Metso Automation Metso Capital Markets Day 2005 Matti Kähkönen, President

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Metso Automation

Metso Capital Markets Day 2005Matti Kähkönen, President

2 © Metso Corporation 2005 Metso CMD 200531.8.2005

Forward looking statements

• It should be noted that certain statements herein which are not historical facts,including, without limitation, those regarding expectations for general economicdevelopment and the market situation, expectations for customer industryprofitability and investment willingness, expectations for company growth,development and profitability and the realization of synergy benefits and costsavings, and statements preceded by ”expects”, ”estimates”, ”forecasts” or similarexpressions, are forward-looking statements. These statements are based oncurrent decisions and plans and currently known factors. They involve risks anduncertainties which may cause the actual results to materially differ from the resultscurrently expected by the company.

• Such factors include, but are not limited to:(1) general economic conditions, including fluctuations in exchange rates andinterest levels which influence the operating environment and profitability ofcustomers and thereby the orders received by the company and their margins(2) the competitive situation, especially significant technological solutionsdeveloped by competitors(3) the company’s own operating conditions, such as the success of production,product development and project management and their continuous developmentand improvement(4) the success of pending and future acquisitions and restructuring.

Presentation content

Metso Automation todayRecent performanceCompetitive positionRoadmaps for growthSummary

Metso Automation today

5 © Metso Corporation 2005 Metso CMD 200531.8.2005

Metso Automation businesses

Pulp & Paper Energy & Process

Process automationand informationmanagement, specialityanalyzers andmeasurements, conditionmonitoring, qualitymeasurements, profilersand controls, machineand drive controls, valves

Process automationand informationmanagement and life cycleservices

Automated-, control-,ESD-, and manual valves,solutions and intelligentcondition monitoring

Valves

6 © Metso Corporation 2005 Metso CMD 200531.8.2005

Solutions from field systems to informationmanagement

Control andAutomated Valves

Quality Measurementsand ControlsProcess Automation

Systems

Transmitters(E+H) -Flowmeters

Analyzers

SpecialtyTransmitters

7 © Metso Corporation 2005 Metso CMD 200531.8.2005

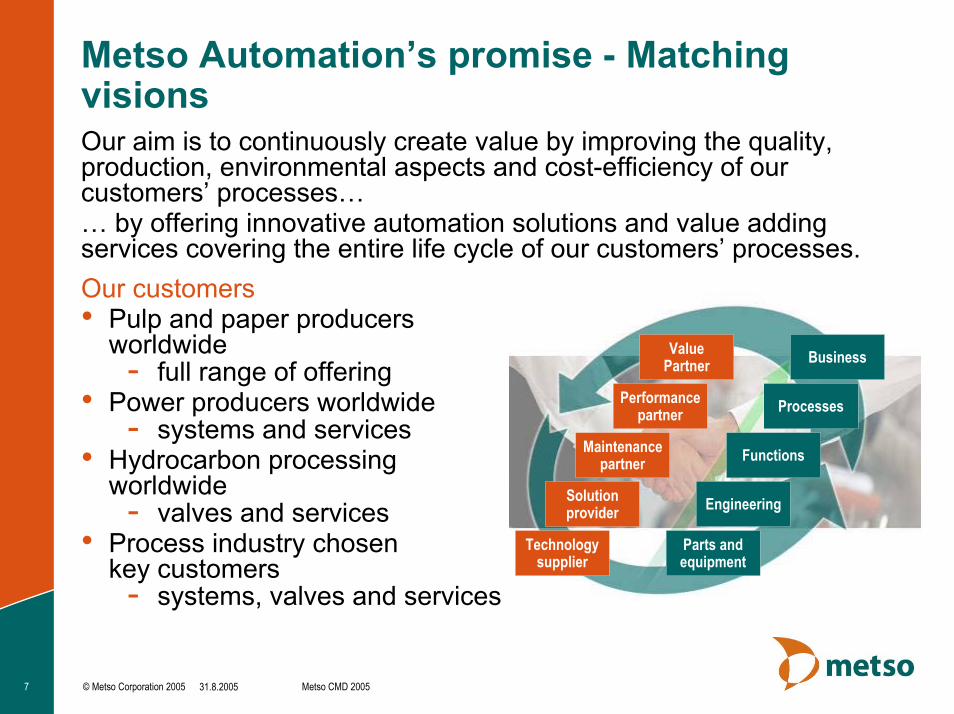

Metso Automation’s promise - MatchingvisionsOur aim is to continuously create value by improving the quality,production, environmental aspects and cost-efficiency of ourcustomers’ processes…… by offering innovative automation solutions and value addingservices covering the entire life cycle of our customers’ processes.Our customers• Pulp and paper producers

worldwide- full range of offering

• Power producers worldwide- systems and services

• Hydrocarbon processingworldwide- valves and services

• Process industry chosenkey customers- systems, valves and services

ValuePartner

Performancepartner

Maintenancepartner

Solutionprovider

Technologysupplier

Business

Processes

Functions

Engineering

Parts andequipment

8 © Metso Corporation 2005 Metso CMD 200531.8.2005

Management Agenda 2006-2008 in a nutshell

• Secure strong profitability- Continuous operational excellence improvement- Productivity programs

• Ensure 5-10% organic growth per annum- Organic growth programs based on the current business and

new products, service and business concept innovations• Strengthen market presence in emerging markets• Accelerate further growth

- Complementary acquisitions• Accelerate development of the Energy & Process business

- Focused investments and resources• Establish solid platform for future growth and new efficient

global business processes- E.g. new ERP system

Recent performance

10 © Metso Corporation 2005 Metso CMD 200531.8.2005

Highlights of recent activities and resultsachieved

• Restructuring measures completed; competitive coststructure

• Continuous improvement process established• Significant reduction of quality costs• Continuous reduction of net working capital

Profit making culture establishedGood basis for profitable growth

11 © Metso Corporation 2005 Metso CMD 200531.8.2005

0

200

400

600

800

1,000

1,200

2001 2002 2003 2004 1-6/050

2

4

6

8

10

12Net sales (MEUR) EBIT-%

Net salesEBIT-%

Financial performance

Net sales and EBIT-% Capital employed & ROCE-%

0

100

200

300

400

500

600

2001 2002 2003 2004 1-6/050

10

20

30

40

50

60

Capital employedROCE-%

Capital employed (MEUR) ROCE-%

EBIT-% bef. non-recurring items and goodwill amortizationNote: Figures for 2001-2003 according to FAS and as of 2004 IFRS2004 excl. reversal of Finnish pension liability

12 © Metso Corporation 2005 Metso CMD 200531.8.2005

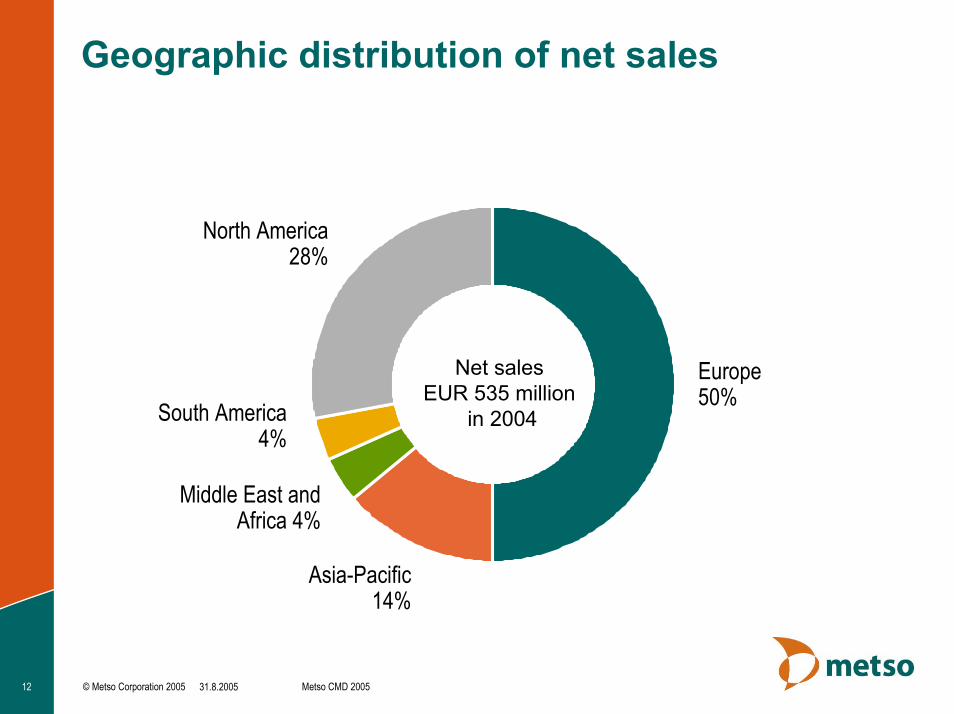

Geographic distribution of net sales

Europe50%

Asia-Pacific14%

Middle East andAfrica 4%

North America28%

South America4%

Net sales EUR 535 million

in 2004

13 © Metso Corporation 2005 Metso CMD 200531.8.2005

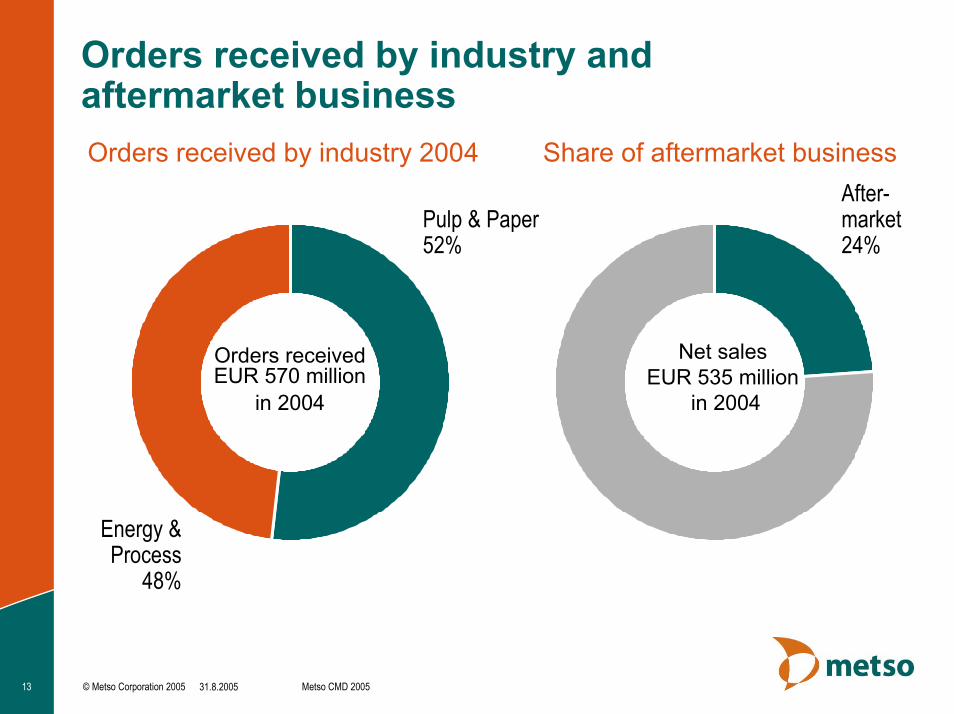

Orders received by industry andaftermarket businessOrders received by industry 2004 Share of aftermarket business

Orders receivedEUR 570 million

in 2004

After-market24%

Pulp & Paper52%

Energy &Process

48%

Net sales EUR 535 million

in 2004

Competitive position

15 © Metso Corporation 2005 Metso CMD 200531.8.2005

Metso Automation - Unique player

Pulp & Paper automation• The best and most unique pulp&paper automation offering in

the world.Valve business• Known for solid, reliable and state-of-the-art valves that

sustain performance with intelligent tools and solutions to getthe best out of customers’ flow controls.

Energy & Process systems• Industry expertise in Industrial boiler plants, Combined Heat

and Power plants (CHP) and Utility power plants. Potentialfor further leverage in emerging markets.

16 © Metso Corporation 2005 Metso CMD 200531.8.2005

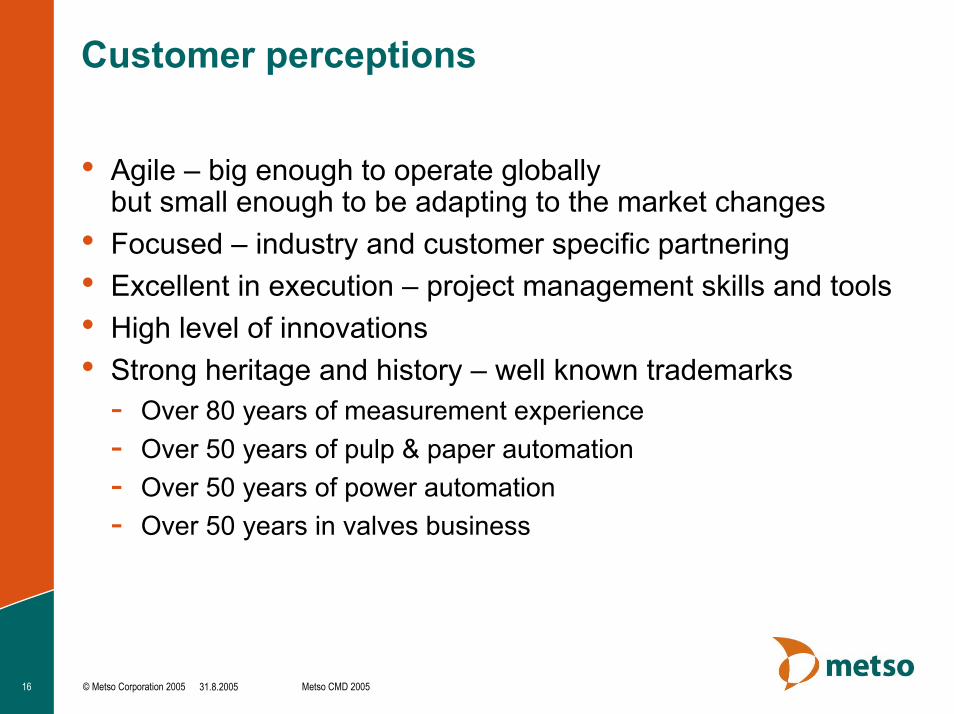

Customer perceptions

• Agile – big enough to operate globallybut small enough to be adapting to the market changes

• Focused – industry and customer specific partnering• Excellent in execution – project management skills and tools• High level of innovations• Strong heritage and history – well known trademarks

- Over 80 years of measurement experience- Over 50 years of pulp & paper automation- Over 50 years of power automation- Over 50 years in valves business

17 © Metso Corporation 2005 Metso CMD 200531.8.2005

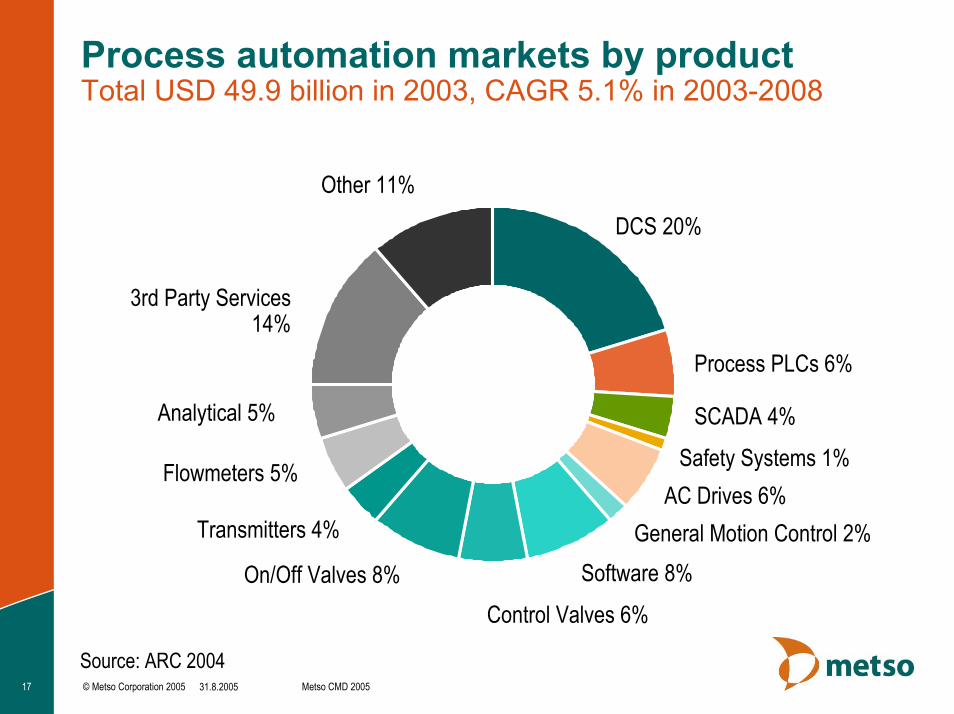

Process automation markets by productTotal USD 49.9 billion in 2003, CAGR 5.1% in 2003-2008

DCS 20%

Source: ARC 2004

Process PLCs 6%

SCADA 4%Safety Systems 1%

AC Drives 6%General Motion Control 2%

Software 8%Control Valves 6%

On/Off Valves 8%

Transmitters 4%

Flowmeters 5%

Analytical 5%

3rd Party Services14%

Other 11%

18 © Metso Corporation 2005 Metso CMD 200531.8.2005

Process automation business by industry

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Power Oil&G EP Pulp &Paper

Chemical Refining Pharma-ceutical

Water &Waste

Food &Beverage

Metals &Mining

Other

2003 2008e % CAGR

Source: ARC 2004

+4.4%

+4.5%

+2.3%+5.2%

+4.8%+8.1%

+7.1%

+6.8%

+4.1%

+4.1%

USD million

19 © Metso Corporation 2005 Metso CMD 200531.8.2005

Markets for Metso Automation

Pulp & Paper Energy & Process

Market size:EUR 3.7 billionTarget market:EUR 2 billionMarket growth: 3.0%Net sales: EUR 300million*Competition: ABB,Honeywell

Market size:EUR 7.1 billionTarget market:EUR 2.2 billionMarket growth: 3.8%Net sales: EUR 60 millionCompetition: ABB, Siemens,Emerson, Invensys,Honeywell, Yokogawa

Market size:EUR 17.3 billionTarget market:EUR 5.7 billionMarket growth: 3.2%Net sales: EUR 270 millionCompetition: Emerson,Flowserve, Dresser,Samson

Valves

*Includes valves

20 © Metso Corporation 2005 Metso CMD 200531.8.2005

Process automation to pulp & paper industryCAGR 2.3 % in 2003-2008

DCS 27%

Source: ARC 2004, Metso

Process PLCs 5%

AC Drives 9%

Software Products 8% (MES etc.)

Control Valves6%

On/Off Valves 12%

Transmitters 4% (pressure, level, temp)

Flow 5%

Analytical 5%(online&offline)

3rd Party Services8%

Other 11%

ConsistencyTransmitters 1%

21 © Metso Corporation 2005 Metso CMD 200531.8.2005

Global industrial valve marketTotal USD 20,251 million in 2003, CAGR 3.7% in 2003-2006

Oil & Gas16.5%

Other industries37.4%

Water & Sewerage16.0%

Chemicals and Paper18.8%

Source: EIF 2002

Power generation11.3%

22 © Metso Corporation 2005 Metso CMD 200531.8.2005

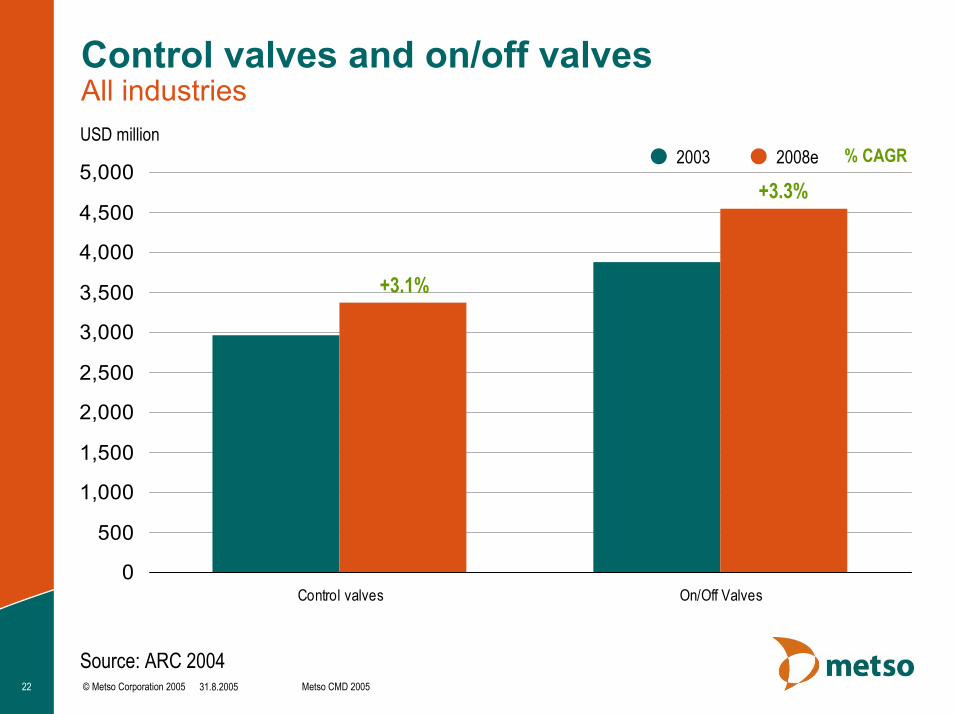

Control valves and on/off valvesAll industries

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Control valves On/Off Valves

2003 2008e % CAGR

Source: ARC 2004

+3.3%

+3.1%

USD million

23 © Metso Corporation 2005 Metso CMD 200531.8.2005

Global markets for distributed controlsystems by industry Total CAGR 3.7%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Power P&P Oil&Gas Chemical Refining Pharma-ceutical

Water &Waste

Metals &Mining

Food &Beverage

Cement &Glass

Other

2003 2008e % CAGR

Source: ARC 2004

+3.8%

+3.8%

+3.8%

+3.8%

+3.5%+4.6%

+3.9% +2.7%+2.8%

+1.6%

USD billion

+5.1%

Roadmaps for growth

25 © Metso Corporation 2005 Metso CMD 200531.8.2005

Building-Controlled risk

Leveraging-Controlled risk

Existing business-”Easiest” growth

Transformation-High risk

Framework for organic growth andcomplementary acquisitions

Distinctive competencies

Mark

ets

Source: IMD

In place Need to add

Est

ablis

hed

New

Build

ing

Leveraging

26 © Metso Corporation 2005 Metso CMD 200531.8.2005

The cornerstones for profitable growth

• Competitive cost structure• Customer and industry focus to add value and provide

results and intelligent reliability - unique value proposition• Emerging markets

- Asia-Pacific- Russia- Latin America

• Continuous high investment level into new products andtechnology

• Installed base markets, new services• Complementary acquisitions

27 © Metso Corporation 2005 Metso CMD 200531.8.2005

Pulp & paper – Strengths

• Customer knowledge• Process, automation and machinery know-how, strong

product portfolio• Unified automation network approach• Good reputation and image as a reliable partner• Execution of large scale projects• Global flexible team of experts• Metso, Kajaani, Neles, PaperIQ, Sensodec and Jamesbury

trademarks

28 © Metso Corporation 2005 Metso CMD 200531.8.2005

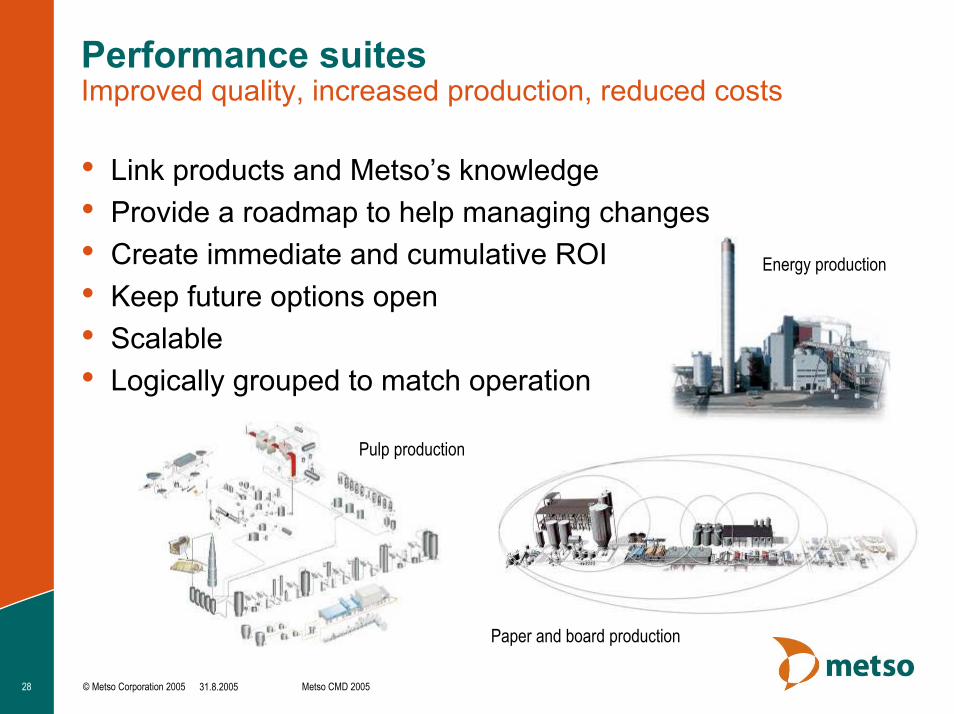

• Link products and Metso’s knowledge• Provide a roadmap to help managing changes• Create immediate and cumulative ROI• Keep future options open• Scalable• Logically grouped to match operation

Performance suitesImproved quality, increased production, reduced costs

Pulp production

Energy production

Paper and board production

29 © Metso Corporation 2005 Metso CMD 200531.8.2005

Case: WISA800: The world'slargest single-line recoveryline

• Metso Automation has suppliedcomplete automation andoptimization for- Recovery boiler and

turbogenerator- New evaporation plant- Tall oil plant- Causticising department- Lime kiln- Upgrade and extension

for the existing fiber line

30 © Metso Corporation 2005 Metso CMD 200531.8.2005

Pulp & paper – Markettrends

• In Europe upgrades for large existingproduction capacity.

• Bigger share of virgin fibers from LatinAmerica.

• Continuous growth of Asia-Pacificpaper production.

• North America will utilize mostlyexisting machines; investmentsoutside North America.

• Capital expenditure down.• Demand for high return investments

increasing.• Importance of automation increasing.• Maintenance outsourcing.

31 © Metso Corporation 2005 Metso CMD 200531.8.2005

Pulp & paper – Growth opportunitiesand actions

• Ageing installed base in North America and Europe- Optimization, performance and life cycle services- Utilize full scope of our offering- Upgrade programs and Metso rebuilds

• Emerging markets- China, Russia, Brazil- Strengthen local resources in sales, service and projects- Metso packages in new machines

• New products and services- Advanced analyzers and sensors- Predictive maintenance and availability services

• One totally open and scalable platform- Embedded automation solutions- Integrate operations and maintenance

32 © Metso Corporation 2005 Metso CMD 200531.8.2005

Valves – Strengths

• Our customers are world leaders - Shell, BP, UPM,SaudiAramco, APP, IP, Technip, Chiyoda etc.

• Global, flexible sales & service and supply chain network• Huge installed base - deliveries since 1950’s• New intelligent products for condition monitoring and

information management• High-end and demanding application technology

33 © Metso Corporation 2005 Metso CMD 200531.8.2005

Case: Shell Nanhai, China

• Annual production of 2.3 million tonsincluding glycols, polyolefins, LDPE,HDPE, PP and MPG

• CNOOC and SHELL joint venturein Guangdong, China

• 3,500 pcs Neles ND9000® intelligentFOUNDATION Fieldbus valvecontrollers

• 3,000 pcs Neles rotary control valves• 1,000 Jamesbury automated and

manual valves• Large installation of Finetrol™ and

ball segment valves• 150 pcs Neles ValvGuard™,

TÜV approved safety devices• Local Metso Automation service

personnel

34 © Metso Corporation 2005 Metso CMD 200531.8.2005

Valves – Market trends

• Global valve markets in energy and hydrocarbon growing.• Global valve industry still fragmented.• Major customers moving production to low cost locations in

Eastern Europe, Latin America and Asia.• High demand for oil and gas products keeps exploration and

production investments high.• Focus on providing additional ancillary services, such as

valve maintenance and repair.• New intelligent monitoring technology.

35 © Metso Corporation 2005 Metso CMD 200531.8.2005

Valves – Growth opportunitiesand actions• Valve business still fragmented

- Active player in industry consolidation• Valves an integral part of our offering

in pulp & paper- One-stop-shop approach and higher service levels

• New products and new applications- Condition monitoring and asset management- Strengthen portfolio by RTD

• Emerging markets- Local assembly and service capabilities- New energy sources - Hydrogen

• Strong key account focus- TOP20 program

• Open architecture- Integrate to any control system

36 © Metso Corporation 2005 Metso CMD 200531.8.2005

Energy & process – Strengths

• Process and application knowledge- Industral boilers, CHP, coal fired,biofuel, waste to energy

• Best experts in pulp & paperpower plants

• Same technology platformas in pulp & paper- Distributed control systems volume

higher in energy & processthan in pulp & paper

• Customer centric focus• Good reference base in India

and China• Execution of large scale projects• Life cycle concept

37 © Metso Corporation 2005 Metso CMD 200531.8.2005

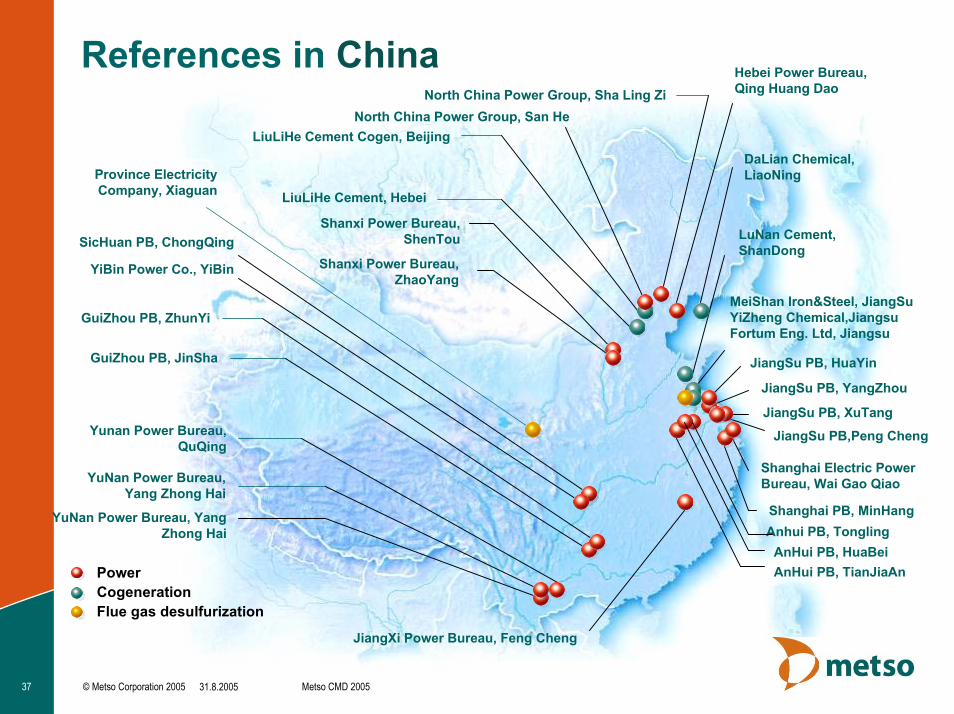

AnHui PB, TianJiaAn

LiuLiHe Cement Cogen, Beijing

LiuLiHe Cement, Hebei

AnHui PB, HuaBei

MeiShan Iron&Steel, JiangSuYiZheng Chemical,JiangsuFortum Eng. Ltd, Jiangsu

LuNan Cement,ShanDong

DaLian Chemical,LiaoNingProvince Electricity

Company, Xiaguan

Anhui PB, Tongling

Hebei Power Bureau,Qing Huang Dao

JiangXi Power Bureau, Feng Cheng

Shanxi Power Bureau,ShenTou

North China Power Group, San HeNorth China Power Group, Sha Ling Zi

GuiZhou PB, JinSha

GuiZhou PB, ZhunYi

JiangSu PB, HuaYin

JiangSu PB, XuTang

JiangSu PB, YangZhou

JiangSu PB,Peng Cheng

Shanghai PB, MinHang

SicHuan PB, ChongQing

YiBin Power Co., YiBin

Yunan Power Bureau,QuQing

Shanghai Electric PowerBureau, Wai Gao QiaoYuNan Power Bureau,

Yang Zhong Hai

Shanxi Power Bureau,ZhaoYang

YuNan Power Bureau, YangZhong Hai

Energy Autom

ation

References in China

PowerCogenerationFlue gas desulfurization

38 © Metso Corporation 2005 Metso CMD 200531.8.2005

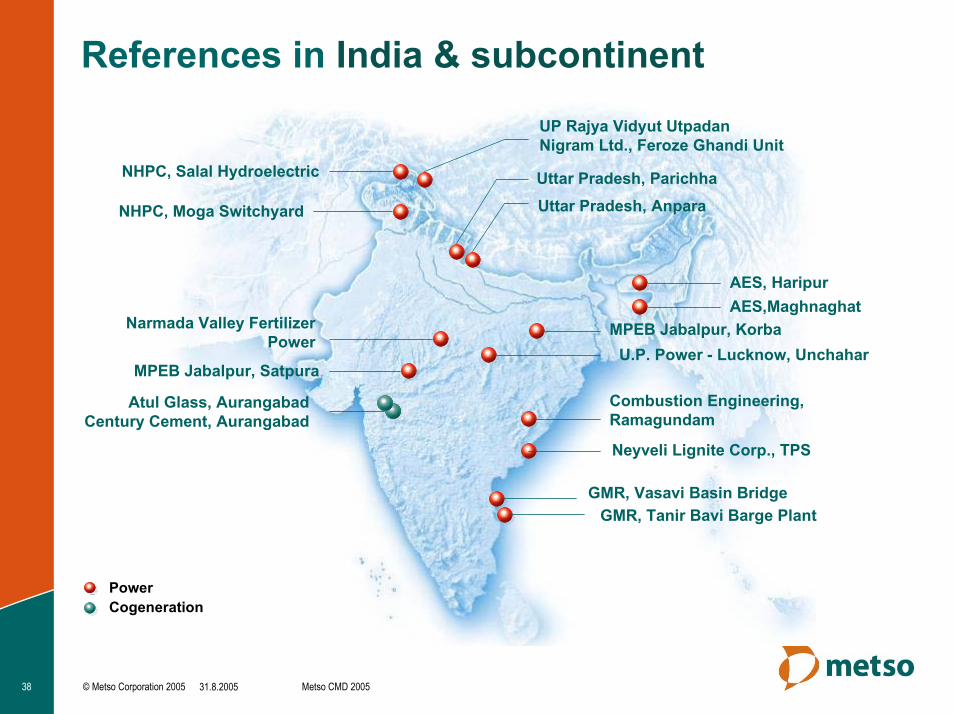

References in India & subcontinent

Atul Glass, AurangabadCentury Cement, Aurangabad

Combustion Engineering,Ramagundam

NHPC, Salal Hydroelectric

MPEB Jabalpur, Korba

MPEB Jabalpur, Satpura

NHPC, Moga Switchyard Uttar Pradesh, AnparaUttar Pradesh, Parichha

UP Rajya Vidyut UtpadanNigram Ltd., Feroze Ghandi Unit

Narmada Valley FertilizerPower

Neyveli Lignite Corp., TPS

U.P. Power - Lucknow, Unchahar

GMR, Vasavi Basin Bridge

AES, HaripurAES,Maghnaghat

GMR, Tanir Bavi Barge Plant

PowerCogeneration

39 © Metso Corporation 2005 Metso CMD 200531.8.2005

Energy & process– Market trends

• Global, deregulation, open competitionand privatization

• Increased price of gas and oil improvingthe outlook for coal-fired power plants

• Environmental regulations willpromote waste to energy power plants

• Rapidly growing markets in China, Indiaand the rest of Asia, market growth alsoin Russia and Latin America

• Continuous high profitability forecast• Continuous outsourcing

40 © Metso Corporation 2005 Metso CMD 200531.8.2005

Energy & process – Growthopportunities and actions

• Expansion to emerging markets- Geographical - China, Russia,

India, Brazil- Pulp & paper power plants- Localization- Increase industry specific

competencies- Partnerships and potential acquisitions

• Expand with our existing customers- Customer relationship management- Life cycle services- New products and services

• Plant management and optimizationapplications- Use as differentiation factor

• Environmental applications- Tools for environmental reporting

Summary

42 © Metso Corporation 2005 Metso CMD 200531.8.2005

Summary

• Restructuring measures completed; competitive coststructure.

• Maintain sustainable, strong profit level through continuousproductivity improvement.

• Ensure 5-10% organic growth per annum.• Customer and industry focus.• Complementary acquisitions.• Strengthen market presence in emerging markets.• Energy & process share of total business volume to

grow faster than in pulp & paper.

Related Documents