Milliman USA - Slide 1 Underwriting Risk Models: An Assessment Underwriting Risk Models: An Assessment Presented by Presented by Urban E. Leimkuhler, FCAS, MAAA Urban E. Leimkuhler, FCAS, MAAA Manager & Senior Consultant Manager & Senior Consultant Milliman - Princeton Milliman - Princeton CAS Annual Meeting – New Orleans CAS Annual Meeting – New Orleans November 10, 2003 November 10, 2003

Milliman USA - Slide 1 Underwriting Risk Models: An Assessment Presented by Urban E. Leimkuhler, FCAS, MAAA Manager & Senior Consultant Milliman - Princeton.

Dec 24, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Milliman USA - Slide 1

Underwriting Risk Models: An AssessmentUnderwriting Risk Models: An Assessment

Presented byPresented by

Urban E. Leimkuhler, FCAS, MAAAUrban E. Leimkuhler, FCAS, MAAAManager & Senior ConsultantManager & Senior Consultant

Milliman - PrincetonMilliman - Princeton

CAS Annual Meeting – New OrleansCAS Annual Meeting – New Orleans

November 10, 2003November 10, 2003

Milliman USA - Slide 2

Underwriting AssessmentUnderwriting Assessment

OutlineOutline

Underwriting Assessment -The Problem Underwriting Assessment -The Problem

Potential SolutionPotential Solution

Suggested ApproachSuggested Approach

The ProcessThe Process

OutcomeOutcome

Milliman USA - Slide 3

Underwriting AssessmentUnderwriting Assessment

Compelling Industry Need for ExcellenceCompelling Industry Need for ExcellenceIn UnderwritingIn Underwriting

Low interest rate environment implies higher target Low interest rate environment implies higher target underwriting returns underwriting returns

Resulting need to maximize performance at Resulting need to maximize performance at individual risk and portfolio levelsindividual risk and portfolio levels

Industry actions affecting underwriting performance Industry actions affecting underwriting performance and readinessand readiness

Value in institutionalizing underwriting excellenceValue in institutionalizing underwriting excellence

Milliman USA - Slide 4

Underwriting AssessmentUnderwriting Assessment

The Problem:The Problem:

Industry failures to effectively train commercial lines Industry failures to effectively train commercial lines

underwritersunderwriters Insufficient value attached to underwritingInsufficient value attached to underwriting

as a differentiator in company performance as a differentiator in company performance Demise of underwriter training programsDemise of underwriter training programs Prolonged soft market underwriting Prolonged soft market underwriting

and pricing practicesand pricing practices No available quick fixesNo available quick fixes

Milliman USA - Slide 5

Underwriting AssessmentUnderwriting Assessment

Potential Solution:Potential Solution:

Institutionalize profitable risk selection and Institutionalize profitable risk selection and managementmanagement

Analyze and quantify the effectiveness of Analyze and quantify the effectiveness of

underwriting and pricing practicesunderwriting and pricing practices

Identify and target opportunities for improvementIdentify and target opportunities for improvement

Implement changes in processesImplement changes in processes

Monitor and measure benefits through regular Monitor and measure benefits through regular

check-upscheck-ups

Milliman USA - Slide 6

Underwriting AssessmentUnderwriting Assessment

Suggested Approach:Suggested Approach:

Evaluate specific areas for improvementEvaluate specific areas for improvement Strategies and guidelinesStrategies and guidelines Information collection and managementInformation collection and management Exposure identification / analysis underlying risk selectionExposure identification / analysis underlying risk selection Application of underwriting and pricing practices to individual riskApplication of underwriting and pricing practices to individual risk Monitoring toolsMonitoring tools

Benchmark and measure performanceBenchmark and measure performance Identify and quantify performance gapsIdentify and quantify performance gaps Report to managementReport to management Implement improvementsImplement improvements Benchmark performance at multiple levelsBenchmark performance at multiple levels

Milliman USA - Slide 7

Underwriting AssessmentUnderwriting Assessment

The ProcessThe Process

Interviews (Evaluate Process)Interviews (Evaluate Process)

File Reviews (Assess Outcomes)File Reviews (Assess Outcomes)

Reports and GraphsReports and Graphs

Milliman USA - Slide 8

Underwriting AssessmentUnderwriting Assessment

Interviews to Evaluate ProcessInterviews to Evaluate Process

Strategies and GuidelinesStrategies and Guidelines

Application of Underwriting / Pricing PracticesApplication of Underwriting / Pricing Practices

Monitoring ToolsMonitoring Tools

Milliman USA - Slide 9

Underwriting AssessmentUnderwriting Assessment

Interviews to Evaluate ProcessInterviews to Evaluate Process

General ManagerGeneral Manager Underwriting ManagerUnderwriting Manager UnderwriterUnderwriter ActuaryActuary Loss ControlLoss Control ClaimsClaims MarketingMarketing

Milliman USA - Slide 10

Underwriting AssessmentUnderwriting Assessment

Interviews to Evaluate ProcessInterviews to Evaluate Process

Strategies and GuidelinesStrategies and Guidelines

Application of Underwriting / Pricing PracticesApplication of Underwriting / Pricing Practices

Monitoring ToolsMonitoring Tools

Milliman USA - Slide 11

Underwriting AssessmentUnderwriting Assessment

Process Interviews-Strategies and Process Interviews-Strategies and GuidelinesGuidelines

Strategies / plans are defined, communicatedStrategies / plans are defined, communicated

and managedand managed Ongoing market assessmentOngoing market assessment Pricing programs and goalsPricing programs and goals Underwriting authorityUnderwriting authority Ratemaking process / rating plan structureRatemaking process / rating plan structure

Milliman USA - Slide 12

Underwriting AssessmentUnderwriting Assessment

Interviews to Evaluate ProcessInterviews to Evaluate Process

Strategies and GuidelinesStrategies and Guidelines

Application of Underwriting / Pricing PracticesApplication of Underwriting / Pricing Practices

Monitoring ToolsMonitoring Tools

Milliman USA - Slide 13

Underwriting AssessmentUnderwriting Assessment

Process Interviews-Underwriting / PricingProcess Interviews-Underwriting / Pricing

Practices - The UnderwriterPractices - The Underwriter

Use of Loss Control information by UnderwritingUse of Loss Control information by Underwriting Role of Premium AuditRole of Premium Audit Familiarity with producer capabilitiesFamiliarity with producer capabilities Management reinforcement through behaviorManagement reinforcement through behavior Feedback loops involving Claims, ActuarialFeedback loops involving Claims, Actuarial

Loss Control and UnderwritingLoss Control and Underwriting

Milliman USA - Slide 14

Underwriting AssessmentUnderwriting Assessment

Use of Loss Control Information by Use of Loss Control Information by

Underwriting - Interview QuestionsUnderwriting - Interview Questions

How effectively are Loss Control resources deployedHow effectively are Loss Control resources deployedby Underwriting?by Underwriting?

How are Loss Control recommendations addressedHow are Loss Control recommendations addressedby the Underwriter?by the Underwriter?

In what other ways is Loss Control asked to assistIn what other ways is Loss Control asked to assistUnderwriting in ensuring effective risk selection, Underwriting in ensuring effective risk selection, pricing and ongoing risk management? What otherpricing and ongoing risk management? What otherinformation is provided?information is provided?

Milliman USA - Slide 15

Underwriting AssessmentUnderwriting Assessment

Process Interviews-Underwriting / PricingProcess Interviews-Underwriting / Pricing

Practices - The ActuaryPractices - The Actuary

Formal rate reviewsFormal rate reviews Manual rate developmentManual rate development Actuaries / underwriters execute decisionsActuaries / underwriters execute decisions

and action plansand action plans Actuarial role in pricingActuarial role in pricing Ratemaking data and data qualityRatemaking data and data quality Actuarial / operating management coordinationActuarial / operating management coordination

Milliman USA - Slide 16

Underwriting AssessmentUnderwriting Assessment

Actuarial / Operating ManagementActuarial / Operating Management

Coordination - Interview QuestionsCoordination - Interview Questions

What ongoing information and advice isWhat ongoing information and advice is

provided by Actuary to Management?provided by Actuary to Management? What action plans are established - and What action plans are established - and

by whom?by whom? How effectively are these executed?How effectively are these executed? How would you characterize relationshipsHow would you characterize relationships

between Actuarial and Management?between Actuarial and Management?

Milliman USA - Slide 17

Underwriting AssessmentUnderwriting Assessment

Interviews to Evaluate ProcessInterviews to Evaluate Process

Strategies and GuidelinesStrategies and Guidelines

Application of Underwriting / Pricing PracticesApplication of Underwriting / Pricing Practices

Monitoring ToolsMonitoring Tools

Milliman USA - Slide 18

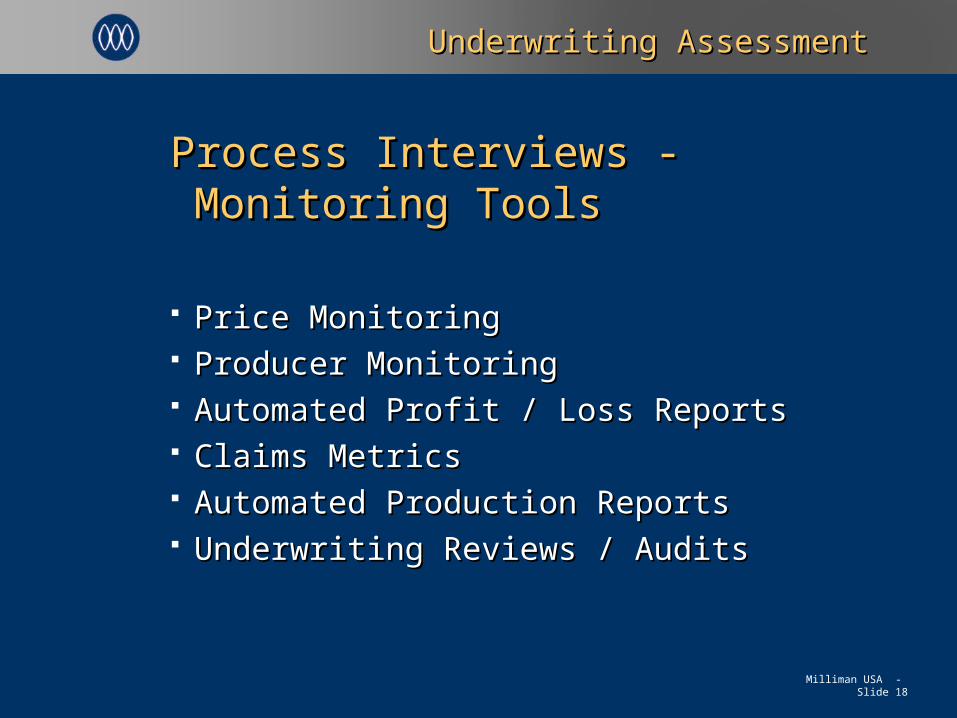

Underwriting AssessmentUnderwriting Assessment

Process Interviews - Monitoring ToolsProcess Interviews - Monitoring Tools

Price MonitoringPrice Monitoring Producer MonitoringProducer Monitoring Automated Profit / Loss ReportsAutomated Profit / Loss Reports Claims MetricsClaims Metrics Automated Production ReportsAutomated Production Reports Underwriting Reviews / AuditsUnderwriting Reviews / Audits

Milliman USA - Slide 19

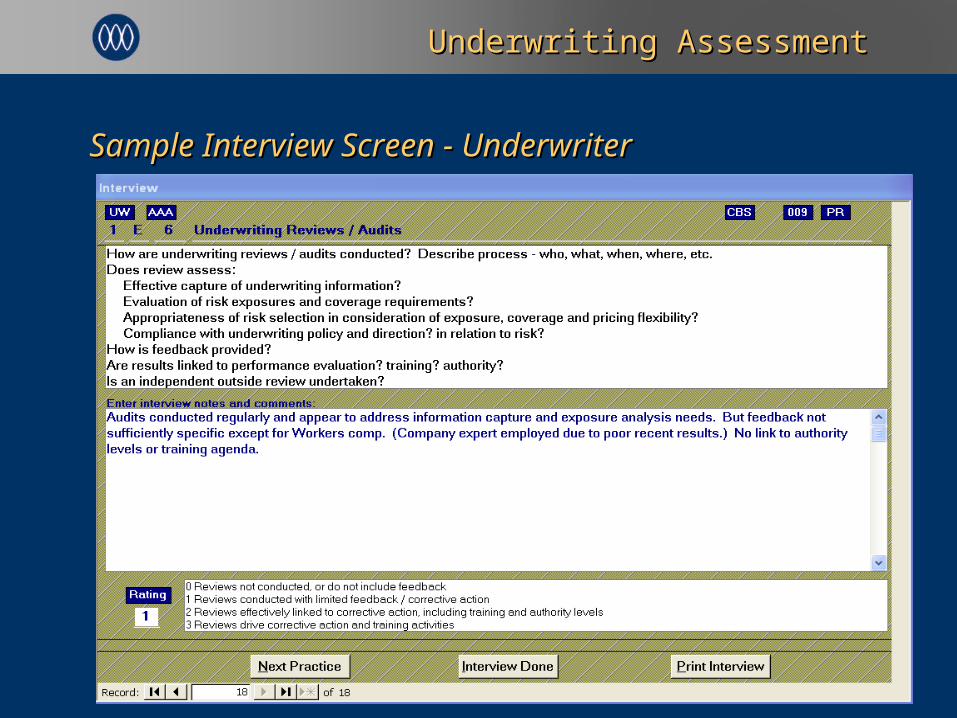

Underwriting AssessmentUnderwriting Assessment

Sample Interview Screen - UnderwriterSample Interview Screen - Underwriter

Milliman USA - Slide 20

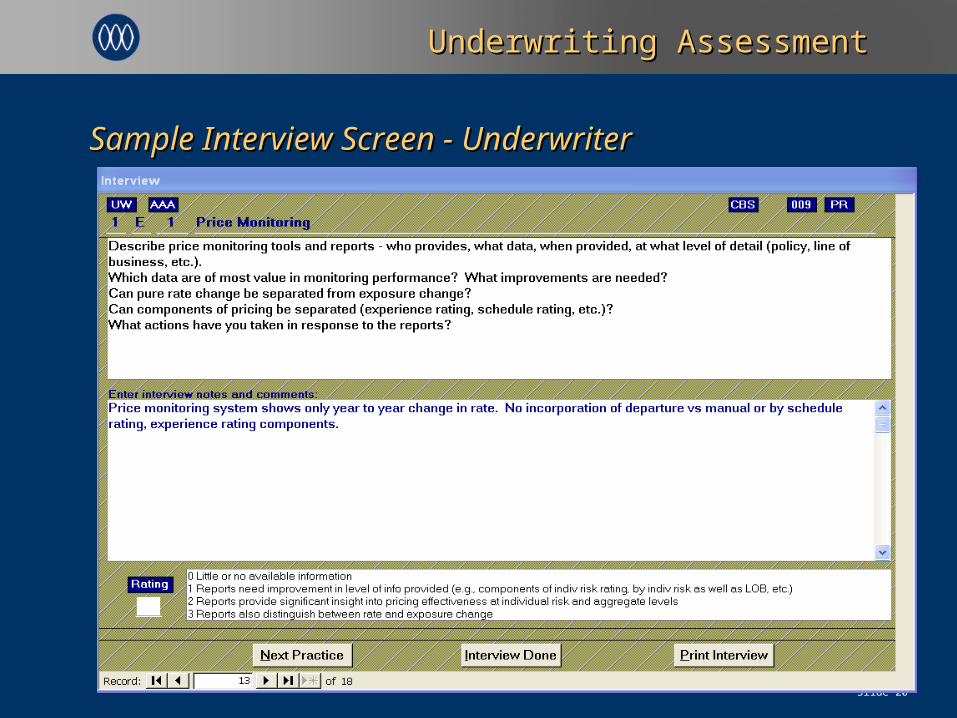

Underwriting AssessmentUnderwriting Assessment

Sample Interview Screen - UnderwriterSample Interview Screen - Underwriter

Milliman USA - Slide 21

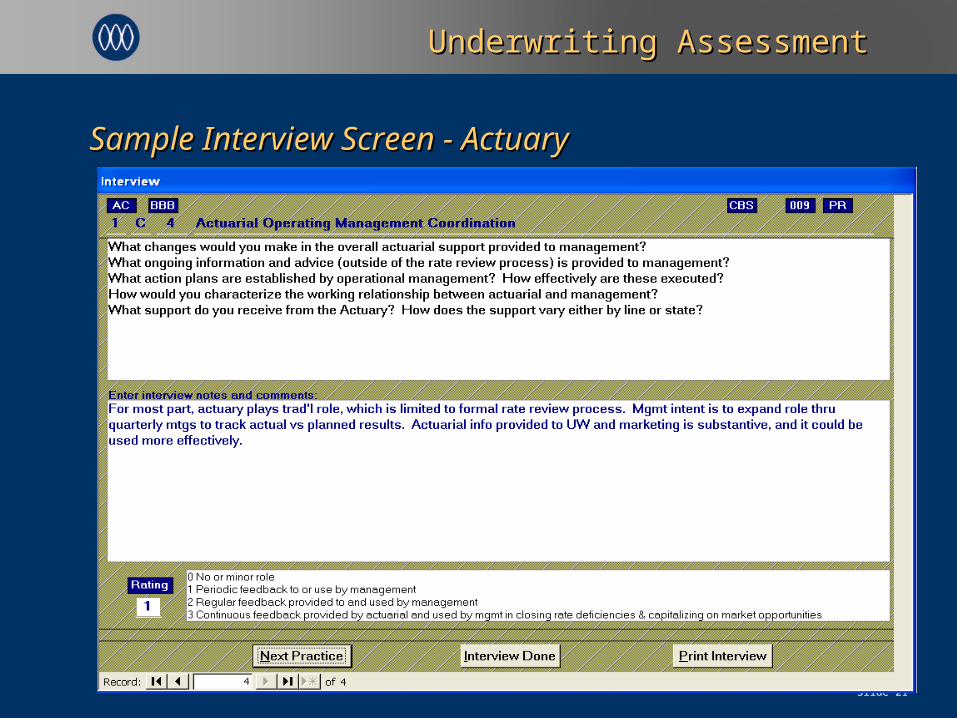

Underwriting AssessmentUnderwriting Assessment

Sample Interview Screen - ActuarySample Interview Screen - Actuary

Milliman USA - Slide 22

Underwriting AssessmentUnderwriting Assessment

The ProcessThe Process

Interviews (Evaluate Process)Interviews (Evaluate Process)

File Reviews (Assess Outcomes)File Reviews (Assess Outcomes)

Reports and GraphsReports and Graphs

Milliman USA - Slide 23

Underwriting AssessmentUnderwriting Assessment

File Reviews to Assess OutcomesFile Reviews to Assess Outcomes

Information Collection / Management Information Collection / Management

Application of Underwriting / Pricing PracticesApplication of Underwriting / Pricing Practices

Underwriting Decision Underwriting Decision

Milliman USA - Slide 24

Underwriting AssessmentUnderwriting Assessment

File Reviews -File Reviews -

Information Collection / ManagementInformation Collection / Management

Risk pre-qualificationRisk pre-qualification Application / renewal questionnaireApplication / renewal questionnaire Availability of loss experienceAvailability of loss experience Loss Control reportsLoss Control reports Access to / use of outside informationAccess to / use of outside information

Milliman USA - Slide 25

Underwriting AssessmentUnderwriting Assessment

File Reviews - Underwriting / Pricing File Reviews - Underwriting / Pricing PracticesPractices

Exposure basisExposure basis Classification assignmentClassification assignment Evaluation of underwriting exposuresEvaluation of underwriting exposures Coverage considerationsCoverage considerations Basis for price decision Basis for price decision Interaction among disciplines that support Interaction among disciplines that support

UnderwritingUnderwriting

Milliman USA - Slide 26

UnderwritingUnderwriting AssessmentAssessment

File Reviews - Underwriting DecisionFile Reviews - Underwriting Decision

Risk selectionRisk selection

Underwriting referral / 2Underwriting referral / 2ndnd opinion opinion

Milliman USA - Slide 27

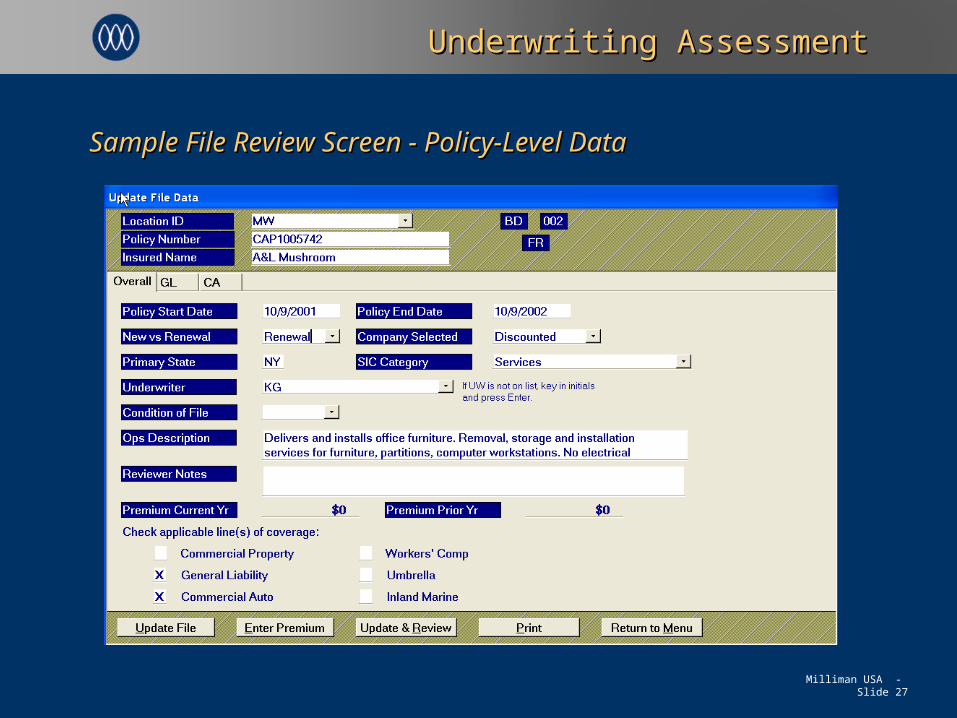

Underwriting AssessmentUnderwriting Assessment

Sample File Review Screen - Policy-Level DataSample File Review Screen - Policy-Level Data

Milliman USA - Slide 28

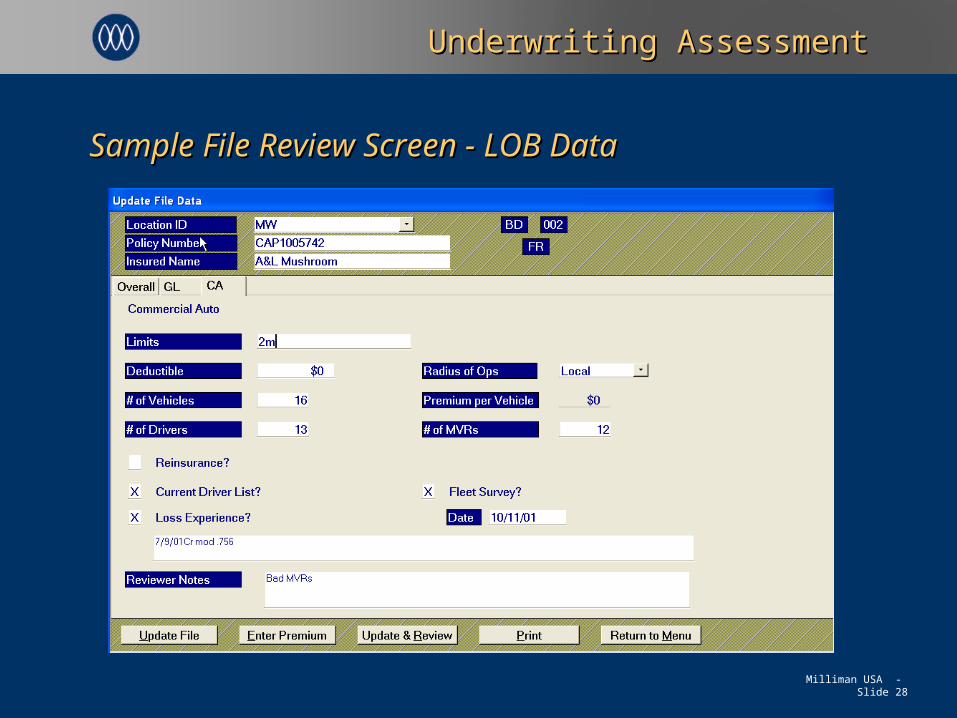

Underwriting AssessmentUnderwriting Assessment

Sample File Review Screen - LOB DataSample File Review Screen - LOB Data

Milliman USA - Slide 29

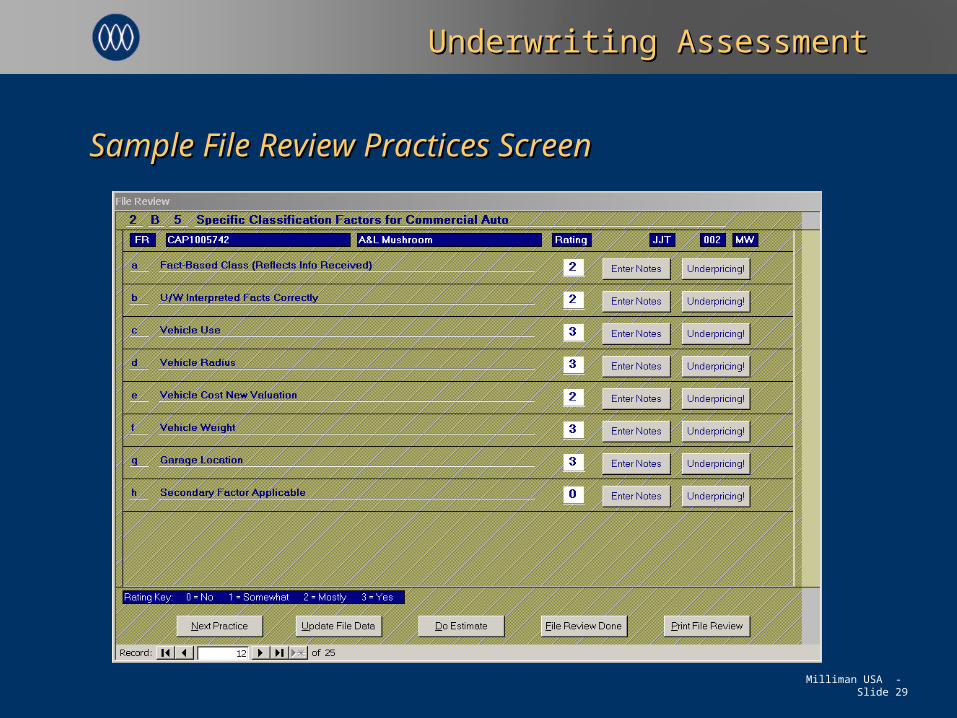

Underwriting AssessmentUnderwriting Assessment

Sample File Review Practices ScreenSample File Review Practices Screen

Milliman USA - Slide 30

Underwriting AssessmentUnderwriting Assessment

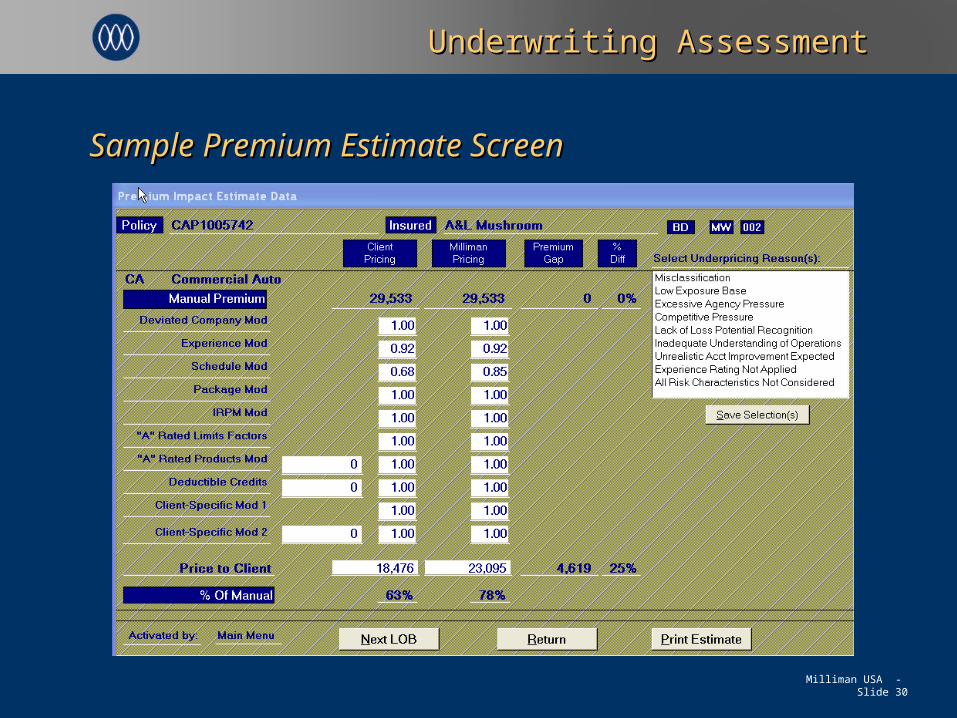

Sample Premium Estimate ScreenSample Premium Estimate Screen

Milliman USA - Slide 31

Underwriting AssessmentUnderwriting Assessment

The ProcessThe Process

Interviews (Evaluate Process)Interviews (Evaluate Process)

File Reviews (Assess Outcomes)File Reviews (Assess Outcomes)

Reports and ChartsReports and Charts

Milliman USA - Slide 32

Underwriting AssessmentUnderwriting Assessment

Milliman USA - Slide 33

Underwriting AssessmentUnderwriting Assessment

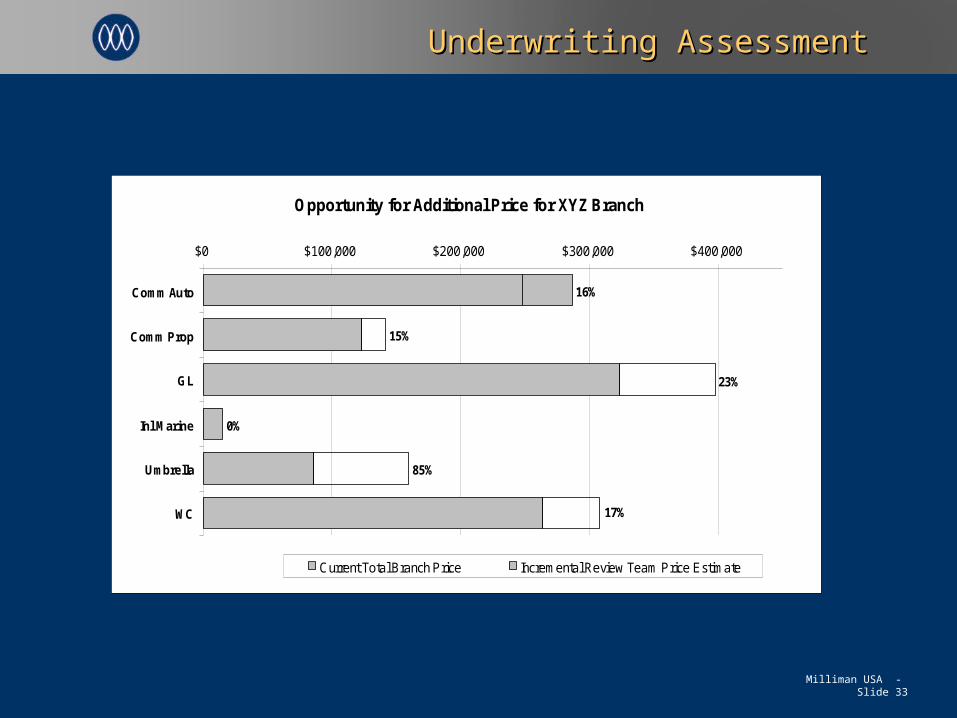

Opportunity for Additional Price for XYZ Branch

0%

16%

15%

23%

85%

17%

$0 $100,000 $200,000 $300,000 $400,000

Comm Auto

Comm Prop

GL

Inl Marine

Umbrella

WC

Current Total Branch Price Incremental Review Team Price Estimate

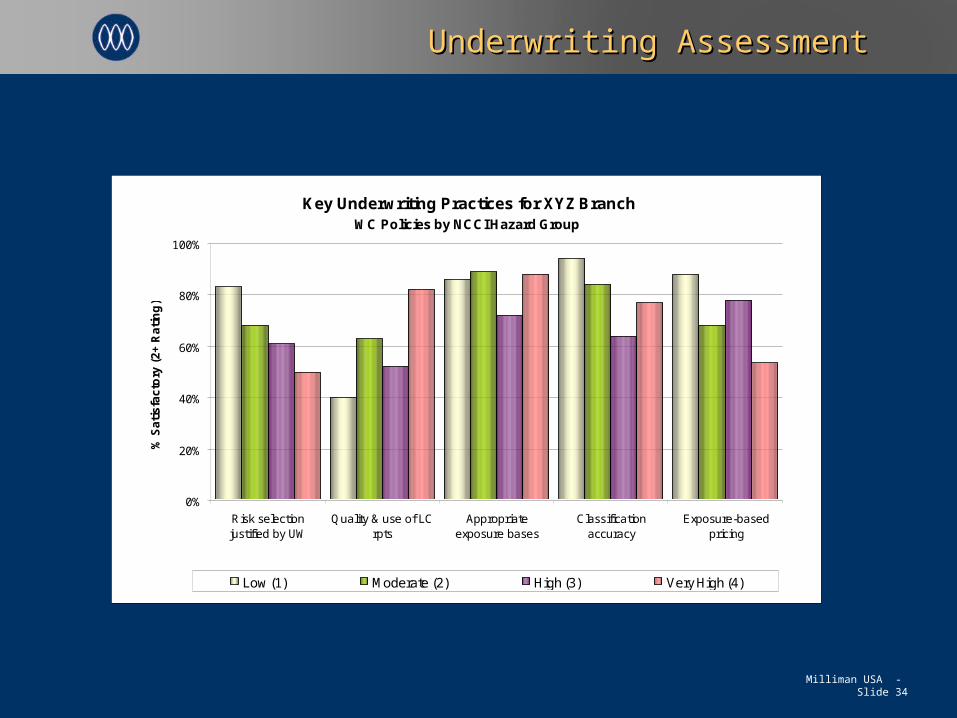

Milliman USA - Slide 34

Underwriting AssessmentUnderwriting Assessment

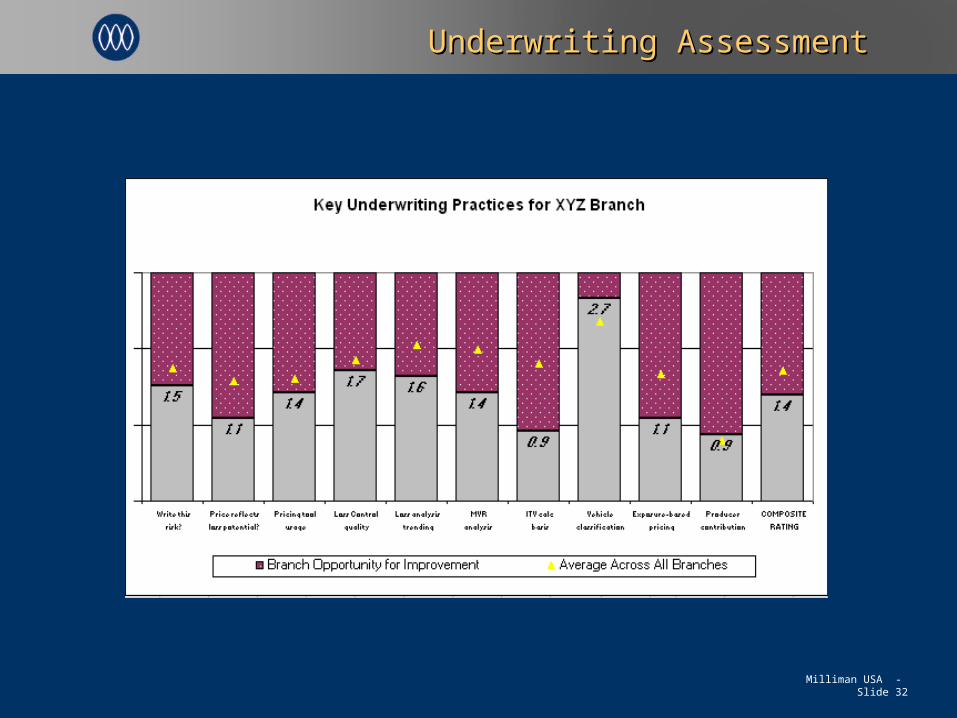

Key Underwriting Practices for XYZ BranchWC Policies by NCCI Hazard Group

0%

20%

40%

60%

80%

100%

Risk selectionjustified by UW

Quality & use of LCrpts

Appropriateexposure bases

Classificationaccuracy

Exposure-basedpricing

% S

ati

sfa

cto

ry (

2+

Ra

tin

g)

Low (1) Moderate (2) High (3) Very High (4)

Milliman USA - Slide 35

Underwriting AssessmentUnderwriting Assessment

The OutcomeThe Outcome

Process Effectiveness Scorecard Process Effectiveness Scorecard File Effectiveness Scorecard File Effectiveness Scorecard Needed Improvements in PerformanceNeeded Improvements in Performance RecommendationsRecommendations Implementation PlanImplementation Plan Platform for Ongoing BenchmarkingPlatform for Ongoing Benchmarking

Related Documents