1984 EXPLANATORY PAPER ON PROPOSED CHEQUES BILL 1984 Prepared by the Attorney-General t s Department, Canberra February 1984

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1984

EXPLANATORY PAPER ON PROPOSED

CHEQUES BILL 1984

Prepared by the Attorney-Generalts Department, Canberra

February 1984

S

I

I

I

1984

EXPLANATORY PAPER ON PROPOSED

cHEQUES BILL 1984

Prepared by the Attorney-General’s Department, Canberra

February 1984

S

SI

IPrinted by Authorityby theCommonwealthGovernmentPrinter

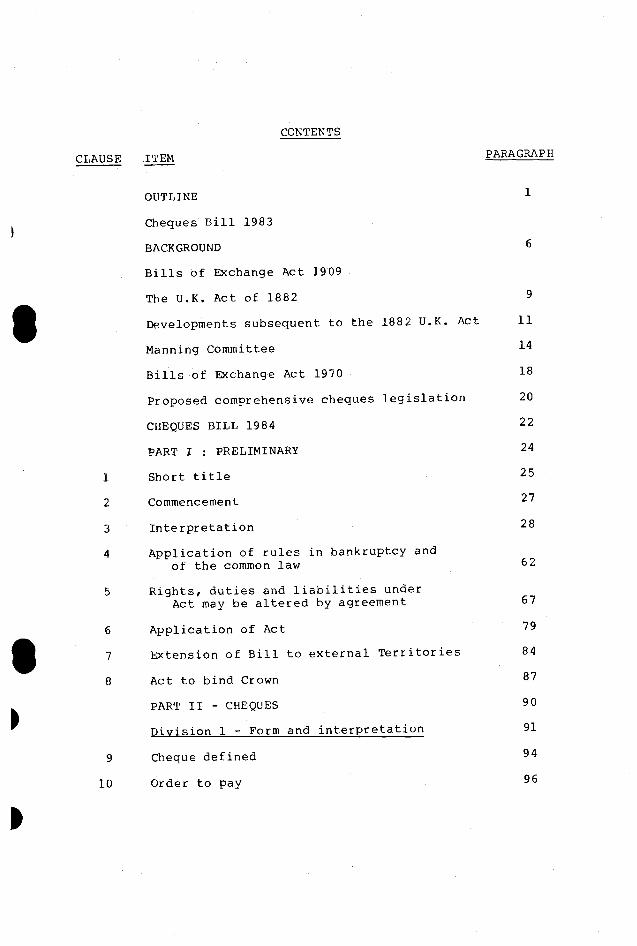

CONTENTS

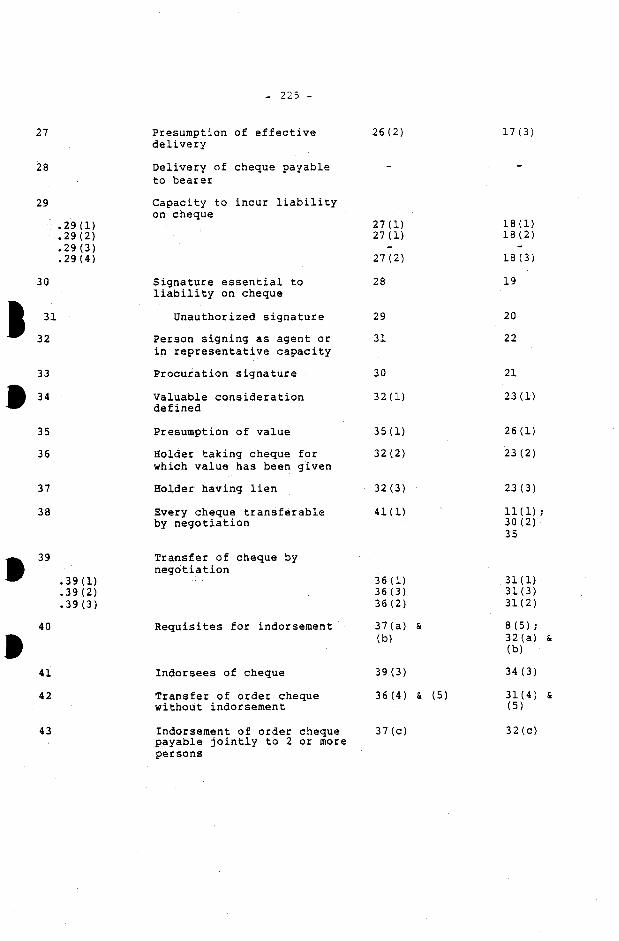

CLAUSE ITEM PARAGRAPH

OUTLINE 1

Cheques Bill 1983

BACKGROUND 6

Bills of Exchange Act 1909

The U.K. Act of 1882 9

Developments subsequent to the 1882 U.K. Act 11

Manning Committee 14

Bills of Exchange Act 1970 18

Proposed comprehensive cheques legislation 20

CHEQUESBILL 1984 22

PART I PRELIMINARY 24

1 Short title 25

2 Commencement 27

3 Interpretation 28

4 Application of rules in bankruptcy andof the common law 62

5 Rights, duties and liabilities underAct may be altered by agreement 67

6 Application of Act 79

7 Extension of Bill to external Territories 84

8 Act to bind Crown 87

PART II - CHEQUES 90

Division 1 - Form and interpretation 91

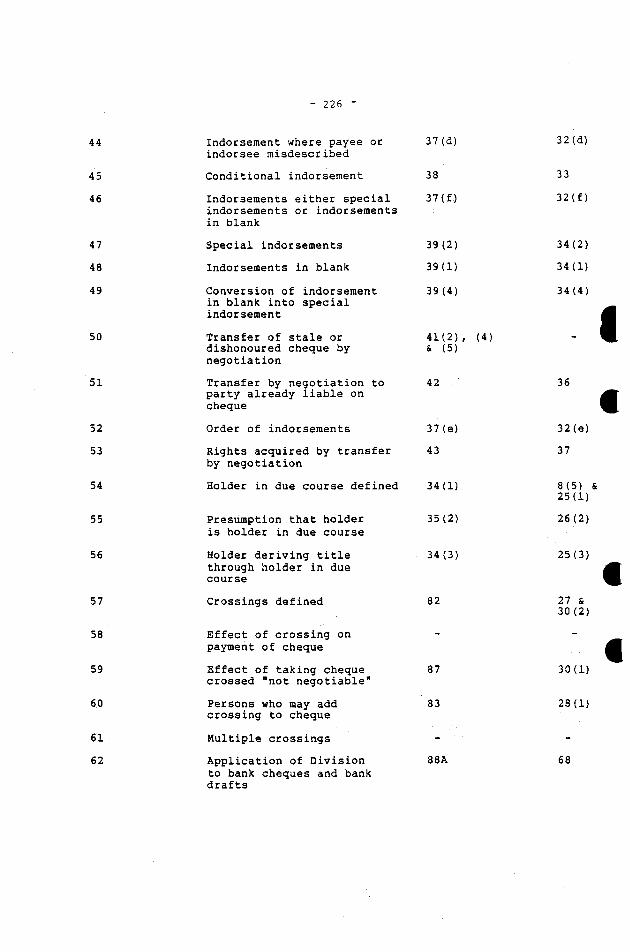

9 Cheque defined 94

10 Order to pay 96

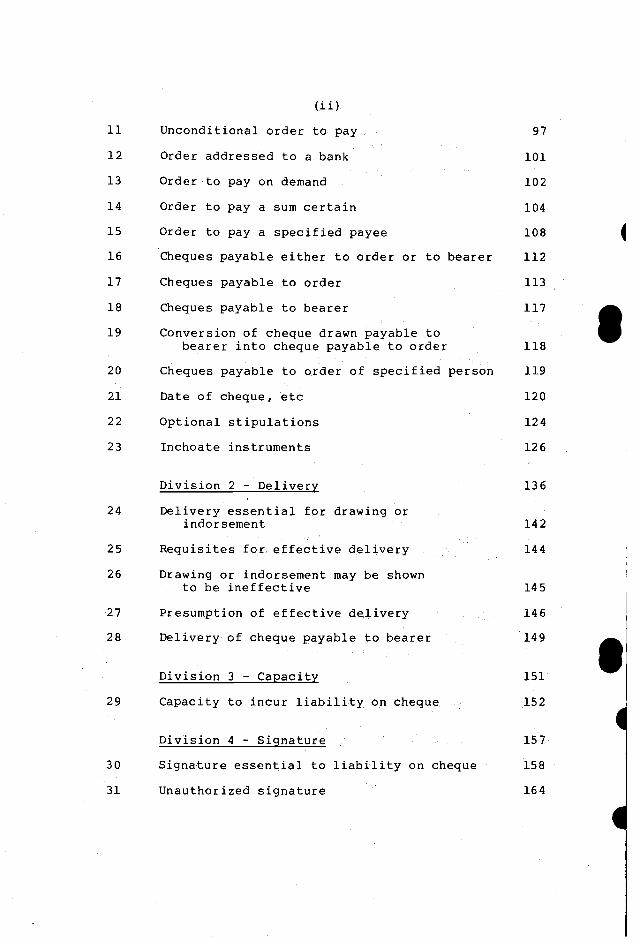

(ii)

11 Unconditional order to pay 97

12 Order addressed to a bank 101

13 Order to pay on demand 102

14 Order to pay a sum certain 104

15 Order to pay a specified payee 108 416 Cheques payable either to order or to bearer 112

17 Cheques payable to order 113

18 Cheques payable to bearer 117

19 Conversion of cheque drawn payable tobearer into cheque payable to order 118

20 Cheques payable to order of specified person 119

21 Date of cheque, etc 120

22 Optional stipulations 124

23 Inchoate instruments 126

Division 2 - Delivery 136

24 Delivery essential for drawing orindorsement 142

25 Requisites for effective delivery 144

26 Drawing or indorsement may be shown

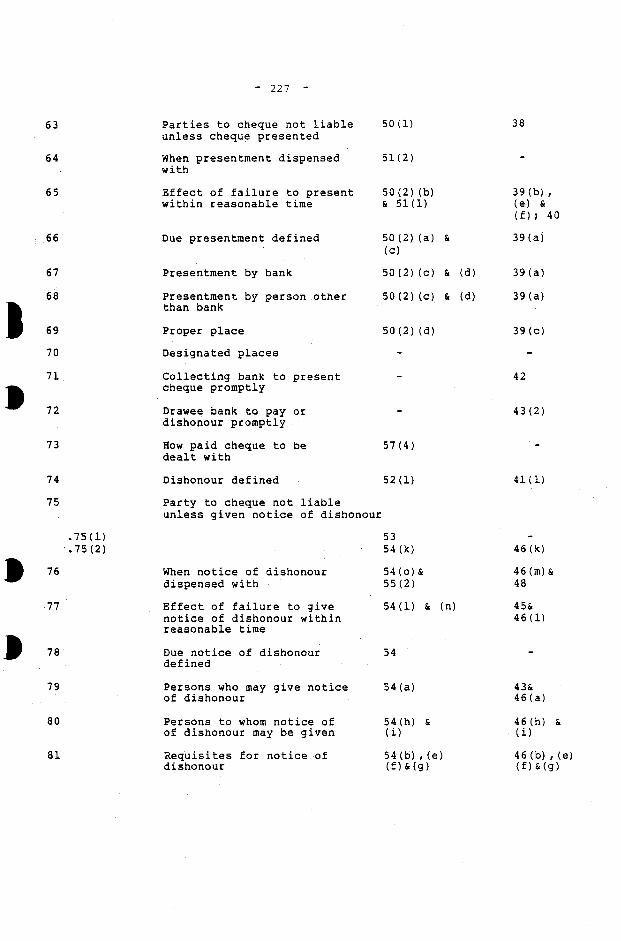

to be ineffective 14527 Presumption of effective delivery 146

28 Delivery of cheque payable to bearer 149

Division 3 - Capacity 151

29 Capacity to incur liability on cheque 152

Division 4 - Signature 157

30 Signature essential to liability on cheque 158

31 Unauthorized signature 164

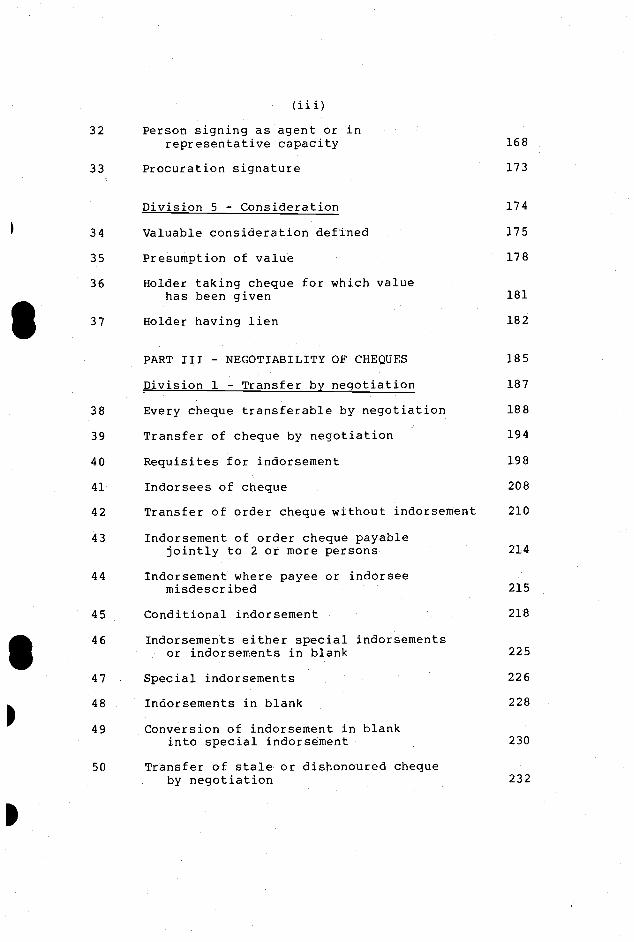

(iii)

32 Person signing as agent or inrepresentative capacity 168

33 Procuration signature 173

Division 5 - Consideration 174

34 Valuable consideration defined 175

35 Presumption of value 178

36 Holder taking cheque for which valuehas been given 181

37 Holder having lien 182

PART III - NEGOTIABILITY OF CHEQUES 185

Division 1 - Transfer by negotiation 187

38 Every cheque transferable by negotiation 188

39 Transfer of cheque by negotiation 194

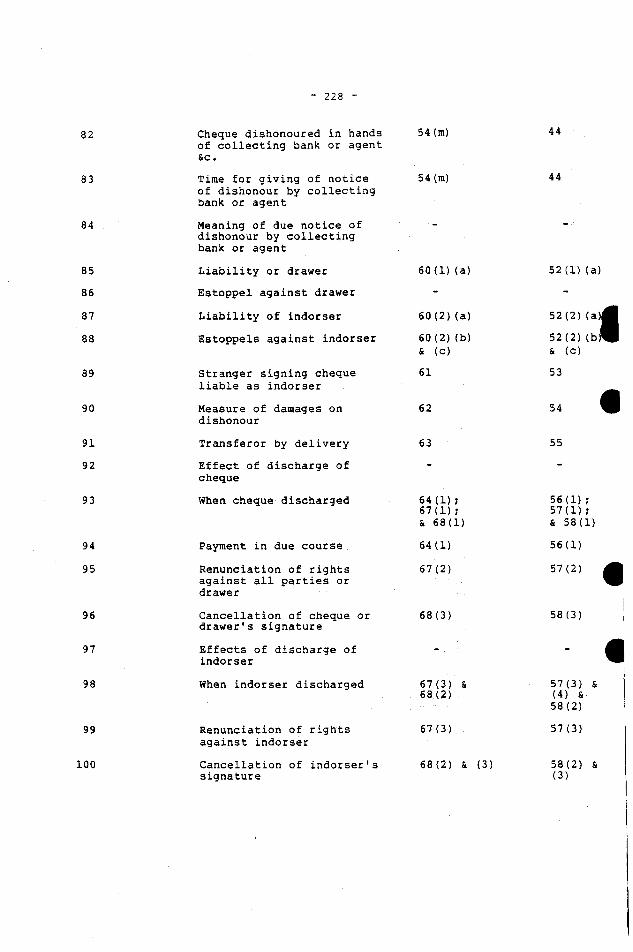

40 Requisites for indorsement 198

41 Indorsees of cheque 208

42 Transfer of order cheque without indorsexnent 210

43 Indorsement of order cheque payablejointly to 2 or more persons 214

44 Indorsemerit where payee or indorseemisdescribed 215

45 Conditional indorsement 218

46 Indorsements either special indorsementsor indorsements in blank 225

47 Special indorsernents 226

48 Indorsements in blank 228

49 Conversion of indorsement in blankinto special indorsement 230

50 Transfer of stale or dishonoured chequeby negotiation 232

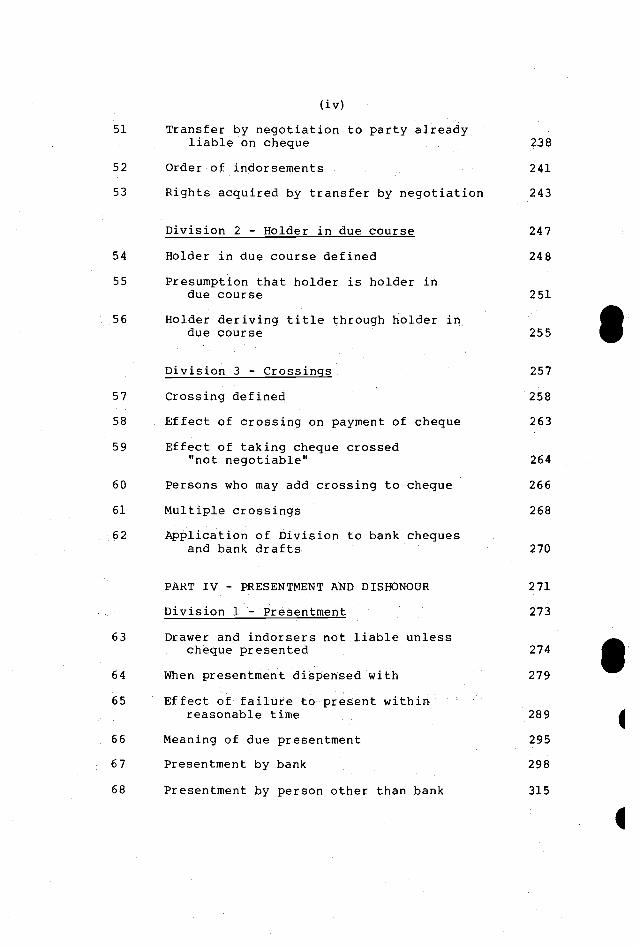

(iv)

51 Transfer by negotiation to party already

liable on cheque 23852 Order of indorsements 241

53 Rights acquired by transfer by negotiation 243

Division 2 - Holder in due course 247

54 Holder in due course defined 248

55 Presumption that holder is holder in

due course 251

56 Holder deriving title through holder in

due course 255

Division 3 — Crossings 257

57 Crossing defined 258

58 Effect of crossing on payment of cheque 263

59 Effect of taking cheque crossed“not negotiable” 264

60 Persons who may add crossing to cheque 266

61 Multiple crossings 268

62 Application of Division to bank cheques

and bank drafts 270

PART IV - PRESENTMENTAND DISHONOUR 271

Division 1 - Presentment 273

63 Drawer and indorsers not liable unlesscheque presented 274

64 When presentment dispensed with 279

65 Effect of failure to present withinreasonable time 289 4

66 Meaning of due presentment 295

67 Presentment by bank 298

68 Presentment by person other than bank 315

I

(v)

69 Proper place 316

70 Designated places 318

71 Collecting bank to present cheque promptly 322

‘72 Drawee bank to pay or dishonour promptly 331

73 How paid cheque to be dealt with 336

Division 2 - Dishonour 341

74 Dishonour defined 342

75 Party to cheque not liable unless givennotice of dishonour 346

76 When notice of dishonour dispensed with 353

77 Effect of failure to give notice ofdishonour within reasonable time 360

78 Due notice of dishonour defined 367

79 Persons who may give notice of dishonour 368

80 Persons to whom notice of dishonour maybe given 369

81 Requisites for notice of dishonour 373

82 Cheque dishonoured in hands of collectingbank agent, etc 379

83 Time for giving notice of dishonour bycollecting bank or agent 385

84 Meaning of due notice of dishonour bycollecting bank or agent 394

PART V - LIABILITIES ON CHEQUES 397

Division 1 - Liabilities of parties 399

85 Liability of drawer 400

86 Estoppel against drawer 404

87 Liability of indorser 409

(vi)

88 Estoppels against indorser 412

89 Stranger signing cheque liable as indorser 414

90 Measure of damages on dishonour 420

91 Transferor by delivery 426

Division 2 - Discharge of liabilities

ot parties 429

92 Effect of discharge of cheque 430

93 When cheque discharged 440

94 Payment in due course 443

95 Renunciation of rights against

all parties or drawer 444

96 Cancellation of cheque or drawer’s

signature 447

97 Effect of discharge of indorser 453

98 When indorser discharged 454

99 Renunciation of right against indorser 457

100 Cancellation of iridorser’s signature 459

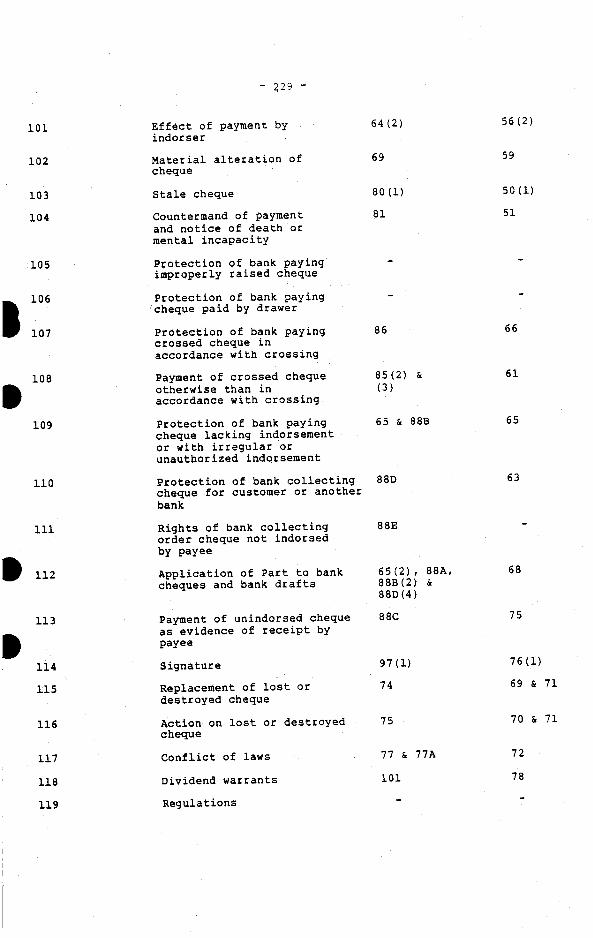

101 Effect of payment by indorser 461

102 Material alteration of cheque 465

PART VI - DUTIES AND LIABILITIES OF BANKS 483

Division 1 - The drawee bank 485

103 Stale cheque 487 5’104 Countermand of payment and notice of death

or mental incapacity 489

105 Protection of bank paying improperly 4raised cheque 493

106 Protection of bank paying chequepaid by drawer 496

I

(vii)

107 Protection of bank paying crossed cheque

in accordance with crossing 498

108 Payment of crossed cheque otherwise than

in accordance with crossing 502

109 Protection of bank paying cheque lackingindorsement or with irregular orunauthorized indorsement 507

Division 2 - The collecting bank 515

110 Protection of bank collecting chequefor customer or another bank 516

111 Rights of bank collecting order chequenot indorsed by payee 521

Division 3 - Miscellaneous 523

112 Application of Part to bank cheques andbank drafts 524

PART VII - MISCELLANEOUS 525 A

113 Payment of unindorsed cheque as evidenceof receipt by payee 526

114 Signature 528

115 Replacement of lost or destroyed cheque 530

116 Action on lost or destroyed cheque 533

117 Conflict of laws 535

118 Dividend warrants 550

119 Regulations 552

(viii)

ABBREVIATIONS

The following is a list of abbreviations used:

Anderson - Uniform Commercial Code (2nd ed.)

BEA - Bills of E~change Act 1909

Bill - Cheques Bill 1984

Byles - Byles on Bills of Exchange (23rd

ed. 1972)

Chalmers - A Digest of the Law of Bills of

Exchange (13th ed.)

Falconbridge - Essays on the Conflict of Laws

(1947)

Manning and - The Law of

Farquharson Banker and Customer in Australia

(1947)

Holden - The Law and Practice of Banking

Vol. 1 Banker and Customer (1970)

Indian BLC Report - Report on Negotiable Instruments

Law of the Banking Laws Committee

(Government of India) (1975)

Manning Report - Report dated 1 May 1964 of the

Committee appointed by the

Commonwealth Government to review

the BEA

(ix)

MD - Draft Bill for proposed Cheques Act

set out in the Fourth Schedule to

Manning Report

Paget - Paget’s Law of Banking (8th ed.)

Rajanayagam - The Law Relating to Negotiable

Instruments in Australia (1980)

Riley - Riley’s Bills of Exchange in

Australia (3rd ed.)

Russell and Edwards - The law relating to Bills of

Exchange in Australia (2nd ed.)

UCC - United States Uniform Commercial

Code : 1972 official text with

comments. 1972 The American Law

Institute and National Conference

of Commissioners on Uniform State

Laws. The main purpose of the Code

is to provide a body of rules on

the principal commercial

transactions to be adopted by the

legislatures of all the American

States and so to produce uniformity

in the legal control of the

principal areas of öommerce. The

first Official Text was produced in

1951 and adopted by the State of

Pennsylvania in 1953. The present

Official Text is that of 1972arid

this has been adopted by all States

except Louisiana which has adopted

only some of the Articles. The

(x)

Conference and the American Law

Institute have established a

Permanent Editorial Board to keep

the Code under review, to make

recommendations for its improvement

and to seek to maintain uniformity

The Code is by no means

self-contained and expressly

provides that the general law on

such matters as principal and

agent, mistake and bankruptcy

continue to apply unless

inconsistent with the express

provisions of the Code

Weaver and Craigie - The Law Relating to Banker and

Customer in Australia (1975)

S4

I

OUTLINE

Cheques Bill 1984

The Cheques Bill 1984 provides for a separate law

relating to cheques.

2. The purpose of the Bill is to revise the provisions

of the BEA applicable to cheques, to clarify the law in areas

of existing uncertainty and to make certain substantive

changes to the law on cheques the majority of which are based

on recommendations of the Manning Committee Report.

3. Considerable work has been carried out in recent

years on the preparation of the legislation. Discussions have

taken place over several years with the Australian Bankers’

Association, the Australian Merchant Bankers’ Association, the

Commercial Law Association of Australia and the Law Council of

Australia, and the assistance of these bodies is gratefully

acknowledged. The views of the State and Northern Territory

Governments, the Australian Association of Permanent Building

Societies, the Australian Association of Credit Union Leagues,

the Australian Bank Employees’ Union, the Commonwealth Bank

Officers’ Association and the Federated Miscellaneous Workers’

Union were also sought in the course of the preparation of the

legislation.

4. The Bill will come into effect on a date to be fixed

by Proclamation.

5. The Bill is being exposed to enable comments to be

made by interested persons. Such comments should be submitted,

in writing, to the Business Affairs Division of the

Attorney-General’s Department, Canberra, by 18 May 1984. The

attention of persons submitting such comments is directed to

the Freedom of Information Act 1982.

—2—

BACKGROUND

Bills of Exchange Act 1909

6. The present statute law in Australia relating to

cheques is contained in the BEA.

7. The BEA deals primarily with bills of exchange and

with the cheque as a particular species of bill.

8. The BEA is ‘in the main a transcript of the English

Act of 1882’ (Stock Motor Ploughs Limited v. Forsyth (1932) 48

C.L.R. 128, 137 per Dixon J.).

The Bills of Exchange Act 1882 (U.K.)

9. The UK Act was drafted by Sir McKenzie Chalmers. Its

preparation has been described by Russell and Edwards (pp. 3

and 4) as follows:

‘Such being the state of things when Chalmerscommenced his work, he began it by preparing asummary of 2,500 reported cases, then collating hissummary With the existing Statutes, he firstpublished a digest which was simply a new form oftext book competing with the existing text books ofChitty and Byles; then he was retained by societiesof bankers and merchants to prepare a consolidatingBill to put before Parliament. Practically, he turnedhis digest into that Bill. Chalmers himself statesthat the success of the Bill depended on the wiselines laid down by Lord Herschell.

He insisted’, says Chalmers, “that the Billshould be introduced in a form which did nothing morethan codify the existing law, and that all amendmentsshould be left to Parliament. A Bill which merely 4improves the form, without altering the substance, ofthe law creates no opposition, and gives very littleroom for controversy. Of course codification pure andsimple is an impossibility. The draftsman comesacross doubtful points of law which he must decideone way or the other. Again, voluminous though ourcase law is, there are occasional gaps which a

—3—

codifying Bill must bridge over if it aims atanything like completeness. Still, in drafting theBills of Exchange Bill, my aim was to reproduce asexactly as possible the existing law, whether itseemedgood, bad or indifferent in its effects.”

In point of fact the statute in its final formdid something more than mere codification. A fewamendments were made to the draft bill by Parliamentin committee. English and Scotch law were broughtinto line on points where the difference was not toowide, and as Chalmers himself states, a few sectionswere designedly inserted to settle doubtful points oflaw.’

10. The UK Act became the pattern for similar codes inmost of the English speaking world:

‘It was intended to be, and has been since, regardedand used as a code of law upon this subject. Sosuccessful were the efforts of those who endeavouredto codify the law and give expression to it in thatenactment, that since 1882 it has stood as the law ofthe United Kingdom with but one amendment, which isincorporated in clause 88 of the measure now beforehonourable senators, making provision for protectinga banker who, in the ordinary course of businessreceives payment of a crossed cheque. Apart from thatamendment, the proposed law as attempted to be setforth in this Bill is the expression of what is thelaw today, not only in the United Kingdom, butpractically also in every one of the States of theCommonwealth.’

(Extract from second reading speech of Senator Keating(Minister for Home Affairs) on Australian Bill that became BEA- 18 July 1907 - Hansard pp 651-2

Developments subsequent to the 1882 U.K. Act

11. Since the end of the nineteenth century there has

been a striking change in commercial practice. The use of

bills of exchange in domestic and international transactions

has declined (even though the bill has become an important

technique in financing in Australia - see D S Clarke

‘Contemporary Practice in the Commercial Bill Market’

9 Commercial Law Association Bulletin (1977) p. 143) and the

use of cheques has increased enormously

—4-

12. In the Uhited Kingdom, a solution to the problem of

unnecessary indorsement of cheques was attempted in the

Cheques Act 1957. The position is the same in New Zealand

where a Cheques Act (1960) along the lines of the 1957 Act was

enacted. Both these Acts were designed to do away with the

necessity for the indorsement of order cheques paid into the

account of the payee.

13. Since the enactment of the BEA, uncertainties have

developed in some areas of the law on cheques while some

provisions in the Act have become obsolete. New computer

technology developed in the last decade for scanning and

processing essential details of cheques now enables those

details to be transmitted between banks more quickly and

cheaply than sending cheques themselves.

Manning Committee

14. On 13 April 1962, the CommonwealthGovernment

established a Committee to review the BEA. This Committee was

chaired by the late Mr Justice Manning of the Supreme Court of

New South Wales and is hereafter referred to as the ‘Manning

Committee’.

15. The terms of reference of the Manning Committee were

as follows:

‘1. To consider the provisions of the Bills ofExchange Act 1909 - 1958 and to recommend anyalterations to that Act that may be thoughtdesirable.

2. In particular to consider whether any of thechanges effected in the British law by theCheques Act, 1957, should be adopted inAustralia.

3. For the purposes of the foregoing, to seek andconsider expressions of opinion from relevantbodies and members of the public.

—5—

4. To report to the Government the conclusions ofthe Committee with regard to 1 and 2 above.

16. The Manning Committee reported on 1 May 1964 and its

main recommendations were as follows:

Cheques Bill

1. There should be a separate Act to deal withcheques (paras. 44 and 319)

2. There should be no provision for the making ofnon-transferable cheques - in the interests ofbanking efficiency and people who do not havecheque accounts (para. 60)

3. There should be no provision for account payeecrossings. The Committee felt that suchcrossings gave no greater protection than a ‘notnegotiable’ crossing (paras. 86 and 87).

4. The use of two parallel transverse lines, withor without the words ‘not negotiable’, should bethe sole method of crossing a cheque (para. 89)

5. The words ‘not negotiable’ should be capable ofbeing used only in conjunction with two paralleltransverse lines (para. 89)

6. Crossings should not involve the words ‘bank’ or‘and company’ (para. 89).

*7~ Where an order cheque is paid to the credit of

the payee’s account, indorsement should not berequired (para. 105)

*8. Recommendation 7 above should apply when the

name of the payee appearing on the chequereasonably and sufficiently identifies thecustomer (para. 111)

*9~ Existing protection for collecting bankreceiving payment ‘in good faith and withoutnegligence’ should be extended to cover allcheques instead of being limited to crossedcheques (para. 127)

*10. The paying bank should be relieved of concern as

to the presence or absence of indorsements onlywhen it pays the cheque to a collecting bank(para. 140)

—6—

*11. A cheque drawn to order, whether indorsed orunindorsed, which appears to have been paid bythe bank on which it is drawn should be primefacie evidence of the receipt by the payee ofthe sum payable by the cheque (para. 164).

12. The definition of a cheque should embrace awriting requiring the bank to pay to bearer, orto a specified person, or to a specified personor order, or to the order of a specified person,or to an object which does not purport tospecify a person, or to such an object or order,or to the order of such an object (para. 190).

13. A cheque containing a notation to the effectthat it is void if not presented within aspecified time should be deemed not to be acheque (para. 192)

14. Where the amount of a cheque appears more thanonce in the cheque and there is a discrepancybetween the amounts the lesser amount should bethe sum payable (para. 194)

15. State Companies Act provisions re signing ofcheques by company officers should be expresslypreserved (para. 201).

16. The period for stale cheques should be 15months, in lieu of present 12 months (para. 203)

17. Express provisions should be made as to thedishonour of cheques, defining the rights andliabilities of the parties (para. 211)

18. A bank with whom a cheque is lodged forcollection should be required to forward thecheque promptly and within a specified time(para. 230)

19. A bank to whom a cheque is presented for paymentshould be required to either pay or give noticeof dishonour forthwith - with a consequentialprovision for alienation of the bank’s liabilitywhere it acts honestly and reasonably etc.(para. 225).

20. There should be an express provision that acustomer has a duty to his bank to draw a chequeso as not to facilitate unauthorised alterations(para. 243).

I

—7—

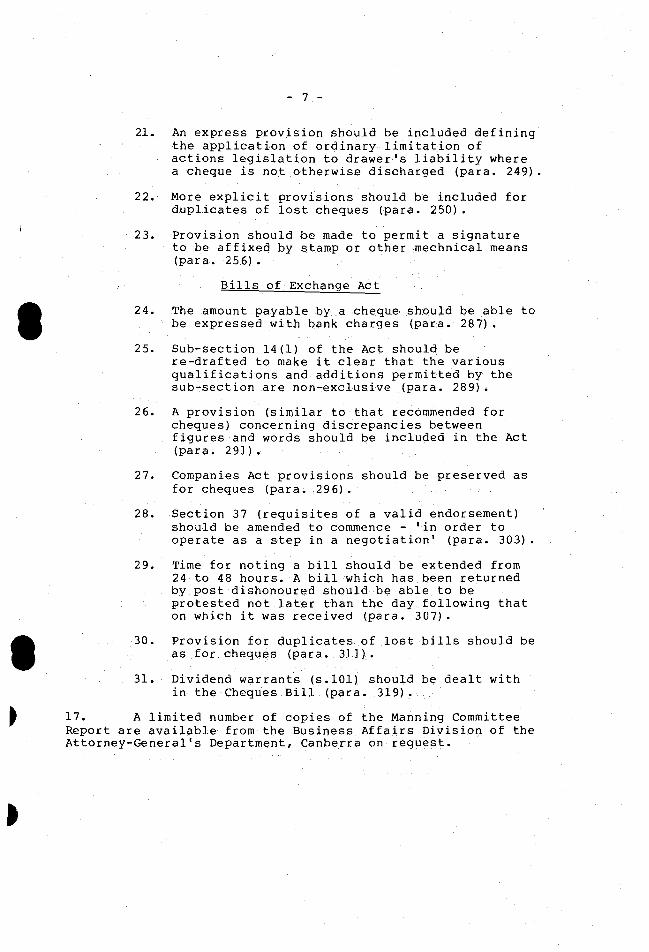

21. An express provision should be included definingthe application of ordinary limitation ofactions legislation to drawer’s liability wherea cheque is not otherwise discharged (para. 249)

22. More explicit provisions should be included forduplicates of lost cheques (para. 250)

23. Provision should be made to permit a signatureto be affixed by stamp or other mechnical means(para. 256)

Bills of Exchange Act

24. The amount payable by a cheque shouLd be able tobe expressed with bank charges (para. 287)

25. Sub-section 14(1) of the Act should bere-drafted to make it clear that the variousqualifications and additions permitted by thesub-section are non-exclusive (para. 289).

26. A provision (similar to that recommended forcheques) concerning discrepancies betweenfigures and words should be included in the Act(para. 291)

27. Companies Act provisions should be preserved asfor cheques (para. 296).

28. Section 37 (requisites of a valid endorsement)should be amended to commence - ‘in order tooperate as a step in a negotiation’ (para. 303)

29. Time for noting a bill should be extended from24 to 48 hours. A bill which has been returnedby post dishorioured should be able to beprotested not later than the day following thaton which it was received (para. 307).

30. Provision for duplicates of lost bills should beas for cheques (para. 311)

31 Dividend warrants (5 101) should be dealt within the Cheques Bill (para. 319).

17. A limited number of copies of the Manning CommitteeReport are available from the Business Affairs Division of theAttorney-General’s Department, Canberra on request.

—8—

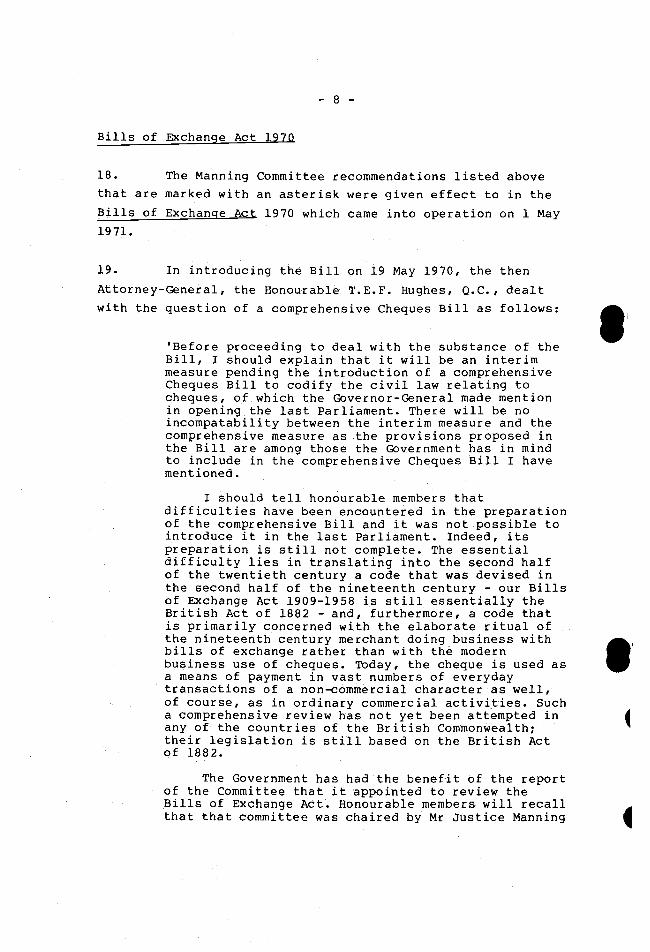

Bills of Exchange Act 19711

18. The Manning Committee recommendations listed above

that are marked with an asterisk were given effect to in the

Bills of Exchange Act 1970 which came into operation on 1 May

1971.

19. In introducing the Bill on 19 May 1970, the then

Attorney-General, the Honourable T.E.F. Hughes, Q.C., dealt

with the question of a comprehensive Cheques Bill as follows:

‘Before proceeding to deal with the substance of theBill, I should explain that it will be an interimmeasure pending the introduction of a comprehensiveCheques Bill to codify the civil law relating tocheques, of which the Governor-General made mentionin opening the last Parliament. There will be noincompatability between the interim measure and thecomprehensive measure as the provisions proposed inthe Bill are among those the Government has in mindto include in the comprehensive Cheques Bill I havementioned.

I should tell honourable members thatdifficulties have been encountered in the preparationof the comprehensive Bill and it was not possible tointroduce it in the last Parliament. Indeed, itspreparation is still not complete. The essentialdifficulty lies in translating into the second halfof the twentieth century a code that was devised inthe second half of the nineteenth century - our Billsof Exchange Act 1909-1958 is still essentially theBritish Act of 1882 - and, furthermore, a code thatis primarily concerned with the elaborate ritual ofthe nineteenth century merchant doing business withbills of exchange rather than with the modernbusiness use of cheques. ‘I\day, the cheque is used asa means of payment in vast numbers of everydaytransactions of a non-commercial character as well,of course, as in ordinary commercial activities. Sucha comprehensive review has not yet been attempted in 4any of the countries of the British Commonwealth;their legislation is still based on the British Actof 1882.

The Government has had the benefit of the reportof the Committee that it appointed to review theBills of Exchange Act. Honourable members will recallthat that committee was chaired by Mr Justice Manning I

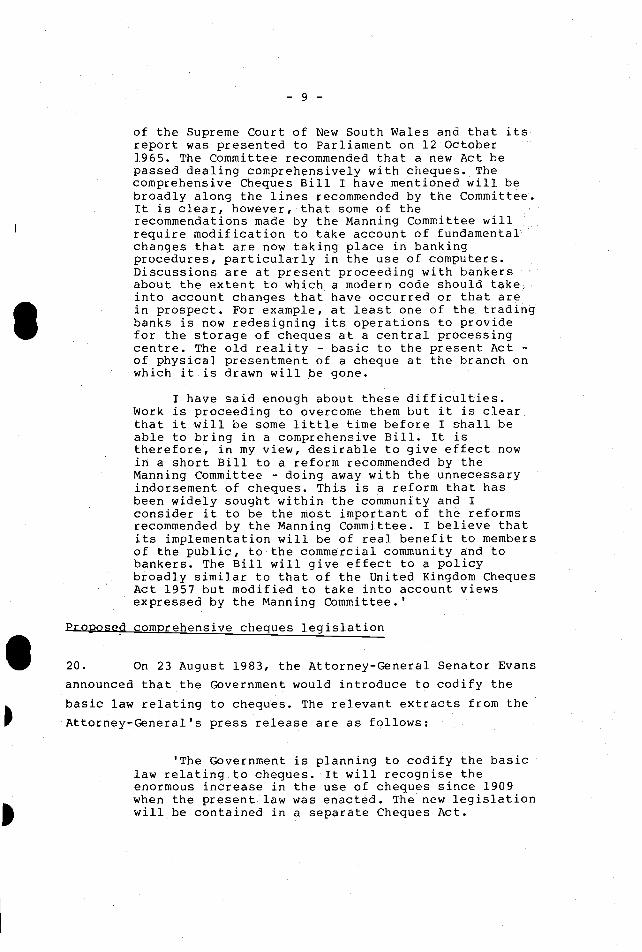

—9—

of the Supreme Court of New South Wales and that itsreport was presented to Parliament on 12 October1965. The Committee recommended that a new Act bepassed dealing comprehensively with cheques. Thecomprehensive Cheques Bill I have mentioned will bebroadly along the lines recommended by the Committee.It is clear, however, that some of therecommendations made by the Manning Committee willrequire modification to take account of fundamentalchanges that are now taking place in bankingprocedures, particularly in the use of computers.Discussions are at present proceeding with bankersabout the extent to which a modern code should takeinto account changes that have occurred or that arein prospect. For example, at least one of the tradingbanks is now redesigning its operations to providefor the storage of cheques at a central processingcentre. The old reality - basic to the present Act -

of physical presentment of a cheque at the branch onwhich it is drawn will be gone.

I have said enough about these difficulties.Work is proceeding to overcome them but it is clearthat it will be some little time before I shall beable to bring in a comprehensive Bill. It istherefore, in my view, desirable to give effect nowin a short Bill to a reform recommended by theManning Committee - doing away with the unnecessaryindorsement of cheques. This is a reform that hasbeen widely sought within the community and Iconsider it to be the most important of the reformsrecommended by the Manning Committee. I believe thatits implementation will be of real benefit to membersof the public, to the commercial community and tobankers. The Bill will give effect to a policybroadly similar to that of the United Kingdom ChequesAct 1957 but modified to take into account viewsexpressed by the Manning Committee.’

Proposed comprehensive cheques legislation

20. On 23 August 1983, the Attorney-General Senator Evans

announced that the Government would introduce to codify the

basic law relating to cheques. The relevant extracts from the

Attorney-General’s press release are as follows:

‘The Government is planning to codify the basiclaw relating to cheques. It will recognise theenormous increase in the use of cheques since 1909when the present law was enacted. The new legislationwill be contained in a separate Cheques Act.

— 10 —

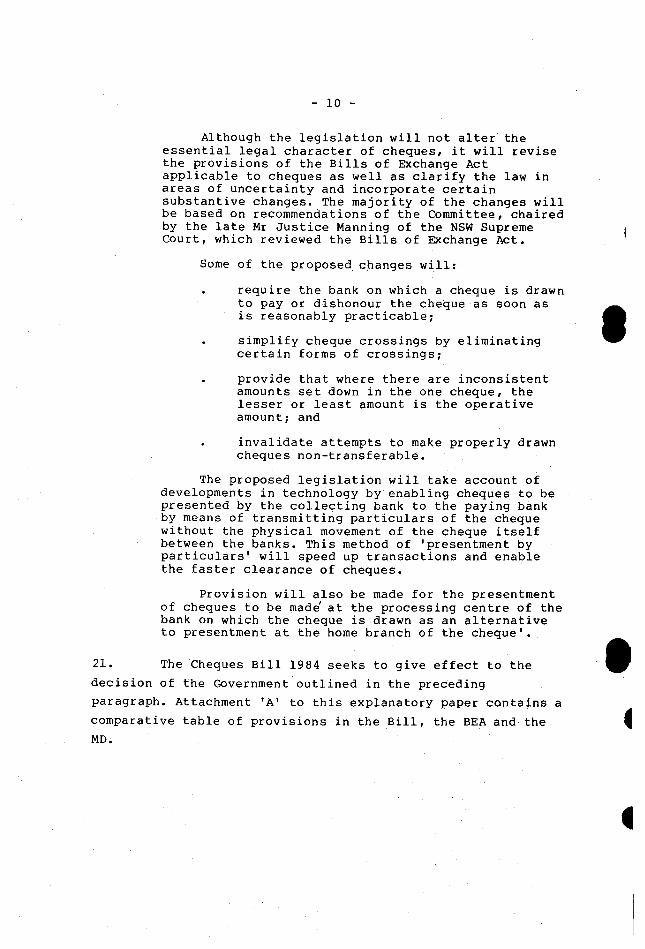

Although the legislation will not alter theessential legal character of cheques, it will revisethe provisions of the Bills of Exchange Actapplicable to cheques as well as clarify the law inareas of uncertainty and incorporate certainsubstantive changes. The majority of the changes willbe based on recommendations of the Committee, chairedby the late Mr Justice Manning of the NSW SupremeCourt, which reviewed the Bills of Exchange Act.

Some of the proposed changes will:

require the bank on which a cheque is drawnto pay or dishonour the cheque as soon asis reasonably practicable;

simplify cheque crossings by eliminatingcertain forms of crossings;

provide that where there are inconsistentamounts set down in the one cheque, thelesser or least amount is the operativeamount; and

invalidate attempts to make properly drawncheques non-transferable.

The proposed legislation will take account ofdevelopments in technology by enabling cheques to bepresented by the collecting bank to the paying bankby means of transmitting particulars of the chequewithout the physical movement of the cheque itselfbetween the banks. This method of ‘presentment byparticulars’ will speed up transactions and enablethe faster clearance of cheques.

Provision will also be made for the presentmentof cheques to be made~at the processing centre of thebank on which the cheque is drawn as an alternativeto presentment at the home branch of the cheque’.

21. The Cheques Bill 1984 seeks to give effect to the

decision of the Government outlined in the preceding

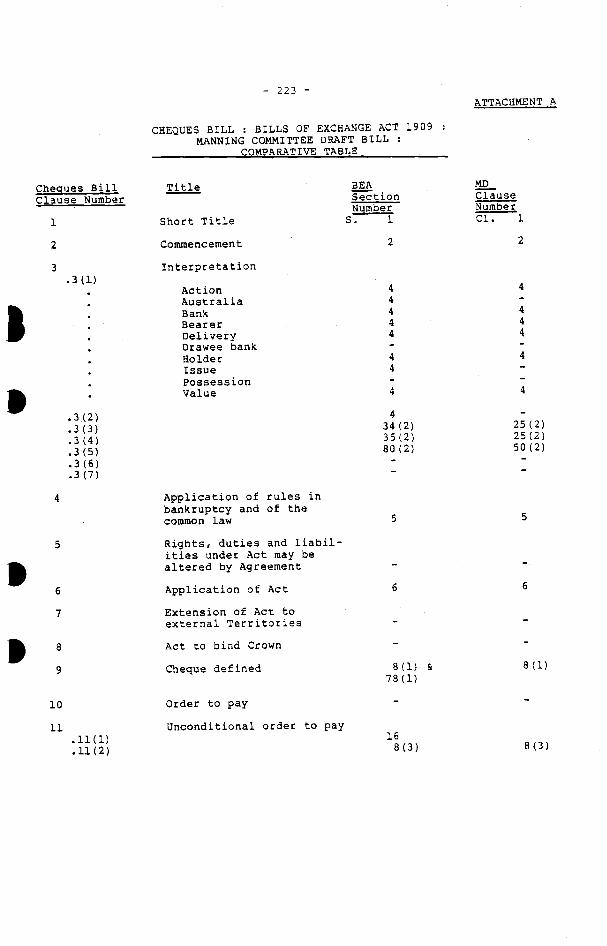

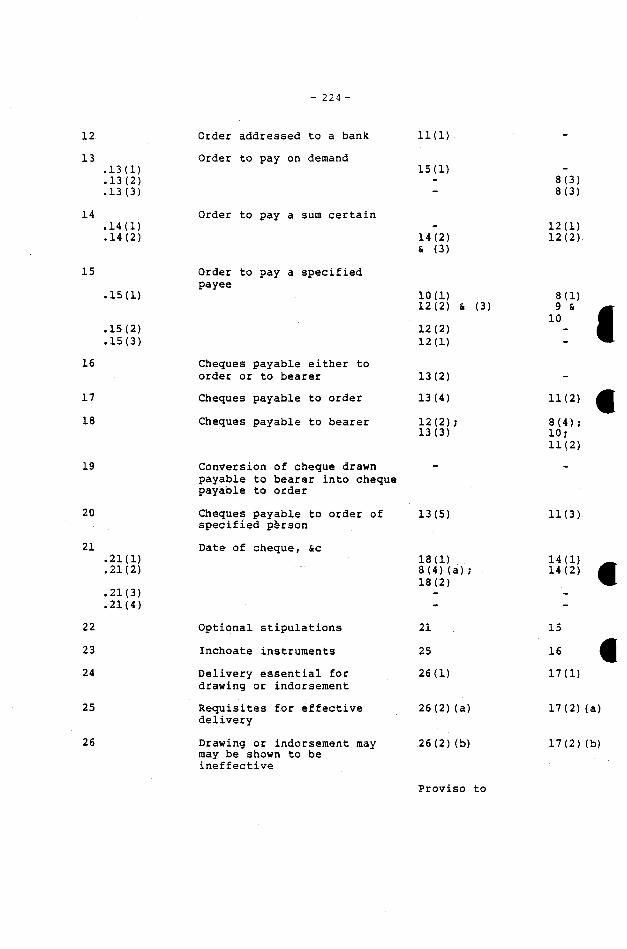

paragraph. Attachment ‘A’ to this explanatory paper contains a

comparative table of provisions in the Bill, the BEA and the 4

I

— 11 —

CHEQUESBILL 1984

22. The Bill is divided into the following parts:

PARTI

PART II

PART III -

PART IV -

PARTV -

PART VI -

PART VII - MISCELLANEOUS

23. The remainder of this explanatory paper deals,

sequentially, with each clause of the Bill.

- PRELIMINARY

- CHEQUES

NEGOTIABILITY OF CHEQUES

PRESENTMENT AND DISHONOUR

LIABILITIES ON CHEQUES

DUTIES AND LIABILITIES OF BANKS

- 12 -

BILL : PART I : PRELIMINARY

24. Part I of the Bill (cls. 1 to 5B) deals with various

preliminary matters.

Cl. 1 Short title

25. When enacted, the Bill will be cited as the Cheques

Act 1984 (Bill cl. 1 - based on MD Cl. 1).

26. The long title of the Bill also refers to ‘certain

other negotiable instruments’ to indicate that the subject

matter of the Bill is not limited to cheques. The Bill

contains provisions that deal with other negotiable

instruments that are not chequesat common law, under the BEA

or under the Bill e.g.:

(a) Inchoate instruments (see Bill ci. 23)

(b) Bank cheques and bank drafts (see e.g. Bill cls.

4 and 6); and

(c) Dividend warrants (see Bill cl. 118)

Cl. 2 : Commencement

27. The Bill will come into operation on a day to be

fixed by the Governor-General by Proclamation (Bill cl.2) .

Commencement will coincide with:

(a) Consequential amendments proposed to be made to

the BEA; and

(b) Certain Regulations that are to be made under

the Cheques Act.

— 13 —

Cl. 3 : Interpretation

28. Various interpretation provisions are included for

the purposes of the Bill (Bill cl. 3):

(a) Defined terms (see Bill s—cl. 3(1));

(b) References to indorsement of a cheque (see Bill

s—cl. 3(2));

(C) Acts done in good faith (see Bill s-cl. 3(3));

(d) Defects in title (see Bill s-cls. 3(4) and 3(5))

(e) Stale cheques (see Bill s-cl. 3(6));

(f) Signatures or indorsements without authority

(see Bill s—cl. 3(7)); and

(g) Exhibition of cheques (see Bill s-cl. 3(8)).

29. Defined Terms. The terms discussed below are defined

(Bill s-cl. 3(1)) for the purposes of the Bill unless the

contrary intention appears.

30. Action. The term ‘action’ will include a

counter-claim or set-off (same definition as in MD ci. 4 - Cf.

definition in UCC 1-201).

This term is used in the following provisions of the

Bill, among others:

Bill cls. 55 and 116.

- 14 -

31. Australia. The term ‘Australia’ will include the

external Territories as the Bill extends to every external

Territory (see Bill cl. 7). This term is used in Bill cl.

117, among others.

32. Acceptance. The term ‘acceptance’ is not defined, in

accordance with the approach of the MD. Acceptance of a cheque

by the bank upon which it is drawn is ~ unusual (Riley

p. 52 and Chalmers p. 139 and pp. 249-250) . It would seem,

however, that it is theoretically possible under the BEA for a

bank to accept a cheque drawn upon it. If the bank were to

accept such a cheque, the bank could be liable on the cheque

as an indorser (see Bill ci. 89).

33. Bank. It is intended that the provisions of the Bill

should apply to all banks, however formed or incorporated.

Specifically, the term ‘bank’ will cover:

(a) The Reserve Bank of Australia (see ss. 26’ and 27

of Reserve Bank Act 1959)

(b) A body corporate authorized under the Banking

Act 1959 to carry on banking business in

Australia (see definition of ‘bank’ in s. 5 of

Banking Act 1959)

(c) State banks (para. (c) of the definition follows

para. 5l(xiii) of the Constitution); and

(d) A person (other than a person referred to in

para. (a) , (b) or (c) above) who carries on the

business of banking outside Australia.

I

— 15 —

34 The following comments are made on the definition of

‘bank’:

(a) Weaver and Craigie (pp. 27-28) have pointed out

that the application of the definition of

‘banker’ in the BEA to Australian ‘banks’ is, in

many cases, somewhat uncertain - the definition

in s-cl. 3(1) of the Bill should overcome this

problem;

(b) If a bank operated by or on behalf of a

Territory were to be established, it would be a

bank of the kind to which para (b) of the

definition applies unless steps were taken to

exclude it from the application of the Banking

Act 1959. The special treatment given in para.

(c) of the definition to a person who carries on

State banking arises from the fact that State

banking (other than State banking extending

beyond the limits of the State concerned) is

specifically excluded from the banking power in

placitum 5l(xiii) of the Constitution. It is for

this reason that State banks are not banks

within the meaning of the Banking Act 1959. No

such exclusion exists in the case of ‘Territory’

banks;

(c) The meaning of the expression ‘the business of

banking’ in para. (d) of the definition has been

considered in a number of cases (see Riley

pp. 16-18; Rajanayagam pp. 137-143 and Weaver

and Craigie pp. 24-28) . Isaacs J., has commented

that:

‘The essential characteristics of thebusiness of banking ... may be described asthe collection of money by receiving

— 16 —

deposits on loan, repayable when and asexpressly or impliedly agreed upon, and theutilization, of the money so collected bylending it again in such sums as arerequired. These are the essential functionsof a bank as an instrument of society. Itis, in effect, a financial reservoirreceiving streams of currency in everydirection, and from which there issueoutflowing streams where and as required tosustain and fructify or assist commercial,industrial or other enterprises oradventures.’

(Commissioners of the State Savings Bank o~Victoria v. Permewan, Wri9ht and Co. Ltd (1915)19 C.L.R. 457 at 470—471)

The term has been qualified in the Bill to make it clear thatit applies only to persons, not being banks, who carry on hebusiness of banking outside Australia. The qualification isconsidered necessary so that it cannot be argued that theexpression applies to non-banks who carry on the business ofbanking in Australia.

35. Bank cheque. The expression ‘bank cheque’ and ‘bank

draft’ are used in the Bill without definition:

(a) It would appear that the meaning of both

expressions is well established in Australia and

that the terms, at least where it is not sought

to draw a distinction between bank cheques and

bank drafts, need not be defined. In Fabre v.

~ (1973) 127 CLR 665 the High Court said (at

pp 670—671)

‘It appears that for a considerable numberof years there has been a practice inAustralia of bankers issuing what have cometo be known as “bank cheques” at therequest of customers who have some reasonto provide cash or its equivalent incommercial transactions - see Union Bank ofAustralia v. McClintock [1922] 1 AC 240, atp. 245 and Manning and Farquharson : Bankerand Customer in Australia (1947), p. 38.These are drafts drawn by a bank usually onitself but occasionally upon another bankin either case they are issued in the form I

— 17 -

of cheques. It has been questioned whethera draft of this kind is a cheque withinsuch a provision as s.78 of the Bills ofExchange Act. The question arose becausethe definition of cheque incorporates thatof bill of exchange and a cheque drawn by abank upon itself is not “addressed by oneperson to another” within the latterdefinition (which is now contained ins.8(l) of the Bills of Exchange Act): seeMeclintock v. Union Bank of Australia Ltd.(1920) 20 S.R. (N.S.W.) 494. In 1932, S~3~A

was inserted in the Bills of Exchange Actmaking a banker’s draft payable on demanddrawn by or on behalf of a bank upon itselfa cheque for the purpose of the crossedcheque provisions of the Bills of ExchangeAct. However, although it may be moreaccurate to refer to a bill of exchangedrawn by a bank on itself as a banker’sdraft, the nomenclature “bank cheque” is,and has for long been, used in Australia todescribe instruments of this kind. Suchinstruments are in common use by solicitorsin the settlement of transactions,including real property transactions, incases where it is inconvenient to carrycurrency and cash or its equivalent isrequired on a settlement. The expression“banker’s cheque” may be somewhat wider inmeaning than “bank cheque” in that it mayinclude a cheque drawn by a bank uponanother bank as well as a “cheque” drawn bya bank upon itself, but it is clear thatboth expressions, “banker’s cheque” and“bank cheque”, refer only to a “cheque”which is drawn by a bank’;

(b) There is some degree of inconsistency in the BEA

(see ss. 65, 88A, 88B, 88C and 88D) in the terms

in which various provisions of that Act are

applied to bank cheques and bank drafts.

Commentators are divided on the question whether

the differences in expression in the BEA have a

different legal effect. Weaver and Craigie (pp.

261-265) are of the view that the different

expressions do not have a different legal effect

and that all of the relevant provisions of the

BEA apply to both bank cheques and bank drafts.

- 18 —

Rajanayagam (pp. 205-209) puts the opposite

view. The Bill has been drafted on the

assumption that all of the relevant provisions

of the Bill should apply to both bank cheques

and bank drafts.

36. Some of the provisions that are specifically applied

to bank cheques and bank drafts are the provisions that deal

with:

(a) The application of rules in bankruptcy and of

the common law (see Bill cl.4);

(b) The application of the Bill itself (see Bill

cl.6); and

(c) The provisions in Part VI of the Bill.

37. Bearer. The word ‘bearer’ has been defined to mean

the person in possession of a cheque payable to bearer (this

definition is to the same effect as in BEA and MD - but cf.

UCC 1—201(5)).

38. This term is used in the following provisions of the

Bill, among others:

Bill cls. 16, 18, 39(3) and 91(1).

39. Delivery. The term ‘delivery’ in relation to a

cheque will mean the transfer of posession of the cheque from

one person to another. Cf.:

(a) BEA and MD, which include the words ‘actual or

constructive’ (but see also the definition of

‘possession’); and

I

— 19 —

(b) UCC 1-201 (14) which limits the term to a

voluntary transfer.

40. The term ‘delivery’ is used in the following

provisions of the Bill, among others:

Bill cls. 24, 25, 26, 27, 42, 91 and 95.

41. Drawee bank. A drawee bank will mean the bank upon

which the cheque is drawn. There is no equivalent provision

in the BEA or MD.

42. The term ‘drawee bank’ is used in the following

provisions of the Bill, among others:

Bill cls. 66, 67, 68, 73, 102, 104, 105 and 108.

43. Holder. The term ‘holder’ will mean:

(a) the payee or indorsee of a cheque payable to

order who is in possession of the cheque as a

payee or indorsee; and

(b) the bearer of a cheque payable to bearer.

44. The term ‘holder’ has been recast when compared with

the BEA (or the MD):

(a) The definition deals separately with cheques

payable to order and cheques payable to bearer.

The BEA definition covers the payee or indorsee

of a cheque payable to bearer both under the

description of payee or indorsee and again under

the description of bearer; and

— 20 —

(b) The definition makes it clear that the payee or

indorsee of a cheque payable to order is the

holder of the cheque only if he is in possession

of the cheque as the payee or indorsee of the

cheque.

45. The term ‘holder’ is used in the following provisions

of the Bill, among others:

Bill cls. 27, 39, 42, 45, 49, 53, 54, 55, 56 and 85.

46. Indorsement. The term ‘indorsement’ is not defined in

the Bill as it is in BEA s.4. The latter provision states that

‘indorsement’ means an indorsement completed by delivery.

There is no equivalent provision in the Bill as it is

considered that:

(a) where ‘indorsement’ is used in the sense defined

in BEA s.4 it is quite clear, from the context,

that the term means the act of indorsing a

cheque completed by delivery (see e.g. Bill

s-cls. 29(4), 65(2) , 88(1) , cl. 101 and s—cls.

117(16) and 118(2)); and

(b) in the vast majority of cases the term

‘indorsement’ is used in the Bill to mean simply

the signing of a cheque by an indorser (see e.g.

Bill cls. 18, 20, s—cl. 21(1), cls. 24, 25;

s—cl. 30(4) , cl. 40, s—cl. 41(2) , paras. 45(a)

and (c), cls. 46, 47, 48, 49, 51, 52, s—cl.

89(1), cl. 109, and s-cl. 110(2)).

47. Issue. The term ‘issue’, in relation to a cheque,

will mean the first delivery of the cheque to a person who

takes the cheque as the holder of the cheque (to same effect

I

— 21 —

as BEA - no such definition in MD) . This term is used in Bill

cl. 117, among others.

48. The requirement in the BEA that the cheque be

‘complete in form’ has not been retained. The following

comments are made in relation to the expression:

(a) The definition of ‘issue’ in UCC 3-102 omits

this requirement apparently because it was

thought to be inconsistent with the inchoate

instrument provisions of the UCC (see Anderson

V. 2, p. 584);

(b) The effect of the requirement would seem to be

that the delivery of a cheque to the payee is

not the issue of the cheque if the cheque is not

complete in form at that time. This could mean

that the first transfer by negotiation of the

cheque after the cheque has been completed also

serves as the issue of the cheque or,

alternatively, that the subsequent completion of

the cheque operates retrospectively so as to

make the earlier delivery of the cheque to the

payee the issue of the cheque. On the first of

these alternatives there could be a transfer by

negotiation of a cheque before its issue. This

would seem to be conceptually inconsistent with

the principles underlying the BEA (see

Rajanayagam p. 62 and Anderson V. 2,

pp. 586-587) . On the second of these

alternatives a cheque that is discharged (see

Bill cl. 93) before its completion could never

be said to have been issued;

— 22 —

(c) The requirement causes difficulty in applying

some of the provisions of the Bill to cheques

that are incomplete in form. For example, the

requirement causes difficulty in applying Bill

cl. 26 (which provides that delivery may be

shown to have been conditional or for a special

purpose) to cheques that are incomplete in form;

(d) The meaning of the requirement is itself

unclear. Can there be a ‘cheque’ before it is

‘complete in form’? In other words, is the

requirement merely superfluous?;

(e) The Indian BLC Report (p. 67) recommended that

the UCC approach of omitting the reference to

completeness in form should be adopted.

49. Person. The term ‘person’ is undefined (cf. BEA and

MD which both had such a definition) . It is not necessary to

define this term (see sec. 22 of the Acts Interpretation Act

1901)

50. Possession. The term ‘possession’ will mean in

relation to a cheque, both actual and constructive possession.

‘Possession’ is not defined separately in the BEA or the MD

but appears in the definition of ‘delivery’. There are various

references in the Bill to a person in possession of a cheque

(e.g. Bill cls. 23, 60 and 61). There seems to be no reason

why the term ‘possession’ in these provisions should not, as

in the definition of ‘delivery’ in the BEA, mean actual or

constructive possession. The meaning given to the term by the

definition would appear to be the meaning currently given to

the term in the BEA (see Chalmers p. 7).

I

— 23 —

51. Value. The term ‘value’ will mean valuable

consideration as defined in Bill ci. 34 (same as BEA and MD

except that there is now a specific cross-reference).

Other interpretation provisions

52. There are also other interpretation provisions

contained in the Bill.

S 53. Acts done in good faith. A reference to an act being

done in good faith will be a reference to the act being done

honestly, whether or not the act is done negligently (Bill

s-cl. 3(2) - based on BEA s. 96 and MD cl. 73).

54. The concept of doing an act or thing in good faith is

used in the following provisions of the Bill, among others:

Bill cis. 54 and 55.

55. Defects in title. Where a person obtains a cheque by

fraud, duress or other unlawful means or for an illegal

consideration, his title to the cheque will be defective (Bill

s-cl. 3(3) - cf. BEA s-sec. 34(2) and MD s-cl. 25(2)). This

provision will not limit by implication the circumstances in

which the title of a person to a cheque is defective (Bill

s-cl. 3(4) - no corresponding provision in BEA or MD)

56. The interpretation provision in s-cl. 3(3), like

s-sec. 34(2) of the BEA, applies, in its terms, only to the

title of the transferor of a cheque. As the s-cl. is not

limited in application to the provision in the Bill that

defines holder in due course for the purposes of the Bill (cf.

BEA s-sec. 34(2)), the indirect application of the s-cl. has,

perhaps, been strengthened from the existing law. However the

language of Bill cls. 55 (‘Presumption that holder is holder

in due course’) and 56 (‘Holder deriving title through holder

— 24 —

in due course’) is still not completely consistent with the

interpretation provision in Bill s-cl. 3(2) . Consideration is

accordingly being given to whether it would be desirable to

have a general defintion of defective title that is capable of

applying directly to both the transferor, and the

transferee/holder, of a cheque.

57. The provisions relating to defects in title are of

general application and will have particular application to

the provisions dealing with:

(a) Transfer of stale or dishonoured cheque (see

Bill s—cls 50(1) and 50(2));

(b) Rights of holder (see Bill s-cls 53(2) and (3));

(c) A holder in due course (see Bill s-cl. 54(1));

and

(d) Payment in due course (see Bill cl. 94).

58. Stale cheque. The term ‘stale cheque’ will mean a

cheque that appears, on its face, to have been drawn for more

than 15 months (Bill s-cl. 3(5). This definition is based on

that in the BEA (s-sec. 80(2)) except that:

(a) The period of time has been extended from 12 to

15 months. This was recommended by the Manning 5Committee (para. 203 - MD s-cl. 50(2)) to

overcome what it felt was an inconvenience under

the present law that:

‘At the beginning of a new calendar year

drawers of cheques may inadvertently refer

to the year just ended when dating their

cheques’; and

— 25 —

(b) The definition of ‘stale cheque’ makes use of

the concept of a cheque appearing, on its face,

to have been ‘drawn’ and not, as in the course

of the BEA, to the cheque having been ‘in

circulation’ for the relevant length of time.

The concept of a cheque having been ‘in

circulation’ is not used elsewhere in the Bill

and seems to be used in the definition as a

colloquial way of saying that a stale cheque is

a cheque that appears, on its face, to have been

issued more than 15 months ago (see Riley

p. 194; Rajanayagam p.109 and Weaver and Craigie

pp. 278, 338 and 367). However the concept of a

cheque becoming stale 15 months after its

‘issue’ is not used in the Bill because of

possible difficulties in identifying when a

cheque is in fact issued i.e., when the drawing

is completed by delivery. The date on which a

cheque is drawn will, on the other hand, will be

able to be easily identified because it will be

conclusively presumed to be the date of the

cheque (see Bill s-cl. 6(2)).

59. Placement of signature or indorsement without

authority. A reference to a signature or indorsement being

written or placed on a cheque without authority will extend to

a forgery (Bill s-cl. 3(6) - no corresponding provision in BEA

or MD).

60. This interpretation provision relates to the

provisions dealing with:

(a) Unauthorized signature (see Bill cl. 31) ; and

— 26 —

(b) The protection of a bank paying a cheque that

lacks an indorsement or with an irregular or

unauthorized indorsement (see Bill para. 109(b)).

61. References to cheques being exhibited. A reference to

a cheque being exhibited will include a reference to a cheque

being delivered (Bill s-cl. 3(7)). This interpretation

provision is intended to overcome any doubt that exhibiting a

cheque may not involve a transfer of possession, and relates

to provisions dealing with: 5(a) Presentment by bank (see Bill cl. 67)

(b) Presentment by person other than bank (see Bill

cl.68); and

(c) Dealing with a paid cheque (see Bill cl. 73).

S

I

— 27 —

Cl. 4 Application of rules in bankruptcy and of the common law

62. Rules in bankruptcy. Nothing in the Bill will affect

the application to cheques of ‘the rules in bankruptcy’ under

the Bankruptcy Act 1966 or the law of an external Territory

(Bill s-cl. 4(1)) and see ss. 124 and 125 of the Bankruptcy

Act 1966)

63. The phrase ‘the rules in bankruptcy’ (used in BEA

S s-sec. 5(1)) has been used in preference to the phrase ‘the

law of bankruptcy’ (used in MD s-cl. 5(1)). The Bankruptcy Act

1966 creates a law of bankruptcy that applies only to the

bankruptcy of natural persons. Although s-sec. 438(2) of the

• Companies Act 1981 applies certain of the rules in bankruptcy

to the winding up of insolvent companies, it does not apply

the law of bankruptcy, as such, to the winding up of companies

(but see s-sec. 438(1) Companies Act 1981 which makes all

debts payable on a contingency and all claims admissible to

proof against the company in every winding up ‘subject in the

case of insolvent companies to the application in accordance

with the provisions of the LCompanies) Act of the Bankruptcy

Act 1966’).

64. Application of common law. The rules of the common

law (including the law merchant) will continue to apply in

relation to cheques except in so far as they are inconsistent

with express provisions of the Bill (Bill s-cl. 4(2) - of the

same effect as BEA s-sec. 5(2) and MD s-cl. 5(2)).

65. Bill s.—cl 4(2) is designed to meet cases not‘ exhaustively dealt with by other provisions and will not apply

where there are express provisions in the Bill inconsistent

with the rules of common law. It preserves, for example, the

common law doctrine of estoppel and the rules of private

international law.

— 28 —

66. Bank cheques and bank drafts. The provisions as to

the application of rules in bankruptcy and of the common law

will also apply to a bank cheque or a bank draft (Bill

s—cl. 4(3)).

Cl. 5 Rights, duties and liabilities under Bill may be

altered by agreement

67. The Bill will not prevent persons altering their own

rights, duties or liabilities by agreement (Bill cl. 5 - no

equivalent in BEA or MD.). However, it is noted that the Bill

is currently being examined with a view to identifying the

provisions (if any) that create rights, duties or liabilities

that should not, as a matter of policy, be altered by

agreement.

68. The purpose of this provision is to correct an

impression which may be otherwise gained that such an

alteration is not possible. The provision should enable the

courts to give direct effect to the intentions of the parties.

The provision can be regarded as a particular instance of the

preservation of the rules of the common law in relation to

cheques (see Bill s-cl. 4(2)) and would not seem to represent

a change from the law applying under the BEA.

69. Position under BEA. Although the BEA appears to

contain a complete and authoritative code relating to the

rights, duties and liabilities of parties on bills of

exchange, the cases show that parties in direct relationship

with each other may negative, invert or otherwise vary the

rights, duties and liabilities established by the BEA. A

particular example concerns the right of parties to a bill to

rights, duties and liabilities arising out of an indorsement.

— 29 —

70. Indorsement. Contrary to the impression gained from

a reading of s-sec. 60(2) of the BEA, it is open to parties to

a bill to alter, by agreement, the rights, duties and

liabilities created by an indorsement of the bill (see

Falconbridge pp. 770-771).

71. Perhaps the clearest judicial exposition of this

principle is to be found in the judgment of the Privy Council

delivered by Sir William Maule in Castrigue v. Buttigieg

((1855) 10 Moo. P.C.C. 94, 108—109; 14 E.R. 427, 433) where he

said:

The liability of an indorser to his immediateindorsee arises out of a contract between them, andthis contract in no case consists exclusively in thewriting popularly called an indorsement, and which isindeed necessary to the existence of the contract inquestion, but that contract arises out of the writtenindorsement itself, the delivery of the Bill to theindorsee, and the intention with which that deliverywas made and accepted, as evinced by the words,either spoken or written, of the parties, and thecircumstances (such as the usage at the place, thecourse of dealing between the parties and theirrespective situations) under which the delivery takesplace: thus a Bill, with an unqualified writtenindorsement, may be delivered and received for thepurpose of enabling the indorsee to receive the moneyfor account of the indorser, or to enable theindorsee to raise money for his own use on the creditof the signature of the indorser, or with an expressstipulation that the indorsee, though for value, isto claim against the drawer and acceptor only, andnot against the indorser, who agrees to sell hisclaim against the prior parties, but stipulates notto warrant their solvency. In all these cases theindorser is not liable to the indorsee, and they areall in conformity with the general law of contracts,which enables parties to them to limit and moditytheir liabilities as they think fit, provided they donot infringe any prohibitory law.’ (emphasis added)

72. In McDonald v. Whitfield (1883) 8 A.C. 733, at

744-745 Lord Watson, delivering the judgment of the Privy

Council, put the matter as follows:

- 30 —

‘Their Lordships see no reason to doubt that theliabilities inter se of the successive indorsers of abill or promissory note must, in the absence of allevidence to the contrary, be determined according tothe ordinary principles of the law-merchant. He whois proved or admitted to have made a priorindorsement must, according to these principles,indemnify subsequent indorsers. But it is a wellestablished rule of law that the whole facts andcircumstances attendant upon the making, issue andtransference of a bill or note may be legitimatelyreferred to for the purpose of ascertaining the truerelation to each other of the parties who put theirsignatures upon it, either as makers or as indorsers;and that reasonable inferences, derived from thesefacts and circumstances, are admitted to the effectof qualifying, altering, or even inverting therelative liabilities which the law-merchant wouldotherwise assign to them. It is in accordance withthat rule that the drawer of a bill is made liable inrelief to the acceptor, when the facts andcircumstances connected with the making and issue ofthe bill sustain the inference that it was acceptedsolely for the accommodation of the drawer. Evenwhere the liability of the party, according to thelaw-merchant, is not altered or affected by referenceto such acts and circumstances, he may still obtainrelief by shewing that the party from whom he claimsindemnity agreed to give it him; but in that case hesets up an independent and collateral guarantee,which he can only prove by means of a writing whichwill satisfy the Statute of Frauds.’ (emphasis added)

73. Similar views have been expressed in a number of

other cases (see Steele v. M’Kinlay (1880) 5 A.C. 754, 778-9,

p~ Lord Watson, and Durack v. Western Australian Trustee

Executor & Agency Co. Ltd. (1944) 72 C.L.R. 189, 207-208, per

Starke J., 212 ~ McTiernan J. and, 221. ~ Williams J.).

The principles enunciated in the passages quoted above form

the basis of the decision in a number of other cases. See, for

example -

- Ferrier v. Stewart (1912) 15 C.L.R. 32

- McDonald v. Nash 1924 A.C. 625

- National Sales Corporation, Ltd. V. Bernardi

[1931] 2 K.B. 188

I

- 31 -

- McCall Brothers, Ltd. v. Hargreaves [1932] 2K.B. 423

- Lombard Banking Ltd. v. Central Garage and

Engineering Co. Ltd. [1963] 1 Q.B. 220

- Yeoman Credit, Ltd. v. Gregory [1963] 1 All E.R.245

- H. Rowe & Co. Pty. Ltd. v. Pitts [1973]2 N.S.W.L.R. 159

74. Position under UCC. The Bill provision, although

S somewhat differently expressed, would seem to have much thesame effect as the UCC 1-102(3) which provides that, withcertain exceptions, the effect of its provisions can be varied

by agreement:

(3) The effect of provisions of this Act may bevaried by agreement, except as otherwise provided inthe Act and except that the obligations of goodfaith, diligence, reasonableness and care prescribedby this Act may not be disclaimed by agreement butthe parties may by agreement determine the standardsby which the performance of such obligations is to bemeasured if such standards are not manifestlyunreasonable.’

75. The rationale of the UCC approach seems to be that it

is appropriate, given the nature of commercial law, for

parties to have the freedom to modify or vary the effect of

the Code on their rights and liabilities.

76. However, unlike UCC 1-102(3) , the Bill provision does

not itself authorize persons to vary, by agreement, their

rights, duties and liabilities under the Bill: the clause

merely ensures that the Bill will not be read as preventing

such variation. Thus the clause would not authorize the making

of an agreement that was otherwise prohibited by law and would

not affect the operation of statutory and common law rules

that lie outside the Bill, e.g., the parole evidence rule (see

Falconbridge pp. 779-787) and the Statute of Frauds.

— 32 —

77. Application of provision to a bank. The Bill

provision is not restricted to the parties to a cheque nor to

rights, duties and liabilities arising on a cheque. It makes

it clear that:

(a) Nothing in the Bill will prevent a bank from

contracting out of its duties and liabilities in

relation to a cheque, e.g., the duty to pay a

crossed cheque only to a bank (see Bill cl. 58)

and

(b) A bank, so far as its customers are concerned,

will be able to contract out of its duties as a

paying bank (under Bill cls 103 and 104 and

s—cl. 108(1)) or extend its area of the

protection (given by cls 105 and 107, s-cl.

108(2) and cl. 109).

78. It would appear that a bank is in the same position

under the BEA (see Burnett v. Westminister Bank Ltd. [1966]

1 Q.B. 742, 761-763). Burnett’s case demonstrates, however,

that there can be considerable practical difficulties for a

bank that seeks to vary its relationship with its

cheque-drawing customers en masse (see Paget pp. 72-73 and

295—296 and Weaver and Craigie pp. 152—153, 265—266, 277, 370

and 371—372).

Cl. 6 Application of Bill

79. The Bill will only apply to cheques drawn on or after

the commencement of the Bill (Bill s-cl. 6(1)). This provision

is based generally on BEA s.6 and MD cl. 6 except that:

(a) It has been recast to put it in a positive,

rather than a negative, form; and

I

— 33 —

(b) It does not refer to the ‘issue’ of a cheque.

MD cl. 6 had the effect of applying the Bill

only to cheques drawn or issued after the

commencement of that Bill. As a cheque cannot be

issued until it has been drawn, Bill ci. 6

achieves the same result as MD ci. 6, but in a

less complicated way.

80. Presumptions. For the purposes of the application of

the Bill, there will be two presumptions:

(a) A cheque will be presumed conclusively to have

been drawn on its date (Bill s-cl. 6(2) - no

equivalent in BEA and MD) ; and

(b) Where a cheque is undated, the cheque will be

presumed to have been drawn on or after the day

on which the Bill comes into operation (Bill

s-cl. 6(3) - no equivalent in BEA or MD). This

deeming will, in practice, only apply in

relatio~n to a cheque whose date of issue is

known, but whose date of drawing is unknown.

Without this deeming provision, the date of an

undated cheque would have to be determined as a

question of fact.

81. A question arises as to whether there would be a

S difficulty if the date that a cheque bears is an altered date.

However, as the provisions dealing with the material

alteration of a cheque are in similar terms in the Bill (see

ci. 74) and in the BEA (see s. 69)), the cheque would be

avoided under whichever of those provisions applied in the

particular case, unless the alteration was made with the

agreement of each of the parties liable on the cheque. In

other words, the alteration of the date of a cheque would not

affect the application of the Bill/ BEA unless the alteration

— 34 —

was made with the agreement of each of the parties liable on

the cheque.

82. Incohate instruments. Where, after the commencement

of the Bill, a signed instrument lacking a material particular

is delivered for the purpose of completing the instrument the

Bill will apply to the completion of that instrument (Bill

s-cl. 6(4) - no equivalent in BEA or MD). This provision is

intended to clarify the application of the Bill to incohate

instruments.

83. Bank cheques and bank drafts. The provisions Srelating to the application of the Bill will also apply to

bank cheques and bank drafts. (Bill s-cl. 6(5)).

Cl. 7 Extension of Bill to external Territories

84. The Bill will extend to every external Territory

(Bill cl. 7):

- Australian Antartic Territory

- Christmas Island

- Cocos (Keeling) Islands

- Norfolk Island

- Territory of Heard and McDonald Island 5,- Coral Sea Islands Territory.

85. The Bill will apply to the Territory of Ashmore and

Cartier Islands by virtue of s-sec. 6(1) of the Ashmore and

Cartier Islands Acceptance Act 1933.

ii

— 35 —

86. To maintain uniformity it is proposed that the BEA

will be amended:

(a) To remove references to Fiji and New Zealand; and

(b) To apply to every external Territory.

Cl. 8 Bill to bind Crown

87. The Bill will bind the Crown in right of the

Commonwealth, of each of the States, of the Northern Territory

and of Norfolk Island (Bill ci. 8). See also:

(a) Bradken Consolidated Ltd v. Broken Hills

Proprietory Co. Ltd. (1979) 145 CLR 107; and

(b) Northern Territory (Self-Government) Act 1978

(s. 51).

Operation of other legislation

88. There is no provision in the Bill corresponding with

MD cl. 7 which provides as follows:

‘7. Nothing in this Act shall affect the operation ofany Act or State Act or Territorial Ordinance orinstrument enacted or made prior to the commencementof this Act on the basis that a cheque is a type ofbill of exchange and the provisions of this Act arenot to be construed as in any way altering or varyingthe provisions of such Act, State Act, TerritorialOrdinance or instrument.’

89. It would be neither appropriate, nor constitutionally

permissible, for a Commonwealth Act to purport to enact

interpretative provisions affecting State laws. It would,

having regard to the stage of constitutional development

reached in the Northern Territory, also be inappropriate to

enact interpretative provisions affecting Northern Territory

— 36 —

laws. In any event, it is difficult to see what purpose would

be achieved by such a provision as MD cl.7. A cheque will,

after the enactment of the Bill, continue to be a type of bill

of exchange. Although it is proposed that the BEA be amended

to ensure that its provisions cease to apply to cheques, a

cheque will still continue to meet the definition of ‘bill of

exchange’ in the BEA.

S

S

I

— 37 —

BILi, : PART II - CHEQUES

90. Part II of the Bill (cls. 9 to 37) deals with the

cheques as such and is divided into the following Divisions:

Division 1 - Form and interpretation

Division 2 - Delivery

Division 3 - Capacity

Division 4 - Signature

Division 5 - Consideration

— 38 —

Division 1 - Form and interpretation

91. Division 1 of Part II of the Bill (cis 9 to 23

inclusive) deals with the form and interpretation of cheques.

92. The basic structure of the initial provisions in the

Division is that a cheque is:

(a) An order to pay (see Bill cl. 10);

(b) That is unconditional (see Bill cl. 11);

(c) In writing (see Bill ci. 9);

(d) Addressed by a person to a bank (see Bill ci.

12)

(e) Signed by the person giving it (see Bill cl. 9);

(f) Requiring the bank to pay on demand (see Bill

ci. 13)

(g) A sum certain in money (see Bill cl. 14)

(h) To or to the order of a specified payee (see

Bill cl. 15) .

93. In specifying the formal conditions with which an

instrument must comply if it is to be a cheque, the Bill

departs somewhat from the structure of the BEA and the MD:

(a) The Bill begins (in s-cl. 9(1)) with a simple

definition of a cheque and, in subsequent

provisions, largely by using the concept of an

instrument containing ‘an order to pay’, expands

upon the various ingredients of the definition.

I

— 39 —

This approach avoids the difficulties involved

in the BEA provisions where a ‘bill’ is often

referred to in the provisions that are applied

in determining whether a particular instrument

is, in fact, a bill;

(b) This approach does, however, have the effect of

strengthening the implication that a cheque must

be drawn on paper, parchment or a similar

substance (see Chalmers p. 12) . It should be

noted that this inference is already contained

in the BEA (see, e.g., s-sec. 10(2) and ss. 16

and 25)

(c) The Bill, like the BEA, does not require that

the person addressing the order to the bank must

be a customer of the bank. However, Paget

pp. 211-212) suggests that it is difficult to

imagine a case where a cheque would be drawn

otherwise than by a customer and also points out

that there are expressions in the BEA provisions

relating to cheques that are not easily

reconciled with the existence of any other type

of cheque (see, however, Paget p. 36).

Cl. 9 Cheque defined

S 94. A cheque has been defined in the Bill as an

unconditional order in writing addressed by a person to

another person (being a bank), signed by the person giving it,

requiring the bank to pay on demand a sum certain in money to

or to the order of a payee specified in the instrument

containing the order or to bearer (Bills-cl. 9(1) - cf. BEA

s-secs 8(1) and 78(1) and MD s-cl. 8(1) - see also para. 82 of

this explanatory paper) . While there is no reference to

— 40 —

‘bearer’ in this definition, the matter is dealt with

elsewhere in the Bill (see s—para. 11(1) (a) (ii)).

95. An instrument that does not comply with this

definition or that orders any act to be done in addition to

the payment of money, will not be a cheque (Bill s-cl. 9(2) -

based on BEA s-sec. 8(2) and MD s-cl. 8(2)).

Cl. 10 Order to pay

96. An order to pay must be more than an authorization or

request to pay (Bill cl. 10 - based on definition of ‘order’

in UCC 3-102(1) (b) ). This provision is declaratory of the

position at common law (see Chalmers p.14; Riley p. 25;

Rajanayagam p. 15 and Falconbridge p. 468) and fills a small

gap in the BEA.

Cl.ll Unconditional order to pay

97. Payment on a contin9ency. An order to pay on a

contingency will not be an unconditional order (Bill

s-cl. 11(1) - based on the second sentence in BEA s.16 - no

equivalent provision in MD). It would seem, in principle, that

the provision is capable of applying to bills payable on

demand (see Riley pp. 45-46 and Chalmers p. 32). An example of

such a bill would be one that required payment of $10 to X if

he is married when he presents the bill for payment.

98. Matters that can be disregarded when determining

whether an order is unconditional. An order to pay will not

be taken to be an unconditional order to pay by reason only

that it is coupled with either or both of the following (Bill

s—cl. 11(2)):

(a) The account to be debited; or

4

— 41 —

(b) The transaction giving rise to the order.

(Bill paras. 11(2) (a) and (b) - based on BEA s-sec. 8(3) and

MD s-cl. 8(3)) (cf. UCC 3-105(1) which makes it clear that a

wide range of matters may be included in a ‘cheque’ without

affecting its nature as an unconditional order to pay. While

the Indian BLC Report (pp. 28-29) favoured the tJCC approach,

Mr Megrah (co-editor of Paget) , thought that such a provision

was unnecessary (see pp. 311-312 of the Report)

99. Payment out of a particular account. The Bill does

not contain any equivalent to the first clause of BEA s-sec.

8(3) (see also MD s-cl. 8(3)). This provision provides that

an order to pay out of a particular fund (e.g. the proceeds of

a sale) is not an unconditional order to pay. It is to be

contrasted with BEA para. 8(3) (a) which states that an order

is unconditional even though it indicates a particular fund or

account out of which the drawee is to re-imburse himself. It

is considered that although these provisions might cover

different fact situations so far as bills of exchange other

than cheques are concerned, confusion would be inevitable if

they were both to be included in the Bill. For example, in the

case of a cheque, drawn on a ‘John Jones No. 3 Account’ it

would be very difficult for a Court to determine whether this

was a (non-permissable) order to pay out of a particular

account or a (permissable) indication of a particular account

to be debited by the bank to which the order was addressed.

100. Receipts. The MD contained a draft provision that

attempted to deal exhaustively with problems that arose from

the presence on a cheque of a form of receipt (see MD s-cl.

8(5)). The placing of receipt forms on cheques seems to have

gained popularity at a time when banks, as a matter of

practice, required their customers to indorse all cheques

lodged for collection. With the amendments of Part III of the

BEA in 1971, this practice has ceased and cheques lodged for

— 42 —

collection are now indorsed only in special cases. As the

practice of providing receipt forms on cheques has fallen into

disuse, the Bill does not make provision with respect to it.

Cl. 12 Order addressed to a bank

101. To be taken to be addressed to a bank, an order to

pay must meet three requirements:

(a) It must be addressed to a bank and to no other

person (Bill para. 12(a));

(b) It must be be addressed to one bank only (Bill

para 8(b)). This requirement is contrary to that

in the BEA s-sec. 11(2) . It would seem to be

implicit in the relationship between banker and

customer that a cheque should always have only

one drawee and that that drawee should be a

bank. This provision makes it clear that an

instrument containing an order addressed to 2 or

more banks is not to be treated as a cheque. The

use of pre-stamped, printed cheque forms

means that it is extremely unlikely that a

person would attempt to draw a cheque otherwise

than in accordance with the paragraph; and

(c) It must name the bank or otherwise indicate it

with reasonable certainty (Bill para 12(c)).

This requirement is based on BEA s-sec. 11(1)

but redrafted to make it clear that the words

‘with reasonable certainty’ qualify the words

‘otherwise indicated’ and not the word ‘named’

(see also Bill s—cl. 15(3) where a similar

problem of construction with the BEA is dealt

with).

4

— 43 —

Cl. 13 Order to pay on demand

102. When an order is an order to pay on demand. An order

to pay will be an order to pay on demand if -

(a) The order is expressed to require payment on

demand, at sight or on presentation; or

(b) No time for payment is expressed in the

instrument containing the order.

(Bill s-cl. 13(1) - based on BEA s-sec. 15(1) - no equivalent

provision in MD)

103. When an order not an order to pay on demand. An

order will not be an order to pay on demand if it is expressed

to require, or requires by implication, any of the following:

(a) Payment otherwise than on demand etc. (Bill

s-cl. 13(2) - no equivalent provision in BEA or

MD). This provision has been included:

(i) To explain, in a negative way, the

requirements of an order to pay on demand,

Bill s—cl. 13(2) it makes it clear that

Bill s-cl. 13(1) provides a comprehensive

specification of the requirements of an

order to pay on demand; and

(ii) To reinforce the point that the postdating

of an instrument does not make the

instrument not payable on demand for the

purpose of determining whether it is a

cheque; or

— 44 —

(b) Payment only -

(i) At or before a particular time (Bill para.

13(3) (a) — based on MD s—cl. 9(3)); or

(ii) If presentation is made at or before a

particular time (Bill s—para. 13(3) (b) —

based on Manning Committee report para.

192)

It would seem, on the reasoning of the Manning

Committee, that b~th kinds of cheques are

equally objectionable. The Committee took the

view ‘that the drawer of a cheque should be

required to accept the ordinary rules as to

limitation and should not be permitted to impose

conditions of this kind for his own greater

protection at the expense of the payee or a

holder’.

Cl. 14 Order to pay a sum certain

104. Reasonable certainty. Subject to the situation where

there is a discrepancy betwø~err~sums specified (dealt with in/ ,~,

Bill s-cl. 14(2) - see par~~f this explanatory paper), an

order to pay will not be an order to pay a sum certain unless

that sum is specified or ascertainable with reasonable

certainty from the instrument containing the order (Bill s-cl.

14(1)).

105. The Manning Committee recommended (para. 194) that

there should be a provision stating expressly that the amount

of a cheque could be expressed in words, figures or both. The

recommendation was prompted by information given to the

Committee that the mechanised preparation of cheques works

best if the amount payable is expressed only in figures. It

4

— 45 —

would seem that, with the technological changes that have

occurred since 1964, this is no longer the case. Accordingly,