MLPA Conference, Orlando June, 2016

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

MLPA Conference, Orlando

June, 2016

2

Notice to Recipients

This presentation is not a prospectus and is not an offer to sell, nor a solicitation of an offer to buy, securities.

Except for the historical information contained herein, the matters discussed in this presentation include

forward-looking statements that involve risks and uncertainties. These risks and uncertainties include, among

other things, market conditions and other factors that are described in KNOT Offshore Partners LP’s (“KNOP”)

filings with the U.S Securities and Exchange Commission (“SEC”), which are available on the SEC’s website at

http://www.sec.gov.

Nevertheless, new factors emerge from time to time, and it is not possible for KNOP to predict all of these

factors. Further, KNOP cannot assess the impact of each such factor on its business or the extent to which any

factor, or combination of factors, may cause actual results to be materially different from those contained in any

forward-looking statement. KNOP expressly disclaims any intention or obligation to revise or publicly update

any forward-looking statements whether as a result of new information, future events or otherwise. The forward-

looking statements contained herein are expressly qualified by this cautionary notice to recipients.

3

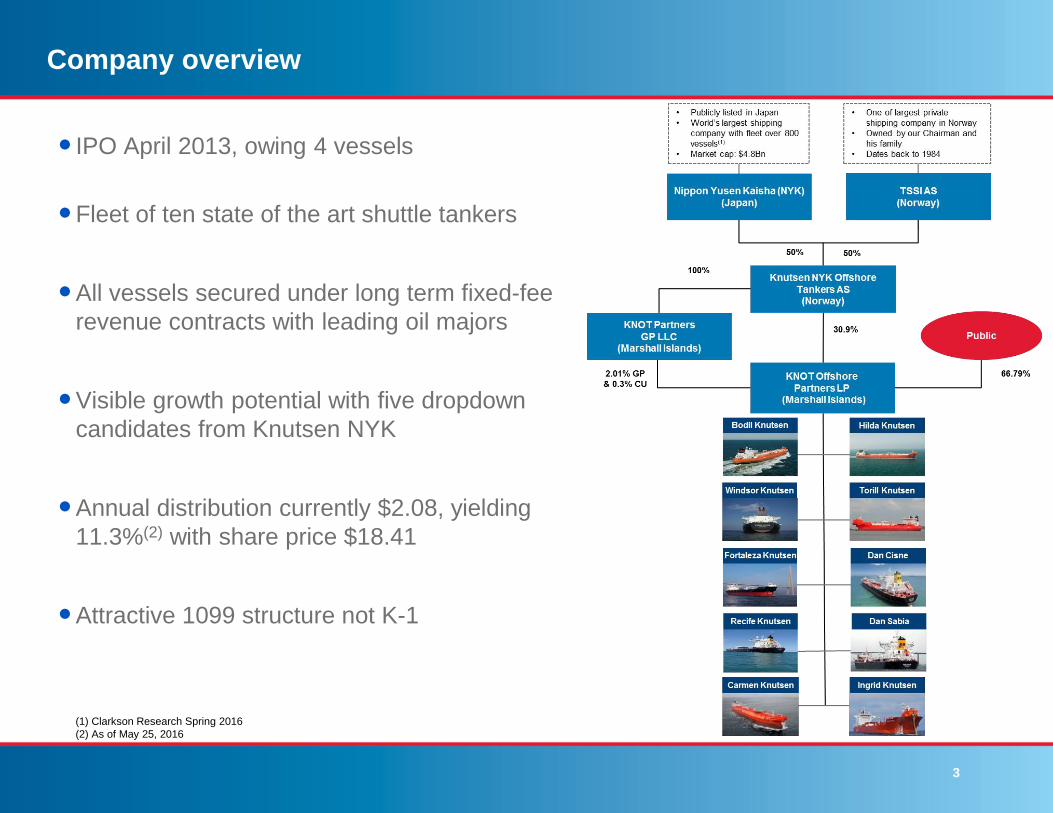

Company overview

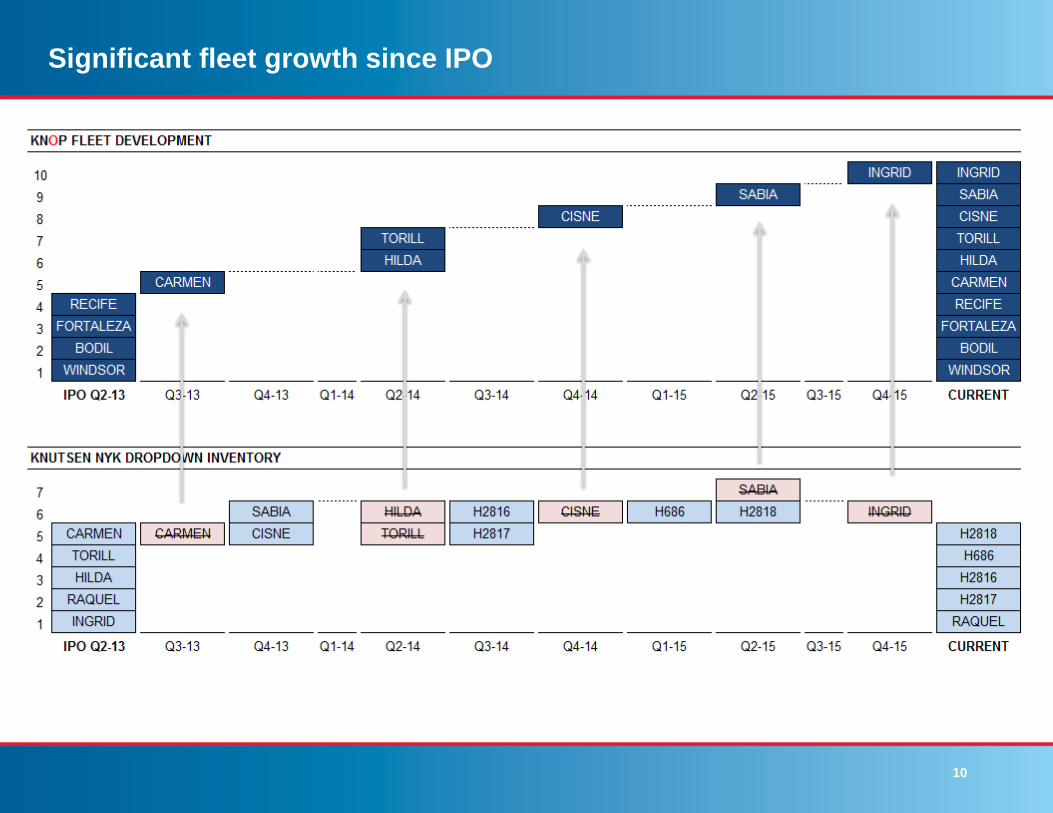

IPO April 2013, owing 4 vessels

Fleet of ten state of the art shuttle tankers

All vessels secured under long term fixed-fee

revenue contracts with leading oil majors

Visible growth potential with five dropdown

candidates from Knutsen NYK

Annual distribution currently $2.08, yielding

11.3%(2) with share price $18.41

Attractive 1099 structure not K-1

(1) Clarkson Research Spring 2016

(2) As of May 25, 2016

4

Business Strategy

Pursue strategic &

accretive acquisitions of

shuttle tankers on long-

term, fixed- rate charters

Expand global operations

in high-growth regions

Manage fleet and deepen

customer relationships to

provide a stable cash flow

base

Right to purchase any existing or any new-build tankers that are under long-term

charters (5 years or more) from Knutsen NYK

– 5 identified candidates; one vessel, Raquel Knutsen delivered in 2015, on 10-

years contract with Repsol Sinopec Brazil and four new-builds; delivery

between 4Q16 and 2Q17

Assess other attractive acquisitions from Knutsen NYK and 3rd parties on

opportunistic basis

Expand operations alongside the growth of global offshore oil production in

proven areas such as the North Sea and Brazil as well as other new markets as

they develop

Focus on strong customer relationships and maintain track record of

consistency, safety and reliability

Actively seek extension and renewal of existing charters for new opportunities

5

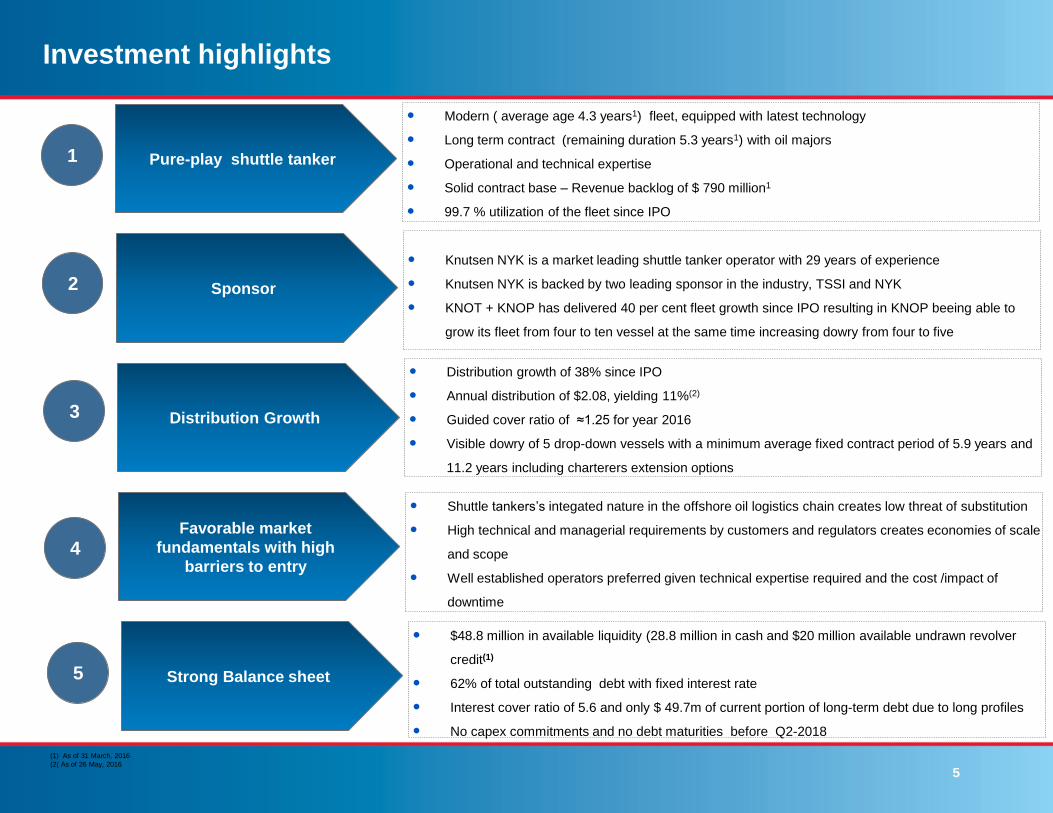

Investment highlights

Pure-play shuttle tanker

Modern ( average age 4.3 years1) fleet, equipped with latest technology

Long term contract (remaining duration 5.3 years1) with oil majors

Operational and technical expertise

Solid contract base – Revenue backlog of $ 790 million1

99.7 % utilization of the fleet since IPO

1

Sponsor

Knutsen NYK is a market leading shuttle tanker operator with 29 years of experience

Knutsen NYK is backed by two leading sponsor in the industry, TSSI and NYK

KNOT + KNOP has delivered 40 per cent fleet growth since IPO resulting in KNOP beeing able to

grow its fleet from four to ten vessel at the same time increasing dowry from four to five

2

Distribution Growth

Distribution growth of 38% since IPO

Annual distribution of $2.08, yielding 11%(2)

Guided cover ratio of ≈1.25 for year 2016

Visible dowry of 5 drop-down vessels with a minimum average fixed contract period of 5.9 years and

11.2 years including charterers extension options

3

Favorable market

fundamentals with high

barriers to entry

Shuttle tankers’s integated nature in the offshore oil logistics chain creates low threat of substitution

High technical and managerial requirements by customers and regulators creates economies of scale

and scope

Well established operators preferred given technical expertise required and the cost /impact of

downtime

4

Strong Balance sheet

$48.8 million in available liquidity (28.8 million in cash and $20 million available undrawn revolver

credit(1)

62% of total outstanding debt with fixed interest rate

Interest cover ratio of 5.6 and only $ 49.7m of current portion of long-term debt due to long profiles

No capex commitments and no debt maturities before Q2-2018

5

(1) As of 31 March, 2016

(2( As of 26 May, 2016

6

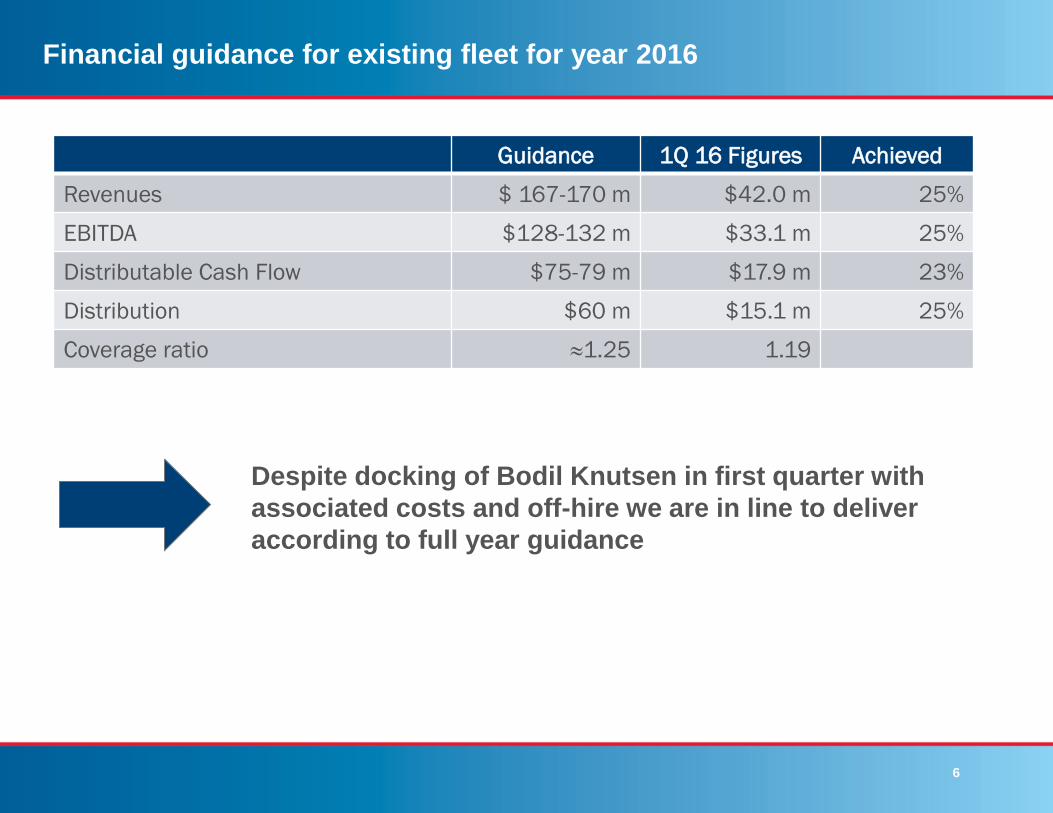

Financial guidance for existing fleet for year 2016

Guidance 1Q 16 Figures Achieved

Revenues $ 167-170 m $42.0 m 25%

EBITDA $128-132 m $33.1 m 25%

Distributable Cash Flow $75-79 m $17.9 m 23%

Distribution $60 m $15.1 m 25%

Coverage ratio ≈1.25 1.19

Despite docking of Bodil Knutsen in first quarter with

associated costs and off-hire we are in line to deliver

according to full year guidance

7

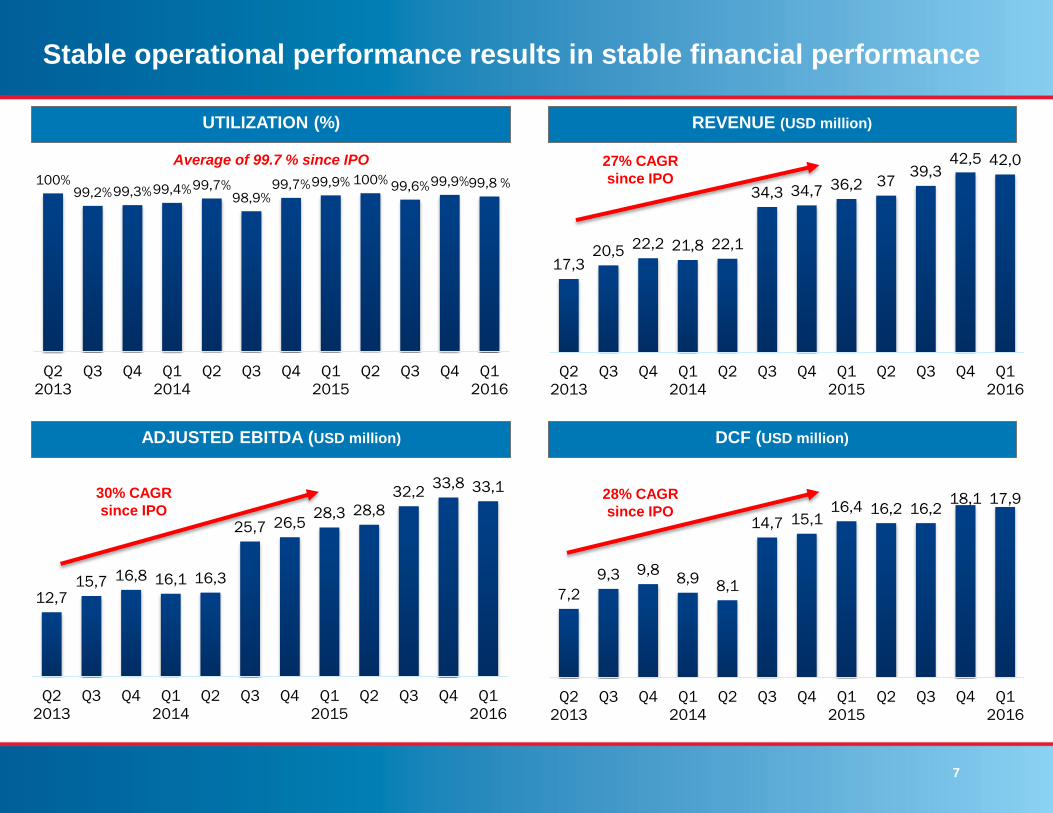

Stable operational performance results in stable financial performance

17,320,5

22,2 21,8 22,1

34,3 34,7 36,2 3739,3

42,5 42,0

Q2

2013

Q3 Q4 Q1

2014

Q2 Q3 Q4 Q1

2015

Q2 Q3 Q4 Q1

2016

REVENUE (USD million)

ADJUSTED EBITDA (USD million)

100%99,2%99,3%99,4%99,7%

98,9%99,7%99,9% 100%

99,6%99,9%99,8 %

Q2

2013

Q3 Q4 Q1

2014

Q2 Q3 Q4 Q1

2015

Q2 Q3 Q4 Q1

2016

UTILIZATION (%)

7,2

9,3 9,88,9

8,1

14,7 15,116,4 16,2 16,2

18,1 17,9

Q2

2013

Q3 Q4 Q1

2014

Q2 Q3 Q4 Q1

2015

Q2 Q3 Q4 Q1

2016

12,715,7 16,8 16,1 16,3

25,7 26,528,3 28,8

32,233,8 33,1

Q2

2013

Q3 Q4 Q1

2014

Q2 Q3 Q4 Q1

2015

Q2 Q3 Q4 Q1

2016

DCF (USD million)

Average of 99.7 % since IPO 27% CAGR

since IPO

28% CAGR

since IPO

30% CAGR

since IPO

8

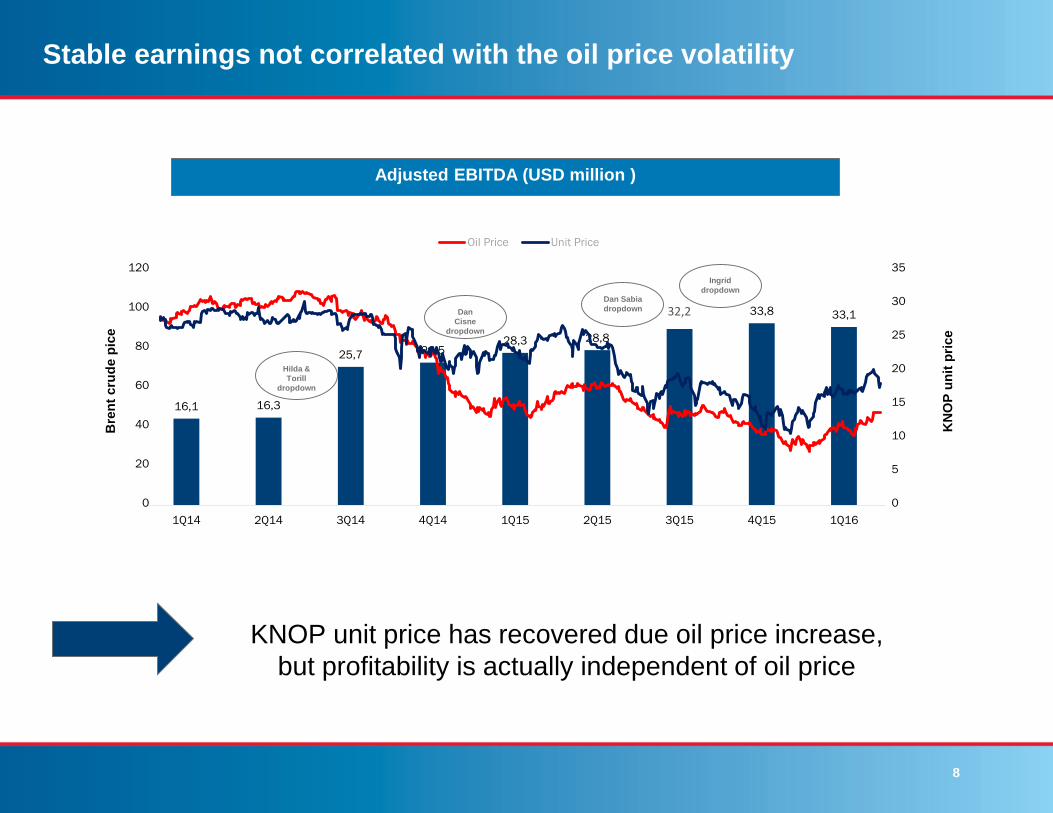

16,1 16,3

25,7 26,528,3 28,8

33,8 33,8 33,1

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16

Stable earnings not correlated with the oil price volatility

0

5

10

15

20

25

30

35

0

20

40

60

80

100

120

Oil Price Unit Price

Adjusted EBITDA (USD million )

Bre

nt

cru

de p

ice

KN

OP

un

it p

rice

KNOP unit price has recovered due oil price increase,

but profitability is actually independent of oil price

Hilda &

Torill

dropdown

Dan

Cisne

dropdown

32,2Dan Sabia

dropdown

Ingrid

dropdown

9

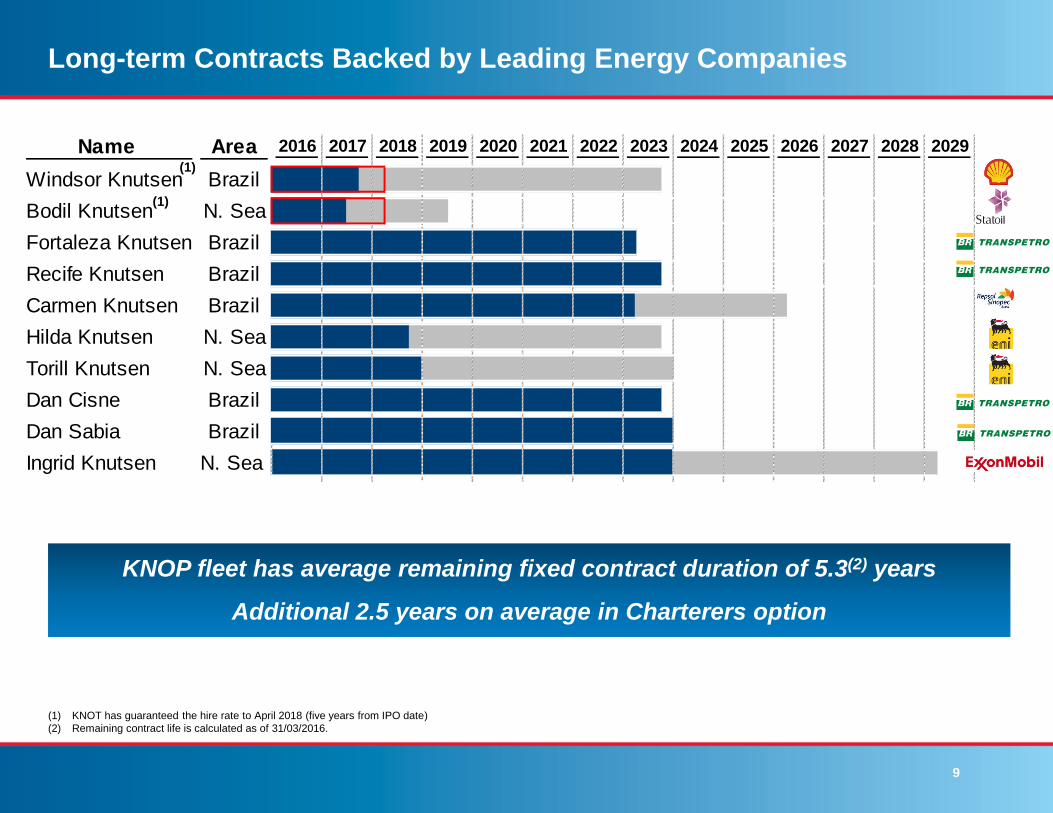

Name Area 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Windsor Knutsen Brazil

Bodil Knutsen N. Sea

Fortaleza Knutsen Brazil

Recife Knutsen Brazil

Carmen Knutsen Brazil

Hilda Knutsen N. Sea

Torill Knutsen N. Sea

Dan Cisne Brazil

Dan Sabia Brazil

Ingrid Knutsen N. Sea

Long-term Contracts Backed by Leading Energy Companies

KNOP fleet has average remaining fixed contract duration of 5.3(2) years

Additional 2.5 years on average in Charterers option

(1) KNOT has guaranteed the hire rate to April 2018 (five years from IPO date)

(2) Remaining contract life is calculated as of 31/03/2016.

(1)

(1)

10

Significant fleet growth since IPO

11

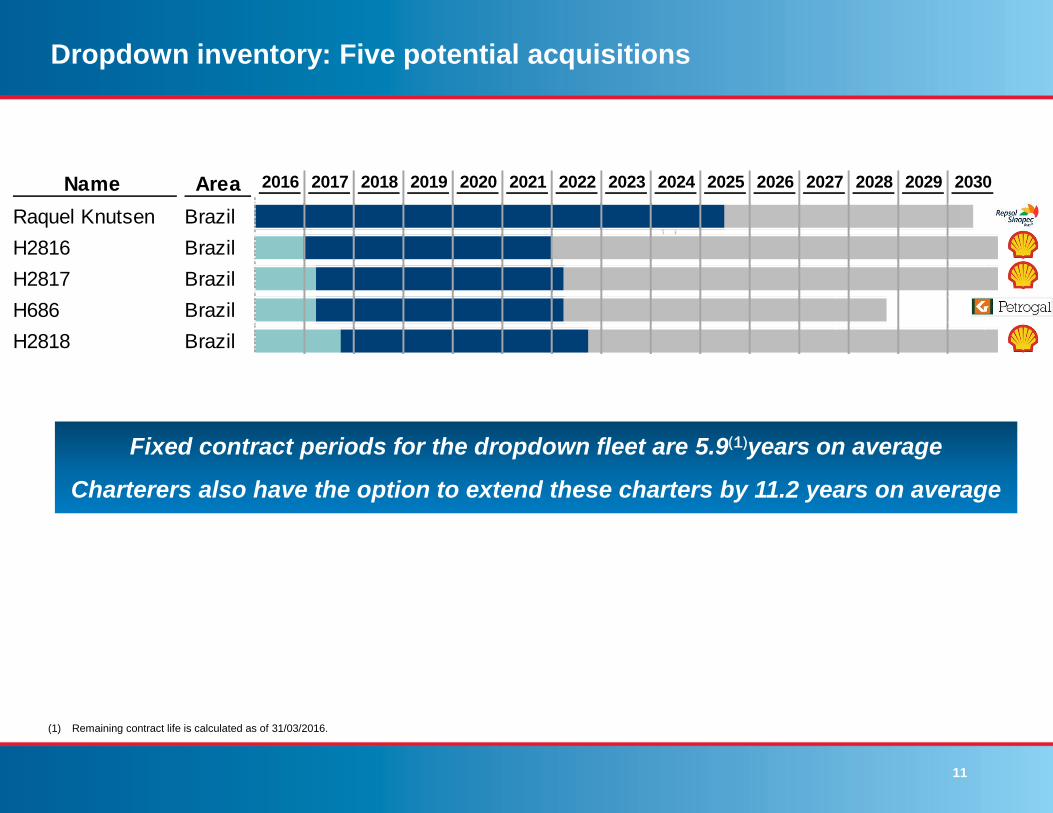

Dropdown inventory: Five potential acquisitions

Fixed contract periods for the dropdown fleet are 5.9(1)years on average

Charterers also have the option to extend these charters by 11.2 years on average

(1) Remaining contract life is calculated as of 31/03/2016.

Name Area 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Raquel Knutsen Brazil

H2816 Brazil

H2817 Brazil

H686 Brazil

H2818 Brazil

12

Shuttle Tanker Market Overview

Shuttle Tanker

Market Overview

13

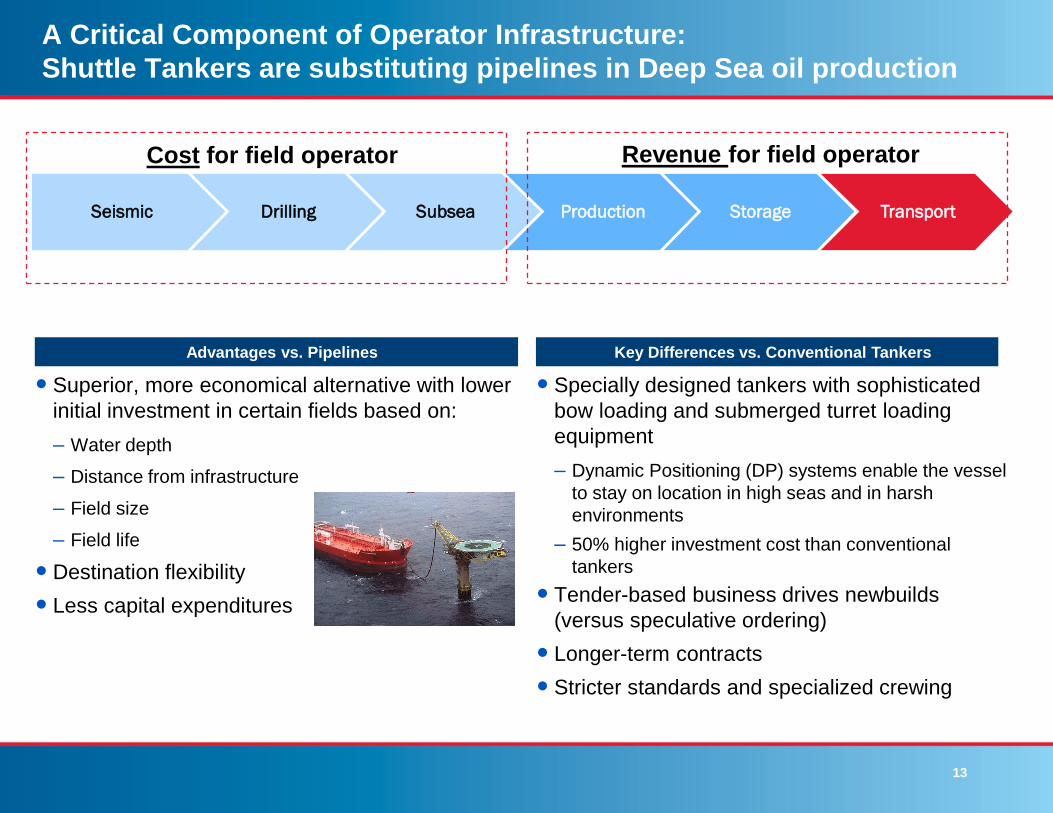

A Critical Component of Operator Infrastructure:

Shuttle Tankers are substituting pipelines in Deep Sea oil production

Superior, more economical alternative with lower

initial investment in certain fields based on:

– Water depth

– Distance from infrastructure

– Field size

– Field life

Destination flexibility

Less capital expenditures

Specially designed tankers with sophisticated

bow loading and submerged turret loading

equipment

– Dynamic Positioning (DP) systems enable the vessel

to stay on location in high seas and in harsh

environments

– 50% higher investment cost than conventional

tankers

Tender-based business drives newbuilds

(versus speculative ordering)

Longer-term contracts

Stricter standards and specialized crewing

Advantages vs. Pipelines Key Differences vs. Conventional Tankers

Seismic Drilling Subsea Production Storage Transport

Cost for field operator Revenue for field operator

14

Specialized Asset Class Standardized Asset Class

Shuttle Tankers Conventional Tankers Dry Bulk Carriers

Function

Transport from FPSO or

production unit to terminal

/ refinery

Transports crude and

products to and from

terminal / refinery

Specializes in break bulk

dry cargoes such as coal

Ordering With contractPredominantly

speculative

Predominantly

speculative

Typical

Trading

Long-term contracts:

(5 - 15 years)

Spot contracts,

sometimes longer

Spot contracts,

sometimes longer

Total Size /

Capacity of

Global Fleet

9mm Dead Weight Tons 440mm Dead Weight Tons 670mm Dead Weight Tons

LNG

Transports to and from

terminal / refinery

With contract /

Speculative

Long-term contracts

(5 - 25 years)

53mm Cubic Meters

Shuttle Tankers:

Niche market where new capacity is based on long term contracts

Sources: Fearnleys and Clarksons February 2016.

Shuttle Tankers are a unique and highly specialized asset class that is integral to the offshore oil infrastructure

72 Vessels

420 Vessels5,300 Vessels 10,500 Vessels

62 m Cubic Meters 505 m Dead Weight Tons 775m Dead Weight Tons99 m Dead Weight Tons

15

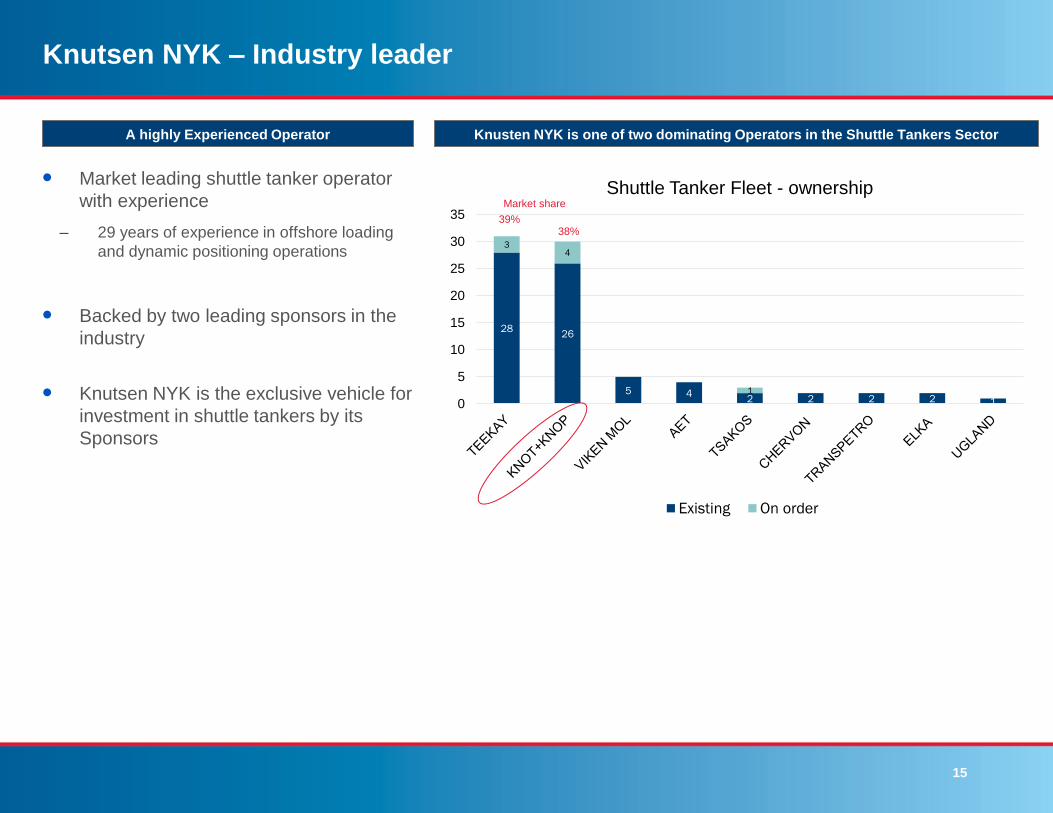

Knutsen NYK – Industry leader

2826

5 42 2 2 2 1

34

1

0

5

10

15

20

25

30

35

Shuttle Tanker Fleet - ownership

Existing On order

Market leading shuttle tanker operator

with experience

– 29 years of experience in offshore loading

and dynamic positioning operations

Backed by two leading sponsors in the

industry

Knutsen NYK is the exclusive vehicle for

investment in shuttle tankers by its

Sponsors

A highly Experienced Operator Knusten NYK is one of two dominating Operators in the Shuttle Tankers Sector

39%38%

Market share

16

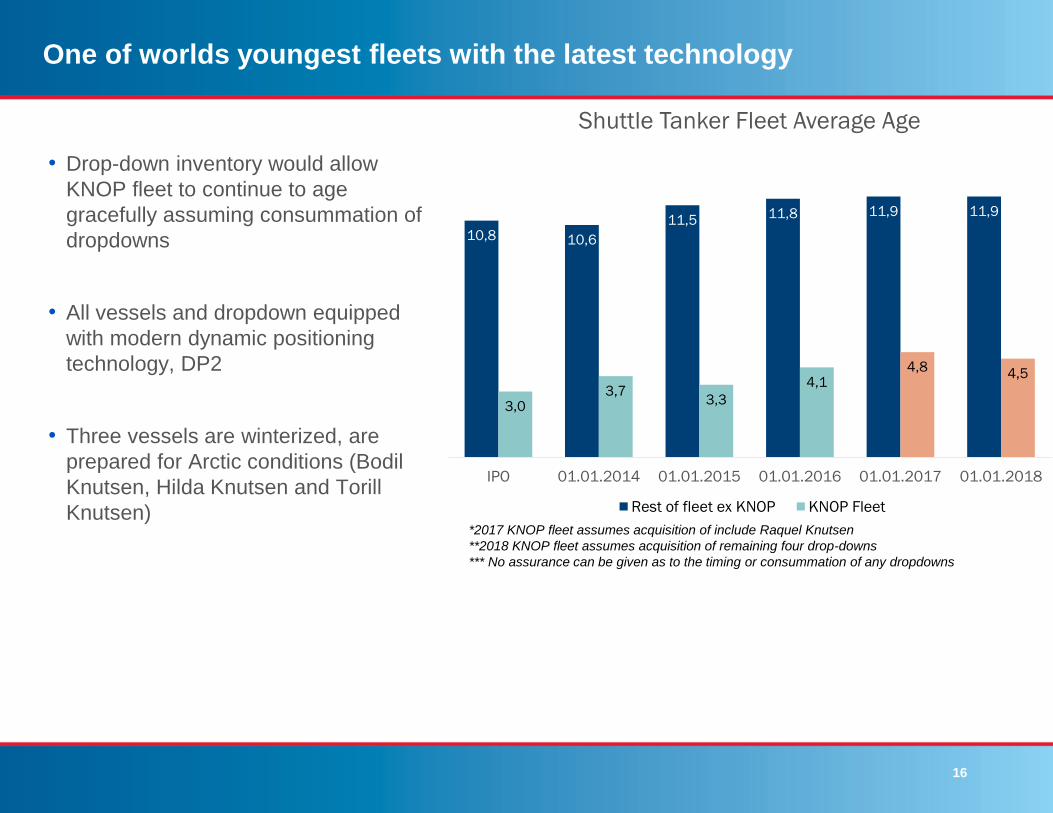

One of worlds youngest fleets with the latest technology

• Drop-down inventory would allow

KNOP fleet to continue to age

gracefully assuming consummation of

dropdowns

• All vessels and dropdown equipped

with modern dynamic positioning

technology, DP2

• Three vessels are winterized, are

prepared for Arctic conditions (Bodil

Knutsen, Hilda Knutsen and Torill

Knutsen)*2017 KNOP fleet assumes acquisition of include Raquel Knutsen

**2018 KNOP fleet assumes acquisition of remaining four drop-downs

*** No assurance can be given as to the timing or consummation of any dropdowns

10,8 10,6

11,511,8 11,9 11,9

3,03,7

3,3

4,14,8

4,5

IPO 01.01.2014 01.01.2015 01.01.2016 01.01.2017 01.01.2018

Shuttle Tanker Fleet Average Age

Rest of fleet ex KNOP KNOP Fleet

17

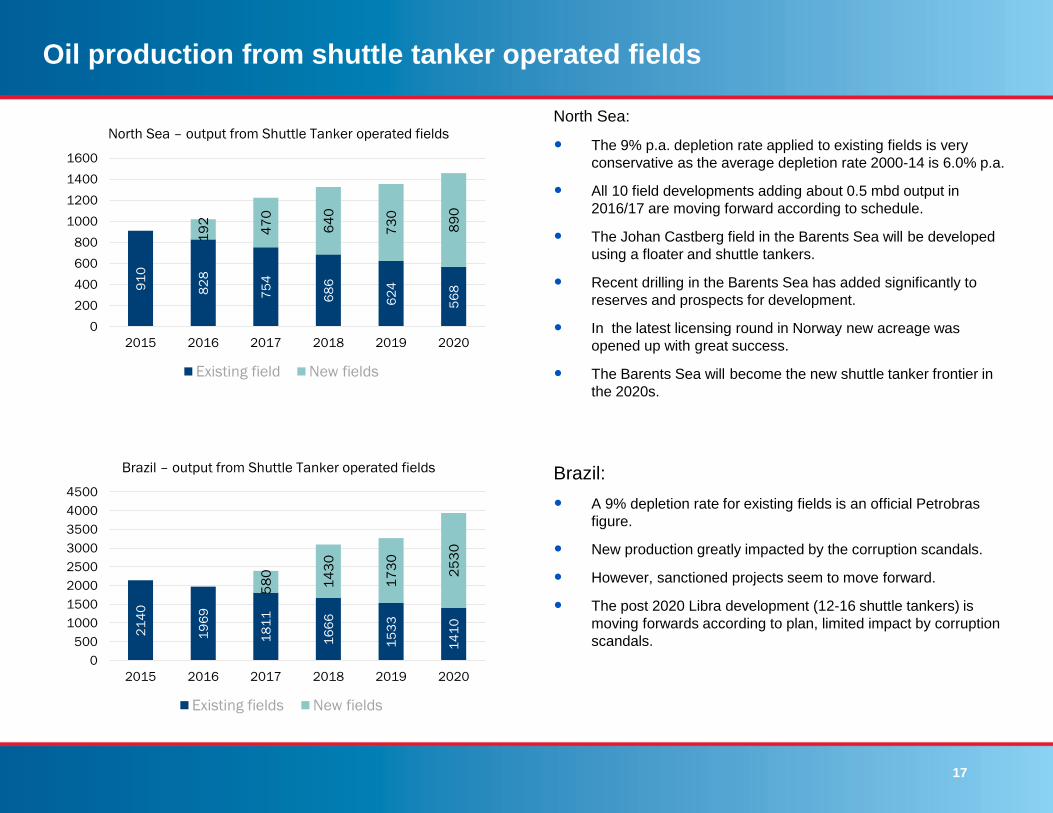

Oil production from shuttle tanker operated fields

91

0

82

8

75

4

68

6

62

4

56

8

19

2

47

0

64

0

73

0

89

0

0

200

400

600

800

1000

1200

1400

1600

2015 2016 2017 2018 2019 2020

North Sea – output from Shuttle Tanker operated fields

Existing field New fields

21

40

19

69

18

11

16

66

15

33

14

10

58

0

14

30

17

30

25

30

0

500

1000

1500

2000

2500

3000

3500

4000

4500

2015 2016 2017 2018 2019 2020

Brazil – output from Shuttle Tanker operated fields

Existing fields New fields

North Sea:

The 9% p.a. depletion rate applied to existing fields is very

conservative as the average depletion rate 2000-14 is 6.0% p.a.

All 10 field developments adding about 0.5 mbd output in

2016/17 are moving forward according to schedule.

The Johan Castberg field in the Barents Sea will be developed

using a floater and shuttle tankers.

Recent drilling in the Barents Sea has added significantly to

reserves and prospects for development.

In the latest licensing round in Norway new acreage was

opened up with great success.

The Barents Sea will become the new shuttle tanker frontier in

the 2020s.

Brazil:

A 9% depletion rate for existing fields is an official Petrobras

figure.

New production greatly impacted by the corruption scandals.

However, sanctioned projects seem to move forward.

The post 2020 Libra development (12-16 shuttle tankers) is

moving forwards according to plan, limited impact by corruption

scandals.

18

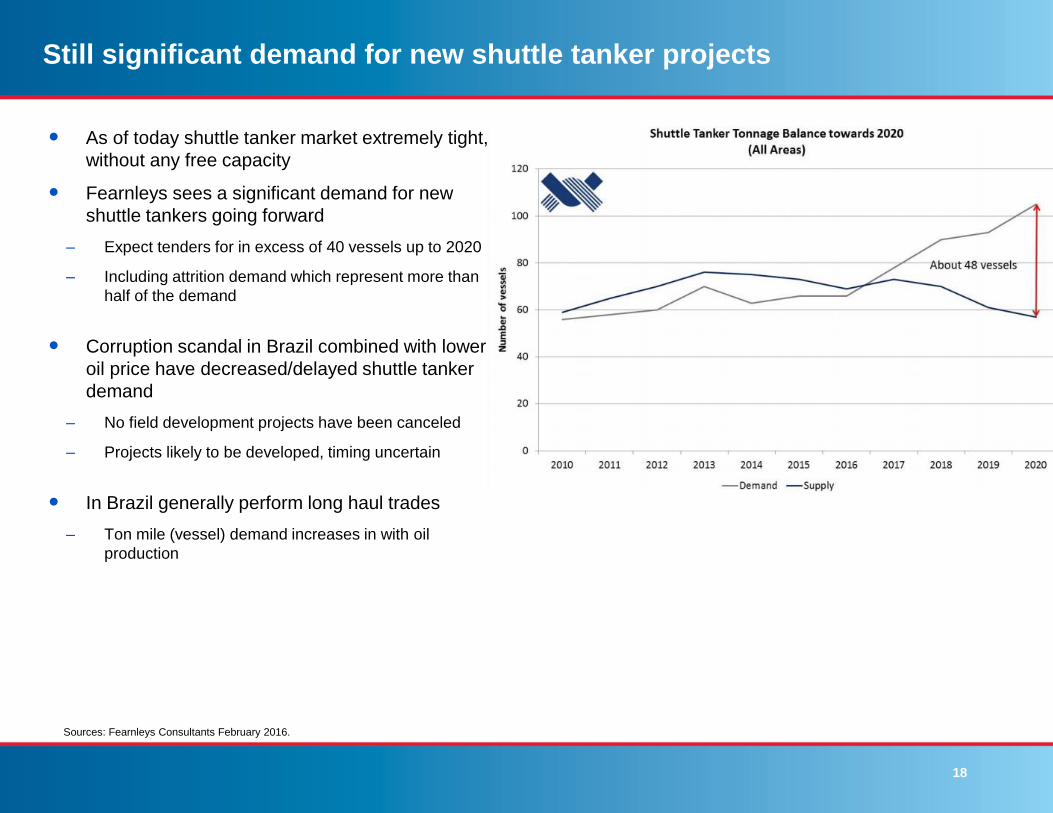

Still significant demand for new shuttle tanker projects

As of today shuttle tanker market extremely tight,

without any free capacity

Fearnleys sees a significant demand for new

shuttle tankers going forward

– Expect tenders for in excess of 40 vessels up to 2020

– Including attrition demand which represent more than

half of the demand

Corruption scandal in Brazil combined with lower

oil price have decreased/delayed shuttle tanker

demand

– No field development projects have been canceled

– Projects likely to be developed, timing uncertain

In Brazil generally perform long haul trades

– Ton mile (vessel) demand increases in with oil

production

Sources: Fearnleys Consultants February 2016.

19

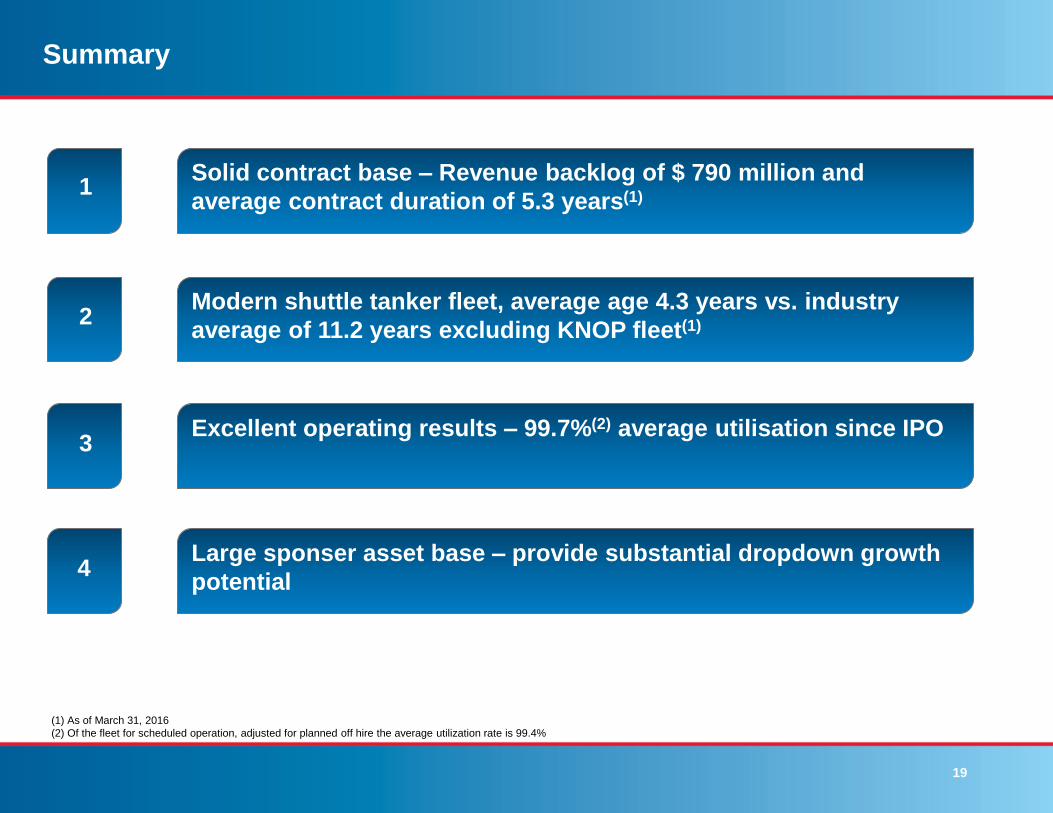

Summary

Solid contract base – Revenue backlog of $ 790 million and

average contract duration of 5.3 years(1)

1

Modern shuttle tanker fleet, average age 4.3 years vs. industry

average of 11.2 years excluding KNOP fleet(1)

Excellent operating results – 99.7%(2) average utilisation since IPO

Large sponser asset base – provide substantial dropdown growth

potential

1

2

3

4

(1) As of March 31, 2016

(2) Of the fleet for scheduled operation, adjusted for planned off hire the average utilization rate is 99.4%

Appendix

APPENDIX

21

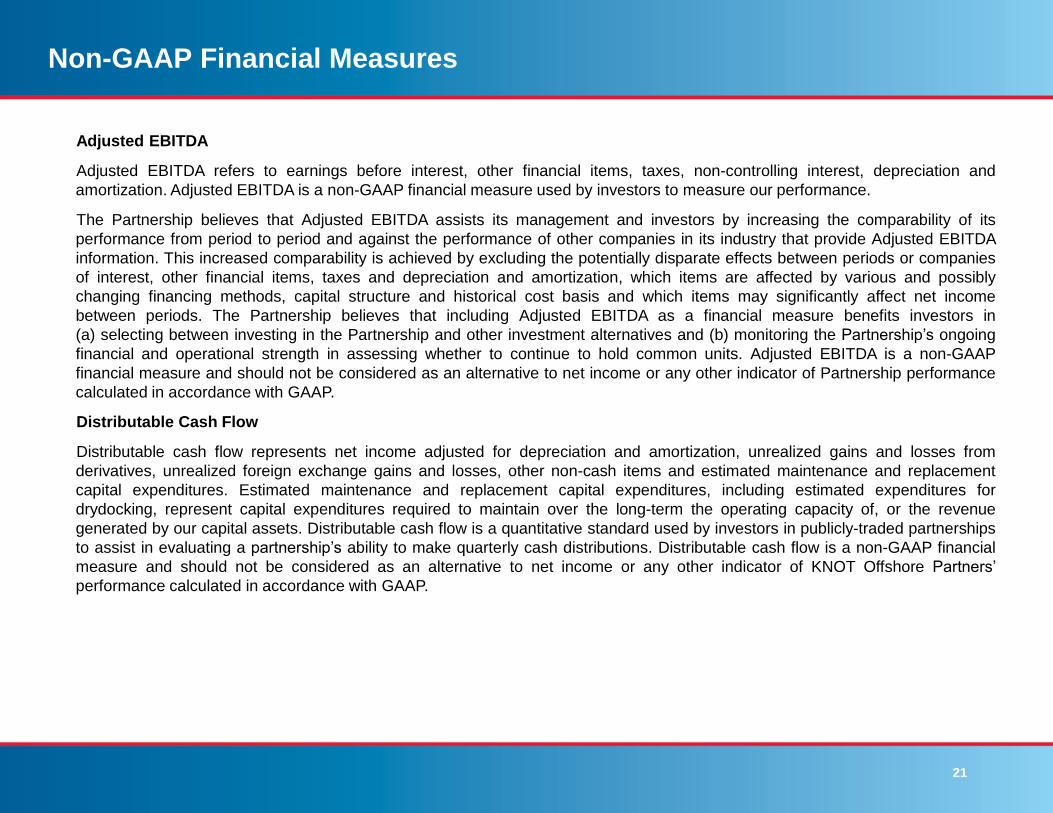

Non-GAAP Financial Measures

Adjusted EBITDA

Adjusted EBITDA refers to earnings before interest, other financial items, taxes, non-controlling interest, depreciation and

amortization. Adjusted EBITDA is a non-GAAP financial measure used by investors to measure our performance.

The Partnership believes that Adjusted EBITDA assists its management and investors by increasing the comparability of its

performance from period to period and against the performance of other companies in its industry that provide Adjusted EBITDA

information. This increased comparability is achieved by excluding the potentially disparate effects between periods or companies

of interest, other financial items, taxes and depreciation and amortization, which items are affected by various and possibly

changing financing methods, capital structure and historical cost basis and which items may significantly affect net income

between periods. The Partnership believes that including Adjusted EBITDA as a financial measure benefits investors in

(a) selecting between investing in the Partnership and other investment alternatives and (b) monitoring the Partnership’s ongoing

financial and operational strength in assessing whether to continue to hold common units. Adjusted EBITDA is a non-GAAP

financial measure and should not be considered as an alternative to net income or any other indicator of Partnership performance

calculated in accordance with GAAP.

Distributable Cash Flow

Distributable cash flow represents net income adjusted for depreciation and amortization, unrealized gains and losses from

derivatives, unrealized foreign exchange gains and losses, other non-cash items and estimated maintenance and replacement

capital expenditures. Estimated maintenance and replacement capital expenditures, including estimated expenditures for

drydocking, represent capital expenditures required to maintain over the long-term the operating capacity of, or the revenue

generated by our capital assets. Distributable cash flow is a quantitative standard used by investors in publicly-traded partnerships

to assist in evaluating a partnership’s ability to make quarterly cash distributions. Distributable cash flow is a non-GAAP financial

measure and should not be considered as an alternative to net income or any other indicator of KNOT Offshore Partners’

performance calculated in accordance with GAAP.

22

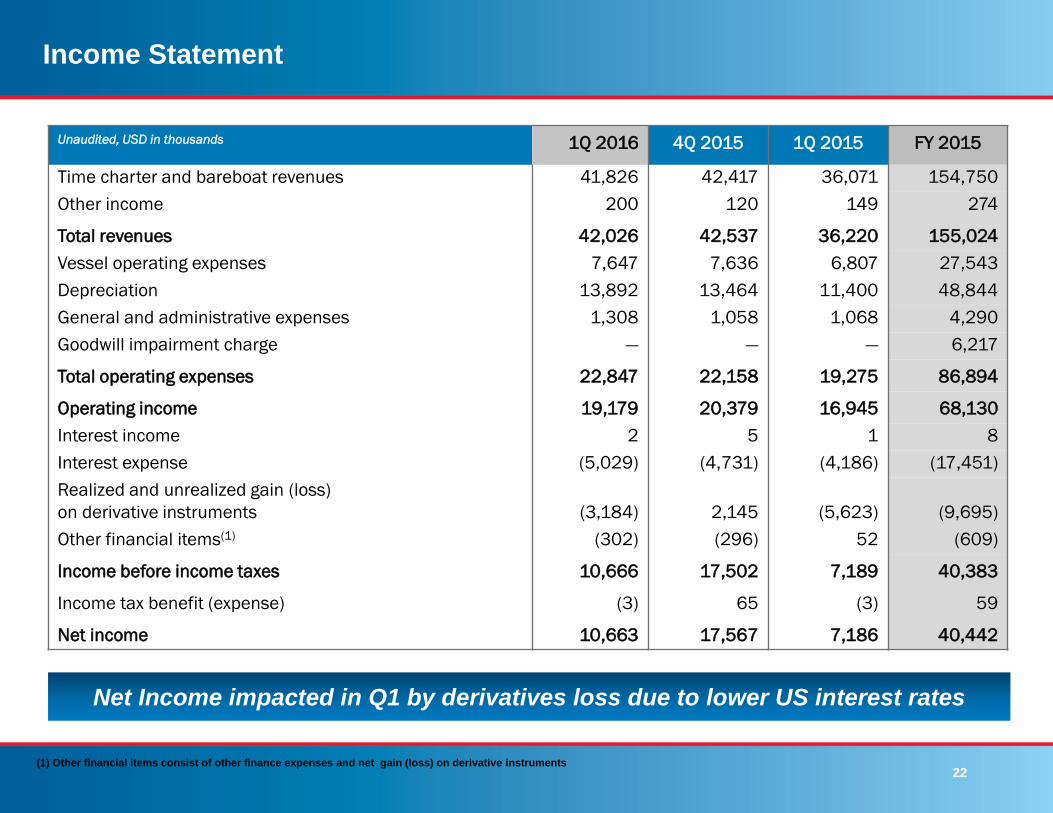

Income Statement

Unaudited, USD in thousands 1Q 2016 4Q 2015 1Q 2015 FY 2015

Time charter and bareboat revenues 41,826 42,417 36,071 154,750

Other income 200 120 149 274

Total revenues 42,026 42,537 36,220 155,024

Vessel operating expenses 7,647 7,636 6,807 27,543

Depreciation 13,892 13,464 11,400 48,844

General and administrative expenses 1,308 1,058 1,068 4,290

Goodwill impairment charge — — — 6,217

Total operating expenses 22,847 22,158 19,275 86,894

Operating income 19,179 20,379 16,945 68,130

Interest income 2 5 1 8

Interest expense (5,029) (4,731) (4,186) (17,451)

Realized and unrealized gain (loss)

on derivative instruments (3,184) 2,145 (5,623) (9,695)

Other financial items(1) (302) (296) 52 (609)

Income before income taxes 10,666 17,502 7,189 40,383

Income tax benefit (expense) (3) 65 (3) 59

Net income 10,663 17,567 7,186 40,442

(1) Other financial items consist of other finance expenses and net gain (loss) on derivative instruments

Net Income impacted in Q1 by derivatives loss due to lower US interest rates

23

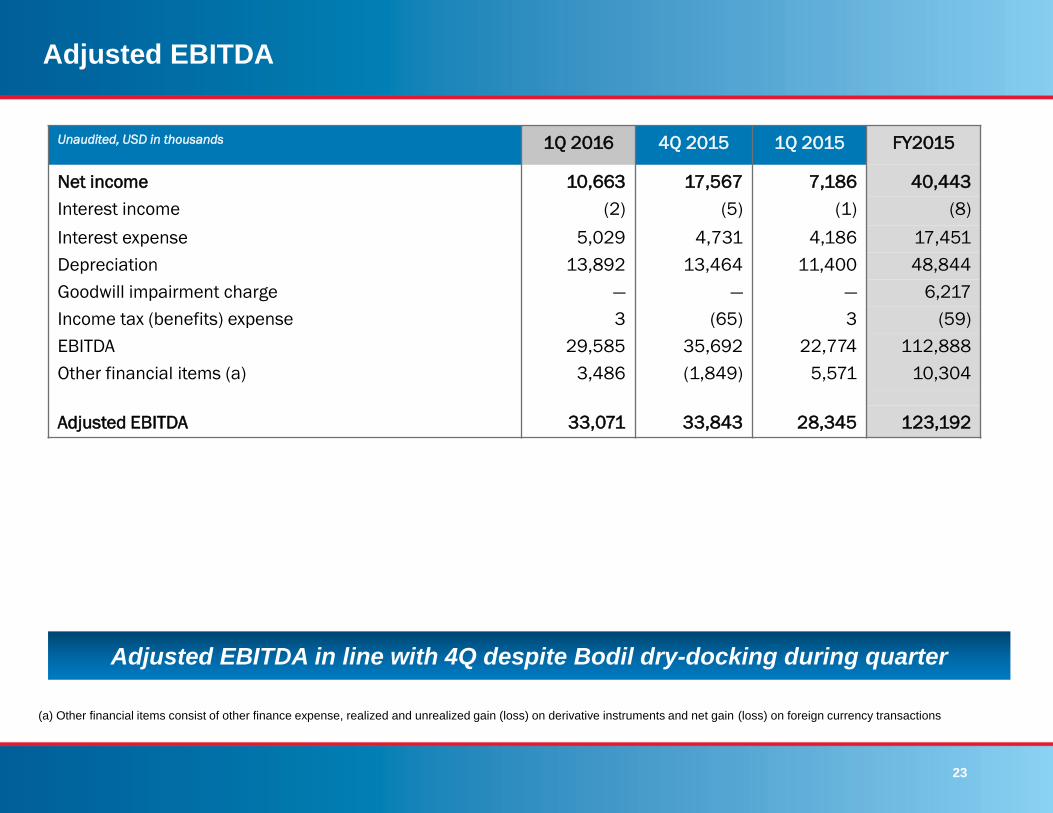

Adjusted EBITDA

Unaudited, USD in thousands 1Q 2016 4Q 2015 1Q 2015 FY2015

Net income 10,663 17,567 7,186 40,443

Interest income (2) (5) (1) (8)

Interest expense 5,029 4,731 4,186 17,451

Depreciation 13,892 13,464 11,400 48,844

Goodwill impairment charge — — — 6,217

Income tax (benefits) expense 3 (65) 3 (59)

EBITDA 29,585 35,692 22,774 112,888

Other financial items (a) 3,486 (1,849) 5,571 10,304

Adjusted EBITDA 33,071 33,843 28,345 123,192

(a) Other financial items consist of other finance expense, realized and unrealized gain (loss) on derivative instruments and net gain (loss) on foreign currency transactions

Adjusted EBITDA in line with 4Q despite Bodil dry-docking during quarter

24

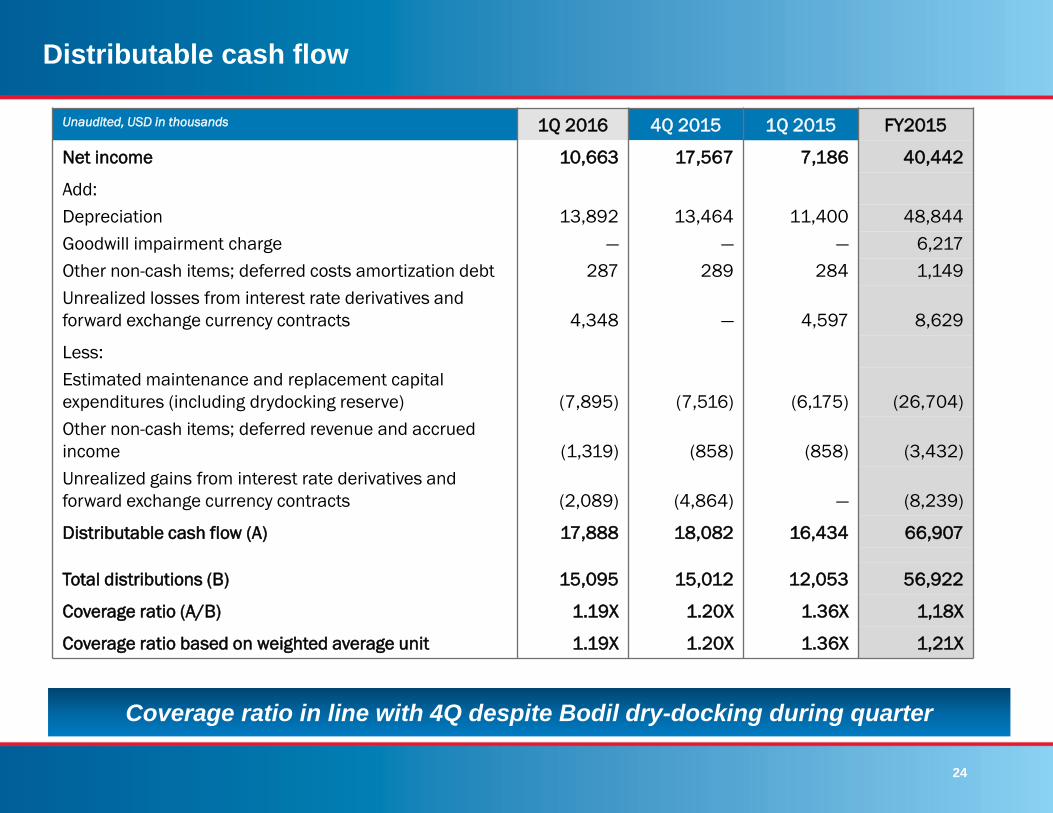

Distributable cash flow

Unaudited, USD in thousands 1Q 2016 4Q 2015 1Q 2015 FY2015

Net income 10,663 17,567 7,186 40,442

Add:

Depreciation 13,892 13,464 11,400 48,844

Goodwill impairment charge — — — 6,217

Other non-cash items; deferred costs amortization debt 287 289 284 1,149

Unrealized losses from interest rate derivatives and

forward exchange currency contracts 4,348 — 4,597 8,629

Less:

Estimated maintenance and replacement capital

expenditures (including drydocking reserve) (7,895) (7,516) (6,175) (26,704)

Other non-cash items; deferred revenue and accrued

income (1,319) (858) (858) (3,432)

Unrealized gains from interest rate derivatives and

forward exchange currency contracts (2,089) (4,864) — (8,239)

Distributable cash flow (A) 17,888 18,082 16,434 66,907

Total distributions (B) 15,095 15,012 12,053 56,922

Coverage ratio (A/B) 1.19X 1.20X 1.36X 1,18X

Coverage ratio based on weighted average unit 1.19X 1.20X 1.36X 1,21X

Coverage ratio in line with 4Q despite Bodil dry-docking during quarter

25

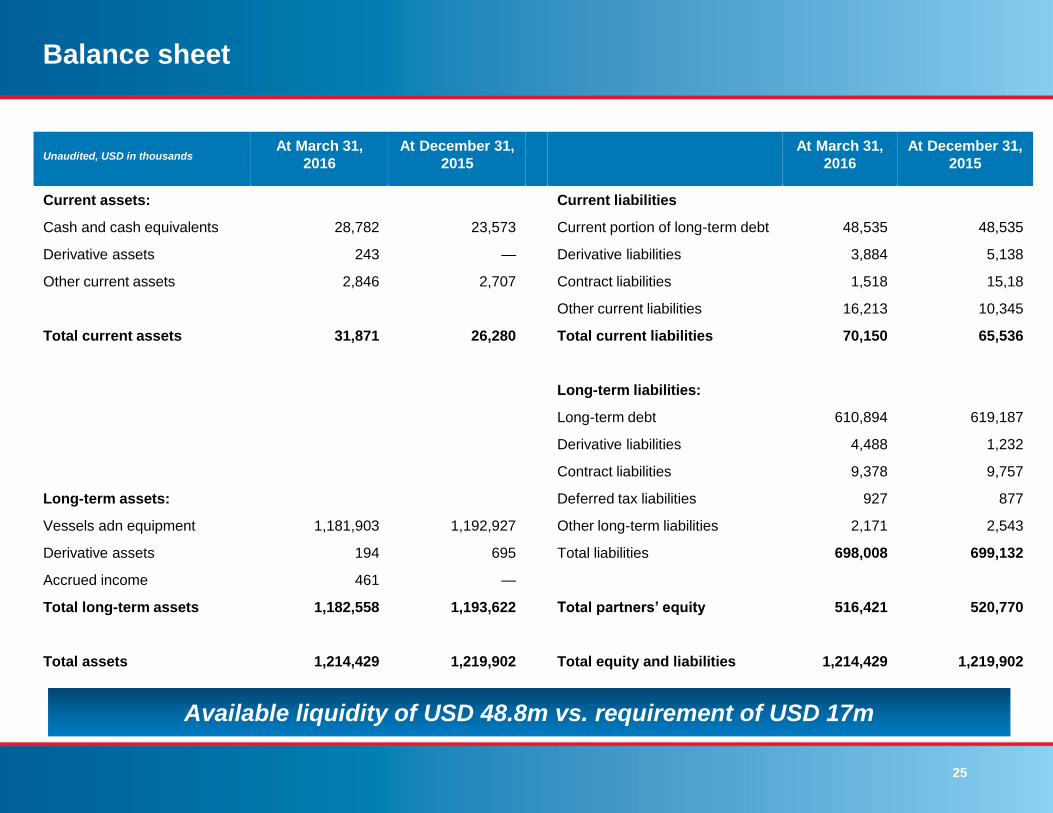

Balance sheet

Unaudited, USD in thousands At March 31,

2016

At December 31,

2015

At March 31,

2016

At December 31,

2015

Current assets: Current liabilities

Cash and cash equivalents 28,782 23,573 Current portion of long-term debt 48,535 48,535

Derivative assets 243 — Derivative liabilities 3,884 5,138

Other current assets 2,846 2,707 Contract liabilities 1,518 15,18

Other current liabilities 16,213 10,345

Total current assets 31,871 26,280 Total current liabilities 70,150 65,536

Long-term liabilities:

Long-term debt 610,894 619,187

Derivative liabilities 4,488 1,232

Contract liabilities 9,378 9,757

Long-term assets: Deferred tax liabilities 927 877

Vessels adn equipment 1,181,903 1,192,927 Other long-term liabilities 2,171 2,543

Derivative assets 194 695 Total liabilities 698,008 699,132

Accrued income 461 —

Total long-term assets 1,182,558 1,193,622 Total partners’ equity 516,421 520,770

Total assets 1,214,429 1,219,902 Total equity and liabilities 1,214,429 1,219,902

Available liquidity of USD 48.8m vs. requirement of USD 17m

Related Documents

![Obesity for medical students.ppt [Read-Only] · Obesity rates could double in n 30 30 years n n n n n n l l l l l l t o o u u u u n l o 50 40 30 20 10 0 % o f p o p u l a t i o n](https://static.cupdf.com/doc/110x72/5f69c2065ed9c21bae08d305/obesity-for-medical-read-only-obesity-rates-could-double-in-n-30-30-years-n-n.jpg)