Merchandise Inventory Chapter 6 6-1 Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

Merchandise Inventory Chapter 6 6-1Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall.

Dec 26, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Merchandise Inventory

Chapter 6

6-1Copyright ©2014 Pearson Education, Inc. publishing as Prentice Hall

Accounting principles and

controls related to merchandise

inventory

6-2

Consistency Principle

• Businesses should use the same accounting methods and procedures from period to period.

• Consistency helps users of financial statement information to compare financial statements from one period to the next.

6-3

A change in the accounting

methods, must be reported to the investors and

creditors in the Notes to the

Financial Statements.

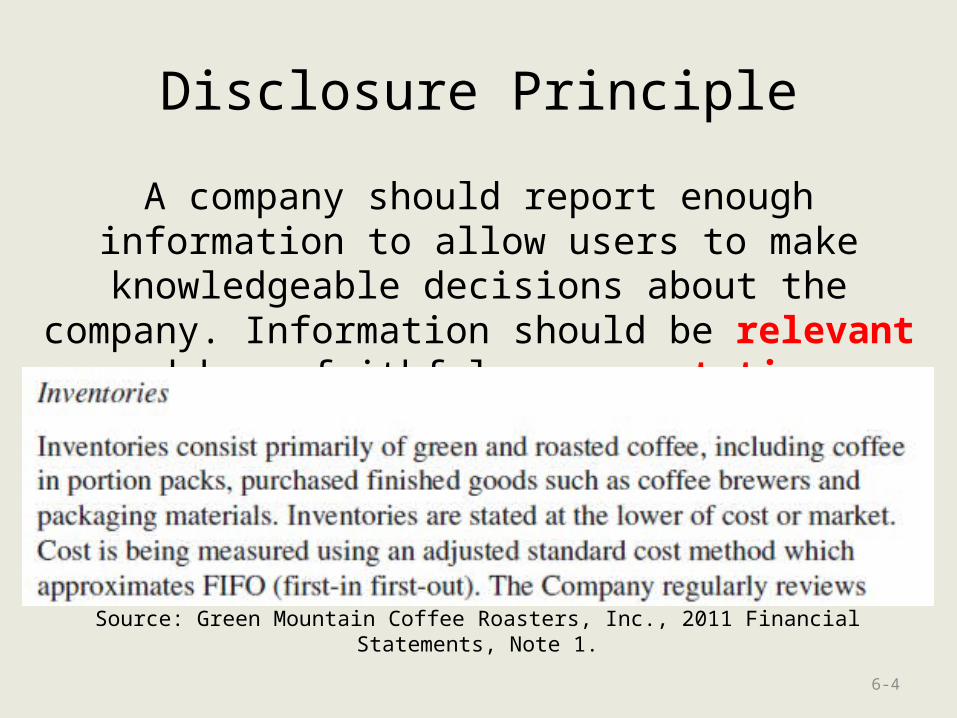

Disclosure Principle

A company should report enough information to allow users to make knowledgeable decisions about the company. Information should be relevant and have

faithful representation.

6-4

Source: Green Mountain Coffee Roasters, Inc., 2011 Financial Statements, Note 1.

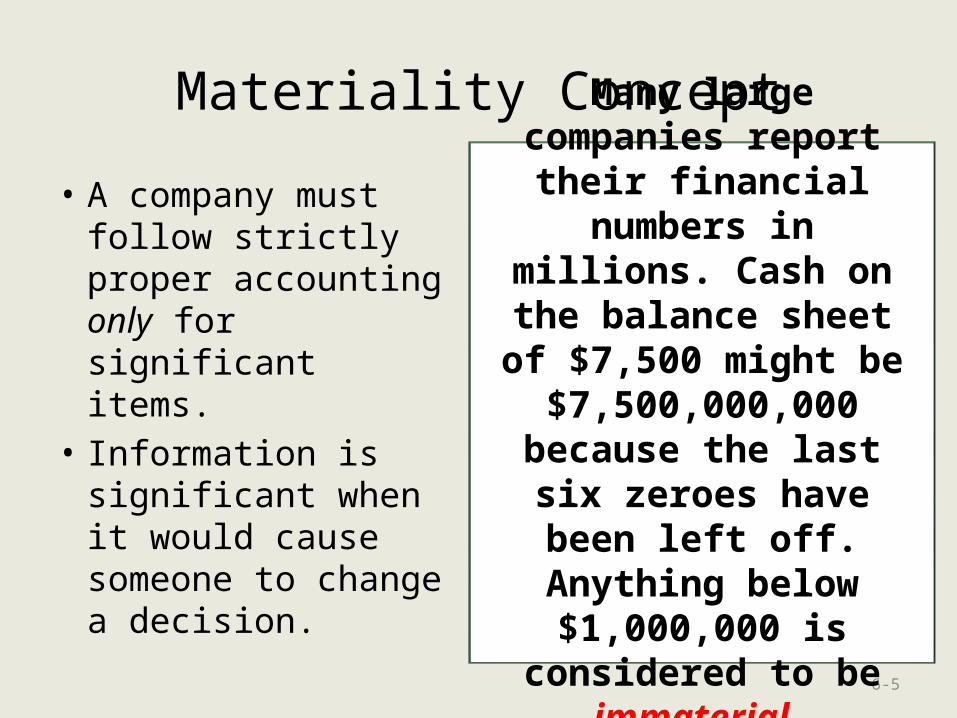

Materiality Concept

• A company must follow strictly proper accounting only for significant items.

• Information is significant when it would cause someone to change a decision.

6-5

Many large companies report their financial numbers in millions. Cash on the balance

sheet of $7,500 might be $7,500,000,000 because the last six zeroes have been left off. Anything

below $1,000,000 is considered to be immaterial.

Conservatism

• A company should report the least favorable figures in the financial statements when two or more possible options are presented.

• Goal: Never overstate assets or net income.

• Anticipate no gains• Provide for probable

losses• Conservatively report

assets and liabilities• When in doubt record an

expense instead of an asset

• Choose options that undervalue the business

6-6

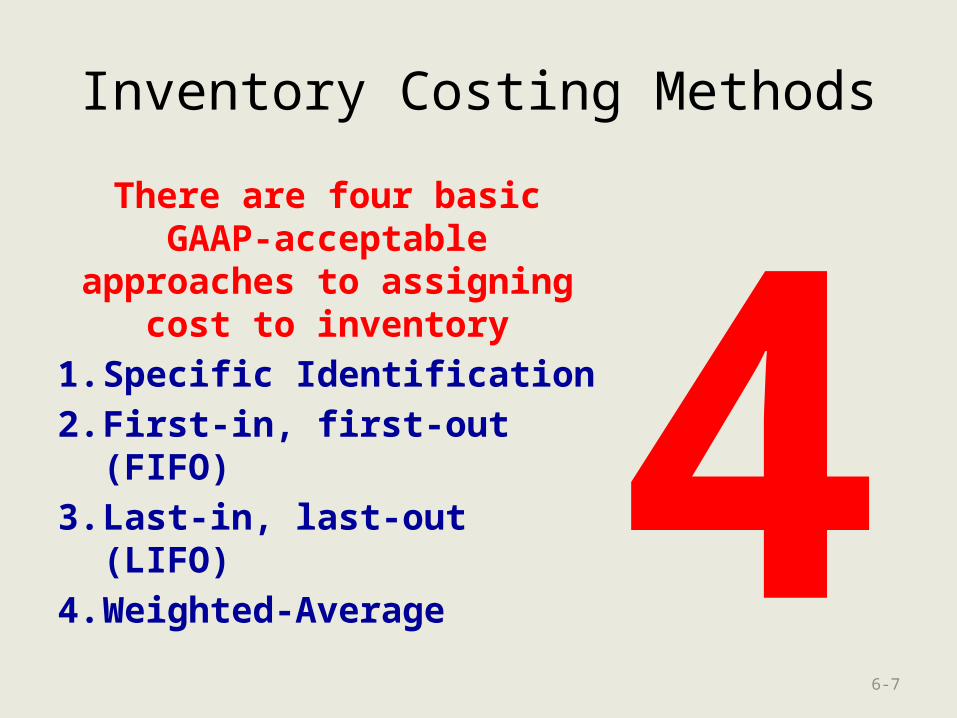

Inventory Costing Methods

There are four basic GAAP-acceptable

approaches to assigning cost to inventory

1. Specific Identification

2. First-in, first-out (FIFO)

3. Last-in, last-out (LIFO)

4. Weighted-Average

6-7

4

Perpetual Specific Identification

• Used when the specific cost for each unit of inventory can be tracked.

• As each unit is sold, its specific cost is transferred from inventory to Cost of Goods Sold.

6-8

Used for inventories that

include:AutomobilesUnique Artwork

JewelsReal Estate

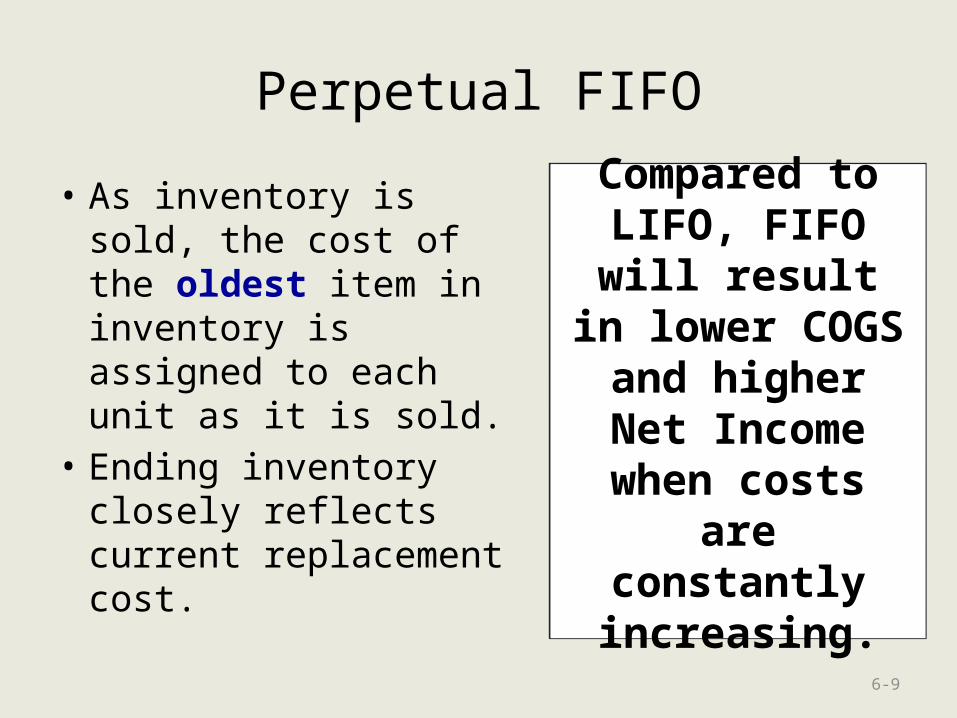

Perpetual FIFO

• As inventory is sold, the cost of the oldest item in inventory is assigned to each unit as it is sold.

• Ending inventory closely reflects current replacement cost.

6-9

Compared to LIFO, FIFO will result in lower

COGS and higher Net Income when

costs are constantly increasing.

Perpetual LIFO

• As inventory is sold, the cost of the newest item in inventory is assigned to each unit as it is sold.

• Cost of Goods Sold closely reflects current replacement cost.

6-10

Compared to FIFO, LIFO will result in higher

COGS and lower Net Income when

costs are constantly increasing.

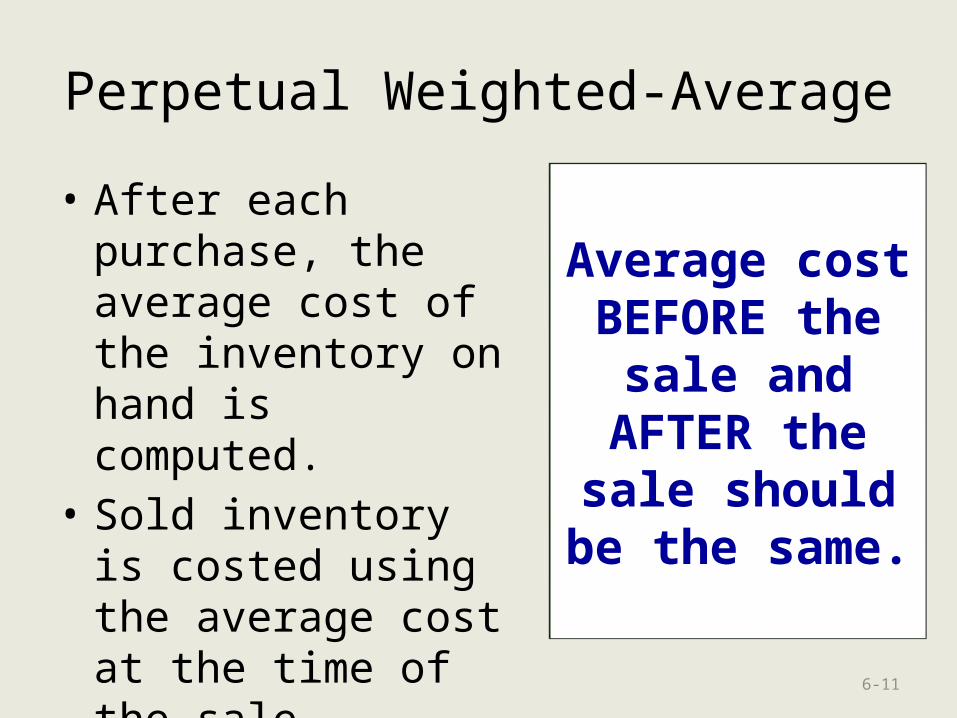

Perpetual Weighted-Average

• After each purchase, the average cost of the inventory on hand is computed.

• Sold inventory is costed using the average cost at the time of the sale.

6-11

Average cost BEFORE the

sale and AFTER the sale should be the

same.

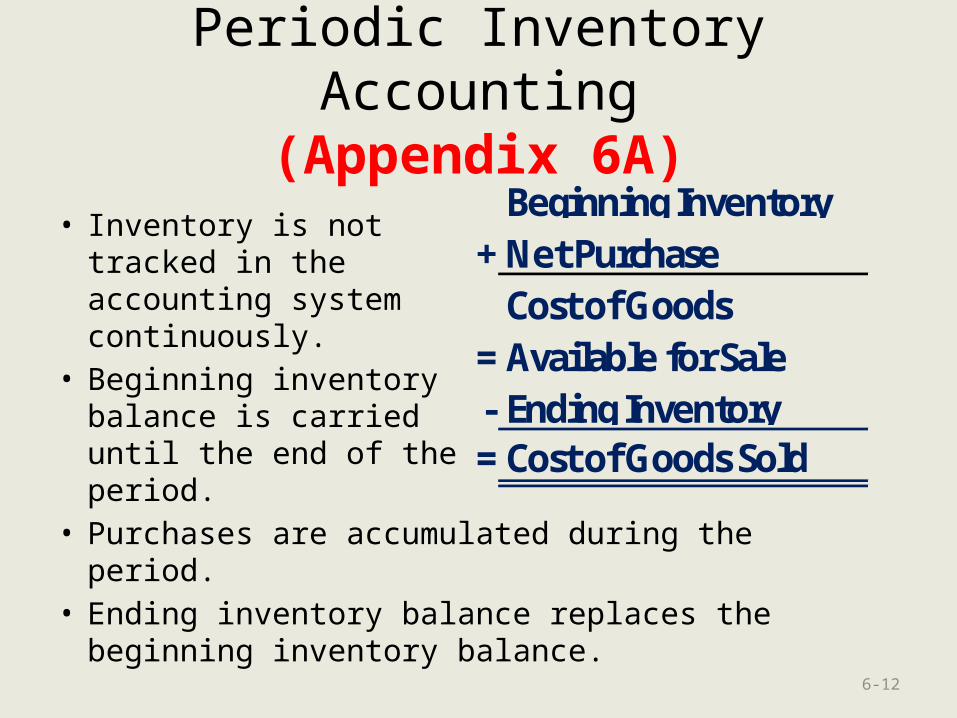

Periodic Inventory Accounting(Appendix 6A)

• Inventory is not tracked in the accounting system continuously.

• Beginning inventory balance is carried until the end of the period.

• Purchases are accumulated during the period.• Ending inventory balance replaces the beginning

inventory balance.6-12

Beginning Inventory + Net Purchase

=Cost of Goods Available for Sale

- Ending Inventory = Cost of Goods Sold

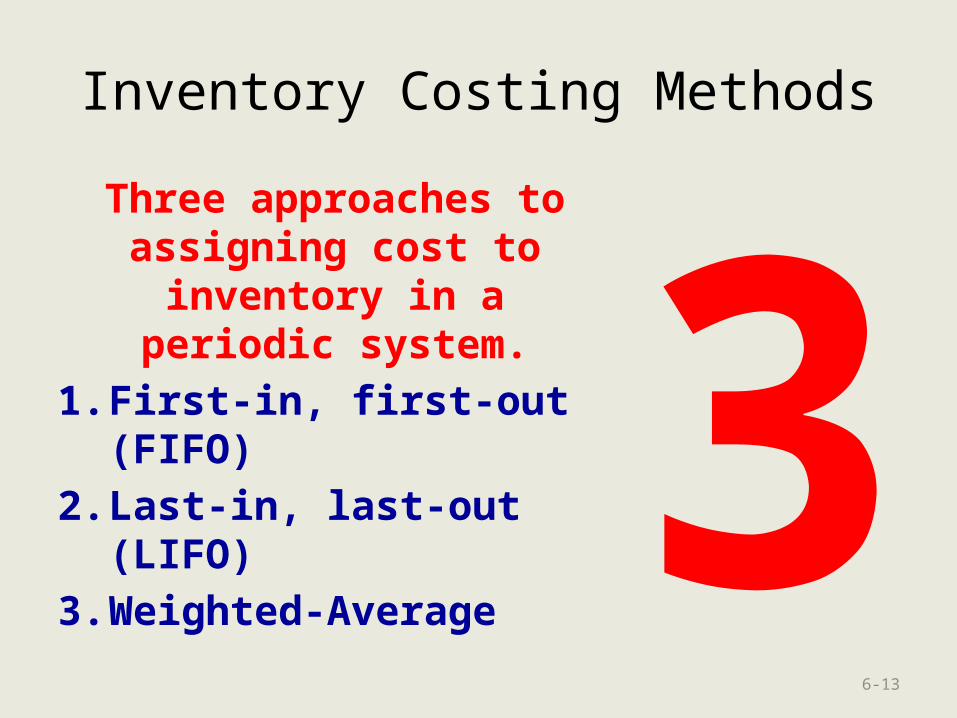

Inventory Costing Methods

Three approaches to assigning cost to inventory

in a periodic system.

1. First-in, first-out (FIFO)

2. Last-in, last-out (LIFO)

3. Weighted-Average

6-13

3

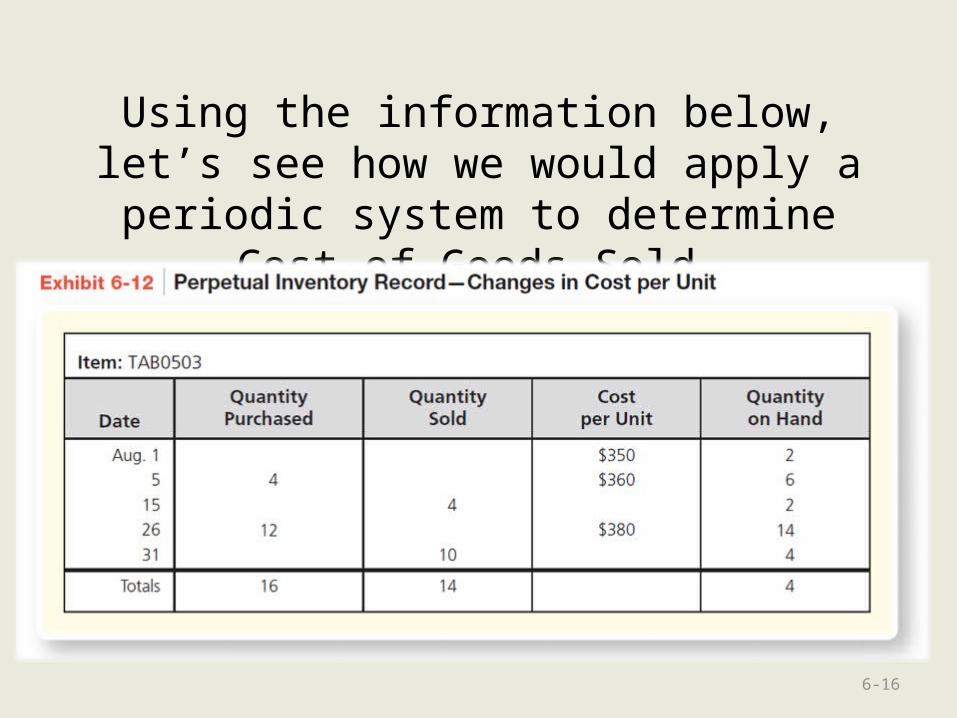

Using the information below, let’s see how we would apply a periodic system to

determine Cost of Goods Sold.

6-14

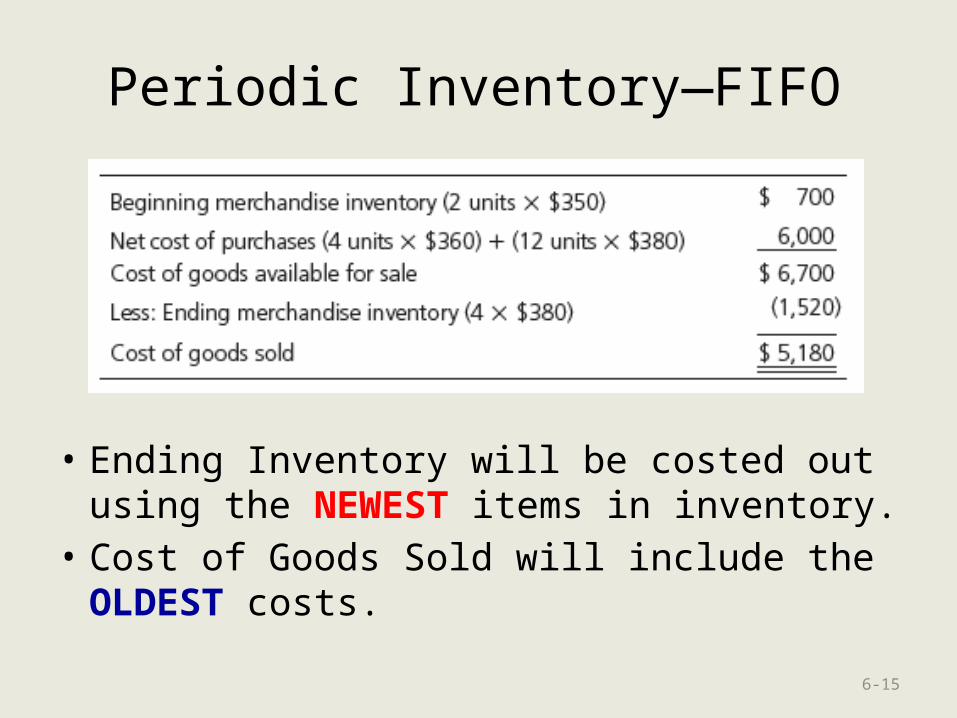

Periodic Inventory—FIFO

• Ending Inventory will be costed out using the NEWEST items in inventory.

• Cost of Goods Sold will include the OLDEST costs.

6-15

Using the information below, let’s see how we would apply a periodic system to

determine Cost of Goods Sold.

6-16

Periodic Inventory—LIFO

• Ending Inventory will be costed out using the OLDEST items in inventory.

• Cost of Goods Sold will include the NEWEST costs.

6-17

Weighted Average-CostThe average-cost per unit is assigned to cost of goods sold and to units remaining in inventory.

18

Average CostCost of Inventory Available

Number of Units Available÷ =

Periodic Inventory—Weighted Average

• Ending Inventory is costed using the AVERAGE cost of inventory.

• Cost of Goods Sold will also be costed using AVERAGE cost of inventory.

6-19

Average cost $6,700 ÷18 = $372.22

6-20

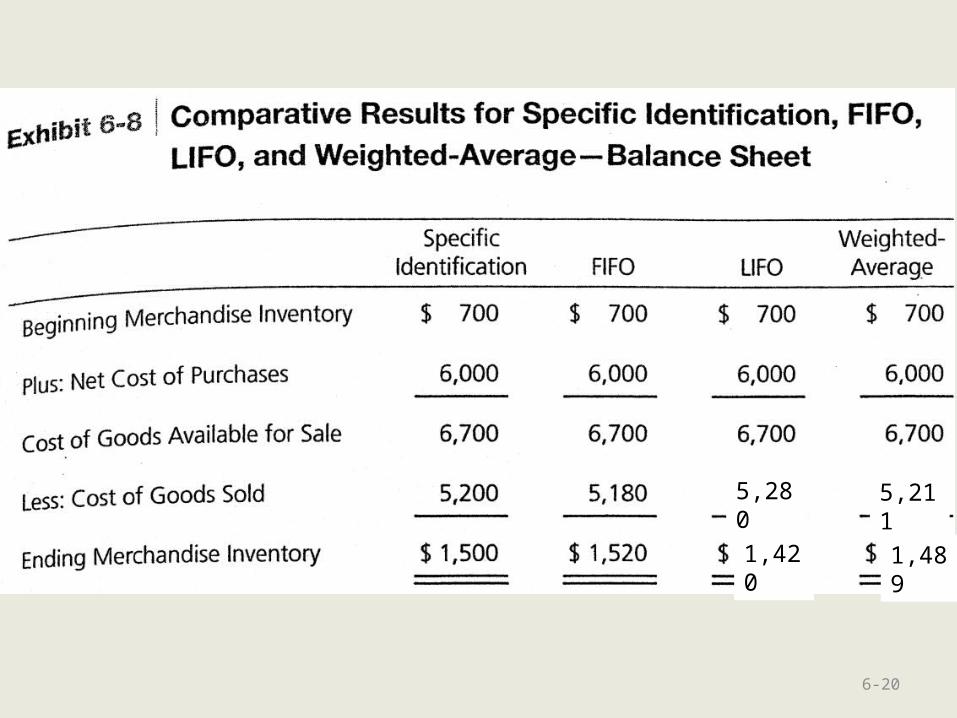

5,280

1,420

5,211

1,489

Note that FIFO results in the highest Gross Profit, while LIFO shows the highest Cost of

Goods Sold.6-21

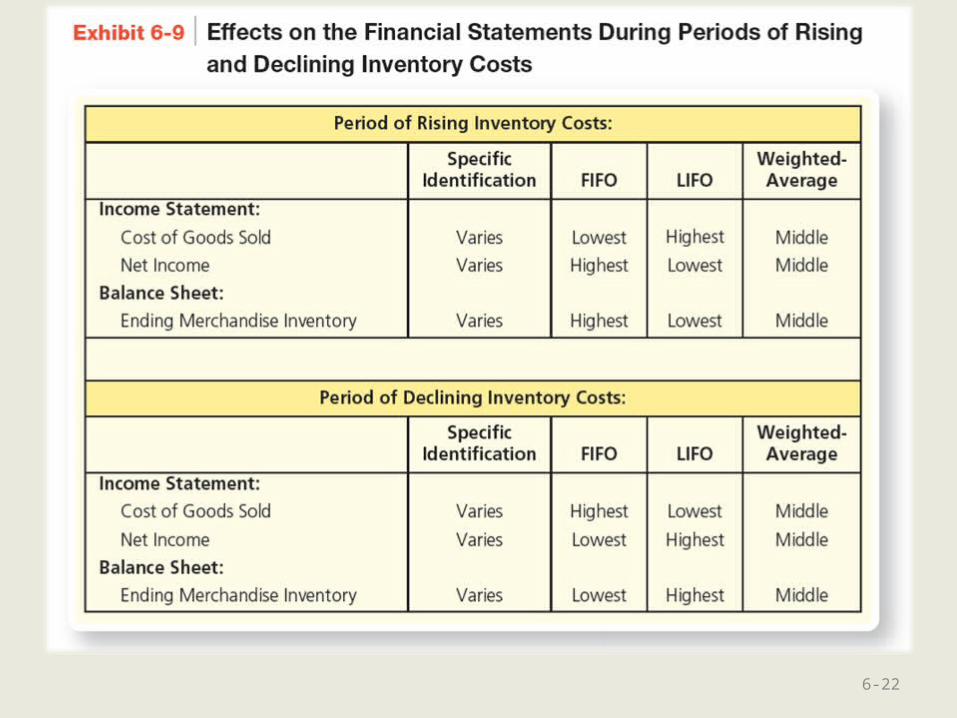

5,280 5,211

1,720 1,789

6-22

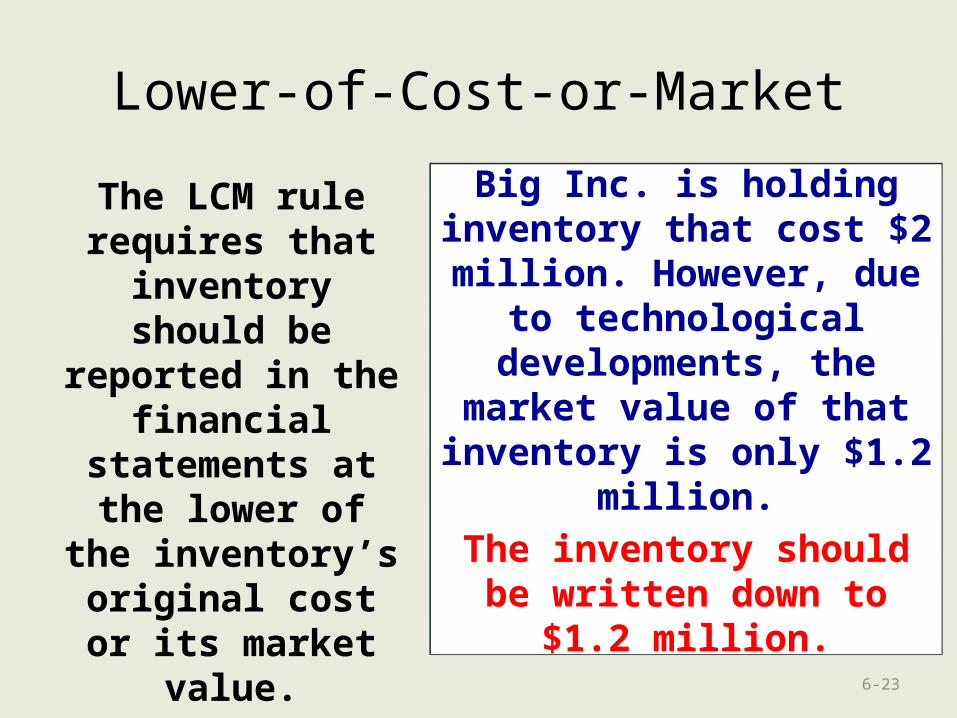

Lower-of-Cost-or-Market

The LCM rule requires that

inventory should be reported in the

financial statements at the

lower of the inventory’s original cost or its market

value.

6-23

Big Inc. is holding inventory that cost $2

million. However, due to technological

developments, the market value of that inventory is

only $1.2 million.

The inventory should be written down to $1.2

million.

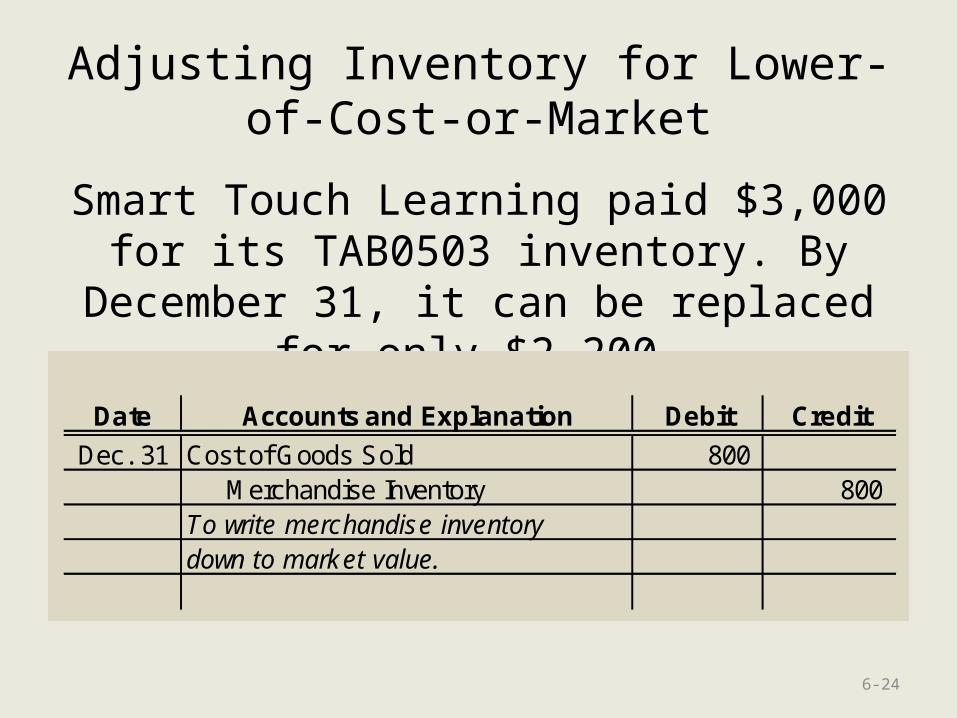

Adjusting Inventory for Lower-of-Cost-or-Market

Smart Touch Learning paid $3,000 for its TAB0503 inventory. By December 31, it can

be replaced for only $2,200.

6-24

Date Accounts and Explanation Debit Credit

Dec. 31 Cost of Goods Sold 800 Merchandise Inventory 800 To write merchandise inventorydown to market value.

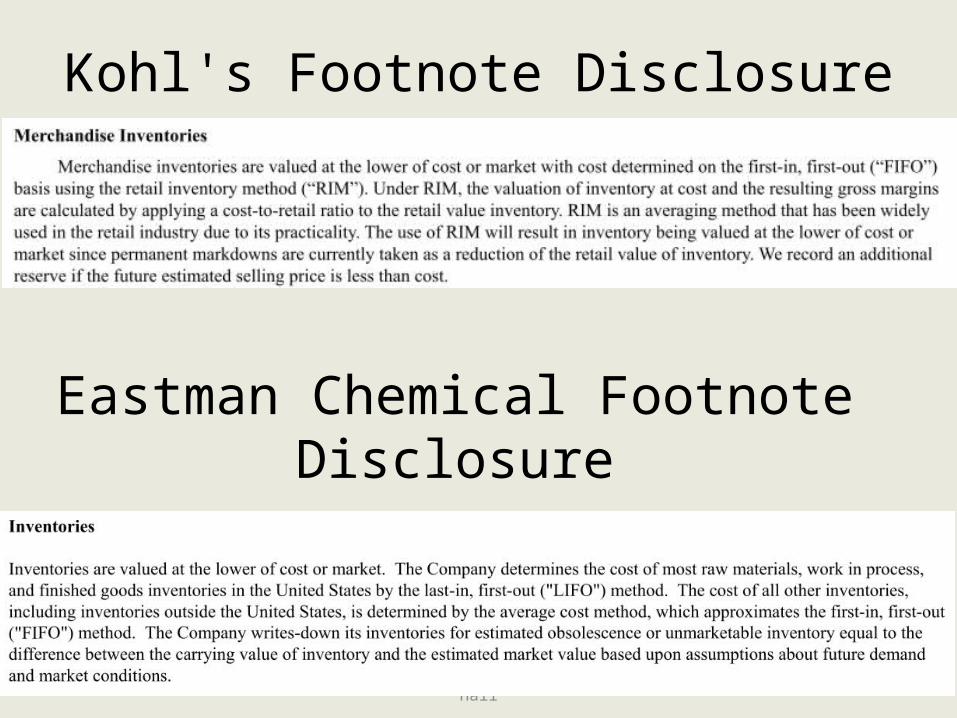

Kohl's Footnote Disclosure

6-25©2014 Pearson Education, Inc. Publishing as Prentice Hall

Eastman Chemical Footnote Disclosure

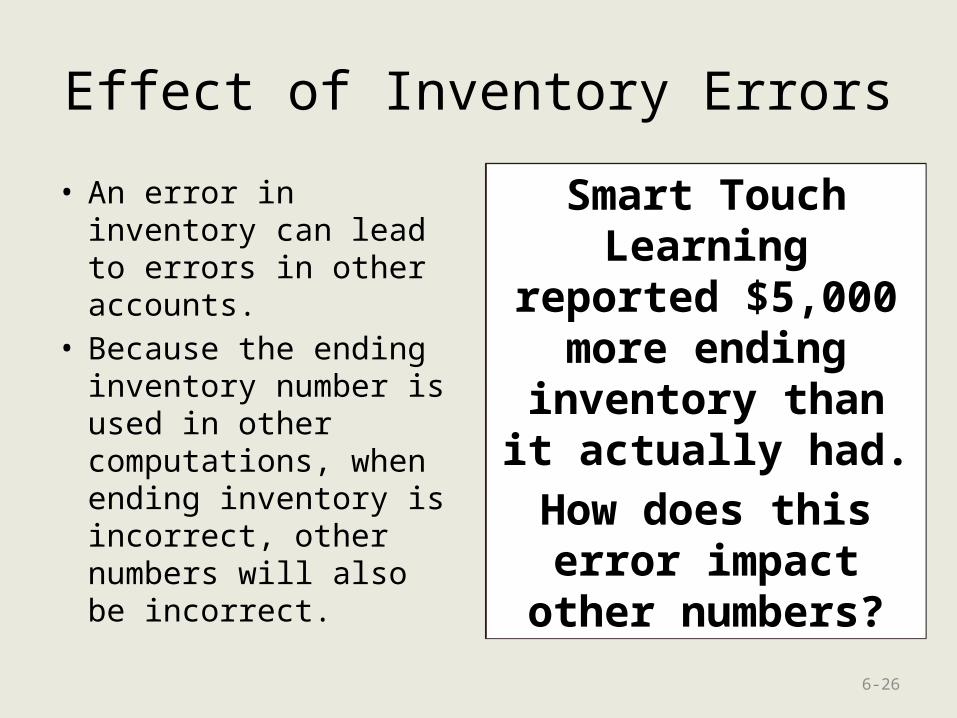

Effect of Inventory Errors

• An error in inventory can lead to errors in other accounts.

• Because the ending inventory number is used in other computations, when ending inventory is incorrect, other numbers will also be incorrect.

6-26

Smart Touch Learning reported

$5,000 more ending inventory than it

actually had.

How does this error impact other

numbers?

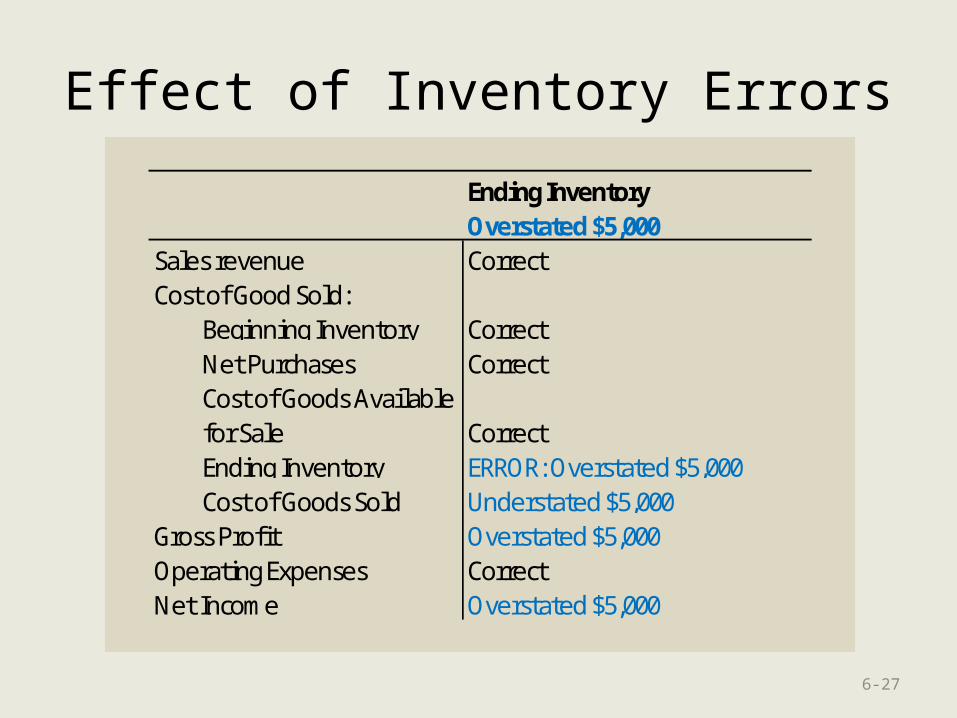

Effect of Inventory Errors

6-27

Ending InventoryOverstated $5,000

Sales revenue CorrectCost of Good Sold:

Beginning Inventory CorrectNet Purchases CorrectCost of Goods Available for Sale CorrectEnding Inventory ERROR: Overstated $5,000Cost of Goods Sold Understated $5,000

Gross Profit Overstated $5,000Operating Expenses CorrectNet Income Overstated $5,000

Effect of Inventory Errors

• A common fraud is for a company to intentionally overstate ending inventory, because it leads to higher Net Income.

• Sometimes ending inventory is understated.

6-28

Suppose that Smart Touch Learning

understated inventory by $1,200.

How does this error impact other

numbers?

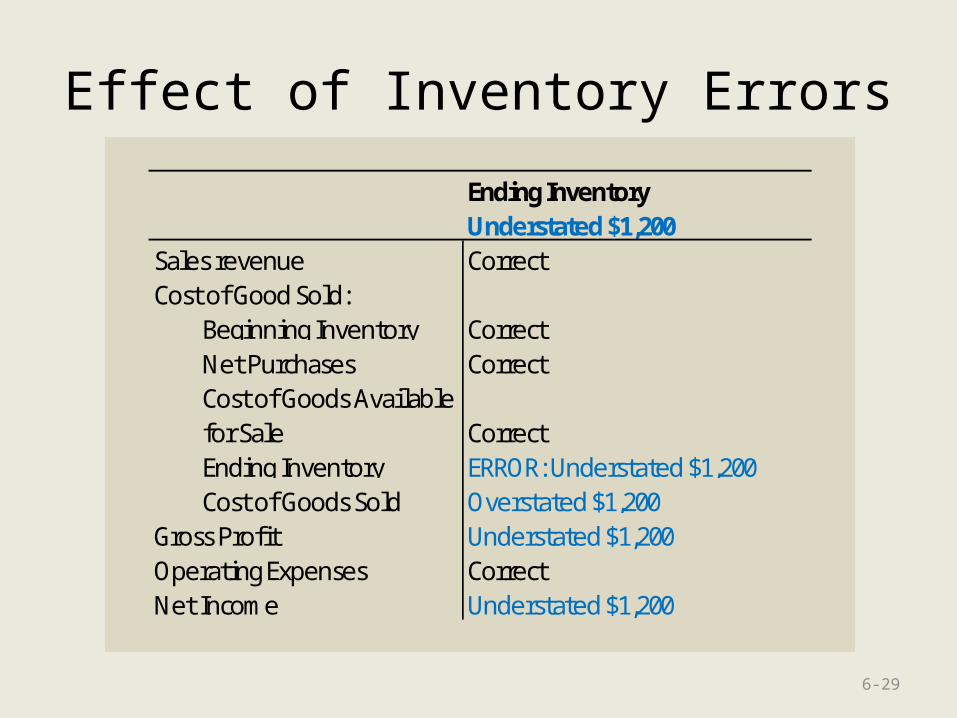

Effect of Inventory Errors

6-29

Ending InventoryUnderstated $1,200

Sales revenue CorrectCost of Good Sold:

Beginning Inventory CorrectNet Purchases CorrectCost of Goods Available for Sale CorrectEnding Inventory ERROR: Understated $1,200Cost of Goods Sold Overstated $1,200

Gross Profit Understated $1,200Operating Expenses CorrectNet Income Understated $1,200

Inventory Errors: Multiple Periods

30

Use inventory turnover and days’

sales in inventory to evaluate business

performance(liquidity)

6-31

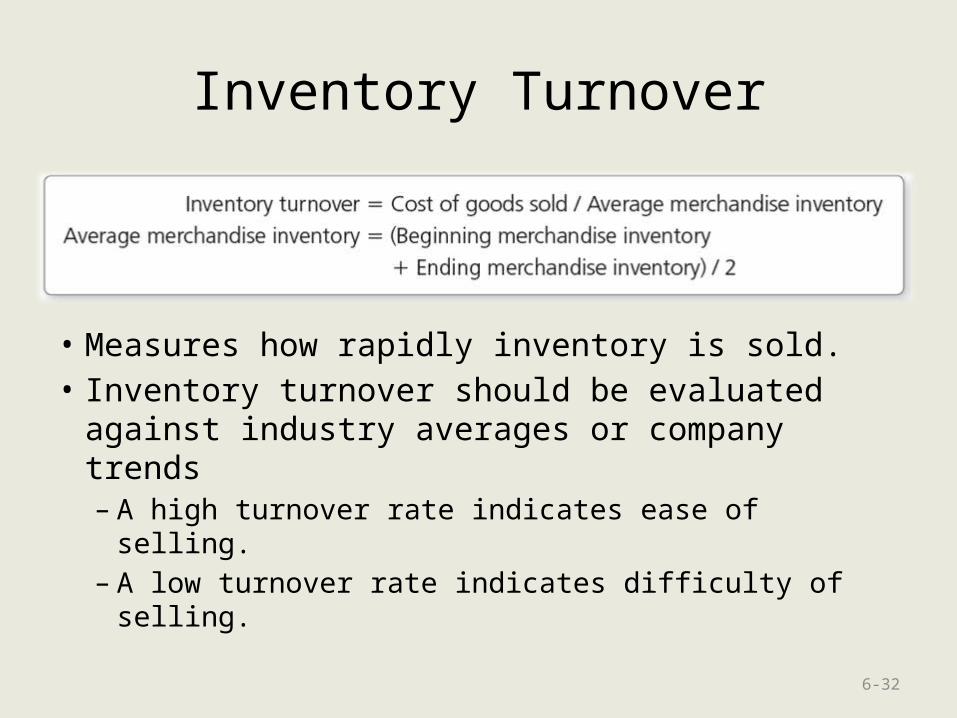

Inventory Turnover

• Measures how rapidly inventory is sold.• Inventory turnover should be evaluated

against industry averages or company trends– A high turnover rate indicates ease of selling.– A low turnover rate indicates difficulty of selling.

6-32

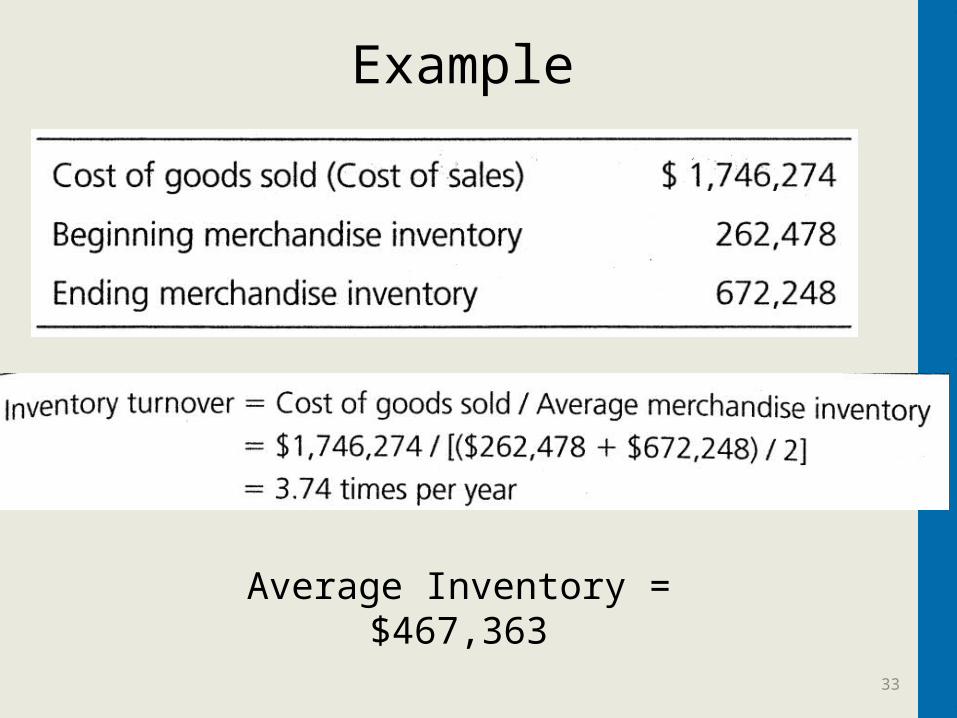

Example

33

Average Inventory = $467,363

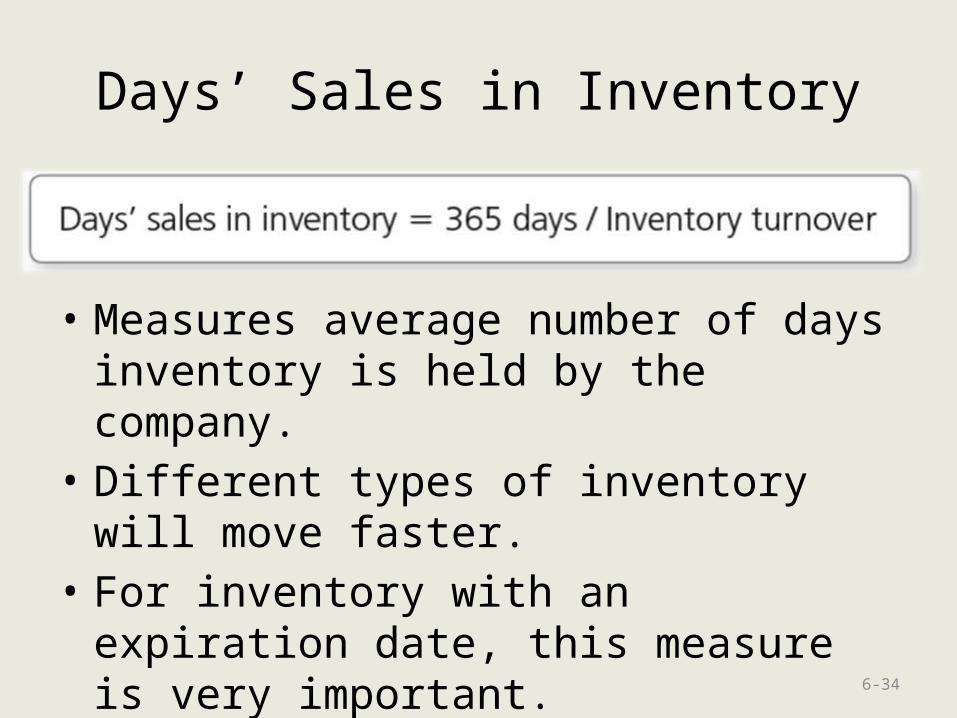

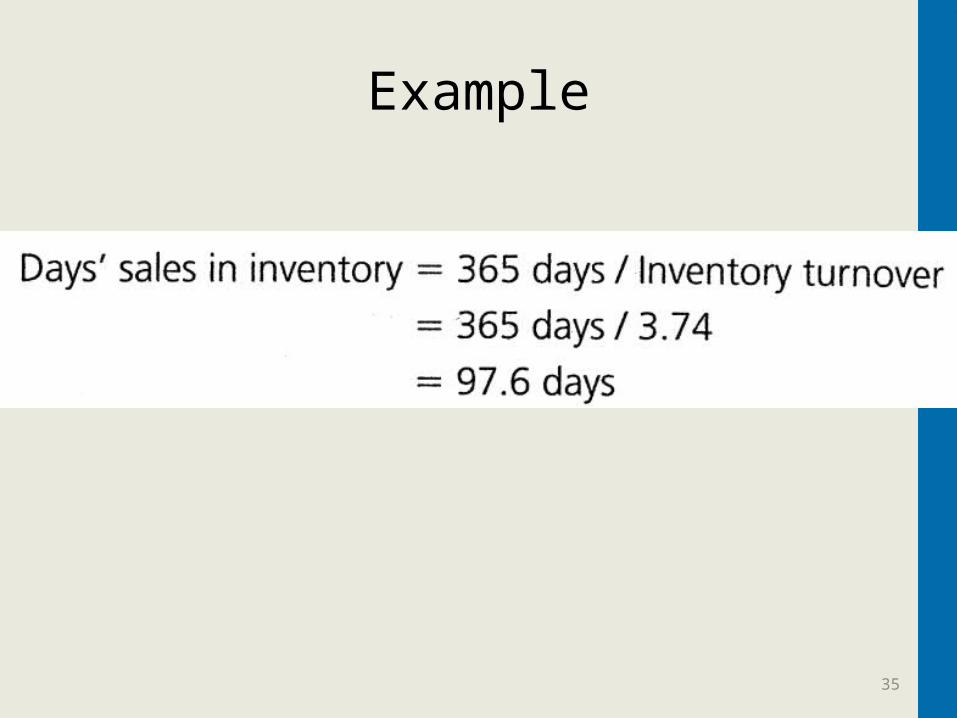

Days’ Sales in Inventory

• Measures average number of days inventory is held by the company.

• Different types of inventory will move faster.

• For inventory with an expiration date, this measure is very important.

6-34

Example

35

Gross profit method and the retail method

(Appendix 6B)

6-36

Inventory Estimation methods

Gross Profit Method

• If the ending inventory cannot be counted, it can be estimated.

• Cost of Goods Sold can be estimated using Sales Revenue and the Gross Profit percent.

• Not acceptable for Financial reporting• Used for interim reporting or casualty loss

estimates 6-37

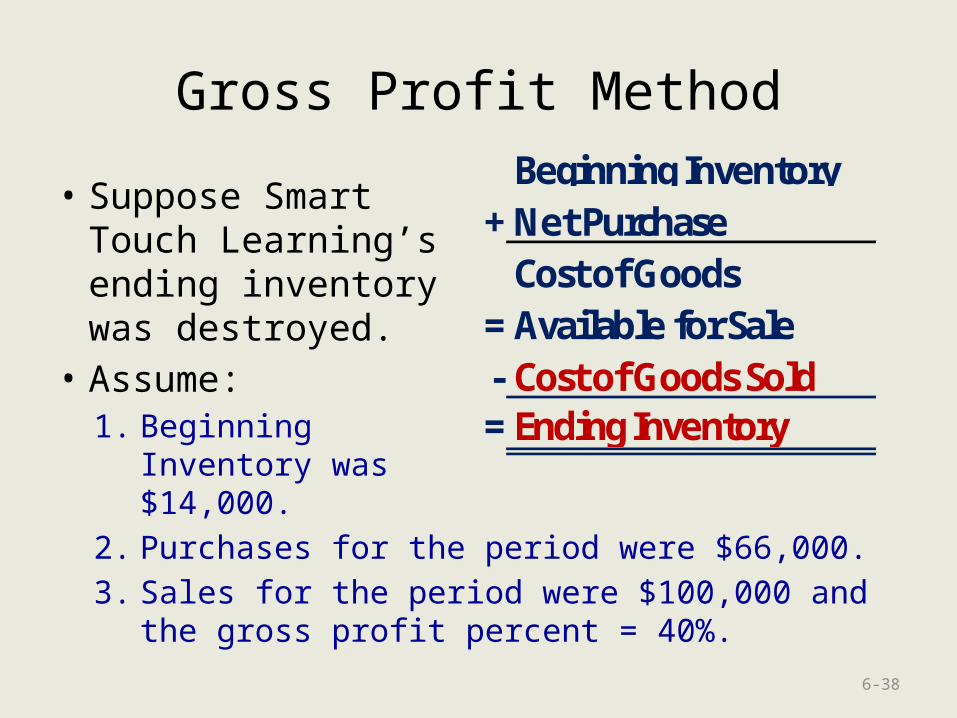

Beginning Inventory + Net Purchases

=Cost of Goods Available for Sale

- Cost of Goods Sold = Ending Inventory

Gross Profit Method

• Suppose Smart Touch Learning’s ending inventory was destroyed.

• Assume:1. Beginning

Inventory was $14,000.

2. Purchases for the period were $66,000.

3. Sales for the period were $100,000 and the gross profit percent = 40%.

6-38

Beginning Inventory + Net Purchase

=Cost of Goods Available for Sale

- Cost of Goods Sold = Ending Inventory

Gross Profit Method

• To estimate Cost of Goods Sold, subtract the normal gross profit from sales.

• $100,000 – $40,000 = $60,000• This will allow you to estimate Ending

Inventory.

6-39

Beg. Inv. $14,000 + Purchases $66,000 = COGA $80,000 - COGS $60,000 = End. Inv. $20,000

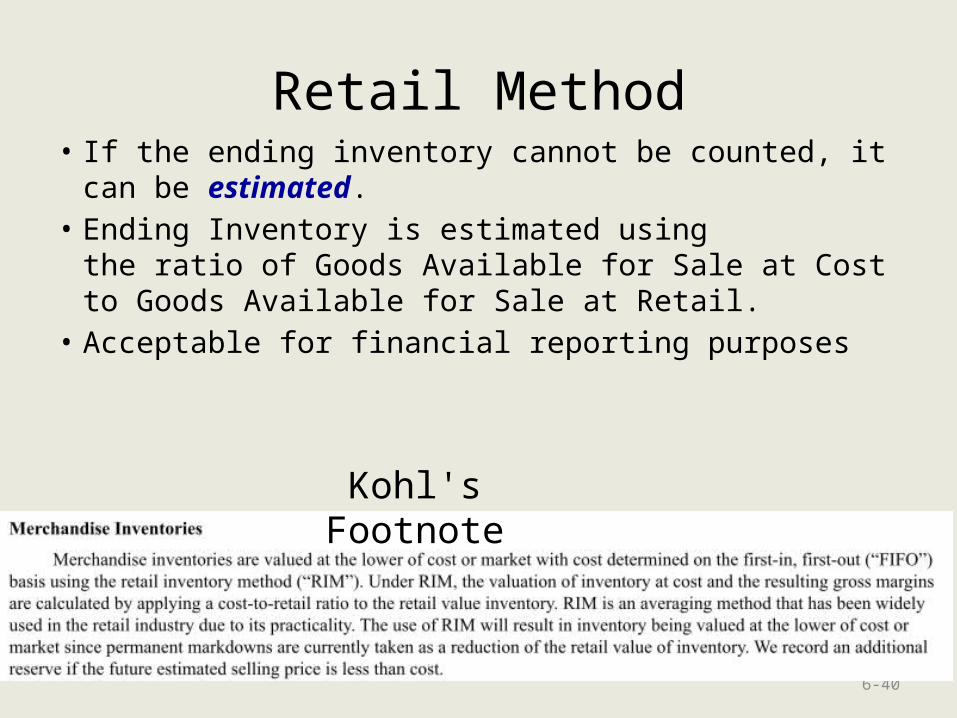

Retail Method• If the ending inventory cannot be counted, it can

be estimated.• Ending Inventory is estimated using

the ratio of Goods Available for Sale at Cost to Goods Available for Sale at Retail.

• Acceptable for financial reporting purposes

6-40

Kohl's Footnote

Related Documents