08 Steven A. Kandarian Executive Vice President & Chief Investment Officer

metlife Investor Day 2008 Investments

Jul 27, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

08

Steven A. Kandarian

Executive Vice President &Chief Investment Officer

2

Defensively Positioned for Current Environment

• Identified weaknesses in certain asset sectors early and took action

• Repositioned portfolio for recession beginning in 2007

• Reduced balance sheet leverage and increased liquidity

08

Market Overview

4

2009 Market View and Themes

Fundamentals deteriorateCreditCredit

Fundamentals deteriorateReal EstateReal Estate

Rates remain lowFedFed

Contained, talk of deflationInflationInflation

Global recessionEconomyEconomy

Well ahead of fundamentalsSpreadsSpreads

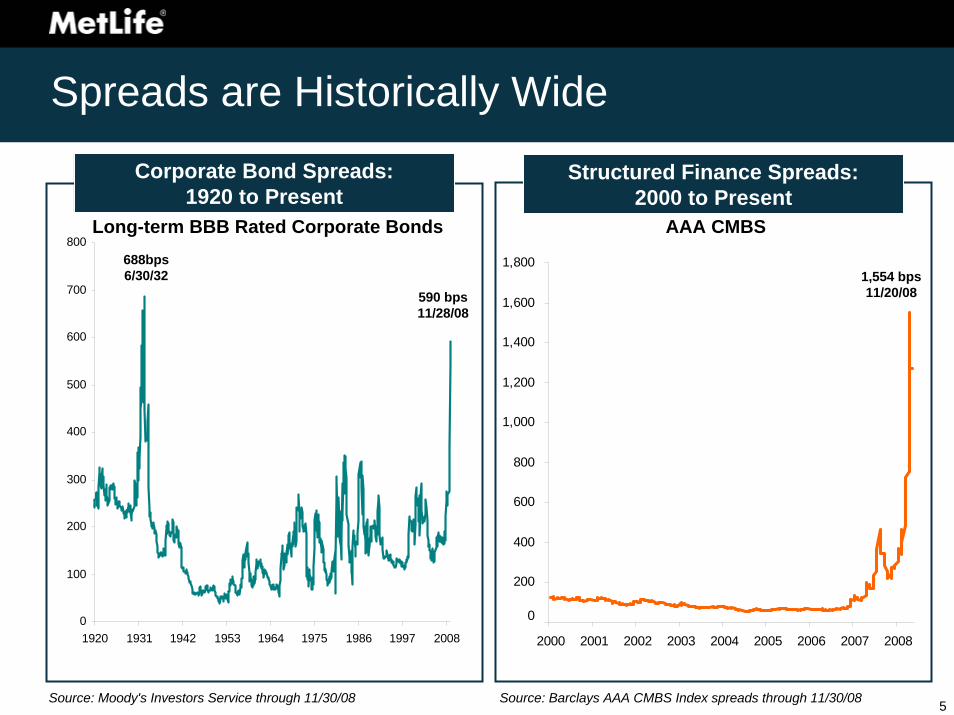

5

0

100

200

300

400

500

600

700

800

1920 1931 1942 1953 1964 1975 1986 1997 2008

Source: Moody's Investors Service through 11/30/08

AAA CMBS

590 bps11/28/08

688bps6/30/32 1,554 bps

11/20/08

Spreads are Historically Wide

Corporate Bond Spreads:1920 to Present

Structured Finance Spreads:2000 to Present

Long-term BBB Rated Corporate Bonds

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2000 2001 2002 2003 2004 2005 2006 2007 2008

0

Source: Barclays AAA CMBS Index spreads through 11/30/08

6

High Yield Spreads and Default Rates Delinked

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

1987 1990 1993 1996 1999 2002 2005 20080

250

500

750

1000

1250

1500

1750

2000

Moody's U.S. Speculative Grade Default Rates

Barclays U.S. Corporate High Yield

Spread over Treasuries(bps)

Spreads through 11/30/08; Default Rate through 10/31/08

Trai

ling

12-m

onth

Def

ault

Rat

e (%

)

The Credit Cycle

08

Portfolio Income

8

$0

$300

$600

$900

$1,200

$1,500

$1,800

$2,100

2003 2004 2005 2006 2007 2008E*2009P

• Alternative Investments– Corporate Joint Ventures– Hedge Funds

• Real Estate Development Joint Ventures and Funds

• Prepayments– Corporate Bond

Prepayments– Commercial Mortgage

Prepayments

• Securities Lending

2009 Plan Variable Income $150 Million per Quarter / $600 Million for Year

Annual Variable Net Investment Income ($ Millions)

*Mid-point of 2008E range between $700 - $810 million

9

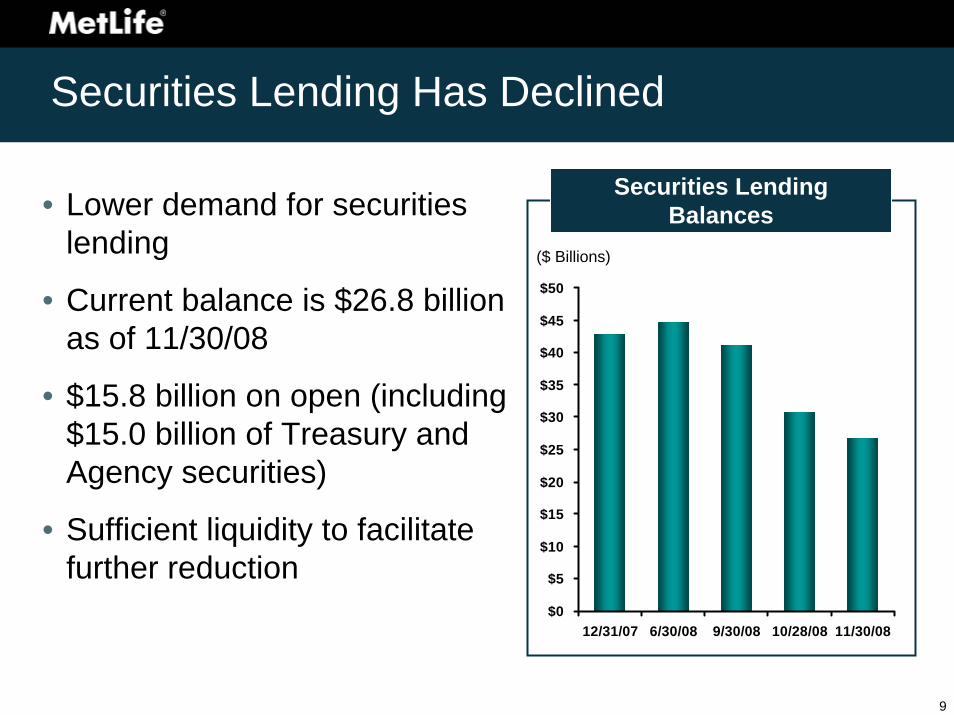

Securities Lending Has Declined

• Lower demand for securities lending

• Current balance is $26.8 billion as of 11/30/08

• $15.8 billion on open (including $15.0 billion of Treasury and Agency securities)

• Sufficient liquidity to facilitate further reduction

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

$50

12/31/07 6/30/08 9/30/08 10/28/08 11/30/08

Securities LendingBalances

($ Billions)

10

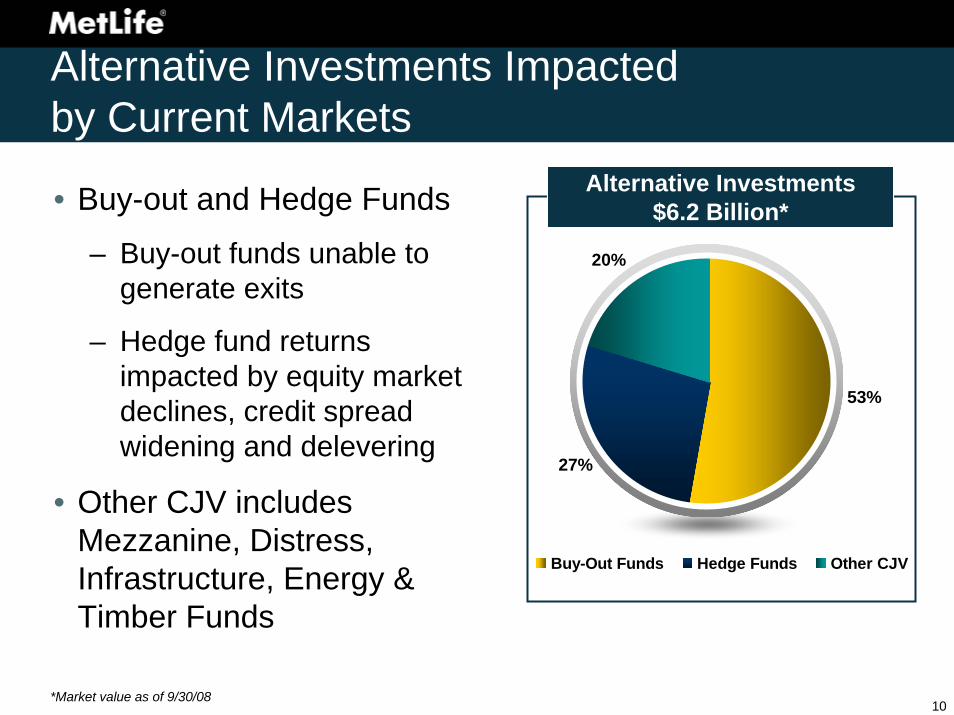

Alternative Investments Impactedby Current Markets

• Buy-out and Hedge Funds

– Buy-out funds unable to generate exits

– Hedge fund returns impacted by equity market declines, credit spread widening and delevering

• Other CJV includes Mezzanine, Distress, Infrastructure, Energy & Timber Funds

53%

27%

20%

Buy-Out Funds Hedge Funds Other CJV

Alternative Investments $6.2 Billion*

*Market value as of 9/30/08

08

Portfolio Overview

12

• Total Portfolio:ᅳ Diversified portfolio across

many sectors

• Liability Driven:ᅳ Asset-liability management

• Team Investment Approach:ᅳ 600+ investment and support

professionals

• Risk Management:ᅳ Part of our culture

MetLife Investments

34.9%

24.8%

16.0%

5.4%

3.2%

3.6%

4.6%

7.5%

*Market value as of 9/30/08

$305.2 Billion of Managed Assets*

Investment Grade Corporate BondsStructured FinanceCommercial and Agricultural MortgagesCash and Short-Term

US Treasury/AgencyBelow Investment Grade CreditReal Estate EquityCorporate Equity

13

Proactively Repositioned Portfolio

U.S. Treasury/Agency 6.9% 5.4%Structured Finance

Residential MBS (RMBS) 18.2% 15.4%Commercial MBS (CMBS) 6.1% 5.2%Asset Backed Securities (ABS) 3.6% 4.2%Total Structured Finance 27.9% 24.8%

Credit'A' or Better Corporates 20.9% 21.2%'BBB' Corporates 15.0% 13.6%Below Invest. Grade Credit 5.7% 4.6%Total Credit 41.6% 39.4%

Real EstateCommercial Mortgages 10.6% 12.0%Agricultural Mortgages 3.2% 4.1%Real Estate Equity 3.2% 3.6%Total Real Estate 17.0% 19.7%

Corporate Equity 3.6% 3.2%Cash & Short-Term 3.0% 7.5%

Total Managed Assets 100.0% 100.0%Market Value of Managed Assets ($ Billions) $318.8 $305.2

MetLife Portfolio Allocation Trend September 30, 2007 September 30, 2008

14

High Quality Structured Finance Portfolio

• $75.7 billion*

• Collateral characteristics and tranche selection is critical

• Less than $200 million of below investment grade structured finance

*Market value as of 9/30/08

09/30/07 09/30/08

RMBS CMBS ABS

Structured Financeas a % of Managed Assets

$88.8B $75.7B

3.6%6.1%

18.2% 15.4%

5.2%4.2%

24.8%27.9%

15

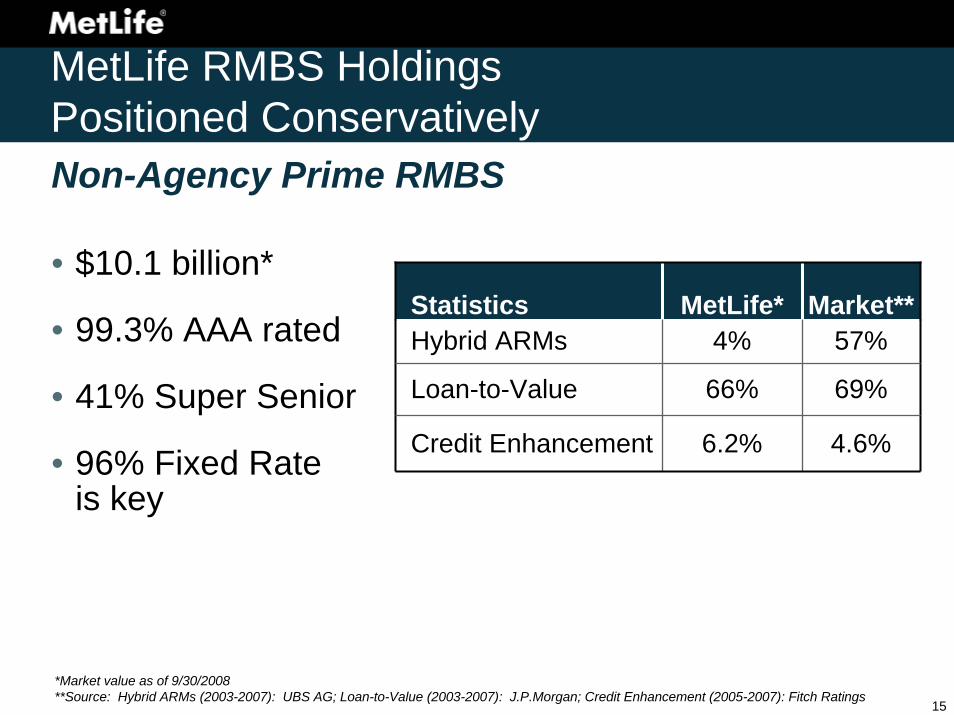

MetLife RMBS HoldingsPositioned Conservatively

• $10.1 billion*

• 99.3% AAA rated

• 41% Super Senior

• 96% Fixed Rate is key

*Market value as of 9/30/2008**Source: Hybrid ARMs (2003-2007): UBS AG; Loan-to-Value (2003-2007): J.P.Morgan; Credit Enhancement (2005-2007): Fitch Ratings

Statistics MetLife* Market**Hybrid ARMs 4% 57%

Loan-to-Value 66% 69%

Credit Enhancement 6.2% 4.6%

Non-Agency Prime RMBS

16

0%

1%

2%

3%

4%

5%

6%

7%

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29

Non-Agency Prime RMBSMetLife versus MarketBetter collateral results in better performance

Market C/E*

Market 60+ DQ60+D

Q o

r C/E

Lev

el

Loan Age in Months*Credit Enhancement as of 9/30/08Source: Intex; Data as of 9/30/08; Delinquencies weighted by Loan Age, 05-07

Credit Enhancement & Delinquencies

17

0%

1%

2%

3%

4%

5%

6%

7%

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29

MET 60+ DQ

Better collateral results in better performance

MET C/E*

Market C/E*

Market 60+ DQ60+D

Q o

r C/E

Lev

el

Loan Age in Months*Credit Enhancement as of 9/30/08Source: Intex; Data as of 9/30/08; Delinquencies weighted by Loan Age, 05-07

Non-Agency Prime RMBSMetLife versus Market

Credit Enhancement & Delinquencies

18

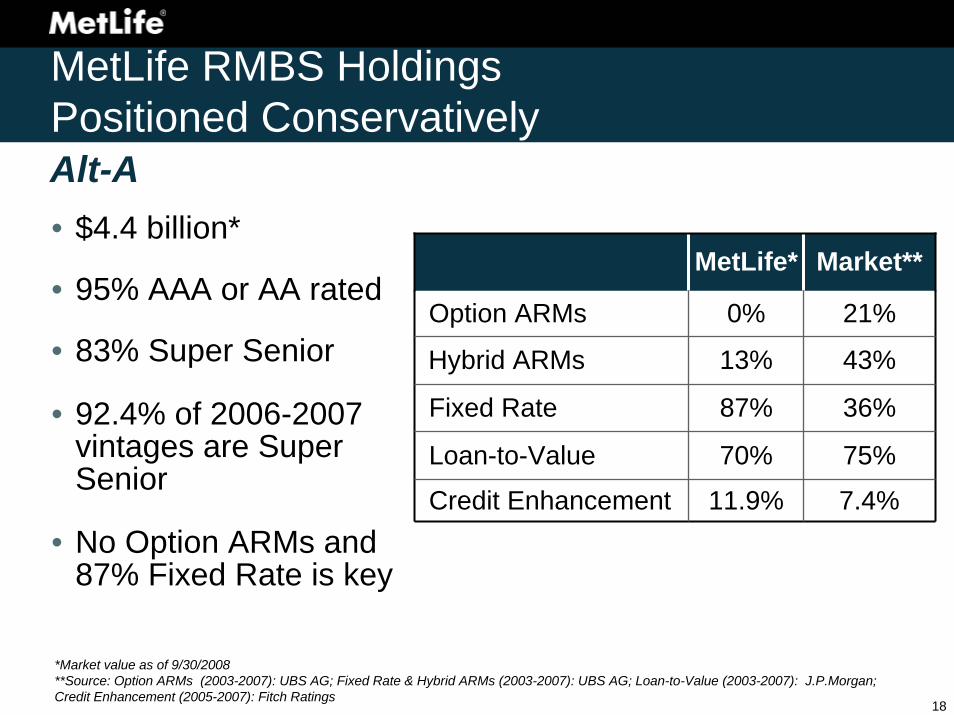

MetLife RMBS HoldingsPositioned Conservatively

• $4.4 billion*

• 95% AAA or AA rated

• 83% Super Senior

• 92.4% of 2006-2007 vintages are Super Senior

• No Option ARMs and 87% Fixed Rate is key

MetLife* Market**

Option ARMs 0% 21%

Hybrid ARMs 13% 43%

Fixed Rate 87% 36%

Loan-to-Value 70% 75%

Credit Enhancement 11.9% 7.4%

Alt-A

*Market value as of 9/30/2008**Source: Option ARMs (2003-2007): UBS AG; Fixed Rate & Hybrid ARMs (2003-2007): UBS AG; Loan-to-Value (2003-2007): J.P.Morgan;Credit Enhancement (2005-2007): Fitch Ratings

19

Alt-A RMBSMetLife versus Market Better collateral results in better performance

Market C/E*

Market 60+ DQ

0%

2%

4%

6%

8%

10%

12%

14%

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29

60+D

Q o

r C/E

Lev

el

Loan Age in Months*Credit Enhancement as of 9/30/08Source: Intex; Data as of 9/30/08; Delinquencies weighted by Loan Age, 05-07

Credit Enhancement & Delinquencies

20

Alt-A RMBSMetLife versus Market Better collateral results in better performance

MET C/E*

Market C/E*

Market 60+ DQ

MET 60+ DQ60+D

Q o

r C/E

Lev

el

0%

2%

4%

6%

8%

10%

12%

14%

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29Loan Age in Months

*Credit Enhancement as of 9/30/08Source: Intex; Data as of 9/30/08; Delinquencies weighted by Loan Age, 05-07

Credit Enhancement & Delinquencies

21

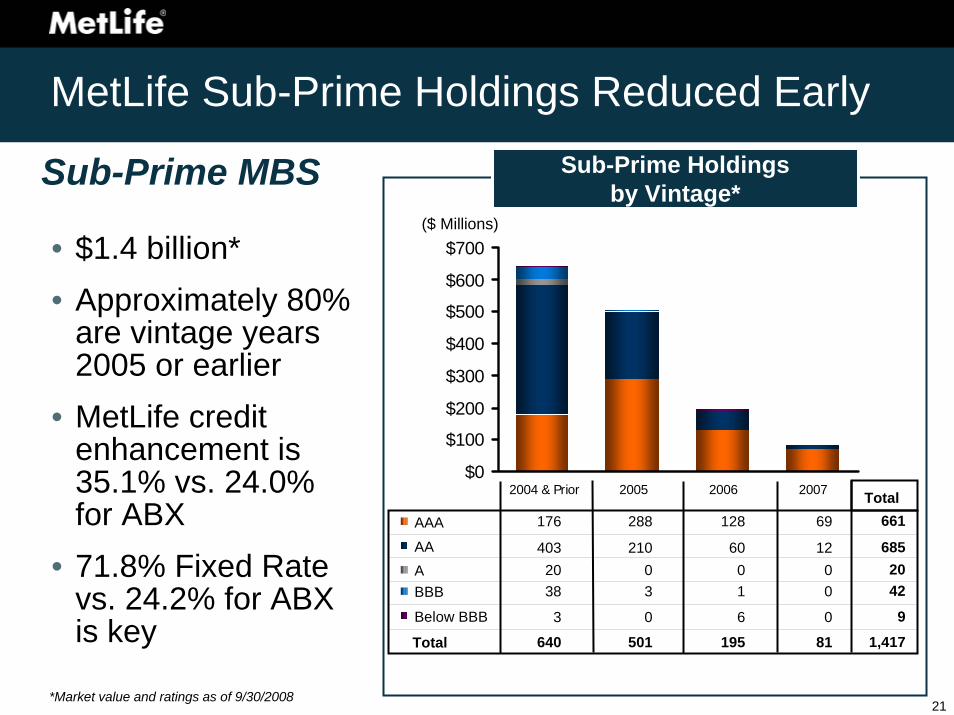

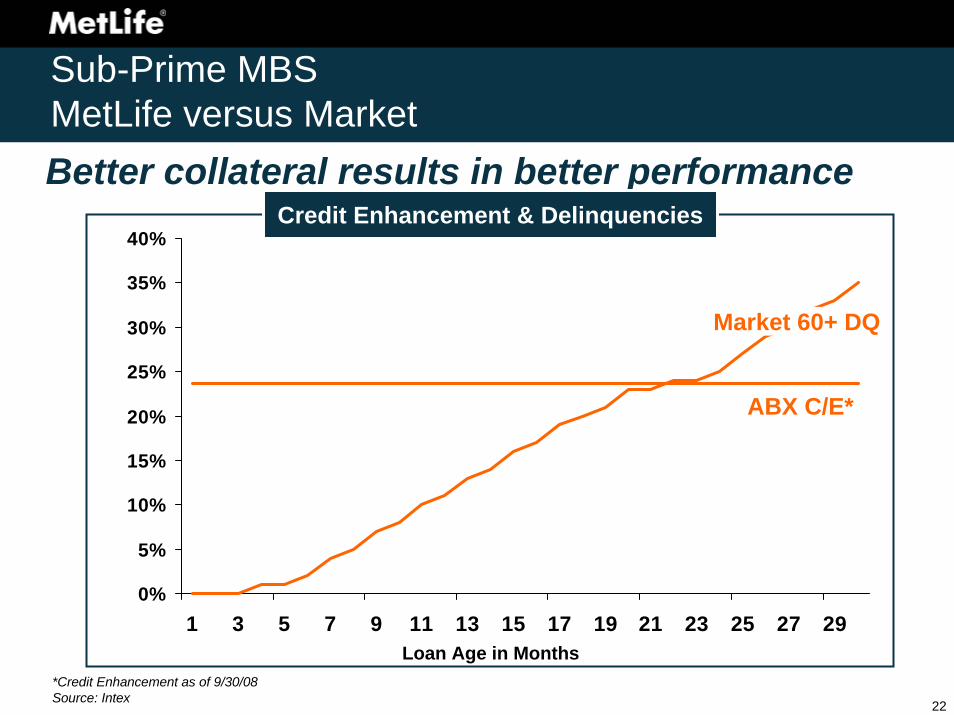

MetLife Sub-Prime Holdings Reduced Early

• $1.4 billion* • Approximately 80%

are vintage years 2005 or earlier

• MetLife credit enhancement is 35.1% vs. 24.0% for ABX

• 71.8% Fixed Rate vs. 24.2% for ABX is key

Sub-Prime MBS

*Market value and ratings as of 9/30/2008

Below BBB 3 0 6 0

BBB 38 3 1 0A 20 0 0 0AA 403 210 60 12

AAA 176 288 128 69

9

4220

685

661Total

Total 640 501 195 81 1,417

$0

$100

$200

$300

$400

$500

$600

$700

2004 & Prior 2005 2006 2007

Sub-Prime Holdingsby Vintage*

($ Millions)

22

Sub-Prime MBSMetLife versus Market

*Credit Enhancement as of 9/30/08Source: Intex

Better collateral results in better performance

0%

5%

10%

15%

20%

25%

30%

35%

40%

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29Loan Age in Months

ABX C/E*

Market 60+ DQ

Credit Enhancement & Delinquencies

23

Sub-Prime MBSMetLife versus MarketBetter collateral results in better performance

0%

5%

10%

15%

20%

25%

30%

35%

40%

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29Loan Age in Months

MET C/E*

MET 60+ DQ

*Credit Enhancement as of 9/30/08Source: Intex

Credit Enhancement & Delinquencies

ABX C/E*

Market 60+ DQ

24

MetLife’s CMBS Positioned for Downturn

• $15.9 billion*• 24% average credit

enhancement for conduits• Can withstand 3 times

historical maximum loss• No exposure to CMBX • Only $139 million in CRE

CDOs

92%

1% 1% 6%

ConduitSingle Asset/Large LoanCRE CDOOther

CMBS Holdings by Type

*Market value as of 9/30/08

25

Seasoned, High Quality CMBS Holdings

• 78% from 2005 and prior vintages vs. 50% of the market

• 90% of 2006-2007 vintages are Super Senior and Senior AAA

CMBS Holdingsby Vintage*

Below BBB 99 24 7 0

BBB 61 3 84 9A 326 29 29 32AA 619 137 85 45

AAA 7,856 3,260 2,101 1,098

*Market value as of 9/30/08

130

157416886

14,316Total

Total 8,961 3,453 2,306 1,184 15,9050

000

1

1

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2004 andPrior

2005 2006 2007 2008

($ Millions)

26

CMBS Price Does Not Convey Full Story

• Fundamental analysis of bond characteristics is key

• Focus on the details

MetLife Bond*

Market Bond*

Price $66 $67

Rating Senior AAA

Senior AAA

Interest Only Loans 39.2% 80.4%Loans on Servicer Watch List 6.4% 49.9%

Vintage 2007 2007

MetLife’s Projections:

Expected Coverage 4.8x 1.7x

*As of 10/31/08

27

Reduced Risk in Credit Portfolio

• $120.3 billion*

• Decreased ‘BBB’ and Below Investment Grade exposure

• Approximately 29% private placements 20.9% 21.2%

15.0% 13.6%

5.7% 4.6%

9/30/2007 9/30/2008

AAA/AA/A BBBBelow Inv Grade

Corporate Creditas a % of Managed Assets

41.6% 39.4%

$132.6B $120.3B

*Market value as of 9/30/08

28

Positioned for Recession

• Began to reposition portfolio for potential recession in 2007

• Actively identified, then sold vulnerable securities, loans and mortgages

• Since October 2007, sold$7.2 billion of assets we believed were vulnerablein a recession

SectorBook Value ($ Millions)

Investment Grade $4,093

Below Investment Grade $2,620

Commercial Mortgages $524

Total $7,237

Vulnerable Assets Sold

29

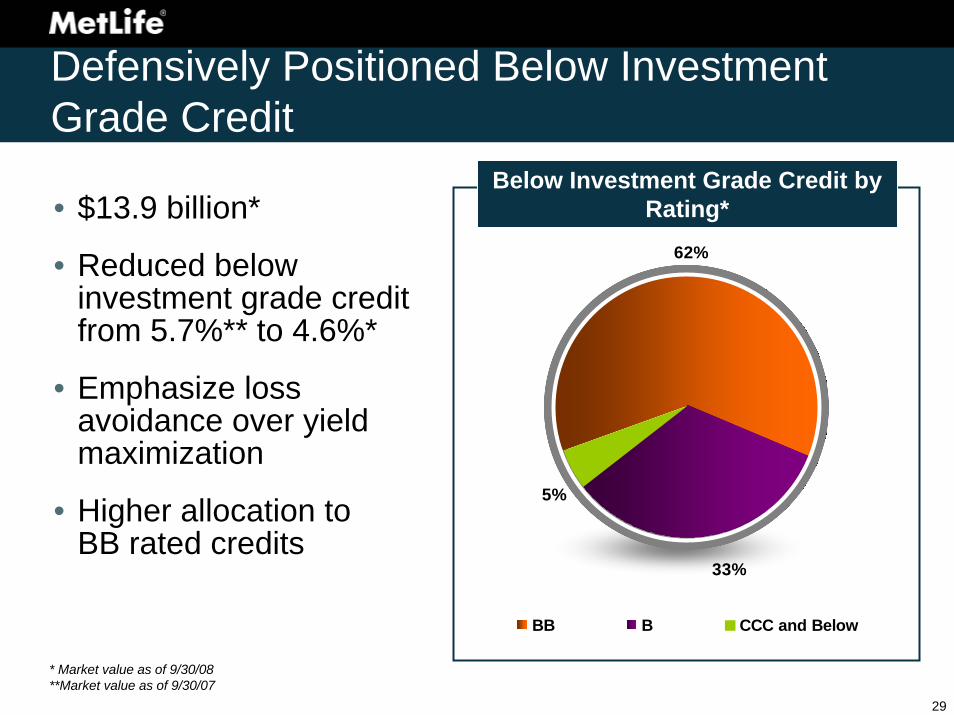

Defensively Positioned Below Investment Grade Credit

• $13.9 billion*

• Reduced below investment grade credit from 5.7%** to 4.6%*

• Emphasize loss avoidance over yield maximization

• Higher allocation to BB rated credits

62%

5%

33%

BB B CCC and Below

Below Investment Grade Credit by Rating*

* Market value as of 9/30/08**Market value as of 9/30/07

30

High Quality Real Estate andAgricultural Investments

9/30/2007 9/30/2008

Real Estate EquityAgricultural MortgagesCommercial Mortgages

Real Estate & Agricultural Investments

as a % of Managed Assets*

$54.1B $59.8B

3.2%3.2%

10.6% 12.0%

4.1%

3.6%19.7%

17.0%

• Focus primarily on Class ‘A’ properties in primary markets

• Loan to Value (LTV)– 57% Commercial Mortgage

Average LTV

– 48% Agricultural Mortgage Average LTV

• Diversified Real Estate equity portfolio

*Market value as of 9/30/08

31

65% 66%63% 62% 61%

55%

50%

55%

60%

65%

70%

75%

80%

2003 2004 2005 2006 2007 2008YTD

70%

CMBS LTV**

Ave

rage

Loa

n to

Val

ue

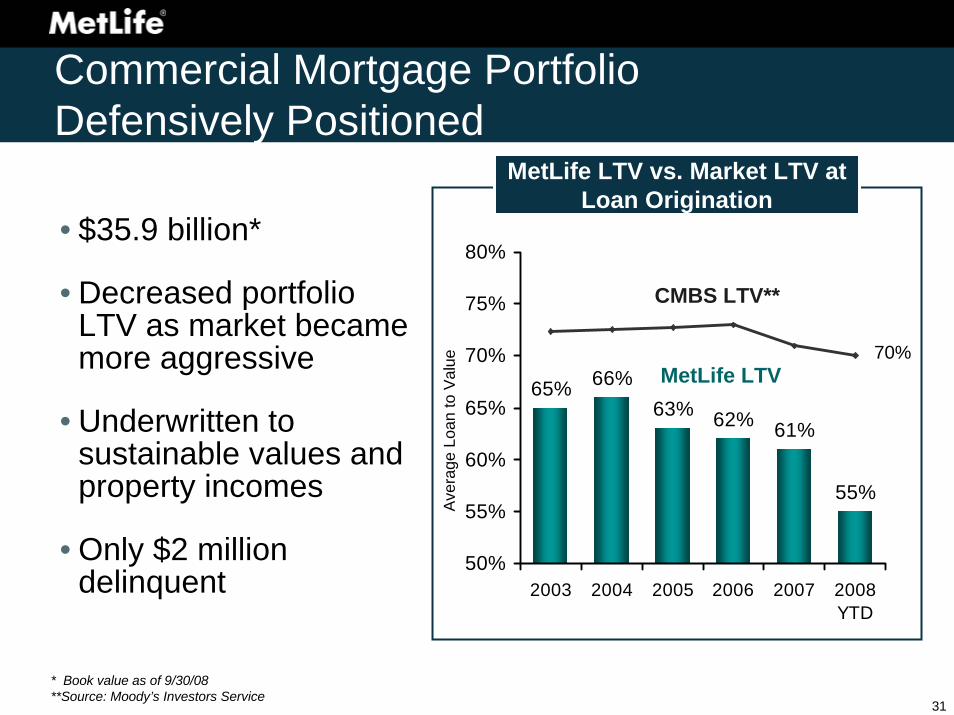

Commercial Mortgage Portfolio Defensively Positioned

• $35.9 billion*

• Decreased portfolio LTV as market became more aggressive

• Underwritten to sustainable values and property incomes

• Only $2 million delinquent

* Book value as of 9/30/08**Source: Moody’s Investors Service

MetLife LTV

MetLife LTV vs. Market LTV at Loan Origination

32

Positioned to Withstand Value Declines

2%

66%

26%

6%

Below 65% LTV 65% to 75% LTV

75-80% LTV Above 80% LTV

• Significantly different fundamentals vs. early 1990s

• On-going pruning of higher risk loans

• Positioned to withstand 40% property value declines

• Less than 2% of portfolio has LTV greater than 80%

Commercial Mortgage Portfolio LTV

As of 9/30/08

08

Unrealized Loss

34

Unrealized Losses Increased Due to Spread Widening

• $12.2 billion fixed maturity net unrealized loss as of 9/30/08

– $16.7 billion gross unrealized loss

– $4.5 billion gross unrealized gain

• Approximately 88% fixed maturity gross unrealized losses rated Investment Grade 1%

19%

6%5%

69%

AAA/AA/A BBB BB B CCC and Lower

$16.7 Billion Fixed Maturity Unrealized Losses by Rating

35

Spreads over Treasuries

*Source: Custom index based on actual 9/30/08 fixed maturity allocations using option adjusted spreads from Barclays US Agency, Barclays US Treasury, Barclays US MBS, Barclays US CMBS, Barclays US ABS, Barclays US Credit, Barclays US High Yield indices

• Spreads on risk sectors have increased since 9/30/08

• Barclays Aggregate increased 36%

• Barclays BBB Credit increased 75%

• Barclays CMBS increased 170%

Spreads Have Increased Dramatically

Custom index spread*

09/30/08 10/15/08 10/31/08 11/14/08 11/30/080

100

200

300

400

500

600

700

Market Spreads

36

Net Unrealized Loss Has Also Increased

*Source: Custom index based on actual 9/30/08 fixed maturity allocations using option adjusted spreads from Barclays US Agency, Barclays US Treasury, Barclays US MBS, Barclays US CMBS, Barclays US ABS, Barclays US Credit, Barclays US High Yield indices

Market Spreads andMetLife’s Net Unrealized Loss**

Spreads over Treasuries

• Net unrealized loss increased

– $12.2 billion at 9/30/08

– Approximately $26.9 billion at 11/30/08

• 63% less than 3 months

• 84% Investment Grade• $2.8 billion greater than

20% and 6 months 0

5,000

10,000

15,000

20,000

25,000

30,000

09/30/08 10/15/08 10/31/08 11/14/08 11/30/080

100

200

300

400

500

600

700

Net

Unr

ealiz

ed L

oss

Net unrealized losses

** MetLife net unrealized loss based on November month-end pricing and management estimates

Custom index spread*

37

Loss Recognition

• Asset Liability Matching– We buy assets to match our liabilities

– Hold the vast majority to maturity

• Robust process to identify credit impairments– Creditworthiness of these securities has not

fundamentally changed since 9/30/08

– $200 - $300 million estimated Q408 after-tax impairments

38

Summary

• Diversified portfolio across fixed income, real estate, agricultural and equity sectors

• Focus on risk management, underwriting and proactive portfolio management

• Defensively positioned for current environment

39

Related Documents