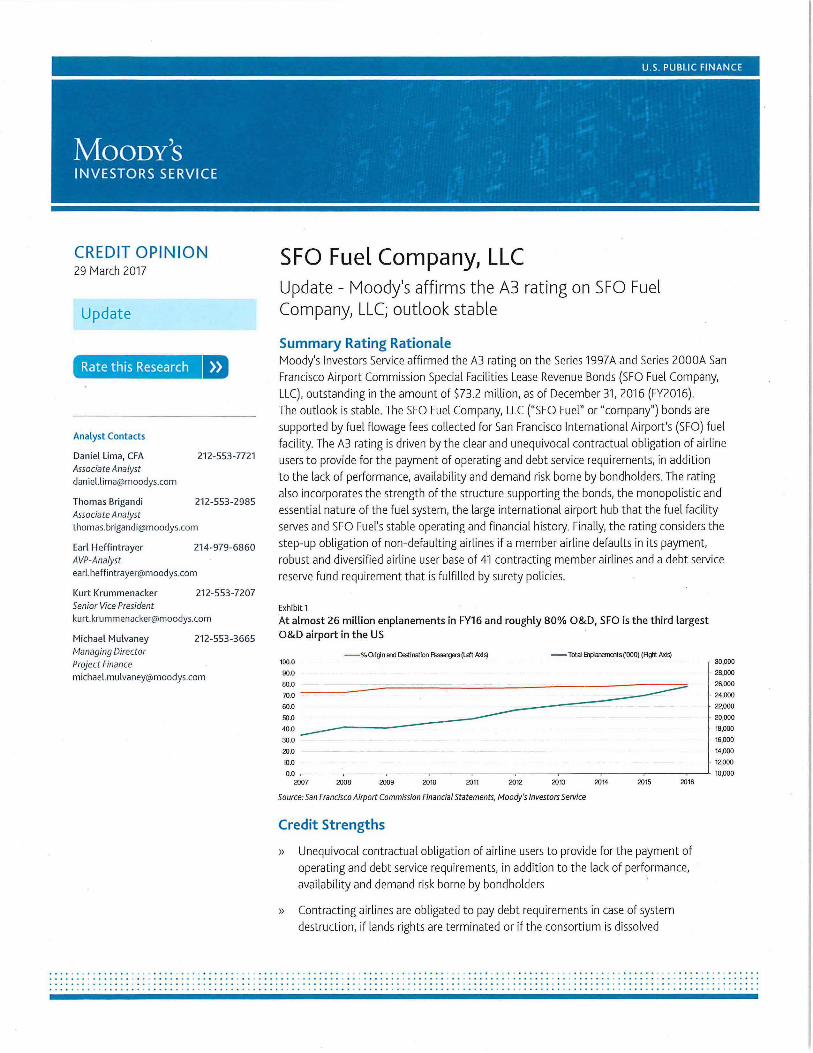

U.S. PUBLIC FINANCE CREDIT OPINION SFO Fuel Company, LLC 29 tvlarch 2017 Update - Moody's affirms the A3 rating on SFO Fuel Update Company 1 LLC; outlook stable Summary Rating Rationale tvloody's Investors Service affirmed the A3 rating on the Series 1997A and Series 2000A San Rate this Research Francisco Airport Commission Special Facilities Lease Revenue Bonds (SFO Fuel Company, LLC), outstanding in the amount of $73.2 million, as of December 31, 2016 (FY2016). The outlook is stable. The SFO Fuel Company, LLC ("SFO Fuel" or "company") bonds are supported by fuel flowage fees collected for San Francisco International Airport's (SFO) fuel Analyst Contacts facility. The A3 rating is driven by the clear and unequivocal contractual obligation of airline Daniel Lima, CFA 212-553-7721 users to provide for the payment of operating and debt service requirements, in addition Associate Analyst to the lack of performance, availability and demand risk borne by bondholders. The rating dani [email protected] also incorporates the strength of the structure supporting the bonds, the monopolistic and Thomas Bri ga nd i 212-553-2985 essential nature of the fuel system, the large international airport hub that the fuel facility Associate Analyst thomas. brigan [email protected] serves and SFO Fuel's stable operating and financial history. Finally, the rating consid ers the step-up obligation of non-defaulting airlines if a member airline defaults in its payment, Earl Heff int rayer 214- 979-6 860 AVP-Analyst robust and diversified airline user base of 41 contracting member airlines and a debt service ear l.heffintraye[email protected] reserve fund requirement that is fulfilled by surety policies. Kurt Krummenacker 212-553-7207 Senior Vice Presi de nt E xh ibit 1 kurt .krummenacke[email protected] At almost 26 million enplanements in FY16 and roughly 80% O&D, SFO is the third Largest O&D airport in the US Michael Mulvaney 212-553-3665 /\1a nagin g Director - % Oajn ind Deli nation Passalgers (Lett Axis) - Total EilPanements{"OOO) (Rgit Axis) 100.0 30.000 Project Fina nce 9Q.O 28.000 michae l.mulvaney@ moodys.com 80.0 ---------- -- --- - -- ---- ---- 26.000 7U.O · 24,000 60.0 22,000 50.0 -------------- . 20,000 40.0 ---- 18,000 30.0 . 16,000 20.0 14,000 10.0 12.000 0.0 10.000 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Source: San Francisco Airport Commission Financial Statements, Moody's Investors Service Credit Strengths » Unequivocal contractual obligation of airline users to provide for the payment of operating and debt service requirements, in addition to the lack of performance, availability and demand risk borne by bondhold ers ' » Contracting airlines are obligated to pay debt require ments in case of system destruction, if lands rights are terminated or if the consortium is d. issolved .. .. .... .. .......... .. .. . .. .. . .. ....... .. ... .. .. .... ... . .. . .. .. .. .. . .. .. ...... .. .... .. . .. .. .......... .. .. . .. .. ...... .. .. .. .. .. ...

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

US PUBLIC FINANCE

CREDIT OPINION SFO Fuel Company LLC 29 tvlarch 2017

Update - Moodys affirms the A3 rating on SFO Fuel

Update Company1 LLC outlook stable

Summary Rating Rationale tvloodys Investors Service affirmed the A3 rating on the Series 1997A and Series 2000A SanRate this Research Francisco Airport Commission Special Facilities Lease Revenue Bonds (SFO Fuel Company LLC) outstanding in the amount of $732 million as of December 31 2016 (FY2016) The outlook is stable The SFO Fuel Company LLC (SFO Fuel or company) bonds are supported by fuel flowage fees collected for San Francisco International Airports (SFO) fuel

Analyst Contacts facility The A3 rating is driven by the clear and unequivocal contractual obligation of airline

Daniel Lima CFA 212-553-7721 users to provide for the payment of operating and debt service requirements in addition Associate Analyst

to the lack of performance availability and demand risk borne by bondholders The ratingdaniellimamoodyscom also incorporates the strength of the structure supporting the bonds the monopolistic and

Thomas Brigandi 212-553-2985 essential nature of the fuel system the large international airport hub that the fuel facilityAssociate Analyst

thomasbrigandimoodyscom serves and SFO Fuels stable operating and financial history Finally the rating considers the step-up obligation of non-defaulting airlines if a member airline defaults in its paymentEarl Heffint rayer 214-979-6860

AVP-Analyst robust and diversified airline user base of 41 contracting member airlines and a debt service earlheffintrayermoodyscom reserve fund requirement that is fulfilled by surety policies Kurt Krummenacker 212-553-7207 Senior Vice President Exh ibit 1 kurt krummenackermoodyscom At almost 26 million enplanements in FY16 and roughly 80 OampD SFO is the third Largest

OampD airport in the USMichael Mulvaney 212-553-3 665 1a nagin g Director - Oajn ind Delination Passalgers (Lett Axis) - Total EilPanementsOOO) (Rgit Axis)

1000 30000 Project Finance 9QO 28000michae lmulvaney moodyscom 800 ---------------- ------ ---- 26000 7UO ~ middot 24000

600 22000

500 -------------- 20000 400 ---- 18000 300 16000

200 14000

100 12000

00 ------------~---------------~ 10000 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Source San Francisco Airport Commission Financial Statements Moodys Investors Service

Credit Strengths

raquo Unequivocal contractual obligation of airline users to provide for the payment of operating and debt service requirements in addition to the lack of performance availability and demand risk borne by bondholders

raquo Contracting airlines are obligated to pay debt require ments in case of system destruction if lands rights are terminated or if the consortium is dissolved

MOODYS INVESTORS SERVICE US PUBLIC FINANCE

raquo Fuel facility lease is coterminous with outstanding bonds maturity

raquo Pledge of facilities rent from all member airlines with a step-up requirement for all members for any financial shortfalls

raquo Monopoly provider of jet fuel at the third largest US airport by OampD enplanements

raquo History of limited expenditure growth and strong fee collection from non-members and airlines in bankruptcy keep costs low for member airlines

Credit Challenges

raquo Debt service reserve fund a key structural component providing critical liquidity to manage disruptions in debt service payments is funded through sureties

raquo Sum sufficient rate covenant and limited requirements for issuing additional bonds provide weak legal protections to bondholders

raquo Potential for additional costs from necessary system improvements environmental remediation or changes in environmental legislation that require system modifications

Rating Outlook The stable outlook is based on Moodys expectation that the contracting airline profile will remain fairly stable and the airlines will continue to provide full financial support for all costs related to the fuel system including any additional increases in capital costs

Factors that Could Lead to an Upgrade

raquo Cash funding the debt service reserve fund

raquo Improved financial position of member airlines

raquo Greater cash reserves

Factors that Could Lead to a Downgrade

raquo Dramatic changes in environmental remediation costs or in capital costs needed to keep the system in compliance with tightening environmental legislation

raquo Events that reduce the strong market position of SFO relative to major nearby airports

raquo Significant reductions in the number of member airl ines

Recent Developments Airline membership in the company has remained fairly stable Total SFO Fuel membership increased marginally from 39 members in FY06 to 41 members in FY16 with United Air Lines In c (United Continental Holdings Inc Corporate Family Rating Ba2 stable) composing roughly 35 of FY16 member gallonage throughput The 41 members continued to see substantial cost benefits as the member fu el system fee per gallon ($ 021) was well below the 22 non-member fuel system fee per gallon ($ 06) in FY16 Capital expenditures are expected to be in the $5 to 7 million range over the next two years

Detailed Rating Considerations

Revenue Generating Base

The San Francisco Airports Commission (Commission) granted a 31 year exclusive concession expiring in June 2028 to SFO Fuel in 1997 to deliver fuel at San Francisco International Airport (SFO) The lease provides for ground rental of certain parcels of land and easements as well as the payment of debt service on bonds issued by the Commission to finance facility improvements

This publication does not announce a credit rating action For any credit ratings referenced in this publication please see the ratings tab on the issuerentity page on wwwmoodyscom fo r the most updated credit rating action information and rating history

29 March 2017 SFO Fu el Company LLC Update - Moodys affirms the A3 rating on SFO Fu e l Compa ny LLC outlook stable

MOODYS INVESTORS SERVICE US PUBLIC FINANCE

SFO Fuel has the exclusive right to lease install operate and maintain the aviation fueling system on the airports lands for provision of jet fuel to air carriers While airlines may tanker to minimize their use of the SFO Fuel system if they choose that risk is very limited due to the cost of tankering For airlines fuel is the single largest cost factor and critical to their ability to operate These factors combined with the long haul nature of the flights from SFO and higher cost of tankering relative to the SFO Fuel facility reinforce the essentiality of the system Airline membership is also a key component to SFO Fuels credit strength and the company currently has 41 members with no member accounting for more than 35 of total fuel gallonage throughput

The SFO Fuel and other fuel facility consortiums contractual framework has been utilized for several decades with a good track record throughout the United States and Canada to establish cooperative fuel storage and distribution systems These structures have demonstrated resilience through high industry volatility airline bankruptcies and numerous mergers Moodys notes that the bond documents provide protections to keep the consortium intact in the event of system failure system bankruptcy or the sudden withdrawal of all or almost all member airlines

SFO maintains a dominant market position in the Bay Area having gained from drawback at other regional airports as airlines have restructured their routes coming out of the recession and airline industry consolidation However SFO still faces some competition from San Jose (City of) CA Airport Enterprise (AZ stable) and Oakland International Airport (Port of Oakland AZ stable) Still SFO serves as the international airport gateway for Northern California These facts are important in order to ensure the long term survival of the airport as a key element of the US air transportation infrastructure and thus the continued demand for fueling services at the airport over the term of the debt

middot Operational and Financial Performance Given the cost recovery framework that results in airl ines covering all operating capital and debt service costs in add ition to the stepshyup obligation of non-defaulting airlines in ten days if a member airline defaults in its payment bondholders are largely protected against demand risk unexpected events and airline credit however not operating risk Moodys notes that Mexicana Airlines Z010 bankruptcy serves as an example of a SFO Fuel member airline filing for bankruptcy and the other members stepping-up and paying for all incremental costs

In addition to a strong step-up provis ion the company can adjust billing to the member airlines to recognize additional costs as member airli nes must provide Z months of net facilities payments upfront as collateral in addition to the provision that withdrawing airlines must pay all obligations accrued up to withdrawal date for the Z4 prior months Furthermore the contractual structure also provides a mechanism to have all SFO Fuel obligations extinguished even in the case of all member airlines withdrawing from the consortium

Pursuant to the interline agreement each contracting airline is requi red to deposit and maintain an operating reserve account equal to twice such contracting airlines estimated average monthly share of the total fuel system charge for the previous 1Z months In the event of a default on amounts due to the company SFO Fuel will draw on the defaulting contracting airlines reserves The company requires similar deposits from its nonmember airlines

LIQUIDITY

SFO Fuel had cash and cash equivalents of approximately $105 million as of December 31 Z016 which was slightly down from $108 million in FYE15

Debt and Other Liabilities As of FY Z016 SFO Fuel has $617 million of Series 1997A and $116 million of Series ZOOOA Special Facilities Lease Revenue Bond debt outstanding Capital expenditures are expected to be in the $5 to 7 million range over the next two years and will be fully funded by the contracting airlines No new debt issuance is expected over the next 1Z months

DEBT STRUCTURE

The debt service profile is flat around $9 million annually until final maturity of both debt series in ZO Z

DEBT-RELATED DERIVATIVES

None

29 March 2017 SFO Fu e l Company LLC Update - Moodys affirms the A3 rating on SFO Fue l Company LLC outlook stable

MOODYS INVESTORS SERVICE US PUBLIC FINANCE

PENSIONS AND OPEB

As of December 31 2015 SFO Fuel has no pensions or OPEB balances outstanding

Management and Governance

SFO Fuel contracts with Aircraft Service International Group Inc (ASll ratings withdrawn) for the operation and administration of the fuel system SFO Fuel is governed by a Fuel Committee that is composed of one representative appointed by each airline that is a member of the company and is a party to an interline agreement among the member airlines and SFO Fuel

Legal Security The bonds are secured by a pledge of the trust estate which is primarily facilities rent paid by member airlines as well as by the debt service reserve fund The debt service reserve fund requirement is fulfilled by the surety policies from Ambac Assurance Corporation (ratings withdrawn) and FSA (Assured Guaranty Municipal Corp rated AZ stable) The company collects user fees from all airlines and others using the facility to offset on a break-even basis its operating costs including facilities rent and additional and reimbursement rents

Use of Proceeds Not applicable

Obligor Profile SFO Fuel is a limited liability non stock membership corporation organized for the purpose of leasing constructing and operating the fuel facilities at San Francisco International Airport SFO) SFO Fuel was organized on May 28 1997 as a limited liability company under the laws of the state of Delaware for the purpose of leasing constructing and operating the fuel system at SFO The San Francisco Airport Commission issued Special Facilities Lease Revenue Bonds on October 7 1997 and May 1 2000 The bonds were issued specifically to finance the costs of acquisition construction modification expansion and installation of certain additions replacements and improvements to the jet fuel receipt storage and distribution system serving SFO certain diesel and gasoline storage and delivery facilities for ground service equipment and related environmental costs SFO Fuel contracts with Aircraft Service International Inc for the operation and administration of the fuel system

Methodology The principal methodology used in this rating was Generic Project Finance Methodology published in December 2010 Please see the Rating Methodologies page on wwwmoodyscom for a copy of this methodology

29 March 2017 SFO Fuel Company LLC Update - Moodys aff irms the A3 ra ting on SFO Fuel Company LLC outlook stable 4

MOODYS INVESTORS SERVICE US PUBLIC FINANCE

copy 2017 Moodys Corporation Moodys Investors Service Inc Moodys Analytics Inc andor their licensors and affiliates (collectively MOODYS) All rights reserved

CREDIT RATINGS ISS UED BY MOODYS INVESTORS SERVICE INC AND ITS RATINGS AFFILIATES ( MIS) ARE MOODYS CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES CREDIT COMMITMENTS OR DEBT OR DEBT-LIKE SECURITIES AND MOODYS PUBLICATIONS MAY INCLUDE MOODYS CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES CREDIT COMMITMENTS OR DEBT OR DEBT-LIKE SECURITIES MOODYS DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT CREDIT RATINGS DO NOT ADDR ESS ANY OTHER RISK INCLUDING BUT NOT LIMITED TO LIQUIDITY RISK MARKET VALUERISK OR PRICE VOLATILITY CREDIT RATINGS AND MOODYS OPINIONS INCLUDED IN MOODYS PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT MOODYS PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLI SHED BY MOODYS ANALYTICS INC CREDIT RATINGS AND MOODYS PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE AND CREDIT RATINGS AND MOODYS PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE SELL OR HOLD PARTICULAR SECURITIES NEITHER CREDIT RATINGS NOR MOODYS PUBLICATIONSCOMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR MOODYS ISSUES ITSCREDIT RATINGS AND PUBLISHES MOODYS PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL WITH DUE CARE MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE HOLDING OR SALE

MOODYS CREDIT RATINGSAND MOODYS PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORSAND IT WOULD BE RECKLESS AND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODYS CREDIT RATINGS OR MOODYS PUBLICATIONSWHEN MAKING AN INVESTMENT DECISION IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW INCLUDING BUT NOT LIMITED TO COPYRIGHT LAW AND NON EOF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED REPACKAGED FURTHER TRAN SMITIED TRAN SFERRED DISS EMINATED REDISTRIBUTED OR RESOLD OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE IN WHOLE OR IN PART IN A ~IY FORM OR MANNER OR BY ANY MEANS WHATSOEVER BY ANY PERSON WITHOUT MOODYS PRIOR WRITIEN CONSENT

All information contained herein is obtained by MOODYS from sources believed by it to be accurate and reliable Because of the possibility of human or mechanical error as well as other factors however all information contained herein is provided AS IS without warranty of any kind MOODYS adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODYS considers to be reliable includ ing when appropriate independent third-party sources However MOODYS is not an auditor and cannot in every instance independentljt verify or validate information received in the rating process or in preparing the Moodys publications

To the extent permitted by law MOODYS and its directors officers employees agents representa tives licensors and suppliers disclaim liability to any person or entity for any indirect special consequential or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use any such information even if MOODYS or any of its directors officers employees agents representatives licensors or suppliers is advised in advance of the possibility of such losses or damages including but not limited to (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument Is not the subject of a particular credit rating assigned by MOODYS

To the extent permitted by law MOODYS and its directors offi cers employees agents representatives licensors and suppliers disclaim liability for any direct or compensatory losses or damages caused to any person or entity including but not limited to by any negligence (but excluding fraud willful misconduct or any other type of liability that for the avoidance or doubt by law cannot be excluded) on the part of or any contingency within or beyond the control of MOODYS or any of its directors officers employees agents representatives licensors or suppliers arising from or in connection with the information contained herein or the use of or inability to use any such information

NO WARRANTY EXPRESS OR IMPLIED AS TO THE ACCURACY TIMELINESS COMPLETENESS MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODYS IN ANY FORM OR MANNER WHATSOEVER

Moodys Investors Service Inc a wholly-owned credit rating agency subsidiary of Moodys Corporation (MCO) hereby discloses that most issuers of debt securities (including corporate and municipal bonds debentures notes and commercial paper) and preferred stock rated by Moodys Investors Service Inc have prior to assignment of any rating agreed to pay to Moodys Investors Service Inc for appraisal and rating services rendered by it fees ranging from $1500 to approximately $2500000 MCO and MIS also maintain policies and procedures to address the independence of Ml Ss ratings and rating processes Information regarding certain affiliations that may exist between directors of MCO and ra ted entities and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5 is posted annually at wwwmoodyscom under the heading Investor Relations - Corporate Governance- Director and Shareholder Affiliation Policy

Additional terms for Australia only Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODYS affil iate Moodys Investors Service Pty Limited ABN 61 003 399 657AFSL 336969 andor Moodys Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (asapplicable) This document is Intended to be provided only to wholesale clients within the meaning of section 761G of the Corporations Act 2001 By continuing to access this document from within Australia you represent to MOODYS that you are or are accessing the document as a representative of a wholesale client and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to retail clients within the meaning of section 761G of the Corporations Act 2001 MOODYS credit rating is an opinion as to the creditworthiness of a debt obligation of the issuer not on the equity securities of the issuer or any form of security that is available to retail investors It would be reckless and inappropriate for retail investors to use MOODYS credit ratings or publications when making an investment decision If in doubt you should contact your financial or other professional adviser

Additional terms for Japan only Moodys Japan KK (MJKK) is a wholly-owned credit rating agency subsidiary or Moodys Group Japan GK which is wholly-owned by Moodys Overseas Holdings Inc a wholly-owned subsidiary of MCO Moodys SF Japan KK (MSFJ) is a wholly-owned credit rating agency subsidiary of MJKK MSFJ is not a Nationally Recognized Statistical Rating Organization (NRSRO) Therefore credit ratings assigned by MSFJ are Non-NRSRO Credi Ra tings Non-NR SRO Credit Ratings are assigned by an entity that is not a NRSRO and consequently the rated obligation will not qualify for certain types or trea tment under US laws MJKKand MSFJ are credit rating agencies registered with the Japan Financial Services Agency and their registration numbers are FSA Commissioner Ratings) No 2 and 3 respectively

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securi ties (including corporate and municipal bonds debentures notes and commercial paper) and preferred stock rated by MJKK or MSFJ (asapplicable) have prior to assignment of any rating agreed to pay to MJKK or MSFJ(as applicable) for appraisal and rating services rendered by it fees ranging from JPYZ00000 to approximately JPY350000000

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements

REPORT NUMBER 1066681

Moonvs INVESTORS SERVICE

29 March 2017 SFO Fu el Company LLC Update - Moodys affirms t he A3 rating on SFO Fu el Company LLC out look stable

MOODYS INVESTORS SERVICE US PUBLIC FINANCE

raquo Fuel facility lease is coterminous with outstanding bonds maturity

raquo Pledge of facilities rent from all member airlines with a step-up requirement for all members for any financial shortfalls

raquo Monopoly provider of jet fuel at the third largest US airport by OampD enplanements

raquo History of limited expenditure growth and strong fee collection from non-members and airlines in bankruptcy keep costs low for member airlines

Credit Challenges

raquo Debt service reserve fund a key structural component providing critical liquidity to manage disruptions in debt service payments is funded through sureties

raquo Sum sufficient rate covenant and limited requirements for issuing additional bonds provide weak legal protections to bondholders

raquo Potential for additional costs from necessary system improvements environmental remediation or changes in environmental legislation that require system modifications

Rating Outlook The stable outlook is based on Moodys expectation that the contracting airline profile will remain fairly stable and the airlines will continue to provide full financial support for all costs related to the fuel system including any additional increases in capital costs

Factors that Could Lead to an Upgrade

raquo Cash funding the debt service reserve fund

raquo Improved financial position of member airlines

raquo Greater cash reserves

Factors that Could Lead to a Downgrade

raquo Dramatic changes in environmental remediation costs or in capital costs needed to keep the system in compliance with tightening environmental legislation

raquo Events that reduce the strong market position of SFO relative to major nearby airports

raquo Significant reductions in the number of member airl ines

Recent Developments Airline membership in the company has remained fairly stable Total SFO Fuel membership increased marginally from 39 members in FY06 to 41 members in FY16 with United Air Lines In c (United Continental Holdings Inc Corporate Family Rating Ba2 stable) composing roughly 35 of FY16 member gallonage throughput The 41 members continued to see substantial cost benefits as the member fu el system fee per gallon ($ 021) was well below the 22 non-member fuel system fee per gallon ($ 06) in FY16 Capital expenditures are expected to be in the $5 to 7 million range over the next two years

Detailed Rating Considerations

Revenue Generating Base

The San Francisco Airports Commission (Commission) granted a 31 year exclusive concession expiring in June 2028 to SFO Fuel in 1997 to deliver fuel at San Francisco International Airport (SFO) The lease provides for ground rental of certain parcels of land and easements as well as the payment of debt service on bonds issued by the Commission to finance facility improvements

This publication does not announce a credit rating action For any credit ratings referenced in this publication please see the ratings tab on the issuerentity page on wwwmoodyscom fo r the most updated credit rating action information and rating history

29 March 2017 SFO Fu el Company LLC Update - Moodys affirms the A3 rating on SFO Fu e l Compa ny LLC outlook stable

MOODYS INVESTORS SERVICE US PUBLIC FINANCE

SFO Fuel has the exclusive right to lease install operate and maintain the aviation fueling system on the airports lands for provision of jet fuel to air carriers While airlines may tanker to minimize their use of the SFO Fuel system if they choose that risk is very limited due to the cost of tankering For airlines fuel is the single largest cost factor and critical to their ability to operate These factors combined with the long haul nature of the flights from SFO and higher cost of tankering relative to the SFO Fuel facility reinforce the essentiality of the system Airline membership is also a key component to SFO Fuels credit strength and the company currently has 41 members with no member accounting for more than 35 of total fuel gallonage throughput

The SFO Fuel and other fuel facility consortiums contractual framework has been utilized for several decades with a good track record throughout the United States and Canada to establish cooperative fuel storage and distribution systems These structures have demonstrated resilience through high industry volatility airline bankruptcies and numerous mergers Moodys notes that the bond documents provide protections to keep the consortium intact in the event of system failure system bankruptcy or the sudden withdrawal of all or almost all member airlines

SFO maintains a dominant market position in the Bay Area having gained from drawback at other regional airports as airlines have restructured their routes coming out of the recession and airline industry consolidation However SFO still faces some competition from San Jose (City of) CA Airport Enterprise (AZ stable) and Oakland International Airport (Port of Oakland AZ stable) Still SFO serves as the international airport gateway for Northern California These facts are important in order to ensure the long term survival of the airport as a key element of the US air transportation infrastructure and thus the continued demand for fueling services at the airport over the term of the debt

middot Operational and Financial Performance Given the cost recovery framework that results in airl ines covering all operating capital and debt service costs in add ition to the stepshyup obligation of non-defaulting airlines in ten days if a member airline defaults in its payment bondholders are largely protected against demand risk unexpected events and airline credit however not operating risk Moodys notes that Mexicana Airlines Z010 bankruptcy serves as an example of a SFO Fuel member airline filing for bankruptcy and the other members stepping-up and paying for all incremental costs

In addition to a strong step-up provis ion the company can adjust billing to the member airlines to recognize additional costs as member airli nes must provide Z months of net facilities payments upfront as collateral in addition to the provision that withdrawing airlines must pay all obligations accrued up to withdrawal date for the Z4 prior months Furthermore the contractual structure also provides a mechanism to have all SFO Fuel obligations extinguished even in the case of all member airlines withdrawing from the consortium

Pursuant to the interline agreement each contracting airline is requi red to deposit and maintain an operating reserve account equal to twice such contracting airlines estimated average monthly share of the total fuel system charge for the previous 1Z months In the event of a default on amounts due to the company SFO Fuel will draw on the defaulting contracting airlines reserves The company requires similar deposits from its nonmember airlines

LIQUIDITY

SFO Fuel had cash and cash equivalents of approximately $105 million as of December 31 Z016 which was slightly down from $108 million in FYE15

Debt and Other Liabilities As of FY Z016 SFO Fuel has $617 million of Series 1997A and $116 million of Series ZOOOA Special Facilities Lease Revenue Bond debt outstanding Capital expenditures are expected to be in the $5 to 7 million range over the next two years and will be fully funded by the contracting airlines No new debt issuance is expected over the next 1Z months

DEBT STRUCTURE

The debt service profile is flat around $9 million annually until final maturity of both debt series in ZO Z

DEBT-RELATED DERIVATIVES

None

29 March 2017 SFO Fu e l Company LLC Update - Moodys affirms the A3 rating on SFO Fue l Company LLC outlook stable

MOODYS INVESTORS SERVICE US PUBLIC FINANCE

PENSIONS AND OPEB

As of December 31 2015 SFO Fuel has no pensions or OPEB balances outstanding

Management and Governance

SFO Fuel contracts with Aircraft Service International Group Inc (ASll ratings withdrawn) for the operation and administration of the fuel system SFO Fuel is governed by a Fuel Committee that is composed of one representative appointed by each airline that is a member of the company and is a party to an interline agreement among the member airlines and SFO Fuel

Legal Security The bonds are secured by a pledge of the trust estate which is primarily facilities rent paid by member airlines as well as by the debt service reserve fund The debt service reserve fund requirement is fulfilled by the surety policies from Ambac Assurance Corporation (ratings withdrawn) and FSA (Assured Guaranty Municipal Corp rated AZ stable) The company collects user fees from all airlines and others using the facility to offset on a break-even basis its operating costs including facilities rent and additional and reimbursement rents

Use of Proceeds Not applicable

Obligor Profile SFO Fuel is a limited liability non stock membership corporation organized for the purpose of leasing constructing and operating the fuel facilities at San Francisco International Airport SFO) SFO Fuel was organized on May 28 1997 as a limited liability company under the laws of the state of Delaware for the purpose of leasing constructing and operating the fuel system at SFO The San Francisco Airport Commission issued Special Facilities Lease Revenue Bonds on October 7 1997 and May 1 2000 The bonds were issued specifically to finance the costs of acquisition construction modification expansion and installation of certain additions replacements and improvements to the jet fuel receipt storage and distribution system serving SFO certain diesel and gasoline storage and delivery facilities for ground service equipment and related environmental costs SFO Fuel contracts with Aircraft Service International Inc for the operation and administration of the fuel system

Methodology The principal methodology used in this rating was Generic Project Finance Methodology published in December 2010 Please see the Rating Methodologies page on wwwmoodyscom for a copy of this methodology

29 March 2017 SFO Fuel Company LLC Update - Moodys aff irms the A3 ra ting on SFO Fuel Company LLC outlook stable 4

MOODYS INVESTORS SERVICE US PUBLIC FINANCE

copy 2017 Moodys Corporation Moodys Investors Service Inc Moodys Analytics Inc andor their licensors and affiliates (collectively MOODYS) All rights reserved

CREDIT RATINGS ISS UED BY MOODYS INVESTORS SERVICE INC AND ITS RATINGS AFFILIATES ( MIS) ARE MOODYS CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES CREDIT COMMITMENTS OR DEBT OR DEBT-LIKE SECURITIES AND MOODYS PUBLICATIONS MAY INCLUDE MOODYS CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES CREDIT COMMITMENTS OR DEBT OR DEBT-LIKE SECURITIES MOODYS DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT CREDIT RATINGS DO NOT ADDR ESS ANY OTHER RISK INCLUDING BUT NOT LIMITED TO LIQUIDITY RISK MARKET VALUERISK OR PRICE VOLATILITY CREDIT RATINGS AND MOODYS OPINIONS INCLUDED IN MOODYS PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT MOODYS PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLI SHED BY MOODYS ANALYTICS INC CREDIT RATINGS AND MOODYS PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE AND CREDIT RATINGS AND MOODYS PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE SELL OR HOLD PARTICULAR SECURITIES NEITHER CREDIT RATINGS NOR MOODYS PUBLICATIONSCOMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR MOODYS ISSUES ITSCREDIT RATINGS AND PUBLISHES MOODYS PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL WITH DUE CARE MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE HOLDING OR SALE

MOODYS CREDIT RATINGSAND MOODYS PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORSAND IT WOULD BE RECKLESS AND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODYS CREDIT RATINGS OR MOODYS PUBLICATIONSWHEN MAKING AN INVESTMENT DECISION IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW INCLUDING BUT NOT LIMITED TO COPYRIGHT LAW AND NON EOF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED REPACKAGED FURTHER TRAN SMITIED TRAN SFERRED DISS EMINATED REDISTRIBUTED OR RESOLD OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE IN WHOLE OR IN PART IN A ~IY FORM OR MANNER OR BY ANY MEANS WHATSOEVER BY ANY PERSON WITHOUT MOODYS PRIOR WRITIEN CONSENT

All information contained herein is obtained by MOODYS from sources believed by it to be accurate and reliable Because of the possibility of human or mechanical error as well as other factors however all information contained herein is provided AS IS without warranty of any kind MOODYS adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODYS considers to be reliable includ ing when appropriate independent third-party sources However MOODYS is not an auditor and cannot in every instance independentljt verify or validate information received in the rating process or in preparing the Moodys publications

To the extent permitted by law MOODYS and its directors officers employees agents representa tives licensors and suppliers disclaim liability to any person or entity for any indirect special consequential or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use any such information even if MOODYS or any of its directors officers employees agents representatives licensors or suppliers is advised in advance of the possibility of such losses or damages including but not limited to (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument Is not the subject of a particular credit rating assigned by MOODYS

To the extent permitted by law MOODYS and its directors offi cers employees agents representatives licensors and suppliers disclaim liability for any direct or compensatory losses or damages caused to any person or entity including but not limited to by any negligence (but excluding fraud willful misconduct or any other type of liability that for the avoidance or doubt by law cannot be excluded) on the part of or any contingency within or beyond the control of MOODYS or any of its directors officers employees agents representatives licensors or suppliers arising from or in connection with the information contained herein or the use of or inability to use any such information

NO WARRANTY EXPRESS OR IMPLIED AS TO THE ACCURACY TIMELINESS COMPLETENESS MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODYS IN ANY FORM OR MANNER WHATSOEVER

Moodys Investors Service Inc a wholly-owned credit rating agency subsidiary of Moodys Corporation (MCO) hereby discloses that most issuers of debt securities (including corporate and municipal bonds debentures notes and commercial paper) and preferred stock rated by Moodys Investors Service Inc have prior to assignment of any rating agreed to pay to Moodys Investors Service Inc for appraisal and rating services rendered by it fees ranging from $1500 to approximately $2500000 MCO and MIS also maintain policies and procedures to address the independence of Ml Ss ratings and rating processes Information regarding certain affiliations that may exist between directors of MCO and ra ted entities and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5 is posted annually at wwwmoodyscom under the heading Investor Relations - Corporate Governance- Director and Shareholder Affiliation Policy

Additional terms for Australia only Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODYS affil iate Moodys Investors Service Pty Limited ABN 61 003 399 657AFSL 336969 andor Moodys Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (asapplicable) This document is Intended to be provided only to wholesale clients within the meaning of section 761G of the Corporations Act 2001 By continuing to access this document from within Australia you represent to MOODYS that you are or are accessing the document as a representative of a wholesale client and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to retail clients within the meaning of section 761G of the Corporations Act 2001 MOODYS credit rating is an opinion as to the creditworthiness of a debt obligation of the issuer not on the equity securities of the issuer or any form of security that is available to retail investors It would be reckless and inappropriate for retail investors to use MOODYS credit ratings or publications when making an investment decision If in doubt you should contact your financial or other professional adviser

Additional terms for Japan only Moodys Japan KK (MJKK) is a wholly-owned credit rating agency subsidiary or Moodys Group Japan GK which is wholly-owned by Moodys Overseas Holdings Inc a wholly-owned subsidiary of MCO Moodys SF Japan KK (MSFJ) is a wholly-owned credit rating agency subsidiary of MJKK MSFJ is not a Nationally Recognized Statistical Rating Organization (NRSRO) Therefore credit ratings assigned by MSFJ are Non-NRSRO Credi Ra tings Non-NR SRO Credit Ratings are assigned by an entity that is not a NRSRO and consequently the rated obligation will not qualify for certain types or trea tment under US laws MJKKand MSFJ are credit rating agencies registered with the Japan Financial Services Agency and their registration numbers are FSA Commissioner Ratings) No 2 and 3 respectively

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securi ties (including corporate and municipal bonds debentures notes and commercial paper) and preferred stock rated by MJKK or MSFJ (asapplicable) have prior to assignment of any rating agreed to pay to MJKK or MSFJ(as applicable) for appraisal and rating services rendered by it fees ranging from JPYZ00000 to approximately JPY350000000

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements

REPORT NUMBER 1066681

Moonvs INVESTORS SERVICE

29 March 2017 SFO Fu el Company LLC Update - Moodys affirms t he A3 rating on SFO Fu el Company LLC out look stable

MOODYS INVESTORS SERVICE US PUBLIC FINANCE

SFO Fuel has the exclusive right to lease install operate and maintain the aviation fueling system on the airports lands for provision of jet fuel to air carriers While airlines may tanker to minimize their use of the SFO Fuel system if they choose that risk is very limited due to the cost of tankering For airlines fuel is the single largest cost factor and critical to their ability to operate These factors combined with the long haul nature of the flights from SFO and higher cost of tankering relative to the SFO Fuel facility reinforce the essentiality of the system Airline membership is also a key component to SFO Fuels credit strength and the company currently has 41 members with no member accounting for more than 35 of total fuel gallonage throughput

The SFO Fuel and other fuel facility consortiums contractual framework has been utilized for several decades with a good track record throughout the United States and Canada to establish cooperative fuel storage and distribution systems These structures have demonstrated resilience through high industry volatility airline bankruptcies and numerous mergers Moodys notes that the bond documents provide protections to keep the consortium intact in the event of system failure system bankruptcy or the sudden withdrawal of all or almost all member airlines

SFO maintains a dominant market position in the Bay Area having gained from drawback at other regional airports as airlines have restructured their routes coming out of the recession and airline industry consolidation However SFO still faces some competition from San Jose (City of) CA Airport Enterprise (AZ stable) and Oakland International Airport (Port of Oakland AZ stable) Still SFO serves as the international airport gateway for Northern California These facts are important in order to ensure the long term survival of the airport as a key element of the US air transportation infrastructure and thus the continued demand for fueling services at the airport over the term of the debt

middot Operational and Financial Performance Given the cost recovery framework that results in airl ines covering all operating capital and debt service costs in add ition to the stepshyup obligation of non-defaulting airlines in ten days if a member airline defaults in its payment bondholders are largely protected against demand risk unexpected events and airline credit however not operating risk Moodys notes that Mexicana Airlines Z010 bankruptcy serves as an example of a SFO Fuel member airline filing for bankruptcy and the other members stepping-up and paying for all incremental costs

In addition to a strong step-up provis ion the company can adjust billing to the member airlines to recognize additional costs as member airli nes must provide Z months of net facilities payments upfront as collateral in addition to the provision that withdrawing airlines must pay all obligations accrued up to withdrawal date for the Z4 prior months Furthermore the contractual structure also provides a mechanism to have all SFO Fuel obligations extinguished even in the case of all member airlines withdrawing from the consortium

Pursuant to the interline agreement each contracting airline is requi red to deposit and maintain an operating reserve account equal to twice such contracting airlines estimated average monthly share of the total fuel system charge for the previous 1Z months In the event of a default on amounts due to the company SFO Fuel will draw on the defaulting contracting airlines reserves The company requires similar deposits from its nonmember airlines

LIQUIDITY

SFO Fuel had cash and cash equivalents of approximately $105 million as of December 31 Z016 which was slightly down from $108 million in FYE15

Debt and Other Liabilities As of FY Z016 SFO Fuel has $617 million of Series 1997A and $116 million of Series ZOOOA Special Facilities Lease Revenue Bond debt outstanding Capital expenditures are expected to be in the $5 to 7 million range over the next two years and will be fully funded by the contracting airlines No new debt issuance is expected over the next 1Z months

DEBT STRUCTURE

The debt service profile is flat around $9 million annually until final maturity of both debt series in ZO Z

DEBT-RELATED DERIVATIVES

None

29 March 2017 SFO Fu e l Company LLC Update - Moodys affirms the A3 rating on SFO Fue l Company LLC outlook stable

MOODYS INVESTORS SERVICE US PUBLIC FINANCE

PENSIONS AND OPEB

As of December 31 2015 SFO Fuel has no pensions or OPEB balances outstanding

Management and Governance

SFO Fuel contracts with Aircraft Service International Group Inc (ASll ratings withdrawn) for the operation and administration of the fuel system SFO Fuel is governed by a Fuel Committee that is composed of one representative appointed by each airline that is a member of the company and is a party to an interline agreement among the member airlines and SFO Fuel

Legal Security The bonds are secured by a pledge of the trust estate which is primarily facilities rent paid by member airlines as well as by the debt service reserve fund The debt service reserve fund requirement is fulfilled by the surety policies from Ambac Assurance Corporation (ratings withdrawn) and FSA (Assured Guaranty Municipal Corp rated AZ stable) The company collects user fees from all airlines and others using the facility to offset on a break-even basis its operating costs including facilities rent and additional and reimbursement rents

Use of Proceeds Not applicable

Obligor Profile SFO Fuel is a limited liability non stock membership corporation organized for the purpose of leasing constructing and operating the fuel facilities at San Francisco International Airport SFO) SFO Fuel was organized on May 28 1997 as a limited liability company under the laws of the state of Delaware for the purpose of leasing constructing and operating the fuel system at SFO The San Francisco Airport Commission issued Special Facilities Lease Revenue Bonds on October 7 1997 and May 1 2000 The bonds were issued specifically to finance the costs of acquisition construction modification expansion and installation of certain additions replacements and improvements to the jet fuel receipt storage and distribution system serving SFO certain diesel and gasoline storage and delivery facilities for ground service equipment and related environmental costs SFO Fuel contracts with Aircraft Service International Inc for the operation and administration of the fuel system

Methodology The principal methodology used in this rating was Generic Project Finance Methodology published in December 2010 Please see the Rating Methodologies page on wwwmoodyscom for a copy of this methodology

29 March 2017 SFO Fuel Company LLC Update - Moodys aff irms the A3 ra ting on SFO Fuel Company LLC outlook stable 4

MOODYS INVESTORS SERVICE US PUBLIC FINANCE

copy 2017 Moodys Corporation Moodys Investors Service Inc Moodys Analytics Inc andor their licensors and affiliates (collectively MOODYS) All rights reserved

CREDIT RATINGS ISS UED BY MOODYS INVESTORS SERVICE INC AND ITS RATINGS AFFILIATES ( MIS) ARE MOODYS CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES CREDIT COMMITMENTS OR DEBT OR DEBT-LIKE SECURITIES AND MOODYS PUBLICATIONS MAY INCLUDE MOODYS CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES CREDIT COMMITMENTS OR DEBT OR DEBT-LIKE SECURITIES MOODYS DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT CREDIT RATINGS DO NOT ADDR ESS ANY OTHER RISK INCLUDING BUT NOT LIMITED TO LIQUIDITY RISK MARKET VALUERISK OR PRICE VOLATILITY CREDIT RATINGS AND MOODYS OPINIONS INCLUDED IN MOODYS PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT MOODYS PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLI SHED BY MOODYS ANALYTICS INC CREDIT RATINGS AND MOODYS PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE AND CREDIT RATINGS AND MOODYS PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE SELL OR HOLD PARTICULAR SECURITIES NEITHER CREDIT RATINGS NOR MOODYS PUBLICATIONSCOMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR MOODYS ISSUES ITSCREDIT RATINGS AND PUBLISHES MOODYS PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL WITH DUE CARE MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE HOLDING OR SALE

MOODYS CREDIT RATINGSAND MOODYS PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORSAND IT WOULD BE RECKLESS AND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODYS CREDIT RATINGS OR MOODYS PUBLICATIONSWHEN MAKING AN INVESTMENT DECISION IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW INCLUDING BUT NOT LIMITED TO COPYRIGHT LAW AND NON EOF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED REPACKAGED FURTHER TRAN SMITIED TRAN SFERRED DISS EMINATED REDISTRIBUTED OR RESOLD OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE IN WHOLE OR IN PART IN A ~IY FORM OR MANNER OR BY ANY MEANS WHATSOEVER BY ANY PERSON WITHOUT MOODYS PRIOR WRITIEN CONSENT

All information contained herein is obtained by MOODYS from sources believed by it to be accurate and reliable Because of the possibility of human or mechanical error as well as other factors however all information contained herein is provided AS IS without warranty of any kind MOODYS adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODYS considers to be reliable includ ing when appropriate independent third-party sources However MOODYS is not an auditor and cannot in every instance independentljt verify or validate information received in the rating process or in preparing the Moodys publications

To the extent permitted by law MOODYS and its directors officers employees agents representa tives licensors and suppliers disclaim liability to any person or entity for any indirect special consequential or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use any such information even if MOODYS or any of its directors officers employees agents representatives licensors or suppliers is advised in advance of the possibility of such losses or damages including but not limited to (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument Is not the subject of a particular credit rating assigned by MOODYS

To the extent permitted by law MOODYS and its directors offi cers employees agents representatives licensors and suppliers disclaim liability for any direct or compensatory losses or damages caused to any person or entity including but not limited to by any negligence (but excluding fraud willful misconduct or any other type of liability that for the avoidance or doubt by law cannot be excluded) on the part of or any contingency within or beyond the control of MOODYS or any of its directors officers employees agents representatives licensors or suppliers arising from or in connection with the information contained herein or the use of or inability to use any such information

NO WARRANTY EXPRESS OR IMPLIED AS TO THE ACCURACY TIMELINESS COMPLETENESS MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODYS IN ANY FORM OR MANNER WHATSOEVER

Moodys Investors Service Inc a wholly-owned credit rating agency subsidiary of Moodys Corporation (MCO) hereby discloses that most issuers of debt securities (including corporate and municipal bonds debentures notes and commercial paper) and preferred stock rated by Moodys Investors Service Inc have prior to assignment of any rating agreed to pay to Moodys Investors Service Inc for appraisal and rating services rendered by it fees ranging from $1500 to approximately $2500000 MCO and MIS also maintain policies and procedures to address the independence of Ml Ss ratings and rating processes Information regarding certain affiliations that may exist between directors of MCO and ra ted entities and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5 is posted annually at wwwmoodyscom under the heading Investor Relations - Corporate Governance- Director and Shareholder Affiliation Policy

Additional terms for Australia only Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODYS affil iate Moodys Investors Service Pty Limited ABN 61 003 399 657AFSL 336969 andor Moodys Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (asapplicable) This document is Intended to be provided only to wholesale clients within the meaning of section 761G of the Corporations Act 2001 By continuing to access this document from within Australia you represent to MOODYS that you are or are accessing the document as a representative of a wholesale client and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to retail clients within the meaning of section 761G of the Corporations Act 2001 MOODYS credit rating is an opinion as to the creditworthiness of a debt obligation of the issuer not on the equity securities of the issuer or any form of security that is available to retail investors It would be reckless and inappropriate for retail investors to use MOODYS credit ratings or publications when making an investment decision If in doubt you should contact your financial or other professional adviser

Additional terms for Japan only Moodys Japan KK (MJKK) is a wholly-owned credit rating agency subsidiary or Moodys Group Japan GK which is wholly-owned by Moodys Overseas Holdings Inc a wholly-owned subsidiary of MCO Moodys SF Japan KK (MSFJ) is a wholly-owned credit rating agency subsidiary of MJKK MSFJ is not a Nationally Recognized Statistical Rating Organization (NRSRO) Therefore credit ratings assigned by MSFJ are Non-NRSRO Credi Ra tings Non-NR SRO Credit Ratings are assigned by an entity that is not a NRSRO and consequently the rated obligation will not qualify for certain types or trea tment under US laws MJKKand MSFJ are credit rating agencies registered with the Japan Financial Services Agency and their registration numbers are FSA Commissioner Ratings) No 2 and 3 respectively

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securi ties (including corporate and municipal bonds debentures notes and commercial paper) and preferred stock rated by MJKK or MSFJ (asapplicable) have prior to assignment of any rating agreed to pay to MJKK or MSFJ(as applicable) for appraisal and rating services rendered by it fees ranging from JPYZ00000 to approximately JPY350000000

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements

REPORT NUMBER 1066681

Moonvs INVESTORS SERVICE

29 March 2017 SFO Fu el Company LLC Update - Moodys affirms t he A3 rating on SFO Fu el Company LLC out look stable

MOODYS INVESTORS SERVICE US PUBLIC FINANCE

PENSIONS AND OPEB

As of December 31 2015 SFO Fuel has no pensions or OPEB balances outstanding

Management and Governance

SFO Fuel contracts with Aircraft Service International Group Inc (ASll ratings withdrawn) for the operation and administration of the fuel system SFO Fuel is governed by a Fuel Committee that is composed of one representative appointed by each airline that is a member of the company and is a party to an interline agreement among the member airlines and SFO Fuel

Legal Security The bonds are secured by a pledge of the trust estate which is primarily facilities rent paid by member airlines as well as by the debt service reserve fund The debt service reserve fund requirement is fulfilled by the surety policies from Ambac Assurance Corporation (ratings withdrawn) and FSA (Assured Guaranty Municipal Corp rated AZ stable) The company collects user fees from all airlines and others using the facility to offset on a break-even basis its operating costs including facilities rent and additional and reimbursement rents

Use of Proceeds Not applicable

Obligor Profile SFO Fuel is a limited liability non stock membership corporation organized for the purpose of leasing constructing and operating the fuel facilities at San Francisco International Airport SFO) SFO Fuel was organized on May 28 1997 as a limited liability company under the laws of the state of Delaware for the purpose of leasing constructing and operating the fuel system at SFO The San Francisco Airport Commission issued Special Facilities Lease Revenue Bonds on October 7 1997 and May 1 2000 The bonds were issued specifically to finance the costs of acquisition construction modification expansion and installation of certain additions replacements and improvements to the jet fuel receipt storage and distribution system serving SFO certain diesel and gasoline storage and delivery facilities for ground service equipment and related environmental costs SFO Fuel contracts with Aircraft Service International Inc for the operation and administration of the fuel system

Methodology The principal methodology used in this rating was Generic Project Finance Methodology published in December 2010 Please see the Rating Methodologies page on wwwmoodyscom for a copy of this methodology

29 March 2017 SFO Fuel Company LLC Update - Moodys aff irms the A3 ra ting on SFO Fuel Company LLC outlook stable 4

MOODYS INVESTORS SERVICE US PUBLIC FINANCE

copy 2017 Moodys Corporation Moodys Investors Service Inc Moodys Analytics Inc andor their licensors and affiliates (collectively MOODYS) All rights reserved

CREDIT RATINGS ISS UED BY MOODYS INVESTORS SERVICE INC AND ITS RATINGS AFFILIATES ( MIS) ARE MOODYS CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES CREDIT COMMITMENTS OR DEBT OR DEBT-LIKE SECURITIES AND MOODYS PUBLICATIONS MAY INCLUDE MOODYS CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES CREDIT COMMITMENTS OR DEBT OR DEBT-LIKE SECURITIES MOODYS DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT CREDIT RATINGS DO NOT ADDR ESS ANY OTHER RISK INCLUDING BUT NOT LIMITED TO LIQUIDITY RISK MARKET VALUERISK OR PRICE VOLATILITY CREDIT RATINGS AND MOODYS OPINIONS INCLUDED IN MOODYS PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT MOODYS PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLI SHED BY MOODYS ANALYTICS INC CREDIT RATINGS AND MOODYS PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE AND CREDIT RATINGS AND MOODYS PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE SELL OR HOLD PARTICULAR SECURITIES NEITHER CREDIT RATINGS NOR MOODYS PUBLICATIONSCOMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR MOODYS ISSUES ITSCREDIT RATINGS AND PUBLISHES MOODYS PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL WITH DUE CARE MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE HOLDING OR SALE

MOODYS CREDIT RATINGSAND MOODYS PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORSAND IT WOULD BE RECKLESS AND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODYS CREDIT RATINGS OR MOODYS PUBLICATIONSWHEN MAKING AN INVESTMENT DECISION IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW INCLUDING BUT NOT LIMITED TO COPYRIGHT LAW AND NON EOF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED REPACKAGED FURTHER TRAN SMITIED TRAN SFERRED DISS EMINATED REDISTRIBUTED OR RESOLD OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE IN WHOLE OR IN PART IN A ~IY FORM OR MANNER OR BY ANY MEANS WHATSOEVER BY ANY PERSON WITHOUT MOODYS PRIOR WRITIEN CONSENT

All information contained herein is obtained by MOODYS from sources believed by it to be accurate and reliable Because of the possibility of human or mechanical error as well as other factors however all information contained herein is provided AS IS without warranty of any kind MOODYS adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODYS considers to be reliable includ ing when appropriate independent third-party sources However MOODYS is not an auditor and cannot in every instance independentljt verify or validate information received in the rating process or in preparing the Moodys publications

To the extent permitted by law MOODYS and its directors officers employees agents representa tives licensors and suppliers disclaim liability to any person or entity for any indirect special consequential or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use any such information even if MOODYS or any of its directors officers employees agents representatives licensors or suppliers is advised in advance of the possibility of such losses or damages including but not limited to (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument Is not the subject of a particular credit rating assigned by MOODYS

To the extent permitted by law MOODYS and its directors offi cers employees agents representatives licensors and suppliers disclaim liability for any direct or compensatory losses or damages caused to any person or entity including but not limited to by any negligence (but excluding fraud willful misconduct or any other type of liability that for the avoidance or doubt by law cannot be excluded) on the part of or any contingency within or beyond the control of MOODYS or any of its directors officers employees agents representatives licensors or suppliers arising from or in connection with the information contained herein or the use of or inability to use any such information

NO WARRANTY EXPRESS OR IMPLIED AS TO THE ACCURACY TIMELINESS COMPLETENESS MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODYS IN ANY FORM OR MANNER WHATSOEVER

Moodys Investors Service Inc a wholly-owned credit rating agency subsidiary of Moodys Corporation (MCO) hereby discloses that most issuers of debt securities (including corporate and municipal bonds debentures notes and commercial paper) and preferred stock rated by Moodys Investors Service Inc have prior to assignment of any rating agreed to pay to Moodys Investors Service Inc for appraisal and rating services rendered by it fees ranging from $1500 to approximately $2500000 MCO and MIS also maintain policies and procedures to address the independence of Ml Ss ratings and rating processes Information regarding certain affiliations that may exist between directors of MCO and ra ted entities and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5 is posted annually at wwwmoodyscom under the heading Investor Relations - Corporate Governance- Director and Shareholder Affiliation Policy

Additional terms for Australia only Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODYS affil iate Moodys Investors Service Pty Limited ABN 61 003 399 657AFSL 336969 andor Moodys Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (asapplicable) This document is Intended to be provided only to wholesale clients within the meaning of section 761G of the Corporations Act 2001 By continuing to access this document from within Australia you represent to MOODYS that you are or are accessing the document as a representative of a wholesale client and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to retail clients within the meaning of section 761G of the Corporations Act 2001 MOODYS credit rating is an opinion as to the creditworthiness of a debt obligation of the issuer not on the equity securities of the issuer or any form of security that is available to retail investors It would be reckless and inappropriate for retail investors to use MOODYS credit ratings or publications when making an investment decision If in doubt you should contact your financial or other professional adviser

Additional terms for Japan only Moodys Japan KK (MJKK) is a wholly-owned credit rating agency subsidiary or Moodys Group Japan GK which is wholly-owned by Moodys Overseas Holdings Inc a wholly-owned subsidiary of MCO Moodys SF Japan KK (MSFJ) is a wholly-owned credit rating agency subsidiary of MJKK MSFJ is not a Nationally Recognized Statistical Rating Organization (NRSRO) Therefore credit ratings assigned by MSFJ are Non-NRSRO Credi Ra tings Non-NR SRO Credit Ratings are assigned by an entity that is not a NRSRO and consequently the rated obligation will not qualify for certain types or trea tment under US laws MJKKand MSFJ are credit rating agencies registered with the Japan Financial Services Agency and their registration numbers are FSA Commissioner Ratings) No 2 and 3 respectively

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securi ties (including corporate and municipal bonds debentures notes and commercial paper) and preferred stock rated by MJKK or MSFJ (asapplicable) have prior to assignment of any rating agreed to pay to MJKK or MSFJ(as applicable) for appraisal and rating services rendered by it fees ranging from JPYZ00000 to approximately JPY350000000

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements

REPORT NUMBER 1066681

Moonvs INVESTORS SERVICE

29 March 2017 SFO Fu el Company LLC Update - Moodys affirms t he A3 rating on SFO Fu el Company LLC out look stable

MOODYS INVESTORS SERVICE US PUBLIC FINANCE

copy 2017 Moodys Corporation Moodys Investors Service Inc Moodys Analytics Inc andor their licensors and affiliates (collectively MOODYS) All rights reserved

CREDIT RATINGS ISS UED BY MOODYS INVESTORS SERVICE INC AND ITS RATINGS AFFILIATES ( MIS) ARE MOODYS CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES CREDIT COMMITMENTS OR DEBT OR DEBT-LIKE SECURITIES AND MOODYS PUBLICATIONS MAY INCLUDE MOODYS CURRENT OPINIONS OF THE RELATIVE FUTURE CREDIT RISK OF ENTITIES CREDIT COMMITMENTS OR DEBT OR DEBT-LIKE SECURITIES MOODYS DEFINES CREDIT RISK AS THE RISK THAT AN ENTITY MAY NOT MEET ITS CONTRACTUAL FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT CREDIT RATINGS DO NOT ADDR ESS ANY OTHER RISK INCLUDING BUT NOT LIMITED TO LIQUIDITY RISK MARKET VALUERISK OR PRICE VOLATILITY CREDIT RATINGS AND MOODYS OPINIONS INCLUDED IN MOODYS PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT MOODYS PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVE MODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLI SHED BY MOODYS ANALYTICS INC CREDIT RATINGS AND MOODYS PUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE AND CREDIT RATINGS AND MOODYS PUBLICATIONS ARE NOT AND DO NOT PROVIDE RECOMMENDATIONS TO PURCHASE SELL OR HOLD PARTICULAR SECURITIES NEITHER CREDIT RATINGS NOR MOODYS PUBLICATIONSCOMMENT ON THE SUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR MOODYS ISSUES ITSCREDIT RATINGS AND PUBLISHES MOODYS PUBLICATIONS WITH THE EXPECTATION AND UNDERSTANDING THAT EACH INVESTOR WILL WITH DUE CARE MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FOR PURCHASE HOLDING OR SALE

MOODYS CREDIT RATINGSAND MOODYS PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORSAND IT WOULD BE RECKLESS AND INAPPROPRIATE FOR RETAIL INVESTORS TO USE MOODYS CREDIT RATINGS OR MOODYS PUBLICATIONSWHEN MAKING AN INVESTMENT DECISION IF IN DOUBT YOU SHOULD CONTACT YOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW INCLUDING BUT NOT LIMITED TO COPYRIGHT LAW AND NON EOF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED REPACKAGED FURTHER TRAN SMITIED TRAN SFERRED DISS EMINATED REDISTRIBUTED OR RESOLD OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE IN WHOLE OR IN PART IN A ~IY FORM OR MANNER OR BY ANY MEANS WHATSOEVER BY ANY PERSON WITHOUT MOODYS PRIOR WRITIEN CONSENT

All information contained herein is obtained by MOODYS from sources believed by it to be accurate and reliable Because of the possibility of human or mechanical error as well as other factors however all information contained herein is provided AS IS without warranty of any kind MOODYS adopts all necessary measures so that the information it uses in assigning a credit rating is of sufficient quality and from sources MOODYS considers to be reliable includ ing when appropriate independent third-party sources However MOODYS is not an auditor and cannot in every instance independentljt verify or validate information received in the rating process or in preparing the Moodys publications

To the extent permitted by law MOODYS and its directors officers employees agents representa tives licensors and suppliers disclaim liability to any person or entity for any indirect special consequential or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use any such information even if MOODYS or any of its directors officers employees agents representatives licensors or suppliers is advised in advance of the possibility of such losses or damages including but not limited to (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument Is not the subject of a particular credit rating assigned by MOODYS

To the extent permitted by law MOODYS and its directors offi cers employees agents representatives licensors and suppliers disclaim liability for any direct or compensatory losses or damages caused to any person or entity including but not limited to by any negligence (but excluding fraud willful misconduct or any other type of liability that for the avoidance or doubt by law cannot be excluded) on the part of or any contingency within or beyond the control of MOODYS or any of its directors officers employees agents representatives licensors or suppliers arising from or in connection with the information contained herein or the use of or inability to use any such information

NO WARRANTY EXPRESS OR IMPLIED AS TO THE ACCURACY TIMELINESS COMPLETENESS MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCH RATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODYS IN ANY FORM OR MANNER WHATSOEVER

Moodys Investors Service Inc a wholly-owned credit rating agency subsidiary of Moodys Corporation (MCO) hereby discloses that most issuers of debt securities (including corporate and municipal bonds debentures notes and commercial paper) and preferred stock rated by Moodys Investors Service Inc have prior to assignment of any rating agreed to pay to Moodys Investors Service Inc for appraisal and rating services rendered by it fees ranging from $1500 to approximately $2500000 MCO and MIS also maintain policies and procedures to address the independence of Ml Ss ratings and rating processes Information regarding certain affiliations that may exist between directors of MCO and ra ted entities and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5 is posted annually at wwwmoodyscom under the heading Investor Relations - Corporate Governance- Director and Shareholder Affiliation Policy

Additional terms for Australia only Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODYS affil iate Moodys Investors Service Pty Limited ABN 61 003 399 657AFSL 336969 andor Moodys Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (asapplicable) This document is Intended to be provided only to wholesale clients within the meaning of section 761G of the Corporations Act 2001 By continuing to access this document from within Australia you represent to MOODYS that you are or are accessing the document as a representative of a wholesale client and that neither you nor the entity you represent will directly or indirectly disseminate this document or its contents to retail clients within the meaning of section 761G of the Corporations Act 2001 MOODYS credit rating is an opinion as to the creditworthiness of a debt obligation of the issuer not on the equity securities of the issuer or any form of security that is available to retail investors It would be reckless and inappropriate for retail investors to use MOODYS credit ratings or publications when making an investment decision If in doubt you should contact your financial or other professional adviser

Additional terms for Japan only Moodys Japan KK (MJKK) is a wholly-owned credit rating agency subsidiary or Moodys Group Japan GK which is wholly-owned by Moodys Overseas Holdings Inc a wholly-owned subsidiary of MCO Moodys SF Japan KK (MSFJ) is a wholly-owned credit rating agency subsidiary of MJKK MSFJ is not a Nationally Recognized Statistical Rating Organization (NRSRO) Therefore credit ratings assigned by MSFJ are Non-NRSRO Credi Ra tings Non-NR SRO Credit Ratings are assigned by an entity that is not a NRSRO and consequently the rated obligation will not qualify for certain types or trea tment under US laws MJKKand MSFJ are credit rating agencies registered with the Japan Financial Services Agency and their registration numbers are FSA Commissioner Ratings) No 2 and 3 respectively

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securi ties (including corporate and municipal bonds debentures notes and commercial paper) and preferred stock rated by MJKK or MSFJ (asapplicable) have prior to assignment of any rating agreed to pay to MJKK or MSFJ(as applicable) for appraisal and rating services rendered by it fees ranging from JPYZ00000 to approximately JPY350000000

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements

REPORT NUMBER 1066681

Moonvs INVESTORS SERVICE

29 March 2017 SFO Fu el Company LLC Update - Moodys affirms t he A3 rating on SFO Fu el Company LLC out look stable

Related Documents