Credit Rating

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Credit Rating

Credit rating

• A credit rating estimates the credit worthiness of an individual, corporation, or even a country. It is an evaluation made by credit bureaus of a borrower’s overall credit history.

• Credit ratings are based on financial history and current assets and liabilities.

• Typically, a credit rating tells a lender or investor the probability of the subject being able to pay back a loan.

• Commercial credit risk is the largest and most elementary risk faced by many banks and it is a major risk for many other kinds of financial institutions and corporations as well.

• Many uncertain elements are involved in determining both how likely it is that an event of default will happen and how costly default will turn out to be if it does occur.

There are four Credit Rating agencies in India

• CRISIL(Credit Rating Information Services of India Ltd)• ICRA(Information and Credit Rating Services ltd)• CARE (Credit Analysis and Research Ltd)• FITCH India

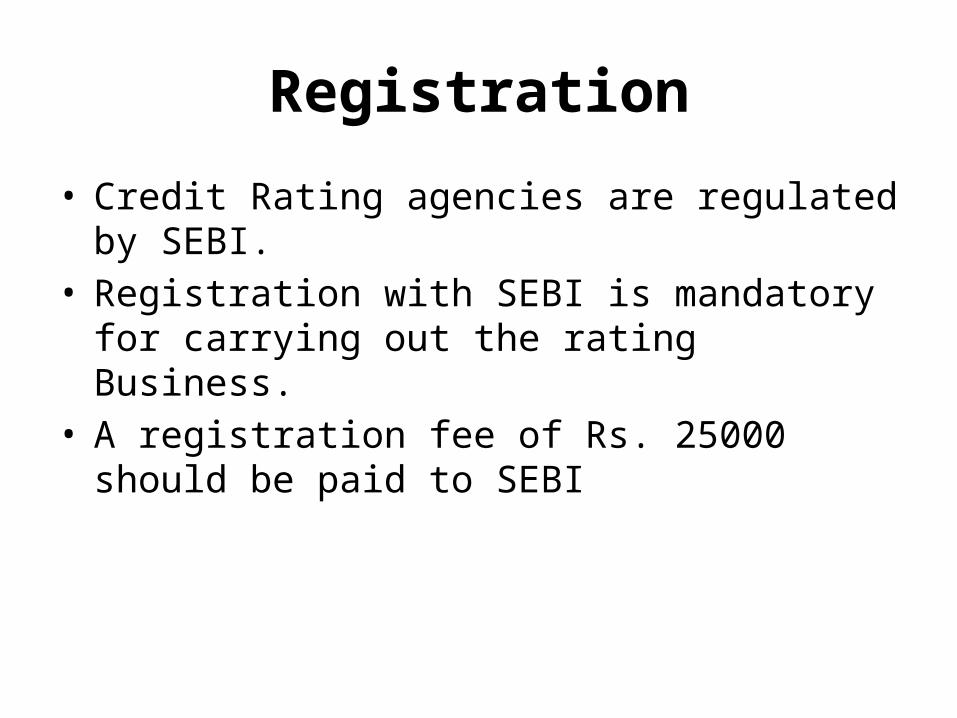

Registration

• Credit Rating agencies are regulated by SEBI.• Registration with SEBI is mandatory for carrying out

the rating Business.• A registration fee of Rs. 25000 should be paid to SEBI

Eligibility Criteria• Is set up and registered as a company• Has specified rating activity as one of its main objects

in its Memorandum of Association.• Has a minimum Net worth of Rs 5 Crore.• Has adequate Infrastructure• Promoters have professional competence, financial

soundness and a general reputation of fairness and integrity in Business transactions , to the satisfaction of SEBI.

• Has employed persons with adequate professional and other relevant experience, as per SEBI directions.

Grant of Certificate of Registration

• SEBI will grant to eligible applicants a Certificate of Registration on the payment of a fee of Rs 5,00,000 subject to certain conditions.

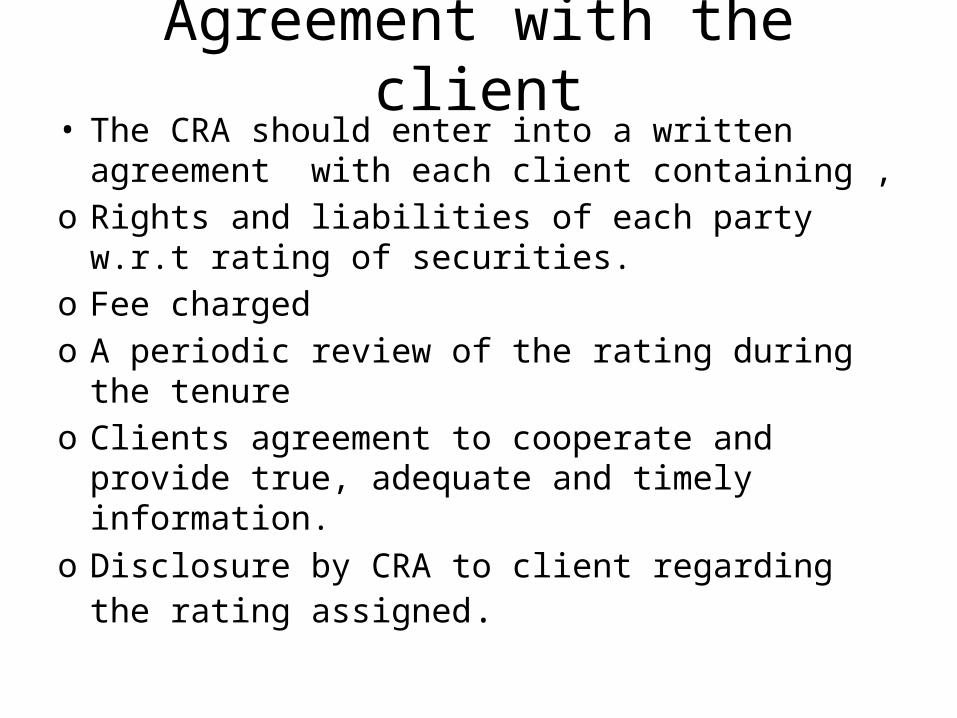

Agreement with the client• The CRA should enter into a written agreement with

each client containing ,o Rights and liabilities of each party w.r.t rating of

securities.o Fee chargedo A periodic review of the rating during the tenureo Clients agreement to cooperate and provide true,

adequate and timely information.o Disclosure by CRA to client regarding the rating

assigned.

CRISIL

• The first rating agency ‘Credit Rating Information Services of India Ltd. , CRISIL, was promoted jointly in 1987 jointly by the ICICI and the UTI. Other shareholders included LIC, HDFC Ltd, General Insurance Corporation of India and several other foreign and Indian Banks.

• It pioneered the concept of credit rating in the country and since then has introduced new concepts in credit rating services and has diversified into related areas of information and advisory activities.

• It became public in 1993.• In 1996, it formed a strategic alliance with S&P rating group.

ICRA Ltd• Information and Credit Rating Services (ICRA) has been promoted by

IFCI Ltd as the main promoter and started operations in 1991.• Other shareholders are UTI, Banks, LIC, GIC, Exim Bank, HDFC and

ILFS.• It provides Rating, Information and Advisory services ranging from

strategic consulting to risk management and regulatory practice.• The main objectives of ICRA are to assist investors both individual and

institutional in making well informed decisions• To assist issuers in raising funds from a wider investor base.• To enable banks, investment bankers, Brokers in placing debt with

investors.• To provide regulators with market driven systems to encourage the

healthy growth of capital markets.• It provides rating services, information services and advisory services.

CARE Ltd.• Credit Analysis and Research Ltd or CARE is promoted by IDBI

jointly with Financial Institutions, Public/Private Sector Banks and Private Finance Companies.

• It commenced its credit rating operations in October, 1993 and offers a wide range of products and Services in the field of Credit Information and Equity Research.

• It also provides advisory services in the areas of securitisation of transactions and structuring Financial Instruments.

• It offers services like 1. Credit rating of debt instruments 2. Advisory services like structuring financial instruments, financing infrastructure projects and municipal finances 3. Information services like providing information to companies, industry and businesses.

Fitch Ratings India Ltd.

• It is the latest entrant in the credit rating Business in the country as a joint venture between the international credit Rating agency Duff and Phelps and JM Financial and Alliance Group.

• In addition to debt instruments, it also rates companies and countries on request.

Rating Process• The process begins with issue of rating request

letter by the issuer of the instrument and signing of the rating agreement.

• CRA assigns an analytical team consisting of two or more analysts one of whom would be the lead analyst and serve as the primary contact.

• Meeting with Management- The analytical team obtains and analyses information relating to its financial statements, cash flow projections and other relevant information.

• Discussion with management on management philosophy, competitive position, financial policies and future plans.

Rating Process cont-• Discussions on financial projections based on

objectives and growth plan , risks and opportunities.

• Rating committee- after meeting with the management the analysts present their report to a rating committee which then decides on the rating.

• After the committee has assigned the rating, the rating decision is communicated to the issuer, with reasons or rationale supporting the rating.

• Dissemination to the Public: Once the issuer accepts the rating, the CRAs disseminate it, along with the rationale, to the print media.

Rating Review for a possible change• The rated company is on the surveillance system of

the CRA, and from time to time, the earlier rating is reviewed. The CRA constantly monitors all rating with respect to new political ,economic, financial development and industry trends.

• Analysts review new information or data available on the company. On preliminary analysis of the new information if the analyst feel that there is a possibility for change in the rating then they meet with the management and proceed with comprehensive rating analysis.

Credit Rating Watch

• During the review monitoring or surveillance exercise, rating analysts might become aware of imminent events like mergers and so on, which effect the rating and warrants a rating change.

• In such a possibility, the issuer’s rating is put on ‘credit watch’ indicating the direction of a possible change and supporting reasons for review.

• Once a decision to either change or present the rating had been made, the issue will be removed from credit watch.

Rating Methodology

• The rating methodology involves an analysis of industry risk, issuer’s business and financial risk. A rating is assigned after assessing all factors that could affect the credit worthiness of the entity. The industry analysis is done first followed by the company analysis.

Credit rating for manufacturing companies

• The main elements of rating methodology are as below• Business risk Analysis : It begins with an assessment of

the company’s environment focusing on the strength of the industry prospects, business cycle as well as competitive factors affecting the industry. The vulnerability of the industry to political factors is also assessed. If a company is involved in more than one business, each segment is analyzed separately. The main factors include Industry Risk, Market position, operating efficiency and legal position.

• Financial risk analysis: Financial risk is analyzed mainly through financial ratios. Emphasis is placed on the ability of the company to maintain /improve its future financial performance.

• The profitability of a company is an important determinant of its ability to withstand business adversity. The main measures of profitability include operating and net margins and returns on capital. The absolute levels of these ratios, trends and comparison of these ratios with other competitors is analyzed. Emphasis is also laid on cash flow patterns.

• The area analyzed are accounting quality, earnings prospects, adequacy of cash flows financial flexibility and interest and tax sensitivity.

• Management Risk: A proper assessment of debt protection levels requires an evaluation of management philosophies and its strategies. The analyst compares the company’s business strategies and financial plans to provide insights into a management’s ability to forecast and implement plans. The areas analyzed include track record of the management, planning and control systems, evaluation of capacity to overcome adverse situations, goals, philosophy and strategies.

Rating symbols/Grades• Rating symbols are a symbolic expression of

the opinion/assessment of the credit rating agency regarding the investment, credit quality, grade of the debt, obligation instrument.

• CRISIL rating symbols: The rating symbols of CRISIL with respect debentures, fixed deposits, short term instruments(CPs), credit assessment, structured obligations, bond funds, bank loans, collective investment schemes, Indian states, real estate developers are as follows.

Rating symbols for Debentures• High Investment Grade:• AAA-(Triple A ) Highest security- Offer the highest

safety against payment of interest and principal• AA(Double A) High Safety - Offer high safety against

payment of interest and principal.• A- Adequate safety- Offer adequate safety against

payment of interest and principal. In adverse conditions might affect such issues.

• BBB(Triple B)- Moderate safety- Offer sufficient safety against payment of interest and principal. Circumstances may lead to weakened capacity to pay interest and principal.

• Speculative grades • BB(Double B)- Inadequate safety- These

instruments carry inadequate safety of timely payment of interest and principal.

• B( High risk)- Instruments rated B have greater risk of default.

• C( Substantial risk)- Risk of default. Repayment can only be expected in favorable conditions.

• D (Default) Such instruments are extremely speculative and default risk is highest.

Rating symbols for Fixed deposits.• FAAA( F triple A)- Highest safety• FAA( F- double A)- High safety• FA- Adequate safety• FB- Inadequate safety• FC- High Risk• FD- Default

Rating symbols for Short term instruments

• P-1 (highest safety)• P-2 (High Safety)• P-3( Adequate safety)• P-4(Inadequate safety)• P_5 (default)

Rating for credit assessment• It indicates the capability of entity to repay the

interest and principal as per the terms of the contract. The rating symbols are as below-

• 1-Very strong capability• 2,3,4- Strong capability• 5,6,7- Adequate capability• 8,9,10- Inadequate capability• 11,12,13 –Poor capability• 14- Default

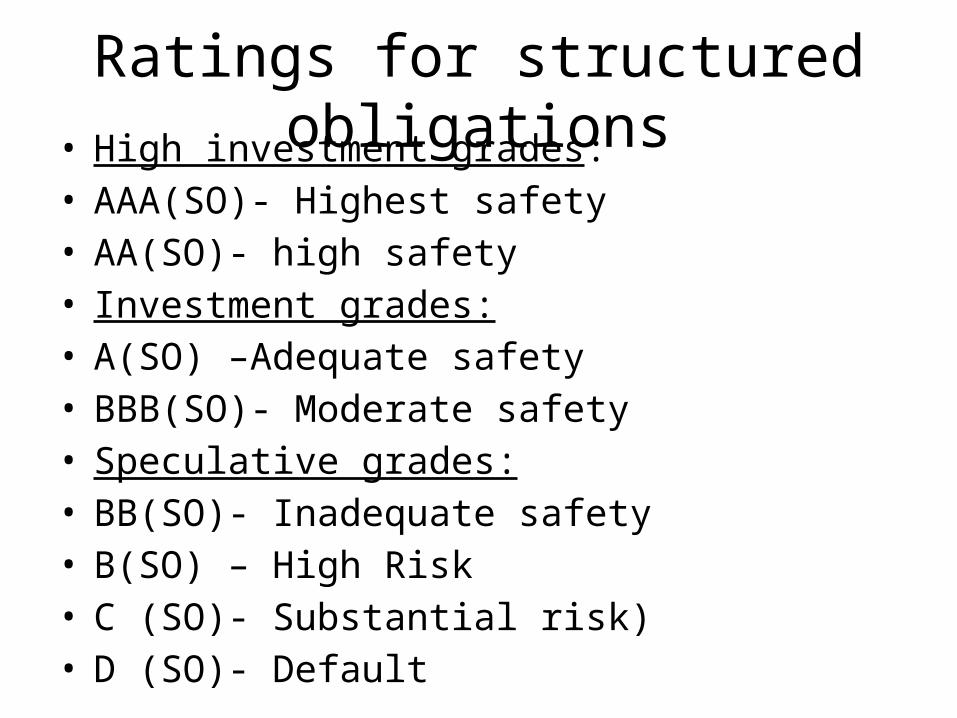

Ratings for structured obligations• High investment grades:• AAA(SO)- Highest safety• AA(SO)- high safety• Investment grades:• A(SO) –Adequate safety• BBB(SO)- Moderate safety• Speculative grades:• BB(SO)- Inadequate safety• B(SO) – High Risk• C (SO)- Substantial risk)• D (SO)- Default

Ratings for bond funds

• AAAf – Very Strong Protection against losses• AAf - Strong Protection against losses• Af- Adequate Protection against losses• BBBf- Moderate Protection against losses• BBf - Inadequate Protection against losses• Cf – vulnerable to credit defaults.

Bank Loan Ratings• BLR-1: strong likelihood of repayment of interest and

principal on bank loan • BLR-2: good likelihood of repayment of interest and

principal on bank loan • BLR-3: satisfactory likelihood of repayment of

interest and principal on bank loan • BLR-4: moderate likelihood of repayment of interest

and principal on bank loan • BLR-5: sub standard , vulnerable to loss• BLR-6: High likelihood of loss

Rating of collective investment schemes.

• GRADE I (high certainty of assured returns)• GRADE II (adequate certainty of assured

returns)• GRADE III (moderate certainty of assured

returns)• GRADE IV ( Inadequate certainty of assured

returns)• GRADE V (high uncertainty of assured returns)

Rating Fees

• Rating agencies charge 0.1 percent of instrument size as the rating fees

• Annual surveillance fees at rate of 0.03 percent to monitor the instrument during its life

THANK YOU

Related Documents