Methodology: Clinical Studies Josh Lerner Empirical Methods in Corporate Finance

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Methodology: Clinical Studies

Josh Lerner

Empirical Methods in Corporate Finance

Long tradition within HBS

Several manifestations:– Case studies.– Book-length analyses.

Distinction between research and classroom cases.

Initially, apparently a response to lack of theoretical frameworks.

Disappearance elsewhere

Major presence in finance journals prior to 1960.

Virtual disappearance as a finance research (as opposed to teaching) methodology.

Changes in past 15 years:– Clinical section of JFE.– Sloan project at NBER.

Why clinical studies?

Limitations of theoretical frameworks:– Idea generation.– Idea validation.

Can undertake analysis without “data snooping,” introducing biases.

Limitations of case studies

Similar to large sample studies:– Sample selection biases.– Data interpretation biases.• May induce false confidence.

Time and energy.

Elements

Theoretical issues.Justification as to why case is

interesting or representative. Hypotheses to be examined.Evidence regarding hypotheses.

Execution is also important

Linkage to theory:– Need to explicitly frame hypotheses.– Need to highlight why interesting

questions.– Need to acknowledge contrary

evidence.

Use of empirical methodology:– Just because small sample shouldn’t

be sloppy!

Today

Three papers.One caveat.One confession.

Cephalon, Inc.

Chacko, Tufano and Verter

JFE, 2001

The case

Biotechnology company bought call options on its own stock:– Issued stock to investment bank in

exchange.– Anticipated approval of drug by FDA,

leading to jump in stock price:• Would then require funds to buyout R&D

partnership, which options would provide.

Objective of study

Use this case to examine Froot, Scharfstein, and Stein [1993]:– At first glance, very close to their

“cash flow hedging”:• See whether factors predicting use of risk-

management are present.• See whether other explanatory efforts are

at work.

Motivation for case selection

“Near textbook example”:–Much of hedging focuses on providing

insurance in case of disappointments:• E.g., farmer contracting to sell grain at set

price in mid-summer.

– FSS argues that firms should match cash flows with investment opportunities.

– Denote four criteria for when cash flow hedging makes sense.

Motivation for case selection (2)

Explicitly consider the four criteria:– Attractiveness of investment opportunity.– Inability to finance without hedging.

• Somewhat cloudy due to licensing option (accounting rationale).

• Aside from this, Cephalon meets key criteria for hedging.

– External financing costly:• Mixed historical evidence.

– Hedging makes cash available: yes.

Methodology

Review of theoretical literature.Review of public documents.Interviews with management and

analysts.Analysis of securities returns,

option pricing.No release needed.

Authors’ conclusions

In large part, motivation for cash flow hedging corresponds to theory.

But importance of accounting considerations seems difficult to reconcile with theory.

Also, case highlights deadweight costs of hedging as well as risk management:– Both sets of costs poorly understood.

Concerns

Rigorous and well-done analysis:– Linkage to theory.– Analytical tools used.– Open-mindedness of authors.–Willingness to grapple with complexity

of situation.

Concerns (2)

Main limitation is giving a sense of generality of phenomenon under study:– Do other firms do such hedging?– Are accounting-based concerns really

critical everywhere?

To what extent is this a special case with little general applicability?

Czech Mate

Desai and Moel

Working Paper, 2005

The case

Investment in Czech media holding company by American entrepreneur (Lauder):– Expropriation by local insider

(Zelezny).• Even though 1% stake!

– Lengthy litigation to recover invested funds.

Objective of study

Law and finance literature:– Focus on institutions…• But typically treat as affecting everyone

equally.

– Also debate between those emphasizing importance of institutions addressing state abuse, private disputes.

Not testing models, but illustrating issues.

Motivation for case selection

Transition economy:– Lots of opportunities for value

extraction.• “Tunneling” phrase originated in Czech

case.

–Media companies a particularly good instance:• Lots of potential private benefits.

Motivation for case selection (2)

Misconceptions:– Often assumed to be closed economy.• In actuality, many points of contact:

– FDI.– International treaties.

– Tunneling seen as hurting minority holders:• Case will illustrate how ownership share

need not matter.

Methodology

Review of theoretical literature.Review of public documents

(especially litigation files).Analysis of securities returns.No release needed.

Authors’ conclusions

Contracts, ownership need not matter:– Zelezny had regulatory support, which

allowed him to extract rents.• A consequence of poorly defined property

rights.

The importance of broader political considerations in resolving dispute:– E.g., Czech desire to join EU.

Media’s private benefits.

Contrast with earlier paper

Critically important topic:– Addressing broad area where

considerable literature.• Also practically critical.

– Careful examination of tangled situation.

–Willingness to suggest where theory has limitations.

Contrast with earlier paper (2)

But less structured analysis:– Not as clear delineation of hypothesis

to be tested.– Less firm foundation in literature.

Who Manages Risk?

Tufano

JF, 1996

Overview

Looks at determinants of risk management in gold industry.

Little evidence that value maximization is driver.

Instead, appears management’s ownership is critical.

Gold industry as a research site

~50 public firms in U.S., Canada.Clearly observable price.Active risk management:– Hedging and insurance commonplace.

Extensive disclosure of risk management activities:– Compiled by stock analysts.

Gold industry as a research site (2)Are agency problems particular

severe here?– Numerous small companies.– Propensity of retail investors to hold

natural resource companies.– Loose Canadian securities oversight.

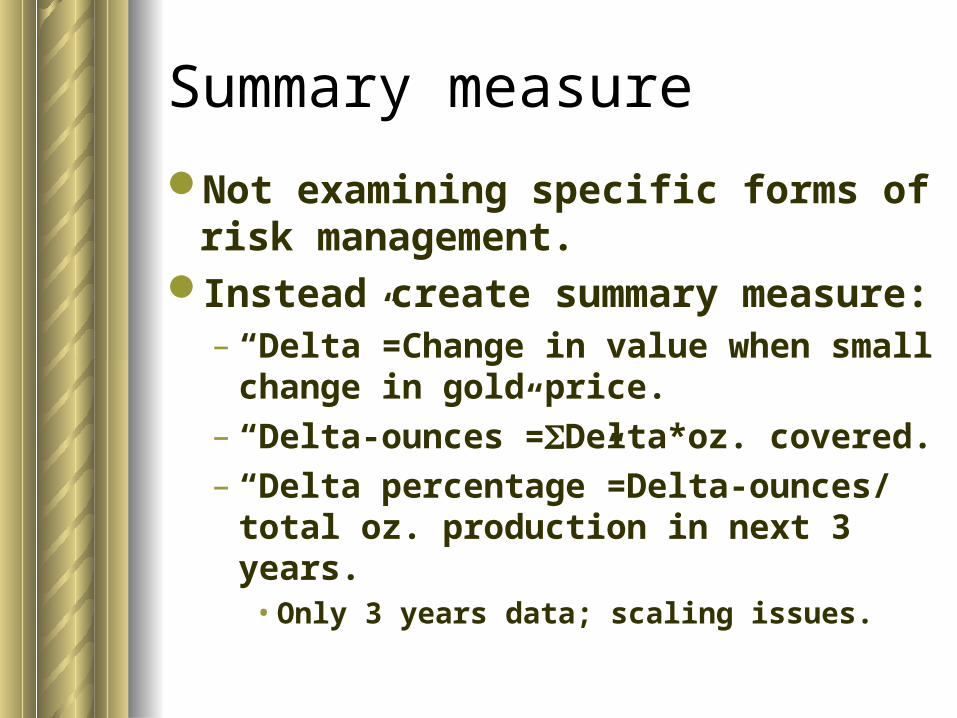

Summary measure

Not examining specific forms of risk management.

Instead create summary measure:– “Delta”=Change in value when small

change in gold price.– “Delta-ounces”=Delta*oz. covered.– “Delta percentage”=Delta-ounces/ total

oz. production in next 3 years. • Only 3 years data; scaling issues.

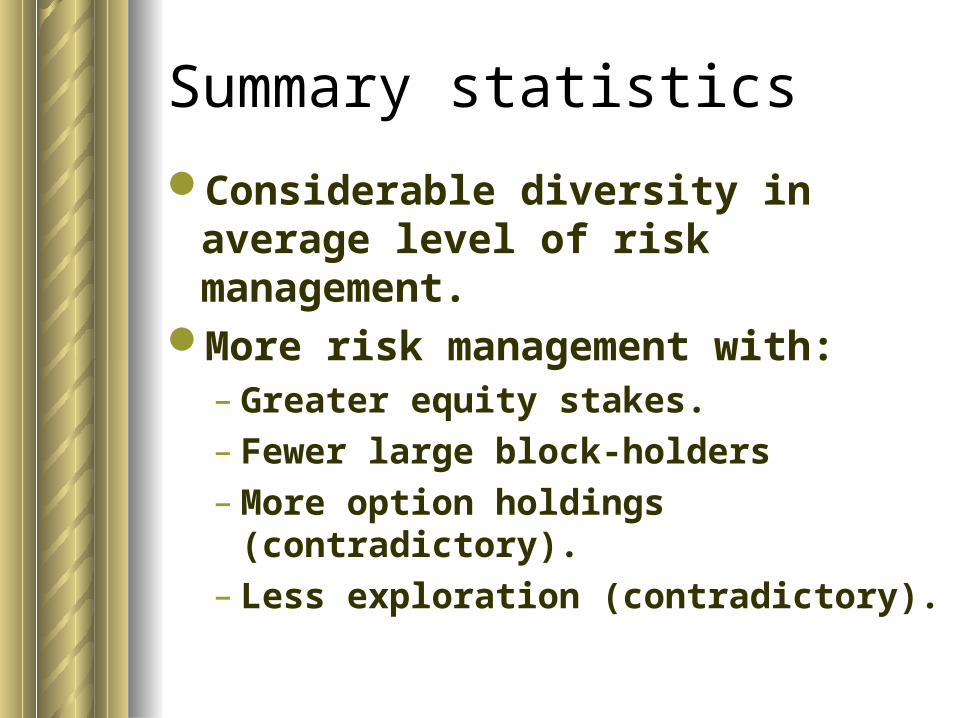

Summary statistics

Considerable diversity in average level of risk management.

More risk management with:– Greater equity stakes.– Fewer large block-holders–More option holdings (contradictory).– Less exploration (contradictory).

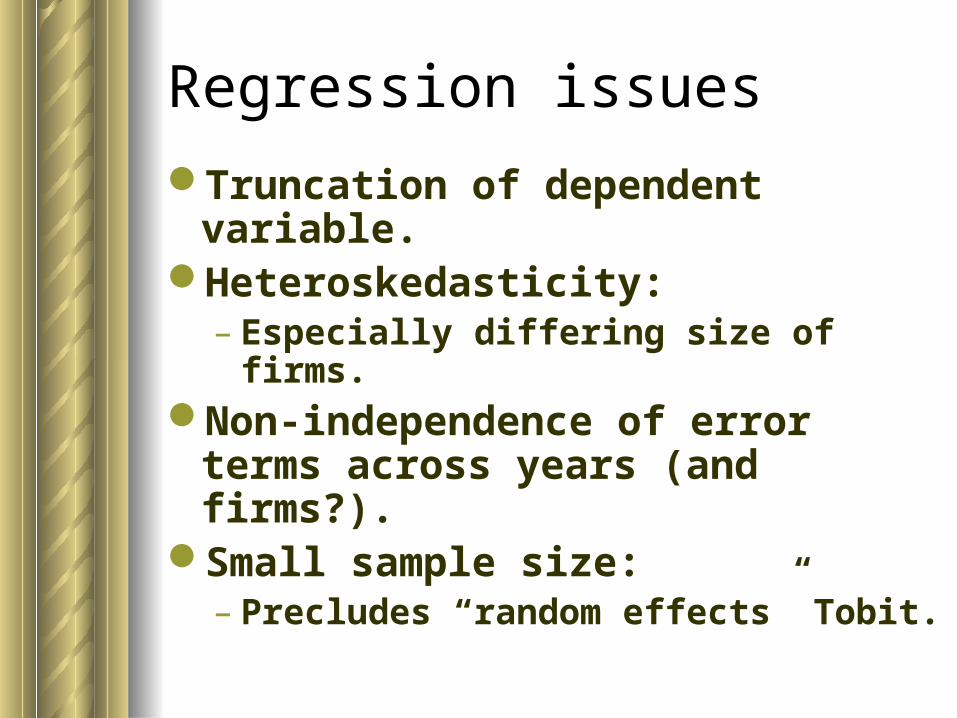

Regression issues

Truncation of dependent variable.Heteroskedasticity:– Especially differing size of firms.

Non-independence of error terms across years (and firms?).

Small sample size:– Precludes “random effects” Tobit.

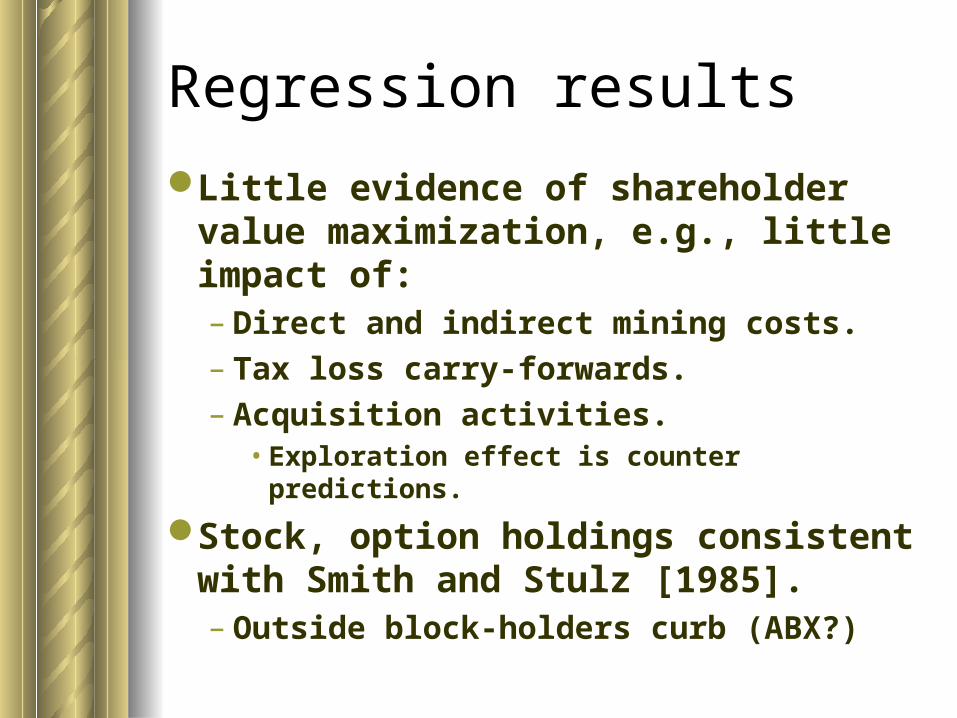

Regression results

Little evidence of shareholder value maximization, e.g., little impact of:– Direct and indirect mining costs.– Tax loss carry-forwards.– Acquisition activities.• Exploration effect is counter predictions.

Stock, option holdings consistent with Smith and Stulz [1985].– Outside block-holders curb (ABX?)

Addressing concerns

Could results reflect size of management team:– Bigger firms have more insiders and

hence bigger holdings?• Look at holdings per capita.

Maybe % holding by management is better measure of conflicts:–Works less well.

Addressing concerns (2)

In distressed firms, equity may be like an option.

Decision may be driven by CEO, not rest of management.

Management age and tenure may affect risk aversion:– Little evidence, except concerning CFO

tenure.

Concerns

Well-suited research site…– My favorite of the clinical studies.

… but challenges with small sample size:– Can be addressed, at least in part.– Some remaining issues as in other paper.

Evidence consistent with theoretical models of risk management.– But representativeness of industry?

Conclusions

Importance of sensitivity to biases:– Selection of study site.– Interpretation of facts.

Importance of execution:– Linkage to theory.– Analytical tools.

Perhaps more useful as complement to other work than an end in itself.

Related Documents