MIDiA Research Mark Mulligan May 2015 Where Does The Streaming Road Lead?

MIDiA Research – Where Does The Streaming Road Lead? A Case For A New Generation Of Streaming Business Models

Jul 28, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

MIDiA Research Mark Mulligan May 2015

Where Does The Streaming Road Lead?

MIDiA Research is a unique music industry focussed syndicated research and analysis service. Our reports leverage proprietary consumer data, market forecasts and indices.

Mark Mulligan is a music industry analyst and consultant of 15 years standing, previously held senior positions at Jupiter and Forrester Research, now heads up MIDiA Research.

MIDiA Research clients pay a one-off annual fee to get online access to our research reports and data to better understand how to respond to tomorrow’s disruption.

Where Does The Streaming Road Lead?

1. Change Is Difficult 2. Not All Audiences Are The Same 3. Pricing & 360° Music Products 4. Conclusions

Where Does The Streaming Road Lead?

1. Change Is Difficult 2. Not All Audiences Are The Same 3. Pricing & 360° Music Products 4. Conclusions

20

10

(millions)

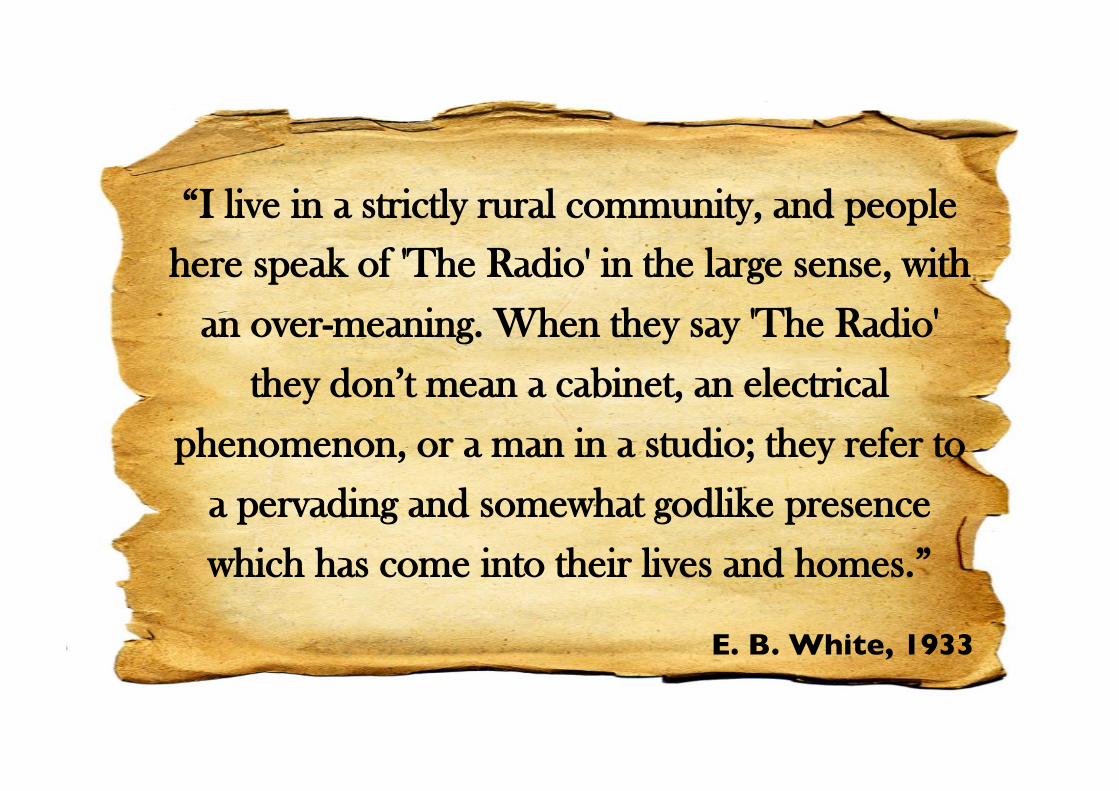

“I live in a strictly rural community, and people here speak of 'The Radio' in the large sense, with

an over-meaning. When they say 'The Radio'

they don’t mean a cabinet, an electrical

phenomenon, or a man in a studio; they refer to

a pervading and somewhat godlike presence

which has come into their lives and homes.”

E. B. White, 1933

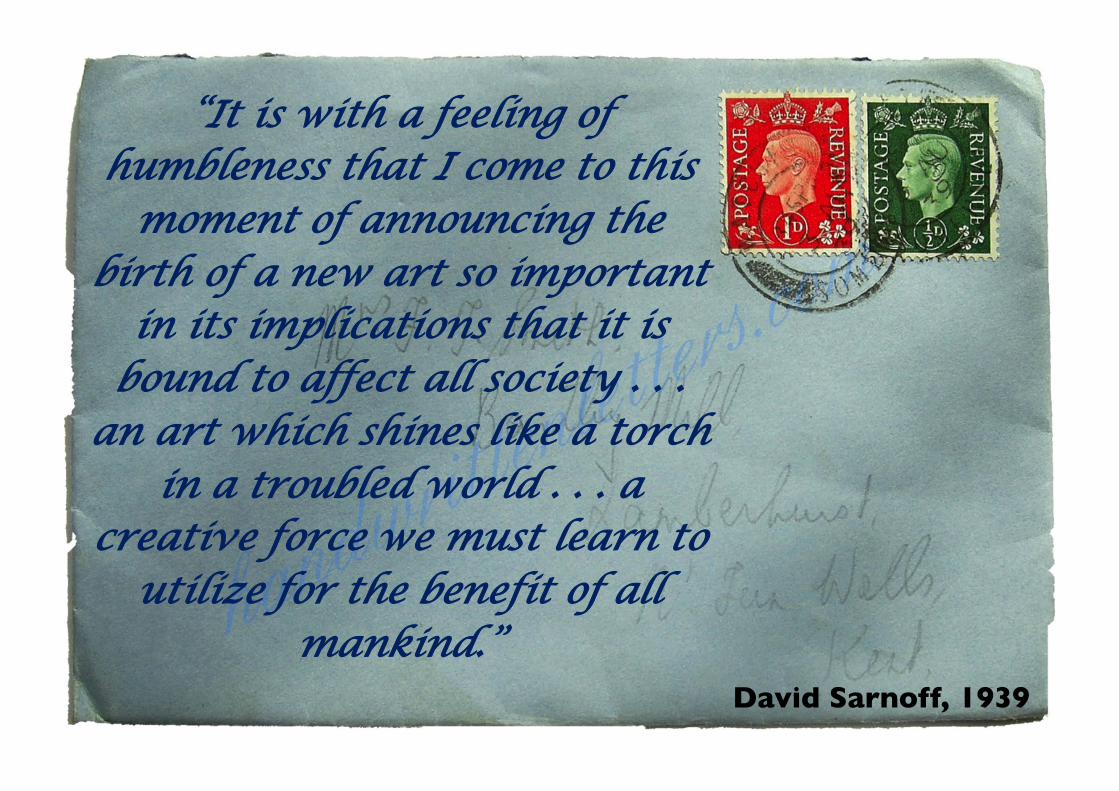

“It is with a feeling of humbleness that I come to this

moment of announcing the birth of a new art so important

in its implications that it is bound to affect all society . . .

an art which shines like a torch in a troubled world . . . a

creative force we must learn to utilize for the benefit of all

mankind.” David Sarnoff, 1939

“ “Spo@fy is the last desperate fart of a

dying corpse. Thom Yorke 2013

Cnut

• Artists and fans are closer than ever • Paying for music has become a lifestyle

choice • New label models are gaining traction • Ownership is evolving • Streaming models are growing • Free dominates • On demand dominates

A LOT HAS AREADY CHANGED

US adult populaPon – 280m

YouTube – 134m

Stream for free – 113m

Buy CDs – 98m

Buy downloads – 82m

Subscribe – 8m

SubscripPons May Be The Future But They’re Only Just Ge[ng Going

Source: MIDiA Research Consumer Survey 12/14 (US) and RIAA

1.6

2.8

1.5

5.3

6.4

5.7

-‐

2.0

4.0

6.0

8.0

2012 2013 2014

Net New Music Subscribers

Net New Neclix Subscribers

The MaturaPon Effect: Digital SubscripPons Have An Inherent AdopPon Ceiling Net New AddiPonal US Subscribers For Neclix And For Music Subscribers

Net New

Sub

scrib

ers

Sources: Neclix annual reports and RIAA

(millions)

Where Does The Streaming Road Lead?

1. Change Is Difficult 2. Not All Audiences Are The Same 3. Pricing & 360° Music Products 4. Conclusions

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

0 50 100 150

Revenue AND Audience: Another Way Of Looking At Music Services

(millions)

Revenu

e

Paid downloads

Premium subscripPons

InteracPve radio

Music video

Free subscripPons

Audience Source: MIDiA Research 9/14

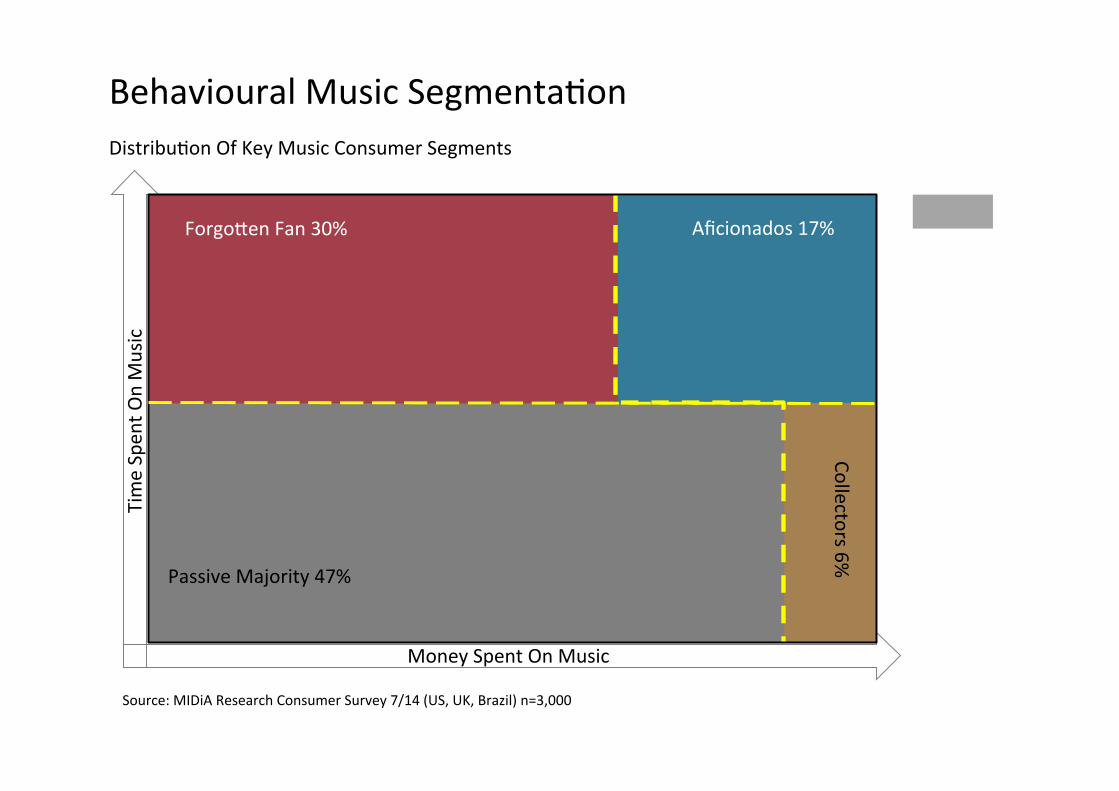

Behavioural Music SegmentaPon DistribuPon Of Key Music Consumer Segments

Source: MIDiA Research Consumer Survey 7/14 (US, UK, Brazil) n=3,000

Aficionados 17%

Collectors 6% Passive Majority 47%

Forgooen Fan 30%

Money Spent On Music

Time Spen

t On Music

Line signifies averages

184bn

48%

23%

17%

52%

61%

59%

21%

23%

Of all consumers

Of total music spending

Buy downloads (66% buy CDs)

Go to gigs and concerts regularly

Stream music

Spend less on downloads than they used to

Used to buy more than an album a month but no longer do so

Have a music subscripPon

The Music Aficionado Is Every ArPst And Label’s Most Valuable Asset Key Aoributes Of Music Aficionados

$ 133.4

$ 40.6

$189.9

$247.3

$0

$100

$200

$300

$400

Lost Physical Music Spend Lost Music Download Spend

Aficionado Lost Spend

Remainder Lost Spend

The Changing Spending Paoerns Of Aficionados Shaped Music Revenues In 2014 Total ‘Lost’ Music Revenue in 2014 That Was Music Aficionado ‘Lost’ Spend

‘Lost’ Music Reven

ue

Data refers to UK, US, France, Italy, Australia, Sweden, Norway Source: MIDiA Research Aficionado Spend Model 1/15

86% of total

59% of total

(millions)

Aficionados were responsible for of all ‘lost’ spending in 2014

72%

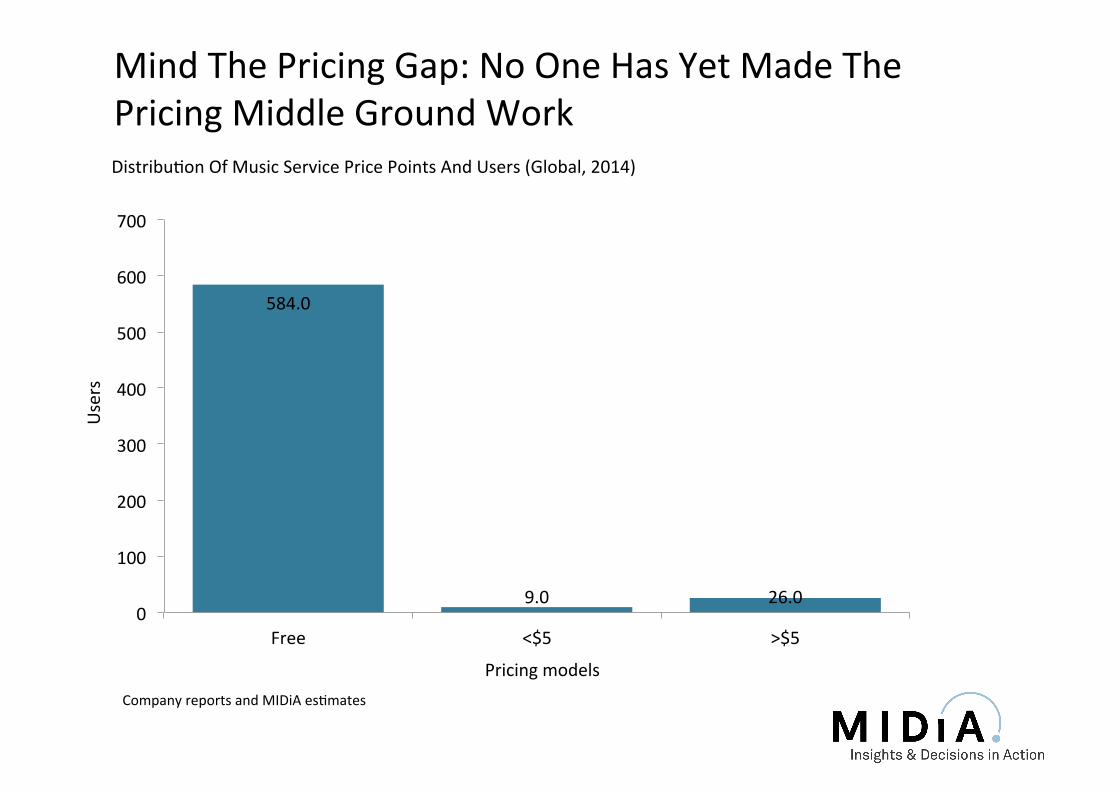

584.0

9.0 26.0 0

100

200

300

400

500

600

700

Free <$5 >$5

Mind The Pricing Gap: No One Has Yet Made The Pricing Middle Ground Work DistribuPon Of Music Service Price Points And Users (Global, 2014)

Pricing models Company reports and MIDiA esPmates

Users

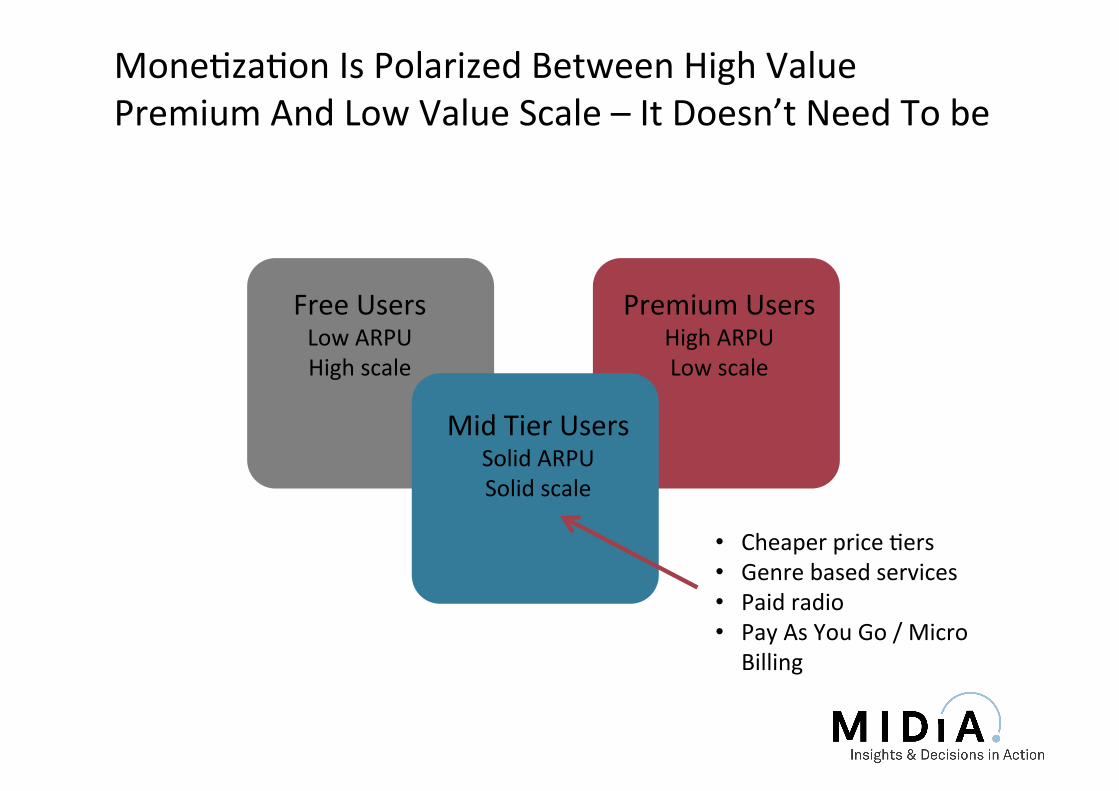

MonePzaPon Is Polarized Between High Value Premium And Low Value Scale – It Doesn’t Need To be

Free Users Low ARPU High scale

Premium Users High ARPU Low scale

Mid Tier Users Solid ARPU Solid scale

• Cheaper price Pers • Genre based services • Paid radio • Pay As You Go / Micro

Billing

Behavioural Music SegmentaPon DistribuPon Of Key Music Consumer Segments

Source: MIDiA Research Consumer Survey 7/14 (US, UK, Brazil) n=3,000

Aficionados 17%

Collectors 6% Passive Majority 47%

Forgooen Fan 30%

Money Spent On Music

Time Spen

t On Music

Line signifies averages

A[tudinal Music SegmentaPon DistribuPon Of Key Music Consumer Segments

Source: MIDiA Research Consumer Survey 7/14 (US, UK, Brazil) n=3,000

Passive Buyers 2%

Aficionados 39%

Passives 17% Disinterested 11%

Forgooen Fan 30%

Consider music worth paying for

Consider m

usic im

portant in life

Line signifies averages

Where Does The Streaming Road Lead?

1. Change Is Difficult 2. Not All Audiences Are The Same 3. Pricing & 360° Music Products 4. Conclusions

Premium e.g. SpoPfy

Mid e.g. iTunes, Pandora One

Free e.g. YouTube, Soundcloud

Revenu

e Scale

The Music MonePzaPon Pyramid

10%

12%

17%

0% 10% 20% 30% 40% 50%

Standard price (e.g. $9.99)

Low price (e.g. $1 a week / $5 a month)

PAYG/Top Up

Out Of A Band Bunch Pay As You Go / Micro Billing Represents The Largest Opportunity Average Interest Levels In Music Service Pricing

% of Consumers

Source: Various MIDiA Surveys

PAYG is the payment opPon with strongest and widest appeal

$0

$50

$100

$150

$200

$250

$300

0 5 10 15 20 25 30 35 40 45 50

HypothePcal US Monthly Revenue And Customer Base Based On Consumer Stated Pricing Interest

$9.99 Delivers The Revenue But Not The Scale Re

venu

e

Customer Base

(millions)

PAYG / Top Up (Assumes $2.50 monthly spend)

$5 a month

$9.99 a month

Music Aficionados Want More Than Just The Song From Their Favourite ArPsts

% of consumer segment

7%

26%

18%

45%

0% 10% 20% 30% 40% 50%

Would pay for an interacPve album app with music, video, photos and interviews

For me music is more than just the song, it is about the singer, band or DJ and their story

Music Aficionados

All consumers

QuesPon asks: Which of the following statements apply to you? Note: Music Aficionados are consumers that spend above average money and Pme with music Source: MIDiA Research Consumer Survey 06/14 (UK, US, Brazil) n = 3,000

PenetraPon By Age Of Super Fans And Consumers Interested In 360° Music Products

Next GeneraPon Music Products Need To Be Dynamic, InteracPve, Social, Curated D.I.S.C. – The Music Format Bill Of Rights

Next GeneraPon, 360° Music Products Will Add Curated Context To The Music 360° Music Product Concept

SubscripPon Services Are Ready-‐Made Placorms For Delivering 360° Products To Super Fans

% of consumer segment

16%

22%

30%

39%

31%

42%

44%

51%

0% 20% 40% 60% 80% 100%

Would pledge money to arPst to get next album to as exclusive app 2 weeks ahead of main release

Would buy merchandize and concert Pckets directly from arPsts within streaming services

Subscribers Aficionados Streamers All consumers

QuesPon asks: Some singers and bands are concerned that streaming music services like YouTube, SpoPfy and Deezer pay too liole money back to them compared to selling CDs or downloads, thus making it hard for many of them to make a living. Considering this please indicate how much you agree with each of the following statement Source: MIDiA Research Consumer Survey 10/14 (UK only) n = 1,000

Interest In AlternaPve Forms Of Fan MonePzaPon By Consumer Segment

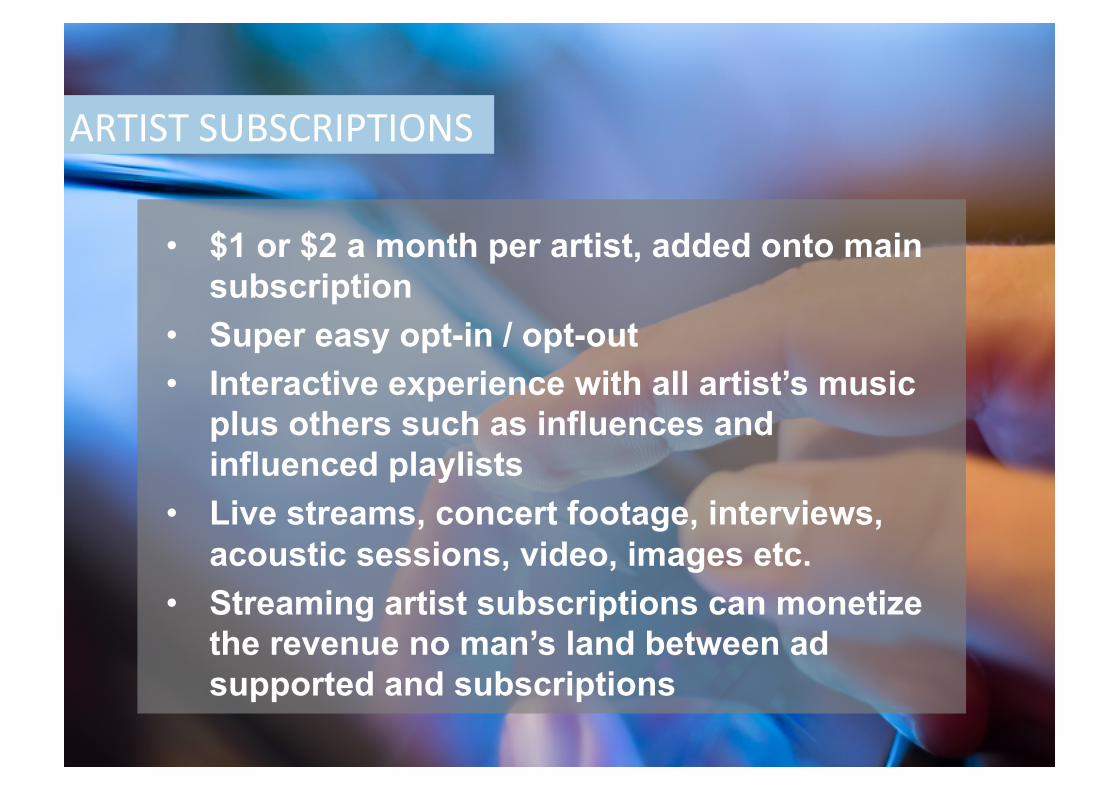

• $1 or $2 a month per artist, added onto main subscription

• Super easy opt-in / opt-out • Interactive experience with all artist’s music

plus others such as influences and influenced playlists

• Live streams, concert footage, interviews, acoustic sessions, video, images etc.

• Streaming artist subscriptions can monetize the revenue no man’s land between ad supported and subscriptions

ARTIST SUBSCRIPTIONS

Where Does The Streaming Road Lead?

1. Change Is Difficult 2. Not All Audiences Are The Same 3. Pricing & 360° Music Products 4. Conclusions

If there’s a gold rush you want to be selling shovels!

Samuel Branan Leland Stanford Levi Strauss

So What Is The Shovel Today?

The Web • InformaPon • Services • Tools

Tradi@onal Music Business • Contacts • MarkePng • DistribuPon

Today’s Music Business • ConnecPons • CuraPon • Engagement

Awakening The definiPve account of the music industry’s digital journey Available from Amazon, iTunes and Google Play Store now!

Contact: Mark Mulligan Phone: +44 (0) 780 11 66 712 Email: [email protected] Web: hop://midiaresearch.com Blog: hop://musicindustryblog.wordpress.com TwiTer: @mark_mulligan

Related Documents