30 ISSN: 2635-2966 (Print), ISSN: 2635-2958 (Online). ©International Accounting and Taxation Research Group, Faculty of Management Sciences, University of Benin, Benin City, Nigeria. Available online at http://www.atreview.org Original Research Article Moderating Effect of Free Cash Flow and Managerial Ownership on Earnings Management of Listed Conglomerate Firms in Nigeria Hamisu Suleiman Kargi 1 & Musa Zakariya 2 1 Department of Accounting, ABU Business School, Ahmadu Bello University, Zaria – Nigeria. [email protected] 2 Department of Accounting, Kaduna Polytechnic, Kaduna – Nigeria. Email: [email protected] For correspondence, email: [email protected] Received: 03/06/2021 Accepted: 29/06/2021 Abstract Financial reports, which ordinarily should provide a true and fair view of the firm's performance and financial status as of the reporting date, are manipulated due to the opportunistic behaviour of some managers. The separation of ownership and control forms the basis of divergent motivation between stockholders and management, resulting in a conflict of interest and agency costs. The management tends to abuse their trust in the presence of excess cash flow in a firm to pursue personal interest while reporting good financial performance. Managerial ownership is considered an important component of ownership structures to mitigate the conflict between managers and shareholders. This study examined the moderating effect of managerial ownership on the relationship between free cash flow and earnings management of conglomerate firms listed on the Nigerian Stock Exchange as at December 31 2017. The study was conducted on all 6 conglomerate firms listed on the Nigerian stock exchange from the period 2005 to 2017. The study used a correlational research design and secondary data from the firms' annual reports and accounted for the periods. Multiple regression was employed in analysing the data. The results showed that free cash flow has a positive and significant effect on earnings management. Managerial ownership has a negative and significant effect on earnings management. In comparison, managerial ownership interaction with free cash flow on earning management has an insignificant negative effect. The study concludes that managerial ownership may likely reduce earnings management in the presence of free cash flow in listed conglomerate firms in Nigeria. Based on the study's findings, it is recommended that managers be encouraged to increase their shareholdings in the firms to better align their

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Accounting & Taxation Review, Vol. 5, No. 2, June 2021

30

ISSN: 2635-2966 (Print), ISSN: 2635-2958 (Online).

©International Accounting and Taxation Research Group, Faculty of Management Sciences,

University of Benin, Benin City, Nigeria.

Available online at http://www.atreview.org

Original Research Article

Moderating Effect of Free Cash Flow and Managerial Ownership

on Earnings Management of Listed Conglomerate Firms in

Nigeria

Hamisu Suleiman Kargi1 & Musa Zakariya

2

1 Department of Accounting, ABU Business School, Ahmadu Bello University, Zaria –

Nigeria. [email protected]

2 Department of Accounting, Kaduna Polytechnic, Kaduna – Nigeria. Email:

For correspondence, email: [email protected]

Received: 03/06/2021 Accepted: 29/06/2021

Abstract

Financial reports, which ordinarily should provide a true and fair view of the firm's

performance and financial status as of the reporting date, are manipulated due to the

opportunistic behaviour of some managers. The separation of ownership and control forms

the basis of divergent motivation between stockholders and management, resulting in a

conflict of interest and agency costs. The management tends to abuse their trust in the

presence of excess cash flow in a firm to pursue personal interest while reporting good

financial performance. Managerial ownership is considered an important component of

ownership structures to mitigate the conflict between managers and shareholders. This study

examined the moderating effect of managerial ownership on the relationship between free

cash flow and earnings management of conglomerate firms listed on the Nigerian Stock

Exchange as at December 31 2017. The study was conducted on all 6 conglomerate firms

listed on the Nigerian stock exchange from the period 2005 to 2017. The study used a

correlational research design and secondary data from the firms' annual reports and

accounted for the periods. Multiple regression was employed in analysing the data. The

results showed that free cash flow has a positive and significant effect on earnings

management. Managerial ownership has a negative and significant effect on earnings

management. In comparison, managerial ownership interaction with free cash flow on

earning management has an insignificant negative effect. The study concludes that

managerial ownership may likely reduce earnings management in the presence of free cash

flow in listed conglomerate firms in Nigeria. Based on the study's findings, it is recommended

that managers be encouraged to increase their shareholdings in the firms to better align their

Kargi & Zakariya. Moderating Effect of Free Cash Flow…

31

interests with that of other shareholders and reduce their opportunistic tendencies. Also,

shareholders and management should exercise good governance practices to identify viable

investment projects into which excess cash flow may be channelled to reduce the managers'

motivation for opportunistic behaviours.

Keywords: Free Cash Flow, Earnings Management, Managerial Ownership, Conflict of

Interest.

JEL Classification Codes: M40

This is an open access article that uses a funding model which does not charge readers or their institutions for access and is

distributed under the terms of the Creative Commons Attribution License. (http://creativecommons.org/licenses/by/4.0) and

the Budapest Open Access Initiative (http://www.budapestopenaccessinitiative.org/read), which permit unrestricted use,

distribution, and reproduction in any medium, provided the original work is properly credited.

© 2020. The authors. This work is licensed under the Creative Commons Attribution 4.0 International License

Citation: Kargi, H.S., & Zakariya, M. (2021). Moderating effect of free cash flow and

managerial ownership on earnings management of listed conglomerate firms in

Nigeria. Accounting and Taxation Review, 5(2): 30-52.

1. INTRODUCTION

The separation of ownership and control in

todays' business world raises serious

concerns and give rise to a conflict of

interest between the shareholders and the

management. The management are expected

to pursue firms' growth towards the

maximisation of the interest of its

stakeholders and as well report the result of

their stewardship. However, conflict of

interest creates the possibility that the

management will not act in the best interests

of the shareholders. These days, reports on

firms' performance are grossly falsified to

enhance published financial statements

artificially. Financial information that

ordinarily should provide a true and fair

view of a firm's performance and financial

status as at the reporting date is manipulated

due to the managers' interest (Uwuigbe,

Ranti, & Bernard, 2015). Consequently, the

public, especially the shareholders, are

misled and have since lost confidence and

trust in the integrity of accounting

information reported to them.

Firms report robust and excellent

performance in their financial reports and

accounts, and not long from such good

reports, they go distressed and collapsed.

Hence, one wonders whether the reports are

credible and reliable in their reflection of

the firm's performance or are mere

manipulating accounting numbers to

mislead their stakeholders in decision

making. The managements have incentives

to manipulate the earnings to maximise their

wealth and possibly the company. Thus, the

financial report presented to the

shareholders may not reflect the company's

true position and, on the other hand, may

encourage fraud and material misstatement

by the reporting companies as this involves

a higher degree of managerial judgment.

This led to growing attention by researchers

Accounting & Taxation Review, Vol. 5, No. 2, June 2021

32

on the quality of earnings reported by

management after the global corporate

financial scandals around the world (Al-

Dhamari & Ismail, 2014).

The manipulation of earnings known as

earnings management occurs when

managers use their judgment in financial

reporting and in structuring transactions to

alter financial reports to either mislead some

stakeholders about the underlying economic

performance of the company or to influence

their contractual outcomes that depend on

reported accounting numbers. The

separation of ownership and control forms

the basis of divergent self-interest

motivation between stockholders and

management. Both seek to maximise their

utility and self-interest, this causes conflicts.

However, since the managers have effective

control of the firm, they have the incentive

and the ability to derive more benefits at the

expense of the shareholders. The costs

associated with the divergence of interest

between the shareholders and the managers

are referred to as agency costs which consist

of; the monitoring cost by the shareholders,

the bonding cost by the management and

losses associated with the sub-optimal

decisions of the management.

One situation that could lead to a conflict of

interest between management and

shareholders is when the firm has excess

cash flow in hand with no available

profitable investment opportunities. The

management tends to abuse the free cash

flow, which results in increased agency

costs, inefficiency in resource allocation and

wrongful investment in projects with

negative net present value. The implication

is that the excessive free cash flow situation

encourages unnecessary management waste

and inefficient resource utilisation (Jensen

1986). Free cash flow is one of such critical

economic conditions under which firm

manager's exhibit behavioural patterns that

may have a severe financial implication on

firm survival and profitability.

The opportunistic behaviour of managers

has brought down big corporations which

were earlier considered be "too big to fail"

to a state of total collapse. Evidence of the

failure of such financial giants includes the

case of Xerox in the year 2000, Enron

Corporation in 2001, WorldCom in May,

2002, Tyco in 2002 and many others and led

to the enactment of the Sarbanes-Oxley Act

of 2002. Other cases include Citibank in

2005, American International Group (AIG)

in 2005, Lenman Brothers in 2008, Saytam

in 2009, Toshiba in 2015 and Kobe steel in

2018, among others. These corporations

initially commanded strong financial respect

by their appearance to have provided sound

financial performance. However, it was later

discovered that they were engaged in

earnings manipulations to produce attractive

economic outcomes (Litt, Sharma, &

Sharma 2013).

Similarly, in Nigeria, some managers were

involved in serious financial crimes by

Chief Executive Officers of some banks like

Oceanic Bank International Nigeria Plc,

Intercontinental Bank Plc, Bank PHB Plc,

Afribank Nigeria Plc, Finbank Plc, and

Equitorial Trust Bank Ltd, leading them to

financial distress and liquidation (Sanusi,

2010). These crimes include window

dressing of accounts, embezzlement,

creative accounting, insider trading and lots

more. Furthermore, the financial scandal of

Cadbury Nigeria Plc in 2006 provides

evidence of earnings manipulation. It was

alleged that the company's management

deliberately overstated their financial

position over a number of years ranging

Kargi & Zakariya. Moderating Effect of Free Cash Flow…

33

between 13 billion to 15 billion Naira

(Ajayi, 2006; Sunday Times, 2007).

In an attempt to reduce conflicting interest

between the owners and managers of

businesses as well as guaranteeing an

improvement in the quality and reliability of

financial reports produced by the firm,

various governments and regulators around

the world have been focusing on corporate

governance and ownership structure

components (managerial ownership,

institutional investors, and block-holders).

Some studies indicate that managerial

ownership influences the monitoring

mechanism a firm adopts including

monitoring earnings management practices

(Dalton et al., 2003; Gulzar & Wang, 2011;

Liu, 2012). Jensen (1986) believes that

shareholders can reduce divergences from

their interests by establishing appropriate

incentives for the managers designed to

restrict the aberrant activities of the

management. Managerial ownership is

considered an important component of

ownership structures to mitigate the conflict

between managers and shareholders. In

Nigeria, there is legislative support for this

issue. Managerial ownership disclosure is a

stipulation of the Companies and Allied

Matters Act, 2020 and the Code of

Corporate Governance 2007 (as amended),

which should be adhered to by all Listed

Companies.

In developed economies, a reasonable

research effort was made in respect of the

relationship between free cash flow and

earnings management. These include the

works of; Jones and Sharma (2001), Chung,

Firth and Kim (2005), Mehdi, Ines, Tawhid

and Faten (2016) carried out in Australia,

the United States of America and France,

respectively. Similarly, in developing

economies, some studies have examined this

relationship. These include the works of;

Bukit and Iskandar (2009) and Fabricio,

Cardoso and Arildelmo (2014) carried out in

Malaysia, India, Brazil and Iran,

respectively. However, Nigeria is different

from these countries in terms of micro and

macro-economic realities, legal and

environmental issues, institutional

arrangements and corporate governance

mechanism sophistication, which may

constitute a motivating factor for earnings

manipulation.

This study attempts to empirically examine

the moderating effect of managerial

ownership on the relationship between free

cash flow and earnings management of

firms in Nigeria. The domain of the study is

listed conglomerate firms in Nigeria. The

motivation for choosing conglomerates

firms is that they constitute firms that are

critical to the development of the country's

real economic sector in Nigeria. It was also

revealed that large-scale multi-faceted

earnings management is associated chiefly

with conglomerates. Due to their unique

structure, they can transfer profitable or

toxic assets to/from their subsidiaries,

related party transactions and so on (Mehta

& Srivastavaare 2009; Yero & Shehu,

2013).

The main objective of this study was to

empirically examine the effect of free cash

flow and managerial ownership on earnings

management of listed conglomerate firms in

Nigeria. The other objective is to

investigate the moderating effect of

managerial ownership on the relationship

between free cash flow and earnings

management of listed conglomerate firms in

Nigeria. In line with the objectives of the

study, it was hypothesised that; free cash

flow has no significant effect on earnings

management of listed conglomerate firms in

Accounting & Taxation Review, Vol. 5, No. 2, June 2021

34

Nigeria, managerial ownership has no

significant effect on earnings management

of listed conglomerate firms in Nigeria and

managerial ownership has no significant

moderating effect on the relationship

between free cash flow and earnings

management of listed conglomerate firms in

Nigeria. The study will cover the period of

13 years from 2005 to 2017, shortly after

introducing the Codes of Corporate

Governance by the Nigerian Securities and

Exchange Commission in 2003 and revised

in 2011. The codes ensure the disclosure of

managerial ownership in the annual report

and accounts of firms in Nigeria.

2. LITERATURE REVIEW

Earnings management is seen as the

manipulation of records to report sound

financial performance over a given period.

According to Schipper (1989), earnings

management also referred to as "disclosure

management" is a situation where

management purposefully intervenes in the

external financial reporting process to

obtain some private gains. The Certified

Fraud Examiners (1993) view earnings

management as "the deliberate

misrepresentation of the financial condition

of an enterprise accomplished through

intentional misstatement or omission of

amounts or disclosure in the financial

statement to deceive financial statement

users". This view considers earnings

management as a fraudulent activity of

management being accomplished through

deception.

There are various foundational managerial

motivations to manage earnings. These

include situations when a company makes a

loss in the preceding accounting year;

Influencing short-term stock prices and

fulfilling capital market expectations

amongst others. Dechew and Sloan (1991)

revealed that chief executive officers in their

later years in office reduce expenditures on

research and development with a view to

increaseing reported earnings. They argue

that this behaviour characterises the short

term nature of many chief executive's

compensation plans. Furthermore, their

study provides support that at least some

managers engages in earnings management

practices in order to accelerate bonus

awards or to secure their jobs.

According to Iturriaga and Hoffmann

(2005), earnings management may emerge

due to agency problems. Managers could

manage earnings to window dress financial

reports to improve their position, obscuring

facts that stakeholders should know or

influence contractual outcomes dependent

on reported accounting numbers.

Furthermore, Roman (2009) opined that

"earnings management occurs when

management has the opportunity to make

accounting decisions that change reported

income and exploit those opportunities".

The availability of excess cash at the

management's disposal in a firm known as

free cash flow (FCF) is one factor that

avails the management with means of

earnings manipulation. According to Bangi,

Medan and Shah (2012), free cash flow can

be viewed as the amount of cash flow above

required for investments in profitable

projects or those with positive net present

values when discounted at the relevant cost

of capital. Also, free cash flow is internally

generated capital, which can be used when

companies cannot obtain external funds due

to an inefficient or imperfect market or

information asymmetry between the

management and capital providers. In the

view of Masky and Chen (2012), FCF

means not just cash flow that is cost-free but

also the cash flow that the manager has the

Kargi & Zakariya. Moderating Effect of Free Cash Flow…

35

discretion to do whatever it wants with

provided their actions may not result in the

firm getting out of business. This could lead

to suboptimal decisions by management.

FCF can be seen as the discretionary

accruals that management presents in

financial reports. According to Lehn and

Poulsen (1989), FCF is defined as net

operating income before depreciation

expenses, after-tax expenses, interest

expenses, and stock dividends, divided by

the total book value of the company's asset

in the previous year. Copeland (1995)

defined free cash flow as "the operating

income after tax plus non-cash expenses

after deducting the investments on working

capital, property, plant, equipment and other

assets". This view is similar to the definition

of Len and Poulson (1989), with little

modification to take care of asset

replenishment expenditures. Mehdi, Tawhid

and Faten (2016) free cash flow was viewed

as the sum of the surplus funds available

after funding profitable projects. These

definitions appear to be very clear and can

be identified in the financial reports of the

firms. Thus, it is the most widely used in

most literature on free cash flow and is the

definition adopted in this study.

Jensen (1986) observed that in firms with

high free cash flows and low growth levels,

the managers are often encouraged to apply

these funds to satisfy their self-motivation

against the maximisation of the

shareholders' interest. Jensen theorised that

managers invest the surplus funds in

investments having negative net present

value rather than sharing the free cash flows

among shareholders, consequently reducing

the market value of the firms. As such,

managers of these firms make an effort to

manipulate the present situation by using

discretionary accruals to increase earnings

to realise their self-motivations.

The presence of free cash flow in a firm

increases earnings management and conflict

of interest between the shareholders and the

management. Jensen (1984) opined that

corporate governance practice in managerial

ownership could address this conflict.

Davies Hillier and McColgan (2005)

believed that managerial ownership was the

manager's stake in a firm, including all

board members, share ownership. Juliarto,

Tower, Zahn and Rusmin, (2013) define

managerial ownership as a "percentage of

shares held by insiders, such as CEO and

directors". From the above definitions, it

appears Juliarto et al. (2013) provides a

more statistically significant view of the

concept as it measures managerial

ownership as a ratio of manager's ownership

to total ownership of the firm.

Some studies suggested that managerial

ownership is influential in reducing earnings

management (alignment of interest

hypothesis). Managers with a high

ownership interest in the firm are less likely

to alter earnings for short term private gains

at the expense of outside shareholders.

Managers whose interest is consistent with

shareholders are more likely to report

earnings that reflect the underlying

economic value of the firm. Similarly, in all

models, Sandra (2012) documented that

managerial ownership is significantly

negatively related to earnings management,

which is consistent with the alignment of

interest hypothesis; the negative relationship

suggests that the higher managerial

ownership, the lower the magnitude of

discretionary accounting accruals.

Managers' stake in the firm's capital could

play the role of an insider in ensuring that

free cash flow is only utilised for the long-

Accounting & Taxation Review, Vol. 5, No. 2, June 2021

36

term gains of the company, which

maximises the interest of the shareholders.

Agency theorists believe that managerial

ownership would provide inputs into the

process of decision making in a firm (Jensen

& Meckling, 1976). Alignment theorists

specifically state that insider ownership

helps align the managers' interest with that

of the owners (Ang., Cole & Lin 2000;

Jensen & Meckling, 1976; Singh &

Davidson, 2003). Managerial ownership is

believed to play an active monitoring role in

using the company's free cash flow to

ensure that only projects having value-

added attributes are executed. Warfield,

Wild, & Wild (1995) uncovered that

managerial ownership is positively

associated with the informativeness of

accounting earnings. They provide evidence

that the association between stock returns

and accounting earnings was significantly

more significant for firms with higher

managerial ownership.

Jaggi and Gul (2000) revealed a direct

positive relationship between earnings

management (discretionary accruals) and

high free cash flows in low growth firms. In

another study, Mehdi et al. (2016)

empirically examine free cash flow and

earnings management: the moderating role

of governance and ownership from the

French perspective. The result revealed that

the percentage of capital held by managers

and free cash flow level was found to have a

positive relationship. However, according to

the findings of Warfield et al. (1995),

managerial ownership has a significant

negative effect on earnings management in a

free cash flow situation. This implies that

managerial ownership has a reducing

moderating impact on the managers'

propensity to engage in earnings practices in

a free cash flow situation.

Raeisi and Vaez (2016) conducted a study

in Tehran covering the period 2009 to 2015,

using the information of 170 companies

chosen by systematic elimination sampling

method; the study results indicate that there

is a significant positive relationship between

free cash flow and earnings management. It

was further revealed that managerial

ownership interacting with Free Cash Flow

(FCF) significantly decreases the

relationship between free cash flow and

earnings management. Rezizadeh and

Talebnia (2016) have similar findings. This

implies that in a free cash flow situation, an

increase in managerial ownership reduces

the motivation of the managers for earnings

management practices.

The presence of free cash flow is one source

of conflict between Shareholders and the

management of a firm. The emphasis is on

the misuse of free cash flow by

management. Jensen first mentioned the free

cash flow hypothesis in 1986. This

hypothesis implies that excessive free cash

flow situation encourages unnecessary

management waste and inefficiency in

allocating resources (Jensen 1986). In

addition, agency theory provides a robust

theoretical framework for analysing the

behaviour of managers in firms' studies. The

theory argued that the separation of

ownership and control forms the basis of

divergent self-interest motivation between

stockholders and management. The concept

of Agency theory formalised by Jensen and

Meckling (1976) provides a framework to

examine contractual relationships when one

party, the principal, engages another party,

the agent, to delegate responsibility to the

latter. It was modelled to explain the

relationship between the shareholders and

the management of firms similar to one

between a principal and an agent. Therefore

Kargi & Zakariya. Moderating Effect of Free Cash Flow…

37

this study is under fined on agency theory

and the free cash flow hypothesis.

Modelling Framework

Based on the theoretical and empirical

review, a framework has been developed on

the study's variables. The reviews suggest

that managerial ownership may reduce the

managers' motivation for earnings

management; hence, the introduction of

managerial ownership to moderate the

relationship between free cash flow and

earnings management. It proposes that free

cash flow has a positive relationship with

earnings management. The model comprises

four variables; free cash flow, earnings

management, managerial ownership and

firm size (figure 1).

Figure 1: Modelling Framework

Moderator Variable

Independent Variable Dependent Variable

Control Variable

Source: Adapted from Popoola, Ratnawati & Hamid (2016)

3. METHODOLOGY

This study adopted the correlation research

design. In line with the positivist approach,

the strategy adopted is considered adequate

and appropriate because it allows for testing

the expected relationships between free cash

flow, moderating role of managerial

ownership and earning management of

listed conglomerate firms in Nigeria. It

gives room for the quantitative data

collection on the study variables and

analysing same using descriptive and

inferential statistics. The population and

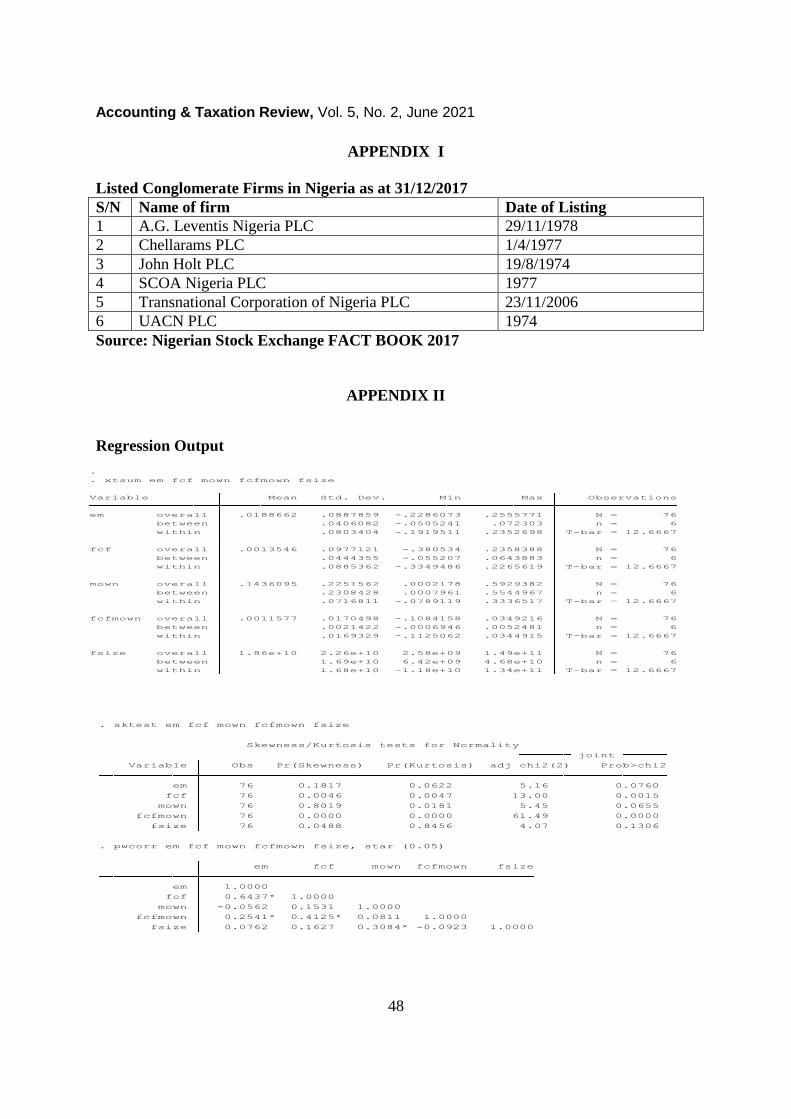

sample of the study consist of all the six (6)

conglomerate firms listed on the Nigerian

Stock Exchange as at December 31 2017

(appendix I). Thus, the study adopted a

census sampling. Data for the analysis was

obtained from the annual reports and

accounts of the listed conglomerate firms in

Nigeria for 13 years from 2005 to 2017. The

panel multiple regressions were adopted to

test the hypotheses of the study empirically.

This is because it helps assess the

relationship between free cash flow and

earnings management of listed

conglomerate companies on the Nigeria

Stock Exchange. Unbalanced panel data

methodology was used as it has the feature

of both time series and cross-sectional.

To examine the effect of managerial

ownership on the relationship between free

Firm Size (FSIZE)

Managerial

Ownership (MOWN)

(MOWN)WWWWN

Free Cash flow (FCF)

Earnings

Management (EM)

Accounting & Taxation Review, Vol. 5, No. 2, June 2021

38

cash flow and earnings management of

listed conglomerate firms in Nigeria, this

study has earnings management as the

dependent variable. In contrast, the

independent variable is free cash flow,

managerial ownership as a moderating

Variable and Firm Size as a control

Variables. Table 1 below shows the

variables of the study, their measurements

and sources.

Table 1. Variable Measurement

Variable/proxy Measurement Source

Earnings Management

(EM)

Discretionary Accruals Residuals Kothari et al. (2005)

Free Cash Flow

(FCF)

Operating Income before depreciation,

after-tax expense, interest payable,

preferred & common stock dividend

divided by the book value of the

company's asset

Lehn and Poulson

Model (1989)

Managerial

Ownership (MOWN)

% of Total shares held by Directors Farouk and Bashir

(2017)

FCFMOWN Free Cash Flow interacted with

Managerial Ownership of firms

Reza and Ghodratalah

(2016)

Firm Size (FSIZE) The Natural log of total Assets Popoola, Ratnawati&

Hamid (2016), Farouk

and Bashir (2017)

Source: Compiled by the Author, 2019

Earnings Management Measurement

The study adopts the performance-based

Jones accrual model considered by scholars

as to the best choice among other models in

estimating earnings management (Kothari,

Leone &Wasley, 2005). The study runs

multiple regressions on the panel data with

total accruals as the dependent variable. The

residual values from this regression model

give the absolute values of discretionary

accruals representing the extent of

opportunistic earnings management.

The model is specified as follow:

TAi,t/Ai,t-1 = α0(1/TAi,t-1)+α1[(ΔREVi,t- ΔRECi,t)/Ai,t-1]+α2(PPEi,t/Ai,t-1)+α3(ROAi,t-1)+εi,t

Where;

TAi,t = total accruals of firm i in year t (total net income-cash flow from operations)

Ai,t-1 = total assets at the beginning of the period of firm i

ΔREVi,t = change in sales between year t and year t-1 of firm i

ΔRECi,t = change in receivable between year t and year t-1 of firm i

PPEi,t = gross value of fixed assets in year t of firm i

ROAi,t-1 = ratio of net Income of firm i to total asset at the beginning of the period

Kargi & Zakariya. Moderating Effect of Free Cash Flow…

39

α0 = constant

α1, α2, α3 = coefficients

εit = residual (prediction error)

Free Cash Flow Measurement

Free cash flow - FCF as defined by Lehn

and Poulson model (1989) was adopted for

this study. FCF was measured as operating

profit before depreciation, after-tax expense,

interest payable, preferred and common

stock dividends divided by the total book

value of the company's asset.

The model is specified as follow:

FCFi,t = (INCi,t - TAXi t - INTEPi,t - PSDIVi,t -CSDIVi,t) /Ai,t-1

Where:

FCFi,t = free cash flow of firm i at year t

INCit = operating income before depreciation of firm i at year t

TAXi,t = total taxes of firm i at year t

INTEPi,t = interest expense of firm i at year t

PSDIVi,t = preferred stock holders’ dividends of firm i in year t

CSDIVi,t = common stock holders’ dividends of firm i at year t

Ai,t-1 = total assets carrying value of firm i in year t-1

Model Specification

The dependent variable for this study is

earnings management proxy by

Discretionary Accruals as measured by

Kothari et al. (2005). This model is

considered more relevant because it clearly

explains earnings management to

stakeholders and other prospective investors

that need information concerning the firms.

The study would employ free cash flow as

an independent variable and managerial

ownership as a moderator. The model below

was adopted based on logical and extant

literature in testing the hypotheses of the

study.

EMi,t =αO+α1FCFi,t+ α2MOWNi,t + α3FCFMOWNi,t + α4FSIZEi,t + ei,t

Where;

EMi,t = earnings management of firm i at year t

FCFi,t = free cash flow of firm i at year t

MOWNi,t = managerial ownership of firm i at year t

FCFMOWNi,t = moderation of free cash flow with managerial ownership of firm i at year t

FSIZE = firm size of firm i at year t

α0 = constant

α1,2,3,4, = coefficient of the regression model

it = firm and time

Accounting & Taxation Review, Vol. 5, No. 2, June 2021

40

e = error term

The robustness tests were conducted to improve the validity of statistical inferences. These

comprise normality, multicollinearity, heteroscedasticity and Hausman tests.

4. ESTIMATION RESULT AND DISCUSSION

Correlation Matrix

Table 2: Correlation Matrix

Variables EM FCF MOWN FCFMOWNS FSIZE

EM 1.000

FCF 0.6437 1.000

MOWN -0.0562 0.1531 1.000

FCFMOWN 0.2541 0.4125 0.0811 1.000

FSIZE 0.0762 0.1627 0.3084 -0.0923 1.000

Source: Correlation matrix result using STATA 13.0

Table 2 displayed the Pearson correlation

coefficient between all pairs of variables in

the study. Table shows the relationship

between the dependent, independent,

moderator and control variables under

study. The correlation matrix in Table 2

indicates a positive and robust relationship

between earnings management (EM) and

free cash flow from the correlation

coefficient of 0.6437. The result suggests

that earnings management will likely

increase with an increase in the free cash of

the firms. However, there is a negative and

weak correlation between earnings

management and managerial Ownership

(MOWN) from the correlation coefficient of

-0.0562. The negative coefficient implies

that earnings management likely decreases

with an increase in managerial ownership.

Further, the table shows a significant

positive relationship between FCFMOWN

and earnings management, as demonstrated

by the correlation coefficient of 0.2541.

Implying that earnings management

increases with the interactive variable

FCFMOWN. However, the relationship is

weak even though it is significant.

Concerning the control variable, the table

shows that firm size (FSIZE) has a positive

and weak correlation with earnings

management with a coefficient of 0.0762.

Considering the correlation coefficients

among the independent variables, the result

shows no problem of harmful

multicollinearity among the independent

variables as all the correlation coefficients

were below 0.80.

Test of Hypotheses

To test the hypotheses of the study certain

robustness tests were conducted. The result

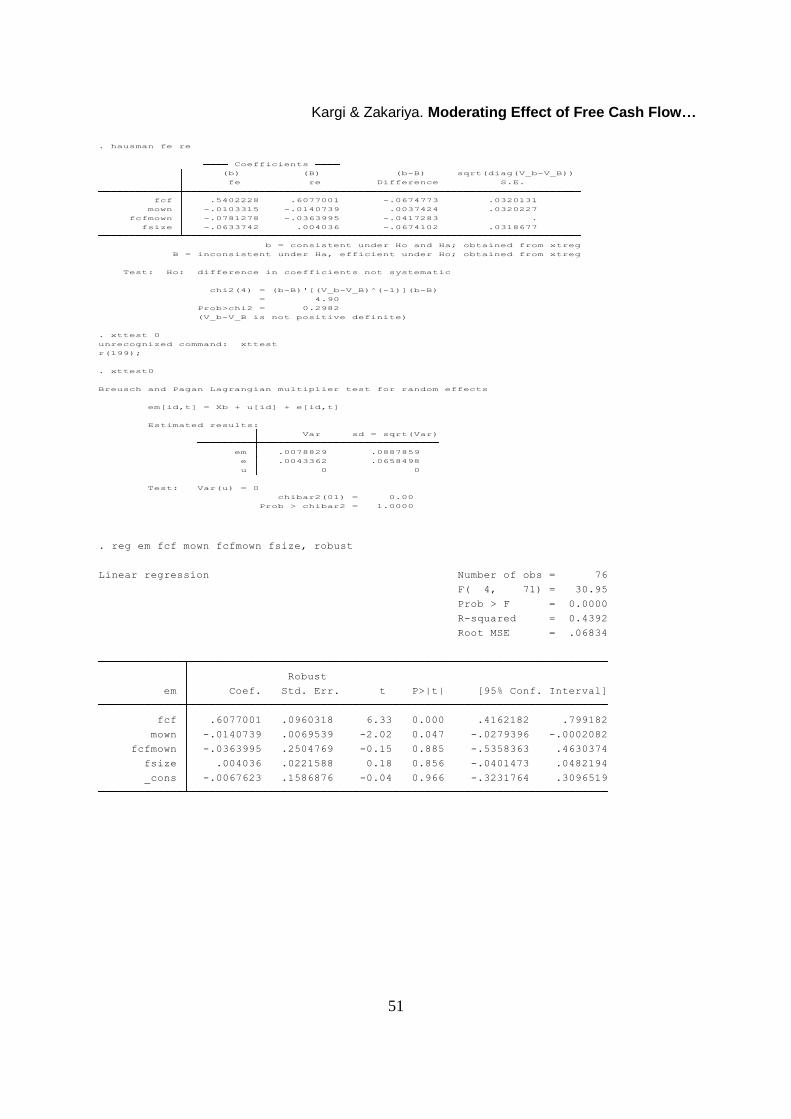

of Breusch- pagan / Cook-Weisbaerg test

for the study (appendix II) indicates the chi2

value of 2.23 with the p-value of 0.1354

suggesting the absence of

heteroscedasticity. The hausman

Kargi & Zakariya. Moderating Effect of Free Cash Flow…

41

specification test was also carried out to

determine the most efficient model between

the fixed and random effect. The test result

(appendix II) revealed that the value of chi2

is 4.90 with the prob>chi2of 0.2982. The

insignificant value as reported by the

probability of chi2 indicates that the

individual effects are random not fixed in

the model hence fixed effect model is

rejected in favour of Random effect model

which is better specified. Further a Breusch

and Pagan lagrangian multiplier test for

random effect was conducted to choose

between the random effect result and OLS

regression. The result revealed that the chi2

value is 0.00 with prob>chi2 = 1.00 thus

suggesting that random effect is not

appropriate (there is no panel effect) and the

100% p-value can be explained from the

indifference in the coefficient, error term

and t-value of both random effect model and

OLS model indicating that the pooled OLS

is not different from the random effect

model. Thus the study conducts and

interprets the Robust OLS. The justification

for this is because the study fails to reject

the null hypothesis in respect of Lagrangian

Multiplier test for random effect model

which states that there is no panel effect. In

addition, the study further conducts the

kernel density test and the curve shows a

bell shape signifying that the data of the

variables used for the study are normally

distributed (appendix III).

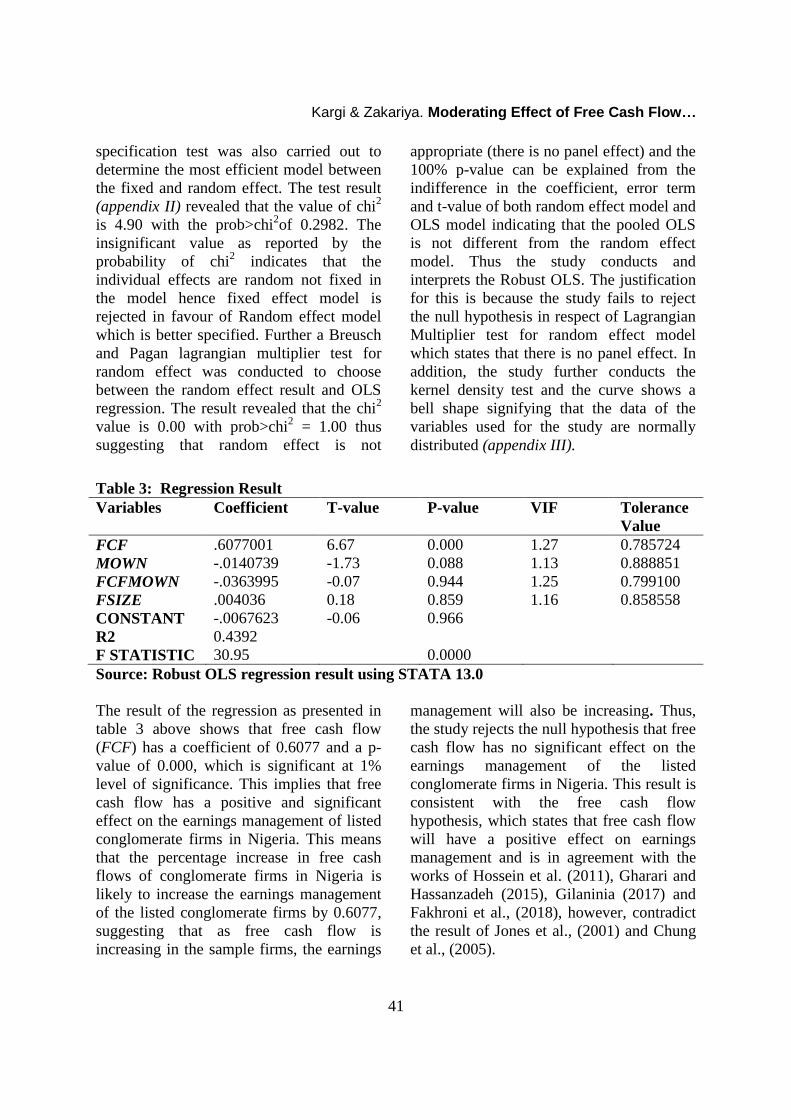

Table 3: Regression Result

Variables Coefficient T-value P-value VIF Tolerance

Value

FCF .6077001 6.67 0.000 1.27 0.785724

MOWN -.0140739 -1.73 0.088 1.13 0.888851

FCFMOWN -.0363995 -0.07 0.944 1.25 0.799100

FSIZE .004036 0.18 0.859 1.16 0.858558

CONSTANT -.0067623 -0.06 0.966

R2 0.4392

F STATISTIC 30.95 0.0000

Source: Robust OLS regression result using STATA 13.0

The result of the regression as presented in

table 3 above shows that free cash flow

(FCF) has a coefficient of 0.6077 and a p-

value of 0.000, which is significant at 1%

level of significance. This implies that free

cash flow has a positive and significant

effect on the earnings management of listed

conglomerate firms in Nigeria. This means

that the percentage increase in free cash

flows of conglomerate firms in Nigeria is

likely to increase the earnings management

of the listed conglomerate firms by 0.6077,

suggesting that as free cash flow is

increasing in the sample firms, the earnings

management will also be increasing. Thus,

the study rejects the null hypothesis that free

cash flow has no significant effect on the

earnings management of the listed

conglomerate firms in Nigeria. This result is

consistent with the free cash flow

hypothesis, which states that free cash flow

will have a positive effect on earnings

management and is in agreement with the

works of Hossein et al. (2011), Gharari and

Hassanzadeh (2015), Gilaninia (2017) and

Fakhroni et al., (2018), however, contradict

the result of Jones et al., (2001) and Chung

et al., (2005).

Accounting & Taxation Review, Vol. 5, No. 2, June 2021

42

From the regression result in table 3,

managerial ownership (MOWN) has a

coefficient of -0.0140739 and a p-value of

0.088, which is significant at 10%.This

implies that managerial ownership has a

negative and significant effect on earnings

management of listed Conglomerates firms

in Nigeria. This means that a percentage

increase in managerial ownership will

reduce the firms' earnings management by

1.4073%. Suggesting that increase in

managerial interest in the shareholdings of

the firms will reduce the managers' tendency

to commit acts of earnings management. It

further means that managers will not want

to take action that will affect their stock

returns; they tend to reduce their

opportunistic behaviour when their

shareholding interests are growing. Based

on this result, the study rejects the null

hypothesis, which states that managerial

ownership has no significant effect on the

earnings management of the listed

conglomerate firms in Nigeria. This result is

also consistent with the alignment of interest

hypothesis and it is in agreement with the

works of Kazemian (2015); Obigbemi,

(2017) and Wiyadi, Tyas ,Trisnawati and

Sasongko, (2017). However, contradicts the

results of Sandra, (2012), Alves, (2012),

Popoola (2016) and Farouk and Bashir

(2017).

Furthermore, from Table 3, free cash flow

moderated by managerial ownership

(FCFMOWN) has a coefficient of -.0363995

and a p-value of 0.949, implying

insignificance. This implies that managerial

ownership has a decreasing effect on

earnings management in a free cash flow

situation of listed conglomerate firms in

Nigeria; however, this effect is insignificant

at all levels of statistical significance. This

suggests that managerial ownership may not

possess the likelihood to reduce earnings

management in the presence of free cash

flow. Thus, suggesting that the interest of

the directors in the shareholders of the listed

conglomerate firms in Nigeria may not

curtail their opportunistic behaviour in the

presence of free cash flow. Based on this

result, although the negative coefficient

upholds the alignment of interest

hypothesis, managerial ownership does not

moderate due to its insignificance nature.

Hence, the study fails to reject the null

hypothesis that states that Managerial

ownership has no significant moderating

effect on the relationship between free cash

flow and earnings management of listed

Conglomerate firms in Nigeria. The result

of this study contradict the effect of Mehdi

et al. (2016); Raeisi and Vaez (2016), and

Rezizaded and Talebnia (2016).

The study's findings revealed that free cash

flow has a significant increasing effect on

earnings management of listed

conglomerate firms in Nigeria. This

signifies that when there is an increase in

excess cash in the firm, management

tendency to misbehave and act

opportunistically in the listed conglomerate

firms in Nigeria increases. This result is in

line with the free cash flow hypothesis and

agency theory which states that conflict of

interest arises between the managers and the

shareholders in free cash flow. Managers

may want to utilise the free cash flow to

benefit, thus creating room for earnings

management. This study is also in line with

the works of Gharari and Hassanzadeh

(2015), Zahra et al. (2015) and Fakhroni et

al. (2018) and contrary to the findings of

Jones et al. (2001).

The study's results further show that there is

a significant decreasing effect of managerial

ownership on earnings management of

Kargi & Zakariya. Moderating Effect of Free Cash Flow…

43

listed conglomerate firms in Nigeria. This

may be due to the managers' stake in the

firms, which makes them closely monitor

the firms' activities to ensure that

shareholders' funds are not appropriated.

Also, the managers' interest in the

shareholdings of the firm is not promoting

managers to maximise their utility function

as against the interest of the shareholders'

wealth maximisation. The findings are

consistent with the agency theory and also

in conformity with the works of Farouk and

Bashir (2017), Popoola, Ratnawati & Hamid

(2016), Sandra (2012), Alves (2012).

However, contrary to Wiyadi et al, (2017),

Kazemian and Zuraidah (2015).

In addition, the study found a decreasing

effect of managerial ownership moderated

with free cash flow on earnings

management of listed conglomerate firms in

Nigeria, though not significant. This finding

may be attributable to the manager's

ownership of listed conglomerate firms' play

in reducing earnings management. Thus, the

managers being part of the shareholders

may not affect how they could manage

earnings in the presence of excess available

cash in the listed conglomerate firms in

Nigeria. This study is contrary to the agency

theory and the research work Raeisi and

Vaez (2016).

Finally, the regression results presented

reveal that the relationship between firm

size and earnings management is positive

but insignificant. This finding suggests that

larger firms are more likely to use

discretionary accruals to manage their

earnings; however, size could not constitute

a significant factor motivating earnings

management practice among the managers.

This finding is in line with Naz, Bhatti,

Ghafoor and Khan (2011), Similarly, this

view is also supported by the findings of

Sun and Rath (2009). On the contrary,

Burgstahler and Dichev (1997) concluded

that both small and large firms engage in

managing earnings to circumvent the

decrease in earnings.

Policy Implication of the Findings

From the analysis conducted, the study's

findings may have implications to investors,

management and policymakers of

conglomerate firms in Nigeria. Firstly, a

critical significance of the results is based

on the fact that free cash flow is a

significant variable affecting the practice of

earning management; there is a possibility

that firms managers may want to take

advantage of excess cash available for their

benefit means their tendency to manipulate.

Therefore, policies should be instituted by

firms to deal with excess cash flows by

immediate profitable investment. Secondly,

regulatory bodies such as Securities and

Exchange Commission (SEC), Nigerian

Stock Exchange (NSE) and Financial

Reporting Council of Nigeria (FRCN)

should be aware of the possibility of

opportunistic behaviour among firms'

managers in conglomerate firms in Nigeria

when excess cash is available. They should

do more by introducing new standards and

reviewing existing ones to address grey

areas that make room for managers to

engage in earnings management in their

corporate governance practice.

5. CONCLUSION AND

RECOMMEDATIONS

The study has provided empirical evidence

on the utility of the explanatory variables in

explaining and predicting the extent of

earnings management of listed

conglomerate firms in Nigeria. The study

concludes that free cash flow and its

moderating effect by managerial ownership

Accounting & Taxation Review, Vol. 5, No. 2, June 2021

44

affect earnings management. However, free

cash flow has a significant positive effect

while managerial ownership and moderation

have negative effects that are significant and

insignificant, respectively.

Therefore, based on the study's findings, it

is recommended that managers be

encouraged to increase their shareholdings

in the firms to better align their interests

with that of other shareholders. This may

enable them to have more sense of

belonging, which may help reduce their

tendency to act opportunistically. Also,

shareholders and management should

exercise good governance practices to

identify viable investment projects into

which excess cash flow may be channelled

to reduce the managers' motivation for

opportunistic behaviours. In addition, firms

should institute an efficient internal control

system capable of monitoring the activities

of managers, and external auditors should

encourage the use ratios in evaluating the

performance of a company relative to its

resources, particularly cash, before forming

an independent opinion on the financial

statement to mitigate manager's chances of

engaging in earnings management practices.

The regulatory agencies such as FRCN,

SEC and NSE should enforce the

compulsory cash flow management policies

such as investment policy and dividend

policy to restore investors and creditors'

confidence.

REFERENCES

Al-Dhamari, R., & Ismail, K. (2014). An

investigation into the effect of surplus

free cash flow, corporate governance

and firm size on earnings predictability,

International Journal of Accounting and

Information Management, Vol. 22 No.

2, pp. 118-133.

Alves, S. (2012). Ownership structure and

earnings management: Evidence from

Portugal. Australasian Accounting,

Business and Finance Journal, 6(1), 57-

74.

Ang, J. S., Cole, R. A., & Lin, J. W. (2000).

Agency costs and ownership structure.

The Journal of Finance, 55(1), 81-106.

Bangi, J., Medan, N., & Shah, U. (2012).

Determinant of corporate cash holding:

Evidence from Canada: International

Journal of Economics and Finance. 4(1)

2014.

Berle, A. A., & Means, G. C. (1932). The

Modern Corporation and Private

Property: Macmillan, New York, 1932.

Bukit, R. B. & Iskandar, T. M. (2009).

Surplus Free Cash Flow, Earnings

Managementand Audit Committee: Int.

Journal of Economics and Management,

3(1), 204 – 223.

Burgstahler, D. Dichev, I. (1997). Earnings

management to avoid earnings decreases

and losses. Journal of Accountingand

Economics, 24, pp. 99–126.

Chung, R., Firth, M. & Kim, J. (2005).

Earning Management, Surplus Free

Cash Flow, and External Monitoring,

Journal of Business Research, 58, 766-

776.

Copeland, T. E., Weston, J. F. & Shastri, K.

(2005). Financial Theory and Capital

Policy, Boston, MA, Addison-Wesley.

Davies, J.R., Hillier, D. & Mccolgan, P.,

(2005). Ownership structure, managerial

behavior and corporate

value. Journal of Corporate Finance, 11

, 645-660.

Kargi & Zakariya. Moderating Effect of Free Cash Flow…

45

Dechow, P., & Sloan, R. (1991). Executive

Incentives and Horizon Problem: An

Empirical Investigation. Journal of

Accounting and Economics, 14, 51-89.

http://dx.doi.org/10.1016/0167-

7187(91)90058-S

Fabricio, T., Cardoso, A. & Aridelmo, J.

(2014). Free Cash Flow and Earnings

Management in Brazil: The Negative

Side of Financial Slack Global Journals

Inc. (USA) 8-11.

Fakhroni, Z., Ghozali, I., Harto, P., &

Yuyetta, E. N. A. (2018). Free cash

flow, investment inefficiency, and

earnings management: evidence from

manufacturing firms listed on the

Indonesia stock exchange. Investment

Management and Financial Innovations.

15, (1)

Farouk, M. A., & Bashir, N. M. (2017).

Ownership structure and earnings

management of listed conglomerates in

Nigeria. Indian-Pacific Journal of

Accounting and Finance, 1(4), 42-54.

Gharari, R., & Hassanzadeh, M. (2015).

Relationship between free cash flows

and discretionary accruals in Tehran

Stock Exchange. Arabian Journal of

Business and Management Review

(OMAN Chapter). 4(.11).

Gujarati, D. N. (2004). Basic Econometrics

(4th ed.). USA:Tata McGraw-Hill.

www.amazon.com

Gulzar, M. A., & Wang, Z. (2011).

Corporate governance characteristics

and earnings management: Empirical

evidence from Chinese Listed firms.

International Journal of Accounting and

Financial Reporting, 1(1), 133–151.

Healy, P., & Wahlen, J. (1999). A review of

the earnings management literature and

implications for standard setters.

Accounting Horizons. 13(4) 365-383.

Healy, P. M. (1985). The effect of bonus

schemes on accounting decisions.

Journal of Accounting and Economics,

7(1-3), 85-107.

Hossein, F., Isfandyari, M., Mohammad, K.,

Ali, B., & Narjes, K.J. (2011). Free cash

flows- information relevancy income

management.

Iturriaga, F. J. L. & P. S. Hoffiman .(2005).

Managers discretionary behavior,

earnings management and internal

mechanisms of corporate governance:

Empirical evidence from Chilean firm.

Corporate Ownership and Control, 3,(1)

17-29.

Jaggi, B., & Gul, A. (2000). Evidence of

accrual managerial: A Test of the free

cash flow and debt monitoring

hypothesis. Working Paper,

www.ssrn.com.

Jensen, M. C. (1986). Agency Costs of Free

Cash Flow, Corporate Finance and

Takeovers: American Economic Review,

76(2), pp.323-329.

Jensen, M. C., & Meckling, W. H. (1976).

Theory of the firm: Managerial

behavior, agency costs and ownership

structure: Journal of Financial

Economics, 3, (4) 305- 360.

Jones, S., & Sharma, R. (2001). The impact

of free cash flow, financial leverage and

accounting regulation on earnings

management in Australia's "old" and

"new" economies. Managerial Finance,

27 (12) 18–39.

Juliarto A,, Tower G., Zahn M. V., &

Rusmin R., (2013). Managerial

ownership influencing tunnelling

behaviour. Australasian Accounting,

Accounting & Taxation Review, Vol. 5, No. 2, June 2021

46

Business and Finance Journal 7(2)

article 3 p26-46

Kazemian, S., & Sanusi, Z. M. (2015).

Earnings management and ownership

Structure. Procedia Economics and

Finance, 31, 618-624.

Kothari, S.P., Leone, A.J., & Wasley, C.E.

(2005). Performance adjusted

discretionary accrual measures. Journal

of Accounting and Economics, 39, 163-

197.

Lehn, K., & Poulsen, A. (1989). Free cash

flow and stockholder gains in going

private transactions. The Journal of

Finance, 44(3), 771-787.

Litt, B., Sharma D., & Sharma V. (2013).

Environmental initiatives and earnings

management, Managerial Auditing

Journal, 29(1): 76-106.

Liu, J. (2012). Board monitoring,

management contracting and earnings

management: Evidence from ASX listed

companies. International Journal of

Economics and Finance, 4(12), 121–

136.

Masky, M. M. & Chen, G. T. (2012). Which

free cash flow is value relevant: The

case of the Energy Industry. Journal of

Finance and Accountancy.

Mehdi, N., Ines, F., Tawhid, C., & Faten, L.

(2016). Free Cash Flow And Earnings

Management: The Moderating Role Of

Governance And Ownership: The

Journal of Applied Business Research,

262-264.

Mehta, S., & Srivastavaare, R. (2009).

Reasons for Corporate Governance

failures. http/www.indianmha.

com/faculty_column/fc974/fc974html

(accessed feb. 2nd, 2011).

Naz, I., Bhatti, K., Ghafoor, A., & Husein,

H. (2011). Impact of firm size and

capital structure on earnings

management: Evidence from Pakistan.

International Journal of Contemporary

Business Studies, 2(12), 22-31.

Obigbemi, I.F. (2017). Ownership Structure

and the Earnings Management Practices

of Nigerian Companies. Journal of

Internet Banking and Commerce. 22(8),

Popoola, O. M. J., Ratnawati, V., & Hamid,

M. A. A. (2016). The interaction effect

of Institutional Ownership and Firm

Size on the relationship between

Managerial Ownership and Earnings

Management

Raeisi, A., & Vaez, S. A. (2016). An

Evaluation of the Relationships between

the Corporate Governance Mechanisms,

the Free Cash Flow, and Earnings

Management in Tehran Stock Exchange

Listed Companies. International Journal

of Humanities and Cultural Studies

(IJHCS) ISSN 2356-5926, 122-140.

Razizadeh R., & Talebnia G., (2016). The

Effect of Managerial Ownership on the

Relationship Between Free Cash Flow

and Earnings Management. The Social

Sciences, 11: 2305-2313.

Reza R., & Ghodratalah T. (2016). the

Effect of Managerial Ownership on the

Relationship Between Free Cash Flow

and Earnings Management: The

Medwell Journal 11(9)2305-2312.

Roman, L. W. (2009). Quality of earnings

and earnings management. Journal of

AICPA, 2-4 Roodposhti, F. R.

&Chashmi, S. A. N. (2010). The impact

of corporate governance mechanisms on

earnings management. African Journal

of Business Management, 5(11), 4143-

4151.

Kargi & Zakariya. Moderating Effect of Free Cash Flow…

47

Rusmin, R., W. Astami, E., & Hartadi, B.

(2014). The impact of surplus free cash

flow and audit quality on earnings

management: The case of growth

triangle countries. Asian Review of

Accounting, 22(3), 217-232.

Sandra, A. (2012). Ownership Structure and

earnings management: Evidence from

Portugal. Australasian Accounting

Business and Finance Journal, 6(1), pp

57–74.

Sanusi, L. S. (2010). The Nigerian Banking

Industry: what went wrong and the way

forward. Delivered at Annual

Convocation Ceremony of Bayero

University, Kano held on, 3(1), 2010.

Schipper, K. (1989). Commentary on

earnings management. Accounting

Horizons, 3(4), pp. 91-102,

Shoaib, K., & Yasushi, S. (2015). Capital

structure and managerial ownership:

Evidence from Pakistan. Business and

Economic Horizons (BEH), 11(2), 131-

142.

Singh, M. & Davidson, W. N. (2003).

Agency costs, ownership structure and

corporate governance mechanisms,

Journal of Banking & Finance 27, 793-

816.

Sun, L., & Rath, S. (2009). An Empirical

Analysis of Earnings Management in

Australia. International Journal

ofHuman and Social Sciences, 4(15), pp.

150- 167.

Certified Fraud Examiners (1993).

PriceWater House report. – The

National Association of Certified Fraud

Examiners, The Punch

Newspaper(February 5, 2015).

Sunday Times, (2007). "Cadbury Nigeria

sued by investors over accounting"

retrieved from

http://business.timesonline.co.uk/tol/bus

iness/industry_sectors/

Uwuigbe, U., Uwuigbe, O. R., & Bernard,

O. (2015). Assessment of the effects of

firms" characteristics on earnings

management of listed firms in Nigeria.

Asian Economic and Financial Review,

5(2): 218-228.

Warfield, T., & Wild, J. (1995). Managerial

Ownership, Accounting Choices, and

Informativeness of Earnings. Journal of

Accounting and Economics, 20: 61-91.

Wiyadi, Tyas, P.L., Trisnawati. R. &

Sasongko, N. (2017). Corporate

Governance Integrated Earnings

Management And Cost Of Equity

Capital: Empirical Study in Indonesia.

South East Asia Journal of

Contemporary Business, Economics and

Law, 13( 2).

Yero, J. I., & Shehu, U. H. (2013). Free

Cash Flow, Growth Opportunity And

Performance Of Nigerian Quoted Food,

Tobacco & Beverages Firms. In

Conference Paper, Presented at the 2nd

Internationl Conference organised by

Faculty of Management Science,

Kaduna State University in March.

Accounting & Taxation Review, Vol. 5, No. 2, June 2021

48

APPENDIX I

Listed Conglomerate Firms in Nigeria as at 31/12/2017

S/N Name of firm Date of Listing

1 A.G. Leventis Nigeria PLC 29/11/1978

2 Chellarams PLC 1/4/1977

3 John Holt PLC 19/8/1974

4 SCOA Nigeria PLC 1977

5 Transnational Corporation of Nigeria PLC 23/11/2006

6 UACN PLC 1974

Source: Nigerian Stock Exchange FACT BOOK 2017

APPENDIX II

Regression Output

within 1.68e+10 -1.18e+10 1.34e+11 T-bar = 12.6667

between 1.69e+10 6.42e+09 4.68e+10 n = 6

fsize overall 1.86e+10 2.26e+10 2.58e+09 1.49e+11 N = 76

within .0169329 -.1125062 .0344915 T-bar = 12.6667

between .0021422 -.0006946 .0052481 n = 6

fcfmown overall .0011577 .0170498 -.1084158 .0349216 N = 76

within .0716811 -.0789119 .3336517 T-bar = 12.6667

between .2308428 .0007961 .5544967 n = 6

mown overall .1436095 .2251562 .0002178 .5929382 N = 76

within .0885362 -.3349486 .2265619 T-bar = 12.6667

between .0444355 -.055207 .0643883 n = 6

fcf overall .0013546 .0977121 -.380534 .2358388 N = 76

within .0803404 -.1919511 .2352698 T-bar = 12.6667

between .0406082 -.0505241 .072303 n = 6

em overall .0188662 .0887859 -.2286073 .2555771 N = 76

Variable Mean Std. Dev. Min Max Observations

. xtsum em fcf mown fcfmown fsize

.

fsize 0.0762 0.1627 0.3084* -0.0923 1.0000

fcfmown 0.2541* 0.4125* 0.0811 1.0000

mown -0.0562 0.1531 1.0000

fcf 0.6437* 1.0000

em 1.0000

em fcf mown fcfmown fsize

. pwcorr em fcf mown fcfmown fsize, star (0.05)

fsize 76 0.0488 0.8456 4.07 0.1306

fcfmown 76 0.0000 0.0000 61.49 0.0000

mown 76 0.8019 0.0181 5.45 0.0655

fcf 76 0.0046 0.0047 13.00 0.0015

em 76 0.1817 0.0622 5.16 0.0760

Variable Obs Pr(Skewness) Pr(Kurtosis) adj chi2(2) Prob>chi2

joint

Skewness/Kurtosis tests for Normality

. sktest em fcf mown fcfmown fsize

Kargi & Zakariya. Moderating Effect of Free Cash Flow…

49

Prob > chi2 = 0.1354

chi2(1) = 2.23

Variables: fitted values of em

Ho: Constant variance

Breusch-Pagan / Cook-Weisberg test for heteroskedasticity

. hettest

Mean VIF 1.20

mown 1.13 0.888851

fsize 1.16 0.858558

fcfmown 1.25 0.799100

fcf 1.27 0.785724

Variable VIF 1/VIF

. vif

_cons -.0067623 .1602774 -0.04 0.966 -.3263462 .3128217

fsize .004036 .0226661 0.18 0.859 -.0411589 .049231

fcfmown -.0363995 .5177248 -0.07 0.944 -1.068713 .9959145

mown -.0140739 .0081238 -1.73 0.088 -.0302722 .0021245

fcf .6077001 .0911034 6.67 0.000 .426045 .7893551

em Coef. Std. Err. t P>|t| [95% Conf. Interval]

Total .591219987 75 .007882933 Root MSE = .06834

Adj R-squared = 0.4076

Residual .331555042 71 .004669789 R-squared = 0.4392

Model .259664944 4 .064916236 Prob > F = 0.0000

F( 4, 71) = 13.90

Source SS df MS Number of obs = 76

. reg em fcf mown fcfmown fsize

Accounting & Taxation Review, Vol. 5, No. 2, June 2021

50

. est store re

rho 0 (fraction of variance due to u_i)

sigma_e .06584982

sigma_u 0

_cons -.0067623 .1602774 -0.04 0.966 -.3209001 .3073756

fsize .004036 .0226661 0.18 0.859 -.0403887 .0484608

fcfmown -.0363995 .5177248 -0.07 0.944 -1.051121 .9783225

mown -.0140739 .0081238 -1.73 0.083 -.0299961 .0018484

fcf .6077001 .0911034 6.67 0.000 .4291407 .7862595

em Coef. Std. Err. z P>|z| [95% Conf. Interval]

corr(u_i, X) = 0 (assumed) Prob > chi2 = 0.0000

Wald chi2(4) = 55.61

overall = 0.4392 max = 13

between = 0.7609 avg = 12.7

R-sq: within = 0.3806 Obs per group: min = 11

Group variable: id Number of groups = 6

Random-effects GLS regression Number of obs = 76

. xtreg em fcf mown fcfmown fsize, re

. est store fe

F test that all u_i=0: F(5, 66) = 2.09 Prob > F = 0.0773

rho .26358836 (fraction of variance due to u_i)

sigma_e .06584982

sigma_u .03939648

_cons .4700969 .279253 1.68 0.097 -.0874498 1.027644

fsize -.0633742 .0391063 -1.62 0.110 -.1414524 .0147041

fcfmown -.0781278 .5047318 -0.15 0.877 -1.085857 .9296018

mown -.0103315 .0330371 -0.31 0.755 -.0762922 .0556293

fcf .5402228 .0965643 5.59 0.000 .3474258 .7330197

em Coef. Std. Err. t P>|t| [95% Conf. Interval]

corr(u_i, Xb) = -0.0527 Prob > F = 0.0000

F(4,66) = 11.41

overall = 0.3525 max = 13

between = 0.0999 avg = 12.7

R-sq: within = 0.4088 Obs per group: min = 11

Group variable: id Number of groups = 6

Fixed-effects (within) regression Number of obs = 76

. xtreg em fcf mown fcfmown fsize, fe

Kargi & Zakariya. Moderating Effect of Free Cash Flow…

51

Prob > chibar2 = 1.0000

chibar2(01) = 0.00

Test: Var(u) = 0

u 0 0

e .0043362 .0658498

em .0078829 .0887859

Var sd = sqrt(Var)

Estimated results:

em[id,t] = Xb + u[id] + e[id,t]

Breusch and Pagan Lagrangian multiplier test for random effects

. xttest0

r(199);

unrecognized command: xttest

. xttest 0

(V_b-V_B is not positive definite)

Prob>chi2 = 0.2982

= 4.90

chi2(4) = (b-B)'[(V_b-V_B)^(-1)](b-B)

Test: Ho: difference in coefficients not systematic

B = inconsistent under Ha, efficient under Ho; obtained from xtreg

b = consistent under Ho and Ha; obtained from xtreg

fsize -.0633742 .004036 -.0674102 .0318677

fcfmown -.0781278 -.0363995 -.0417283 .

mown -.0103315 -.0140739 .0037424 .0320227

fcf .5402228 .6077001 -.0674773 .0320131

fe re Difference S.E.

(b) (B) (b-B) sqrt(diag(V_b-V_B))

Coefficients

. hausman fe re

_cons -.0067623 .1586876 -0.04 0.966 -.3231764 .3096519

fsize .004036 .0221588 0.18 0.856 -.0401473 .0482194

fcfmown -.0363995 .2504769 -0.15 0.885 -.5358363 .4630374

mown -.0140739 .0069539 -2.02 0.047 -.0279396 -.0002082

fcf .6077001 .0960318 6.33 0.000 .4162182 .799182

em Coef. Std. Err. t P>|t| [95% Conf. Interval]

Robust

Root MSE = .06834

R-squared = 0.4392

Prob > F = 0.0000

F( 4, 71) = 30.95

Linear regression Number of obs = 76

. reg em fcf mown fcfmown fsize, robust

Accounting & Taxation Review, Vol. 5, No. 2, June 2021

52

APPENDIX III

02

46

8

De

nsity

-.2 -.1 0 .1 .2Fitted values

kernel = epanechnikov, bandwidth = 0.0191

Kernel density estimate

Related Documents