Mexico’s Unfulfilled Potential A Discussion of the Recent BIPP Study: Scenarios for Oil Supply, Demand and Net Exports for Mexico Kenneth B Medlock III, PhD James A Baker III and Susan G Baker Fellow in Energy and Resource Economics, and Senior Director, Center for Energy Studies, James A Baker III Institute for Public Policy Adjunct Professor, Department of Economics Rice University November 2, 2012 James A Baker III Institute for Public Policy Rice University Presentation to the Dallas Federal Reserve Branch Conference “Mexico: How to Tap Progress”

Mexico’s Unfulfilled Potential A Discussion of the Recent BIPP Study: Scenarios for Oil Supply, Demand and Net Exports for Mexico Kenneth B Medlock III,

Dec 23, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Mexico’s Unfulfilled PotentialA Discussion of the Recent BIPP Study:

Scenarios for Oil Supply, Demand and Net Exports for Mexico

Kenneth B Medlock III, PhDJames A Baker III and Susan G Baker Fellow in Energy and Resource

Economics, andSenior Director, Center for Energy Studies, James A Baker III Institute for

Public PolicyAdjunct Professor, Department of Economics

Rice UniversityNovember 2, 2012

James A Baker III Institute for Public PolicyRice University

Presentation to the Dallas Federal Reserve Branch

Conference “Mexico: How to Tap Progress”

Discussion Points

• Some basic points• Projections for oil demand, supply and net

exports• Implications of the story lines

• What needs to happen?• Can the course change?

• Broader developments in the global market• The role of unconventional resources• Where does Mexico fit?

2

On the Concepts of Resources and Production

• We generally define total resource as:– Ultimate = Produced + Proved + Potential (or Undiscovered)

• Thus, we can assess, albeit with uncertainty, the extent of the total technically recoverable resource.– Even this is insufficient because economic recoverability is

really the subset that matters, and even this is dynamic.• The ultimate scale of unconventional resources is still

a big unknown due to a relative lack of exploration– Uncertainty remains in the resource estimates for shale– Tight oil resources are becoming mainstream– Heavy oil from tar sands and oil shale

A note on what politics can mean for supply

• Geopolitics can present barriers to investment (risk premiums, limited access), effectively shrinking the size of the resource box (below).– Barriers to investment reduce the impact of exploration, limit the

ability to respond to higher long run prices, and limit the impact of innovation.

Price increase,Cost decrease

Exploration, Technological improvement

Proved Probable Possible

Sub-Economic Resource

Undiscovered Resource

Discovered/Identified Resource

Increasing Economic Viability

Increasing Geologic Uncertainty

Source: Modified from McKelvey, V.E., “Mineral Resource Estimates and Public Policy,” American Scientist, 1972

Geopolitics

Scenarios for Mexico’s Oil Demand, Supply and Net Exports

5

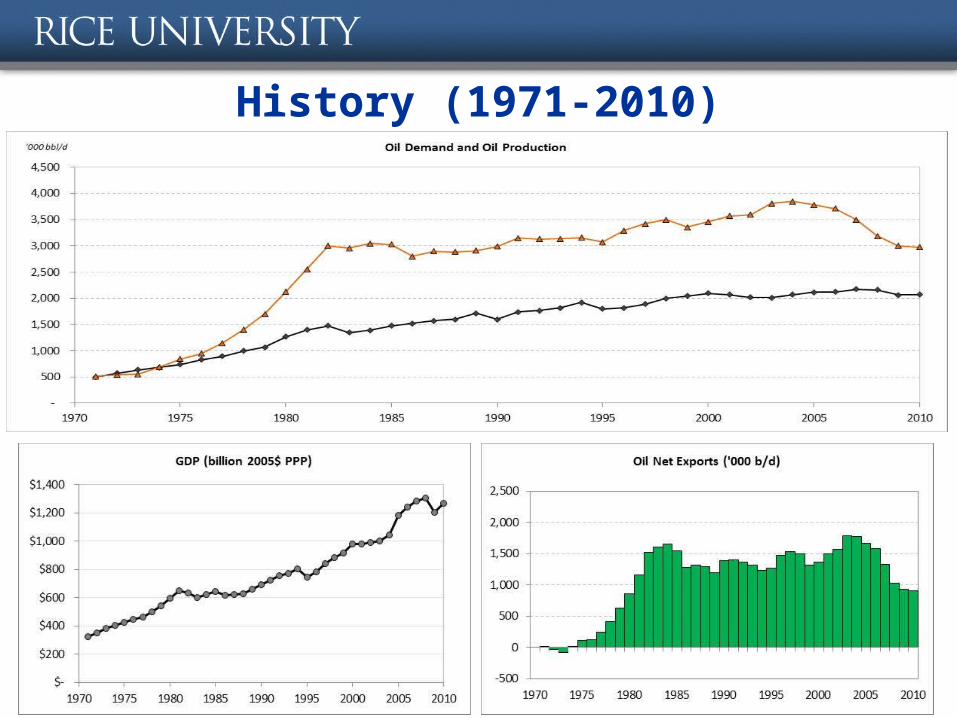

History (1971-2010)

Projection – Business as Usual• Business-as-usual

- GDPgr = 1.44%; POPgr= 0.44%; Poil,2040 = $90/bbl

- Resource = 29.83 billion bbls; Reserve replace = 0.83 billion bbls/y

• Mexico becomes net importer in 2027.

Projection – Alternate Assumptions • The result, however, is highly contingent on

- Reserve replacement (+); New discoveries, such as deep water (+)

- Domestic demand growth (-)

• Pictured: US-type reserve replacement with GoM Discovery

The Intersection of Market Structure

and Regulation:An Example – US Unconventional Oil

9

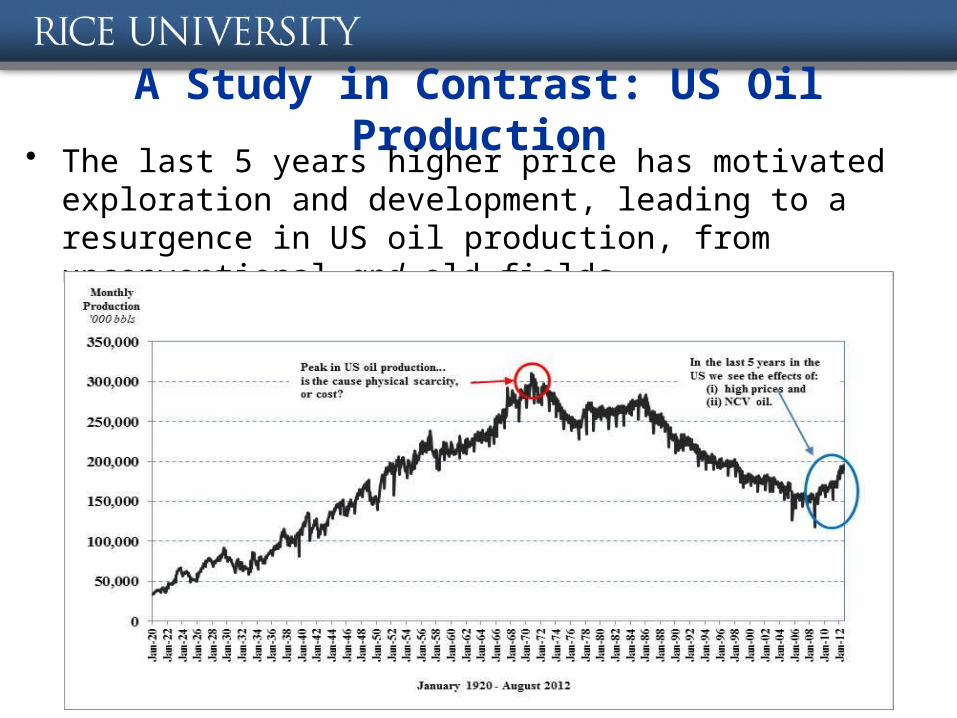

A Study in Contrast: US Oil Production• The last 5 years higher price has motivated

exploration and development, leading to a resurgence in US oil production, from unconventional and old fields.

Ongoing developments in US Tight Oil• Resource potential in US is distributed widely.

- For example, North Dakota (Bakken), Texas/New Mexico (Permian – Avalon, Bone Springs, Wolfcamp, South Texas – Eagleford), Ohio (Utica), Pennsylvania (Marcellus), Colorado/Wyoming (Niobrara), Florida (Sunniland), Louisiana (Tuscaloosa), Oklahoma (Mississippi Lime), California (Monterrey). o Not all shales are created equal, but the total technically

recoverable resource endowment may exceed 40 billion barrels.

o To date, activity in the Bakken and Eagleford accounts for most US tight oil production (about 680 thous b/d).

• Market structure and regulation facilitate entry my multiple firms and high efficiency.

11

The Potential for Change

12

Upstream Firm Efficiency: A Function of Operating Conditions

13

• Average revenue efficiency (pictured) for 2000-2009, sourced from Hartley and Medlock, 2012.

• Unlike most international majors, PEMEX is burdened by government objectives, which lowers estimated efficiency.

• Absent change, PEMEX is not likely to move to the frontier.

Questions/Comments

14

Related Documents