Montgomery County Medical Society Playbook for Surviving as an Independent Physician in Maryland October 25, 2012

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Montgomery County Medical Society

Playbook for Surviving as an Independent Physician in

MarylandOctober 25, 2012

Agenda

• National and Local Challenges for Independent Physicians

• Physician Responses

• Options Assessments

2

Health Care: The Economic Engine

GDP 2010 (USD)1. United States $15.04 T2. China $ 11.3 T3. Japan $ 4.46 T4. Germany $ 3.3 T5. US health economy $2.7 T*

6. France $ 2.6 T7. UK $ 2.2 T8. Brazil $ 2.1 T

Sources: World Development Indicators database, World Bank, 1 July 2011

* 2011 stat CMS

3

Health Care Spending Sources

4

Health Care Spending Uses

5

Poor Public Payers

6

Source: Avalere Health analysis of American Hospital Association Annual Survey data, 2010, for community hospitals.

(1) Includes Medicaid Disproportionate Share payments.

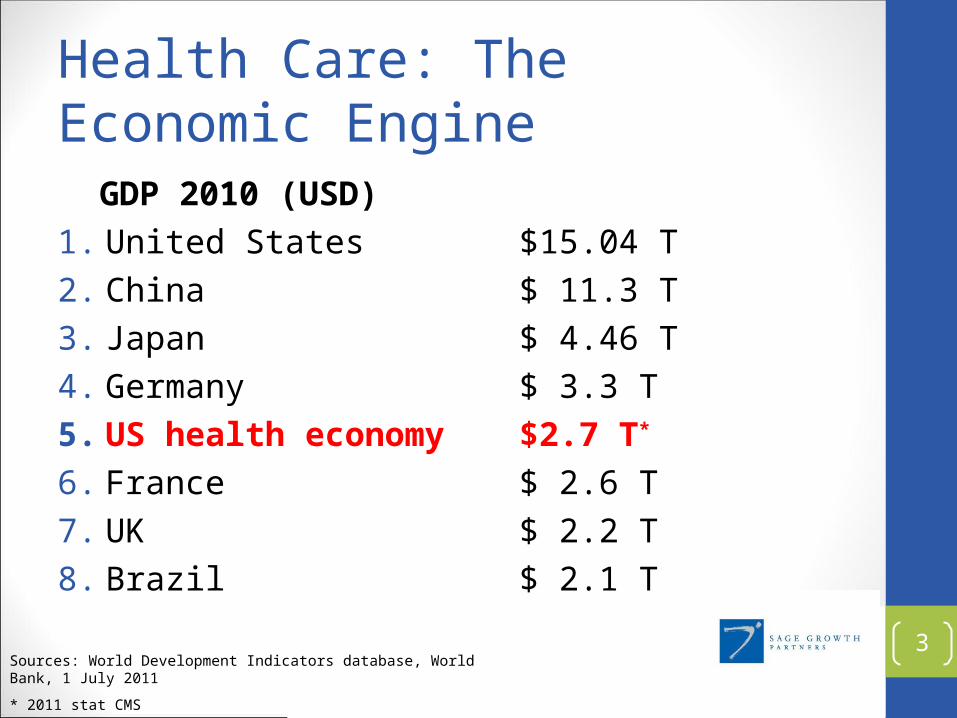

Medicaid Enrollment (millions) andExpenditure Projections (billions)

Source: American Action Forum. Sustainability of Medicaid: Action Steps for Governors to Achieve Meaningful Reform. Adapted from Office of the Actuary, “2010 Actuarial Report on the Financial Outlook for Medicaid,” Centers for Medicare and Medicaid Services, December 21, 2010

7

The Demographic Tsunami

• One-quarter of all Medicare recipients• Have 5 or more chronic conditions• See 13 physicians per year• 50 prescriptions per year

• Over 13,000 different drugs being sold in the U.S. in 2007• 16x what was available 50 years ago

• Over 900,000 physicians in the U.S. • 75% are in practices of less than 8 physicians

• Hard to support a “system” of care 8

Arrested Development– Consumer Sovereignty

Notes: Personal health care expenditures are spending for health care services, excluding administration and net cost of insurance, public health activity, research, and structures and equipment. Out-of-pocket health insurance premiums paid by individuals are not included in Consumer Out-of-Pocket; they are counted as part of Private Health Insurance. Medicaid spending for the State Children's Health Insurance Program (which began in 1998) is included in Other Government Programs, not in Medicaid.

Source: Kaiser Family Foundation calculations using NHE data from Centers for Medicare and Medicaid Services, Office of the Actuary, National Health Statistics Group, at http://www.cms.hhs.gov/NationalHealthExpendData/ (see Historical; National Health Expenditures by type of service and source of funds, CY 1960-2009; file nhe2009.zip).

2009Public 47.4% Private

52.6%

1999Public 42.6% Private

57.4%

$1.1 Trillion $2.1 Trillion

9

Cost Challenges for Maryland Physicians• Salaries

• Taxes

• Retail Space

10

Maryland Salaries vs. Regional and National

RN

291111

LPN

292061

Medical Assistant

319092

Receptionist

434171

Medical Records & HIT

292071

National $33.23 $20.21 $14.51 $12.85 $17.27

Maryland $36.29 $24.14 $15.61 $13.49 $19.54

Delaware $34.64 $22.78 $14.38 $11.79 $16.95

Virginia $31.59 $18.88 $14.63 $12.94 $17.09

Pennsylvania $32.28 $20.63 $14.45 $12.75 $16.44

11Source: Bureau of Labor Statistics, 2011.

Tax Impact

State Overall RankCorporate Tax

RankIndividual Income

Tax Rank

Delaware 14 50 29

Virginia 27 6 38

Maryland 41 15 45

Pennsylvania 19 46 12

12

Source: 2013 State Business Tax Climate Index, Tax Foundation

Location, Location, Location

Class A and Class B physician space is approximately 15%-25% greater than bordering

states such as Virginia, Delaware, and Pennsylvania.

13

PHYSICIAN RESPONSES14

Visits to physicians who were part of a group practice with 6–10 physicians increased 46%

Visits to physicians who were solo practitioners decreased 21%

1997-2007

15

Safety in Numbers

Independent Physicians and Hospital Systems

• 65% of established physicians were placed in hospital-owned practices

• 49% of physicians hired out of residency or fellowship were placed within hospital-owned practices

All information based on 2009 MGMA survey.16

Physician Hospital Integration

• Hospitals need physicians to lower cost and control spending• Fee-for-service being squeezed• ACOs

• Physicians want financial security• Higher overhead costs• Shrinking Medicare reimbursement rates

Physician Interest in Hospital Alignment

17

Why Physician Hospital Alignment?• MGMA Connexion article “United we stand: Power shifts marginalize

physician practices – unless we act and integrate” by By Joel Sauer, CEO, Heart Center Medical Group, Fort Wayne, Ind.

18

Time to Dance?

•Washington Adventist Hospital•Shady Grove Adventist Hospital•Shady Grove Adventist Emergency Center at Germantown

•Holy Cross Hospital

• Suburban Hospital Healthcare System

• Montgomery Medical Center

19

Press Release Quotes“Johns Hopkins Medicine expanding D.C. footprint. Baltimore health giant to open clinics, add doctors in Northwest.”--Washington Business Journal, June 8, 2012

“Holy Cross Hospital maintains a range of relationships with many affiliated physicians…and has started construction on Holy Cross Germantown Hospital, which will be the first new hospital in Montgomery County in 35 years”--Holy Cross Hospital Website, September 25, 2012

20

“Adventist strikes deal with D.C. doctors’ group.” --Washington Business Journal, Nov. 29, 2011

INDEPENDENCE: OPTIONS ASSESSMENT 21

Understand Health Reform

• Expanded enrollment in Medicaid and commercial insurance

• New state exchange coming online 1/1/14

• New insurers entering the market

• “Back to the future” payment models • Percentage of premium• Risk-bearing contracts• Bundled payments• Global budgeting schemes

22

Baseline Internal Capabilities

• Staff

• Location

• Patient population and “stickiness with consumer”

• Financial position and opportunities for operating improvement

• What is your “special sauce”?

23

Know Your Business, Market, and Competition• Specialty and level of compensation

• Understand projections of service demand over 5-10 years

• Inventory hospitals and health systems and project what consolidation might look like in 5-15 years

• Inventory of physician entities• Large medical groups, IPAs, PHOs

• Inventory of health plans

24

Business Model Options

• IPA• Mergers

• Merger of two physicians in same specialty• Merger of physicians to create complete spectrum of services• Merger of several physicians in a small market

• Micropractice• Concierge

• Physician(s) go concierge• Physician(s) work with MDVIP or MD Squared to take them

concierge• Active Practice Management—ride out until retirement

25

Face Facts but Remain Hopeful

• Explore employment options

• Explore options to join or start group

• If specialty physician – can you join a PC practice or PC dominated multi-specialty group?

• Pursue discussions with all payers and contracting entities

26

Related Documents