Completing the cycle The buyout market gave a steady performance in 2013 but it was in the exit market that we saw an improved level of return to investors. The value of IPOs and secondary buyouts increased in 2013, but trade sales dropped. 2014 needs the return of the corporate buyer to complete the deal cycle. Multiple Issue 1 2014 Private Equity Transaction Advisory Services

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Completing the cycleThe buyout market gave a steady performance in 2013 but it was in the exit market that we saw an improved level of return to investors.

The value of IPOs and secondary buyouts increased in 2013, but trade sales dropped.

2014 needs the return of the corporate buyer to complete the deal cycle.

Multiple Issue 1 2014

Private Equity Transaction Advisory Services

About MultipleMultiple is a quarterly publication summarizing trends in buyouts* across Europe.

EY and Equistone Partners Europe are proud to sponsor the Centre for Management Buyout Research (CMBOR), whose data is analyzed in Multiple.

The following analysis and commentary is based on research recorded by CMBOR.

Countries covered: Austria, Belgium, Czech Republic, Denmark, Finland, France, Germany, Hungary, Ireland, Italy, Netherlands, Norway, Poland, Portugal, Romania, Spain, Sweden, Switzerland, Turkey and the UK.

*�Buyouts:�CMBOR�defines�buyouts�as�over�50%�of�shares�changing�ownership�with�management�or�private�equity,�or�both having a controlling stake upon deal completion. Equity funding must primarily be from private equity funds and the�bought-out�company�must�have�its�own�financing�structure,�e.g.,�management�buyout�(MBO)�or�management�buy-in (MBI).

For�full�details�on�the�CMBOR�methodology,�please�refer�to�page�15.

Welcom

eMultiple January 2014 | 2

The data in this report was captured on 7 January 2014.

“ The European PE market has seen a sustained recovery over the past year and the outlook�for�2014�is�upbeat�as�confidence�continues�to�grow.�The�total�value�of�exits�has�surpassed�new�deal�values�and�the�IPO�market�has�been�the�real�hero�in�2013.�While secondary buyouts have remained steady, the lack of activity from European corporates has been disappointing.

“ As economic prospects continue to improve, the PE market is clearly making the most of�the�good�conditions�for�exiting�and�returning�capital�to�investors.�However,�it�will�need to be more innovative, looking further afield in its hunt for both new investment opportunities and corporate buyers, if it is to continue to deliver the strong returns it has historically been able to achieve.”Sachin Date, Europe, Middle East, India and Africa (EMEIA) Private Equity Leader, EY

Multiple January 2014 | 3

Contents4 2014 outlook

5 2013 in headlines

6 Pipeline prospects

7 Current conditions

9 Deal dynamics

11 Market watch

12 Country spotlight

16 Contacts

17 Further insights

2014 outlookMegadeal trend will continue• A healthy pipeline suggests there will be an increase in the

number of €1b-plus deals in the coming 12 months.

IPOs will continue to offer viable exit route• A number of portfolio companies are already planning IPOs

for�2014,�as�the�backlog�of�exits�will�continue�to�clear.

Fund-raising will drive more deals• PE houses will be able to raise more funds as investors seek

higher�yields�and�exits�continue,�following�a�successful�fund-raising�year�in�2013.

Non-European investors continue buying spree• US and Asian investors will continue to be attracted to

European assets as economic recovery begins to bed in. That said, the speed of this recovery may differ between the individual economies.

Will European corporates rejoin the market?• The�dearth�of�corporate�buyers�in�the�exit�market�is�arguably�

putting a brake on full recovery, as investors need to be able to�explore�all�avenues�as�they�seek�to�clear�their�portfolio�overhang. While the return of the IPO market is very welcome, corporates�need�to�play�their�part�as�well�in�2014.

IPO activity• 2013�was�a�record�year�for�IPO�by�volume�since�2007�

for some markets. However, many other markets were still�impacted�by�the�financial�crisis.

• Size�matters(ed):�2013�saw�many�visible�and�large�PE-backed IPOs.

IPO markets• Mixed�IPO�weather�conditions�across�EMEIA.

• General sentiment was impacted by monetary policy of ECB/FED,�country�economic�outlooks,�selection�index�levels�and low(est) interest rates.

• There were record highs (i.e., FTSE, DAX) in some EMEIA selection indices and very low volatility (i.e., VDAX, VSTOXX) feed IPO activity despite moments of crisis.

• Investor votes in the EY IPO survey, with regard to country appetite, showed UK and Germany as prime investment locations in EMEIA sectors.

Sectors• 2013�was�the�year�of�real�estate�IPOs.

• In�2014,�the�technology�sector�is�expected�to�make� a comeback.

• A�shift�from�value�to�growth�investments�is�expected�on�the�investor side, as there is much liquidity looking for return by investing and taking more risk appetite IPO activity.

Sustainable in 2014?• Sentiment�has�improved�every�quarter�in�FY13,�with�a�positive�

outlook�for�2014.

IPO market summary

Dr. Martin Steinbach EY IPO Leader EMEIA

Multiple January 2014 | 4

Jan Feb Mar Apr May Jun Jul SepAug Oct Nov Dec

Q1 2013

Deal: Largest UK deal in 2013 (B&M Retail, €1.2b)Exit: One GmbH/Orange €1.3b (trade sale)

Deal: Largest Dutch deal in 2013 (Mediq, €0.8b)Exit: Dematic €0.8b (secondary)

Deal: Largest Italian deal in 2013 (Cerved Business Information, €1.1b)Exit: Esure Insurance €1.4b (IPO)Stat: Retail becomes highest valued sector in Q1 2013 (€3.8b), overtaking manufacturing (€2.8b)

Deal: Largest Norwegian deal in 2013 (Aibel, €1.2b)Exit: Taminco €1b (IPO)

Deal: Largest deal of the month (Cabot Financial, €0.9b, UK) Exit: Constellium €1.4b (IPO)

Deal: Largest Swiss deal in 2013 (Archroma, €0.4b)Exit: The Colomer group €0.5b (trade sale)

Deal: Largest Austrian deal in 2013(AHT Cooling Systems, €0.6b)Exit: Merlin Entertainments €3.8b (IPO)

Deal: Largest Spanish deal in 2013 (Befesa, €1.1b)Largest French deal in 2013 (Allflex, €1b)Exit: Ista €3.1b (secondary)

Deal and exit: Largest German deal and exit in 2013 (Springer Science & Business Media, €3.3b)

Deal: Largest Danish deal in 2013 (Unifeeder, €0.4b)Exit: Stille & Linde/Kion €2.4b (IPO)Stat: European buyout market reaches €21.8b in first half of year

Deal: Largest deal of the month (CeramTec, €1.5b, DE)Exit: Gambro € 3.1b (trade sale)Stat: Refinancings hit highest level (€31.6b) since 2007

Deal: Largest Finnish deal in 2013 (Terveystalo, €0.7b)Exit: Moncler €2.6b (IPO)Stat: IPO market reaches highest value ever (€25b) by end of 2013

Q4 2013Q3 2013Q2 2013

Springer was the largest buyout of 2013• BC Partners agreed to buy Springer Science & Business Media

for�€3.3b�from�EQT�in�a�secondary�buyout�that�was�the�largest�PE-backed acquisition in Germany for seven years.

IPO market returned to life• There�were�some�20�exits�made�through�initial�public�offerings�

(IPOs)�during�the�year,�raising�more�than�€25b�during�the�year,�the�highest�total�value�ever�recorded.�In�2012,�there�was�only one IPO.

Germany claimed the largest buyouts of the year• Out�of�the�nine�€1b-plus�buyout�deals�of�2013,�four�were�

German, while only two were from the UK. The four German deals happened to be the four largest during the year as well.

Lowest level of megadeals since 2009• The�nine�€1b-plus�deals�in�2013�had�a�combined�total�of�just�

under�€15b,�making�2013�the�quietest�year�for�megadeals�since�the�low�of�2009.

Confidence remained fragile, but Eurozone fears abated• The�year�began�with�fears�that�the�financial�crisis�in�Cyprus�

could spread to other Eurozone economies, but such fears proved unfounded as the zone stabilized during the year. Even so, non-Eurozone countries appeared to remain attractive to outside investors.

Post-crisis deals began to exit• By�the�end�of�2013,�seven�of�the�top�20�exits�were�from�

post-2009�deals,�showing�that�PE�has�been�able�to�buy�at�good�prices and weather poor market conditions to grow their assets and�successfully�exit�in�a�three-�to�five-year�period.

2013 in headlines

Rising upAttracting interest

Slow start, but still all to play for

Completing the cycle

Multiple January 2014 | 5

Pipeline€12bfrom 17 deals

Pipeline prospectsThe�2013�recovery�in�the�buyout�market�looks�like�it�will�be�sustained�in�2014.�The�new�year�will�get�off�to�a�strong�start,�with�a�number�of�large�deals�set�to�complete�in�the�first�quarter�of�the�year.�These�include�Scout24,�Germany’s�largest�property�and�dating�portal�owned�by�Deutsche�Telekom,�which�will�be�acquired�by�US�PE�firm�Hellman�&�Friedman�in�a�deal�valued�at�€1.8b�(Bloomberg);�and�3i’s�investment�in�Scandlines,�a�Baltic�Sea�ferry�operator,�valued�at�€1.3b�(3i�press�release).

In�the�UK,�we�will�see�the�completion�of�CVC’s�acquisition�of�domestic�appliance�insurance�group�Domestic�&�General,�with�a�value�of�€750m�(CVC�press�release).�And�US�investor�Corsair’s�acquisition�of�314�RBS�bank�branches�will�see�the�return�of�the�Williams�&�Glynn�bank�brand�when�the�€710m�deal (ft.com) completes.

The�exit�pipelines�also�remain�healthy.�Japan’s�Lixil�and�the�Development�Bank�of�Japan�are�set�to�acquire�bathroom�fitting�maker�Grohe�in�a�€3b�deal.�The�deal�will�mark�the�largest�investment�made�by�a�Japanese�company�in�a�German�rival�(ft.com)�and�provide�an�exit�for�TPG�Capital.

The�deal�pipeline�suggests�the�IPO�exit�route�will�remain�popular.�Companies,�such�as�UK’s�discount�retailer�Poundland,�are�said�to�be�planning�a�flotation�during�2014�(telegraph.co.uk).

Food can maker Mivisa Envases is set to be acquired by US consumer goods packaging manufacturer, Crown�Holdings,�in�a�€1.2b�deal�that�will�see�Blackstone�achieve�an�exit�from�the�company.

“Private�equity�has�entered�2014�feeling�more�optimistic than it has done for a number of years. This optimism partly stems from the reopening of the IPO window.

While�public�listings�have�been�a�viable�exit�route�in�the�US�for�some�18�to�24�months,�it has only been in the last year that IPO investors have begun welcoming new issues from�Europe’s�listed�companies.�PE�has�been�quick to capitalize on this shift in sentiment.”Sachin Date EMEIA Private Equity Leader, EY

Multiple January 2014 | 6

Value and volume down in 2013• With�a�total�value�of�€52.3b,�the�buyout�market�in�2013�was�the�lowest�since�2009,�although�

close�to�matching�2012’s�levels.�It�was�a�similar�story�in�terms�of�volume;�at�539,�the�number�of�deals�was�again�the�lowest�since�2009.�The�figures�were�disappointing�in�the�light�of�a�strong�third�quarter�of�the�year,�with�€20.6b�of�deals,�compared�with�€9.9b�in�the�fourth�quarter.�And�at�121,�the�fourth�quarter�was�the�least�active�in�terms�of�number�since�Q4�2009.

Exits outstrip buyouts• The�value�of�exits�during�2013�surpassed�the�value�of�new�deals�for�the�fourth�year�running,�

suggesting that PE houses are making headway with their backlogs of portfolio companies. In�2013,�there�were�393�exits,�raising�nearly�€76.5b�for�investors.�Secondary�buyouts�raised�the�highest�value�(€30.5b),�while�trade�sales�were�the�most�popular�(175�trade�exits).�The�largest�exit�of�the�year�was�the�flotation�of�Merlin�Entertainments�Group.

• The�exit�hero�in�2013�has�been�the�IPO�—�20�flotations�during�2013�raised�more�than�€25b,�the�highest�ever�value,�and�the�largest�number�since�2007’s�34�IPOs.�This�performance�reflects�the�context�of�the�equity�markets�as�a�whole,�which�returned�to�favor�for�investors�during�2013.�Investors have been able to recognize the underlying quality of assets coming to market at good prices. Such businesses are well run, with transparent governance, and can look to equity investors�for�the�next�stage�of�their�growth.

Germany challenges UK dominance• The�German�buyout�market�saw�€12.1b�of�deals�in�2013,�seriously�challenging�the�UK’s�position�

as�the�largest�buyout�market�by�value�in�Europe�(€16.2b).�However,�by�volume,�the�UK�market�continued�its�dominance,�with�188�deals�during�the�year.�France�was�the�second-busiest�market,�with�96�deals.

Debt rises to the highest ratio since 2007• 2013�marked�the�first�time�that�the�debt�ratio�in�deals�rose�above�50%�since�2007.�In�deals�valued�

at�more�than�€100m,�debt�accounted�for�51%,�while�equity�dropped�to�42%,�the�lowest�since�2007.

Increase in “dry powder”• 2013�saw�an�uptick�in�the�levels�of�“dry�powder”�—�existing�funds�available�at�PE�houses�to�be�

invested.�Buyout�firms�currently�have�more�than�US$391b�in�capital�available�to�fund�new�deals,�up�10%�relative�to�the�end�of�2012.�These�funds�will�need�to�find�a�home�in�2014,�so�could�lead�to an increase in buyout activity or else they could put a brake on further fund-raising activity. Globally,�2013�was�the�best�year�for�PE�fund-raising�since�2008.�Firms�raised�a�collective�US$401b,�well�above�the�US$341b�they�raised�in�2012.

Refinancing value improves• Some�€43.1b�of�debt�was�refinanced�during�2013,�significantly�up�on�the�€24.6b�of�2012,�reflecting�

improving�conditions�in�the�debt�market.�This�refinancing�performance�was�the�best�since�2007,�suggesting�that�the�finance�markets�are�open,�with�banks�racing�to�be�competitive.�However,�one�should�sound�a�note�of�caution,�as�quantitative�easing�tapering�could�have�an�impact�during�2014.

Current conditions

European buyouts — volume and value

Source: CMBOR, Equistone Partners Europe, EY — year 2013 to end Q4 only

Total number Total value (€m)Q

1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q40

50

100

150

200

250

0

5,000

10,000

15,000

20,000

25,000

2010 2011 2012 2013

€m

Tota

l num

ber

Multiple January 2014 | 7

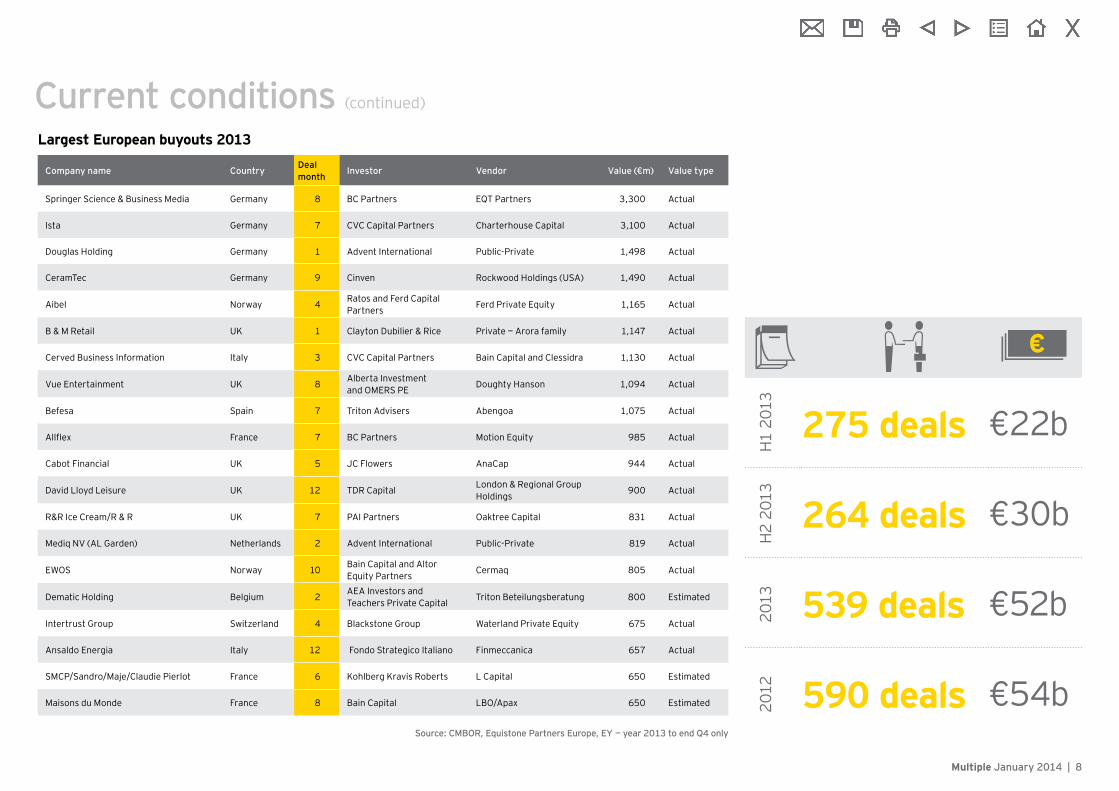

Current conditions (continued)

Company name Country Deal month Investor Vendor Value (€m) Value type

Springer Science & Business Media Germany 8 BC Partners EQT�Partners� 3,300 Actual

Ista Germany 7 CVC Capital Partners Charterhouse Capital 3,100 Actual

Douglas Holding Germany 1 Advent International Public-Private 1,498 Actual

CeramTec Germany 9 Cinven Rockwood Holdings (USA) 1,490 Actual

Aibel Norway 4 Ratos and Ferd Capital Partners Ferd Private Equity 1,165 Actual

B & M Retail UK 1 Clayton Dubilier & Rice Private�—�Arora�family 1,147 Actual

Cerved Business Information Italy 3 CVC Capital Partners Bain Capital and Clessidra 1,130 Actual

Vue Entertainment UK 8 Alberta Investment and OMERS PE Doughty Hanson 1,094 Actual

Befesa Spain 7 Triton Advisers Abengoa 1,075 Actual

Allflex France 7 BC Partners Motion Equity 985 Actual

Cabot Financial UK 5 JC�Flowers� AnaCap 944 Actual

David Lloyd Leisure UK 12 TDR Capital London & Regional Group Holdings 900 Actual

R&R Ice Cream/R & R UK 7 PAI Partners Oaktree Capital 831 Actual

Mediq NV (AL Garden) Netherlands 2 Advent International Public-Private 819 Actual

EWOS Norway 10 Bain Capital and Altor Equity Partners Cermaq 805 Actual

Dematic Holding Belgium 2 AEA Investors and Teachers Private Capital Triton Beteilungsberatung 800 Estimated

Intertrust Group Switzerland 4 Blackstone Group Waterland Private Equity 675 Actual

Ansaldo Energia Italy 12 Fondo Strategico Italiano Finmeccanica 657 Actual

SMCP/Sandro/Maje/Claudie�Pierlot France 6 Kohlberg Kravis Roberts L Capital 650 Estimated

Maisons du Monde France 8 Bain Capital LBO/Apax� 650 Estimated

Source: CMBOR, Equistone Partners Europe, EY — year 2013 to end Q4 only

Largest European buyouts 2013

275 deals €22b

264 deals €30b

539 deals €52b

590 deals €54b

H1�2

013

H2�

2013

2013

2012

Multiple January 2014 | 8

Deal dynamicsBy�value,�secondary�buyouts�remain�significantly�more�popular�than other sources of transactions. This area accounted for nearly�€31.2b�of�deals�during�2013.�Local�divestment�and�private sales were the second and third most popular sources. However,�by�value,�at�€7.9b�and�€6.8b�respectively,�they�were�some way off that of the secondary buyout market.

For�the�first�time�since�2007,�debt�accounted�for�more�than�50%�of�the�deals�in�the�€100m-plus�range.�At�51%,�the�level�of�debt�was�notably�higher�than�the�38.4%�recorded�in�2012.�At�the�same�time,�the�equity�ratio�in�this�bracket�fell�from�59.1%�in�2012�to�42%�in�2013.�Mezzanine�finance�accounted�for�4.5%�of�deal�value�in�2013,�with�loan�note�and�other�financing�making�up�the�remaining�2.5%.

Deal size

2012 2013 Q3 2013 Q4 2013

€1b-plus 13 9 5 0

€500m–€1b 16 16 4 6

€100m–€500m 75 79 20 20

Up�to�€100m 486 435 114 95

Total number of deals 590 539 143 121

“ It was a great year for the credit markets. We saw very healthy banking and capital markets, debt funds continuing to raise substantial sums of capital ready for deployment, retail bond markets continuing to mature, strong structured finance issuance and credit market support mechanisms, such as Funding for Lending, really making their presence felt.

“ With M&A volumes remaining low, most of the transactions we supported in the early part of the year related to growth capital, refinancing and dividend recapitalizations. The dynamic has begun to shift in the last quarter, as corporates use cash and liquidity to seek M&A opportunities.

“�We�are�very�excited�about�2014.�We�believe�credit�markets will remain healthy, with the acquisitions cycle beginning to find swagger. Corporates with a clear credit proposition should find great support�across�the�debt�markets�in�2014.“Chris Lowe, Debt and Capital Advisory Partner, EY, UK

For more information visit ey.com/uk/cdainsights

Mixed story in terms of deal sizesThere�were�133�deals�in�the�mid-market�range�(deals�with�a�value�of�between�€50m�and�€500m)�during�2013,�down�from�146�in�2012,�and�there�were�16�deals�in�the�€500m�to�€1b�bracket,�similar�to�the�volume�of�deals�in�2012.�The�combined�deal�values�for�each�segment�was�broadly�similar�between�2012�and�2103,�suggesting�investors�remained�committed�to�their�involvement in such deals.

The four largest deals were all based in Germany, the largest of which was Springer Science & Business Media. There were no €1b-plus deals in the fourth quarter of the year, although David�Lloyd�Leisure�in�the�UK�was�close,�with�a�value�of�€893m.

Multiple January 2014 | 9

Largest European exits 2013

Company name Country Exit month Vendor Investor Exit value

(€m) Exit type

Merlin Entertainments Group UK 11 Blackstone Group Flotation 3,816 Flotation

Springer Science & Business Media Deutschland Germany 8 EQT�Partners BC Partners 3,300 Secondary

buyout

Ista Germany 7 Charterhouse Capital Partners CVC Capital Partners 3,100 Secondary

buyout

Gambro Sweden 9 Investor AB and EQT�Partners

Baxter�International�Inc�(USA) 3,059 Trade Sale

Numericable/Altice One/Coditel Belgium 11 Cinven Flotation 3,000 Flotation

Moncler Italy 12 Carlyle Group Flotation 2,550 Flotation

Stille & Linde/Kion Germany 6 KKR Flotation 2,392 Flotation

Partnership Assurance/Partnership Group Holdings UK 6 Cinven Flotation 1,802 Flotation

European�Oxo/Oxo�Group/Oxea Germany 12 Advent International Oman Oil company 1,800 Trade Sale

Esure Insurance UK 3 Motion Equity and Penta Capital Partners Flotation 1,398 Flotation

Constellium France 5 Apollo Global Management Flotation 1,380 Flotation

Just�Retirement�(Avalon�Acquisitions) UK 11 Permira Flotation 1,344 Flotation

One GmbH/Orange Austria Telecommunication Austria 1 Mid Europa Partners Hutchinson�3G�(Hong�Kong) 1,300 Trade sale

Aibel Norway 4 Ferd Private Equity Ratos/Ferd Capital 1,165 Secondary buyout

Cerved Business Information Italy 3 Bain Capital and Clessidra CVC Capital Partners 1,130 Secondary buyout

ProSiebenSat1 Media Germany 11 Kohlberg Kravis Roberts and Permira Flotation 1,120 Flotation

Vue Entertainment UK 8 Doughty Hanson Omers PE 1,094 Secondary buyout

Allflex UK 7 Fleming Ventures BC Partners 971 Secondary buyout

Taminco Belgium 4 Apollo Global Management Flotation 963 Flotation

Cabot Financial UK 5 AnaCap JC�Flowers� 944 Secondary buyout

Source: CMBOR, Equistone Partners Europe, EY — year 2013 to end Q4 only

Deal dynamics (continued)

Multiple January 2014 | 10

ManufacturingThe�156�deals�in�the�manufacturing�sector�accounted�for�more�than�€12.5b�of�value�in�2013.�The�year�saw�manufacturing�re-establish�its�position as the most popular sector for PE-backed deals, having slipped behind business and support services�(by�value�if�not�volume)�in�2012.

The largest manufacturing deal of the year was the�foreign�divestment�of�Germany’s�CeramTec,�the global manufacturer of high-performance ceramics,�which�was�valued�at�nearly�€1.5b�when it completed in September. The second-largest manufacturing sector deal was Aibel, the Norwegian oil and gas engineering services supplier, which was acquired in a secondary buyout, with a value of €1.2b.

During�the�year,�104�manufacturing�companies�successfully�completed�an�exit�for�their�investors,�with�a�combined�value�of�more�than�€15.1b.

Business and support services (BSS)As noted earlier, the business and support services sector lost its top position by value to

manufacturing this year, having been the most valuable�sector�in�2012.�During�2013,�77�companies were acquired in buyout deals, with a�combined�value�of�more�than�€9.7b.

The�largest�deal�in�the�sector�during�2013�was�Ista,�the�German�energy�saving�consultancy�—�a�secondary�buyout�valued�at�€3.1b.�The�deal�for Cerved Business Information, the Italian business information database provider, ranked second, with a value of €1.1b.

The�sector�was�also�the�second�largest�for�exits�during�2013,�with�60�companies�being�sold�on�for�a�combined�value�of�€11.3b.

Telecommunications, media and technology (TMT)The TMT sector maintained its position as the third�most�valuable�sector�for�buyouts�in�2013,�with�75�deals�valued�at�€7b.�The�largest�TMT�deal during the year was also the largest deal overall�—�the�€3.3b�Springer�Science�&�Business�Media secondary buyout.

The�sector�was�also�the�third�largest�in�2013�for�exits,�with�a�combined�value�of�nearly�€10b.

Market watchQ4

28 deals €1.8b

2013

156 deals €12.5b

Manufacturing

Q4

20 deals €1.1b

2013

77 deals €9.7b

BSS

Q4

13 deals €0.8b

2013

75 deals €7b

TMT

Q4

9 deals €1b

2013

27 deals €3.3b

Healthcare“�In�terms�of�completed�PE�deals,�activity�in�the�EU�healthcare�sector�for�2013�was�down�compared�with�the�previous�year�and�lower�than�expected.�Trade�players were quite active in the market, a number of the deals took longer to close�than�anticipated,�and�some�processes�that�were�planned�for�2013�have�been�delayed�to�2014.�Having�said�this,�there�is�still�strong�interest�in�the�sector�among�financial�sponsors�and�the�outlook�for�2014�is�more�robust.“Adrian Gibb, Head of Life Sciences and Healthcare Practice, TAS, EY UK&I

Multiple January 2014 | 11

While�remaining�the�most�active�in�Europe�by�value�and�volume,�buyout�activity�in�the�UK�during�2013�was�down�on�the�previous�year.�By�the�end�of�2013,�some�188�deals�had�completed,�with�a�combined�value�of�€16.2b.�This�compares�with�the�206�deals,�valued�at�more�than�€20b,�recorded�in�2012.

The�absence�of�any�€1b-plus�deals�in�the�fourth�quarter�meant�that�the�final�quarter�of�the�year�with�45�deals�at�a�total�value�of�€3.5b,�was�significantly�lower�than�Q4�2012�which�had�a�total�of�50�deals�at�€5.5b.

However, the relative security that sterling offers has ensured that businesses are still attractive to investors, particularly US and Asian, looking to gain a foothold in Europe.

The�UK�market�has�also�led�the�way�for�IPO�exits.�Three�of�the�largest�10�exits�were�UK�based,�and�all�of�them�were�flotations.�The�largest�exit�was�Merlin�Entertainments�Group,�which�raised�€3.8b�in�an�IPO�in�November.

UK Q4: 45 deals €3.5b 2013: 188 deals €16.2b

Country spotlight

Multiple January 2014 | 12

The�German�buyout�market�can�now�be�said�to�performing�as�expected,�vying�with�the�UK�as�the�most�active�market�in�Europe�by�value.�Its�67�deals�during�2013�(2012:�70)�had�a�combined�value�of�€12.1b�(2012:�€8.3b).�However,�this�high�valuation�was�undoubtedly�bolstered�by�a�handful�of�megadeals,�including�Springer�Science�&�Business�Media�(€3.3b),�Ista�(€3.1b),�Douglas�Holding�(€1.5b)�and�CeramTec�(€1.5b).

Any�uncertainty�that�may�have�been�caused�by�the�German�general�election�soon�disappeared,�though�the�majority�of�value�was�achieved�during�the�third�quarter�(€9.1b).�In�comparison,�only�€646m�was�achieved�in�Q4�2013.

Some�€16.5b�was�also�returned�to�investors�through�43�German�exits�during�the�year.�As�well�as�the�secondary�buyouts�at�Springer�and�Ista,�this�total�includes�the�flotation�of�Stille�&�Linde/Kion,�which�raised�€2.4b�for�its�investors.

Germany Q4: 18 deals €646m 2013: 67 deals €12.1b

Country spotlight (continued)

Multiple January 2014 | 13

France’s�total�combined�value�for�2013�was�dragged�down�by�a�slow�fourth�quarter�of�the�year,�when�16�deals�achieved�a�combined�value�of�just�€472m.�However,�France�is�still�Europe’s�third�most�active�buyout�market.�Overall,�it�saw�96�deals�with�a�collective�value�of�€6.6b�during�2013,�compared�with�101�deals�valued�at�€6.3b�in�2012.

The�largest�deal�of�the�year�was�Allflex,�valued�at�€985m.�This�deal�was�one�of�only�four�€500m-plus�deals�completed�during�the�year�and,�for�the�second�year�in�a�row,�the�French�market�failed�to�produce�any�€1b-plus�deals�—�in�2011,�there�were�four�such�deals.

The�slowdown�during�the�fourth�quarter�was�emphasized�by�the�fact�that�the�largest�deal�in�the�final�three�months�of�the�year�was�valued�at�€150m.�The�next�largest�in�the�fourth�quarter�was�Europeene�des�Desserts�(€100m),�followed�by�Carre�Blanc�(€60m).

France Q4: 16 deals €472m 2013: 96 deals €6.6b

Country spotlight (continued)

Multiple January 2014 | 14

CMBOR methodologyThe data only includes the buyout stage of the PE market (management buyout (MBO), management buy-in (MBI), institutional buyout (IBO), buy-in management buyout (BIMBO)) and does not include any other stage, such as seed, start-up, development or expansion�capital.

Unless otherwise stated, the data includes all buyouts, whether PE-backed or not, and there is no size limit to deals recorded.

In�order�to�be�included�as�a�buyout,�over�50%�of�the�issued�share�capital�of�the�company�has�to�change�ownership�with�either�management�or�a�PE�company�or�both�jointly�having�a controlling stake upon deal completion.

Buyouts and buy-ins must be either management led or led by a PE company using equity capital primarily raised from one or more PE funds.

Transactions that are deemed not to adhere to the PE or MBO/MBI model are not included.

Transactions that are funded from other types of funds, such as real estate and infrastructure,�are�not�included.�Deals�in�which�a�PE�firm�buys�property�as�an�investment�are not included.

In order to be included, the target company (the buyout) must have its own separate financing�structure�and�must�not�be�held�as�a�subsidiary�of�a�parent�holding�company�after the buyout.

Firms�that�are�purchased�by�companies�owned�by�a�PE�firm�are�treated�as�acquisitions�and are not included in the buyout statistics. However, these deals are recorded in the “acquisitions by buyout companies” statistics.

All quoted values derive from the total transaction value of the buyout (enterprise value) and include both equity and debt.

The buyout location is the location of the headquarters of the target company, and it is not related to the location of the PE company.

The quarterly data only counts information on transactions that formally close in that quarter, and does not include announced deal information.

Multiple January 2014 | 15

Marketing:Katherine SquierTransaction Advisory Marketing+�44�20�7951�[email protected]

Sachin DateEMEIA Private Equity Leader+�44�20�7951�[email protected]

Country contacts:Marc GunsBelgium+�32�2�774�[email protected]

Peter WellsCentral and Southeast Europe+�420�225�335�[email protected]

Leonid SavelievCommonwealth of Independent States+�7�495�705�[email protected]

Paul GerberFrance +�33�1�55�61�09�[email protected]

Klaus SulzbachGermany, Switzerland and Austria+�49�6196�996�[email protected]

Umberto NobileItaly+�39�028�066�[email protected]

Olivier Coekelbergs Luxembourg +�352�42�124�8424� [email protected]

Maurice van den HoekNetherlands+�31�88�40�[email protected]

Michel ErikssonNordics+�46�8�520�593�[email protected]

Pedro Rodriguez FernandezSpain+�34�915�727�[email protected]

Demet OzdemirTurkey+�90�212�368�[email protected]

Bridget WalshUnited Kingdom and Ireland+�44�20�7951�[email protected]

For more information, please visit ey.com/multiple.

Contacts

Multiple January 2014 | 16

Further insights

Credit Markets 2013–2014Our annual publication providing analysis and opinions�on�credit�markets.�The�first�edition�discusses the issues that have impacted the credit markets�during�2013�and�gives�a�view�on�what�2014�might�bring�for�businesses�navigating�debt�markets and capital providers.

Financing the future energy landscapeOur annual review of global oil and gas transaction activity. In this report, we look at some of the main trends�in�oil�and�gas�deal�activity�over�2013�and�the�outlook�for�transactions�in�the�sector�in�2014.�We analyze the diverse dynamics in the upstream, midstream,�downstream�and�oilfield�services�(OFS)�segments, as well as look at the regional trends that underlie the macroenvironment.

Global Corporate Divestment Study 2014The�2014�Global Divestment Study focuses on how companies review their portfolios and the leading�practices�of�those�that�are�able�to�maximize�divestment outcomes.

2014 APAC PE outlook reportThe APAC PE market is robust, and survey respondents�expect�it�to�stay�strong�in�the�coming year as opportunities abound and credit remains ample.

Capital InsightsHow can companies combine the best traditional business methods with innovative approaches to help shape their destinies?

Global PE CFO surveyOur�inaugural�global�survey�of�PE�chief�financial�officers�finds�widespread�belief�in�near-term�growth and an eagerness to leverage skills forged by the crisis.

View reportView report

View report

View report

View report

View report

View report

Multiple January 2014 | 17

EY��|��Assurance�|�Tax�|�Transactions�|�Advisory

About EYEY�is�a�global�leader�in�assurance,�tax,�transaction�and�advisory�services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

About EY’s Transaction Advisory ServicesHow you manage your capital agenda today will define your competitive position tomorrow. We work with clients to create social and economic value by helping them make better, more informed decisions about strategically managing capital and transactions in fast changing-markets.�Whether�you’re�preserving,�optimizing,�raising�or�investing�capital,�EY’s�Transaction�Advisory�Services�combine�a�unique�set�of�skills,�insight�and�experience�to�deliver�focused�advice.�We�help�you�drive competitive advantage and increased returns through improved decisions across all aspects of your capital agenda.

©�2014�EYGM�Limited.�All Rights Reserved.

EYG�no.�DE0500

EMEIA Marketing Agency 1000696

ED�0115

This material has been prepared for general informational purposes only and is not intended to�be�relied�upon�as�accounting,�tax�or�other�professional�advice.�Please�refer�to�your�advisors�for specific advice.

ey.com/multiple

EY — recognized by mergermarket as top of the European league tables for accountancy advice on transactions in calendar year 2012 and 2013

The views of third parties set out in this publication are not necessarily the views of the global EY�organization�or�its�member�firms.�Moreover,�they�should�be�seen�in�the�context�of�the�time�they were made.

Related Documents