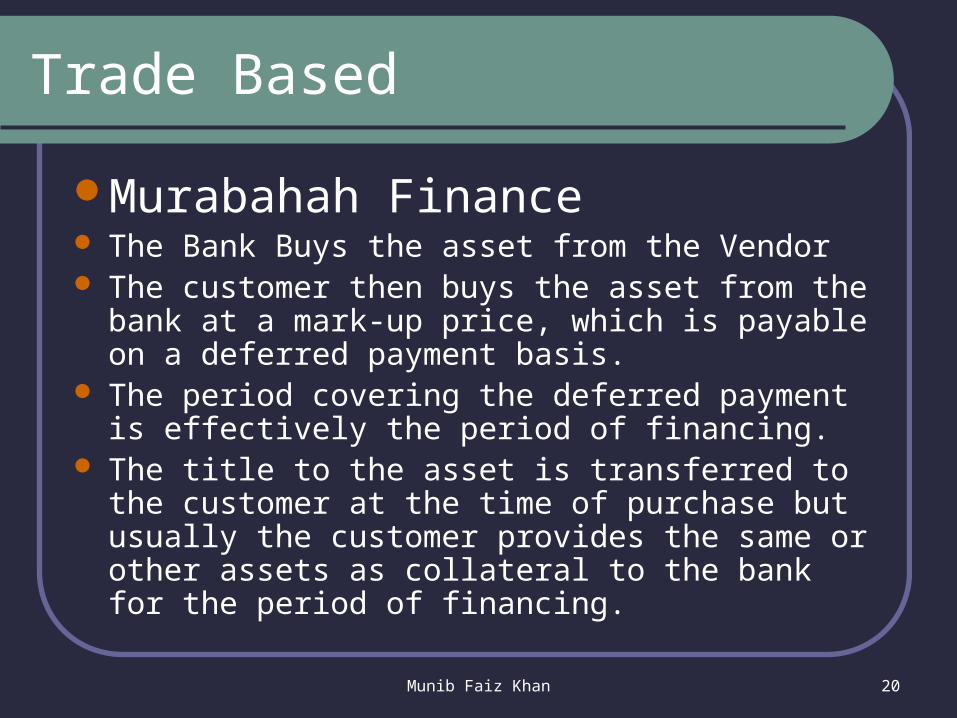

Murabahah Finance The Bank Buys the asset from the Vendor The customer then buys the asset from the bank at a

mark-up price, which is payable on a deferred payment basis.

The period covering the deferred payment is effectively the period of financing.

The title to the asset is transferred to the customer at the time of purchase but usually the customer provides the same or other assets as collateral to the bank for the period of financing.

Munib Faiz Khan 21

Trade Based

Salam Financing A Salam (sometimes referred to as Salaf) is a short

term agreement in which a financial institution makes full pre-payments for future delivery of a specified quantity of goods on a specified date.

A salam is primarily a deferred delivery sale contract usually used for commodity finance. It is similar to a forward contract where delivery is in the future in exchange for spot payment. To mitigate the asset risk a financier can enter into parallel Salam

Munib Faiz Khan 22

Rental Based

Ijarah Finance The bank buys the asset from the vendor The bank then leases the asset to the

customer Periodic rentals are collected by the bank The title of the asset remains with the bank

under as operating Ijarah Title passes to the customer under a Lease

ending with transfer of ownership, either gradually over the period of the contract, at the end.

Munib Faiz Khan 23

DIFFERENCE BETWEEN ISLAMIC AND CONVENTIOANL BANKING

Islamic Banking

1) Functions and operations are based on Shariah principles

Conventional Banking

1)Functions and operations are based on fully man made principles

Munib Faiz Khan 24

DIFFERENCE BETWEEN ISLAMIC AND CONVENTIOANL BANKING

Islamic Banking

2) Promote risk-sharing between provider of capital (investor) and user of funds (entrepreneurs)

Conventional Banking

2) Investor is assured of pre-determined rate of interest

Munib Faiz Khan 25

DIFFERENCE BETWEEN ISLAMIC AND CONVENTIOANL BANKING

Islamic Banking

3) Aim at maximising profit but subject to Shariah restrictions

Conventional Banking

3) Aim at maximising profit without any restrictions

Munib Faiz Khan 26

DIFFERENCE BETWEEN ISLAMIC AND CONVENTIOANL BANKING

Islamic Banking

4) Partners, investor and traders, buyer or seller relationship

Conventional Banking

4) Creditor-Debtor relationship

Munib Faiz Khan 27

DIFFERENCE BETWEEN ISLAMIC AND CONVENTIOANL BANKING

Islamic Banking

5) Encourage asset-based financing and based on commodity trading

Conventional Banking

5) Based on money trading. Money is a medium of exchange and not a commodity, its sale and purchase is prohibited in Islam.

Munib Faiz Khan 28

DIFFERENCE BETWEEN ISLAMIC AND CONVENTIOANL BANKING

Islamic Banking

6) No right of profit if there is no risk involved. The profit and loss sharing depositor may lose money in case of loss.

Conventional Banking

6) It is almost risk free banking and depositor has no risk of losing its money because interest is guaranteed.

Munib Faiz Khan 29

DIFFERENCE BETWEEN ISLAMIC AND CONVENTIOANL BANKING

Islamic Banking

7) one of the service-oriented functions of the Islamic banks to be a Zakat Collection Centre and they also pay out

their Zakat.

Conventional Banking

7) It does not deal with Zakat.

Munib Faiz Khan 30

DIFFERENCE BETWEEN ISLAMIC AND CONVENTIOANL BANKING

Islamic Banking

8) Islamic bank can only guarantee deposits for deposit account, which is based on the principle of al-wadiah, thus the depositors are guaranteed repayment of their funds, however if the account is based on the mudarabah concept, client have to share in a loss position..

Conventional Banking

8) A conventional bank has to guarantee all its deposits.

Munib Faiz Khan 31

Thank You…………!!!!!!

Related Documents