Mobile Cellular: Cutting the cord Tim Kelly & Michael Minges (ITU) CTO Annual Council, Gaborone, 21 September 1999 The views expressed in this presentation are those of the authors, and do not necessarily reflect the opinions of the ITU or its membership. Tim Kelly can be contacted by e-mail at: [email protected].

Mobile Cellular: Cutting the cord Tim Kelly & Michael Minges (ITU) CTO Annual Council, Gaborone, 21 September 1999 The views expressed in this presentation.

Dec 10, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Mobile Cellular:Cutting the cord

Tim Kelly & Michael Minges (ITU)CTO Annual Council, Gaborone,

21 September 1999

The views expressed in this presentation are those of the authors, and do not necessarily reflect the opinions of the ITU or its membership. Tim Kelly can be contacted by e-mail at: [email protected].

Mobile Cellular: Mobile Cellular: Cutting the cordCutting the cord

The Mobile RevolutionSupplying MobileRegulating MobileMobile AccessPricing MobileA Mobile Future

Examples from SADC

A Mobile RevolutionA Mobile Revolution

Source: ITU World Telecommunication Indicators Database.

More than 300 million users250’000 new users added each dayUsers double every 20 monthsCompetitive markets

Worldwide mobile cellular subscribers (millions)

553423161191

144

215

318

38%

9%6%4%

13%

3%2%

20%

27%

1990 91 92 93 94 95 96 97 98

Mobile as % of fixed-line telephone

subscribers

Mobile growth in SADC regionMobile growth in SADC region(excluding South Africa)(excluding South Africa)

Source: ITU

Over 100% growthAlmost as many

new mobile and fixed-line subscribers added in 1998

Penetration rate doubling each year

0.21

0.02

0.05

0.10

0

50

100

150

200

250

1995 1996 1997 1998

New telephone subscribers in SADC countries (000s) *

* Excluding South Africa

Mobile

Mobile density

Fixed

Supplying MobileSupplying Mobile

Note: Analogue systems include: AMPS (Advanced Mobile Phone System), NMT (Nordic Mobile Telephony), TACS (Total Access Communications System). Digital systems include: CDMA (Code Division Multiple Access), GSM (Global System for Mobile), PDC (Personal Digital Cellular), PHS (Personal Handyphone System), TDMA (Time Division Multiple Access).Source: ITU, adapted from Ericsson, Dataquest, GSM MoU, CDMA Development Group.

Worldwide cellular subscribers by technology, 1998 1st generation,

analogue 2nd generation,

digital 3rd generation,

IMT-2000 global roaming multimedia

(Internet, data, video, voice)

multi-mode (in-building, terrestrial, satellite)

7%

TDMA/D-AMPS

6% PDC11%

CDMAPHS2%

AMPS23%

NMT2%

TACS5%

GSM44%

Analogue30%

Digital 70%

Status of Mobile in SADC Status of Mobile in SADC regionregion

Mobile cellular start-upSADC countries

AngolaFeb. 94

NamibiaApril 95

BotswanaJune 98 South

AfricaJune 94

ZambiaAug.95

TanzaniaSep. 94

Zim -babweSep.96

MalawiDec. 95

Swazi -land

Nov.98

LesothoMay 96

MauritiusMay 89

Mozam -bique

Nov.97

Source : ITU.

< 0.1%

> 5%~ 1%

0.2 - .05%

Penetration

Mobile established fairly recently in all countries of SADC region

GSM is dominant standard

Roaming agreements evolving

Regulating MobileRegulating Mobile

Source: ITU World Telecommunication Indicators Database.

A relative lack of regulation<1% of world market under

monopolyKey issues: Coverage

and interconnect

Number of countries with mobile cellular competition

2838

49

6172

93

1993 1994 1995 1996 1997 1998

Market structures, SADCMarket structures, SADC

Private sector participation in all but one SADC country

Competition in 6 SADC countries

Cellular market structureSADC countries

Angola

Namibia

Botswana

South Africa

Zambia

Tanzania

Zim-babwe

Malawi

Lesotho

Mauritius

Swazi-land

Competitive with fixed PTO participation

100% state-owned

Fixed PTO+private investors

Competitive no fixed PTO participation

Number of mobile operators

Mozam-bique

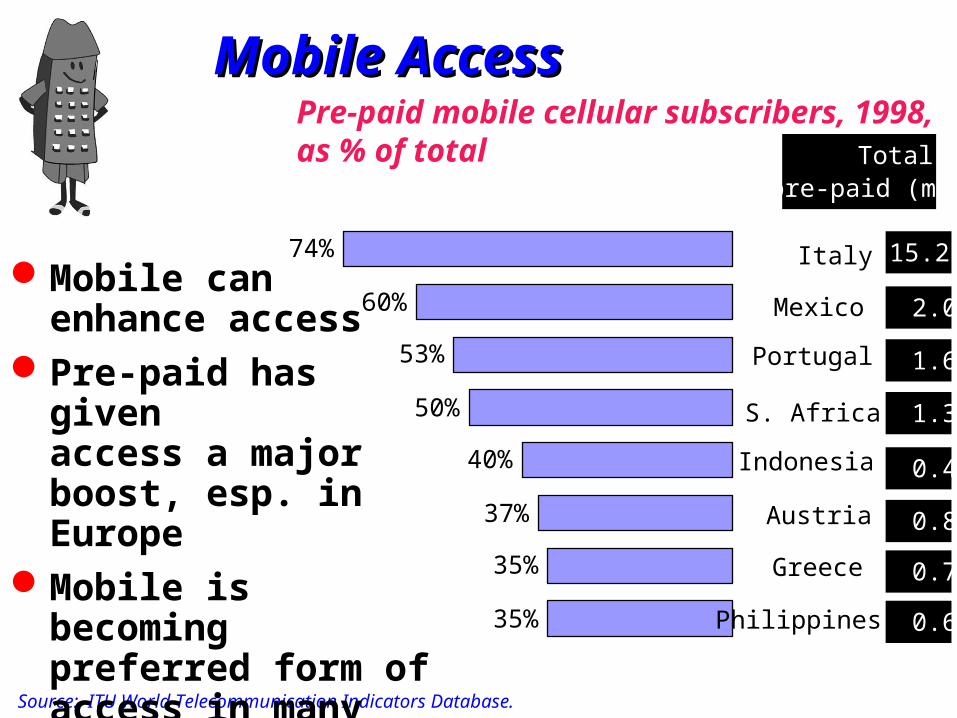

Mobile AccessMobile Access

Source: ITU World Telecommunication Indicators Database.

Mobile can enhance access

Pre-paid has given access a major boost, esp. in Europe

Mobile is becoming preferred form of access in many developing countries

Pre-paid mobile cellular subscribers, 1998, as % of total Total

pre-paid (m)

15.2

2.0

1.6

1.3

0.4

0.8

0.7

0.6

74%

60%

53%

50%

40%

37%

35%

35%

Italy

Mexico

Portugal

S. Africa

Indonesia

Austria

Greece

Philippines

©ITU / A. de Ferron

Mobile as a tool in achieving Mobile as a tool in achieving Universal Universal ServiceService

SADC operators have few Universal Service Obligations

Except in South Africa where they had to install 30’000 cellular payphones in 5 years

Cellular is quicker to implement and less prone to copper theft

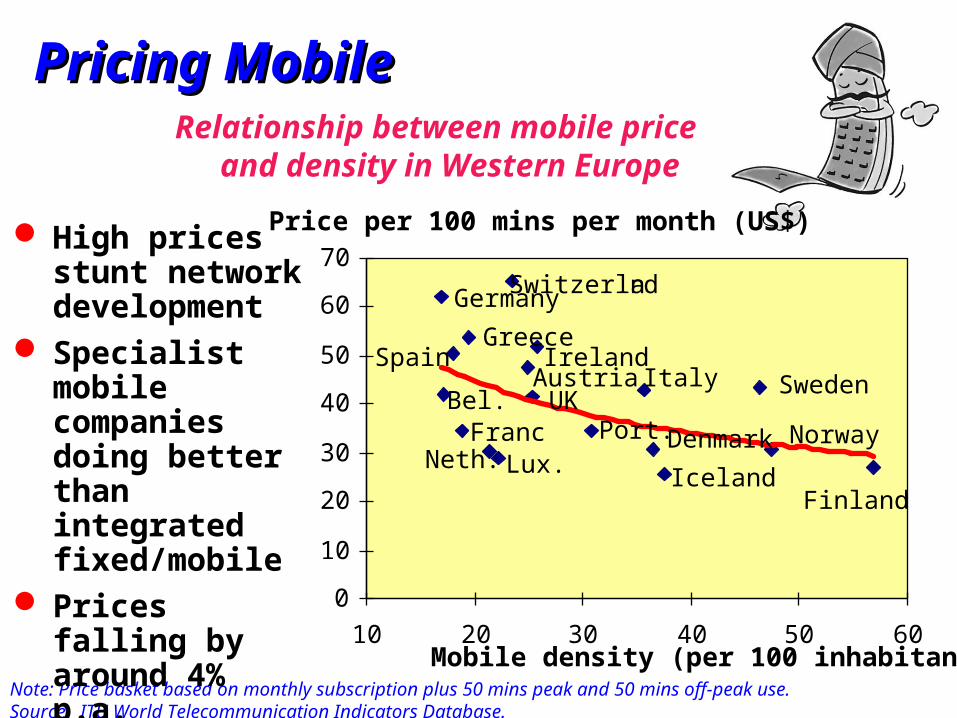

Pricing MobilePricing Mobile

Note: Price basket based on monthly subscription plus 50 mins peak and 50 mins off-peak use.Source: ITU World Telecommunication Indicators Database.

High prices stunt network development

Specialist mobile companies doing better than integrated fixed/mobile

Prices falling by around 4% p.a.

Relationship between mobile price and density in Western Europe

Mobile density (per 100 inhabitants)

Price per 100 mins per month (US$)

0

10

20

30

40

50

60

70

10 20 30 40 50 60

Switzerland

AustriaUK

Ireland

Finland

Sweden

Norway

Germany

GreeceSpain

Bel.Franc

Italy

Port.Neth.

Denmark

IcelandLux.

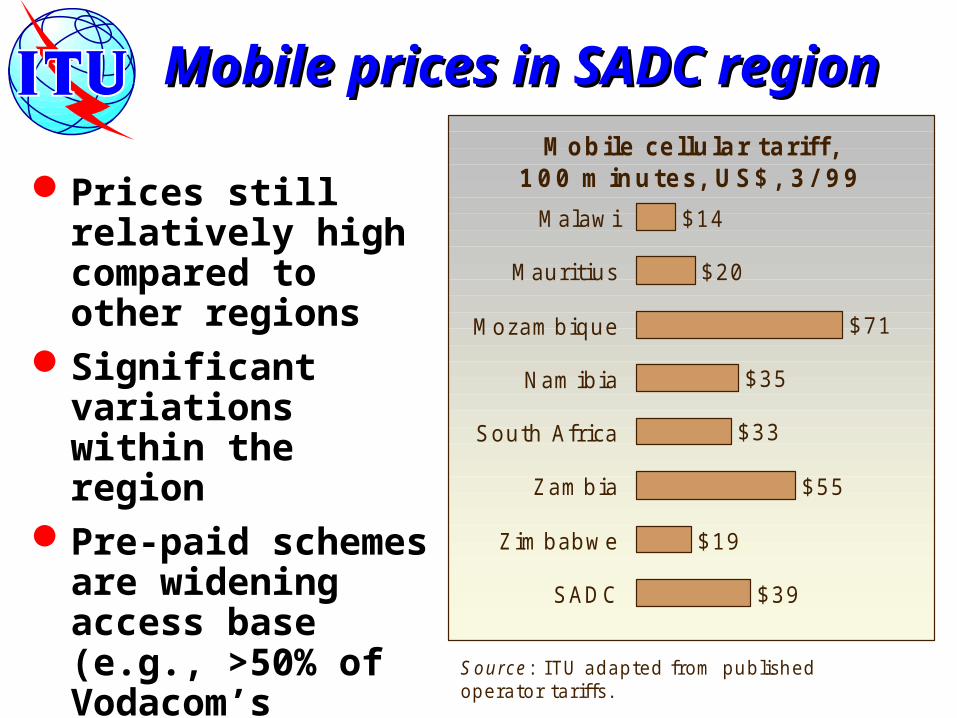

$14

$20

$71

$35

$33

$55

$19

$39

Malawi

Mauritius

Mozambique

Namibia

South Africa

Zambia

Zimbabwe

SADC

Mobile cellular tariff , 100 minutes, US$, 3/ 99

Source: I TU adapted from publishedoperator tariffs.

Mobile prices in SADC regionMobile prices in SADC region

Prices still relatively high compared to other regions

Significant variations within the region

Pre-paid schemes are widening access base (e.g., >50% of Vodacom’s subscribers)

A mobile futureA mobile future

Source: 1990-1998 data from ITU World Telecommunication Indicators Database. 1999-2010 ITU projections.

Mobile has overtaken fixed-lines in Cambodia, Finland and Italy

Mobile subscribers to overtake fixed-line worldwide before 2010?

Mobile revenue to overtake fixed-line after 2004?

Fastest growth in developing countries

Actual and projected subscriber growth, fixed-lines and mobile, millions, 1990-2010

0

500

1'000

1'500

2'000

1990 2000 2010

Fixed

Mobile

Cross-over between fixed and Cross-over between fixed and mobile subscribers, S. Africamobile subscribers, S. Africa

0

5

10

15

20

25

30

1990 1992 1994 1996 1998 2000

Fixed-line

Mobile

Subscribers per 100

inhabitants January 2000, at density

11.85 ??

For more information ...For more information ...Publication launch:

10 October 1999 (TELECOM ‘99)

Available on paper and online (PDF format)

World Telecom Indicators Database available online

Website:

http://www.itu.int/ti

Other reports launched at TELECOM ‘99Other reports launched at TELECOM ‘99 Direction of Traffic 1999: Trading Telecom Minutes Trends in Telecom Reform 1999: Convergence Internet for Development (updated with latest data)

Related Documents