Monetary Theory and Policy Graphs David L. Kelly Department of Economics University of Miami Box 248126 Coral Gables, FL 33134 [email protected] First Version: Spring 2011

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Monetary Theory and PolicyGraphs

David L. Kelly

Department of EconomicsUniversity of Miami

Box 248126Coral Gables, FL 33134

First Version: Spring 2011

I Introduction

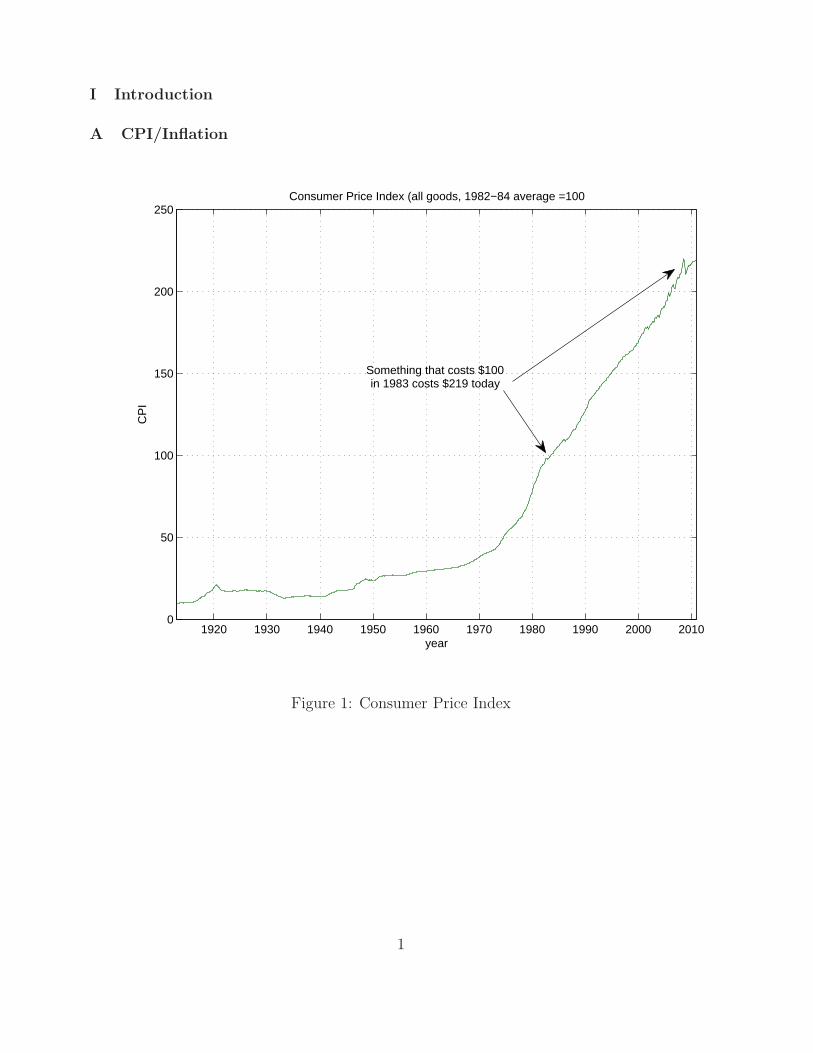

A CPI/Inflation

1920 1930 1940 1950 1960 1970 1980 1990 2000 20100

50

100

150

200

250

year

CP

I

Consumer Price Index (all goods, 1982−84 average =100

Something that costs $100in 1983 costs $219 today

Figure 1: Consumer Price Index

1

1920 1930 1940 1950 1960 1970 1980 1990 2000 2010−20

−15

−10

−5

0

5

10

15

20

25

year

cpi i

nfla

tion

CPI Inflation

1970s oil crises

Great Moderation

Deflation duringGreat Depression

Figure 2: Consumer Price Index Inflation

2

1930 1940 1950 1960 1970 1980 1990 2000 20100

200

400

600

800

1000

1200

1400

1600

1800

2000

year

M1

M1 over time

Little growthbefore WWII

Postwar Expansion

Current ExpansionBy the FED

Figure 3: M1

3

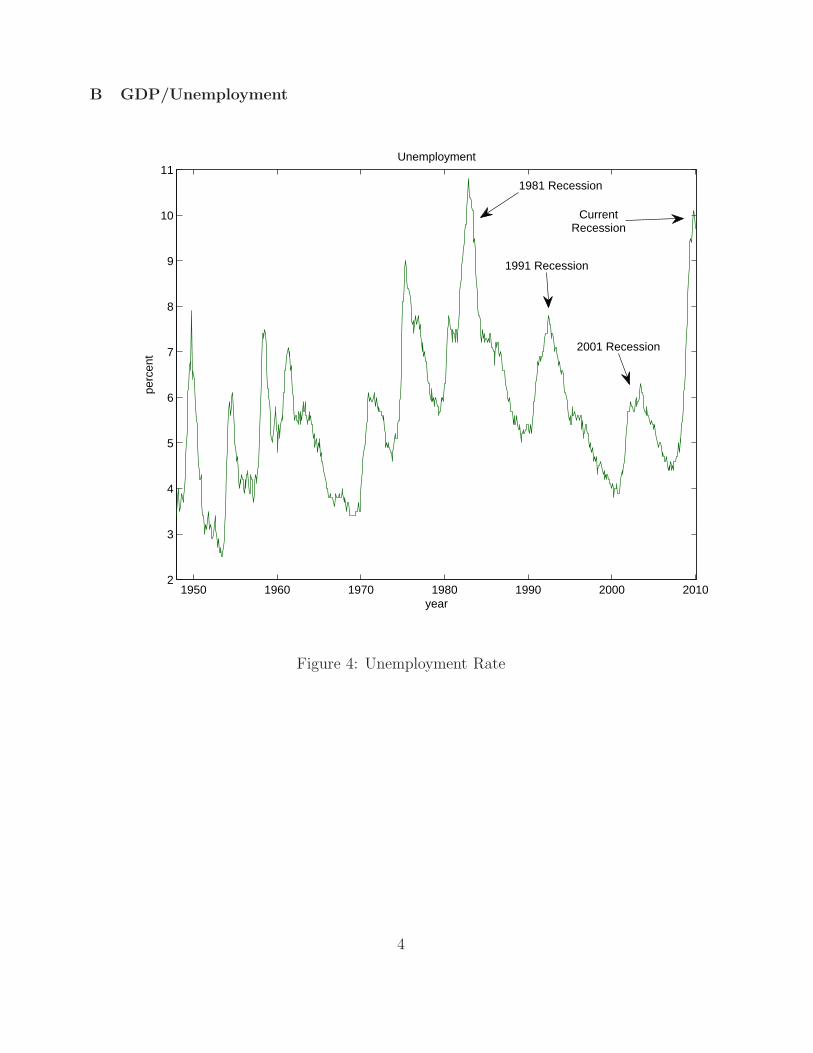

B GDP/Unemployment

1950 1960 1970 1980 1990 2000 20102

3

4

5

6

7

8

9

10

11

year

perc

ent

Unemployment

1981 Recession

1991 Recession

2001 Recession

CurrentRecession

Figure 4: Unemployment Rate

4

1950 1960 1970 1980 1990 2000 20100

2000

4000

6000

8000

10000

12000

14000

year

Bill

ions

of d

olla

rs

Real GDP 2005 chained dollars

1991 recession

2001 recession

current recession

Figure 5: Real GDP

5

2 3 4 5 6 7 8 9 10 11−4

−2

0

2

4

6

8

10

12

14

u

π

Shifting Phillips Curve

Before 19701970−31974−821982−961997+

Figure 6: Inflation and Unemployment: The shifting Phillips Curve

6

1980 1982 1985 1987 1990 1992 1995 1997 2000 2002 2005 2007−5

0

5

10

15

20

25

year

R

Taylor Rule vs Actual FED Funds

recent deviations from Taylor rule

Taylor RuleActual FED Funds

Figure 7: The Taylor Rule

7

C Recessions

0 5 10 15−6

−4

−2

0

2

4

6

8

10

12

14

Quarters after GDP peaked

Real Gross Domestic Product (GDP): last 4 recessions. Percent change from previous peak

1981−821990−9120012008−2009

Figure 8: RGDP: Last 4 recessions

8

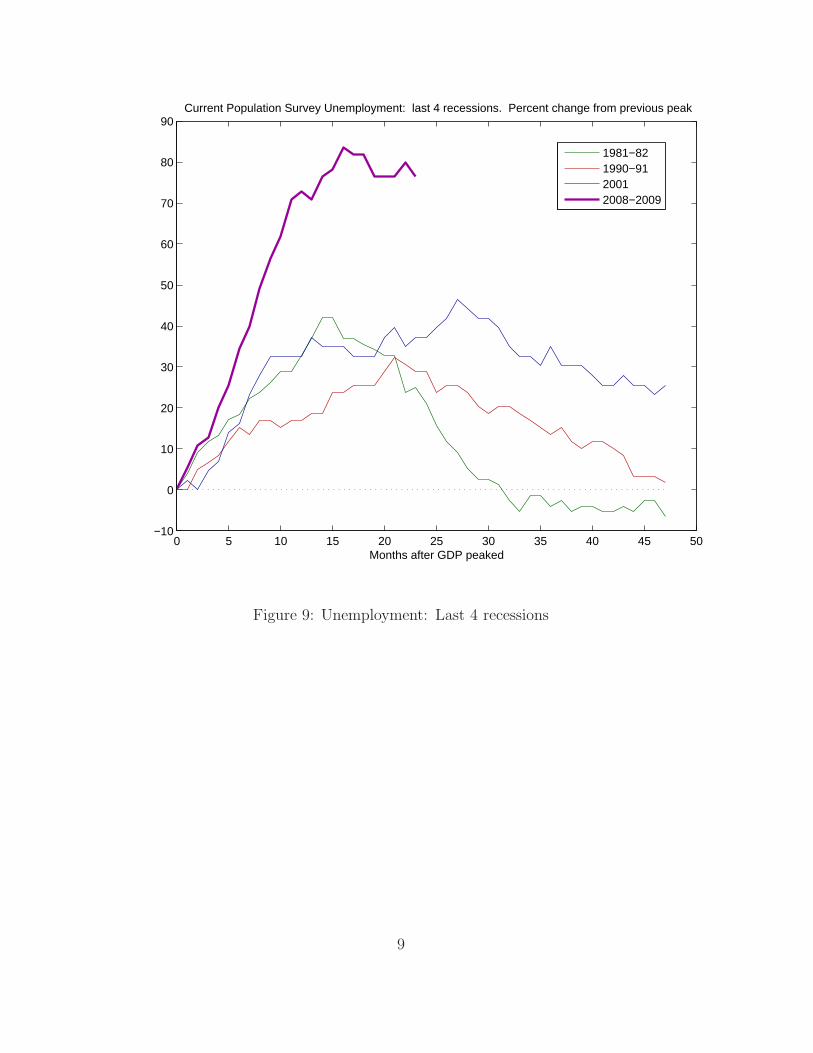

0 5 10 15 20 25 30 35 40 45 50−10

0

10

20

30

40

50

60

70

80

90

Months after GDP peaked

Current Population Survey Unemployment: last 4 recessions. Percent change from previous peak

1981−821990−9120012008−2009

Figure 9: Unemployment: Last 4 recessions

9

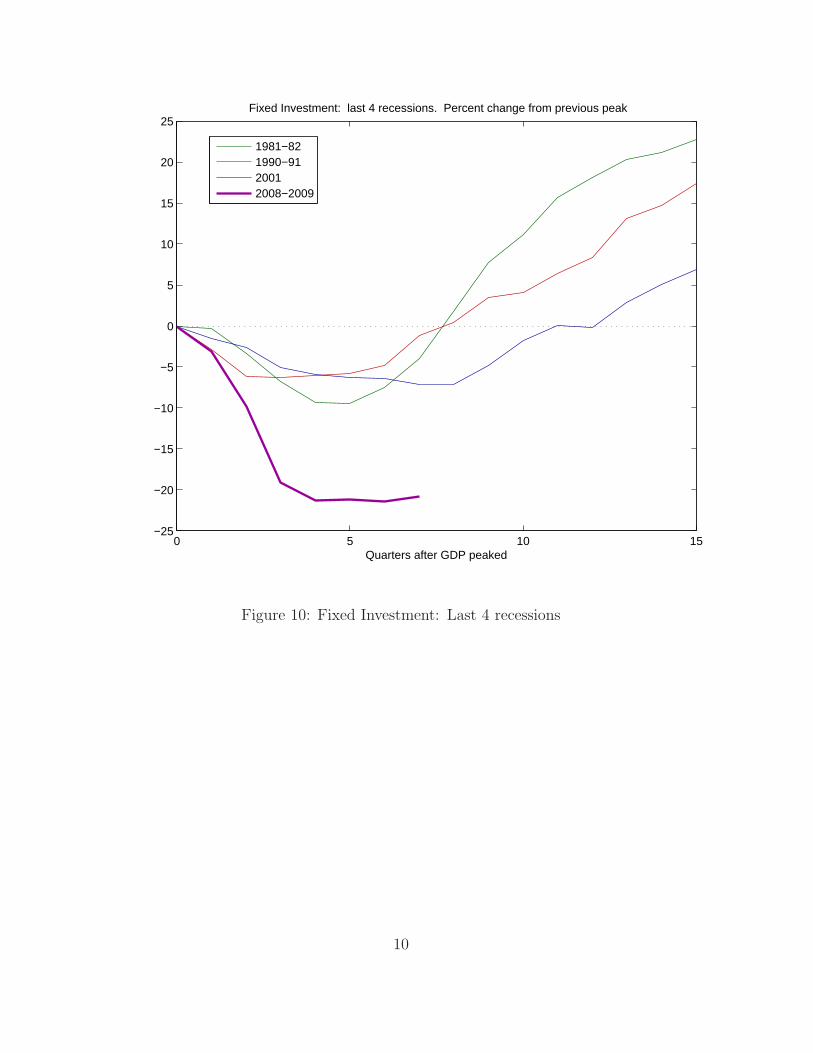

0 5 10 15−25

−20

−15

−10

−5

0

5

10

15

20

25

Quarters after GDP peaked

Fixed Investment: last 4 recessions. Percent change from previous peak

1981−821990−9120012008−2009

Figure 10: Fixed Investment: Last 4 recessions

10

0 5 10 15−30

−20

−10

0

10

20

30

40

Quarters after GDP peaked

Residential Investment: last 4 recessions. Percent change from previous peak

1981−821990−9120012008−2009

Figure 11: Residential Investment: Last 4 recessions

11

II Money

A Measures of Money

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 20100

1000

2000

3000

4000

5000

6000

7000

8000

9000

Year

Bill

ions

of d

olla

rs

M1 and M2, Seasonally Adjusted, Over Time

M1M2

Figure 12: M1 and M2 over time.

12

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 20102

2.5

3

3.5

4

4.5

5

5.5

6

Year

Bill

ions

of D

olla

rs

M2/M1, Seasonally Adjusted, Over Time

M2/M1 Linear Trend

High NominalInterest Rates

Low NominalInterest Rates

Figure 13: Ratio of M2 to M1 over time. Deregulation and technological advances result inhouseholds shifting to M2. But decisions to hold M1 versus M2 are closely related to realinterest rates and inflation.

13

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 20100

200

400

600

800

1000

1200

1400

1600

1800

2000

Year

H

Monetary Base, Not Seasonally Adjusted

Figure 14: Monetary Base Over Time. The monetary base more than doubled during thecrises.

14

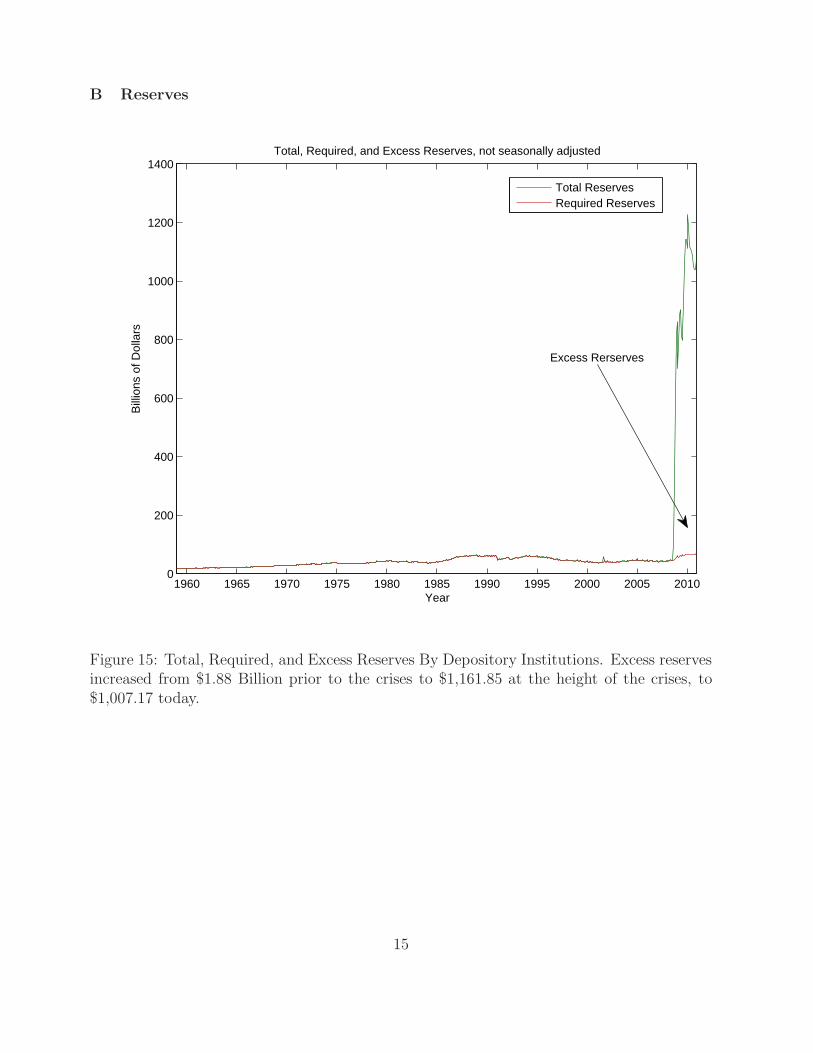

B Reserves

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 20100

200

400

600

800

1000

1200

1400

Year

Bill

ions

of D

olla

rsTotal, Required, and Excess Reserves, not seasonally adjusted

Total ReservesRequired Reserves

Excess Rerserves

Figure 15: Total, Required, and Excess Reserves By Depository Institutions. Excess reservesincreased from $1.88 Billion prior to the crises to $1,161.85 at the height of the crises, to$1,007.17 today.

15

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

40

50

60

70

80

90

100

Year

Bill

ions

of D

olla

rs

Total, Required, and Excess Reserves, not seasonally adjusted

Total ReservesRequired Reserves

Excess Reserves

Figure 16: Total, Required, and Excess Reserves since 1990.

16

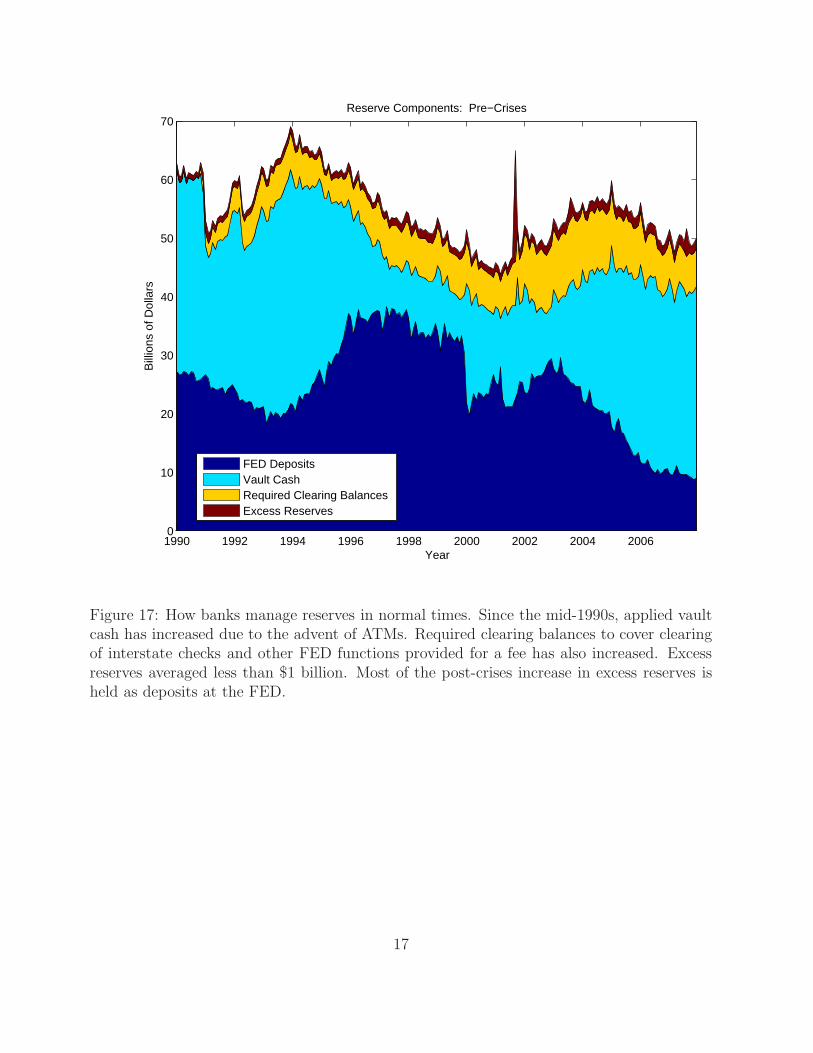

1990 1992 1994 1996 1998 2000 2002 2004 20060

10

20

30

40

50

60

70

Year

Bill

ions

of D

olla

rs

Reserve Components: Pre−Crises

FED DepositsVault CashRequired Clearing BalancesExcess Reserves

Figure 17: How banks manage reserves in normal times. Since the mid-1990s, applied vaultcash has increased due to the advent of ATMs. Required clearing balances to cover clearingof interstate checks and other FED functions provided for a fee has also increased. Excessreserves averaged less than $1 billion. Most of the post-crises increase in excess reserves isheld as deposits at the FED.

17

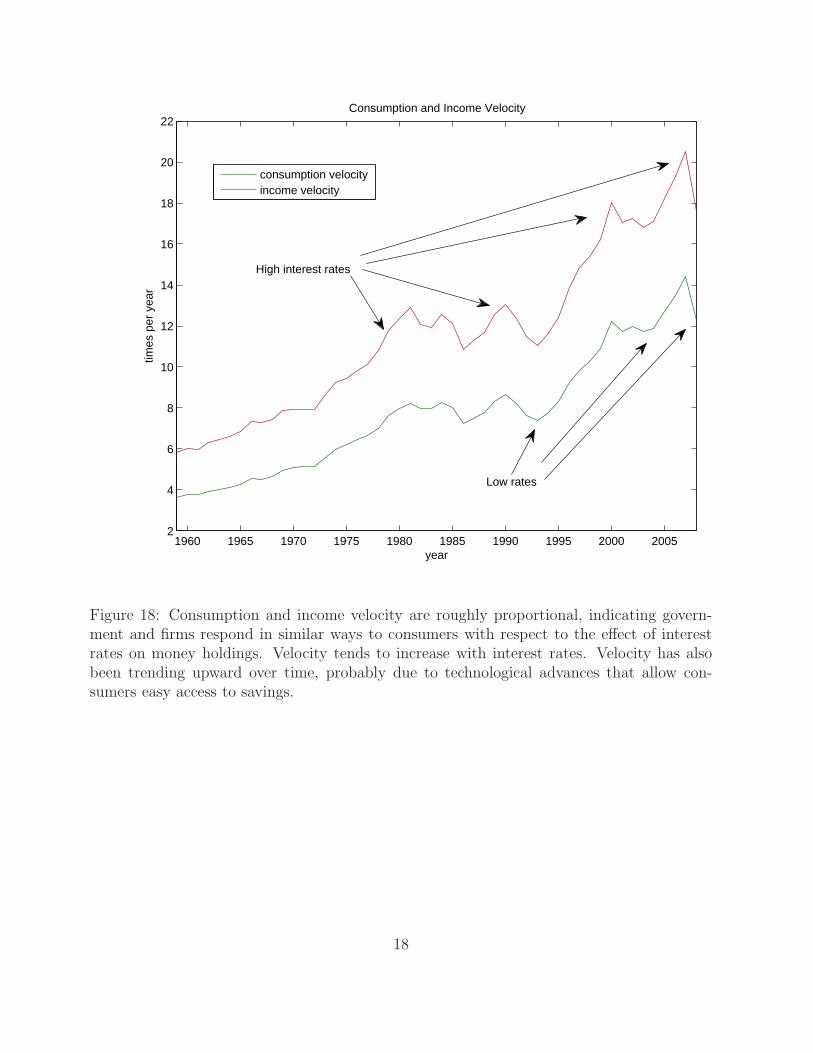

1960 1965 1970 1975 1980 1985 1990 1995 2000 20052

4

6

8

10

12

14

16

18

20

22

year

times

per

yea

r

Consumption and Income Velocity

consumption velocityincome velocity

High interest rates

Low rates

Figure 18: Consumption and income velocity are roughly proportional, indicating govern-ment and firms respond in similar ways to consumers with respect to the effect of interestrates on money holdings. Velocity tends to increase with interest rates. Velocity has alsobeen trending upward over time, probably due to technological advances that allow con-sumers easy access to savings.

18

III Phillips Curve

Figure 19: Original Phillips Curve.

19

Y∆

π

0

6162

63 6465

6667

68

69

BoomsRecessions

Figure 20: Original Phillips Curve using GDP.

20

Figure 21: Inflation and long run growth. Graph is Figure (1) from Bruno, M. and WilliamEasterly “Inflation Crises and Long Run Growth,” Journal of Monetary Economics, vol. 41(February 1998): pp. 3-26.

21

−3 −2 −1 0 1 2 3 4−1

0

1

2

3

4

5US Phillips Curve: 1960 − 1998

∆ Y

π

Figure 22: US Phillips Curve: more time periods.

22

2 3 4 5 6 7 8 9 10 11−4

−2

0

2

4

6

8

10

12

14

u

π

Shifting Phillips Curve

Before 19701970−31974−821982−961997+

Figure 23: US Phillips Curve.

23

IV Implementation

Jan60 Jan70 Jan80 Jan90 Jan00 Jan100

2

4

6

8

10

12

14

16

18

20

Date

perc

ent

Federal Funds Rate

Target H

Target R

Target E

Figure 24: Federal Funds Rate. When the FED targets H , volatility in R increases. Whenthe FED targets the FED funds rate, volatility in R reduces. Remaining volatility in theFED funds rate is due to frequent adjustments of the target.

24

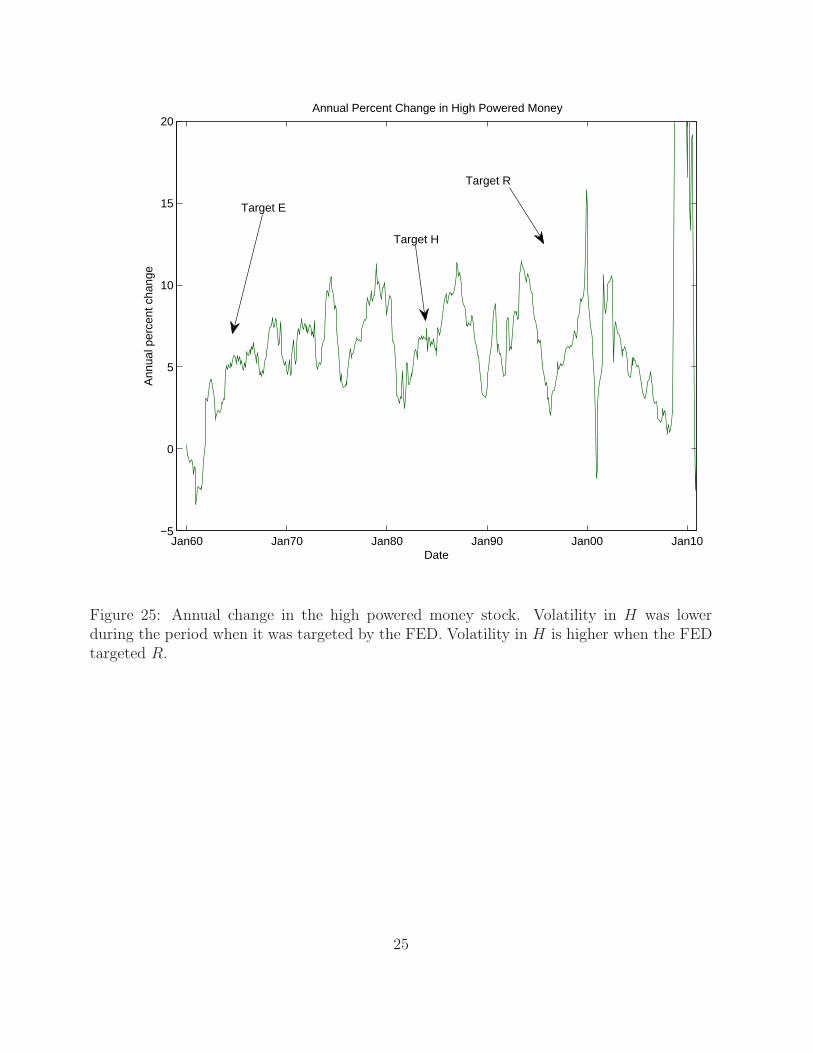

Jan60 Jan70 Jan80 Jan90 Jan00 Jan10−5

0

5

10

15

20

Date

Ann

ual p

erce

nt c

hang

e

Annual Percent Change in High Powered Money

Target H

Target R

Target E

Figure 25: Annual change in the high powered money stock. Volatility in H was lowerduring the period when it was targeted by the FED. Volatility in H is higher when the FEDtargeted R.

25

Related Documents