WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 1 WGU MBA Capstone – Task 3, Part A: Finding 15%: The Recovery of Lost Profits Assessment Code: JKT2 Student Name: Western Governors University Teresa Sjostrom Student ID: 301283000301283 Date: Feb 19, 2015 Mentor Name: Maryann Coty

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 1

WGU MBA Capstone – Task 3, Part A: Finding 15%: The Recovery of Lost Profits

Assessment Code: JKT2

Student Name: Western Governors University Teresa Sjostrom

Student ID: 301283000301283

Date: Feb 19, 2015

Mentor Name: Maryann Coty

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 2

Table of Contents

BACKGROUND INFORMATION ....................................................................................................................................... 3

PROBLEM OR BUSINESS NEED ....................................................................................................................................... 6

FUNCTIONAL AREAS ......................................................................................................................................................... 8

MARKETING ........................................................................................................................................................................ 8

PRODUCTION .................................................................................................................................................................. 10

FINANCIALS ..................................................................................................................................................................... 11

THE SOLUTION................................................................................................................................................................ 12

MARKETING ..................................................................................................................................................................... 13

PRODUCTION .................................................................................................................................................................. 15

FINANCIALS ..................................................................................................................................................................... 17

IMPLEMENTATION ........................................................................................................................................................ 20

FINANCIAL AND ORGANIZATIONAL IMPACT .......................................................................................................... 23

REFERENCE LIST ............................................................................................................................................................ 28

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 3

Background Information

The company is a manufacturer of custom interiors for U. S. over-the-road cars, busses,

and trailers. The company is one of about 50 companies of its kind in the US that average between

$5 and $15 Million in annual revenues. The industry is regional due to the need for frequent

maintenance and repairs, winterizing and upkeep for this type of vehicle conversion. Customers

typical buy from company’s they know and trust locally, similar to a local auto dealership.

The company was founded and operated by its owner 35 years ago, and has seen steady

growth and profits continually, up until the past five years. The product and the workmanship are

strong and stable, as is the company’s reputation for top quality and innovative designs. The

company opened with revenues under one million per year, but has grown substantially,

purchasing a new building seven years ago where they can produce a completed trailer per day

versus one per month just a few years ago. Throughout this growth cycle, the profitability

remained successfully between 15-22% of revenues under the owner’s supervision.

Images courtesy RVIA, 2015

Five years ago, the owner’s wife was diagnosed with cancer. At 60 years old, the owner

chose to turn the business over to his children, who had been working throughout the business for

the past 25 years. The son is operating as the Sales Manager (who also manages production,

engineering, and purchasing), and the daughter is the Office Manager, who also managed Human

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 4

Resources and Accounting. From the day these two took the reins, the profits have fallen sharply.

After five years of struggle, the owner acknowledges that there is a lack of education and ability

in the children. Upon further research, the children have no formal education beyond high school,

had their house and car payments paid out of company funds, and exhibited extreme immature

behavior among themselves and towards all employees. The employees claim that they have

become victims of the finger pointing and in the middle of opposing orders daily.

As marketing kept the orders coming in, the employees did whatever they could to build

the quality product as they had learned from the owner. From the day the children took charge,

however, financials show a trail of increased expenses, consistent profit losses, and questionable

accounting. Analyzing the monthly and annual statements, the costs per product shipped are rising

each month. The company now sits in a position of net annual loss for the second year in a row.

The owner is now very angry and frustrated, refusing to bail the company out. From the results in

analysis of the financials at a departmental level, the direct expenses for production and delivery

of each unit have risen over 30% since the children took charge of the company. Thirty percent!

On top of this issue, the new overhead expenses are adding another 5% in expenses. Thirty percent

to the net profit line is a hugely profitable business for a manufacturing company in the US. Thirty

percent of the revenues in 2014 ($9.7 Million) is $2.92 Million. What must be determined is where

did the profits go and exactly why is this company now failing. Without the bailout by the owner,

the company will be forced to close because this type of customization in a production environment

requires a minimum of $2.0 Million at current unit production rates. With the cash position in the

negative for year ending 2014, the company will be forced to close the doors if the owner does not

invest this $2.0 Million immediately.

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 5

This is a very serious situation for the company, as well as a very volatile one. Due to this

situation, the owner has specifically asked for a review, and that every issue found in the

organization is reported in detail. The reasoning for this request is in an effort to learn from

businesses outside the company. The owner feels that since this is the only business he has

managed fully on his own, that he may not know what he does not know, and it may be hurting

the company. His goal for this review is to form recommendations that will return the company

to a profitable business and remain open for his employees. To complete this request, this report

will include comments and issues not commonly included in a report of this type. With the amount

and degree of damage done so quickly, immediate thoughts were that the children were simply

stealing money, but also that there was much more causing this problem? Resolved to help, a

project plan was initiated with the owner and his newly appointed “Drill Sargent” Operations

Manager Bryan Payne. Bryan was a former coworker, known to be both capable intellectually,

and intimidating enough to send anyone in his way running for cover. He was the perfect person

for this job. Bryan is an Operations and IT expert, heavily technical, and a bit tough to understand

at times because he was so brilliant. Bryan needed a partner that could provide insight and

analysis, functionally and financially, to be able to pinpoint the issues and develop a solution.

Within two weeks of receiving the financials and conferencing with Bryan to identify the business

processes behind each of the report, the analysis showed the potential for a substantial difference

for the company, and presented a way to make changes that would save all those employees from

losing their jobs. It was clear that there were many issues, but the main opportunity was in

controlling the expense line. The largest and most impacted area was targeted, cost accounting

throughout the operation. Initial estimates determined that it is possible to reduce the expenses by

10-15% this year if the company was willing to get to work and quickly implement some changes.

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 6

Problem or Business Need

The company is a 35 year old, privately owned vehicle interior manufacturing company

with revenues of $10.0 Million in 2014. The interior company and/or its dealers make the sale for

a specific customized unit via a contract sales agreement. The company operates through standing

partnership agreements with several vehicle “shell” companies, who provide the vehicle shell as

specified by the engineering department for the custom interior designed in the sales contract. The

company then schedules production, pays the shell company for the custom shell to arrive on a

specified date, manufactures the interior as per specification, and delivers the finished product to

the customer.

The customer accepts delivery by purchasing the vehicle through standard cash or bank

loans. All units must be paid for in full prior to delivery to customer. Due to state registration of

vehicle law, the unit is the property of the shell manufacturer; therefore, the company does not

release a unit without full payment. Once the unit is released to a customer, the company has no

legal ownership to the work content or the vehicle, as the shell becomes a registered state vehicle

and bank liens are placed on the Vehicle Identification Number of the shell (VIN), not the interior.

The company has been under the management of the owner and his wife since inception in

1980, but since 2005 when his wife passed from cancer, the owner has allowed a two of his children

to operate the company. Profits have declined steadily since 2005, and drastically since 2009, when

the recreational vehicle industry sustained a 50% drop in sales due to the recession.

The company is operated with a staff of 10 managers and 85 full time employees, plus

another 100+ part time employees as needed. The company is a custom manufacturer that has a

large partnership in custom interior manufacturing for the horse trailer industry, a $4.0 Billion

division of the recreational vehicle industry in the United States.

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 7

The problem or need for the company is to implement a plan to reduce direct material and

labor expenses by a minimum of 15%, and hopefully 20-25%. Per the owner, who is funding the

company’s working capital to be able to remain open at this time, the requirement is that the

company must show that they have established methods to control these expenses going forward,

and must begin seeing at least 5-10 % for the third and fourth quarter of 2015, and 15% for 2016

forward. These percentages coincide with the amount that will be necessary to allow the owner

to recover his investments due to poor controls for the past two years, as well as return his company

to an expected range of 15-20% minimum net profits.

The company is operating in the red due to increases in expenses in direct material, direct

and indirect labor, freight/expedition charges for raw materials, and revenue losses due to missed

delivery dates. The direct production expenses have increased over 30% per unit since 2009 and

the company has no processes in place to be able to define or address the problem.

The current front-end business processes include a pricing sheet to cost the product,

including all options, and form a contractual “agreement of sale” based on the specific customer

order details. The production, inventory, and accounting systems from that point on are not

capable of tracking the costs of the raw materials ordered for that contract to the product as it

proceeds through production. There is no inventory management system. There are anywhere

from 15-30 vehicles in process at one time, with many using the same or interchangeable raw

materials. There company has no means to account for the true cost of a product in labor or raw

materials; therefore, there is no accountability on the production floor. Every employee knows

that parts and labor are not tracked, leading to a high risk for theft and waste. The facility is over

60,000 square feet and has no security points when open, making it difficult to monitor activities

of every person.

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 8

There is a definite issue with the children and their hostile and demeaning management

style contributing to this issue. It is a logical conclusion that due to a hostile and uncontrolled

physical environment, both waste and theft are contributing to the company’s extreme material

and labor production expenses.

Functional Areas

The loss in profits is a result of both lost sales and uncontrolled expenses within the

company. With serious sales declines experienced from 2008-2010 (during the U. S. recession)

and a new $2.8 Million building purchased in 2004 and filled with production equipment, the

overhead is creating negative monthly expense impact not previously a part of the operation. In

addition to capital overhead increases, the direct operating costs per unit have increased over

30% since 2005, two thirds of it since 2009. To implement a solution to recover at much as can

be within the very short amount of time left for this company to remain in business, the main

areas that must be impacted are the key departments that order, consume, and account for the

expenses in labor and materials: the Marketing, Production, and Finance areas.

MARKETING

The Marketing Department of the Company is responsible for building and closing the

revenues through sales contracts with Customers, both private and business-to-business. Ninety-

five percent of all products are business-to-business contract sales through recreational vehicle

dealerships. The contract will include a specified shell vehicle manufacturer and costs, and the

cost for the Company to complete a custom interior for the specified vehicle. The contract is a

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 9

pre-written form with pages and pages of available options and costs for customization. The

Dealer will select the options that the customer wishes, and total the contract to complete the sale.

All contracts require review by the Marketing, Engineering and Production Departments for design

and costing issues, approval of new costs, special requests, insurance of manufacturing standards,

etc. Contracts are active once approved through the Sales Manager (the son, also the longest-term

employee with design review experience), and final approval from the Operations Manager.

Once approved by the Company and the Customer, the unit placed on the schedule and added into

the production cycle based on the timing required for completion in the contract.

The critical piece of this marketing process is in estimating the correct pricing for exactly

what customizations the Customer ordered. Most every unit produced has several “off the cost

sheet” special requests that must be defined and cost to accurately reflect the work necessary for

the customizations included on the contract. Once the contract is approved, any differences in the

actual costs cannot be recovered. The unit must be delivered through the contract at the contract

price. The Marketing Department is responsible for the creation and maintenance of the pricing

sheets within the contract.

Review of the pricing sheets quickly showed that they have not been updated for seven

years. It is clear that this is causing a good portion of the problem. Raw material prices were

outdated in every area. Labor rates were also seven years behind. In approaching why this

occurred, the company stated that they had np way of knowing the actual costs; therefore, they

have never changed the pricing sheets. This issue is estimated to be contributing 10-12% of the

expenses problem. It also identifies the real problem: The Company has no means of product

costing or tracking of material and labor costs by unit. The pricing sheets they are using are simply

the last “snapshot” of costs that were taken seven years ago that worked well then.

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 10

Upon further review of the process for finalizing the contracts and the pricing sheets

prepared by marketing, a serious problem exists that is difficult to change without exact costs, as

pricing is listed at a very detailed level, allowing almost “too much information” to be passed

through to the customer, and creating backlash by showing actual markups for raw materials. In

addition, these policies will create a serious perception problem when the correct prices are

inserted, because the Customers and Dealers will immediately know that a price increase has

occurred in the entire product line, making them very unhappy. It is clear that changes need to be

made to address the contract structure and pricing provided by marketing going forward.

PRODUCTION

Once the unit is scheduled into production, the company then orders the vehicle shell to

match the specifications of the interior customization. The shell vehicle is one production unit,

and is scheduled to arrive on a specific date correlating with the date that the purchasing

department has defined that all raw materials will be in stock, and the delivery date. The production

process is completed in six phases, with each phase having a specific station for the specified skills,

labor, and tools to complete the phase. The high-level phases of production are as follows:

1. Framing

2. Electrical and Plumbing

3. Wall and Ceiling Construction, Cabinet Set

4. Installation of Appliances and Entertainment

5. Custom Décor and Specialty Trim – All Hardware

6. Installation of Flooring and All Finishing

As mentioned above, there are 15-30 vehicles in process at any one time across these six

main stations. Any delays due to construction issues or late raw materials will cause issues in the

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 11

timing and position sequence of the entire production schedule for all 15-30 units on the production

floor. If this occurs, it quickly becomes expensive in labor and overhead, as well as causing the

product to miss its delivery date per the contract, thus reducing revenues.

Upon first hand review of the production processes and procedures, the labor for each

station spent about 20-30% of their day either looking for parts, redoing a mistake in construction

as per the blueprints, or searching for a lead or supervisor to help with clarification of the design

or in construction. There was also a full time “expeditor” purchasing person staffed just to find

ways to quickly get parts needed, at any

costs. This person has been provided a

company truck, and his job is to run around

all over the state picking up parts that were

supposed to be in stock. He also orders

tremendous amounts of COD and Overnight

shipments that have very high freight costs.

Image: The Company, 2015

FINANCIALS

Analysis of the finance reports revealed the loss in profits were across the board in added

expenses for the production, purchasing, and delivery departments. Specifically, the general areas

of labor, material, and freight charges were each responsible for significant increases in expenses

per unit produced, totaling over 30% in direct expense increase versus results five years earlier.

The most interesting find in the analysis of the financials was the lack of detail available

to drill down further into the categories that were causing the expense problem. Specifically, no

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 12

attempt is made to compare the contracts and pricing sheets for the years’ revenues to the actual

expenses in materials and labor for the product produced. The lack of detail in the cost breakdown

and reporting from all departments did not allow any correlation between the units produced and

the materials, labor, or overhead costs. This lack of accountability in the financial accounting

system is the cause of the inability to identify where the expense increases are occurring by unit.

It was immediately noted that without the ability to identify costs per unit, or at a minimum per

category, there would be no means to identify the actual expense problem areas.

The growth in the past ten years has created a more complex working and production

environment that requires a more accurate and accountable costing system to manage the business.

Review of the core financial systems used for general accounting and payroll revealed that the

general ledger was held at only the department level, and that the accounts payable and accounts

receivable were not cross-referenced with the purchasing logs or the sales contracts. Essentially,

this means that the managers of the company have no means or tools to be able to identify their

expense issues. This issue must be resolved by reviewing the accounting system and the business

processes to provide a means to assign and track materials and labor by unit, as well as identify

the on hand inventory verses amount needed for upcoming production.

The Solution

The solution for the company to be able to reduce their expenses by at least 15% will

require two things: a system that allows the recording and tracking of costs by unit, and a revised

business process across all departments that accurately accounts for the materials and labor that is

required for each unit produced. The accounting system currently utilized by the company is a

Small Business Quickbooks System. After reviewing the options for inventory management and

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 13

tracking software, it was found that the best option for adding this functionality was in upgrading

the current Quickbooks Software to a 2015 Edition of Quickbooks Premier Manufacturing and

Wholesale. This option was selected because it offered all of the sales, inventory, purchasing and

cost tracking detail by unit produced, while also integrating with the current systems in accounting

and payroll. The company was using a ten-year-old version of the Quickbooks Small Business

Software, however, it was found that the core structure and accounting modules were compatible

and worked pretty much the same, with a few added features that would also be a nice addition in

the accounting areas. This was the logical choice for a solution for the company, as it would give

them all the features of cost accounting by unit, while not having to implement an entirely new

system for financial accounting. This meant that the system could be upgraded easily on a

weekend, and then the added modules could be available to begin collection of costs data to input

the next day. From this point, the company would count and input all inventory into the system

by month end, and begin the next month with a new sales and reporting system by unit produced.

This solution would mean changes to each of the functional areas, as follows:

MARKETING

The marketing department is currently signing contracts with pricing that is out of date,

with no way of accurately improving on their estimates. The Marketing Manager had expressed

her frustrations with the process, and her understanding of the need to update the contracts to the

managers. She had identified the issue and submitted changes that she could verify; however,

management had been unwilling to allow changes to the pricing sheets over the past seven years.

The solution, an upgrade to the Quickbooks System that adds in a module for manufacturing

business needs, will replace and address this problem for the Marketing Department.

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 14

To resolve the expense problem from the front end (the Sales Contract), the new system

implementation will replace the current contract and associated pricing sheets with “Sales Orders”

within the Quickbooks (QB) system. The Sales Order within the QB system includes internalized

actual costing based on 1) current inventory held value, or 2) inventory/on order value as per

purchase order agreement in process. The Customer Contract will be re-written to reference the

Sales Order (with pricing breakdown included) instead of the current “Pricing Sheets.” The

marketing department will implement a new process for estimations using the Quickbooks Sales

Order System. All department employees will be trained on the new system, as they had not

previously utilized Quickbooks Software. It is not anticipated that this will be a difficult transition

or a substantial process change for the current marketing team, as all marketing department

employees are very computer literate.

The marketing department’s pricing attachment for the Sales Contract will be updated to

reflect the appropriate level of detail in pricing, which will be an extrapolation of necessary detail

levels retrieved from the product build (assembly) module within the QB Inventory and Purchasing

Management System. These new processes and the accurate pricing they offer will ensure that all

contracts are reflect current pricing information no older than the latest purchase order price. It

should also be noted that the level of detail in the customer pricing sheet will be minimized going

SALES CONTRACTS

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 15

forward to reduce the possibility of contractual issues and show only “customized selections”

pricing as options, not the entire build cost down to the nuts and bolts, as previously included.

PRODUCTION

The production department will implement a series of business process changes that allow

the supervisors to assign parts and labor to the production unit in which they are utilized. The

current production tracking system is non-existent, so this tracking will initially be looked at as a

negative due to a bit more paperwork than prior operations. The current path of a unit build is

tracked on a set of design drawings that move through the process with the unit. These drawing

and instructions are carefully followed throughout the build, with Supervisor signoff required at

each phase completion. The assignment of labor

hours per day will be added to these design

sheets and signed off by the supervisor daily.

Each employee will record their number of

hours and employee number for each unit they

worked on during the day. This process will

only take a few seconds, as 90% of employees

do not work on more than 1-2 units in a day.

The tracking for the parts that will include high level, or unique tracking for items that are:

1) specific to the unit’s customization, 2) special ordered in quantities, or 3) large dollar category

parts. Examples of these type of items are Satellite Dishes, A/C and Heating Units, Appliances,

TV’s, Specialty Leathers, Hardware, or Flooring, etc. These items represent the high dollar

amounts that are causing the issues in expenses. Tracking will not be recorded or standard items

like nuts, bolts, framing, wiring, insulation, etc. It is not practical or efficient to track these common

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 16

items. Costs for common items are assigned in accounting by adding a predetermined standard

cost/cubic foot of the unit that is being produced.

The new QB module for Manufacturing includes an inventory management system that is

linked to the purchase order management system. As the purchasing department orders new items,

they are automatically added into inventory and set up to be received. The inventory management

system is equipped with a simple scanner that checks in the items and puts them into inventory.

The inventory cage has always been utilized for storage of parts; however, there was an open door

policy and no tracking for the items previously. The inventory cage is now monitored, and the

gate is locked. The employees will go to the cage and ask for the part they need, and the inventory

employee will now scan in the part and assign it to the unit that they are working in. No parts will

leave the cage without a unit assignment. This is a big change for the production floor, but is

necessary to reduce parts expenses.

At the end of each day of work, the supervisor submits a “percent completion, estimate of

completion, and issues list for every unit on the floor by unit position. New procedures will add

a checkpoint that ensures that managers review and resolve issues at the close of the daily

production shift. Any departments that have issues needing resolution, parts needed, delays, or

have not completed their labor assignments are reviewed and resolved before leaving the building

for the evening so that at 6:00 a.m. the following morning when the production staff clock in, they

have assignments that allow them to go straight to work without delay. This review process is

informal today, but must change to a formal end of day process going forward. The production

floor is currently scheduled to work 6:00 a.m. to 2:30 or 4:30 p.m. depending on the volume of

work on the floor. The department managers will meet at 4:45 p.m. daily to review all issues and

set assignments for the following day before leaving the building.

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 17

FINANCIALS

The accounting department will now have some of the much needed features at their

disposal in the new module of the Quickbooks System to allow them the determine where the

expenses are getting off track versus the Sales Contract costs. They are thrilled that this is now

possible, and determined that although it is a higher level of detail to manage and match, the

tracking will result in net savings in their own time as well as expense savings for the company.

The reporting that is included in the QB module allows an easy comparison of the purchases versus

the inventory versus the units produced, in detail for all items by category.

The new modules, along with the information gathered from the new business processes in

the marketing department and on the production floor, will quickly allow the management and the

department heads the ability to drill down further into month end closing to identify what happened

to cause each unit to be over on expenses. It is highly probable that a good portion of the waste

and theft will be reduced just with the implementation of the system. Every employee will know

that as they check out a part from inventory, it will be assigned to their name and the unit they are

working on. The process will no longer allow any employee to pull from inventory without being

tracked to their ID, including Supervisors and Managers. In addition, all parts checked out for a

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 18

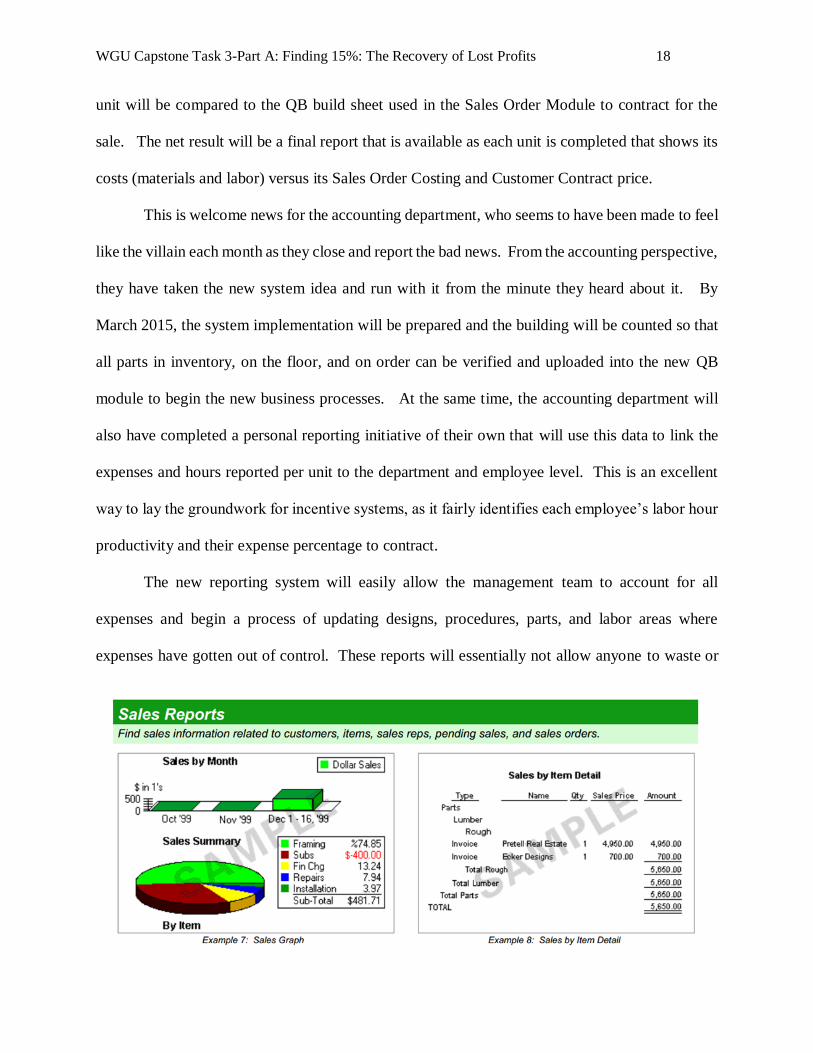

unit will be compared to the QB build sheet used in the Sales Order Module to contract for the

sale. The net result will be a final report that is available as each unit is completed that shows its

costs (materials and labor) versus its Sales Order Costing and Customer Contract price.

This is welcome news for the accounting department, who seems to have been made to feel

like the villain each month as they close and report the bad news. From the accounting perspective,

they have taken the new system idea and run with it from the minute they heard about it. By

March 2015, the system implementation will be prepared and the building will be counted so that

all parts in inventory, on the floor, and on order can be verified and uploaded into the new QB

module to begin the new business processes. At the same time, the accounting department will

also have completed a personal reporting initiative of their own that will use this data to link the

expenses and hours reported per unit to the department and employee level. This is an excellent

way to lay the groundwork for incentive systems, as it fairly identifies each employee’s labor hour

productivity and their expense percentage to contract.

The new reporting system will easily allow the management team to account for all

expenses and begin a process of updating designs, procedures, parts, and labor areas where

expenses have gotten out of control. These reports will essentially not allow anyone to waste or

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 19

steal parts, or run around the shop without accountability for their hours of labor. For the

accounting area, they can now easily explain what is causing expense increases, which relieves

their stress and allows them to do their job, financial accounting. Once all initial data and system

verifications have been completed and the QB Premier Product is scheduled to be implemented,

the Operations Manager and Accounting Lead will prepare all data and set the upgrade schedule

for QB to coincide with the first day of the month following the month-end closing for Quarter 1,

on March 31, 2015. This will give the company a good “End-of-Quarter” transition for

comparison, and will be much easier to identify and explain with all bankers, vendors, customers,

and dealers that will also have to be updated to introduce the new processes for the marketing,

sales, inventory management, and purchase order processes.

The accounting department is the official “keeper” of all Sales Contracts, and will remain

as so. Since it is common for Sales Contracts to be altered through Change Orders while in pre-

production and sometimes production if it cannot be helped, the accounting lead is the owner of

the Sales Contract and all associated Change Orders, thus the only person that is 100% aware of

the final net cost of the unit as the Customer takes delivery. Therefore, accounting lead will be

the only person (except the owner) in the building that has the authority and training to accept the

Customer’s receipt of payment and verify the funds deposited to be able to sign-off on the release

of a unit to the customer for delivery. This will close the expense cycle, ensure accountability for

all employees, and is estimated to, without even the

effort of added benefits in collaboration with this

new data, improve the materials and labor line by

15% within the year.

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 20

Implementation

The review and analysis for this project included documentation of the following:

1. Interviews with Management and Employees

2. Profitability / Financial Review 3. Current Operational and Paper Flow Processes

4. Layout / Physical Plant Review

5. Time Studies – General & Production

6. Observations from Tour/Walkthrough 7. Recommendations going forward

8. Quantified Expected Results

The implementation of the project to correct expense issues found will include the

Upgrade of the QB System, the revision of business and paperwork procedures in marketing,

production, and accounting, and the shift in management to have all departments report to the

Operations Manager. The Operations Manager is responsible for the reduction of the expense

issues and the profitability of the company, and will utilize and manage all departments in

accordance with reaching this goal.

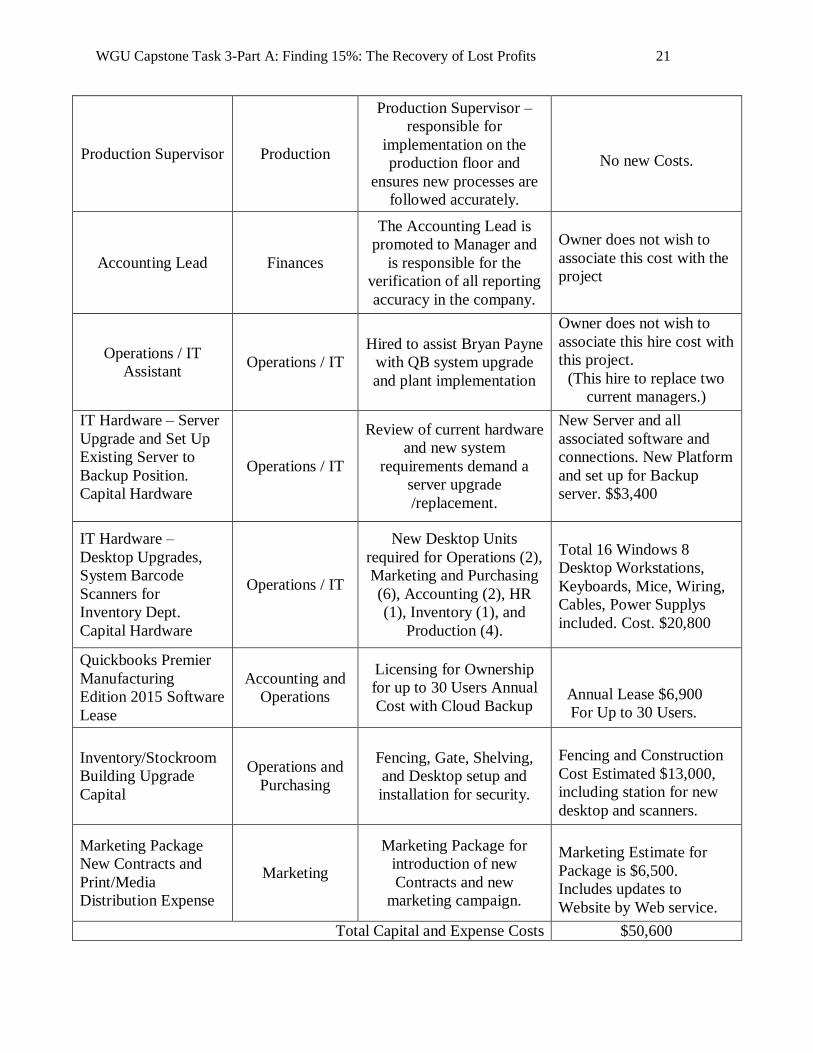

The resources below are required to complete the implementation of the QB Systems Upgrade:

Resource (people,

capital, equipment)

Functional

Area

Additional Details Costs

Owner All

Owner is official person

behind the project, and

wishes to be keep up to

date on progress and

recommendations.

None.

Operations Manager Finance

The Operations Manager is

new hire, placed in the

position to resolve the

expense problem. He is

primary contact through

and will then implement.

Owner does not wish to

associate this hire cost with

this project.

(This hire to replace two

current managers.)

Marketing Manager

Marketing/Sales

Marketing Manager –

Responsible for training

and implementation in

marketing and purchasing,

revision of sales processes.

No new Costs.

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 21

Production Supervisor

Production

Production Supervisor –

responsible for

implementation on the

production floor and

ensures new processes are

followed accurately.

No new Costs.

Accounting Lead

Finances

The Accounting Lead is

promoted to Manager and

is responsible for the

verification of all reporting

accuracy in the company.

Owner does not wish to

associate this cost with the

project

Operations / IT

Assistant

Operations / IT

Hired to assist Bryan Payne

with QB system upgrade

and plant implementation

Owner does not wish to

associate this hire cost with

this project.

(This hire to replace two

current managers.)

IT Hardware – Server

Upgrade and Set Up

Existing Server to

Backup Position.

Capital Hardware

Operations / IT

Review of current hardware

and new system

requirements demand a

server upgrade

/replacement.

New Server and all

associated software and

connections. New Platform

and set up for Backup

server. $$3,400

IT Hardware –

Desktop Upgrades,

System Barcode

Scanners for

Inventory Dept.

Capital Hardware

Operations / IT

New Desktop Units

required for Operations (2),

Marketing and Purchasing

(6), Accounting (2), HR

(1), Inventory (1), and

Production (4).

Total 16 Windows 8

Desktop Workstations,

Keyboards, Mice, Wiring,

Cables, Power Supplys

included. Cost. $20,800

Quickbooks Premier

Manufacturing

Edition 2015 Software

Lease

Accounting and

Operations

Licensing for Ownership

for up to 30 Users Annual

Cost with Cloud Backup

Annual Lease $6,900

For Up to 30 Users.

Inventory/Stockroom

Building Upgrade

Capital

Operations and

Purchasing

Fencing, Gate, Shelving,

and Desktop setup and

installation for security.

Fencing and Construction

Cost Estimated $13,000,

including station for new

desktop and scanners.

Marketing Package

New Contracts and

Print/Media

Distribution Expense

Marketing

Marketing Package for

introduction of new

Contracts and new

marketing campaign.

Marketing Estimate for

Package is $6,500.

Includes updates to

Website by Web service.

Total Capital and Expense Costs $50,600

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 22

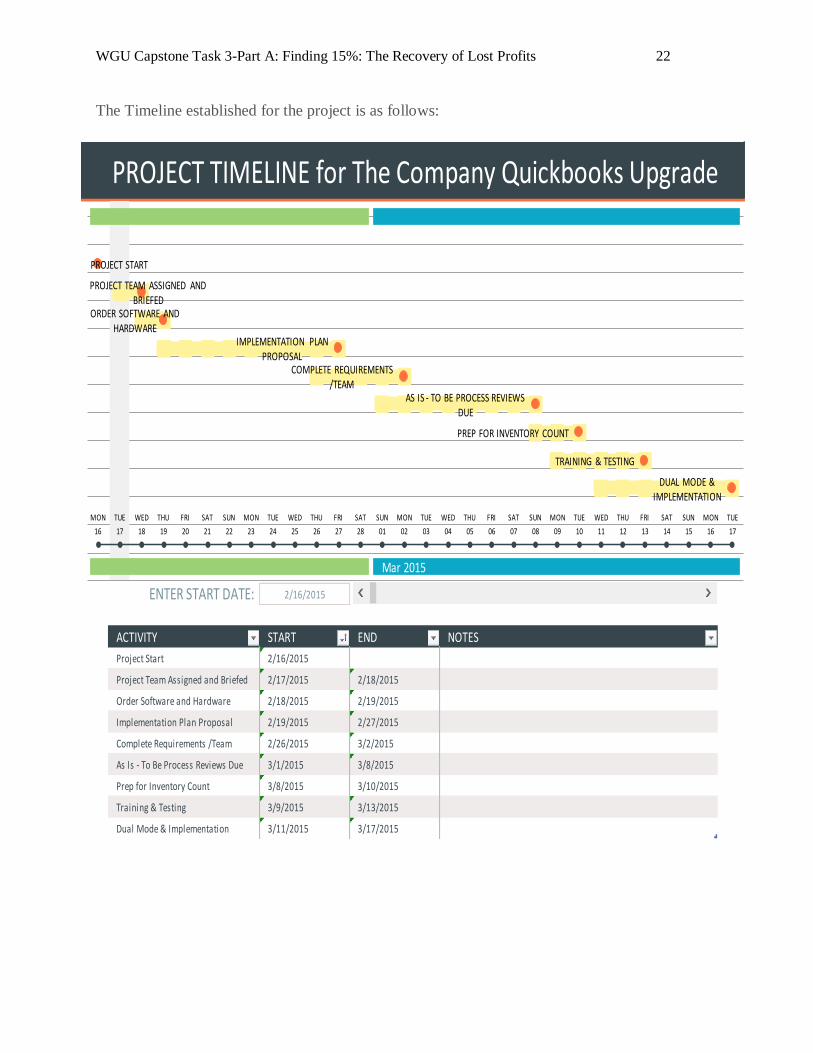

The Timeline established for the project is as follows:

PROJECT TIMELINE for The Company Quickbooks Upgrade

ENTER START DATE: 2/16/2015

ACTIVITY START END NOTES

Project Start 2/16/2015

Project Team Assigned and Briefed 2/17/2015 2/18/2015

Order Software and Hardware 2/18/2015 2/19/2015

Implementation Plan Proposal 2/19/2015 2/27/2015

Complete Requirements /Team 2/26/2015 3/2/2015

As Is - To Be Process Reviews Due 3/1/2015 3/8/2015

Prep for Inventory Count 3/8/2015 3/10/2015

Training & Testing 3/9/2015 3/13/2015

Dual Mode & Implementation 3/11/2015 3/17/2015

PROJECT START

PROJECT TEAM ASSIGNED AND BRIEFED

ORDER SOFTWARE AND HARDWARE

IMPLEMENTATION PLAN PROPOSAL

COMPLETE REQUIREMENTS /TEAM

AS IS - TO BE PROCESS REVIEWS DUE

PREP FOR INVENTORY COUNT

TRAINING & TESTING

DUAL MODE & IMPLEMENTATION

Mar 2015

16 17 18 19 20 21 22 23 24 25 26 27 28 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

MON TUE WED THU FRI SAT SUN MON TUE WED THU FRI SAT SUN MON TUE WED THU FRI SAT SUN MON TUE WED THU FRI SAT SUN MON TUE

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 23

Financial and Organizational Impact

Financial Impact

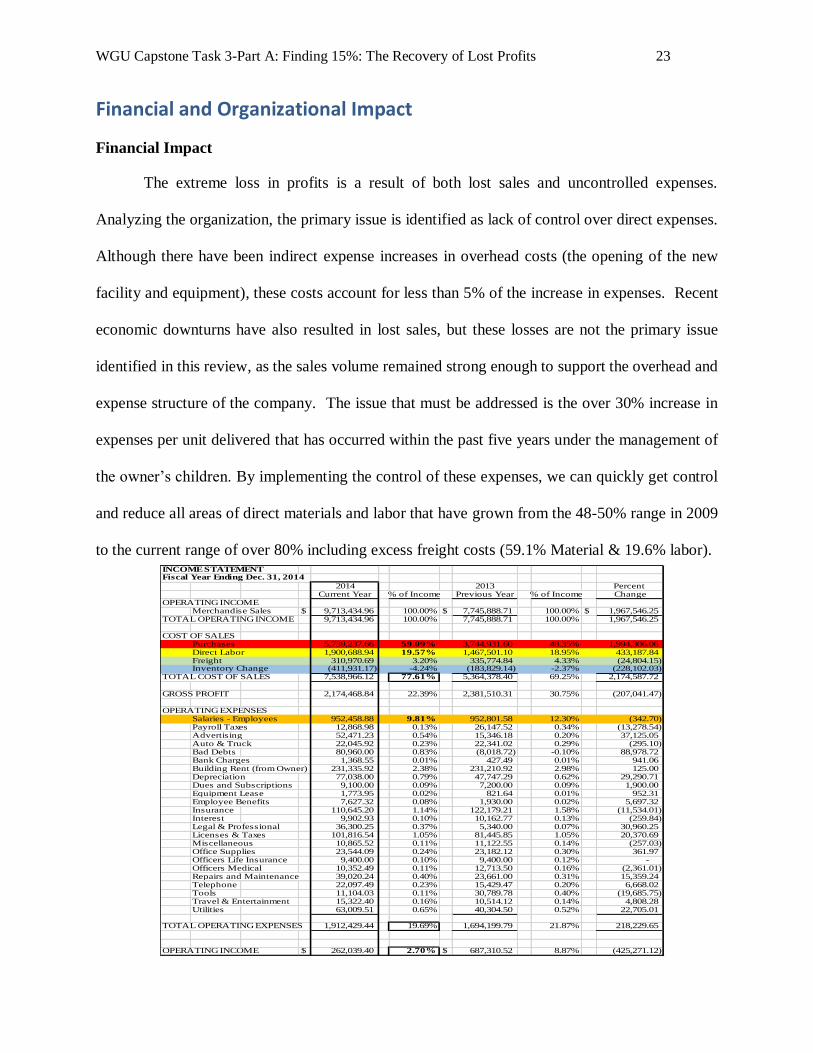

The extreme loss in profits is a result of both lost sales and uncontrolled expenses.

Analyzing the organization, the primary issue is identified as lack of control over direct expenses.

Although there have been indirect expense increases in overhead costs (the opening of the new

facility and equipment), these costs account for less than 5% of the increase in expenses. Recent

economic downturns have also resulted in lost sales, but these losses are not the primary issue

identified in this review, as the sales volume remained strong enough to support the overhead and

expense structure of the company. The issue that must be addressed is the over 30% increase in

expenses per unit delivered that has occurred within the past five years under the management of

the owner’s children. By implementing the control of these expenses, we can quickly get control

and reduce all areas of direct materials and labor that have grown from the 48-50% range in 2009

to the current range of over 80% including excess freight costs (59.1% Material & 19.6% labor). INCOME STATEMENTFiscal Year Ending Dec. 31, 2014

2014 2013 Percent Current Year % of Income Previous Year % of Income Change

OPERATING INCOMEMerchandise Sales $ 9,713,434.96 100.00% $ 7,745,888.71 100.00% $ 1,967,546.25

TOTAL OPERATING INCOME 9,713,434.96 100.00% 7,745,888.71 100.00% 1,967,546.25

COST OF SALESPurchases 5,739,237.66 59.09% 3,744,931.60 48.35% 1,994,306.06 Direct Labor 1,900,688.94 19.57% 1,467,501.10 18.95% 433,187.84 Freight 310,970.69 3.20% 335,774.84 4.33% (24,804.15) Inventory Change (411,931.17) -4.24% (183,829.14) -2.37% (228,102.03)

TOTAL COST OF SALES 7,538,966.12 77.61% 5,364,378.40 69.25% 2,174,587.72

GROSS PROFIT 2,174,468.84 22.39% 2,381,510.31 30.75% (207,041.47)

OPERATING EXPENSESSalaries - Employees 952,458.88 9.81% 952,801.58 12.30% (342.70) Payroll Taxes 12,868.98 0.13% 26,147.52 0.34% (13,278.54) Advertising 52,471.23 0.54% 15,346.18 0.20% 37,125.05 Auto & Truck 22,045.92 0.23% 22,341.02 0.29% (295.10) Bad Debts 80,960.00 0.83% (8,018.72) -0.10% 88,978.72 Bank Charges 1,368.55 0.01% 427.49 0.01% 941.06 Building Rent (from Owner) 231,335.92 2.38% 231,210.92 2.98% 125.00 Depreciation 77,038.00 0.79% 47,747.29 0.62% 29,290.71 Dues and Subscriptions 9,100.00 0.09% 7,200.00 0.09% 1,900.00 Equipment Lease 1,773.95 0.02% 821.64 0.01% 952.31 Employee Benefits 7,627.32 0.08% 1,930.00 0.02% 5,697.32 Insurance 110,645.20 1.14% 122,179.21 1.58% (11,534.01) Interest 9,902.93 0.10% 10,162.77 0.13% (259.84) Legal & Professional 36,300.25 0.37% 5,340.00 0.07% 30,960.25 Licenses & Taxes 101,816.54 1.05% 81,445.85 1.05% 20,370.69 Miscellaneous 10,865.52 0.11% 11,122.55 0.14% (257.03) Office Supplies 23,544.09 0.24% 23,182.12 0.30% 361.97 Officers Life Insurance 9,400.00 0.10% 9,400.00 0.12% - Officers Medical 10,352.49 0.11% 12,713.50 0.16% (2,361.01) Repairs and Maintenance 39,020.24 0.40% 23,661.00 0.31% 15,359.24 Telephone 22,097.49 0.23% 15,429.47 0.20% 6,668.02 Tools 11,104.03 0.11% 30,789.78 0.40% (19,685.75) Travel & Entertainment 15,322.40 0.16% 10,514.12 0.14% 4,808.28 Utilities 63,009.51 0.65% 40,304.50 0.52% 22,705.01

TOTAL OPERATING EXPENSES 1,912,429.44 19.69% 1,694,199.79 21.87% 218,229.65

$ 262,039.40 2.70% $ 687,310.52 8.87% (425,271.12) OPERATING INCOME

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 24

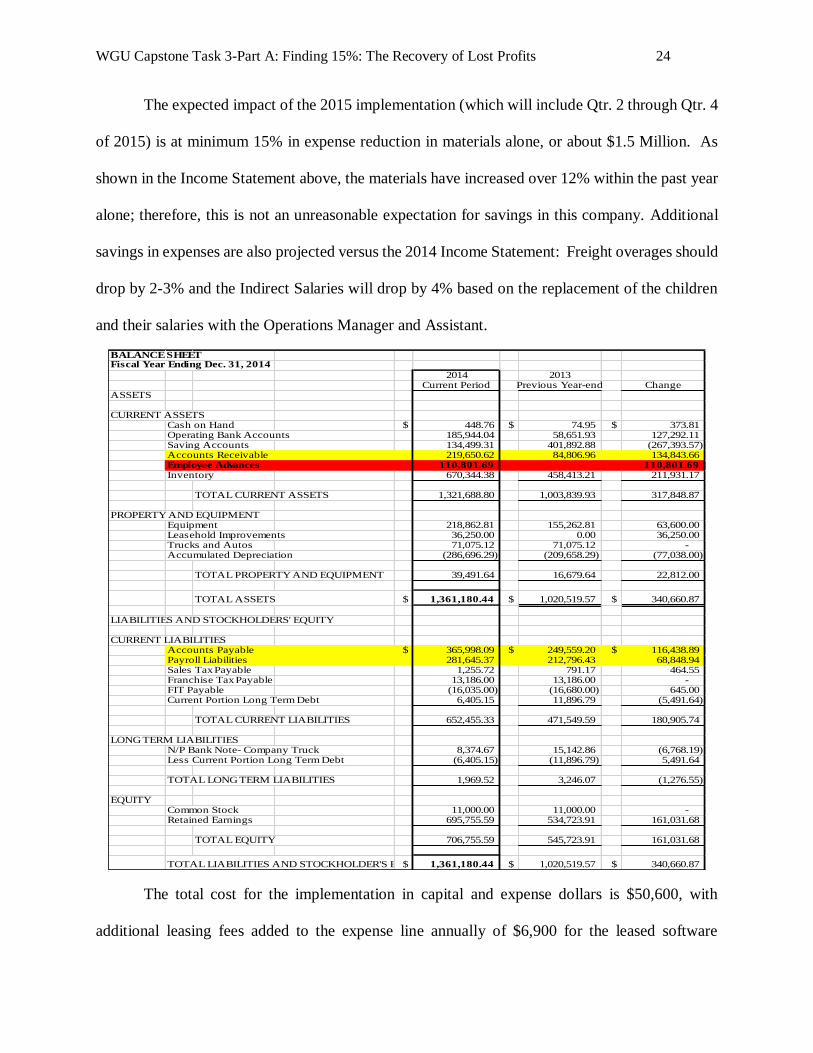

The expected impact of the 2015 implementation (which will include Qtr. 2 through Qtr. 4

of 2015) is at minimum 15% in expense reduction in materials alone, or about $1.5 Million. As

shown in the Income Statement above, the materials have increased over 12% within the past year

alone; therefore, this is not an unreasonable expectation for savings in this company. Additional

savings in expenses are also projected versus the 2014 Income Statement: Freight overages should

drop by 2-3% and the Indirect Salaries will drop by 4% based on the replacement of the children

and their salaries with the Operations Manager and Assistant.

The total cost for the implementation in capital and expense dollars is $50,600, with

additional leasing fees added to the expense line annually of $6,900 for the leased software

BALANCE SHEET

2014 2013Current Period Previous Year-end Change

ASSETS

CURRENT ASSETSCash on Hand $ 448.76 $ 74.95 $ 373.81Operating Bank Accounts 185,944.04 58,651.93 127,292.11Saving Accounts 134,499.31 401,892.88 (267,393.57)Accounts Receivable 219,650.62 84,806.96 134,843.66Employee Advances 110,801.69 - 110,801.69Inventory 670,344.38 458,413.21 211,931.17

TOTAL CURRENT ASSETS 1,321,688.80 1,003,839.93 317,848.87

PROPERTY AND EQUIPMENTEquipment 218,862.81 155,262.81 63,600.00 Leasehold Improvements 36,250.00 0.00 36,250.00 Trucks and Autos 71,075.12 71,075.12 - Accumulated Depreciation (286,696.29) (209,658.29) (77,038.00)

TOTAL PROPERTY AND EQUIPMENT 39,491.64 16,679.64 22,812.00

TOTAL ASSETS $ 1,361,180.44 $ 1,020,519.57 $ 340,660.87

LIABILITIES AND STOCKHOLDERS' EQUITY

CURRENT LIABILITIESAccounts Payable $ 365,998.09 $ 249,559.20 $ 116,438.89 Payroll Liabilities 281,645.37 212,796.43 68,848.94 Sales Tax Payable 1,255.72 791.17 464.55 Franchise Tax Payable 13,186.00 13,186.00 - FIT Payable (16,035.00) (16,680.00) 645.00 Current Portion Long Term Debt 6,405.15 11,896.79 (5,491.64)

TOTAL CURRENT LIABILITIES 652,455.33 471,549.59 180,905.74

LONG TERM LIABILITIESN/P Bank Note- Company Truck 8,374.67 15,142.86 (6,768.19) Less Current Portion Long Term Debt (6,405.15) (11,896.79) 5,491.64 TOTAL LONG TERM LIABILITIES 1,969.52 3,246.07 (1,276.55)

EQUITYCommon Stock 11,000.00 11,000.00 - Retained Earnings 695,755.59 534,723.91 161,031.68

TOTAL EQUITY 706,755.59 545,723.91 161,031.68

TOTAL LIABILITIES AND STOCKHOLDER'S EQUITY$ 1,361,180.44 $ 1,020,519.57 $ 340,660.87

Fiscal Year Ending Dec. 31, 2014

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 25

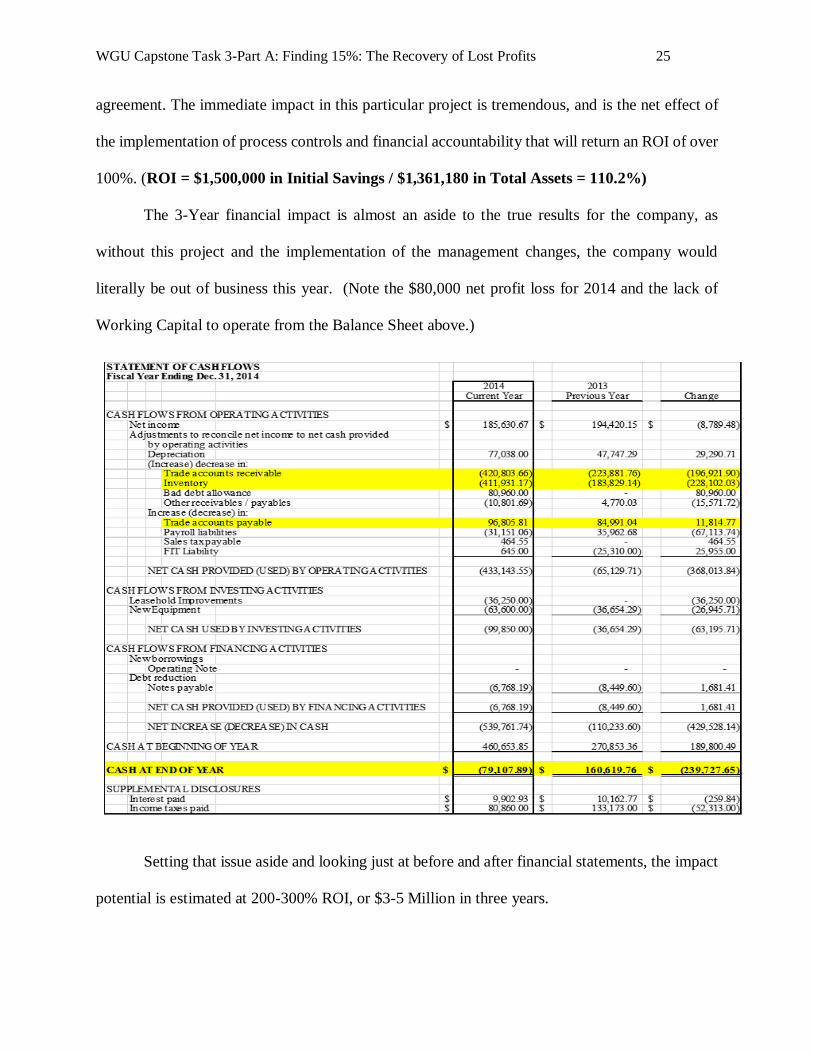

agreement. The immediate impact in this particular project is tremendous, and is the net effect of

the implementation of process controls and financial accountability that will return an ROI of over

100%. (ROI = $1,500,000 in Initial Savings / $1,361,180 in Total Assets = 110.2%)

The 3-Year financial impact is almost an aside to the true results for the company, as

without this project and the implementation of the management changes, the company would

literally be out of business this year. (Note the $80,000 net profit loss for 2014 and the lack of

Working Capital to operate from the Balance Sheet above.)

Setting that issue aside and looking just at before and after financial statements, the impact

potential is estimated at 200-300% ROI, or $3-5 Million in three years.

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 26

This company is in one of those situations that reads as incredible, yet happens every day

in small businesses and family run companies. As the Cash Flow Statement identifies, the savings

will not even stop there. The negative assets shown in Trade Accounts Receivable and Inventory

Adjustments are also areas that can (and must be) corrected under the watch of the new Operations

Manager. These items identify that the previous managers are unwilling or unable to collect the

receivables from Vendors, Customers, or Partners, and also have lost or misused almost half a

million in inventory parts in 2014, creating the year end cash flow issue that caused the Owner to

seek out help in the form of this project.

Organizational Impact

Although not the outcome wished for, the Owner has expressed that he was aware of the

issues and saw all of the signs leading up to these issues over the past five years. Shocked by the

extremes, he expressed no hesitation when replacing the children after reviewing the facts and

verifying what was necessary to repair the company. However disappointing, the Owner was

willing to save the company and the employees, and to do the right thing. The Organization is

better for these decisions, and will do well going forward based on all indicators. The employees

(and department managers) have expressed their extreme happiness at the replacement of the

children with competent and visionary management. The structure and the demeanor of the

organization has completely turned around because of these decisions. The company

structure has changed from a privately owned workshop mentality to a solid organizational

hierarchy with the competence of a public company.

This company could have been one like many other small businesses that close every day

in the US. As referenced in the book “Beating the Midas Curse” written by Attorneys and Estate

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 27

Planning Experts Rob Zeeb and Perry Cochell, “studies that show 65% of second-generation

family businesses fail and a mind-boggling 90% of third-generation businesses fail!”

(Cochell and Zeeb, 2005) The top three reason that these businesses fail all include references to

following generations that 1) are unwilling, 2) are incapable, or 3) have not been trained to take

over the business by the first generation owner. The net result in any of these cases is the lack

of appropriate succession planning for an organization. This company has experienced this

exact situation. In this case, however, the Owner must be commended for his dedication and

determination to his employees, as the choices made were indeed difficult ones for any parent.

Because of these decisions, the company will now learn how to be successful as a profitable

organization in an industry that is growing extremely fast.

Images courtesy RVIA, 2015

WGU Capstone Task 3-Part A: Finding 15%: The Recovery of Lost Profits 28

Reference List

Cochell, P. L., & Zeeb, R. C. (2005). Beating the Midas cur$e. West Linn, OR: Heritage

Institute Press.

Kreitner, Kinicki, R., & Angelo. (2009). Organizational Behavior, 9th Edition. Retrieved from

http://online.vitalsource.com/books/0077771788/id/T6-2

Quickbooks, Inc. (2015). Inventory Management System - QuickBooks Enterprise. Retrieved

from http://enterprisesuite.intuit.com/products/advanced-inventory/

Project Management Institute. (2015). Project Management | Managing Small Projects; The

Critical Steps. Retrieved from http://www.projecttimes.com/articles/managing-small-

projects-the-critical-steps.html

RVIA. (2014, September). The Recreation Vehicle Industry Association: Historical Glance.

Retrieved from http://www.rvia.org/?ESID=histglance

Related Documents