Paper to be presented at the 35th DRUID Celebration Conference 2013, Barcelona, Spain, June 17-19 MNC Subsidiary Closure: What Stays When the MNC Leaves? Pedro de Faria University of Groningen Innovation Management and Strategy [email protected] Wolfgang Sofka Copenhagen Business School Department of Strategic Management and Globalization [email protected] Miguel Torres Preto Instituto Superior Técnico - Technical University of Lisbon IN+ Center for Innovation, Technology and Policy Research [email protected] Abstract We investigate the consequences of MNC subsidiary closures for employees who lose their jobs. We ask to what degree the foreign knowledge that they were exposed to is valued in their new job. We argue theoretically that this foreign knowledge is both valuable and not readily available in the host country but is also distant and therefore difficult to absorb. We predict an inverse u-shaped relationship between the exposure to foreign knowledge and the salary in the new job. We empirically support our predictions for a sample of almost 140,000 affected employees in Portugal from 2002 to 2009. Jelcodes:F23,O30

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Paper to be presented at the

35th DRUID Celebration Conference 2013, Barcelona, Spain, June 17-19

MNC Subsidiary Closure: What Stays When the MNC Leaves?Pedro de Faria

University of GroningenInnovation Management and Strategy

Wolfgang SofkaCopenhagen Business School

Department of Strategic Management and [email protected]

Miguel Torres Preto

Instituto Superior Técnico - Technical University of LisbonIN+ Center for Innovation, Technology and Policy Research

AbstractWe investigate the consequences of MNC subsidiary closures for employees who lose their jobs. We ask to whatdegree the foreign knowledge that they were exposed to is valued in their new job. We argue theoretically that thisforeign knowledge is both valuable and not readily available in the host country but is also distant and therefore difficultto absorb. We predict an inverse u-shaped relationship between the exposure to foreign knowledge and the salary in thenew job. We empirically support our predictions for a sample of almost 140,000 affected employees in Portugal from2002 to 2009.

Jelcodes:F23,O30

1

MNC SUBSIDIARY CLOSURE: WHAT STAYS WHEN THE MNC LEAVES?

ABSTRACT

We investigate the consequences of MNC subsidiary closures for employees who lose their

jobs. We ask to what degree the foreign knowledge that they were exposed to is valued in their new

job. We argue theoretically that this foreign knowledge is both valuable and not readily available in

the host country but is also distant and therefore difficult to absorb. We predict an inverse u-shaped

relationship between the exposure to foreign knowledge and the salary in the new job. We empirically

support our predictions for a sample of almost 140,000 affected employees in Portugal from 2002 to

2009.

Keywords: Knowledge and Productivity Spillovers; Knowledge Management; FDI

2

INTRODUCTION

Knowledge flows between the subsidiaries of Multinational Companies (MNCs) and their host

countries have been a central topic in International Business research (Meyer & Sinani, 2009 provide a

recent review). Many host country governments provide substantial incentives to attract foreign direct

investment (FDI) as channels for knowledge flows that benefit the productivity of domestic firms.

However, the results are oftentimes disappointing because MNCs prevent such knowledge flows or

domestic firms cannot absorb them (Feinberg & Majumdar, 2001; Zhao, 2006; Alcacer & Chung,

2007). An element that is largely absent in the discussion so far is knowledge flows that originate from

MNC subsidiaries closing down. Knowledge that the employees could absorb while working for

foreign MNC subsidiaries becomes available to host country firms. We are, to the best of our

knowledge, the first to study the value that new employers assign to the foreign knowledge that former

employees were exposed to in their old position with the closed, foreign MNC subsidiary. More

precisely, we infer the valuation of the foreign knowledge by the new employer based on salary

differences with otherwise identical former employees of domestic firms.

Our study ties into existing research along three dimensions. Firstly, divestures of MNC

subsidiaries are frequent challenges to the management of MNCs (see Berry, 2012 for a recent

review). They imply that the MNC optimizes its asset structure across countries through investments

in some host countries and divestures in others (Chakrabarti, Vidal, & Mitchell, 2011). However, this

stream of literature has predominantly focused on the MNC perspective by explaining why certain

subsidiaries are divested and what the effects are on MNC performance (Boddewyn, 1983, Boddewyn,

1979; Nachum & Song, 2011). We focus instead on the value that the former employees of MNC

subsidiaries can bring to their new employers. Secondly, MNCs have been found to compete with

local firms in the host country labor market. De Backer and Sleuwaegen (2003) find that the entry of

an MNC propels highly skilled individuals to opt for a career at the subsidiary of an MNC instead of a

career in a domestic firm. We investigate the interesting situation in which the conditions are reversed,

i.e. skilled employees become available again to the domestic job market. Finally, knowledge flows

through personnel mobility have been a major topic in International Business and Strategic

3

Management literature because employees can transfer not only codifiable elements but also valuable

tacit knowledge (Almeida & Kogut, 1999; Song, Almeida, & Wu, 2003; Agrawal, Cockburn, &

McHale, 2006). We investigate a unique situation in which the foreign subsidiary releases the

employees as carriers of its knowledge voluntarily by closing down the subsidiary. In sum, the focus

of our study is novel in the sense that we consider that local subsidiary employees can tie MNC

knowledge to the host country and that this knowledge is fully released once the MNC closes its

subsidiary and the employees are free to transfer their unique knowledge.

Closing this theoretical gap has high practical relevance. The closures of foreign subsidiaries

and resulting job losses have provoked outrage and public protests in many host countries in recent

past. Examples include the protests over pharmaceutical company Merck Organon closing its R&D

center in the Netherlands, Nokia shifting mobile phone production from Germany to Romania, and

Deutsche Post closing its sorting center at Wilmington Airpark in Ohio. Hence, theoretical predictions

and empirical tests on the consequences of these job losses are important for a broad audience: Job

seekers have a more comprehensive basis to evaluate their career planning when it involves working

for an MNC subsidiary. MNC managers can optimize divesture policies taking into account

unintended effects from knowledge outflows. Policymakers can design fitting support instruments for

employees who have lost their jobs as the result of MNC closures.

We develop new theory for International Business through an interdisciplinary approach. We

use a model of Labor Economics as the starting point because the consequences of firm closures on

employees are studied intensively in this field. This particular group of job seekers is typically defined

as “displaced” employees because they were not dismissed because of individual, low performance or

misconduct (Kletzer, 1998). Labor Economics postulates that employees build knowledge stocks

throughout their careers. These knowledge stocks differ in their degree of specificity for use outside of

the firm in which they were acquired. A displaced employee may face a steep decline in future salaries

if heri knowledge stock is highly specific to the firm that has just closed down. The closure has

essentially depreciated her individual knowledge stock. Empirically, displacement has been found to

have a persistent, negative effect on future earnings (Couch & Placzek, 2010). However, these

4

earnings losses can be reduced if more of the knowledge stock of a displaced employee can be

transferred to the new employer.

We build on this displacement model for the particular case of MNC employees along the

dimension of distance between host country and MNC knowledge. On the one hand, we argue that

working for an MNC subsidiary has exposed the displaced employee to knowledge that is otherwise

not available in the host country. MNCs act as social communities and can transfer even tacit

knowledge across national borders that could otherwise not be codified or licensed (Kogut & Zander,

1993). This makes the knowledge of a displaced employee from a foreign MNC particularly valuable.

The transferred knowledge of MNCs is typically valuable in itself (Kronborg & Thomsen, 2009) and

not readily available in the host country. Hiring firms can create unique combinations with their

existing knowledge stock and generate competitive advantages based on unique products and

processes. On the other hand, foreign knowledge is oftentimes not fully applicable in the host country.

It is developed in the dual context of host country and MNC, which means it does not necessarily fit

with the requirements of local firms (Almeida & Phene, 2004). Foreign knowledge is more distant

from the host country firm’s existing knowledge stocks (Meyer & Sinani, 2009). This distance makes

it difficult to assess, integrate, and exploit for new employers. In sum, we expect an inverse u-shaped

relationship between the foreign knowledge a displaced worker was exposed to and her future

earnings. Within a comparison group of displaced employees, a worker who lacks any foreign

knowledge will not be able to distinguish herself; one with exclusively foreign knowledge will find it

hard to find a new employer who can evaluate and utilize the knowledge.

Furthermore, we argue that two factors moderate the threshold at which the advantages of

foreign knowledge are outweighed by the costs associated with evaluating and integrating distant

knowledge. Firstly, foreign MNC subsidiaries are evaluated in comparison to other subsidiaries and

host countries (Chakrabarti et al., 2011). Closed down MNC subsidiaries may still be highly

productive within a host country comparison group. Consequently, the value of knowledge of

displaced employees of these foreign MNC subsidiaries will increase with their productivity, and new

5

employers have incentives to pay more. As a result, the inverse u-shaped relationship outlined above

should be positively moderated.

Secondly, new employers are heterogeneous in their ability to assess, integrate, and exploit the

foreign knowledge that a displaced employee can bring to their firm. Leading firms have higher

absorptive capacities (Cohen & Levinthal, 1994) and more potentials for recombining foreign

knowledge with existing knowledge stocks (Salomon & Jin, 2010). As a consequence, they should pay

higher salaries to a displaced employee with foreign knowledge because they can derive more value

from the employee and are better prepared to absorb the distant knowledge. Again, we predict a

positive moderation of the inverse u-shaped relationship.

We test and support these hypotheses for a sample of almost 140,000 displaced employees in

Portugal between 2002 and 2009 based on dynamic fixed effects regression models. Our findings have

immediate relevance for management research and practice.

On the academic side, we provide fresh impulses for research that has investigated knowledge

flows based on labor mobility between firms in general (Agrawal et al., 2006) as well as between

MNCs and their host countries in particular (Almeida & Kogut, 1999). More precisely, we find that

the closure of a foreign MNC subsidiary creates a pool of foreign knowledge in the host country that is

valued by the new employers as evidenced by comparatively higher salaries for displaced employees

of foreign MNC subsidiaries and domestic firms respectively. However, this pool of knowledge is not

equally valued by all host country firms; i.e., leading firms assign higher values to the foreign

knowledge. The combination of both effects provides new opportunities to theoretically model the

interaction between MNCs and the host country in which MNCs cannot automatically be assumed to

prevent knowledge flows (as opposed to e.g. Alcacer & Chung, 2007; Zhao, 2006). Also, the closure

of a foreign MNC subsidiary is not necessarily a completely negative event for the host country

(extending the work reviewed recently by Berry, 2012). What is especially intriguing for International

Business research focused on competition between MNCs and host country firms in factor markets is

the notion that the crowding-out of host country labor markets once an MNC enters the market (De

Backer & Sleuwaegen, 2003) cannot be simply reversed if the MNC leaves. Instead, we find an

6

inverse u-shaped relationship. Apparently, some foreign knowledge is too specific to the MNC and

cannot be valued by host country firms.

In Labor Economics research, job displacement is a well-studied and reviewed phenomenon

(Kletzer, 1998). Our findings indicate that foreign MNC subsidiaries are distinctive based on the

particularly valuable knowledge they provide as well as the specificity for using it. Studies that ignore

this unique situation of displaced employees of foreign MNCs suffer from biases in their findings.

THEORY

International Business literature has devoted a great deal of attention to MNCs’ interactions

with their host country environment. One of the most interesting aspects within this context is the

competition for skilled workers, scientists, and engineers with host country rivals (Almeida & Kogut,

1999; De Backer & Sleuwaegen, 2003). However, these studies are narrowly focused on the hiring of

new employees into MNC subsidiaries. Little is known about what happens to host country employees

if the foreign subsidiary closes down.

Closures of subsidiaries are not an unusual occurrence (a recent review can be found in Berry,

2012). They are part of an MNC’s reconfiguration of international assets to maximize performance

resulting in investments in some locations and divestment in others (Chakrabarti et al., 2011). We will

focus on the consequences for the former employees of the closed down foreign subsidiary.

With our model we want to explain the value of an employee’s knowledge in her new job

once her former employer, the foreign subsidiary, has closed down. We assume that the salary is the

expected value of the productivity that the employee will bring to her new firm (Ranft & Lord, 2000).

We argue that this expected value is a function of the employee’s knowledge stock.

The closure of a subsidiary entails that the employees are not dismissed because of individual

misbehavior or low performance. Following Kletzer (1998) we define this particular group of

employees as “displaced”, i.e. as “…individuals with established work histories, involuntarily

separated from their jobs by mass layoff or plant closure (rather than because of individual job

performance), who have little chance of being recalled to jobs with their old employer” (Kletzer, 1998:

116). Displacement has been studied intensively in Labor Economics. The literature reviews of Fallick

7

(1996), Kletzer (1998), and, more recently, Couch and Placzek (2010) show that job displacement

results in earnings losses, which appear to persist for a very long time.

This loss in earnings is typically explained by the way in which employees acquire knowledge

while working for a company. Knowledge stocks, routines, and procedures at the firm level shape the

potential for knowledge acquisition of each employee. It is important to note that the resulting

knowledge stock of the employees varies in how specific it is to the firm in which it was acquired

(Kletzer, 1998). Employee knowledge that is general in nature can be applied in different contexts and

organizations, e.g. using standard software tools or word processors. Specific employee knowledge,

however, only has value in the particular context or organization in which it was acquired, e.g.

operating custom-made machinery or software. Logically, the value of an employee’s knowledge

stock for another firm is limited to the general, transferable component. If the firm in which the

specific knowledge stock was accumulated closes down, the knowledge stock of the employees

depreciates because the strictly firm-specific components will not be of value to future employers.

However, the severity of the resulting drop in salary for displaced employees varies. Empirical

evidence shows that earnings losses are larger when displaced employees change to a position that

does not share a large amount of similarities with their previous jobs, e.g. in different industries,

occupations, or geographic regions (Jacobson, LaLonde, & Sullivan, 1993; Fallick, 1996). This

variation can be explained based on the distance in knowledge stocks between the closed down firm

and the new firm. Firms that are more similar (i.e. less distant) are more likely to benefit from

knowledge exchanges because it is easier to recognize and value external knowledge (Lane &

Lubatkin, 1998). With increasing similarity, a new employer will recognize value in the knowledge

stock of a displaced employee that other employers cannot. Consequently, the wage of a displaced

employee in a new job is comparatively higher if the new employer is similar to the past employer.

We argue that this theoretical model from Labor Economics is only partially able to predict

the future earnings of displaced employees of foreign MNC subsidiaries for two primary reasons.

Firstly, the model underestimates the degree to which displaced workers of foreign MNC subsidiaries

were exposed to knowledge that is valuable and not readily available in the host country. This

8

particular knowledge should increase their value to future employers compared to competitors in the

job market with strictly domestic knowledge stocks. Secondly, having worked for a foreign subsidiary

before adds a layer of distance to the displaced employee’s knowledge stock that is distinctively

different from industry or regional difference. We will explore both extensions of the model.

Employees who have developed their knowledge stock working for a foreign MNC subsidiary

have had access to a pool of valuable knowledge that is otherwise not readily available in the host

country. This follows the basic rationale that knowledge flows much more easily within countries than

across country boundaries (Audretsch & Feldman, 1996). These boundaries between knowledge pools

in different countries persist because of linguistic, cultural, or institutional differences at the national

level (Kogut, 1991). It can also be traced back to limitations in the willingness of knowledge carriers,

e.g. scientists or engineers, to move (Almeida & Kogut, 1999). MNCs have been found to be

especially efficient channels to overcome barriers in international knowledge flows. They can function

as social communities with shared routines and understandings of knowledge across international

subsidiaries (Kogut & Zander, 1993). Hence, tacit elements of the MNCs’ knowledge stock can be

transferred efficiently. Employees who are exposed to these intra-MNC knowledge flows can build a

unique knowledge stock in the host country.

New employers can benefit from this access to unique knowledge in the host country along

two dimensions. Firstly, they can increase the uniqueness of the firms existing knowledge stock by

creating novel combinations (Cassiman & Veugelers, 2006). Unique knowledge facilitates the creation

of products, processes, and services that cannot be easily imitated by competitors. This uniqueness

makes it a major source of sustainable competitive advantage (King, 2007). Secondly, the acquisition

of external knowledge allows firms to shorten the time and reduce the resources necessary for

developing the knowledge in-house (Fleming & Sorenson, 2004). In sum, displaced employees of

foreign MNC subsidiaries have a higher potential to create value for their new employers than the

average displaced employee. Their salaries should therefore be comparatively higher.

However, the knowledge originating from foreign MNCs is also significantly more distant

from the knowledge stock of the average new employer in the host country. The domestic environment

9

shapes the knowledge stock of firms and their employees. They become aligned with the host country

environment based on exposure over time, through interactions, feedback mechanisms, as well as

shared experiences (Zaheer & Mosakowski, 1997). In this regard, the knowledge that employees can

acquire from foreign MNC subsidiaries is necessarily more distant. Employees of MNCs operate in a

dual context (Almeida & Phene, 2004). Practices and procedures have to be compatible with both host

country as well as intra-MNC requirements. This implies that by design, foreign MNC subsidiaries

cannot seamlessly fit into the host country context because this would create frictions within the MNC.

Mezias (2002) finds for example that intra-MNC management practices increase the probability for

labor lawsuits of subsidiaries in the US. Foreign MNC subsidiaries have been found to suffer from a

persistent liability of foreignness, resulting in comparatively more frequent errors, risk, and additional

costs (Zaheer, 1995; Zaheer & Mosakowski, 1997). Hence, the knowledge that a displaced employee

has acquired at a foreign MNC subsidiary will be more distant from the new employer’s knowledge

stock compared with the average displaced employee. With increasing distance, a new employer

would find it difficult to evaluate the knowledge that the displaced worker could bring to the company.

As a result, the salary of the displaced worker could be expected to be lower than for domestic

counterparts.

In conclusion, we arrive at a theoretical model in which displaced employees differ from the

average displaced employee along two dimensions. The knowledge that the displaced employees have

acquired at the foreign MNC subsidiary is valuable but also more distant for new employers in the

host country. We argue that the theoretical predictions on the new salary of these displaced employees

depend on the degree to which they were exposed to foreign knowledge. In this sense, all displaced

workers have a profile based on the knowledge acquisition in their previous firm that consists of

domestic and foreign knowledge. The total knowledge that they have acquired while working for a

firm is finite. A displaced employee of a domestic firm would have a knowledge profile that is 100%

domestic without any foreign knowledge. This would not be rare for a new employer but also not

distant and therefore not difficult to transfer, all other things being equal. The distinctive value of the

knowledge of a displaced employee increases with the share of foreign knowledge, but so does the

10

distance with the new employer’s knowledge stock because the domestic component decreases. In

extreme cases, the displaced worker was exclusively exposed to foreign knowledge. This would imply

that both potential value and distance are at a maximum. A future employer could acquire a great deal

of otherwise unavailable knowledge by hiring the displaced worker but would have hardly any basis

on which to evaluate it. We conclude that a combination of domestic and foreign knowledge

outperforms the extreme cases of strictly domestic and strictly foreign knowledge profiles. The

relationship of the share of foreign knowledge that a displaced employee was exposed to and her

salary with a new firm can therefore be expected to be inverse u-shaped. We propose:

Hypothesis 1. The relationship between the level of a displaced employee’s exposure to foreign

knowledge and her salary in the new job is inverse u-shaped; i.e., it increases up to a certain

threshold after which it declines.

Performance deficits are the primary reason for the closure of international MNC subsidiaries

(Berry, 2012). This would suggest that the knowledge that a displaced employee can bring to a new

firm is generally less valuable. However, the performance comparisons of MNC subsidiaries are based

on intra-MNC benchmarks and reference groups. They cannot be readily extended to comparisons

with host country rivals. Put differently, an MNC subsidiary may be very successful compared to host

country competitors and still be closed down because the MNC can shift its activities to subsidiaries

with even higher productivity (e.g. based on comparative cost advantages).

MNC subsidiaries are heterogeneous in the roles that they perform for the MNC as a whole.

Some subsidiaries have mandates that are merely exploiting existing MNC knowledge, e.g. in

production, while others explore new products, processes, and markets (Cantwell & Mudambi, 2005).

For the purpose of our study it is important that subsidiaries of an MNC are in competition with one

another for these mandates (Birkinshaw & Hood, 1998). The decision on the closure of a particular

MNC subsidiary is therefore not necessarily an indication of its own performance. It merely implies

that another subsidiary can take over its mandate based on superior capabilities.

A firm interested in hiring the displaced employee of a foreign MNC subsidiary will assign

little relevance to intra-MNC comparisons of subsidiary performances. Instead, the firm will evaluate

11

the knowledge that the displaced worker can bring to the company relative to host country standards.

The value that a new employer can therefore assign to a displaced worker depends on how productive

the foreign MNC subsidiary was compared to the host country average. A highly productive foreign

MNC subsidiary may have been closed down based on intra-MNC criteria. The same logic cannot be

applied to displaced employees of strictly domestic firms.

In sum, we have argued in hypothesis 1 that the relationship between the salary of a displaced

employee and her exposure to foreign knowledge is inverse u-shaped in nature. This curvilinear

relationship is essentially the result of a trade-off between the unique value of the knowledge that a

displaced worker of a foreign MNC subsidiary can bring to the new company and the distance of this

knowledge from the firm’s existing knowledge stock. Based on the previous arguments, we conclude

that the value of the knowledge from the closed down MNC subsidiary is higher if the subsidiary was

more productive than the host country average, all other things being equal. Consequently, for

displaced employees of highly productive, foreign MNC subsidiaries, the threshold at which the value

of the knowledge that they bring to the new company is outweighed by increasing costs for absorbing

it, should occur at higher shares of foreign knowledge in a displaced worker’s knowledge profile. Put

differently, the knowledge of a displaced employee of an unproductive, foreign MNC subsidiary

would not outweigh the costs for absorbing it into the new employer’s knowledge stock. We propose:

Hypothesis 2. The relationship between the level of a displaced employee’s exposure to foreign

knowledge and her salary in the new job increases up to a certain threshold after which it

declines, and this relationship is positively moderated by the productivity of the foreign MNC

subsidiary. This threshold occurs at higher levels of the displaced employee’s exposure to

foreign knowledge.

Finally, the new employers of displaced workers cannot be assumed to be homogeneous in

their ability to absorb foreign knowledge. Some may benefit more from access to foreign knowledge

through displaced employees than others. A major discussion in International Business literature has

been whether leading or lagging firms benefit more from international knowledge (for recent reviews

see Meyer & Sinani, 2009 or Salomon & Jin, 2010). The leading or lagging status is typically inferred

12

based on the technological capabilities of a company compared to the average firm in a country and an

industry. Intuitively lagging firms have more to gain from accessing international knowledge.

However, most empirical studies find that leading companies benefit most from acquiring

international knowledge (Penner-Hahn & Shaver, 2005; Salomon & Jin, 2010).

There are two primary explanations for these findings. Firstly, leading companies can already

draw from a superior knowledge stock. This allows them to realize more valuable complementarities

when they integrate this existing knowledge stock with foreign knowledge (Penner-Hahn & Shaver,

2005). Secondly, a firm’s ability to absorb external knowledge depends upon its prior related

knowledge (Cohen & Levinthal, 1994). A firm with an established, superior knowledge stock will find

it easier to identify valuable knowledge in its environment, assimilate it with existing knowledge

stocks, and exploit its value more fully (Cohen & Levinthal, 1990, Cohen & Levinthal, 1989). Taking

both arguments together, lagging firms will find that the foreign knowledge is of comparatively less

use for them but very costly to absorb (Meyer & Sinani, 2009).

This line of argumentation can be directly translated to our setting. A leading host country

firm should be able to derive more value from hiring the displaced employees of foreign MNC

subsidiaries because it has more opportunities to exploit valuable complementarities and larger

capacities to absorb the knowledge. This implies that the trade-off between the value of foreign

knowledge and its distance to existing knowledge stocks is less pronounced. Leading firms can absorb

more foreign knowledge before experiencing the detrimental effects from absorbing distant

knowledge. We hypothesize:

Hypothesis 3. The relationship between the level of a displaced employee’s exposure to foreign

knowledge and her salary in the new job increases up to a certain threshold after which it

declines, and this relationship is positively moderated by the productivity of the hiring firm.

This threshold occurs at higher levels of the displaced employee’s exposure to foreign

knowledge.

13

EMPIRICAL STUDY

Data and Sample

We use the Quadros de Pessoal (QP) micro-data, a Portuguese longitudinal matched

employer-employee data set for the period 2002-2009 to test the hypotheses. Portugal is an especially

fitting host country on which to study our research question because the country has been a major

recipient of foreign direct investment (FDI) following its accession to the European Union (EU) and

the single European currency, the euro (OECD, 2013). This is mostly explained by comparatively low

labor costs, economic reforms, and access to the large EU markets. However, the country has found

itself in competition for FDI with Eastern European countries joining the EU. Portugal has attracted

investments from major, foreign MNCs such as Volkswagen (Germany) and Renault (France) but has

also experienced painful retreats of foreign MNCs such as when the biggest exporting firm of the

country, the subsidiary of German semiconductor producer Qimonda, closed its operations down, and

when General Motors moved production to Spain. Hence, Portugal provides an ideal setting for

studying displacement following foreign MNC subsidiary closures. Portugal has been suffering

recently from a financial crisis, which required severe macroeconomic corrections. We therefore

choose an observation period from 2002 to 2009 that should not suffer from these extraordinary

effects. In sum, Portugal provides an empirical setting in this period that allows generalizable insights

for many other medium technology-intensive countries worldwide that compete for FDI.

QP is gathered annually by the Portuguese Ministry of Labor and includes data from all

private firms with at least one wage earner. Participation is mandated by law, and misinformation is

punishable. The integrity of the data collection is therefore high. Biases originating from selection or

narrow industry coverage can be eliminated (the data do not cover public administration). The survey

collects detailed information on each individual employee as well as basic information about the firm,

such as size, ownership, sales turnover, industry (ISIC), and location (NUTS).

Each annual survey includes 300,000 firms and nearly 3,000,000 workers who can be tracked

over time through a unique identification number. Our sample comprises employees who moved from

a closing firm to another firm in Portugal the subsequent year. Following Mata and Portugal (2002),

14

we classify a firm as a closing firm when it does not report information for three years in a row (this

time lag allows the differentiation between firms that closed down and firms with missing values).ii

Firms can also divest subsidiaries through alternative methods, e.g. sales or initial public offerings

(IPOs) (Berry, 2012). For the purpose of our study, it is crucial to capture employee displacement

following subsidiary closure. Employees may also experience changes in wages if their company is

sold. We avoid this potential source of bias by including only employees from closed down firms

(foreign and domestic) in our sample because we can apply identical closure identification to them.

Our unit of observation is the individual displaced employee. We capture 138,256 displaced

employees from 36,684 firms in our sample during the observation period. 646 foreign MNCs have

closed subsidiaries during the observation period and displaced 17,139 employees.

Variables

Dependent variable. Based on the widely accepted assumption that the wage is a reflection of

the value attributed by the firm to the employee (Ranft & Lord, 2000), our dependent variable is the

hourly wage of the displaced employee in the new firm (in logs). We deflate it using the yearly

consumer price index. The fact that we only observe employees who find a job after the displacement

might imply a selection problem. Displaced employees may remain unemployed, retire, or stop

searching for employment. Our dataset covers exclusively employed persons and cannot be merged

with alternative data sources, e.g. unemployment records, due to data protection laws. This has two

consequences for our empirical analysis. Firstly, our findings are limited to displaced employees who

find a new job within one year and this should be born in mind when interpreting the empirical results.

We conduct a consistency check estimation with a two-year time horizon which supports the results of

the main model. Secondly, the estimations would only suffer from a selection bias if displaced

employees of foreign MNC subsidiaries would have a significantly different probability for finding a

new job than domestic counterparts. This is not the case. The correlation between foreign ownership of

a former employer and the probability of finding a new job is just 0.07 in QP.

Independent variables. We argue theoretically that foreign MNC subsidiary employees have

15

foreign knowledge that differentiates them from domestic firm employees. However, knowledge is

elusive to measure. There is a rich stream of literature on entry mode choices based on transaction

economics, emphasizing that MNCs choose wholly owned subsidiaries as well as equity joint ventures

depending on the level of intra-MNC knowledge that they will transfer to the host country and need to

protect (Hennart, 2009). Firms increase equity shares when they face appropriability hazards of their

knowledge (Oxley, 1997). The equity share of a foreign MNC in a subsidiary can therefore be

considered as a proxy for the foreign knowledge that was transferred (Blodgett, 1991). We test our

hypotheses by including a variable that measures the displaced employee’s exposure to foreign

knowledge: the percentage of foreign capital of the closing firm. Since we predict an inverse u-shaped

relationship between this variable and the dependent variable, the squared term is also included. The

share of foreign ownership is only an indirect measure of exposure to foreign knowledge.

Firms may also possess foreign knowledge based on exporting, and our variable based on

foreign capital investment cannot capture this (Cassiman & Golovko, 2011). A control variable for

exporting is not available. However, this factor induces a downward bias in our estimations because

the displaced employees of export-intensive, domestically owned firms will end up in the control

group. Significant findings should therefore be considered as conservative estimates.

In hypotheses 2 and 3 we claim that the value given by companies to the displaced employee’s

access to foreign knowledge is also dependent on the level of productivity of the closing firm and the

level of productivity of the new employer. Productivity is measured as labor productivity, i.e. sales per

employee. To test these hypotheses, we include the variables of sales per worker of the closing firm

and sales per worker of the hiring firm in our model, and we interact them with the foreign capital

variable. We follow Brauer & Wiersema (2012) for testing the shift of a threshold in the inverse u-

shaped relationships (Hypotheses 2 and 3) and interact these variables with both the linear and the

quadratic term of the share of foreign capital.

16

Control variables. We control for several other employee and firm characteristics that were

identified by the literature to influence wage levels.

Firstly, we identify a number of control variables at the individual level. The level of

education also influences the wage level of an employee. Three binary variables categorize employees

according to their education level: basic, secondary, and college education. We include a binary

variable controlling for gender, since female employees have been found to earn lower wages than

their male colleagues. We also control for the employee’s experience in the firm as well as in general

through her age (Psacharopoulos, 1985). Furthermore, we control for the nationality of the employee

including a binary variable that identifies foreign individuals. This allows us to eliminate biases

originating from expat employees who may have provided foreign knowledge. Within each firm,

employees have different functions that imply different levels of complexity, skill requirements,

responsibility, and, consequently, wage. Therefore, we control for the employee’s function within the

closing firm by including two binary variables for functions: Professionals as well as

managers/supervisors (apprentices, interns, and trainees as well as untrained workers constitute the

control group).

Secondly, it is likely to expect serial correlation when using wages as a dependent variable.

We include the average wage of the last two years that the employee worked for at the closed firm.

This variable is specific to the individual employee but not merely a binary variable as with standard

fixed effects estimations. Past wages allow controlling for any other unobserved factor not controlled

elsewhere. Empirical models dealing with individuals are quite likely to suffer from these omitted

variable biases because individuals are highly heterogeneous and wage differences could be based on

hardly observable factors such as motivation or social connections. However, these factors should

have become visible in the wages of the displaced employee in the past. We will return to this variable

when describing the estimation method.

Thirdly, at the firm level, we control for the firm size, knowledge-intensity, the industry, and

the share of foreign capital of the hiring firm. We measure the firm size using the natural logarithm of

the number of employees in the firm. Larger firms may have more resources for hiring new employees

17

(Gibson & Stillman, 2009). Also, especially MNC subsidiaries have been found to vary in their

knowledge-intensity (Cantwell & Mudambi, 2005). We use the share of employees with college

education to capture this effect. We also include four binary variables that differentiate industries

because the opportunities and mechanisms for absorbing external knowledge have been found to be

highly industry-specific (Koehler, Sofka, & Grimpe, 2012): manufacturing (ISIC code 15-37), energy

and construction (ISIC code 40-45), services (ISIC code 50-74), and community, social, and personal

services (ISIC code 75-99). Our reference group is the primary sector (ISIC code 1-14). We include a

binary variable that identifies individuals that did not switch industries (at the two-digit ISIC level) as

it may indicate a separate devaluation of specific knowledge (Kletzer, 1998). The share of foreign

capital of the hiring firm is included because, as discussed in the theory section, the existence of

foreign capital may affect the wage policy of a firm and influence the dependent variable.

Fourthly, we control for differences in the efficiencies of labor markets. Labor markets are

geographically confined. We include a binary variable that identifies firms located in Portugal’s two

large metropolitan areas (Lisbon and Oporto). These regions have an intense economic activity when

compared with the rest of the country, since they contain around 70% of the wage employees present

in QP.

Also, in more inefficient labor markets, new firms may not need to pay higher salaries for the

value that they recognize in displaced employees because of a surplus in labor supply. This situation

cannot be ruled out because, due to the closure, many job seekers will enter the job market at the same

time. However, this situation would add a downward bias to our estimation results; i.e., it would

become increasingly unlikely that we would find significant differences in wages. Hence, we may

underestimate the effects but not overestimate them if labor markets are not fully efficient.

Finally, year binary variables are included for the years 2006, 2007, 2008, and 2009 in order to

control for the business cycle (2005 is the reference year). The other years of the observation period

are not used for the estimation because we calculate the past wage variable based on the initial years.

18

Descriptive Statistics and Correlations

Table 1 provides descriptive statistics (the correlation coefficients for the independent and the

control variables are available upon request). The descriptive statistics allow the characterization of

the average displaced employee in our sample: He is a 38 years old, Portuguese man with limited

education and more than six years of tenure in the closing firm. He is hired by a firm in the same

industry and earns a slightly higher wage than in the previous two years with the closing firm. We

inspect the dataset for multicollinearity. We find an average variance inflation factor of 6.58 which is

within commonly applied standards (for a discussion see Brauer & Wiersema, 2012). To ensure that

estimation results are not biased by multicollinearity we conduct consistency check estimations that

rely on sample splits instead of multiplicative interaction terms (Salomon & Jin, 2010). They provide

no indication of multicollinearity determining the estimation results (see end of results section).

‘Table 1 goes about here’

Estimation Method

Estimating empirical models with wage as the dependent variable has two primary challenges.

Firstly, individuals have many unobserved characteristics that may bias the estimation results, e.g.

motivation. Secondly, wages are highly time-dependent, e.g. based on union labor contracts, and serial

correlation becomes a challenge. We address both issues by estimating dynamic fixed effects models,

which include pre-sample information of the dependent variable (i.e. wages before displacement).

Lach & Schankerman (2008) introduce this approach that has the advantage that it does not rely on the

assumption of strict exogeneity of the regressors, leading still to efficient estimators and accounting

for the impact of unobserved fixed effects on the firm level. The approach has multiple advantages

(Salomon & Jin, 2010; Czarnitzki, Hottenrott, & Thorwarth, 2011). It reduces the risk for serial

correlation of errors and allows for a dynamic, firm-specific component, as opposed to the static

nature of most fixed-effect specifications.

19

RESULTS

Table 2 shows the results of the regression analyses. We report the coefficients of the dynamic

fixed effects regression model. Model I shows the baseline model specification without any interaction

effects and is the basis for testing hypothesis 1. Model II and model III introduce the interaction terms

of the foreign capital variable with the productivity of the closing firm variable and with the

productivity of the hiring firm, respectively. We test these hypotheses in separate models because of

concerns of multicollinearity. These two models will allow us to test hypotheses 2 and 3.

‘Table 2 goes about here’

Table 1 shows that the linear term of the share of foreign capital of the closed firm is positive

and the quadratic term is negative and significant in all the specifications of the model. These findings

support hypothesis 1 since they show an inverse u-shaped relationship between the share of foreign

knowledge that a displaced employee was exposed to and her salary with a new firm. Figure 1

illustrates this finding. The threshold occurs at 63% of foreign ownership. Besides, we find that the

salary of a displaced employee is a substantial 6% higher than the average for every standard deviation

of foreign capital in the closed firm. Hence, the effect is significant and has considerable magnitude.

In sum, the wage of a displaced employee in a new firm increases with the level of her access

to foreign knowledge until a certain threshold is reached. At this point, there exists an optimal balance

between novelty and distance of the knowledge. Beyond this threshold, the advantages of exposure to

foreign knowledge are outweighed by the need to absorb increasingly distant knowledge in the new

firm. As stated in the development of the hypotheses, we find that the combination of domestic and

foreign knowledge outperforms the extreme cases of strictly domestic and strictly foreign knowledge

profiles.

‘Figure 1 goes about here’

The main effect of the variable that measures the productivity of the closing firm, sales per

worker, is positive and significant at the 99% level. The interaction effects with the linear and the

quadratic terms of the foreign capital variable are also significant at the 99% level. The interaction

with the linear effect is negative but positive with the quadratic term. These results show that for more

20

productive firms the inverse u-shaped relationship between the share of foreign capital of the closing

firm and the wage of the displaced employee becomes flatter. The coefficients of the interaction terms

do not provide an immediate answer to hypothesis 2 because with a change in the linear and quadratic

slopes the threshold could shift in both directions. We graph the relationship in Figure 2. It shows the

relationship between the foreign capital variable of the closed firm and wage in the new firm, at three

different levels of productivity of the closed firm: 25%-percentile, mean, and 75%-percentile. It shows

a shift of the threshold to higher values when the productivity of the closing firm increases, giving

support to hypothesis 2 (equivalent mathematical derivation available upon request). Hence, the

inverse u-shaped relationship tested in hypothesis 1 is positively moderated by the productivity of the

closed firm.

‘Figure 2 goes about here’

Model 3 shows similar results for the productivity of the hiring firm variable and for the

associated interaction terms. The main effect of this variable is positive and significant at the 99%

level. The interaction effects with the linear and the quadratic terms of the foreign capital variable of

the closed firm are also significant at the 99% level. The interaction with the linear effect is negative

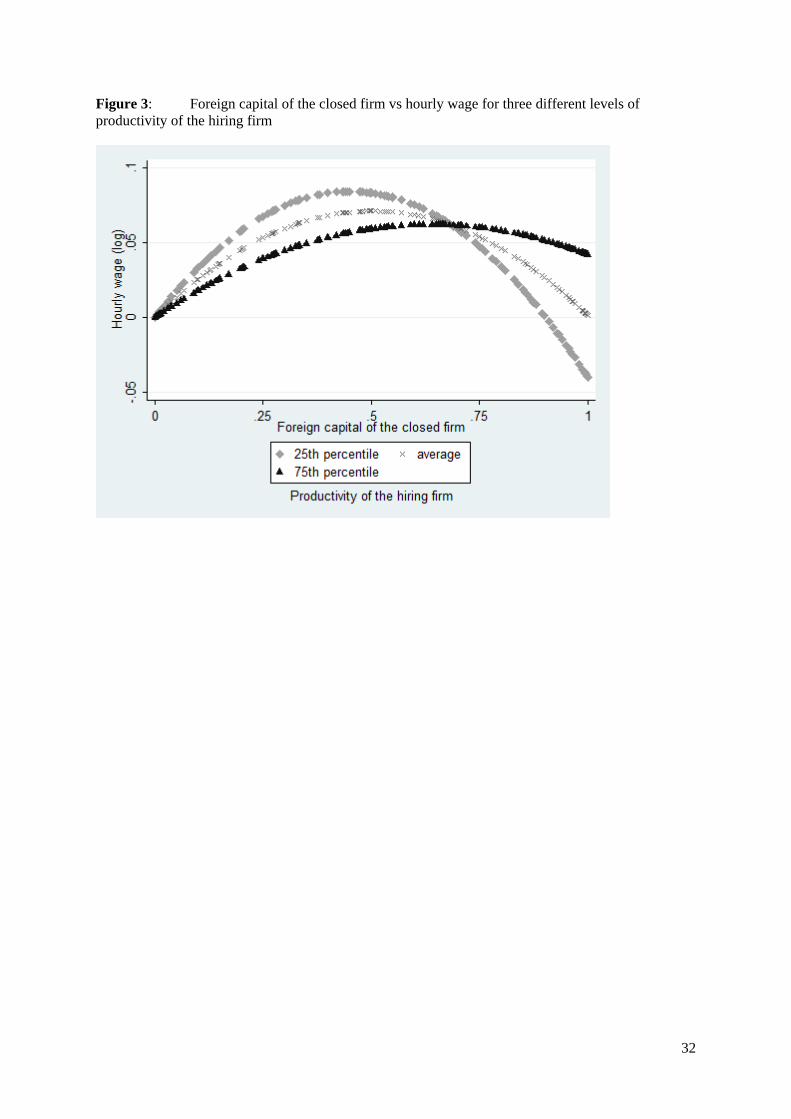

and positive for the quadratic term. Figure 3 shows the relationship between the share of foreign

capital of the closed firm and the wage in the hiring firm for three different levels of productivity of

the hiring firm: 25%-percentile, mean, and 75%-percentile. The graph provides evidence that supports

hypothesis 3 (an equivalent mathematical derivation available upon request). When employees join

firms with higher productivity, the advantages associated to the novelty of the foreign knowledge gain

more relative weight when compared with the possible disadvantages associated to knowledge

distance. Hence, the inverse u-shaped relationship tested in hypothesis 1 is positively moderated by the

productivity of the hiring firm.

‘Figure 3 goes about here’

The results for the control variables are in line with the literature, showing the robustness of

our model. Wages increase with education, age, experience, and degree of responsibility and are lower

for female employees. At the firm level, firm size and productivity lead to higher wages.

21

We test the consistency of the estimation results through a variety of procedures such as

alternative dynamic fixed effect specifications, replacing continuous variables of foreign capital with

category-dummies and sample splits. All tests support our main findings and are available upon

request.

DISCUSSION AND CONCLUSION

In this study we adopt the perspective of the displaced employees of closed MNC subsidiaries.

We investigate the value of the foreign knowledge that they were exposed to while working for the

MNC subsidiary for their new employers. Our theoretical predictions are fully supported by the

empirical study. We find that the foreign knowledge is valuable when we compare displaced

employees of closed MNC subsidiaries with counterparts of closed domestic firms. However, the

relationship is not linear but inverse u-shaped because at a certain threshold the advantages of

accessing foreign knowledge are outweighed by the costs of evaluating and absorbing it. This

threshold occurs at higher levels of exposure to foreign knowledge if the MNC subsidiary was leading

in the host country and when the new employer is leading in the host country. We had predicted the

latter relationship based on the theoretical argument that these leading companies benefit more from

combinations with an already existing superior knowledge stock and stronger absorptive capacities.

Our findings have immediate relevance for research and practice. From a research perspective

the implications are threefold. Firstly, we introduce displacement as a channel for knowledge flows

between MNC subsidiaries and the host country, an element which is currently absent in the literature

(e.g. in the review of Meyer & Sinani, 2009). Our findings show that MNCs create a valuable pool of

knowledge for host country firms when they close down subsidiaries. The displaced employees are

conceptually different from employees who are selectively hired from other companies for acquiring

knowledge (Song et al., 2003). In the case of displacement, the MNC makes knowledge carriers

voluntarily available by closing down its subsidiary. The importance of this channel for knowledge

flows is most likely underestimated in current International Business research because of two factors:

closures occur frequently (Berry, 2012), and knowledge transfers through individuals are highly

efficient (they can transfer tacit elements of knowledge as opposed to codified ones such as licensing)

22

(Agrawal, 2006). At the same time, we find that not all MNC subsidiaries produce knowledge of high

value. Instead, the value increases with productivity of the closed down MNC subsidiary compared to

the host country. Similarly, leading firms are more likely to extract value from the knowledge of the

displaced employees when they hire them. Hence, future studies would (a) suffer from biases if they

ignore the knowledge flow channel through displacement and (b) assume that knowledge sources and

recipients from displacement are randomly distributed among host country firms.

Secondly, International Business studies have found a crowding-out of human resources in the

host country when MNCs enter (De Backer & Sleuwaegen, 2003). Interestingly, the reverse

mechanism cannot be assumed to hold when the MNC leaves. We find instead that parts of the

knowledge that employees acquire while working for MNC subsidiaries cannot be valued by new

employers once the distance to host country knowledge stocks increases.

Finally, Labor Economics has studied job displacement intensively (Kletzer, 1998). However,

the specific situation of foreign MNC subsidiaries has been largely absent in the discussion so far. The

situation of displaced employees of such firms is significantly different from all other displaced

employees in the host country because they were exposed to knowledge that is otherwise not available.

Subsequently, this knowledge is not only particularly valuable in the host country but also more

distant and hence difficult to absorb. Studies that ignore this particular effect suffer from biased

results.

With regard to practice we find three primary groups that will benefit from our findings.

Firstly, individual job seekers can incorporate our findings in their decision making. Fully rational

decision makers would like to maximize their earnings over the course of their careers. This includes

necessarily the likelihood of being displaced. We find that the negative outcomes of such an event are

comparatively lower if an employer provides both domestic and foreign knowledge. Such an employer

should therefore be the preferable choice for a job seeker, all other things being equal. Secondly, the

management of MNCs at global headquarters has to consider the valuable knowledge that it makes

available to host country rivals when it closes down a subsidiary and must try to capture that

knowledge. If the subsidiary under consideration for closing is productive by host country standards

23

and if there are host country firms that can absorb the knowledge embedded in its employees, a sale is

preferable to the closure. Finally, policymakers are oftentimes called upon to intervene when foreign

MNC subsidiaries close down. While the closure of foreign MNC subsidiaries can attract

disproportionately more media attention, the displaced employees are generally better off than

displaced employees of strictly domestic firms. Our findings indicate that support measures, such as

temporary employment agencies, subsidies, and job centers, are best directed at displaced workers

who had no or exclusive exposure to foreign knowledge. In both cases, the cuts in salaries that they

can expect in the new job are especially pronounced.

Finally, our study provides future opportunities to understand in more detail the relationships

that we discovered. Firstly, not all types of knowledge of displaced employees can be assumed to be

equally valuable in new jobs. We suspect that relational knowledge, e.g. contacts to leading foreign

customers or suppliers, could be at least as valuable as technological knowledge. Secondly, not all

employees in an MNC subsidiary are exposed equally to foreign knowledge. Some may work

intensively with colleagues in other subsidiaries and global headquarters while others may largely deal

with domestic issues. Accordingly, their opportunities for absorbing foreign knowledge differ.

Qualitative studies are required to study such distinctions in more detail.

24

REFERENCES

Agrawal, A. 2006. Engaging the Inventor: Exploring Licensing Strategies for University Inventions and the Role of Latent Knowledge. Strategic Management Journal, 27(1): 63-79. Agrawal, A., Cockburn, L., & McHale, J. 2006. Gone but Not Forgotten: Knowledge Flows, Labor Mobility, and Enduring Social Relationships. Journal of Economic Geography, 6(5): 571-91. Alcacer, J. & Chung, W. 2007. Location Strategies and Knowledge Spillovers. Management Science, 53(5): 760-76. Almeida, P. & Kogut, B. 1999. Localization of Knowledge and the Mobility of Engineers in Regional Networks. Management Science, 45(7): 905-17. Almeida, P. & Phene, A. 2004. Subsidiaries and Knowledge Creation: The Influence of the Mnc and Host Country on Innovation. Strategic Management Journal, 25(8/9): 847-64. Audretsch, D. B. & Feldman, M. P. 1996. R&D Spillovers and the Geography of Innovation and Production. American Economic Review, 86(3): 630-40. Berry, H. 2012. When Do Firms Divest Foreign Operations? Organization Science, forthcoming. Birkinshaw, J. & Hood, N. 1998. Multinational Subsidiary Evolution: Capability and Charter Change in Foreign-Owned Subsidiary Companies. Academy of Management Review, 23(4): 773-95. Blodgett, L. L. 1991. Partner Contributions as Predictors of Equity Share in International Joint Ventures. Journal of International Business Studies, 22(1): 63-78. Boddewyn, J. J. 1983. Foreign and Domestic Divestment and Investment Decisions: Like or Unlike? Journal of International Business Studies, 14(3): 23-35. Boddewyn, J. J. 1979. Foreign Divestment: Magnitude and Factors. Journal of International Business Studies, 10(1): 21-27. Brauer, M. F. & Wiersema, M. F. 2012. Industry Divestiture Waves: How a Firm's Position Influences Investor Returns. Academy of Management Journal, 55(6): 1472-92. Cantwell, J. & Mudambi, R. 2005. Mne Competence-Creating Subsidiary Mandates. Strategic Management Journal, 26(12): 1109-28. Cassiman, B. & Golovko, E. 2011. Innovation and Internationalization through Exports. Journal of International Business Studies, 42(1): 56-75. Cassiman, B. & Veugelers, R. 2006. In Search of Complementarity in Innovation Strategy: Internal R&D and External Knowledge Acquisition. Management Science, 52(1): 68-82. Chakrabarti, A., Vidal, E., & Mitchell, W. 2011. Business Transformation in Heterogeneous Environments: The Impact of Market Development and Firm Strength on Retrenchment and Growth Reconfiguration. Global Strategy Journal, 1(1-2): 6-26. Cohen, W. M. & Levinthal, D. A. 1990. Absorptive Capacity: A New Perspective on Learning and Innovation. Administrative Science Quarterly, 35(1): 128-53.

25

Cohen, W. M. & Levinthal, D. A. 1994. Fortune Favors the Prepared Firm. Management Science, 40(2): 227-51. Cohen, W. M. & Levinthal, D. A. 1989. Innovation and Learning: The Two Faces of R&D. The Economic Journal, 99: 569-96. Couch, K. A. & Placzek, D. W. 2010. Earnings Losses of Displaced Workers Revisited. American Economic Review, 100(1): 572-89. Czarnitzki, D., Hottenrott, H., & Thorwarth, S. 2011. Industrial Research Versus Development Investment: The Implications of Financial Constraints. Cambridge Journal of Economics, 35(3): 527-44. De Backer, K. & Sleuwaegen, L. 2003. Does Foreign Direct Investment Crowd out Domestic Entrepreneurship? Review of Industrial Organization, 22(1): 67-84. Fallick, B. C. 1996. A Review of the Recent Empirical Literature on Displaced Workers. Industrial and Labor Relations Review, 50(1): 5-16. Feinberg, S. E. & Majumdar, S. K. 2001. Technology Spillovers from Foreign Direct Investment in the Indian Pharmaceutical Industry. Journal of International Business Studies, 32(3): 421-37. Fleming, L. & Sorenson, O. 2004. Science as a Map in Technology Search. Strategic Management Journal, 25(8-9): 909-28. Gibson, J. & Stillman, S. 2009. Why Do Big Firms Pay Higher Wages? Evidence from an International Database. Review of Economics and Statistics, 91(1): 213-18. Hennart, J.-F. 2009. Down with Mne-Centric Theories! Market Entry and Expansion as the Bundling of Mne and Local Assets. Journal of International Business Studies, 40(9): 1432-54. Jacobson, L. S., LaLonde, R. J., & Sullivan, D. G. 1993. Earnings Losses of Displaced Workers. American Economic Review, 83(4): 685-709. King, A. W. 2007. Disentangling Interfirm and Intrafirm Causal Ambiguity: A Conceptual Model of Causal Ambiguity and Sustainable Competitive Advantage. Academy of Management Review, 32(1): 156-78. Kletzer, L. G. 1998. Job Displacement. Journal of Economic Perspectives, 12(1): 115-36. Koehler, C., Sofka, W., & Grimpe, C. 2012. Selective Search, Sectoral Patterns, and the Impact on Product Innovation Performance. Research Policy, 41(8): 1344-56. Kogut, B. 1991. Country Capabilities and the Permeability of Borders. Strategic Management Journal, 12(Special Issue Summer): 33-47. Kogut, B. & Zander, U. 1993. Knowledge of the Firm and the Evolutionary Theory of the Multinational Corporation. Journal of International Business Studies, 24(4): 625-45. Kronborg, D. & Thomsen, S. 2009. Foreign Ownership and Long-Term Survival. Strategic Management Journal, 30(2): 207-19.

26

Lach, S. & Schankerman, M. 2008. Incentives and Invention in Universities. RAND Journal of Economics, 39(2): 403-33. Lane, P. J. & Lubatkin, M. 1998. Relative Absorptive Capacity and Interorganizational Learning. Strategic Management Journal, 19(5): 461-77. Mata, J. & Portugal, P. 2002. The Survival of New Domestic and Foreign-Owned Firms. Strategic Management Journal, 23(4): 323-43. Meyer, K. E. & Sinani, E. 2009. When and Where Does Foreign Direct Investment Generate Positive Spillovers? A Meta-Analysis. Journal of International Business Studies, 40(7): 1075-94. Mezias, J. M. 2002. Identifying Liabilities of Foreignness and Strategies to Minimize Their Effects: The Case of Labor Lawsuit Judgement in the United States. Strategic Management Journal, 23: 229-44. Nachum, L. & Song, S. 2011. The Mne as a Portfolio: Interdependencies in Mne Growth Trajectory. Journal of International Business Studies, 42(3): 381-405. Oxley, J. E. 1997. Appropriability Hazards and Governance in Strategic Alliances: A Transaction Cost Approach. Journal of Law, Economics, and Organization, 13(2): 387-409. Penner-Hahn, J. & Shaver, J. M. 2005. Does International Research and Development Increase Patent Output? An Analysis of Japanese Pharmaceutical Firms. Strategic Management Journal, 26(2): 121-40. Psacharopoulos, G. 1985. Returns to Education: A Further International Update and Implications. Journal of Human Resources, 20(4): 583-604. Ranft, A. L. & Lord, M. D. 2000. Acquiring New Knowledge: The Role of Retaining Human Capital in Acquisitions of High-Tech Firms. Journal of High Technology Management Research, 11(2): 295-319. Salomon, R. & Jin, B. 2010. Do Leading or Lagging Firms Learn More from Exporting? Strategic Management Journal, 31(10): 1088-113. Song, J., Almeida, P., & Wu, G. 2003. Learning-by-Hiring: When Is Mobility More Likely to Facilitate Interfirm Knowledge Transfer? Management Science, 49(4): 351-65. Zaheer, S. 1995. Overcoming the Liability of Foreignness. Academy of Management Journal, 38(2): 341-64. Zaheer, S. & Mosakowski, E. 1997. The Dynamics of the Liability of Foreignness: A Global Study of Survival in Financial Services. Strategic Management Journal, 18(6): 439-64. Zhao, M. 2006. Conducting R&D in Countries with Weak Intellectual Property Rights Protection. Management Science, 52(8): 1185-99.

27

TABLES

Table 1: Descriptive statistics

Variable Mean Standard

deviation

Wage in the new firm 5.940 5.324Last 2 years average wage – old firm (log) 5.655 5.025Foreign capital - old firm (share) 0.095 0.279Sales per worker - old firm (in thousands) 135.979 580.669Sales per worker - new firm (in thousands) 115.400 878.111Basic education (d) 0.236 0.424Secondary education (d) 0.216 0.411Tertiary education (d) 0.107 0.309Gender (d) 0.398 0.490Age 37.861 10.065Tenure in the old firm 6.367 7.081No industry switch after displacement (d) 0.881 0.323Foreign nationality (d) 0.052 0.223Professionals (d) 0.659 0.474Managers / supervisors (d) 0.128 0.334Employees with higher education - old firm (share)0.104 0.181Foreign capital - new firm (share) 0.115 0.304Size – new firm (log) 1550.737 4179.411Location Lisbon/Oporto (d) 0.516 0.500Manufacturing (d) 0.244 0.430Energy (d) 0.151 0.358Services (d) 0.514 0.500Community, social and personal services (d) 0.066 0.2482006 (d) 0.150 0.3572007 (d) 0.194 0.3952008 (d) 0.201 0.4012009 (d) 0.206 0.405Nº observations 138256

28

Table 2: Results of dynamic fixed effects regression on hourly salary in new firm

I II III

Foreign capital - old firm (share) 0.173*** 1.864*** 1.221*** (0.018) (0.139) (0.186)

Foreign capital squared - old firm (share) -0.138*** -2.463*** -1.651***

(0.018) (0.145) (0.189)

Sales per worker - old firm (log) 0.001* -0.000 0.001† (0.001) (0.001) (0.001)

Foreign capital - old firm * Sales per worker - old firm

-0.142*** (0.012)

Foreign capital squared - old firm * Sales per worker - old firm

0.196*** (0.012)

Sales per worker - new firm (log) 0.018*** 0.017*** 0.015*** (0.001) (0.001) (0.001)

Foreign capital - old firm * Sales per worker - new firm

-0.089*** (0.016)

Foreign capital squared - old firm * Sales per worker new firm

0.130*** (0.016)

Last 2 years average wage – old firm (log) 0.728*** 0.724*** 0.726*** (0.002) (0.002) (0.002)

Basic education (d) 0.031*** 0.030*** 0.031*** (0.002) (0.002) (0.002)

Secondary education (d) 0.079*** 0.077*** 0.079*** (0.002) (0.002) (0.002)

Tertiary education (d) 0.143*** 0.142*** 0.143*** (0.003) (0.003) (0.003)

Gender (d) -0.060*** -0.061*** -0.060***

(0.002) (0.002) (0.002)

Age 0.001*** 0.001*** 0.001*** (0.000) (0.000) (0.000)

Tenure in the old firm 0.001*** 0.001*** 0.001*** (0.000) (0.000) (0.000)

No industry switch after displacement (d) 0.001 0.002 0.000

(0.002) (0.002) (0.002)

Foreign nationality (d) -0.006† -0.006* -0.006* (0.003) (0.003) (0.003)

Professionals (d) 0.057*** 0.057*** 0.058*** (0.002) (0.002) (0.002)

Managers / supervisors (d) 0.184*** 0.186*** 0.186*** (0.003) (0.003) (0.003)

Employees with higher education - old firm (share)

0.131*** 0.129*** 0.129*** (0.005) (0.005) (0.005)

Foreign capital - new firm (share) -0.004† 0.004 -0.003 (0.003) (0.003) (0.003)

29

I II III

Size – new firm (log) 0.011*** 0.011*** 0.011*** (0.000) (0.000) (0.000)

Location Lisbon/Oporto (d) 0.016*** 0.017*** 0.015*** (0.002) (0.002) (0.002)

Manufacturing (d) -0.042*** -0.030*** -0.038***

(0.005) (0.005) (0.005)

Energy (d) -0.020*** -0.011* -0.017***

(0.005) (0.005) (0.005)

Services (d) -0.018*** -0.007 -0.015***

(0.004) (0.005) (0.005)

Community, social and personal services (d) -0.011* 0.007 -0.005 (0.005) (0.005) (0.005)

2006 (d) -0.027*** -0.024*** -0.026***

(0.002) (0.002) (0.002)

2007 (d) -0.027*** -0.025*** -0.026***

(0.002) (0.002) (0.002)

2008 (d) -0.022*** -0.021*** -0.023***

(0.002) (0.002) (0.002)

2009 (d) -0.011*** -0.008*** -0.010***

(0.002) (0.002) (0.002)

Constant 0.113*** 0.129*** 0.135*** (0.009) (0.009) (0.009)

Observations 138,256 138,256 138,256 R-squared 0.813 0.814 0.814 F test 22308.526 20910.308 20859.100 † p<0.10, * p<0.05, ** p<0.01, *** p<0.001; standard errors in parentheses.

30

FIGURES

Figure 1: Foreign capital of the closed firm vs hourly wage

31

Figure 2: Foreign capital of the closed firm vs hourly wage for three different levels of productivity of the closed firm

32

Figure 3: Foreign capital of the closed firm vs hourly wage for three different levels of productivity of the hiring firm

33

i For convenience in writing and reading, we choose the female form as a default when we refer to

employees throughout the text, i.e. by using “she” and “her.” This should not be misunderstood as

relating exclusively to women. All theoretical argumentations apply to male and female employees

equally, but “her/his” and “she/he” would make the text harder to read and distract from the core of

the article.

ii Based on this procedure, mergers and acquisitions cannot be ruled out; however, Mata and Portugal

(2002) show that this problem occurs in very few cases and does not differently affect MNC

subsidiaries and domestic firms. Therefore, this factor cannot be expected to bias our results.

Related Documents