ACCOUNTING FOR DECISION-MAKING STUDY GUIDE PROGRAMME : MBA Final Year CREDIT POINTS : 20 points NOTIONAL LEARNING: 200 hours over 1 semester TUTOR SUPPORT : [email protected] Copyright © 2014 MANAGEMENT COLLEGE OF SOUTHERN AFRICA All rights reserved; no part of this book may be reproduced in any form or by any means, including photocopying machines, without the written permission of the publisher REF: ACCDM 2014

MBA 2 Accounting for Decision Making Jan 2014

Dec 27, 2015

Mancosa reading text

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ACCOUNTING FOR

DECISION-MAKING

STUDY GUIDE

PROGRAMME : MBA Final Year

CREDIT POINTS : 20 points

NOTIONAL LEARNING: 200 hours over 1 semester

TUTOR SUPPORT : [email protected]

Copyright © 2014

MANAGEMENT COLLEGE OF SOUTHERN AFRICA

All rights reserved; no part of this book may be reproduced in any form or by any means, including

photocopying machines, without the written permission of the publisher

REF: ACCDM 2014

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 1

MODULE CONTENTS: ACCOUNTING FOR DECISION-MAKING

TOPIC

NUMBER

TOPIC

PAGE(S)

Readings

3

1

Accounting information and managerial decisions

5

2

Financial statements and accounting concepts

17

3

Accounting for and presentation of assets, liabilities and owners’ equity

40

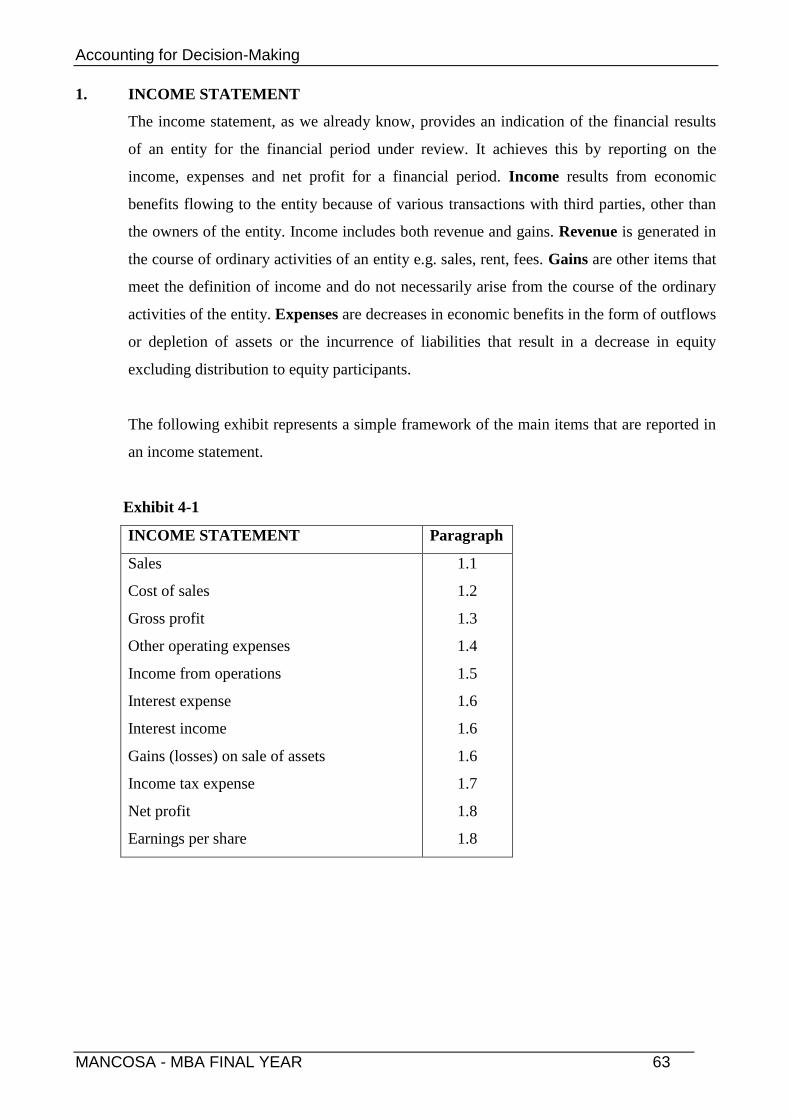

4

Income statement and cash flows

61

5

Financial Analysis

82

6

Cost-volume-profit (CVP) relationships

125

7

Cost analysis for planning, control and decision-making

153

8

Transfer pricing for decentralised enterprises

183

9

Corporate governance

193

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 2

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 3

READINGS

Prescribed

Marshall D.H., Mcmanus W.W. and Viele D.F. (2011) Accounting: What the numbers mean,

9th

Edition, McGraw-Hill: New York

Recommended

The following books are highly recommended for further reading.

The books that are recommended for each topic are indicated at the start of the topic.

Atrill P and Mc Laney E (2002) Management Accounting for Non-specialists, Third edition,

Pearson Education Limited: Essex

Berry A. and Jarvis R. (2006) Accounting in a business context, Fourth edition, Thomson

Learning: London (Chapter 3)

Davies T. and Pain B. (2002) Business Accounting and Finance, First Edition, McGraw-Hill:

UK

Drury C. (2005) Management Accounting for Business, Third edition, Thomson Learning:

London

Gowthorpe C. (2005) Business Accounting and Finance for non-specialists, Second edition,

Thomson Learning: London

Hand L., Isaaks C. and Sanderson P (2005) Introduction to Accounting for Non-Specialists,

First edition, Thomson Learning: London

Ingram R.W., Albright T.L., Baldwin B.A. and Hill J.W. (2005) Accounting: Information for

Decisions, Third edition, Thomson South-Western: Canada

Jackson S. and Sawyers R (2006) Management Accounting, International Student Edition,

Thomson South-Western: Singapore

Lubbe I. and Watson A. (2006) Accounting: GAAP Principles, First edition, Oxford

University Press Southern Africa: Cape Town

Niemand A.A., Meyer L., Botes V.L. and van Vuuren S.J. (2004) Fundamentals of Cost and

Management Accounting, Fifth edition, LexisNexis Butterworths: Durban

Warren C.S. (2007) Survey of Accounting, Third edition, Thomson South Western: USA

Wood F. and Sangster A. (2005) Business Accounting, Tenth edition, Prentice Hall: China

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 4

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 5

TOPIC 1

ACCOUNTING INFORMATION AND MANAGERIAL DECISIONS

LEARNING OUTCOMES

Students should be able to:

► identify the wide range of users of financial information.

► describe the uses of financial information.

► compare and contrast management accounting and financial accounting.

► distinguish between the information needs of external and internal users.

► explain the significance of internal auditing.

► describe the role of the management accountant.

► apply a basic decision-making model.

► recognise the risk in decision-making.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 6

CONTENTS

1. Introduction

2. Accounting information and managerial decisions

3. Internal auditing

4. The role of the management accountant

5. A basic decision-making model

6. Role of risk in decision-making

7. Self-assessment activities and solutions

READING

Prescribed

Marshall D.H., Mcmanus W.W. and Viele D.F. (2011) Accounting: What the numbers mean,

9th

Edition, McGraw-Hill: New York. (Chapter 1)

Recommended

Davies T. and Pain B. (2002) Business Accounting and Finance, First Edition, McGraw-Hill:

UK (Chapters 1 and 2)

Jackson S. and Sawyers R (2006) Management Accounting, International Student Edition,

Thomson South-Western: Singapore. (Chapter 1)

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 7

1. INTRODUCTION

The original purpose of accounting was to record transactions and present financial

statements. However, accounting has evolved and the American Accounting

Association sees accounting as “the process of identifying, measuring and

communicating economic information to permit judgements and decisions by users of

information”. A major focus of accounting now is the input that it provides for

decision-making.

2.

ACCOUNTING INFORMATION AND MANAGERIAL DECISIONS

All organisations – large or small; manufacturing, retail or service; profit or non-

profit – have a need for accounting information. The primary role of accounting is

to provide useful information for the decision-making needs of financiers (investors,

lenders, owners), managers and others both inside and outside the organisation.

Accounting is link between business activities and business decisions. Ingram et al

(2005: 59) uses the following model to describe the link:

Exhibit 1-1

Business

Activities

Operating

Investing

Financing

Accounting

Measuring

Recording

Reporting

Analysing

Business

Decisions

Actions Based on Business Decisions

Business environments have changed dramatically. Companies of all sizes now

compete in a dynamic global marketplace. Clients demand specialised products and

services and information relating to product availability, order status and delivery

times. Suppliers require information on their clients’ sales and stock levels in order

to tailor their production schedules and delivery times. Shareholders demand greater

returns and capital gains from their investments.

All these changes necessitate more effective management of knowledge within an

organisation. Organisations generate great volumes of data. Data becomes

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 8

information when it is organised, processed and summarised. Information becomes

knowledge when it is shared and exploited to add value to an organisation.

Accounting information includes both financial and non-financial information used

by decision-makers. Jackson and Sawyers (2006: 5) portray a contemporary view of

accounting information as follows:

Exhibit 1-2

Accounting information

Traditional Financial

Accounting

Information

Non-financial

Information

Financial

information

▪ Balance sheet

▪ Income statement

▪ Cost of goods

manufactured

▪ Gross profit

▪ Operating expenses

Other quantitative

information

▪ Percentage of defects

▪ Number of customer

complaints

▪ Warranty claims

▪ Units in inventory

▪ Budgeted hours

Qualitative

information

▪ Customer satisfaction

▪ Employee satisfaction

▪ Product or service quality

▪ Reputation

The responsibilities of accountants within an organisation tend to be split between the

main functions of financial accounting and management accounting. Financial

accounting is the area of accounting that is primarily concerned with the preparation

of general use financial statements for use by creditors, investors and other users

outside the business (external users). Management accounting, on the other hand, is

primarily concerned with generating financial and non-financial information for use

by managers in their decision-making roles within the organisation (internal users).

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 9

? THINK POINT

What are the information needs of external users?

The major differences between financial and management may be tabulated as

follows:

Management accounting Financial accounting

User groups Internal users: Managers External: Owner(s); Lenders,

Creditors; Investors

Nature of reports Reports tend to be specific usually

with some decision in mind.

Reports tend to be general-purpose

useful to a wide range of users.

Legal

requirements

Management accounting reports

are not required by law since they

are for internal use only.

Financial reports are required by law

and are also regulated in terms of

content and format.

GAAP Management accounting reports

are not subject to the practices and

principles of GAAP (Generally

Accepted Accounting Practice).

Financial reports must conform to

the practices and principles set by

GAAP.

Time focus The emphasis is on the future but

also provides information on past

performance.

It reflects on the financial result and

financial position for the past period.

Nature of

information

Information used may be less

objective and verifiable.

Objective and verifiable information

is needed to prepare reports.

Frequency of

reporting

Reports are produced as often as

required by managers even on a

weekly basis.

Reports are produced annually

although some businesses prepare

half-yearly or even quarterly reports.

Focus on the

whole or parts of

the business

Focuses on parts of the business

e.g. a certain department as well

as the business as a whole.

Focuses on the performance of the

business as a whole.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 10

●

●

●

●

The information needs of external users (refer to think point above) may be

summarised as follows:

Investors have invested money in an enterprise. They require information on the

return on their investments and the financial position of the enterprise.

Creditors and lenders of money (e.g. banks) will be interested to know whether the

amounts owing to them will be paid on the due date.

Employees concern with accounting information has to do with job security,

employment opportunities and salary negotiations.

Government: Financial results are required by the government tax collection agency

to calculate the taxes payable to the government. Statistical analyses are also done by

the government to enable it to plan and draft policies.

●

The information needs of internal users (managers) may be summarised as

follows:

Information is needed to enable managers to make better and informed decisions.

Management requires a steady flow of information to respond to possible problems.

This information could be in the form of reports, spreadsheets, graphs etc. Managers

have to evaluate the information and make their decisions.

● Up-to-date accounting information is needed for effective planning. Planning relate

to the setting of goals or objectives and the formulation of policy.

● Information is also required for control purposes. It can help decision-makers to

determine that they are not where they want to be. The accounting information can

help them to determine what went wrong and what they might do get back on track.

3.

INTERNAL AUDITING

An annual audit of accounts is a legal requirement for public companies. According

to Davies and Pain (2002: 248) the main duty of external auditors is to report to

shareholders and others whether, in their opinion, the financial statements show a true

and fair view, and comply with statutory, regulatory and accounting standard

requirements. However, the report does not guarantee that the financial statements are

correct, that the organisation will not fail and that there has been no fraud. As a result

internal auditing became a necessity.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 11

According to the Institute for Internal Auditors (UK) internal audit “is an

independent appraisal function established within an organisation to examine and

evaluate its activities as a service to the organisation. The objective of internal

auditing is to assist members of the organisation in the effective discharge of their

responsibilities. To this end, internal auditing furnishes them with analyses,

appraisals, recommendations, counsel and information concerning the activities

reviewed.”

The internal auditors report to the audit committee of the company. The committee

should consist of members of the board of directors who are not part of the

organisation’s management.

4. THE ROLE OF THE MANAGEMENT ACCOUNTANT

As a consequence of the advances made in accounting information systems and the

automation of accounting functions, the role of the management accountant has

shifted from collecting data to analysing information and creating knowledge from

this information. The role of management accountants is to interpret information and

put it into a suitable format for other managers, thereby facilitating management

decision-making. The work of management accountants often involves close co-

ordination with the financial, production and marketing functions of an organisation.

5.

A BASIC DECISION-MAKING MODEL

Decision-making, a key element of management accounting, is a process of

identifying various courses of action (alternatives) and selecting the most appropriate

one. Jackson and Sawyers (2006: 13) suggest a four-step decision-making model that

allows one to approach complex decisions in an orderly manner. Although the model

may not guarantee that all decisions will be correct, it does increase the probability of

making a good decision. The model may be illustrated as follows in Exhibit 1-3:

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 12

Exhibit 1-3

TThhee DDeecciissiioonn––MMaakkiinngg mmooddeell

Step 4 Select the best option

Step 3 Identify and analyse available options

Step 2 Identify objectives

Step 1 Define the problem

Step 1: Define the problem

Defining the problem accurately is important as many decision-makers make bad

decisions through trying to solve the wrong problem. The input of managers of all the

functional areas is advised in order to get a clearer picture of the underlying problem.

For example, if the organisation is experiencing a problem with it’s control over

expenses, the co-operation of all functional mangers is essential in getting to the root

of the problem.

Step 2: Identify objectives

This step involves the identification of objectives in finding a solution to the problem.

The objectives may be quantitative (e.g. reduce expenses by 20 per cent) or

qualitative (train employees in cost reduction techniques) or a combination of both.

Step 3: Identify and analyse available options

The options available to attain the objectives must now be identified and analysed.

One must consider the relevant variables that affect the problem as well as alternative

courses of action. It is recommended that more than one option and multiple variables

be considered.

Step 4: Select the best option

The decision-maker must examine the extent to which each of the options will

achieve the objective(s). Decisions should be based on both quantitative and

qualitative information. It must be borne in mind that decisions are often made

against the backdrop of uncertainty and the element of risk is usually present. Once

the best option is selected, the decision is implemented and the results are evaluated.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 13

6.

ROLE OF RISK IN DECISION-MAKING

As mentioned above, most decisions involve risk. The attitude of the decision-maker

towards risk has a significant influence on the option that is chosen. Decision makers

who are risk seekers will rate alternatives differently from decision-makers who are

risk-averse. For example, risk-averse decision makers may rate more highly a

machine needed in production that is made by established manufacturers than one

made by a new company.

Another way of adjusting for risk is by taking into account the possibility that

certain events may occur. For example, in the choice of a machine, it is possible that

the price of the machine may increase before the decision to purchase is made.

The third way of considering risk is to establish the sensitivity of the decisions to

changes in the key variables that were considered during the analysis. For example,

the purchaser of the machine may not be totally sure of getting the best financing

options from all the manufacturers. The purchaser may now consider the cost of the

machine taking into account all possible financing options. If this adjustment changes

the decision, then the decision is sensitive to changes in that variable. If not, then the

decision is not sensitive to that variable.

7.

7.1

7.1.1

7.1.2

7.1.3

7.1.4

7.1.5

7.1.6

SELF-ASSESSMENT ACTIVITIES AND SOLUTIONS

Accounting information is used by individuals and organisations for a variety of

reasons. Identify the type of accounting information that may be of interest to each of

the following potential users:

Loan manager of a bank

Labour union representing employees

Production manager

Shareholders

Sales managers

President of the company

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 14

7.2

Financial and management accounting information serve different purposes.

State whether the following phrases describe management accounting or financial

accounting:

7.2.1

7.2.2

7.2.3

7.2.4

7.2.5

7.2.6

7.2.7

7.2.8

Must adhere to GAAP

Future orientation

Reports results by segments

Focus is on past performance

Emphasises reporting on the whole company

Information is often less precise

Highly customisable

Reports are produced as often as required

7.3

Why do you think that the internal auditors of a public company should report to the

audit committee and not to the finance director?

7.4

Your company wants to replace the existing office computer. After a lot of thought

and investigation, you are now seriously considering three options. The basic

information about each computer is as follows (Note the basic price includes the

central processing unit (CPU) with 80 gigabite (GB) hard drive, keyboard and

mouse):

Basic price

Processor speed

Monitor (17 inch)

CD or DVD writer

Speakers

Upgrade hard drive

Microsoft office package

Total price

Computer A

R4 800

2.8 Gigahertz

R800 (ordinary)

R200 (CD)

R200

R350 (120 GB)

R1 200

R7 550

Computer B

R5 200

3.0 Gigahertz

R850 (ordinary)

R450 (DVD)

R250

R400 (160 GB)

R1 400

R8 550

Computer C

R5 400

3.2 Gigahertz

R1 300 (LCD)

R400 (DVD)

R200

R520 (200 GB)

R1 350

R9 170

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 15

Required

7.4.1

7.4.2

7.4.3

7.4.4

Define the problem that may have led to the consideration of replacing the existing

office computer.

What are the objectives in choosing a computer? Identify both quantitative and

qualitative objectives. Which is the most important objective to you? Why?

Given the circumstances in your company, what are the available options in choosing

a new computer? Name the quantitative and qualitative factors affecting these

options.

From the options available, which is the best choice? Why?

SOLUTIONS

7.1

7.1.1

7.1.2

7.1.3

7.1.4

7.1.5

7.1.6

Loan manager of a bank

Labour union representing

employees

Production manager

Shareholders

Sales managers

President of the company

Some examples include:

Ability to service debt and repay capital

Ability to compensate employees; job security

Production costs; budgeted figures

Profitability; Earnings per share; Net asset

value

Sales forecasts; actual sales; selling expenses

Profitability; market share; share price

7.2

7.2.1

7.2.2

7.2.3

7.2.4

7.2.5

7.2.6

7.2.7

7.2.8

Must adhere to GAAP

Future orientation

Reports results by segments

Focus is on past performance

Emphasises reporting on the whole company

Information is often less precise

Highly customisable

Reports are produced as often as required

Financial accounting

Management accounting

Management accounting

Financial accounting

Financial accounting

Management accounting

Management accounting

Management accounting

7.3

The responsibility for the system of recording transactions rests with the finance

director. The finance director could prevent crucial information from being passed

on to others in the organisation. The audit committee meets on several occasions

during the year and it offers a degree of objectivity.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 16

7.4

7.4.1

7.4.2

7.4.3

7.4.4

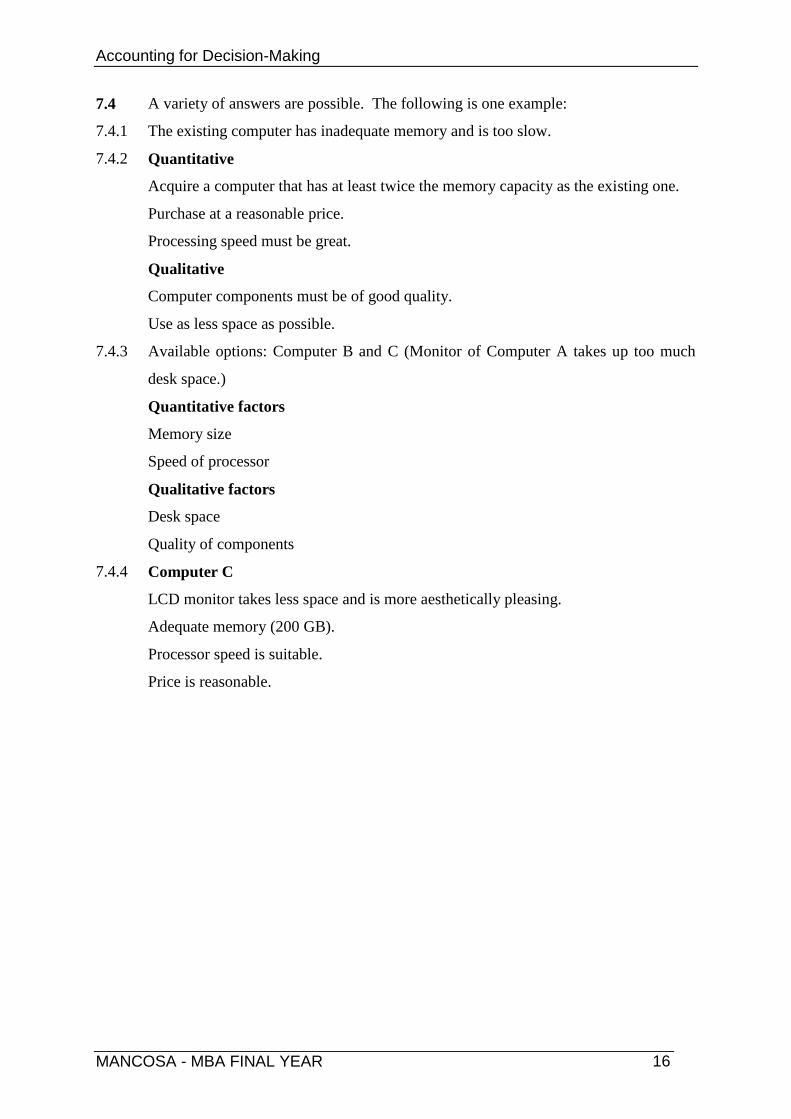

A variety of answers are possible. The following is one example:

The existing computer has inadequate memory and is too slow.

Quantitative

Acquire a computer that has at least twice the memory capacity as the existing one.

Purchase at a reasonable price.

Processing speed must be great.

Qualitative

Computer components must be of good quality.

Use as less space as possible.

Available options: Computer B and C (Monitor of Computer A takes up too much

desk space.)

Quantitative factors

Memory size

Speed of processor

Qualitative factors

Desk space

Quality of components

Computer C

LCD monitor takes less space and is more aesthetically pleasing.

Adequate memory (200 GB).

Processor speed is suitable.

Price is reasonable.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 17

TOPIC 2

FINANCIAL STATEMENTS AND ACCOUNTING CONCEPTS

LEARNING OUTCOMES

Students should be able to:

► explain what transactions are.

► describe the kind of information contained in financial statements.

► describe the integration of the financial statements.

► explain the purpose of financial statements.

► outline the main accounting concepts.

► outline the meaning and usefulness of the accounting equation.

► show the effects of transactions on the accounting equation and subsequently on the

financial statements.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 18

CONTENTS

1. What is a transaction?

2. Financial statements

3. Accounting concepts

4. Accounting equation

5. Self-assessment activities and solutions

READING

Prescribed

Marshall D.H., Mcmanus W.W. and Viele D.F. (2011) Accounting: What the numbers mean,

9th

Edition, McGraw-Hill: New York. (Chapters 2 and 4)

Recommended

Berry A. and Jarvis R. (2006) Accounting in a business context, Fourth edition, Thomson

Learning: London. (Chapter 3)

Davies T. and Pain B. (2002) Business Accounting and Finance, First Edition, McGraw-Hill:

UK (Chapters 1 – 4)

Ingram R.W., Albright T.L., Baldwin B.A. and Hill J.W. (2005) Accounting: Information for

Decisions, Third edition, Thomson South-Western: Canada. (Chapter F4)

Warren A.S. (2007) Survey of Accounting, Third Edition, Thomson South-Western: USA

(Chapter 1)

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 19

1. WHAT IS A TRANSACTION?

According to Warren (2007: 48) a transaction is an economic event that under

generally accepted accounting practice affects one or more elements of the financial

statements and must therefore be recorded. Transactions are initially recorded in

journals, then summarised in accounts in a ledger and the effects of them are later

reflected in the financial statements.

2.

FINANCIAL STATEMENTS

Financial statements report on the financial position of an organisation at a certain

point in time and the changes in the financial position over a period of time. The

financial statements and what they are intended to report on are illustrated below:

FINANCIAL STATEMENT REPORTS ON:

Balance sheet Financial position on a certain date.

Income statement Profit for a particular period.

Statement of changes in equity Investments by and distributions to owners.

Statement of cash flows Cash flows during the period.

The financial statements are usually accompanied by notes on the accounting policies

and detailed information about many of the amounts reflected in the financial

statements. The notes are intended to assist the reader of the statements by providing

additional information that is deemed necessary by the organisation and its auditors.

The kind of information contained in financial statements, financial statement

relationships and the purpose of financial statements are now discussed.

2.1

Balance sheet

The balance sheet reports on the financial position of an organisation at a specified

point in time. It is basically a summary of an organisation’s assets, equity and

liabilities at a point in time. This is in contrast to the income statement, statement of

cash flows and statement of changes in equity that report changes in the financial

position. The following is an example of a balance sheet in a simple form:

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 20

Exhibit 2-1

MVN ENTERPRISES

BALANCE SHEET AS AT 31 MARCH 20.6

ASSETS

Property, plant and equipment

Inventory (merchandise)

Accounts receivables

Cash

Total assets

EQUITY AND LIABILITIES

Equity

Liabilities

Non-current debt

Accounts payables

Total equity and liabilities

R

247 000

19 000

28 500

151 400

445 900

220 650

100 000

125 250

445 900

The two main sections of the balance sheet are:

* Assets

* Equity and liabilities

Notice that the amounts for these two sections are the same viz. R445 900.

This equality is also known as the accounting equation:

Assets = Equity + Liabilities

R445 900 = R220 650 + R225 250

The following are brief explanations of the items in the balance sheet:

Assets are the resources that are controlled by an enterprise from which economic

benefits will be derived either now or in the future.

Liabilities are claims on the assets of an organisation. Simply put, it refers to what

an organisation owes.

Equity or Owner’s equity may be viewed as the residual claim that the owner(s) has

on the assets of the organisation after all the liabilities have been settled. It normally

consists of two parts viz. that which is invested in the organisation and that which is

earned by the organisation and left in the organisation (i.e. retained profits).

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 21

Property, plant and equipment refer to non-current assets such as land, buildings,

vehicles, machines and equipment that have a useful life of more than one year.

Inventory refers to the merchandise that has been purchased but not yet sold.

Accounts receivable represents the amounts owing by customers for merchandise

sold to them on credit.

Cash represents cash on hand and cash kept at the bank.

Non-current debts are debts that are payable after more than one year from the

balance sheet date.

Accounts payable represents amounts owing to suppliers for merchandise purchased

on credit.

A major purpose of the balance sheet is to provide financial information to external

users. It is an important statement to creditors who require information about assets

and claims to these assets.

2.2

Income statement

The income statement reports on the profit (or loss) made by an organisation over a

certain period of time. It reflects the revenue generated through its operating

activities (e.g. sales) and then deducting the expenses incurred in generating that

revenue and operating the organisation. Losses and gains arising from non-operating

activities are also reported.

The following is a simplified format of an income statement:

Exhibit 2-2

MVN ENTERPRISES

INCOME STATEMENT FOR THE YEAR ENDED 31 MARCH 20.6

R

Sales 300 000

Cost of sales (200 000)

Gross profit 100 000

Selling, general and administrative expenses (54 950)

Operating profit/Income from operations 45 050

Interest expense (15 000)

Net profit 30 050

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 22

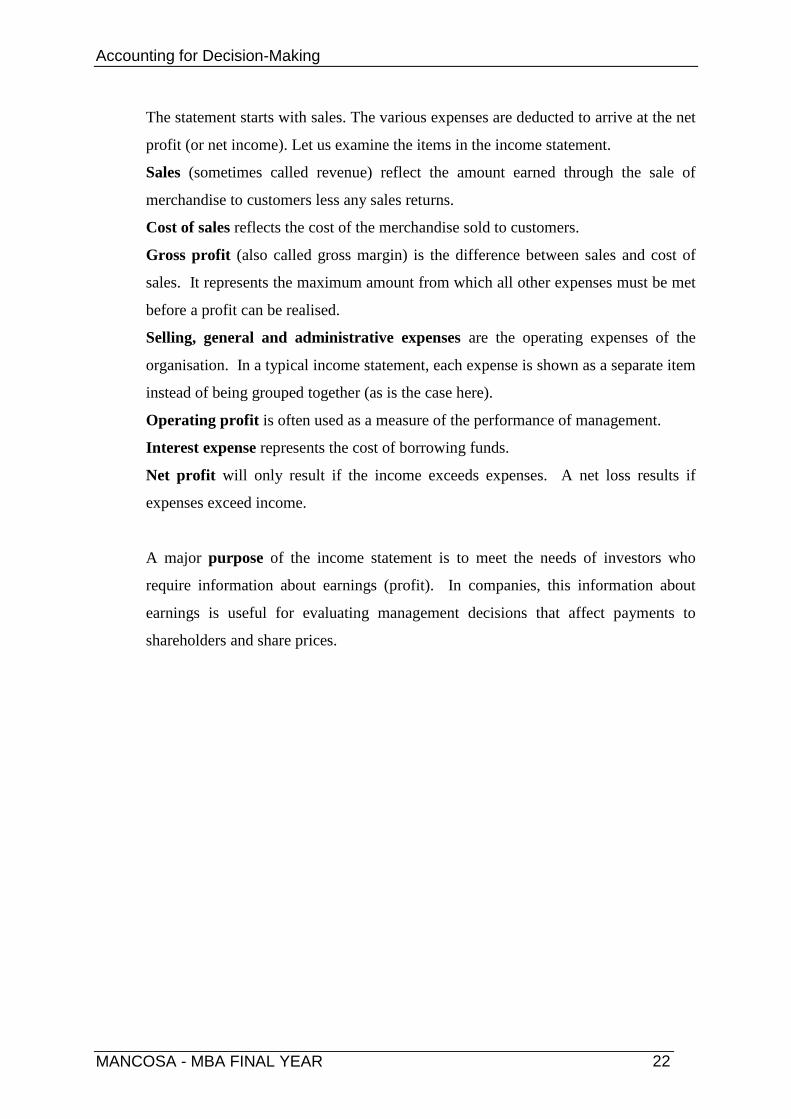

The statement starts with sales. The various expenses are deducted to arrive at the net

profit (or net income). Let us examine the items in the income statement.

Sales (sometimes called revenue) reflect the amount earned through the sale of

merchandise to customers less any sales returns.

Cost of sales reflects the cost of the merchandise sold to customers.

Gross profit (also called gross margin) is the difference between sales and cost of

sales. It represents the maximum amount from which all other expenses must be met

before a profit can be realised.

Selling, general and administrative expenses are the operating expenses of the

organisation. In a typical income statement, each expense is shown as a separate item

instead of being grouped together (as is the case here).

Operating profit is often used as a measure of the performance of management.

Interest expense represents the cost of borrowing funds.

Net profit will only result if the income exceeds expenses. A net loss results if

expenses exceed income.

A major purpose of the income statement is to meet the needs of investors who

require information about earnings (profit). In companies, this information about

earnings is useful for evaluating management decisions that affect payments to

shareholders and share prices.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 23

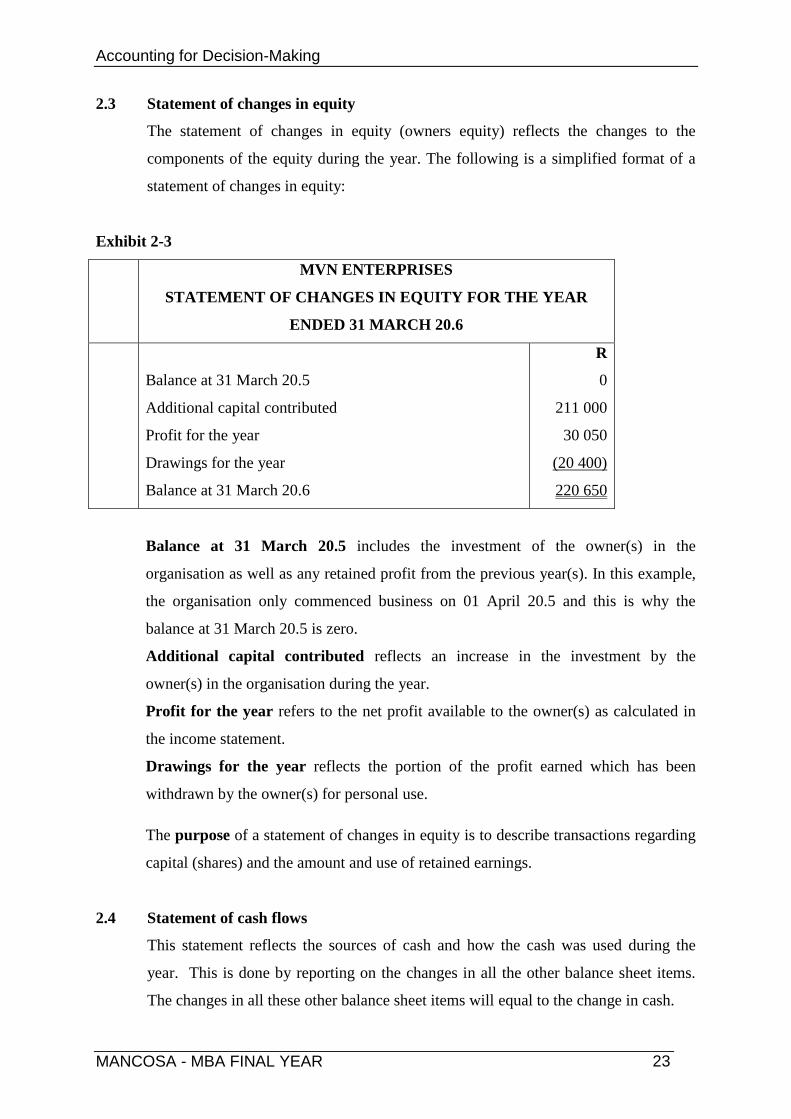

2.3

Statement of changes in equity

The statement of changes in equity (owners equity) reflects the changes to the

components of the equity during the year. The following is a simplified format of a

statement of changes in equity:

Exhibit 2-3

MVN ENTERPRISES

STATEMENT OF CHANGES IN EQUITY FOR THE YEAR

ENDED 31 MARCH 20.6

Balance at 31 March 20.5

Additional capital contributed

Profit for the year

Drawings for the year

Balance at 31 March 20.6

R

0

211 000

30 050

(20 400)

220 650

Balance at 31 March 20.5 includes the investment of the owner(s) in the

organisation as well as any retained profit from the previous year(s). In this example,

the organisation only commenced business on 01 April 20.5 and this is why the

balance at 31 March 20.5 is zero.

Additional capital contributed reflects an increase in the investment by the

owner(s) in the organisation during the year.

Profit for the year refers to the net profit available to the owner(s) as calculated in

the income statement.

Drawings for the year reflects the portion of the profit earned which has been

withdrawn by the owner(s) for personal use.

The purpose of a statement of changes in equity is to describe transactions regarding

capital (shares) and the amount and use of retained earnings.

2.4

Statement of cash flows

This statement reflects the sources of cash and how the cash was used during the

year. This is done by reporting on the changes in all the other balance sheet items.

The changes in all these other balance sheet items will equal to the change in cash.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 24

The following is an example of a simple statement of cash flows:

Exhibit 2-4

MVN ENTERPRISES

CASH FLOW STATEMENT FOR THE YEAR ENDED 31 MARCH

20.6

R

Cash flows from operating activities 120 800

Operating profit 45 050

Non cash flow adjustment: Depreciation 13 000

Profit before working capital changes 58 050

Working capital changes: 77 750

Increase in inventory (19 000)

Increase in accounts receivable (28 500)

Increase in accounts payable 125 250

Cash generated from operations 135 800

Interest paid (15 000)

Cash flows from investing activities (260 000)

Non-current assets purchased (260 000)

Cash flows from financing activities 290 600

Cash received from owner 190 600

Cash received from non -current loan 100 000

Increase in cash 151 400

Cash flows from operating activities is a focal point for most stakeholders as an

organisation cannot survive in the long-term unless it generates sufficient cash flows

from its operating activities.

Depreciation is added back to profit as it is a book entry and cash is not affected.

The increase in inventory is subtracted because cash was paid to increase inventory.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 25

The increase in accounts receivable is subtracted since it reflects sales that have not

yet been received.

The increase in accounts payable is added since cash has not been paid for products

or services received.

Cash flows from investing activities reflect the cash used to purchase assets that

have a long life.

Cash flows from financing activities include amounts received from the owner(s) to

increase capital and amounts received (or paid) through long-term borrowing.

The net increase in cash can be verified as it is also equal to the difference in the

cash balances at 31 March 20.5 (0) and 31 March 20.6 (R151 400).

The purpose of the statement of cash flows is to provide information to investors,

creditors and other users to assess the ability of the organisation to meet its cash

requirements.

2.5

Financial statement relationships

The financial statements of MVN Enterprises (discussed above) will be used to

illustrate the financial statement relationships. Refer to exhibit 2-5.

The balance sheet at 31 March 20.5 has no amounts since MVN Enterprises only

commenced business on 01 April 20.5. The integration of the financial statements is

as follows:

The net profit in the income statement also appears in the statement of changes in

equity as an addition to retained earnings. The net profit also affects the retained

earnings component of equity in the balance sheet.

The statement of changes in equity and balance sheet are integrated. The retained

earnings on 31 March 20.6 also appears as part of equity in the balance sheet.

The balance sheet and the statement of cash flows are also integrated. The cash that

appears in the balance sheet also appears as the end of the financial year cash in the

statement of cash flows.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 26

Exhibit 2-5

FFIINNAANNCCIIAALL SSTTAATTEEMMEENNTT RREELLAATTIIOONNSSHHIIPPSS

*31 March 20.5 Financial year 20.6 31 March 20.6*

MVN Enterprises

Statement of cash flows for the

year ended 31 March 20.6

Operating activities 120 800

Investing activities (260 000)

Financing activities 290 600

Net change in cash 151 400

MVN Enterprises Cash on 31 March 20.5 151 400 MVN Enterprises

Balance Sheet at 31 Mar 20.5 Balance Sheet at 31 Mar 20.6

Assets MVN Enterprises MVN Enterprises Assets

Cash - Income statement for the year Statement of changes in equity Cash 151 400

All other assets - ended 31 March 20.6 for the year ended 31 March 20.6 All other assets 294 500

- Revenue 300 000 Paid-in capital 211 000 445 900

Expenses (269 950) Retained earnings:

Equity & liabilities Net profit 30 050 Opening balance 0 Equity & liabilities

Equity Net profit 30 050 Equity

Capital - Drawings (20 400) Capital 211 000

Retained earnings - Closing balance 9 650 Retained earnings 9 650

Total equity - Total change in equity 220 650 Total equity 220 650

Liabilities - Liabilities 225 250

- 445 900

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 27

? THINK POINT

Davies and Pain (2002: 23) uses the imagery of a video cassette player with pause and play

buttons to associate with the financial statements viz. income statement, balance sheet and

statement of cash flows. Can you explain the imagery?

3.

ACCOUNTING CONCEPTS

Many important decisions are made from financial statements and it is important to

understand the principles or concepts that underpin the preparation of financial information.

These concepts are practices that accountants have agreed upon over a period of time.

Marshall et al (2011: 47) use the following model to illustrate the concepts:

Exhibit 2-6

Accounting entity

Assets = Equity + Liabilities Going concern

(Accounting equation) (continuity)

Procedures for sorting,

classifying, and presenting

(bookkeeping)

Selection of alternative

methods of reflecting the

effect of certain transactions

(accounting)

Transactions Financial statements

- Unit of measurement - Accounting period - Consistency

- Cost principle - Matching revenue and expense - Full disclosure

- Objectivity - Revenue recognised at time of sale - Materiality

- Accrual concept - Conservatism

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 28

3.1

The accounting concepts may be explained as follows:

Concepts related to the whole model

The accounting equation must be in balance every time transactions are recorded in the

accounting records.

Accounting entity refers to the entity (organisation) for which the financial statements are

prepared.

In terms of the going concern concept it is presumed that the entity will continue to operate

in the future. The amounts reflected in the balance sheet thus do not reflect the liquidation

value of the assets.

3.2

Concepts related to transactions

In South Africa, the Rand is the unit of measurement for all transactions. Adjustments are

not made to the buying power of the Rand.

In terms of the cost principle transactions are recorded at their original cost to the entity as

measured in Rands.

Objectivity ensures that transactions are recorded the same way in all situations. The use of

the Rand as a unit of measurement and the cost principle facilitates objectivity.

3.3

Concepts related to bookkeeping procedures and the accounting process

These concepts apply to the accounting period. The accounting period, which is usually

one year, is the period of time chosen to report on the results of operations and the financial

position.

In terms of the matching concept all income earned and expenses incurred to earn the

income are matched with each other to calculate the profit (or loss) for the period for which

they relate.

Revenue is recognised at the time of sale, which is when ownership of the product is

passed to the buyer.

In terms of the accrual concept revenue is recognised at the point of sale and expenses are

recognised as they are incurred, even if the cash receipt or payment occurs at another time

or in another accounting period.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 29

3.4

Concepts related to financial statements

The consistency concept is based on the principle uniformity that prevails in the

accounting treatment of like items within each accounting period and from one period to

the next. This will ensure that meaningful comparisons can be made using an entity’s

financial statements for several years.

Full disclosure requires that financial statements and notes include all the necessary

information that will prevent the users of the financial statements from being misled.

Information is regarded as material if its omission or misrepresentation could influence the

economic decision of users taken on the basis of the financial statements. The concept of

materiality also implies that the amounts reflected in the financials statements need not be

stated with absolute preciseness.

Conservatism in accounting requires accountants to be conservative when in doubt. When

the principle of conservatism is applied to making judgements, lower profits and asset

valuations are estimated rather than higher values.

4.

ACCOUNTING EQUATION

We already know that the accounting equation (derived from the balance sheet) is

expressed as follows:

Assets = Equity + Liabilities

Every financial transaction will cause a change in the accounting equation. However, the

equation will remain in balance after every transaction. The equation can be stated in an

expanded form as to include items in each of the three elements of the equation:

Assets = Equity + Liabilities

Equipment Inventory Receivables Bank = Capital Income Expenses + Payables

Note that income and expenses appear under equity as they are used to calculate the net

profit/loss that in turn increases/decreases equity.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 30

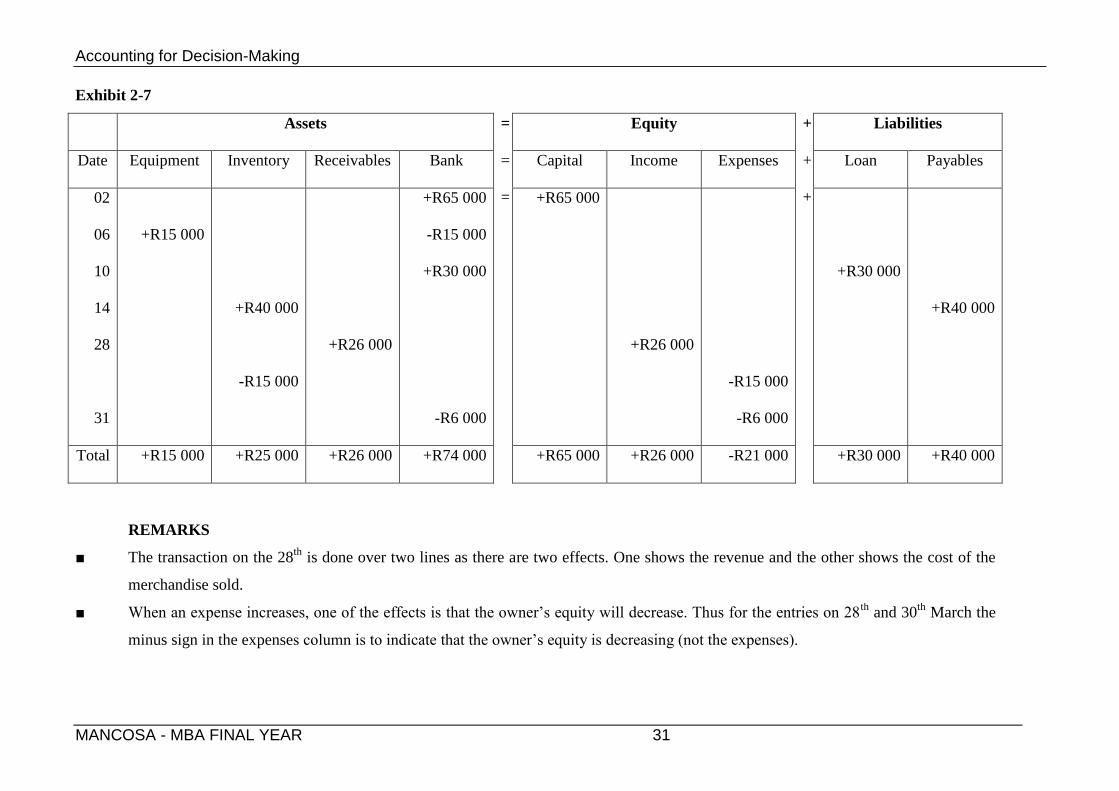

The following example will be used to illustrate the operation of the accounting equation.

Example 1

02

06

10

14

28

31

Transactions for March 20.6

The owner of Tulani Enterprises commenced her business by investing R65 000 cash.

Purchased equipment for R15 000 cash.

The owner obtained a long-term loan of R30 000 from the bank.

Purchased merchandise on credit, R40 000.

Sold merchandise that cost R15 000 for R26 000 on credit.

Paid salaries to the employees, R6 000

Exhibit 2-7 illustrates the effect of the above transactions on the accounting equation.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 31

Exhibit 2-7

Assets = Equity + Liabilities

Date Equipment Inventory Receivables Bank =

=

Capital Income Expenses +

+

Loan Payables

02

06

10

14

28

31

+R15 000

+R40 000

-R15 000

+R26 000

+R65 000

-R15 000

+R30 000

-R6 000

+R65 000

+R26 000

-R15 000

-R6 000

+R30 000

+R40 000

Total +R15 000 +R25 000 +R26 000 +R74 000 +R65 000 +R26 000 -R21 000 +R30 000 +R40 000

■

REMARKS

The transaction on the 28th

is done over two lines as there are two effects. One shows the revenue and the other shows the cost of the

merchandise sold.

■ When an expense increases, one of the effects is that the owner’s equity will decrease. Thus for the entries on 28th

and 30th

March the

minus sign in the expenses column is to indicate that the owner’s equity is decreasing (not the expenses).

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 32

The simplified formats of the financial statements from the data from exhibit 2-7 are

presented below in exhibit 2-8:

Exhibit 2-8

TULANI ENTERPRISES

INCOME STATEMENT FOR THE MONTH ENDED 31 MARCH 20.6

R

Revenue 26 000

Expenses (21 000)

Net profit 5 000

TULANI ENTERPRISES

STATEMENT OF CHANGES IN EQUITY FOR THE MONTH

ENDED 31 MARCH 20.6

Opening balance

Additional capital contributed

Net profit

Closing balance

R

0

65 000

5 000

70 000

TULANI ENTERPRISES

BALANCE SHEET AS AT 31 MARCH 20.6

ASSETS

Property, plant and equipment

Inventory (merchandise)

Accounts receivables

Cash

Total assets

EQUITY AND LIABILITIES

Equity

Liabilities

Long-term debt

Accounts payables

Total equity and liabilities

R

15 000

25 000

26 000

74 000

140 000

70 000

30 000

40 000

140 000

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 33

TULANI ENTERPRISES

STATEMENT OF CHANGES IN CASH FLOWS FOR THE

MONTH ENDED 31 MARCH 20.6

R

Cash flows from operating activities (6 000)

Net profit 5 000

Add (Deduct) items not affecting cash

Increase in inventory (25 000)

Increase in accounts receivable (26 000)

Increase in accounts payable 40 000

Cash flows from investing activities (15 000)

Purchase of plant, machinery and equipment (15 000)

Cash flows from financing activities 95 000

Capital contributed 65 000

Cash received from long-term loan 30 000

Net increase in cash for the year 74 000

Cash (opening balance) 0

Cash (closing balance) 74 000

5.

5.1

SELF-ASSESSMENT ACTIVITIES AND SOLUTIONS

Indicate whether each of the following is regarded as a financing activity (F), investing

activity (I) or operating activity (O). Write down the letter F, I or O in the spaces provided.

5.1.1.

5.1.2

5.1.3

5.1.4

5.1.5

5.1.6

___

___

___

___

___

___

New machinery was purchased for installing in the factory.

A loan was obtained from the bank.

R1 000 was received from a customer for goods sold.

The organisation’s old computer was sold for R900.

The owner increased her capital contribution in the business.

Two more secretaries were employed.

5.2

A balance sheet may be said to represent assets and claims to assets. Who has claims to the

assets of an entity?

5.3 Assume that you are reviewing a balance sheet that has two sections viz. assets as well

equity and liabilities. What questions can you answer by examining the assets? What

questions can you answer by examining the equity and liabilities?

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 34

5.4 The income statement as well as the statement of cash flows provides information about

the operating activities during a financial year. Apart from possible statutory requirements,

why are both statements included in an organisation’s financial report? How can decision-

makers use of information in each statement?

5.5 You are considering a move from a small well-established retailer to a public company

that was established 18 months ago. You have a job interview next week. Your business

friends advised you to investigate the company before the interview. They say that if the

company’s business plan fails, there is a great chance that the company may not be a going

concern. Name some questions that you would like to get answers to before the interview?

5.6 Discuss the implications of the preparation of the income statement if there were no

accounting concepts.

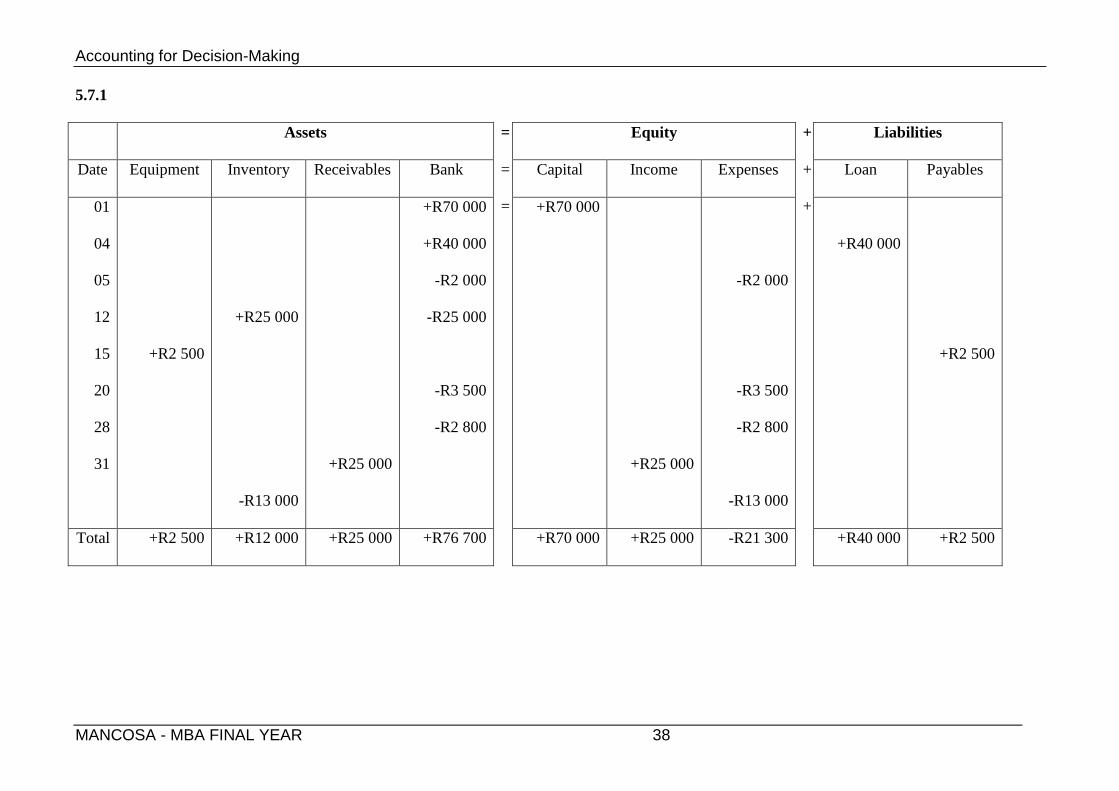

5.7 Valpre Enterprises had the following transactions during its first month of business, May

20.6.

May

01

Patricia Zuma set up a bank account in the name of the business and deposited R70 000 of

her own funds into the account.

04 She supplemented her capital by taking a long-term loan with her bank, R40 000.

05 The rent for May 20.6 was paid by cheque, R2 000.

12 Goods for resale costing R25 000 were purchased by cheque.

15 A cash register machine was purchased on account, R2 500.

20 Paid advertising costs for the grand opening of the firm, R3 500.

28 Employees were paid R2 800 in wages.

31 Sold goods that cost R13 000 for R25 000 on credit.

Required

5.7.1 Use the format presented in exhibit 2-7 to analyse the above transactions.

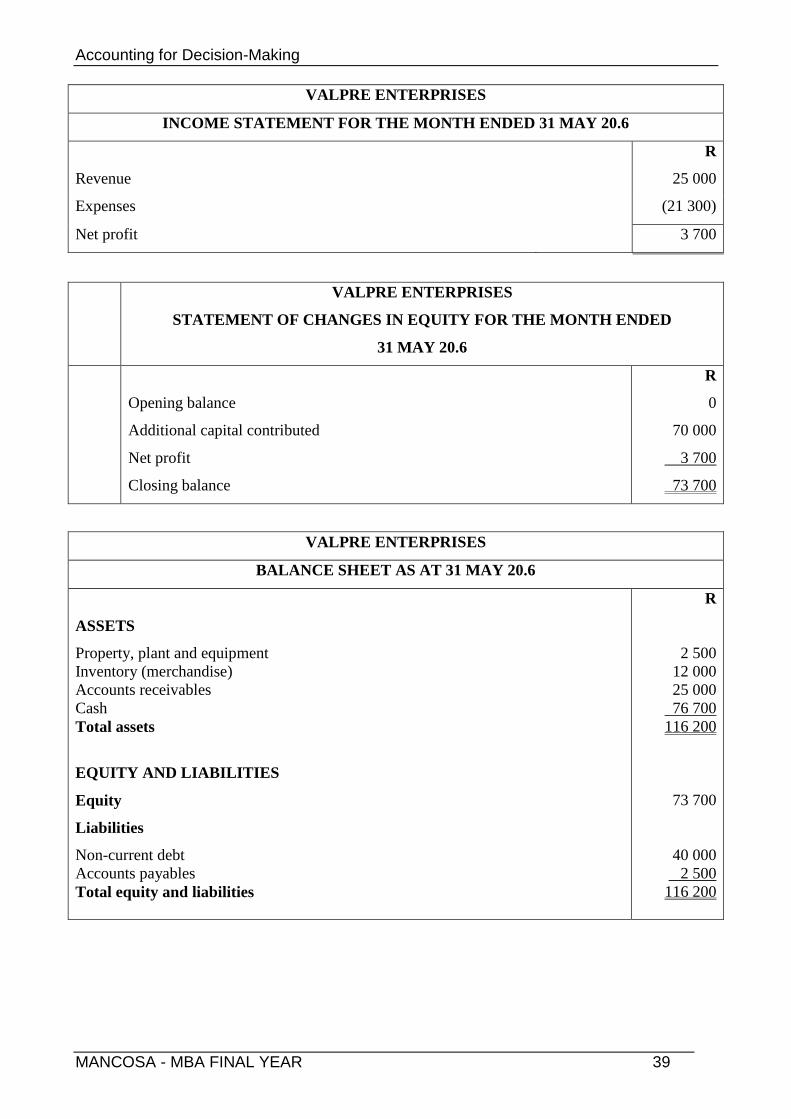

5.7.2 Use the total of the effects of the transactions (as calculated in 5.7.1) to prepare the:

5.7.2.1 Income statement for May 20.6.

5.7.2.1 Statement of changes in equity for the month ended 31 May 20.6.

5.7.2.2 Balance sheet on 31 May 20.6.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 35

SOLUTIONS

? THINK POINT

The balance sheet is a financial snapshot at a moment in time. The financial position of an

organisation is comparable to pressing the “pause” button on a video player. The video in

play mode shows what is happening as time goes on. When you press “pause” the video

stops on a picture. However, this picture does not tell what has happened over the period of

time up to the pause.

The income statement is the video in “play” mode. Net profit is calculated from revenues

earned throughout the period between two “pauses”, minus expenses incurred from earning

those revenues.

The statement of cash flows is the video again in “play” mode. It summarises the cash

inflows and outflows and calculates the net change in the cash position throughout the

period between two “pauses”.

5.1

5.1.1.

5.1.2

5.1.3

5.1.4

5.1.5

5.1.6

I

F

O

I

F

O

New machinery was purchased for installing in the factory.

A loan was obtained from the bank.

R1 000 was received from a customer for goods sold.

The organisation’s old computer was sold for R900.

The owner increased her capital contribution in the business.

Two more secretaries were employed.

5.2

Firstly, the suppliers of credit and loans (liabilities).

Secondly, after liabilities have been settled, the investor(s) in the business.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 36

5.3

Are the non-current assets optimally utilised?

Which non-current assets need replacement because they are reaching the end of their

economic life?

Are the investments providing a satisfactory return?

Are there any capital gains on the investment?

Is the organisation holding too much inventory?

Is there too much owing by debtors?

Is there too much of cash lying idle in the bank?

How much of borrowed capital is there compared to own capital?

Did the owner(s) get a satisfactory return on investment?

Will the business be able to make repayments on loans and service the debt?

Will the organisation be able to pay off its short-term debts?

To what extent is the organisation taking advantage of credit offered by suppliers?

5.4

The income statement shows how the profit or loss has been achieved during the year. It

does this by showing us the revenues that have been generated and the costs that were

incurred to generate those revenues. Consequently, it shows the increase or decrease in

wealth of the business during the period. The statement of cash flows on the other hand

describes the events that affected the organisation’s cash during the financial year. The

statement identifies how much cash an organisation has, where the cash came from and

how the organisation used the cash during the financial year.

Use of the statements by decision-makers

Owners and decision-makers use the income statement to evaluate how well the

organisation has performed. However, the income statement (or the balance sheet for that

matter) does not show or analyse the key changes that have taken place in an organisation’s

financial position that a statement of cash flows will reveal. For example:

■ how much capital expenditure (e.g. buildings, machinery) was made and how it was

financed?

■ what was the extent of the new borrowing and how much debt was repaid?

■ how much did the organisation need to fund increases in debtors and stock requirements?

■ how much of the company’s funding was obtained from funds generated from its operating

activities and how much by new external funding?

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 37

5.5

Are there any published financial statements available for analysis?

How much has been invested in the company by shareholders?

Is the company profitable?

Is the company generating sufficient cash to meet its cash payments?

Are any analyses by the press available?

What is the present customer base?

5.6

If accountants prepare income statements as they see fit, comparability between

organisations and across time periods would be extremely difficult.

The lack of accounting concepts will open the way for accountants to manipulate figures in

the income statement. Some may “window dress” the income statement to make it look

better than it actually is. The reliability of figures in the income statement would then be

brought into question.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 38

5.7.1

Assets = Equity + Liabilities

Date Equipment Inventory Receivables Bank =

=

Capital Income Expenses +

+

Loan Payables

01

04

05

12

15

20

28

31

+R2 500

+R25 000

-R13 000

+R25 000

+R70 000

+R40 000

-R2 000

-R25 000

-R3 500

-R2 800

+R70 000

+R25 000

-R2 000

-R3 500

-R2 800

-R13 000

+R40 000

+R2 500

Total +R2 500 +R12 000 +R25 000 +R76 700 +R70 000 +R25 000 -R21 300 +R40 000 +R2 500

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 39

VALPRE ENTERPRISES

INCOME STATEMENT FOR THE MONTH ENDED 31 MAY 20.6

R

Revenue 25 000

Expenses (21 300)

Net profit 3 700

VALPRE ENTERPRISES

STATEMENT OF CHANGES IN EQUITY FOR THE MONTH ENDED

31 MAY 20.6

Opening balance

Additional capital contributed

Net profit

Closing balance

R

0

70 000

3 700

73 700

VALPRE ENTERPRISES

BALANCE SHEET AS AT 31 MAY 20.6

ASSETS

Property, plant and equipment

Inventory (merchandise)

Accounts receivables

Cash

Total assets

EQUITY AND LIABILITIES

Equity

Liabilities

Non-current debt

Accounts payables

Total equity and liabilities

R

2 500

12 000

25 000

76 700

116 200

73 700

40 000

2 500

116 200

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 40

TOPIC 3

ACCOUNTING FOR AND PRESENTATION OF ASSETS, LIABILITIES

AND OWNERS’ EQUITY

LEARNING OUTCOMES

Students should be able to:

► identify the various current assets and report them correctly in the balance sheet.

► explain why internal controls are important.

► identify the various non-current assets and be able to report them in the balance sheet.

► explain the different methods of depreciation for financial accounting purposes.

► present the various current and non-current liabilities in the balance sheet.

► describe how the components of owners’ equity are reported in the balance sheet.

► interpret information presented in the balance sheet.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 41

CONTENTS

1. Introduction

2. Assets

3. Owners’ equity

4. Liabilities

5. Self-assessment activities and solutions

READING

Prescribed

Marshall D.H., Mcmanus W.W. and Viele D.F. (2011) Accounting: What the numbers mean,

9th

Edition, McGraw-Hill: New York. (Chapters 5, 6, 7 and 8)

Recommended

Davies T. and Pain B. (2002) Business Accounting and Finance, First Edition, McGraw-Hill: UK

(Chapter 2)

Ingram R.W., Albright T.L., Baldwin B.A. and Hill J.W. (2005) Accounting: Information for

Decisions, Third edition, Thomson South-Western: Canada. (Chapter F4)

Lubbe I. and Watson A. (2006) Accounting: GAAP Principles, First edition, Oxford University

Press Southern Africa: Cape Town. (Chapter 17)

Warren A.S. (2007) Survey of Accounting, Third Edition, Thomson South-Western: USA

(Chapter 5, 6, 7 and 8)

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 42

1.

INTRODUCTION

As previously mentioned, a balance sheet summarises an entity’s assets, liabilities and

owners’ equity at a specific time in point. The focus of this topic is to make sense of the

presentation of assets, owners’ equity and liabilities in a balance sheet. The following

illustration (balance sheet of a company) is a picture of what is to follow:

Exhibit 3-1

BALANCE SHEET Paragraph

Non-current assets

Land

Buildings and equipment

Assets acquired by lease

Intangible assets

Natural resources

Other non-current assets

Current assets

Inventories

Notes receivable

Accounts receivable

Short-term marketable securities

Cash and cash equivalents

2.1

2.2

2.3

2.4

2.5

2.6

2.7

2.8

2.9

2.10

2.11

Owners’ equity

Ordinary shares

Preference shares

Retained earnings

Non-current liabilities

Long-term debt

Other long-term liabilities

Current liabilities

Accounts payable

Short-term debt

Current maturities of long-term debt

3.1

3.2

3.3

4.1

4.2

4.3

4.4

4.5

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 43

2.

ASSETS

Assets, as we already know, are the resources that are controlled by an enterprise from

which economic benefits will be derived either now or in the future. Assets may be

classified as current or non-current. Current assets include cash and those assets that are

expected to be turned into cash within one year. Non-current assets include land, buildings,

equipment, intangible assets and natural resources. Let us examine the presentation of

assets in the balance sheet.

2.1

NON-CURRENT ASSETS

Land

Land that is owned by an organisation is shown on the balance sheet at its original cost.

This is in keeping with the cost principle. The costs that the organisation incur to ensure

that the land is ready for use is regarded as being part of the original cost. These costs

include the purchase price of the land, legal fees and any other costs related to acquiring the

land. Land that is purchased for investment purposes is classified as a separate non-current

asset and is also reported at its original cost. No depreciation is calculated for land. If land

is sold, the profit or loss on the sale will be reported in the income statement during the

period in which the sale occurred.

2.2

Buildings and equipment

Building and equipment, like land, are reported at their original cost which includes the

purchase price and any other costs necessary to get them ready for use. Interest costs

incurred on loans acquired to finance the construction of buildings are capitalised (i.e.

recorded as an asset rather than an expense) until the buildings are ready for use. Costs that

are incurred to install new equipment are also capitalised.

In terms of the matching concept depreciation is calculated on buildings and equipment.

When buildings or equipment are purchased the original cost is regarded as a prepayment

of economic benefits that the organisation will reap in the future years. A part of the asset’s

cost is deducted from income that was generated through the use of the asset. Depreciation

expense is recorded in each financial year. In the balance sheet, the cost of the asset and its

accumulated depreciation (cumulative total of all the depreciation expense that has been

recorded over the life of the asset up to the balance sheet date) are reported as follows:

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 44

Buildings

Accumulated depreciation

R400 000

(80 000)

Net book value of buildings R320 000

It is more commonly reported as follows

Building, less accumulated depreciation of R80 000 R320 000

These are many methods of calculating depreciation that result in different patterns of

depreciation by financial year. The two broad categories of calculating depreciation are the

accelerated depreciation methods and the straight-line depreciation method. Accelerated

depreciation methods (e.g. declining balance and sum-of-the-years’ digits) result in a

higher depreciation expense (and thus lower net profit) in the early years of the life of the

asset. In the later years, deprecation expense will be less and net profit will be higher.

Using the straight-line method the depreciation expense is spread evenly over the life of

the asset.

? THINK POINT 1

According to a survey of American companies in 2000, it was found that 82% of companies

used the straight-line method to calculate depreciation. What motivation could there be for

the higher preference of the straight-line method.

When a depreciable asset is sold or scrapped, the cost of the asset and its accumulated

depreciation must be removed from the books. Profits or losses on disposal of depreciable

assets are not considered to be part of operating income. If the amount is material, it is

shown separately as either other income or other expenses. If the amount is not material, it

will be reported as miscellaneous other income.

2.3 Assets acquired by capital lease

Sometimes an organisation may lease (rent) an asset instead of purchasing it. If the lease

agreement results in the lessee assuming the benefits and risk of ownership of the leased

asset, it is called a capital lease. Such an asset will be reported in the lessee’s balance sheet

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 45

with the purchased assets. The accompanying liability will also be reported in the balance

sheet. In the lessee’s income statement the cost of the leased asset will be taken as the

depreciation amount and the financing cost will be reflected as interest expense.

2.4

Intangible assets

Marshall et al (2011: 213) defines an intangible asset as “a long-lived asset represented by a

contractual right, or an asset that is not physically identifiable”. One type of intangible asset

includes leasehold improvements, patents and trademarks; another type is called goodwill.

The cost of most intangibles is spread over time as expenses and this is known as

amortization. In other words the cost of an intangible asset from the balance sheet is

allocated to the income statement as an expense.

When a tenant makes modifications to the building it leases (e.g. constructing private

offices), the cost of such modifications (called leasehold improvements) is amortised over

their useful life to the tenant or over the life of the lease (whichever is shorter).

A patent is a licence granted by a government giving the owner sole control or use of an

invention for a period of 20 years.

A trademark is a name, term or symbol used to identify a business and its product.

Organisations can gain exclusive use of a trademark by registering it.

The exclusive right to publish and sell a literary, artistic or musical composition is granted

by a copyright.

The cost of obtaining a patent, trademark or copyright is capitalised and amortized over its

estimated useful life or statutory life (whichever is shorter). The cost of developing a

patent, trademark or copyright is usually not significant compared to purchasing them from

another organisation.

Goodwill refers to an intangible asset of an organisation that is created from such

favourable factors as good location, product quality, reputation, high customer loyalty and

managerial skill. Goodwill is recorded in the accounts only after it is determined

objectively by a transaction e.g. purchase of an entity for more than the market value of the

net assets. The excess is recorded as goodwill and reported as an intangible asset and is not

amortized. However, goodwill is tested annually for impairment. If the book value of the

goodwill is greater than the fair value, an impairment loss is realised equal to that excess.

The impairment loss is recorded in the income statement and the book value of the goodwill

will be decreased in the balance sheet.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 46

2.5

Natural resources

Paper, petroleum and mining companies purchase or lease land that contains oil, wood or

minerals. The cost of the land primarily reflects the natural resources. The amount that is

reported for natural resources in the balance sheet is the cost of the asset minus depletion.

Depletion is the allocation of the cost of the natural resources to the periods that benefited

from their use.

2.6

Other non-current assets

Examples of other non-current assets include long-tem investments and notes receivable

that mature more than 12 months after the balance sheet date. When they become

receivable within a year, they will be re-classified as current assets.

2.7

CURRENT ASSETS

Inventories

Inventories in service organisations consist mainly of office supplies and other items of a

relatively low value. For manufacturing and merchandising organisations, the sale of

merchandise is the most important source of operating income. Cost of sales is usually the

largest expense that is deducted from sales to determine net profit. For these entities

inventories is an important current asset. Turning over inventory as quickly as possible will

enhance return on investment. The cost of items of inventory purchased includes not only

the invoice amount but also other purchasing costs e.g. freight and materials handling

charge.

There are several accepted practices of valuing inventory for reporting purposes. Inventory

valuations (and thus cost of sales) differ from method to method due to the change in the

cost of items of inventory during the financial year. The specific identification, weighted

average, first-in first-out (FIFO) and last-in first-out (LIFO) methods will now be briefly

discussed.

According to the specific identification method, when an item is sold the cost of the item is

obtained from the entity’s records. This amount is transferred from the Inventory account to

the Cost of sales account. The cost of the items held in inventory at the end of the year will

be disclosed in the balance sheet.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 47

The weighted average is applied to individual items of inventory. The average cost is

weighted by taking into account the number of units of opening inventory and each

purchase. This average is used to calculate the cost of sales and the value of closing

inventory.

The first-in first-out (FIFO) method transfers to the Cost of sales account the oldest costs

incurred in purchasing the inventory that was sold and thus values closing inventory at the

most recent costs of the merchandise purchased.

Under the last-in first-out (LIFO) method, the most recent costs of the merchandise

purchased are taken as Cost of sales and the closing inventory is valued at the oldest costs.

It is clear from the above that inventory valuation has an impact on both profitability and

liquidity. The impact of each of the four methods described above must be understood in

making judgements and decisions especially when comparing different entities. Consider

the following:

When costs are increasing during the year, the cost of sales will be lower and profits higher

under FIFO than under LIFO. The reverse happens when costs decrease during the year.

Inventories are reported in the balance sheet at the lower of cost or market. Sometimes

for some items of inventory the market value is lower than cost due to factors such as

obsolescence or damage. Reporting inventory at lower of cost or market is the application

of the accounting concept of conservatism.

2.8

Notes receivable

If a debtor experiences difficulty in settling a debt on due date, the entity may convert the

debt to a note receivable. The effect of this on the balance sheet is that accounts receivable

will decrease and notes receivable will increase. A note usually includes provisions relating

to maturity date, some form of security, penalties for non-payment and interest rate

associated with the loan. A note receivable may also be used when an entity lends money to

another entity and takes a note from that entity.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 48

2.9

Accounts receivable

Accounts receivable refer to amounts receivable from customers for merchandise sold or

for services rendered on credit. Accounts receivable are reported at net realisable value i.e.

the amount expected to be received from debtors. The net realisable value is less than the

amount of the receivable originally recorded because of bad debts and cash discounts.

Despite doing a thorough check on the creditworthiness of customers, losses through bad

debts are inevitable. The credit manager is expected to estimate as accurately as possible,

from the accounts receivable, the expected bad debts (known as allowance/provision for

bad debts). Obviously, recent collection experience and the current economic conditions

prevailing would be taken into account. An adjustment entry is made to reduce the carrying

value of the accounts receivable. The presentation of allowance for bad debts under current

assets in the balance sheet is as follows:

Accounts receivable

Allowance for bad debts

R20 000

(1 000)

Net accounts receivable R19 000

Cash discounts are often allowed to debtors if the account is paid within a stated period

e.g. within 10 days of the date of sale. Credit terms allowed to customers usually state that

if the amount owing is not paid within the discount period, it must be paid in full within 30

days of the invoice date. The credit term is often abbreviated as 2/10, n30. In the balance

sheet, accounts receivable is reduced to allow for the estimated cash discounts that are

expected to be granted to debtors who pay within the discount period. The accounting

treatment of cash discounts is similar to that of allowance for bad debts.

2.10 Short-term marketable securities

An entity can improve its return on investment by investing cash that is not required for

daily operations in short-term marketable securities. For this to materialise, the drawing up

of cash budgets is essential. Marketable securities that mature with one year of the balance

sheet date are presented as cash equivalents (part of current assets) in the balance sheet. A

security that is held to its maturity date is reported in the balance sheet at cost since it is

usually the same as its market value. Debt and equity securities that may be classified as

trading or available-for-sale are reported at market value. Furthermore, any unrealised

profit or loss is recognised.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 49

2.11

Cash and cash equivalents

Cash includes money kept for change, petty cash funds, undeposited cash and cash

immediately available to the organisation in its bank accounts. Cash equivalents are short-

term investments readily convertible into cash. Since cash on hand and cash in cheque

accounts earn little or no interest, there must be a cash management system in place to

invest cash that is not currently required for the organisation’s operation. Management must

also have policies in place to reduce the chances of embezzlement of cash.

? THINK POINT 2

As a financial manager, what control measures would you put in place to reduce the

chances of embezzlement of cash by employees?

An internal control system is important in the management of cash and may consist of

financial and administrative controls. Using financial control, there must be a separation of

duties i.e. more than one person must be responsible for a transaction from beginning to

end. Administrative controls are usually included in policy and procedure manuals e.g.

investigation of a customer’s creditworthiness before credit is granted. The process of bank

reconciliation is also a form of internal control.

3.

OWNERS’ EQUITY

A company issues share capital to its shareholders under certain conditions and with certain

rights and obligations. The owners’ equity of a company (also called shareholders’ equity)

is made up of the capital provided by shareholders to the company, plus the net profit (after

tax) and gains retained in the company, less any dividends distributed to shareholders.

3.1

Ordinary shares

The ordinary shareholders are the ultimate owners of the company. They have a claim to all

the assets that remain in the company after all liabilities and preference shareholders claims

have been settled. Ordinary shareholders are not entitled to receive any stated dividend

amount and could even not receive dividends in some years at all. They have the right to

elect the directors of the company.

Accounting for Decision-Making

MANCOSA - MBA FINAL YEAR 50

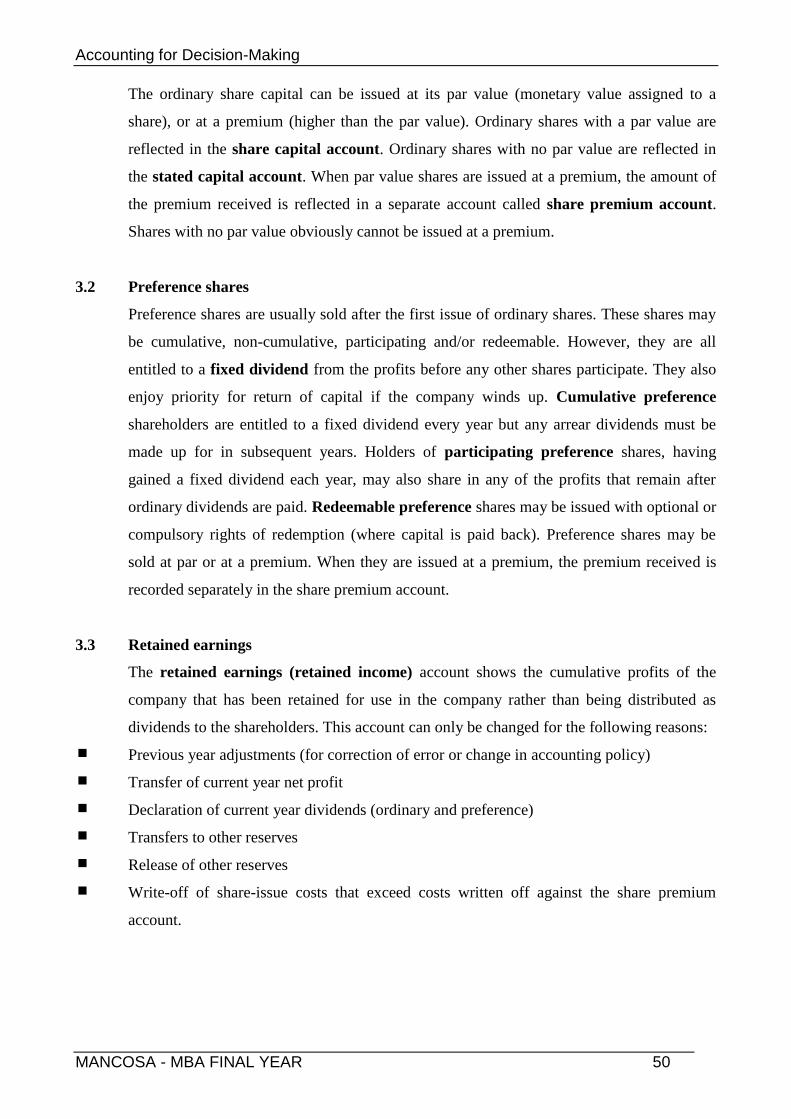

The ordinary share capital can be issued at its par value (monetary value assigned to a

share), or at a premium (higher than the par value). Ordinary shares with a par value are

reflected in the share capital account. Ordinary shares with no par value are reflected in

the stated capital account. When par value shares are issued at a premium, the amount of

the premium received is reflected in a separate account called share premium account.

Shares with no par value obviously cannot be issued at a premium.

3.2

Preference shares

Preference shares are usually sold after the first issue of ordinary shares. These shares may

be cumulative, non-cumulative, participating and/or redeemable. However, they are all

entitled to a fixed dividend from the profits before any other shares participate. They also

enjoy priority for return of capital if the company winds up. Cumulative preference

shareholders are entitled to a fixed dividend every year but any arrear dividends must be