Measurement of Market Risk

Measurement of Market Risk. Market Risk Directional risk Relative value risk Price risk Liquidity risk Type of measurements –scenario analysis –statistical.

Dec 14, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Measurement of Market Risk

Market Risk

• Directional risk

• Relative value risk

• Price risk

• Liquidity risk

Type of measurements

– scenario analysis

– statistical analysis

Scenario Analysis

• A scenario analysis measures the change in market

value that would result if market factors were changed

from their current levels, in a specified way. No

assumption about probability of changes is made.

• A stress test is a measurement of the change in the

market value of a portfolio that would occur for a

specified unusually large change in a set of market

factors.

Value at Risk

• A single number that summarizes the likely loss in

value of a portfolio over a given time horizon with

specified probability.

• C-VaR states expected loss conditional on change in

value in the left tail of the distribution.

• Three approaches

– Historical simulation

– Model-building approach

– Monte Carlo simulation

Historical Simulation

• Identify market variables that determine the portfolio

value

• Collect data on movements in these variables for a

reasonable number of historical days

• Build scenarios that mimic changes over the

historical period

• For each scenario calculate the change in value of

the portfolio over the specified time horizon

• From this empirical distribution of value changes

calculate VaR

Model Building Approach

• Portfolio of n-assets

• Calculate mean and standard deviation of change in

the value of portfolio for one day

• Assume normality

• Calculate VaR

Monte Carlo Simulation

• Value of the portfolio today

• Draw samples from the probability distribution of

changes of the market variables

• Using the sampled changes calculate the new portfolio

value and its change

• From the simulated probability distribution of changes

in portfolio value calculate VaR

Pitfalls of Normal Distribution Based VaR

• Normality assumption may not be valid for tail part of the

distribution

• VaR of a portfolio is not less than weighted sum of VaR

of individual assets (not sub-additive)

• Expected shortfall conditional on the fact that loss is

more than VaR is a sub-additive measure of risk

Pitfalls of Value-at-Risk

• VaR is a statistical measurement of price risk

• VaR assumes a static portfolio. It does not take into

account

– Structural change in the portfolio that would

contractually occur during the period

– Dynamic hedging of the portfolio

• VaR calculation has two basic components

– Simulation of changes in market rates

– Calculation of resultant changes in the portfolio value

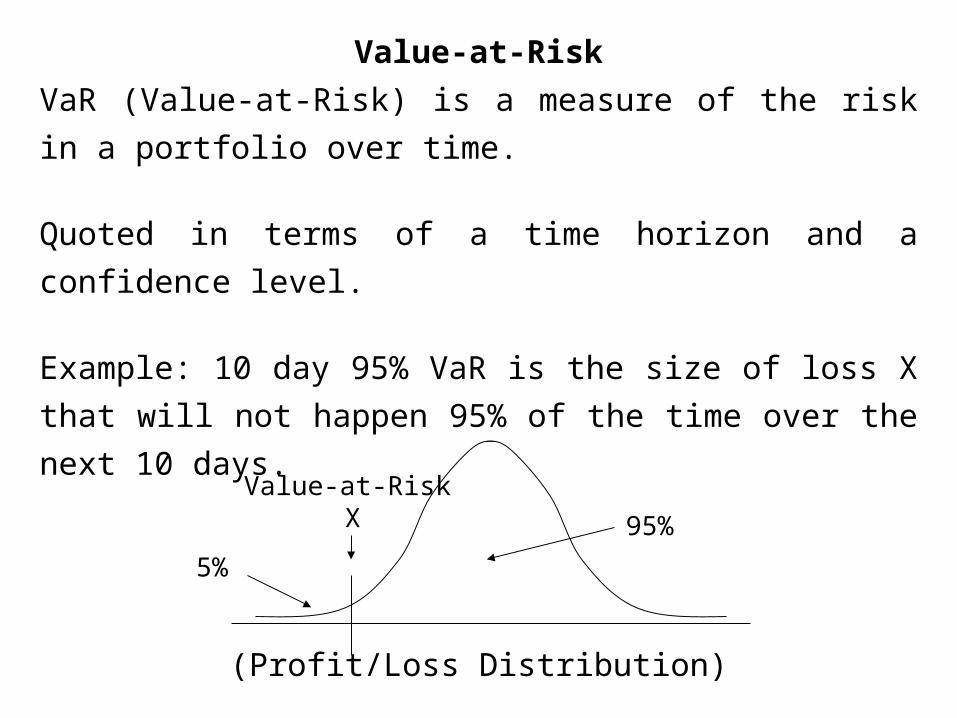

Value-at-Risk

VaR (Value-at-Risk) is a measure of the risk in a portfolio over

time.

Quoted in terms of a time horizon and a confidence level.

Example: 10 day 95% VaR is the size of loss X that will not

happen 95% of the time over the next 10 days.

(Profit/Loss Distribution)

5%

95%XValue-at-Risk

Value-at-Risk Levels

Two standard VaR levels are 95% and 99%.

95% is 1.645 standard deviations from the mean

99% is 2.33 standard deviations from the mean

mean

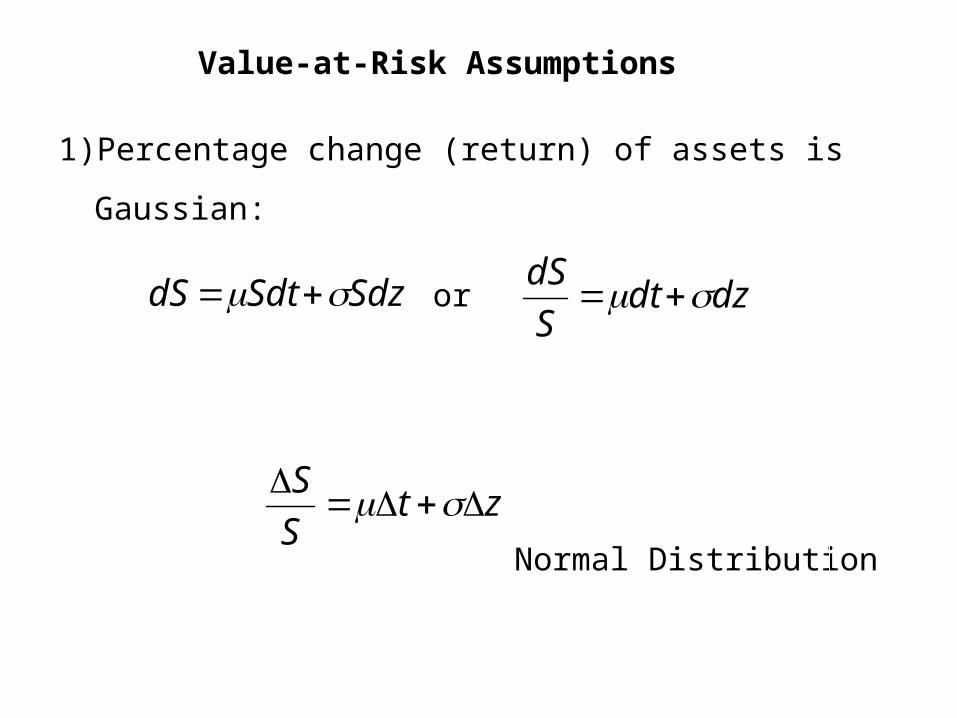

Value-at-Risk Assumptions

1) Percentage change (return) of assets is Gaussian:

SdzSdtdS dzdtS

dS or

ztS

S

Normal Distribution

Value-at-Risk Assumptions

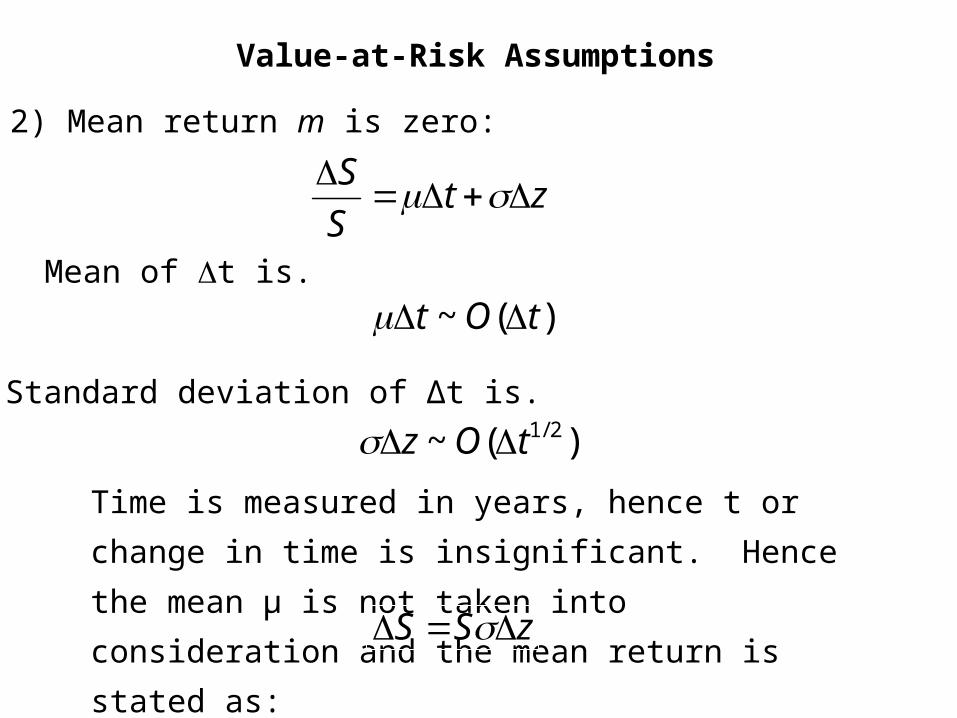

2) Mean return m is zero:

ztS

S

Mean of t is.

)(~ tOt

Standard deviation of ∆t is.

)(~ 2/1tOz Time is measured in years, hence t or change in

time is insignificant. Hence the mean μ is not taken

into consideration and the mean return is stated as: zSS

VaR and Regulatory Capital

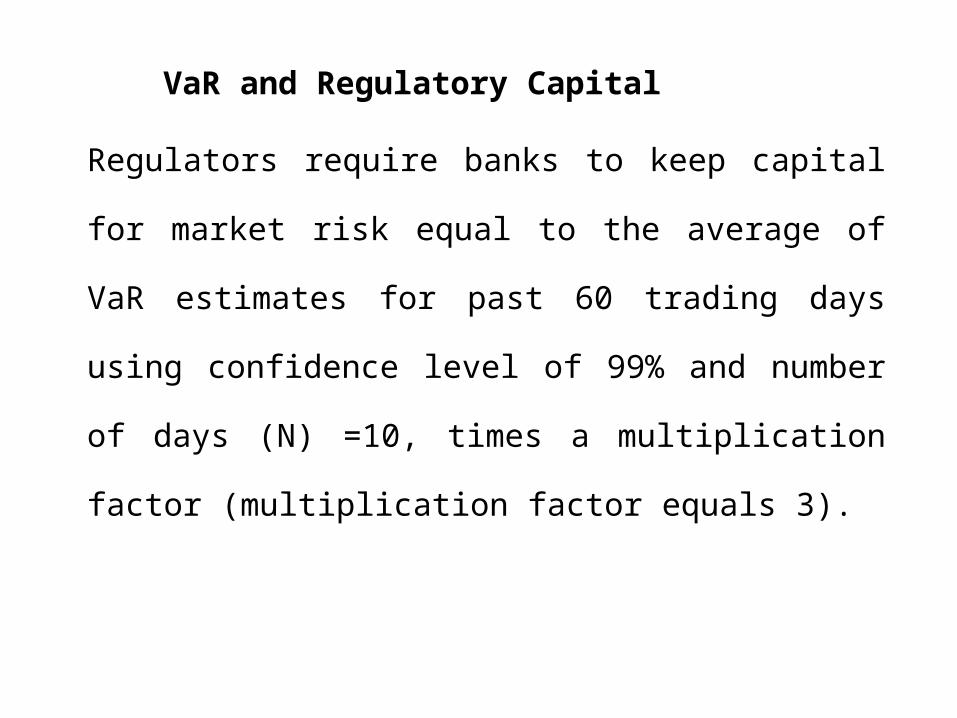

Regulators require banks to keep capital for market risk

equal to the average of VaR estimates for past 60

trading days using confidence level of 99% and number

of days (N) =10, times a multiplication factor

(multiplication factor equals 3).

Advantages of VaR

• Captures an important aspect of risk in a single number

• Easy to understand

• Indicates the worst loss that could happen

Daily Volatilities

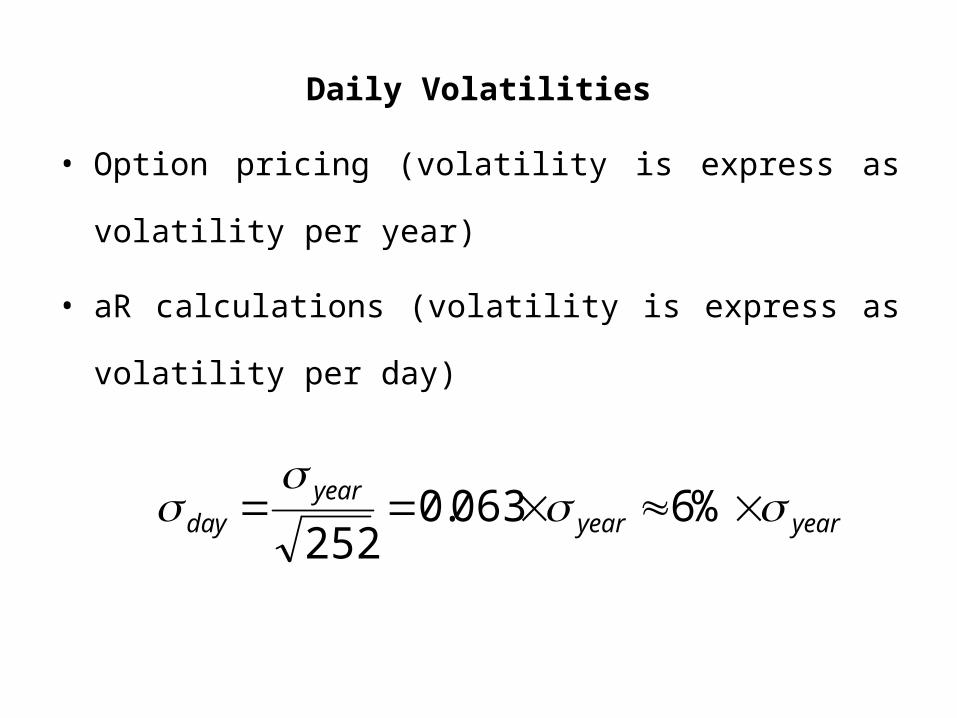

• Option pricing (volatility is express as volatility per year)

• aR calculations (volatility is express as volatility per day)

yearyearyear

day

%6063.0252

Daily Volatility

• day is defined as the standard deviation of the

continuously compounded return in one day

• In practice it is also assumed that it is the standard

deviation of the proportional change in one day

Example

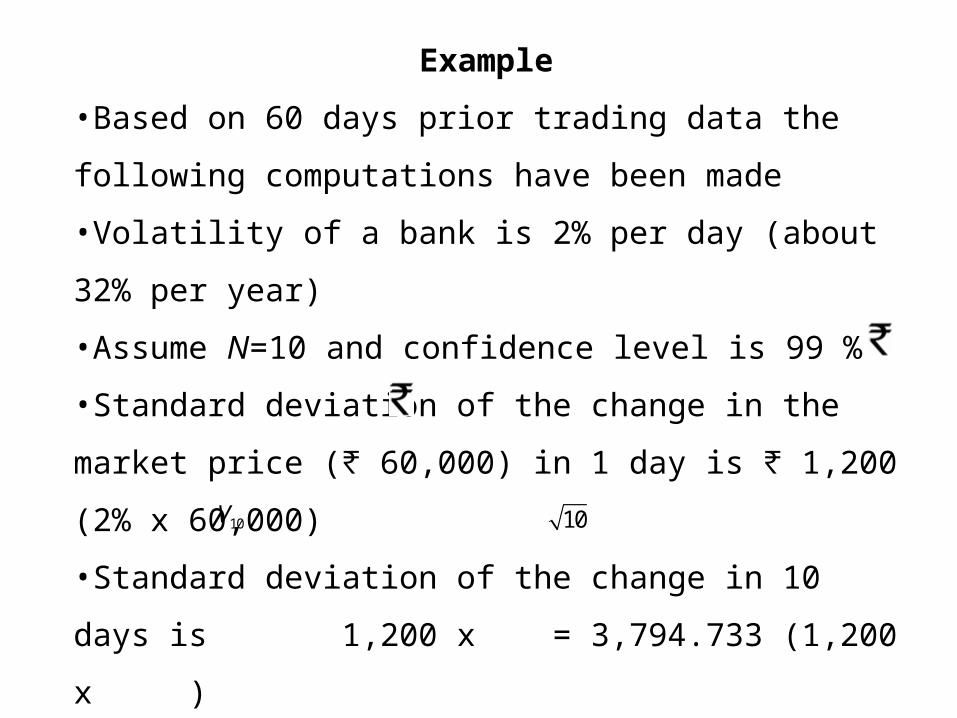

•Based on 60 days prior trading data the following

computations have been made

•Volatility of a bank is 2% per day (about 32% per year)

•Assume N=10 and confidence level is 99 %

•Standard deviation of the change in the market price ( ₹

60,000) in 1 day is 1,200 (2% x 60,000)₹

•Standard deviation of the change in 10 days is 1,200

x = 3,794.733 (1,200 x )

10V 10

Example (continued)

• Assume that the expected change in the value of the

bank’s share is zero

• Assume that the change in the value of the bank’s share

is normally distributed

• Since N(0.01)= -2.33, ({Z<-2.33}=0.01)

the VaR is

2.33 x 3,794.733 = 8,846.728.₹

Example (continued)

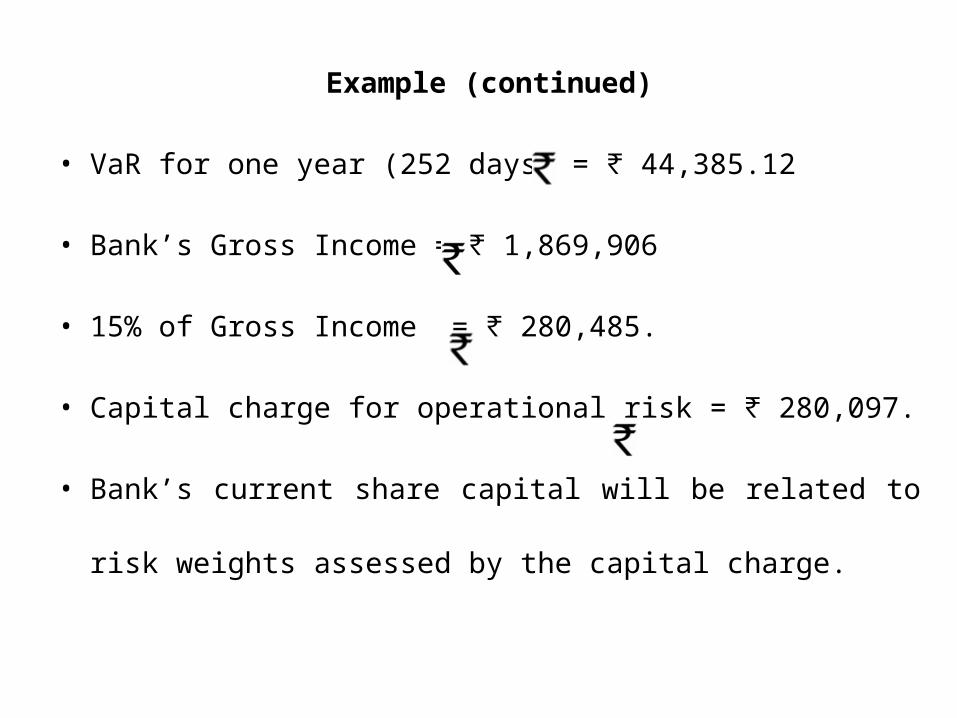

• VaR for one year (252 days) = 44,385.12₹

• Bank’s Gross Income = 1,869,906 ₹

• 15% of Gross Income = 280,485.₹

• Capital charge for operational risk = 280,097.₹

• Bank’s current share capital will be related to risk weights

assessed by the capital charge.

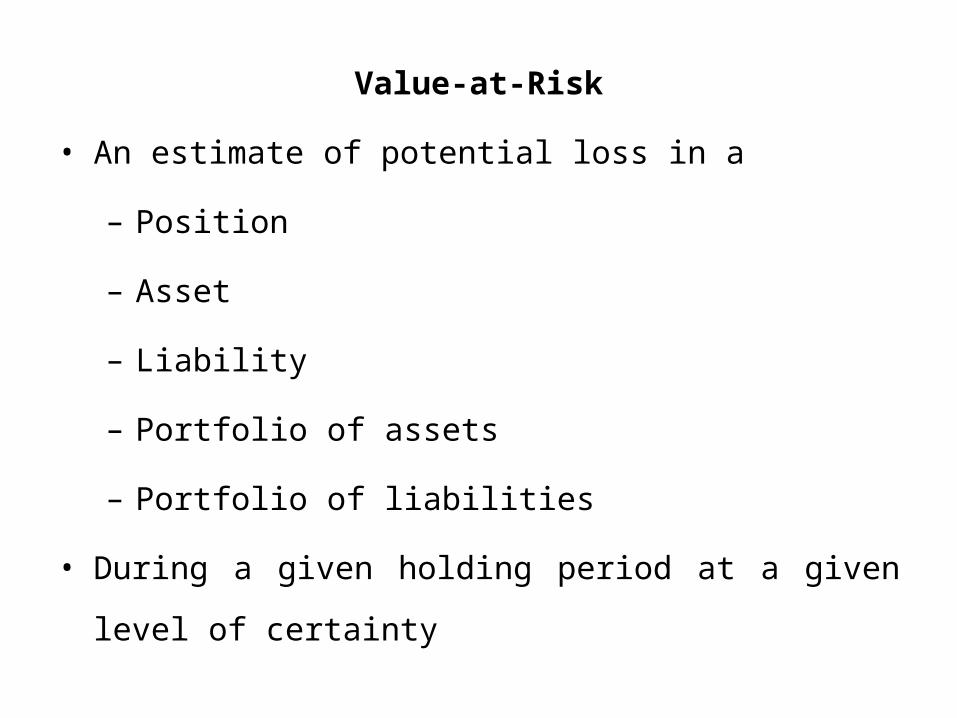

Value-at-Risk

• An estimate of potential loss in a

– Position

– Asset

– Liability

– Portfolio of assets

– Portfolio of liabilities

• During a given holding period at a given level of certainty

Value-at-Risk

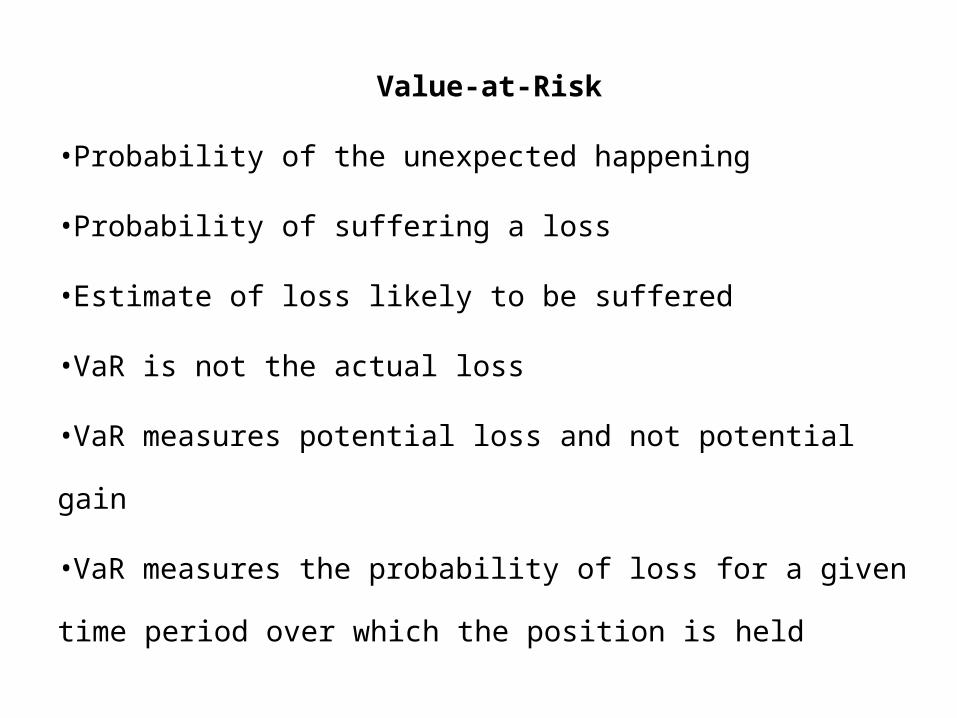

•Probability of the unexpected happening

•Probability of suffering a loss

•Estimate of loss likely to be suffered

•VaR is not the actual loss

•VaR measures potential loss and not potential gain

•VaR measures the probability of loss for a given time period

over which the position is held

Bank for International Settlement (BIS)

• VaR is a measurement of market risk

• Provision of capital adequacy for market risk, subject to

approval by banks' supervisory authorities

• Computation of VaR changes based on the estimated

time period

– One day

– One week

– One month

– One year

Bank for International Settlement (BIS)

•Holding period for an instrument will depend on liquidity of

the instrument

•Varying degrees of certainty changes potential loss

•VaR estimates that the loss will not exceed a certain

amount

•VaR will change with different levels of certainty

VaR Methodology

• Computed as the expected loss on a position from an

adverse movement in identified market risk parameter(s)

• Specified probability over a nominated period of time

• Volatility in financial markets is calculated as the

standard deviation of the percentage changes in the

relevant asset price over a specified asset period

• Volatility for calculation of VaR is specified as the

standard deviation of the percentage change in the risk

factor over the relevant risk horizon

VaR Computation Method

• Correlation Method

– Variance – covariance method

– Deterministic approach

– Change in value of the position computed by combining

the sensitivity of each component to price changes in

the underlying assets

VaR Computation Method

• Historical Simulation

– Change in the value of a position using the actual historical movements of the underlying assets

– Historical period has to be adequately long to capture all possible events and relationships between the various assets and within each asset class

– Dynamics of the risk factors captured since simulation follows every historical move

VaR Computation Method

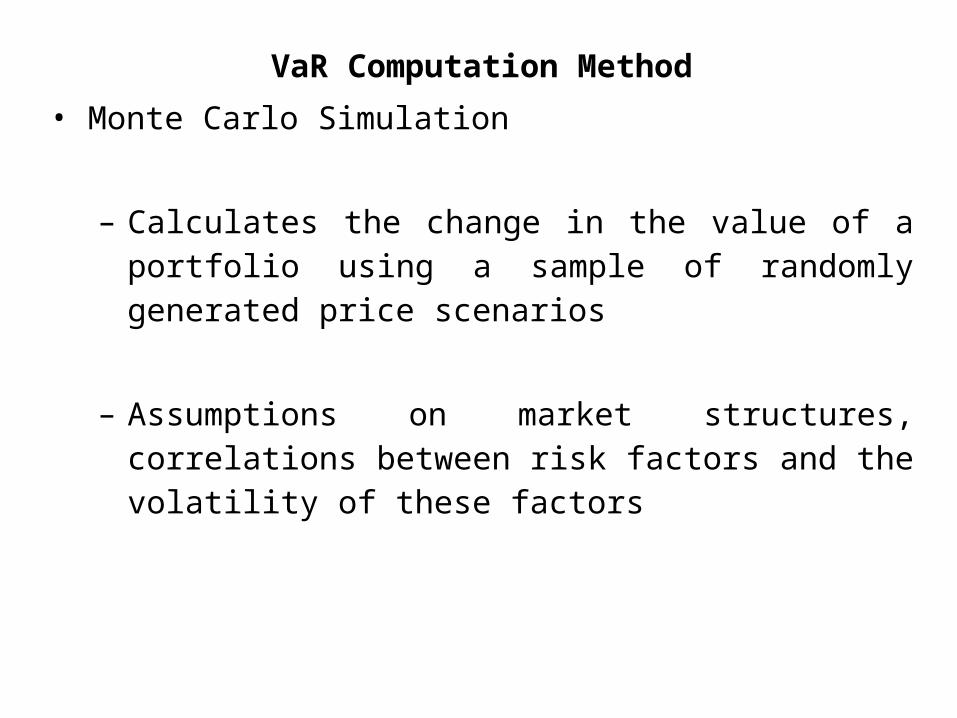

• Monte Carlo Simulation

– Calculates the change in the value of a portfolio using a sample of randomly generated price scenarios

– Assumptions on market structures, correlations between risk factors and the volatility of these factors

VaR Application

• Basic parameters

– Holding period

– Confidence interval

– Historical time period (observed asset prices)

• Closer the models fit economic reality, more accurate the

estimated

• There is no guarantee that the numbers returned by

each VaR method will be near each other

VaR Application

• VaR is used as a Management Information System (MIS)

tool in the trading portfolio

• Risk by levels

• Products

• Geography

• Level of organisation

• VaR is used to set risk limits

• VaR is used to decide the next business

VaR Limitation

• VaR does not substitute

– Management judgement

– Internal control

• VaR measures market risk

– Trading portfolio

– Investment portfolio

• VaR is helpful subject to the extent of

– Measurement parameters

Back Testing

• Backtests compare realized trading results with model

generated risk measures

• Evaluate a new model

• Reassess the accuracy of existing models

• Banks using internal VaR models for market risk capital

requirements must backtest their models on a regular

basis

Back Testing

• Banks back test risk models on a monthly or quarterly

basis to verify accuracy

• Observe whether trading results fall within pre-specified

confidence bands as predicted by the VaR models

• If the models perform poorly establish cause for poor

performance

– Check integrity of position

– Check market data

– Check model parameters

– Check methodology

Stress Testing

• Banks gauge their potential vulnerability to exceptional,

but plausible, events

• Stress testing addresses the large moves in key market

variables that lie beyond day to day risk monitoring but

that could potentially occur

Stress Testing

• Process of stress testing involves

– Identifying potential movements

– Market variables to stress

– How much to stress them

– What time frame to run the stress analysis

– Shocks are applied to the portfolio

• Revaluing the portfolios

– Effect of a particular market movement on the value of

the portfolio

– Profit and Loss

– Effects of different shocks of different magnitudes

Stress Testing Technique

• Scenario analysis

• Evaluating the portfolios

– under various expectations

– evaluating the impact

• changing evaluation models

• volatilities and correlations

• Scenarios requiring no simulations

– analyzing large past losses

Stress Testing Technique

• Scenarios requiring simulations

– Running simulations of the current portfolio subject to

large historical shocks

• Bank specific scenario

– Driven by the current position of the bank rather than

historical simulation

• Subjective than VaR

• Identify undetected weakness in the bank's portfolio

Efficiency of a Stress Test

• Relevant to the current market position

• Consider changes in all relevant market rates

• Examine potential regime shifts (whether the current risk

parameters will hold or break down)

• Consider market illiquidity

• Consider the interrelationship between market and credit

risk

Application of Stress Tests

• Stress tests produce information summarising the bank’s

exposure to extreme but possible circumstances

• Role of risk managers in the bank is gathering and

summarising information to enable senior management

to understand the strategic relationship between the

bank’s risk taking

– Extent and character of financial leverage employed

– Risk appetite

– Stress scenarios created on a regular basis

– Stress scenarios monitored over time

Application of Stress Tests

•Influence decision-making

•Manage funding risk

•Provide a check on modelling assumptions

•Set limits for traders

•Determine capital charges on trading desks’ positions

Limitations of Stress Test

• Stress tests are often neither transparent nor

straightforward

• Depends on a large number of practitioner choices

• Choice of risk factors to stress

• Methods of combining factors stressed

• Range of values considered

Limitations of Stress Test

•Time frame to analyse

•Risk manager is faced with the considerable tasks of

analyzing the results and identifying implications

•Stress test results interpretation for the bank is based on

qualitative criteria

•Manage bank’s risk-taking activities is subject to

interpretations

Related Documents