Money-Maker or World Saviour? – Compromising Logics to Manage Sustainability in Banking Master’s Thesis 30 credits Department of Business Studies Uppsala University Spring Semester of 2019 Date of Submission: 2019-05-29 Annelie André Molly Larson Supervisor: Jaan Grünberg

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Money-Maker or World Saviour? – Compromising Logics to Manage Sustainability in Banking

Master’s Thesis 30 credits Department of Business Studies Uppsala University Spring Semester of 2019

Date of Submission: 2019-05-29

Annelie André Molly Larson Supervisor: Jaan Grünberg

Acknowledgements First and foremost, we would like to thank Nordea and all the respondents for taking the time

to participate in our study. Your contribution is truly appreciated and your insights made it

possible to fulfill the purpose of this thesis. We would also like to thank our seminar group for

giving us constructive feedback throughout the process. Your comments and suggestions have

certainly helped us along the way. Last but not least, we would like to thank our supervisor Jaan

Grünberg for challenging and supporting us during this journey. Your precious help has

contributed with valuable guidance and improved our thesis greatly. For those who will be

reading this thesis, we hope that you will find the thesis and the topic as intriguing as we do.

Uppsala 29th of May 2019

______________________ ______________________

Annelie André Molly Larson

Abstract With the increasing demands of engaging in sustainability, the financial industry’s dominating

market logic is currently being challenged. Banks are therefore experiencing demands to

manage and legitimize sustainability, identified as containing both a market- and social logic,

into a profit driven context. The aim of this study was thus to explore, at a micro level, how

multiple logics of sustainability can be managed and legitimized in an organization where the

dominant logic is being challenged. This was done by conducting a case study where the

primary data was collected through semi-structured interviews with employees from Group

Sustainable Finance (GSF) who are responsible for driving the sustainability agenda at Nordea.

The results demonstrate that sustainability has been managed through a compromising strategy

where elements of both the market- and social logic has been altered to appropriately suit the

context characterized by profit maximization. During the process, an interesting finding

evolved concerning how the micro perspective exposed the existence of conflicts within a single

logic, defined as intra-logic conflicts. The results also contributed to identify stakeholder

triggers as well as how normative-, instrumental-, and value rhetorical strategies are applied to

legitimize Nordea’s sustainability practices.Keywords: Institutional Logics, Multiple Logics, Sustainability, Compromising Strategy,

Micro Perspective, Rhetorical Strategies, Legitimacy, Banking

Table of Content

1. Introduction .................................................................................................. 1 1.1 Background .................................................................................................................. 1 1.2 Problem Statement ........................................................................................................ 2

1.3 Purpose and Research Question .................................................................................... 3

1.4 Thesis Disposition ........................................................................................................ 4

2. Theoretical Framework ................................................................................ 5 2.1 Development of Institutional Theory ............................................................................. 5

2.2 Defining Institutional Logics ........................................................................................ 6

2.3 Multiple Logics in the Institutional Environment .......................................................... 8 2.3.1 Compromising and Combining Logics ................................................................... 8

2.4 Applying Multiple Logics on Sustainability .................................................................. 9

2.5 Sustainability within the Banking Sector ..................................................................... 11

2.6 Institutionalization of Sustainability in Organizations ................................................. 12 2.6.1 Legitimizing Sustainability Practices through Communication ............................. 13

2.7 Theoretical Summary and Model of Analysis.............................................................. 14

3. Method ........................................................................................................ 17 3.1 Research Approach ..................................................................................................... 17

3.2 Research Design ......................................................................................................... 17 3.2.1 Selection of Case and Respondents ...................................................................... 18

3.3 Data Collection ........................................................................................................... 19 3.3.1 Interviews ............................................................................................................ 19

3.3.1.1 Constructing the Interview Guide .................................................................. 21 3.3.2 Secondary Data .................................................................................................... 22

3.4 Data Analysis ............................................................................................................. 23 3.4.1 Thematic Analysis ............................................................................................... 23

3.5 Ethical Considerations ................................................................................................ 25

4. Sustainable Finance at Nordea .................................................................. 26 4.1 Presenting Nordea and Group Sustainable Finance ..................................................... 26

4.2 Nordea’s Perception of Sustainability ......................................................................... 27 4.2.1 Sustainable Finance as a Business Opportunity .................................................... 28

4.3 Maximizing Profit and Saving the World .................................................................... 30 4.3.1 Altering Sustainability to the Banking Sector ....................................................... 30

4.3.2 Combining Profitability with Doing Societal Good .............................................. 32 4.3.3 Prioritizing Different Demands within Sustainable Responsibility ........................ 33

4.4 Nordea’s Journey Towards a Sustainable Future ......................................................... 33 4.4.1 Sustainability in Practice ...................................................................................... 34

4.4.1.1 Sustainable Products ..................................................................................... 36

4.5 Creating Acceptance for Nordea’s Sustainability Practices ......................................... 37 4.5.1 Formalizing Sustainability Practices ..................................................................... 38 4.5.2 Communicating Benefits of Sustainability............................................................ 39 4.5.3 Communicating Good Citizenship ........................................................................ 40

5. Analysis ....................................................................................................... 42 5.1 Perception of Sustainability ........................................................................................ 42

5.2 Managing Multiple Logics .......................................................................................... 44 5.2.1 Compromising Logics of Sustainability................................................................ 44 5.2.2 Combining Logics of Sustainability ..................................................................... 45 5.2.3 Managing Intra-Logic Conflicts ........................................................................... 46

5.3 Sustainability Practices ............................................................................................... 47 5.3.1 Institutionalization of Sustainability Practices ...................................................... 47

5.4 Legitimizing Sustainability ......................................................................................... 48 5.4.1 Normative Rhetoric .............................................................................................. 49 5.4.2 Instrumental Rhetoric ........................................................................................... 50 5.4.3 Value Rhetoric ..................................................................................................... 51

6. Conclusions ................................................................................................. 53 6.1 Limitations and Future Research ................................................................................. 54

7. References ................................................................................................... 55

Appendix ......................................................................................................... 61 Interview Guide ................................................................................................................ 61

1

1. Introduction 1.1 Background Sustainability has become a popular topic in today’s society. The fast consumption of resources

is making consumers more concerned of their own environmental impact as well as the impact

by other actors (Butler, 2018). Governments and media have also enhanced their awareness on

sustainability issues which has contributed to organizations experiencing higher demands

regarding their engagement in environmental and societal concerns (Borglund et al., 2008;

Hunoldt et al., 2018). Among organizations, the idea of sustainability has previously been

associated to organizational initiatives concerning ‘Corporate Social Responsibility’, CSR

(Carroll, 1999; Sheehy, 2015). Lately, however, the idea has developed into a more holistic

perspective involving all actors and their care for creating a sustainable future (Butler, 2018).

The increased global awareness of sustainability issues has therefore made it essential for

organizations to communicate their sustainability engagement in order to be perceived

legitimate (Furusten, 2013; Marais, 2012). By not conforming to the external pressures of

addressing sustainability issues, an organization’s reputation might become damaged which can

jeopardize its chances for future success and survival (Marais, 2012). In the banking sector, the increased demands on sustainability became particularly evident after

the financial crisis in 2008 when a strong wave of criticism was raised towards the banking

sector’s narrow focus on short-term results and lack of corporate responsibility (Borglund et

al., 2008; Jacob, 2012; Lauesen, 2013). Before the crisis, the financial industry’s engagement

in sustainability issues was in the shadow of other industries which were considered to have a

more direct environmental impact (Branco & Rodrigues, 2006; Cai et al., 2012; Thien, 2015).

The banking sector has thus previously received limited attention although banks possess an

influential role in societal and environmental concerns through investing and lending capital to

various industries and infrastructure projects (Kell, 2018; O’Sullivan & O’Dwyer, 2009). As a

result of the increased attention towards sustainability, financial leaders have begun to

recognize that success is not only measured by profits and costs, but rather by also taking

environmental, social and governmental (ESG) aspects into account (Raza, 2018).

Sustainability engagement has thus become increasingly important in the financial industry and

contributed to the establishment of ‘sustainable finance’.

2

1.2 Problem Statement When studying organizations and how they respond to external demands, institutional theory

can provide useful insights. Institutional theory implies that organizations operate in

institutional environments where they need to respond to institutionalized pressures in order to

achieve legitimacy (Butler, 2010; DiMaggio & Powell, 1983; Dowling & Pfeffer, 1975; Meyer

& Rowan, 1977; Suchman, 1995). However, since society is composed of multiple institutional

logics containing different principles for what is considered legitimate behaviour, organizations

can experience and interpret different influences to their practices (Thornton & Ocasio, 2008).

The institutional environment is thus characterized as being dynamic and complex, wherefore

organizations may be exposed to multiple institutional logics of legitimate behavior (Thornton

& Ocasio, 2008; Pache & Santos, 2013).

By applying institutional logics to sustainability, it is possible to acknowledge that there are

different reasons behind organizations’ engagement in sustainability practices. Scholars have

for example described how organizations can approach sustainability as fulfilling their societal

responsibility (Furusten, 2013; Grankvist, 2009; McElhaney, 2009; Wang, 2014). However,

there are also studies which rather emphasize that organizations engage in sustainability

practices due to a strategic approach towards corporate responsibility. Meaning that business

leaders have acknowledged that by integrating sustainability into their business strategy,

organizations perceive themselves becoming more efficient and profitable in the long-run

(McElhaney, 2009; Porter & Kramer, 2011).

The different perceptions behind organizations’ sustainability practices makes it possible to

define two conflicting logics of sustainability. A market logic which considers the involvement

in sustainability as driven by profit maximization, and a social logic which considers that

organizations ought to engage in sustainability practices in order to contribute to the greater

good. These conflicting logics of sustainability can also be related to Windell (2007) and

Bakker et al. (2016) categorization of actors engaging in sustainability; containing the money-

makers who perceive sustainability as a business opportunity and hence correspond with the

market logic, and the world saviours who perceive sustainability as doing social good and thus

conforms with the social logic. Consequently, multiple logics can make it difficult for

organizations to work with sustainability practices since different approaches contributes to a

confusion of what sustainability activities that should be applied, and how these should be

integrated (Høvring, 2017; Windell, 2007). Therefore, it becomes important for organizations

3

to successfully manage multiple and possibly contradicting logics as they function as references

for appropriate and legitimate behaviour (Pache & Santos, 2013; Smets et al., 2012; Thornton

& Ocasio, 2008). For example, Pache and Santos (2013) have suggested that by applying a

compromising- or combining strategy, organizations may overcome challenges and conflicts

that emerge in the managing of multiple logics. Furthermore, as it is essential for organizations

to be considered legitimate by the society in which it operates, scholars have also established

that professionals can use different rhetorical strategies to develop legitimacy for their

sustainability practices (Marais, 2012; Windell, 2007). Normative-, instrumental-, and value

rhetoric can therefore be applied depending on the relevant context and on what type of

legitimacy an organization wishes to develop (Marais, 2012).

Although studies regarding institutional logics have received increased attention within the

academia, the primary focus has been on the field level and thus overlooked the important micro

level origins which arise by individuals’ actions at work (Powell & Colyvas, 2008; Reay &

Hinings, 2009; Smets et al., 2012). In addition, the managing of multiple logics is poorly

understood and studies regarding how organizations respond to the complexity of multiple

logics are thus called for (Greenwood et al., 2010; Lindberg, 2014; Pache & Santos, 2010).

Furthermore, as the financial industry has a long history of focusing on profit maximization,

the context has been dominated by a market logic which has guided its organizing principles as

well as the understanding of what constitutes legitimate values and behaviour (Almandoz, 2014;

Davis, 2009; Thornton & Ocasio, 2008). Therefore, with the increasing demands of engaging

in sustainability, the financial industry is experiencing the challenge to successfully manage

and incorporate sustainability, containing both a market- and social logic, into a market driven

context. As the dominant market logic is being challenged, the banking sector thus appears as

a particular suitable context to study how multiple logics of sustainability can be managed and

legitimized at a micro level.

1.3 Purpose and Research Question The aim of this paper is to examine how multiple logics of sustainability can be managed in the

financial industry which historically has been recognized as being dominated by a market logic.

Moreover, since research within institutional logics has called for further studies exploring the

micro perspective, the study intends to make a theoretical contribution by exploring how an

organization can cope with multiple logics in their work. By conducting a case study, the study

4

also contributes with practical knowledge of how professionals responsible for driving an

organization’s sustainability practices can manage multiple logics and through rhetorical

strategies legitimize their sustainability practices in a context dominated by a market logic. In

view of the above considerations, the study intends to answer the following research question:

- How can multiple logics of sustainability be managed and legitimized in an

organization where the dominant logic is being challenged?

1.4 Thesis Disposition The thesis will be structured as follows. Chapter 2 will present a theoretical framework

highlighting the development of institutional theory, institutional logics, and how multiple

logics relate to sustainability. The theoretical section will also cover the establishment of

sustainability within the banking sector and rhetorical strategies which can be applied to

legitimize sustainability practices. In Chapter 3, the methodological considerations will be

further described, including the selection of case and respondents as well as how data was

collected. Chapter 4 will present the study’s empirical findings which in Chapter 5 will be

analyzed following the thesis’ model of analysis. Lastly, in Chapter 6, the main conclusions

will be presented and discussed together with limitations and suggestions for future research.

5

2. Theoretical Framework

This section begins with an introduction to institutional theory and the development of

institutional logics. Following, a discussion concerning the management of multiple logics

and the notion of sustainability in the banking sector is described. Thereafter, the

institutionalization of sustainability and legitimization of sustainability practices through

communication is presented. Finally, the chapter ends with a theoretical summary and an

illustration of the thesis’ model of analysis.

2.1 Development of Institutional Theory Institutional theory has for several decades been representing a dominant approach when

analyzing the interaction between an organization and its environment (Alvesson & Spicer,

2018; Guth, 2016). The study of institutions began with Selznick’s (1948) empirical research

on organizations and how they become affected by influences in their institutional environment.

In the seventies, Meyer and Rowan (1977) entered the institutional arena and emphasized the

role of modernization when rationalizing rules that are taken for granted by the society and

captured the process of isomorphism. The notion of isomorphism, which is organizations

tendency to become similar to each other, was further developed by DiMaggio and Powell

(1983) who placed it in a setting of organizational fields. DiMaggio and Powell’s (1983)

approach of isomorphism developed into ‘the new institutionalism’ which involved an

emphasis on legitimacy rather than efficiency. The authors thus argued that the success and

survival of an organization was dependent on the society’s perception of organizational

legitimacy. More specifically, by obtaining legitimacy, the organizational behavior is perceived

desirable and appropriate by the society (Dowling & Pfeffer, 1975; Suchman, 1995).

Consequently, although some scholars have criticized institutional theory for being vague and

include over-reach concepts (Alvesson & Spicer, 2018), the theory is considered a valuable

theoretical lens for analyzing how organizations are influenced by, and manage external

expectations from their institutional environment (Gauthier, 2013; Scott & Meyer, 1994).

During the nineties, a new approach to institutional analysis was created and it posited

institutional logics as defining the content and meaning of institutions (Friedland & Alford,

1991; Thornton & Ocasio, 1999). In contrast to previous studies, institutional logics discover

the effects that logics have on individuals and organizations, and thus disregard the notion of

isomorphism. Researchers adopting this approach consider the concept of institutional logics

6

to shape rational and mindful behaviour, while also allowing organizations to shape and change

institutional logics as well (Thornton & Ocasio, 2008). In parallel with the establishment of

institutional logics, another framework which also conceptualizes and explores institutional

dynamics has been developed. Lately, this has made the conversation of institutional theory to

become dominated by two schools of thought, namely institutional logics and institutional work

(Zilber, 2015). Institutional work, which was coined by Lawrence and Suddaby (2006), has a

bottom-up focus and emphasizes how individual action affects an institution or set of

institutions (Lawrence et al., 2011). Therefore, as this study aims to analyze what and how

multiple field level influences may impact organizational practices, institutional work is not the

most equipped framework to use due to its focus on creating, maintaining and disrupting

institutions. Institutional logics, however, remain central within institutional theory and is

applicable in this thesis as it highlights the importance of social context when shaping the

behaviour of social actors (Lindberg, 2014). Previous research has however primarily studied

institutional logics as a field level concept and relatively few studies has taken organizations as

the level of analysis (Lindberg, 2014; Pache & Santos, 2013; Smets et al., 2012; Zilber, 2015).

Important micro level dynamics have therefore been disregarded which in turn has contributed

to a lack of understanding of how logics are perceived and managed (Lindberg, 2014).

2.2 Defining Institutional Logics When Friedland and Alford (1991:248) developed the concept of institutional logics, they

defined it as “a set of material practices and symbolic constructions - which constitutes its

organizing principles and which is available to organizations and individuals to elaborate”.

Institutional logics can therefore be explained as the way social reality is constructed and is

central in shaping the interpretations that people have on their own work, as well as the actions

by others. Following this view, society is considered to be composed of multiple institutional

logics which are available to individuals and organizations as bases for their actions (Lindberg,

2014; Thornton & Ocasio, 2008). As a result, individuals within an organization will have to

consider and manage these different logics in their daily activities. Applying the approach of

institutional logics is therefore fruitful in this thesis when aiming to enhance the understanding

of what guides action, as well as how organizations can manage being influenced by several

different logics.

7

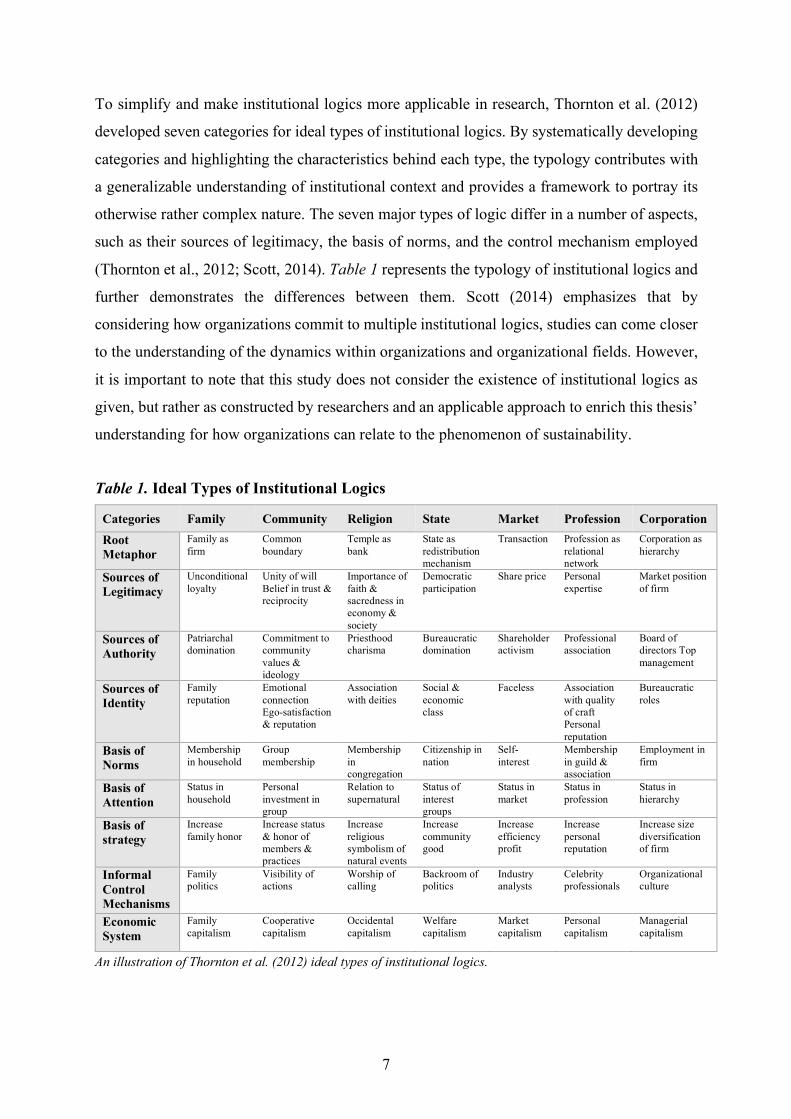

To simplify and make institutional logics more applicable in research, Thornton et al. (2012)

developed seven categories for ideal types of institutional logics. By systematically developing

categories and highlighting the characteristics behind each type, the typology contributes with

a generalizable understanding of institutional context and provides a framework to portray its

otherwise rather complex nature. The seven major types of logic differ in a number of aspects,

such as their sources of legitimacy, the basis of norms, and the control mechanism employed

(Thornton et al., 2012; Scott, 2014). Table 1 represents the typology of institutional logics and

further demonstrates the differences between them. Scott (2014) emphasizes that by

considering how organizations commit to multiple institutional logics, studies can come closer

to the understanding of the dynamics within organizations and organizational fields. However,

it is important to note that this study does not consider the existence of institutional logics as

given, but rather as constructed by researchers and an applicable approach to enrich this thesis’

understanding for how organizations can relate to the phenomenon of sustainability.

Table 1. Ideal Types of Institutional Logics

Categories Family Community Religion State Market Profession Corporation

Root Metaphor

Family as firm

Common boundary

Temple as bank

State as redistribution mechanism

Transaction Profession as relational network

Corporation as hierarchy

Sources of Legitimacy

Unconditional loyalty

Unity of will Belief in trust & reciprocity

Importance of faith & sacredness in economy & society

Democratic participation

Share price Personal expertise

Market position of firm

Sources of Authority

Patriarchal domination

Commitment to community values & ideology

Priesthood charisma

Bureaucratic domination

Shareholder activism

Professional association

Board of directors Top management

Sources of Identity

Family reputation

Emotional connection Ego-satisfaction & reputation

Association with deities

Social & economic class

Faceless Association with quality of craft Personal reputation

Bureaucratic roles

Basis of Norms

Membership in household

Group membership

Membership in congregation

Citizenship in nation

Self-interest

Membership in guild & association

Employment in firm

Basis of Attention

Status in household

Personal investment in group

Relation to supernatural

Status of interest groups

Status in market

Status in profession

Status in hierarchy

Basis of strategy

Increase family honor

Increase status & honor of members & practices

Increase religious symbolism of natural events

Increase community good

Increase efficiency profit

Increase personal reputation

Increase size diversification of firm

Informal Control Mechanisms

Family politics

Visibility of actions

Worship of calling

Backroom of politics

Industry analysts

Celebrity professionals

Organizational culture

Economic System

Family capitalism

Cooperative capitalism

Occidental capitalism

Welfare capitalism

Market capitalism

Personal capitalism

Managerial capitalism

An illustration of Thornton et al. (2012) ideal types of institutional logics.

8

2.3 Multiple Logics in the Institutional Environment Organizations operating in complex and dynamic institutional environments can come across

institutional pluralism (Pache & Santos, 2013; Reay & Hinings, 2009; Thornton et al., 2012).

Kraatz and Block (2008:243) explain institutional pluralism by making the following metaphor,

“if institutions are broadly understood as ‘the rules of the game’ that direct and circumscribe

organizational behaviour, then the organization confronting institutional pluralism plays in two

or more games at the same time”. Organizations that are managing institutional pluralism are

therefore subject for multiple demands coming from more than one logic (ibid).

Although it has been acknowledged that several institutional logics can co-exist within an

institution, the predominant view has been that there is one dominant logic that guides

organizational action (Lindberg, 2014; Scott, 2014). Lately, however, there has been an increase

of studies showing how fields are guided by multiple logics, which has contributed to a quest

for research concerning how organizations experience and practically respond to the complexity

arising from multiple institutional logics (Greenwood et al., 2010; Pache & Santos, 2013). In

current studies of multiple logics, researchers have found both competitive and cooperative

aspects of logics (Goodrick & Reay, 2011; Lounsbury, 2008; Swan et al., 2010). The

multiplicity of logics, as well as the degree to which such logics are incompatible, ultimately

influences an organization’s possibility to practically manage multiple logics (Lindberg, 2014;

Scott, 2014).

2.3.1 Compromising and Combining Logics In the beginning of institutional research, authors suggested that organizations could manage

conflicting logics through decoupling (Meyer & Rowan, 1977). Decoupling involves the

process of separating formal structure from actual organizational practices as a response to

institutional pressures and for legitimacy purposes (Boxenbaum & Jonsson, 2008; Meyer &

Rowan, 1977). However, as more studies have been conducted, the structure of decoupling has

received less attention and new approaches involving compromising or combining multiple

logics have been established to reconcile conflicting demands (Kraatz & Block, 2008; Oliver,

1991). By compromising conflicting demands, organizations can perform practices that are

influenced by multiple logics which elements have been altered in order to create a balance

between the logics (Pache & Santos, 2013). This can for example be enacted as conforming to

the minimum standard of what is expected in each logic, crafting a new behavior that brings

9

elements of the conflicting logics together, or by influencing institutional referents to alter their

demands (ibid). The compromising approach can thus ease an organization’s ability to be

perceived legitimate by different referent groups by incorporating elements of each logic.

Nevertheless, holding an approach to constantly compromise between competing logics can

also cause weaknesses as it does not allow organizations to obtain complete support from its

referent groups since some of their expectations are disregarded. The approach may also be

inapplicable when the multiple logics imply goals or practices that are not compatible with each

other, and thus results in an inability to meet the institutional referents’ expectations (Pache &

Santos, 2010).

By applying an approach of combining conflicting logics, rather than to compromise them, an

organization can try to take advantage of how multiple logics can create opportunities for a

broader range of appropriate behaviour (Greenwood et al., 2010; Reay & Hinings, 2009). This

approach thus contributes to organizations performing a combination of activities that are

drawn from each logic in an attempt to secure support from different referent groups.

Consequently, in contrast to the compromising approach where certain elements of the logics

are incorporated, this approach entails combining the different logics without modifying them

(Pache & Santos, 2013). There are however some limitations to this approach as well. Similar

to the compromising approach, the combination of several logics involves the challenge of

fulfilling competing demands while also being perceived legitimate by the audience (ibid).

Nevertheless, successful attempts of combining logics at an organizational level have the

capacity to influence the organizational field which might contribute to the creation of altered

institutionalized practices (Smets et al., 2012).

2.4 Applying Multiple Logics on Sustainability As emphasized in the introduction to this thesis, the phenomenon of sustainability can be

interpreted and managed differently. Scholars have for example described the reason behind

engaging in sustainability as contributing to social good or performing it based on business

reasons (Grankvist, 2009; McElhaney, 2009; Wang, 2014). Relating the different approaches

on sustainability to the scheme of institutional logics presented in Table 1 by Thornton et al.

(2012), it is possible to apply the view of sustainability as driven by either a state logic of

citizenship and welfare, or from a market logic driven by maximization of shareholder profit.

This interpretation of sustainability is also applicable to Windell (2007) and Bakker et al. (2016)

10

categorization of different actors engaging in sustainability, involving the money-makers and

the world saviours. The money-makers and world saviours have divergent perspectives of the

meaning and implications of sustainability. Actors that can be defined as money-makers are

practicing sustainability driven by its perception of enhancing business opportunities. The

practices are therefore conducted as a response to market demand as well as the opinion that

sustainability contributes to increase profitability; something which can be related to the

characteristics of the market logic. In contrast, the world saviours can be related to the social

logic and involves practicing sustainability to contribute to social good and change the world

for the better. The profitability of engaging in sustainability practices is hence not considered

the most significant reason (ibid).

Drawing on the divisions of logics emphasized by Thornton et al. (2012), as well as Windell

(2007) and Bakker et al. (2016) categorization of actors engaging in sustainability practices,

this thesis study sustainability from a market- and social logic perspective. The market logic is

similar to the one described by Thornton et al. (2012) although it is adjusted to the literature of

sustainability. Furthermore, by analyzing influences from a social logic rather than a state logic

perspective, the thesis adds on to Thornton et al. (2012) logics by incorporating a global

perspective. The reason behind the usage of a social logic is hence based on the perception that

sustainability issues are not limited to states nor country borders. Although the market- and

social logic are simplified approaches of sustainability, the logics entail elements that are

commonly discussed in regards to sustainability and will therefore constitute the foundation for

this thesis when analyzing how an organization perceives, manages and legitimizes

sustainability in the financial industry. Figure 1 represents the market- and social logic and

further demonstrates the differences between them.

Figure 1. Elements of Market- and Social Logic

11

2.5 Sustainability within the Banking Sector As the financial industry has a long history of focusing on optimizing financial return, the

context has been dominated by a market logic which has guided the understanding of what

constitutes legitimate values and behaviour (Almandoz, 2014; Davis, 2009; Thornton & Ocasio,

2008). In terms of sustainability practices, banks have previously experienced limited

stakeholder expectations concerning the involvement in sustainability issues (Borglund et al.,

2008; Kell, 2018; Sun et al., 2011). Investors were for example initially reluctant to

sustainability practices, claiming that their fiduciary duty were limited to the maximization of

shareholder profit. The banking sector’s engagement in sustainability issues have thus

previously been in the shadow of other industries which are considered to have a more direct

environmental impact (Branco & Rodrigues, 2006; Cai et al., 2012). The lack of attention

towards banks’ corporate responsibility has therefore contributed to a literature gap within

financial research (Branco & Rodrigues, 2006; Kell, 2018).

Lately, however, the demands on the financial industry have changed and banks are nowadays

expected to engage in practices for social and environmental sustainability (Borglund et al.,

2008; Kell, 2018). This became particularly evident after the financial crisis in 2008 which

raised a strong wave of criticism towards the banking sector’s narrow focus on short-term

results and lack of corporate responsibility (Borglund et al., 2008; Jacob, 2012; Lauesen, 2013).

The dominating market logic’s focus on profit maximization thus became challenged and

required banks to incorporate and engage in new practices to fulfill their stakeholders’

sustainability demands. The demands that evolved in the aftermath of the crisis strengthened

the regulations wherefore banks had to a wider extent engage in sustainability and increase

disclosures regarding their sustainability practices (Chelli et al., 2014; Lauesen, 2013).

Within the banking sector, banks also possess a wider responsibility since they are involved in

investing and lending capital to various industries and infrastructure projects which may have

an impact on societal and environmental concerns (Cai et al., 2012; Kell, 2018; O’Sullivan &

O’Dwyer, 2009). As a result of the increased responsibility, as well as the acknowledgement

that banks can be involved in controversial investment decisions, the notion of sustainable

finance has become an established concept within the industry (ibid). The European

Commission (2019) defines sustainable finance as the provision of finance to investments while

taking environmental, social, and governmental aspects into account. Even though sustainable

finance has become a common occurrence, it is still rather unclear how banks can approach the

12

concept and how sustainability activities are applied in practice (Chelli et al., 2014; O’Sullivan

& O’Dwyer, 2009). Consequently, this type of study is requested (Branco & Rodrigues, 2006;

Smets et al., 2012; Thien, 2015) and the financial industry is of particular relevance since the

incorporation of sustainability, which holds both a market- and social logic, can contribute to

insights in practices that will influence the market logic dominating field.

2.6 Institutionalization of Sustainability in Organizations Sustainability practices can neither be seen as a fixed script, nor a tool that can guarantee

organizations to obtain legitimacy (Sahlin & Wedlin, 2008; Schultz & Wehmeier, 2010).

Instead, the institutionalization of sustainability rather represents a dynamic process where the

outcome reflects the interplay between actors, actions, and expectations in the relevant context

(ibid). It is also important to be aware and consider how each actor’s own interpretations and

personal values influence and shape the institutionalization process (Schultz & Wehmeier,

2010). Consequently, to gain a better understanding for how practices become institutionalized

within organizations, it is necessary to view the interplay between actors in their current context

and how they reinforce and influence each other (Sahlin & Wedlin, 2008).

As an idea of new practices travels through an organization, it will encounter existing practices

and ideas which will influence the translation process. Schultz and Wehmeier (2010) have

described the process of how new ideas of sustainability enter corporate life, and how it begins

by being translated to the organization’s context. However, as organizations begin

communicating and performing their sustainability activities, the idea will become modified

and hence change from its original form. Nevertheless, the translation of ideas is an ongoing

process in the sense that it never becomes finalized. This is a result of what is being translated

constantly changes as it travels through different fields, settings and encounters already

embedded practices (Sahlin & Wedlin, 2008). Although the institutionalization process of

sustainability practices can be described as an unpredicted process dependent on the

individual’s own interpretations, prior research has found that it is possible to influence what

becomes legitimate sustainability practices through strategic communication (Marais, 2012;

Schultz & Wehmeier, 2010).

13

2.6.1 Legitimizing Sustainability Practices through Communication As strategic communication has been identified as an influential tool to legitimize sustainability

(Schultz & Wehmeier, 2010), it is for the purpose of this thesis relevant to look further into

how professionals can communicate their sustainability practices to make them legitimate.

Windell (2007) has explored how professionals can spur the legitimization of sustainability

practices and hence contribute to the institutionalization of sustainability. Windell’s (2007)

study of commercializing and mobilizing CSR entails three stages: labelling fluffy ideas,

packaging fluffy ideas, and mobilizing a label. In the first stage, the various labels of CSR are

reduced to one common label in order to raise awareness for businesses’ social responsibility

and to create a market demand for services addressing CSR. Stage two involves packaging

fluffy labels wherefore the concept of CSR is packaged into sellable products and services. In

the last stage, the label of CSR is mobilized by using rhetorical strategies built on economic

arguments which aim to convince the business community about the values of performing CSR.

The arguments are thus based on profit and efficiency improvements and contributes to make

CSR a comprehensible business idea.

The rhetorical stage in Windell’s (2007) study also relates to Marais’s (2012) study which

highlights three rhetorical strategies that can be applied to legitimize sustainability practices.

Marais’ (2012) three rhetorical strategies are labelled normative-, instrumental-, and value

rhetoric, and these are applied depending on what stakeholder the organization is

communicating with and what type of legitimacy the organization wishes to develop. The

normative rhetoric is used to develop corporate cognitive legitimacy and focus on creating trust

among the stakeholders by emphasizing the organization’s willingness to follow accepted

sustainability norms and standards. In order for an organization to create legitimacy based upon

trust, top management will thus need to communicate statements to the stakeholders regarding

the organization’s sustainability position and activities. The second strategy, instrumental

rhetoric, is applied to develop pragmatic legitimacy which concerns the self-interest of the

organization’s stakeholders. Instrumental rhetoric thus aims to demonstrate how the

stakeholder may benefit by the organization being engaged in sustainability practices. If the

organization satisfy stakeholders’ utility, the stakeholders will support the organization and the

practices will be considered legitimate. This rhetoric is thus similar to Windell’s (2007) third

stage which also aims to establish legitimacy by communicating how the organization’s

sustainability involvement may benefit the stakeholder. Marais (2012) last strategy, the value

rhetoric, entails approaching the stakeholders’ feelings and emotions which contributes to

14

create moral legitimacy. In this rhetorical strategy, organizations gain legitimacy for their

sustainability practices by emphasizing attributes of good citizenship as their communication

evolves around values and shared moral principles. This contributes to make the stakeholders

approve the practices and hence consider them legitimate.

For the purpose of this study, the authors have incorporated Windell’s (2007) stages, involving

the establishment and commercialization of sustainability, with Marais’ (2012) rhetorical

strategies to examine how sustainability practices can become legitimate through

communication. Although Windell’s (2007) study focuses on how consultants have managed

to establish and sell CSR services to corporations, the strategy can also be applied on actors

within an organization as they aim to legitimize and implement sustainability in a profit driven

context. Furthermore, while Marais’ (2012) study focuses on top management, the rhetorical

strategies can provide valuable insights when analyzing how professionals responsible for

driving an organization’s sustainability practices can gain legitimacy through their

communication.

2.7 Theoretical Summary and Model of Analysis The literature review has introduced institutional theory and presented the development of

institutional logics which has shed light on some of the challenges associated with multiple

logics that organizations have to successfully manage in order to legitimize their practices. By

exploring the perception of sustainability, this thesis will consider the conflict between the

market- and social logic, while also analyzing how rhetorical strategies can be applied to

legitimize sustainability practices. The empirical research in this thesis will hence be conducted

at a micro level, although the logics that are influencing the work are emerging from the macro

level. By adding a contribution to Thornton et al. (2012) division of logics, and by incorporating

the categorization of actors engaging in sustainability (Bakker et al., 2016; Windell, 2007), this

thesis will apply the market logic as characterized by profit maximization and money-makers,

and the social logic featured by social welfare and world saviours. These two logics will thus

constitute the foundation in the analysis for how a bank perceives and manages multiple logics

of sustainability.

15

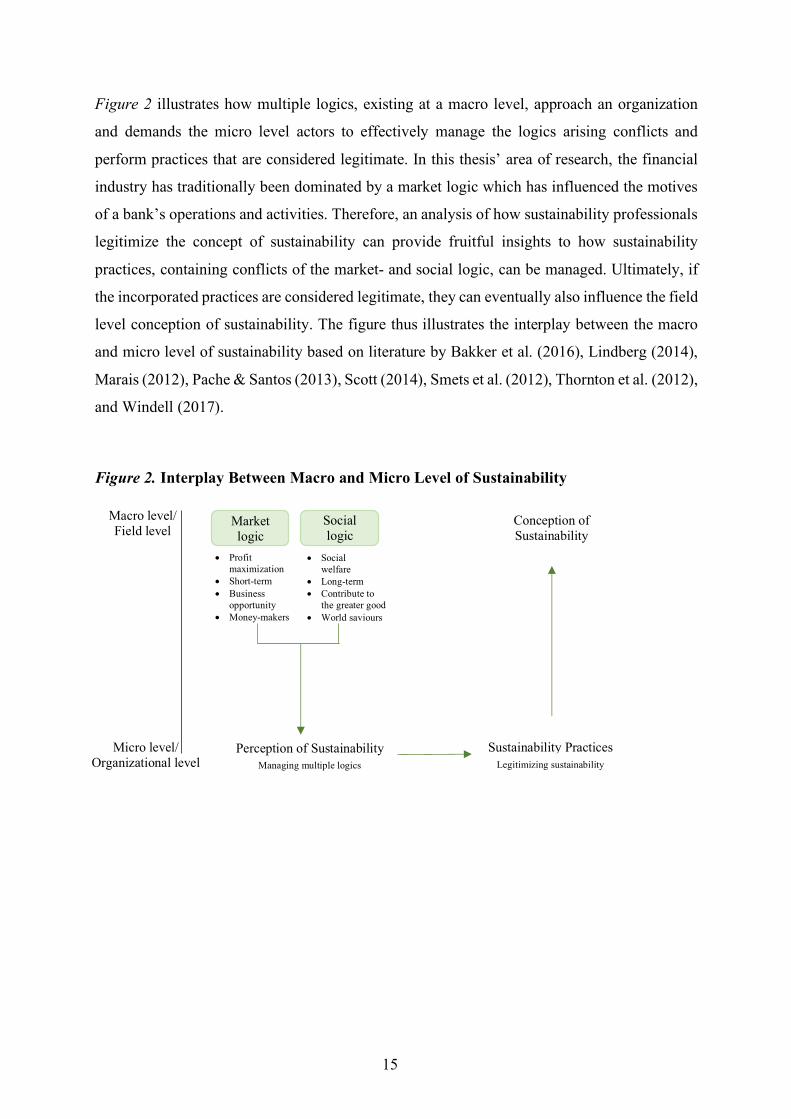

Figure 2 illustrates how multiple logics, existing at a macro level, approach an organization

and demands the micro level actors to effectively manage the logics arising conflicts and

perform practices that are considered legitimate. In this thesis’ area of research, the financial

industry has traditionally been dominated by a market logic which has influenced the motives

of a bank’s operations and activities. Therefore, an analysis of how sustainability professionals

legitimize the concept of sustainability can provide fruitful insights to how sustainability

practices, containing conflicts of the market- and social logic, can be managed. Ultimately, if

the incorporated practices are considered legitimate, they can eventually also influence the field

level conception of sustainability. The figure thus illustrates the interplay between the macro

and micro level of sustainability based on literature by Bakker et al. (2016), Lindberg (2014),

Marais (2012), Pache & Santos (2013), Scott (2014), Smets et al. (2012), Thornton et al. (2012),

and Windell (2017).

Figure 2. Interplay Between Macro and Micro Level of Sustainability

Managing multiple logics

Macro level/ Field level

Micro level/ Organizational level

Market logic

Social logic

• Profit maximization

• Short-term • Business

opportunity • Money-makers

• Social welfare

• Long-term • Contribute to

the greater good • World saviours

Perception of Sustainability

Sustainability Practices

Conception of Sustainability

Legitimizing sustainability

16

Figure 3 illustrates the thesis’ model of analysis. Based on the above literature review, the

study’s model of analysis will focus on the micro level aspects of managing multiple logics and

how sustainability practices can become legitimized. The first part of the analysis model will

explore how the concept of sustainability is perceived and how sustainability professionals,

through compromising or combining multiple logics of sustainability, adapt sustainability to

suit the financial industry and its dominating market logic. The second part of the analysis will

focus on the sustainability practices and how sustainability professionals legitimize their

practices through normative-, instrumental- and value rhetorical strategies.

Figure 3. Model of Analysis

Social logic

Macro level/ Field level

Micro level/ Organizational level

Perception of Sustainability

Sustainability Practices

Managing multiple logics • Compromising • Combining

Legitimizing sustainability • Normative

rhetoric • Instrumental

rhetoric • Value rhetoric

Market logic

17

3. Method

This section begins with a presentation of the thesis’ research approach and design followed

by a description of how primary- and secondary data was collected. This part also entails

how the interviews were conducted and how the operationalization was made. Finally, the

chapter ends with a discussion of the data analysis and ethical considerations.

3.1 Research Approach In order to gain insights into the micro level perspective of managing multiple logics, this thesis

has been conducted as an exploratory research. An explorative design was considered

appropriate since it clarifies the phenomenon of sustainability and how multiple logics may

influence sustainability practices. Moreover, Bryman and Bell (2017) argue that an explorative

research is a suitable method to use when the area of study is poorly addressed; which is the

case for this thesis (Greenwood et al., 2010; Lindberg, 2014; Pache & Santos, 2010; Powell &

Colywas, 2008; Reay & Hinings, 2009; Smets et al., 2012). Furthermore, the thesis has applied

an abductive approach where the authors have moved back and forth between theory and

research in order to gradually understand the multiple logics of sustainability and how the

managing of these influences’ organizational practices. This approach enabled valuable

reflections between existing theory and practice, and was of particular relevance for this study

since research exploring the micro level perspective of institutional logics is limited. The study

has hence been steered by a theoretical framework while also allowing the findings to be fed

back into the stock of theory (Bryman & Bell, 2017; Saunders et al., 2016; Yin, 2014).

Moreover, in an attempt to enhance reliability, the authors have aimed to explicitly explain how

the phenomenon of sustainability is applied in the research. Consequently, this transparency

intends to make it possible for other researchers to perform a similar set of study (Saunders et

al., 2016).

3.2 Research Design As the aim of this paper is to examine how a bank can manage multiple logics of sustainability

and legitimize their sustainability practices, the research has been conducted as a qualitative

case study. A qualitative case study has proven to be appropriate since it allowed the studied

organization’s perception, as well as the respondents’ experiences, to become prominent

(Saunders et al., 2016; Yin, 2014). The research design has therefore contributed to the

18

possibility to draw inferences out of the perceptions of sustainability, the managing of multiple

logics, and how the bank’s sustainability practices are legitimized through rhetorical strategies.

Due to criticism concerning the external validity of case study results (ibid), the findings are

not interpreted to reflect the perception and managing of multiple logics across the financial

field. The performed case study rather provides a practical example and aims to contribute with

a deeper understanding for the complexity of managing multiple logics through studying it in

one relevant organization. The research design is therefore considered appropriate for this study

and its intended purpose.

3.2.1 Selection of Case and Respondents The Nordic bank Nordea constitutes the case of this study and exemplifies how multiple logics

of sustainability can be managed in a context that historically has been recognized as being

driven by a market logic. Nordea was selected due to their increased involvement in

sustainability initiatives which are reflected in the organization’s continuous development of

new sustainable products such as sustainable funds and green mortgages (Nordea, 2019a).

Furthermore, Nordea has as the only Nordic bank been ranked as one of the world’s top 100

most sustainable corporations (Corporate Knights, 2019). In addition, having access to in-depth

insights to Nordea’s sustainability work facilitated a sufficient data collection which further

contributed to make the bank an appropriate case to study. Therefore, in view of Nordea’s

engagement in sustainability, the bank is considered a proper organization for analyzing how

sustainability, consisting of multiple logics, can be managed and legitimized in a market driven

context.

In order to answer the research question, professionals responsible for setting and driving the

sustainability agenda within Nordea Group has been interviewed. At Nordea, Group

Sustainable Finance (GSF) is responsible for integrating sustainability throughout the

organization, as well as driving the sustainability agenda both internally and externally.

Professionals within this team were therefore relevant to interview in order to explore how

multiple logics of sustainability are managed, and how rhetorical strategies are being used to

legitimize sustainability practices in a market driven context. In accordance to Bryman and Bell

(2017) and Jacobsen (2002), the authors have applied a purposive sampling as the aim of the

sampling was to choose participants in a strategic way so that the sampled respondents were

relevant to the research question. This selection of respondents is also promoted by Saunders

et al. (2016) as they argue that interviewing experts is a favorable way to conduct exploratory

19

research. However, the authors are aware that the purposive sample venture that potential

respondents who possess important information in other parts of the organization might get

excluded from the study (Bryman & Bell, 2017). Nevertheless, the benefits of interviewing

people from GSF who drives Nordea’s sustainability work exceeded the drawbacks as their

responses contributed to a profound analysis and represents Nordea’s take on sustainability.

3.3 Data Collection 3.3.1 Interviews The study’s primary data consisted of ten interviews with respondents from GSF. Studies

conducted on a limited number of interviews are often criticized for their lack of external

validity as such studies are not considered to represent a wider population (Bryman & Bell,

2017). However, since this study aims to investigate the management of conflicting logics and

how Nordea legitimize their sustainability practices, the authors consider the chosen

respondents as able to contribute to a sufficient analysis for the thesis’ intended purpose.

Additionally, similar answers were identified already after five interviews wherefore ten

interviews were considered to represent a proper number of interviews in order to reach a

saturation for the studied topic. Table 2 will further elucidate the interview details.

Table 2. Description of Interviews

Respondent Position at Group Sustainable Finance (GSF) Date Duration

Respondent 1 Head of Thematic Research 2019.03.18 55:33 min Respondent 2 Sustainability Expert & Executive Advisor 2019.03.18 53:51 min

Respondent 3 Sustainability Expert & ESG Advisor 2019.03.19 50:40 min Respondent 4 Business Area Lead, Personal Banking 2019.03.21 49:00 min

Respondent 5 Business Area Lead, Commercial and Business Banking 2019.03.21 47:48 min Respondent 6 Business Area Lead, Wholesale Banking 2019.03.22 41:36 min

Respondent 7 Deputy Head of GSF, Business Development 2019.03.22 53:56 min Respondent 8 Sustainability Reporting Expert 2019.03.26 52:27 min

Respondent 9 Communication Manager 2019.03.26 49:50 min Respondent 10 Business Area Lead, Asset & Wealth Management 2019.04.04 43:43 min

The interviews were conducted by applying a semi-structured approach which according to

Jugesten and Mik-Meyer (2011) is appropriate when performing an exploratory research. The

interviews were thus following an interview guide which were established prior to the

20

interviews and operationalized upon the theoretical framework. The guide was used during all

occasions to entail a similar structure and it is presented in Appendix A. The semi-structured

interviews thus facilitated the possibility to ask open questions concerning sustainability and

how GSF manages and drives the concept within Nordea. Furthermore, in accordance to

Saunders et al. (2016), the semi-structured approach made it possible for the authors to deviate

from a set structure of questions and instead make room for new insights which emerged during

the interviews.

Nine of the interviews were made at the respondents’ workplace in Stockholm, and one

interview was conducted through a video-chat due to the respondent being positioned in

Finland. All the interviews were conducted in Swedish in order to make the respondents feel

more comfortable while speaking their native language. The intention was thus to create a calm

atmosphere which hopefully would result in more detailed answers (Bryman & Bell, 2017).

During all ten interviews, both authors were present although it was mainly one who was

leading the interview in order to secure an active conversation involving follow-up questions.

The other author was in charge of making sure that the discussion had covered the questions in

the interview-guide while also taking some notes and contributing with follow-up questions if

something had to be further elaborated. All respondents gave their consent to become recorded

during the interview which enabled both authors to give their full attention to the discussion.

The recordings also made it possible to transcribe the interviews word-by-word which

facilitated the possibility to go over the material and make sure that all data was taken into

consideration; which increases the reliability of the study (Bryman & Bell, 2017; Saunders et

al., 2016).

Since recordings have been used during all interviews, the authors have considered the

possibility that the respondents have chosen to express themselves more carefully. However,

considering that the thesis does not wish to explore individual opinions concerning

sustainability, but rather represents the organization’s take on sustainability, the interviews have

not been of a sensitive character wherefore the recordings should not have had any major impact

on the responses. Furthermore, since one of the interviews was performed through a video-chat,

the authors were aware of the risk that some of the personal interaction may have become

damaged. However, the contribution made by this respondent was considered important to

include in the study in order to receive data covering all of Nordea’s four business areas.

21

3.3.1.1 Constructing the Interview Guide The interview guide was, in addition to the opening questions, divided into four main parts;

Perception of Sustainability, Managing Conflicting Logics of Sustainability, Sustainability

Practices and Legitimizing Sustainability Practices. The questions thus follow the thesis’ model

of analysis and the interview guide can be found in Appendix A.

The first part of the interview guide concerned the perception of sustainability and aimed to

explore how the respondents apply Nordea’s perception of sustainability to the financial

industry. The first question was therefore asked in order to understand the respondent’s opinion

of incorporating sustainability in the banking sector which emphasized the logic related to

sustainability. Moreover, the respondent was given the opportunity to describe Nordea’s

purpose of engaging in sustainability which associated to the market- and social logic (Thornton

et al., 2012) as well as Bakker et al. (2016) and Windell’s (2007) definition of actors engaging

in sustainability: the money-makers and the world saviours. The questions therefore enabled

the authors to draw inferences out of the responses to get a deeper understanding of Nordea’s

perception of sustainability and connect it to the literature concerning market- and social logic.

The second part of the interview guide involved the managing of conflicting logics, wherefore

the authors wished to explore the respondents’ opinions concerning different elements in the

market- and social logic together with challenges of implementing sustainability. Therefore,

this part included questions concerning how GSF manages conflicting logics which is

connected to literature that emphasize how organizations can incorporate different strategies in

an attempt to reconcile conflicting demands (Kraatz & Block, 2008; Oliver, 1991). This is

primarily related to Pache and Santos (2013) and Reay and Hinings’ (2009) discussion of

compromising and combining conflicting logics. Consequently, these questions made it

possible to identify the difficulties that GSF is experiencing when incorporating their

sustainability practices, as well as how the challenges of multiple logics are being managed.

The third part involved questions regarding Nordea’s sustainability practices and this section

of the interview aimed to gain a further understanding of what is included in Nordea’s

sustainability work. To receive a deeper understanding of how the sustainability practices are

implemented in the organization, this section also included a specific question regarding how

the sustainability practices are integrated in the bank. This question facilitated the possibility to

explore how the practices could be connected to the co-existence of multiple logics discussed

22

by Lindberg (2014) and Thornton et al. (2012). The questions therefore explored Nordea’s

sustainability practices and contributed to the possibility to understand how GSF integrates

sustainability throughout the organization.

The last part of the interview guide covered the legitimizing of sustainability practices and

strived to explore how the practices become legitimized and how the respondents choose to

communicate in order to develop legitimacy. The questions thus explored how Nordea’s

sustainability practices are communicated and if the used rhetoric depends on which

stakeholder Nordea approaches. This part relates to Marais’ (2012) three different rhetorical

strategies which can be applied in order to legitimize sustainability practices. The questions

also relate to the third stage in Windell’s (2007) study which concerns how rhetorical strategies,

founded on appealing arguments for the relevant stakeholders, are applied by actors to

legitimize sustainability. This part has therefore contributed to insights of how Nordea’s

sustainability practices are being rhetorically communicated to gain legitimacy and acceptance

by their stakeholders.

3.3.2 Secondary Data Apart from the interviews, secondary data consisting of documents produced by Nordea have

been utilized to enrich the understanding of how multiple logics of sustainability are managed

in the organizational context. In order to gather data regarding Nordea’s sustainability practices

and how these relate to the market- and social logic, the study included information available

on the organization’s website, reports such as “Sustainability Report 2018” as well as brochures

communicating Nordea’s engagement within sustainability, e.g. “Sustainable Finance at

Nordea”. In addition, the secondary data consisted of Nordea’s Sustainable Finance YouTube

videos and LinkedIn posts as these also constitute an essential part of Nordea’s communication

regarding their sustainability practices.

By combining different sources of data, the authors have been able to compare the results

obtained in the interviews with the findings from the secondary data (Bryman & Bell, 2017).

This facilitated the possibility to identify common approaches towards sustainability and how

the managing of multiple logics is conducted at Nordea. Complementing the interviews with

secondary data also made it possible to analyze the rhetorical strategies applied to legitimize

Nordea’s sustainability practices, while also exposing potential inconsistencies between how

the concept of sustainability is managed by the respondents and presented in the secondary data.

23

Consequently, by using several sources of data when conducting the research, the authors have

applied triangulation which increases the study’s reliability (Patel & Davidson, 2011; Saunders

et al., 2016).

3.4 Data Analysis As the research aims to study the managing of multiple logics at a micro level, the unit of

analysis is on an organizational level. The coding process involved reviewing all collected data

and labelling data that seem to be of theoretical significance or that appear prominent within

the social worlds of those being studied (Saunders et al., 2016). The collected data was thus

reviewed and the authors searched for concepts, phrases and keywords that were considered

relevant in relation to the thesis’ purpose and model of analysis. Nevertheless, the authors have

acknowledged that their own interpretations can have influenced the data analysis as they are

the only ones deciding what is considered to be of interest in the collected data which can affect

the study’s validity (Braun & Clarke, 2006; Bryman & Bell, 2017). The authors have however

tried to avoid being biased by analyzing the data independently and then combining their

findings which contributes to improve the analysis of the data since it involves diverse

perspectives (Patel & Davidson, 2011).

3.4.1 Thematic Analysis By using a thematic analysis, the coded data was initially sorted into various themes connected

to the thesis’ model of analysis. This involved the perception of sustainability, managing

multiple logics of sustainability, sustainability practices and rhetoric used to legitimize the

sustainability practices. These were later extended with subcategories which were identified as

relevant for the thesis model of analysis, see Table 3. However, the analysis process has not

been linear but rather an ongoing process where data has been reviewed and connected to the

relevant themes that have emerged. In thematic analysis, it is important to make sure that the

identified themes do not overlap each other (Braun & Clarke, 2006), which is challenging when

studying institutional logics that are rather vague in its nature. Nonetheless, the authors strived

to create as distinctive themes as possible in order to clarify and separate each theme from each

other.

24

After the process of identifying themes, they were connected to the relevant theory and the

research purpose. This approach resulted in a detailed analysis of some aspects of the data, but

also an exclusion of the remaining data. Therefore, the authors have acknowledged and been

aware of the thematic analysis’ risk of fragmenting data which can cause a loss in the context

of what has been said; something which is considered a limitation in this type of analysis

(Bryman & Bell, 2017). However, in order to minimize this limitation, the authors have

performed a cautious thematic analysis, which as previously described involved reviewing the

data apart and then together. Moreover, as the thematic analysis aimed to study different

concepts of logics, it was important that the authors strived to identify the underlying

assumptions connected to the literature.

Table 3. Coding Scheme

Main Theme Subcategory Codes Representative Quotations

Perception of Sustainability

Market Logic

• Profit maximization • Business opportunity • Competitive • Self-interest

“Sustainability is business” “Sustainability is about surviving and preparing ourselves for what the future holds”

Social Logic

• Responsibility • Social welfare • Contribute to the

greater good • Long-term • Circular economy

“By being a central part of the society, Nordea has a big responsibility to transfer capital to more sustainable solutions” “It is part of Nordea’s duty to drive the shift towards a sustainable future”

Managing Multiple Logics

Compromising

• Altering elements of logics

• Adapting sustainability to finance

• Social concern without performing charity

“Sustainability has nowadays become correctly adapted to the financial sector” “If it is done correctly, sustainable investments will give better returns while also contributing to something good - it is a win-win”

Combining

• Not altering elements of logics

• Two-sided purpose • Business-driven &

good corporate citizen

“The primarily purpose is to make money, but this cannot be made at any cost” “Two-sided purpose, making money while contributing to a sustainable development”

Intra-Logic Conflicts

• Conflicts within one logic

• Prioritizing demands • Satisfy stakeholders

“Since sustainability involves environmental and societal concerns that usually are integrated, we have to find a way to manage these different demands” “We cannot shut down the oil industry one day to another because then we would not take our social responsibility as that would make people unemployed”

25

Sustainability Practices

Sustainability Agenda

• Strategic direction • Leadership position • GSF’s responsibility • Integrate sustainability • Institutionalization of

sustainability

”GSF sets and drives the sustainability agenda throughout Nordea by setting targets and developing position statements” ”Sustainability has to become a part of Nordea’s DNA”

Activities & Products

• Initiatives • Ambassador forum • E-learning • Star-fund • Green bond • Green mortgage

“We have developed an E-learning to educate all employees at Nordea. It is necessary to raise awareness and involve the employees within the organization” “It is important to offer something concrete to our customers, show them how profitability and sustainability is compatible”

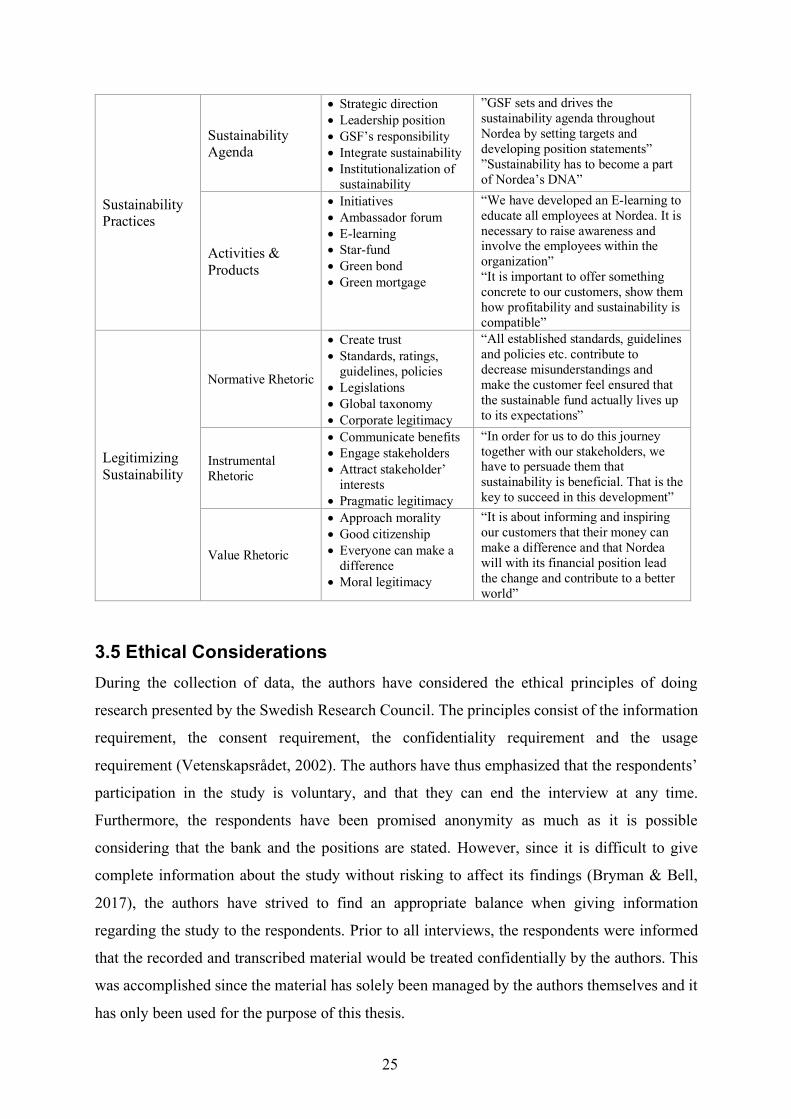

Legitimizing Sustainability

Normative Rhetoric

• Create trust • Standards, ratings,

guidelines, policies • Legislations • Global taxonomy • Corporate legitimacy

“All established standards, guidelines and policies etc. contribute to decrease misunderstandings and make the customer feel ensured that the sustainable fund actually lives up to its expectations”

Instrumental Rhetoric

• Communicate benefits • Engage stakeholders • Attract stakeholder’

interests • Pragmatic legitimacy

“In order for us to do this journey together with our stakeholders, we have to persuade them that sustainability is beneficial. That is the key to succeed in this development”

Value Rhetoric

• Approach morality • Good citizenship • Everyone can make a

difference • Moral legitimacy

“It is about informing and inspiring our customers that their money can make a difference and that Nordea will with its financial position lead the change and contribute to a better world”

3.5 Ethical Considerations During the collection of data, the authors have considered the ethical principles of doing

research presented by the Swedish Research Council. The principles consist of the information

requirement, the consent requirement, the confidentiality requirement and the usage

requirement (Vetenskapsrådet, 2002). The authors have thus emphasized that the respondents’

participation in the study is voluntary, and that they can end the interview at any time.

Furthermore, the respondents have been promised anonymity as much as it is possible

considering that the bank and the positions are stated. However, since it is difficult to give

complete information about the study without risking to affect its findings (Bryman & Bell,

2017), the authors have strived to find an appropriate balance when giving information

regarding the study to the respondents. Prior to all interviews, the respondents were informed

that the recorded and transcribed material would be treated confidentially by the authors. This

was accomplished since the material has solely been managed by the authors themselves and it

has only been used for the purpose of this thesis.

26

4. Sustainable Finance at Nordea

This section presents the empirical findings beginning with an introduction of the selected

case. Following, Nordea’s perception of sustainability and the underlying motives for

integrating sustainability is presented. Thereafter, the sustainability involvement is

emphasized, involving Nordea’s sustainability practices and products. Finally, the chapter

ends with a description of how sustainability is communicated to become legitimized.

4.1 Presenting Nordea and Group Sustainable Finance Nordea Bank Abp is the leading bank in the Nordic region with about 30 000 employees

(Nordea, 2019b). Nordea is a full-service bank divided into four business areas: Personal

Banking, Commercial and Business Banking, Wholesale Banking, and Asset and Wealth

Management. Through their different business areas, Nordea offers a broad range of expertise

and products to meet the specific needs of private-, corporate- and institutional customers. More

particularly, Nordea’s Personal Banking has the largest customer base in the Nordic region with

about 9 million household customers. The second business area, Commercial and Business

Banking, serves, advices and partners with corporate customers by covering their business

needs through e.g. payments, cash management and financial solutions. The third business area,

Nordea Wholesale Banking, provides financial solutions to the biggest corporate- and

institutional customers. Lastly, Asset and Wealth Management offers investment, savings and

pensions solutions to individuals and institutional investors (ibid).

Group Sustainable Finance (GSF) is responsible for setting the sustainability agenda for Nordea

Group and is a Nordic team that consists of 25 people. The team works towards all business

areas where they collaborate with each business area to drive and integrate sustainability

throughout Nordea’s organization. Ultimately, GSF sets the strategic sustainability direction

and targets while also supporting business areas and group functions in the implementation

process (Nordea, 2019c).

“We [GSF] are a group function that are responsible for Nordea’s sustainability

involvement by setting the sustainability agenda and driving the sustainability

work”

27

Consequently, GSF has an influential role in forming how Nordea should approach

sustainability issues as well as what sustainability practices the bank should develop and

prioritize.

4.2 Nordea’s Perception of Sustainability When exploring the perception of sustainability, the respondents highlight that sustainability is