INTERNATIONAL CORPORATE GOVERNANCE Stephen Ong, BSc(Hons) Econs (LSE), MBA International Business(Bradford) Visiting Fellow, Birmingham City University Visiting Professor, Shenzhen University MBA1034 GOVERNANCE, LAW & ETHICS

Mba1034 cg law ethics week 3 international corporate governance

Jul 15, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

INTERNATIONAL CORPORATE GOVERNANCE

Stephen Ong, BSc(Hons) Econs (LSE),

MBA International Business(Bradford)

Visiting Fellow, Birmingham City University

Visiting Professor, Shenzhen University

MBA1034 GOVERNANCE, LAW & ETHICS

• Discussion : Maximizing shareholder-value1

• Corporate Control, Ownership Rights & Governance Systems

2

• Case study : AIG3

Today’s Overview

1. Open Discussion : Maximizing Shareholder Value

Brendan McSweeney, (2008),"Maximizing shareholder-value: A panacea for economic growth or a recipe for economic and social disintegration?", Critical Perspectives on International Business, Vol. 4 No.1: pp. 55 – 74

1. Open Discussion : Maximizing Shareholder Value

1. Higher Profits by Cutting costs?

2. Dividend policies

3. Share price reflects firm performance

4. Financing methods

2.1 Corporate Control Across the World

1.Reviews the differences in corporate

control patterns across the world.

2.Corporate control and ownership in the

UK and USA differ markedly from

corporate control and ownership in the

rest of the world - widely held shares vs

concentrated shareholding.

3.Differences in the concentration of

control and types of shareholders.

Learning Outcomes

• By the end of this lecture, you should be able to:1.Describe the differences in the levels corporate

control across the world

2.Be aware of differences in the importance of various types of shareholders across regions and countries

3.Explain why the Berle-Means hypothesis does not hold outside the UK and the USA.

Introduction

• The previous lecture mentioned that the principal–agent model has only limited applicability.

• The model is based on the Berle-Means premise of a separation of ownership and control in stock-exchange listed firms.

• However, this premise is only valid in the UK and the USA.

• In most the rest of the world, listed corporations tend to have large shareholders.

Introduction (Continued)

• In what follows, we focus on control rather than ownership for two reasons

1. Corporate governance is about the distribution of power within the corporation and this power depends, among other factors, on the votes held by various shareholders

2. In most countries, there are disclosure requirements for the ownership of control rights, but not for cash flow rights.

The Evolution of Control after the IPO

• Berle and Means hypothesis states that, as companies grow, they experience a separation of ownership and control.

• It is this separation which creates conflicts of interests between the managers and the owners (the shareholders).

• A first step towards testing the validity of this hypothesis is to focus on what happens around the initial public offering (IPO).

The Evolution of Control after the IPO (Continued)

• The IPO consists of the firm– obtaining a listing on a recognised stock

exchange, and

– offering its shares to the public for the first time.

• Comparison of the evolution of control in German and UK IPOs matched by – size (market capitalisation), and

– initial control (family control)

over the six years after the IPO. (Goergen1998)

• Definition of a large shareholder was a shareholder with at least 25% of the votes.

• Distinction between

– the pre-IPO or initial shareholder, and

–new large shareholders.

• The remainder was treated as the free float.

The Evolution of Control after the IPO

(Continued)

German firms UK firms

Time after

IPO (years)

Initial

share-

holder

s

(%)

Free float

(%)

New large

share-

holders

(%)

Initial

share-

holders

(%)

Free float

(%)

New

large

share-

holders

(%)

Immediatel

y

76.4 22.2 1.5 62.8 37.2 0.1

1 73.7 24.0 2.4 51.4 43.1 5.5

2 69.6 25.0 5.4 47.3 39.5 13.3

3 64.9 25.3 9.8 37.7 36.0 26.4

4 59.4 25.0 15.5 33.6 37.6 28.8

5 50.7 26.3 23.1 31.4 36.5 32.1

6 45.0 24.8 30.2 30.0 40.8 29.2

Goergen (1998), Goergen and Renneboog (2003)

Table 1 – Evolution of control in German and UK IPOs

• The evolution of control is different in the two countries– Initial shareholders of German IPOs keep

majority control for 5 years after IPO

– Initial shareholders of UK IPOs lose control 2years after IPO

– Free float is higher in UK IPOs

– No difference in terms of control held by new shareholders.

The Evolution of Control after the IPO

(Continued)

• There is no separation of ownership and control in Germany.

• German firms also tend to go public later (about 50 years after their foundation) than UK firms (about 13 years).

The Evolution of Control after the IPO

(Continued)

Corporate Control in Western Europe and the USA

• The first detailed study on Europe was conducted by the European Corporate Governance Network (ECGN), the predecessor of the European Corporate Governance Institute (ECGI).

• The study was commissioned by the Directorate General for Industry of the European Commission.

• The study was published in Barca, F. and M. Becht (2001), The Control of Corporate Europe, Oxford: Oxford University Press.

Corporate Control in Western Europe and the USA (Continued)

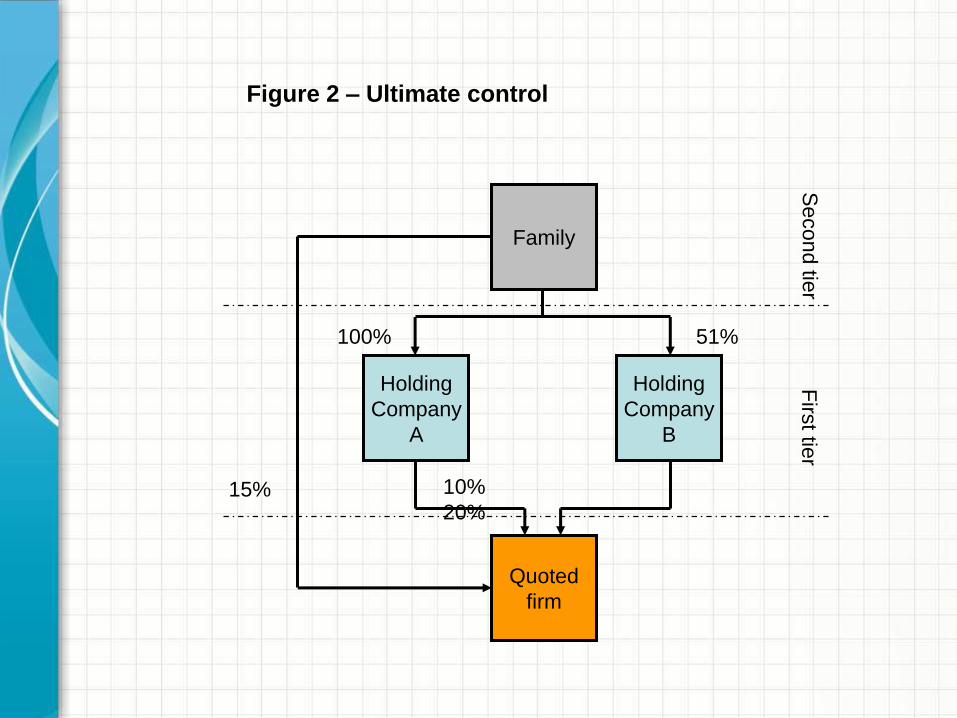

• This study focuses on ultimate control– Control refers to the ownership of voting rights

– Control may be held indirectly.

• There are various ways of defining control including– a majority of votes as a majority is required for most

decisions voted at the AGM,

– a supermajority as some decisions require 75% of the votes (e.g. the approval of a takeover offer), and

– a blocking minority of 25% which is sufficient to block decisions requiring a supermajority.

Figure 1 – Direct or first-tier control

Family

Holding

Company

A

Holding

Company

B

Quoted

firm

15% 10% 20%

Firs

t tier

Second tie

r

?

Figure 2 – Ultimate control

Family

Holding

Company

A

Holding

Company

B

Quoted

firm

100% 51%

15% 10%

20%

Firs

t tier

Second tie

r

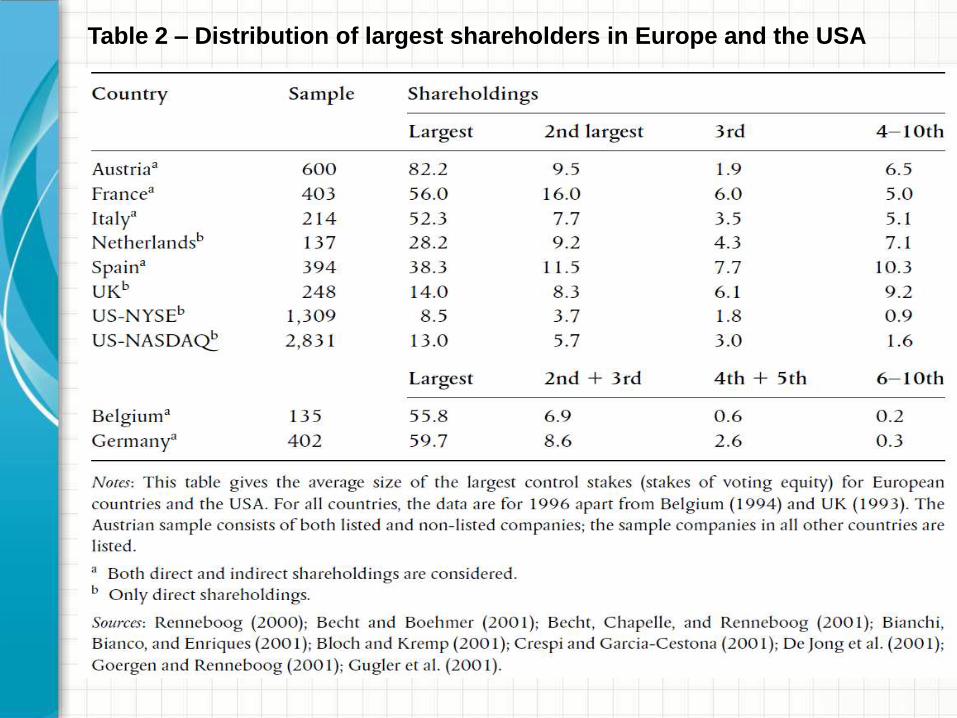

Table 2 – Distribution of largest shareholders in Europe and the USA

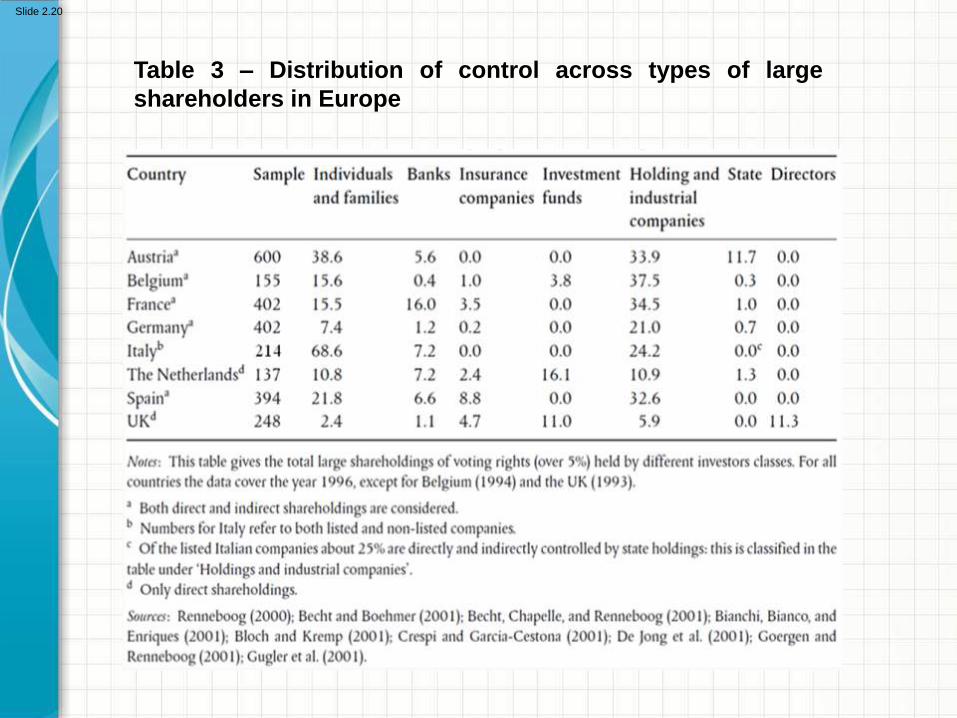

Table 3 – Distribution of control across types of large

shareholders in Europe

Slide 2.20

• Levels of control– Continental WesternEurope:

• In most firms a majority of votes is held by one shareholder or a group

• Most firms have a shareholder with a blocking minority• Potential agency problems between minority shareholders and

large shareholder

– UK and US• Most firms are widely held• A coalition of the 3 largest shareholders votes for only 30%• Potential agency problems between shareholders and

management

Corporate Control in Western Europe and

the USA (Continued)

• Nature of control

– Industrial and holding firms are the major shareholders in most of Continental Europe

– Institutional shareholders are main shareholders in the UK and Netherlands

– Family control is important in Continental Europe

– Control by the management is important in the UK.

Corporate Control in Western Europe and

the USA (Continued)

– Bank stakes are small:• They range from 0.4 to 7.2% in most of Continental

Europe

• The exception is France with 16%

• However, figures may underestimate control by banks

– In some countries, customers deposit their shares with the bank and the bank votes for the shares

– Figures exclude proxy votes

– Proxy votes are the votes from the shares held by the banks’ customers that the banks exercise on behalf of their customers.

Corporate Control in Western Europe and

the USA (Continued)

Corporate Control in Asia

• Asia has its own corporate governance characteristics.

• In Japan, some firms are part of keiretsus.

• A keiretsu is a group of industrial companies with close ties to a single banks which acts as the principal lender to the group.

• The bank is also a shareholder of the group’s companies and there may be cross-shareholdings between the group companies.

Corporate Control in Asia (Continued)

• The keiretsus originated from the pre-WWII zaibatsus.

• Zaibatsus were groups of industrial companies or conglomerates – controlled by families via a holding firm at the top of

the group, and– with a bank as one of the group companies providing

the financing.

• An example of a keiretsu originating from a zaibatsu is the Mitsubishi group of companies.

• Korea’s industrial landscape is dominated by chaebols.

• A chaebol is a group of industrial companies controlled by a family.

• Examples of famous chaebols are Hyundai, LG and Samsung.

• China started an ambitious programme of economic reforms in the 1980s giving managers of state-owned enterprises (SOEs) more power.

Corporate Control in Asia (Continued)

• In the early 1990s, China set up the Shenzen and Shanghai stock exchanges.

• From now on Chinese SOEs were allowed to issue shares to individual investors.

• Chinese SOEs have complex ownership and control structures.

Corporate Control in Asia (Continued)

• They tend to have 5 major types of shareholders– the central government,– legal persons (institutions and founders),– employees,– domestic investors (A shares), and– foreign investors (B and H shares).

• The largest shareholder holds about 43% of the shares.

• The government is the largest shareholder in 67% of the firms.

Corporate Control in Asia (Continued)

• India is dominated by conglomerates or so called business groups.

• About 60% of the 500 largest firms on the Bombay Stock Exchange are part of business groups.

• These are typically controlled by families.

• Control and ownership structures are highly complex and opaque with ownership pyramids and cross-holdings.

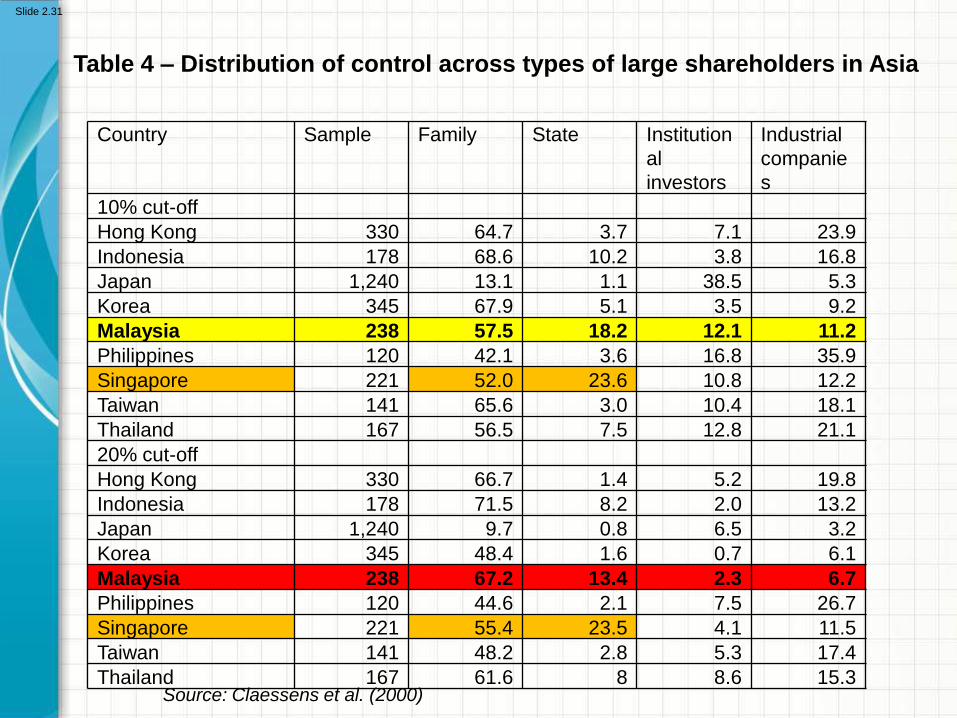

Corporate Control in Asia (Continued)

Figure 6 – Percentage of listed Asian firms with

a 10% shareholder

Source: Claessens et al.

(2000)

Slide 2.30

Country Sample Family State Institution

al

investors

Industrial

companie

s

10% cut-off

Hong Kong 330 64.7 3.7 7.1 23.9

Indonesia 178 68.6 10.2 3.8 16.8

Japan 1,240 13.1 1.1 38.5 5.3

Korea 345 67.9 5.1 3.5 9.2

Malaysia 238 57.5 18.2 12.1 11.2

Philippines 120 42.1 3.6 16.8 35.9

Singapore 221 52.0 23.6 10.8 12.2

Taiwan 141 65.6 3.0 10.4 18.1

Thailand 167 56.5 7.5 12.8 21.1

20% cut-off

Hong Kong 330 66.7 1.4 5.2 19.8

Indonesia 178 71.5 8.2 2.0 13.2

Japan 1,240 9.7 0.8 6.5 3.2

Korea 345 48.4 1.6 0.7 6.1

Malaysia 238 67.2 13.4 2.3 6.7

Philippines 120 44.6 2.1 7.5 26.7

Singapore 221 55.4 23.5 4.1 11.5

Taiwan 141 48.2 2.8 5.3 17.4

Thailand 167 61.6 8 8.6 15.3

Table 4 – Distribution of control across types of large shareholders in Asia

Source: Claessens et al. (2000)

Slide 2.31

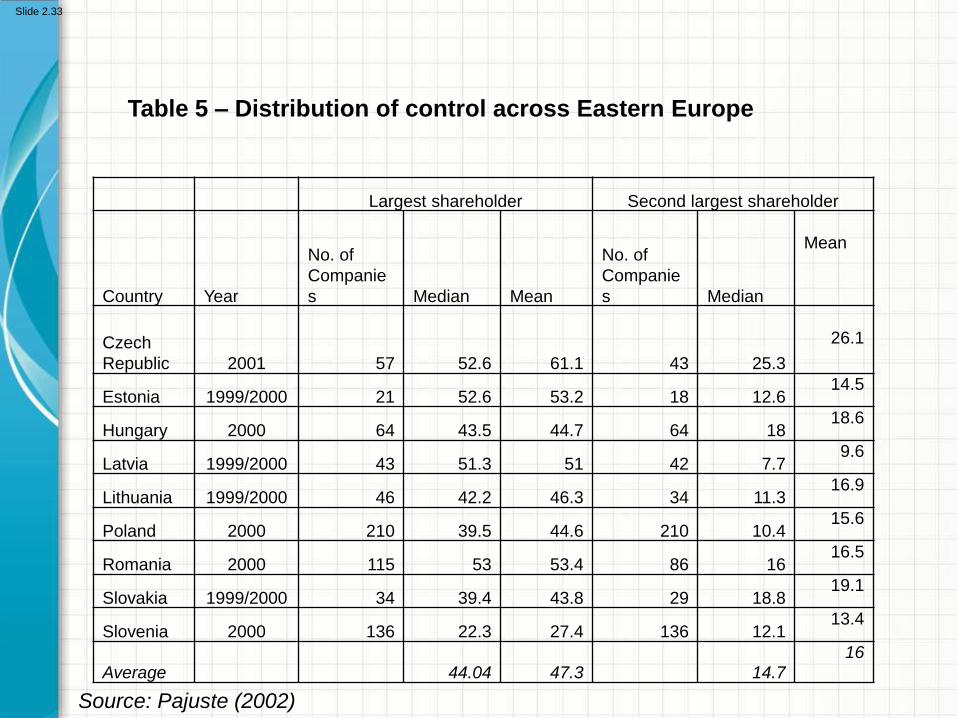

Corporate Control in Transitional Economies

• The former Communist Bloc started its transition to a market economy in the early 1990s.

• Albeit slightly lower than in Western Europe, control is also concentrated.

• However, the votes held by the second largest shareholder can be substantial.

Largest shareholder Second largest shareholder

Country Year

No. of

Companie

s Median Mean

No. of

Companie

s Median

Mean

Czech

Republic 2001 57 52.6 61.1 43 25.3

26.1

Estonia 1999/2000 21 52.6 53.2 18 12.614.5

Hungary 2000 64 43.5 44.7 64 1818.6

Latvia 1999/2000 43 51.3 51 42 7.79.6

Lithuania 1999/2000 46 42.2 46.3 34 11.316.9

Poland 2000 210 39.5 44.6 210 10.415.6

Romania 2000 115 53 53.4 86 1616.5

Slovakia 1999/2000 34 39.4 43.8 29 18.819.1

Slovenia 2000 136 22.3 27.4 136 12.113.4

Average 44.04 47.3 14.7

16

Table 5 – Distribution of control across Eastern Europe

Source: Pajuste (2002)

Slide 2.33

Conclusions

• The Berle-Means hypothesis is only upheld for the UK and the USA.

• The main types of shareholders differ between the UK-USA and the rest of the world.

CASE DISCUSSION : AIG

The Nonmarket Environment of the Banking Industry

Issues

Interests

Institutions

Information

Group Discussion Casestudy : AIG

1. Identify the corporate governance issuesthat AIG faced.

2.2 Control vs Ownership Rights

1. Review the various devices that create a

wedge between control and ownership.

2. Differences between control and

ownership as they determine the types of

conflicts of interests that a company and

its stakeholders may be subject to.

Learning Outcomes

• By the end of this lecture, you should be able to:

1. Distinguish ownership from control

2. Explain how to obtain the various combinations of weak or strong control with dispersed or concentrated ownership

3. Define security benefits and private benefits of control

4. Assess the importance and amplitude of private benefits of control across countries.

Introduction

• While in the UK and the USA most listed corporations are widely held, in the rest of the world corporations tend to have large shareholders with significant control.

• How do these large shareholders manage to stay in control?

• The short answer is that they leverage control, i.e. they manage to hold a substantial percentage of voting rights while holding fewer cash flow rights.

Introduction (Continued)

• We have already seen one way of leveraging control which is ownership pyramids, but there are others.

• More generally, we shall analyse the various combinations of dispersed or concentrated ownership and weak or strong control.

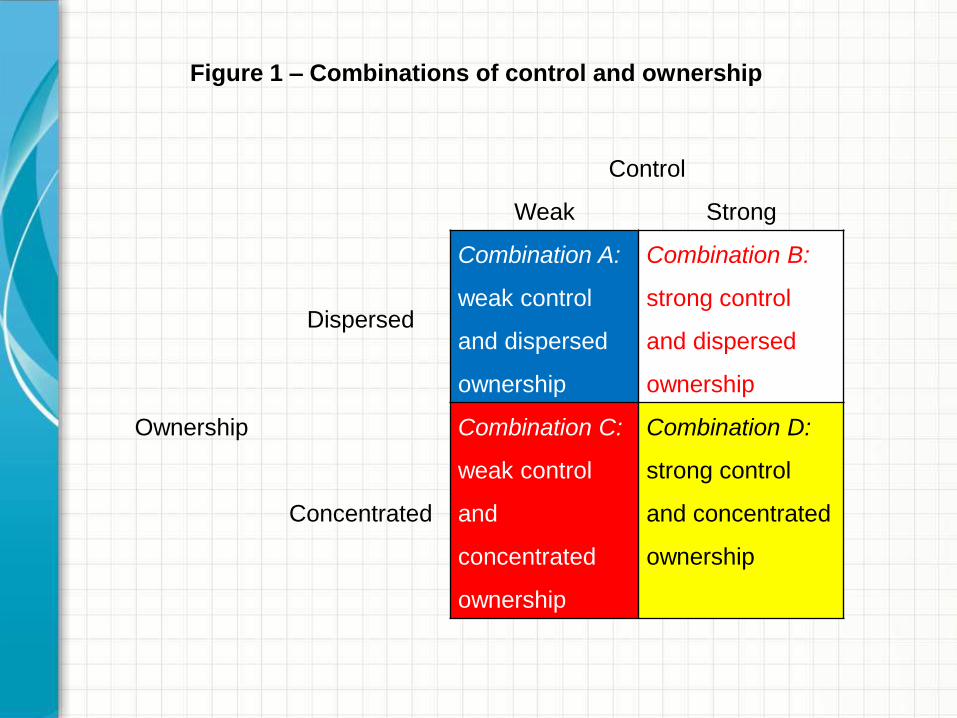

Combinations of Ownership and Control

• We shall distinguish between two extremes for both control and ownership

– strong versus weak control

– concentrated versus dispersed ownership.

Control

Weak Strong

Ownership

Dispersed

Combination A:

weak control

and dispersed

ownership

Combination B:

strong control

and dispersed

ownership

Concentrated

Combination C:

weak control

and

concentrated

ownership

Combination D:

strong control

and concentrated

ownership

Figure 1 – Combinations of control and ownership

Combinations of Ownership and Control

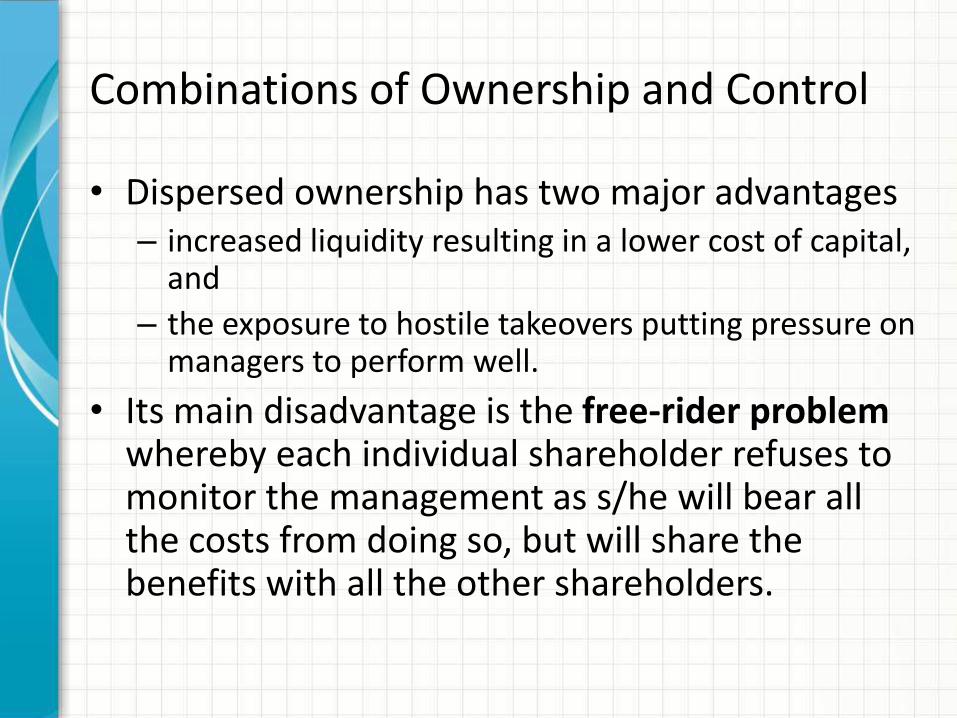

• Dispersed ownership has two major advantages– increased liquidity resulting in a lower cost of capital,

and

– the exposure to hostile takeovers putting pressure on managers to perform well.

• Its main disadvantage is the free-rider problem whereby each individual shareholder refuses to monitor the management as s/he will bear all the costs from doing so, but will share the benefits with all the other shareholders.

Combinations of Ownership and Control (Continued)

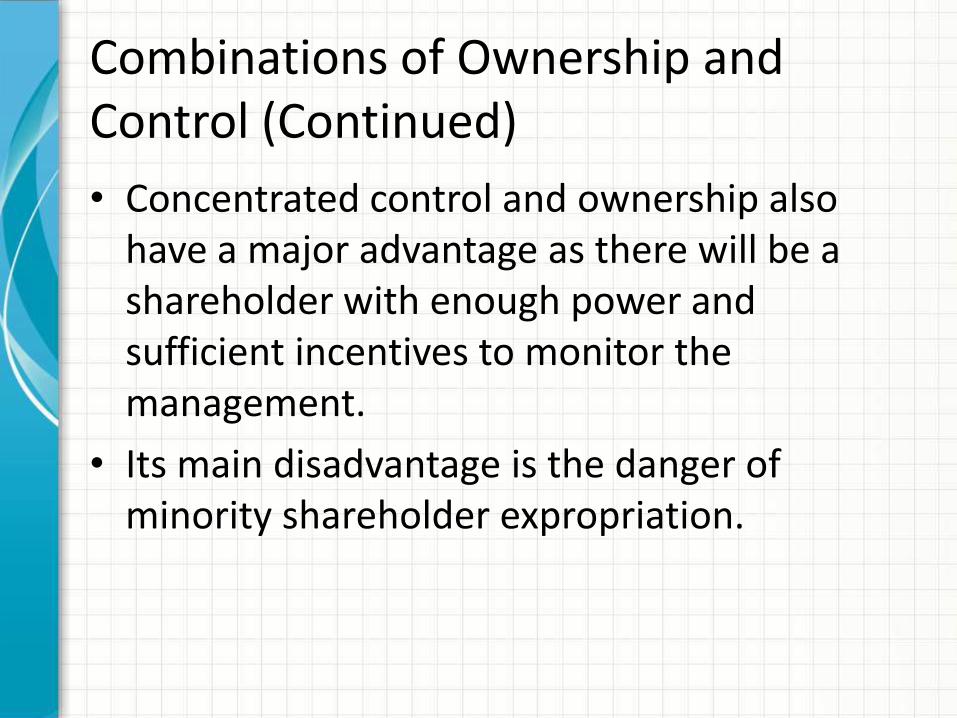

• Concentrated control and ownership also have a major advantage as there will be a shareholder with enough power and sufficient incentives to monitor the management.

• Its main disadvantage is the danger of minority shareholder expropriation.

• A priori, we expect– combination A to apply to most Anglo-American

firms, and

– combination D to most Continental European firms.

• However, due to several mechanisms, combination D does not apply to most Continental European firms.

• As a result, combination B prevails outside the UK and the USA.

Combinations of Ownership and Control

(Continued)

Combination A: Dispersed Ownership and Weak Control

• Case of most UK and US firms.

• Advantages of liquidity and takeover market.

• Disadvantages of insufficient monitoring.

• Main conflict of interests is between the management and the shareholders.

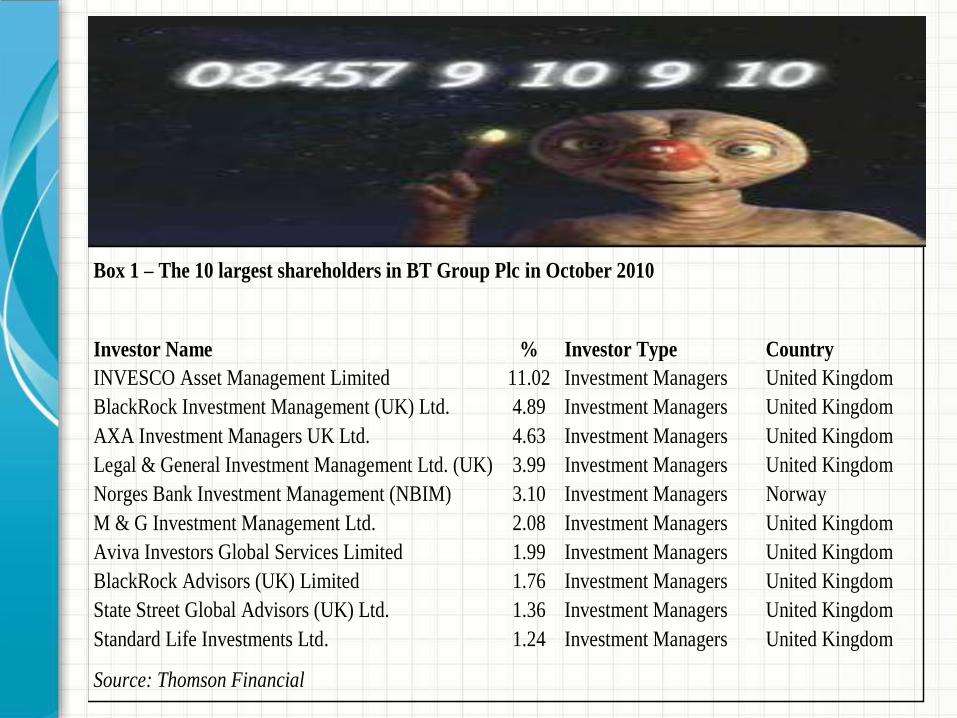

Box 1 – The 10 largest shareholders in BT Group Plc in October 2010

Investor Name % Investor Type Country

INVESCO Asset Management Limited 11.02 Investment Managers United Kingdom

BlackRock Investment Management (UK) Ltd. 4.89 Investment Managers United Kingdom

AXA Investment Managers UK Ltd. 4.63 Investment Managers United Kingdom

Legal & General Investment Management Ltd. (UK) 3.99 Investment Managers United Kingdom

Norges Bank Investment Management (NBIM) 3.10 Investment Managers Norway

M & G Investment Management Ltd. 2.08 Investment Managers United Kingdom

Aviva Investors Global Services Limited 1.99 Investment Managers United Kingdom

BlackRock Advisors (UK) Limited 1.76 Investment Managers United Kingdom

State Street Global Advisors (UK) Ltd. 1.36 Investment Managers United Kingdom

Standard Life Investments Ltd. 1.24 Investment Managers United Kingdom

Source: Thomson Financial

Box 2 – The 10 largest shareholders in The Coca Cola Company in October 2010

Investor Name % Investor Type Country

Berkshire Hathaway Inc. 8.66 Investment Managers United States

Vanguard Group, Inc. 3.62 Investment Managers United States

State Street Global Advisors (US) 3.46 Investment Managers United States

BlackRock Institutional Trust Company, N.A. 3.29 Investment Managers United States

Fidelity Management & Research 2.80 Investment Managers United States

Capital World Investors 2.59 Investment Managers United States

SunTrust Bank 2.38 Investment Managers United States

Fayez Sarofim & Co. 0.85 Investment Managers United States

Davis Selected Advisers, L.P. 0.84 Investment Managers United States

Grantham, Mayo, Van Otterloo & Co., L.L.C. 0.83 Investment Managers United States

Source: Thomson Financial

Slide 3.52

Combination B: Dispersed Ownership and Strong Control

• This combination prevails in most corporations outside the UK and the USA.

• Active market in the shares.

• There is a controlling shareholder with enough power to prevent the managers from expropriating the shareholders.

• However, there is also an increased risk of minority shareholder expropriation.

Box 3 – Ownership and control of BBS AG

Source: Hoppenstedt Aktienführer 2007

Slide 3.54

Goergen, International Corporate Governance, 1st Edition © Pearson Education Limited 2012

Combination C: Concentrated Ownership and Weak Control

• This is a fairly rare combination.

• It applies to only a few firms across the world, including German firms with voting caps.

• Minority shareholders are protected as no single shareholder is able to dominate.

• Lack of monitoring and low liquidity.

Box 3.4 Voting cap in Nestlé SA

Nestlé SA has a provision in its articles of association specifying a voting cap which prevents any

person from voting directly or indirectly for more than 5% of the equity. Under this provision, legal

entities that have links via equity holdings, voting rights, common management or any other form

will be considered as a single shareholder.

Source: Nestlé SA, 2010 corporate governance report

Combination D: Concentrated Ownership and Control

• This combination creates strong monitoring incentives.

• However, there is also low liquidity and a reduced takeover probability.

• Volkswagen AG holds 99% of the shares of Audi AG.

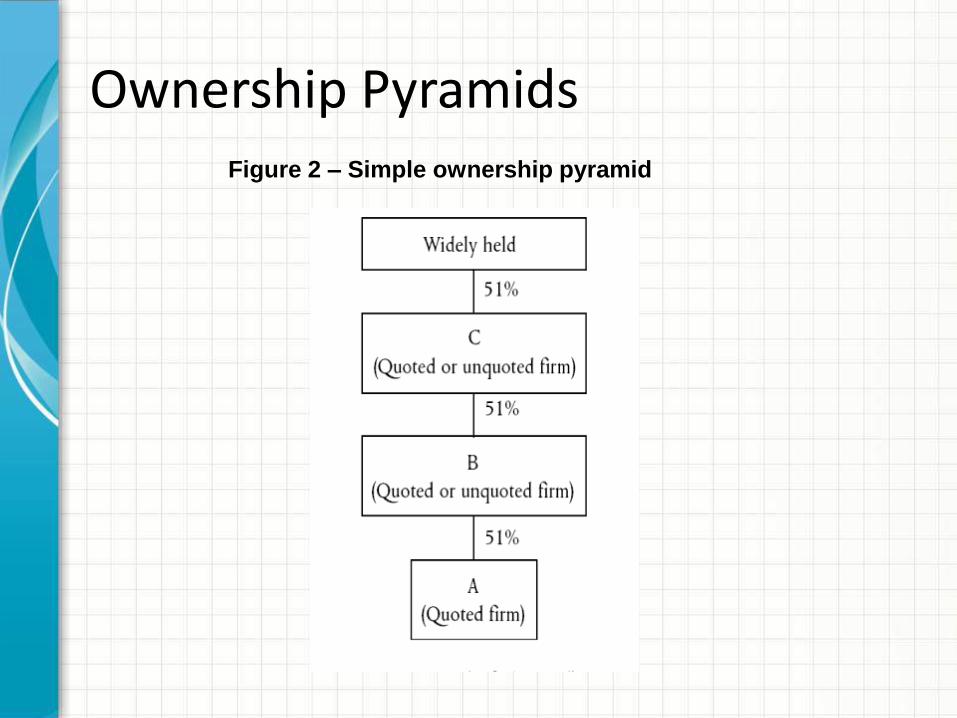

How to Achieve Dispersed Ownership and Strong Control• There are five main ways of achieving this

combination – ownership pyramids,– proxy votes,– voting coalitions,– dual-class shares, and– clauses in the articles of association that confer

additional votes to long-term shareholders.

• They all consist of leveraging control, i.e. having control while holding a lower ownership stake.

Ownership PyramidsFigure 2 – Simple ownership pyramid

Proxy Votes

• We have already discussed proxy votes held by banks.

• These proxy votes originate from the shares of the banks’ customers deposited with the banks.

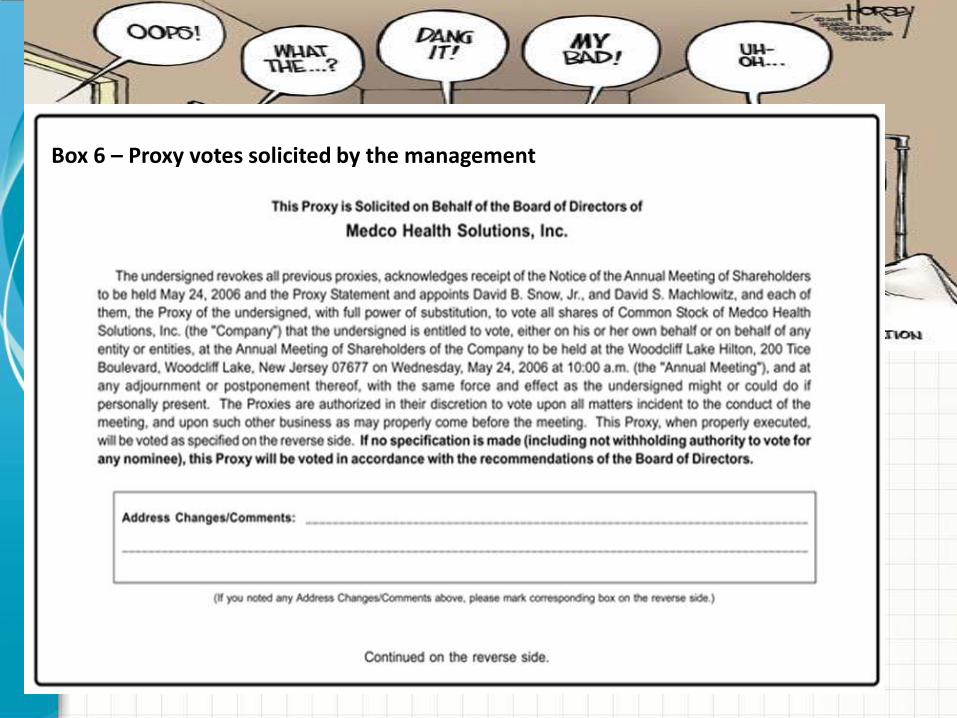

• However, proxy votes may also be solicited by– the management, or

– small shareholders seeking the support of the other shareholders to obtain approval for a motion they intend to put forward at the shareholders’ meeting.

Box 6 – Proxy votes solicited by the management

Voting Coalitions

• A voting coalition or voting pool consists of several shareholders agreeing to vote in the same way.

• In practice, voting coalitions are rare, especially those that persist in the long term.

• One reason for the infrequency of voting coalitions may be the costs imposed by regulation.

Voting Coalitions (Continued)

• The UK City Code on Takeovers requires shareholders that have acquired a stake of at least 30% to make a tender offer to the remaining shareholders.

• The same rule applies to voting coalitions.

• However, there is evidence that in the UK voting coalitions are formed on an ad hocbasis to intervene in poorly performing companies.

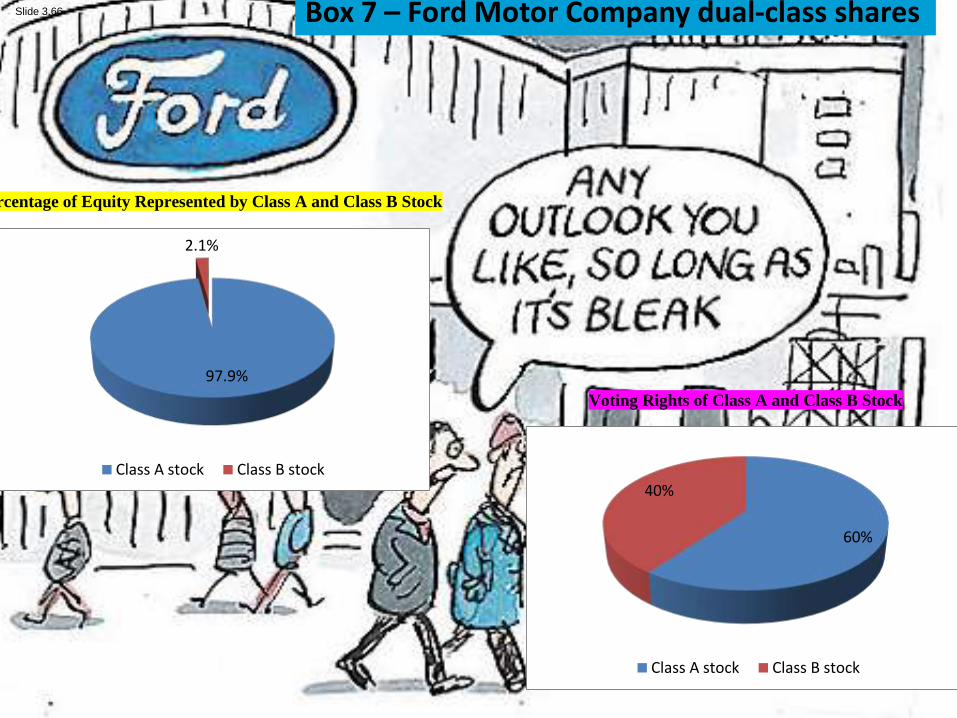

Dual-class Shares

• Companies with dual-class shares have two classes of shares– a class with voting rights or superior voting rights, and

– a second class with no voting rights or fewer voting rights.

• While non-voting shares have the disadvantage of no vote, in some countries these shares confer preferential dividend rights and a higher seniority (e.g. German preference shares).

• Dual-class shares are issued by some Continental European firms, but also some American firms.

Box 7 – Ford Motor Company dual-class shares

Percentage of Equity Represented by Class A and Class B Stock

97.9%

2.1%

Class A stock Class B stock

Voting Rights of Class A and Class B Stock

60%

40%

Class A stock Class B stock

Slide 3.66

Ford Motor Company has dual-class shares outstanding. The common stock represents

roughly 97% of the equity (33 / (33 + 1)) and the class B stock 3%. However, the common

stock has only 60% of the votes compared to 40% for class B.

Source: Ford Motor Company – 2009 annual report p.77 & p.150

“The Ford family holds all 71 million shares of the company's Class B stock, along with a

small number of the company's […] common shares. Under rules designed to preserve family

control and drafted when the company went public in 1956, the family holds 40 percent of

the voting power at the company as long as it continues to own at least 60.7 million shares of

the Class B stock [...]”

Source: Keith Brasher (2000), Ford Motor to Pay $10 Billion Dividend and Ensure Family

Control, New York Times, 14 April, Section C, p.1.

Conferring Additional Votes to Long-term Shareholders

• Many French companies confer additional voting rights to their long-term shareholders via a clause in their articles of association.

• Frequently, such clauses are put in place at the time of the IPO and are also retrospective.

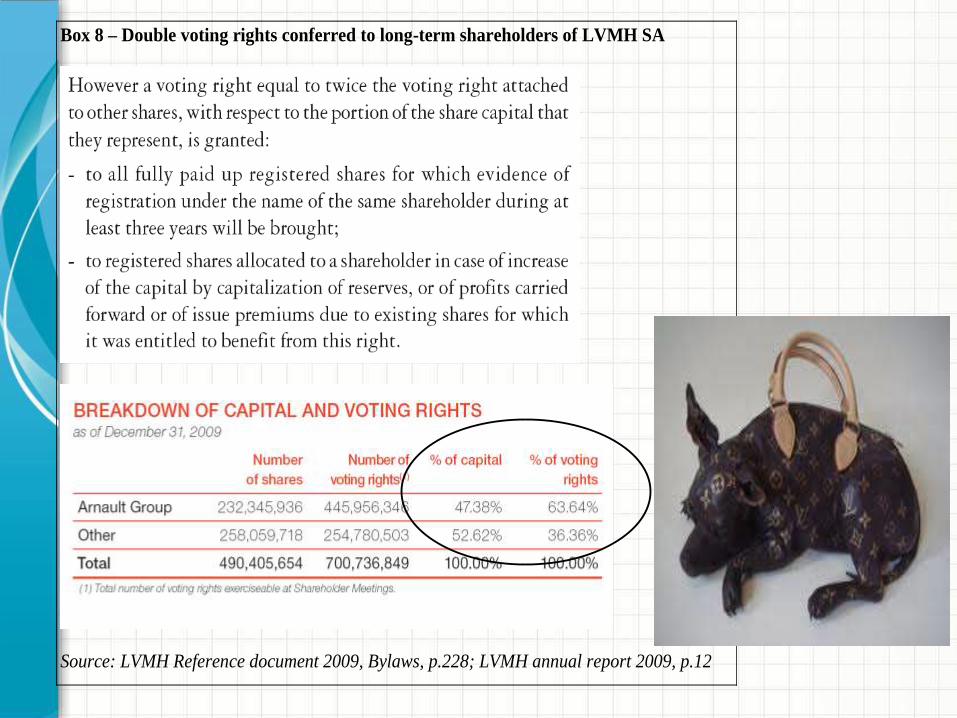

Box 8 – Double voting rights conferred to long-term shareholders of LVMH SA

Source: LVMH Reference document 2009, Bylaws, p.228; LVMH annual report 2009, p.12

The Consequences of Dispersed Ownership and Concentrated Control• Sanford Grossman and Oliver Hart argue that

large stakes create benefits of control.• There are two types

– security benefits originate from the increase in firm value due the monitoring of the management and they are shared by all the shareholders

– private benefits are extracted from the firm by the large shareholder and are at the expense of the minority shareholders.

• The latter include tunnelling, transfer pricing, nepotism and infighting.

The Consequences of Dispersed Ownership and Concentrated Control (Continued)

• The five main ways of achieving dispersed ownership with concentrated control all violate the rule of one-vote one-share.

• The main consequence of violating this rule is the increase in private benefits of control and the increased probability of minority shareholder expropriation.

• While private benefits are difficult to quantify, there are nevertheless empirical studies that have tried to do exactly that.

The Consequences of Dispersed Ownership and Concentrated Control (Continued)• The study by Michael Barclay and Clifford

Holderness was one of the first such studies.

• They measure the value of private benefits by the premium above the market price paid by the buyer of a block of shares.

• However, Jeffrey Zwiebel argues that one also needs to take into account the size of the block changing hands.

Table 1 – Block premiums per country

Notes: The block premium is the difference between the price per share paid for the block and the stock

price two days after the announcement of the transfer of the block divided by the latter price and multiplied

by the proportion of cash flow rights presented by the block.

Source: Dyck and Zingales (2004)

Slide 3.73

Conclusions

• The combination of ownership and control determines the main potential conflict of interests.

• Combination A prevails in the UK and the USA whereas combination B prevails elsewhere.

• How to achieve combination B and its main consequence.

2.3 Corporate Governance

Systems1. Taxonomies of corporate governance

systems.

2. Economics and politics of Global

Capitalism.

3. Hierarchy of systems relating to law and

investor protection; electoral systems; and

political orientation of governments in power.

4. Institutional arrangements and economic

performance.

Learning Outcomes

• By the end of this lecture, you should be able to:1. Understand the economic and political context

which has enabled global capitalism to rise

2. Critically review the assumptions underlying the taxonomies from the law and finance literature and those from the VOC literature

3. Assess the possible limitations of the various taxonomies as well as the validity of their predictions

4. Explain path dependence and distinguish between the two types of path dependence.

Introduction

• This lecture reviews the various taxonomies of corporate governance systems.

• It is important to realise that the various taxonomies have very different premises.

• The taxonomies from the law and finance assume that– individuals maximise their utilities in the presence of

institutions which constrain their behaviour, and– there is a zero-sum game between improving the

rights of investors and those of workers.

Introduction (Continued)

• In contrast, the varieties of capitalism literature

– focus on the concept of complementarities, and

– do not assume that there is a zero-sum game between worker and investor rights.

The Rise of Global Capitalism• In their 1932 book, Adolf Berle and Gardiner

Means identified a new social phenomenon and major step in the development of capitalism.

• This was the emergence of a class of professional managers running firms on behalf of their owners.

• The first challenge faced by this new class was the stock market crash of 1929 and the Great Depression of the 1930s.

The Rise of Global Capitalism (Continued)

• The Great Depression gave start to large-scale government programmes globally to revive the economy.

• The most famous one was US President Franklin Delano Roosevelt’s New Deal.

• As a response to the recent failures of its commercial banks, the USA introduced the Glass-Steagall Act in 1933.

• The Act introduced a segmentation between commercial banks and investment banks.

The Rise of Global Capitalism (Continued)• In summer 1944, the Bretton Woods agreement

created new global economic institutions for the post-WWII period– the International Monetary Fund (IMF), and– the International Bank for Reconstruction and

Development (IBRD) or World Bank.

• It also set up a system of fixed currency exchange rates.

• At the end of WWII, the USA and the USSR emerged as the two pillars of political power.

The Rise of Global Capitalism (Continued)

• The post-WWII period saw substantial improvements in workers’ rights and the emergence of the welfare state.

• The class of professional managers now faced a class of blue- and white-collar workers represented by powerful unions.

• In Germany, the Co-determination system was put in place consisting of workers councils and workers board representation.

The Rise of Global Capitalism (Continued)

• During the 1960s, Western economies experienced unprecedented economic growth.

• However, at the beginning of the 1970s the Bretton woods system was in crisis– The USA had a massive trade

deficit due to the Vietnam war– The deficit was financed by

printing more dollars which fuelled inflation

– In 1971, President Nixon put an end to the convertibility of the dollar into gold.

The Rise of Global Capitalism (Continued)• The 1973/4 oil crisis further fuelled inflation.

• By 1976, the Bretton Woods agreement had broken down and all major currencies were now floating.

• Developed countries were now experiencing stagflation, i.e. stagnation combined with high inflation and unemployment, caused by high oil prices as well as a spiral of wage and price adjustments.

• Few believed that Keynesian economic policies would be a way out of the crisis.

The Rise of Global Capitalism (Continued)• The crisis gave rise to neoliberalism as a new

political ideology.• Neoliberalism is the doctrine that

– markets are better at allocating economic resources, and

– individuals are better at making economic decisions

than governments.• The next few decades were to be dominated by

this new doctrine, also called financialisation or globalisation.

The Rise of Global Capitalism (Continued)

• Financialisation refers to different, but related phenomena

– the increasingly important role of capital markets and the financial services industry compared to the manufacturing industry, and

– the process of turning any asset generating cash flows into a financial security or a derivative.

The Rise of Global Capitalism (Continued)

• In 1979, the Conservatives won the elections in the UK and Margaret Thatcher became Prime Minister.

• In 1980, Ronald Reagan, A Republican, became the President of the USA.

• Both engaged in programmes of market liberalisation and deregulation.

• Thatcher curbed trade union power with a succession of laws during the 1980s.

• Trade union membership fell from roughly 50% to 34% in 1990.

The Rise of Global Capitalism (Continued)

• The UK was the first country in Europe to start an ambitious programme of privatisation.

• Two of the major aims of the privatisationprogramme were

– to widen share ownership, and

– to encourage employee share ownership.

• Other European countries were to follow with their own privatisation programmes.

The Rise of Global Capitalism (Continued)

• In the USA, Ronald Reagan was a fervent follower of supply-side economics.

• According to supply-side economics, a necessary and sufficient condition to achieve economic growth is to reduce barriers to the supply side of the economy.

• Reagonomics consisted of keeping inflation low by controlling the supply of money, reducing tax and government spending.

The Rise of Global Capitalism (Continued)• The 1970s and 1980s also saw a wave of

deregulation of the major financial markets.• On 1 May 1975 (May Day), the US stock

exchanges moved from a system of fixed commissions to negotiated commissions.

• As a result of this decrease in trading costs– a lot of foreign companies applied for a cross-listing

in the USA, and– a major chunk of the trading in their shares moved to

the USA.

The Rise of Global Capitalism (Continued)• In response to the loss of business to the

USA, the London Stock Exchange underwent major changes in 1986 (Big Bang).

• The most important change was to remove minimum commissions on stock trades.

• The 1980s and 1990s also saw the demutualisation of British building societies.

The Rise of Global Capitalism (Continued)

• In 1985, Mikhail Gorbachev succeeded Leonid Brezhnev as head of state of the USSR.

• He is famous for– his glasnost (opening of the USSR), and

– perestroika (economic and political reform) policies.

• During the late 1980s, revolutions swept across the Communist Bloc resulting in– the reunification of West and East Germany, and

– the breakdown of the USSR.

The Rise of Global Capitalism (Continued)

• In 1992, the Single European Actcame into effect in the European Union– It removed barriers to capital flows

and the movement of EU citizens within the EU

– It brought about a liberalisation of financial and labour markets.

• In the USA, the Gramm-Leach-Bliley Act of 1999 practically repealed the 1933 Glass-SteagallAct.

• Banks were now allowed to conduct both commercial and investment banking.

First Attempts to ClassifyCorporate Governance Systems

• The British economist John Hicks and the American business historian Alfred Chandler Jr. were the first to attempt to categorise the different systems of capitalism.

• Hicks distinguishes between– market-based economies, and

– bank-based economies.

• The former rely on well developed capital markets and the issue of publicly traded securities to finance corporate investments.

First Attempts to ClassifyCorporate Governance Systems (Continued)

• Chandler studied the differences between American, British, German and Japanese capitalism from a historical perspective.

• Mark Roe highlights the importance of past regulation to understand differences in corporate governance across countries.

• In particular, banking regulation has had a major impact on whether a national economy develops into a market-based or bank-based system.

• Julian Franks and Colin Mayer have developed a more nuanced classification which does not just focus on the sources of financing for corporations.

• They distinguish between insider systems and outsider systems.

• Insider systems are characterised by– concentrated control and complex ownership structures,

– managers being monitored and disciplined by the large shareholder, and

– underdeveloped takeover and stock markets.

• Continental Europe is a representative of this system.

First Attempts to Classify

Corporate Governance Systems (Continued)

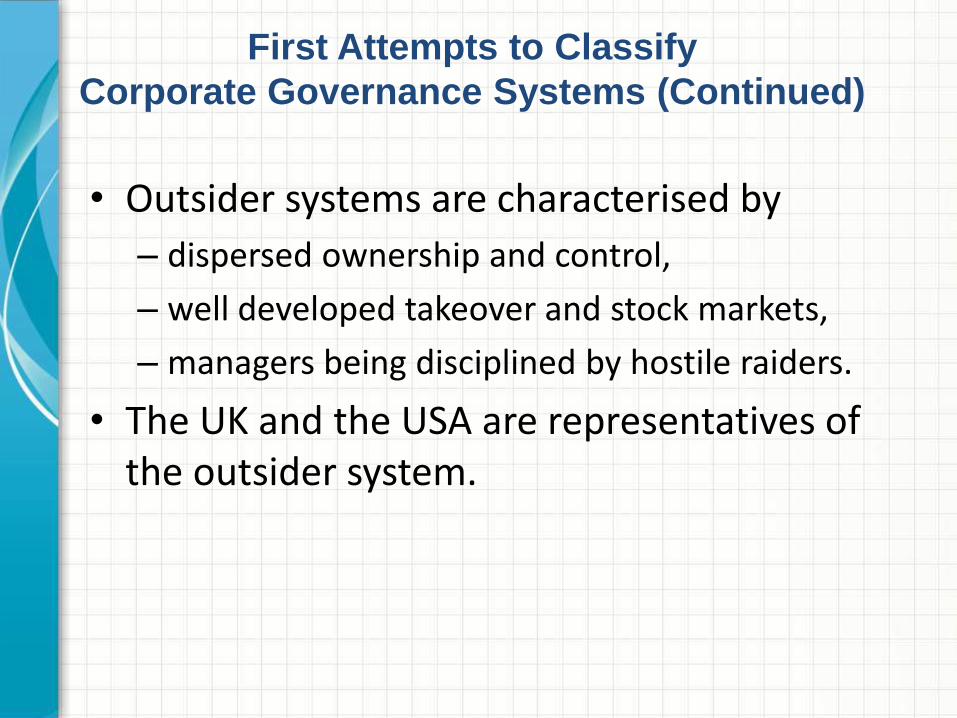

• Outsider systems are characterised by

– dispersed ownership and control,

– well developed takeover and stock markets,

– managers being disciplined by hostile raiders.

• The UK and the USA are representatives of the outsider system.

First Attempts to Classify

Corporate Governance Systems (Continued)

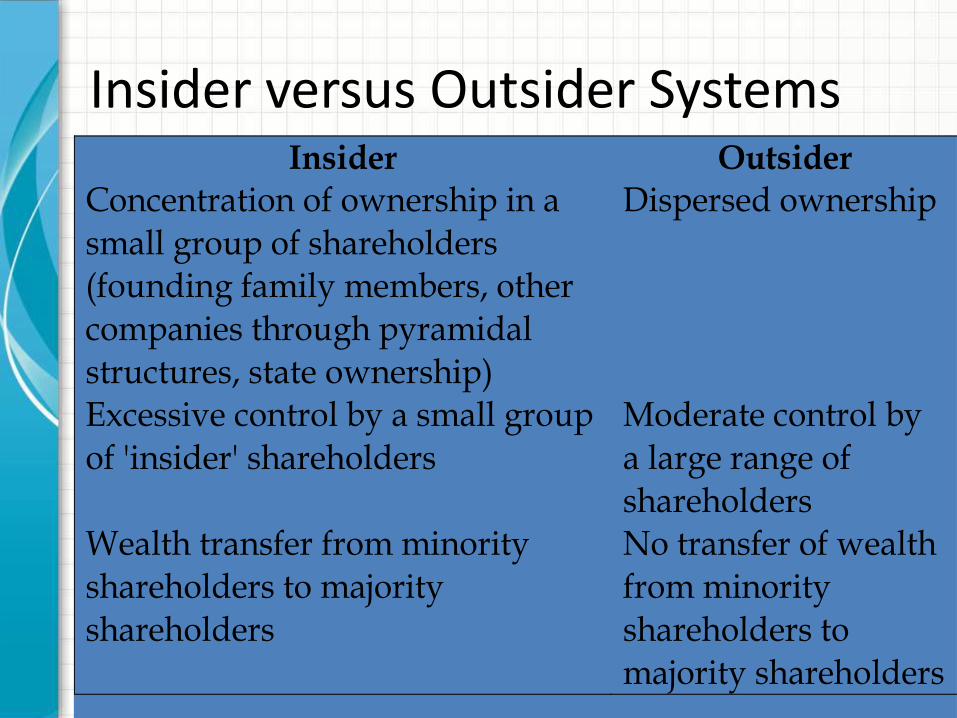

Insider versus Outsider SystemsInsider Outsider

Firms owned predominantly by inside shareholders who also wield control over management

Large firms controlled by managers but owned predominantly by outside shareholders

System characterised by little separation of ownership and control such that agency problems are rare

System characterised by separation of ownership and control which engenders significant agency problems

Hostile take-over activity is rare

Frequent hostile take-overs acting as a disciplining mechanism on company management

Insider versus Outsider SystemsInsider Outsider

Concentration of ownership in a small group of shareholders (founding family members, other companies through pyramidal structures, state ownership)

Dispersed ownership

Excessive control by a small group of 'insider' shareholders

Moderate control by a large range of shareholders

Wealth transfer from minority shareholders to majority shareholders

No transfer of wealth from minority shareholders to majority shareholders

Insider versus Outsider Systems

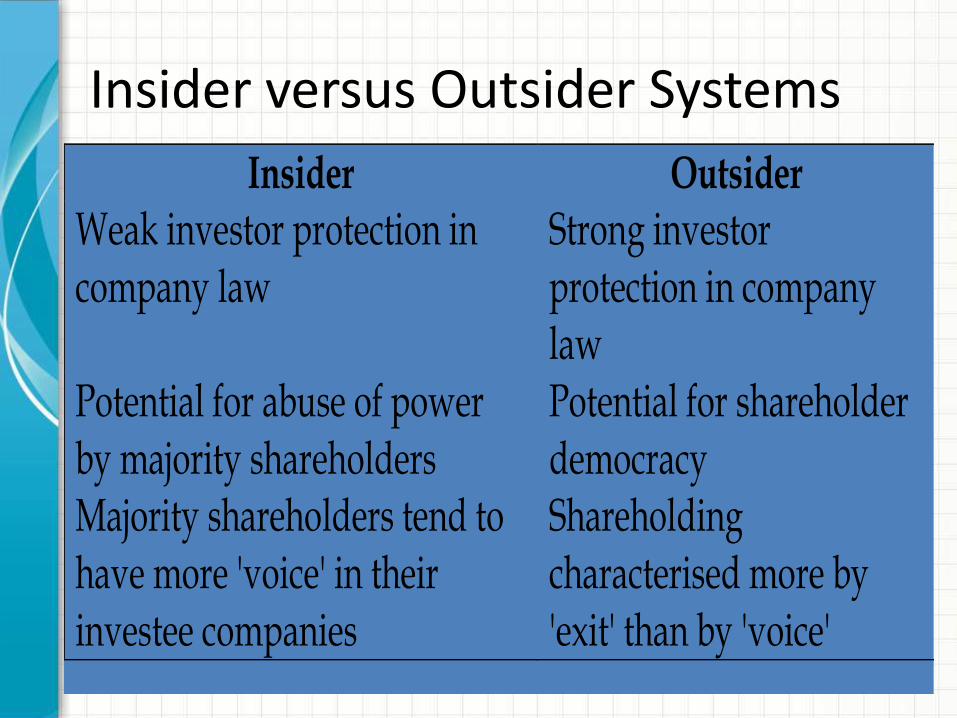

Insider Outsider Weak investor protection in company law

Strong investor protection in company law

Potential for abuse of power by majority shareholders

Potential for shareholder democracy

Majority shareholders tend to have more 'voice' in their investee companies

Shareholding characterised more by 'exit' than by 'voice'

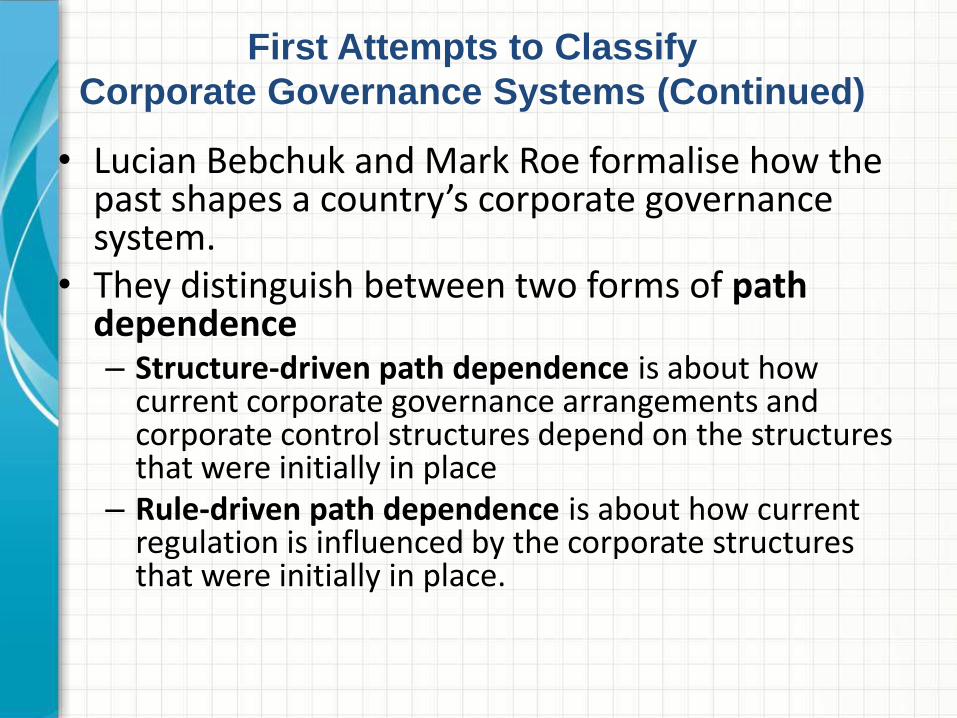

• Lucian Bebchuk and Mark Roe formalise how the past shapes a country’s corporate governance system.

• They distinguish between two forms of path dependence– Structure-driven path dependence is about how

current corporate governance arrangements and corporate control structures depend on the structures that were initially in place

– Rule-driven path dependence is about how current regulation is influenced by the corporate structures that were initially in place.

First Attempts to Classify

Corporate Governance Systems (Continued)

• The characteristics of national systems will tend to persist over time given the structure-driven and rule-driven path dependences.

First Attempts to Classify

Corporate Governance Systems (Continued)

Legal Families

• Rafel La Porta, Florencio Lopez-de-Silanes, Andrei Shleifer and Robert Vishny have started the law and finance literature.

• Their theory is based on the importance of property rights, in particular investor protection.

• They argue that in countries where investor protection is high capital markets are highly developed.

• Ultimately, the degree of investor protection drives economic growth.

Legal Families (Continued)

• La Porta et al. distinguish between two broad legal families, i.e. common law and civil law.

• Common law is case-based law.

• Judges pronounce judgements on the cases presented to them in a court of law.

• These judgements then create precedents for other similar future cases.

• Civil law originates from Roman law.

• It relies on extensive codes of law.

• The role of judges is limited to interpreting the law texts in court.

• La Porta et al. argue that the reliance on codes of law makes civil law less flexible and more reactive than common law which can easily adjust to new ways of managerial abuses.

• Common law is the law of the UK, the USA and most of the former colonies of the UK.

Legal Families (Continued)

• Within the broader family of civil law, La Porta et al. distinguish between– French (or Latin) law prevailing in French speaking

and Southern European countries,

– German law prevailing in Germanic countries as well as China and Japan, and

– Scandinavian law.

• Their antidirector rights index measures how well shareholders are protected against the management or the large shareholder.

Legal Families (Continued)

• Their creditor rights index measures how creditor rights are protected.

• La Porta et al. find that shareholder protection and creditor protection are

– highest in common law countries,

– lowest in French law countries, and

– somewhere in between in countries of German and Scandinavian law.

Legal Families (Continued)

• They also study the link between – investor and creditor protection on one side, and– the size of capital markets on the other side.

• They find that the size of stock markets, as measured by the number of domestic listed firms, is – largest in common law countries, – smallest in French law countries, and– somewhere in between in countries of German and

Scandinavian law.

Legal Families (Continued)

• However, when stock market size is measured by the value of IPO firms, the relationship with investor protection is less clear.

• The relationship between creditor protection and the size of the debt market is also somewhat ambiguous as German law countries have much larger debt markets than common law countries.

• Finally, La Porta et al. find a negative link between investor protection and the concentration of control.

Legal Families (Continued)

• They conclude that control remains concentrated in countries with weak investor protection to avoid expropriation by the managers.

Legal Families (Continued)

Political Determinants ofCorporate Governance• Mark Roe proposed politics and political

ideology as the main driver of corporate governance.

• Political ideology determines how countries achieve social peace.

• The Continental European social democracieshave achieved social peace by favouring employees over investors.

• Layoffs will be relatively hard, unemployment benefits and unemployment will be high.

Political Determinants ofCorporate Governance (Continued)

• Managers will less likely focus exclusively on the maximisation of shareholder value.

• High incentive packages for managers will also be less common to avoid the envy of other social classes.

• There will be less takeover activity as takeovers may generate layoffs.

• In summary, social democracies seek social equality at the cost of economic efficiency.

• Control will stay concentrated as this is the only way to keep managers and employees at bay.

• In countries with more conservative governments, the focus will be on improving investor rights.

• Given the strong investor rights, ownership and control will separate.

• Roe tests his prediction on OECD countries and finds support for it– Ownership and control are more concentrated

in countries with left-wing governments.

Political Determinants of

Corporate Governance (Continued)

• Marco Pagano and Paolo Volpin propose an alternative theory based on electoral systems.

• Their theoretical model is based on three different types of economic actors

– managers,

– employees, and

– rentiers.

Political Determinants of

Corporate Governance (Continued)

• Managers run the firms on behalf of the rentiers, but do not themselves own shares.

• Rentiers live off the revues of their investments.

• Both managers and employees prefer weaker investor rights.

• Weaker investor rights give more power to managers and facilitate the extraction of private benefits of control.

• They also provide better job security for employees, in particular less productive employees.

Political Determinants of

Corporate Governance (Continued)

• While managers and employees have similar preferences, rentiers are assumed to be a less homogenous group.

• Pagano and Volpin distinguish between majoritarian electoral systems and proportional electoral systems.

• Under a majoritarian system, the political party with a majority of districts wins the elections.

• Pagano and Volpin assume that the pivotal district is the district of the rentiers.

Political Determinants of

Corporate Governance (Continued)

• Hence, under a majoritarian system political parties will cater for the rentiers and focus on improving investor rights.

• Under a proportional system, the political party that obtains a majority of votes wins the elections.

• Under the latter, political parties will focus on the homogenous group of the managers and workers.

• The focus will be on employee rights at the expense of investor rights.

Political Determinants of

Corporate Governance (Continued)

• Pagano and Volpin test their theory on 21 OECD countries.

• In line with their predictions, they find that countries with more proportional voting systems have stronger employment protection and weaker investor rights.

• However, they only find that the La Porta et al. legal families only explain the levels of employee rights, but not those of investor rights.

• They conclude that the proportionality of the electoral system is better at explaining the level of investor rights than the legal family.

Political Determinants of

Corporate Governance (Continued)

The Varieties of Capitalism Literature

• So far, the focus has been on the law and finance literature which argues that the main role of institutions is to constrain the behaviour of managers and employees.

• Contrary to La Porta et al. and Pagano and Volpin, Roe does not advocate the superiority of one particular system.

• Nevertheless, he also assumes that strong investor rights cannot coexist with strong employee protection.

The Varieties of Capitalism Literature(Continued)

• In contrast, the varieties of capitalism (VOC) literature does not favour a particular system.

• Peter Hall and David Soskice study a wide range of questions relating to the distribution of wealth and the resolution of economic coordination problems.

• They argue that economic systems are not just about investments in assets and technologies.

• They are also about investments in human capital.

• The way economic coordination problems are solved depends on whether an economy is – a liberal market economy (LME) or– a coordinated market economy (CME).

• In LMEs, the coordination mechanism is the markets.

• Labour markets and markets for assets are highly flexible and developed.

• Firms tend to invest in highly marketable and liquid assets.

The Varieties of Capitalism Literature

(Continued)

• There is an emphasis on assets with relatively short payback periods.

• In-house training of employees is kept to a minimum to avoid competitors from free-riding on the firm’s efforts.

• Innovation is mainly of the blue skies nature.• LMEs tend to excel in highly competitive,

innovative industries as well as low value-added services industries.

• The UK, the USA and Australia are LMEs.

The Varieties of Capitalism Literature

(Continued)

• CMEs are based on complex networks to coordinate economic decision making.

• Markets, including labour and capital markets, are fairly illiquid and inflexible.

• Hence, there is less focus on highly liquid and generic assets.

• The emphasis tends to be on more specific, less marketable assets.

• Firms provide more in-house training and powerful employers associations avoid free-riding.

The Varieties of Capitalism Literature

(Continued)

• High employee protection and inflexible labour markets provide incentives for workers to invest in firm-specific skills.

• CMEs tend to do well in industries associated with incremental innovation such as high value-added manufacturing.

• France, Germany and Italy are examples of CMEs.

The Varieties of Capitalism Literature

(Continued)

• The concept of complementarities is key to the VOC literature.

• Two institutions have complementarities if their joint existence increases the efficiency of one or both of them.

• This concept implies that substantially different sets of institutions may still have very similar levels of economic output and wealth creation.

The Varieties of Capitalism Literature

(Continued)

How Do the Various Taxonomies Perform?• The first attempts to arrive at taxonomies

consisted of finding commonalities as well as differences across countries in terms of corporate governance.

• More recent attempts have been based on theoretical foundations, generating predictions as to– how institutional arrangements come about, and– how existing institutional arrangements explain

differences in corporate governance and corporate or economic performance.

How Do the Various Taxonomies Perform? (Continued)

• A basic criticism of La Porta et al. is its static nature.

• Taken to an extreme, today’s characteristics of the Italian corporate governance system are mainly due to what happened in the distant past, starting with the 12 Tables that laid down the foundation of Roman law in the 5th century BC.

• La Porta et al. justify the static nature of their theory by the fact that law only changes slowly over time.

• There also exist four more specific critiques of La Porta et al.

• The first critique has been formulated by Michael Graff.

• He argues that the La Porta et al. antidirector rights index includes criteria that are irrelevant whereas other, relevant criteria have been excluded.

• When the index is adjusted as proposed by Graff, there is no longer a link between investor protection and legal origin.

How Do the Various Taxonomies Perform?

(Continued)

• Holger Spamann’s critique is based on errors of encoding.

• He finds errors for 33 out of the 49 countries covered by La Porta et al. due to their use of secondary sources.

• After these errors have been corrected, the link between legal families and investor protection no longer exists.

How Do the Various Taxonomies Perform?

(Continued)

• Amir Licht, Chanan Goldschmidt and Shalom Schwartz argue that culture is the true driver behind differences in corporate governance.

• Using survey evidence, they find that countries that were under British rule are much more willing to deal with conflicts of interests in a court of law.

• They find a strong relationship between cultural attitudes and investor and creditor protection.

How Do the Various Taxonomies Perform?

(Continued)

• They argue that the persistence of cultural attitudes may explain why the countries of the former Communist Bloc have failed to improve investor protection despite wide-ranging legal reforms.

• Finally, Julian Franks, Colin Mayer and Stefano Rossi find that the separation of ownership and control in the UK can be traced back to the period before 1930 when investor protection was still low.

How Do the Various Taxonomies Perform?

(Continued)

• Franks et al. argue that the proximity of shareholders to their investee companies via local stock exchanges acted as a substitute for strong investor rights.

• There has also been criticism of the simple version of the VOC literature.

• The dichotomous version has been criticised to fail to account for the distinct character of Rhineland economies, the Nordic social democracies and Southern Europe.

How Do the Various Taxonomies Perform?

(Continued)

Research into Corporate Governance Systems Worldwide

• Shleifer and Vishny (1997) surveyed the extant research into corporate governance, focusing on the influence of countries' legal systems on corporate governance

• investor legal protection and ownership concentration

• High degree of legal investor protection was necessary to persuade investors to hand their money over to companies

• Legal systems characterised by low levels of investor protection were found to be associated with poorly developed capital markets

• Without strong investor protection, management can expropriate shareholders' funds

Research into Corporate Governance Systems Worldwide …

La Porta, Lopez-de-Silanes, Shleifer and Vishny (1997)

• Explained there were three general legal traditions operating across the globe

• French origin legal system is known to afford the lowest level of investor protection

• English origin legal system of common law affords the highest level of investor protection

• German and Scandinavian origin legal systems lie somewhere in between

La Porta, Lopez-de-Silanes, Shleifer and Vishny (1998)

• Studied the ownership structure of the ten largest nonfinancial corporations for a cross-section of 49 countries

• Supported the insider model for many East Asian economies characterised by a concentration of ownership, resulting in control of companies being held predominantly by a small number of owners, although less so in Japan and South Korea

Moving towards Convergence?

• Corporate governance standardisation is one way of building confidence in a country's financial markets and of enticing investors to risk funds

The OECD Principles

• First OECD Principles (1999)• Organisation for Economic Co-operation and Development• The Revised OECD Principles 2004• OECD has expanded to include 30 members, with the

accession of the Slovak Republic in December 2000• The OECD Principles (2004) stated that the 1999 principles

provided specific guidance for legislative and regulatory initiatives in OECD member countries but also in non-member states

• The 1999 principles have been thoroughly reviewed in order to take account of recent developments and experiences in both OECD member and non-member countries

The OECD Principles …

• In reviewing the 1999 principles, the OECD drew on a the findings of a comprehensive survey of how member countries addressed a variety of corporate governance challenges

• The revised principles have maintained the spirit of a non-binding and principles-based approach, which recognised the need to adapt implementation to varying economic, legal and cultural situations

• The need for sound corporate governance systems at a global level is reinforced in the preamble to the revised principles,

The OECD Principles …

• "If countries are to reap the full benefits of the global capital market, and if they are to attract long-term 'patient' capital, corporate governance arrangements must be credible, well understood across borders and adhere to internationally accepted principles" (OECD, 2004, p.13).

The revised principles cover the following areas :i. Ensuring the basis for an effective

corporate governance framework;

ii. The rights of shareholders and key ownership functions;

iii. The equitable treatment of shareholders;

iv. The role of stakeholders;

v. Disclosure and transparency; and

vi. The responsibilities of the board. It seems that stakeholders have been given greater weight in the redrafted version of the principles.

The revised principles cover the following areas …

(i) The corporate governance framework should promote transparent and efficient markets, be consistent with the

rule of law and clearly articulate the division of responsibilities among different supervisory, regulatory and

enforcement authorities.

(ii) The corporate governance framework should protect and facilitate the exercise of shareholders' rights.

(iii) The corporate governance framework should ensure the equitable treatment of all shareholders, including

minority and foreign shareholders. All shareholders should have the opportunity to obtain effective redress for

violation of their rights.

(iv) The corporate governance framework should recognise the rights of stakeholders established by law or through

mutual agreements and encourage active co-operation between corporations and stakeholders in creating wealth,

jobs, and the sustainability of financially sound enterprises.

(v) The corporate governance framework should ensure that timely and accurate disclosure is made on all material

matters regarding the corporation, including the financial situation, performance, ownership, and governance of the

company.

(vi) The corporate governance framework should ensure the strategic guidance of the company, the effective

monitoring of management by the board, and the board's accountability to the company and the shareholders.

The ICGN Statement on the OECD Principles• The International Corporate Governance Network

(ICGN)

• is an international organisation comprising of many groups interested in corporate governance reform

• OECD (2004) stressed that good standards of corporate governance are essential if countries are to attract international investment

• The CalPERS Principles

• CalPERS, the California Public Employees' Retirement System

The Outcome of Corporate Governance Convergence• A 'one size fits all' approach is unrealistic, as "alien

practices cannot be transplanted or imposed"

• Potential for countries to be forced into Anglo-American style capitalism

• Mayer (2000) argued against corporate governance convergence suggesting that systems should remain inherently different so as to promote competition and take advantage of comparative advantage

Corporate Governance in the European Union: ‘One Size Does Not Fit All'

• EU Commission has adopted attitude towards corporate governance that, "one size does not fit all“

• This is based on the belief that it is not possible to have one set of corporate governance principles for all European Union members

• Legal frameworks vary tremendously across European Union member states.

European Union Countries

• Culture and traditions also have a significant impact on corporate governance developments

• In EU countries there is a wide diversity in legal frameworks, cultures, traditions, religious beliefs and patterns of corporate ownership structure

Comply or Explain in EU

• Commission has decided that legislation should not be the driving force for EU corporate governance reform

• Harmonising corporate governance across EU, through legislation, the forced adoption of a common code, is not a practicale possibility

• EU Commission has decided to apply the 'comply or explain' approach to corporate governance

The Important Role of Shareholdersin the EU

• Commission has established that the driving force for good corporate governance should be shareholders

• Shareholders are an essential corporate governance mechanism for holding companies to account

• They should be fully informed and should act responsibly by exercising their voting rights

Shareholder Voting Rights in EU

• There are ongoing problems with corporate governance reform within the EU

• If shareholders are to drive corporate governance reform, they need to be able to exercise their rights

• There are significant obstacles to cross-border voting at the moment

• A key issue for the Commission is to facilitate cross-border voting.

Control-Enhancing Mechanisms and the 'One Share One Vote' Debate

• Debate surrounding

"One share: One vote“

• Every shareholder SHOULD own one voting right for every share he/she owns

• This is a core corporate governance principle, deriving from the established need to treat all shareholders equally (OECD, 2004).

• In many EU companies the ratio can be ten, twenty, or even one hundred votes per share, for certain, privileged shareholders

• The privileged shareholders can be, for example, founding family members

• Even where shares are sold to other shareholders, the rights on the new shares are often different (one share: one vote) such that the founding family members retain control.

Control-Enhancing Mechanisms and the 'One Share One Vote' Debate …

ABI Study (2005)(See Directions Paper)

• Association of British Insurers (ABI) study examined application of 'one share one vote' principle in EU

• Examined capital structure of EU companies to establish what proportion applied the 'one share one vote' principle

• Findings indicated that 65% of companies applied 'one share one vote', but identified some 'striking' exceptions to the principle

• Multiple voting rights were found, especially in France, Sweden and the Netherlands

EU Study 2007

• EU produced an in-depth report on the proportionality principle:

• "proportionality between ultimate economic risk and control means that share capital which has an unlimited right to participate in the profits of the company or in the residue on liquidation, and only such share capital, should normally carry control rights, in proportion to the risk carried. The holders of these rights to the residual profits and assets of the company are best equipped to decide on the affairs of the company as the ultimate effects of their decisions will be borne by them"

EU Study 2007 …

• This study identified a far wider range of control-enhancing mechanisms which do not follow the proportionality principle, but which are used widely throughout member states

• The findings of the study suggest that a 'one share one vote' policy would not difficulties of excessive control by concentrations of shareholders.

Other control-enhancing mechanisms include:

• pyramidal structures, available in all the member states surveyed and used in three-quarters of them;

• shareholder agreements available in all the countries surveyed and used in 69% of them, and;

• cross shareholdings used in 31% of the countries surveyed

… One share One vote• Although 'one share one vote' has been

advocated by institutional investor representative organisations, there has been resistance from the EU corporate community, who favour investor choice, with transparency, rather than regulation of dual share classes, being the essential mechanism of accountability

Board Structure and Performance in EU• EU-wide adoption of good corporate

governance practice with respect to the appointment of non-executive directors on corporate boards

• BUT• definition of independence has been applied

in a 'flexible' manner. • Most EU member states disclosing

remuneration

Choice of Language for Corporate Communications

• Which language should be used for the annual general meeting?

• Which language should corporate disclosures and documents be presented in?

• How can shareholders exercise informed votes if they cannot understand the language in which voting forms are presented?

Commission's approach to dealing with such problems in corporate governance is as follows:

• 1. Consultation

• 2. Recommendation or directive

• 3. Ex post evaluation

• 4. If recommendations or directives do not deliver then their usefulness is questionable

• 5. Ex post, if objectives not achieved, what can be done next?

• An evaluation is necessary after regulation

Corporate Governance in Developing

Economies: The Case of Uganda

• Research into corporate governance in Africa is in its infancy

• Study by Wanyama (2007) represents the first attempt to reflect on corporate governance issues in Uganda

• Issues and conclusions apply to many developing economies

Wanyama (2007)

• Research aimed:-

• to examine whether principles of corporate governance have led to significant improvements in corporate governance in Ugandan companies

• To discover whether guidelines are enough to develop good corporate governance, or whether more is needed.

Wanyama et al. (2007, p.16).

• "… the level of implementation of corporate governance guidelines in Uganda is poor …. attributed ….to the lack of an appropriate framework to support implementation and enforce compliance with the guidelines"

Factors Impeding Corporate Governance Improvements in Uganda

• Cultural and social factors:-• pressure from extended families for financial

support, leading to bribery and corrupt practices• hierarchical structures (heads of families/ age)• Sexism• Tribalism• Economic factors:-• tax levels• Remuneration• inflation and poverty

Other problems

• Shareholder advocacy (means by which shareholders can hold boards to account) was identified as a serious weakness in Ugandan corporate governance

• Family ownership structures make it difficult for shareholders to exercise their rights in Uganda.

A Need for MoreEthical Business Practices

• Unethical conduct significant obstacle to good corporate governance:-

• sexual harassment of employees;• fear of whistleblowing • political and other corporate appointments not

based on merit• bribery and corruption• poor accounting disclosures• lack of ethics among senior corporate employees,

such as integrity, punctuality, honesty and accountability

• inadequate protection of employees' rights, leading to exploitation and harassment

Wanyama suggested:

• "… extra resources need to be provided to enable the legal, regulatory and enforcement agencies to perform their work adequately, while the governance framework also needs to take into account the specific cultural context of Uganda, where respect for elders and the protection of the family is a major concern. In addition, the economic policies of the country need to be scrutinised to ensure that they foster and nurture good corporate governance practices in Uganda, most fundamentally by ensuring that the population … receives a fair wage or living allowance so that the motivation to cheat or take bribes is reduced"

Global Convergence ofCorporate Governance• Involves striking a balance between

retaining individual characteristics of a country and adopting a market-based, Anglo-Saxon form of governance

• Involves improving ETHICS in business

• Involves improving corporate governance in SPIRIT not just by following codes of practice

Conclusions

• The rise of global capitalism.

• First attempts at categorising corporate governance systems.

• Path dependence.

• The law and finance literature and the hierarchy of corporate governance systems.

• The VOC literature and the concept of complementarities.

• Corporate governance convergence

Further Reading• Solomon, Jill (2010) Corporate Governance and

Accountability 3rd Edition, Wiley, UK. Ch.7-8

• Larcker, David & Tayan, Brian (2011) Corporate Governance Matters, FT Press/Pearson New Jersey. Ch.2

• Goergen, Marc (2012) International Corporate Governance, Pearson. Ch.2-7

• Monks, A.G. & Minow, N. (2011) Corporate Governance, 5th Edition, Wiley. Ch.5

• CIMA - Performance Strategy: Study Text (2011) BPP Learning Media Ltd. Part B : 3

• Baron, David P.(2013) Business and its environment, 7th Edition, Pearson

Ideas for Next Discussion

• Carcello, Joseph V; Hermanson, Dana R; Ye, Zhongxia (Shelly) (2011) Corporate Governance Research in Accounting and Auditing: Insights, Practice Implications, and Future Research Directions, Auditing30. 3 (Aug 2011): 1-31.

QUESTIONS?

Related Documents