1 Media Bias in Financial Newspapers: Evidence from Early Twentieth Century France Vincent Bignon & Antonio Miscio February 2009 Abstract The financial market was well developed in France in the years before World War I, and there were many newspapers that provided information to investors. Yet contemporaries faulted the financial press for inaccuracy and biases. This study implements a quantitative test to assess these accusations. The results show that, although firms’ media coverage was affected because firms paid to appear in newspapers, the performance of firms actually touted by the press was good, overall. Thus, the media bias is better explained by newspapers recommending investments according to their editorial policy and then inducing firms to pay for those recommendations. Keywords: Media coverage, newspapers, media bias, financial markets JEL Classifications: G11, G12, L15, O16, N13 Acknowledgments: We benefited from suggestions of the participants of the 1 st Euroclio conference in Paris (France), the 10 th ESNIE 2008 in Cargese (France), the 28 th APHES in Guimarães (Portugal), and of seminars at Rutgers University, Université Paris Ouest Nanterre (EconomiX), and Université d’Orléans (LEO). We also thank Olivier Accominotti, Sara Bertin, Norbert Gaillard, George Gallais-Hamonno, John Landon-Lane, John Nye, Yannick Perez, Camila VamMalle, Anne-Gael Vaubourg, and Eugen White for comments and insights. We are especially grateful to Régis Breton and Marc Flandreau for many discussions and comments. Vincent Bignon acknowledges support of the Mercatus Center at George Mason University while finishing the paper. This paper benefited from funding by the Agence Nationale de la Recherche, project # 05-JCJC-0225. The usual disclaimer applies. V. Bignon: Research fellow at EconomiX, Université Paris Ouest Nanterre La Défense, Bâtiment K, 200 avenue de la République, 92001 Nanterre cedex. Maître de Conférences at IUFM – Université Paris 12. E-mail: vbignon@u- paris10.fr . A. Miscio: LEO, Université d’Orléans. Faculté de Droit, d'Economie et Gestion, Rue de Blois, 45067 Orléans cedex 2. E-mail: [email protected]

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

1

Media Bias in Financial Newspapers: Evidence from Early Twentieth Century France

Vincent Bignon & Antonio Miscio

February 2009

Abstract The financial market was well developed in France in the years before World War I, and there were many

newspapers that provided information to investors. Yet contemporaries faulted the financial press for inaccuracy and

biases. This study implements a quantitative test to assess these accusations. The results show that, although firms’

media coverage was affected because firms paid to appear in newspapers, the performance of firms actually touted

by the press was good, overall. Thus, the media bias is better explained by newspapers recommending investments

according to their editorial policy and then inducing firms to pay for those recommendations.

Keywords: Media coverage, newspapers, media bias, financial markets

JEL Classifications: G11, G12, L15, O16, N13

Acknowledgments: We benefited from suggestions of the participants of the 1st Euroclio conference in Paris (France), the 10th ESNIE 2008 in Cargese (France), the 28th APHES in Guimarães (Portugal), and of seminars at Rutgers University, Université Paris Ouest Nanterre (EconomiX), and Université d’Orléans (LEO). We also thank Olivier Accominotti, Sara Bertin, Norbert Gaillard, George Gallais-Hamonno, John Landon-Lane, John Nye, Yannick Perez, Camila VamMalle, Anne-Gael Vaubourg, and Eugen White for comments and insights. We are especially grateful to Régis Breton and Marc Flandreau for many discussions and comments. Vincent Bignon acknowledges support of the Mercatus Center at George Mason University while finishing the paper. This paper benefited from funding by the Agence Nationale de la Recherche, project # 05-JCJC-0225. The usual disclaimer applies. V. Bignon: Research fellow at EconomiX, Université Paris Ouest Nanterre La Défense, Bâtiment K, 200 avenue de la République, 92001 Nanterre cedex. Maître de Conférences at IUFM – Université Paris 12. E-mail: [email protected]. A. Miscio: LEO, Université d’Orléans. Faculté de Droit, d'Economie et Gestion, Rue de Blois, 45067 Orléans cedex 2. E-mail: [email protected]

2

1. Introduction

Among the key elements of the development of financial markets are the quantity and quality of

information provided to investors on financial assets and on their issuers. The French financial

market experienced a remarkable development during the first wave of globalisation (Rajan and

Zingales 2003). Consequently, about two million investors held at least some of the several

thousands of stocks and bonds listed on the Paris stock exchange (Neymarck 1911). Although

newspapers were an active—indeed, unique—medium for spreading financial information with

“hundreds of living titles” (Albert 1972, p. 261), most contemporaries pointed to the low

informational content of financial newspapers (Lysis 1912; Kaufmann 1914). Those judgments

were based on qualitative evidence, whereas in this paper we construct a quantitative test to

assess the accuracy of the financial press.

Numerous contemporaries linked the poor content of financial newspapers with the

payments made by providers of the information. This is clearly a distinct and noticeable feature

of these particular newspapers. Contemporaries blamed this feature for creating a conflict of

interest and ultimately for biasing the information published. Calling such arrangements bribery

and decrying the venality of the French press, they further argued that “in our society, those who

have money have the newspapers and consequently, the public opinion” (Lysis 1912, p. 168).

Most historians (see e.g. Feis 1965; Albert 1972) subsequently went along with assuming that

these periodicals contained little valuable information. However, a closer look at this market

indicates that countervailing forces could have been at work. Albert (1972) wrote that “a reliable

financial press did nonetheless exist although their independence of thought could have been

questioned”. Martin (2006) discussed the so-called venality of the press and judged that the

phenomenon could have been overestimated by contemporaries whose negative assessments,

moreover, were accepted too uncritically by historians.

3

Although payments were part of a publication contract, the idea that newspapers slanted

information still needs to be proven. After all, a newspaper was also paid by its readers and thus

was unlikely to have acted against their interests. More precisely, from the literature on two-

sided markets we borrow the idea that an intermediary can set up a payment structure requiring

that both sides (information providers and readers) pay to cover the publication’s cost (Rochet

and Tirole 2004; Anderson and Gabszewicz 2006). Consequently, the mere existence of

payments to journals from information providers does not, in itself, prove information distortion.

Rather, the effect on editorial policy of such payments is an empirical question that needs

quantitative assessment. In this paper we use the information published during six months by a

sample of four newspapers concerning all firms listed on the stock market in order to test

whether those payments induced a (potential) coverage bias.1 This allows us to assess whether

published information was biased toward paying firms and to see if this could have devalued the

portfolios of the reader-investors. We show that payments did modify the distribution of

published information toward paying firms. However, this did not always make these investors

worse off.

In spite of the media’s widespread development since the 19th century and its importance

for financial development, few in the field of economic history have studied this issue. Some

look at the effect of the diffusion of price lists in newspapers before the Industrial Revolution

and argue that this facilitated arbitrage among places (Neal 1988; McCusker and Gravejstijn

1991; Flandreau et al. 2008). Gille (1959) provided a comprehensive history of this industry in

France during the Second Empire. Flandreau (2003) showed how information on sovereign debt

was produced and spread during the Belle Epoque. Hautcoeur (2006) provided insights on the

use of stock index in the French financial periodicals before 1914. Esteves (2007) proposed a

1 In the political context, D’Alessio and Allen (2000) defined three types of media bias: the gatekeeping bias, which is the preference for selecting stories from one (political) party or the other; the coverage bias, which considers the relative amounts of coverage each party receives; and the X bias, which focuses on the favorability of coverage.

4

detailed account of the diffusion of information on sovereign bonds through such bondholders’

periodicals as the Banker’s magazine. Our paper contributes to this literature by assessing the

accuracy of financial newspapers in early 20th-century France.

This paper is also related to the burgeoning literature that developed at the crossroads of

media economics and finance or political science. We borrow from the political science literature

a focus on measuring the bias. A few authors have recently attempted to measure the slanting of

news by media in the political area (Groseclose and Milyo 2005; Gentzkow and Shapiro 2006).

We differ from that work in focusing on financial newspapers. This allows us to provide a

measure of how investors might have been hurt by media bias. This paper is also linked to those

that measure the media’s relation with the financial markets. Some work in this vein shows that,

by diffusing information, the press helped to reduce economic inefficiencies such as private

benefits captured by a CEO (Dyck and Zingales 2004; Dyck et al. 2008). But most of these

papers concern measuring and explaining the media bias in reporting financial market

information. Huberman and Regev (2001) gave an example of the media’s effect on stock price

that stemmed solely from the reporting of soft information. Some other authors use the “event

study” approach to test for the impact of market newspapers’ stories on stock prices (Chan 2003;

Bhattacharya 2004). In the field of finance, the most similar approach is that of Reuter (2004)

and Reuter and Zitzewitz (2006), who studied the bias created by advertisements in the selection

of a newspaper’s coverage of products. In contrast, we study the coverage of listed firms and the

impact of a different payment scheme. Our paper is also linked to Gentzkow et al. (2004), who

studied the rise of independence in the political press during 19th-century America.

The rest of this paper is organized as follows. Section 2 explores the various scandals that

hurt the press. Section 3 presents our data and explains the test that is implemented in Section 4.

Section 5 presents the results, and Section 6 concludes.

5

2. Information slanting and hidden payments to newspapers

Much as many persons use today’s rating agencies, historians have used various financial

scandals to infer the efficiency of the media that disseminate information on financial assets. The

anecdotal evidence is said to demonstrate that payments made by information sources to

newspapers distorted the information published. In Section 2.1 we present these various affairs

and the claims historians infer from their study. It is often argued that studying the various

scandals is the best (if not the only) possible method for judging the accuracy of the press. In

Section 2.2 we propose an alternate proxy for the payments made to newspapers by firms and

explain its rationale.

2.1. Newspapers in turmoil: From the Panama scandal to the Rochette affair

During the two decades from the 1890s to World War I, a common opinion was spread through

journals, books, and parliamentary reports that the press was actually bribed by its information

sources and that this necessarily distorted the information published.

The opinion that the press was bribed to slant2 published information first appeared after

the Panama scandal burst on the scene in 1892. This scandal was openly discussed and resulted

in a report by a special commission of lawmakers as well as a court decision. It was then

revealed that politicians and journals had been paid to put a positive spin on Panama’s activities

and, notably, to foster the success of the company’s bond issues. The company had paid

newspapers and journalists for announcements, advertising, and favourable editorial coverage,

paying between 12 and 13 million francs to newspapers between 1880 and 1888 while it raised

about 1.5 billion from the public (Martin 2006, p. 23).3

2 Defined by Hayakawa (1940) as the process of deliberately selecting details that are favorable or unfavorable to the subject being described. 3 Although most newspapers received some payments, they might be relatively modest compared with the operating income or the amount of advertising revenue. Eveno (2003, p. 67) computed that Le Figaro (its manager and journalists) received 500,450 francs from the Panama company during the period (amounting to 55,600 francs per annum) while its annual operating income fluctuated between 1.88 and 2.58 million.

6

The scandal led to charges of corruption leveled at both the press and the political

system. It caused Anatole Leroy-Beaulieu—then a professor at Sciences Po—to question the

very organization of the democratic system, blaming “extravagant governments, drudge

lawmakers and a venal press”. The press was especially attacked because the scandal revealed

that it worked at odds with the romantic vision of the journalist who uses his pen as “a sword

pure of any shed blood” and so is “the modern knight, the righter of wrongs” (Leroy-Beaulieu

1896, p. 733).4

As a result, perception of the newspapers’ accuracy changed among the general public

and the elite. Discussions revolved around the role played by money in slanting the published

information. The Revue Bleue, an influential periodical among the elite, opened its columns in

1897 to debate on the “responsibilities of the contemporaneous press”. Henry Beranger, the

discussion’s initiator, argued that “cash, when it reigns, is never a principle of superiority and

quite always a principle of corruption” and that “our legislator planned the independence of the

press towards judges or the police, but they did not foresee the slavery of the press towards

business men and the plutocracy”. Yet not all contemporaries shared this view. Georges

Clémenceau—a lawmaker and journalist at L’aurore—argued that the newspapers’ readership

must be blamed for failing to identify the truth; the novelist Emile Zola and the socialist

lawmaker Jean Jaurès pointed that one should be confident in the outcome of a free competition

that sorts out good journals from bad.

March 1908 saw another financial affair that linked politics, the financial market, and the

media. This was the Rochette affair,5 which also ended up in a commission of the National

Assembly and a court judgment. Rochette was a financier who owned two banks, about a dozen

other companies (notably mines), and three financial newspapers. When he tried to take over Le

petit journal—a newspaper owned and managed by Senator Charles Prevet—the Paris’ préfet 4 He had earlier written that, “among all the vileness of the Panama scandal, the role played by the press was the most shameful” (Leroy-Beaulieu 1894, p. 733). 5 The most reliable source of information on the Rochette affair is the parliamentary report (Folleville 1911).

7

Lépine (the highest representative of the French government in Paris) searched for investors to

lodge a complaint against Rochette, who was accused of releasing flawed and possibly altered

information on his companies. According to the 1910 judgement, he attempted to influence

investors through his own newspapers 6 and by contracting with other newspapers to publicize

his companies. Rochette was convicted and sentenced to three years in jail. This financial

turmoil revivified the public debate on the mutual influence of newspapers and financiers.

In this context of periodic scandals, contemporaries such as Lysis blamed the “quite

universal corruption of our [French] press, paid, sold, indentured by the financial powers” (1912,

p. 168).7 Paul Leroy Beaulieu, editor of l’Economiste Français, argued that when “articles and

advertising are mixed up, it is clear that the press is losing its authority. It should no longer be

regarded as a collection of information and people must distrust it” (Cassagnac 1893, pp. 4–5).

Kaufmann, a German economist who published a detailed analysis of French banks, agreed and

asserted that the financial press “does not have a value as an source of information; It is, as

perfectly put by Lysis—and besides few exceptions that are becoming rarer—an advertisement

press rather than an opinion press” (1914, p. 210; emphasis in original).

Building on those judgements, French historians—with the notable exception of Marc

Martin—blamed this venality for weakening the press’s credibility among the public. As Albert

(1972, pp. 266–267) asserted, “financial advertising contributed to a significant extent to give to

the French people a distorted view of the facts”; he added: “It exerted a real censorship on the

economic information which resulted, in the short run, in a discredit of the business world to

French eyes and in the long run, to divert their attention from economic issues.” Jeanneney

(1981) observed that opinions published in newspapers “were not for sure independent of secret

subsidies” (p. 210) and noted that financial advertising “takes the shape of misleading editorial

analysis” (p. 211).

6 Finance Pratique, Bulletin Hebdomadaire du Banco Franco Espagnol and Moniteur de la Banque et de la Bourse. 7 See also Esteves (2007, pp. 5–6) for an account of Lysis’s grievances.

8

Although such financial affairs clearly hurt the welfare of investors, relying on them to

assess the quality of financial newspapers is misleading because investors are typically not

sufficiently informed on enough firms to judge fairly. Therefore, in order to evaluate the quality

of the French financial press, we must construct a quantitative test capable of measuring the

effect of payments made to newspapers on their editorial policy. Toward this end, we must

isolate a variable that can be used to find traces of those payments, which we describe in more

detail next.

2.2. Direct payments to newspapers

During the Panama scandal, a fear of their newspapers’ lost credibility led some editors to

reconsider current advertising arrangements. Paul de Cassagnac, a lawmaker of the Bonapartist

party and editor of L’Autorité, argued in 1893 that receiving funds from companies is not, per se,

an indication of corruption as long as the editorial content and the advertising section appear as

two different and clearly separate sections of the newspaper. This view of payments to

newspapers became dominant later in the century, but this particular solution was not

implemented before 1914 (Delporte 1999). Until then, firms continued to pay for editorial

articles, not for advertising as that term is normally understood.

Payments were made to newspapers because the payer expected, in exchange, some

coverage or some spinning of the news. Although it has proved impossible to re-enact each

payment made by firms to newspapers, there are many indications of the payment pattern. In his

handbook intended for small investors, Neymarck (1911, pp. 63–64) indicated that, when a stock

is introduced on the market, “the promotion in the newspapers using advertisement and articles”

was common and that, in this, France was just following the widespread practice in America and

England. He further added that it would have been a “mistake to believe that those expenses

could have been avoided” (p. 66). Oscar Marinitsch, who worked in the financial advertising

sector and wrote a book in 1892 to inform on stock exchange practices, pointed out that “the

9

good—as well as the bad—deals cannot succeed without the help of the press” and that

consequently the information providers “contracted with the journalists or editor of the financial

press or of the newspapers’ financial section” (Marinitsch 1892, p. 292).

Payments were not made directly from firms to newspapers; rather, they were

intermediated by the investment banks (Lajeune vilar 1895). The correspondence of Raffalovich

(1931)—a distinguished economist but also a secret advisor of the Russian Finance minister, and

thus the dispatcher of Russian Tsarist funds to French newspapers—acknowledged that he

received the indication summing up all payments made to newspapers through the Banque de

Paris et des Pays Bas.8 One of the advantages of this delegation was that pooling the payments

of various firms gave banks more bargaining power against newspapers and so allowed banks to

become a greater threat to them (Raffalovich 1931, p. 207).9 Another reason for delegation could

have been that banks knew more than firms did about the workings of the media industry. Since

banks also provided firms with other services such as financial advertisements and legal

representation (and since this fact was publicly known), “direct payments made by firms to

newspapers are suitably proxied by these firms’ relationships with their investment banks.

3. Methodology and samples on newspapers and securities

Although payments could have distorted the information available to investors and hence their

allocation of funds to financial assets (Merton 1987), we show in Section 3.1 that such payments

do not in themselves prove information distortion. In order to assess newspapers’ quality, in

Section 3.2 we propose a quantitative test of the (potential) induced distortions.

3.1. Theoretical background

8 Raffalovich (1931, pp. 74, 176, 205, 208). 9 Newspapers regularly asked for an increase in advertising from the Russian Empire. A letter of 20 October 1908 stated: ‘A contract between the representative of the Finances ministry and the various newspapers will have the drawback of overexciting the envies because they will have for the first time to negotiate directly with a government official of Russia instead of a bank employee.’ (Raffalovich 1931, p. 207).

10

A financial newspaper is a firm that selects a set of information and reveals it to its readers. Most

of the discussion implied by this definition revolves around the elements that determine the

news’ selection and especially on whether it is made with the precision and neutrality of normal

news reports. Potential biases arise because newspapers are intervening in a two-sided market.

On one side they form relationships with the information providers (the supply side of news) and

with the advertising market; on the other side they interact with readers by selling issues (the

demand side). Financial newspapers can thus be viewed as “matchmakers”: some firms are

highlighted (to the potential advantage of reader-investors) by their selection to the sample of

firms covered in each issue.

As noticed by Rochet and Tirole (2004), most markets are two-sided. But on most of

those markets the payment structure (who pays what on which side of the market) is neutral. If

there is some externality between the two sides, then a Coasian bargaining can implement the

first-best allocation because it allows agents to be compensated ex post for losses induced by the

externality (Coase 1960). The main point of this literature is to focus on markets where one side

imposes on the other an externality for which Coasian bargaining cannot compensate. Clearly,

the selection of information published by newspapers exerted an externality on their readers.

Moreover, because information is a public good, it is difficult to find a mechanism making

readers pay entirely for this externality.

An important consequence of the theory of two-sided markets in this context is that the

payment structure is no longer neutral: it becomes an instrument for inducing both sides of the

market to participate. Numerous papers have shown that the price charged to one side of the

market can be used to subsidize the other side. With the financial newspapers, this implies that

charging information providers to publish information was neither corrupt nor venal but, rather,

simply an indirect subsidy paid by information providers to readers. This need not create an

11

economic inefficiency, since those payments may have been a precondition of the newspaper’s

existence.

However, efficiency would suffer if newspapers switched their news coverage to poorly

performing firms, since this could lead investors to make poor choices in their portfolio

allocation. Yet a newspaper’s objectives can be influenced both by its readers’ preferences and

by its relations with information providers or advertisers. Therefore, it is natural to test for bias

resulting from supply-side payments by assessing whether a newspaper is hewing to the best

interests of its readers or of its advertisers.

From the reader’s point of view, a financial newspaper is a collection of pieces of

information on financial assets and on events that could affect their prices. We can expect

rational readers to buy one issue of a given newspaper if the value of the information content—

its accuracy and relevance to the financial market—is greater than the cost of buying it. The

newspaper then has an incentive to build a reputation for accuracy (Coase 1974) whose effect is

to “selectively reduce [an] agent’s cost of collecting information and evaluating information”

(Dyck & Zingales 2002). Gentzkow and Shapiro (2006) provided an additional result by

showing that, when media compete on the basis of reputation, slanting is reduced if consumers

can easily learn the “true” information.

Of course, newspapers wish to maintain their relations with sources of primary material.

The firms themselves are the principal information providers through disclosure of their

accounting figures, sales records, and/or business perspectives (e.g., information on new

contracts). Although a reader benefits from learning all types of news, firms typically have a

vested interest in disclosing only information whose expected impact is to increase the stock

price (else disclosure could damage the firm’s value). Hence the firm has an incentive to use

newspapers to signal positive information to investors, and it is more than willing to pay for that.

Even when a firm has no interest in disclosing some information, it may be that someone inside

12

the firm (or a third party, such as a competitor) does. In this way, a newspaper can use its

relationships with all information providers to raise its revenue by demanding payments. Such

advertising does help to reduce a newspaper’s price and hence to increase the readership, but it

could create two biases. First, it could alter the distribution of published information toward

paying firms. Second, it could bias this distribution toward positive news.

In sum, each of the relationships managed by newspapers (readers and advertisers or

information sources) can decrease the value—for rational consumers—of the published

information. When investors have preferences regarding some subset of firms, a media outlet

may well bias disclosed information toward that subset in order to increase readership. When a

newspaper’s informational content is strongly linked to advertisers, the likely effect is to bias the

distribution of news toward advertising firms (as compared to the case of no advertising).

Finally, when information is not freely available, the relationship between newspaper editors and

information providers will bias published information toward those sources that have an interest

in widening their audience.

3.2. Testing for the accuracy of firms’ media coverage

We’ve shown that two tests must be conducted in order to measure the potential biases. First, we

test for the “positive news” bias that sources induce by computing the ratio of negative to total

information published in each newspaper. Second, we assess the accuracy of the press by

proposing and testing determinants of the media coverage of firms listed on the stock market. It

is worth noting that our test of coverage bias also yields results on the slanting of information by

newspapers when providers must pay to have information published, because the payment often

entails not only coverage but also some spinning of the news.

The regressions take into account that a newspaper could have targeted one of several

different readerships. It might target liquidity traders—that is, those who must be able to sell

their financial assets when needed. In that case, a newspaper would tend to cover firms with high

13

liquidity on the market and those with asset prices of (relatively) low volatility. Another potential

target was the rentiers (i.e., long-term investors with a “buy and hold” strategy). In all cases

we’ll assume that the quantity of positive information on firms published by one newspaper

defines a portfolio of assets. A newspaper that wanted to maximize the value of information for

these investors should choose a portfolio according to the mean-variance theory. Readers of the

rentier type seek information on low-risk firms generating relatively low yields (e.g., large firms

with a high market capitalization) or on firms with high yields but at high risk. The need to

attract a targeted readership means that the regression results on financial variables will define

the profile of each newspaper.

We will also allow firms’ coverage to reflect the newspaper tendency to write about

enterprises with a wide audience (Nguyen-Dang 2006). This will bias the selection of news

toward big firms or some sectors. We also check for any relation between a firms’ country of

registration and its press exposure. This effect will be negative if investors were reluctant to hold

stocks issued by foreign firms (e.g., because it was costly to enforce property rights in another

judicial system). Finally, another newspaper motive could have been to provide coverage of

firms operating abroad, given that such information would be more difficult and expensive (than

with a domestic firm) for an individual investor to gather directly.

The regression also takes into account the possible bias induced by advertising.10 Two

channels could have influenced the media. First, as documented in Reuter (2004) and Reuter and

Zitzewitz (2006), one can expect a positive correlation between firms’ coverage and the volume

of their advertising. Moreover, since newspapers also received payments – mediated by

investment banks – from firms for the publication in the editorial part, we include a variable to

proxy for those payments (see Section 2.2). 10 This bias was documented by Reuter (2004) and Reuter and Zitzewitz (2006). Reuter (2004) found only limited evidence for a positive correlation between product reviews and advertising. Reuter and Zitzewitz (2006) showed that major personal finance magazine are ‘more likely to recommend funds from families that have advertised within their pages in the past’, but they document no such relationship for newspapers (e.g., the New York Times or the Washington Post) covering more general subjects for a wider audience.

14

The test of coverage bias is implemented using the number of times a firm received

coverage in a given newspaper as the left-hand-side variable (Exposure). On the right-hand side

we have a set (SP) of financial variables that reflect the firm’s stock market performance, a set

(FC) of variables that describe the firm’s characteristics, a measure (Ads) of each firm’s

advertising volume in the newspaper, and a proxy (Banks) for direct payments made to

newspaper. This yields the following model:

Exposure = constant + a(SP) + b(FC) + c(Ads) + e(Banks) + ui

We are interested in knowing how the set of financial variables interacts with the Ads and

DP variables. The null assumption is as follows. When its readers are rational investors (i.e. they

want to learn about events that can affect their financial assets), we expect a newspaper’s editor

to select the most accurate available information in order to maximize readership (and build

reputation). Thus we expect to find that financial variables are significant and that payments

variables (both Ads and Banks) are insignificant. However, the desired reputation effect could be

negated by payments that might boost the exposure of the paying firms. In this case, financial

variables may well appear to be insignificant while those on payments do not, indicating that

payments were the main driver of the newspapers’ editorial policy.

A third possibility is that both types of variables (payments and financial) are significant.

In that case, it would be hard to distinguish the effect on investors’ welfare of payments made by

firms from the effect of financial performance. We tackle this issue by computing various

measures—of the quality of a newspaper’s editorial content under various counterfactual

scenarios—that use the regression results to remove the potential effect of our payment variables

on media coverage. The measures used to assess the quality of the newspapers’

recommendations are the mean of the return (i.e., the mean of the stock’s dividend/price ratio)

and the variance of the return, both computed for each newspaper based on the sample of firms

that it covered. These measures will allow us to assess whether or not a given investor was worse

15

off (in terms of return) when those payment variables that could affect media coverage of a firm

are included in the computation.

4. Database and sample of newspapers

To test the accuracy of newspaper’s coverage, we used a sample of four newspapers; see Section

4.1. The most reputable were chosen, since it’s likely that rational readers will also have chosen

them to get information on traded securities. In order to account for the selection (or not) of

firms by newspaper, the characteristics of the entire population of firms listed on the stock

market were also gathered. This information is described in Section 4.2.

4.1. The sample of newspapers

The number of financial periodicals at the beginning of the 20th century was gauged by Albert

(1972) to be in the hundreds. However, among the 186 periodicals active in 1891, Marinitsch

(1892, p. 292) pointed that 25 were unofficial mouthpieces of credit banks, another 25 were

managed by journalists of various renown, and the rest were owned by financial intermediaries.

In selecting the sample of newspapers to be analyzed, we restricted our choice to weekly

journals with a wide coverage of financial markets. We selected two of the most reputable

periodicals, L’Economiste Européen (hereafter EURO) and the Rentier (RENT, published every

ten days). These newspapers had a good reputation, were managed by independent journalists

who were also economists,11 and resembled modern financial periodicals in presenting detailed

macroeconomic information, news on firm activities, some accounting figures, and a full list of

security quotations. Moreover, these two were among the few that did not offer any

(supplementary) financial services, as the subtitle to Le Rentier indicated from 27 July 1906

11 Edmond Théry and Alfred Neymarck, respectively.

16

onward.12 To test for a potential effect of ownership on the editorial policy we added two other

newspapers, the Journal des Intérêts Financiers (INTFIN) and La Semaine Financière (SEM).

The former was owned and managed by a bank (the Crédit Mobilier Français); the latter,

although it appeared to be independent and was managed by journalist Charles Bourdon, offered

its readers financial brokerage services and was probably linked to the Banque des Français.13

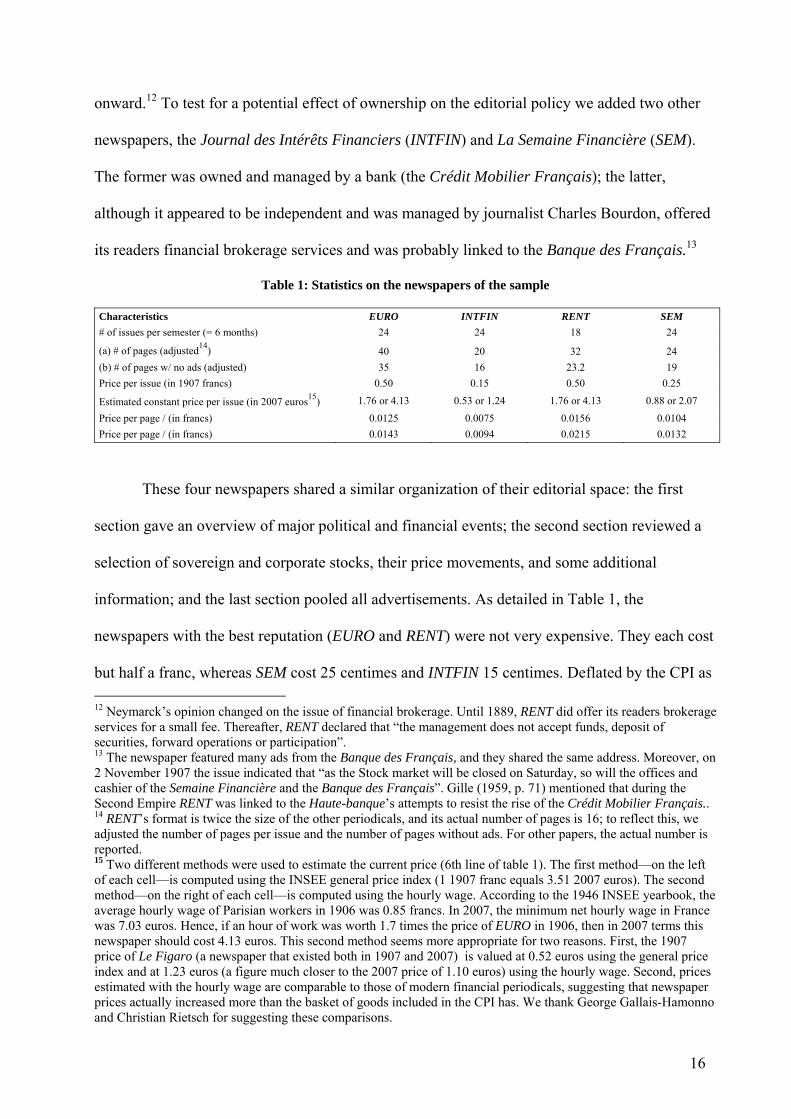

Table 1: Statistics on the newspapers of the sample

Characteristics EURO INTFIN RENT SEM # of issues per semester (= 6 months) 24 24 18 24

(a) # of pages (adjusted14) 40 20 32 24 (b) # of pages w/ no ads (adjusted) 35 16 23.2 19 Price per issue (in 1907 francs) 0.50 0.15 0.50 0.25

Estimated constant price per issue (in 2007 euros15) 1.76 or 4.13 0.53 or 1.24 1.76 or 4.13 0.88 or 2.07

Price per page / (in francs) 0.0125 0.0075 0.0156 0.0104 Price per page / (in francs) 0.0143 0.0094 0.0215 0.0132

These four newspapers shared a similar organization of their editorial space: the first

section gave an overview of major political and financial events; the second section reviewed a

selection of sovereign and corporate stocks, their price movements, and some additional

information; and the last section pooled all advertisements. As detailed in Table 1, the

newspapers with the best reputation (EURO and RENT) were not very expensive. They each cost

but half a franc, whereas SEM cost 25 centimes and INTFIN 15 centimes. Deflated by the CPI as 12 Neymarck’s opinion changed on the issue of financial brokerage. Until 1889, RENT did offer its readers brokerage services for a small fee. Thereafter, RENT declared that “the management does not accept funds, deposit of securities, forward operations or participation”. 13 The newspaper featured many ads from the Banque des Français, and they shared the same address. Moreover, on 2 November 1907 the issue indicated that “as the Stock market will be closed on Saturday, so will the offices and cashier of the Semaine Financière and the Banque des Français”. Gille (1959, p. 71) mentioned that during the Second Empire RENT was linked to the Haute-banque’s attempts to resist the rise of the Crédit Mobilier Français.. 14 RENT’s format is twice the size of the other periodicals, and its actual number of pages is 16; to reflect this, we adjusted the number of pages per issue and the number of pages without ads. For other papers, the actual number is reported. 15 Two different methods were used to estimate the current price (6th line of table 1). The first method—on the left of each cell—is computed using the INSEE general price index (1 1907 franc equals 3.51 2007 euros). The second method—on the right of each cell—is computed using the hourly wage. According to the 1946 INSEE yearbook, the average hourly wage of Parisian workers in 1906 was 0.85 francs. In 2007, the minimum net hourly wage in France was 7.03 euros. Hence, if an hour of work was worth 1.7 times the price of EURO in 1906, then in 2007 terms this newspaper should cost 4.13 euros. This second method seems more appropriate for two reasons. First, the 1907 price of Le Figaro (a newspaper that existed both in 1907 and 2007) is valued at 0.52 euros using the general price index and at 1.23 euros (a figure much closer to the 2007 price of 1.10 euros) using the hourly wage. Second, prices estimated with the hourly wage are comparable to those of modern financial periodicals, suggesting that newspaper prices actually increased more than the basket of goods included in the CPI has. We thank George Gallais-Hamonno and Christian Rietsch for suggesting these comparisons.

17

computed by the French statistical office (INSEE), the 2007 value of these prices ranges between

0.88 and 1.76 euros per issue. Computing the actual cost using hourly wages gives higher but

comparable figures (between 1.24 and 4.13 euros). The cost per page of editorial content was

also cheap, though it varied substantially and ranged from less than 1 centime for INTFIN to 2.15

centimes for RENT.

To assess media exposure, we counted how many times each publicly traded company

received exposure in each of the four newspapers. These pieces of information were collected for

the period from 1 July to 31 December 1907. To minimize possible effects stemming from a bear

or a bull market, we chose a period that was characterized by a fairly stable stock price index;

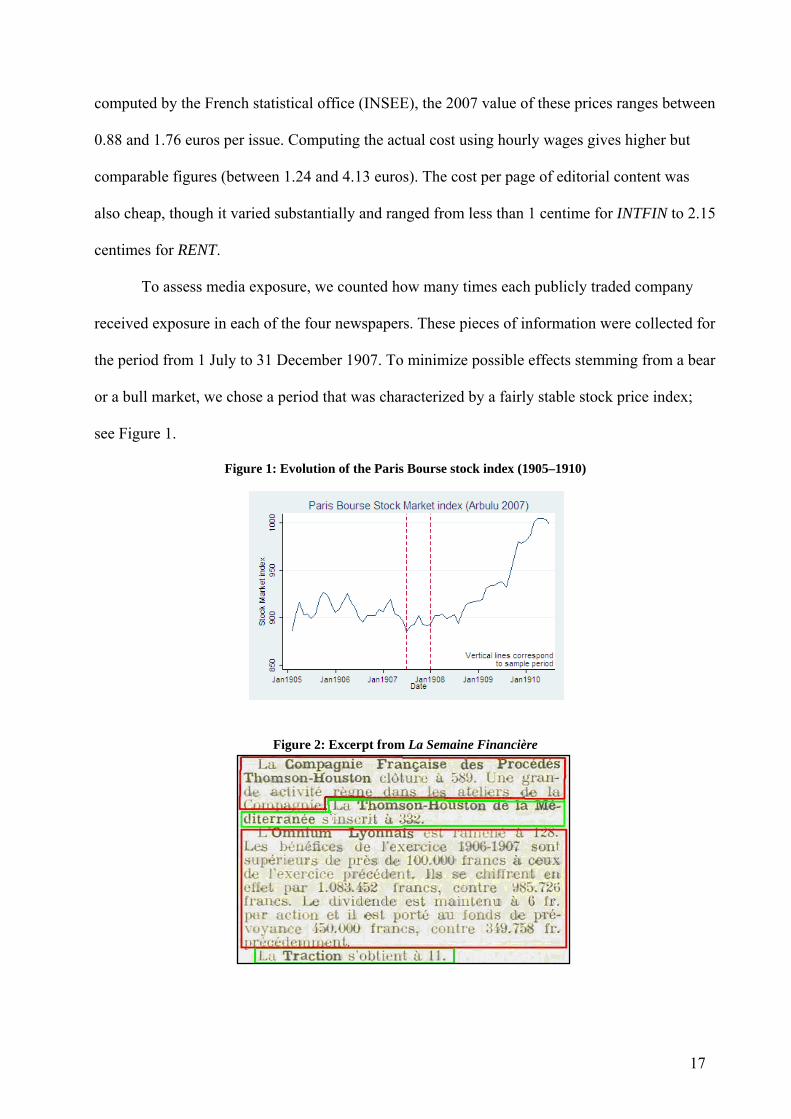

see Figure 1.

Figure 1: Evolution of the Paris Bourse stock index (1905–1910)

Figure 2: Excerpt from La Semaine Financière

18

The information published was coded as follows. We considered as significant any piece

of information richer than the stock price. Each newspaper published a list of prices in a separate

section, and each piece of information that mentioned only the stock price of the company was

coded as 0; richer pieces of information were coded as 1. Figure 2 is an excerpt from the 16

November 1907 edition of SEM that illustrates our coding methodology. For Thomson-Houston

de la Méditerranée and Traction, the newspaper gives only the stock price (outlined in red in the

figure) and so a value of 0 was assigned. Readers obtained more valuable information (outlined

in green) for the other two companies mentioned in Figure 2, such as “the factories of the

Compagnie Française des Procédés Thomson Houston experienced a significant business

activity” and that Omnium Lyonnais made higher profits in 1906–1907 than before. Hence these

two observations were each coded as 1 in the database. We performed this exercise for all the

information published on firms in the four newspapers.

The sum of the number of “news releases” concerning a given company defines a statistic

that accounts for the media coverage of this firm in a given newspaper. The descriptive statistics

of the sample indicate that, altogether, 929 firms were mentioned or discussed a total of 4,817

times. Because of missing data for explanatory variables, our analysis will henceforth focus on a

reduced sample of 705 firms that altogether received 4,414 such write-ups.

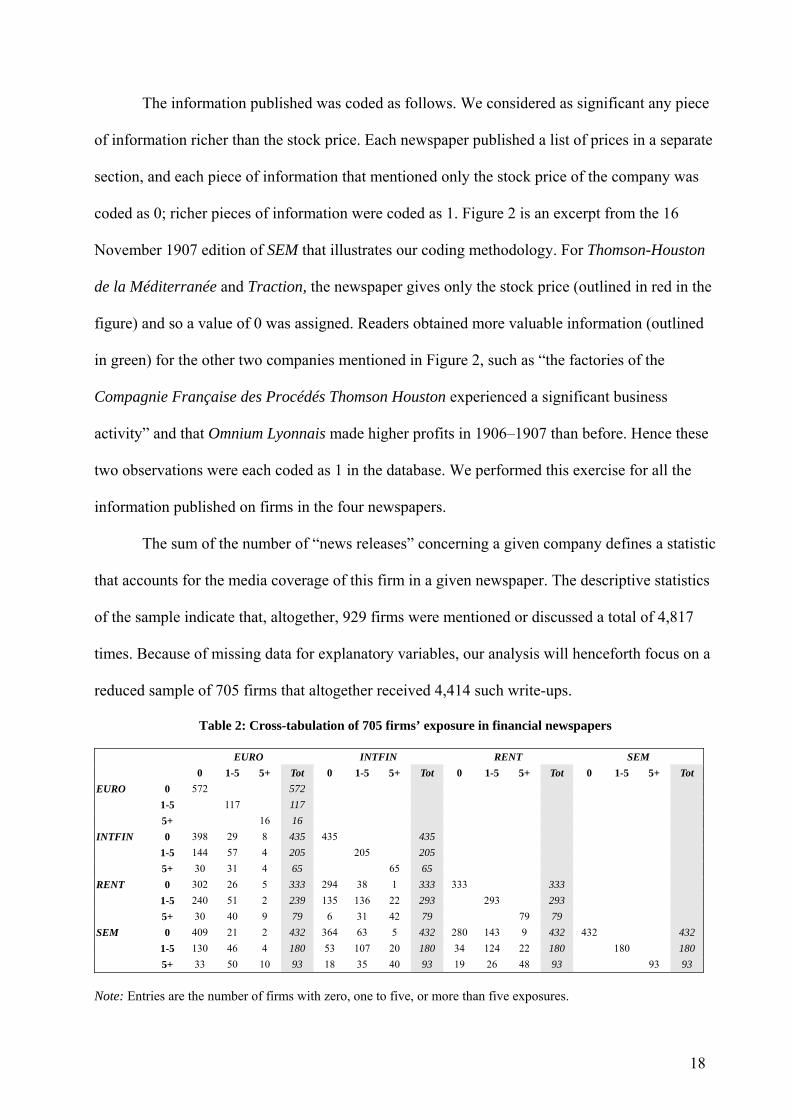

Table 2: Cross-tabulation of 705 firms’ exposure in financial newspapers

EURO INTFIN RENT SEM 0 1-5 5+ Tot 0 1-5 5+ Tot 0 1-5 5+ Tot 0 1-5 5+ Tot

EURO 0 572 572 1-5 117 117 5+ 16 16

INTFIN 0 398 29 8 435 435 435 1-5 144 57 4 205 205 205 5+ 30 31 4 65 65 65

RENT 0 302 26 5 333 294 38 1 333 333 333 1-5 240 51 2 239 135 136 22 293 293 293 5+ 30 40 9 79 6 31 42 79 79 79

SEM 0 409 21 2 432 364 63 5 432 280 143 9 432 432 432 1-5 130 46 4 180 53 107 20 180 34 124 22 180 180 180 5+ 33 50 10 93 18 35 40 93 19 26 48 93 93 93

Note: Entries are the number of firms with zero, one to five, or more than five exposures.

19

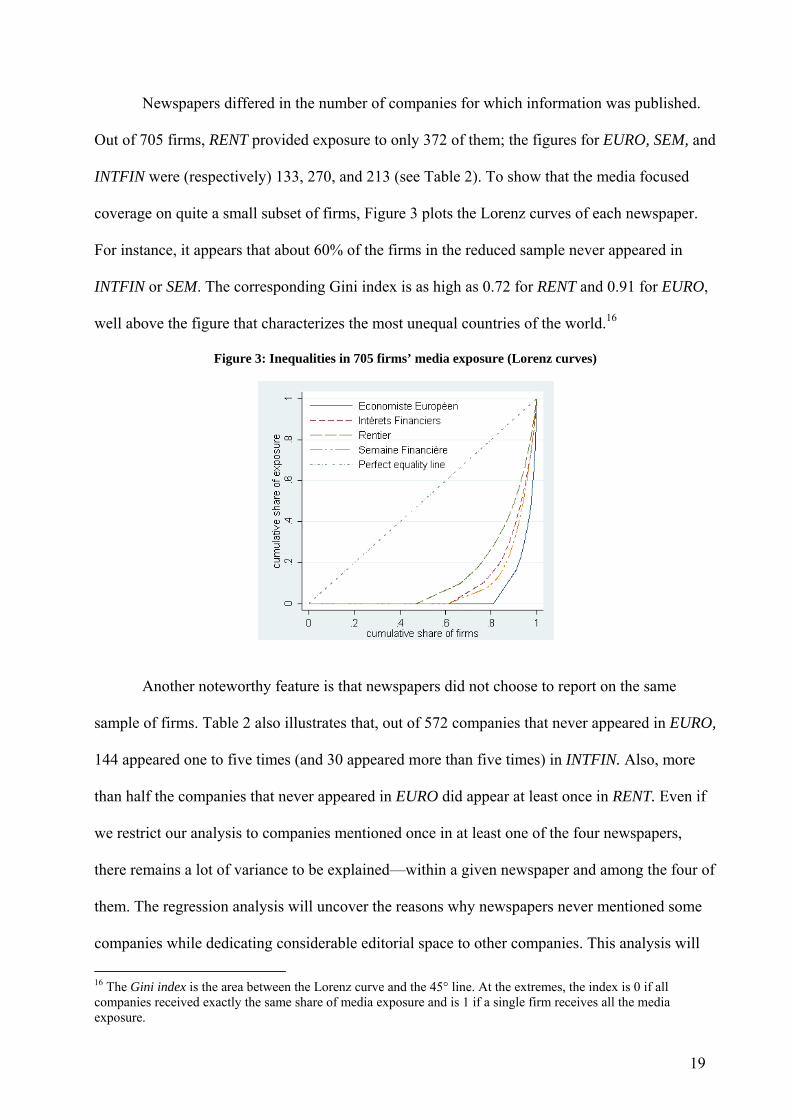

Newspapers differed in the number of companies for which information was published.

Out of 705 firms, RENT provided exposure to only 372 of them; the figures for EURO, SEM, and

INTFIN were (respectively) 133, 270, and 213 (see Table 2). To show that the media focused

coverage on quite a small subset of firms, Figure 3 plots the Lorenz curves of each newspaper.

For instance, it appears that about 60% of the firms in the reduced sample never appeared in

INTFIN or SEM. The corresponding Gini index is as high as 0.72 for RENT and 0.91 for EURO,

well above the figure that characterizes the most unequal countries of the world.16

Figure 3: Inequalities in 705 firms’ media exposure (Lorenz curves)

Another noteworthy feature is that newspapers did not choose to report on the same

sample of firms. Table 2 also illustrates that, out of 572 companies that never appeared in EURO,

144 appeared one to five times (and 30 appeared more than five times) in INTFIN. Also, more

than half the companies that never appeared in EURO did appear at least once in RENT. Even if

we restrict our analysis to companies mentioned once in at least one of the four newspapers,

there remains a lot of variance to be explained—within a given newspaper and among the four of

them. The regression analysis will uncover the reasons why newspapers never mentioned some

companies while dedicating considerable editorial space to other companies. This analysis will

16 The Gini index is the area between the Lorenz curve and the 45° line. At the extremes, the index is 0 if all companies received exactly the same share of media exposure and is 1 if a single firm receives all the media exposure.

20

enable us to assess each journal’s editorial policy, that is, the choices made when selecting the

subsample of firms to feature.

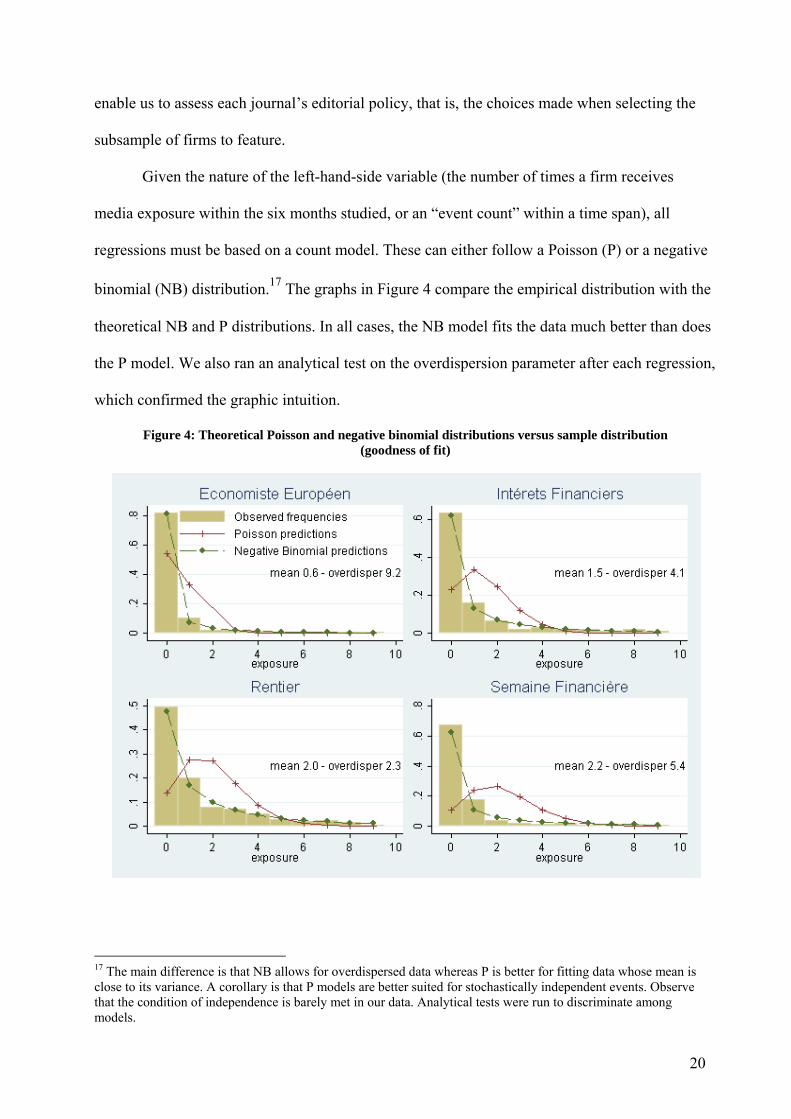

Given the nature of the left-hand-side variable (the number of times a firm receives

media exposure within the six months studied, or an “event count” within a time span), all

regressions must be based on a count model. These can either follow a Poisson (P) or a negative

binomial (NB) distribution.17 The graphs in Figure 4 compare the empirical distribution with the

theoretical NB and P distributions. In all cases, the NB model fits the data much better than does

the P model. We also ran an analytical test on the overdispersion parameter after each regression,

which confirmed the graphic intuition.

Figure 4: Theoretical Poisson and negative binomial distributions versus sample distribution (goodness of fit)

17 The main difference is that NB allows for overdispersed data whereas P is better for fitting data whose mean is close to its variance. A corollary is that P models are better suited for stochastically independent events. Observe that the condition of independence is barely met in our data. Analytical tests were run to discriminate among models.

21

4.2. Database

The list of covariates is organized into three groups. The first includes all variables summing up

the financial performance, and the second adds controls for characteristics of the firm. Finally,

the third group concerns payments made by firms to newspapers. In this section we describe how

these variables were constructed.

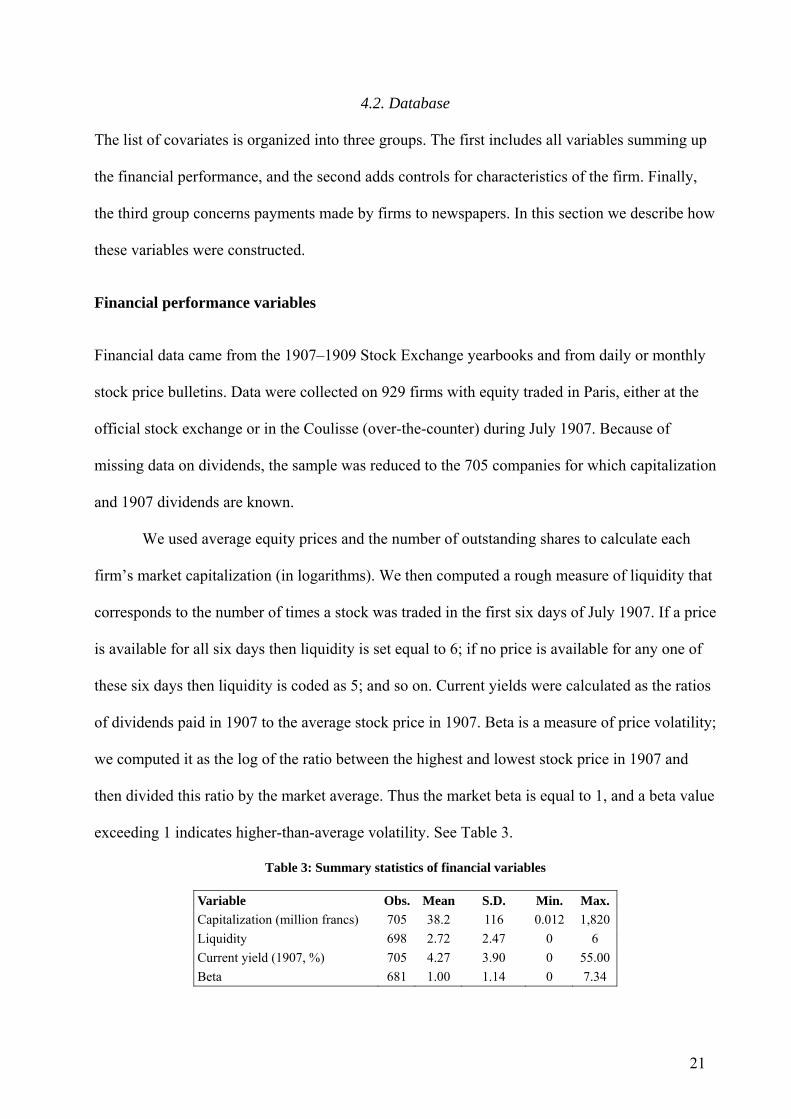

Financial performance variables

Financial data came from the 1907–1909 Stock Exchange yearbooks and from daily or monthly

stock price bulletins. Data were collected on 929 firms with equity traded in Paris, either at the

official stock exchange or in the Coulisse (over-the-counter) during July 1907. Because of

missing data on dividends, the sample was reduced to the 705 companies for which capitalization

and 1907 dividends are known.

We used average equity prices and the number of outstanding shares to calculate each

firm’s market capitalization (in logarithms). We then computed a rough measure of liquidity that

corresponds to the number of times a stock was traded in the first six days of July 1907. If a price

is available for all six days then liquidity is set equal to 6; if no price is available for any one of

these six days then liquidity is coded as 5; and so on. Current yields were calculated as the ratios

of dividends paid in 1907 to the average stock price in 1907. Beta is a measure of price volatility;

we computed it as the log of the ratio between the highest and lowest stock price in 1907 and

then divided this ratio by the market average. Thus the market beta is equal to 1, and a beta value

exceeding 1 indicates higher-than-average volatility. See Table 3.

Table 3: Summary statistics of financial variables

Variable Obs. Mean S.D. Min. Max. Capitalization (million francs) 705 38.2 116 0.012 1,820 Liquidity 698 2.72 2.47 0 6 Current yield (1907, %) 705 4.27 3.90 0 55.00 Beta 681 1.00 1.14 0 7.34

22

Firm characteristics

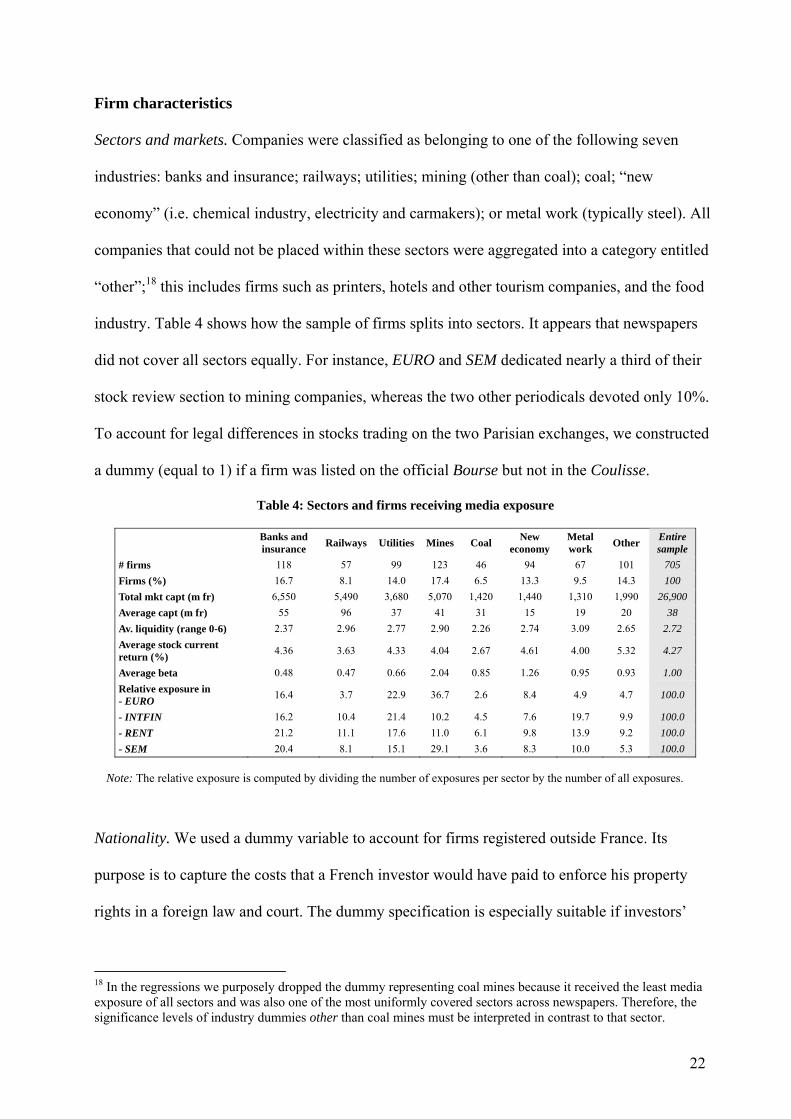

Sectors and markets. Companies were classified as belonging to one of the following seven

industries: banks and insurance; railways; utilities; mining (other than coal); coal; “new

economy” (i.e. chemical industry, electricity and carmakers); or metal work (typically steel). All

companies that could not be placed within these sectors were aggregated into a category entitled

“other”;18 this includes firms such as printers, hotels and other tourism companies, and the food

industry. Table 4 shows how the sample of firms splits into sectors. It appears that newspapers

did not cover all sectors equally. For instance, EURO and SEM dedicated nearly a third of their

stock review section to mining companies, whereas the two other periodicals devoted only 10%.

To account for legal differences in stocks trading on the two Parisian exchanges, we constructed

a dummy (equal to 1) if a firm was listed on the official Bourse but not in the Coulisse.

Table 4: Sectors and firms receiving media exposure

Banks and insurance Railways Utilities Mines Coal New

economy Metal work Other Entire

sample # firms 118 57 99 123 46 94 67 101 705 Firms (%) 16.7 8.1 14.0 17.4 6.5 13.3 9.5 14.3 100 Total mkt capt (m fr) 6,550 5,490 3,680 5,070 1,420 1,440 1,310 1,990 26,900 Average capt (m fr) 55 96 37 41 31 15 19 20 38 Av. liquidity (range 0-6) 2.37 2.96 2.77 2.90 2.26 2.74 3.09 2.65 2.72 Average stock current return (%) 4.36 3.63 4.33 4.04 2.67 4.61 4.00 5.32 4.27

Average beta 0.48 0.47 0.66 2.04 0.85 1.26 0.95 0.93 1.00 Relative exposure in - EURO 16.4 3.7 22.9 36.7 2.6 8.4 4.9 4.7 100.0

- INTFIN 16.2 10.4 21.4 10.2 4.5 7.6 19.7 9.9 100.0 - RENT 21.2 11.1 17.6 11.0 6.1 9.8 13.9 9.2 100.0 - SEM 20.4 8.1 15.1 29.1 3.6 8.3 10.0 5.3 100.0

Note: The relative exposure is computed by dividing the number of exposures per sector by the number of all exposures.

Nationality. We used a dummy variable to account for firms registered outside France. Its

purpose is to capture the costs that a French investor would have paid to enforce his property

rights in a foreign law and court. The dummy specification is especially suitable if investors’

18 In the regressions we purposely dropped the dummy representing coal mines because it received the least media exposure of all sectors and was also one of the most uniformly covered sectors across newspapers. Therefore, the significance levels of industry dummies other than coal mines must be interpreted in contrast to that sector.

23

costs were mainly fixed cost. Finally, the dummy “colony” captures the effect of a firm operating

in a French colony (52 firms).

Distance. In order to account for differences in coverage explained by mere geography, we

computed a measure of distance that relies on the country in which the firms operated its (main)

business. The measure captures the difficulty that investors might encounter in gathering

information about firms. This is especially important because many companies (87 in our

sample) operated outside the country in which they were registered (mostly France, the United

Kingdom, and Belgium). To account for the familiarity that investors might have felt toward

some country, distance is (inversely) weighted by the country share in the total capitalization of

the listed companies.19

Payments to newspapers

Advertisements. Firms could pay for two types of ads. The advertisement section included

commercial announcements of new products or services such as railway fares, insurance

companies’ policies, the opening of a new branch by a given bank, and so forth. Issuers of

publicly traded securities also used such advertising as a medium to inform the wider public on

financial news, such as the introduction of a new security on the market or shareholders’

meeting, and also to announce the serial numbers of bonds drawn at the lottery for

reimbursement. We have counted the number of advertisements of both types paid by each

company. The regressions used two specifications for this variable, either the actual number of

ads or a dummy (equal to 1) if the company advertised in the newspaper. As shown in Table 5,

firms that advertised have, on average, a significantly higher capitalization and lower stock

19 The intuition behind this measure is that as the number of stocks from a particular country grows, so should the flow of information from that country to Paris, making it seem to be less distant. Thus, high availability of information is assumed to reduce the country’s perceived distance in investors’ minds (and vice versa). The significance and sign of the variable in the regressions are not affected by this weighting.

24

volatility than firms that did not advertise. But in terms of returns, the differences between these

two types of firms are insignificant.

Table 5: Effect of advertising (N = 705 firms) as measured by two-sample t-test with unequal variances EURO INTFIN RENT SEM no ads ads no ads ads no ads ads no ads ads

Log capitalization Obs. 634 71 531 174 599 106 532 173 Mean 6.91 7.64 6.90 7.22 6.87 7.62 6.89 7.24 Difference –0.74*** –0.32*** –0.75*** –0.35*** Current yield Obs. 634 71 531 174 599 106 532 173 Mean 0.0428 0.0415 0.0433 0.0407 0.0426 0.0434 0.0432 0.0412 Difference 0.0013 0.0026 –0.0008 0.0019 Beta Obs. 612 69 508 173 575 106 510 171 Mean 1.03 0.74 1.07 0.78 1.06 0.70 1.09 0.72 Difference 0.29*** 0.29*** 0.36*** 0.37*** *** = difference between means significant at 99% level.

Bank dummies. As previously mentioned, banks provided firms several services such as financial

advertisements, legal representation in France for foreign companies, and payment of coupons

and dividends. Because financial yearbooks indicate which bank was appointed to pay a

company’s dividends and coupons, we use this information as a proxy for the bank to which each

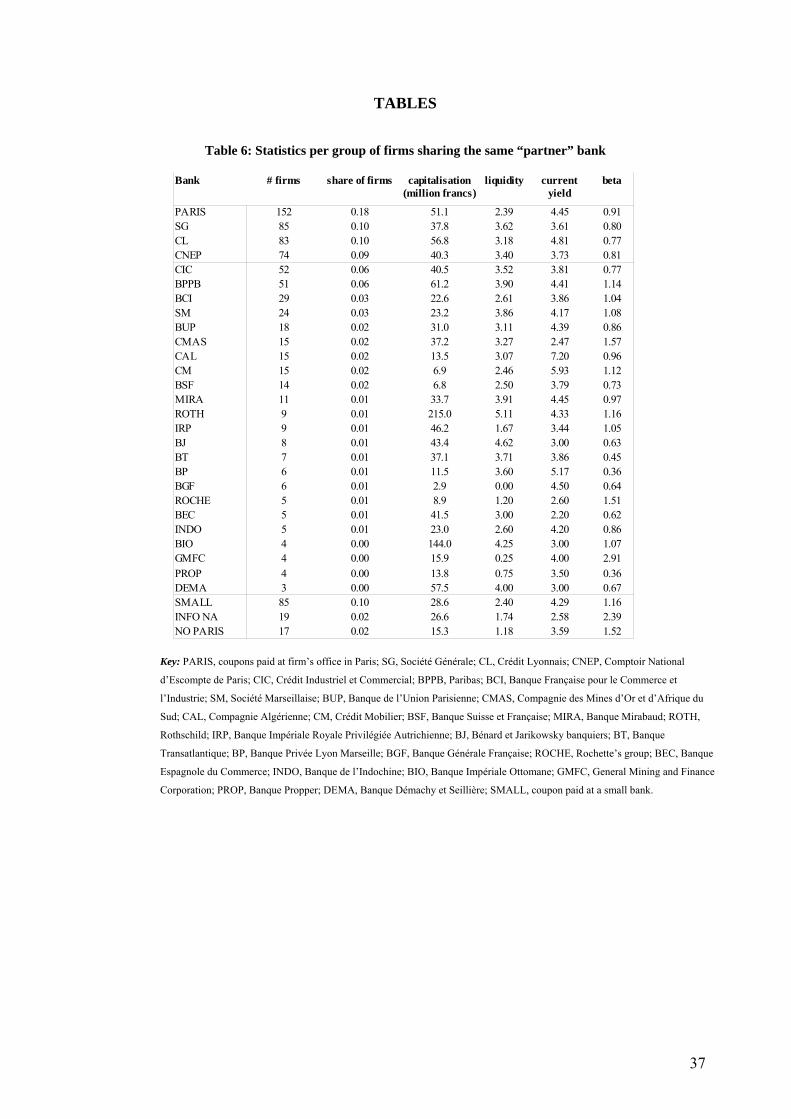

firm delegated their relation with newspapers. Table 6 presents the group averages of financial

variables for all companies sharing the same partner bank.20 The largest group consists of

companies whose coupons were paid only in their own Paris office, without any bank

intermediation. Then come the three biggest French deposit banks at the time (Crédit Lyonnais,

Société Générale, and Comptoir National d'Escompte de Paris), each having a market share of

9–10%. The rest of the market was shared among a handful of smaller yet active investment

banks and myriad other intermediaries all aggregated here as “small banks”. We also included a

dummy variable (no_paris) for companies that had no representation in the city and another

dummy (info_na) for companies whose coupon payment information was unavailable.

[INSERT TABLE 6 ABOUT HERE]

20 Although group averages are calculated on the the sample of 705 firms, some are included in more than one group because they had more than one partner bank.

25

4. Results

Our aim is to discover whether media exposure is a function either of a firm’s financial

performance or of payments that it made to newspapers. This test is implemented by matching

the sample of firms cited in the media and the characteristics of the population of listed firms.

We first review results concerning the impact of financial variables on editorial policy, and then

we quantify the bias created by payments.

4.1. Various targeted readerships

The first result is that editors did not choose the content of their periodicals at random, since they

were valuable to readers as guidelines for investments only if they highlighted some firms and

profiled their position in the market. Consequently, most financial variables are significant in the

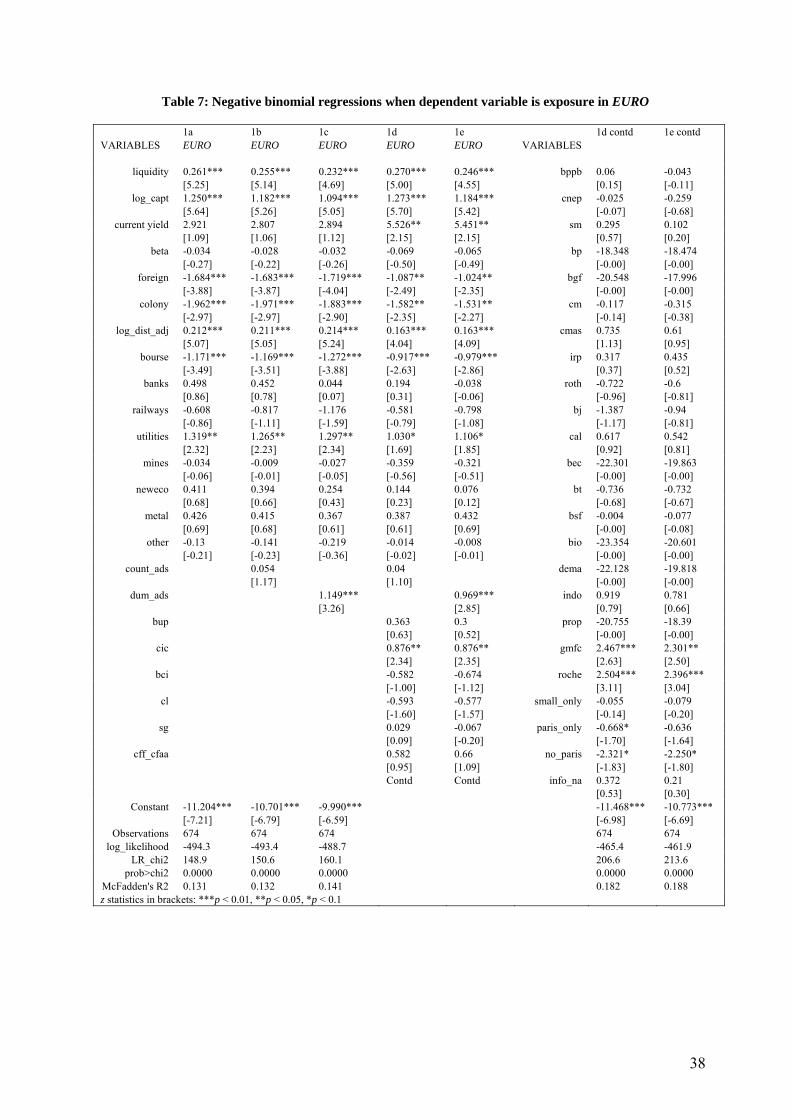

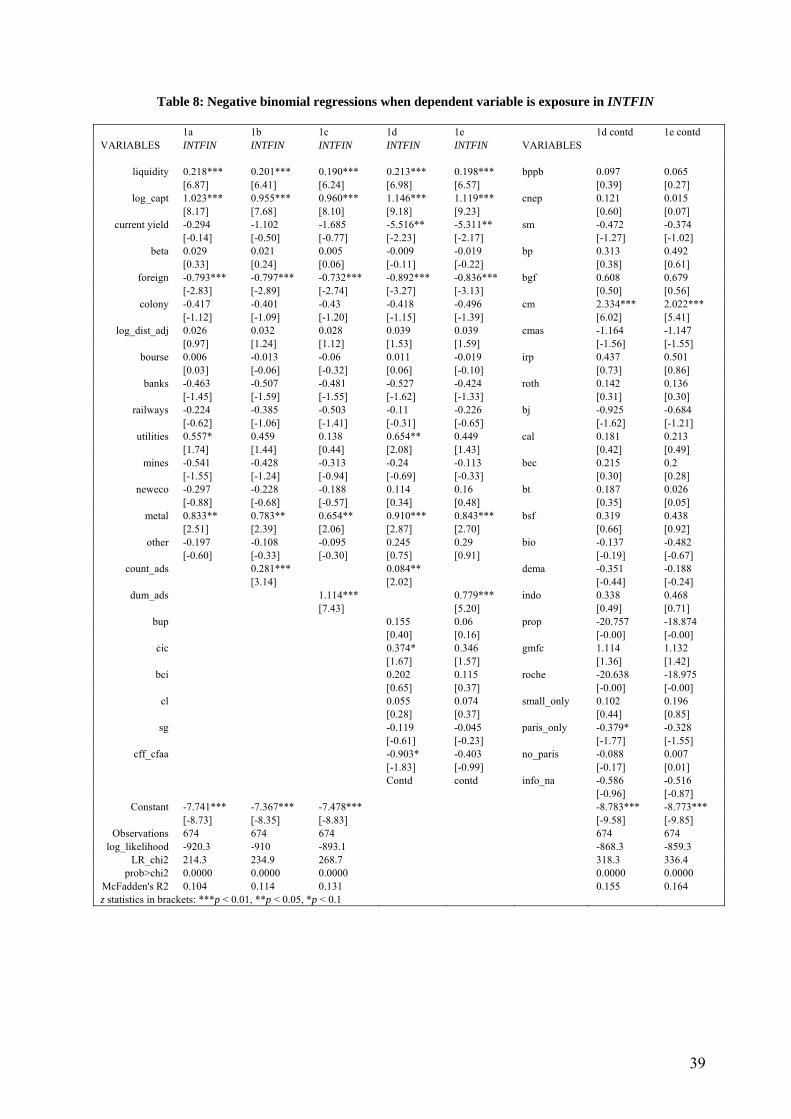

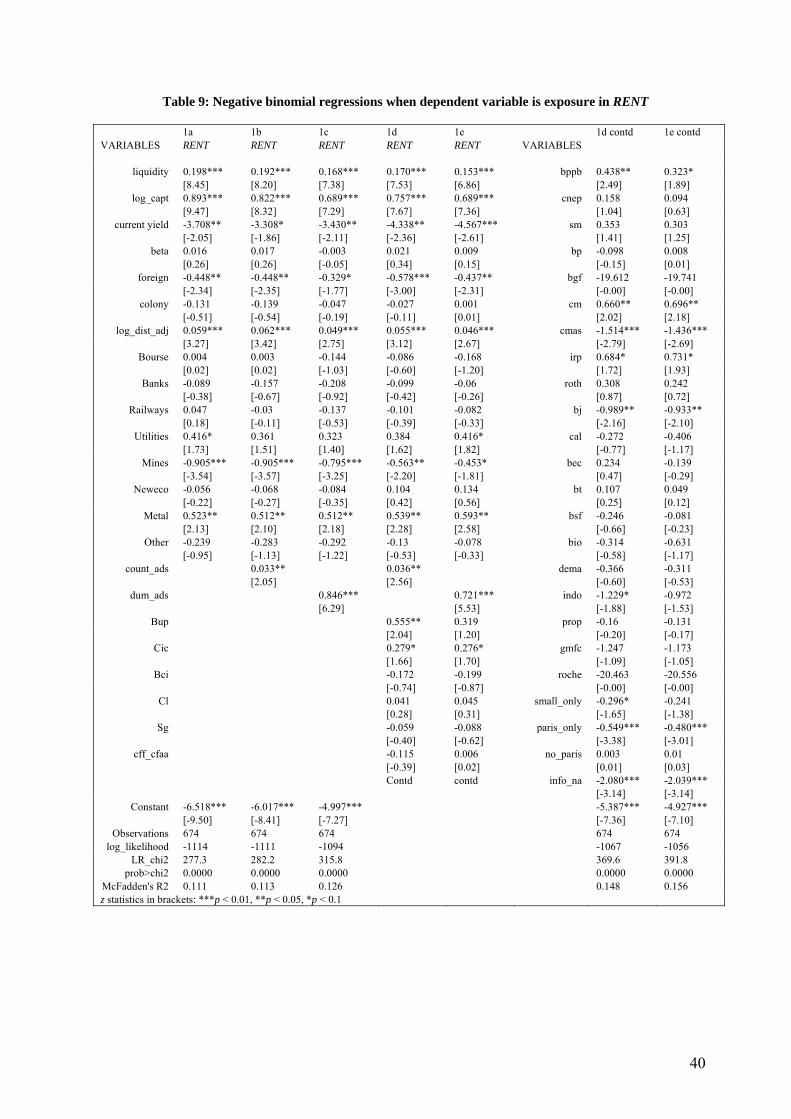

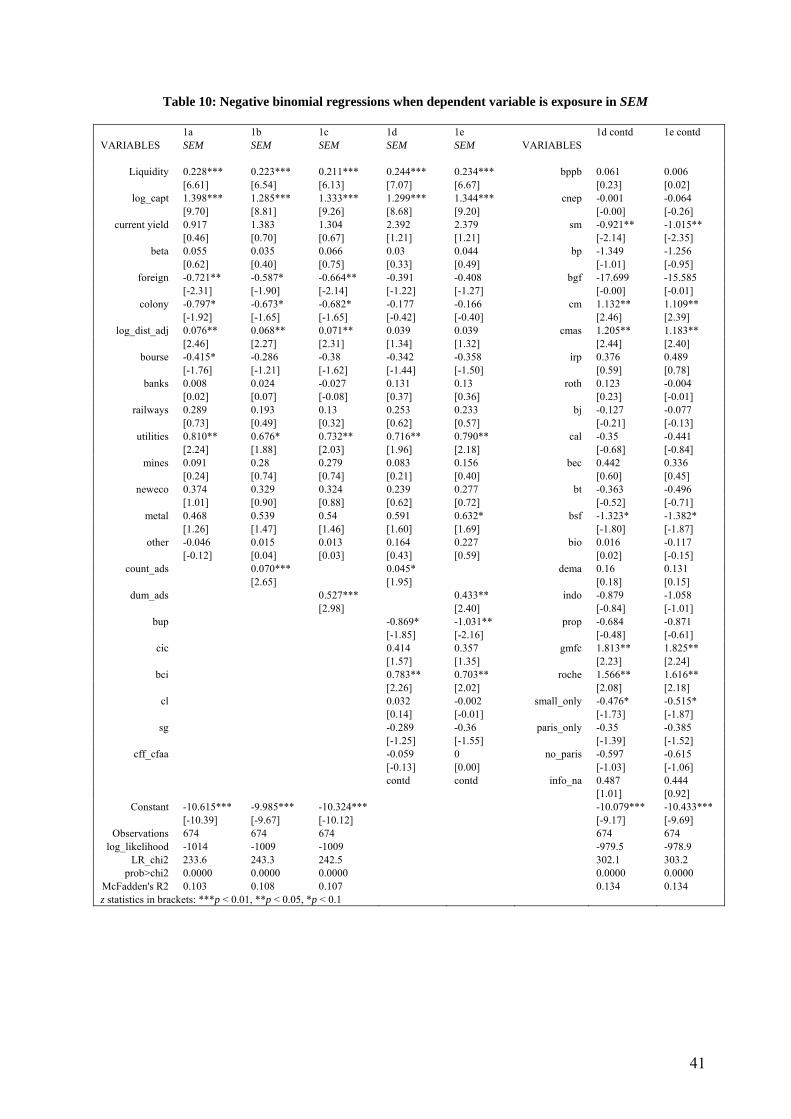

regression. Tables 7–10 give the regression outputs for each newspaper. They show that a firm’s

market capitalization and stock liquidity is always positively correlated with its media exposure.

The measure of stock price variance is never significant, which could indicate that most

newspapers did not target liquidity traders but rather investors with a buy-and-hold strategy (i.e.,

rentiers).

[INSERT TABLE 7 ABOUT HERE]

[INSERT TABLE 8 ABOUT HERE]

[INSERT TABLE 9 ABOUT HERE]

[INSERT TABLE 10 ABOUT HERE]

The significance of those financial variables changes across newspapers, which can be

interpreted as indicating that different groups of readers (e.g., risk-averse versus risk-neutral

investors) were being targeted. For example, EURO tends to prefer firms not listed on the official

stock exchanges; the other three periodicals did not exhibit such a preference. Columns 1d and

1e of Tables 7–10 show the results of including the bank dummy in the regression. The sign of

26

current return in these columns confirms that newspapers were indeed trying to differentiate their

products by highlighting different subsets of companies. Whereas EURO promoted firms with

relatively high current returns, both INTFIN and RENT reported on those with lower returns.

Two reasons can explain this. First, firms with a lower yield also feature a lower default risk (not

measured in this regression); second, a lower return implies a higher price/dividend ratio. Thus

INTFIN and RENT may have been focusing on “blue chip” firms (i.e., those with a high growth

potential).

Another dimension on which newspapers competed was the sectors that were covered. As

we saw in Table 4, they did not cover all sectors equally. Because industries had different

characteristics, regressions help to test for newspapers specialization in a multivariate setting.

For instance, even though banks and insurance companies together represented 16–21% of all

write-ups (ranging from the most-exposed to the third most-exposed of our eight industry

categories), they had the second-highest average capitalization and one of the lowest beta values.

Hence, once all variables are factored into the analysis, banks turn out to be not significantly

different from coal mines—the least-exposed industry. Utilities were overrepresented in all four

newspapers, while RENT and INTFIN also favored the metal industry. Finally, RENT tended to

cover mining firms significantly less than the other industries. It seems fair to conclude that the

varying exposure across journals (and within a given journal) reflected firms’ characteristics and

the newspapers’ choices of which industries to cover most extensively.

Being registered in a foreign country had a negative impact on media exposure. We

interpret this lower coverage as the logical counterpart of investors’ lesser willingness to hold

foreign stocks owing to higher enforcement costs;21 ceteris paribus, a French contract would

have been easier to enforce and thus more attractive. This does not mean that French investors or

21 Although we displayed the specification with the dummy, we also tried to model this in terms of distance between Paris and the foreign country. That variable was not significant in half the regressions, whereas the dummy was always significant (and negative). This could reflect that the costs of enforcing contracts abroad were of a “fixed” nature and thus not proportional to distance.

27

financial newspapers neglected stocks of firms operating abroad. In fact, a substantial share of

savings was invested in foreign assets, so investors needed information that would help them

monitor such investments. Consequently, more information was needed on more-distant firms in

order to compensate for the increased difficulty of monitoring them directly. With the exception

of INTFIN, the periodicals in our sample accommodated investors by granting relatively more

coverage to firms whose activities were farther away from France.

The evidence suggests that media outlets were of actual value to investors, enabling

readers to make more informed investment choices. Moreover, editors evidently used various

criteria when choosing companies, thereby competing on various dimensions to attract readers.

Our next step is to assess the size of the resulting biases.

4.2. Testing for biases originating in advertisements and direct payments

A newspaper’s coverage could have been distorted either by the volume of advertising or by

direct payments. The variable Bank is taken as the proxy for payments of the editorial content by

firms. We shall discuss the effect of sequentially including these variables in the regressions,

provide a measure of the biases’ importance, and give some insights on the positive bias.

A first test of the positive information bias can be given, in a rough fashion, by

computing the proportion of negative published information. We adopted a rather restrictive

definition of negative news; thus, such events as a small decrease in sales or a decision not to pay

dividends despite positive earnings were not classified as negative.22 With this criterion, only

5.1% of the write-ups in EURO, 4.9% in INTFIN, 8.2% in RENT, and 3.5% in SEM were

negative. Given these low figures, it seems that newspapers were somewhat reluctant to publish

negative information. However, when we ran all regressions with a new dependent variable—the

proportion of positive published information —the results were strikingly similar to those

22 Classifications based on quality judgments are less objective than those based on quantities. This fact is what ultimately led us to focus our analysis on the quantity of information (i.e., the amount of media exposure).

28

reported in Tables 7–10. This suggests that the firms about which negative news was published

were otherwise not much different from the others.

To check whether companies featured in the advertising section also had their exposure

boosted in the editorial section, we added in the regressions two alternative measures of

advertising; see columns 1b and 1c of Tables 7–10. The significance of the financial variables is

not disrupted by our introducing this variable, and the coefficients remain fairly stable. It does

appear that advertising expenses increased a company’s exposure in the editorial section,

although the effect is more ambiguous in EURO.

However, the advertising variable is ineffective in capturing the effect of direct payments

on a newspaper’s editorial policy. In Section 2 we showed that the relationship a firm had with a

bank is a reasonable proxy for such payments, and Table 6 reported on whether the choice of a

partner bank had any impact on firms’ media exposure. Columns 1d and 1e in Tables 7–10 (one

for each periodical) give the results for the bank dummies. It shows that companies that paid

newspapers directly had significantly less exposure in RENT and that companies paying via non-

Parisian banks received less exposure in EURO. Together, the latter variables (advertising and

payments to newspapers) give us some idea of the relative advantage of having a bank as

intermediary—especially if the bank is not too small and has at least an office in Paris.

Out of 26 bank dummies, only a few for each journal turn out to be significant. As

expected, a firm linked to the Crédit Mobilier Français would benefit from a boost of exposure

in the journal (INTFIN) owned by the same bank. But even the most reputable journals seemed

to have been linked to one or more banks: EURO is positively associated with the CIC, the

GMFC, and Rochette’s group; RENT is positively associated with the BPPB, the CIC, and the

CM and is negatively associated with the CMAS and the BJ (see table footnotes for

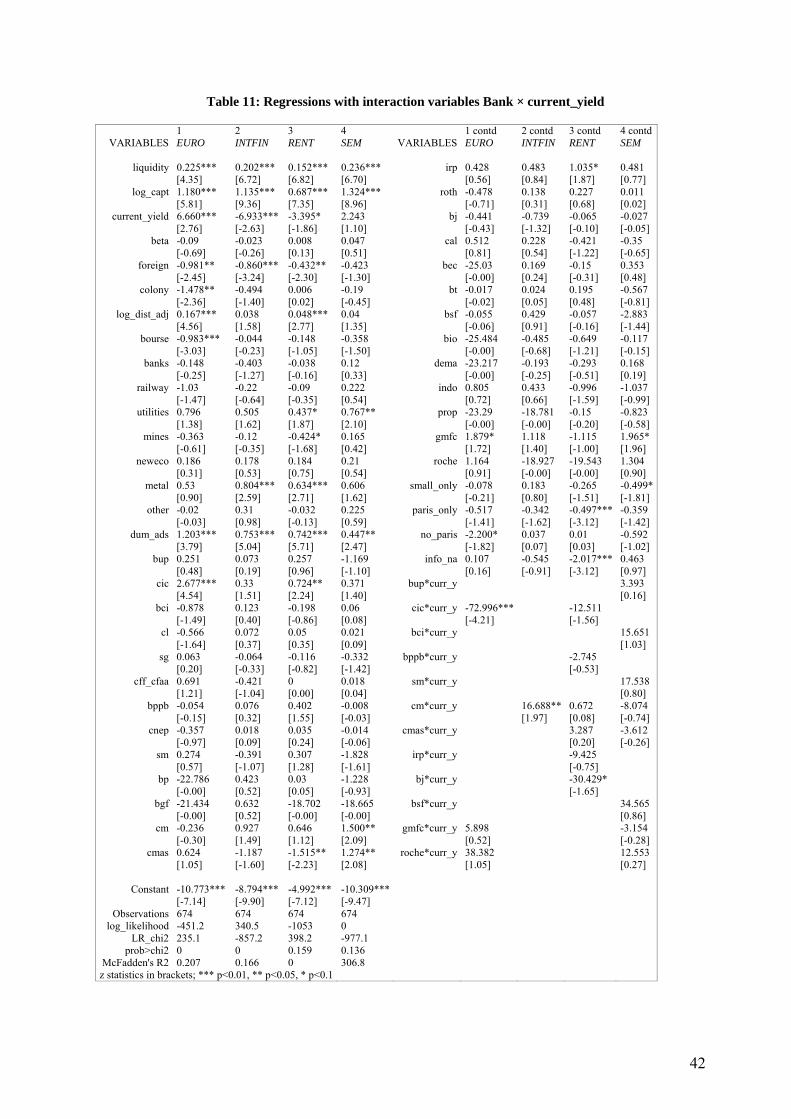

abbreviations). In a separate set of regressions (see Table 11), we test whether there was an

29

interaction effect between the bank dummies and the firms’ capitalization and current yield.23

The results show that, in some cases, introducing the interaction term eliminates the bank

effect’s significance. A significant positive (resp. negative) coefficient on the interaction term

suggests that banks choose to boost (resp. hinder) the exposure of companies that yielded a

higher return among its portfolio elements.

[INSERT TABLE 11 ABOUT HERE]

The significance of some of the bank dummy variables indicates that editorial content

was biased toward some firms. Two methods can be used to judge the size of the impact of these

biases on investors: (i) computing the marginal effect of the coefficient of the bank dummies;

and (ii) constructing counterfactual scenarios.

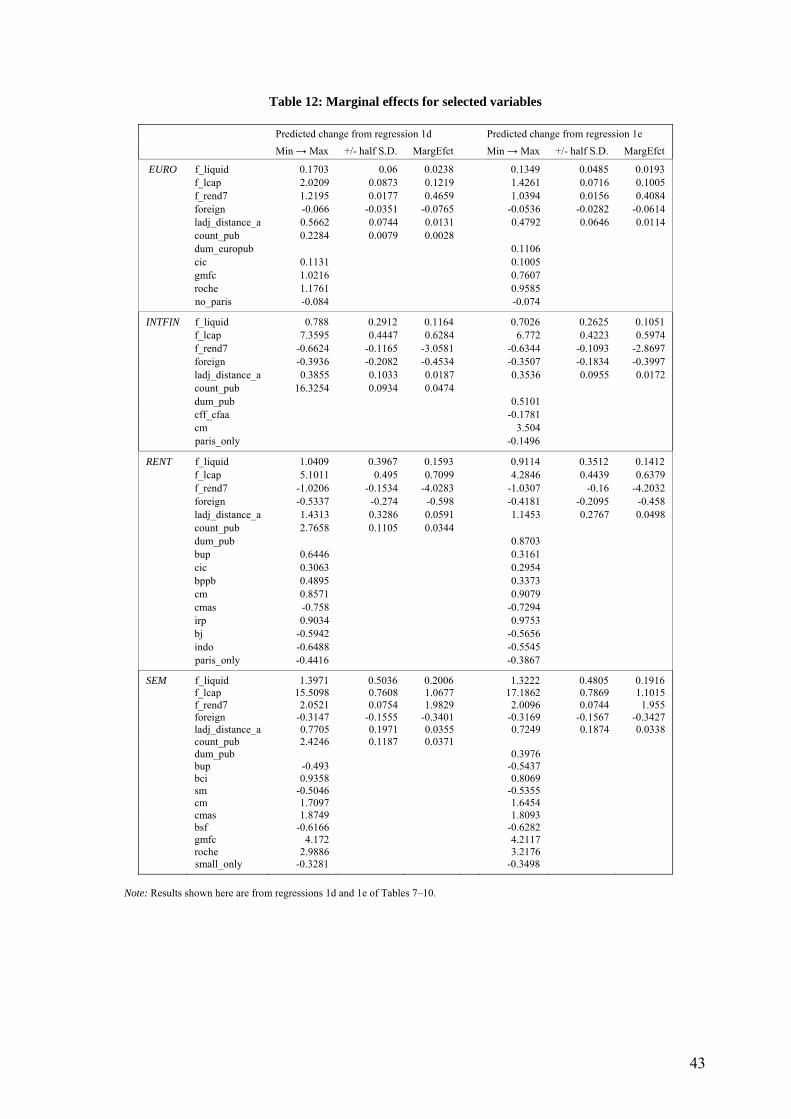

First, Table 12 shows the marginal effect of the bank dummy variables and allows us to

compare them with the effect of financial variables on predicted media exposure. The predicted

change in the number of write-ups in EURO for the average firm would increase by 0.0079 if the

number of ads were to increase by half a standard deviation (i.e., 1.39 ads), holding all the other

variables at their mean. The number of write-ups would actually increase by 0.2284 if a company

increased its number of ads from zero to forty (the maximum). In gauging whether this is a small

effect, we should compare it to the marginal effect of the other variables in the same regression.

Hence we could argue that the number of ads a firm bought in EURO had a negligible effect on

the firm’s exposure in that paper. Similarly, if the average firm increased the number of its ads in

INTFIN by half a standard deviation (or 0.98 ads) then its exposure in the editorial sections

would increase by 0.0934, a marginal effect that is 12 times greater than in the other newspaper.

We could give further examples. The influence of banks is easier to assess. For instance, firms

23 The interaction terms Bank × log_capitalization were almost never significantly different from zero, so in the table we show only the set of regressions with the interaction terms Bank × current_yield. The bank dummies used to construct interaction variables are those whose coefficients were significantly different from 0 in both the 1d and 1e regressions of the respective newspaper (see Tables 7–10).

30

linked with Rochette or GMFC experienced a substantial increase in exposure in both EURO and

SEM.

[INSERT TABLE 12 ABOUT HERE]

Second, we look at the overall editorial policy and compare it to counterfactual scenarios

in which firms purchase no advertising and/or are not linked to any particular bank.24 We assess

alternative asset allocations by assuming that investors followed newspapers’ content as a

guideline when selecting their portfolios. For each newspaper we constructed five different

portfolios in which the weight given to each firm is proportional to:

1. its actual number of write-ups (portfolio E for EURO, I for INTFIN, R for RENT, S for

SEM);

2. its positive write-ups (portfolios E+, I+, R+, S+);

3. counterfactual predicted write-ups assuming that firms purchased no newspaper

advertising (E+1, I+1, R+1, S+1);

4. counterfactual predicted write-ups assuming that firms had no link with any bank that

was significant in regression 1e of the respective journal (E+2, I+2, R+2, S+2);

5. counterfactual predicted write-ups assuming that firms purchased no advertising and had

no links with the banks mentioned in portfolio 4 (E+3, I+3, R+3, S+3).

Figure 5 plots the different combinations of stock price variance and current yield (that

proxy for risk and return) of these portfolios. For obvious reasons we will consider the portfolios

described at 2 (above) as the baseline for constructing counterfactual scenarios. The first

observation is that these portfolios (i.e., E+, I+, R+, S+) behaved consistently with the theory,

according to which risk and return move in the same direction. For example, as would be

expected from its title, RENT privileged those stocks with both a lower return and a lower risk, a

24 Counterfactual scenarios correspond to the predicted number of write-ups a firm would receive in a given journal if it had a different profile. To derive these scenarios, we multiplied the estimated coefficients from regressions 1e of Tables 7–10 by a modified data set in which the appropriate variables were changed (e.g. changing the Ads dummy from 1 to 0 when we wanted to simulate that firms did not advertise in that newspaper).

31

feature of likely appeal to risk-averse investors; in contrast, EURO seems to have targeted risk-

seeking readers. This confirms once again that journals differentiated their products by

highlighting different subsets of firms.

Figure 5: Performance of actual and counterfactual portfolios

In light of this evidence, it is difficult to rank the performance of journals without

knowing the preferences of investors. As for whether advertising (Ads) and direct payments of

the editorial content (proxied by Banks) distorted portfolio allocation, the answer is not clear-cut.

All portfolios based on actual media exposure fall within the confidence interval of their

respective benchmark based on positive news only, which indicates that there is not much

statistical difference between the set of all and the subset of positive write-ups. Moreover, about

half of the counterfactual portfolios are not significantly different (or nearly so) from the

baseline. In all other cases, the resulting allocation differs only in terms of the proxy for risk. For

example, portfolios 1 and 3 of both EURO and INTFIN are riskier than the benchmark but are

not significantly more rewarding. It thus seems that the influence of advertisements and banks

might actually have been to lower risk or, more accurately, to bring it back in line with the

journal’s editorial policy. This hypothesis is consistent with the following strategy: When

32

newspapers care about their reputation and their readership but at the same time need to increase

their revenue from information sources, they could accept payment only from companies like

those that they wanted to highlight. This explains why some banks appear in the regressions with

a negative sign. Rather than evidence of not extorting money from those banks, this suggests that

newspapers simply didn’t consider a company that was not in line with their editorial policy.

5. Conclusion

This paper provides quantitative evidence of how four of the main financial newspapers in early

20th-century France selected what information to publish on listed firms. We show that firms’

media exposure is positively correlated with the financial variables of the firm and that

newspapers differentiate their readerships along the various financial variables. Newspapers

were thus selecting firms according to their editorial policy. We also find that the ownership of a

newspaper by a bank does make a difference: it leads to media overexposure of firms in its

portfolio (in terms of what their financial performance would merit). We test whether payments

made by banks affected media exposure and find significant correlations for some banks in each

newspaper. To assess the importance of these biases, counterfactual scenarios were constructed

to simulate whether biases could have resulted in a distortion in the allocation of funds. Our

results show that the observed allocation was not inferior to the counterfactual one. Indeed, for

two of the four newspapers, the biases increased both the return and the risk of the resulting

portfolio. We interpret these results as demonstrating that the development of financial markets

was indeed accompanied by a financial press that performed reasonably well. This conclusion

stands in sharp contrast to most of the literature concerning these phenomena.

33

References

Albert P. (1972). Histoire générale de la presse française, tome 3, Paris: PUF

Anderson S. P. and Gabszewicz J. J. (2006). The Media and Advertising: A Tale of Two-Sided

Markets. Handbook on the Economics of Art and Culture 1, 567-614

Arbulu P. (2007). Le marché parisien des actions au 19ème siècle Le marché financier français au

XIXe siècle 2, G. Gallais Hamonno ed., Publications de la Sorbonne, 365-458

Bhattacharya, U., N. Galpin, R. Ray, and Yu X. (2004). The Role of the Media in the Internet

IPO Bubble. Working paper Indiana University

Bencivengo Y., 2004, Les réseaux d'influence de la banque Rothschild, manuscript.

Béranger H. (1897). Les responsabilités de la presse contemporaine La revue bleue 8, 706-10.

Cassagnac (de) P.. (1893). La publicité dans les journaux. Paris: Imprimerie de Paul Dupont

Chan, W.S. (2003). Stock Price Reaction to News and No-News: Drift and Reversal After

Headlines Journal of Financial Economics, 70, 2, 223-260.

Chancelier I., 2001, Messieurs Mirabaud et Cie : D'Aigues Vives à Paris, via Genève et Milan,

Editions Familiales, 290 pages.

Coase, R. (1960). The Problem of Social Cost. Journal of Law and Economics 3, 1–44

Coase R. (1974). The Market for Goods and the Market for Ideas, American Economic Review

64, 384-91.

D'Alessio D. and Allen M. (2000). Media bias in presidential elections: a meta-analysis. Journal

of Communication 50, 133-156

Delporte, C. (1999). Les journalistes en France 1880-1950. Paris: Le Seuil.

Dupont H., 1890, Les Mines d’Or de l’Afrique du Sud. Paris: Librairie Lemaire et Dupont.

Dyck, A. and Zingales L. (2002). The Corporate Governance Role of the Media The Right to

Tell: The Role of Mass Media in Development. Washington: The World Bank

Dyck, A. and L. Zingales. (2004). Private Benefit of Control: An International Comparison

Journal of Finance 59, 533-596

Dyck, A., N. Volchkova and Zingales L. (2008). Corporate Governance Role of the Media:

Evidence from Russia Journal of Finance (forthcoming)

Esteves, R. (2007). Quis Custodiet Quem? Sovereign Debt and Bondholders’ Protection Before

1914. Working paper Oxford University

Eveno, P. (2003). L’argent de la presse française. Paris: Editions du CHTS

Feis, H. (1930, 1965). Europe, the world’s banker, 1870-1914, New York: Norton Library

34

Flandreau, M. (2003). Caveat Emptor: Copying with Sovereign Risk Under the International

Gold Standard International Financial History in the Twentieth Century, System and Anarchy,

Flandreau M., Holtfrerich C.-L. and James H. eds, Cambridge University Press.

Flandreau, M., C. Galimard, C. Jobst and Noguès-Marco P. (2008). Monetary Geography Before

the Industrial Revolution Cambridge Journal of Regions, Economy and Society forthcoming.

Folleville (de), D. (1911). Rapport de la commission chargée de procéder à une enquête sur les

circonstances qui ont préparé, précédé, accompagné ou suivi l'arrestation du financier

Rochette, Paris: Imprimerie de la chambre des députés

Gentzkow, M., Glaeser, E. and Goldin, C. (2004). The Rise of the Fourth Estate: How

Newspapers Became Informative and why it mattered. NBER 10791.

Gentzkow, M. and Shapiro, J. (2006). Media Bias and Reputation. Journal of Political Economy

114, 280-316

Gille, B. (1959). Etat de la presse économique et financière en France. Histoire des entreprises 4,

58-76.

Groseclose, T. J. and Milyo J. (2005). A Measure of Media Bias Quarterly Journal of Economics

120, 1191–237

Hautcoeur, P.C. (2006). Why and how to measure stock market fluctuations? Working paper

Hayakawa, S. I. (1940), Language in thought and action. San Diego: Harcourt Brace Jovanovich

Houston D., 1897, Copper Manual: Copper Mines and Copper Statistics, New York: J.W. Pratt

Huberman, G. and Regev, T. (2001). Contagious Speculation and a Cure for Cancer: A Non-

event that Made Stock Prices Soar. Journal of Finance 56, 387-396

Jeanneney, J.-N. (1984). La vénalité du journalisme financier pendant l’entre deux guerre.

L’argent caché. Paris: Points Seuil.

Kaufmann, E. (1914). La banque en France. Paris: Giard & Briére

Lajeune-Vilar, A. (1895). Les coulisses de la presse. Paris: A. Charles

Leroy-Beaulieu, A. (1896). L’internationale de l’or et la bancocratie. Revue des deux mondes

135, 42-68

Long, J. (1972). Russian Manipulation of the French Press. Slavic Review 31, 343-54

Lysis (Letailleur E.). (1912). Contre l'oligarchie financière, 11th ed., Paris: Albin Michel

Marinitsch, O. (1892). La Bourse théorique et pratique. Paris: Ollendorf

Martin, M. (2006). Retour sur « l’abominable vénalité de la presse française. Le Temps des

Médias 1, 22-33.

Merton, R. C. (1987). A Simple Model of Capital market Equilibrium with Incomplete

Information. Journal of Finance 42, 483-510.

35

Neal, L. (1988). The Rise of a Financial Press: London and Amsterdam, 1681-1810. Business

History 30, 163-78.

Neymark, A. (1911). Finances contemporaines. Paris: Félix Alcan