A pure-play paperboard company Mika Joukio CEO, Metsä Board Metsä Board Capital Markets Day 2017

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

A pure-play paperboard company

Mika Joukio CEO, Metsä Board

Metsä BoardCapital Markets Day 2017

Disclaimer

This presentation includes forward-looking statements. The words “believe,” “expect,” “anticipate,” “intend,” “may,” “plan,” “estimate,” “will,” “should,” “could,” “aim,” “target,” “might,” or, in each case, their negative, or any similar expressions identify certain of these forward-looking statements. Others can be identified from the context in which the statements are made. By their nature, forward-looking statements are subject to assumptions, risks and uncertainties. Although we believe that the expectations reflected in these forward-looking statements are reasonable, actual results may differ, even materially, from those expressed or implied by these forward-looking statements. We urge presentation participants not to place undue reliance on such statements.

The information and views contained in this presentation are provided as at the date of this presentation and are subject to change without notice. Metsä Board does not undertake any obligation to publicly update or revise forward-looking statements, whether as a result of new information, future events or otherwise, except to the extent legally required.

Viewers should understand that this presentation does not constitute, and should not be construed as, an offer to buy or subscribe for Metsä Board’s securities anywhere in the world or an inducement to enter into any investment activity relating to the same. No part of this presentation should form the basis of, or be relied on in connection with, any contract or commitment or decision to invest in Metsä Board securities whatsoever. Potential investors are instructed to acquaint themselves with MetsäBoard’s annual accounts, interim reports and stock exchange releases as well as other information published by Metsä Board to form a comprehensive picture of the company and its securities.

Metsä Board publishes inside information according to Market Abuse Regulation (MAR) and rules of the Nasdaq Helsinki.

2017 CMD Joukio 2

Metsä Board Corporate Management Team

Mika JoukioCEO

Chairman of CMT since 2014

Ari KivirantaSVP, Production and

Technology

Member of CMT since 2014

Jussi NoponenCFO

Member of CMT since 2016

Sari PajariSVP, Business

Development

Member of CMT since 2011

Seppo PuotinenSVP, Marketing and

Sales

Member of CMT since 2005

Susanna TainioSVP, HR

Member of CMT since 2015

2017 CMD Joukio 3

• Metsä Board today

• Operating environment

• Husum integrated mill

• Summary

4

Content

2017 CMD Joukio

• Market leader in folding boxboard and

white fresh fibre linerboard in Europe,

global market leader in coated white

fresh fibre linerboard*

• Customers are brand owners,

converters, corrugated box

manufacturers and merchants

• Global sales to over 100 countries

• Strong fibre know-how and self-

sufficiency in pulp

5

Metsä Board A leading European producer of

premium fresh fibre paperboards

2017 CMD Joukio

Metsä Board

Competitor 1

Competitor 2

Competitor 3

Competitor 4

Others

Folding boxboardin Europe,

total capacity 3.6m tonnes

Metsä Board

Competitor 1

Competitor 2

Competitor 3

Competitor 4

Others

White fresh fibre linerboard in Europe,

total capacity 2.2m tonnes

37% 31%

* Annual global demand for coated white fresh fibre linerboard is 1m

tonnes, of which Metsä Board‘s share is 35–40%

Focus

Focus on premium fresh fibre paperboards for consumer and retail

packaging

Growth

Grow profitably together with brand owner, converter and merchant

customers globally in businesses that benefit from our safe and

sustainable paperboards

Profitability

Profitability is based on superior cost efficiency and healthy sales

prices driven by high-quality pulps and unique technical know-how

2017 CMD Joukio 6

Metsä Board’s vision is to be the preferred supplier

of premium paperboards creating value for

customers globally

50% of Metsä Board’s folding boxboard sales are negotiated directly with brand owners

7

Brand owners play an important role in packaging

BRAND OWNERS

FOLDING BOXBOARD WHITE LINERBOARDS

MERCHANTS

CORRUGATED BOX

MANUFACTURERS

CONVERTERS

2017 CMD Joukio

Solutions for a wide variety of brand applications

In pack On shelf On display On the go In graphics

Packaging

solutions for

consumer

goods

Retail-ready

tray solutions

Display and

point-of-sale

solutions

Solutions for

food service

Solutions for

graphical uses

2017 CMD Joukio 8

2017 CMD Joukio 9

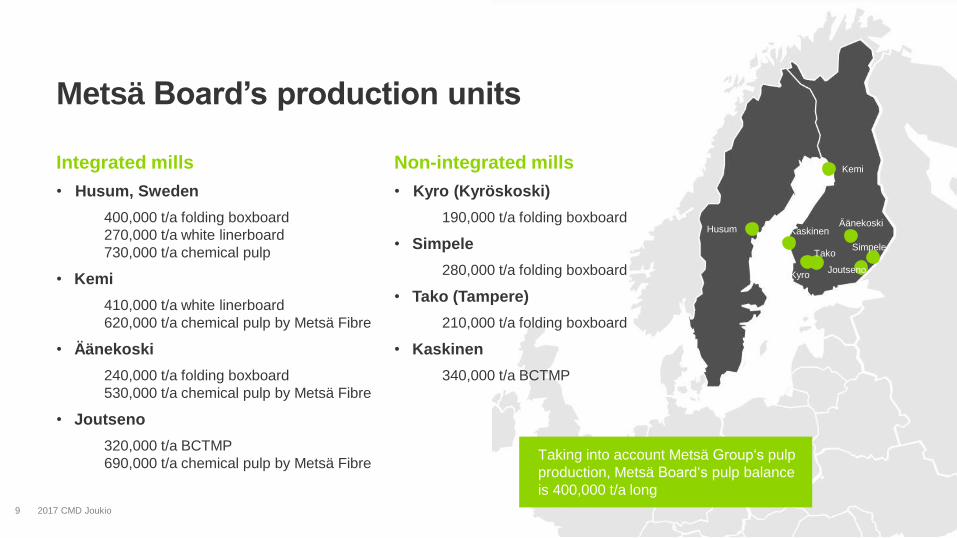

Metsä Board’s production units

Äänekoski

Simpele

Joutseno

Tako

Kyro

KaskinenHusum

KemiIntegrated mills

• Husum, Sweden

400,000 t/a folding boxboard

270,000 t/a white linerboard

730,000 t/a chemical pulp

• Kemi

410,000 t/a white linerboard

620,000 t/a chemical pulp by Metsä Fibre

• Äänekoski

240,000 t/a folding boxboard

530,000 t/a chemical pulp by Metsä Fibre

• Joutseno

320,000 t/a BCTMP

690,000 t/a chemical pulp by Metsä Fibre

Non-integrated mills

• Kyro (Kyröskoski)

190,000 t/a folding boxboard

• Simpele

280,000 t/a folding boxboard

• Tako (Tampere)

210,000 t/a folding boxboard

• Kaskinen

340,000 t/a BCTMP

Taking into account Metsä Group‘s pulp

production, Metsä Board‘s pulp balance

is 400,000 t/a long

Lightweight

• Up to 30% lighter than competing grades

(eg SBS, WLC) with at least the same stiffness

Purity and safety

• Important in food and food service packaging,

eg recycled paperboard should not be in

direct contact with food products

Sustainability

• Wood raw material is 100% traceable to sustainably

managed northern forests

Quality

• Excellent printability and runnability

10

Metsä Board’s paperboards have

many competitive advantages

2017 CMD Joukio

2017 CMD Joukio 11

Strong improvement in productivity over time

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

1,900

2,000

1,000

1,300

1,600

1,900

2,200

2,500

2,800

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017E

Productivity (capacity) Personnel average

Production capacity (tonnes) per employee at current millsPersonnel

Capacity, t per

employee

12

0

30

60

90

120

150

180

2011 2012 2013 2014 2015 2016 2017E

Maintenance capex Growth capex Depreciation

Clearly lower capex in 2017E

UR

mill

ion

Capex and depreciation

2017 CMD Joukio

Metsä Board’s growth clearly exceeds

average market growth

13

0

250

500

750

1,000

1,250

1,500

1,750

2,000

2012 2013 2014 2015 2016 2018 target

Fresh fibre linerboard Folding boxboard

Metsä Board’s annual paperboard deliveries, 1,000 tonnes

2017 CMD Joukio

Operating environment

Global trends driving growth in packaging

• Growing consumption

• Stronger demand for sustainable

packaging

• Greater significance of resource

efficiency drives circular economy and

life-cycle thinking

• Increasing regulation brings additional

obligations

• Social responsibility throughout the

value chain

2017 CMD Joukio 15

2017 CMD Joukio 16

Globally growing paperboard market

PAPERBOARD 5-YEAR GROWTH FORECAST EMEA Americas APAC

Folding boxboard (FBB)

Food service board (FSB)

Coated white kraftliner n/a

Uncoated white kraftliner n/a

Other fresh fibre paperboards (eg SBS, CUK)

Recycled paperboards (eg WLC)

+2%/a or more

+1 to +2%/a

-1 to +1%/a

-1 to -2%/a

-2%/a or more

Source: Metsä Board‘s own estimate

17

Metsä Board's regional goals

GROWTH

IN THE

AMERICAS

IN THE COMING

YEARS

MAINTAIN

THE STRONG

MARKET

POSITION IN

EUROPE

FOCUS ON

PREMIUM

PAPERBOARD

SEGMENTS IN

THE ASIA-PACIFIC

REGION

AMERICASSHARE OF SALES IN 2016

17%

EMEASHARE OF SALES IN 2016

75%

APACSHARE OF SALES IN 2016

8%

2017 CMD Joukio

18

GROWTH

IN THE

AMERICAS

IN THE COMING

YEARS

MAINTAIN

THE STRONG

MARKET

POSITION IN

EUROPE

FOCUS ON

PREMIUM

PAPERBOARD

SEGMENTS IN

THE ASIA-PACIFIC

REGION

AMERICASSHARE OF SALES IN 2016

17%

EMEASHARE OF SALES IN 2016

75%

APACSHARE OF SALES IN 2016

8 %

EUROPE

• A leading market position with

strong, long-lasting customer

relationships – especially with

brand owners

• Safety is increasing significance

in food packaging

• Paperboard is a strong

alternative to plastics and

aluminium

• Growing e-commerce

increasing demand for high-end

white-top kraftliners

2017 CMD Joukio

Metsä Board's growth drivers in Europe

19

GROWTH

IN THE

AMERICAS

IN THE COMING

YEARS

MAINTAIN

THE STRONG

MARKET

POSITION IN

EUROPE

FOCUS ON

PREMIUM

PAPERBOARD

SEGMENTS IN

THE ASIA-PACIFIC

REGION

AMERICASSHARE OF SALES IN 2016

17%

EMEASHARE OF SALES IN 2016

75 %

APACSHARE OF SALES IN 2016

8 %

AMERICAS

• Local production not able to meet rising trend of

lightweighting

• Non-integrated converters looking for alternative

board suppliers

• Paperboard a strong alternative to plastics –

especially in food service applications

• Growing e-commerce increasing demand for

high-end white-top kraftliners

2017 CMD Joukio

Metsä Board's growth drivers in Americas

Husum integrated mill

2017 CMD Joukio 21

• Launched at the end of 2014

• Two paper machines closed in 2015

• One paper machine converted to produce linerboard (BM2)

• New folding boxboard machine (BM1) started up in February

2016

• Enhancements to the pulp mill and the mill site’s own port

• New extrusion coating line started up in April 2017

Folding boxboard production

• Capacity approximately 400,000 t/a

• Deliveries mainly to Americas and

food service globally

Linerboard production

• Capacity approximately 270,000 t/a

• Deliveries to Europe and Americas

Husum investment programme

• EUR 38 million investment, capacity of 100,000 t/a

• PE-coated* paperboard is an alternative to plastics

• Targeted at food packaging and food service

applications

• In 2016, Metsä Board introduced PE-coated

paperboards

• Supports growth in a new customer segment

2017 CMD Joukio 22

New state-of-the-art extrusion

coating line

* PE=polyethylene, the most common barrier

material used against moisture and grease

Raw materialLogistics

Raw materialExtrusion

Raw materialPaperboard

Raw materialPulp

23

The integrated mill model improves efficiency and

sustainability of the supply chain

• Certified wood resources

• Own deep water port

• Own pulp mill at the mill site

• Paperboard production (BM1)

• Extrusion coating line (EM1)

Raw materialRaw materialHusum integrated mill:

2017 CMD Joukio

• Metsä Board is today a pure-play

paperboard company

• Global trends driving stronger

demand for sustainable packaging

• Strong market demand and Metsä

Board's latest investments support

growth in the coming years

2017 CMD Joukio 24

Summary

Related Documents