MÖBEL WALTHER ANNUAL REPORT 2000

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

M Ö B E L W A L T H E R A N N U A L R E P O R T

2 0 0 0

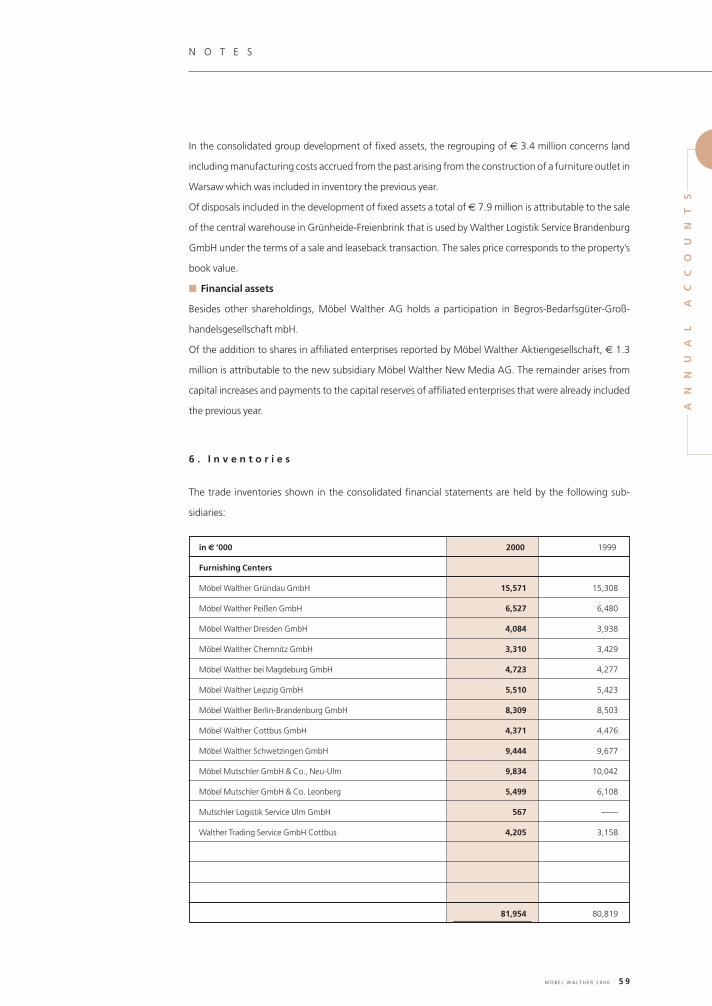

MÖ

BE

LW

AL

TH

ER

AG

AN

NU

AL

RE

PO

RT

20

00

033800_WA_English_Umschlag 16.05.2001 11:50 Uhr Seite 1

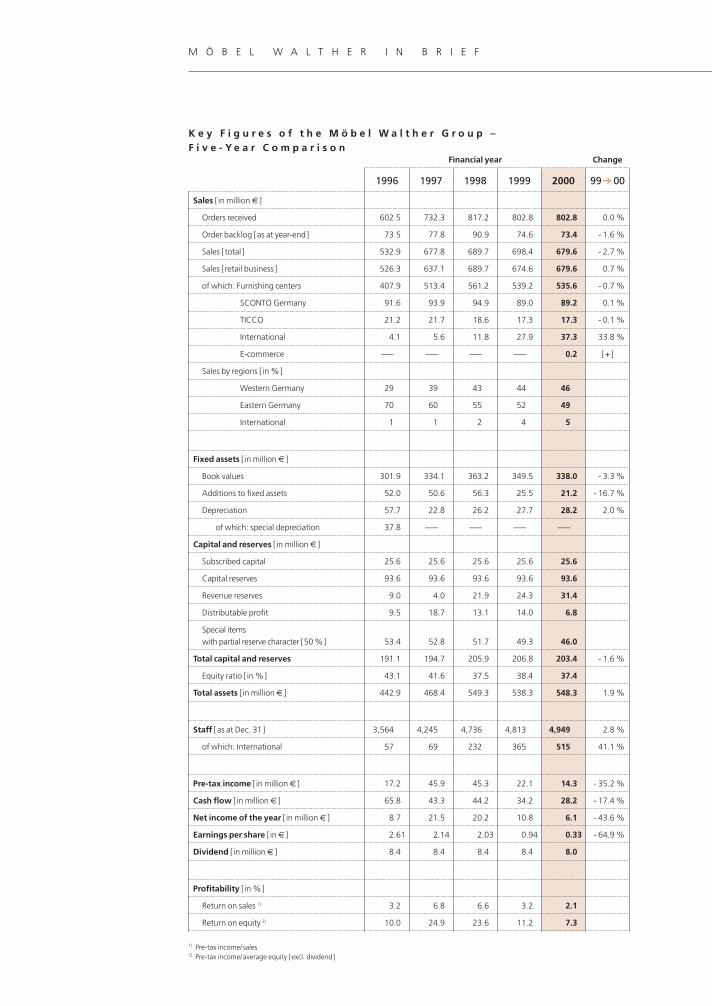

K e y F i g u r e s o f t h e M ö b e l W a l t h e r G r o u p –F i v e - Y e a r C o m p a r i s o n

Financial year Change

Sales [ in million € ]

Orders received 602.5 732.3 817.2 802.8 802.8 0.0 %

Order backlog [as at year-end] 73.5 77.8 90.9 74.6 73.4 - 1.6 %

Sales [ total ] 532.9 677.8 689.7 698.4 679.6 - 2.7 %

Sales [ retail business ] 526.3 637.1 689.7 674.6 679.6 0.7 %

of which: Furnishing centers 407.9 513.4 561.2 539.2 535.6 - 0.7 %

SCONTO Germany 91.6 93.9 94.9 89.0 89.2 0.1 %

TICCO 21.2 21.7 18.6 17.3 17.3 - 0.1 %

International 4.1 5.6 11.8 27.9 37.3 33.8 %

E-commerce ––– ––– ––– ––– 0.2 [+ ]

Sales by regions [ in %]

Western Germany 29 39 43 44 46

Eastern Germany 70 60 55 52 49

International 1 1 2 4 5

Fixed assets [ in million € ]

Book values 301.9 334.1 363.2 349.5 338.0 - 3.3 %

Additions to fixed assets 52.0 50.6 56.3 25.5 21.2 - 16.7 %

Depreciation 57.7 22.8 26.2 27.7 28.2 2.0 %

of which: special depreciation 37.8 ––– ––– ––– –––

Capital and reserves [ in million € ]

Subscribed capital 25.6 25.6 25.6 25.6 25.6

Capital reserves 93.6 93.6 93.6 93.6 93.6

Revenue reserves 9.0 4.0 21.9 24.3 31.4

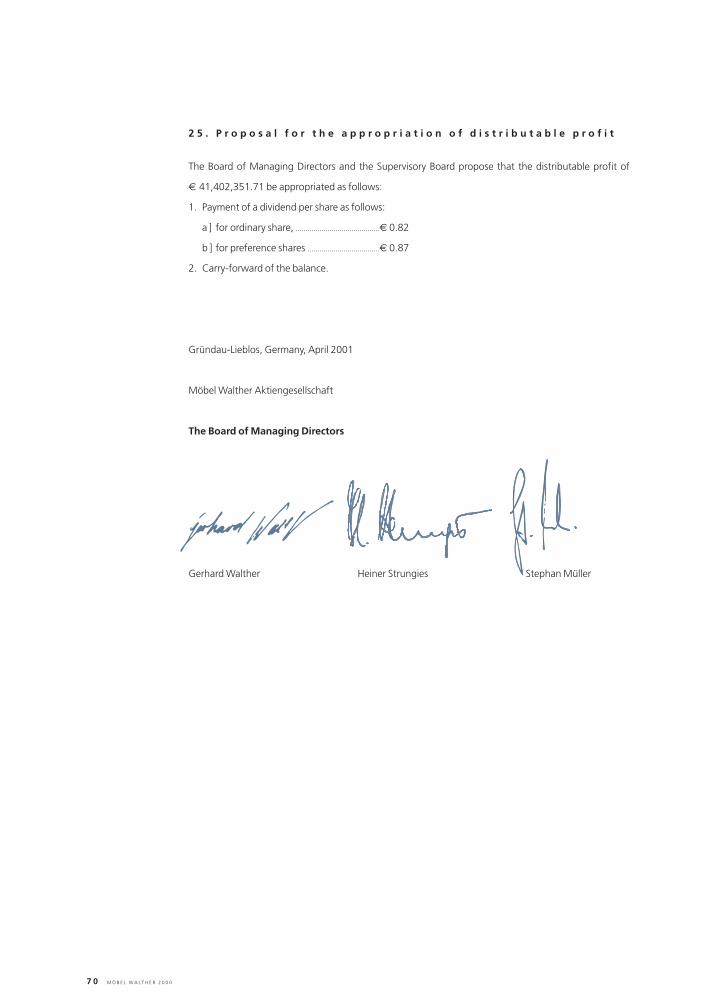

Distributable profit 9.5 18.7 13.1 14.0 6.8

Special items with partial reserve character [50 %] 53.4 52.8 51.7 49.3 46.0

Total capital and reserves 191.1 194.7 205.9 206.8 203.4 - 1.6 %

Equity ratio [ in %] 43.1 41.6 37.5 38.4 37.4

Total assets [ in million € ] 442.9 468.4 549.3 538.3 548.3 1.9 %

Staff [as at Dec. 31] 3,564 4,245 4,736 4,813 4,949 2.8 %

of which: International 57 69 232 365 515 41.1 %

Pre-tax income [ in million € ] 17.2 45.9 45.3 22.1 14.3 - 35.2 %

Cash flow [ in million € ] 65.8 43.3 44.2 34.2 28.2 - 17.4 %

Net income of the year [ in million € ] 8.7 21.5 20.2 10.8 6.1 - 43.6 %

Earnings per share [ in € ] 2.61 2.14 2.03 0.94 0.33 - 64.9 %

Dividend [ in million € ] 8.4 8.4 8.4 8.4 8.0

Profitability [ in %]

Return on sales 1] 3.2 6.8 6.6 3.2 2.1

Return on equity 2] 10.0 24.9 23.6 11.2 7.3

1996 1997 1998 1999 2000 99➔ 00

1] Pre-tax income/sales2] Pre-tax income/average equity [excl. dividend]

M Ö B E L W A L T H E R I N B R I E F

033800_WA_English_1RZ 16.05.2001 13:25 Uhr Seite 1

1990

127

1991

180

1992

237

1993

277

1994

409

1995

514

1996

602

1997

732

1998

817

1999

803

2000

803

million €

625

375

250

125

500

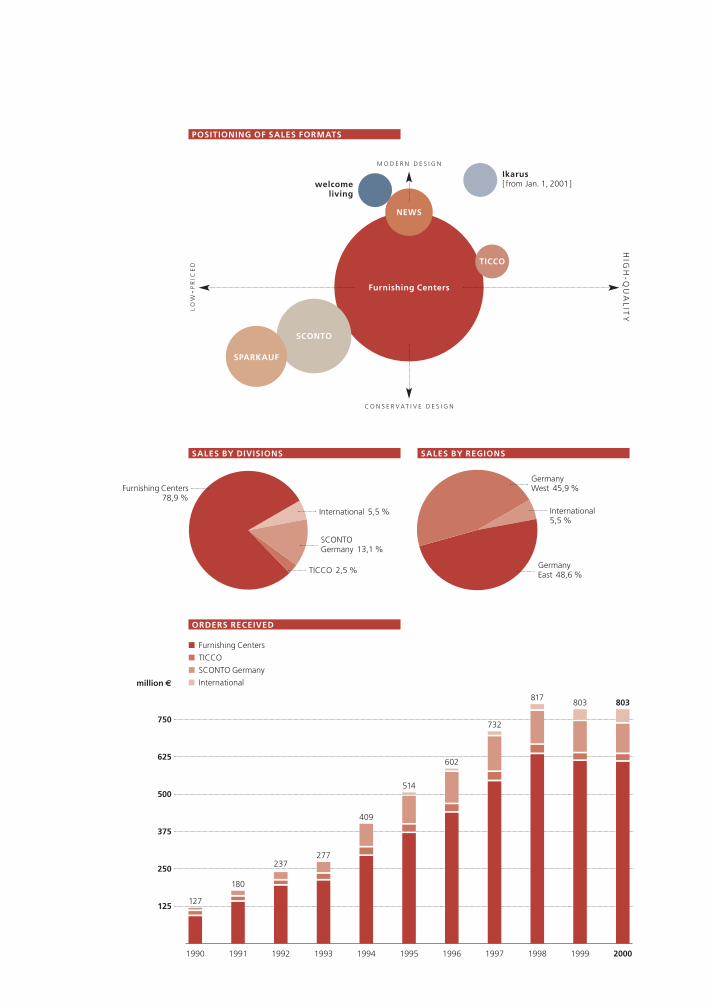

ORDERS RECEIVED

SALES BY DIVISIONS SALES BY REGIONS

POSITIONING OF SALES FORMATS

750

■ Furnishing Centers

■ TICCO

■ SCONTO Germany

■ International

HIG

H-Q

UA

LIT

Y

M O D E R N D E S I G N

NEWS

C O N S E R V A T I V E D E S I G N

LO

W-P

RIC

ED

SCONTO

Furnishing Centers

SPARKAUF

TICCO

welcome living

Ikarus[ from Jan. 1, 2001]

Germany East 48,6 %

GermanyWest 45,9 %

International5,5 %

Furnishing Centers 78,9 %

SCONTOGermany 13,1 %

International 5,5 %

TICCO 2,5 %

033800_WA_English_1RZ 16.05.2001 13:27 Uhr Seite 1

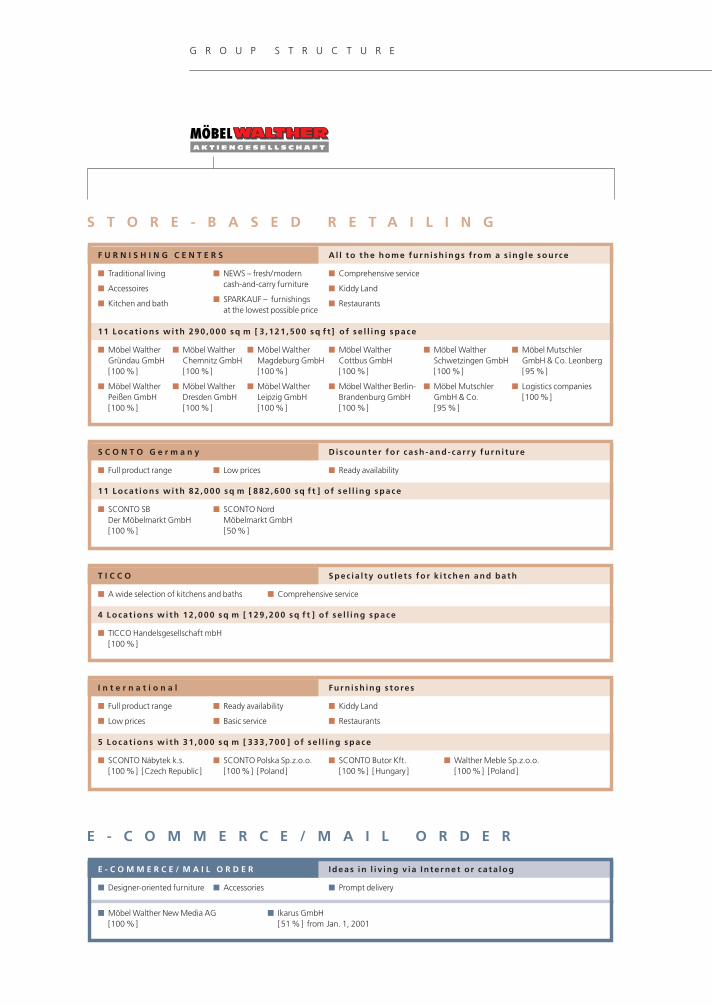

G R O U P S T R U C T U R E

S C O N T O G e r m a n y

11 Loca t ions w i th 82 ,000 sq m [ 882 ,600 sq f t ] o f se l l i ng space

D i s counte r fo r ca sh -and - ca r ry fu r n i tu re

■ SCONTO SB Der Möbelmarkt GmbH[100 %]

■ Full product range ■ Low prices ■ Ready availability

■ SCONTO NordMöbelmarkt GmbH[50 %]

T I C C O

4 Loca t ions w i th 12 ,000 sq m [ 129 ,200 sq f t ] o f se l l i ng space

Spec ia l ty out le t s fo r k i t chen and bath

■ TICCO Handelsgesellschaft mbH[100 %]

■ A wide selection of kitchens and baths ■ Comprehensive service

E - C O M M E R C E / M A I L O R D E R Ideas in l i v ing v ia In te r net o r ca ta log

■ Möbel Walther New Media AG[100 %]

■ Ikarus GmbH [51 %] from Jan. 1, 2001

■ Designer-oriented furniture ■ Accessories ■ Prompt delivery

I n t e r n a t i o n a l

5 Loca t ions w i th 31 ,000 sq m [ 333 ,700 ] o f se l l i ng space

Fur n i sh ing s to res

■ SCONTO Nábytek k.s.[100 %] [Czech Republic ]

■ SCONTO Polska Sp.z.o.o.[100 %] [Poland]

■ SCONTO Butor Kft.[100 %] [Hungary ]

■ Walther Meble Sp.z.o.o.[100 %] [Poland]

■ Full product range

■ Low prices

■ Ready availability

■ Basic service

■ Kiddy Land

■ Restaurants

S T O R E - B A S E D R E T A I L I N G

E - C O M M E R C E / M A I L O R D E R

F U R N I S H I N G C E N T E R S

11 Loca t ions w i th 290 ,000 sq m [ 3 ,121 ,500 sq f t ] o f se l l i ng space

A l l to the home fu r n i sh ings f rom a s ing le source

■ Möbel WaltherGründau GmbH [100 %]

■ Möbel WaltherPeißen GmbH [100 %]

■ Traditional living

■ Accessoires

■ Kitchen and bath

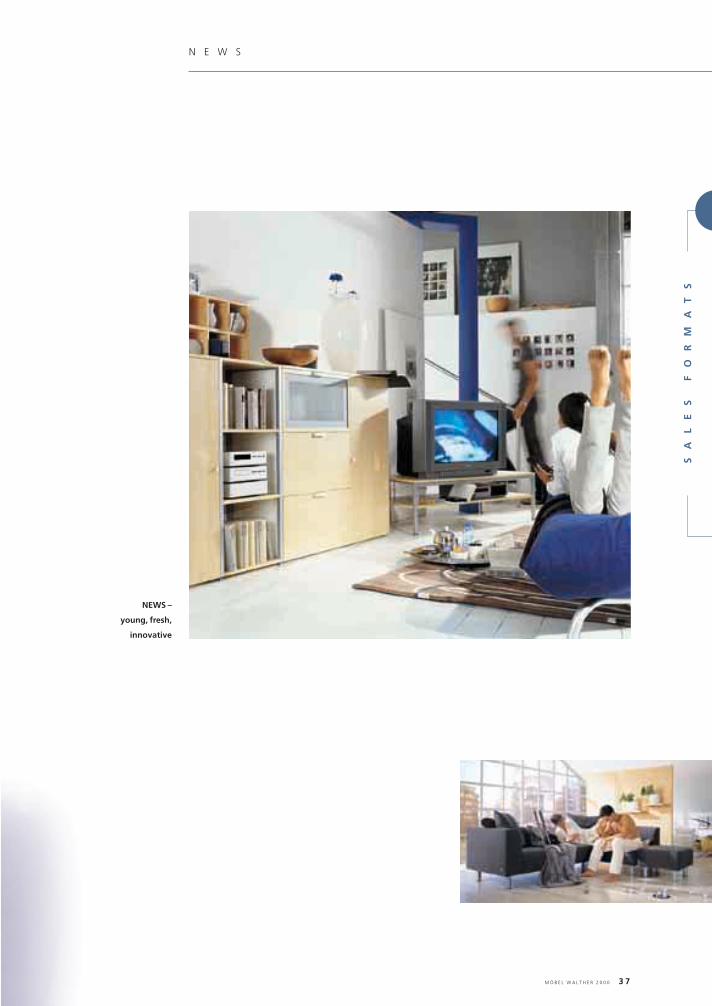

■ NEWS – fresh/moderncash-and-carry furniture

■ SPARKAUF – furnishingsat the lowest possible price

■ Comprehensive service

■ Kiddy Land

■ Restaurants

■ Möbel WaltherChemnitz GmbH [100 %]

■ Möbel WaltherDresden GmbH [100 %]

■ Möbel WaltherMagdeburg GmbH [100 %]

■ Möbel WaltherLeipzig GmbH [100 %]

■ Möbel WaltherCottbus GmbH [100 %]

■ Möbel Walther Berlin-Brandenburg GmbH [100 %]

■ Möbel WaltherSchwetzingen GmbH [100 %]

■ Möbel MutschlerGmbH & Co.[95 %]

■ Möbel Mutschler GmbH & Co. Leonberg[95 %]

■ Logistics companies[100 %]

033800_WA_English_Umschlag 16.05.2001 11:53 Uhr Seite 2

M ö b e l W a l t h e r f i t f o r t h e f u t u r e

Consumer behavior is undergoing change. For today’s customers, all

options are open. Individuality is their highest priority. Moreover, con-

sumers seek »convenience«- all things that make life comfortable and

pleasant.

Retail strategies must be adapted to this change in customer behavior.

Retailing is on the move. And we are moving with the times by shifting

our focus to new directions:

■ We are addressing our target groups even more purposefully with

new sales formats and changes in existing marketing channels.

■ Our new range of services makes buying even simpler.

■ We are acquiring new customers by penetrating new regions.

In this annual report, we wish to inform you of our strategies and mea-

sures for securing the company’s future in a changing retailing environ-

ment.

M Ö B E L W A L T H E R 2 0 0 0 1

033800_WA_English_1RZ 16.05.2001 11:19 Uhr Seite 1

To our Shareholders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

The Möbel Walther Share . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

Business Environment . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

Business Development . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

Profit & Dividend . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Investments & Finance . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Employees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Outlook & Strategy . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Risik Report . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

Furnishing Centers . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

NEWS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

Discount . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

Kitchen & Bath . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

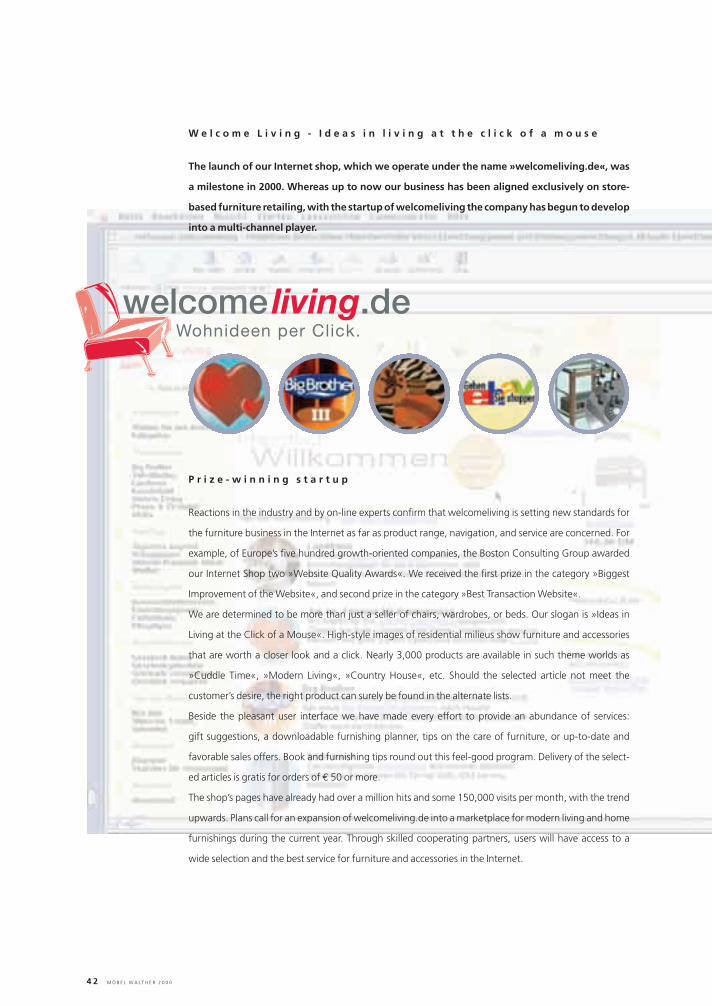

Welcome Living . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

Service & Logistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

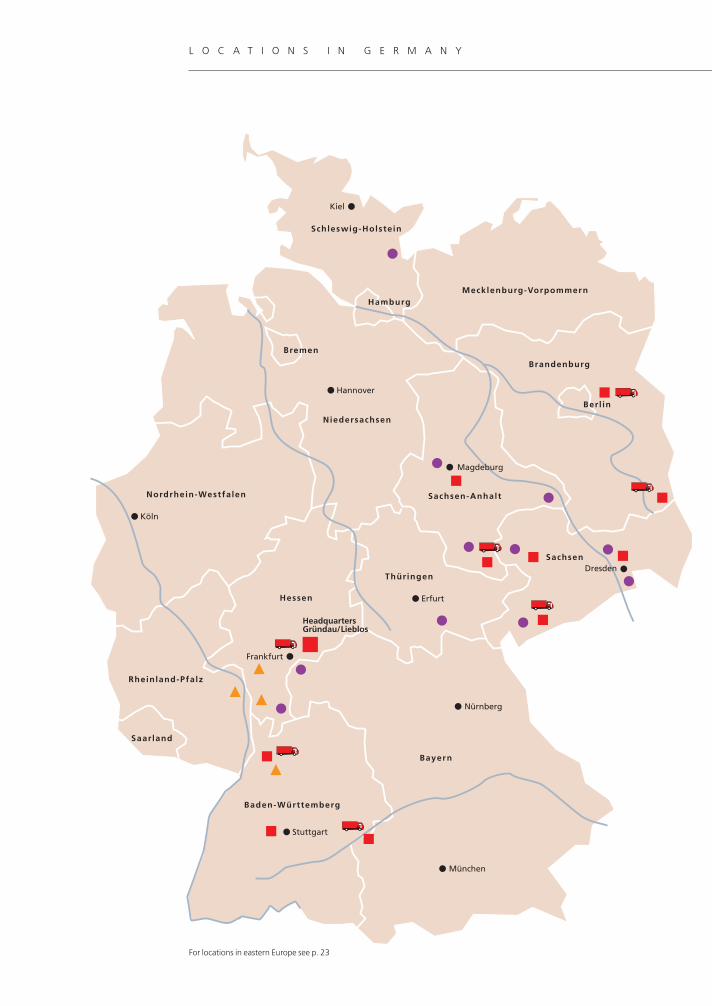

Locations in Germany . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 71

Management Report 2000

Sales Formats

Further Information

Annual Accounts 2000

2 M Ö B E L W A L T H E R 2 0 0 0

033800_WA_English_1RZ 16.05.2001 13:32 Uhr Seite 2

M A N A G E M E N T B O A R D

Gerhard Walther

Gründau-Lieblos, * 1949

Chairman of the

Board of Managing Directors

since 1986

Corporate development, logistics,

organization, specialty outlets,

and purchasing

Stephan Müller

Linsengericht, * 1964

Member of the

Board of Managing Directors

since 1997

Furnishing centers

Heiner Strungies

Bruchköbel, * 1947

Member of the

Board of Managing Directors

since 1986

Controlling, finance, and human

resources

from left to right

M Ö B E L W A L T H E R 2 0 0 0 3

033800_WA_English_1RZ 16.05.2001 11:19 Uhr Seite 3

4 M Ö B E L W A L T H E R 2 0 0 0

Your company is experiencing a process of rapid change. The business environ-

ment is changing. We are moving with the times in order to take advantage of

future opportunities for growth. This situation gives rise to many questions,

which I am pleased to answer here.

How has business developed over the last year?

There is no question that the way in which business developed in 2000 was

unsatisfactory all in all. Up to the end of the third quarter, figures were in line

with expectations. However, in the last quarter of 2000 demand for furniture –

as well as consumption in Germany as a whole – collapsed abruptly. As a

consequence, instead of the targeted 3% increase in sales, we experienced more or less

stagnation. At € 14.3 million, pre-tax profits were significantly below our targets and the

figures for the previous year. Nonetheless, we shall maintain the dividend level of the

previous year. With a dividend yield of 8.9 % for ordinary shares and 11.8 % for preference

shares [ including tax credit, based on the share price at the end of March 2001], we are

among the companies offering the highest dividend yields in Germany.

How would you evaluate the development of the share?

Many over-inflated share prices in the new economy have burst in recent months. In

contrast, our shares have demonstrated resilience: prices have even increased slightly over

the last year. Our performance was a little better than the SDAX. Admittedly, the level of

our shares is low. However, with shareholders‘ equity of more than € 200 million, strong

reserves in real estate, considerable profits and a high dividend yield, there is no doubt that

our market capitalization of € 121 million [March 2001] represents an undervaluation in

conventional terms.

Has the competitive situation changed over the last year?

We are still one of Germany‘s three biggest furniture retailers. Our sales figures have

developed in line with the industry in general. Naturally we have felt the comparatively

weaker demand in eastern Germany a little more than other companies who are only

active in the west. In eastern Europe, we have already achieved a very good and profi-

table position in the Czech Republic which we intend to expand further in the future. We

are only starting activities in Poland and Hungary.

Where does the new facility planned for Eschborn fit in?

Our Eschborn facility, located west of Frankfurt/Main and planned to open in 2002, is

certainly one of the best locations for furniture in Germany. This facility has been designed

as a theme center »World of Living« and concentrates on interior design – a unique

D e a r s h a r e h o l d e r s ,

033800_WA_English_1RZ 16.05.2001 11:19 Uhr Seite 4

M Ö B E L W A L T H E R 2 0 0 0 5

T O O U R S H A R E H O L D E R S

format for Germany. What makes this location so special is the fact that Möbel Walther

will not be the only furniture retailer in this center, but will share the space with other

suppliers whose business also lies in the area of home furnishings and interior design. The

wide range of products on offer will increase attractiveness, while also making it possible

to spread out the risk involved through additional income from rental.

What are your expectations for eastern Europe?

The neighboring countries of eastern Europe are markets with a solid future. Our early

entry into the market means that we have a perfect opportunity to participate in the re-

covery process in these countries. The success of our stores in the Czech Republic points

the way for future developments in Poland and Hungary.

Where do you see the strengths of Möbel Walther?

In the store-based retailing – this is and is set to remain the basis for our business – we are

well positioned in the most attractive market segments, while our comprehensive service

distinguishes us from the competition. The further development of Möbel Walther into a

multi-channel player [ store-based retailing, e-commerce and mail order ] will broaden the

company’s base, enabling us to address our customers through all sales channels. The

»World of Living« theme center in Eschborn near Frankfurt/Main is a business concept

that will provide good opportunities in the highly competitive environment of a stag-

nating market. Finally, we should emphasize our expertise in logistics. This also represents

an opportunity to become active in the growing market for logistical services in business

with third parties.

E-commerce: Is initial euphoria now at an end?

Yes, this is certainly true of companies whose business is based entirely on the Internet.

However, our structure is quite different because we have a strong base in store-based

business. The winners in e-commerce will be traditional retailers which expand their

activities from store-based business to include e-commerce. This has been our strategy.

We use the Internet to acquire new customer groups that would not have been available

to us through conventional business. To this are added synergy effects between the

various sales formats – particularly in the area of logistics. This is where we enjoy consider-

able competitive advantages over »pure« Internet dealers. Thus, e-commerce represents

a rational addition to our business activities with good prospects for the future.

Where do you identify risks?

Sales, and therefore profitability development in all business units, is largely determined

by the demand for furniture. We respond to this risk through the variety of our sales for-

033800_WA_English_1RZ 16.05.2001 11:19 Uhr Seite 5

6 M Ö B E L W A L T H E R 2 0 0 0

mats and increasing internationalization. The indicators for Germany point to stable mar-

ket development in the coming years. Interior design and home furnishings will continue

to enjoy a high profile. I believe that the risks involved in our international expansion can

be calculated. Our business in the Czech Republic is no longer in its infancy and is already

achieving good results. Prospects are also good in Poland and Hungary.

What is the intended path of Möbel Walther over the next five years?

We will further develop our market position in Germany and eastern Europe. Because of

its innovative concept, the new center in Eschborn will represent an important milestone

for business in Germany. For eastern Europe, we expect the share in consolidated sales to

treble to over 15 %. In the e-commerce/mail order sector we identify a sales potential

of approximately € 25 million in 2005. In addition, we will build up a new business field

in real estate in order to achieve much higher added value for our own property through

professional property management.

The way has been paved to a successful future.

Gerhard Walther, CEO

033800_WA_English_1RZ 16.05.2001 11:19 Uhr Seite 6

M Ö B E L W A L T H E R 2 0 0 0 7

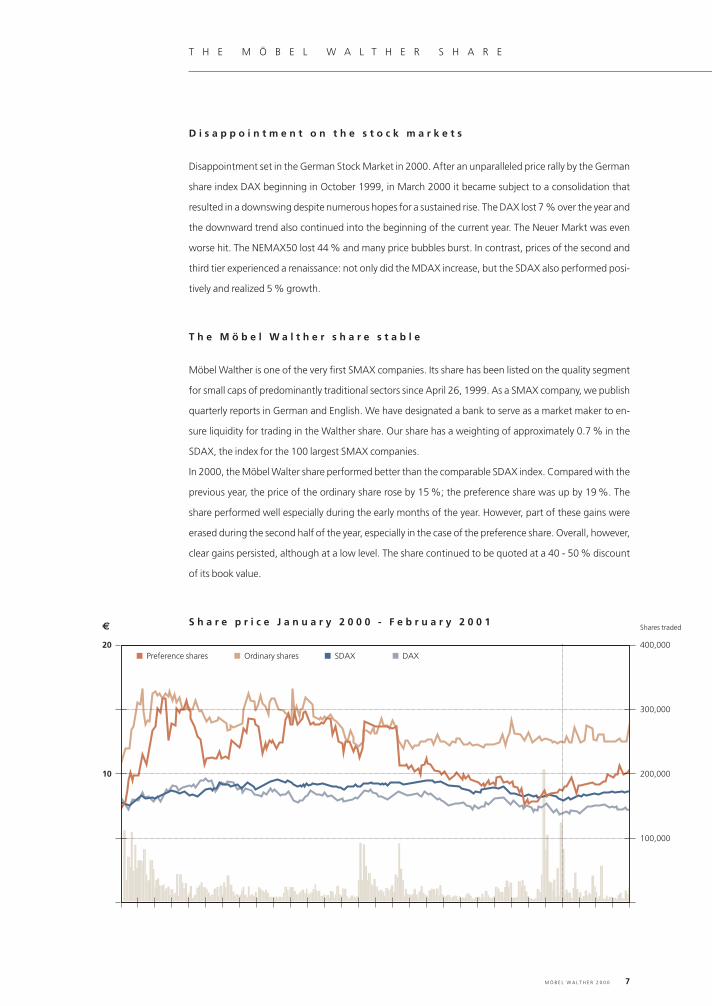

T H E M Ö B E L W A L T H E R S H A R E

S h a r e p r i c e J a n u a r y 2 0 0 0 - F e b r u a r y 2 0 0 1

20

10

400,000

300,000

200,000

100,000

€ Shares traded

■ Preference shares ■ Ordinary shares ■ DAX■ SDAX

Möbel Walther is one of the very first SMAX companies. Its share has been listed on the quality segment

for small caps of predominantly traditional sectors since April 26, 1999. As a SMAX company, we publish

quarterly reports in German and English. We have designated a bank to serve as a market maker to en-

sure liquidity for trading in the Walther share. Our share has a weighting of approximately 0.7 % in the

SDAX, the index for the 100 largest SMAX companies.

In 2000, the Möbel Walter share performed better than the comparable SDAX index. Compared with the

previous year, the price of the ordinary share rose by 15 %; the preference share was up by 19 %. The

share performed well especially during the early months of the year. However, part of these gains were

erased during the second half of the year, especially in the case of the preference share. Overall, however,

clear gains persisted, although at a low level. The share continued to be quoted at a 40 - 50 % discount

of its book value.

D i s a p p o i n t m e n t o n t h e s t o c k m a r k e t s

T h e M ö b e l W a l t h e r s h a r e s t a b l e

Disappointment set in the German Stock Market in 2000. After an unparalleled price rally by the German

share index DAX beginning in October 1999, in March 2000 it became subject to a consolidation that

resulted in a downswing despite numerous hopes for a sustained rise. The DAX lost 7 % over the year and

the downward trend also continued into the beginning of the current year. The Neuer Markt was even

worse hit. The NEMAX50 lost 44 % and many price bubbles burst. In contrast, prices of the second and

third tier experienced a renaissance: not only did the MDAX increase, but the SDAX also performed posi-

tively and realized 5 % growth.

033800_WA_English_1RZ 16.05.2001 11:19 Uhr Seite 7

8 M Ö B E L W A L T H E R 2 0 0 0

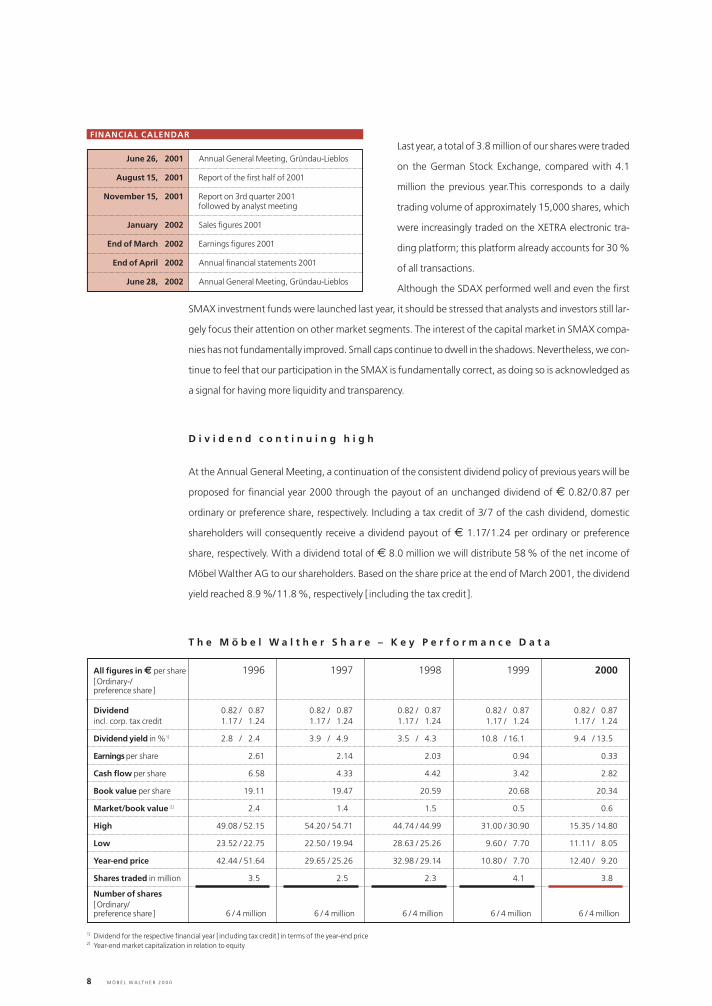

Last year, a total of 3.8 million of our shares were traded

on the German Stock Exchange, compared with 4.1

million the previous year.This corresponds to a daily

trading volume of approximately 15,000 shares, which

were increasingly traded on the XETRA electronic tra-

ding platform; this platform already accounts for 30 %

of all transactions.

Although the SDAX performed well and even the first

SMAX investment funds were launched last year, it should be stressed that analysts and investors still lar-

gely focus their attention on other market segments. The interest of the capital market in SMAX compa-

nies has not fundamentally improved. Small caps continue to dwell in the shadows. Nevertheless, we con-

tinue to feel that our participation in the SMAX is fundamentally correct, as doing so is acknowledged as

a signal for having more liquidity and transparency.

D i v i d e n d c o n t i n u i n g h i g h

At the Annual General Meeting, a continuation of the consistent dividend policy of previous years will be

proposed for financial year 2000 through the payout of an unchanged dividend of € 0.82/0.87 per

ordinary or preference share, respectively. Including a tax credit of 3/7 of the cash dividend, domestic

shareholders will consequently receive a dividend payout of € 1.17/1.24 per ordinary or preference

share, respectively. With a dividend total of € 8.0 million we will distribute 58 % of the net income of

Möbel Walther AG to our shareholders. Based on the share price at the end of March 2001, the dividend

yield reached 8.9 %/11.8 %, respectively [ including the tax credit ].

All figures in € per share 1996 1997 1998 1999 2000[Ordinary-/preference share ]

Number of shares [Ordinary/preference share ] 6 / 4 million 6 / 4 million 6 / 4 million 6 / 4 million 6 / 4 million

T h e M ö b e l W a l t h e r S h a r e – K e y P e r f o r m a n c e D a t a

1] Dividend for the respective financial year [ including tax credit ] in terms of the year-end price2] Year-end market capitalization in relation to equity

Dividend 0.82 / 0.87 0.82 / 0.87 0.82 / 0.87 0.82 / 0.87 0.82 / 0.87incl. corp. tax credit 1.17 / 1.24 1.17 / 1.24 1.17 / 1.24 1.17 / 1.24 1.17 / 1.24

Dividend yield in %1] 2.8 / 2.4 3.9 / 4.9 3.5 / 4.3 10.8 / 16.1 9.4 / 13.5

Earnings per share 2.61 2.14 2.03 0.94 0.33

Cash flow per share 6.58 4.33 4.42 3.42 2.82

Book value per share 19.11 19.47 20.59 20.68 20.34

Market/book value 2] 2.4 1.4 1.5 0.5 0.6

High 49.08 / 52.15 54.20 / 54.71 44.74 / 44.99 31.00 / 30.90 15.35 / 14.80

Low 23.52 / 22.75 22.50 / 19.94 28.63 / 25.26 9.60 / 7.70 11.11 / 8.05

Year-end price 42.44 / 51.64 29.65 / 25.26 32.98 / 29.14 10.80 / 7.70 12.40 / 9.20

Shares traded in million 3.5 2.5 2.3 4.1 3.8

June 26, 2001 Annual General Meeting, Gründau-Lieblos

August 15, 2001 Report of the first half of 2001

November 15, 2001 Report on 3rd quarter 2001 followed by analyst meeting

January 2002 Sales figures 2001

End of March 2002 Earnings figures 2001

End of April 2002 Annual financial statements 2001

June 28, 2002 Annual General Meeting, Gründau-Lieblos

FINANCIAL CALENDAR

033800_WA_English_1RZ 16.05.2001 11:19 Uhr Seite 8

M Ö B E L W A L T H E R 2 0 0 0 9

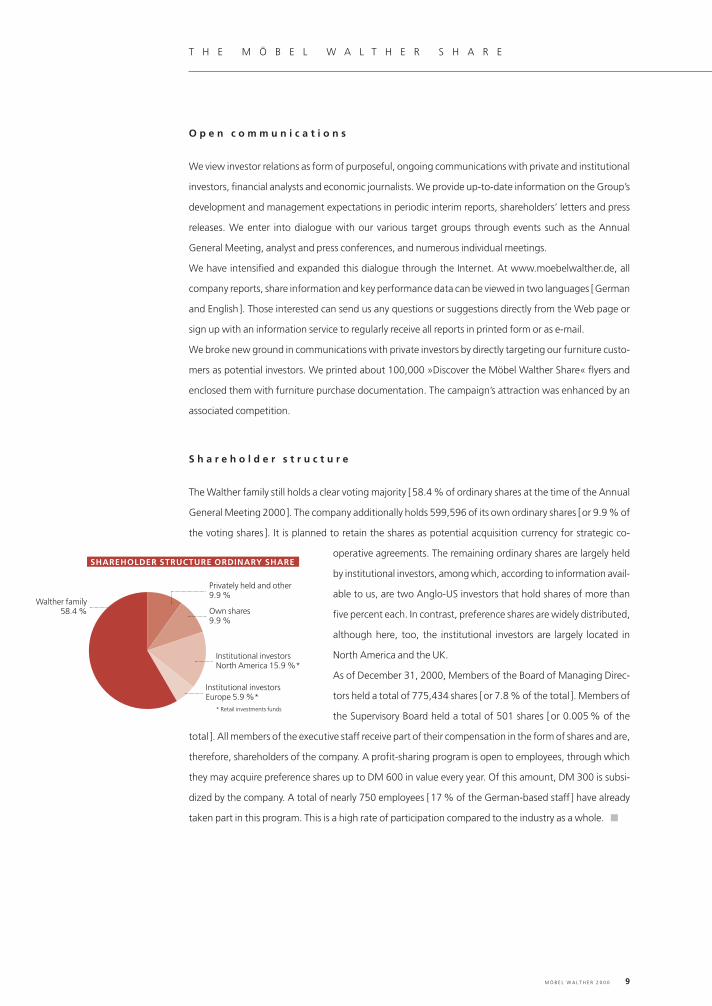

O p e n c o m m u n i c a t i o n s

We view investor relations as form of purposeful, ongoing communications with private and institutional

investors, financial analysts and economic journalists. We provide up-to-date information on the Group’s

development and management expectations in periodic interim reports, shareholders’ letters and press

releases. We enter into dialogue with our various target groups through events such as the Annual

General Meeting, analyst and press conferences, and numerous individual meetings.

We have intensified and expanded this dialogue through the Internet. At www.moebelwalther.de, all

company reports, share information and key performance data can be viewed in two languages [German

and English ]. Those interested can send us any questions or suggestions directly from the Web page or

sign up with an information service to regularly receive all reports in printed form or as e-mail.

We broke new ground in communications with private investors by directly targeting our furniture custo-

mers as potential investors. We printed about 100,000 »Discover the Möbel Walther Share« flyers and

enclosed them with furniture purchase documentation. The campaign’s attraction was enhanced by an

associated competition.

S h a r e h o l d e r s t r u c t u r e

The Walther family still holds a clear voting majority [58.4 % of ordinary shares at the time of the Annual

General Meeting 2000]. The company additionally holds 599,596 of its own ordinary shares [or 9.9 % of

the voting shares ]. It is planned to retain the shares as potential acquisition currency for strategic co-

operative agreements. The remaining ordinary shares are largely held

by institutional investors, among which, according to information avail-

able to us, are two Anglo-US investors that hold shares of more than

five percent each. In contrast, preference shares are widely distributed,

although here, too, the institutional investors are largely located in

North America and the UK.

As of December 31, 2000, Members of the Board of Managing Direc-

tors held a total of 775,434 shares [or 7.8 % of the total ]. Members of

the Supervisory Board held a total of 501 shares [or 0.005 % of the

total ]. All members of the executive staff receive part of their compensation in the form of shares and are,

therefore, shareholders of the company. A profit-sharing program is open to employees, through which

they may acquire preference shares up to DM 600 in value every year. Of this amount, DM 300 is subsi-

dized by the company. A total of nearly 750 employees [17 % of the German-based staff ] have already

taken part in this program. This is a high rate of participation compared to the industry as a whole. ■

SHAREHOLDER STRUCTURE ORDINARY SHARE

Walther family58.4 %

Institutional investorsNorth America 15.9 %*

Own shares9.9 %

Privately held and other9.9 %

Institutional investorsEurope 5.9 %*

* Retail investments funds

T H E M Ö B E L W A L T H E R S H A R E

033800_WA_English_1RZ 16.05.2001 11:19 Uhr Seite 9

1 0 M Ö B E L W A L T H E R 2 0 0 0

■ M A R K E T P E N E T R A T I O N I N H U N G A R Y

■ L A U N C H O F O N - L I N E S H O P

■ O P E R A T I N G S A L E S U P 0 . 7 %

■ F U R N I T U R E R E T A I L E R S W E A K

■ P R E - T A X P R O F I T A T € 1 4 . 3 M I L L I O N

■ C O N T I N U E D H I G H D I V I D E N D

R e t a i l i n g i m p r o v e s

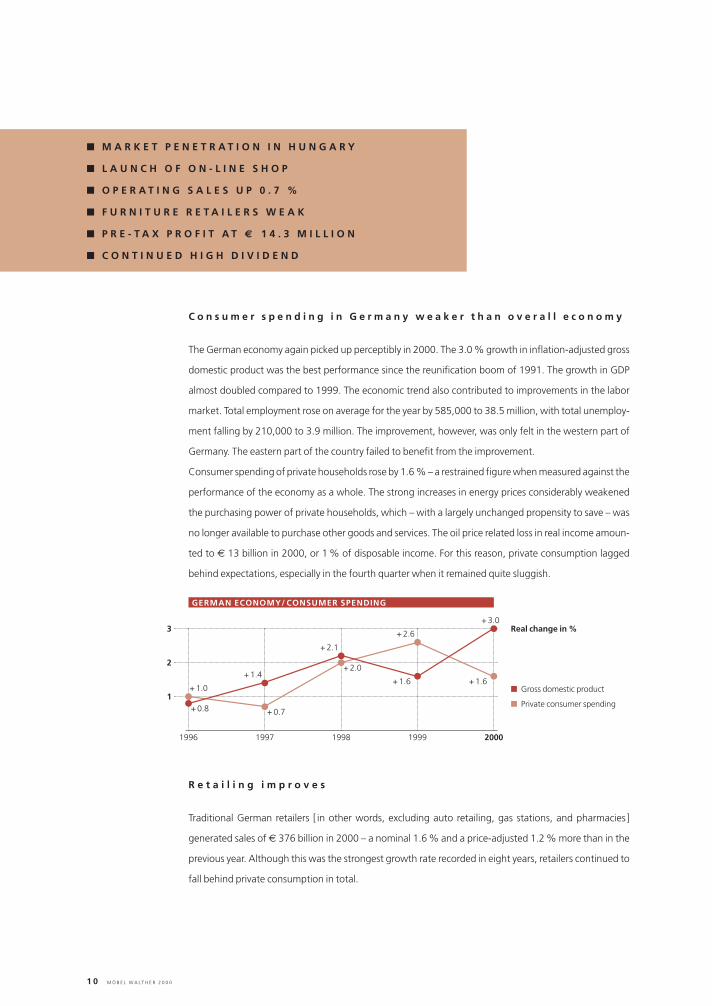

The German economy again picked up perceptibly in 2000. The 3.0 % growth in inflation-adjusted gross

domestic product was the best performance since the reunification boom of 1991. The growth in GDP

almost doubled compared to 1999. The economic trend also contributed to improvements in the labor

market. Total employment rose on average for the year by 585,000 to 38.5 million, with total unemploy-

ment falling by 210,000 to 3.9 million. The improvement, however, was only felt in the western part of

Germany. The eastern part of the country failed to benefit from the improvement.

Consumer spending of private households rose by 1.6 % – a restrained figure when measured against the

performance of the economy as a whole. The strong increases in energy prices considerably weakened

the purchasing power of private households, which – with a largely unchanged propensity to save – was

no longer available to purchase other goods and services. The oil price related loss in real income amoun-

ted to € 13 billion in 2000, or 1 % of disposable income. For this reason, private consumption lagged

behind expectations, especially in the fourth quarter when it remained quite sluggish.

C o n s u m e r s p e n d i n g i n G e r m a n y w e a k e r t h a n o v e r a l l e c o n o m y

Real change in %

■ Gross domestic product

■ Private consumer spending

1996 1997 1998 1999 2000

+ 0.8

+ 1.0

+ 0.7

+ 2.0

+ 2.6

+ 1.6+ 1.4

+ 2.1

+ 1.6

+ 3.0

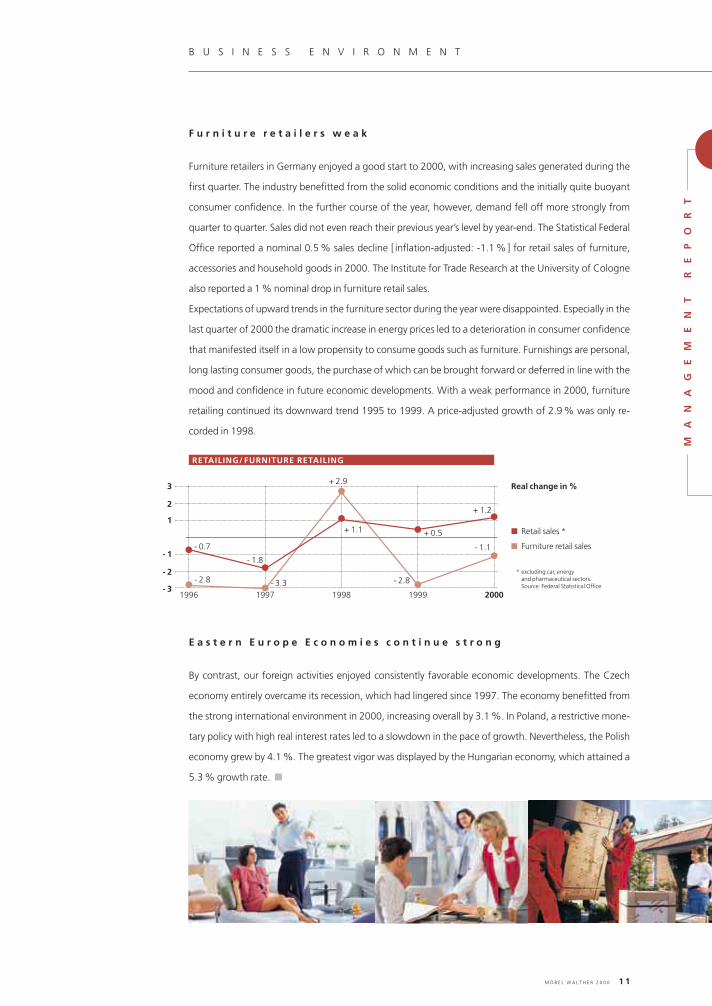

Traditional German retailers [ in other words, excluding auto retailing, gas stations, and pharmacies ]

generated sales of € 376 billion in 2000 – a nominal 1.6 % and a price-adjusted 1.2 % more than in the

previous year. Although this was the strongest growth rate recorded in eight years, retailers continued to

fall behind private consumption in total.

GERMAN ECONOMY/ CONSUMER SPENDING

1

2

3

033800_WA_English_1RZ 16.05.2001 11:19 Uhr Seite 10

M Ö B E L W A L T H E R 2 0 0 0 1 1

B U S I N E S S E N V I R O N M E N T

MA

NA

GE

ME

NT

R

EP

OR

T

E a s t e r n E u r o p e E c o n o m i e s c o n t i n u e s t r o n g

By contrast, our foreign activities enjoyed consistently favorable economic developments. The Czech

economy entirely overcame its recession, which had lingered since 1997. The economy benefitted from

the strong international environment in 2000, increasing overall by 3.1 %. In Poland, a restrictive mone-

tary policy with high real interest rates led to a slowdown in the pace of growth. Nevertheless, the Polish

economy grew by 4.1 %. The greatest vigor was displayed by the Hungarian economy, which attained a

5.3 % growth rate. ■

* excluding car, energy and pharmaceutical sectors.Source: Federal Statistical Office

Real change in %

■ Retail sales *

■ Furniture retail sales

1996 1997 1998 1999 2000

- 2.8 - 2.8

- 0.7

- 3.3

- 1.8

+ 1.1

- 1.1

+ 2.9

+ 0.5

+ 1.2

RETAILING/ FURNITURE RETAILING

- 1

1

3

2

- 2

- 3

F u r n i t u r e r e t a i l e r s w e a k

Furniture retailers in Germany enjoyed a good start to 2000, with increasing sales generated during the

first quarter. The industry benefitted from the solid economic conditions and the initially quite buoyant

consumer confidence. In the further course of the year, however, demand fell off more strongly from

quarter to quarter. Sales did not even reach their previous year’s level by year-end. The Statistical Federal

Office reported a nominal 0.5 % sales decline [ inflation-adjusted: -1.1 %] for retail sales of furniture,

accessories and household goods in 2000. The Institute for Trade Research at the University of Cologne

also reported a 1 % nominal drop in furniture retail sales.

Expectations of upward trends in the furniture sector during the year were disappointed. Especially in the

last quarter of 2000 the dramatic increase in energy prices led to a deterioration in consumer confidence

that manifested itself in a low propensity to consume goods such as furniture. Furnishings are personal,

long lasting consumer goods, the purchase of which can be brought forward or deferred in line with the

mood and confidence in future economic developments. With a weak performance in 2000, furniture

retailing continued its downward trend 1995 to 1999. A price-adjusted growth of 2.9 % was only re-

corded in 1998.

033800_WA_English_1RZ 16.05.2001 11:19 Uhr Seite 11

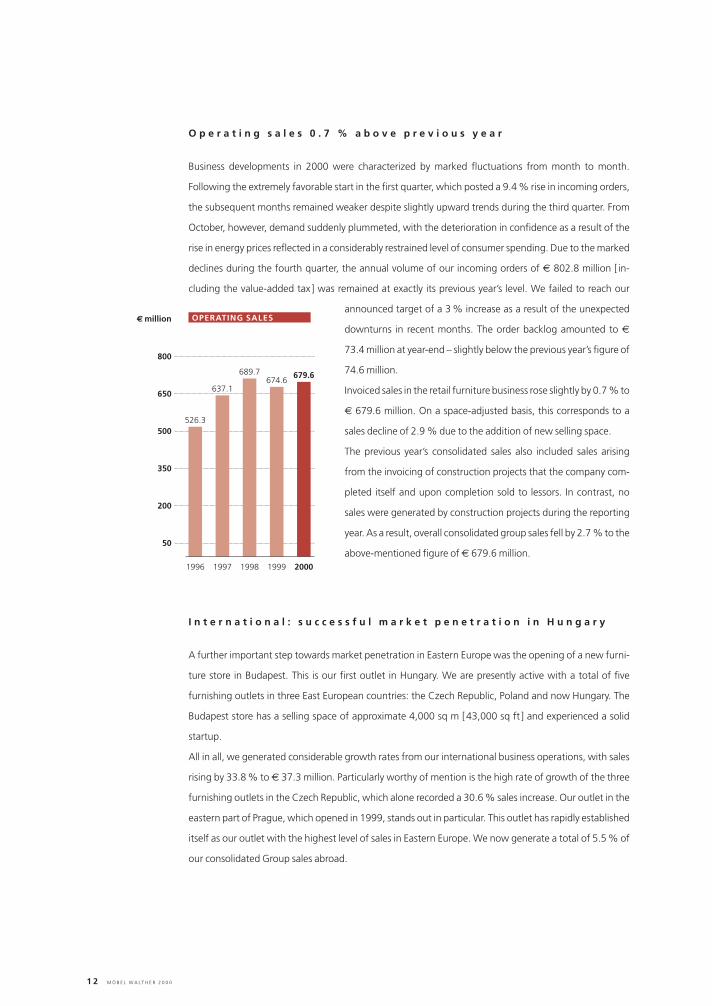

Business developments in 2000 were characterized by marked fluctuations from month to month.

Following the extremely favorable start in the first quarter, which posted a 9.4 % rise in incoming orders,

the subsequent months remained weaker despite slightly upward trends during the third quarter. From

October, however, demand suddenly plummeted, with the deterioration in confidence as a result of the

rise in energy prices reflected in a considerably restrained level of consumer spending. Due to the marked

declines during the fourth quarter, the annual volume of our incoming orders of € 802.8 million [ in-

cluding the value-added tax ] was remained at exactly its previous year’s level. We failed to reach our

announced target of a 3 % increase as a result of the unexpected

downturns in recent months. The order backlog amounted to €

73.4 million at year-end – slightly below the previous year’s figure of

74.6 million.

Invoiced sales in the retail furniture business rose slightly by 0.7 % to

€ 679.6 million. On a space-adjusted basis, this corresponds to a

sales decline of 2.9 % due to the addition of new selling space.

The previous year’s consolidated sales also included sales arising

from the invoicing of construction projects that the company com-

pleted itself and upon completion sold to lessors. In contrast, no

sales were generated by construction projects during the reporting

year. As a result, overall consolidated group sales fell by 2.7 % to the

above-mentioned figure of € 679.6 million.

A further important step towards market penetration in Eastern Europe was the opening of a new furni-

ture store in Budapest. This is our first outlet in Hungary. We are presently active with a total of five

furnishing outlets in three East European countries: the Czech Republic, Poland and now Hungary. The

Budapest store has a selling space of approximate 4,000 sq m [43,000 sq ft ] and experienced a solid

startup.

All in all, we generated considerable growth rates from our international business operations, with sales

rising by 33.8 % to € 37.3 million. Particularly worthy of mention is the high rate of growth of the three

furnishing outlets in the Czech Republic, which alone recorded a 30.6 % sales increase. Our outlet in the

eastern part of Prague, which opened in 1999, stands out in particular. This outlet has rapidly established

itself as our outlet with the highest level of sales in Eastern Europe. We now generate a total of 5.5 % of

our consolidated Group sales abroad.

1 2 M Ö B E L W A L T H E R 2 0 0 0

O p e r a t i n g s a l e s 0 . 7 % a b o v e p r e v i o u s y e a r

I n t e r n a t i o n a l : s u c c e s s f u l m a r k e t p e n e t r a t i o n i n H u n g a r y

1996 1997 1998 1999 2000

526.3

637.1

689.7 679.6674.6

€ million

50

200

350

500

650

OPERATING SALES

800

033800_WA_English_1RZ 16.05.2001 11:19 Uhr Seite 12

Sales in € million 2000 1999 Change

Furnishing centers 535.6 539.2 - 0.7 %

SCONTO Germany 89.2 89.0 + 0.1 %

TICCO 17.3 17.3 - 0.1 %

International 37.3 27.9 + 33.8 %

E-commerce 0.2 ––– [+] %

Other ––– 1.2 [–] %

Retail furniture business 679.6 674.6 + 0.7 %

Invoicing of construction projects ––– 23.8 [–] %

Group 679.6 698.4 - 2.7 %

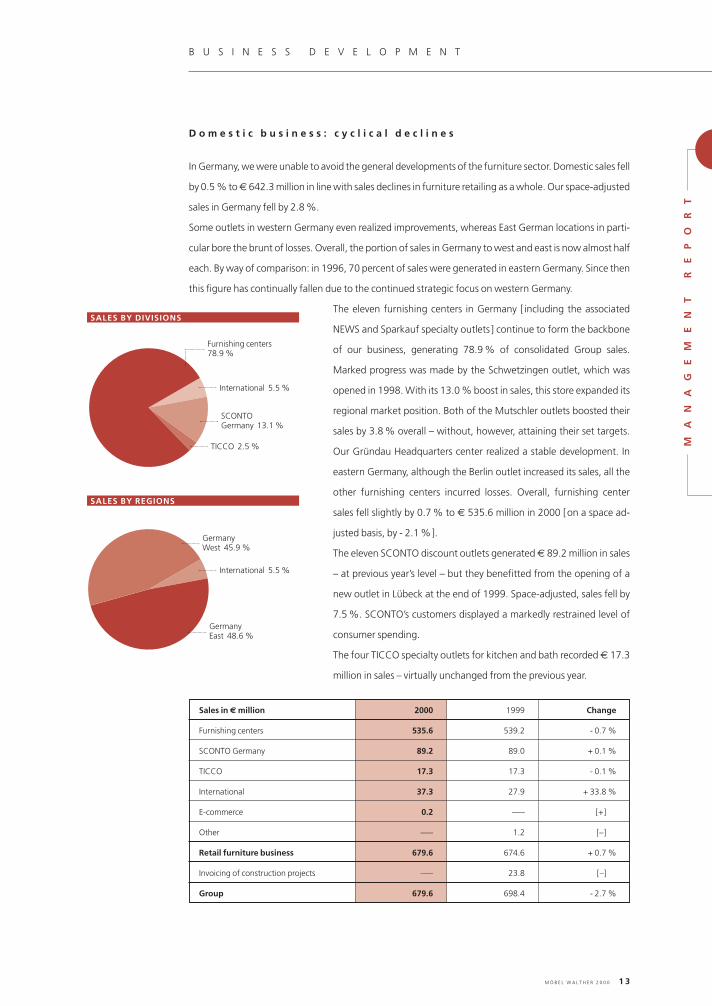

In Germany, we were unable to avoid the general developments of the furniture sector. Domestic sales fell

by 0.5 % to € 642.3 million in line with sales declines in furniture retailing as a whole. Our space-adjusted

sales in Germany fell by 2.8 %.

Some outlets in western Germany even realized improvements, whereas East German locations in parti-

cular bore the brunt of losses. Overall, the portion of sales in Germany to west and east is now almost half

each. By way of comparison: in 1996, 70 percent of sales were generated in eastern Germany. Since then

this figure has continually fallen due to the continued strategic focus on western Germany.

The eleven furnishing centers in Germany [ including the associated

NEWS and Sparkauf specialty outlets ] continue to form the backbone

of our business, generating 78.9 % of consolidated Group sales.

Marked progress was made by the Schwetzingen outlet, which was

opened in 1998. With its 13.0 % boost in sales, this store expanded its

regional market position. Both of the Mutschler outlets boosted their

sales by 3.8 % overall – without, however, attaining their set targets.

Our Gründau Headquarters center realized a stable development. In

eastern Germany, although the Berlin outlet increased its sales, all the

other furnishing centers incurred losses. Overall, furnishing center

sales fell slightly by 0.7 % to € 535.6 million in 2000 [on a space ad-

justed basis, by - 2.1 %].

The eleven SCONTO discount outlets generated € 89.2 million in sales

– at previous year’s level – but they benefitted from the opening of a

new outlet in Lübeck at the end of 1999. Space-adjusted, sales fell by

7.5 %. SCONTO’s customers displayed a markedly restrained level of

consumer spending.

The four TICCO specialty outlets for kitchen and bath recorded € 17.3

million in sales – virtually unchanged from the previous year.

M Ö B E L W A L T H E R 2 0 0 0 1 3

B U S I N E S S D E V E L O P M E N T

D o m e s t i c b u s i n e s s : c y c l i c a l d e c l i n e s

SALES BY DIVISIONS

SALES BY REGIONS

Germany East 48.6 %

GermanyWest 45.9 %

International 5.5 %

Furnishing centers 78.9 %

SCONTOGermany 13.1 %

International 5.5 %

TICCO 2.5 % MA

NA

GE

ME

NT

R

EP

OR

T

033800_WA_English_1RZ 16.05.2001 11:19 Uhr Seite 13

1 4 M Ö B E L W A L T H E R 2 0 0 0

Whereas up to now the Möbel Walther Group has based its operations exclusively on store-based fur-

niture retailing, we have begun to develop the company into a multi channel player. Our Internet shop,

which operates under the name »welcomeliving.de«, has been on-line since August 11, 2000. Industry

experts confirm that »welcomeliving« is setting new standards in the furniture business as far as product

range, navigation and service are concerned. The Internet shop is part of our e-commerce division and is

run by our newly founded subsidiary Möbel Walther New Media AG.

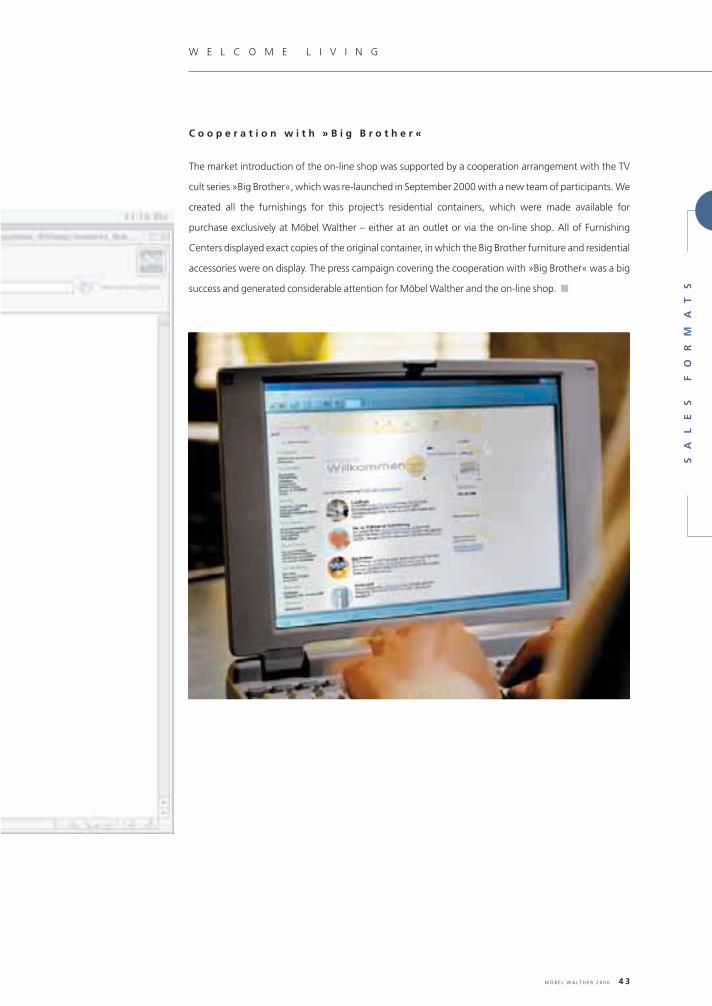

The market introduction of the on-line shop was supported by a cooperation with the TV cult series »Big

Brother«. All the furnishings of the TV house were provided by Möbel Walther and could be exclusively

bought at Möbel Walther stores or through the on-line shop. Between September and December,

containers built to the exact specifications of the original TV house were on display in all the furnishing

centers. These presented »Big Brother« furniture and furnishing accessories. The press campaign cover-

ing the cooperative arrangements with »Big Brother« generated enormous media response as well as

considerable attention for Möbel Walther and the on-line shop. The € 145 thousand in sales that were

generated is just the beginning.

W e l c o m e l i v i n g . d e : O n - l i n e s h o p l a u n c h e d o n t h e I n t e r n e t

033800_WA_English_1RZ 16.05.2001 11:20 Uhr Seite 14

M Ö B E L W A L T H E R 2 0 0 0 1 5

P R O F I T & D I V I D E N D

Due to the weak development of sales in the fourth quarter, the earnings for the last months, which

normally contribute a very large proportion to the annual profits, were much lower than in the previous

year and failed to meet our expectations, largely because of circumstances in the industry. Accordingly,

we show a pre-tax profit of € 14.3 million, significantly less than the previous year’s figure of € 22.1

million. These profits include amounts released from the special item with a partial reserve portion total-

ling € 6.6 million [previous year € 4.7 million] – amounts that up until 1996 were booked against special

depreciation under Section 4 of the Law on Development Areas.

The gross profit margin on operative business [ that is excluding the influence of the invoicing of con-

struction projects in the previous year ] improved by 0.7 percentage points to 43.8 %. This shows that it

was possible to combat increasing price pressure on special offers through counter-measures - such as the

increased direct import of furniture through our subsidiary Walther Trading Service GmbH. Personnel ex-

penses corresponded to a quota of 20.4 % of sales, 0.8 percentage points more than in the previous year.

The reasons: employment rose abroad – in particular in anticipation of the new openings in Budapest and

Warsaw [2001]. At home, an increase in the wage bill had to be accepted, while sales dropped off slightly.

In addition, there was considerable additional personnel expenditure as part of the changeover in the

material management system. The other operating expenses rose by 1.3 percentage points to a quota of

18.1 % of sales. This was due on the one hand to increased spending on advertising. On the other hand,

space costs increased due to expansion and higher energy costs.

The consolidated pre-tax profits are made up of the results from the five business segments/divisions –

plus the results of the group headquarters, including other companies [ in particular real estate companies

abroad] and consolidation items.

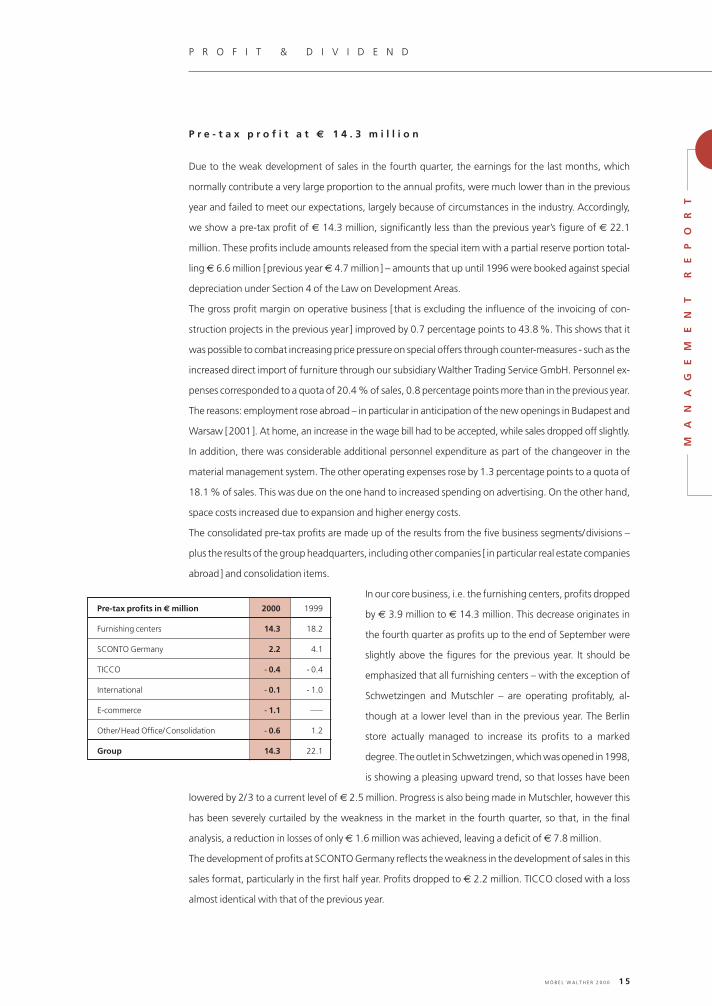

In our core business, i.e. the furnishing centers, profits dropped

by € 3.9 million to € 14.3 million. This decrease originates in

the fourth quarter as profits up to the end of September were

slightly above the figures for the previous year. It should be

emphasized that all furnishing centers – with the exception of

Schwetzingen and Mutschler – are operating profitably, al-

though at a lower level than in the previous year. The Berlin

store actually managed to increase its profits to a marked

degree. The outlet in Schwetzingen, which was opened in 1998,

is showing a pleasing upward trend, so that losses have been

lowered by 2/3 to a current level of € 2.5 million. Progress is also being made in Mutschler, however this

has been severely curtailed by the weakness in the market in the fourth quarter, so that, in the final

analysis, a reduction in losses of only € 1.6 million was achieved, leaving a deficit of € 7.8 million.

The development of profits at SCONTO Germany reflects the weakness in the development of sales in this

sales format, particularly in the first half year. Profits dropped to € 2.2 million. TICCO closed with a loss

almost identical with that of the previous year.

P r e - t a x p r o f i t a t € 1 4 . 3 m i l l i o n

Pre-tax profits in € million 2000 1999

Furnishing centers 14.3 18.2

SCONTO Germany 2.2 4.1

TICCO - 0.4 - 0.4

International - 0.1 - 1.0

E-commerce - 1.1 –––

Other/Head Office/Consolidation - 0.6 1.2

Group 14.3 22.1

MA

NA

GE

ME

NT

R

EP

OR

T

033800_WA_English_1RZ 16.05.2001 11:20 Uhr Seite 15

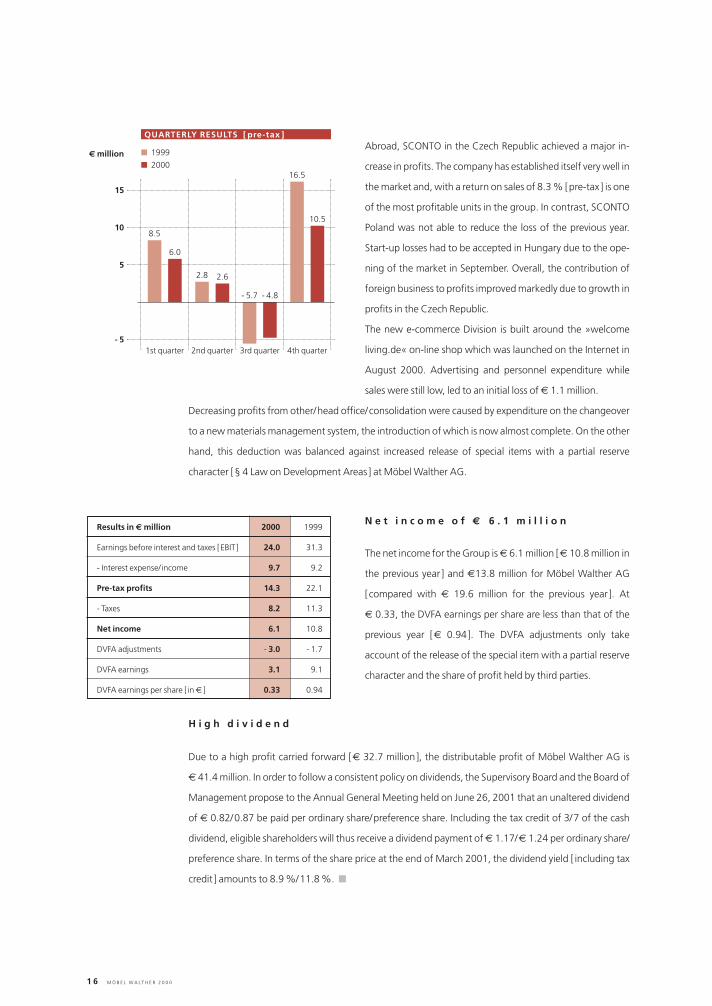

Abroad, SCONTO in the Czech Republic achieved a major in-

crease in profits. The company has established itself very well in

the market and, with a return on sales of 8.3 % [pre-tax ] is one

of the most profitable units in the group. In contrast, SCONTO

Poland was not able to reduce the loss of the previous year.

Start-up losses had to be accepted in Hungary due to the ope-

ning of the market in September. Overall, the contribution of

foreign business to profits improved markedly due to growth in

profits in the Czech Republic.

The new e-commerce Division is built around the »welcome

living.de« on-line shop which was launched on the Internet in

August 2000. Advertising and personnel expenditure while

sales were still low, led to an initial loss of € 1.1 million.

Decreasing profits from other/head office/consolidation were caused by expenditure on the changeover

to a new materials management system, the introduction of which is now almost complete. On the other

hand, this deduction was balanced against increased release of special items with a partial reserve

character [§ 4 Law on Development Areas ] at Möbel Walther AG.

1 6 M Ö B E L W A L T H E R 2 0 0 0

1st quarter

8.5

6.0

2.8 2.6

- 5.7 - 4.8

16.5

10.5

2nd quarter 3rd quarter 4th quarter

€ million

15

10

5

- 5

QUARTERLY RESULTS [ pre-tax ]

■ 1999

■ 2000

The net income for the Group is € 6.1 million [€ 10.8 million in

the previous year ] and €13.8 million for Möbel Walther AG

[compared with € 19.6 million for the previous year ]. At

€ 0.33, the DVFA earnings per share are less than that of the

previous year [€ 0.94]. The DVFA adjustments only take

account of the release of the special item with a partial reserve

character and the share of profit held by third parties.

N e t i n c o m e o f € 6 . 1 m i l l i o n

Due to a high profit carried forward [€ 32.7 million], the distributable profit of Möbel Walther AG is

€ 41.4 million. In order to follow a consistent policy on dividends, the Supervisory Board and the Board of

Management propose to the Annual General Meeting held on June 26, 2001 that an unaltered dividend

of € 0.82/0.87 be paid per ordinary share/preference share. Including the tax credit of 3/7 of the cash

dividend, eligible shareholders will thus receive a dividend payment of € 1.17/€ 1.24 per ordinary share/

preference share. In terms of the share price at the end of March 2001, the dividend yield [ including tax

credit ] amounts to 8.9 %/11.8 %. ■

H i g h d i v i d e n d

Results in € million 2000 1999

Earnings before interest and taxes [EBIT ] 24.0 31.3

- Interest expense/ income 9.7 9.2

Pre-tax profits 14.3 22.1

- Taxes 8.2 11.3

Net income 6.1 10.8

DVFA adjustments - 3.0 - 1.7

DVFA earnings 3.1 9.1

DVFA earnings per share [ in € ] 0.33 0.94

033800_WA_English_1RZ 16.05.2001 11:20 Uhr Seite 16

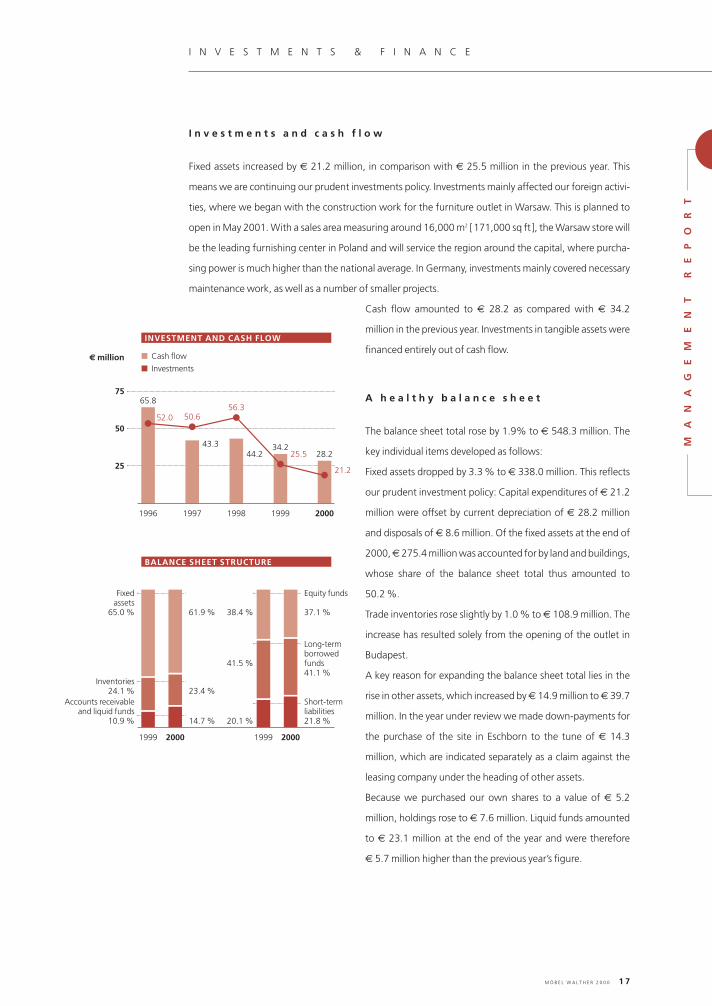

The balance sheet total rose by 1.9% to € 548.3 million. The

key individual items developed as follows:

Fixed assets dropped by 3.3 % to € 338.0 million. This reflects

our prudent investment policy: Capital expenditures of € 21.2

million were offset by current depreciation of € 28.2 million

and disposals of € 8.6 million. Of the fixed assets at the end of

2000, € 275.4 million was accounted for by land and buildings,

whose share of the balance sheet total thus amounted to

50.2 %.

Trade inventories rose slightly by 1.0 % to € 108.9 million. The

increase has resulted solely from the opening of the outlet in

Budapest.

A key reason for expanding the balance sheet total lies in the

rise in other assets, which increased by € 14.9 million to € 39.7

million. In the year under review we made down-payments for

the purchase of the site in Eschborn to the tune of € 14.3

million, which are indicated separately as a claim against the

leasing company under the heading of other assets.

Because we purchased our own shares to a value of € 5.2

million, holdings rose to € 7.6 million. Liquid funds amounted

to € 23.1 million at the end of the year and were therefore

€ 5.7 million higher than the previous year’s figure.

A h e a l t h y b a l a n c e s h e e t

Fixed assets increased by € 21.2 million, in comparison with € 25.5 million in the previous year. This

means we are continuing our prudent investments policy. Investments mainly affected our foreign activi-

ties, where we began with the construction work for the furniture outlet in Warsaw. This is planned to

open in May 2001. With a sales area measuring around 16,000 m2 [171,000 sq ft ], the Warsaw store will

be the leading furnishing center in Poland and will service the region around the capital, where purcha-

sing power is much higher than the national average. In Germany, investments mainly covered necessary

maintenance work, as well as a number of smaller projects.

Cash flow amounted to € 28.2 as compared with € 34.2

million in the previous year. Investments in tangible assets were

financed entirely out of cash flow.

M Ö B E L W A L T H E R 2 0 0 0 1 7

I N V E S T M E N T S & F I N A N C E

€ million ■ Cash flow

■ Investments

I n v e s t m e n t s a n d c a s h f l o w

1996 1997 1998 1999 2000

65.8

52.0

43.344.2 28.2

34.2

25

50

75

INVESTMENT AND CASH FLOW

50.656.3

25.5

21.2

BALANCE SHEET STRUCTURE

1999 2000 1999 2000

61.9 %

Fixed assets

65.0 %

Equity funds

37.1 %

23.4 %Inventories

24.1 %

Long-termborrowedfunds41.1 %

Accounts receivableand liquid funds

10.9 %

Short-termliabilities21.8 %20.1 %14.7 %

41.5 %

38.4 %

MA

NA

GE

ME

NT

R

EP

OR

T

033800_WA_English_1RZ 16.05.2001 11:20 Uhr Seite 17

Equity [ including 50 % of the special item with reserve portion] dropped slightly by 1.6 % to € 203.4

million. The equity ratio reached 37.1 % after 38.4 % in the previous year. The equity share of Möbel

Walther AG amounts to 51.6 % [51.4 % in the previous year ]. Thus, we continue to demonstrate a high

level of capital.

Liabilities to banks rose by € 4.6 million to € 177.2 million. It

should be remembered that we made payments to the tune of

€ 14.3 million as bridging finance for the purchase of the site in

Eschborn.

It was possible to considerably increase the down-payments

received from customers, rising by € 8.5 million to € 19.7

million. This also contributed to a considerable reduction in

working capital [ trade inventories and trade accounts receiv-

able minus trade accounts payable and advance payments from

customers ]. In all, the capital tied up in working capital was

reduced by € 17.4 million to € 25.0 million.

The coverage of fixed assets by equity capital in the Group

amounts to 60.2 % [59.2 % in the previous year ], while fixed assets and inventories together are funded

by equity capital and long-term borrowed funds to 91.9 % [89.7 % in the previous year ]. These coverage

figures indicate a healthy financial structure. ■

1 8 M Ö B E L W A L T H E R 2 0 0 0

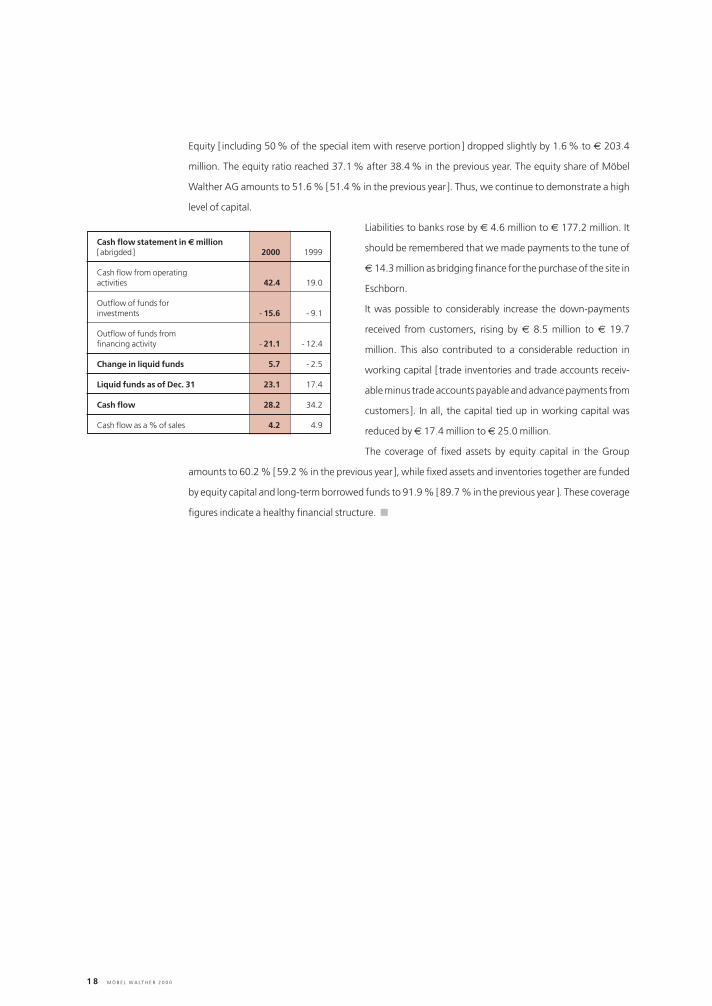

Cash flow statement in € million[abrigded] 2000 1999

Cash flow from operatingactivities 42.4 19.0

Outflow of funds forinvestments - 15.6 - 9.1

Outflow of funds fromfinancing activity - 21.1 - 12.4

Change in liquid funds 5.7 - 2.5

Liquid funds as of Dec. 31 23.1 17.4

Cash flow 28.2 34.2

Cash flow as a % of sales 4.2 4.9

033800_WA_English_1RZ 16.05.2001 11:20 Uhr Seite 18

M Ö B E L W A L T H E R 2 0 0 0 1 9

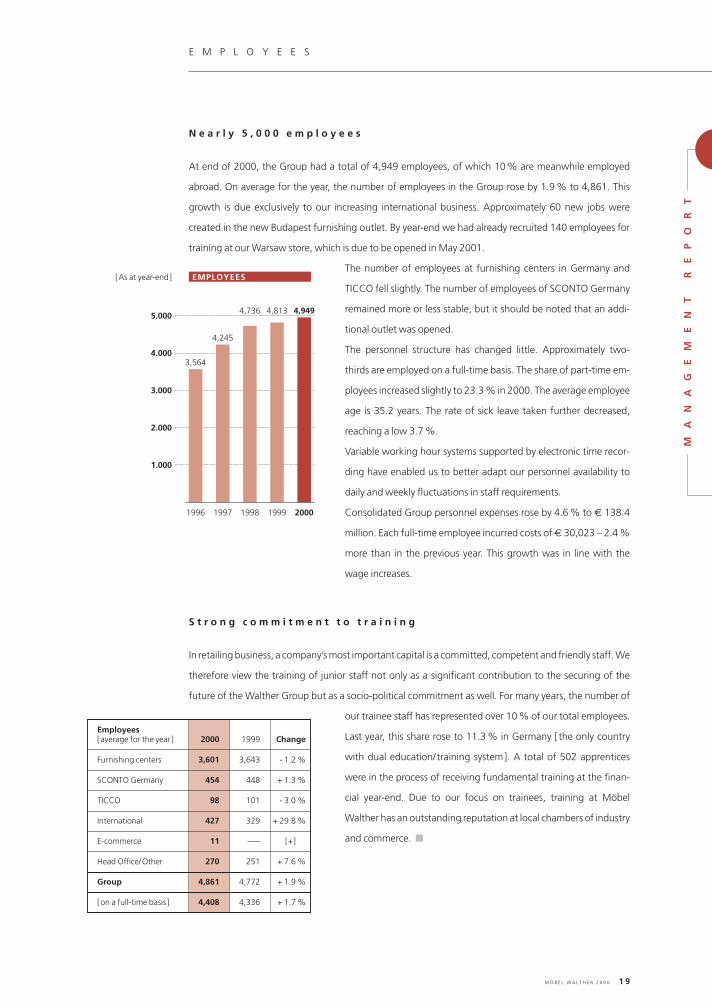

E M P L O Y E E S

At end of 2000, the Group had a total of 4,949 employees, of which 10 % are meanwhile employed

abroad. On average for the year, the number of employees in the Group rose by 1.9 % to 4,861. This

growth is due exclusively to our increasing international business. Approximately 60 new jobs were

created in the new Budapest furnishing outlet. By year-end we had already recruited 140 employees for

training at our Warsaw store, which is due to be opened in May 2001.

The number of employees at furnishing centers in Germany and

TICCO fell slightly. The number of employees of SCONTO Germany

remained more or less stable, but it should be noted that an addi-

tional outlet was opened.

The personnel structure has changed little. Approximately two-

thirds are employed on a full-time basis. The share of part-time em-

ployees increased slightly to 23.3 % in 2000. The average employee

age is 35.2 years. The rate of sick leave taken further decreased,

reaching a low 3.7 %.

Variable working hour systems supported by electronic time recor-

ding have enabled us to better adapt our personnel availability to

daily and weekly fluctuations in staff requirements.

Consolidated Group personnel expenses rose by 4.6 % to € 138.4

million. Each full-time employee incurred costs of € 30,023 – 2.4 %

more than in the previous year. This growth was in line with the

wage increases.

In retailing business, a company’s most important capital is a committed, competent and friendly staff. We

therefore view the training of junior staff not only as a significant contribution to the securing of the

future of the Walther Group but as a socio-political commitment as well. For many years, the number of

our trainee staff has represented over 10 % of our total employees.

Last year, this share rose to 11.3 % in Germany [ the only country

with dual education/ training system]. A total of 502 apprentices

were in the process of receiving fundamental training at the finan-

cial year-end. Due to our focus on trainees, training at Möbel

Walther has an outstanding reputation at local chambers of industry

and commerce. ■

N e a r l y 5 , 0 0 0 e m p l o y e e s

S t r o n g c o m m i t m e n t t o t r a i n i n g

1996 1997 1998 1999 2000

3,564

4,245

4,736 4,9494,813

1.000

2.000

3.000

4.000

5.000

EMPLOYEES[As at year-end]

Employees [average for the year ] 2000 1999 Change

Furnishing centers 3,601 3,643 - 1.2 %

SCONTO Germany 454 448 + 1.3 %

TICCO 98 101 - 3.0 %

International 427 329 + 29.8 %

E-commerce 11 ––– [+] %

Head Office/Other 270 251 + 7.6 %

Group 4,861 4,772 + 1.9 %

[on a full-time basis ] 4,408 4,336 + 1.7 %

MA

NA

GE

ME

NT

R

EP

OR

T

033800_WA_English_1RZ 16.05.2001 11:20 Uhr Seite 19

2 0 M Ö B E L W A L T H E R 2 0 0 0

■ E N T R Y I N T O T H E M A I L O R D E R B U S I N E S S

■ G O O D P R O S P E C T S I N E A S T E R N E U R O P E

■ E - C O M M E R C E H A S P O T E N T I A L

■ T H E E S C H B O R N C E N T E R : A U N I Q U E C O N C E P T

■ R E A L E S T A T E A S T H E T H I R D P I L L A R O F B U S I N E S S

■ E X P E C T A T I O N S F O R 2 0 0 1

With effect from January 1, 2001 we have acquired a 51 % shareholding in the mail order company

Ikarus GmbH in Linsengericht. Ikarus was founded in 1993 and specializes in designer furniture and

accessories. The mail order company has around 2,000 products in its catalog and achieved sales of

€ 2 million in the year 2000.The shares in Ikarus GmbH are held by Möbel Walther New Media AG.

The company founder and former sole proprietor Volker Hohmann will stay on as managing director

at Ikarus.

This majority shareholding represents another important step on the way to becoming a multi-channel

player that runs e-commerce and mail order operations as well as store-based retailing. This acquisition

will give rise to synergy effects, particularly for our on-line sales. With effect from April 2001, products

from Ikarus will supplement the Internet range on offer from »welcomeliving«.

E n t r y i n t o t h e m a i l o r d e r b u s i n e s s

German consumers are the highest spenders in Europe on furniture and interior design. In 1999, sales per

capita in Germany were € 415 compared with € 245 on average in the EU. In all, the turnover for

furniture and interior design products in the EU amounted to € 91.8 billion in 1999. According to the

European Retail Institute, a total of € 34.0 billion was achieved in Germany alone, € 4.1 billion in the

commercial sector and € 29.9 billion in the private consumer sector.

Furniture retailers enjoyed a 74 % share of this market volume of € 34.0 billion. The rest is shared among

such sales channels as DIY stores, office specialists and mail order companies. In particular, mail order

companies were able to expand their share of furniture market sales in recent years. This underpins our

decision to enter the mail order business.

P r o s p e c t s f o r t h e G e r m a n f u r n i t u r e m a r k e t

033800_WA_English_1RZ 16.05.2001 11:20 Uhr Seite 20

M Ö B E L W A L T H E R 2 0 0 0 2 1

O U T L O O K & S T R A T E G Y

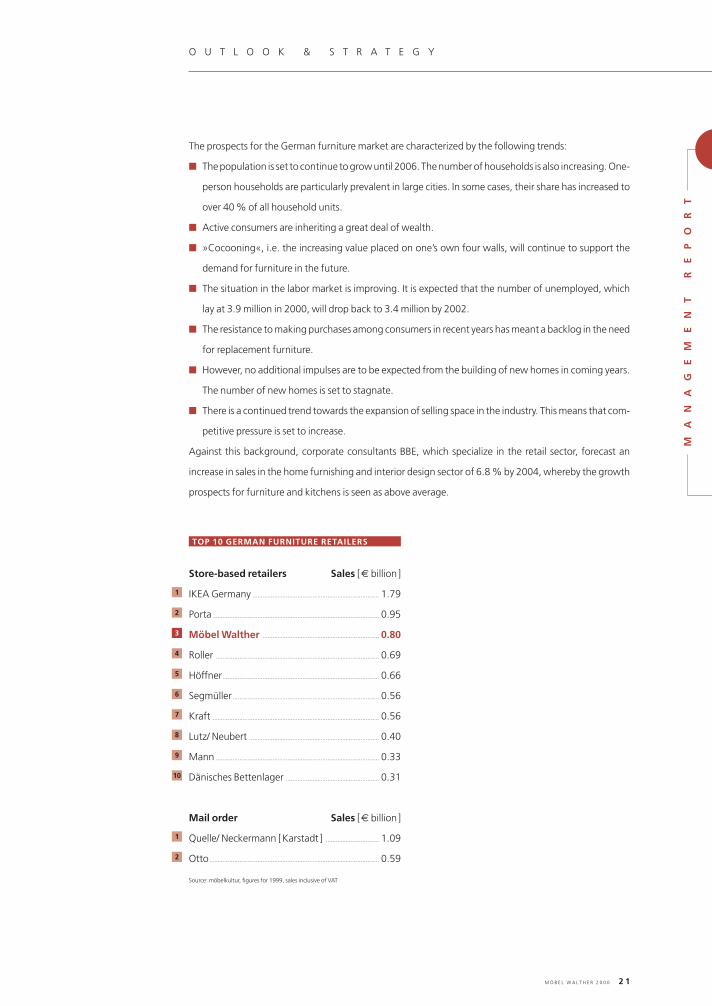

The prospects for the German furniture market are characterized by the following trends:

■ The population is set to continue to grow until 2006. The number of households is also increasing. One-

person households are particularly prevalent in large cities. In some cases, their share has increased to

over 40 % of all household units.

■ Active consumers are inheriting a great deal of wealth.

■ »Cocooning«, i.e. the increasing value placed on one’s own four walls, will continue to support the

demand for furniture in the future.

■ The situation in the labor market is improving. It is expected that the number of unemployed, which

lay at 3.9 million in 2000, will drop back to 3.4 million by 2002.

■ The resistance to making purchases among consumers in recent years has meant a backlog in the need

for replacement furniture.

■ However, no additional impulses are to be expected from the building of new homes in coming years.

The number of new homes is set to stagnate.

■ There is a continued trend towards the expansion of selling space in the industry. This means that com-

petitive pressure is set to increase.

Against this background, corporate consultants BBE, which specialize in the retail sector, forecast an

increase in sales in the home furnishing and interior design sector of 6.8 % by 2004, whereby the growth

prospects for furniture and kitchens is seen as above average.

1

2

3

4

5

6

7

8

9

10

IKEA Germany ............................................................................ 1.79

Porta .................................................................................................... 0.95

Möbel Walther ...................................................................... 0.80

Roller .................................................................................................. 0.69

Höffner.............................................................................................. 0.66

Segmüller ........................................................................................ 0.56

Kraft .................................................................................................... 0.56

Lutz/ Neubert .............................................................................. 0.40

Mann .................................................................................................. 0.33

Dänisches Bettenlager ........................................................ 0.31

TOP 10 GERMAN FURNITURE RETAILERS

Store-based retailers Sales [€ billion]

1

2

Quelle/ Neckermann [Karstadt ] ................................ 1.09

Otto...................................................................................................... 0.59

Mail order Sales [€ billion]

Source: möbelkultur, figures for 1999, sales inclusive of VAT

MA

NA

GE

ME

NT

R

EP

OR

T

033800_WA_English_1RZ 16.05.2001 11:20 Uhr Seite 21

2 2 M Ö B E L W A L T H E R 2 0 0 0

Prospects for consumer spending in Germany in 2001 are positive: Employment has grown over the last

year and is expected to increase further. People’s worries about being made redundant have receded. Net

incomes are also increasing tangibly, due also to the drop in income tax with effect from January 1, 2001.

Overall, disposable income for private households is increasing by more than € 50 billion, representing a

yearly figure of around € 1,300 per household. According to forecasts, private consumption will in-

crease by about 2.2 % in real terms, thereby growing slightly faster than the overall gross national

product at 2.1 %, thanks to tax relief.

This is why the Association of German Retailers is cautiously optimistic in its forecasts of a real growth in

sales in the retail sector of 2.0 %. Expectations are mainly based on the second half of the year. The

German Association of Furniture, Kitchen and Interior Retailers forecasts a [nominal ] growth in sales of

3 to 4 % for 2001.

B e t t e r p r o s p e c t s f o r c o n s u m p t i o n i n 2 0 0 1

We have been active on the international front since 1995. We have chosen this step very consciously in

order to reduce our dependence on the German market. We see above-average opportunities in the neigh-

boring countries of eastern Europe [Czech Republic, Poland and Hungary ]. The need to catch up with

furniture and interior fittings is considerable here, while these economies are growing much faster than

Germany or the EU territory.

Over € 400 per capita is spent on furniture every year in Germany. Spending on furniture in the adjoining

countries of eastern Europe is only about one tenth of this figure [ see table p. 24]. There is a lot of

catching up to be done here, even if this is not going to be an over-night development. However, Poland,

the Czech Republic and Hungary, which a have a total population of almost 60 million will become mem-

bers of the European Union in the foreseeable future, binding them even closer to central Europe, in

particular Germany. The economic strength of the region around Prague in the Czech republic is already

greater than the EU average.

T h e C z e c h R e p u b l i c , H u n g a r y a n d P o l a n d a s m a r k e t s o f t h e f u t u r e

In Germany, the furniture industry has been struggling with a restrained level of consumer spending

since 1995. This has considerably increased the pressure for structural adjustments among the 10,000

firms in the industry. Since the mid 1990’s the number of bankruptcies has been around 100 per year,

while the yearly average prior to this was only 50 closures. These figures do not include the silent closures

of many small companies without legal proceedings, a number which is estimated to be higher than that

of official bankruptcies.

This development will intensify in the future. Structural streamlining will shift weight even further in favor

of large retailers such as Möbel Walther, which have gained further market shares in recent years. In view

of our market position and our broadly based sales formats, both in conventional business and in e-

commerce and mail order, we believe we are well prepared for this structural process.

S t r u c t u r a l s t r e a m l i n i n g

033800_WA_English_1RZ 16.05.2001 11:20 Uhr Seite 22

M Ö B E L W A L T H E R 2 0 0 0 2 3

O U T L O O K & S T R A T E G Y

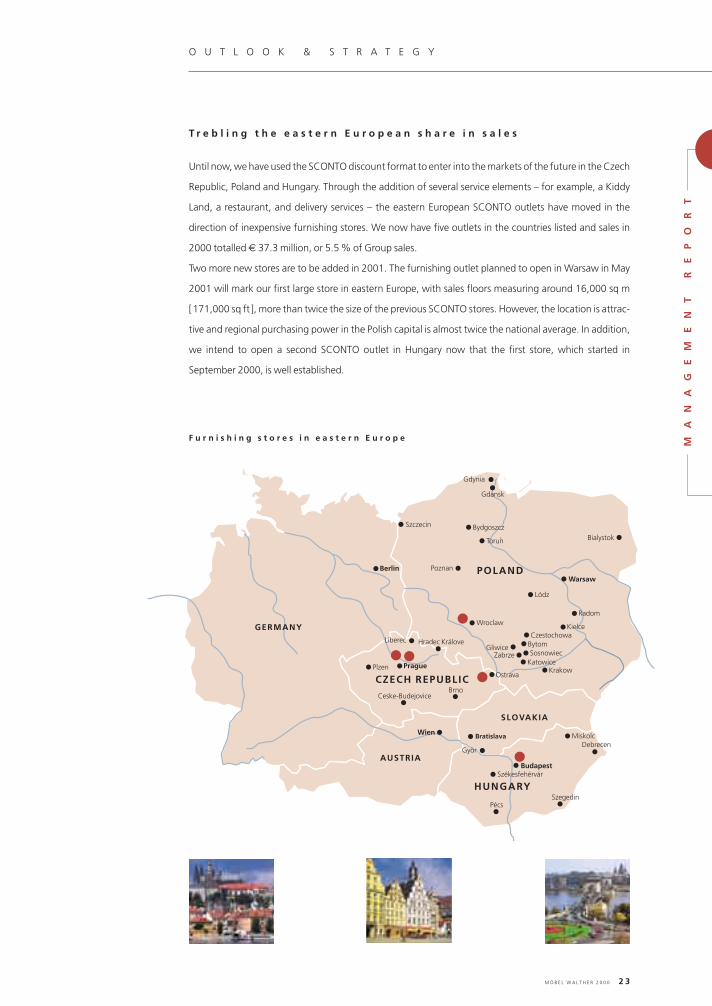

Until now, we have used the SCONTO discount format to enter into the markets of the future in the Czech

Republic, Poland and Hungary. Through the addition of several service elements – for example, a Kiddy

Land, a restaurant, and delivery services – the eastern European SCONTO outlets have moved in the

direction of inexpensive furnishing stores. We now have five outlets in the countries listed and sales in

2000 totalled € 37.3 million, or 5.5 % of Group sales.

Two more new stores are to be added in 2001. The furnishing outlet planned to open in Warsaw in May

2001 will mark our first large store in eastern Europe, with sales floors measuring around 16,000 sq m

[171,000 sq ft ], more than twice the size of the previous SCONTO stores. However, the location is attrac-

tive and regional purchasing power in the Polish capital is almost twice the national average. In addition,

we intend to open a second SCONTO outlet in Hungary now that the first store, which started in

September 2000, is well established.

T r e b l i n g t h e e a s t e r n E u r o p e a n s h a r e i n s a l e s

SLOVAKIA

HUNGARY

CZECH REPUBLIC

GERMANY

AUSTRIABudapest

Miskolc

Györ

Warsaw

Berlin

BratislavaWien

Radom

Kielce

Krakow

Zabrze

Czestochowa

SosnowiecBytom

Gdynia

Wroclaw

Poznan

Bydgoszcz

Torun

Lódz

Szczecin

Gdansk

Székesfehérvár

PlzenOstrava

Debrecen

Ceske-Budejovice

Hradec Králove

Brno

Liberec

Bialystok

PécsSzegedin

Katowice

Gliwice

F u r n i s h i n g s t o r e s i n e a s t e r n E u r o p e

POLAND

Prague

MA

NA

GE

ME

NT

R

EP

OR

T

033800_WA_English_1RZ 16.05.2001 11:20 Uhr Seite 23

2 4 M Ö B E L W A L T H E R 2 0 0 0

@e

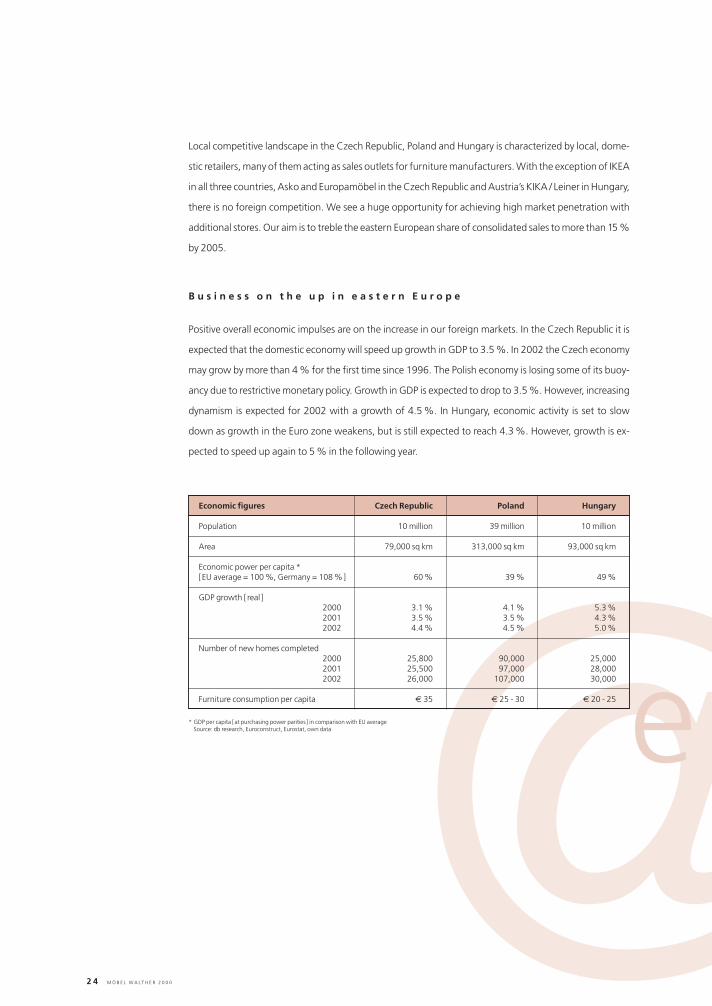

Positive overall economic impulses are on the increase in our foreign markets. In the Czech Republic it is

expected that the domestic economy will speed up growth in GDP to 3.5 %. In 2002 the Czech economy

may grow by more than 4 % for the first time since 1996. The Polish economy is losing some of its buoy-

ancy due to restrictive monetary policy. Growth in GDP is expected to drop to 3.5 %. However, increasing

dynamism is expected for 2002 with a growth of 4.5 %. In Hungary, economic activity is set to slow

down as growth in the Euro zone weakens, but is still expected to reach 4.3 %. However, growth is ex-

pected to speed up again to 5 % in the following year.

Local competitive landscape in the Czech Republic, Poland and Hungary is characterized by local, dome-

stic retailers, many of them acting as sales outlets for furniture manufacturers. With the exception of IKEA

in all three countries, Asko and Europamöbel in the Czech Republic and Austria’s KIKA / Leiner in Hungary,

there is no foreign competition. We see a huge opportunity for achieving high market penetration with

additional stores. Our aim is to treble the eastern European share of consolidated sales to more than 15 %

by 2005.

B u s i n e s s o n t h e u p i n e a s t e r n E u r o p e

Economic figures Czech Republic Poland Hungary

Population 10 million 39 million 10 million

Area 79,000 sq km 313,000 sq km 93,000 sq km

Economic power per capita *[EU average = 100 %, Germany = 108 %] 60 % 39 % 49 %

GDP growth [ real ]2000 3.1 % 4.1 % 5.3 %2001 3.5 % 3.5 % 4.3 %2002 4.4 % 4.5 % 5.0 %

Number of new homes completed2000 25,800 90,000 25,0002001 25,500 97,000 28,0002002 26,000 107,000 30,000

Furniture consumption per capita € 35 € 25 - 30 € 20 - 25

* GDP per capita [at purchasing power parities ] in comparison with EU averageSource: db research, Euroconstruct, Eurostat, own data

033800_WA_English_1RZ 16.05.2001 11:20 Uhr Seite 24

M Ö B E L W A L T H E R 2 0 0 0 2 5

O U T L O O K & S T R A T E G Y

@-commerceSelling through the Internet [e-commerce] is a relatively new sales channel, which was born in a state

of euphoria. However, a number of businesses have already failed – particularly companies solely based

on the Internet. Our structure is quite different because we already have a strong base in conventional

store-based business. The winners in e-commerce will be traditional retailers who have expanded their

activities – starting with store-based business – to include e-commerce, just as we have done with

»welcomeliving«.

Our »welcomeliving« on-line shop has been available on the Internet since August 2000. With almost

3,000 items on offer, the shop currently offers the broadest range of furnishings available on the Internet.

Our aim is to develop »welcomeliving« as a comprehensive living and lifestyle portal.

We see the advantage of Internet business not only in the direct sales generated in this way, but also in

access to new target groups that could not be reached through store-based business. To this are added

synergy effects between the various sales formats. Our furniture stores mean that we have the advantage

of already being well-known in several regions in Germany, providing a good basis for trust in Internet or

mail order business. Tomorrow’s customers will feel free to switch between the various sales formats,

depending on what is most convenient and least time-consuming for him. Both pre-selection and

product comparisons can take place in the store, by means of the Internet or using the catalog, as well as

a whole range of combinations of all of these options.

It should also be emphasized that we can also use key elements from our conventional retail business

for the new sales formats – starting with the organization of purchasing, advertising, IT, through to the

whole of logistics. We therefore regard the e-commerce/mail order business area as an important

supplement to our conventional offers. All three sales channels will complement and enhance each other.

In the long term, the e-commerce/mail order business area is expected to become an important pillar

for sales and revenue. We expect sales of around € 25 million by the year 2005.

I n t e r n e t – p a r t o f t h e m i x

E - c o m m e r c e : P o t e n t i a l f o r m u l t i - c h a n n e l p l a y e r s

MA

NA

GE

ME

NT

R

EP

OR

T

033800_WA_English_1RZ 16.05.2001 11:20 Uhr Seite 25

2 6 M Ö B E L W A L T H E R 2 0 0 0

The fundamental trends in on-line shopping continue to point upwards:

■ Purchasing through the Internet is the fashionable thing to do. This is because it is convenient

for the customer – no need to worry about business hours, no queues, no searching for parking,

time-saving, uncomplicated. Of course, the customer also expects that the goods he has ordered will

be delivered quickly and efficiently. This particular area – in other words, logistics – is one of our key

strengths.

■ Penetration with on-line connections will continue to grow rapidly.

■ An increasing number of people are prepared to buy over the Internet. Surveys point to an increasing

willingness to make on-line purchases. Forsa estimates the number of Germans who went on a

shopping spree in the Internet in 2000 at 7.3 million. More than 34 % of all Internet users have made

on-line purchases more than five times.

The Association of German Retailers estimates retail sales over the Internet at around € 2.5 billion in the

year 2000. Although this represents a modest 0.5 % of total retail sales, it is expected that the proportion

will increase to between 5 and 10 % in ten years time. By that time, Internet sales for some product groups,

such as CDs, books and computer equipment, will be as standard as conventional sales.

What is the potential for furniture retailing on the Internet? There is no doubt that some furniture is of

limited suitability for on-line shopping. This includes products requiring a lot of planning or furniture

where tactile experience is an essential part of the selection process. However, investigations show that

almost 20 % of all on-line buyers have ordered goods from the furnishings or homewares categories. The

fact that mail order companies achieve major sales with furniture [ see table on page 21] underlines the

potential for sales channels that complement conventional furniture sales. Finally, our own experience

with »welcomeliving« demonstrates that furniture can be sold over the Internet. Around two thirds of

sales achieved with »welcomeliving« are for furniture and only one third is for home accessories.

033800_WA_English_1RZ 16.05.2001 11:20 Uhr Seite 26

M Ö B E L W A L T H E R 2 0 0 0 2 7

O U T L O O K & S T R A T E G Y

In addition to conventional store-based business – our bread and butter – and e-commerce/mail order,

we intend to set up a third business area in the future: real estate. To date we have used our real estate

almost exclusively for our own purposes in order to operate store-based business. In the future we intend

to achieve much higher added value through professional real estate management.

The book value of our land and buildings is € 275 million. Cost of acquisition total € 348 million and

market values are even higher. We mainly have very good locations with the option of extending and

leasing additional space to third parties. This increases the attraction of the locations and generates

additional revenue. We have three locations in eastern Europe that are big enough to be developed into

shopping centers, thereby rounding off our planned furnishing centers. The same applies to the site at

Eschborn near Frankfurt. However, we also have locations in which it makes sense to optimize our sales

areas by subletting. All in all, there is an enormous potential for added value in our own properties and

this is to be exploited in the future.

As a first step in building up this business area, we have obtained approval from the General Shareholders’

Meeting in August 2000 to transfer the real estate business into an independent subsidiary. We expect to

complete this transaction this year.

R e a l e s t a t e a s a n e w b u s i n e s s a r e a

MÖBEL WALTHER AG

Store-based retailing E-commerce/mail order Real estate

Eschborn, west of Frankfurt/Main, is an extremely attractive location: High spending power, but up to

now insufficient supply of furniture make Eschborn one of the best locations for furniture in Germany.

We have developed a concept that is completely new to Germany: we are not planning to build a classic

furniture store, but rather a theme center »World of Living«, placing the emphasis on interior design.

What makes this project special is the fact that Möbel Walther will not be the only furniture retailer in

this store, but will share the space with other suppliers from the furnishings and interiors industry. This

solution means that the location will be much more attractive thanks to the wide range of products on

offer. It also means that the risk is spread out because returns on our investment come not only from

our retail activities, but also from property rental. The theme center in Eschborn is thus also a perfect

example of planned further development of real estate within the Group.

T h e E s c h b o r n c e n t e r : a u n i q u e c o n c e p t

MA

NA

GE

ME

NT

R

EP

OR

T

033800_WA_English_1RZ 16.05.2001 11:20 Uhr Seite 27

2 8 M Ö B E L W A L T H E R 2 0 0 0

A powerful logistics system that gets goods to customers quickly and reliably is essential if customers

are to be offered »convenience« when they come to buy furniture. This is precisely one of our key areas

of expertise which we intend to further extend by developing our logistics structure. We are planning

to expand our regional logistics centers to enable associated stores to be supplied with new products.

The new system will mean that even more product will be available for the customer to drive away –

a response to the customer’s wish to avoid waiting and lead times. At the same time, overall stocks will

actually be reduced.

Our strength in logistics is useful not only in conventional business. Internet sales and mail order business

require a high level of expertise in handling and delivery. Our competitive advantage lies in the fact