MICROCREDIT AND ECONOMIC DEVELOPMENT: ENTREPRENEURSHIP OR SELF-EMPLOYMENT? Joana Vieira dos Reis Robalo Master of Science in Business Administration Supervisor: Prof. Doutora Sofia Santos, Auxiliar Professor., ISCTE Business School, Departament of Marketing, Operations and General Management January 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

MICROCREDIT AND ECONOMIC DEVELOPMENT:

ENTREPRENEURSHIP OR SELF-EMPLOYMENT?

Joana Vieira dos Reis Robalo

Master of Science in Business Administration

Supervisor:

Prof. Doutora Sofia Santos, Auxiliar Professor., ISCTE Business School, Departament of

Marketing, Operations and General Management

January 2015

Microcredit and Economic Development: Entrepreneurship or Self-employment?

II

Microcredit and Economic Development: Entrepreneurship or Self-employment?

III

Abstract

The present thesis aims to answer the central research question “Can microcredit be

considered as an entrepreneurial activity capable of creating innovative and value-added

businesses rather than a self-employment movement with few effects on economic

development?”. Considering the quantitative method, three hypothesis have been tested:

H1) The majority of microcredit applicants are unemployed individuals; H2) Microcredit

applicants tend to apply the money in businesses with innovative features and H3) Micro

entrepreneurs create only their own job and not for others. Regarding the qualitative

approach, two sub questions have been placed: SQ1) In what conditions and why do

people apply to microcredit programs and SQ2) In what sectors do the microcredit

applicants invest?

Although microcredit and microfinance industry is young in Europe and there is still a

long path to cover, the research conducted showed that microcredit is a promising sector

that is growing and evolving rapidly. If in previous years microcredit and microfinance

projects were mostly strict to promote self-employment through traditional activities,

nowadays this reality is changing and the type of business created is increasingly adopting

value-added features.

This research concludes that although microcredit does not nurture highly innovative

businesses, it can in fact be considered as an entrepreneurial activity capable of creating

value-added businesses that can have a role on job creation as well as in lessening of

social exclusion, positively affecting economic development.

Key words: Microcredit; Microfinance; Entrepreneurship; Economic Development

JEL Classification System: G210, O190

Microcredit and Economic Development: Entrepreneurship or Self-employment?

IV

Resumo

A presente tese tem como objectivo responder à questão “Pode o microcrédito ser

considerado como uma actividade empreendedora capaz de criar negócios inovadores e

de valor acrescentado em vez de um movimento de auto-emprego com poucos efeitos no

desenvolvimento económico?”. Considerando o método quantitativo, três hipóteses

foram testadas: H1) A maioria dos candidatos ao microcrédito são desempregados; H2)

Os candidatos ao microcrédito tendem a aplicar o dinheiro em negócios com

características pouco inovadoras e H3) Os microempreendedores criam apenas o seu

próprio posto de trabalho e não para outros. Relativamente ao método qualitativo, duas

sub-questões foram colocadas: SQ1) Em que condições e porque é que as pessoas

recorrem ao microcrédito? e SQ2) Em que sectores é que os candidatos ao microcrédito

investem?

Apesar da indústria do microcrédito e da microfinança ser relativamente recente na

Europa, a pesquisa conduzida mostrou que o microcrédito é um sector promissor que tem

vindo a evoluir rapidamente. Se anteriormente os projectos de microcrédito e a

microfinança eram quase restritos à promoção do auto-emprego através de criação de

actividades tradicionais, hoje em dia esta realidade está a mudar.

Esta pesquisa conclui que, apesar do microcrédito não fomentar negócios altamente

tecnológicos, pode de facto ser considerado uma activade empreendedora capaz de criar

negócios com valor acrescentado que podem desempenhar um papel na criação de

emprego bem como na diminuição da exclusão social, afectando positivamente o

desenvolvimento económico.

Palavras chave: Microcrédito; Microfinança; Empreendedorismo; Desenvolvimento

Económico

Classificações do JEL: G210, O190

Microcredit and Economic Development: Entrepreneurship or Self-employment?

V

Acknowledgements

“No duty is more urgent than that of returning thanks”

— James Allen

The development and conclusion of this thesis would not be possible without the support,

accessibility and contribution of some people. Sofia Santos - my supervisor, Ana

Mendonça and Sara Silva from ANDC, Amílcar Martins and António Curto from

CASES, António Oliveira from BES, Joana Lopes from AUDAX and lastly - but

defintely not the least, Tânia Sousa from Millennium BCP. To them, I would like to

express my deep gratitude and appreciation for their involvement.

At the same time, the encouragement and inspiration given by my family and friends

throughout this period was essential to the culmination of this thesis. Having them

accompanying the steps of this journey was of an incredible value and for that I am

grateful.

Thank you.

Microcredit and Economic Development: Entrepreneurship or Self-employment?

VI

Contents

Abstract ........................................................................................................................... III

Resumo ............................................................................................................................. V

Acknowledgements .......................................................................................................... V

I. List of Tables ........................................................................................................ VIII

II. List of Figures ....................................................................................................... VIII

III. List of acronyms ................................................................................................ VIII

1. Introduction .............................................................................................................. 2

2. Literature Review ......................................................................................................... 4

2.1 Unemployment ...................................................................................................... 4

2.2 Economic development and Economic growth ..................................................... 6

2.2.1 Theory of Economic Development ................................................................ 6

2.3 Entrepreneurship & Self-employment ................................................................... 7

2.3.1 Entrepreneurship ................................................................................................. 7

2.3.2 Self-Employment ........................................................................................... 7

2.3.3 Motivations..................................................................................................... 8

2.4 Linking Entrepreneurship and Self-employment with Unemployment ................ 9

2.4.1 Casual Relation .............................................................................................. 9

2.4.2 Practical outcomes........................................................................................ 10

2.5 Social Entrepreneurship and Social Economy .................................................... 11

2.5.1 Social Economy Entities .............................................................................. 11

2.5.2 Social Economy in Europe ........................................................................... 12

2.6 Entrepreneurship Action Plan 2020 and European Microfinance Network ........ 13

2.7 Micro, Small and Medium-Sized Enterprises...................................................... 15

2.8 Microcredit and microfinance ............................................................................. 16

2.9 Summary .............................................................................................................. 20

2. Literature Review’s Conceptual Framework .......................................................... 22

Microcredit and Economic Development: Entrepreneurship or Self-employment?

VII

3. Microfinance Industry ............................................................................................ 24

4.1 Microfinance in Europe ....................................................................................... 25

4.2 Microfinance in Portugal ..................................................................................... 29

4. Conceptual Microfinance Industry Framework ...................................................... 31

6. Future Trends in Microfinance ................................................................................... 32

7. Methodology and Method .......................................................................................... 34

7.1 Methodology ........................................................................................................ 34

7.1.1 Inductive approach ............................................................................................ 34

7.2 Method ................................................................................................................. 35

7. 2.1 Mixed Methods Approach ............................................................................... 35

7.2.1.1 Qualitative Approach ..................................................................................... 36

7.2.1.2. Quantitative approach ................................................................................... 37

8. Data Analysis: Content and Results Analysis ............................................................ 41

8.1 Qualitative: Content Analysis .............................................................................. 41

8.2 Quantitative: Results Analysis ............................................................................ 44

8.3 Summary .............................................................................................................. 47

9. Discussion ................................................................................................................... 49

10. Conclusions .............................................................................................................. 56

10.1. Theoretical and Practical Implications ............................................................. 57

10.2. Practical Recommendations .............................................................................. 59

11. Further Research ....................................................................................................... 61

12. References ................................................................................................................ 62

Appendix ........................................................................................................................ 65

Appendix 1 – Inquiry to Microcredit and Microfinance Applicants .............................. 66

Appendix 2 – Results from the Inquiry .......................................................................... 69

Microcredit and Economic Development: Entrepreneurship or Self-employment?

VIII

I. List of Tables

Table 1 - Categorization of SME .................................................................................... 15

Table 2 – MICROINVEST and INVEST + main characteristics ................................... 30

Table 3 - Future relations between providers and clients ............................................... 32

Table 4 - Interaction with the microcredit and microfinance institutions ...................... 37

Table 5 - Interaction with the entrepreneurship institutions ........................................... 37

II. List of Figures

Figure 1-Unemployment rates seasonally adjusted, January 2000 - May 2014 ............... 5

Figure 2-Youth unemployment rates seasonally adjusted, January 2000 - May 2014 ..... 5

Figure 3 - Social Economy Sector Distribution ............................................................. 12

Figure 4 - Weight of the categories enterprises in EU25 ............................................... 16

Figure 5 - Evolution of the microcredit borrowings ....................................................... 24

Figure 6 - Evolution of the average loan per borrower in USD ..................................... 25

Figure 7 - Microfinance Institutions in Europe .............................................................. 26

Figure 8 - Microfinance Institutions in Europe .............................................................. 27

Figure 9 - Occupation of the applicants to microcredit and microfinance ..................... 45

Figure 10 - Innovation level in the businesses created ................................................... 45

Figure 11 - Number of employed persons on each business created ............................. 45

Microcredit and Economic Development: Entrepreneurship or Self-employment?

IX

III. List of acronyms

ANDC - Associação Nacional de Direito ao Crédito

ANJE – Associação Nacional de Jovens Empresários

APE – Associação Portuguesa de Empreendedores

BES – Banco Espírito Santo

CASES - Cooperativa António Sérgio para a Economia Social

CGAP - Consultative Group to Assist the Poor

CIP - Competitiveness and Innovation Programme

EIB- European Investment Bank

EIF – European Investment Fund

EMN - European Microfinance Network

EPMF - European Progress Microfinance Facility

EPPA - European Parliament Preparatory Action

ICT - Information and Communication Technologies

INPI – Instituto Nacional da Propriedade Industrial

IEFP - Instituto do Emprego e Formação Profssional

IFDEP - Instituto para o Fomento e Desenvolvimento do Empreendedorismo em Portugal

JASMINE - Joint Action to Support Microfinance Institutions

JEREMIE – Joint European Resources for Micro and Medium Enterprises

MFI – Microfinance Institution

MAP - Multi-Annual Programme for the promotion of enterprise and entrepreneurship

UNEP – United Nations Environment Program

Microcredit and Economic Development: Entrepreneurship or Self-employment?

1

“If opportunity doesn't knock, build a door”

— Milton Berle

Microcredit and Economic Development: Entrepreneurship or Self-employment?

2

1. Introduction

According to the European Commission, in 2008, Europe entered in the worst crisis of

the last half a century. Since then, most of the countries in the European Union have been

struggling with unemployment rates, facing a serious handicap to both economic and

social development (European Commission, 2013). A possible identified solution to

overcome this problem consists in the development of entrepreneurship, namely through

the support of microfinance and microcredit associations. To the European Commission,

microcredit is an important key to growth, employment and social cohesion (European

Progress Microfinance Facility, 2010). Despite this optimistic position, several authors

doubt microcredit contributions in developed countries. Congregado (2010), Shane

(2009) and Baumol (2008) defend that self-employment only has temporary effects on

the unemployment level and does not nurture firms that generate innovation and wealth.

C.Ahlin (2011) goes further and questions the entire system of microcredit in developed

countries. As one can see, there are controversial opinions regarding microcredit and its

impacts, and although there are some authors that talk about the effects of

entrepreneurship and self-employment in the unemployment levels, the literature fails in

making the direct connection between microcredit and economic development.

The knowledge of the real effects of microfinance in developed countries is important

since it has numerous implications at economic, social and political levels. By

understanding if microcredit can contribute to economic development and to a broad

creation of jobs, entities such as the European Commission can develop action plans with

the proper measures to foster economy and achieve the goals of reducing unemployment

and consequently diminishing the social exclusion.

The present thesis aims not only to explore the concepts of entrepreneurship and

microcredit, but mostly understand their real contributions to reduce unemployment and

boost growth in the European Union, more particularly in Portugal. Considering this, the

research question is related with the extent to which microcredit can be considered an

entrepreneurial activity capable of creating innovative and value-added businesses

rather than a self-employment movement with few effects on economic development.

Microcredit and Economic Development: Entrepreneurship or Self-employment?

3

“Microfinance is an idea whose time has come”

— Koffi Annan

Microcredit and Economic Development: Entrepreneurship or Self-employment?

4

2. Literature Review

This section will begin by defining the notions of unemployment, economic development

and economic growth. Based on Schumpeter’s Theory of Economic Development, it will

explore in what extend the previous concepts of unemployment, economic development

and economic growth may be related to entrepreneurship and to self-employment and

how can they influence each other. The theories of entrepreneurship and self-employment

will therefore be explained and the connection between them and unemployment will be

explored, emphasizing the causality of this relation and its practical outcomes. The

concepts of social entrepreneurship and social economy will also be analised, together

with the activities developed in the entrepreneurship area by the European Commission,

namely the development of the Entrepreneurship Action Plan 2020 and the creation of

the European Microfinance Network, centring on the importance of Micro, Small and

Medium Enterprises. Next, the focus will be given to the microcredit and microfinance

sector, on its roots and its evolution, as well as the development of the microfinance sector

in Europe. Finally, a brief summary will be presented.

2.1 Unemployment

Europe entered in 2008 in a severe crisis and since then several countries of the European

Union have been passing through a severe period, struggling with unemployment rates

(European Commission, 2011). Unemployment, as defined by Eurostat considering the

guidelines of the International Labour Organization, refers to someone aged between 15

or 16 years to 74, without working during the reference week but actively searching for

employment during the last four weeks, being available to start working within the next

two weeks (or has already found a job to start within the next three months). The

unemployment rate translates the number of unemployed people as percentage of the

labour force (Eurostat Glossary). The labour force, also known as the active population,

includes both employed and unemployed people and excludes the economically inactive

(such as pre-school children, school children, students and pensioners) (Eurostat

Glossary). Another important concept is youth unemployment, defined by Eurostat as the

people between the ages of 15 and 24, inclusive, who are unemployed.

According to data from Eurostat1 concerning the year of 2013, although there are still

some member states with low unemployment rates, such as Austria (4,8%) or Germany

1 http://epp.eurostat.ec.europa.eu/statistics_explained/index.php/Unemployment_statistics

Microcredit and Economic Development: Entrepreneurship or Self-employment?

5

(5,3%), there are countries with alarming rates, such as Greece (27,6%) and Spain

(27,2%). In July, the Euro area (EA18) unemployment rate was 12,1%, corresponding to

26.654 million unemployed people. The following graphics illustrate the evolution of

unemployment and youth unemployment in Europe:

Figure 1-Unemployment rates seasonally adjusted, January 2000 - May 2014

Source: Eurostat, 2014

Figure 2-Youth unemployment rates seasonally adjusted, January 2000 - May 2014

Source: Eurostat, 2014

Microcredit and Economic Development: Entrepreneurship or Self-employment?

6

2.2 Economic development and Economic growth

The high levels of unemployment are a barrier to the economic development and to

economic growth (Quintana, 2012). Economic development can be defined as the

quantitative and qualitative changes in an existing economy, and involves the sustained

and resolute actions of communities and policymakers that intend to improve the

standards of living and the general welfare of the citizens as well as the economic health

of a specific region2. A similar but more restrict concept is economic growth, which can

be perceived as a sub category of economic development and respects to the general

increase in a country’s products and services output (Carruthers, 2010).

2.2.1 Theory of Economic Development

According to Schumpeter’s Theory of Economic Development (1934), economic

development has three pillars: the technological innovation, the credit for new

investments and the entrepreneur. To Schumpeter (1934), economic development is

endogenous, spontaneous and discontinuous. The entrepreneur is an agent of change and

the main carrier of economic development, and through his creative destruction, he is able

to break vicious economic cycles and create new paradigms, boosting competitiveness

and creating opportunities. Beyond the figure of the entrepreneur and the importance of

the bank credit for the economic development, the truly pioneering feature of

Schumpeter’s theory was the idea of creative destruction trough innovations and the

notion that bank credit was a prerequisite to innovation and to the foundation of new

enterprises (Hagemann, 2013). This happens since the entrepreneurs need financial means

to invest in their activities, which is given to them in form of credit by banking systems.

As it was said, the entrepreneur is an agent of change. Through the access to financing

sources, in which microcredit is included, the entrepreneur is capable of contributing to

the inversion of vicious economic cycles and ultimately create new opportunities and

stimulate economic development.

2 http://www.whatiseconomics.org/economic-development

Microcredit and Economic Development: Entrepreneurship or Self-employment?

7

2.3 Entrepreneurship & Self-employment

2.3.1 Entrepreneurship

The origin of the term entrepreneur comes from France in the 17th century and it was used

to describe someone who undertakes a significant project or activity. In fact, in a

minimalist sense, an entrepreneur is purely an individual who starts and/or runs a small

business (McLean, 2006) or someone who is self-employed (Hamilton, 2000). However,

considering a business approach, an entrepreneur is more than that. The concept has been

evolving throughout time: Jean-Baptiste Say (1803) defined an entrepreneur as an

economic agent who unites all means of production to create a product, and by selling it,

he is able to pay rents, wages and interests and remain with a profit. To Schumpeter

(1934:168), entrepreneurs are “innovators who use a process of shattering the status quo

of the existing products and services to set up new products and services”. Peter Drucker

(1964:28) defines an entrepreneur as someone who “searches for change, responds to it

and exploits opportunities”. According to Dees (1998:2), the term identifies the

“venturesome individuals who stimulated economic progress by finding new and better

ways of doing things”. Looking further into the literature, one can identify some attributes

repeated in several definitions of entrepreneur, such as the fact of being risk-taker,

innovator and creator of economic value. Despite these broader definitions of

entrepreneurship, if considering the minimalist sense defined by McLean (2006) or

Hamilton (2000), it can be difficult to distinguish between an entrepreneur and a self-

employed individual.

2.3.2 Self-Employment

A concept that is often connected to entrepreneurship is self-employment. A self-

employed person is defined by European Migration Network s an individual who is “the

sole or joint owner of an unincorporated enterprise (one that has not been incorporated,

i.e. formed into a legal corporation) in which he/she works, unless they are also in paid

employment which is their main activity” (European Migration Network, 2014:4).

Despite the similarities between the two concepts of entrepreneurship and self-

employment, a criticism pointed to self-employment is that most of the people that

become self-employed are not entrepreneurs in the sense of people creating businesses

that generate innovative businesses (Baumol, 2008; Shane, 2009). This leads to a key

Microcredit and Economic Development: Entrepreneurship or Self-employment?

8

aspect of the entrepreneurial activity that often lacks to self-employment by itself: value

added features. According to the Business Dictionary (2010), this refers to “extra features

of a business that go beyond the ordinary expectations and provide competitive edges”.

As it was stated before, through the offer of new products and services and the continual

improvements in the existing ones, entrepreneurs positively contribute to economic

growth and development. To do so, entrepreneurs rely on innovation, defined by the

European Commission on its Green Paper on Innovation (1996:54) as “the commercially

successful exploitation of new technologies, ideas or methods through the introduction of

new products or processes3, or through the improvement of existing ones.” According to

Simmie (2002), innovation is a result of an interactive learning process that involves often

several actors from inside and outside the companies. To Schumpeter (1911), it may

consist on the introduction of a new product, a new method of production, the opening of

a new market, a new source of supply or new forms of organization.

In order to better understand both entrepreneurship and self-employment, it is important

to go through the motivations that lead to the entrepreneurial activity.

2.3.3 Motivations

The motivations to entrepreneurial activity can be seen through three different angles:

economic, psychological and social. The first one underlines economic and

environmental factors that stimulate entrepreneurial activity, such as the dimension of the

markets, the rhythm of technological changes, the structure of the market or the industrial

dynamic (Tushman and Anderson, 1986). Economic incentives to entrepreneurial activity

include taxation policy, sources of financing and raw materials, easy access to

information and market opportunities, among others. The second one (psychological)

focuses on the individual traits of the entrepreneur, which means that the entrepreneurial

action relies on personal human attributes, such as the willingness to face uncertainty, the

propensity to accept risks and the need for achievement of the individuals. (McClelland,

1961). Lastly, the third prism (social) defends that entrepreneurship depends on cultural

factors and societal values, such as religious beliefs, customs or the functioning of the

institutions. Although each perspective gives special emphasis to different factors, these

3 The innovation process comprises the organizational business practices, new management systems, new

methods of labour organization and new methods of organizing external relations.

Microcredit and Economic Development: Entrepreneurship or Self-employment?

9

approaches are not exclusive and even complement each other, since there are several

dimensions that influence entrepreneurship (Eckhardt and Shane, 2003). More recently,

new studies have also shown that besides the factors previously mentioned, genetic

features may also influence the likelihood that people will be self-employed (Nicolaou

and Shane, 2009).

2.4 Linking Entrepreneurship and Self-employment with Unemployment

Connecting unemployment with self-employment and entrepreneurship comes from

Oxenfeldt (1943), who defends that unemployed individuals with low prospects for wage-

employment will find in self-employment a feasible alternative. Mandelman (2009)

completed this theory and stated that the nature of self-employment has two perspectives.

In the first one, the unemployed and those with less schooling and lower wages are more

likely to become self-employed, since in a segmented labour market they would be worse

positioned for finding good salaried and appellative opportunities. In the same line, older,

better-educated and well-paid workers with experience in the salaried sector would be

less likely to enter the self-employment sector once they already have comfortable

positions in the labour market. A second perspective takes in account liquidity constraints,

and thereby the experienced and best-salaried workers should be more likely to start their

own business, since they have accumulated the required capital and have easy access to

good business opportunities and financing sources. The unemployed, on the other hand,

tend to hold inferior endowments of human capital and entrepreneurial skills required to

start and sustain a new firm. This theory therefore suggests that high unemployment rates

may imply lower levels of personal wealth and so high unemployment may be associated

with a low degree of self-employment.

2.4.1 Casual Relation

Regarding the casual relation between self-employment and entrepreneurship with

unemployment, authors such as Blau (1987), Evans and Jovanovic (1989) defined the

refugee effect and the entrepreneurial effect. In the refugee effect, high unemployment

rates induce people to become self-employed since the opportunity cost of creating a start-

up firm has decreased. On the other hand, in the entrepreneurial effect, entrepreneurship

and self-employment contribute to the reduction of unemployment by creating new

ventures and new jobs. As one can see, the casual link between entrepreneurship and

Microcredit and Economic Development: Entrepreneurship or Self-employment?

10

employment is opposite in the two theories: while in the first one is the high

unemployment that encourages self-employment, the second suggests that is the decision

people make voluntarily to become entrepreneurs that will reduce unemployment at a

macro-economic level (Thurik et al., 2008). The two perspectives represent a virtuous

cycle, since unemployment promotes self-employment and self-employment reduces

unemployment. Although both theories are widely accepted, studies have showed that the

entrepreneurial effects are stronger than the refugee effects (Thurik et al., 2008).

2.4.2 Practical outcomes

Despite the theoretical positive effects of self-employment, several authors doubt its

practical outcomes. Some of the literature focusing on the decision to become an

entrepreneur suggests that public policy can reduce unemployment by providing

instruments to promote entrepreneurship, but does not necessarily stimulate economic

growth. To Thurik (2008), it is not clear that high rates of self-employment automatically

lead to improved performance. According to Millán & Román (2010), self-employment

is a tool for fighting unemployment that will only have temporary effects: Firstly, self-

employed show a low probability of survival and, in most cases, only a small number of

them will remain as self-employed once the economy recovers. Secondly, only a minority

of self-employed will hire other workers. In fact, in the EU-15 33,5% of self-employed

are job creators (Eurostat, 2009). There are even those who state that self-employment

rates may be inefficiently high (Carree et al., 2008) and that too much self-employment

can be characteristic of poor economies of scale in production and R&D rather than a

signal of vibrant entrepreneurial activity (Thurik et. at., 2008).

Finally, to Gries & Naudé (2010), technological innovation, improvements in

productivity and even economic growth do not automatically imply human development.

To them, although entrepreneurship is a determinant of economic growth, it does not

imply that it directly contributes to human development.

Understanding the casual relationship between self-employment and unemployment and

what are their real contributions to economic growth and development is of extreme

importance so that the policy makers can have the right basis to fruitfully develop

measures that promote entrepreneurship and self-employment and fight unemployment.

Taking into consideration these growing concerns, the concepts of social

entrepreneurship and social economy are emerging.

Microcredit and Economic Development: Entrepreneurship or Self-employment?

11

2.5 Social Entrepreneurship and Social Economy

Apart from entrepreneurship and self-employment, an evolving concept is social

entrepreneurship. To Reis (1999), social entrepreneurship is purely the application of

sound business practices to the operation of non-profit organizations. Some authors go

further and describe it as an “innovative approach for dealing with complex social needs”

(Johnson, 2000:2). To Anderson and Dees (2002:192), social entrepreneurship translates

the pursuit of “new and better ways to create and sustain value”. In this line, social

entrepreneurs are driven by social goals and aim to increase social value, contributing to

the welfare or well-being on a given community. This originates a new sector among

economies between the private (business) and public sectors (government): the social

economy sector. This sector includes organizations such as cooperatives, mutual

societies, non-profit associations, foundations and social enterprises (European

Commission, 2013). It can be defined as the dynamic created by a set of organizations

whose activity and existence is based on people and on its social utility (Curto & Martins,

2013).

2.5.1 Social Economy Entities

Social economy entities are mostly small and medium sized enterprises, and therefore

they are included in the Commission’s policy aiming at promoting enterprises, regardless

of their business form. According to the European Commission, social enterprises in

particular favour community’s interests in detriment of profit maximisation and they

frequently offer innovative goods and services and resort to original methods. Social

economy enterprises have therefore common characteristics (Curto & Martins, 2013),

such as:

Contribution to a more efficient market competition and encouragement of

solidarity and cohesion;

The primary purpose is not to obtain a return on capital;

Generally managed in accordance with the principles of solidarity and mutuality;

Adaptable to changing social and economic circumstances, as they are flexible and

innovative;

Based on active membership and commitment and very frequently on voluntary

participation.

Microcredit and Economic Development: Entrepreneurship or Self-employment?

12

Since these enterprises associate economic performance, democratic operation and

solidarity amongst members, they also contribute to the implementation of some of the

Community goals, particularly in the fields of employment, social cohesion, regional and

rural development, environmental protection, consumer protection and social security

policies (European Commission, 2013). Considering this, the Commission wants to create

a favourable environment for the development of social businesses and social economy

in Europe.

2.5.2 Social Economy in Europe

Social economy enterprises represent 10% of all European businesses, translating 2

million enterprises across Europe and employing over 11 million paid employees,

equivalent to 6% of the working population in the EU (European Commission, 2013).

The distribution of the sector is characterized in the following graphic:

Figure 3 - Social Economy Sector Distribution

Source: European Commission, 2013

The goal of the Commission regarding social economy enterprises is to guarantee that

they have the proper conditions to “compete effectively in their markets and on equal

terms with other forms of enterprise, without any regulatory discrimination and

respecting their particular principles, modus operandi, needs, particular goals, ethos and

working style4” (European Commission, 2013).

To promote this particular form of entrepreneurship, the Commission has been supporting

several projects in related areas, namely examining and reviewing legislation, identifying

4 http://ec.europa.eu/enterprise/policies/sme/promoting-entrepreneurship/social-economy/, accessed

07/12/2013

26%

4%70%

Cooperatives Others Non Profit Associations

Microcredit and Economic Development: Entrepreneurship or Self-employment?

13

and sharing good practices and also collecting statistical data. In 1989, the Commission

adopted a Communication on “Business in Social Economy Sector” and since then

several projects and activities have been done to promote the sector. In 2000 was founded

the Social Economy Europe, an EU representative institution for social economy. It aims

to “promote the social and economic input of the social economy enterprises and

organisations, to promote the role and values of social economy actors in Europe and to

reinforce the political and legal recognition of the social economy and of cooperatives,

mutual societies, associations and foundations at EU level5.” Also, as SME, social

economy enterprises benefit as well from Community programs, such as the

Competitiveness and Innovation Programme6 and other funds specially targeted to

regional development and research programmes.

Following these programmes, the European Commission settled the Entrepreneurship

Action Plan 2020, which aims to foster Europe’s entrepreneurial activity and boost

economic development. In the same ambit, the European Commission also took part in

the European Microfinance Network, promoting microcredit and microfinance across

Europe.

2.6 Entrepreneurship Action Plan 2020 and European Microfinance Network

As Congregado (2010) mentions, entrepreneurship and self-employment can contribute

to reduce unemployment by two channels: through the direct effect of an individual who

is unemployed becoming self-employed and through the indirect effect of an eventual

extra job creation by entrepreneurs in running enterprises that require outside job.

In the current economic crisis, problems related to the low rates of company’s creation

and company’s growth are a reality in Europe. According to the Flash Eurobarometer 354

(2012), 19% of EU respondents have started a business or taken over one and 4% is

planning to start one. This means that 77% of the respondents have never started a

business, taken over one nor intend to. In this line, 58% of the EU respondents say they

would prefer to work as an employee rather than being self-employed and more than a

5 http://www.socialeconomy.eu.org/spip.php?rubrique11, accessed 07/12/2013 6 CIP is a legal basis for all Community action relating to competitiveness and innovation. It covers

entrepreneurship, SME policy, industrial competitiveness, innovation, ICT development and use,

environmental technologies and intelligent energy.

Microcredit and Economic Development: Entrepreneurship or Self-employment?

14

fifth of EU respondents do not see self-employment as a feasible alternative. Regarding

the motives, the most appointed are the lack of capital or financial resources (21%), the

current economic climate (12%), the lack of skills to be self-employed (8%), the lack of

a business idea (7%), the difficulty in reconciling self-employment with family

commitments (6%) and finally the risk of failure and its consequences (5%).

Despite this scenario, new enterprises have been seen as a crucial ingredient in creating a

job-rich recovery in Europe, therefore it is necessary to empower Europe's entrepreneurs

and stimulate them to be more adaptable, creative and to have greater impact in a

globalised competition. As it was stated before, entrepreneurship can be motivated by

factors such as the taxation policy, industrial policy, sources of finance, availability of

investment and market opportunities, among others. Following this reasoning, in order to

bring Europe to the desired levels of employment and foster economic development, the

European Commission is creating a series of measures that aim to boost investment and

promote entrepreneurship, reinvigorating Europe’s entrepreneurs and pushing

entrepreneurial activity. These measures are defined on the Entrepreneurship Action Plan

2020 – Reigniting the Entrepreneurial Spirit in Europe and intend to “restore confidence,

creating the best possible environment for entrepreneurs by putting them at the heart of

business policy and practice, revolutionising the culture of entrepreneurship”. Thus, this

plan is based on three action pillars7 that intend to set out the foundations for future

growth and competitiveness. According to the European Commission, the plan is a

“blueprint for decisive action to unleash Europe's entrepreneurial potential, to remove

existing obstacles and to revolutionise the culture of entrepreneurship in Europe”. The

main changes that will happen in this panorama will be the inclusion of entrepreneurial

education and experience in school’s curricula, a reduction of the time and bureaucracy

necessary to start up a business, obtain the necessary licenses and permits and complete

bankruptcy procedures, and finally the creation of a mentoring, advice and support

program for potential entrepreneurs.

As it was said before, the lack of proper sources of financing translates one of the main

restraints to entrepreneurship in Europe. In order to surpass this strain and improve the

7 The action pillars of the Entrepreneurship Action Plan 2020 are: 1 – Entrepreneurial education and training

to support growth and business creation; 2 – Create an environment where entrepreneurs can flourish and

grow and 3 – Role models and reaching out to specific groups.

Microcredit and Economic Development: Entrepreneurship or Self-employment?

15

access to finance, the European Commission also plays an important role in the EMN

(European Microfinance Network), a non-profit association that aims to promote

microfinance, self-employment and microenterprises development, improving the

regulatory framework at European Union and Member State levels. The EMN was

launched in 2003 to bring together microfinance practitioners and people involved in

microfinance activities all over Europe and it had 22 members. Nowadays it has 87 active

members and partners located in 22 European countries. These members and partners are

practitioners, researchers and financial institutions. EMN has become a major actor in the

microfinance field in Western Europe and the creation of this network has proved to be

an essential step in the promotion of microfinance in the European Union, assisting the

fight against unemployment and social exclusion through the development of micro,

small and medium-sized enterprises.

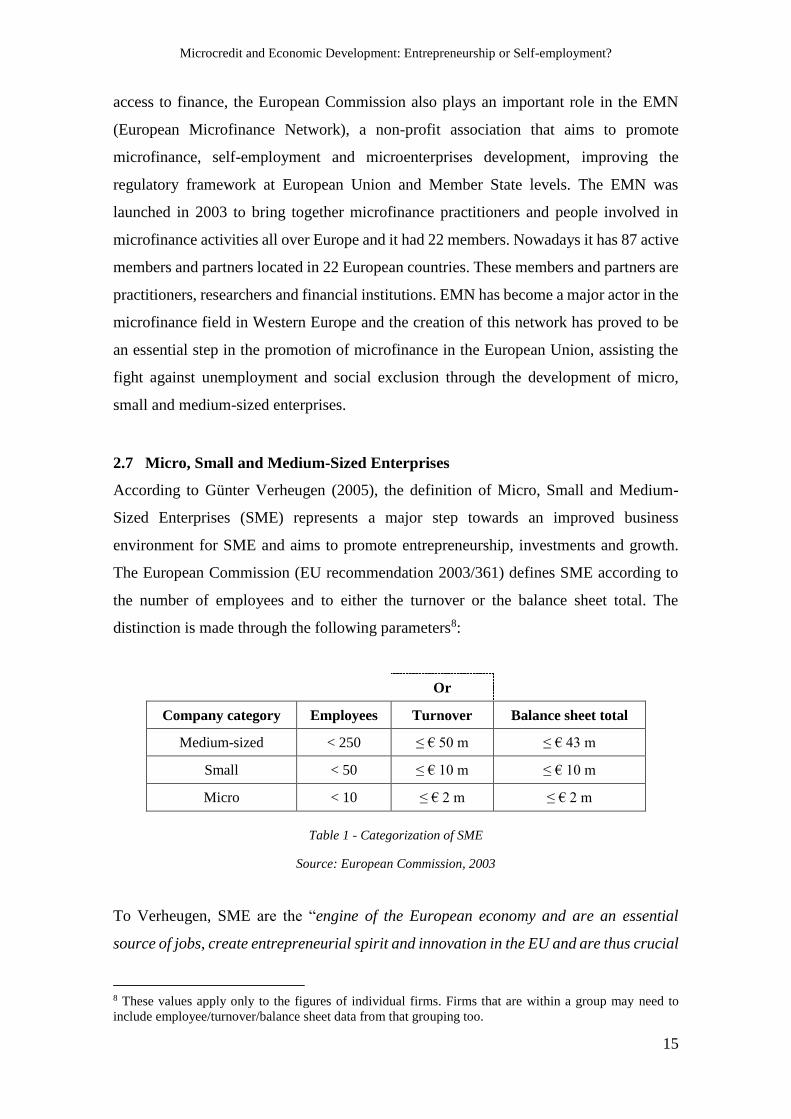

2.7 Micro, Small and Medium-Sized Enterprises

According to Günter Verheugen (2005), the definition of Micro, Small and Medium-

Sized Enterprises (SME) represents a major step towards an improved business

environment for SME and aims to promote entrepreneurship, investments and growth.

The European Commission (EU recommendation 2003/361) defines SME according to

the number of employees and to either the turnover or the balance sheet total. The

distinction is made through the following parameters8:

Or

Company category Employees Turnover Balance sheet total

Medium-sized < 250 ≤ € 50 m ≤ € 43 m

Small < 50 ≤ € 10 m ≤ € 10 m

Micro < 10 ≤ € 2 m ≤ € 2 m

Table 1 - Categorization of SME

Source: European Commission, 2003

To Verheugen, SME are the “engine of the European economy and are an essential

source of jobs, create entrepreneurial spirit and innovation in the EU and are thus crucial

8 These values apply only to the figures of individual firms. Firms that are within a group may need to

include employee/turnover/balance sheet data from that grouping too.

Microcredit and Economic Development: Entrepreneurship or Self-employment?

16

for fostering competiveness and employment9”. As Figure 4 illustrates, SME’s in EU25

represent almost 99% of all enterprises, providing around 75 million jobs (SME User

Guide, 2012). According to the European Commission (2011)10, microenterprises

represent 91% of the total enterprises in EU25, and the average company has five

workers. Despite the micro size of these companies, microenterprises account for 53% of

all jobs in EU25, having an enormous importance to European economy. One third of

these start-ups are launched by people who are unemployed (Relatório de Execução do

Instrumento de Microfinanciamento Progress, 201311).

Figure 4 - Weight of the categories enterprises in EU25

Source: European Commission, 2011

According to the European Commission (2011), microenterprises face particular

problems due to their small size and limited resources, such as finding the finance to get

the business going. To the European Investment Fund, the ability of a financial system to

reach such small entities is crucial for the achievement of general socio-economic

improvement. Microcredit and microfinance practices can be seen as a mechanism to

reach such small entities.

2.8 Microcredit and microfinance

Apart from self-employment and entrepreneurship, a concept that is becoming more and

more explored is microcredit. According to the Consultative Group to Assist the Poor

(CGAP), microfinance is the “provision of basic financial services to poor (low income)

people, who traditionally lack access to banking and related services12”. To the European

9 http://ec.europa.eu/enterprise/policies/sme/files/sme_definition/sme_user_guide_en.pdf, accessed at

08/12/2013 10http://ec.europa.eu/enterprise/policies/sme/promoting-entrepreneurship/crafts-micro-

enterprises/index_en.htm, accessed at 09/12/2013 11 ec.europa.eu/social/BlobServlet?docId=12682&langId=pt, , accessed at 09/12/2013 12 http://www.cgap.org/about/faq/what-microfinance, accessed at 08/12/2013

86% 88% 90% 92% 94% 96% 98% 100%

Micro SME Big

Microcredit and Economic Development: Entrepreneurship or Self-employment?

17

Commission (2009), the meaning of microcredit sets apart from the poverty idea implied

by CGAP and is defined as a loan under 25.000 euros given to support the development

of self-employment and microenterprise that has both economic and social impacts. At

an economic level, it aims to create activities that generate income, creating jobs and

developing microenterprises and regions, and at a social level it ambitions to reduce social

exclusion and also the financial inclusion of individuals. Besides microcredit, another

important and broader notion is microfinance, defined by the United Nations

Environment Program (UNEP) as referring to “loans, savings, insurance, transfer

services, microcredit loans and other financial products targeted at low-income

clients13”. These concepts differ from commercial banking since they relate to small loan

sizes, quick and easy access, non-traditional credit worthiness evaluation, and alternative

collateral requirements.

The first documented experience related to microcredit goes back to 1846, when, in the

south of Germany, the local farmers became tied to loan sharks after a rigorous winter.

As a solution, the German Mayor Raiffensem created the Bread Association, in which he

gave flour to the farmers so that they could make bread, being able to pay their debts with

the profit obtained from their sales. Since then, many other isolated actions similar to

microcredit have been done worldwide, but the stepping-stone to the development and

diffusion of microcredit was set by Muhammad Yunus in 1976. Like Raiffensem in

Germany, Yunus in Bangladesh noticed that several people were asking credit to the loan

sharks in order to run their own businesses, and despite the high interest rates charged,

they were able to pay their debts. Yunus started then to lend his own money to some

people who wanted to develop productive activities, and after numerous success cases,

he founded in 1983 the first microcredit institution – the Grameen Bank. His work led

him to the Nobel Peace Prize in 2006 in the field of Humanitarian Work, recognizing his

efforts to create economic and social development from below14.

With the success in Bangladesh, microcredit quickly expanded to other parts of the world,

especially to third world countries, being appointed as a popular tool for economic and

social development (Eunice, 2011).

13 http://capacity4dev.ec.europa.eu/unep/topic/microfinance, accessed at 08/12/2013 14 http://www.nobelprize.org/nobel_prizes/peace/laureates/2006/yunus-facts.html

Microcredit and Economic Development: Entrepreneurship or Self-employment?

18

Although “it was long thought that microfinance was limited to developing countries”

(Guichandut, 2006:55), microcredit has been more recently extending to developed

countries, namely in the European Union. While in developing countries the aim of

microcredit is to reduce poverty, promote self-employment and improve the

empowerment of socially excluded persons, in industrialized countries the goal is firstly

encouraging self-employment and entrepreneurship (Brana, 2011).

2.8.1 Microfinance in Europe

According to the European Investment Fund (2012), microfinance is long recognised by

European policy-makers as an instrument that not only boosts entrepreneurship and

competitiveness, but also promotes social inclusion. However, considering the legal and

political environments, the development of the European microfinance sector is still at an

early phase regarding its scale and broader impact, and faces a continuing gap between

supply and demand, as it will be explained in the next section – Microfinance Industry.

Considering the Progress Microfinance15 Report (2010), microfinance’s targets

individuals who lost their job or are at risk of losing it, individuals facing difficulties

entering the labour market, people at risk of social exclusion as well as vulnerable people

with difficulties accessing the credit market. It also targets microenterprises, especially

those in the social economy sector which employ individuals on the previous situations.

As in developing countries, microfinance in Europe started with social purposes.

However, unlike developing countries, microfinance in Europe has not moved forward to

a more professionalized business approach. The European Microfinance Network (2007)

presents some assumptions to explain why European microfinance schemes have not

managed to overcome obstacles and reach financial sustainability, namely the fact that

micro entrepreneurs have more options to finance their projects compared to

entrepreneurs in developing countries and financial markets are well developed, with

banks reaching the majority of the population. Nevertheless, over the past years, the

European Commission has been promoting several actions in order to support

microfinance (EIF, 2012/13), namely:

15 The European Progress Microfinance Facility is an initiative in which the European Commission and the

European Investment Bank have made available EUR 205 million of funding to microfinance services.

Microcredit and Economic Development: Entrepreneurship or Self-employment?

19

Risk protection to financial institutions, namely banks, guarantee institutions and

counter-guarantee institutions, for new micro-credit portfolios, under the Growth

and Employment Initiative (2000), the Multi-Annual Programme for the promotion

of enterprise and entrepreneurship (2005) and the Competitiveness and Innovation

Framework Programme (2013), all managed by the EIF;

The Joint European Resources for Micro and Medium Enterprises (“JEREMIE”)

scheme, managed by the EIF on behalf of the European Union (2007-2013), aiming

to improve the access to finance, including micro-credit using European Structural

Funds;

The European initiative for the development of microcredit in support of growth

and employment (2007), a broader EU policy move to use public funds to contribute

to the development and long-term sustainability of the sector.

Despite the growing importance given to microfinance, there are still several criticisms

pointed out to it, namely the fact that most of its institutions are dependent on subsidies

and are unable to operate profitably enough to cover its costs (Christen & Rosenberg,

2000). In fact, according to the Deutsche Bank (2007), only 2% of all the MFIs worldwide

are financially sustainable, and in the most cases, these are bigger, established, regulated

and relatively well-known MFIs.

Also, to Banerjee and Newman (1993), production organized within a firm is often more

efficient that production organized across small autonomous individuals, due to

economies of scale and specialization effects and to Matsuyama (2007), microcredit

improves micro-borrowers access to capital and technology, but does not seem to allow

them to reach optimal capital scale and technology levels.

Finally, there are authors such as Ahlin (2011) who defend that microfinance may rely on

poor economies to survive, in the sense that microcredit may need a vibrant informal

economy, a situation that tends to grow rarer as a country develops. Besley and Coate

(1995) also believed that microcredit is at best an anti-poverty tool and not a stepping-

stone to broader development.

Microcredit and Economic Development: Entrepreneurship or Self-employment?

20

As one can see, there are different opinions regarding microcredit and microfinance and

its practical impacts: while some believe microcredit and microfinance can represent a

possible answer to foster economic development in Europe, others doubt is outcomes,

especially considering the European panorama.

2.9 Summary

This section focused on the important concepts and existing ideas regarding microcredit

and entrepreneurship and intended to set a basis for further research. The main ideas to

retain are the following:

The high levels of unemployment in Europe are a barrier to the economic

development and to economic growth. According to Schumpeter (1911), economic

development is supported by technological innovation, by the credit for new

investments and by the entrepreneur. Throughout time there have been several

definitions of entrepreneur and most of them repeat some attributes such as the fact

of being risk-taker, innovator and creator of economic value. Self-employment sets

apart from entrepreneurship due to the fact that most of the self-employed people

do not create innovative businesses.

Connecting unemployment with self-employment and entrepreneurship comes

from Oxenfeldt (1943) and was later developed by Mandelman (2009), who

defends that the nature of self-employment can have two perspectives, and both

unemployed and experienced workers have probabilities to become self-employed.

Regarding the casual relation between self-employment and entrepreneurship with

unemployment, authors such as Blau (1987), Evans (1989) and Jovanovic (1989)

defined the “refugee effect” and the “entrepreneurial effect”, which have an

opposite causal link between entrepreneurship and employment. Although several

authors defend the positive effects of entrepreneurship and self-employment,

authors such as Thurik (2008), Carree (2008) and Millán & Román (2010) doubt

its practical outcomes.

Despite these negative ideas, the European Commission strongly believes that

entrepreneurship and self-employment are crucial for an European recovery and

therefore is trying to promote them, namely trough the creation of the

Microcredit and Economic Development: Entrepreneurship or Self-employment?

21

Entrepreneurship Action Plan 2020 and the European Microfinance Network. By

doing so, the expansion of microcredit in Europe is being promoted. According to

the European Commission (2009), microcredit is a loan under 25.000 euros given

to support the development of self-employment and microenterprises. Regardless of

the growing importance given to microfinance, authors such as Besley & Coate

(1995), Christen & Rosenberg, (2000), Matsuyama (2007) and Ahlin (2011) point

out several criticisms to it.

Although there are some authors that have studied the impacts of entrepreneurship and

self-employment on the employment level, the literature fails in making the direct

connection between microcredit and unemployment. The major topics of the Literature

Review are briefly schematized in the next page and the following sections will explore

the mentioned gap between microcredit and unemployment.

Microcredit and Economic Development: Entrepreneurship or Self-employment?

22

2. Literature Review’s Conceptual Framework

The unemployed are more

likely to become self-

employed. vs

Experienced and best-

salaried workers are more

likely to start their own

business.

Nature Casual Relation Practical Outcomes

Entrepreneurship Action Plan 2020 and European Microfinance Network

Development of measures that promote entrepreneurship and fight unemployment

Mandelman (2009)

Blau (1987)

Evans & Jovanovic (1989)

Refugee effect

Entrepreneurial effect

Does not necessarily

stimulate economic growth;

Temporary effects;

Does not automatically

imply human development.

Unemployment Self-employment

Thurik (2008) Carree et al. (2008)

Millán & Román (2010)

Risk-Taker

Innovator

Creator of Economic Value

Theory of Economic Development

Schumpeter (1911)

High levels of unemployment in Europe

Economic development and growth

Technological

Innovation

Credit for new

investments

Entrepreneurship

Self-employment No Value Added Features

Baumol (2008) & Shane (2009)

Effects on Unemployment

VS Motivations

Tushman & Anderson (1986), Eckhardt (2003)

Economic

Psychological

Social

Expansion of microcredit and

microfinance in Europe

Social Entrepreneurship and Social Economy

Microcredit and Economic Development: Entrepreneurship or Self-employment?

23

“This is not charity. This is business: business with a social

objective, which is to help people get out of poverty”

—Muhammad Yunus

“This is not charity. This is business: business with a social

objective, which is to help people get out of poverty”

—Muhammad Yunus

Microcredit and Economic Development: Entrepreneurship or Self-employment?

24

3. Microfinance Industry

The microfinance industry is now quite diverse in terms of organizational types, with

Microfinance Institutions (MFIs) organized as Non-Governmental Organizations

(NGOs), banks, credit cooperatives and nonbank financial institutions (Hartarska, 2005).

The majority of the MFIs start as NGOs and finance their business via donations and/or

public money, and over time, they develop to formal financial institutions and regulated

entities.

According to the European Microfinance Network, the estimations are that exist 10.000

microfinance institutions worldwide, and among these, 2.000 report to the Microfinance

Information Exchange (MIX). The MIX is a non-profit organization that provides

performance information on microfinance institutions, funders, networks and service

providers dedicated to serving the financial sector needs for low-income clients. MIX

accomplishes its mission through a variety of platforms, being the most important the Mix

Market, in which instant access to financial and social performance of the MFIs is

provided. Considering data from the EIF, in 2008 the microfinance institutions that

reported to the MIX had 70 million borrowers and an equivalent number of savers. In

Asia, Africa, Latin America and Middle East, the majority of the clientele are women,

accounting for 98 percent of borrowers, while in the Eastern Europe and Central Asia,

women represent 47 percent of the borrowers. The evolution of the borrowings can be

seen in the following graphics:

Figure 5 - Evolution of the microcredit borrowings

Source: MixMarket, 2013

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

2009 2010 2011 2012

Borrowings

Africa East Asia and the Pacific

Eastern Europe and Central Asia Latin America and the Caribbean

Middle East and North Africa South Asia

Microcredit and Economic Development: Entrepreneurship or Self-employment?

25

Figure 6 - Evolution of the average loan per borrower in USD

Source: MixMarket, 2013

4.1 Microfinance in Europe

The microfinance industry is young in Europe and represents a growing sector with a

considerable potential (EMN, 2013). Despite its early life, the microfinance industry is

quite heterogeneous in terms of organizational types, due to the disparity of the legal and

institutional frameworks in the member states and the diversity of microcredit providers.

Credit organizations can be divided into two groups, based on the importance given to

microfinance services: those whose primary activity is granting microcredit accounts for

35% of all the participants, while the remaining organizations process microfinance as a

side activity. As a consequence, lending practices in microcredit vary considerably

depending on the type of institution providing micro loans, its legal setup, the

environment in which it operates and its own ability to apply sound and efficient

management procedures. Microfinance institutions in Europe are organized as showed in

the following graphic:

0

2000

4000

6000

8000

10000

2009 2010 2011 2012 2013

Average loan per borrower (USD)

Africa East Asia and the Pacific

Eastern Europe and Central Asia Latin America and the Caribbean

Middle East and North Africa South Asia

Microcredit and Economic Development: Entrepreneurship or Self-employment?

26

Figure 7 - Microfinance Institutions in Europe

Source: European Investment Fund, 2010

According to the EIF (2010), in the EU-15, MFIs are mostly characterised by having

“small size, very low or inexistence of profitability, very limited access to external sources

of funding, social lending activity mainly targeting disadvantaged groups,

unstandardized operational procedures16”. Also, as it was stated in the previous chapter,

many microfinance institutions heavily depend on subsidies to cover its costs.

Microfinance in Europe presents a dichotomy between Western and Central/Eastern

Europe namely in terms of intermediary profile, target beneficiaries and loan size (EIF,

2012). In Western European countries, microfinance has a strong focus on social

inclusion and therefore pays limited attention to profitability, while in Eastern Europe

there is a large presence of commercial intermediaries. The global microcredit demand in

the European Union reaches the 700.000 new loans, with a global value of 6.296 million

euros, and an average loan of 9000 euros.

In 2005, Europe had the following institutions providing microfinance services:

16 http://www.eif.org/news_centre/publications/EIF_WP_2009_001_Microfinance.pdf, accessed at

08/12/2013

28%

26%17%

28%

NGO Foundations Public Institutions Banks, Saving Banks and other Credit Institutions

Microcredit and Economic Development: Entrepreneurship or Self-employment?

27

Figure 8 - Microfinance Institutions in Europe

Source : EMN, 2005

As it was stated before, microfinance is a young and heterogeneous sector in Europe,

especially with regards to the diversity of institutional models, lending approaches and

regulatory frameworks (EMN, 2013). As lending practices vary significantly, the

European Commission identified as an important element to promote best practices in the

sector the development of a European Code of Good Conduct for Microcredit Provision.

This code intends to set a high bar for microfinance operations in Europe in line with

international policies and worldwide development of the sector and aims to benefit the

microfinance sector at large, including its funders, investors, customers, owners,

regulators and partner organizations. The code is divided into five sections: customer and

investor relations, governance, reporting standards, management information and risk

management, and its adoption is purely voluntary and is not expected to disrupt any

legislative requirements in any of the EU member countries (EMN, 2013).

Microcredit and Economic Development: Entrepreneurship or Self-employment?

28

The European Commission have been developing plenty of programmes in the field of

microfinance and microcredit, namely CIP, EPPA, JASMINE, JEREMIE and EPMF

(EMN, 2013):

The Competitiveness and Innovation Framework Programme (CIP) has several

schemes to facilitate access to loans and equity finance for SME where market

gaps have been identified. They cover different needs depending on the stage of

development of the small and medium sized enterprises;

The European Parliament Preparatory Action (EPPA) aims to foster the

development of microcredit in Europe on a sustainable basis, complementing

other European Investment Fund and European Commission’s initiatives in the

microfinance sector;

The Joint Action to Support Microfinance Institutions (JASMINE) was a pilot

initiative launched in 2008 by the European Commission, Directorate General for

Regional Policy, the European Investment Bank Group and the European

Parliament, helping non-bank microfinance institutions to scale up their

operations and maximise the impact of microfinance products on microenterprises

development and unemployment reduction within the European Union;

JEREMIE is a joint initiative developed by the European Commission in co-

operation with the European Investment Bank Group and other financial

institutions in order to make cohesion policy more efficient and sustainable.

JEREMIE offers EU Member States the opportunity to use part of their EU

Structural Funds to finance small and medium-sized enterprises by means of

equity, loans or guarantees, through a revolving Holding Fund acting as an

umbrella fund;

The European Progress Microfinance Facility (EPMF) provides covered

guarantees partially casing portfolios of micro-credits or of guarantees on micro-

credits to selected intermediaries authorised to provide microfinance instruments.

Despite the support from the European Commission in recent years to the microfinance

sector through these programmes, there is still a need to invest in capacity building and

refinancing of MFI’s in Europe, allowing them to improve their institutional capacities

and providing them with access to sustainable funding sources (EMN, 2013). In fact, as

it was mentioned by several European Institutions’ representatives in the 11th EMN

Microcredit and Economic Development: Entrepreneurship or Self-employment?

29

Annual Conference, MFI’s currently have a limited capacity to meet growing demand for

financial and coaching services from new entrepreneurs, which makes the provision of

economic support for business development services a priority.

4.2 Microfinance in Portugal

Microcredit as an instrument of social inclusion and of support to job creation was first

introduced in Portugal by Associação Nacional de Direito ao Crédito (ANDC) in 1999.

ANDC is a non-profit association founded in 1998 and was the pioneer in the

development of microcredit in Portugal. To do so, a partnership between three entities of

three different sectors was established: ANCD, from the social economy sector;

Millennium-BCP, from the private sector, and finally the Instituto de Emprego e

Formação Profissional (IEFP), from the public sector. Until 2005, Millennium-BCP had

an exclusive partnership with ANDC, but since then the range of the association had

become broader and is currently working with other banks, namely the Caixa Geral de

Depósitos (GDD) and Banco Espíirito Santo. Montepio and BPI are other banks that also

provide microfinance services.

Apart from banks, CASES (Cooperativa António Sérgio para a Economia Social) is

another entity that offers services related with microcredit and microfinance. Together

with IEFP, CASES is responsible by the National Microcredit Plan, which is a subsidized

credit line in the ambit of Programa de Apoio ao Empreendedorismo e à Criação do

Próprio Emprego, which intends to support of the creation of SME. The projects within

the National Microcredit Plan can benefit of a technical support from its creation to its

consolidation, during the first two years. The technical support activities consist on the

accompaniment of the approved project, formation and consulting in the management or

viability of the project. These activities are assured by representative entities from the

social economy sector that work with CASES or by non-profit entities from the private

sector or local authorities accredited by IEFP. IEFP, in partnership with CGD, Sociedade

de Garantia Mútua (SGM) and Sociedade de Investimento (SPGM), have two credit lines:

MICROINVEST and INVEST +. The main characteristics of these two lines can be seen

in the table below:

Microcredit and Economic Development: Entrepreneurship or Self-employment?

30

Maximum Amount Deadlines Interest Rate

Investing Financing 7 years, with 2 years of

capital shortage and 1 year

of integral bonification of

interests.

Reimbursement: 5 years,

with monthly constant

capital repayment

EURIBOR

30days + 0,25%

and minimum

rate of 1,5% and

maximum rate

of 3,5%.

MICROINVEST €20.000 €20.000

INVEST +

€20.000

to

€200.000

€100.000

(95% of the

investment and

€50.000 per full

time job created)

Table 2 – MICROINVEST and INVEST+ main characteristics

Source: Caixa Geral de Depósitos (CGD), 2009

The microcredit bank provider’s panorama in Portugal is summarized below:

Millennium BCP – grants maximum credit of €25.000 for a period of five years.

For credits until €7.000, the line is four years. The spread practiced depends on

the risk and on the type of business. In eight years, Millennium BCP has approved

2888 projects summing a value of €25,8 million;

CGD – operates over the protocol between ANDC and IEFP. The credit given

varies between €15.000 and €20.000 and the term can range between five or seven

years. Through this channel, CGD has granted €12,6 million;

BES – As CGD, it operates in partnership with ANDC and IEFP. The maximum

credit given is €20.000 over four years. Since 2009 it has supported 1000 projects,

giving €16 million;

BPI – Has a protocol with IEFP and MICROINVEST credit lines and it has a own

bank line. The maximum amount is €25.000 for four years or €20.000 for seven

years, according to the different instruments. BPI has supported 879 projects,

summing €20 million;

Montepio – Develops projects and partnerships in microcredit since 2006. The

amount given varies between €500 and €25.000 and the term goes from 6 months

up to 4 years.

The following scheme condenses the microfinance industry in Europe and shows the main

microcredit institutions in Portugal.

Microcredit and Economic Development: Entrepreneurship or Self-employment?

31

4. Conceptual Microfinance Industry Framework

CIP

Microfinance and Microcredit in Portugal

MFI’s types

worldwide

European Commission Initiatives

Hantarska (2005)

Credit Cooperatives

NGO’s

Banks

JEREMIE EPMF JASMINE EPPA

Promotion of the Microfinance and Microcredit Industry in Europe

Non-bank financial

institutions

Microcredit developed in

Bangladesh Grameen Bank (1983)

Microfinance in

Europe

Young Industry

Growing Sector

Heterogonous

ANDC Millennium BCP

CGD

BES

BPI

Montepio

CASES IEFP National Microcredit Plan

MICROINVEST

INVEST +

Microcredit and Economic Development: Entrepreneurship or Self-employment?

32

6. Future Trends in Microfinance

According to the report to MicroNed17 developed by Triodos Facet, a consultancy

company specialised in the promotion and development of sustainable SME, the sector

of microfinance is facing some trends that began in the past years and are likely to

continue, in which the key words are growth, scaling up, increased use of technology,

integration in mainstream finance and segmentation. Considering this, the future relations

between the different providers and clients are described in the following table:

Providers Products Clients

Banks;

Finance Companies;

NGOs;

Savings & Credit coops;

Big box consumer

reltailers;

Property developers;

Money transfer agencies;

Other new providers.

Micro loan & Small loan;

Educational loan;

Credit card;

Mortgage;

Consumer loan;

Checking & Savings

account;

Supplier Credit;

Leasing;

Other new products.

Families;

Micro entrepreneurs;

Small farmers;

Families in their different

roles: as consumers,

house builders, parents,

savers, insurance takers,

part of money flow

networks.

Table 3 - Future relations between providers and clients

Source: Triodos Facet, 2009

The prospect of microfinance will depend on how the industry manages the challenges

caused by its rapid growth. A survey developed in 2008 by the Centre for the Study of

Financial Innovation to microfinance practitioners, investors and analysts identified 20

risks that could aim the progress of microfinance. Among these, six of the top 10 were

management risks, namely management quality, corporate governance, cost control,

staffing, technology management and credit risk management.