Module 4.2 Treasury Management INTRODUCTION TO PUBLIC FINANCE MANAGEMENT

Module 4.2 Treasury Management INTRODUCTION TO PUBLIC FINANCE MANAGEMENT.

Dec 16, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Module 4.2 Treasury Management

INTRODUCTION TO PUBLIC FINANCE MANAGEMENT

Module map

Treasury Appetizer Game

Requirements:•- 4 players (Treasury and 3 line ministries), One table•- budget size €119 billion, paid in quarterly tranches

Rules:•- Each line ministry spends according to approved budget•- Line ministries can put left over funds on a bank account

Three simulations:•1. ‘Standard’ developing country (no TSA and no transparency)•2. one Treasury Single Account (+ full transparency)•3. also a domestic capital market (interest rate 25%)

• 1. Definition and objectives

• 2. Problems with poor cash management

• 3. Efficient Cash Management

• 4. Cash flow forecasting

• 5. Treasury Single Account

• 6. Debt Management

Module Outline

4

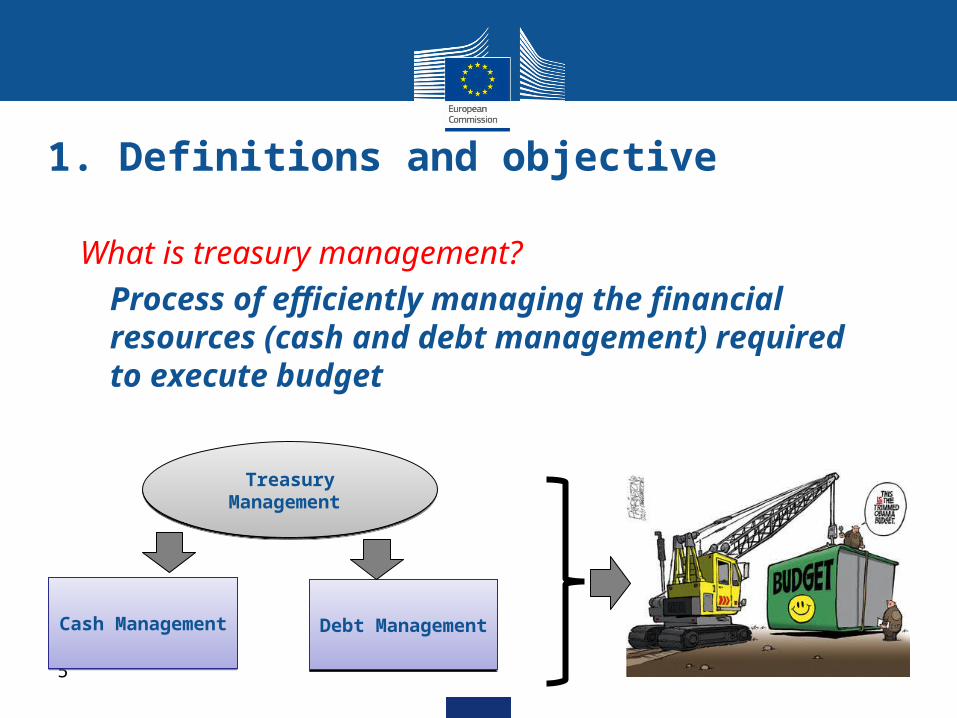

What is treasury management? Process of efficiently managing the

financial resources (cash and debt management) required to execute budget

1. Definitions and objective

5

Treasury Management

Treasury Management

Debt Management

Debt Management

Cash Management

Cash Management

Cash management:

Avoid disruptive cash rationing

Avoid payments arrears

Support smooth financing of expenditure plans: use cash and minimize short-term borrowing costs

1. Definitions and objectives

6

1. Definitions and objectives

Smoothing expenditure plans

1. Definitions and objectives

Cash Management:

Optimize use of cash resources: surplus cash invested in interest-earning financial assets

Conduct cost-effective borrowing operations

Consistency with the monetary policy

• 1. Definition and objectives

• 2. Problems with poor cash management

• 3. Efficient Cash & Debt Management

• 4. Cash flow forecasting

• 5. Treasury Single Account

• 6. Debt Management

Module Outline

9

Macro-economic instability: revenues unpredictable & shortfalls lead to in-year budget cuts

Unpredictable in-year reallocations between MDAs

Payments arrears accumulate, as MDAs enter into spending commitments that may be consistent with approved budget, but not supported by cash availability

2. Problems with poor cash management

10

“Cash rationing” accompanied by commitment controls used as a means of controlling expenditure according to cash availability

Budget support from donors useful if it is predictable. Unpredictable budget support leads to same problems as unpredictable revenues

2. Problems with poor cash management

11

Cash rationing opposite of efficient cash management. Will have adverse impact on service delivery

Danger is ”institutionalisation” of cash rationing, after need for IMF programs and cash rationing has gone

2. Problems with poor cash management

12

• 1. Definition and objectives

• 2. Problems with poor cash management

• 3. Efficient Cash Management

• 4. Cash flow forecasting

• 5. Treasury Single Account

• 6. Debt Management

Module Outline

14

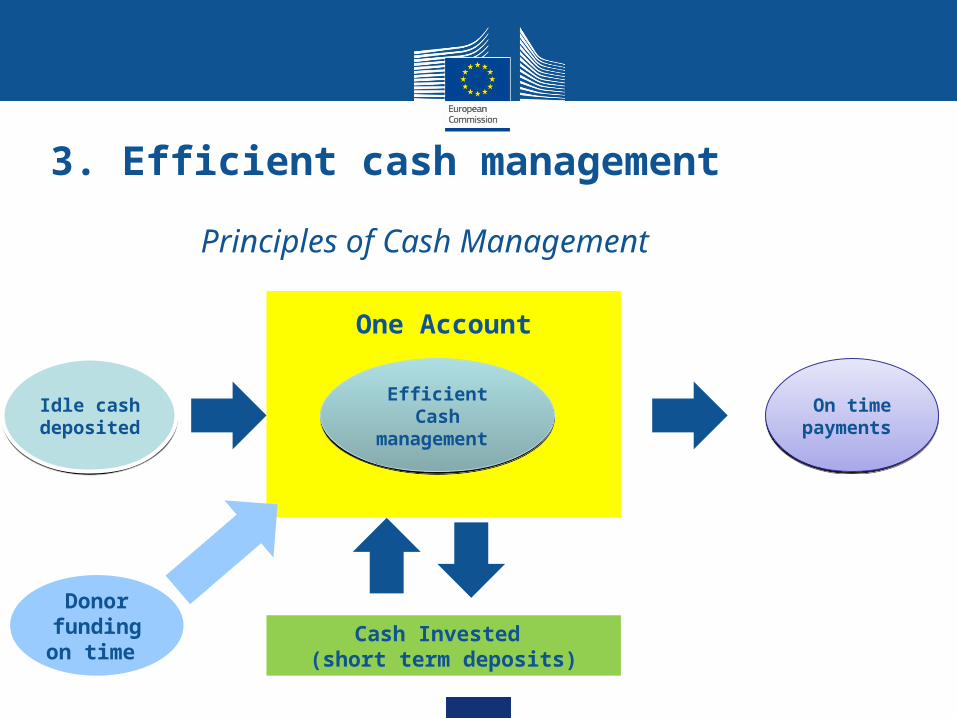

3. Efficient cash management

One Account

Efficient Cash management Efficient Cash management

On time payment

s

On time payment

s

Idle cash deposite

d

Idle cash deposite

d

Cash Invested (short term deposits)

Principles of Cash Management

Donor funding on time

How to do this?

A pre-condition: sound budget preparation discussed in previous units

Weekly/monthly cash flow forecasting (revenue & donor funding, spending)

One unit in charge - cash management unit

Treasury Single Account (TSA)

Recording, monitoring and management of debt

3. Efficient Cash Management

16

• 1. Definition and objectives

• 2. Problems with poor cash management

• 3. Efficient Cash & Debt Management

• 4. Cash flow forecasting

• 5. Treasury Single Account

• 6. Debt Management

Module Outline

17

4. Cash flow forecasting

18

Annual budget

Ministries

Departments

Agencies

Sub National

Monthly Revenue & Expenditure Forecasting

CashManagementUnit

CashManagementUnit

4. Cash flow forecasting

CashManagement

Unit

CashManagement

Unit

Warrant

A cash plan

1 2 3 4 5 6 7 8 9 10 11 12Expenditures

PersonnelGoods and ServicesInterestsTransfersInvestment/domestic fund

ResourcesRevenuesBudget support

----> Investment/borrowing

• Cash plans should be updated monthly, but

• Cash plans should be announced in advance• To MDA• To the domestic financial market, if used for

borrowing

• Use in preparing borrowing plans or cash rationing • Do they take into account effectively

procurement plans?

Some issues

• 1. Definition and objectives

• 2. Problems with poor cash management

• 3. Efficient Cash & Debt Management

• 4. Cash flow forecasting

• 5. Treasury Single Account

• 6. Debt Management

Module Outline

22

• Definition of Treasury Single account:

A bank account or a set of linked bank accounts used for all/most government transactions

• In case of linked bank accounts it are “zero” balance accounts: any balances “swept” back into TSA each day.

Treasury Single Account (TSA)

23

• Advantages• No more idle balances in MDAs' bank accounts• Idle cash balances in TSA invested in interest

earning financial assets• TSA facilitates accounting control through bank

reconciliations • TSA facilitates timely & comprehensive accounting

statements/reports, which, in turn, facilitate cash flow forecasting

5. Treasury Single Account

24

Different types of Treasury Single Account •The Treasury releases funds into MDA sub-accounts in central bank or treasury-controlled MDA accounts in commercial banks which are the Treasury’s fiscal agent

•The MDA bank provides to the MDA overdraft facilities up to a cash limit notified by the Treasury. The MDA bank is reimbursed daily by the Treasury (Sri Lanka –Colombo)

5. Treasury Single Account

25

5. Treasury Single Account Case 1. Payment via centralised Treasury

Case 2. Payment via spending agencies' bank accounts

Spending Agency

Treasury Banking system

Supplier

Treasury

Payment order

Check

Clearance Ceilings

Transfer

SpendingAgency

BankingSystem

Supplier

Banking system

Fiscal Agent

Retail Bank

Supplier Account

Central Bank TSA

Payments

Receipts

Daily

Not common in all countries In many countries there are still hundreds of MDA bank accounts

Idle cash balances may lie in these accounts, resulting in lower interest earnings and higher interest expenses through unnecessary borrowing

5. Treasury Single Account

27

Not common in all countries: Even if centralised TSA, donor-funded projects accounts are often kept outside the TSA and the Treasury controls

There is domestic resistance to the implementation of the TSA. Multiple bank accounts facilitate budget ring-fencing and potentially corrupt behaviour

Establishing TSA may require strong political leadership

5. Treasury Single Account

28

• 1. Definition and objectives

• 2. Problems with poor cash management

• 3. Efficient Cash & Debt Management

• 4. Cash flow forecasting

• 5. Treasury Single Account

• 6. Debt Management

Module Outline

29

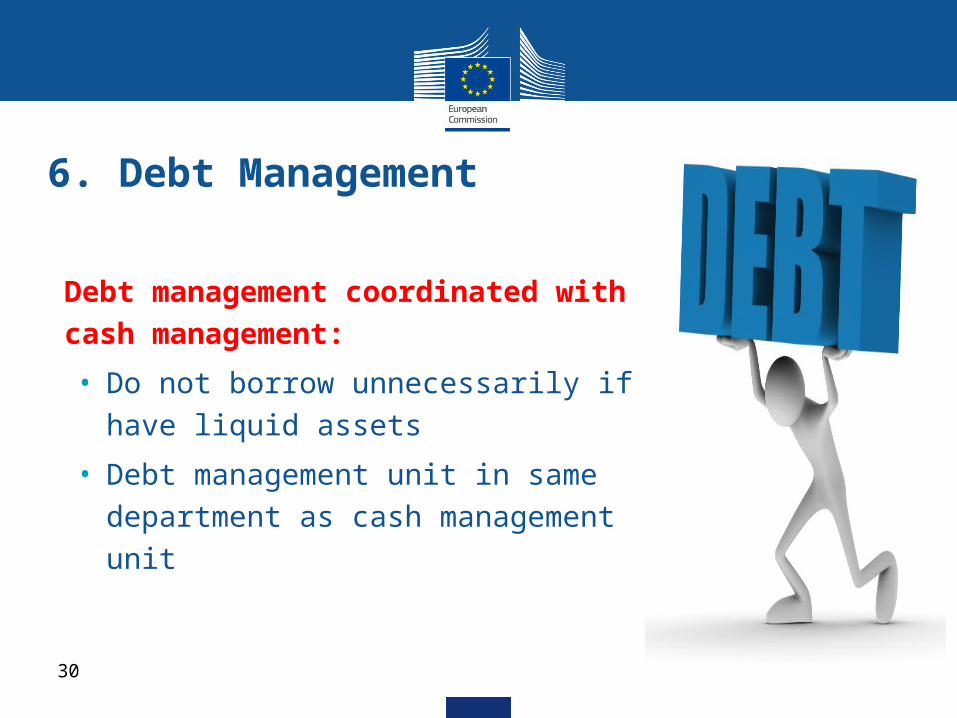

• Debt management coordinated with cash management:

• Do not borrow unnecessarily if have liquid assets

• Debt management unit in same department as cash management unit

6. Debt Management

30

• Only borrow:

• When no grant-financing alternatives available

• For medium/long term borrowing

• Best loan financing option selected:

• Take into account floating/fixed rate interest rate options, maturity, grace period, currency

• Use concessional (e.g. IDA) debt options if available low interest rate, long grace and repayment periods

6. Debt Management

31

6. Debt management

• Good debt management information system: comprehensive, accurate, timely

• Use IT packages, for example:

• DMFAS (UNCTAD)

• CS-DRMS (CommonWealth)

Loan Guarantees

Government needs clear strategy for issuing guarantees to guard against contingent liabilities becoming actual liabilities

Includes guarantees to sub-national governments, state owned enterprises & private companies

6. Debt Management

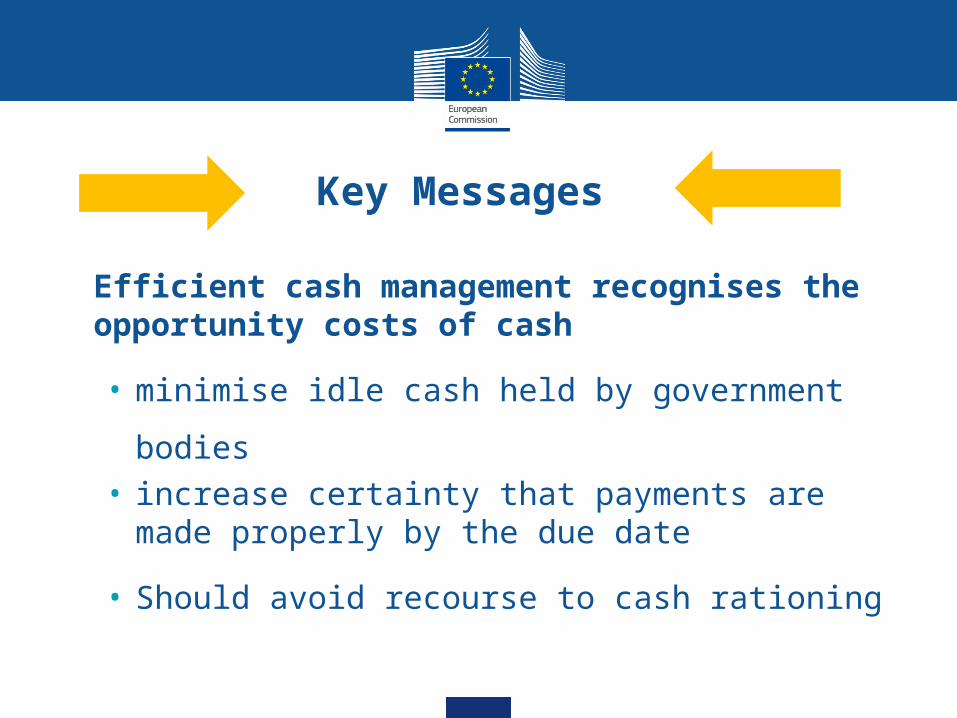

Key Messages

• Efficient cash management recognises the opportunity costs of cash

• minimise idle cash held by government bodies• increase certainty that payments are made

properly by the due date

• Should avoid recourse to cash rationing

Key Messages

• Directions for improving cash management • Preparing regularly cash forecasts• Moving to a Treasury Single Account

• Cash and debt management should be closely coordinated

Related Documents