Morgan Stanley Global Consumer Conference Morgan Stanley Global Consumer Conference John Cahill Chairman & CEO Al Drewes Chief Financial Officer John Cahill Chairman & CEO Al Drewes Chief Financial Officer November 6, 2003 November 6, 2003

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Morgan StanleyGlobal Consumer ConferenceMorgan StanleyGlobal Consumer Conference

John CahillChairman & CEO

Al DrewesChief Financial Officer

John CahillChairman & CEO

Al DrewesChief Financial Officer

November 6, 2003November 6, 2003

Statements made in this presentation that relate to futureperformance or financial results of this company areforward-looking statements, which involve uncertaintiesthat could cause actual performance or results to materiallydiffer. We undertake no obligation to update any of thesestatements. Listeners are cautioned not to place unduereliance on these forward-looking statements. Thesestatements should be taken in conjunction with theadditional information about risk and uncertainties setforth in the company’s annual report on Form 10-K.

Statements made in this presentation that relate to futureperformance or financial results of this company areforward-looking statements, which involve uncertaintiesthat could cause actual performance or results to materiallydiffer. We undertake no obligation to update any of thesestatements. Listeners are cautioned not to place unduereliance on these forward-looking statements. Thesestatements should be taken in conjunction with theadditional information about risk and uncertainties setforth in the company’s annual report on Form 10-K.

Perspective on ProgressPerspective on Progress

• Financial Outlook• Financial Outlook

• Priority 2: Improving Performance in Mexico• Priority 2: Improving Performance in Mexico

• Priority 1: Achieving Topline Growth in the U.S.• Priority 1: Achieving Topline Growth in the U.S.

Perspective on ProgressPerspective on Progress

• Priority 1: Achieving Topline Growth in the U.S.• Priority 1: Achieving Topline Growth in the U.S.

U.S. Topline MomentumU.S. Topline Momentum

• Second Half Actions ProvideMomentum into 2004

– Volume Improving– Pricing Trends Solid– Continued Strong Execution

• Second Half Actions ProvideMomentum into 2004

– Volume Improving– Pricing Trends Solid– Continued Strong Execution

Customer DynamicsCustomer DynamicsConsumer Trends Drive Focus and OpportunityConsumer Trends Drive Focus and Opportunity

• Pressure on ColaGrowth asConsumption Shifts

• Innovation Requiredto Fuel Growth

• Importance of ColdDrink and FoodService

• Opportunity toIncrease Can Pricing

• Pressure on ColaGrowth asConsumption Shifts

• Innovation Requiredto Fuel Growth

• Importance of ColdDrink and FoodService

• Opportunity toIncrease Can Pricing

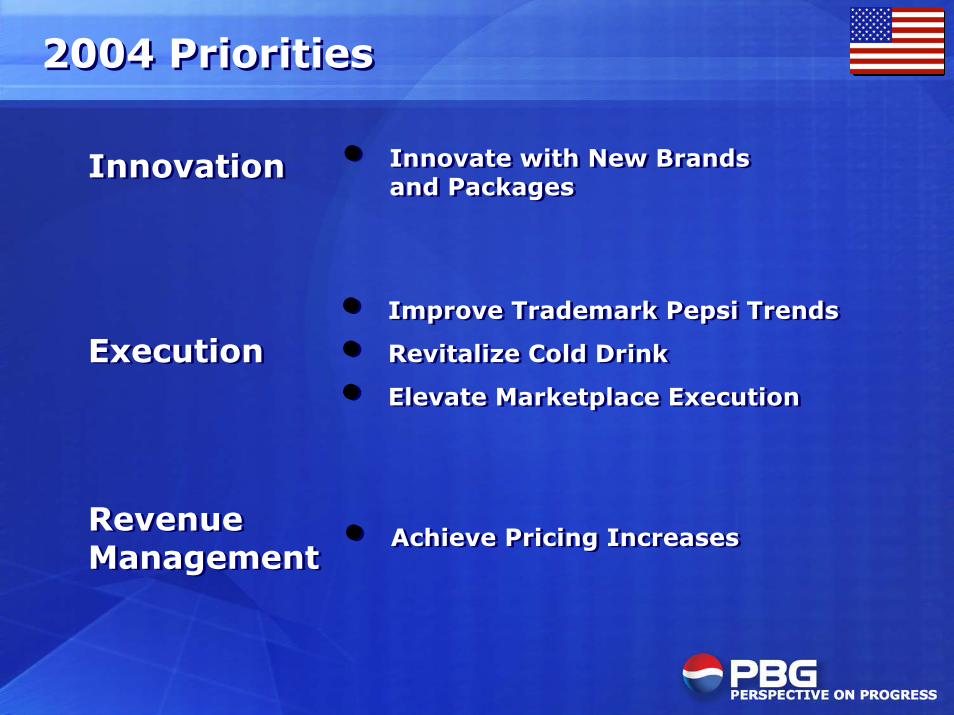

2004 Priorities2004 Priorities

InnovationInnovation • Innovate with New Brandsand Packages

• Innovate with New Brandsand Packages

• Achieve Pricing Increases• Achieve Pricing Increases

• Improve Trademark Pepsi Trends

• Revitalize Cold Drink

• Elevate Marketplace Execution

• Improve Trademark Pepsi Trends

• Revitalize Cold Drink

• Elevate Marketplace Execution

ExecutionExecution

RevenueManagementRevenueManagement

� Innovation - Brands� Innovation - Brands

� Innovation - Brands� Innovation - Brands

� Innovation - Brands� Innovation - Brands

“Greatest orange drinkever created…”“Greatest orange drinkever created…”

“You should reallyrethink this…”“You should reallyrethink this…”

“It is morallywrong…”“It is morallywrong…”

� Innovation - Package� Innovation - Package

Fridge MateFridge Mate

� Innovation - Package� Innovation - Package

8 oz. Cans8 oz. Cans

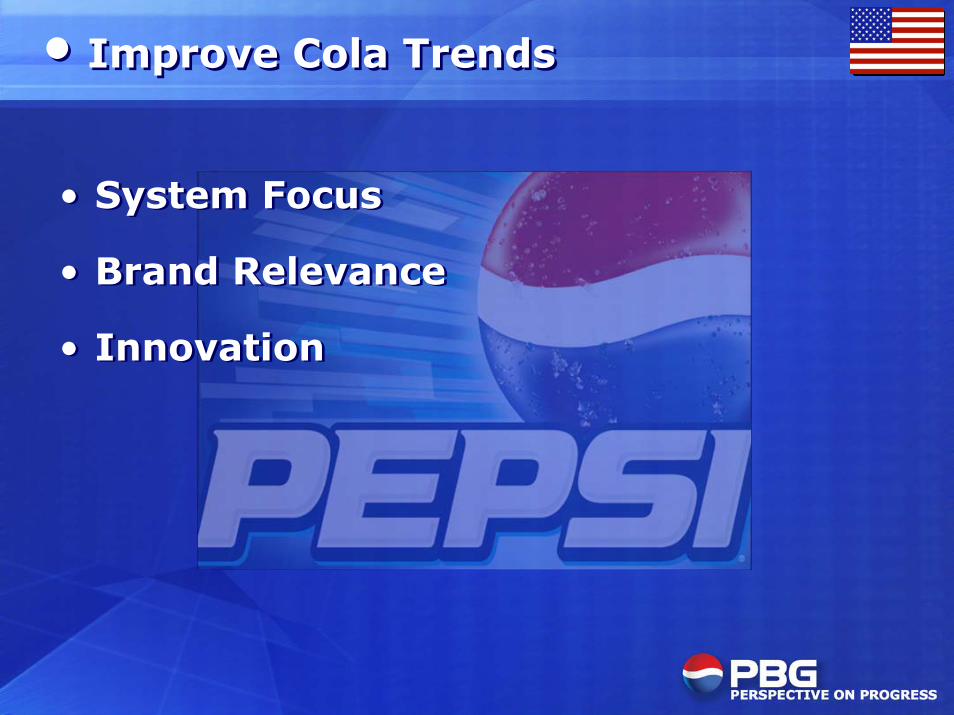

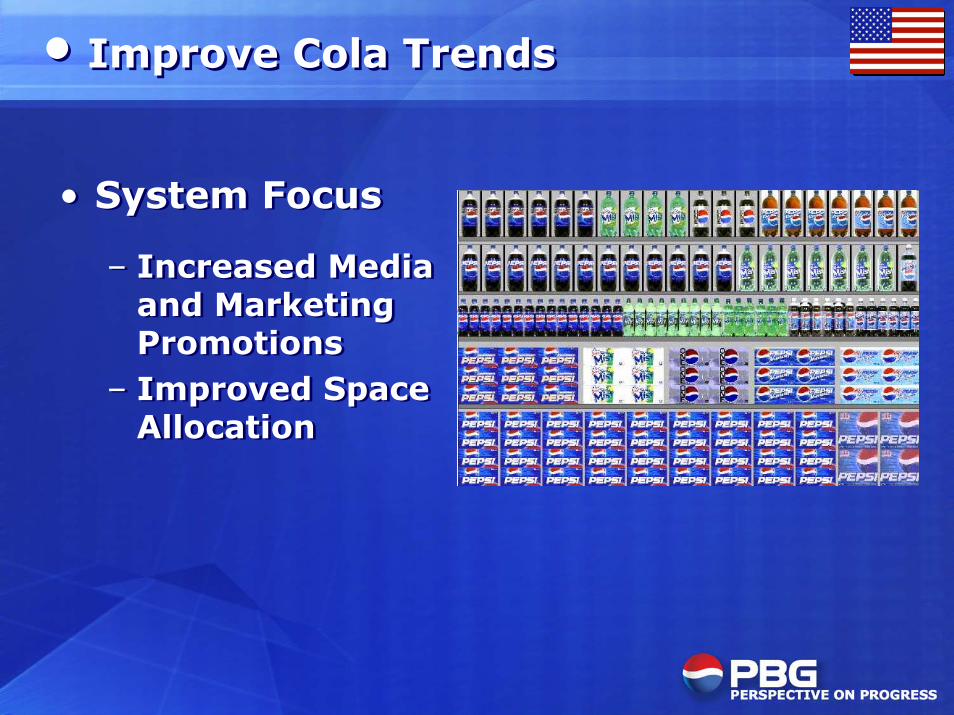

• Improve Cola Trends• Improve Cola Trends

• Improve Cola Trends• Improve Cola Trends

• System Focus

• Brand Relevance

• Innovation

• System Focus

• Brand Relevance

• Innovation

• Improve Cola Trends• Improve Cola Trends

• System Focus

– Increased Mediaand MarketingPromotions

– Improved SpaceAllocation

• System Focus

– Increased Mediaand MarketingPromotions

– Improved SpaceAllocation

• Improve Cola Trends• Improve Cola Trends

• Brand Relevance

– Dialing Up Diets– Marketing

Promotions• Super Bowl• iTunes• Academy

Awards

• Brand Relevance

– Dialing Up Diets– Marketing

Promotions• Super Bowl• iTunes• Academy

Awards

• Improve Cola Trends• Improve Cola Trends

• Innovation

– Pepsi Vanilla– New Packaging

• Innovation

– Pepsi Vanilla– New Packaging

• Revitalize Cold Drink• Revitalize Cold Drink

� Elevate Marketplace Execution� Elevate Marketplace ExecutionAquafina: The DSD AdvantageAquafina: The DSD Advantage

� Elevate Marketplace Execution� Elevate Marketplace ExecutionAquafina: The DSD AdvantageAquafina: The DSD Advantage

• Majority of PBGMarkets Have PricingOpportunities

• Framework forAchieving Rate andMix Improvements

• CSDs Continue toOffer GreatConsumer Value

• Majority of PBGMarkets Have PricingOpportunities

• Framework forAchieving Rate andMix Improvements

• CSDs Continue toOffer GreatConsumer Value

� Net Revenue per Case Management� Net Revenue per Case Management

2004 Target: Increase of 2%2004 Target: Increase of 2%

U.S. SummaryU.S. Summary

• Innovate with New Brands and Packages

• Improve Trademark Pepsi Trends

• Revitalize Cold Drink

• Elevate Marketplace Execution

• Achieve Pricing Increases

• Innovate with New Brands and Packages

• Improve Trademark Pepsi Trends

• Revitalize Cold Drink

• Elevate Marketplace Execution

• Achieve Pricing Increases

Perspective on ProgressPerspective on Progress

• Priority 2: Improving Performance in Mexico• Priority 2: Improving Performance in Mexico

Improving Performance in MexicoImproving Performance in Mexico

Improving Performance in MexicoImproving Performance in Mexico

Central

South

Southeast

Mexico TerritoriesMexico Territories

Northeast

Metro

Brand and Channel OverviewBrand and Channel Overview

• Weak Macroeconomic Factors

• Cost and Competitive Pressures

• Weak Macroeconomic Factors

• Cost and Competitive Pressures

2003 Dynamics2003 Dynamics

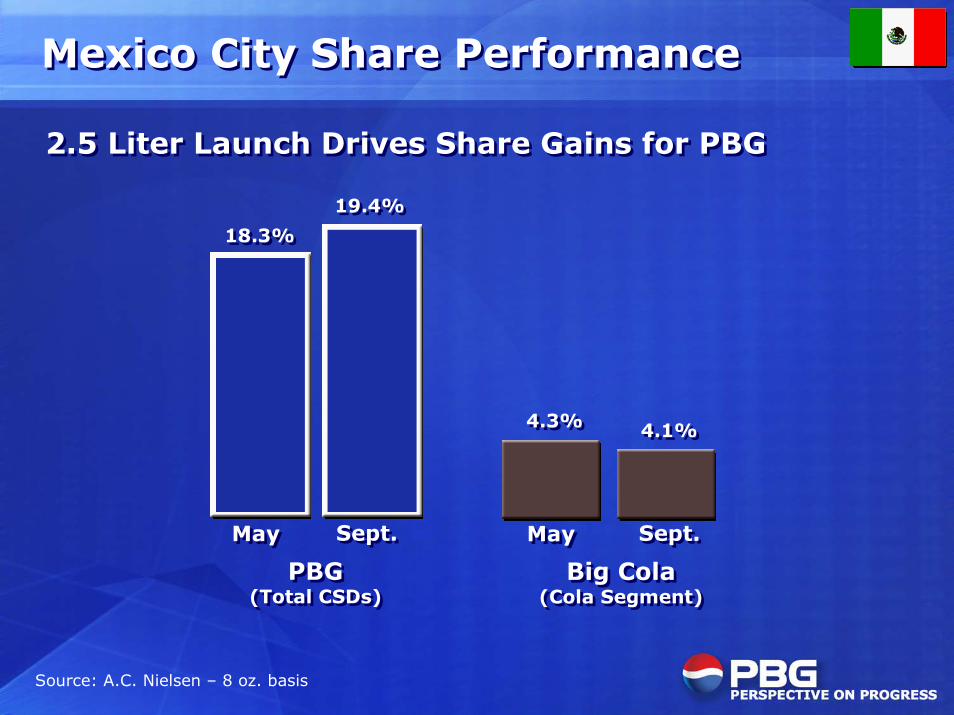

Mexico City PerformanceMexico City Performance

2.5 Liter Launch Drives Share Gains for PBG2.5 Liter Launch Drives Share Gains for PBG

Mexico City Share PerformanceMexico City Share Performance

18.3%18.3%

MayMay Sept.Sept.

PBG(Total CSDs)

PBG(Total CSDs)

19.4%19.4%

4.3%4.3%

MayMay Sept.Sept.

Big Cola(Cola Segment)

Big Cola(Cola Segment)

4.1%4.1%

Source: A.C. Nielsen – 8 oz. basis

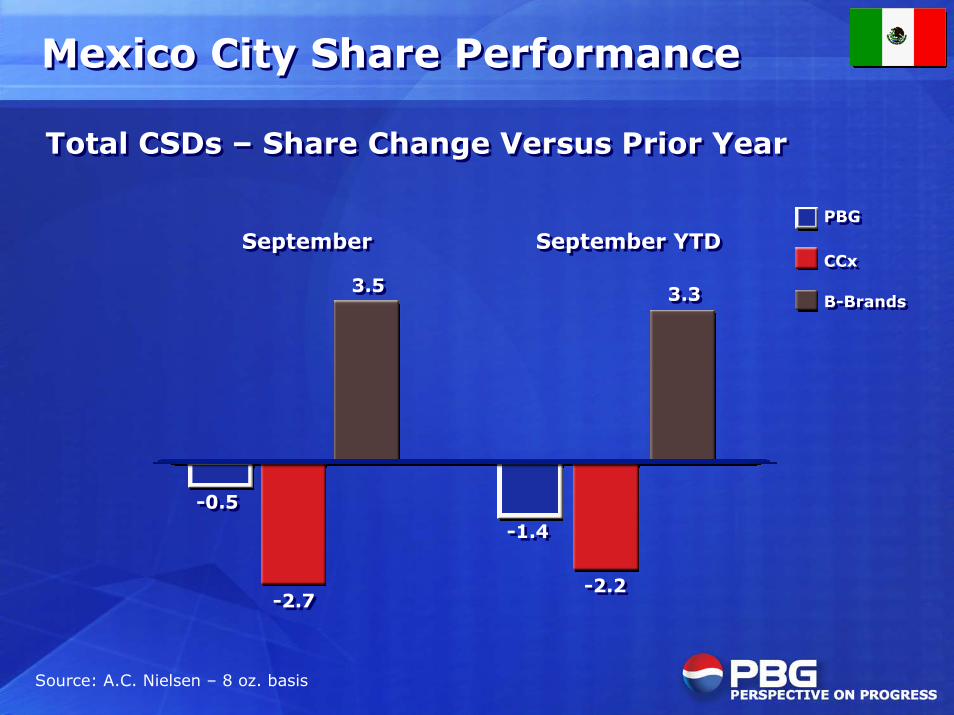

Mexico City Share PerformanceMexico City Share Performance

Total CSDs – Share Change Versus Prior YearTotal CSDs – Share Change Versus Prior Year

SeptemberSeptember September YTDSeptember YTD

3.53.5

-2.7-2.7

-0.5-0.5

-2.2-2.2

-1.4-1.4

3.33.3

PBGPBG

CCxCCx

B-BrandsB-Brands

Source: A.C. Nielsen – 8 oz. basis

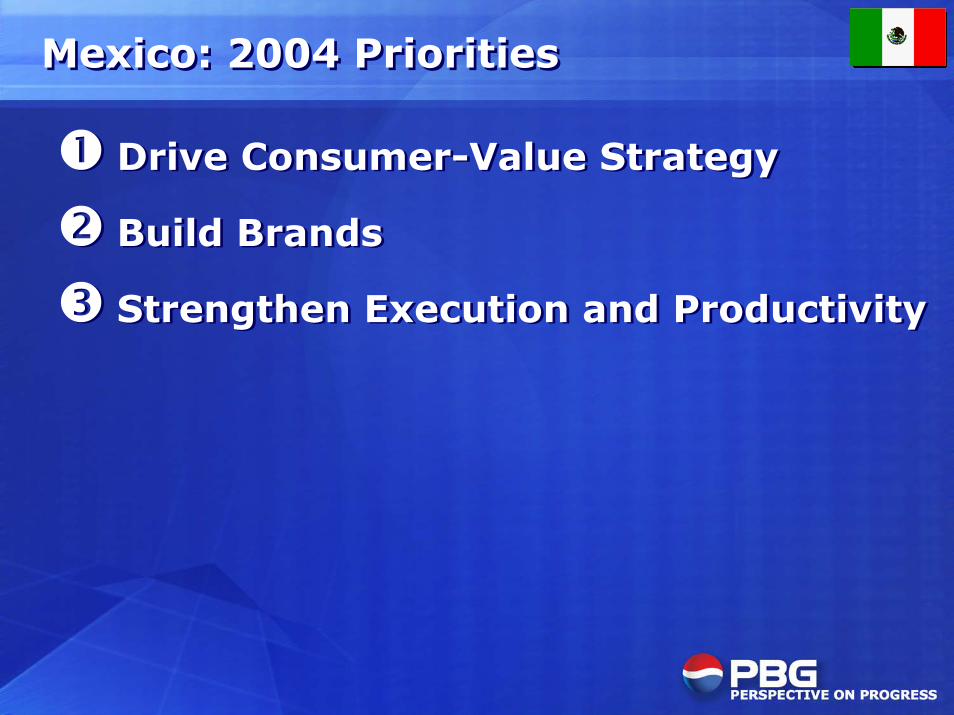

Mexico: 2004 PrioritiesMexico: 2004 Priorities

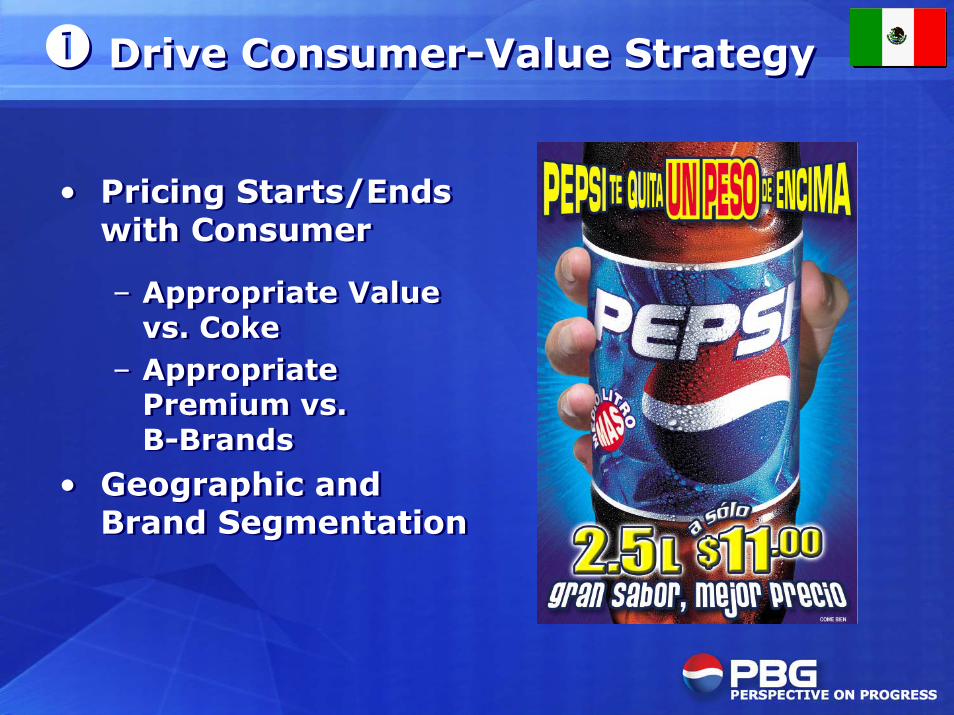

� Drive Consumer-Value Strategy

� Build Brands

� Strengthen Execution and Productivity

� Drive Consumer-Value Strategy

� Build Brands

� Strengthen Execution and Productivity

• Pricing Starts/Endswith Consumer

– Appropriate Valuevs. Coke

– AppropriatePremium vs.B-Brands

• Geographic andBrand Segmentation

• Pricing Starts/Endswith Consumer

– Appropriate Valuevs. Coke

– AppropriatePremium vs.B-Brands

• Geographic andBrand Segmentation

� Drive Consumer-Value Strategy� Drive Consumer-Value Strategy

� Build Brands� Build Brands

� Build Brands - Electropura� Build Brands - Electropura

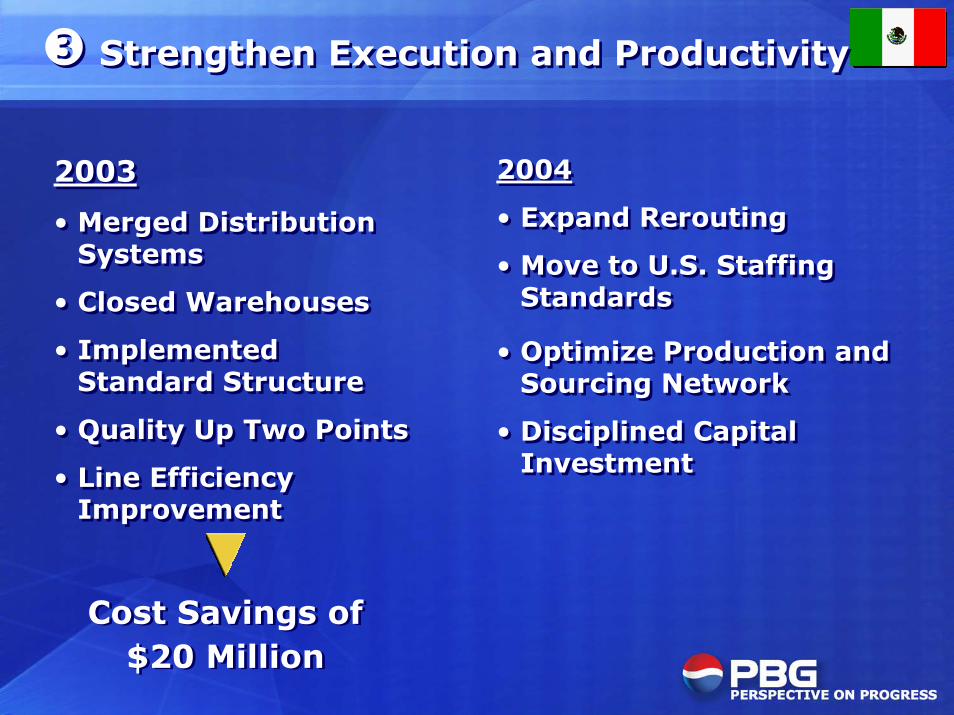

2004

• Expand Rerouting

• Move to U.S. StaffingStandards

• Optimize Production andSourcing Network

• Disciplined CapitalInvestment

2004

• Expand Rerouting

• Move to U.S. StaffingStandards

• Optimize Production andSourcing Network

• Disciplined CapitalInvestment

2003

• Merged DistributionSystems

• Closed Warehouses

• ImplementedStandard Structure

• Quality Up Two Points

• Line EfficiencyImprovement

2003

• Merged DistributionSystems

• Closed Warehouses

• ImplementedStandard Structure

• Quality Up Two Points

• Line EfficiencyImprovement

� Strengthen Execution and Productivity� Strengthen Execution and Productivity

Cost Savings of$20 Million

Cost Savings of$20 Million

Mexico SummaryMexico Summary

Perspective on ProgressPerspective on Progress

• Financial Outlook• Financial Outlook

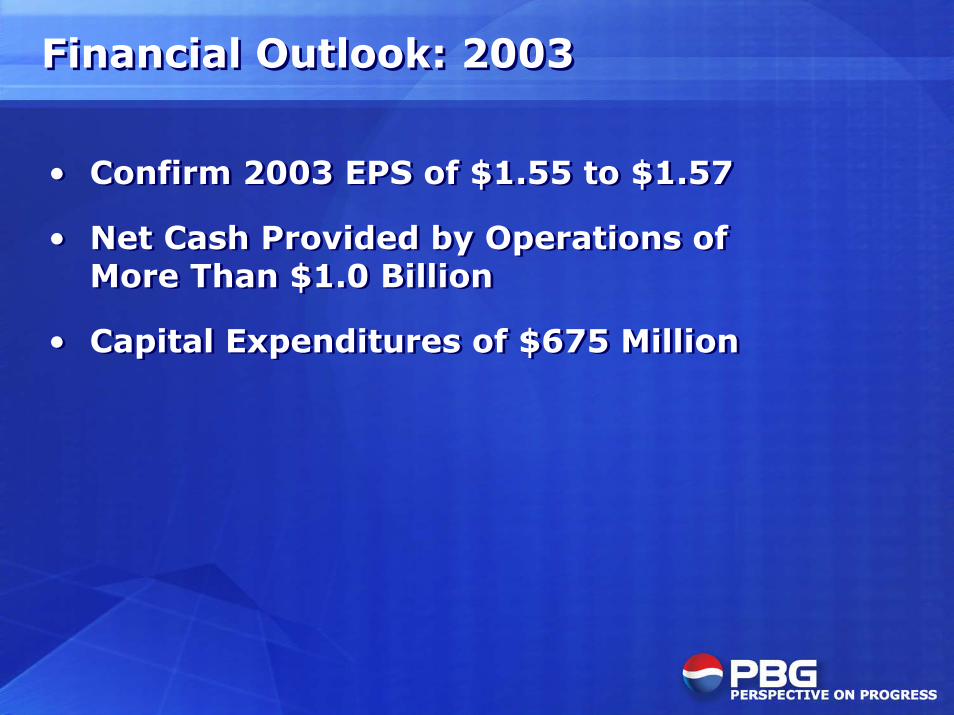

Financial Outlook: 2003Financial Outlook: 2003

• Confirm 2003 EPS of $1.55 to $1.57

• Net Cash Provided by Operations ofMore Than $1.0 Billion

• Capital Expenditures of $675 Million

• Confirm 2003 EPS of $1.55 to $1.57

• Net Cash Provided by Operations ofMore Than $1.0 Billion

• Capital Expenditures of $675 Million

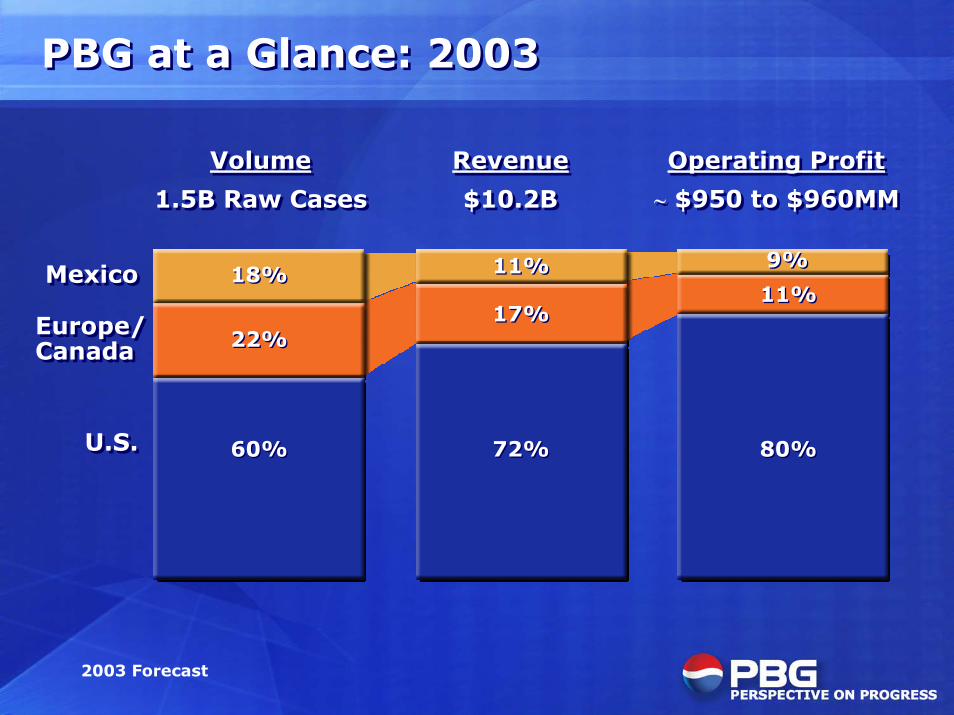

PBG at a Glance: 2003PBG at a Glance: 2003

Operating Profit

� $950 to $960MM

Operating Profit

� $950 to $960MMRevenue

$10.2B

Revenue

$10.2B

2003 Forecast

MexicoMexico

60%60%

22%22%

18%18%

72%72%

17%17%

11%11%

80%80%

11%11%

9%9%

Volume

1.5B Raw Cases

Volume

1.5B Raw Cases

Europe/Canada Europe/Canada

U.S.U.S.

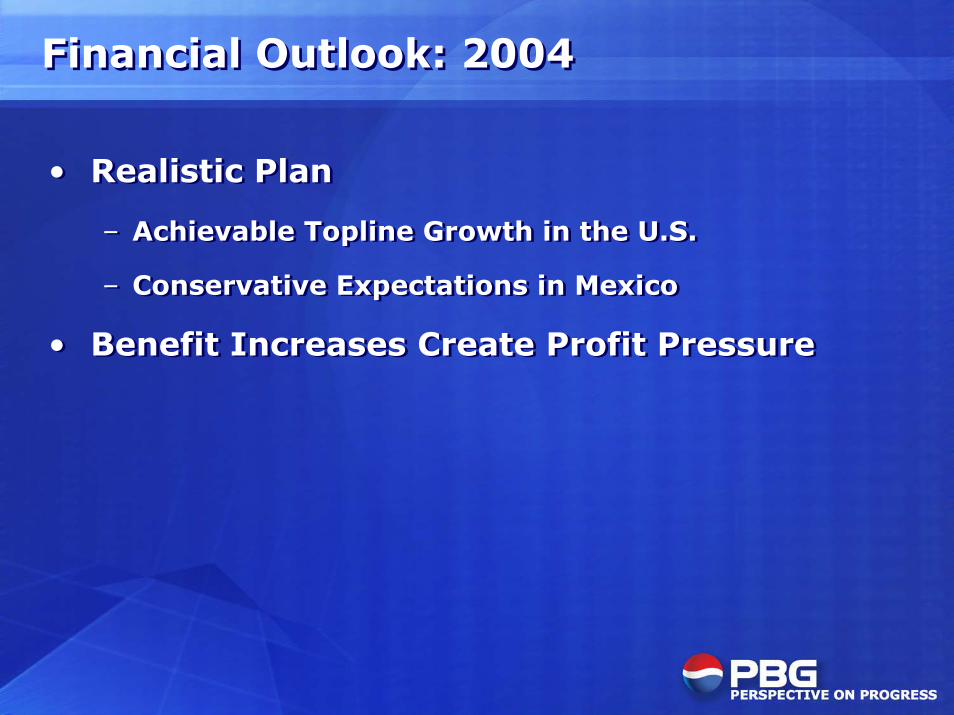

Financial Outlook: 2004Financial Outlook: 2004

• Realistic Plan

– Achievable Topline Growth in the U.S.

– Conservative Expectations in Mexico

• Benefit Increases Create Profit Pressure

• Realistic Plan

– Achievable Topline Growth in the U.S.

– Conservative Expectations in Mexico

• Benefit Increases Create Profit Pressure

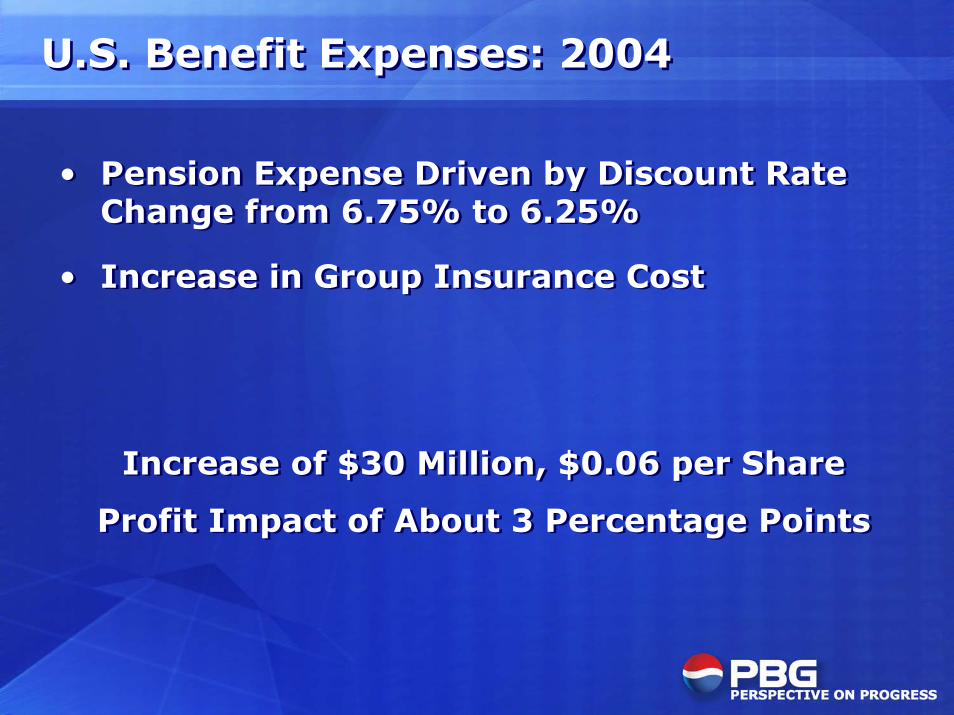

U.S. Benefit Expenses: 2004U.S. Benefit Expenses: 2004

• Pension Expense Driven by Discount RateChange from 6.75% to 6.25%

• Increase in Group Insurance Cost

• Pension Expense Driven by Discount RateChange from 6.75% to 6.25%

• Increase in Group Insurance Cost

Increase of $30 Million, $0.06 per Share

Profit Impact of About 3 Percentage Points

Increase of $30 Million, $0.06 per Share

Profit Impact of About 3 Percentage Points

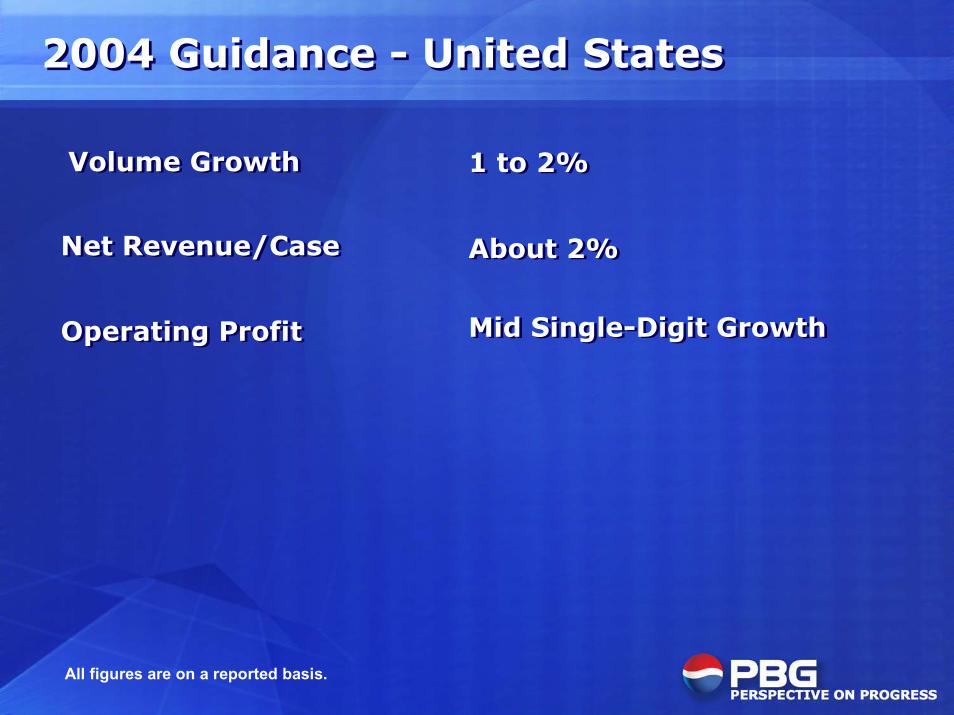

2004 Guidance - United States2004 Guidance - United States

1 to 2%1 to 2%

Net Revenue/CaseNet Revenue/Case

Operating ProfitOperating Profit

About 2%About 2%

Mid Single-Digit GrowthMid Single-Digit Growth

Volume GrowthVolume Growth

All figures are on a reported basis.

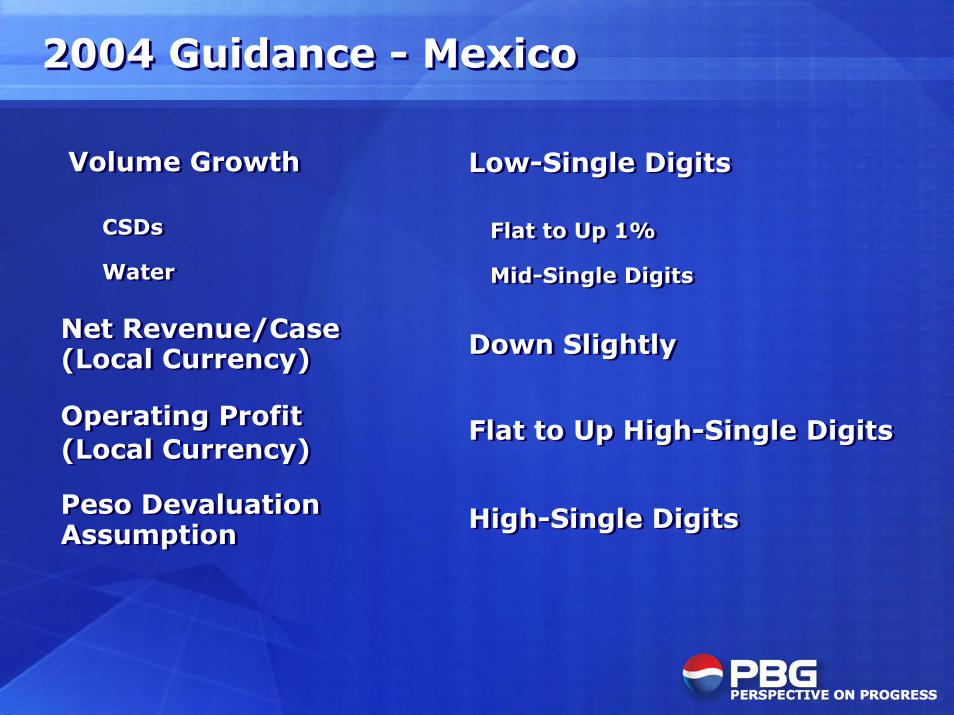

2004 Guidance - Mexico2004 Guidance - Mexico

CSDs

Water

CSDs

Water

Net Revenue/Case(Local Currency)Net Revenue/Case(Local Currency)

Operating Profit(Local Currency)Operating Profit(Local Currency)

Peso DevaluationAssumptionPeso DevaluationAssumption

Flat to Up 1%

Mid-Single Digits

Flat to Up 1%

Mid-Single Digits

Down SlightlyDown Slightly

Flat to Up High-Single DigitsFlat to Up High-Single Digits

High-Single DigitsHigh-Single Digits

Low-Single DigitsLow-Single DigitsVolume GrowthVolume Growth

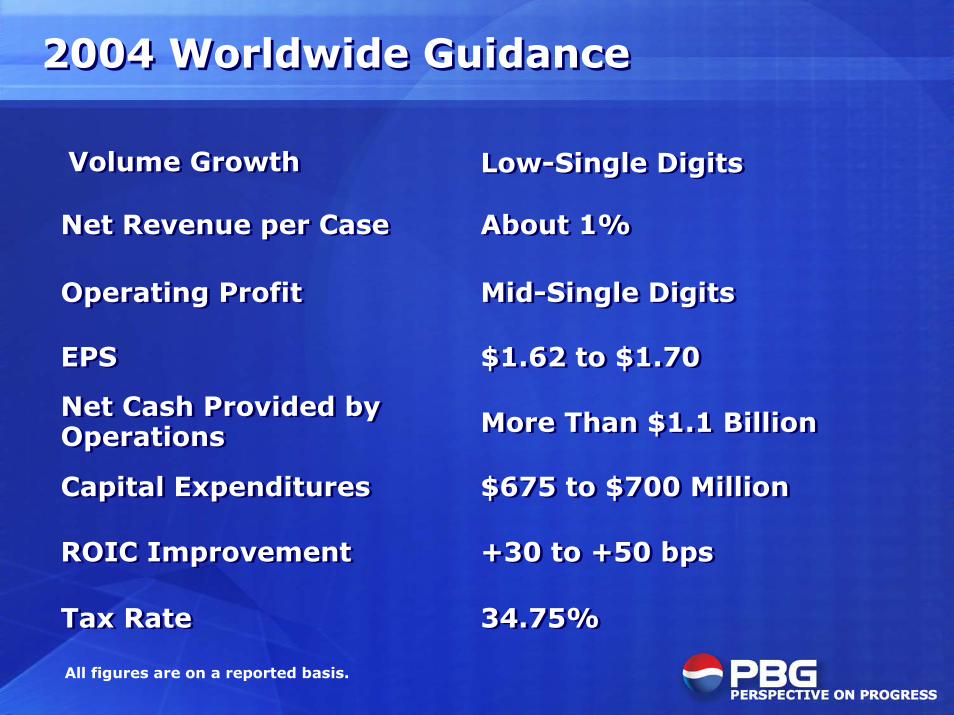

2004 Worldwide Guidance2004 Worldwide Guidance

All figures are on a reported basis.

EPSEPS

Net Cash Provided byOperationsNet Cash Provided byOperations

Capital ExpendituresCapital Expenditures

ROIC ImprovementROIC Improvement

Tax RateTax Rate

Net Revenue per CaseNet Revenue per Case

Operating ProfitOperating Profit

$1.62 to $1.70$1.62 to $1.70

More Than $1.1 BillionMore Than $1.1 Billion

$675 to $700 Million$675 to $700 Million

+30 to +50 bps+30 to +50 bps

34.75%34.75%

About 1%About 1%

Mid-Single DigitsMid-Single Digits

Low-Single DigitsLow-Single DigitsVolume GrowthVolume Growth

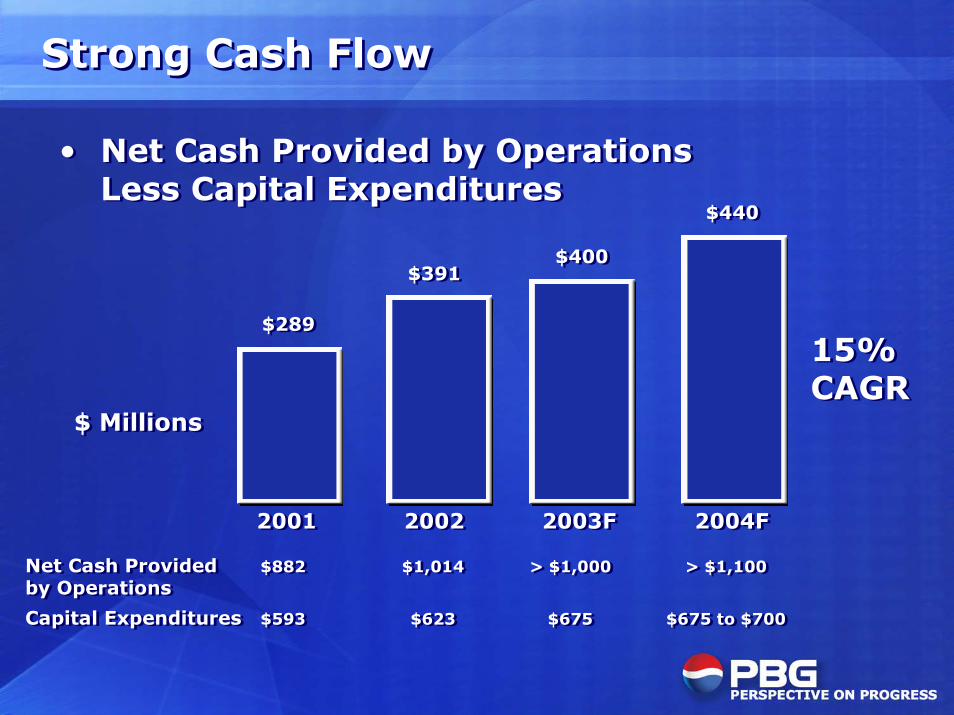

Strong Cash FlowStrong Cash Flow

• Net Cash Provided by OperationsLess Capital Expenditures

• Net Cash Provided by OperationsLess Capital Expenditures

$289$289

$391$391$400$400

$440$440

20012001 20022002 2003F2003F 2004F2004F

$ Millions$ Millions

15%CAGR15%CAGR

Net Cash Provided $882 $1,014 > $1,000 > $1,100by Operations

Capital Expenditures $593 $623 $675 $675 to $700

Net Cash Provided $882 $1,014 > $1,000 > $1,100by Operations

Capital Expenditures $593 $623 $675 $675 to $700

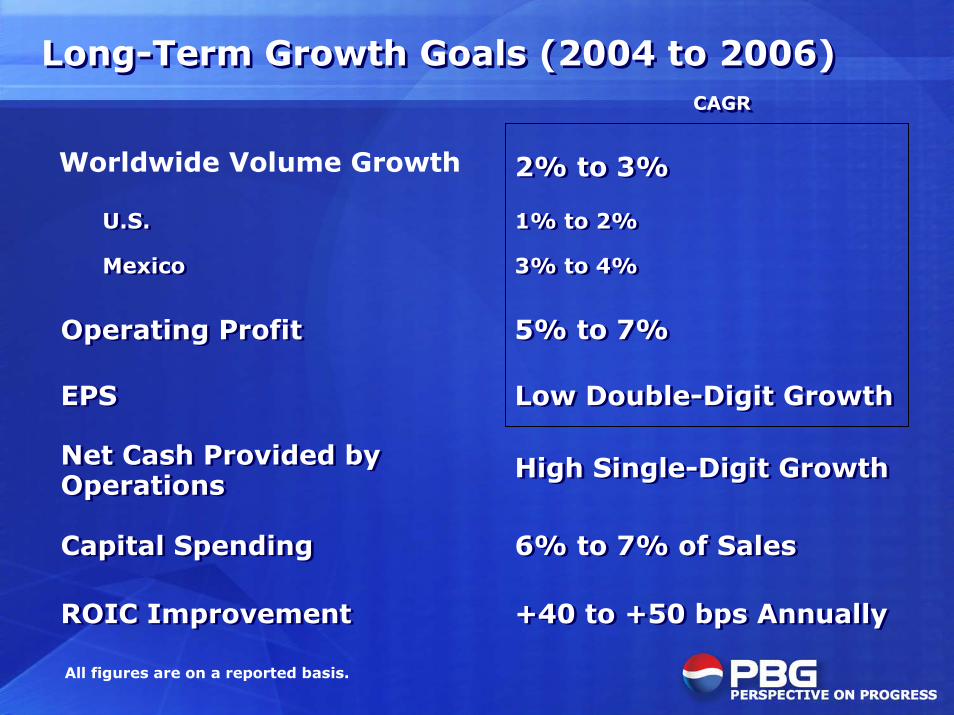

Long-Term Growth Goals (2004 to 2006)Long-Term Growth Goals (2004 to 2006) CAGR CAGR

EPSEPS

Net Cash Provided byOperationsNet Cash Provided byOperations

2% to 3%2% to 3%

1% to 2%

3% to 4%

1% to 2%

3% to 4%

Operating ProfitOperating Profit 5% to 7%5% to 7%

Low Double-Digit GrowthLow Double-Digit Growth

High Single-Digit GrowthHigh Single-Digit Growth

U.S.

Mexico

U.S.

Mexico

Capital SpendingCapital Spending 6% to 7% of Sales6% to 7% of Sales

ROIC ImprovementROIC Improvement +40 to +50 bps Annually+40 to +50 bps Annually

All figures are on a reported basis.

Worldwide Volume Growth

SummarySummary

• Goals Are Clear

• Organization Is Focused

• Plans Address Challenges

• Strong Cash Flow Growth

• Continued Improvement in ROIC

• Goals Are Clear

• Organization Is Focused

• Plans Address Challenges

• Strong Cash Flow Growth

• Continued Improvement in ROIC

Related Documents