McGraw-Hill Ryerson© 15 15 Bonds & SF 15 - 1 McGraw-Hill Ryerson© Chapter 15

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

McGraw-Hill Ryerson©

1515 1515Bonds

& SF

Bonds

& SF

15 - 1

McGraw-Hill Ryerson©

Chapter 15Chapter 15

McGraw-Hill Ryerson©

1515 1515Bonds

& SF

Bonds

& SF

15 - 2

Calculate

… the market price of a bond on any date

After completing this chapter, you will be able to:

… the yield to maturity of a bond on any interest payment date

Learning ObjectivesLearning Objectives

LO 1.LO 1.

LO 2.LO 2.

McGraw-Hill Ryerson©

1515 1515Bonds

& SF

Bonds

& SF

15 - 3

… fixed Income investments

McGraw-Hill Ryerson©

1515 1515Bonds

& SF

Bonds

& SF

15 - 4

Face Value (or denomination)… the principal amount that the issuer is

required to pay to the bond holder on the maturity date

Coupon… interest rate paid on face value… rate normally fixed for life of bond… paid semiannually

Basic Concepts & Definitions of

Main CharacteristicsMain Characteristics

McGraw-Hill Ryerson©

1515 1515Bonds

& SF

Bonds

& SF

15 - 5

Basic Concepts & Definitions of

… are fixed Income investments i.e. they have a fixed interest rate or coupon payable on the principal amount

Main CharacteristicsMain Characteristics

… the issue date is the date on which the loan was made and on which interest starts to accrue

… a bond is basically a loan used to raise funds for the organization or institution, e.g. CSB’s, Municipalities…

… borrower is required to make periodic payments of interest only

McGraw-Hill Ryerson©

1515 1515Bonds

& SF

Bonds

& SF

15 - 6

Basic Concepts & Definitions of

Main CharacteristicsMain Characteristics

… on the maturity date of the bond,

the full principal amount is repaid along with the final interest payment

… issued with maturities ranging from 2 to 30 years

McGraw-Hill Ryerson©

1515 1515Bonds

& SF

Bonds

& SF

15 - 7

Do Canada Savings Bonds have exactly the

same characteristics as Marketable Bonds?Canada Savings

Bonds

Canada Savings Bonds

Marketable Bonds

Marketable Bonds

You can cash in a CSB before its scheduled maturity date and

receive the full face value

plus accrued interest

You can cash in a CSB before its scheduled maturity date and

receive the full face value

plus accrued interest

You cannot do this with a M B

You cannot do this with a M B

If you want to cash in before it matures, you must do this through an investment

dealer in the “bond market”

If you want to cash in before it matures, you must do this through an investment

dealer in the “bond market”

McGraw-Hill Ryerson©

1515 1515Bonds

& SF

Bonds

& SF

15 - 8

If the market rate falls below the coupon rate, the bond’s price rises above its face value

If the market rate falls below the coupon rate, the bond’s price rises above its face value

If the market rate rises above the coupon rate, the bond’s price falls below its face value

If the market rate rises above the coupon rate, the bond’s price falls below its face value

Market Rate

Market Rate

CouponRate

CouponRate

Bond Price

Bond Price

Face Value

Face Value

Market Rate

Market Rate

CouponRate

CouponRate

Bond Price

Bond Price

Face Value

Face Value

Effects of Interest Rate Changes on Bond Prices

Effects of Interest Rate Changes on Bond Prices

McGraw-Hill Ryerson©

1515 1515Bonds

& SF

Bonds

& SF

15 - 9

2b = coupon rate (compounded semiannually)

FV = Face Value of the bond

2b = coupon rate (compounded semiannually)

FV = Face Value of the bond

Effects of Interest Rate Changes on Bond Prices

Effects of Interest Rate Changes on Bond Prices

Fair Market Value of a Bond

Present Value of the Interest Payments

Present Value of the Face Value

Formula Formula Bond Price = b(FV)1 – (1 + i)- n

i+ FV(1 + i)- n

ExampleExample

McGraw-Hill Ryerson©

1515 1515Bonds

& SF

Bonds

& SF

15 - 10

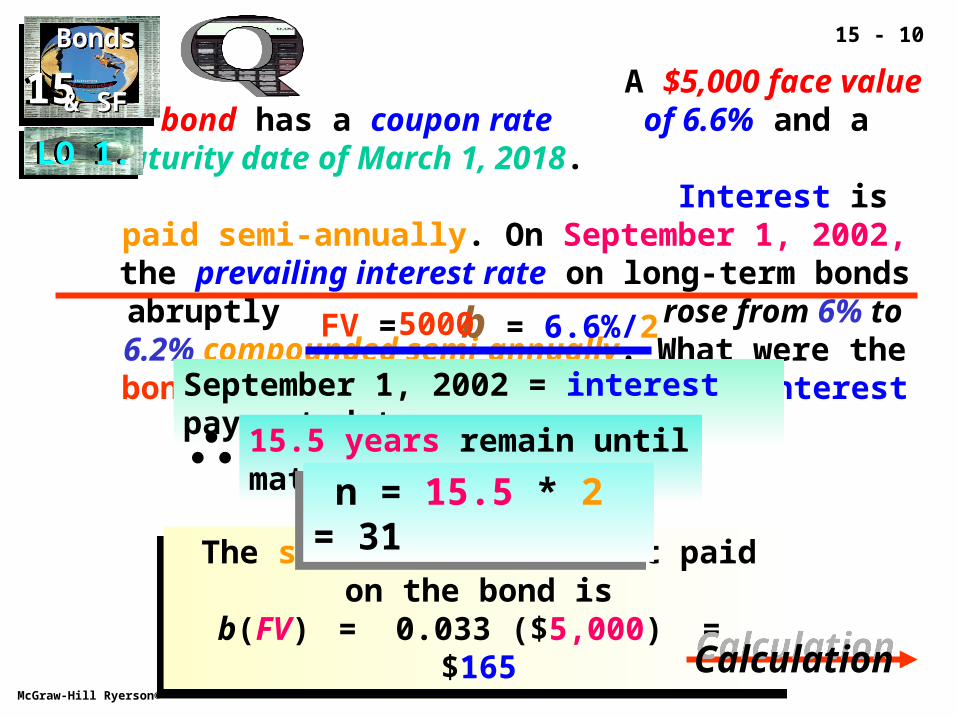

A $5,000 face value bond has a coupon rate of 6.6% and a maturity date of March 1, 2018. Interest is paid semi-annually. On September 1, 2002, the prevailing interest rate on long-term bonds abruptly rose from 6% to 6.2% compounded semi-annually.

What were the bond's prices before and after the interest rate change?

The semi-annual interest paid on the bond isb(FV) = 0.033 ($5,000) = $165

The semi-annual interest paid on the bond isb(FV) = 0.033 ($5,000) = $165

FV = b = 6.6%/25000

September 1, 2002 = interest payment date

15.5 years remain until maturity

n = 15.5 * 2 = 31 n = 15.5 * 2 = 31

CalculationCalculation

LO 1.LO 1.

McGraw-Hill Ryerson©

1515 1515Bonds

& SF

Bonds

& SF

15 - 11

31

2 6 165

Calculate the bond price before the market rate increase.

5000

$5,300.01 is the bond price before the rate increase

$5,300.01 is the bond price before the rate increase

PV = -5300.01

A $5,000 face value bond has a coupon rate

of 6.6% and a maturity date of March

1, 2018. Interest is

paid semi-annually. On September 1, 2002, the prevailing interest rate

on long-term bonds abruptly rose from 6% to 6.2%

compounded semi-annually. What were

the bond's prices before and after the interest

rate change?

A $5,000 face value

bond has a coupon rate of 6.6% and a

maturity date of March 1, 2018.

Interest is paid semi-annually. On September 1, 2002, the prevailing interest rate

on long-term bonds abruptly rose from 6% to 6.2%

compounded semi-annually. What were

the bond's prices before and after the interest

rate change?

McGraw-Hill Ryerson©

1515 1515Bonds

& SF

Bonds

& SF

15 - 12

6.2

Calculate the bond price after the market rate increase.

$5,197.38 is the bond price after the rate

increase

$5,197.38 is the bond price after the rate

increase

PV = -5197.38

Bond price decreased by…

$5,300.01 – 5,197.38

= $128.51= $128.51

A $5,000 face value

bond has a coupon rate of 6.6% and a

maturity date of March 1, 2018.

Interest is paid semi-annually. On September 1, 2002, the prevailing interest rate

on long-term bonds abruptly rose from 6% to 6.2%

compounded semi-annually. What were

the bond's prices before and after the interest

rate change?

A $5,000 face value

bond has a coupon rate of 6.6% and a

maturity date of March 1, 2018.

Interest is paid semi-annually. On September 1, 2002, the prevailing interest rate

on long-term bonds abruptly rose from 6% to 6.2%

compounded semi-annually. What were

the bond's prices before and after the interest

rate change?

McGraw-Hill Ryerson©

1515 1515Bonds

& SF

Bonds

& SF

15 - 13

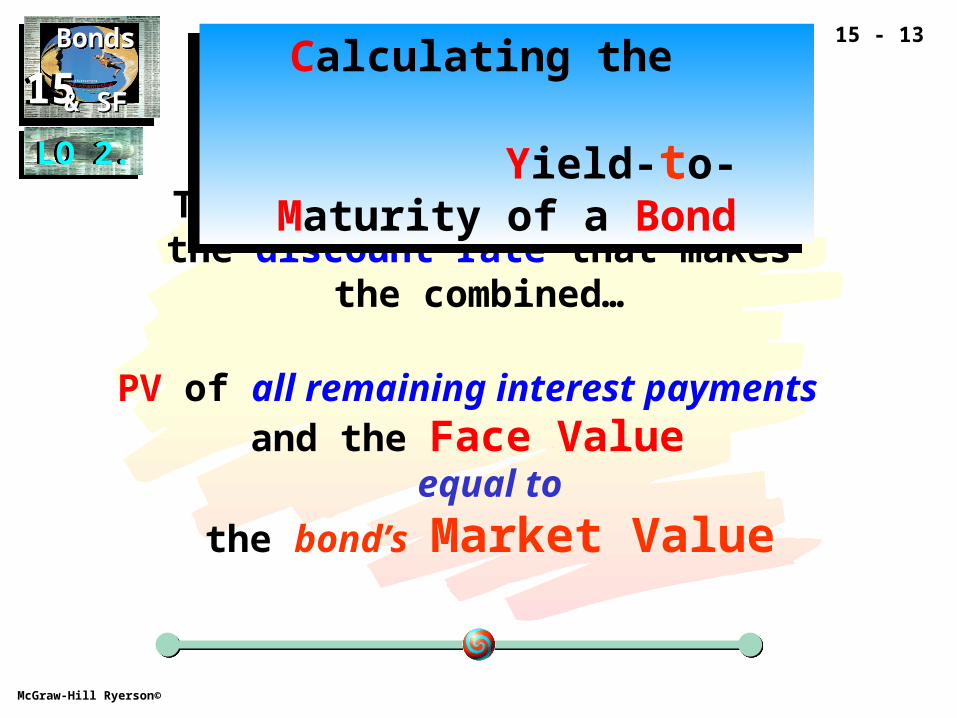

The bond’s yield-to-maturity is the discount rate that makes the

combined…

Calculating the Yield-to-Maturity of a

Bond

Calculating the Yield-to-Maturity of a

Bond

PV of all remaining interest payments and the Face Value

equal to

the bond’s Market Value

LO 2.LO 2.

McGraw-Hill Ryerson©

1515 1515Bonds

& SF

Bonds

& SF

15 - 14

Calculating the Yield-to-Maturity of a Bond

Calculating the Yield-to-Maturity of a Bond

A $1,000 face value Province of Manitoba bond, bearing interest at 5.8% payable semiannually, has 11 years

remaining until maturity. What is the bond’s yield to maturity (YTM) at its current market price of $972?

22922

1000972

P/Y = 2I/Y = 6.154

The bond’s YTM is 6.154% The bond’s YTM is 6.154%

PMT = 1000*5.8%/2

PMT = 1000*5.8%/2

McGraw-Hill Ryerson©

1515 1515Bonds

& SF

Bonds

& SF

15 - 15 Pricing a Bond

between Interest Payment Dates

Pricing a Bond between

Interest Payment Dates

A $1,000, 20 year, 6% coupon bond was issued on August 15, 2000. It was sold on Nov 3, 2002 to yield

the purchaser 6.5% compounded semiannually until maturity. At what price did the bond sell?

Calculate the PV of the remaining payments on the preceding interest

payment date.

Calculate the PV of the remaining payments on the preceding interest

payment date.

Calculate the FV of the Step 1 result on the date of sale.

Calculate the FV of the Step 1 result on the date of sale.

McGraw-Hill Ryerson©

1515 1515Bonds

& SF

Bonds

& SF

15 - 16

Pricing a Bond between Interest Payment Dates

Pricing a Bond between Interest Payment Dates

A $1,000, 20 year, 6% coupon bond was issued on August 15, 2000. It was sold on Nov 3, 2002 to yield the purchaser 6.5% compounded semiannually until

maturity. At what price did the bond sell?

23036

10006.5

P/Y = 2P/V = -947.40

On August 15, 2002, the bond’s value is $947.40

On August 15, 2002, the bond’s value is $947.40

Most recent

interest payment date is

August 15, 2002

Most recent

interest payment date is

August 15, 2002

PMT = 1000*6.0%/2

PMT = 1000*6.0%/2

McGraw-Hill Ryerson©

1515 1515Bonds

& SF

Bonds

& SF

15 - 17

Pricing a Bond between Interest Payment Dates

Pricing a Bond between Interest Payment Dates

P/Y = 2P/V = -947.40

Calculate the FV of $947.40 on Nov.3, 2002

We need to find: a) # of days between interest payment dates, and

b) # of days from Aug.15 to Nov.3

We need to find: a) # of days between interest payment dates, and

b) # of days from Aug.15 to Nov.3

A $1,000, 20 year, 6% coupon bond was issued on August 15, 2000. It was sold on Nov 3, 2002 to yield the purchaser 6.5% compounded semiannually until

maturity. At what price did the bond sell?

McGraw-Hill Ryerson©

1515 1515Bonds

& SF

Bonds

& SF

15 - 18

11.0302

Using… Texas Instruments BAII PLUS

i

Days Between DatesDays Between Dates

2nd

Enter

Date

CPT

Enter

08.1502

Calculate… the time from Aug.

15th to Nov. 3rd

DBD = 80

… the time from

Aug. 15th,2002 to Feb. 15th,2003

DBD = 184

02.1503

2nd

Date

CPT

Enter

McGraw-Hill Ryerson©

1515 1515Bonds

& SF

Bonds

& SF

15 - 19

Pricing a Bond between Interest Payment Dates

Pricing a Bond between Interest Payment Dates

0.4348

947.40

P/Y = 2 .4348

The bond sold for $960.67 on Nov.3, 2002The bond sold for $960.67 on Nov.3, 2002

N = 80/184 N = 80/184FV= 960.67

A $1,000, 20 year, 6% coupon bond was issued on August 15, 2000. It was sold on Nov 3, 2002 to yield the purchaser 6.5% compounded semiannually until

maturity. At what price did the bond sell?

McGraw-Hill Ryerson©

1515 1515Bonds

& SF

Bonds

& SF

15 - 20

http://www.finpipe.com/fixed.htm

This site provides complete details on how bonds function. Just click on the areas that the site provides for information.

This site provides complete details on how bonds function. Just click on the areas that the site provides for information.

Click here:Click here:

McGraw-Hill Ryerson©

1515 1515Bonds

& SF

Bonds

& SF

15 - 21

This completes Chapter 15This completes Chapter 15

Related Documents