LAPPEENRANTA UNIVERSITY OF TECHNOLOGY Faculty of Technology New Packaging Solutions Tomi Juutilainen Multi-axis solutions in packaging machines in Europe Examiners: Ph.D, Professor Henry Lindell Dr.Sc (Eng), Professor Juha Varis Supervisor: Key Account Support Manager Gert-Jan Nijmolen

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

LAPPEENRANTA UNIVERSITY OF TECHNOLOGY

Faculty of Technology

New Packaging Solutions

Tomi Juutilainen

Multi-axis solutions in packaging machines in Europe

Examiners: Ph.D, Professor Henry Lindell

Dr.Sc (Eng), Professor Juha Varis

Supervisor: Key Account Support Manager Gert-Jan Nijmolen

TIIVISTELMÄ

Lappeenrannan teknillinen yliopisto

Teknillinen tiedekunta

New Packaging Solutions

Tomi Juutilainen

Multi-axis solutions in packaging machines in Europe

Diplomityö

2013

87 sivua, 27 kuvaa, 8 taulukkoa ja 10 liitettä

Tarkastajat: Professori Henry Lindell

Professori Juha Varis

Hakusanat: Automaatio, liikkeenohjaus, moniakselikäyttö, pakkauskone

Työn tarkoituksena oli selvittää moniakselisovellusten markkinapotentiaali Euroopassa

valmistetuissa pakkauskoneissa. Tässä tutkimuksessa moniakselisovellus tarkoittaa

kokoonpanoa, missä tehonsyöttö on toteutettu DC syöttösillalla eri akseliohjaimille ja

ohjausäly on keskitetty yhteen muita ohjaavaan yksikköön. Markkinapotentiaalin

selvitykseen käytettiin pakkauskoneautomaatiotutkimusta. Tutkimus tarkastelee

Euroopassa myytyjen ja valmistettujen pakkauskoneiden kustannusrakennetta

tuoteryhmittäin. Tuoteryhmien tarkempaa erittelyä ja moniakselisovellusten suhdeluvun

löytämistä varten käytettiin arviointia sekä globaalia liikkeenohjaustutkimusta.

Moniakselisovellusten suhdeluvulla pystyttiin arvioimaan missä maassa ja

pakkauskonesektorissa on suurin markkinapotentiaali. Tutkimusten lisäksi

pakkausalalle suunnatuilla yrityshaastatteluilla pyrittiin keräämään tietoa

pakkauskoneiden nykytilanteesta sekä mahdollisista kehityssuuntauksista.

Suurimmat markkinapotentiaalit löytyvät Saksasta ja Italiasta, mitkä ovat suurimmat

pakkauskonevalmistajat Euroopassa. Merkittävintä kasvua Euroopan alueella seuraavan

2-3 vuoden aikana ilmenee Turkissa, missä vuosittainen kasvu pakkausteollisuudessa on

lähes samalla tasolla kuin keskimääräinen koneenrakennuksen kasvu Aasiassa.

Pohjoismaista suurin markkinapotentiaali on Ruotsissa, mikä ylsi 35 sijalle vertailussa.

Yrityshaastattelujen perusteella automaatiokomponentit tulevat lähivuosina pysymään

saman tehoisina, eikä akselimäärissä ole näkyvissä muutosta. Integroidut

koneturvallisuusominaisuudet yhdessä universaalin ohjelmiston kanssa olivat

merkittävimmät suuntaukset. Toisin kuin yleisesti teollisuudessa, pakkauskoneiden

energiansäästötavoitteet ovat ja tulevat olemaan matalalla tasolla seuraavina vuosina.

ABSTRACT

Lappeenranta University Of Technology

Faculty of Technology

New Packaging Solutions

Tomi Juutilainen

Multi-axis solutions in packaging machines in Europe

Master’s thesis

2013

87 pages, 27 pictures, 8 tables and 10 attachments

Examiners: Ph.D, Professor Henry Lindell

Dr.Sc (Eng), Professor Juha Varis

Key words: Automation, motion control, multi-axis solution, packaging machine

The objective of this thesis was to examine the potential of multi-axis solutions in

packaging machines produced in Europe. The definition of a multi-axis solution in this

study is a construction that uses a common DC bus power supply for different

amplifiers running the axes and the intelligence is centralized into one unit. The cost

structure of a packaging machine was gained from an automation research, which

divided the machines according to automation categories. The automation categories

were then further divided into different sub-components by evaluating the ratio of

multi-axis solutions compared to other automation components in packaging machines.

A global motion control study was used for further information. With the help of the

ratio, an estimation of the potential of multi-axis solutions in each country and

packaging machine sector was completed. In addition to the research, a specific

questionnaire was sent to five companies to gain information about the present situation

and possible trends in packaging machinery.

The greatest potential markets are in Germany and Italy, which are also the largest

producers of packaging machinery in Europe. The greatest growth in the next few years

will be seen in Turkey where the annual growth rate equals the general machinery

production rate in Asia. The greatest market potential of the Nordic countries is found in

Sweden in 35th position on the list. According to the interviews, motion control

products in packaging machines will retain their current power levels, as well as the

number of axes in the future. Integrated machine safety features together with a

universal programming language are the desired attributes of the future. Unlike

generally in industry, the energy saving objectives are and will remain insignificant in

the packaging industry.

PREFACE

The project has finally come to an end. First of all, I want to thank my supervisor Gert-

Jan Nijmolen, Professors Henry Lindell and Juha Varis who made the project run

smoothly. Secondly, I want to give thanks to my closest friends and to my employer

who supported me during the whole project. I have to say that the schedule was

extremely tight because of working parallel to this project but I’m satisfied with the

results. Now it is time to ease up for a while before the next project.

.

CONTENTS

1. Introduction ............................................................................................................ 10

1.1 Packages and packaging ............................................................................................... 12

1.1.1 General properties of a package ............................................................................................ 13

1.1.2 Package information and appearance ................................................................................... 13

1.2 Packaging lines and machines ......................................................................................... 15

1.2.1 Selection criteria ..................................................................................................................... 16

1.3 Grouping of packaging machines .................................................................................... 19

1.4 Machine safety and standards ......................................................................................... 21

1.4.1 Standards and Directives in machinery ................................................................................. 21

1.4.2.1 The Machinery Directive .................................................................................................. 22

1.4.2.2 Essential Health & Safety Requirements .......................................................................... 23

1.4.3 CEN ......................................................................................................................................... 24

1.4.4 EN standards .......................................................................................................................... 25

1.4.5 EN Harmonized European Standards ................................................................................... 26

1.4.6 Safety standards in packaging machinery ............................................................................. 26

1.5 Global markets for servo systems – Motion control ...................................................... 28

1.5.1 Global revenues for motion control products ........................................................................ 28

1.5.2 EMEA ..................................................................................................................................... 29

1.5.3 APAC ...................................................................................................................................... 30

1.5.4 America ................................................................................................................................... 30

1.5.4 Japan ....................................................................................................................................... 31

1.5.6 Fluctuations in motion control ............................................................................................... 32

1.5.7 Packaging machinery in motion control ................................................................................ 34

1.6 Packaging machinery in EMEA and Europe ................................................................. 35

1.6.1 Definitions for macroeconomic indicators ............................................................................. 36

1.6.2 Definitions for end-user indicators ........................................................................................ 36

1.6.3 Trends influencing the markets ............................................................................................. 37

1.7 EMEA markets in packaging machinery ....................................................................... 39

1.7.1 Packaging machinery markets in EMEA by country ........................................................... 40

1.8 Automation in Packaging Machinery in Europe and EMEA ....................................... 41

1.8.1 Typical automation components ............................................................................................ 42

1.8.1.1 PLC – Programmable Logic Controller ............................................................................ 43

1.8.1.2 Motor drives..................................................................................................................... 43

1.8.1.3 Visualization components ................................................................................................ 44

1.8.1.4 Motion control ................................................................................................................. 45

1.8.1.5 Other automation products ............................................................................................... 47

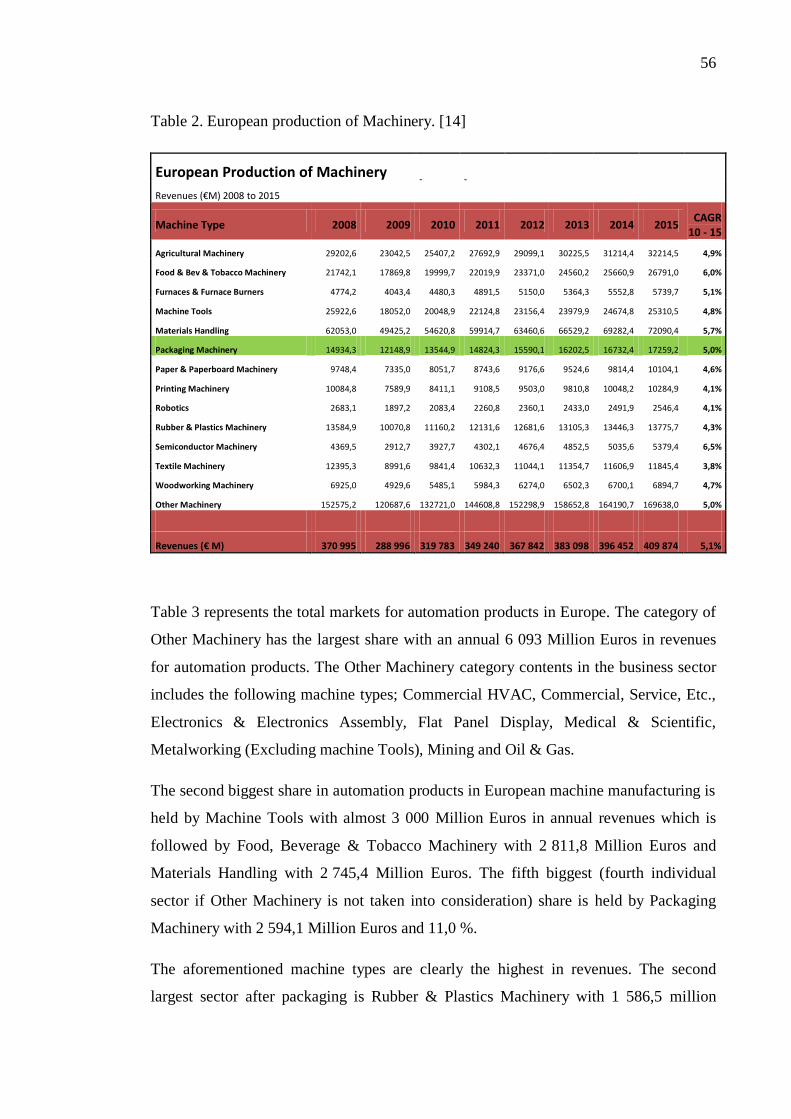

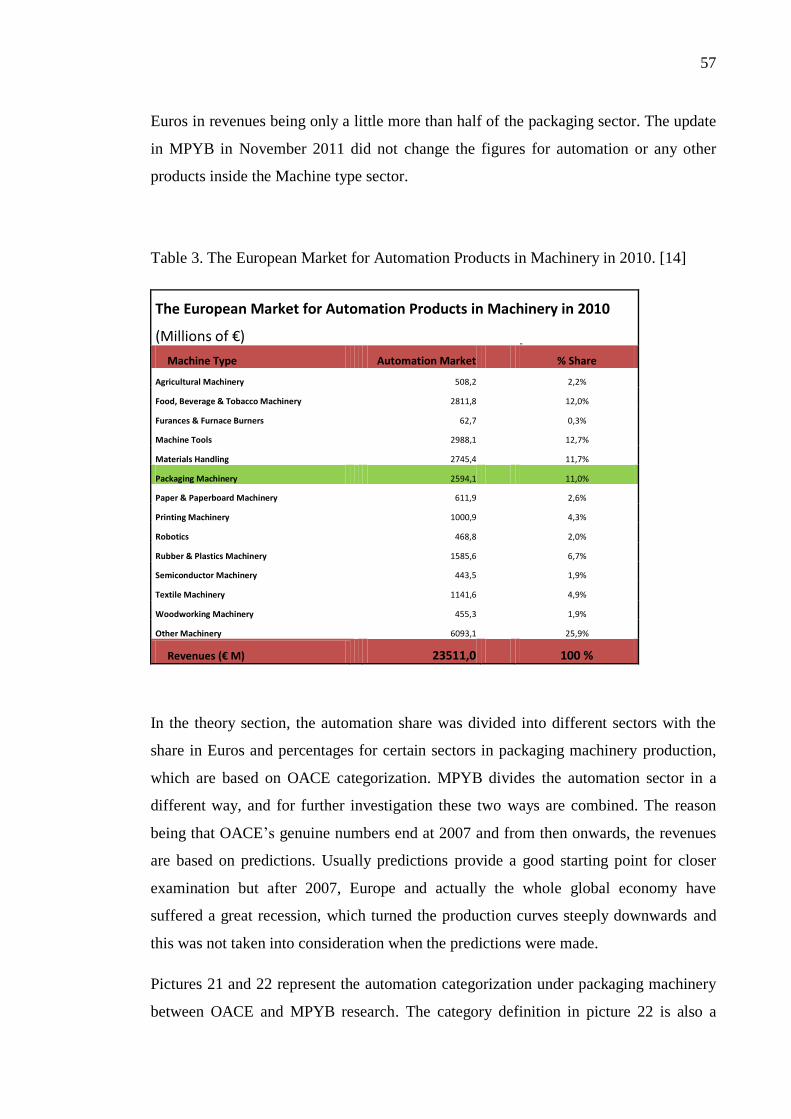

1.9 Cost structure of a packaging machine produced in EMEA......................................... 48

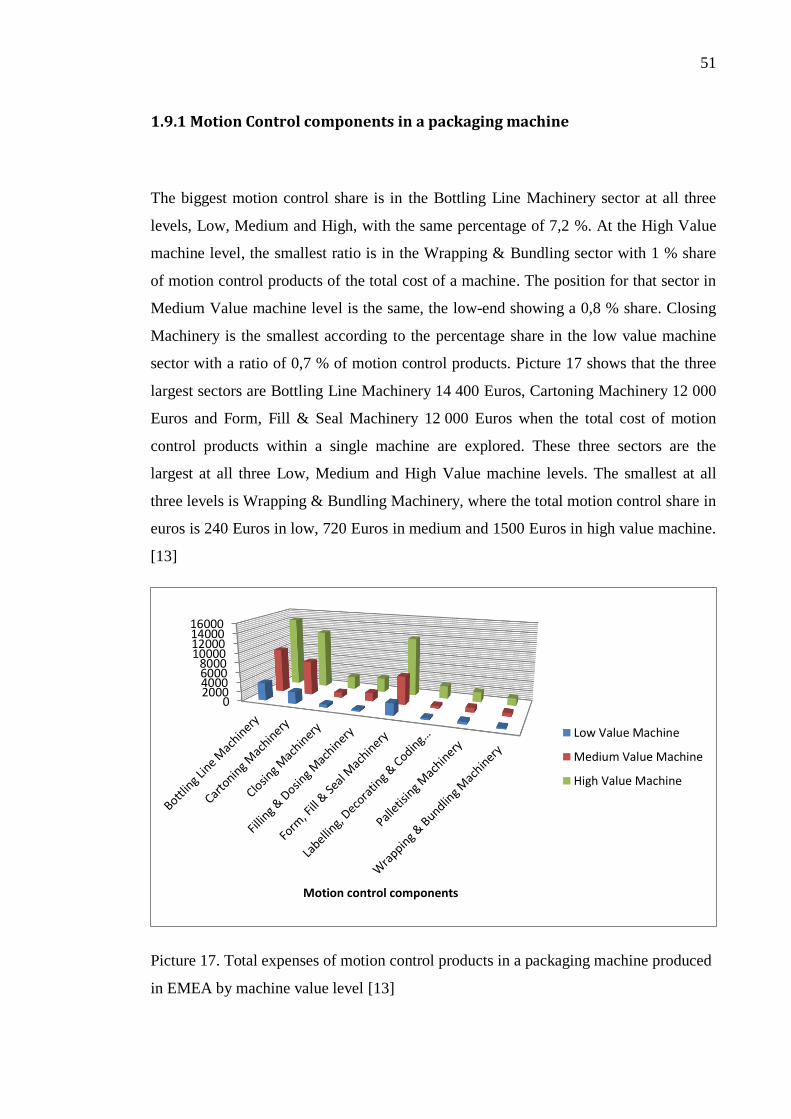

1.9.1 Motion Control components in a packaging machine ........................................................... 51

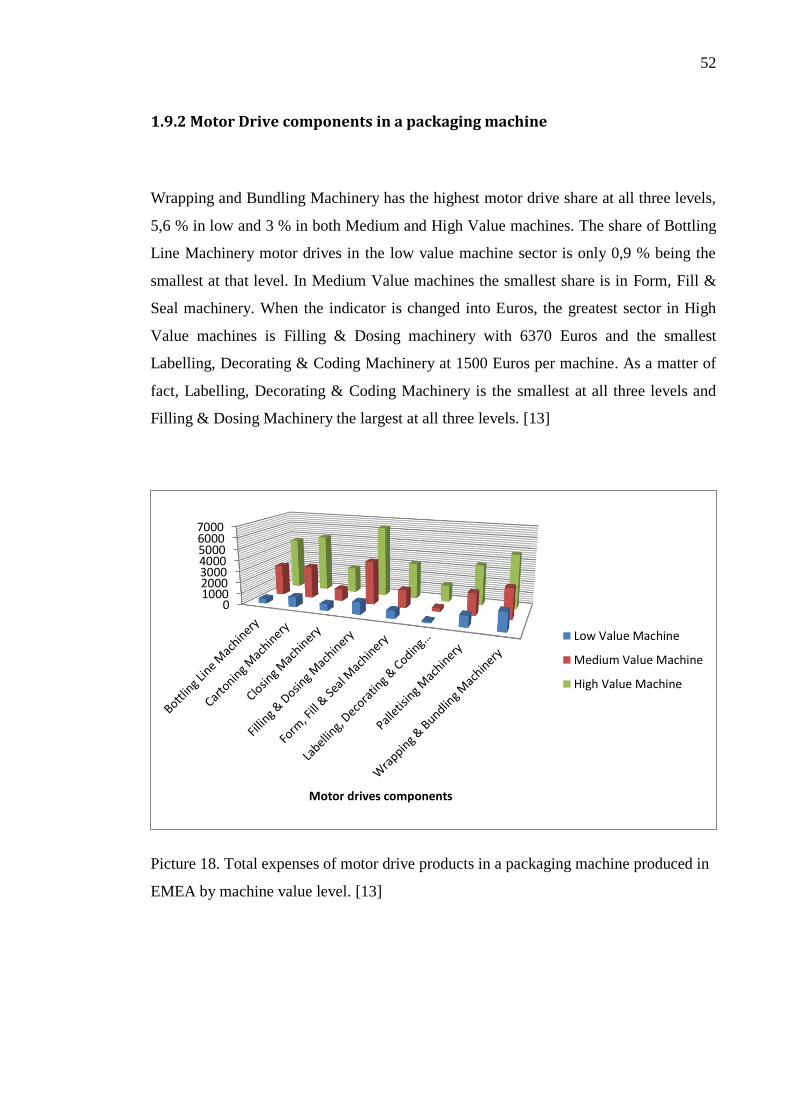

1.9.2 Motor Drive components in a packaging machine ................................................................ 52

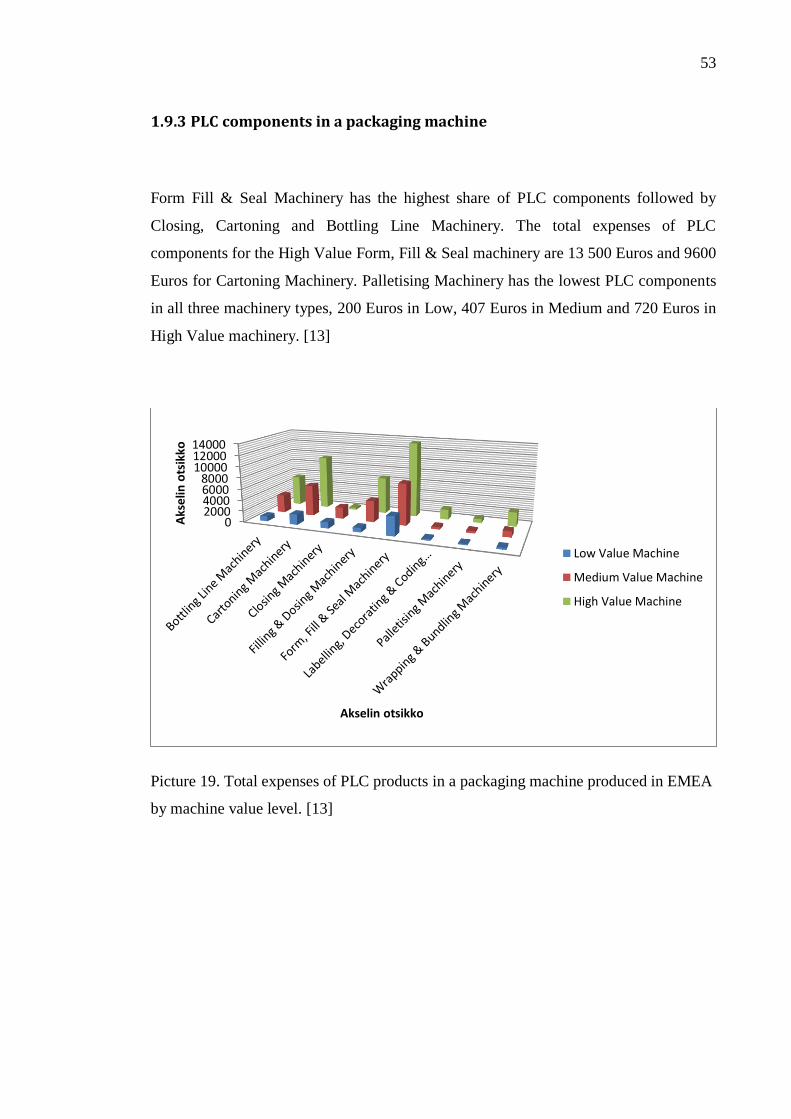

1.9.3 PLC components in a packaging machine ............................................................................. 53

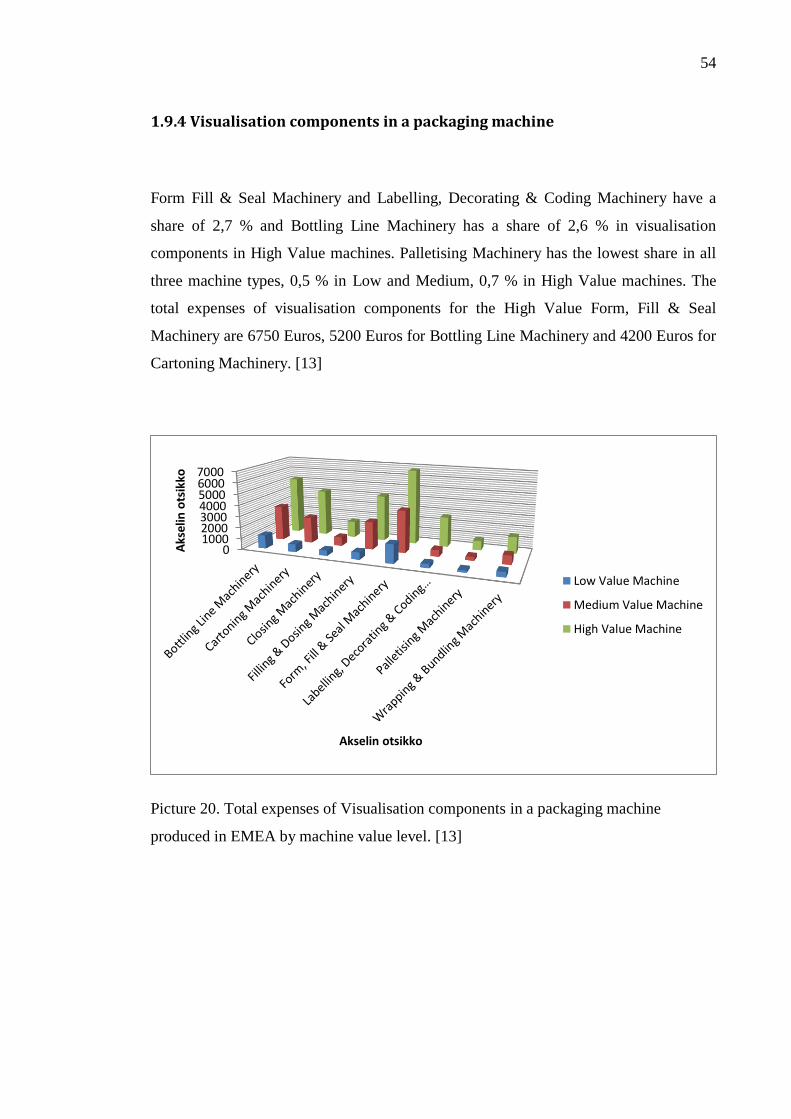

1.9.4 Visualisation components in a packaging machine ............................................................... 54

2. Methodology............................................................................................................ 55

2.1 Research on the potential market share for multi-axis solutions in packaging

machinery in Europe ............................................................................................................. 55

2.2 The combination of the studies ........................................................................................ 60

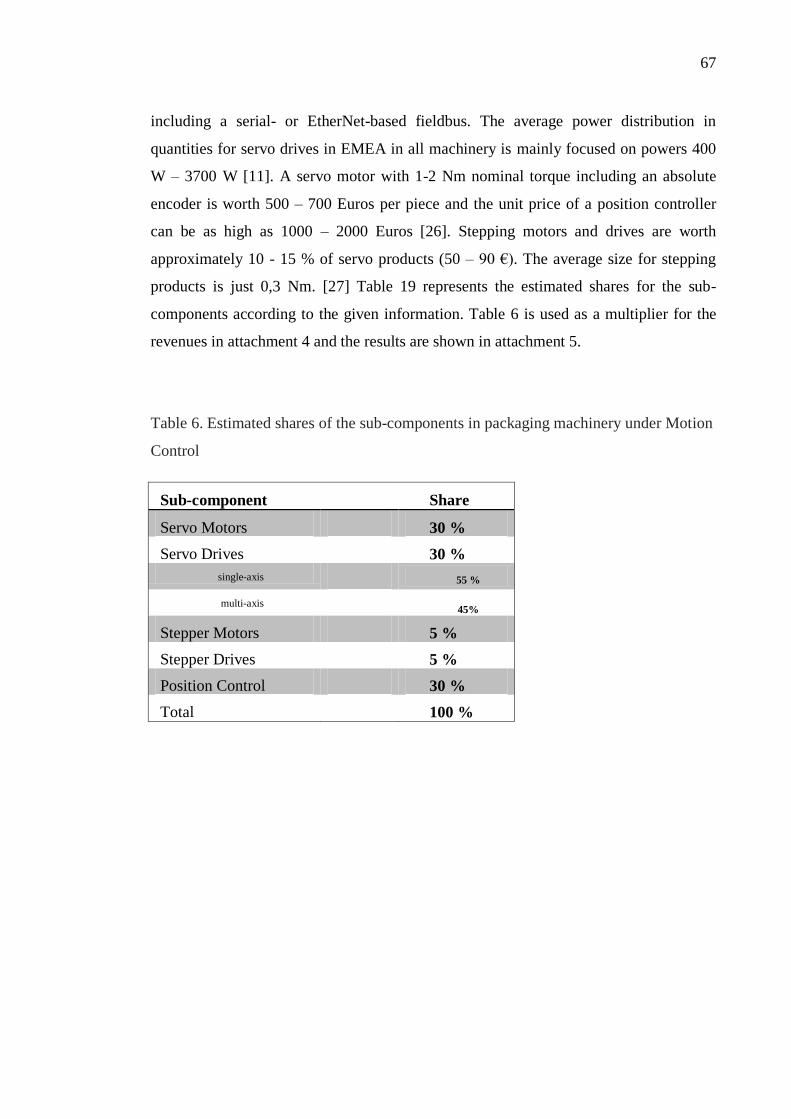

2.2 Company Interviews ........................................................................................................ 68

2.2.1 The current situation .............................................................................................................. 69

2.2.1.1 Questions related to the current solution ........................................................................... 69

2.2.2 Future...................................................................................................................................... 70

2.2.2.1 Questions related to future solutions ................................................................................. 71

2.3 ABB Italy Interview ......................................................................................................... 72

2.3.1 Questions for ABB Italy ...................................................................................................... 72

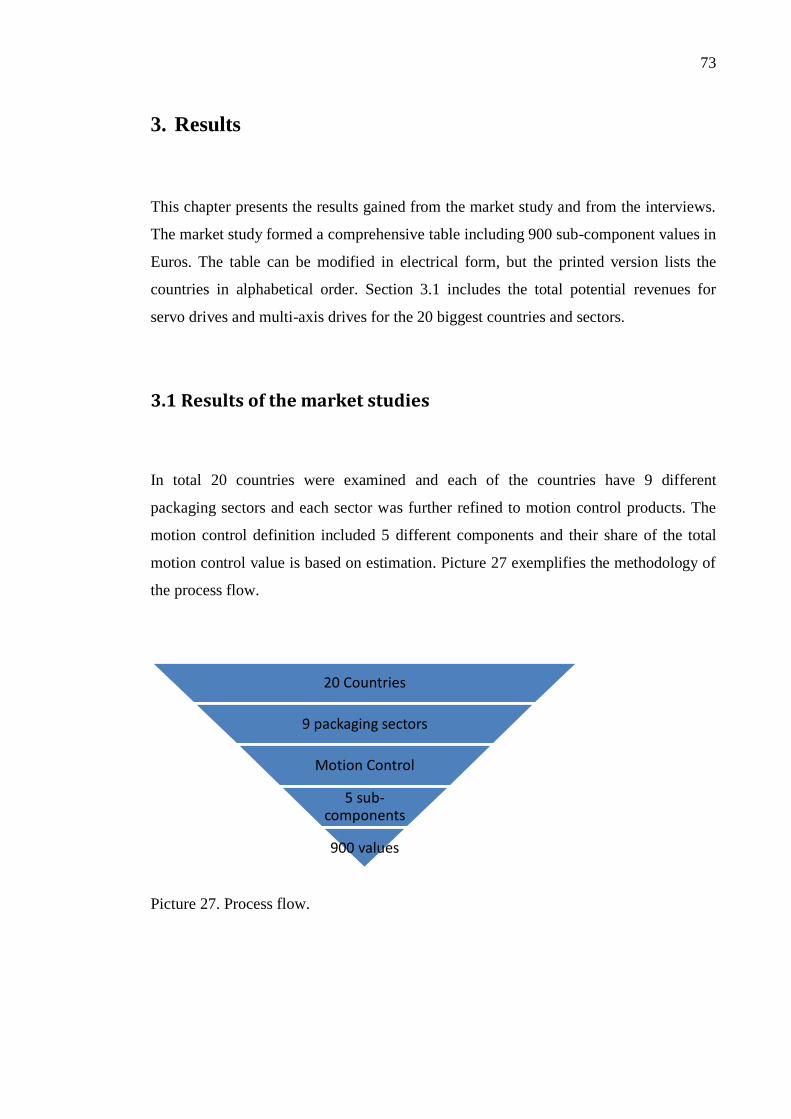

3. Results...................................................................................................................... 73

3.1 Results of the market studies ........................................................................................... 73

3.2 Results of the interviews .................................................................................................. 77

3.2.1 Present concept ....................................................................................................................... 77

3.2.2 Future concept ........................................................................................................................ 78

3.3 Results from ABB Italy .................................................................................................... 79

4. Analysis ...................................................................................................................... 81

5. Discussion and conclusions ....................................................................................... 83

REFERENCES .............................................................................................................. 86

ATTACHMENTS ......................................................................................................1-10

Abbreviations

AC Alternating Current

APAC Asia Pacific

CAGR Compound Annual Growth Rate

CAM Rotating piece in a mechanical linkage

CEN European Committee for Standardization

CENELEC European Committee for Electrotechnical Standardization

CNC Computerized Numerical Control

CPU Central Processing Unit

DC Direct Current

EEA European Economic Area

EHSR Essential Health and Safety Requirements

EMEA Europe, Midde East & Africa

EN European Standard

EU European Union

FFS Form-fill-seal

GMC General Motion Control

HMI Human Machine Interface

HVAC Heating, Ventilation and Air Conditioning

IMS Electronics Market Research & Consultancy

IP Ingress Protection Rating

ISO International Organization for Standardization

I/O Input/Output

MPYB The Machine Builders Year Book – Europe

PET Polyethylene Terephthalate

PLC Programmable Logic Controller

OACE Opportunities for Automation Companies in the EMEA Packaging

Machinery Industry

OEM Original Equipment Manufacturer

ROI Return Of Investment

STO Safe Torque Off

V Volt

VFFS Vertical-form-fill-seal

W Watt

10

1. Introduction

Our community is developing fast and the changing lifestyles of consumers are pushing

the machine manufacturers into a position where a wide and rapidly expanding range of

products need to be packed. The growth is fastest in regions where the standard of

living is at a lower level. Asia, Africa and Southern America are the greatest growth

areas in the industry, including packaging machinery. Nevertheless, this study only

focuses on Europe, as Europe is still the biggest region producing packaging machinery.

The Packaging industry is a very complicated field with multiple angles, which sets

challenges for all working in the area. The aim of this study was to find out the potential

market share of multi-axis solutions of the European packaging industry. The multi-axis

solution is not just a single component; it consists of various intricate parts. The most

challenging point of this study is that at the moment ABB is a not a major global player

in the packaging machinery automation and as a result lacks application specific

offering and solution knowledge. Multi-axis solutions are characterized by a common

DC bus for several drives which are fed from a single rectifier. A multi-axis solution is

a cost effective package for many reasons, for example it is very compact due to its

small size, energy saving due to the possibility of power sharing and cost effective due

to its modifiable structure. The ABB product range covers almost every industrial field

but the business in packaging automation is at a very low level. The result of the study

provides targets for ABB staff both in component designing and in business planning

for the sales organization.

In Europe, the markets and industries are growing steadily with annual rates of a few

percent while simultaneously the less developed countries are reaching massive, almost

triple growth rates. Despite this, the markets in Europe are very interesting; the average

unit price in motion control products is raising and packaging machinery is one of the

largest motion control product users. This study also gives an overview of the present

markets globally in the field of motion control products. After exemplifying how the

markets are spread globally and how they are developing in different regions, the focus

is moved to the packaging field in Europe. The general data of motion control markets

11

is collected from the latest Motion Control IMS research, which examines the subject

from a global perspective. The data for packaging machinery markets is collected from

two surveys, which were the Opportunities for Automation Companies in the EMEA

Packaging Machinery Industry and The Machine Builders Year Book – Europe. The

survey focusing on automation was carried out in 2008 which was just before the global

recession started at the end of 2008. The other survey, The Machine Builder Year Book

was published at the beginning of 2011 and updated in November 2011. The Machine

Builder Year Book did not define the packaging machinery as precisely as the

Opportunities for Automation Companies in EMEA, and therefore these two surveys

were combined to gain a more in-depth understanding. The categorization for the

component definition was taken from the Opportunities for Automation Companies in

EMEA and the revenues from The Machine Builder Year Book. However, neither of

these studies evaluated the market share of multi-axis solutions. The combination of the

two aforementioned studies was not enough to determine the potential revenues for

multi-axis solutions, and therefore the motion control study was used to gain as precise

information as possible of the potential market share in packaging machinery. The

Motion Control World 2011, which examines machinery production on a larger scale,

reports that the packaging machinery sector is one of the greatest motion control

product users worldwide. As multi-axis solutions are listed under motion control, the

data could be applied from that study. After acquiring a large amount of information

from different sources, an estimation of the potential of multi-axis solutions in European

packaging machinery was attained. The results are depicted on rewritable Excel sheets

that can be modified by analyzing and modifying the possible shares for different

components listed under motion control.

The second part of the study was completed through interviewing companies working in

the packaging industry. Four of the interviewed companies’ core business is to build

packaging machines. Three of them were from Finland and one from Italy. Three of the

four Finnish companies export their machines worldwide and the remaining company

mainly focuses on automation design in their local market. The questionnaire was

divided into two sections, where the first part handled the present situation and the

second part included questions about the future. In total 30 questions were presented to

12

the interviewees. The questions, composed in collaboration with ABB staff, were

designed to release as much useful data as possible.

1.1 Packages and packaging

Packages and packaging machinery cover a range of subjects including regulation,

directives, standards, automation and mechanics amongst other things. The primary

function of a package is to protect the packaged product from environmental harm.

However, today in addition to the primary function there are many other important

issues that a modern package has to provide for. With the requirement that a package

has to carry multiple integrated features, a packaging machine has to be able to form the

desired package in a very short time and to a high standard of quality. It is common that

a single packaging machine high in accuracy and speed needs to be integrated into the

whole packaging line. A packaging line can consist of multiple packaging machines.

Almost everything is packaged, which results in the range of packages and packaging

machinery being extensive.

The packaging industry is an interdisciplinary field of study combining art, science and

technology in the materials and machines that are used. The user group of packages is

wide, for almost every single person and company use specific packages. There are

packages for consumers and companies and both are divided into several sectors with a

very different nature in products as well as packages. Each type of package needs a

customized packaging line which sets challenges for both the companies whose core

business it is to sell products including the packaging transaction and for the companies

who are manufacturing packaging lines. [1]

13

There are certain criteria that need to be met in order to produce a functional package.

To fulfill the criteria of a functional package it has to: [1]

Protect the product from the environment

Protect the environment from the packaged product

Maintain the given feature of a product

Enable highly efficient production and distribution

Improve the hygiene and security of the user and consumer

Report facts about the product, production, manufacturing company and recycling

Be as efficient as possible in saving energy and space in transportation

Be as efficient as possible in production costs

1.1.1 General properties of a package

The packaged product has to be protected against physical, chemical and biological

stresses. During the packaging process and transportation the package is under stress

which sets requirements for a package to handle vibrations, shocks, moisture, dust and

pressing. In foodstuff packaging the main threats to avoid are light and oxygen which

can be listed under chemical stresses. With the right packaging selection, biological

stresses such as pests, odors and flavors to the packaged product can be prevented.

Protection also acts as proof of the origin and quality of a packaged product because a

consumer can be mislead to buy a fake, broken or spoiled product. Many packages are

designed to be suitable, not just for the packaged product, but also with certain

dimensions and structures in mind, so that the package itself can be further packaged

into a transportation package with high efficiency in space. [1]

1.1.2 Package information and appearance

Different sectors have their own decrees in package labelling. For example, foodstuff

package labelling is different to the ones used in cosmetic packages. Usually the labels

14

include information about product preservation, best before dates, usage and

maintenance instructions and other critical information. The information in package

labelling is useful not just for the end users but also for the packaging chain parties who

transport and sell the packages. Product usability information means multiple things,

two of which can be regarded as being high in value: the use of the packaged product

and the further recycling of the package. An environmentally friendly and safe package

guarantees that products or packages are disposed of correctly and ensures that there is

enough information for users not to harm themselves or the environment. [1]

The package has to be attractive enough, and give signals about the product to gain the

attention of consumers in order for them to buy it. A well-designed outward appearance

of a package is a great advertisement in image forming and promotes sales. The

possibilities in design are very broad nowadays because of the fast evolution in

techniques. Packaging companies spend vast amounts of money and time on designing a

package that is suitable, stylish and manufactured according to legislation. A consumer

easily recognizes a suitable product if the package provides a clear appearance with

certain symbols, branch marks or even slogans or any kind of signs with which the

product can be identified [1].

15

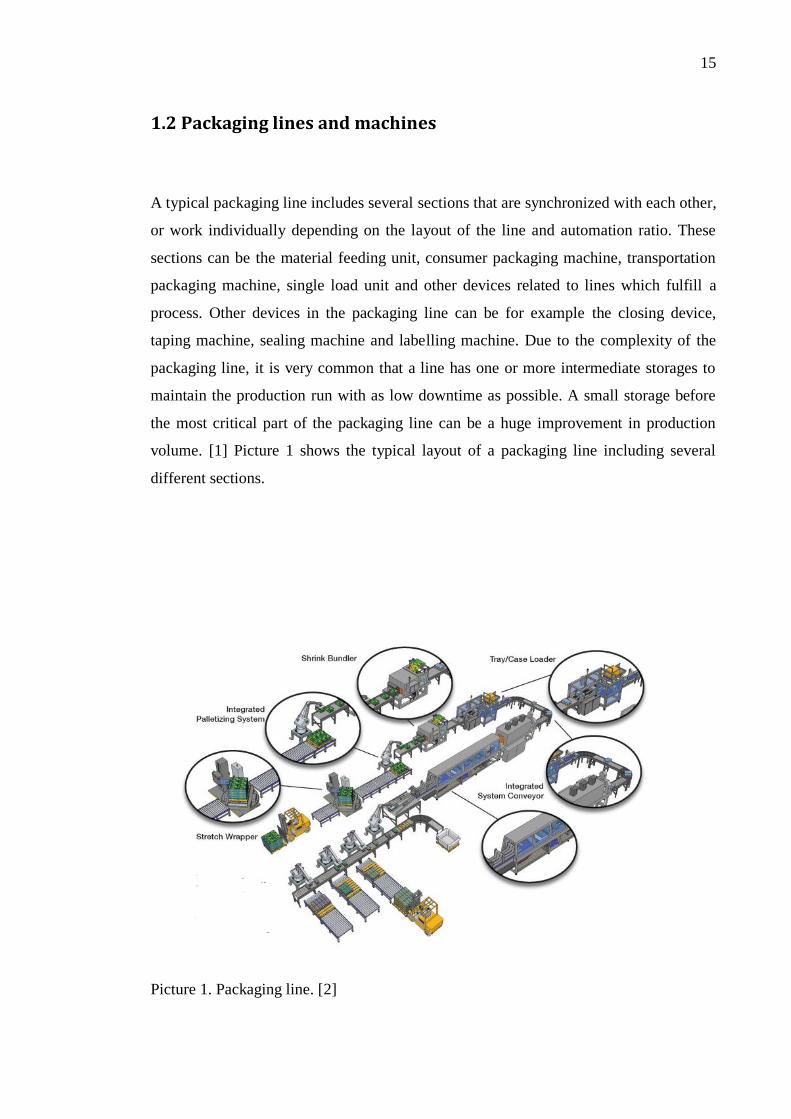

1.2 Packaging lines and machines

A typical packaging line includes several sections that are synchronized with each other,

or work individually depending on the layout of the line and automation ratio. These

sections can be the material feeding unit, consumer packaging machine, transportation

packaging machine, single load unit and other devices related to lines which fulfill a

process. Other devices in the packaging line can be for example the closing device,

taping machine, sealing machine and labelling machine. Due to the complexity of the

packaging line, it is very common that a line has one or more intermediate storages to

maintain the production run with as low downtime as possible. A small storage before

the most critical part of the packaging line can be a huge improvement in production

volume. [1] Picture 1 shows the typical layout of a packaging line including several

different sections.

Picture 1. Packaging line. [2]

16

1.2.1 Selection criteria

The package itself is a cost for the product manufacturer which drives them to make

decisions on packaging selection. The possible alternatives in product packaging are [2]:

Straight after the production line

Packaging near consumer markets

Using subcontracting in packaging

Externalize packing

Product without a package

The selection has to be made based on what is the most suitable location for packaging

machinery, which in turn depends on the possible production facilities and products that

need to be packed. If the packaging machinery is located directly after the production

line, it has to be fast enough not to slow down the whole process. But with some

products, such as in the food industry, it is necessary to pack the product immediately

after the production line has accomplished manufacturing the product.

High expectations of quality and quantities set demands for the packaging line

manufactures to meet the requirements of packaging companies, as well as of end users.

The greater the demands, the faster the machines are expected to create packages.

Therefore, mechanical durability plays a great role already during the packaging process

and not only after the product has been packed. [5] Mechanical durability is necessary

in order to maintain the desired production speed with as low downtime as possible.

Automation in packaging machines together with complex mechanics is also an

essential part of the whole system.

The product itself is one of the main criteria in packaging line and machinery selection,

in addition to the rate of production, logistics, market location, customer demands and

the expertise of the packaging company [1]. In machinery selection, it is highly

recommended to gain as much information as possible about the product itself. The

importance of product specification is on as high a level as selecting the packaging

materials [4]. Before starting packaging, a company has to form a deep calculation of

the needed capital, operating expenses and possible waste expenses, not forgetting the

17

risk analysis for the machinery. Over time, operating costs in packaging transactions

rise compared to what they are when the initial investment is made. The required

amount of operators to run the machine is an essential part of the operating expenses,

and it is fairly common that small companies use very simple machines that require

more manpower. Fully automated packaging lines are dependent on the production

volume, for the reason that a single investment is substantially higher than it is in less

automated machines. A fully automated packaging line can be an enormous investment

in the beginning but offers many benefits, such as better package uniformity and

quality, improved hygiene and fewer downtime periods. [1]

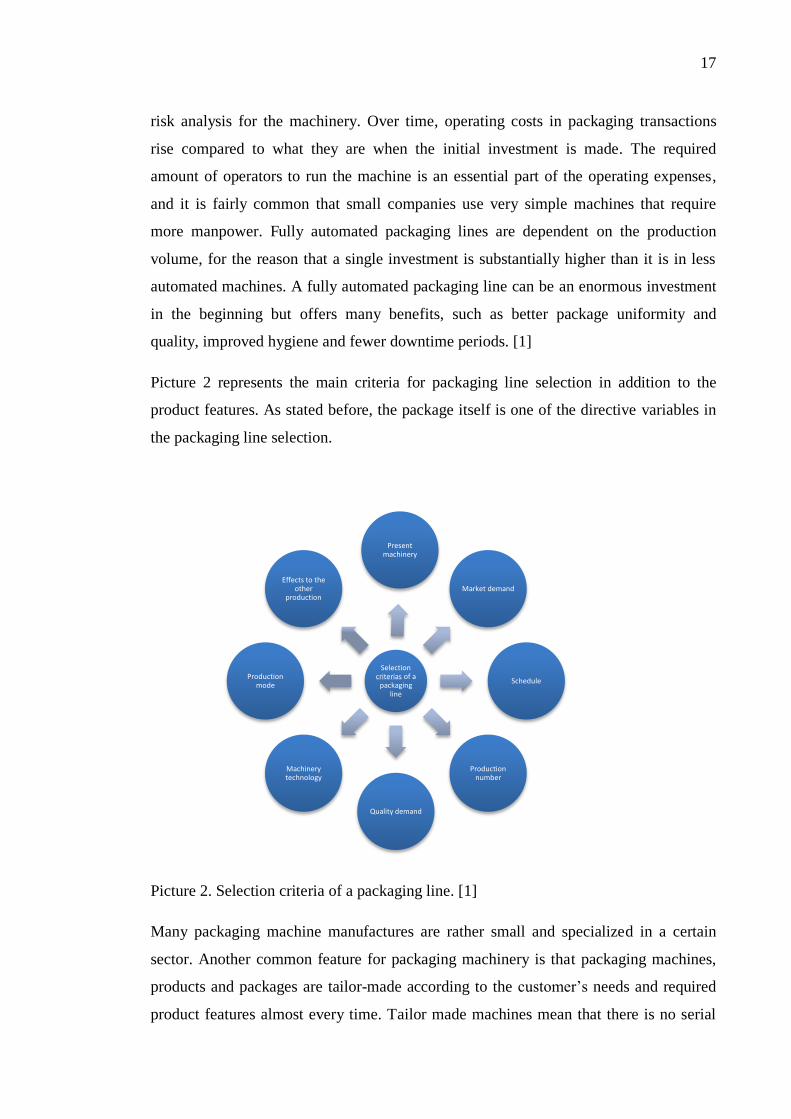

Picture 2 represents the main criteria for packaging line selection in addition to the

product features. As stated before, the package itself is one of the directive variables in

the packaging line selection.

Picture 2. Selection criteria of a packaging line. [1]

Many packaging machine manufactures are rather small and specialized in a certain

sector. Another common feature for packaging machinery is that packaging machines,

products and packages are tailor-made according to the customer’s needs and required

product features almost every time. Tailor made machines mean that there is no serial

Selection criterias of a

packaging line

Present machinery

Market demand

Schedule

Production number

Quality demand

Machinery technology

Production mode

Effects to the other

production

18

production and the supplied machines are delivered in small batches, with a few

exceptions in the industry.

A packaging machine covers multiple phases and separate axes for different tasks.

Frequently, the axes need to be synchronized with each other and in the past these were

usually driven by one single mechanical power shaft wherefrom the ratios for different

parts of the machine were implemented with levers. This means that when the power

shaft is on the move the other phases are also moving with the defined ratio. It provides

very accurate synchronization where the axes are always in the desired position. In

modern packaging machines the control of different axes is done by using motion

control products for controlling several induction or servo motors.

It is very common that a packaging machine is controlled from one computed system.

One common feature of modern packaging machine control is that all the axes are

working in a closed loop. The definition of a closed loop is that a motor is equipped

with a device that provides motor shaft position feedback to the system, which makes

the process more accurate and faster. The controlling signals from the main system to

the motor controllers are usually sent in digital, analog or fieldbus forms. [1]

Packaging speeds in modern packaging machines are respectably fast. For example, a

wrapping machine wrapping sweets is able to wrap more than 1000 sweets per minute;

this cannot be detected with the human eye due to the high speed. The starting point in

packaging machine design is to give a target speed defining how many packages or how

many kilograms have to be packed during a given time frame. The target can be defined

in pieces, weight or units requiring packaging in a given varying time period between a

minute and one year. Despite the demanding targets on machinery speed, the designed

maximum capacity is not always the setting that is used in production. A line is made up

of several different parts which need to run together smoothly. [1] There might be

sections or single tasks that are not as fast as the single packaging machine, so the

production speed is limited to the lowest part of the line. If a single machine is working

alone it can be ran at full speed, but seldom are machines running at the designed

maximum speed. There are other important points to consider regarding production

speed, such as a decrease in quality, and the number of incorrect packages; both of

which are more likely to occur as the machine speed grows. [5]

19

1.3 Grouping of packaging machines

The range of different kinds of packaging machines is wide and the given names for

certain machines come from the operating method or the product brand name. For

example, the name of the filling machine comes from the operation it performs. The

same can be said of many others, such as the names of the sacking machine and

pouching machine. The prevailing language in the packaging branch is English and

many machinery names derive from the English initials. The FFS machine is a very

common packaging machine type and the initials stand for form-fill-seal, which also

describes the operating function of the machine. Different machines are divided into

vertical and horizontal machines according to the direction of the material flow in the

machine. One example of vertical machines is VFFS, vertical-form-fill-seal machine,

also known as Transwrap, which is a brand of a certain manufacturer. [1]

Packaging machines can be grouped and classified according to the operating method

and product that is being packed. Standard EN 415-1 stands for the security of

packaging machines: Part 1. Vocabulary and classifying of packaging machinery and

devices related to packaging machines. In the following list the most common types of

packaging machines according to the EN 415.-1 standard are presented. The standard is

in use in many countries and it simplifies the selection criteria of a packaging line

dividing machines into their own compartments, which makes the search for a suitable

supplier easier for packaging companies. The most relevant standards are introduced in

more detail later. [3]

Grouping of packaging machinery according to German machine manufacturers. [3]

Filling Machines

o piece products

o grains

o powders

o liquids

Sealing machines (Filling and sealing machines)

o flexible packages

o carton packages

o ampoules, capsules

o tubes

o bottles, cans, goblet, bowls, plates….

o barrels, buckets

20

Form-fill-seal machines

o track materials

o seamed small pouches

o other flexible packages

o bubble packages

o other heat formable packages

Machinery for products that need to be protected

o vacuum packaging

o shielding gas packaging

o aseptic packaging

o medicine packaging (GMP)

Wrapping machines

o partly or full wrapping machines

o spiral wrapping machines

o shrink or surface film machines

Group packaging machines

o Housing, base, erection, filling and sealing machines

o wrapping machines

o film wrapping machines

o palletizing and unloading machines

o single unit load verifying machines

o single unit load dressing machines

Other packaging machines

o sack opening and emptying machines

o metal can, tube and cover machines

o testing and controlling machines

o cleaning and drying machines

o labelling, finishing and gluing machines

21

1.4 Machine safety and standards

Every machine has to be safe enough not to cause any harm to the environment and

humans. The policy on safety has been tightened lately and it is not rare that a company

appoints a specific person whose primary job description is exclusively to take care of

machine safety. The safety level of old-fashioned machines is considerably low

compared to the current level. Modern devices are designed so that they should not be

able to harm humans or cause injuries while the machine is running or stopped. There

are many directives, some of which are common to all machinery sectors, and some

which are valid only within a specific region and sector. For packaging machinery there

are also a lot of standards and directives but the most relevant EN 415 – X standards

related to machine safety are only briefly introduced. Standards are not usually available

free of charge and none were purchased for the use of this research. The world of

standards and directives is very complex and would require dedication on the subject;

therefore the subject is dealt with only superficially here.

1.4.1 Standards and Directives in machinery

Inside the world of European directives for machinery in the industry, two can be

highlighted as the most relevant. [4]

The Machinery Directive

The Use of Work Equipment by Workers at Work Directive

Both directives are directly related to Essential Health and Safety Requirements (EHSR)

and can be utilized to confirm equipment safety in The Use of Work Equipment by

Workers at Work Directive.

22

1.4.2.1 The Machinery Directive

The machinery directive covers the supply of new machinery, safety components and

other products. It is against the law to supply machinery to the EU area without

fulfilling the directive. The definition for machinery within the directive is that the

machine is a combination of a fitted drive system including at least one section, which

is capable of performing a task without the help of a human. [4]

The present valid directive (2006/42/EY) was implemented on 29th

of December 2009

and obligates the machinery manufacturer or authorized representative to assure that the

supplied equipment is in conformity with the directive. [4]

Ensuring that the applicable EHSRs contained in Annex I of the Directive are

fulfilled

A technical file is prepared

Appropriate conformity assessment is carried out

An “EC Declaration of Conformity” is given

CE Marking is affixed where applicable

Instructions for safe use are provided

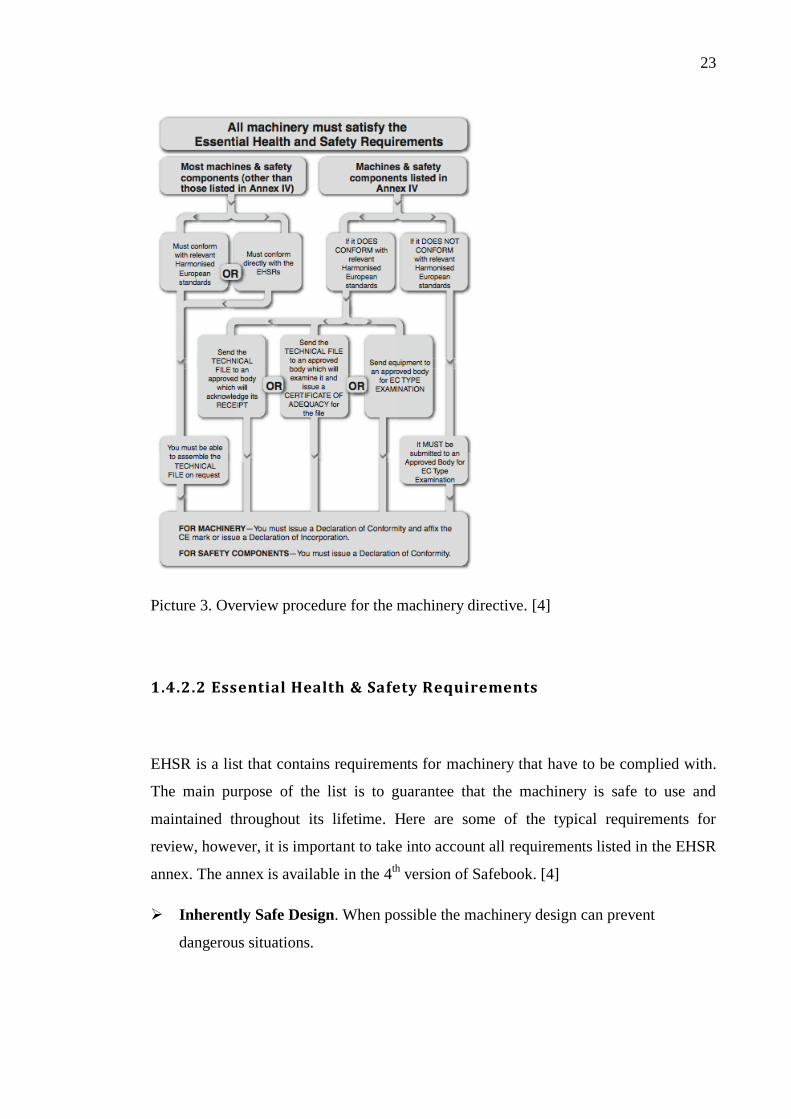

Picture 3 represents the guidance of procedures for fulfilling the machinery directive.

23

Picture 3. Overview procedure for the machinery directive. [4]

1.4.2.2 Essential Health & Safety Requirements

EHSR is a list that contains requirements for machinery that have to be complied with.

The main purpose of the list is to guarantee that the machinery is safe to use and

maintained throughout its lifetime. Here are some of the typical requirements for

review, however, it is important to take into account all requirements listed in the EHSR

annex. The annex is available in the 4th

version of Safebook. [4]

Inherently Safe Design. When possible the machinery design can prevent

dangerous situations.

24

Additional Protection Devices. When it is not possible to design the machinery to

be safe enough, certain safety equipment can be used to prevent any hazards. These

safety products can be for example safety locks, light-curtains or safety (sensing)

mats.

Personal Protective Equipment and/or Training must be used if the methods

above are not adequate in guaranteeing the safety of the machinery.

Machinery controls and control systems must be safe and must not be capable of

starting unexpectedly. Machines must be equipped with at least one or more emergency

stop device, and the surrounding environment has to be appropriate, including adequate

lighting and handling of the machine. The machinery structure has to be stable where

the used materials are appropriate and do not include sharp edges or surfaces that could

cause damage. The machine designer or liable authorized person has to be able to prove

that the machinery is in conformity with EHRS. A statement should include relevant

information about the machinery, such as specifications, results from the tests and

drawings. [4]

1.4.3 CEN

CEN (The European Committee for Standardization) is the leading and only recognized

organization in Europe according to directive 98/34/EC for the planning, drafting and

adoption of European Standards in all places where an economic activity occurs.

CENELEC and ETSI are the only exceptions where the CENELEC is related to

electrotechnology and ETSI is related to telecommunication. [7]

25

CEN Vision:

”to make a contribution to Europe's innovative capacity, global competitiveness,

sustainable growth, and to welfare of its citizens, by being the organisation of choice

for raising standards”[6]

CEN being a non-profit organization, founded in Belgium in 1975, is working to

remove trade barriers and improve and support the European economy, the welfare of

citizens and the environment. CEN offers a base for the development of EU standards

and technical instructions. A total of 33 national members across Europe are working

together with CEN to develop European Standards, EN’s. EN standards decrease

development and testing costs with very wide market reach in European internal

markets. These EN standards are also national standards in every member country,

which means that 1 European standard equals 33 National standards. CEN signed the

Vienna Agreement with the ISO (International Organization for Standardization) in

1991. ISO is CEN’s counterpart on a global scale and the agreement verifies

cooperation between these two participants in improving the technical compatibility and

adoption of the same text for both ISO and EN. [7]

1.4.4 EN standards

A European Standard, EN, is known as a very complicated process that causes further

costs for manufacturers. Regardless of this, it is one of the most important standards in

the whole business. EN standards are not known among all organizations, and maybe

the information is not relevant for all working in the industry. As a phrase or word,

“standards” is often interpreted as being boring or even considered inconsequential,

even though organizations have to take them into consideration while designing or

manufacturing technological products. In actual fact, standards push the manufactures

into a better market position and are crucial factors in gaining visibility for the company

inside, and even outside Europe. Standardization provides benefits for all parties related

to the manufacturing of technological products. Increased product safety, high quality

26

products, lower costs in testing and transactions can be mentioned as the best benefits

enabled by standardization. [8]

1.4.5 EN Harmonized European Standards

The following standards are common to all countries in EEA, produced by CEN and

CENELEC. The use of standards is voluntary but designing and manufacturing a

machine according to these standards is the most direct way of ensuring compliance

with EHSR of the Machinery Directive. [4]

Type A. Standards: Cover aspects applicable to all types of machines.

Type B. Standards: Subdivided into 2 groups.

Type B1 Standards: Cover particular safety and ergonomic aspects of machinery.

Type B2 Standards: Cover safety components and protective devices.

Type C. Standards: Cover specific types or groups of machines.

It is noteworthy that complying with a C standard automatically presumes conformity

with the EHSR. If it is not possible to find a suitable C standard for use, A and B

standards can be used as part or full proof of the EHSR conformity.

1.4.6 Safety standards in packaging machinery

For packaging machinery safety standardization, CEN has published nine different EN

standards which are shown below. Three standards are under development, two of

which are updates of the existing EN415-1 and EN415-6, but EN 415-10 is completely

new and stands for general requirements of packaging machine safety. EN 415-10 will

be implemented in November 2013, while the current status is still under approval. [9]

27

CEN/TC 146 standards under development for packaging machines [9]:

FprEN 415-10 General Requirements

prEN 415-1 rev Terminology and classification of packaging machines and

associated equipment

EN 415-6:2013 Pallet wrapping machines

CEN/TC 146 published standards for packaging machines [9]:

EN 415-1:2000+A1:2009 Terminology and classification of packaging machines

and associated equipment

EN 415-2:1999 Pre-formed rigid container packaging machines

EN 415-3:1999+A1:2009 Form, fill and seal machines

EN 415-4:1997 and AC:2002 Palletisers and depalletisers

EN 415-5:2006+A1:2009 Wrapping machines

EN 415-6:2006+A1:2009 Pallet wrapping machines

EN 415-7:2006+A1:2008 Group and secondary packaging machines

EN 415-8:2008 Strapping machines

EN 415-9:2009 Noise measurement methods for packaging machines, packaging

lines and associated equipment, grade of accuracy 2 and 3

28

1.5 Global markets for servo systems – Motion control

The investigation of the motion control markets is based on the IMS Motion Control

World 2011. The same organization has also carried out the research where the

packaging machinery production in EMEA is investigated. The scope of the industries

and markets is limited to GMC and CNC, General motion control products and

Computerized Numerical Control. GMC is more relevant to packaging machinery

because the global revenues in GMC for packaging machinery are approximately six to

seven hundred times bigger than CNC on a global scale.

1.5.1 Global revenues for motion control products

Estimated world revenues for motion control products for the year 2011 were predicted

to be just short of 13 Billion U.S dollars with a very high growth rate because of strong

recovery from the recession that occurred during 2008 and 2009. The growth rate

stabilized back to its normal growth level in 2012. An average annual growth rate for

motion control products is forecasted to be 6.2 % from 2008 to 2015 which drives the

total motion control revenues up to nearly 18 Billion U.S dollars with more than 22.000

thousand units shipped. The growth rate for motion control products is dependent on

machinery production recovery in each sector. The Machine tool sector has been the

market booster after economic depression and the sector has a high share in motion

control markets representing over 45 % of the total market. [11]

29

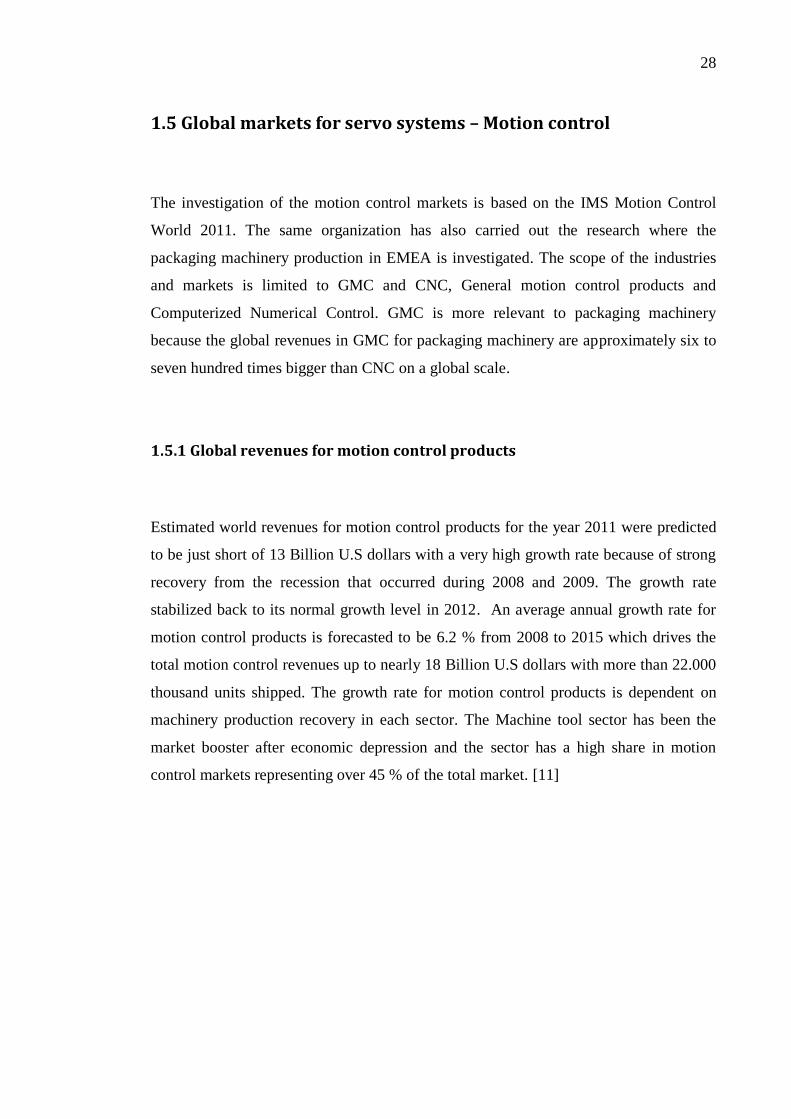

Picture 4. The share of motion control revenues by region. [11]

1.5.2 EMEA

Because of the high number of machine builders, the most substantial area for motion

controls has long been EMEA. Despite the depressive years of 2008 and 2009, EMEA

still holds the leading position in the motion control market with annual revenues of 3.4

Billion U.S dollars in 2010. Total sales of the motion control products in EMEA for

2011 were predicted to be nearly 4 Billion U.S dollars. However, forecasts for longer

periods show that the Asia Pacific area is about to take EMEA’s place as the leading

motion control user region. If the forecast holds true, the Asia Pacific region will

overtake EMEA in 2014. The recovery from the recession has been difficult due to

economic problems in the area. Growth rates are also forecasted to be lower than for

other regions with 0,3 % in unit supply and 2.4 % in CAGR revenues up to 2015. [11]

EMEA motion control markets;

33,50%

American motion control

markets; 13,90%

Asia Pacific motion control

markets; 30,10%

Japanese motion control markets;

22,50%

30

1.5.3 APAC

The second largest motion control product market area is Asia Pacific with 30.1 % of

the market share in 2010. During the recession, China’s economy was able to make

positive growth while other countries and continents suffered with negative numbers.

China’s motion control markets grew almost 6.0 % during 2009 and the estimated

growth for 2010 was 36.2 %. This means that Asia Pacific has been able to gain over 10

percent of the total motion control markets since 2008 with the help of strong

machinery production. This area differs from the others because the demand in

equipment technology is lower than it is in the other areas. The equipment does not

have to be as flexible and high in performance as in EMEA; but the quality and life

cycle are not the qualities to bargain with. Even if requirements on flexibility and

performance levels are not high, the quality and expected life span for motion control

products, as well as for servo drives and motors should be at the same level as

elsewhere. This phenomenon has an effect on both local and international machine

builders who are supplying, or just about to enter the area markets. Another important

factor in Asia Pacific markets is that China, which is holding the markets for magnets, is

one of the growing countries in machine building and is able to control the supply of

magnets for the benefit of domestic use. In fact, controlling the supply may increase

prices in other areas but in Asia Pacific, prices are more likely to remain at the same

level, which sets challenges to international machine builders. The Asia Pacific markets

are predicted to rise 15.1 % in revenues and 17.1 % in unit supply from 2008 to 2015.

[11]

1.5.4 America

The American motion control market share was about 13.9 % in 2010 with 1.4 Million

U.S dollars. American markets started to recover earlier than the EMEA area with very

strong performance in sectors such as packaging and semiconductor equipment. The

first nine months of 2011 in machine tool sales showed that the sales increased an

31

incredible 80 % compared to levels in 2010. But in general the motion control markets

are predicted to rise 5.7 % in sales and 2.0 % in units during the period from 2008 to

2015. [11]

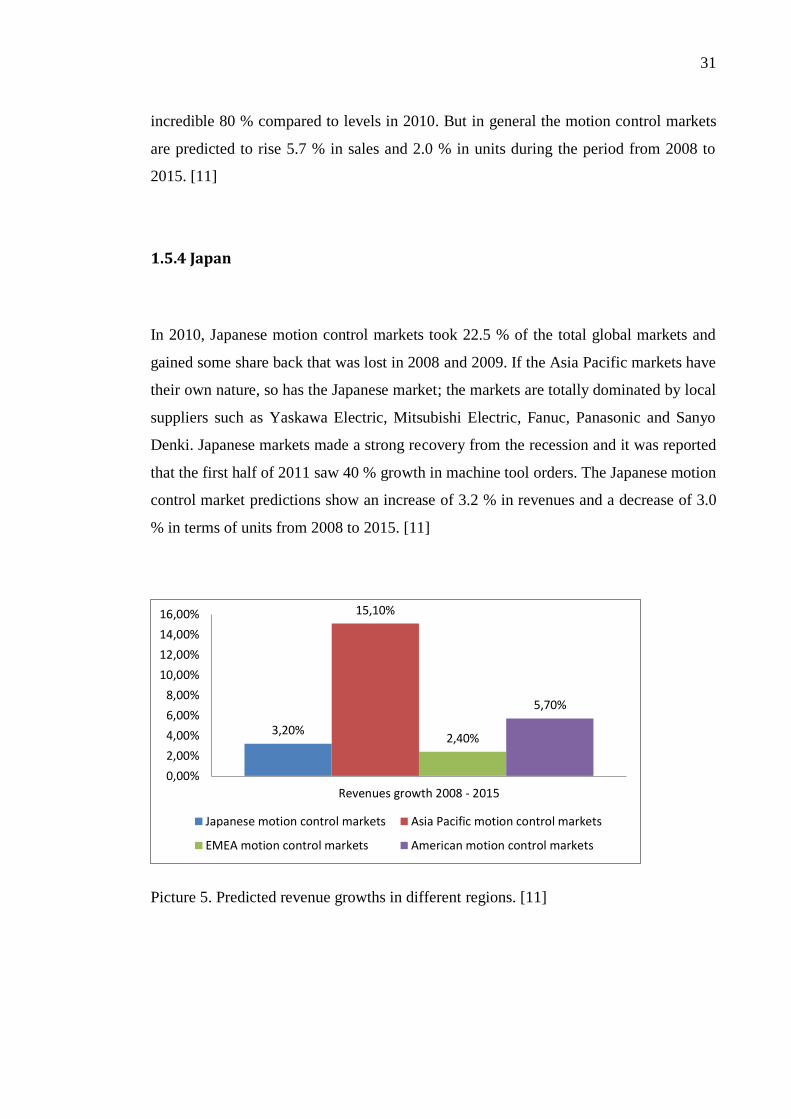

1.5.4 Japan

In 2010, Japanese motion control markets took 22.5 % of the total global markets and

gained some share back that was lost in 2008 and 2009. If the Asia Pacific markets have

their own nature, so has the Japanese market; the markets are totally dominated by local

suppliers such as Yaskawa Electric, Mitsubishi Electric, Fanuc, Panasonic and Sanyo

Denki. Japanese markets made a strong recovery from the recession and it was reported

that the first half of 2011 saw 40 % growth in machine tool orders. The Japanese motion

control market predictions show an increase of 3.2 % in revenues and a decrease of 3.0

% in terms of units from 2008 to 2015. [11]

Picture 5. Predicted revenue growths in different regions. [11]

3,20%

15,10%

2,40%

5,70%

0,00%

2,00%

4,00%

6,00%

8,00%

10,00%

12,00%

14,00%

16,00%

Revenues growth 2008 - 2015

Japanese motion control markets Asia Pacific motion control markets

EMEA motion control markets American motion control markets

32

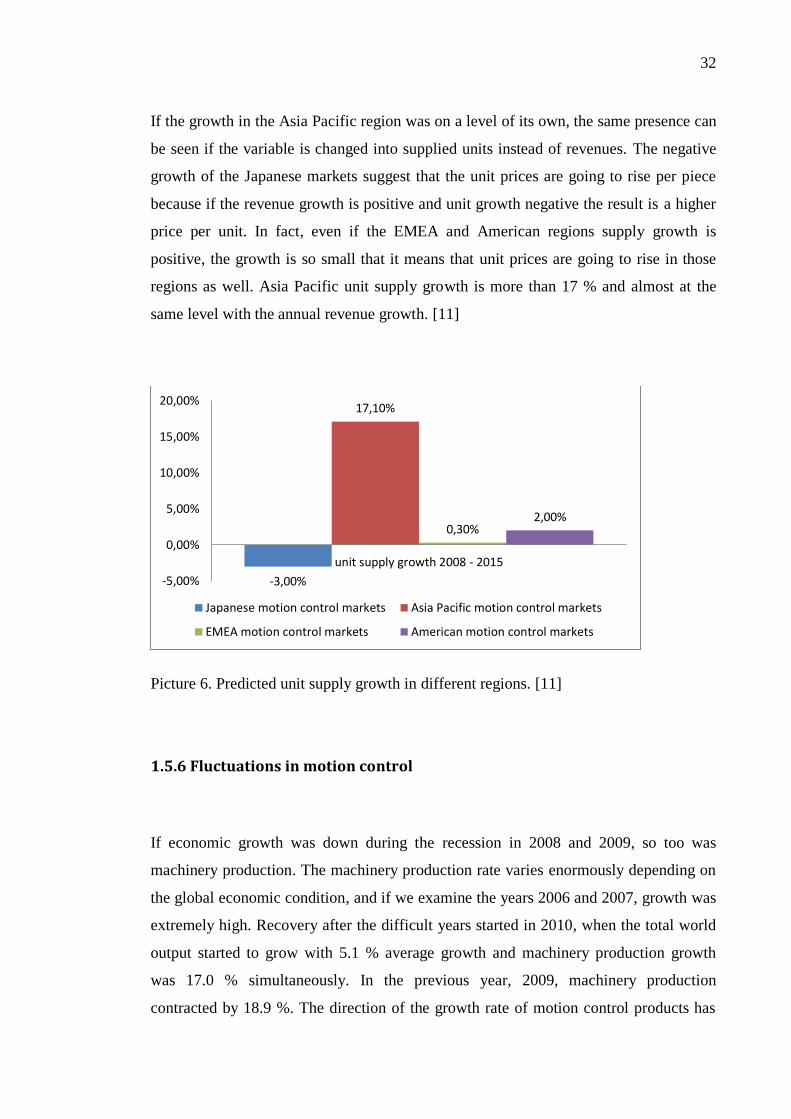

If the growth in the Asia Pacific region was on a level of its own, the same presence can

be seen if the variable is changed into supplied units instead of revenues. The negative

growth of the Japanese markets suggest that the unit prices are going to rise per piece

because if the revenue growth is positive and unit growth negative the result is a higher

price per unit. In fact, even if the EMEA and American regions supply growth is

positive, the growth is so small that it means that unit prices are going to rise in those

regions as well. Asia Pacific unit supply growth is more than 17 % and almost at the

same level with the annual revenue growth. [11]

Picture 6. Predicted unit supply growth in different regions. [11]

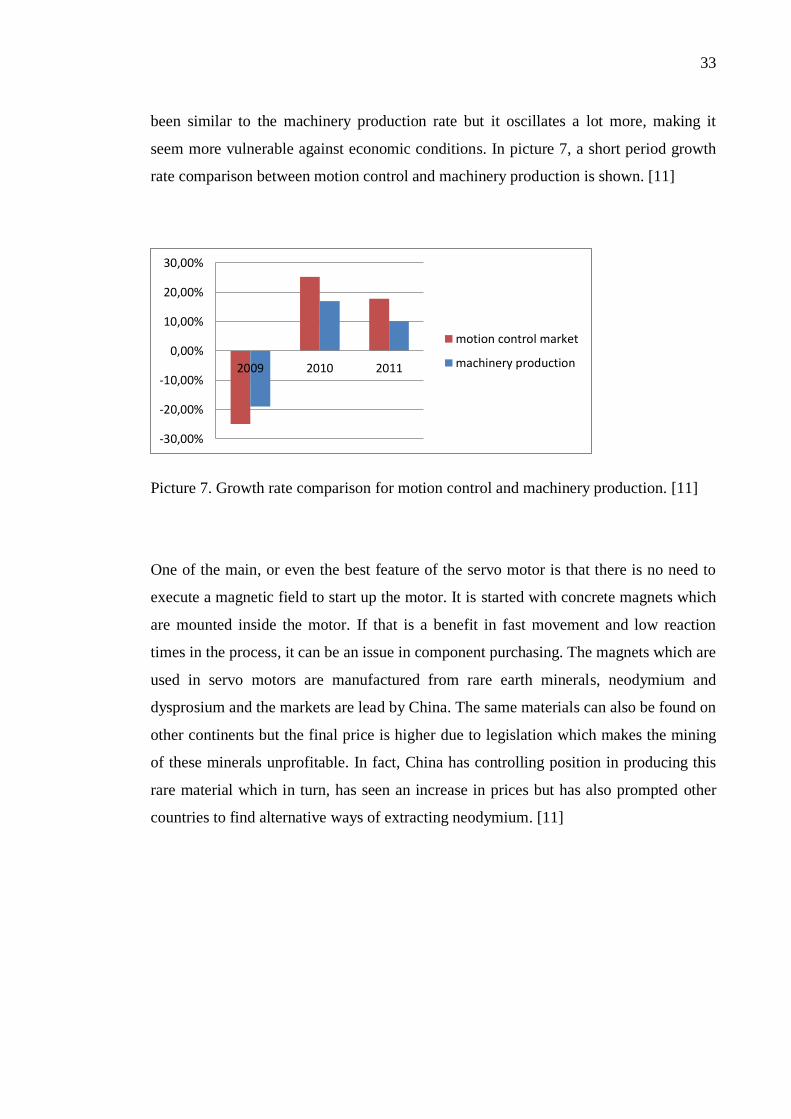

1.5.6 Fluctuations in motion control

If economic growth was down during the recession in 2008 and 2009, so too was

machinery production. The machinery production rate varies enormously depending on

the global economic condition, and if we examine the years 2006 and 2007, growth was

extremely high. Recovery after the difficult years started in 2010, when the total world

output started to grow with 5.1 % average growth and machinery production growth

was 17.0 % simultaneously. In the previous year, 2009, machinery production

contracted by 18.9 %. The direction of the growth rate of motion control products has

-3,00%

17,10%

0,30% 2,00%

-5,00%

0,00%

5,00%

10,00%

15,00%

20,00%

unit supply growth 2008 - 2015

Japanese motion control markets Asia Pacific motion control markets

EMEA motion control markets American motion control markets

33

been similar to the machinery production rate but it oscillates a lot more, making it

seem more vulnerable against economic conditions. In picture 7, a short period growth

rate comparison between motion control and machinery production is shown. [11]

Picture 7. Growth rate comparison for motion control and machinery production. [11]

One of the main, or even the best feature of the servo motor is that there is no need to

execute a magnetic field to start up the motor. It is started with concrete magnets which

are mounted inside the motor. If that is a benefit in fast movement and low reaction

times in the process, it can be an issue in component purchasing. The magnets which are

used in servo motors are manufactured from rare earth minerals, neodymium and

dysprosium and the markets are lead by China. The same materials can also be found on

other continents but the final price is higher due to legislation which makes the mining

of these minerals unprofitable. In fact, China has controlling position in producing this

rare material which in turn, has seen an increase in prices but has also prompted other

countries to find alternative ways of extracting neodymium. [11]

-30,00%

-20,00%

-10,00%

0,00%

10,00%

20,00%

30,00%

2009 2010 2011

motion control market

machinery production

34

1.5.7 Packaging machinery in motion control

In 2010 the total GMC market was approximately 6.1 Billion U.S dollars together with

over 11 Million units and took a market share of almost 56 % of the total motion control

market. At the same time CNC motion control markets were smaller in revenues 4.8

Billion U.S dollars and in supplied units 3.8 Million. The much smaller unit supply in

CNC is due to higher average unit price. The higher unit price in CNC motion control

products is explained by the units used in the machine tool sector, which are very high

in the degree of technology. Both GMC and CNC motion control areas are predicted to

increase just over 6% yearly from 2008 to 2015. Packaging machinery requires more

motion control products than other machinery due to the large number of motion axes in

the average packaging machine. Sales of motion control products in packaging

machinery were 637,7 Million U.S dollars in 2010, where as the share for GMC was

636,7 and for CNC 1,0 Million U.S dollars. It is remarkable that in total scale the

packaging industry represents 6,3 % of the total revenues but under GMC products the

share is an impressive 11,0 %. The growth of motion control products in packaging

machinery is predicted as 10,7 % CAGR up to 2015. [10] The research shows that the

ratio in revenues between the stand-alone and multi-axis solution is approximately 55 %

versus 45 % on a global scale in all machinery. The ratio is leaning towards multi-axis

solutions according to the predictions, and after a couple of years, the ratio will be 50 %

for both solutions. The method of calculation for the single- or multi-axis solution is

that a drive is a single axis solution if each encased drive has its own electrical supply.

The definition of a multi-axis solution is that a drive DC bus has to be connected but the

power supply can be centralized or decentralized. [12]

35

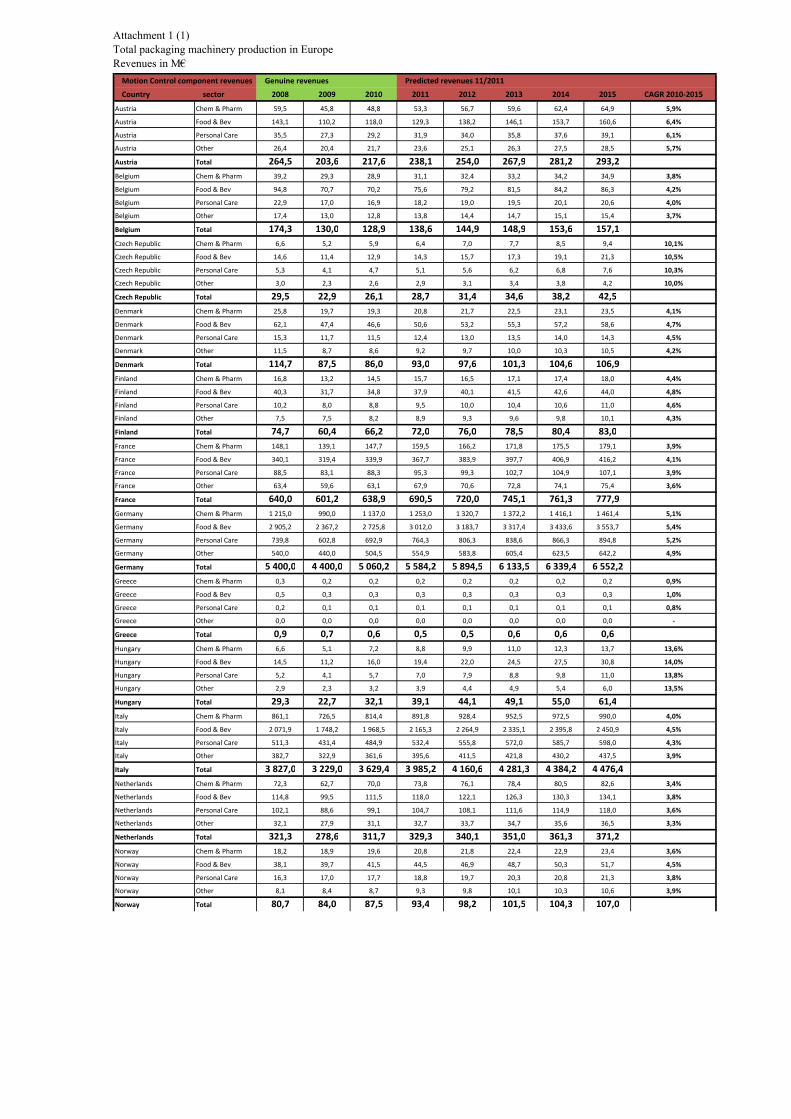

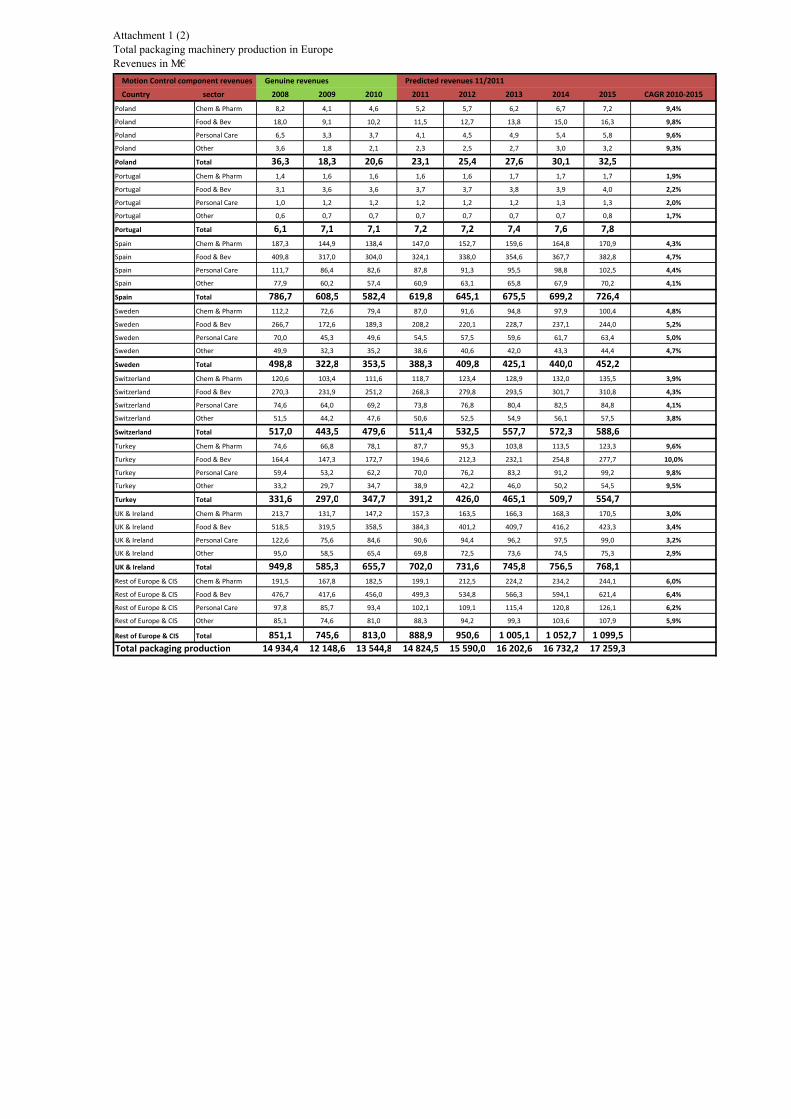

1.6 Packaging machinery in EMEA and Europe

The market data, categorization and machinery cost structure are collected from the year

2007 and the values starting from 2008 up to 2015 are based on estimations. That is

why the numbers given in currency may not be applicable due to the recession which

started at the end of 2008. There are still available data with which to count the ratios

between different machinery types, the grade of automation, and relation between

different countries and sectors. In this chapter the main idea is to show the cost structure

in a packaging machine between different packaging sectors.

The packaging machinery market has been divided into nine market areas [13]:

Bottling line machinery

Cartoning machinery

Closing machinery

Filling & dosing machinery

Form, fill & seal machinery

Labelling, decorating & coding machinery

Palletising machinery

Wrapping & bundling machinery

Other packaging machinery

IMS research has selected five different indicators with which to predict market growth

because packaging machinery is spread over such a wide area, and therefore cannot be

predicted by using a single indicator. Two of the selected indicators were

macroeconomic and the other three were industry-specific projections. Macroeconomic

indicators were industrial and manufacturing output, and the other three indicators used

were growth profiles for the sectors: Food, Beverages and Personal care (toiletries and

cosmetics). [13]

36

1.6.1 Definitions for macroeconomic indicators

The industrial production indicator is the output of industrial establishments handling

mining and quarrying, manufacturing and electricity, gas and water supply. Industrial

production is an outstanding indicator because of its latitude as a yardstick of a nation’s

productivity and manufacturing output, together with the services surrounding total

manufacturing output. But the service part of industrial production is not related to

packaging machinery growth and has been taken into account. [13]

Manufacturing output is defined as a sum of intermediate, investment and consumer

goods, being a subset of overall industrial production. It only measures the physical

output of goods used in the production of other goods or those which are sent directly to

the end market. There is a direct correlation between the trends in the physical output of

goods and trends within packaging machinery production to manufacture these goods.

[13]

1.6.2 Definitions for end-user indicators

The food sector was the most extensive market area for packaging machinery in EMEA

in 2007. Food processing is closely tied to packaging machinery as when food

processing lines are updated, it is a common phenomenon that packaging lines are

simultaneously modernized. [13]

The beverage sector is close behind the food sector and is also tightly linked with

packaging machinery. In Western Europe, bottled water in plastic bottles is a trend that

drives growth in the beverage business and covers over 30 % of all beverages. Milk is

the second most packed liquid after water and has a share of over 20 % of all beverages

as well as very high predicted growth. The other two major beverage products are soft

drinks and beer, with a combined share of over 30 %. [13]

Personal care, toiletries and cosmetics is in very high growth speed according to the

predictions that assume that growth per year could be from 6 % up to 10 %. The

37

cosmetics sector is expected to be the broadest as a result of better life quality in today’s

world, which shows in usage of cosmetic products. [13]

1.6.3 Trends influencing the markets

There are many facts that drive growth either in a positive or negative direction in the

packaging machinery field. While focusing on the EMEA area, it is good to know that

Asia together with Eastern Europe are big players in packaging machinery due to the

rising standards of living as well as their increasing populations. Yet even today, the

market area of Asia and Eastern Europe is more focused on packaging machinery with

lower demands and lower prices. Low-cost manufacturing creates competition, and the

predicted revenues regarding units and volume are high even with a low margin

machine.

If a low-cost type packaging machine is preferred elsewhere, in EMEA flexibility,

reliability and speed are the key words describing the demands of a packaging machine.

The flexibility and fast changeovers of packaging machines have had a positive effect

on EMEA packaging machinery. The simplest configuration enables a company to pack

different kinds of packages with different dimensions with just one packaging machine.

[13] It is possible because a packaging machine can be supplied with very flexible,

increased levels of automation and the changeovers can be fast with minimum down

time [5]. This is becoming more and more important as packages vary but companies

are not willing to tie their capital to a wide range of machines.

Technological innovations are much appreciated in the packaging machinery business

and the trend is that the more a packaging machine is able to work alone without

external human work, the better it is for total productivity. A good example is of a robot

able to work without humane pauses with a very high work trace. Highly automated

packaging machines have numerically grown a great deal lately and that is why motion

control products, such as servo motors and drives, have become common in the

machinery. The mechanical part of a packaging machine has experienced an update as

well, and therefore many machines have been equipped with linear guides instead of

38

mechanical cam, lever and bearing assemblies. The reason for the changeover to linear

guide technology is simply that the machines need less maintenance without

compromising the quality of production or product being packed. [13]

Flexibility is in high valuation in packaging machines but so is functionality. It is not

unusual to find packaging machines that can form or fill different kinds of packages. In

the packaging machinery business, returns on investment enable the users to select the

best choice in regaining the invested money as soon as possible; so accordingly the

fastest machine is not always selected. Obviously, the speed of the machine is relevant

but when various product types need to be packed the total sum of different variables

are combined. These variables can be for example machine productivity, flexibility,

time to train users and maintenance time between production runs. Each of these

variables rates differently depending on the user but a general target is the minimization

of the ROI (Return Of Investment). [13]

Green values in packaging have increased the demands for the ability to recycle and

avoid extra waste. For example, in the dairy industry milk products using cartons as

their material have seen a shift towards PET packages due to the ease of recycling these

products. The package alone is not the only issue in green values, and the future will see

an increased concentration on the energy efficiency of packaging machinery. But even

if these green values are forcing packages to become as environmentally friendly as

possible, single portion packages are also demanding high interest. The reason is

different; a single-person type household has multiplied significantly in recent years and

such a household is a common user of single portion packages. [13]

39

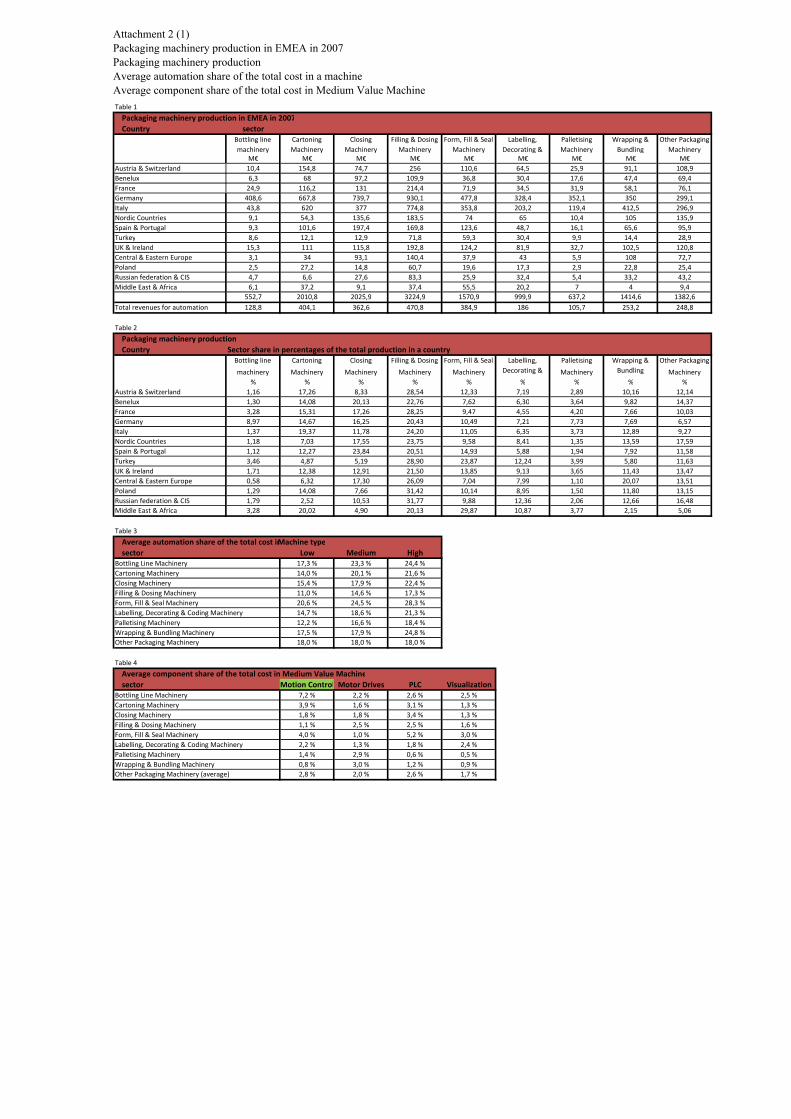

1.7 EMEA markets in packaging machinery

OACE (Opportunities for Automation Companies in the EMEA Packaging Machinery

Industry) divides the packaging machinery business into two different areas which are

the machines sold in EMEA and the machines produced in EMEA. The bill of

automation of the machines sold to EMEA was not available. The data for the

automation share of the total cost was available only for machines which were produced

in EMEA. The total packaging sales revenues in EMEA are relatively smaller than the

total production revenues because only a small amount of packaging machines are

imported, except at the low end of the market where service is a less important factor to

machine builders. [13]

The total market for packaging machines sold in EMEA was estimated to be worth 10,3

Billion Euros in 2007 with a forecast of total sales being near 13 Billion Euros in 2012,

with 4,5 % CAGR. Total production of packaging machinery was 13,8 Billion Euros in

EMEA in 2007 with almost 200.000 pieces manufactured. Filling & Dosing machinery

was the product type with the highest revenue, the second highest was Closing

machinery and the third was Cartoning Machinery in both areas, sold and produced, in

EMEA. [13]

The latest study represents the total packaging machinery production in Europe & CIS

countries (not in EMEA) and comes to approximately 14,4 Billion Euros in 2008 and

13,2 Billion Euros in 2009. The total fall in machinery production from 2008 to 2009

was 25,6 % on average where the packaging machinery area suffered with less than 9 %

average drop in revenues in production. [14]

Packaging machinery is the fifth largest market sector in the machinery business in

Europe after material handling, agricultural machinery, machine tool and food &

beverage and tobacco machinery. European machinery in production revenues was

372,5 Billion Euros in 2008, 289,3 Billion Euros in 2009 and estimated to be 339

Billion Euros in 2010 and growing with 5 % CAGR up to 2015. If these sectors are

explored more closely, they expose that from the automation point of view, the

packaging sector is the fourth highest area in revenues. The total usage of automation

components in packaging machines was 2,6 Billion Euros in revenues in 2010 adopting

40

an 11 % share of the total revenues in automation components used in machinery

production in Europe. [14]

1.7.1 Packaging machinery markets in EMEA by country

The central and western European countries have a huge appetite for consuming

processed foods and beverages. In 2007, Germany was the most extensive market

region in EMEA with 2,8 Billion Euros in revenues which was followed by Italy with

1,8 Billion Euros revenue. The third greatest region in EMEA was the UK & Ireland

with total revenues of 0,926 Billion Euros. The largest packaging machinery production

country in 2007 was Germany with 4,6 Billion Euros, in addition it was the biggest

consumer, followed by the second largest producer Italy with 3,2 Billion Euros [13]

After the correction to the European Machinery production yearbook – 2011 Edition,

Italy was placed as the biggest European country in revenues in packaging machinery

manufacturing. But after revenue values were corrected, Germany still held the position

of being the biggest packaging machinery country in Europe.

41

1.8 Automation in Packaging Machinery in Europe and EMEA

The ratio of automation in packaging machinery has been in high growth, since

prices of automation products have fallen to a reasonable level and there has been

tremendous evolution in technology. It is very common that functions that were only

possible with mechanical solutions can be executed using electrical axes. A typical

example of a mechanical solution is the power-shaft function where several

components are connected to each other and the motion is synchronized. The same

idea can be implemented with modern automation components with the desired

accuracy, speed and flexibility. Actually, flexibility is better in solutions where

automation components are used because if the components are not mechanically

connected, a single component can be modified to make the desired motion without

influencing the other components and the motion is adjustable when the device is

running or stopped, depending on the type of automation used. Automation

components need fewer maintenance procedures but on the other hand, they require a

qualified employee for designing and commissioning.

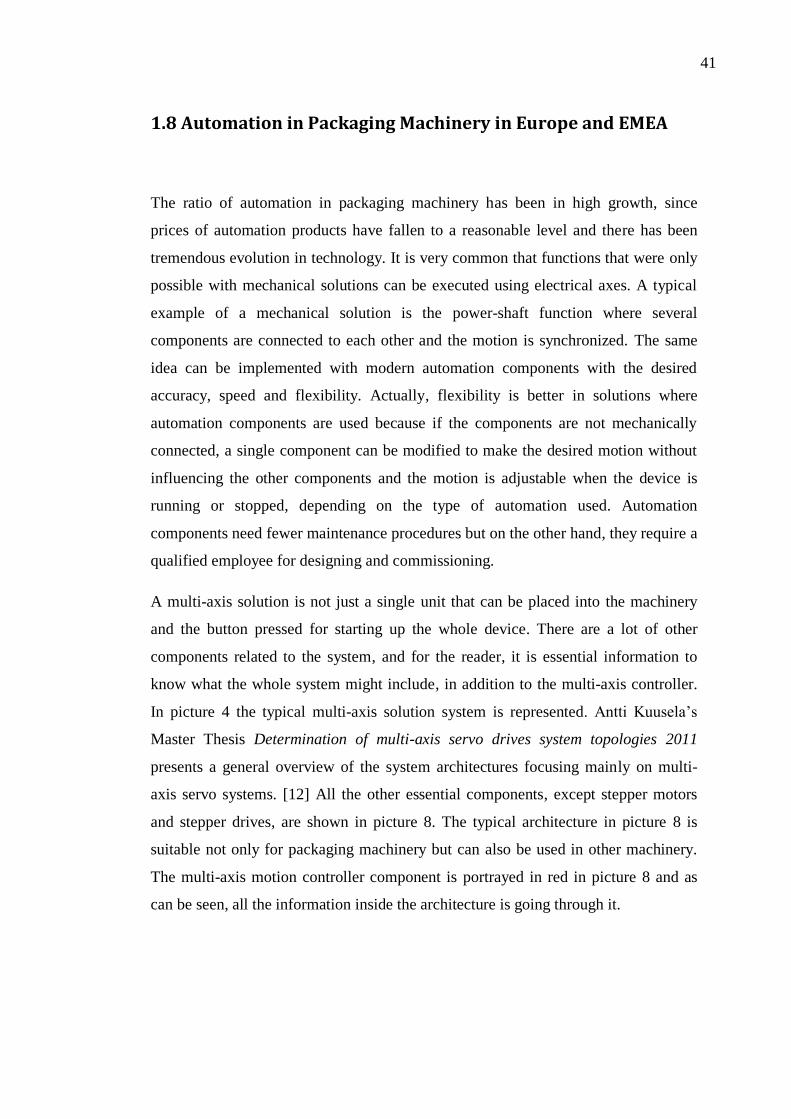

A multi-axis solution is not just a single unit that can be placed into the machinery

and the button pressed for starting up the whole device. There are a lot of other

components related to the system, and for the reader, it is essential information to

know what the whole system might include, in addition to the multi-axis controller.

In picture 4 the typical multi-axis solution system is represented. Antti Kuusela’s

Master Thesis Determination of multi-axis servo drives system topologies 2011

presents a general overview of the system architectures focusing mainly on multi-

axis servo systems. [12] All the other essential components, except stepper motors

and stepper drives, are shown in picture 8. The typical architecture in picture 8 is

suitable not only for packaging machinery but can also be used in other machinery.

The multi-axis motion controller component is portrayed in red in picture 8 and as

can be seen, all the information inside the architecture is going through it.

42

Picture 8. Typical automation architecture in multi-axis solution. [12]

1.8.1 Typical automation components

A modern packaging machine includes many automated tasks where a user does not

have to do any physical work. Therefore, a lot of automation components are required to

create the motion for the designed mechanics. Packaging machines are able to receive

the packaged piece, form a suitable package and convey it forward to the next station or

to the next packaging phase.

According to Opportunities for Automation Companies in the EMEA Packaging

Machinery Industry – IMS, the description for automation components is divided

into the following components which are introduced briefly with a picture after the

description. [13]

43

1.8.1.1 PLC – Programmable Logic Controller

PLC is a microprocessor-based device used in discrete manufacturing for line and

machinery controlling. The common programming language used is IEC 61131

based and the devices are RISC-based. [13] A normal system includes a CPU

(Central Processing Unit), I/O’s (digital or analog input/output module) and a

fieldbus card. The main component is the CPU and all the other components are

options which can be added to expand the system. One CPU can handle 320 digital

I/O points which after the needed I/O’s has to be decentralized and at the same time

the same CPU supports up to four different types of fieldbuses [23].

Picture 9. ABB AC500 PLC with I/O and fieldbus options. [15]

1.8.1.2 Motor drives

A motor drive is a piece of equipment that can adjust the speed of a motor by

controlling the frequency [13]. Motor drives are used more frequently after the

development in techniques. The invention was released at the end of the 1970s when

a 5,5 kW drive was the width of a normal human being and nearly two meters high.

Today, a modern drive (or frequency converter) has significantly decreased in size,

now being a very small piece of equipment. A modern 5,5 kW drive is approximately

150 mm in height, 100 mm in width and 100 mm in depth. While the physical size of

a drive has decreased a great deal, the technical features have increased in many

ways. The most recent technical features in a drive are that they support many kinds

44

of fieldbuses, have some kind of integrated safety feature and the software can be

modified by the user. [24]

Picture 10. ABB ACS355 frequency converter for motor speed controlling. [16]

1.8.1.3 Visualization components

Visualization components are for example operator terminals such as HMI (Human

Machine Interfaces), displays that can show text and graphics and Industrial PC’s.

[13] HMI provides a practical user interface for machinery controlling. Usually a

HMI includes a touch screen or push buttons where a user can follow desired

variables and make changes to the configuration. Industrial PC’s are more

complicated equipment because they are able to control a full machine, including

several available options such as fieldbuses and I/O’s and in some cases IPC can be

used to replace PLC [12].

Picture 11. ABB CP650 control panel. [16]

45

1.8.1.4 Motion control

Motion control includes servo motors containing an integrated feedback device,

including brushed DC servo motors [13]. The range of servo motors is broad

including many options for feedback. The feedback is usually selected depending on

the need for accuracy, environment or price. The most versatile encoder type for

feedback is the multi-turn absolute encoder because it is extremely precise and the

shaft position information is genuine, even if the main supply is lost during the run.

Thus, it can be noted that the absolute encoder remembers its position permanently.

There are some weaknesses in absolute encoders because the principle is based on

optical activity, which is not as robust as the principle in resolver feedback. A servo

motor including resolver feedback can be mounted in harsh environments due to the

better duration in the resolver. The principle in the resolver is based on an

electromagnetic field surrounding the magnetic poles, and is therefore less vulnerable

to external threats [12].

Picture 12. ABB MS-servo motor series with resolver feedback. [18]

Fully enclosed servo drives with a single power output that can control the current,

speed or position of any servo motor are listed as motion control products. In multi-

axis systems each drive is counted individually. [13] A modern servo drive has to

have a position feedback because the repository is usually an application that needs

to be very dynamic and accurate. A servo drive can be controlled via fieldbus, pulse

train or digital or analog signals. [25]

46

Picture 13. ABB Microflex e150 servo drive with integrated EtherCat fieldbus. [19]

The remaining products under motion control are the stepper motors with or without

feedback, 2-, 3- or 5-phase, hybrid and stepper motors with an integrated drive. If the

drive is supplied separately it is considered a fully enclosed stepper drive or amplifier

for the controlling of speed and position in stepper motors. [13]

Picture 14. ABB DSMS-series stepper motors with integrated drive. [20]

The fifth main component under motion control is the position controller. The

definition of a position controller is that the structure is PLC-based, PC-based or a

stand-alone type. In picture 15, a typical position controller provided by ABB is

shown. Usually a position controller is able to run several axes at the same time by

using I/O’s or a fieldbus. The power supply is not fed from the position controller but

the information on desired speed, position or torque is. A position controller is

connected to the drive which runs the motor. [21]

47

Picture 15. ABB NextMove e100 motion controller. [21]

1.8.1.5 Other automation products

The following components are listed under Other automation components:

Pneumatic components, hydraulic drives and valves, mechanical linear & rotary

handling systems, machine-safety products, low-voltage products, machine-vision

systems and other automation equipment.

48

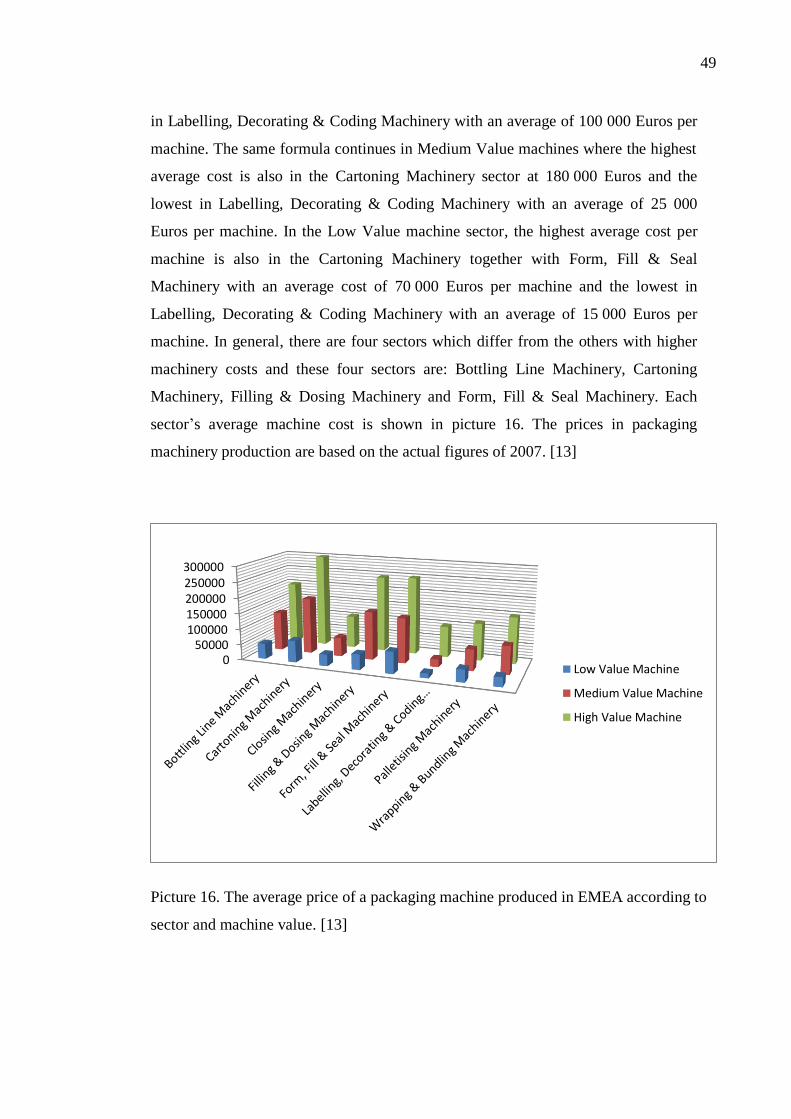

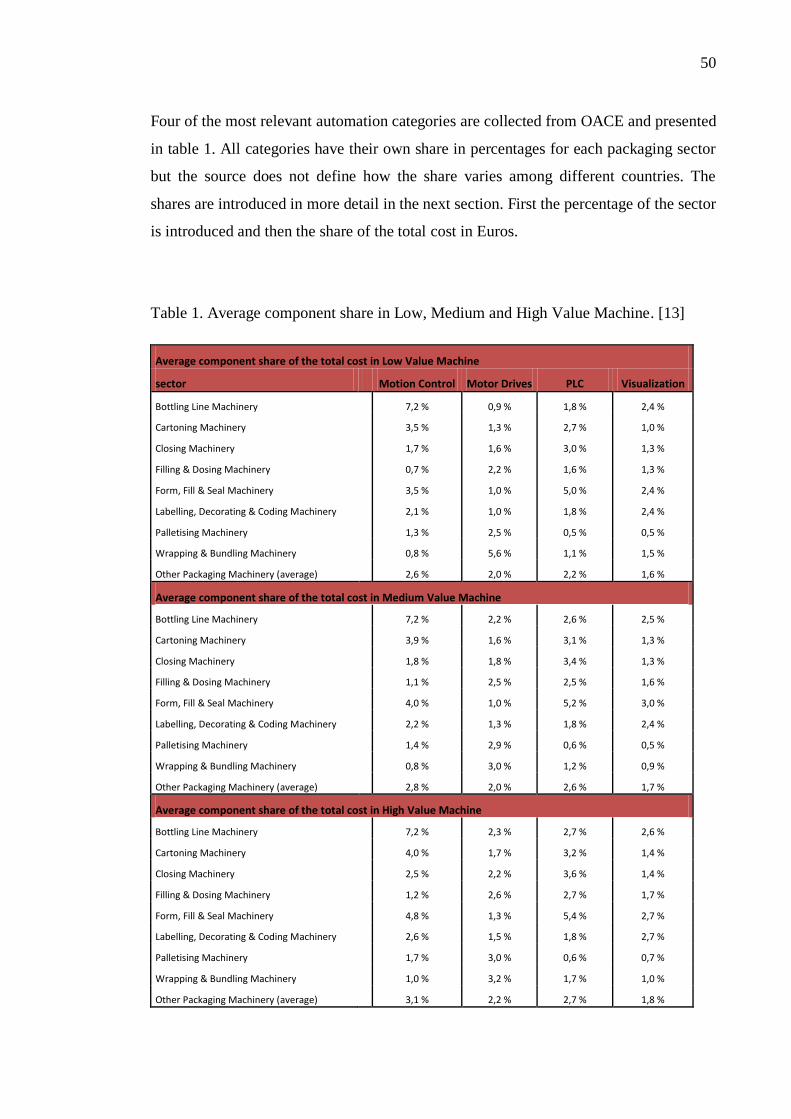

1.9 Cost structure of a packaging machine produced in EMEA

In this part of the research, the Packaging machine cost structure is introduced in

more detail and with the total cost of a packaging machine in mind. As described

earlier, the packaging machinery industry is divided into eight (or nine if sector

Other is taken into account) different sectors, and each sector is split into three value

levels; low, medium and high. All levels are examined separately with the same

indicators. There are five different indicators which are under exploration:

The total cost of a packaging machine