Q4FY19 – Result Update May 22, 2019 Sanghi Industries Downside Scenario Current Price Price Target 75 18.9% Upside Scenario STRONG BUY 63 Q4FY19 Result Update Strong revenue growth due to strong volumes and stable realizations The company posted a revenue of INR 276 crore for the quarter, up by 8.8% y-o-y & 3.8% q-o-q due to sharp increase in volumes led by flat realization. Total sales volume for the quarter stood at 0.675 mt up by ~8.9% y-o-y, driven by the demand growth in its key markets which stood at 7-8%. Management expects volume’s to be around 3-3.2 mt by FY20E led by strong demand from Mumbai and south gujarat markets. Maharashtra recorded volume growth of 80% in Q4FY19 and management expects this to be the key driver in future volumes. EBITDA/Ton grew by 2.3% y-o-y, below estimates owing to cost escalations EBITDA/Ton for the quarter stood at INR 681, thereby recording growth of 2.3% y-o-y & 95.3% q-o-q in Q4FY19. Higher raw material cost (up by 53.9% y-o-y to INR 397/ton), as well as freight cost (up by 18.4% y-o-y to INR 159/ton). The company is stocking up coal, due to the unavailability of lignite, leading to a change in the fuel mix. The fuel mix as on FY19 is 76% imported coal and management expects it to be at the same levels going ahead. Also, the cost differential between lignite and coal is now down to about INR 0.05-0.10 paise/Kcal due to which coal seems to be a good option as compared to lignite. The current coal inventory is of 4 months as on FY19. Estimated capex is on track The company has completed 70% of civil work for the capacity expansion to 8.1mt. The new capacity addition is expected to be commissioned by Q1FY21. The existing capacity is operating at 65% utilization levels, post expansion management has guided that new capacity will run at 40% utilization levels. We believe that the new capacity will not be able to run at management guided levels due to overcapacity situation in Gujarat which remains the key market and much more will be dependent on housing projects and government capex in FY21E. Valuations The company witnessed a good quarter, and continues to be one of the lowest variable-cost producers in the industry, due to its locational advantage (proximity to good quality marine limestone reserves) as well as captive thermal power plant of 63 MW. We expect the low availability of lignite is to be replaced with coal stock and expect savings to come from its CPP and WHRS plants. A higher proportion of PPC and slag cement in its sales mix, combined with the increased capacity (leading to a higher pricing power) will improve the realization. At a CMP of INR 63, the company trades at a EV/ton of 44.7 on FY21 earnings. However, we don’t forsee much benefits from expansion due to which we reduce our target price to INR 75 giving an upside of 18.9%. (i.e. valuing the stock at FY21E EV/Ton of $55/Ton, 11x FY21E EV/EBITDA) Market Data Industry Cement Sensex 38970 Nifty 11709 Bloomberg Code SNGI:IN Eq. Cap. (INR Crores) 251 Face Value (INR) 10 52-w H/L 50/104 Market Cap (INR Crores) 1557.5 Valuation Data FY19 FY20E FY21E P/E (x) 30.1 18.2 17.1 EV/EBITDA (x) 14.1 11.7 10.9 EV/Ton ($) 77.9 87.4 44.7 Sanghi Industries Ltd Vs SENSEX Mar’19 Dec’18 Mar’18 Promoters 65.71 65.71 65.72 FIIs 4.76 4.79 8.77 DIIs 12.38 9.39 9.30 Retail 17.15 20.11 16.21 100.0 100.0 100.0 Shareholding Pattern (INR Crores) FY17 FY18 FY19 FY20E FY21E Net Sales 997.5 1026.4 1105.8 1206.2 1302.7 Growth% 3% 8% 9% 8% EBITDA 198.2 215.8 154.0 213.9 232.1 Growth% 9% -29% 39% 8% Reported PAT 63.1 93.3 52.6 86.8 92.5 Growth% 48% -44% 65% 7% EPS (INR) 2.87 3.72 2.10 3.46 3.68 P/E (x) 23.9 18.0 30.1 18.2 17.1 EV/EBITDA (x) 10.5 9.2 14.1 11.7 10.9 EV/Ton ($) 76.0 75.4 77.9 87.4 44.7 * Read last page for disclaimer & rating rationale * Source: Company, NSPL Research Institutional Research HEAD OF RESEARCH Vaibhav Chowdhry Vaibhav.Chowdhry @ nalandasecurities.com NALANDA SECURITIES PRIVATE LIMITED 310-311 Hubtown Solaris, NS Phadke Marg, Opp Teli Gali, Andheri East, Mumbai 69 +91-22-6281-9649 | [email protected] | www.nalandasecurities.com ASSOCIATE Aditya Khetan aditya.khetan @ nalandasecurities.com 60 80 100 120 140 160 180 200 05-2016 08-2016 11-2016 02-2017 05-2017 08-2017 11-2017 02-2018 05-2018 08-2018 11-2018 02-2019 Sanghi Sensex

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Q4

FY1

9 –

Re

sult

Up

dat

e

May 22, 2019

Sanghi IndustriesDownside

Scenario

Current

Price

Price

Target

7518.9%

Upside

Scenario

STRONG BUY

63Q4FY19 Result Update

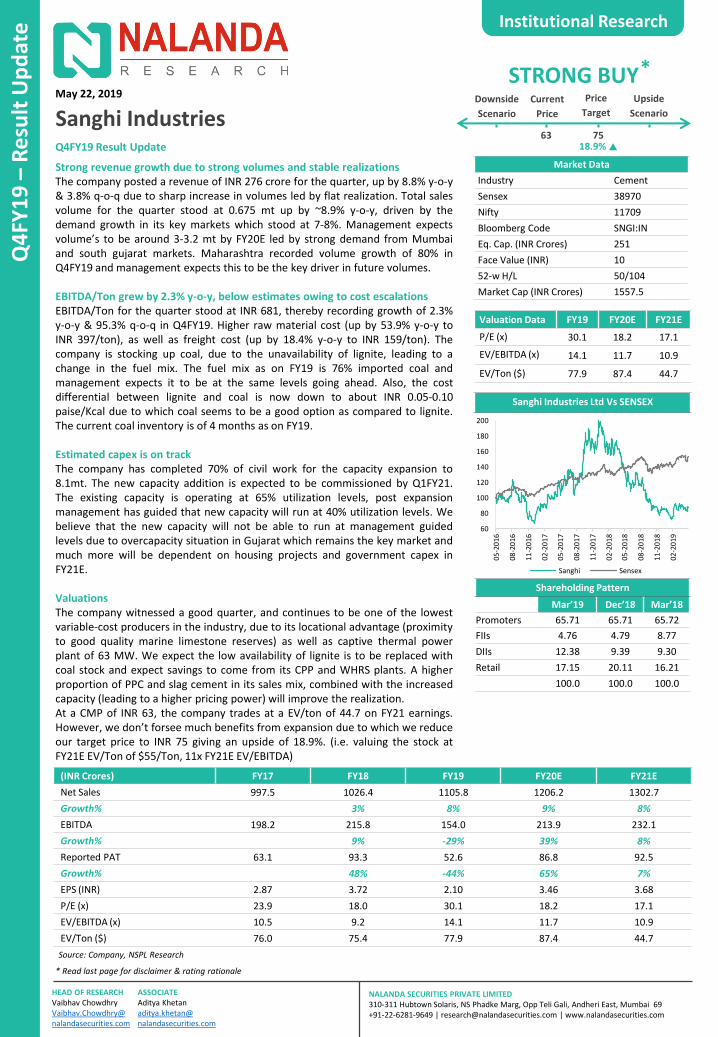

Strong revenue growth due to strong volumes and stable realizationsThe company posted a revenue of INR 276 crore for the quarter, up by 8.8% y-o-y& 3.8% q-o-q due to sharp increase in volumes led by flat realization. Total salesvolume for the quarter stood at 0.675 mt up by ~8.9% y-o-y, driven by thedemand growth in its key markets which stood at 7-8%. Management expectsvolume’s to be around 3-3.2 mt by FY20E led by strong demand from Mumbaiand south gujarat markets. Maharashtra recorded volume growth of 80% inQ4FY19 and management expects this to be the key driver in future volumes.

EBITDA/Ton grew by 2.3% y-o-y, below estimates owing to cost escalationsEBITDA/Ton for the quarter stood at INR 681, thereby recording growth of 2.3%y-o-y & 95.3% q-o-q in Q4FY19. Higher raw material cost (up by 53.9% y-o-y toINR 397/ton), as well as freight cost (up by 18.4% y-o-y to INR 159/ton). Thecompany is stocking up coal, due to the unavailability of lignite, leading to achange in the fuel mix. The fuel mix as on FY19 is 76% imported coal andmanagement expects it to be at the same levels going ahead. Also, the costdifferential between lignite and coal is now down to about INR 0.05-0.10paise/Kcal due to which coal seems to be a good option as compared to lignite.The current coal inventory is of 4 months as on FY19.

Estimated capex is on trackThe company has completed 70% of civil work for the capacity expansion to8.1mt. The new capacity addition is expected to be commissioned by Q1FY21.The existing capacity is operating at 65% utilization levels, post expansionmanagement has guided that new capacity will run at 40% utilization levels. Webelieve that the new capacity will not be able to run at management guidedlevels due to overcapacity situation in Gujarat which remains the key market andmuch more will be dependent on housing projects and government capex inFY21E.

ValuationsThe company witnessed a good quarter, and continues to be one of the lowestvariable-cost producers in the industry, due to its locational advantage (proximityto good quality marine limestone reserves) as well as captive thermal powerplant of 63 MW. We expect the low availability of lignite is to be replaced withcoal stock and expect savings to come from its CPP and WHRS plants. A higherproportion of PPC and slag cement in its sales mix, combined with the increasedcapacity (leading to a higher pricing power) will improve the realization.At a CMP of INR 63, the company trades at a EV/ton of 44.7 on FY21 earnings.However, we don’t forsee much benefits from expansion due to which we reduceour target price to INR 75 giving an upside of 18.9%. (i.e. valuing the stock atFY21E EV/Ton of $55/Ton, 11x FY21E EV/EBITDA)

Market Data

Industry Cement

Sensex 38970

Nifty 11709

Bloomberg Code SNGI:IN

Eq. Cap. (INR Crores) 251

Face Value (INR) 10

52-w H/L 50/104

Market Cap (INR Crores) 1557.5

Valuation Data FY19 FY20E FY21E

P/E (x) 30.1 18.2 17.1

EV/EBITDA (x) 14.1 11.7 10.9

EV/Ton ($) 77.9 87.4 44.7

Sanghi Industries Ltd Vs SENSEX

Mar’19 Dec’18 Mar’18

Promoters 65.71 65.71 65.72

FIIs 4.76 4.79 8.77

DIIs 12.38 9.39 9.30

Retail 17.15 20.11 16.21

100.0 100.0 100.0

Shareholding Pattern

(INR Crores) FY17 FY18 FY19 FY20E FY21E

Net Sales 997.5 1026.4 1105.8 1206.2 1302.7

Growth% 3% 8% 9% 8%

EBITDA 198.2 215.8 154.0 213.9 232.1

Growth% 9% -29% 39% 8%

Reported PAT 63.1 93.3 52.6 86.8 92.5

Growth% 48% -44% 65% 7%

EPS (INR) 2.87 3.72 2.10 3.46 3.68

P/E (x) 23.9 18.0 30.1 18.2 17.1

EV/EBITDA (x) 10.5 9.2 14.1 11.7 10.9

EV/Ton ($) 76.0 75.4 77.9 87.4 44.7

* Read last page for disclaimer & rating rationale

*

Source: Company, NSPL Research

Institutional Research

HEAD OF RESEARCHVaibhav ChowdhryVaibhav.Chowdhry@ nalandasecurities.com

NALANDA SECURITIES PRIVATE LIMITED310-311 Hubtown Solaris, NS Phadke Marg, Opp Teli Gali, Andheri East, Mumbai 69+91-22-6281-9649 | [email protected] | www.nalandasecurities.com

ASSOCIATEAditya Khetanaditya.khetan@ nalandasecurities.com

60

80

100

120

140

160

180

200

05-2

016

08-2

016

11-2

016

02-2

017

05-2

017

08-2

017

11-2

017

02-2

018

05-2

018

08-2

018

11-2

018

02-2

019

Sanghi Sensex

Sanghi Industries Ltd. | Q4FY19 - Result Update | Page 2

Q4FY19 Result Analysis

(INR Crores) Q4FY19 Q3FY19 Q4FY18 Y-o-Y Q-o-Q

Net Sales 276.0 266.1 253.6 8.8% 3.7%

COGS 26.8 44.0 16.0 67.8% -39.0%

Employee Expenses 10.3 8.5 15.1 -31.5% 21.6%

Power and Fuel 70.2 68.6 67.9 3.3% 2.2%

Freight and Forwarding 10.7 10.8 8.3 28.5% -0.8%

Other Expenses 112.0 102.1 105.1 6.5% 9.7%

Total Expenses 229.9 233.9 212.4 8.3% -1.7%

EBITDA 46.0 32.1 41.3 11.6% 43.2%

Depreciation 13.4 18.7 18.5 -27.4% -28.2%

Other Income 7.4 5.5 13.1 -43.5% 34.2%

EBIT 40.0 19.0 35.9 11.6% 110.7%

Finance Cost 13.6 14.7 17.3 -21.4% -7.5%

PBT 26.4 4.3 18.6 42.1% 513.0%

Taxes 0.0 0.0 0.0 0% 0%

Net Profit 26.4 4.3 18.6 42.1% 513.0%

• The company’s net sales rose 8.8% y-o-y & 3.7% q-o-q to INR 276 crore in Q4FY19.• Raw material cost grew by 67.8% y-o-y & declined by 39.0% to INR 26.8 crore in Q4FY19.• Employee cost declined by 31.5% y-o-y & inclined by 21.6% q-o-q to INR 10.3 crore in Q4FY19.• EBITDA for the company grew by 11.6% y-o-y & 43.2% q-o-q to INR 46 crore with EBITDA margins at 16.7% in Q4FY19 as against

16.3% in Q4FY18 and 12.1% in Q3FY19.• EBITDA/Ton for the quarter stood at INR 681, thereby recording growth of 2.3% y-o-y & 95.3% q-o-q in Q4FY19.• The cement volumes grew by 8.9% y-o-y & and declined by 26.6% q-o-q to 0.675 mt in Q4FY19.• Reported PAT grew by 42.1% y-o-y & 513% q-o-q to INR 26.4 crore in Q4FY19. PAT margins stood at 9.6% in Q4FY19 as against

7.3% in Q4FY18 and 1.6% in Q3FY19.

(INR/Ton) Q4FY19 Q3FY19 Q4FY18 Y-o-Y Q-o-Q

Realization 4089 2892 4090 0.0% 41.4%

RM Cost 397 478 258 53.9% -17.0%

Employee Cost 153 92 244 -37.3% 65.2%

Power and Fuel 1040 746 1095 -5.0% 39.5%

Freight and Forwarding 159 117 134 18.4% 35.0%

Other Expenditure 1659 1110 1695 -2.1% 49.5%

Total Expenditure 3406 2542 3426 -0.6% 34.0%

EBITDA 681 349 666 2.3% 95.3%

Key Concall Highlights• The company reported 70% utilization in Q4FY19 and 65% in FY19 which is below the industry benchmark of 70-75% in FY19.• Blended cement stood at 36% in Q4FY19 as against 31% in Q4FY18 and 33% in Q3FY19.• Realization stood at 4089 per ton on sales volume of 0.625 mt, reporting flat growth y-o-y & 41.4% q-o-q in Q4FY19.• The coal mix is 6% imported coal and remaining is lignite. Dependency on more imported coal mix would gradually lead to

decline in power cost as lignite and coal prices have difference of mere 0.05-0.1 paise/Kcal.• Coal inventory of 4 months is piled up by the company due to which the inventory has shot up by 60.8% y-o-y to INR 237.3 crore

in FY19. Management expects the inventory to remain at the same or upper levels going ahead.• Sales volume breakup in Q4FY19 is 83% Gujarat and remaining 17% others including Maharashtra, kerala etc. Management

indicated Maharashtra sales volume grew by strong growth of 50%. We believe this is owing to strong housing projects kick inmetropolitan regions like Mumbai.

• On the expansion front the management sounded optimistic on completing the scheduled work on time and expects theexpansion to start at 40% utilization at start.

• Q1FY20 to report better pricing growth which remained subdued in Q4FY19, as INR 15-20/kg price increase has taken place inGujarat and expect the pricing to remain stable till Q1FY20 and gradual softening in Q2FY20 owing to monsoon season.

HEAD OF RESEARCHVaibhav ChowdhryVaibhav.Chowdhry@ nalandasecurities.com

NALANDA SECURITIES PRIVATE LIMITED310-311 Hubtown Solaris, NS Phadke Marg, Opp Teli Gali, Andheri East, Mumbai 69+91-22-6281-9649 | [email protected] | www.nalandasecurities.com

ASSOCIATEAditya Khetanaditya.khetan@ nalandasecurities.com

Source: Company, NSPL Research

Realization/Ton (Calculated on sales volume)

Margins inclined sequentially owing to decline in raw material cost

EBITDA/Ton (Calculated on sales volume)

Sanghi Industries Ltd. | Q4FY19 - Result Update | Page 3

HEAD OF RESEARCHVaibhav ChowdhryVaibhav.Chowdhry@ nalandasecurities.com

NALANDA SECURITIES PRIVATE LIMITED310-311 Hubtown Solaris, NS Phadke Marg, Opp Teli Gali, Andheri East, Mumbai 69+91-22-6281-9649 | [email protected] | www.nalandasecurities.com

ASSOCIATEAditya Khetanaditya.khetan@ nalandasecurities.com

910

826

502

541

968

977

848

666

638

523

349

681

-9%

-39

%

8%

6%

18%

69

%

23%

-34

%

-46

%

-59

%

2%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

0

200

400

600

800

1000

1200

Q1

FY1

7

Q2

FY1

7

Q3

FY1

7

Q4

FY1

7

Q1

FY1

8

Q2

FY1

8

Q3

FY1

8

Q4

FY1

8

Q1

FY1

9

Q2

FY1

9

Q3

FY1

9

Q4

FY1

9

%INR

EBITDA/Ton % Growth YoY

65 47 42 42 66 47 62 41 43 32

32

46

24.3

%

22.8

%

15.6

%

17.2

%

22.9

%

22.7

%

22.1

%

16.3

%

15.8

%

13.3

%

12.1

%

16.7

%

11%

13%

15%

17%

19%

21%

23%

25%

0

10

20

30

40

50

60

70

Q1

FY1

7

Q2

FY1

7

Q3

FY1

7

Q4

FY1

7

Q1

FY1

8

Q2

FY1

8

Q3

FY1

8

Q4

FY1

8

Q1

FY1

9

Q2

FY1

9

Q3

FY1

9

Q4

FY1

9

%

INR

Cro

res

EBITDA EBITDA Margin

37

52

36

25

3220

31

54

43

23

43

01

38

30

40

90

40

42

39

37

28

92

40

89

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

Q1

FY1

7

Q2

FY1

7

Q3

FY1

7

Q4

FY1

7

Q1

FY1

8

Q2

FY1

8

Q3

FY1

8

Q4

FY1

8

Q1

FY1

9

Q2

FY1

9

Q3

FY1

9

Q4

FY1

9

INR

Realizations per tonn

Profit & Loss (INR Crores) FY17 FY18 FY19 FY20E FY21E

Net sales 997.5 1026.4 1105.8 1206.2 1302.7

COGS 78.9 66.4 97.2 107.1 118.0

Employee Expenses 52.5 53.9 41.7 45.4 50.0

Power and fuel 231.0 242.8 298.6 329.0 355.3

Transportation cost 333.3 333.0 366.8 404.0 436.4

Other Expenses 103.6 114.4 102.6 106.7 111.0

EBITDA 198.2 215.8 154.0 213.9 232.1

D&A 73.1 72.4 71.3 79.5 88.0

Other income 2.2 22.0 27.3 20.0 26.3

EBIT 127.4 165.4 109.9 154.5 170.4

Interest Expense 64.2 72.1 57.3 67.7 78.0

PBT 63.1 93.3 52.6 86.8 92.5

Tax 0.0 0.0 0.0 0.0 0.0

PAT 63.1 93.3 52.6 86.8 92.47

EPS 2.87 3.72 2.1 3.46 3.68

Balance Sheet (INR Crores) FY17 FY18 FY19 FY20E FY21E

Share Capital 220.0 251.0 251.0 251.0 251.0

Reserves & Surplus 894.0 1,346.9 1,399.4 1,486.2 1,578.6

Shareholder's Funds 1,114.0 1,597.9 1,650.4 1,737.2 1,829.6

Long-term borrowings 459.0 550.8 538.9 718.9 748.9

Other non-current liabilities 102.6 73.6 57.2 57.2 57.2

Long term provisions 48.1 38.3 38.4 38.3 38.3

Non-current liabilities 609.7 662.8 634.5 814.4 844.4

Short-term borrowings 127.8 163.0 217.0 217.0 217.0

Trade payables 142.1 132.7 193.0 220.1 242.5

Other current liabilities 61.7 77.8 105.6 105.6 105.6

Short-term provisions 10.3 20.2 32.9 20.2 20.2

Current liabilities 341.9 393.7 548.7 563.0 585.3

Total Equity and Liabilities 2,065.6 2,654.3 2,833.6 3,114.6 3,259.4

Gross Block 2,749.1 3,008.2 3,315.7 3,798.2 3,998.2

Less: Accum. Depreciation 1,130.1 1,202.5 1,273.8 1,353.3 1,441.3

Net Fixed Assets 1,619.0 1,802.3 2,041.9 2,444.9 2,556.9

Deferred Tax Assets 58.5 87.1 86.0 86.0 86.0

Other Non-current Assets - 33.7 103.4 103.4 103.4

Non-current Assets 1,677.5 1,923.1 2,231.3 2,634.3 2,746.4

Inventories 186.6 147.5 237.3 264.2 284.5

Trade receivables 23.9 32.1 44.2 52.9 64.2

Bank balance 16.1 427.6 428.6 428.6 428.6

Cash and cash equivalents 16.3 428.1 166.7 9.1 10.2

Other current assets 161.3 123.7 154.1 154.1 154.1

Current Assets 388.1 731.3 602.2 480.2 513.0

Total Assets 2,065.6 2,654.3 2,833.6 3,114.6 3,259.4

Sanghi Industries Ltd. | Q4FY19 - Result Update | Page 4

HEAD OF RESEARCHVaibhav ChowdhryVaibhav.Chowdhry@ nalandasecurities.com

NALANDA SECURITIES PRIVATE LIMITED310-311 Hubtown Solaris, NS Phadke Marg, Opp Teli Gali, Andheri East, Mumbai 69+91-22-6281-9649 | [email protected] | www.nalandasecurities.com

ASSOCIATEAditya KhetanAditya.khetan@ nalandasecurities.com

Source: Company, NSPL Research

RATIOS FY17 FY18 FY19 FY20E FY21E

Particulars

EBITDA/Ton 678.8 862.5 577.0 742.1 745.5

Sales Volume (Mn tons) 2.9 2.5 2.7 2.9 3.1

Growth (%)

Total Sales -2% -5% 1% 14% 8%

EBITDA -2% 9% -29% 39% 8%

PAT -38% 48% -44% 65% 7%

Profitability (%)

EBITDA Margin 19.9% 21.0% 13.9% 17.7% 17.8%

NPM 6.3% 9.1% 4.8% 7.2% 7.1%

RoE (%) 5.7% 5.8% 3.2% 5.0% 5.1%

RoCE (%) 6.9% 6.8% 4.4% 5.6% 5.9%

Debt Ratios

Net Debt/EBITDA 2.9 1.4 3.8 4.3 4.1

Net Debt/Equity 0.5 0.2 0.4 0.5 0.5

Interest Coverage 2.0 2.3 1.9 2.3 2.2

Per share data / Valuation

EPS (INR.) 2.9 3.7 2.1 3.5 3.7

BPS (INR.) 50.7 63.7 65.8 69.2 72.9

P/E (x) 23.9 18.0 30.1 18.2 17.1

EV/EBITDA (x) 10.5 9.2 14.1 11.7 10.9

EV/Ton ($) 76.0 75.4 77.9 87.4 44.7

Cash Flow (INR Crores) FY17 FY18 FY19 FY20E FY21E

PBT 63.0 93.4 52.6 86.8 92.5

Depreciation & Amortization 73.1 72.4 71.3 79.5 88.0

(Incr)/Decr in Working Capital 199.8 222.3 181.3 234.0 258.4

Cash Flow from Operating 76.0 221.8 63.8 212.6 249.0

(Incr)/ Decr in Gross PP&E -75.2 -289.1 -310.9 -482.5 -200.0

Cash Flow from Investing -7.9 -684.4 -310.9 -482.5 -200.0

(Decr)/Incr in Debt 2.1 140.5 42.1 180.0 30.0

Finance costs -70.3 -68.2 -57.3 -67.7 -78.0

Cash Flow from Financing -68.2 462.9 -15.2 112.3 -48.0

Incr/(Decr) in Balance Sheet Cash -0.1 0.2 -262.3 -157.6 1.1

Cash at the Start of the Year 0.2 0.2 0.4 -261.9 -419.5

Cash at the End of the Year 0.2 0.4 -261.9 -419.5 -418.4

Cash and Bank Balances 16.3 428.1 166.7 9.1 10.2

Sanghi Industries Ltd. | Q4FY19 - Result Update | Page 5

HEAD OF RESEARCHVaibhav ChowdhryVaibhav.Chowdhry@ nalandasecurities.com

NALANDA SECURITIES PRIVATE LIMITED310-311 Hubtown Solaris, NS Phadke Marg, Opp Teli Gali, Andheri East, Mumbai 69+91-22-6281-9649 | [email protected] | www.nalandasecurities.com

ASSOCIATEAditya Khetanaditya.khetan@ nalandasecurities.com

Source: Company, NSPL Research

OUR RECENT REPORTS

Dalmia Bharat Coromandel International Meghmani Organics IndoStar Capital

Minda Industries Sharda Cropchem Heidelberg Cements Manappuram Finance

Prataap Snacks Aarti Industries Shriram TransportIG Petrochemicals

Disclaimer:This report has been prepared by Nalanda Securities Pvt. Ltd(“NSPL”) and published in accordance with the provisions of Regulation 18 of the Securities and Exchange Board of India(Research Analysts) Regulations, 2014, for use by the recipient as information only and is not for circulation or public distribution. NSPL includes subsidiaries, group and associatecompanies, promoters, directors, employees and affiliates. This report is not to be altered, transmitted, reproduced, copied, redistributed, uploaded, published or made available toothers, in any form, in whole or in part, for any purpose without prior written permission from NSPL. The projections and the forecasts described in this report are based upon anumber of estimates and assumptions and are inherently subject to significant uncertainties and contingencies. Projections and forecasts are necessarily speculative in nature, and itcan be expected that one or more of the estimates on which the projections are forecasts were based will not materialize or will vary significantly from actual results and suchvariations will likely increase over the period of time. All the projections and forecasts described in this report have been prepared solely by authors of this report independently.None of the forecasts were prepared with a view towards compliance with published guidelines or generally accepted accounting principles.This report should not be construed as an offer to sell or the solicitation of an offer to buy, purchase or subscribe to any securities, and neither this report nor anything containedtherein shall form the basis of or be relied upon in connection with any contract or commitment whatsoever. It does not constitute a personal recommendation or take into accountthe particular investment objective, financial situation or needs of individual clients. The research analysts of NSPL have adhered to the code of conduct under Regulation 24 (2) ofthe Securities and Exchange Board of India (Research Analysts) Regulations, 2014. The recipients of this report must make their own investment decisions, based on their owninvestment objectives, financial situation or needs and other factors. The recipients should consider and independently evaluate whether it is suitable for its/ his/ her/their particularcircumstances and if necessary, seek professional / financial advice as there is substantial risk of loss. NSPL does not take any responsibility thereof. Any such recipient shall beresponsible for conducting his/her/its/their own investigation and analysis of the information contained or referred to in this report and of evaluating the merits and risks involved insecurities forming the subject matter of this report. The price and value of the investment referred to in this report and income from them may go up as well as down, and investorsmay realize profit/loss on their investments. Past performance is not a guide for future performance. Actual results may differ materially from those set forth in the projection.Except for the historical information contained herein, statements in this report, which contain words such as ‘will’, ‘would’, etc., and similar expressions or variations of such wordsmay constitute ‘forward‐looking statements’. These forward‐looking statements involve a number of risks, uncertainties and other factors that could cause actual results to differmaterially from those suggested by the forward‐looking statements. Forward‐looking statements are not predictions and may be subject to change without notice. NSPL undertakesno obligation to update forward‐looking statements to reflect events or circumstances after the date thereof. NSPL accepts no liabilities for any loss or damage of any kind arising outof use of this report.This report has been prepared by NSPL based upon the information available in the public domain and other public sources believed to be reliable. Though utmost care has beentaken to ensure its accuracy and completeness, no representation or warranty, express or implied is made by NSPL that such information is accurate or complete and/or isindependently verified. The contents of this report represent the assumptions and projections of NSPL and NSPL does not guarantee the accuracy or reliability of any projection,assurances or advice made herein. Nothing in this report constitutes investment, legal, accounting and/or tax advice or a representation that any investment or strategy is suitable orappropriate to recipients’ specific circumstances. This report is based / focused on fundamentals of the Company and forward‐looking statements as such, may not match with areport on a company’s technical analysis report. This report may not be followed by any specific event update/ follow‐up.

Following table contains the disclosure of interest in order to adhere to utmost transparency in the matter;

Disclosure of Interest Statement

Details of Nalanda Securities Pvt. Limited (NSPL)

• NSPL is a Stock Broker registered with BSE, NSE and MCX ‐ SX in all the major

segments viz. Cash, F & O and CDS segments. Further, NSPL is a Registered

Portfolio Manager and is registered with SEBI

• SEBI Registration Number: INH000004617

Details of Disciplinary History of NSPL No disciplinary action is / was running / initiated against NSPL

Research analyst or NSPL or its relatives'/associates' financial interest in

the subject company and nature of such financial interest

No (except to the extent of shares held by Research analyst or NSPL or its

relatives'/associates')

Whether Research analyst or NSPL or its relatives'/associates' is holding

the securities of the subject companyNO

Research analyst or NSPL or its relatives'/associates' actual/beneficial

ownership of 1% or more in securities of the subject company, at the

end of the month immediately preceding the date of publication of the

document

NO

Research analyst or NSPL or its relatives'/associates' any other material

conflict of interest at the time of publication of the documentNO

Has research analyst or NSPL or its associates received any compensation

from the subject company in the past 12 monthsNO

Has research analyst or NSPL or its associates managed or co‐managed

public offering of securities for the subject company in the past 12 monthNO

Has research analyst or NSPL or its associates received any compensation

for investment banking or merchant banking or brokerage services from

the subject company in the past 12 months

NO

Has research analyst or NSPL or its associates received any compensation

for products or services other than investment banking or merchant

banking or brokerage services from the subject company in the past 12

months

NO

Has research analyst or NSPL or its associates received any compensation

or other benefits from the subject company or third party in connection

with the document.

NO

Has research analyst served as an officer, director or employee of the

subject companyNO

Has research analyst or NSPL engaged in market making activity for the

subject companyNO

Other disclosures NO

Rating Legend

Strong Buy More than 15%

Buy 5% - 15%

Hold 0 – 5%

Reduce -5% - 0

Sell Less than -5%

Sanghi Industries Ltd.

Date CMP (INR) Target Price (INR) Recommendation

May 22, 2019 63 75 Strong Buy

November 19, 2018 63 86 Strong Buy

August 09, 2018 87 104 Strong Buy

Sanghi Industries Ltd. | Q4FY19 - Result Update | Page 7

HEAD OF RESEARCHVaibhav ChowdhryVaibhav.Chowdhry@ nalandasecurities.com

NALANDA SECURITIES PRIVATE LIMITED310-311 Hubtown Solaris, NS Phadke Marg, Opp Teli Gali, Andheri East, Mumbai 69+91-22-6281-9649 | [email protected] | www.nalandasecurities.com

ASSOCIATEAditya Khetanaditya.khetan@ nalandasecurities.com

Related Documents