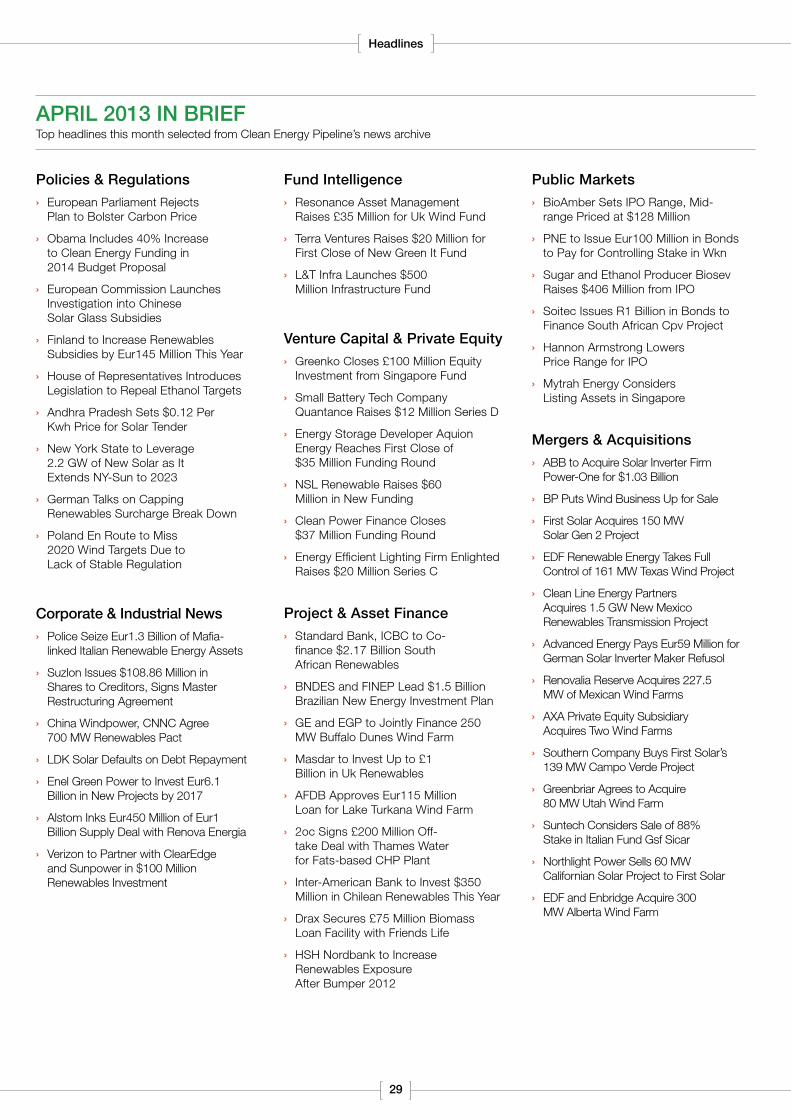

1 S uccessful solar inverter manufacturers have emerged as the most desirable acquisition targets in the photovoltaic (PV) supply chain, as reflected by Switzerland-based power group ABB’s announcement in April that it has agreed to acquire US inverter maker Power One at a valuation of $1.03 billion. The deal is the fifth largest M&A transaction announced in the entire clean energy space this year, and is the largest acquisition of a pure-play solar technology company since French oil giant Total bought a controlling stake in US solar cell, panel and system maker SunPower Corp for $1.37 billion in June 2011. ABB said it aims to leverage Power One’s global business with its own operations to create the world’s largest supplier of PV inverters, a section of the market that has proven relatively resistant to the tide of bankruptcies and losses that have plagued solar module, cell and wafer makers over the past two years. A recent IHS study showed that aggregate revenue in the global inverter market hit $7.1 billion in 2012, a 5% increase on the previous year. SMA Solar, the current market leader, did report a 55% fall in consolidated net profit for 2012 due to solar subsidy cuts in Europe, but the key statistic in those results was that its net profit remained healthy at Eur75.1 million, a far cry from the enormous losses incurred by leading companies in other PV sub-sectors. The Power One takeover is just one of several M&A deals launched in the inverter sector this year. Colorado-based power conversion group Advanced Energy Industries paid Eur59 million ($76.6 million) to acquire German solar inverter maker REFUsol earlier in April, less than a month after SMA paid $37 million to acquire a 72.5% stake in Chinese counterpart Jiangsu Zeversolar New Energy. The reason that inverter makers have become so prized is that an inverter is a genuinely specialised product that can play a crucial role in improving the bankability and long-term profitability of a solar farm, as opposed to a module, which has essentially become a commodity. In a presentation at the launch of the Clean Energy Europe Finance Guide 2013 last month, SMA Solar Vice President of Sales Tomas Goetz said: “If you look at a PV plant today, you can pick between 10 and 15 Tier One modules and it’s justified to say modules are a commodity. You don’t get much of a difference whatever ABB BETS BIG ON SOLAR INVERTER MARKET WITH POWER ONE BUY CONTENTS Issue #14 May 2013 Editorial Review...............................1 { ABB bets big on solar inverter market with Power One buy Data..................................................3 Interviews & Analysis.......................5 { Clean energy investment drops to new four- year low in 1Q13 { LifeCos and Japanese banks fill Canadian project finance gap left by retreat of European banks { Valuations for German onshore wind farms have risen to all-time high { Cleantech VC investor Electranova seeks additional corporate partners { Apex Wind Energy aims to add asset management to development activities { Balance sheet investors dominate Alberta wind energy financing { German offshore wind market opens up for UK cable provider JDR { OneRoof Energy set to close new equity round and solar leasing fund within 90 days { ‘eBay for solar’ company offers streamlined approach to project M&A { Bidder intends to ramp up Suntech’s Goodyear plant to 100 MW { Germany’s cash incentive for energy storage systems approved and awaiting final details { Likelihood of Crown Estate Round 4 hinges on CfD implementation { NREL to diversify funding base post- sequestration and focus on systems integration { US energy conversion start-up targets $10- 15 million equity round { US waste heat company targets global acquisitions in bid for growth { Shale gas will not have major impact on UK energy market this decade { US gas prices set to rise as market evolves, but cheap shale gas is here to stay Headlines.......................................29 Events............................................31 Ronan Murphy Editor Clean Energy Pipeline A division of VB/Research Ltd. Centaur Media plc WELLS POINT 79 Wells Street London, W1T 3QN +44 (0) 207 251 8000 (EMEA) +1 202 386 6715 (Americas) Managing Editor: Estelle Lloyd Editor: Ronan Murphy Production Editor: Tom Naylor Sales Director: Sonja van Linden Tol www.cleanenergypipeline.com Subscription enquiries: [email protected] Monthly Clean Energy Investment Analysis & News Report MONTHLY REVIEW www.cleanenergypipeline.com Image courtesy of ABB Group

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Successful solar inverter manufacturers have emerged as the most desirable

acquisition targets in the photovoltaic (PV) supply chain, as reflected by Switzerland-based power group ABB’s announcement in April that it has agreed to acquire US inverter maker Power One at a valuation of $1.03 billion.

The deal is the fifth largest M&A transaction announced in the entire clean energy space this year, and is the largest acquisition of a pure-play solar technology company since French oil giant Total bought a controlling stake in US solar cell, panel and system maker SunPower Corp for $1.37 billion in June 2011.

ABB said it aims to leverage Power One’s global business with its own operations to create the world’s largest supplier of PV inverters, a section of the market that has proven relatively resistant to the tide of bankruptcies and losses that have plagued solar module, cell and wafer makers over the past two years.

A recent IHS study showed that aggregate revenue in the global inverter market hit $7.1 billion in 2012, a 5% increase on the previous year.

SMA Solar, the current market leader, did report a 55% fall in consolidated net profit for 2012 due to solar subsidy cuts in Europe, but the key statistic in those results was that its net profit remained healthy at Eur75.1 million, a far cry from the enormous losses incurred by leading companies in other PV sub-sectors.

The Power One takeover is just one of several M&A deals launched in the inverter

sector this year. Colorado-based power conversion group Advanced Energy Industries paid Eur59 million ($76.6 million) to acquire German solar inverter maker REFUsol earlier in April, less than a month after SMA paid $37 million to acquire a 72.5% stake in Chinese counterpart Jiangsu Zeversolar New Energy.

The reason that inverter makers have become so prized is that an inverter is a genuinely specialised product that can play a crucial role in improving the bankability and long-term profitability of a solar farm, as opposed to a module, which has essentially become a commodity.

In a presentation at the launch of the Clean Energy Europe Finance Guide 2013 last month, SMA Solar Vice President of Sales Tomas Goetz said: “If you look at a PV plant today, you can pick between 10 and 15 Tier One modules and it’s justified to say modules are a commodity. You don’t get much of a difference whatever

ABB BetS Big On SOlAr inverter mArket with POwer One BUy

COntentSissue #14 may 2013

editorial review...............................1 { ABB bets big on solar inverter market with

Power One buy

Data..................................................3

interviews & Analysis.......................5 { Clean energy investment drops to new four-

year low in 1Q13

{ LifeCos and Japanese banks fill Canadian project finance gap left by retreat of European banks

{ Valuations for German onshore wind farms have risen to all-time high

{ Cleantech VC investor Electranova seeks additional corporate partners

{ Apex Wind Energy aims to add asset management to development activities

{ Balance sheet investors dominate Alberta wind energy financing

{ German offshore wind market opens up for UK cable provider JDR

{ OneRoof Energy set to close new equity round and solar leasing fund within 90 days

{ ‘eBay for solar’ company offers streamlined approach to project M&A

{ Bidder intends to ramp up Suntech’s Goodyear plant to 100 MW

{ Germany’s cash incentive for energy storage systems approved and awaiting final details

{ Likelihood of Crown Estate Round 4 hinges on CfD implementation

{ NREL to diversify funding base post-sequestration and focus on systems integration

{ US energy conversion start-up targets $10-15 million equity round

{ US waste heat company targets global acquisitions in bid for growth

{ Shale gas will not have major impact on UK energy market this decade

{ US gas prices set to rise as market evolves, but cheap shale gas is here to stay

headlines.......................................29

events............................................31

ronan murphy

Editor

Clean energy PipelineA division of VB/Research Ltd.Centaur Media plcWELLS POINT79 Wells StreetLondon, W1T 3QN

+44 (0) 207 251 8000 (EMEA)+1 202 386 6715 (Americas)

managing editor: Estelle Lloydeditor: Ronan MurphyProduction editor: Tom NaylorSales Director: Sonja van Linden Tol

www.cleanenergypipeline.com

Subscription enquiries: [email protected]

Monthly Clean Energy Investment Analysis & News Report

MoNthly REvIEwwww.cleanenergypipeline.com

Imag

e co

urte

sy o

f AB

B G

roup

2

lowered industrial output and created a surplus of allowances in the market.

In that sense, the failure of backloading could be beneficial in that it may force European legislators to address the complete restructuring effort needed to make the ETS viable. However, this task will be made all the more difficult by the political message sent out by the vote, which indicates that European Union governments willing to sacrifice climate goals in favour of protecting industry now outnumber those who are not.

Siemens maintains offshore wind dominance as vestas suffers fresh crisis

German engineering group Siemens secured a 924 MW contract in April to supply offshore wind turbines to three projects in Germany, cementing the industrial group’s dominance of the European offshore wind market.

At the same time, its main European offshore wind rival, Denmark-based Vestas, appointed its third chief financial officer (CFO) in 18 months in a bid to reverse heavy financial losses.

The Siemens order comprised 154 offshore wind turbines that will be delivered to Danish utility DONG Energy for the Gode Wind projects on Germany’s coast, which are expected to be built out from 2015.

DONG acquired the development-stage wind farms from PNE Wind last year.

Siemens will supply its 6 MW turbine model to DONG for the Gode Wind projects. Last year, the two companies agreed a Eur2.5 billion deal for Siemens to deliver 300 of the same models to DONG’s UK projects between 2014 and 2017.

The scale of the new contract means Siemens is well-placed to maintain its position as the largest supplier of offshore wind turbines in Europe. It accounted for 58% of the 4,995 MW of offshore wind capacity installed in the continent’s waters as of the end of 2012, according to European Wind Energy Association data. Siemens’ turbines also represented 74% of the 1,166 MW brought online during 2012.

In direct contrast, Vestas, the world’s second-largest manufacturer of offshore wind turbines by installed volume, did not install any offshore turbines in Europe last year despite providing 28% of the continent’s overall capacity to date.

Vestas’s attempts to catch up with Siemens in the offshore space were hindered by the company’s wider financial difficulties, which were exacerbated in April when CFO Dag Andresen stood down due to personal reasons after less than a year in the role.

Andresen was immediately replaced by Marika Fredrikkson, formerly the CFO of car safety equipment giant Autoliv. She takes on the daunting task of reversing the fortunes of a company that announced a post-tax loss of Eur963 million in 2012, following a Eur166 million loss the previous year.

Falling demand in the global onshore wind market has forced Vestas into an extensive restructuring and downsizing of its workforce. Its offshore business has been impacted in the form of delays to its next-generation 7 MW turbine. It confirmed last year that the first prototype of this design is now expected to be installed in Denmark in 2014 instead of 2013.

By contrast, Siemens is already trialling its own next-generation 6 MW wind turbine. The design was first tested in 2011 and in January this year trials started at the Gunfleet Sands III demonstration wind farm in UK waters.

Ronan Murphy Editor

you choose. At the end of the day it’s the inverter that makes the difference between a producing power plant and a distressed asset.”

Carbon market vote leaves european Union clean energy policy in disarray

The European Parliament’s rejection in April of a plan to boost the ailing carbon Emissions Trading Scheme (ETS) leaves serious doubt over the programme’s future, and the ability of Brussels to drive investment in clean energy.

A proposal to ‘backload’ the imminent release of 900 million new carbon emissions allowances to the end of the decade was voted down by 334 to 315, causing the price of carbon to subsequently fall 50% to a record low of Eur2.55 per tonne.

Although dramatic, in real terms the price fall made no difference, as the price of carbon has already been too low to incentivise low carbon investment for months. The high of Eur30 per tonne reached in 2008 was in reality merely the base minimum required for the scheme to have a viable impact on industry.

The backloading proposal was always a measure that would have deferred addressing the main issue - that the recession impacting the Eurozone has

editorial review

3

Data

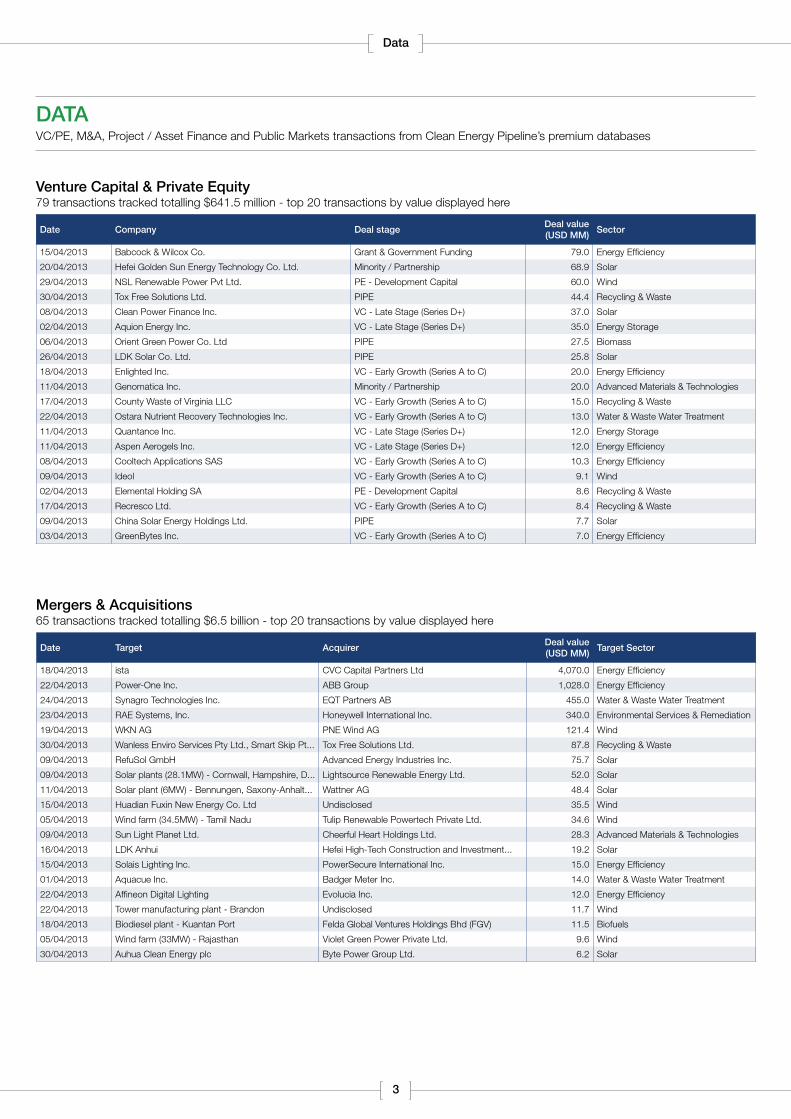

DAtAVC/PE, M&A, Project / Asset Finance and Public Markets transactions from Clean Energy Pipeline’s premium databases

venture Capital & Private equity79 transactions tracked totalling $641.5 million - top 20 transactions by value displayed here

mergers & Acquisitions65 transactions tracked totalling $6.5 billion - top 20 transactions by value displayed here

Date Company Deal stageDeal value (USD mm)

Sector

15/04/2013 Babcock & Wilcox Co. Grant & Government Funding 79.0 Energy Efficiency

20/04/2013 Hefei Golden Sun Energy Technology Co. Ltd. Minority / Partnership 68.9 Solar

29/04/2013 NSL Renewable Power Pvt Ltd. PE - Development Capital 60.0 Wind

30/04/2013 Tox Free Solutions Ltd. PIPE 44.4 Recycling & Waste

08/04/2013 Clean Power Finance Inc. VC - Late Stage (Series D+) 37.0 Solar

02/04/2013 Aquion Energy Inc. VC - Late Stage (Series D+) 35.0 Energy Storage

06/04/2013 Orient Green Power Co. Ltd PIPE 27.5 Biomass

26/04/2013 LDK Solar Co. Ltd. PIPE 25.8 Solar

18/04/2013 Enlighted Inc. VC - Early Growth (Series A to C) 20.0 Energy Efficiency

11/04/2013 Genomatica Inc. Minority / Partnership 20.0 Advanced Materials & Technologies

17/04/2013 County Waste of Virginia LLC VC - Early Growth (Series A to C) 15.0 Recycling & Waste

22/04/2013 Ostara Nutrient Recovery Technologies Inc. VC - Early Growth (Series A to C) 13.0 Water & Waste Water Treatment

11/04/2013 Quantance Inc. VC - Late Stage (Series D+) 12.0 Energy Storage

11/04/2013 Aspen Aerogels Inc. VC - Late Stage (Series D+) 12.0 Energy Efficiency

08/04/2013 Cooltech Applications SAS VC - Early Growth (Series A to C) 10.3 Energy Efficiency

09/04/2013 Ideol VC - Early Growth (Series A to C) 9.1 Wind

02/04/2013 Elemental Holding SA PE - Development Capital 8.6 Recycling & Waste

17/04/2013 Recresco Ltd. VC - Early Growth (Series A to C) 8.4 Recycling & Waste

09/04/2013 China Solar Energy Holdings Ltd. PIPE 7.7 Solar

03/04/2013 GreenBytes Inc. VC - Early Growth (Series A to C) 7.0 Energy Efficiency

Date target AcquirerDeal value (USD mm)

target Sector

18/04/2013 ista CVC Capital Partners Ltd 4,070.0 Energy Efficiency

22/04/2013 Power-One Inc. ABB Group 1,028.0 Energy Efficiency

24/04/2013 Synagro Technologies Inc. EQT Partners AB 455.0 Water & Waste Water Treatment

23/04/2013 RAE Systems, Inc. Honeywell International Inc. 340.0 Environmental Services & Remediation

19/04/2013 WKN AG PNE Wind AG 121.4 Wind

30/04/2013 Wanless Enviro Services Pty Ltd., Smart Skip Pt... Tox Free Solutions Ltd. 87.8 Recycling & Waste

09/04/2013 RefuSol GmbH Advanced Energy Industries Inc. 75.7 Solar

09/04/2013 Solar plants (28.1MW) - Cornwall, Hampshire, D... Lightsource Renewable Energy Ltd. 52.0 Solar

11/04/2013 Solar plant (6MW) - Bennungen, Saxony-Anhalt... Wattner AG 48.4 Solar

15/04/2013 Huadian Fuxin New Energy Co. Ltd Undisclosed 35.5 Wind

05/04/2013 Wind farm (34.5MW) - Tamil Nadu Tulip Renewable Powertech Private Ltd. 34.6 Wind

09/04/2013 Sun Light Planet Ltd. Cheerful Heart Holdings Ltd. 28.3 Advanced Materials & Technologies

16/04/2013 LDK Anhui Hefei High-Tech Construction and Investment... 19.2 Solar

15/04/2013 Solais Lighting Inc. PowerSecure International Inc. 15.0 Energy Efficiency

01/04/2013 Aquacue Inc. Badger Meter Inc. 14.0 Water & Waste Water Treatment

22/04/2013 Affineon Digital Lighting Evolucia Inc. 12.0 Energy Efficiency

22/04/2013 Tower manufacturing plant - Brandon Undisclosed 11.7 Wind

18/04/2013 Biodiesel plant - Kuantan Port Felda Global Ventures Holdings Bhd (FGV) 11.5 Biofuels

05/04/2013 Wind farm (33MW) - Rajasthan Violet Green Power Private Ltd. 9.6 Wind

30/04/2013 Auhua Clean Energy plc Byte Power Group Ltd. 6.2 Solar

4

Data

Project / Asset Finance120 completed transactions tracked totalling $6.0 billion - top 50 transactions by value displayed here

Date Project Financing typeDeal value (USD mm)

Sector

08/04/2013 Wind farm (250MW) - Buffalo Dunes Tax equity finance 370.0 Wind

03/04/2013 Wind farm (300MW) - Halkirk Pre construction debt 340.2 Wind

22/04/2013 Solar plant (128MW) - Brandenburg Equity finance 261.0 Solar

02/04/2013 Solar plant (50MW) - Broken Hill Construction debt 209.0 Solar

12/04/2013 Waste to energy plants - China Government guarantee / finance 200.0 Biomass

18/04/2013 Solar plant (100MW) - Gulang Phase II Construction debt 192.2 Solar

02/04/2013 Solar plant (150MW) - Haian Construction debt 189.6 Solar

24/04/2013 Solar plant (50MW) - Rajasthan (Godawari Green) Construction debt 129.0 Solar

09/04/2013 Wind farm (50MW) - FWEL-II (Foundation Wind Energy-II... Construction debt 126.7 WInd

08/04/2013 Solar plant (50MW) - Hainan Zhou Construction debt 117.0 Solar

30/04/2013 Solar Plant (44MW) - Touwsrivier Project debt 111.0 Solar

16/04/2013 Solar plant (50MW) - Ganbala, Chuxiong Yi Autonomous... Construction debt 110.0 Solar

08/04/2013 Biomass plant (19MW) - Beckton Equity finance 107.2 Biomass

25/04/2013 Solar plant (30MW) - Aura solar I Government guarantee / finance, Pre constru... 100.0 Solar

17/04/2013 Biomass plants - China Construction debt 100.0 Biomass

16/04/2013 Solar plant (50MW) - Gansu Nantan Construction debt 99.4 Solar

17/04/2013 Solar plant (50MW) - Gulang Phase I Construction debt 96.8 Solar

27/04/2013 Solar plants (30MW) - Sukhothai Construction debt 94.8 Solar

30/04/2013 Wind farm (45MW) - Yereimentau, Akmola Government guarantee / finance 94.0 Wind

23/04/2013 Wind farm (50.4MW) - La Guajira Phase II Government guarantee / finance 93.7 Wind

15/04/2013 Solar plant (57MW) - Nakhonpathom and Suphanburi Construction debt 85.0 Solar

04/04/2013 Wind farm (38MW) - El Candal Construction debt 82.5 Wind

23/04/2013 Solar plant (20MW) - Atwell Island Project debt 80.0 Solar

08/04/2013 Solar plant (26MW) - Borrego Springs Project debt 80.0 Solar

12/04/2013 Wind farm (49.5MW) - Shiziping Construction debt 78.8 Wind

04/04/2013 Wind farm (36MW) - El Segredal Construction debt 78.1 Wind

02/04/2013 Solar plant (33MW) - Rajasthan Construction debt 77.2 Solar

01/04/2013 Hydro plant (48MW) - San Bartolo Pre construction debt 76.7 Hydro

08/04/2013 Wind farm (48MW) - Lulong Construction debt 73.3 Wind

24/04/2013 Wind farm (49.5MW) - Bayannur Construction debt 71.6 Wind

09/04/2013 Solar plant (30MW) - Binhai New Area, Haian County, Jia... Construction debt 70.2 Solar

02/04/2013 Solar plants (22MW) - Tulare Pre construction debt 70.2 Solar

02/04/2013 Solar plants - Tuticorin, China. Construction debt 69.0 Solar

07/04/2013 Wind farm (49.5MW) - Zijingshan Construction debt 67.9 Wind

15/04/2013 Wind farm (54MW) - Jaisalmer Construction debt 65.7 Wind

30/04/2013 Electricidade dos Açores 2011-2016 investment prog... Government guarantee / finance 65.1 Geothermal

02/04/2013 Solar plant (27MW) - M&B Switchgears Ltd Construction debt 63.2 Solar

09/04/2013 Wind farm (48MW) - Bijiashan, Jiangsi Pre construction debt 63.1 WInd

02/04/2013 Solar plant (30MW) - Laoying Yan Construction debt 61.5 Solar

11/04/2013 Solar plant (18MW) - Foothills Phase II Equity finance 57.4 Solar

11/04/2013 Solar plant (100MW) - Helios 1 and 2 Government guarantee / finance 55.3 Solar

16/04/2013 Solar plant (17MW) - Foothills Phase I Equity finance 54.2 Solar

17/04/2013 Solar plant (14MW) - El Salvador Government guarantee / finance 51.0 Solar

11/04/2013 Solar plant (16MW) - Davis-Monthan Air Force Base Government guarantee / finance, Pre constru... 51.0 Solar

16/04/2013 Wind farm (32MW) - Zhumadian, Henan Construction debt 48.0 Wind

23/04/2013 Wind farm (25.2MW) - La Guajira Phase I Government guarantee / finance, Pre constru... 46.9 Wind

17/04/2013 Solar plant (20MW) - Liuyuan Phase I Construction debt 46.8 Solar

02/04/2013 Solar plant (20MW) - Zoucheng Construction debt 46.8 Solar

27/04/2013 Wind farm (22MW) - Bieshan Construction debt 40.1 Wind

25/04/2013 Solar plant (20MW) - Uqturpan (Wushen) Longbai Construction debt 40.1 Solar

Public markets

Date issuer issue typeProceeds

(USD mm)Sector

23/04/2013 Alupar Investimento S.A. IPO 421.0 Energy Efficiency

16/04/2013 Biosev IPO 406.0 Biofuels

5

CleAn energy inveStment DrOPS tO new FOUr-yeAr lOw in 1Q13

Ronan Murphy

Investment in global clean energy fell to $46.1 billion in 1Q 2013, the lowest quarterly level since 2Q 2009, according to a preliminary data analysis released by Clean Energy Pipeline.

Total investment declined 35% sequentially from the $70.7 billion recorded in 4Q12 and 31% from $66.6 billion invested a year ago in 1Q12.

The decrease was attributable to a massive drop of more than 50% in clean energy project finance caused by an abrupt slowdown of activity in the US and South Africa.

US investment in wind energy, the country’s largest renewable power sector, fell from a record $5.8 billion in 4Q12 to $1.6 billion in 1Q13, the lowest quarterly volume recorded in the past four years. The dip was caused by Congress’s delayed renewal of the wind energy production tax credit (PTC), which caused developers to rush projects to financial close in the fourth quarter in fear of the incentive expiring on December 31.

Although the PTC was eventually renewed, the delay meant very few projects were sufficiently advanced to close financing in 1Q12. The uncertainty surrounding the PTC last year means that investment in wind projects is likely to remain depressed in 2Q13. Developers may bring projects closer to construction in 3Q and 4Q, but the sector is likely to record far less investment this year than last.

Project finance levels in the fourth quarter of 2012 were also heavily boosted by the first round of South Africa’s renewable energy tender, under which 28 projects totalling $5.7 billion reached financial close.

The second South African tender, which is estimated to represent $3.3 billion of investment, was originally slated to take place in 1Q13, but has been delayed to this summer at the earliest, leaving a gaping hole in global investment levels.

“At the end of last year a rush to finance US wind energy projects before the expected

from 4Q12 to $1.67 billion. Although the figure was 27% less than the $2.31 billion invested in 1Q12, it was still the first quarter-on-quarter increase since 3Q11.

The main driver for VC/PE activity was the biofuel sector, which received $319 million, or 19% of all investment. This is the first time that biofuel received the most VC/PE investment of any cleantech sector in a single quarter, and was attributable to a $292 million investment in January by Brazilian development bank BNDES in ethanol developer GraalBio (now known as GranBio).

Public market activity fell to a new four-year low of $586 million in 1Q13, despite two major deals in the form of US smart grid company Silver Spring Networks’ $93 million flotation on the New York Stock Exchange and UK wind energy investment fund Greencoat UK Wind’s $394 million offering on the London Stock Exchange.

The continued decline in spite of these deals was due to a virtual cessation of Chinese clean energy public market transactions, which is a role reversal from recent years, when Asia has propped up clean energy public market figures hit by a virtual freeze on European and North American activity. ■

expiration of the PTC and the closure of $5.7 billion financing for the first round of South African renewable energy projects artificially boosted investment volumes,” said Douglas Lloyd, Chief Executive Officer of Clean Energy Pipeline. “It was always going to be difficult to match this level of activity, particularly in the first quarter of the year.

“However, this sharp quarterly decline is not a one off. Total new investment has now fallen from a quarterly high of $88.3 billion in 4Q10 to $46 billion in 1Q13. Given ongoing subsidy cuts, low natural gas prices in North America and fragile capital markets, it’s hard to predict a reversal of this trend in the coming year.”

Global clean energy M&A activity tumbled to $11 billion in 1Q13, almost half the $20.8 billion recorded in 4Q12 and the $21.7 billion tracked in the corresponding period of 2012. The decrease was caused by an absence of large deals, with only three exceeding $500 million taking place during the quarter. Those transactions were valued at a combined total of $1.7 billion, significantly less than the $12.3 billion worth of similarly sized deals announced in 4Q12.

Clean energy venture capital and private equity (VC/PE) investment was the one industry bright spot in 1Q13, rising 1%

interviews & Analysis

total new Clean energy investment – 1Q09 to 1Q13

Source: Clean Energy Pipeline / VB/Research Ltd.

StAtiStiCS AnD trenDS

1Q13

4Q12

3Q12

2Q12

1Q12

4Q11

3Q11

2Q11

1Q11

4Q10

3Q10

2Q10

1Q10

4Q09

3Q09

2Q09

1Q09

Small-scale project investmentProject & asset finance

Venture capital & private equity (excluding buyouts) Public markets

0

20

40

60

80

100

Dea

l val

ue ($

bill

ion)

4-QUARTER MOVINGAVERAGE

6

June 27th 2013 • London Marriott Hotel Grosvenor Square

THE UK ENERGY SUMMIT 2013Building a sustainable and affordable future?

Roger Harrabin

Energy and Environment Analyst

BBC

Rt Hon Edward Davey MP

Secretary of State

Department of Energy and Climate

Angela Knight CBE

Chief Executive Officer

Energy UK

Nick Molho

Head of Energy Policy

WWF-UK

Douglas Parr

Chief Scientist and Policy Director

Greenpeace UK

HEAR FRoM ExPERtS iNCLUDiNG

www.energysummituk.com

Join top policy makers, industry executives and influential thinkers for a thought provoking, solutions focused debate on the future of UK Energy policy. Gain insight into how the UK will balance securing a long term energy supply with affordability and the impact of global trends.

Derek Lickorish

Chairman

Fuel Poverty Advisory Group

Join the conversation on Twitter #UKEnergy / @EG_Energy

GOLD SPONSOR

UK Energy 2013-Media partners full page ad.indd 1 02/05/2013 11:33

7

liFeCOS AnD JAPAneSe BAnkS Fill CAnADiAn PrOJeCt FinAnCe gAP leFt By retreAt OF eUrOPeAn BAnkS

Ronan Murphy

The renewable energy project finance market in Canada has remained buoyant despite a retreat from European banks thanks to increased participation from Japanese lenders and Canadian life insurance companies (LifeCos), according to a new quarterly report by KPMG and Clean Energy Pipeline.

European banks have lowered their exposure to Canadian renewables as a result of their overall lending capacity being impacted by the ongoing sovereign debt crisis in the Eurozone and the imposition of new financing regulations such as Basel III.

Japanese financial institutions increased their lending to renewable energy projects worldwide last year. Sumitomo Mitsui Banking Corp, Bank of Tokyo-Mitsubishi UFJ and Mizuho Corporate Bank were all in the top six debt providers for number of deals in Clean Energy Pipeline’s league table for renewable energy project financing in 2013.

These banks all raised their exposure to the Canadian market in 2012 and 2013, attracted by Canada’s continuing political stability and strong economy. Notable project finance deals supported by Japanese debt include the $700 million financing of Pattern Energy’s 270 MW South Kent wind farm in Ontario in March 2013; the $282 million financing of the British Columbia-based 99 MW Cape Scott wind farm in December 2012; the $300 million financing of Invenergy LLC’s 156 MW Des Moulins wind farm in Quebec in the same month; and the C$227 million financing in July 2012 of a 60 MW solar portfolio in Ontario owned by Northland Power.

Speaking in an interview for the report, Paul Bradley, Chief Financial Officer of Northland Power, told Clean Energy Pipeline: “The state of the project finance market is excellent for good projects. On the bank side a number of well structured renewable energy projects are still getting long-tenor money. The European banks have pulled away which left a bit of a void in the long

interviews & Analysis

tenor market but this has been picked up by the life companies and the Japanese banks have stepped up.

“Long-term money is certainly still out there. For example we just closed a C$227 million financing for our first six solar projects and we got an 18-year tenor from Union Bank, Bank Mizuho and CIT. It was harder to get but we got it none the less. There is a bit of a loss of financing capacity in the market but it’s only the very marginal projects that have lost out.”

Another increasingly prominent source of project finance for clean energy projects in Canada is Canadian life insurance (LifeCos) companies looking for long-term, predictable assets which they can lend to.

Michael Bernstein, President and Chief Executive Officer of Capstone Infrastructure, an investor in Canadian clean energy projects, explained that the LifeCos bolster the markets for financing of clean energy projects in Canada through private placements, and also offer the opportunity for increased participation from Canadian commercial banks.

“We have a pretty deep private placement market in the form of both underwriters who will go to smaller institutions to do either a rated or unrated 18-20 year (or even longer) bond placement, or the traditional Canadian LifeCos, such as Canada Life, Manulife and Sunlife, who were amongst the very first investors in renewable energy infrastructure,” he said. “Financing is still available through these avenues.

“Some of the Canadian banks are stepping up to a certain degree although these tend

to be the mini-perm structures with the idea that the take out is with the LifeCos or with a privately placed debt issuance.”

While LifeCos will invest in wind and solar projects, it is hydro that fits best with their desire for extremely long-term assets. Power purchase agreements for hydro facilities can be up to 40 years.

Jean Trudel, Chief Investment Officer of Canadian power producer Inngergex Energy, said: “[Hydro} is not a banking market but more of a life insurance company market. The last financing we closed in July 2012 was for an under-construction stage hydro facility where we got 39-year money at just over 5%, which was very compelling. Canadian bonds are so low right now that the all in rates are very attractive.”

Georges Arbache, Vice President, Global Power & Utilities, Transactions and Restructuring, at KPMG, stated that the amount of financing available per deal under private placements involving Canadian LifeCos is generally subject to a soft cap of $450-$500 million.

“With an attractive low rate environment, developers are rushing to secure favourable long-term financing structures, primarily filled by Life Insurance Company private placement solutions,” he said.

“While other options exist, non-Canadian LifeCo’s tend to be materially more expensive. Japanese Banks can be an option, however we rarely see more than 15-year debt being offered at wider spreads. That said, rated long-term bond solutions are becoming available, which may reduce some of the shortfall with tighter pricing.” ■

PrOJeCt FinAnCe

global Project / Asset Finance by Quarter and region – 1Q09 to 1Q13

Source: Clean Energy Pipeline / VB/Research Ltd.

1Q13

4Q12

3Q12

2Q12

1Q12

4Q11

3Q11

2Q11

1Q11

4Q10

3Q10

2Q10

1Q10

4Q09

3Q09

2Q09

1Q09

0

10

20

30

40

50

60

Asia PacificEurope North America Rest of the World Number of deals

Dea

l val

ue ($

bill

ion) N

umb

er of d

eals

0

100

200

300

400

500

600

8

vAlUAtiOnS FOr germAn OnShOre winD FArmS hAve riSen tO All-time high

Ronan Murphy

Valuations of onshore wind projects in Germany have risen to an “all-time high” due to increased appetite from municipal utilities and investors seeking a safe haven from volatility in other European markets, according to a leading investor in the sector.

Michael Ebner, Head of Infrastructure at investment firm KGAL GmbH, told Clean Energy Pipeline: “Prices of renewable energy projects are going up to all-time high levels. In the wind sector, where feed-in tariffs are relatively stable, prices have increased by 10%-15% during the past two years.”

Mergers and acquisitions (M&A) in the German wind farm sector increased significantly in 2012, with 27 German wind projects acquired for a total of $1.6 billion, a significant increase on the 19 projects totalling $971 million transacted in 2011, according to Clean Energy Pipeline data.

A Clean Energy Pipeline survey of more than 200 senior executives active in the German renewable sector concluded that operational onshore wind farms are currently being sold at between Eur1.5 million and Eur2.2 million per megawatt, depending on the characteristics of the location.

One of the main sources of demand that is driving up prices for clean energy projects, most notably onshore wind and solar farms, is the need for municipal utilities to acquire new generation assets to replace the coal and nuclear plants that are coming offline in Germany over the next two decades.

Baden-Wuerttemberg-based utility EnBW said in 2011 that it would invest Eur8 billion in clean power through to 2020 and closed a Eur822 million capital increase in June 2012 to achieve this goal.

Mannheim-based MVV Energie has committed to invest Eur3 billion by 2020 in renewable energy, efficient cogeneration of power and heat, and the maintenance and modernisation of existing power plants and grid infrastructure.

Bavarian utility Stadtwerke Muenchen aims to power the entire city of Munich

from renewable sources by 2025 and has earmarked a budget of Eur9 billion to do so.

The appetite for renewables among municipal utilities is more urgent than their large national counterparts such as RWE and E.ON, due in part to the fact that the major players are more advanced in building out their own renewable capacity.

Another major factor is that national players are not under as much pressure to meet political clean energy targets as utilities that are owned by federal states. EnBW, for example, is 46.55% indirectly owned by the federal state of Baden-Wuerttemberg, which is currently governed by a coalition between the Green Party and the Social Democrats.

“Utilities are one of the major acquirers of renewable energy assets,” said Ebner. “It’s not the big four German utilities such as E.ON and RWE, but the smaller municipality-owned utilities. They are very keen right now to acquire onshore wind and solar photovoltaic (PV) assets in Germany and even abroad. Their appetite has definitely increased in the past two years. There are political reasons for this as their owners want them to offer renewable energy to clients. The Munich utility for example has set a goal that 100% of its electricity will be produced by renewable sources by 2025. So they have to acquire.”

The municipal utilities face an array of other new entrants seeking to acquire German onshore wind farms. Due to a strong economy, stable feed-in tariff and steady financial support from state bank KfW, Germany remains a safe haven for investors fleeing from other European markets, which are enduring economic and regulatory pressures.

For long-term, low-risk institutional investors in particular, onshore wind assets are preferred ahead of every other renewable energy asset – 78% of respondents in a Clean Energy Pipeline survey of more than 200 industry executives said they believe that operational German onshore wind projects are attractive to long-term, low-risk institutional investors rather than operational solar PV (70%) and offshore wind projects (61%).

David Jones, Head of Renewables at Allianz Capital Partners, an investment unit of insurance giant Allianz, told Clean Energy Pipeline: “There is a lot of competition in German onshore wind M&A as new entrants have come to the market that were not there a few years ago. This includes municipal utilities, Swiss utilities, retail funds and also a lot of international investors such as ourselves.

“Appetite to acquire German onshore wind farms is currently very high. This is in part driven by a retreat to safety from the more peripheral countries in Europe. It is definitely a sellers’ market at moment. Prices are going up and returns are going down.”

The sheer demand for German onshore wind farms means that traditional developers are dominating the sellers’ market, with most utilities and investors disinclined to sell stable, long-term revenue-generating assets, according to Jones.

“There are some secondary sales by utilities and funds that are looking for liquidity, but the main sellers of onshore wind farms in Germany are still the developers,” he said. ■

interviews & Analysis

m&A to what extent do you agree that the following german assets are attractive to long term low risk investors?

Operating offshore wind projects

Operating utility-scale solar PV projects

Portfolios of operating small scale solar PV projects

Operating onshore wind projects

22%

15%

19%

13% 49% 30% 9%

51% 23% 8%

57%

56% 24% 6%

19% 3%

Strongly agree Agree Disagree Strongly disagree

Source: Clean Energy Pipeline / VB/Research Ltd.

9

ventUre CAPitAl

CleAnteCh vC inveStOr eleCtrAnOvA SeekS ADDitiOnAl COrPOrAte PArtnerS

Rob Lavine

Cleantech venture capital (VC) fund Electranova Capital is seeking additional corporate investors to enhance its strategic focus, Partner Nicolas Chaudron told Clean Energy Pipeline.

The France-based fund was launched in May last year with contributions of Eur30 million from French utility EDF and Eur10 million from German insurance giant Allianz. It aims to invest in new energy and environmental technologies and is managed by IdInvest Partners, a French private equity firm with more than Eur3 billion under management, for which Chaudron has overseen cleantech investments since 2006.

Chaudron said Electranova is seeking additional investors, and is currently in talks with “a couple” of prospective partners. It is focusing on corporates from different parts of the cleantech sector, and the economic barrier to entry is relatively low.

“For financial investors, it starts at Eur2 million,” he said. “But for corporate investors, since we are looking at one or two additional players, the number of spots is limited but the size is higher; it starts at Eur10 million.”

Electranova is particularly looking for investors able to bring a strategic element along with their financial contribution. Allianz’s investment forms part of its greater asset management activities but for EDF, the financial value of the venture is outweighed by the strategic aspect of being able to gain access to current cleantech innovation, and to source better technologies for its own business units.

“Allianz are not [making] direct investments in venture capital so this is a kind of investment strategy that they cannot develop internally,” Chaudron said. “The conviction of EDF is that they need to partner with a venture capital firm because they obviously have the industry knowledge, but they have less experience in dealing with investment cycles, particularly with start-ups.

“This is what they were seeking in IdInvest Partners. We have one of the best track records in venture capital in Europe in general and we have some experience in cleantech as well.”

IdInvest manages the investments of Electranova independently of its corporate partners, Chaudron said, but is open to feedback from EDF, and the two companies work closely on identifying new trends and prospective areas for growth within cleantech. Typically, EDF’s contributions to the fund generally come in three stages.

“The first one is that EDF brings us some additional deal flow, particularly outside of

Europe,” Chaudron explained. “They have people in the US and they have people in Asia. Number two: they bring industrial and technical expertise when we evaluate those investment opportunities. EDF has 2,000 R&D people, which means that there is almost always an expert within EDF about [each] specific technology and we get unlimited access to those resources.

“Point three [is], after we invest in a company we can open doors for it within EDF. Obviously there is no obligation for an EDF business unit to become a customer of a portfolio company if it doesn’t make sense for the business unit but when it makes sense we have the ability to accelerate the business relationship.”

Electranova aims to make four or five new investments each year. Typically, it will invest Eur2-5 million in the first round in which it participates, and then double that amount over the lifetime of each portfolio company. It is stage-agnostic, and has so far backed France-based smart grid technology provider Actility and Seatower, a Norwegian designer of foundations for offshore wind installations.

Chaudron said that the European cleantech VC sector differs from its American counterpart in the sense that, despite there being a sense of disillusionment hanging around cleantech investment in both regions, Europe is ►

interviews & Analysis

Obviously we were affected by the solar crisis and we lost money there but at the same time, in those days we were working on some exits in renewable energy companies as well, and with the kind of returns you expect from venture capital.

“

”

10

probably in less of a downturn right now because the hype around cleantech was less pronounced in the boom years, due to the European VC sector being less prone to hype cycles in general.

The decline of the European solar equipment industry over the last 18 months has impacted IdInvest, causing Odersun, one of its portfolio companies, to go bankrupt. Despite this, the wide range of industries covered by cleantech means that a firm with a diversified portfolio like IdInvest is unlikely to be hit too deeply by a failure in any single sector.

“So far this is actually the only bankruptcy in one of our cleantech portfolio companies,” said Chaudron. “Obviously we were affected by the solar crisis and we lost money there but at the same time, in those days we were working on some exits in renewable energy companies as well, and with the kind of returns you expect from venture capital.

“We build a portfolio [and] there are going to be winners and there are going to be some losers as well,” he added. “One of

interviews & Analysis

global venture Capital and Private equity investment - 1Q09 to 1Q13

Source: Clean Energy Pipeline / VB/Research Ltd.

100

50

0

150

200

250

300

0

1

2

3

4

5

6

PE - DevelopmentCapital

VC - Late Stage(Series D+)

VC - Early Growth(Series A to C)

1Q13

4Q12

3Q12

2Q12

1Q12

4Q11

3Q11

2Q11

1Q11

4Q10

3Q10

2Q10

1Q10

4Q09

3Q09

2Q09

1Q09

Number ofdeals

Dea

l val

ue ($

bill

ion) N

umb

er of d

ealsTBLI CONFERENCE™ USA 2013

“Rethink the past and move on”

In existence for over 15 years, TBLI CONFERENCE consists of two annual conferences. These two-day events are the prime annual global networking and learning event on Environmental, Social and Governance (ESG) and Impact Investing.

WHAT TO EXPECTMeet 350+ finance professionals on ESG and Impact Investing. Learn about recent developments in 16 Workshops and 2 Round tables. Find new business partners, Free mobile app networking platform.

Register Now: bit.ly/tbliconferenceusa2013

PROGRAM FEATURESOpening Keynote Speaker: Paul Rose - Vice President of the Royal Geographical Society, Explorer and Broadcaster.

Roundtable 1 - "Sandy, Climate Change and Impact Investing"Roundtable 2 - "Measurement of ESG and Impact Investing"

16 Workshops on Integrating ESG in Portfolios, Sustainable Forestry, Wealth Management, Microfinance, Green Building, Intergrated Reporting, and more...

Grand Dinner with two high-level keynote speakers, maximum 200 guests.

BECOME A SPONSORAre you interested in promoting your organization at TBLI CONFERENCE? Sponsor levelsstart at $ 5,000 and offer free passes, Grand Dinner invitations and exposure of your organization. For more information contact Frank Stevens at [email protected].

BECOME A SPEAKERThe provisional program is now online. Are you interested in speaking in one of the workshops? More information at www.tbliconference.com.

FIND OUT MORE ABOUT TBLISee who sponsored or visit www.tbliconference.com for the program. Also visitwww.tbligroup.com and learn more about other services of TBLI.

www.tbliconference.com

“The World will benefit when economy supports well-being”

the advantages, and one of the challenges of cleantech, is that cleantech is not an industry, it’s more a theme that [has] different versions in each of the industries you play.

“So you can get cleantech in the energy industry, in the building industry, in the transportation industry, and we [see] opportunities in each of those sectors today.” ■

11

TBLI CONFERENCE™ USA 2013

“Rethink the past and move on”

In existence for over 15 years, TBLI CONFERENCE consists of two annual conferences. These two-day events are the prime annual global networking and learning event on Environmental, Social and Governance (ESG) and Impact Investing.

WHAT TO EXPECTMeet 350+ finance professionals on ESG and Impact Investing. Learn about recent developments in 16 Workshops and 2 Round tables. Find new business partners, Free mobile app networking platform.

Register Now: bit.ly/tbliconferenceusa2013

PROGRAM FEATURESOpening Keynote Speaker: Paul Rose - Vice President of the Royal Geographical Society, Explorer and Broadcaster.

Roundtable 1 - "Sandy, Climate Change and Impact Investing"Roundtable 2 - "Measurement of ESG and Impact Investing"

16 Workshops on Integrating ESG in Portfolios, Sustainable Forestry, Wealth Management, Microfinance, Green Building, Intergrated Reporting, and more...

Grand Dinner with two high-level keynote speakers, maximum 200 guests.

BECOME A SPONSORAre you interested in promoting your organization at TBLI CONFERENCE? Sponsor levelsstart at $ 5,000 and offer free passes, Grand Dinner invitations and exposure of your organization. For more information contact Frank Stevens at [email protected].

BECOME A SPEAKERThe provisional program is now online. Are you interested in speaking in one of the workshops? More information at www.tbliconference.com.

FIND OUT MORE ABOUT TBLISee who sponsored or visit www.tbliconference.com for the program. Also visitwww.tbligroup.com and learn more about other services of TBLI.

www.tbliconference.com

“The World will benefit when economy supports well-being”

12

APex winD energy AimS tO ADD ASSet mAnAgement tO DevelOPment ACtivitieS

Rob Lavine

Virginia-based wind energy developer Apex Wind Energy plans to add asset management to its range of services, President and Chief Operating Officer Mark Goodwin told Clean Energy Pipeline.

Founded in 2009, Apex Wind acquires projects in the early stages of development before bringing them through construction and selling them on to operators. Typical of this approach is the 300 MW Canadian Hills project, which Apex completed in January having negotiated its sale eight months earlier to Atlantic Power Corporation, which provided $310 million in construction financing.

“It is relatively common for a developer such as ourselves to structure a deal, as we did with Canadian Hills, where we would sell a project either before or at close of construction finance,” Goodwin said. “In some cases we would continue to be the construction manager and finish development on a development services agreement through COD [commercial operation date].

“We’re thinking, long term, that Apex would evolve into a company that perhaps takes larger minority stakes in our projects and not only manages construction but also does asset management of a project on behalf of more financial-type investors. That may be possible in the short term, but I think a majority of the projects we’re working on right now have a structure similar to [Canadian Hills].”

Apex’s model has generally relied on it purchasing batches of development projects, such as the 500 MW of potential capacity acquired from IPA Wind Development last year. However, Goodwin confirmed that the developer is considering boosting its asset management portfolio through the acquisition of operational projects, and is assessing how the cash generation component of operational wind farms would fit into its business model.

“We would contemplate that [but] we would probably need an investor or a partner,” he said. “If we evolved down that

path we would have to keep in mind the financing structures and policies that are in place, including the PTC (Production Tax Credit) component.”

Apex has several wind projects ready to enter construction in the next year, Goodwin said, though some, particularly in Texas, still need to secure power purchase agreements (PPAs) through requests for proposals (RFPs). The developer is currently in bilateral talks concerning PPAs for other parts of its portfolio, and aims to scale up activity to three large-scale projects each year.

“Right now I think we’re carrying a pipeline of 5-6 GW and I would be optimistic that we’ll be successful in one, two, possibly three large projects a year pending policy,” Goodwin stated. “With consistent policy, maybe there’s not a skipped year – 2013 is probably a skipped year because the [PTC] extension came so late – so I would be very happy with 200-600 MW in a given year.”

The one-year extension of the PTC, seen as instrumental in the growth of wind energy installations in the US, came late but its renewal at the end of 2012 is still seen as a positive. Goodwin said that, despite inefficiencies and problems with the PTC, Apex still views it as a largely successful instrument.

“We have a number of projects that do very well with the way the PTC works - high-capacity-factor projects that bring a lot of PTCs to them,” Goodwin said, adding that Apex hopes for the introduction of additional financial structures for wind development, particularly Master Limited Partnerships (MLPs), which are already available to fossil fuel projects. A bill to make MLPs accessible to renewable developers was introduced in 2012 but is yet to become law.

“It’s a retail capital raising structure that would come in at project level and allow a company like Apex to raise equity for a specific project at a very competitive cost of capital,” said Goodwin. “It would also be helpful to the model where Apex is managing projects on behalf of those MLPs.”

In addition to targeting PPAs for its development portfolio, Apex is also seeking capital, Goodwin stated.

“In the immediate side of things, we have a very strong portfolio of late-stage projects and so the type of capital we’re looking for is for filling in the capital requirements of a late-stage project,” he said. “So the type and size of capital are along the lines that we would use at a project level for PPA security, interconnects, turbine deposits,” he added. “It’s in line with finding the right sponsors for these late-stage projects.”

Apex is also one of the few US-based developers actively exploring offshore wind, which Goodwin said it views as part of a long-term vision, but is concentrating on onshore wind for the time being.

Offshore would fit in with a development strategy that has seen Apex concentrate on large-scale projects, a preference that Goodwin said was partly driven by a focus on high-voltage grid connections where there is good transmission capacity.

“We also like the economies of scale in a larger project size,” he explained. “For a development company it’s almost as hard in some cases to develop a project that is 50 MW as it is to develop one that is 300 MW, so there’s obviously more bang for your buck to do a larger project.

“We started Apex in 2009 and we have been rolling up early and mid-stage development assets during that time and continue to do that, so we haven’t excluded certain regions where the project sizes are smaller, such as the mid-Atlantic or New England.

“We know we can’t do as big a project [in those markets] but we think of them as potentially a stronger power marketing environment where we can build successful projects as well,” he added. “It’s a balance but I think it’s correct to suggest that we lean toward larger projects.” ■

interviews & Analysis

T O R O N T O 20 3

COME AND NETWORK AT CANADA’S LARGEST

WIND ENERGY CONFERENCE

www.canwea2013.ca

CANADIAN WIND ENERGY ASSOCIATIONANNUAL CONFERENCE & EXHIBITIONTORONTO, ONTARIO | OCTOBER 7–10, 2013

This premier event will bring together over 2,500 experts from around the world to discuss opportunities in Canada’s growing wind energy industry. It will provide an exclusive opportunity to network and generate new business leads.

canwea-conf13-ad-CEP-1pg-print-v1.pdf 1 13-04-29 3:27 PM

winD

For a development company it’s almost as hard in some cases to develop a project that is 50 MW as it is to develop one that is 300 MW.

“”

13

T O R O N T O 20 3

COME AND NETWORK AT CANADA’S LARGEST

WIND ENERGY CONFERENCE

www.canwea2013.ca

CANADIAN WIND ENERGY ASSOCIATIONANNUAL CONFERENCE & EXHIBITIONTORONTO, ONTARIO | OCTOBER 7–10, 2013

This premier event will bring together over 2,500 experts from around the world to discuss opportunities in Canada’s growing wind energy industry. It will provide an exclusive opportunity to network and generate new business leads.

canwea-conf13-ad-CEP-1pg-print-v1.pdf 1 13-04-29 3:27 PM

14

BAlAnCe Sheet inveStOrS DOminAte AlBertA winD energy FinAnCing

Ronan Murphy

Power companies that finance projects from their balance sheets are the primary source of investment for wind farms in Alberta, according to Dan Balaban, Chief Executive Officer of developer Greengate Power.

Greengate announced in April that it sold the 300 MW Blackspring Ridge wind farm in Vulcan County, Alberta, to EDF EN Canada Inc. and Enbridge Inc., both of which will own 50% stakes in the project.

Balaban told Clean Energy Pipeline that Blackspring Ridge, which is expected to cost about C$600 million ($593.37 million), will now be financed from the buyers’ balance sheets.

“We worked hard on financing the project but ultimately the sale made more economic sense,” he said. “The execution complexity was far lower than putting the financing together.”

Blackspring Ridge will be Alberta’s largest wind farm once it is operational. Greengate also developed the biggest existing wind farm in the province, the 150 MW Halkirk Wind project, which was sold to energy group Capital Power in June 2011. Capital Power subsequently financed the Halkirk Wind Project from its balance sheet.

Alberta is the only deregulated energy market in Canada, which means power producers cannot sign conventional power purchase agreement (PPA) contracts with utilities. Instead, all energy is sold on the merchant market, which would traditionally

put wind at a cost disadvantage compared to fossil fuels.

For Blackspring Ridge, Greengate negated that merchant risk by signing a separate 20-year PPA for the sale of renewable energy credits generated by the project to Californian utility Pacific Gas & Electric (PGE). The additional revenue provided by the renewable energy credit sales makes the project more economically viable.

“We mitigated the merchant power aspect through the renewable energy credit PPA with PG&E, but there is still a merchant element and that is where a balance sheet player is handy, because financing for a merchant project is very complicated,” said Balaban, who emphasised that despite the complexity, it is still possible to secure project debt financing from a mixture of Canadian, US and European banks.

Balaban explained that the prevalence of balance sheet financiers for wind farms in Alberta is a consequence of the province’s vast oil and gas reserves, which mean it is home to energy groups with significant capital resources and an urgent demand for power to support their extraction activities.

“Alberta is the energy centre of Canada,” he said. “It is home to a lot of large energy companies and the power sector tends to be dominated by strategics like Enbridge and Capital Power. They are already familiar with the Alberta energy market and have home-field advantage.

“The other thing is that these wind farms are very large projects. Balance sheet players tend to have the capacity to do them.”

Power demand is growing by more than 3% per year in Alberta and is forecast to

continue doing so for the next 20 years. The province is heavily reliant on an ageing fleet of coal power stations that are scheduled to be retired on a mass scale over the next several years, which will create a gap that needs to be filled by multiple forms of energy generation.

Balaban is hopeful that Alberta could introduce new legislation to encourage energy groups to invest in renewable energy to offset the environmental cost of their fossil fuel activities. Extraction of oil from Alberta’s tar sands is a vital pillar of the province’s economic ambitions going forward but has been heavily criticised by environmental groups for its impact on global greenhouse gas emissions and the local landscape.

The impact of tar sands oil extraction could be offset to a certain extent if more renewable power was introduced into the mix that serves these energy-intensive operations.

“Every barrel of oil we produce requires additional power to be brought online,” said Balaban. “Right now that is mostly served by dirty coal facilities, so we have a dual problem of emissions from the oil sands and emissions from the power required to support production of oil.

“I have been advocating for Alberta to implement a clean electricity standard that would require a power product to be of a certain emissions intensity. That would allow PPAs to be issued that would encourage additional wind development based on provincial policy rather than outside jurisdiction.”

Greengate still has six projects totalling 850 MW under development in Alberta. Three are in the advanced stages and are now the company’s main priority: The 150 MW Paintearth project, the 150 MW Sterling Wind project and the 150 MW Wheatland Wind project.

All three of these wind farms are either adjacent or close to existing wind farms, which means the cost of grid connections is lower and the sites have proven to be viable in terms of wind generation and construction viability.

Balaban said the earliest any of the three wind farms will start construction is 2014. As with its previous projects, the company will pursue project financing but is also prepared to sell before construction begins. ■

interviews & Analysis

15

germAn OFFShOre winD mArket OPenS UP FOr Uk CABle PrOviDer JDr

Ronan Murphy

Germany’s offshore wind sector has emerged as a viable market for UK-based subsea transmission cable supplier JDR, the company’s Chief Executive Officer Andrew Norman told Clean Energy Pipeline.

JDR, which was the cable supplier for a series of major UK offshore wind farms such as London Array and Greater Gabbard, won its first German offshore wind contract in September 2012, when WindMW GmBH agreed to buy cables from the company for the 288 MW Meerwind project in the German North Sea.

German offshore wind, which JDR had previously considered to be not a viable market due to the dominance of German supply chain companies, is now an integral part of the company’s strategy, Norman said. This is due to a lull in UK development between the end of the Crown Estate’s Round 2 build-out and the anticipated start of Round 3 in 2014/15.

“We are actively pursuing German projects between Round 2 and 3,” Norman said. “It is a slightly different market in terms of the contractual norms, which are very stringent. They are very rigorous in terms of their supplier selection.

“They are more comfortable with German suppliers working around them, so we were very pleased to have broken into that market and I think we did that because we have the track record, we’ve got the technology and we’ve got the experience.”

JDR was brought into the Meerwind project relatively late in development. Cable suppliers are usually involved in a project right from the beginning, but JDR was contracted to supply Meerwind one year after the wind farm reached financial close in April 2011.

“We were brought in fairly late in that contract process but were able to ramp up and respond very quickly, from an engineering, contract negotiation and capacity point of view,” said Norman.

“The project was very much financially driven. There was a set of investors that

knew what they wanted to do. They knew what they wanted it to cost and they knew the window they needed to get it done to make a return. I think what they figured out was that the suppliers they had originally spoken to could not get them there. The driver for bringing us in was the commercial success of the project.”

JDR has a letter of intent in place for a second German offshore wind project and hopes to finalise the agreement imminently.

While Germany presents a valuable opportunity for JDR, Norman stressed that the company is well advanced in its preparation for UK Round 3, which represents the potential development of 25 GW of offshore wind capacity. JDR is confident that Round 3 projects are on course to come online from 2016/17 onwards, which would mean supply chain orders could start to be made from 2014 onwards.

“We are actively qualifying and developing the products for Round 3 in cooperation with the operators and engineering companies that will develop it,” Norman said. “I think those orders will start being placed next year, with production to begin sometime after that.”

The UK Department of Energy and Climate Change awarded JDR a grant of up to £1 million in March 2013 to invest in

the research and development of high-voltage array cabling that could lower the cost of offshore wind power.

Expansion into the offshore wind sector helped drive JDR to record revenues of £129.9 million in 2012, an increase of 56% compared to £83.2 million in 2011. It also announced record earnings before interest, tax, depreciation and amortisation (EBITDA) of £25.8 million in 2012, compared to a loss of £4.1 million the previous year.

The company is benefitting from the £35 million investment it made in its plant in Hartlepool, northern England, which last year completed an extensive upgrade that has granted JDR the extra manufacturing capacity needed to address growing demand in the offshore wind and oil and gas markets.

JDR already has international offshore oil and gas operations in Thailand and Houston, Texas, but the Hartlepool plant investment means it is capable of expanding further into nascent offshore wind markets in other geographies.

“Our strategic plan is to double the size of our business in the next four years,” said Norman. “What we are thinking about now is where do we go next? We have already had conversations in the US, where we’ve been talking actively about real projects, and there will be opportunities in Asia and China.

“What the UK can bring is the technology lead. Even though from a purely manufacturing view it is going to be highly competitive, can we create a technology advantage that can outweigh the benefits of low-cost local manufacturing? It’s a great opportunity in the UK.” ■

interviews & Analysis

Our strategic plan is to double the size of our business in the next four years.“”

16

OnerOOF energy Set tO ClOSe new eQUity rOUnD AnD SOlAr leASing FUnD within 90 DAyS

Rob Lavine

OneRoof Energy is set to expand its solar rooftop installation business into at least four new states over the next four months, in which time it will close another equity round and leasing fund, the company’s President and Chief Executive Officer David Field told Clean Energy Pipeline.

Headquartered in California, OneRoof installs solar systems on residential rooftops and offers leasing options through its SolarSelect financing programme. SolarSelect attracted $100 million in investment from Morgan Stanley and Main Street Power Company in March, and OneRoof is currently in the process of raising both additional lease financing and another equity round.

“Within the next 90 days we’ll be closing another round of equity and, net, it’ll probably be in the $20-30 million [range],” said Field. “We closed our most recent lease fund, with Morgan Stanley…recently [and] we’re continuing to talk to other parties to add to that.”

That additional capital will be used to drive geographic growth. OneRoof aims to expand from the three states in which it currently operates - Hawaii, California and Arizona – into Colorado, Connecticut, New York and New Jersey by late summer, though its future growth is likely to be limited to states that have hospitable regulatory conditions for solar installations.

“I think that on average there are eight to 12 states in the US that work well for residential solar,” Field said. “The top five states probably do about 80% of the business, so it’s the type of situation where as long as you’re focused on the top half, you’ve probably covered most of the available marketplace.

“That said, we’re starting to see opportunities in many other states because as the cost of solar comes down and you can achieve grid parity in non-traditional solar markets, it opens up new geographic markets.

“In some states like California you no longer need any subsidies because the price of electricity is at a level where solar is really competing on a grid parity basis…[but in] certain other states, if the utility rates are lower, you do need to have some kind of local incentive in order to drive solar adoption.”

OneRoof generally relies on one or two large partners to help it reach new areas but it also aims to leverage as many local installation partners as possible as it expands. Like its competitors, it sells its installations through local dealers, but it intends to increase the range of third party intermediaries through which it can operate in order to boost business.

“The whole idea on our side was how do you expand the pool, how do you expand the opportunity for solar in key markets,” Field explained. “The challenge was selling direct to the homeowner. We have found that unless you have a large presence it’s very hard to go direct to the consumer. Of the two companies that sell direct to homeowners, one is SolarCity, which does a very good job of it because they’ve got a large presence; the other is Sungevity, which sells via the internet.

“We’ll go to market with roofing contractors in some areas, and we’ve built our platform in order to enable a roofing contractor to sell and install solar. We’ll also go to market in some areas with an array of mortgage brokers or financial advisors that will actually be selling OneRoof leases, and again, we adapted our platform in order to facilitate a third party that really is not expert in solar to be able to sell solar on our behalf, and then we will actually do

the installations and manage the customer relationships.”

OneRoof’s most significant strategic partner is Hanwha, the Korean conglomerate that is also the parent company of China-based solar panel maker Hanwha SolarOne. Hanwha provided $30 million of development financing to OneRoof in January this year after contributing to the installer’s initial $50 million fund in 2011.

Field called the partnership “a very important relationship for us”, and revealed that Hanwha supplied 60% of the panels used in OneRoof’s installations last year. Although the US government imposed import tariffs on Chinese-made panels last year, the CEO dismissed the idea that the move would have much of an impact on panel prices in the US, simply because developers and installers can source cheap equipment made in alternative markets such as Taiwan.

“It’s unfortunate but to be quite frank, I don’t think it made any difference in the marketplace whatsoever,” he stated. “It may have made a couple of cents difference because it costs a couple or a few cents more to process Taiwanese cells, as an example, but I think at the end of the day it had little to no effect.”

Aside from geographic expansion into new states, OneRoof’s is also set to start meeting demand from commercial and industrial customers, markets Field said the company would probably target in the next year.

The CEO added that OneRoof was unlikely to be affected by recent difficulties in the solar sector since investors view his company as a financial services business as opposed to an upstream solar operator. A more crucial outcome from the solar manufacturing crisis is likely to be the fall in the cost of installing and financing its systems.

“I would say, when I look at the industry in general, that we’ve all benefited from a reduction in solar panel prices, but the greater benefits come from lowering the cost of capital that is used to finance solar leases,” Field said. “We’re seeing more [and] greater reductions in that than in the reduction in solar panel prices, and so that’s where the big opportunity is.” ■

interviews & Analysis

www.greenpowerconferences.com+44 (0)20 7099 0600

Secure investors.Manage risk.Guarantee bankability.

Our senior speaker line-up includes:

� Benchmark yourself against theindustry leaders: Over 40 expertspeakers delivering up-to-the-minutemarket intelligence and insight

� Meet the decision-makers: 80%+ ofattendees in 2012 were at VP/directorlevel or above

� Make your projects bankable:Understand what attracts investors toprojects

Join us at THE premier annual windfinance gathering

4th annual

Global Wind Power Finance & Risk

Chris Hunt, Managing Director, Riverstone

Tom Murley, Head of Renewable Energy, HgCapital

Keiji Okagaki,Vice President,Marubeni Europower

Magnus Goodlad, Head of Renewables, Hermes GPE

Rui Teixeira,Chief Financial Officer,EDP Renewables

Dominik Thumfart, Managing Director, Infrastructure &Energy Finance, Deutsche Bank

Martin Neubert, Senior Director, Head of Partnerships, Wind Power, Dong Energy

Ian Berry, Fund Manager – Infrastructure andRenewable Energy, Aviva Investors

Tavraj Banga, Director, Terra Firma

Dima Rifai, Chief Executive Officer, Paradigm Change Capital

Organised by:Part of:Silver Sponsor:Gold Sponsor:

This conference, organised byGreen Power Conferences,

demonstrates that well organised, wellfocused events, and with the rightspeakers invited, is still the best way towin businesses and contact potentialclients and suppliersHead of Energy and Environmental Finance, KfW-IPEX Bank,Global Wind Power Finance & Investment Congress 2012

CONFERENCE AND EXHIBITION19-20 June 2013, London, UK

For more information or to register your place, visit www.greenpowerconferences.com/windfinancecall +44 (0)20 7099 0600Please quote VIP code CEP1

Silver Sponsor:

Gold Sponsor:

Dr Cord Landsmann, Chief Financial Officer, E.ON C&R

Robert Mansley,Managing Director,GIB

David Jones,Managing Director,Allianz CapitalPartners

Joseph Slamm, Partner, Hudson CEP

12311 Global Wind Finance A4 Advert updates_8838 Offshore Wind USA Brochure 07/05/2013 12:24 Page 1

SOlAr

In some states like California you no longer need any subsidies because the price of electricity is at a level where solar is really competing on a grid parity basis.

“”

17

www.greenpowerconferences.com+44 (0)20 7099 0600

Secure investors.Manage risk.Guarantee bankability.

Our senior speaker line-up includes:

� Benchmark yourself against theindustry leaders: Over 40 expertspeakers delivering up-to-the-minutemarket intelligence and insight

� Meet the decision-makers: 80%+ ofattendees in 2012 were at VP/directorlevel or above

� Make your projects bankable:Understand what attracts investors toprojects

Join us at THE premier annual windfinance gathering

4th annual

Global Wind Power Finance & Risk

Chris Hunt, Managing Director, Riverstone

Tom Murley, Head of Renewable Energy, HgCapital

Keiji Okagaki,Vice President,Marubeni Europower

Magnus Goodlad, Head of Renewables, Hermes GPE

Rui Teixeira,Chief Financial Officer,EDP Renewables

Dominik Thumfart, Managing Director, Infrastructure &Energy Finance, Deutsche Bank

Martin Neubert, Senior Director, Head of Partnerships, Wind Power, Dong Energy

Ian Berry, Fund Manager – Infrastructure andRenewable Energy, Aviva Investors

Tavraj Banga, Director, Terra Firma

Dima Rifai, Chief Executive Officer, Paradigm Change Capital

Organised by:Part of:Silver Sponsor:Gold Sponsor:

This conference, organised byGreen Power Conferences,

demonstrates that well organised, wellfocused events, and with the rightspeakers invited, is still the best way towin businesses and contact potentialclients and suppliersHead of Energy and Environmental Finance, KfW-IPEX Bank,Global Wind Power Finance & Investment Congress 2012

CONFERENCE AND EXHIBITION19-20 June 2013, London, UK

For more information or to register your place, visit www.greenpowerconferences.com/windfinancecall +44 (0)20 7099 0600Please quote VIP code CEP1

Silver Sponsor:

Gold Sponsor:

Dr Cord Landsmann, Chief Financial Officer, E.ON C&R

Robert Mansley,Managing Director,GIB

David Jones,Managing Director,Allianz CapitalPartners

Joseph Slamm, Partner, Hudson CEP

12311 Global Wind Finance A4 Advert updates_8838 Offshore Wind USA Brochure 07/05/2013 12:24 Page 1

18

interviews & Analysis

‘eBAy FOr SOlAr’ COmPAny OFFerS StreAmlineD APPrOACh tO PrOJeCt m&A

Ronan Murphy

German company Milk the Sun is pioneering a low-cost, streamlined online service for connecting sellers of solar photovoltaic (PV) projects with prospective buyers, Chief Executive Officer Felix Krause told Clean Energy Pipeline.

Launched in March 2012, Milk the Sun is a web-based platform on which owners of photovoltaic assets can essentially put them up for sale, in a manner broadly similar to online auction giant eBay. Milk the Sun vets information provided by the sellers, removing the layers of additional interlocutors typically required for a clean energy M&A deal.

Users of the platform are granted direct contact to the sellers along with immediate information collected by Milk the Sun on key project issues such as grid connection, feed-in tariff (FiT) access, performance data and lease details. Milk the Sun receives a small commission for every successful transaction.

Krause founded Milk the Sun following his own negative experiences with agent costs in the PV project development market.

“In 2009 I founded a company to develop solar projects in Germany and England,” he said. “We realised that the market is totally inefficient. We had an interesting project of 4 MW that failed because of a chain of agents, which cost the company a lot of money. For future projects, we were looking for an eBay-like service to promote them, but there wasn’t any such thing, so we decided in mid-2011 to do it ourselves.”