Modelling health care costs: practical examples and applications Andrew Briggs Philip Clarke University of Oxford & Daniel Polsky Henry Glick University of Pennsylvania

Modelling health care costs: practical examples and applications Andrew Briggs Philip Clarke University of Oxford & Daniel Polsky Henry Glick University.

Dec 22, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Modelling health care costs: practical examples and applications

Andrew Briggs

Philip Clarke

University of Oxford

&

Daniel Polsky

Henry Glick

University of Pennsylvania

Modelling health care costs:Presentation overview

• Statement of problem• Examples of cost distributions

– Overall– By treatment group

• Testing cost differences– Raw scale– Transformations– Back transformation

• Multivariate analysis– Raw scale– Transformation

• Summary/future directions

Modelling health care costs:Statement of problem

• Common to collect cost data in clinical trials

• Cost data almost always skewed and may exhibit substantial kurtosis

• Nevertheless, arithmetic means are the concern of decision makers– Only the mean can be used to estimate total

cost of care– Only total cost of care will lead to balanced

budgets

• Cost models have a role beyond the simple estimation of within trial analysis– May be used to generalise to broader

populations– May be used for sub-group analysis

Modelling health care costs:Examples of cost distributions

1.BOAES

Fra

ctio

n

Cost0 5000 10000 15000

0

.2

.4

.6

2.UKPDS

Fra

ctio

n

cost0 500 1000 1500 2000 2500

0

.2

.4

.6

Modelling health care costs:Examples of cost distributions

3.ACT

Fra

ctio

n

Cost0 100000 200000 300000

0

.1

.2

4.Dan

Fra

ctio

n

Cost0 100000 200000

0

.2

.4

.6

.8

Modelling health care costs:Examples of cost distributions

5.SAH

Fra

ctio

n

Cost0 100000 200000

0

.1

.2

.3

6.HG

Fra

ctio

n

Cost0 25000 50000 75000100000

0

.1

.2

Modelling health care costs:Cost distributions by treatment

1.BOAES: control group

Fra

ctio

n

Cost0 5000 10000 15000

0

.2

.4

.6

1.BOAES: treatment group

Fra

ctio

n

Cost0 5000 10000 15000

0

.2

.4

.6

Modelling health care costs:Cost distributions by treatment

2.UKPDS: control group

Fra

ctio

n

cost0 500 1000 1500 2000 2500

0

.2

.4

.6

2.UKPDS: treatment group

Fra

ctio

n

cost0 500 1000 1500 2000 2500

0

.2

.4

.6

Modelling health care costs:Cost distributions by treatment

3.ACT: control group

Fra

ctio

n

Cost0 100000 200000 300000

0

.1

.2

.3

3.ACT: treatment group

Fra

ctio

n

Cost0 100000 200000 300000

0

.1

.2

.3

Modelling health care costs:Cost distributions by treatment

4.Dan: control group

Fra

ctio

n

Cost0 100000 200000

0

.2

.4

.6

.8

4.Dan: treatment group

Fra

ctio

n

Cost0 100000 200000

0

.2

.4

.6

.8

Modelling health care costs:Cost distributions by treatment

5.SAH: control group

Fra

ctio

n

Cost0 100000 200000

0

.1

.2

.3

5.SAH: treatment group

Fra

ctio

n

Cost0 100000 200000

0

.1

.2

.3

Modelling health care costs:Cost distributions by treatment

6.HG: control group

Fra

ctio

n

Cost0 25000 50000 75000100000

0

.1

.2

6.HG: treatment group

Fra

ctio

n

Cost0 25000 50000 75000100000

0

.1

.2

Approaches for testing cost differences

• Parametric T-test or nonparametric bootstrap on untransformed cost– Both unbiased

– Inefficient?

• (Log) transformation of cost– Straight retransformation biased

– Use

– Or non-parametric smearing

• Generalised linear models– lognormal:

– Expectation modelled directly so no retransformation problem

– Wide variety of possible link function/distributions

2exp 0.5iE C

ln i iE C t

1exp expi iE C

N

Zhou’s test based on log normality

• Special case of homogeneity of log variances – test of geometric means is equivalent to test of arithmetic means

• By symmetry: for special case of homogeneity of log means – test of equality of log variances is equivalent to test of arithmetic means?

• Zhou’s proposed test combines the two

2 20 1 1 0 0

2 20 1 1 0 0

2 20 1 1 0 0

2 20 1 0 1 1

: exp 0.5 exp 0.5

: 0.5 0.5

: 0.5 0.5 0

: 0 .

H

H

H

H iff

P-values and confidence intervals for back-transformed cost differences

Dataset P-value Cost diff (95% CI)

1. BOAE

T-test: raw cost

Bootstrapped means

Zhou (bootstrap)

Log (smeared)

GLM: log link / normal

GLM: B-C link / normal

0.013

0.012

0.026

<0.001

0.019

0.019

149

149

107

212

149

149

(31 -

(44 -

(21 -

(146 -

(26 -

(26 -

267)

255)

191)

278)

259)

260)

2. UKPDS

T-test: raw cost

Bootstrapped means

Zhou (bootstrap)

Log (smeared)

GLM: log link / normal

GLM: B-C link / normal

0.971

0.938

0.988

0.165

0.971

0.971

0

0

0

5

0

0

(-8 -

(-8 -

(-14 -

(-2 -

(-8 -

(-8 -

8)

8)

12)

13)

8)

8)

3. ACT

T-test: raw cost

Bootstrapped means

Zhou (bootstrap)

Log (smeared)

GLM: log link / normal

GLM: B-C link / normal

0.179

0.172

0.005

0.393

0.185

0.182

-15,523

-15,523

-136,747

14,162

-15,523

-15,523

(-38,248 -

(-37,854 -

(-611,607 -

(-18,321 -

(-37,212 -

(-37,458 -

7,201)

6,665)

-21,014)

47,530)

7,790)

7,509)

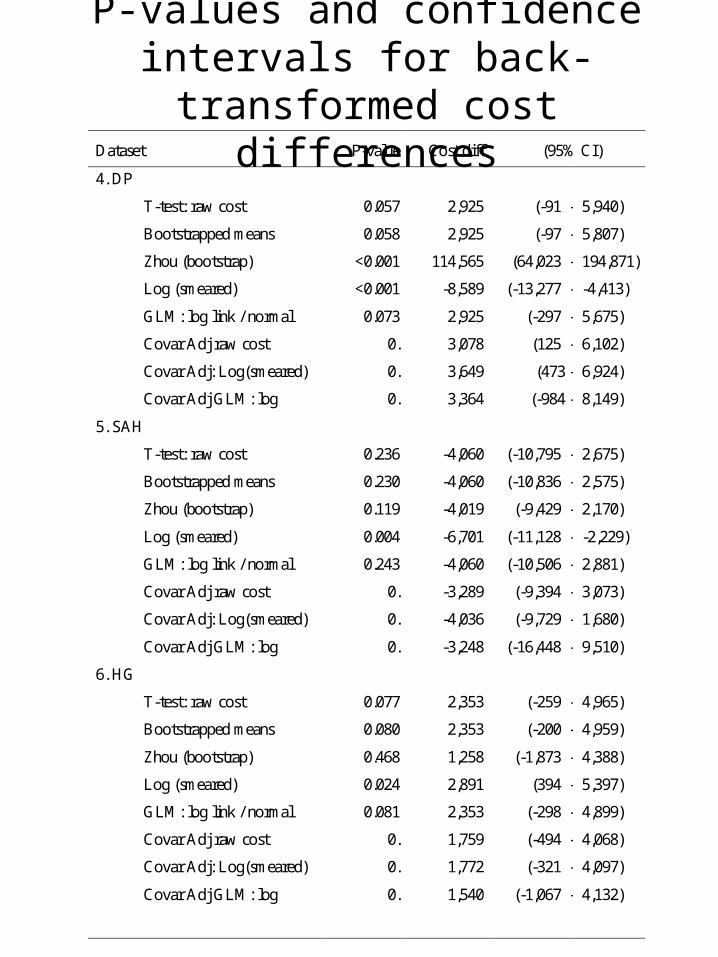

P-values and confidence intervals for back-transformed cost differences

Dataset P-value Cost diff (95% CI)

4. DP

T-test: raw cost

Bootstrapped means

Zhou (bootstrap)

Log (smeared)

GLM: log link / normal

GLM: B-C link / normal

0.057

0.058

<0.001

<0.001

0.073

0.071

2,925

2,925

114,565

-8,589

2,925

2,925

(-91 -

(-97 -

(64,023 -

(-13,277 -

(-297 -

(270 -

5,940)

5,807)

194,871)

-4,413)

5,675)

5701)

5. SAH

T-test: raw cost

Bootstrapped means

Zhou (bootstrap)

Log (smeared)

GLM: log link / normal

GLM: B-C link / normal

0.236

0.230

0.119

0.004

0.243

0.244

-4,060

-4,060

-4,019

-6,701

-4,060

-4,060

(-10,795 -

(-10,836 -

(-9,429 -

(-11,128 -

(-10,506 -

(-10,484 -

2,675)

2,575)

2,170)

-2,229)

2,881)

2,909)

6. HG

T-test: raw cost

Bootstrapped means

Zhou (bootstrap)

Log (smeared)

GLM: log link / normal

GLM: B-C link / normal

0.077

0.080

0.468

0.024

0.081

0.081

2,353

2,353

1,258

2,891

2,353

2,353

(-259 -

(-200 -

(-1,873 -

(394 -

(-298 -

(-295 -

4,965)

4,959)

4,388)

5,397)

4,899)

4,903)

Approaches to model selection

• Examine fit using standard regression diagnostics– R2, normal probability plots etc.

– Summarises fit to observed data

• Test the predictive ability of the models directly– Ability to predict observations

not used in model fitting

Predictive ability of the models

A simulation experiment 1. Sample was split into two equal parts

• Part i designated ‘training sub-sample’

• Part ii designated ‘test sub-sample’

2. Each model fitted using the training sub-sample and costs predicted for the test sub-sample

3. Mean square error calculated foreach model

Process repeated in 10,000 trials

Results of a simulation exercise

Model mean SE RMSE

OLS (cost) 10466 53 102OLS log(cost) no smearing 16072 226 127OLS log(cost) smeared 47432 1489 218OLS sqrt(cost) no smearing 10821 55 104OLS sqrt(cost) smearing 10441 54 102Poisson regression 11427 70 1072-part OLS (‘+’ve cost) 10467 53 1022-part OLS log(‘+’ve cost) no smearing

11298 54 1062-part OLS log(‘+’ve cost) smearing

11689 51 1082-part OLS sqrt(‘+’ve cost) no smearing

10616 55 1032-part OLS sqrt(‘+’ve cost) smearing

10429 54 102Tobit 10757 51 104

SE – estimated standard error of the mean

RMSE – root mean squared error

Mean squared error

P-values and confidence intervals for back-transformed cost differences

Dataset P-value Cost diff (95% CI)

1. BOAE

T-test: raw cost

Bootstrapped means

Zhou (bootstrap)

Log (smeared)

GLM: log link / normal

Covar Adj raw cost

Covar Adj: Log(smeared)

Covar Adj GLM: log

0.013

0.012

0.026

<0.001

0.019

0.

0.

0.

149

149

107

212

149

180

222

154

(31 -

(44 -

(21 -

(146 -

(26 -

(70 -

(126 -

(-48 -

267)

255)

191)

278)

259)

300)

338)

289)

2. UKPDS

T-test: raw cost

Bootstrapped means

Zhou (bootstrap)

Log (smeared)

GLM: log link / normal

Covar Adj raw cost

Covar Adj: Log(smeared)

Covar Adj GLM: log

0.971

0.938

0.988

0.165

0.971

0.

0.

0.

0

0

0

5

0

-1

0

-2

(-8 -

(-8 -

(-14 -

(-2 -

(-8 -

(-9 -

(-7 -

(-13 -

8)

8)

12)

13)

8)

6)

8)

7)

3. ACT

T-test: raw cost

Bootstrapped means

Zhou (bootstrap)

Log (smeared)

GLM: log link / normal

Covar Adj raw cost

Covar Adj: Log(smeared)

Covar Adj GLM: log

0.179

0.172

0.005

0.393

0.185

0.

0.

0.

-15,523

-15,523

-136,747

14,162

-15,523

-18,378

-12,602

-25,230

(-38,248 -

(-37,854 -

(-611,607 -

(-18,321 -

(-37,212 -

(-43,078 -

(-47,687 -

(-57,500 -

7,201)

6,665)

-21,014)

47,530)

7,790)

6,555)

24,271)

7,039)

P-values and confidence intervals for back-transformed cost differencesDataset P-value Cost diff (95% CI)

4. DP

T-test: raw cost

Bootstrapped means

Zhou (bootstrap)

Log (smeared)

GLM: log link / normal

Covar Adj raw cost

Covar Adj: Log(smeared)

Covar Adj GLM: log

0.057

0.058

<0.001

<0.001

0.073

0.

0.

0.

2,925

2,925

114,565

-8,589

2,925

3,078

3,649

3,364

(-91 -

(-97 -

(64,023 -

(-13,277 -

(-297 -

(125 -

(473 -

(-984 -

5,940)

5,807)

194,871)

-4,413)

5,675)

6,102)

6,924)

8,149)

5. SAH

T-test: raw cost

Bootstrapped means

Zhou (bootstrap)

Log (smeared)

GLM: log link / normal

Covar Adj raw cost

Covar Adj: Log(smeared)

Covar Adj GLM: log

0.236

0.230

0.119

0.004

0.243

0.

0.

0.

-4,060

-4,060

-4,019

-6,701

-4,060

-3,289

-4,036

-3,248

(-10,795 -

(-10,836 -

(-9,429 -

(-11,128 -

(-10,506 -

(-9,394 -

(-9,729 -

(-16,448 -

2,675)

2,575)

2,170)

-2,229)

2,881)

3,073)

1,680)

9,510)

6. HG

T-test: raw cost

Bootstrapped means

Zhou (bootstrap)

Log (smeared)

GLM: log link / normal

Covar Adj raw cost

Covar Adj: Log(smeared)

Covar Adj GLM: log

0.077

0.080

0.468

0.024

0.081

0.

0.

0.

2,353

2,353

1,258

2,891

2,353

1,759

1,772

1,540

(-259 -

(-200 -

(-1,873 -

(394 -

(-298 -

(-494 -

(-321 -

(-1,067 -

4,965)

4,959)

4,388)

5,397)

4,899)

4,068)

4,097)

4,132)

Modelling health care costs:Summary

• Different approaches to modelling health care cost can lead to quite different estimates

• Difficult to tell which is most appropriate• Transforming cost data can be more

efficient– GLM intuitive in modelling expectations– But modelling log cost better for heavy tails?

• Covariate adjustment can help precision and should be used whenever possible– Will be used to extrapolate beyond the data– Creates sub-group effects with transformed

models– Creates challenges for summarising

incremental cost across different covariate patterns

Modelling health care costs:Log cost distributions by treatment

1.BOAES: treatment group

Fra

ctio

n

Natural log of cost0 2 4 6 8 10

0

.1

.2

1.BOAES: control group

Fra

ctio

n

Natural log of cost0 2 4 6 8 10

0

.1

.2

Modelling health care costs:Log cost distributions by treatment

2.UKPDS: control group

Fra

ctio

n

Natural log of cost0 2 4 6 8 10

0

.1

.2

2.UKPDS: treatment group

Fra

ctio

n

Natural log of cost0 2 4 6 8 10

0

.1

.2

Modelling health care costs:Log cost distributions by treatment

3.ACT: control group

Fra

ctio

n

Natural log of cost0 2 4 6 8 10 12 14

0

.1

.2

3.ACT: treatment group

Fra

ctio

n

Natural log of cost0 2 4 6 8 10 12 14

0

.1

.2

Modelling health care costs:Log cost distributions by treatment

4.Dan: treatment group

Fra

ctio

n

Natural log of cost0 2 4 6 8 10 12 14

0

.1

.2

4.Dan: control group

Fra

ctio

n

Natural log of cost0 2 4 6 8 10 12 14

0

.1

.2

Modelling health care costs:Log cost distributions by treatment

5.SAH: control group

Fra

ctio

n

Natural log of cost0 2 4 6 8 10 12 14

0

.1

.2

5.SAH: treatment group

Fra

ctio

n

Natural log of cost0 2 4 6 8 10 12 14

0

.1

.2

Modelling health care costs:Log cost distributions by treatment

6.HG: treatment group

Fra

ctio

n

Natural log of cost0 2 4 6 8 10 12 14

0

.1

.2

6.HG: control group

Fra

ctio

n

Natural log of cost0 2 4 6 8 10 12 14

0

.1

.2

Related Documents