aegon.com Tim Gilmour Chief Marketing Officer DATE: October 2013 MAXIMISING VALUE FROM DIRECT MARKETING: CUSTOMER ENGAGEMENT

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

aegon.com

Tim Gilmour

Chief Marketing Officer

DATE: October 2013

MAXIMISING VALUE FROM DIRECT MARKETING:

CUSTOMER ENGAGEMENT

2

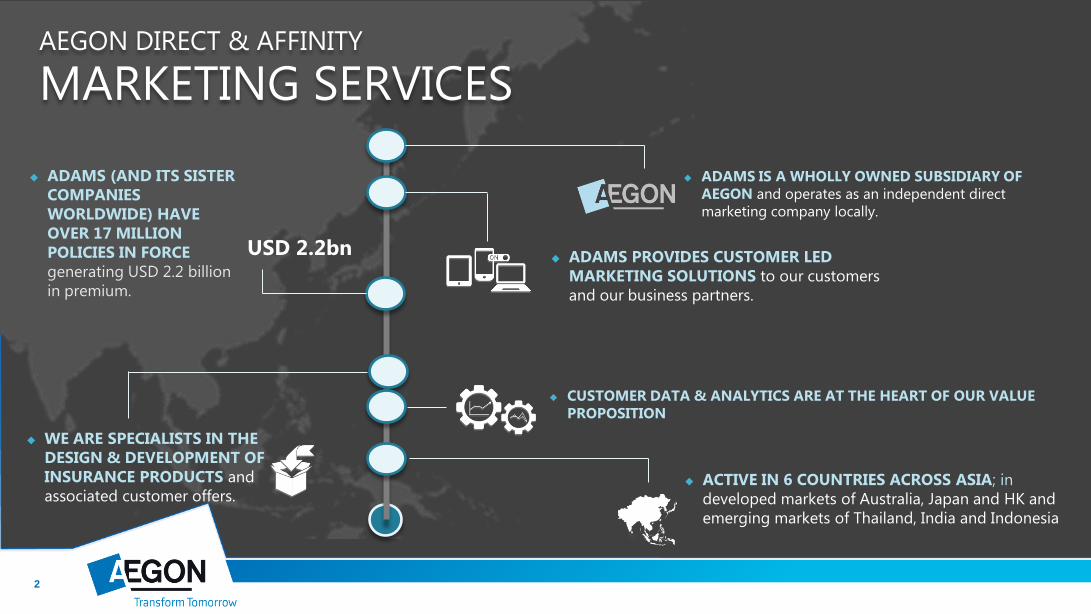

AEGON DIRECT & AFFINITY

MARKETING SERVICES

ADAMS IS A WHOLLY OWNED SUBSIDIARY OF AEGON and operates as an independent direct marketing company locally.

ADAMS PROVIDES CUSTOMER LED MARKETING SOLUTIONS to our customers and our business partners.

WE ARE SPECIALISTS IN THE DESIGN & DEVELOPMENT OF INSURANCE PRODUCTS and associated customer offers.

CUSTOMER DATA & ANALYTICS ARE AT THE HEART OF OUR VALUE PROPOSITION

ACTIVE IN 6 COUNTRIES ACROSS ASIA; in developed markets of Australia, Japan and HK and emerging markets of Thailand, India and Indonesia

USD 2.2bn

ADAMS (AND ITS SISTER COMPANIES WORLDWIDE) HAVE OVER 17 MILLION POLICIES IN FORCE generating USD 2.2 billion in premium.

3

ADAMS FOOTPRINT IN ASIA

AUSTRALIA Since 1999

INDIA Since 2008

INDONESIA Since 2012

HONG KONG Since 2006

JAPAN Since 2001

THAILAND Since 2005

4

CUSTOMER ENGAGEMENT

MOBILE

TECHNOLOGY

BIG DATA

DIGITAL

E-COMMERCE

MY AGENDA TODAY

5

DIRECT MARKETING TODAY OBTM, push strategies have been/are the norm – call list for commission

Traditional channels coming under threat for a number of reasons including:

Products lack real relevance – (maybe our industry does too??) Customer’s are using a different buying cycle Digital is changing the way customers interact Mobile means people are always connected and have access to information Data is more protected than ever and you need customer’s permission to use it Some database owners are short term in their approach – increased demands, lack of customer centricity, burn

out E-commerce is having some success Aggregators – what’s that all about?

Everybody is now talking about Digital & E-commerce & Social Media & Technology & Big Data & Mobile Platforms &

Innovations

So what will direct marketing look like TOMORROW?

6

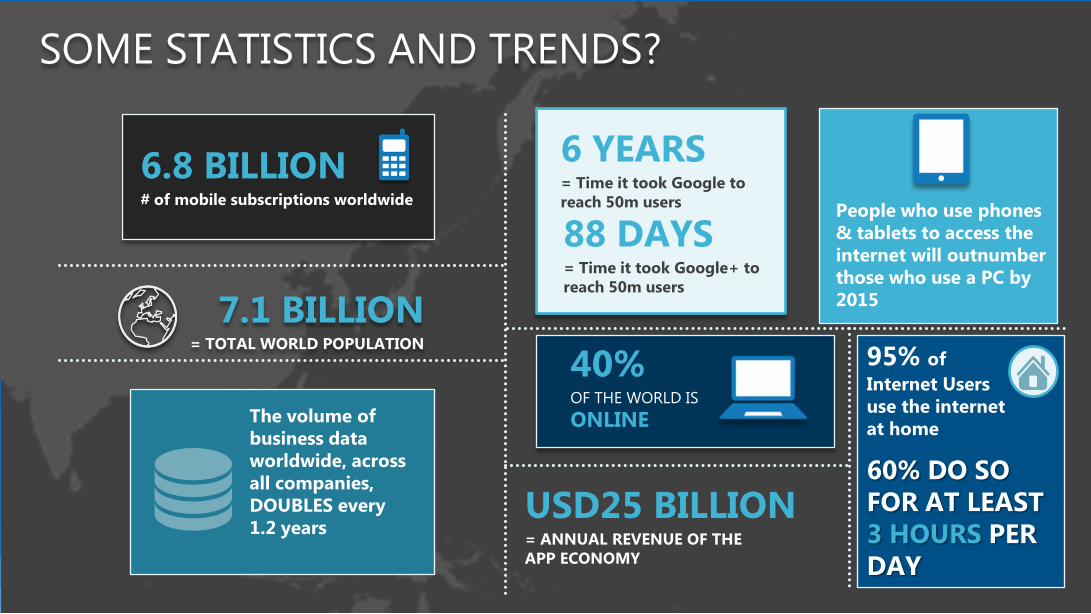

SOME STATISTICS AND TRENDS?

6 YEARS = Time it took Google to reach 50m users

88 DAYS = Time it took Google+ to reach 50m users

6.8 BILLION # of mobile subscriptions worldwide

7.1 BILLION = TOTAL WORLD POPULATION

40% OF THE WORLD IS

ONLINE

People who use phones & tablets to access the internet will outnumber those who use a PC by 2015

95% of

Internet Users use the internet at home

60% DO SO FOR AT LEAST 3 HOURS PER DAY

USD25 BILLION = ANNUAL REVENUE OF THE APP ECONOMY

The volume of business data worldwide, across all companies, DOUBLES every 1.2 years

7

AND SOME MORE STATS …. (SEEMS TO BE ALL ABOUT DIGITAL)

68% OF LIFE INSURERS IN ASIA SAY THAT “integrating digital and media with other distribution channels” is

the top challenge they face in delivering their digital strategy*

Asia Pacific insurers attribute slow digital growth to LEGACY TECHNOLOGY ISSUES (63%), but also blames REGULATION (44%), a lack of compelling BUSINESS CASE (41%) and PERCEIVED CUSTOMER DATA/SECURITY ISSUES (40%) *

79% of Asia insurers “ONLY PLAY THE DIGITAL GAME” or are “still learning to use digital capabilities for a competitive advantage”

57% say that CURRENT OPERATING MODELS DO NOT FACILITATE DIGITAL STRATEGY and 47% have no business case of no unified digital strategy*

NEARLY 70% of insurers spend LESS THAN 10% of business and IT development budgets on digital*

ONLY 10% HAVE MADE TRANSFORMATIONAL CHANGES to digital capabilities*

*Ernst & Young Digital Survey 2013

8

“Enriching the customer experience” and “regaining more direct control of the customer relationship” through a meaningful customer engagement strategy is the key to success

9

CUSTOMER ENGAGEMENT – WHAT IS IT?

Not just a product sale…… it’s about maximising lifetime value

It incorporates:

A 2-way process – between you, and your customer

A strong Customer Value Proposition that keeps them coming back

Must have relevance - product, language, positioning, content, ongoing dialogue.

A mutually beneficial relationship. One built on trust, honesty, transparency and mutual need

Requires constant evolution to make sure it stays relevant, and needed

Incorporates digital communication & e-commerce and other channel integration

Promotes a willing exchange of data

Founded on the ability to manage that data and drive insights that will improve the UX

Facilitated by technology & software - CRM

MOBILE

TECHNOLOGY

BIG DATA

DIGITAL

E-COMMERCE

CHANNEL INTEGRATION

10

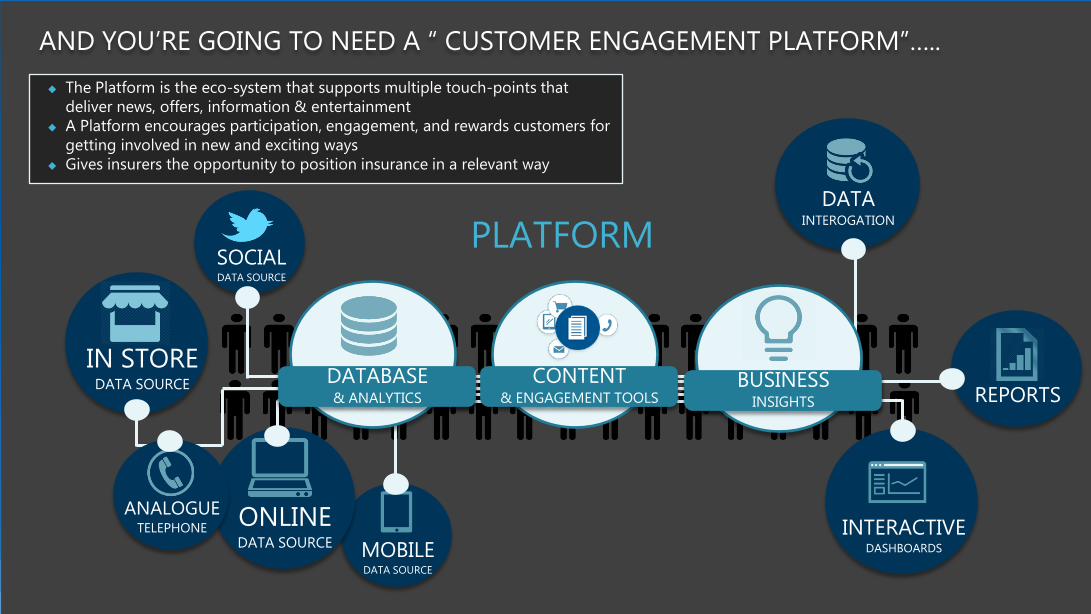

AND YOU’RE GOING TO NEED A “ CUSTOMER ENGAGEMENT PLATFORM”…..

SOCIAL DATA SOURCE

MOBILE DATA SOURCE

ONLINE DATA SOURCE

REPORTS

INTERACTIVE DASHBOARDS

DATA INTEROGATION

PLATFORM

IN STORE DATA SOURCE

The Platform is the eco-system that supports multiple touch-points that deliver news, offers, information & entertainment

A Platform encourages participation, engagement, and rewards customers for getting involved in new and exciting ways

Gives insurers the opportunity to position insurance in a relevant way

DATABASE & ANALYTICS

ANALOGUE TELEPHONE

CONTENT & ENGAGEMENT TOOLS

BUSINESS INSIGHTS

11

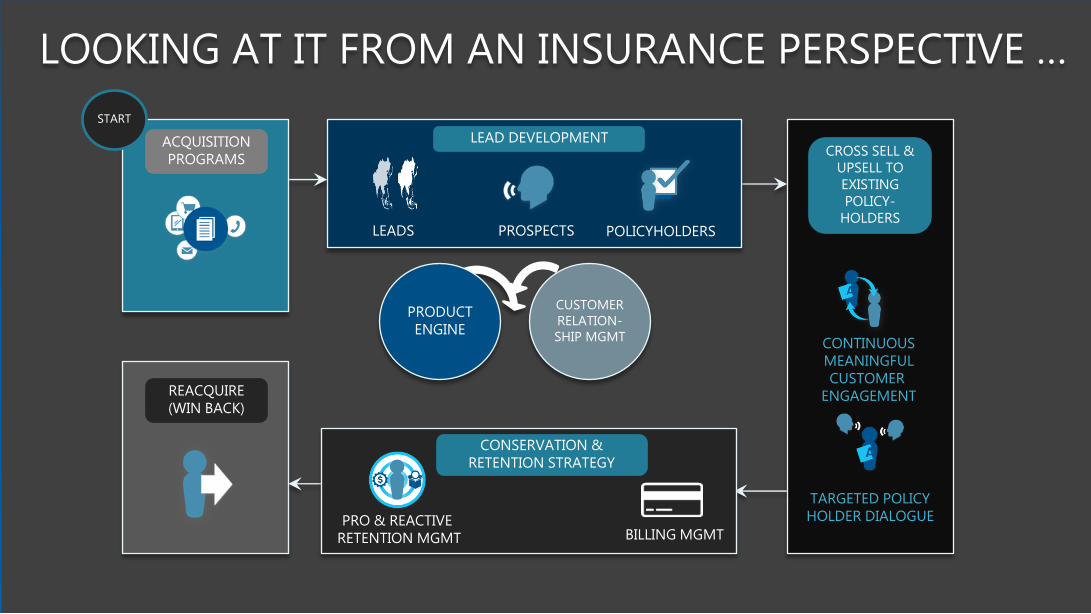

CROSS SELL & UPSELL TO EXISTING POLICY-

HOLDERS

TARGETED POLICY HOLDER DIALOGUE

CONTINUOUS MEANINGFUL CUSTOMER

ENGAGEMENT REACQUIRE (WIN BACK)

LEADS PROSPECTS POLICYHOLDERS

LEAD DEVELOPMENT ACQUISITION PROGRAMS

CONSERVATION & RETENTION STRATEGY

PRO & REACTIVE RETENTION MGMT BILLING MGMT

PRODUCT ENGINE

CUSTOMER RELATION-SHIP MGMT

LOOKING AT IT FROM AN INSURANCE PERSPECTIVE …

START

12

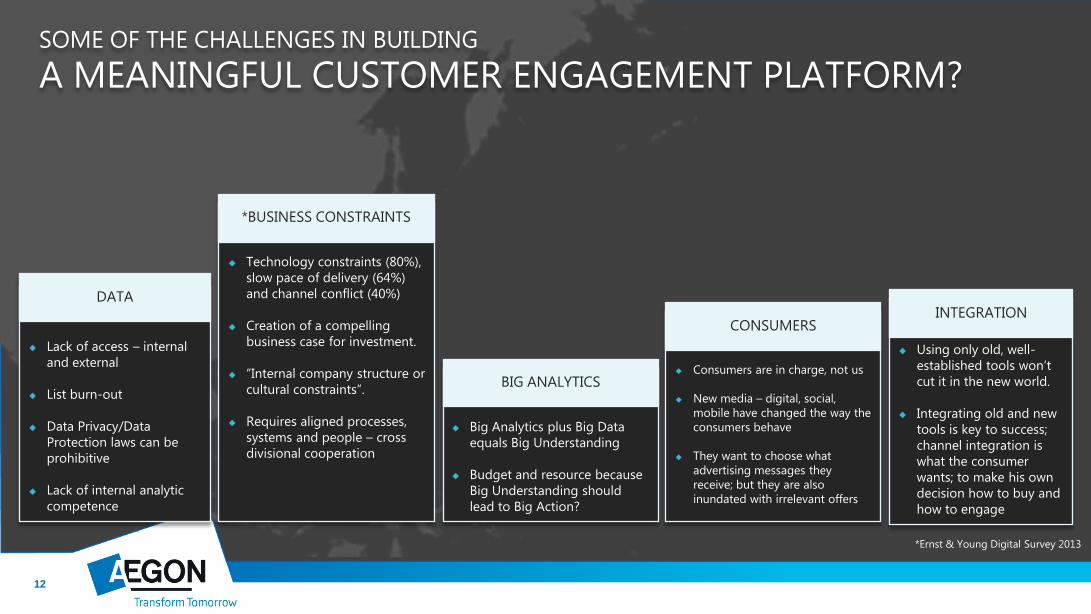

SOME OF THE CHALLENGES IN BUILDING

A MEANINGFUL CUSTOMER ENGAGEMENT PLATFORM?

Consumers are in charge, not us

New media – digital, social, mobile have changed the way the consumers behave

They want to choose what advertising messages they receive; but they are also inundated with irrelevant offers

CONSUMERS

Big Analytics plus Big Data equals Big Understanding

Budget and resource because Big Understanding should lead to Big Action?

BIG ANALYTICS

Using only old, well-established tools won’t cut it in the new world.

Integrating old and new tools is key to success; channel integration is what the consumer wants; to make his own decision how to buy and how to engage

INTEGRATION

Technology constraints (80%), slow pace of delivery (64%) and channel conflict (40%)

Creation of a compelling business case for investment.

“Internal company structure or cultural constraints”.

Requires aligned processes, systems and people – cross divisional cooperation

*BUSINESS CONSTRAINTS

*Ernst & Young Digital Survey 2013

Lack of access – internal and external

List burn-out

Data Privacy/Data

Protection laws can be prohibitive

Lack of internal analytic competence

DATA

13

DATA

DATA DRIVEN INSIGHTS SHOULD BE DRIVING CHANGE IN YOUR

BUSINESS A strong intelligence function is becoming increasingly more important for companies

Fact based marketing Risk analysis and management Fraud detection Process improvements Product enhancements Predictive underwriting Brand building Reward and recognition

Meaningful customer engagement demands thorough

customer insight

Segments – sub-segments – groups - individuals

FOR THOSE COMPANIES WITHOUT A MEANINGFUL DATA STRATEGY

THINGS ARE GOING TO GET MORE CHALLENGING BECAUSE

1. The volume, variety and timeliness of information e.g.

social media

2. The proliferation of channels – online and mobile

3. Advances in computing power and improvements in software.

14

MARKET INNOVATIONS

15

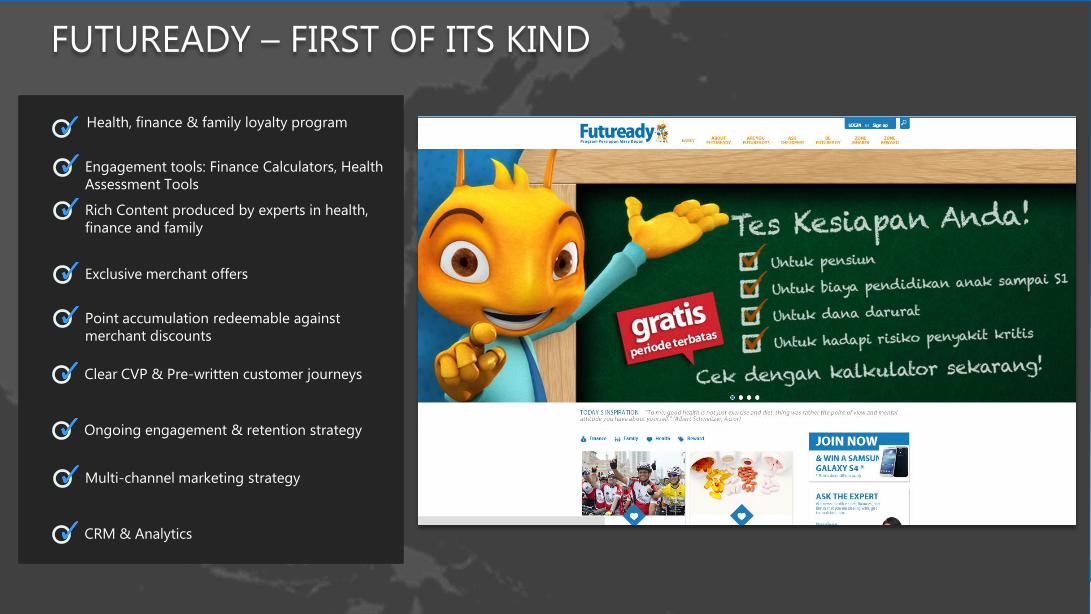

FUTUREADY – FIRST OF ITS KIND

Health, finance & family loyalty program

Engagement tools: Finance Calculators, Health Assessment Tools

Rich Content produced by experts in health, finance and family

Exclusive merchant offers

Point accumulation redeemable against merchant discounts

Clear CVP & Pre-written customer journeys

Ongoing engagement & retention strategy

Multi-channel marketing strategy

CRM & Analytics

16

DIRECT MARKETING INNOVATIONS IN THE NEW WORLD

DISCOVERY VITALITY

Discovery Life has been successful in tapping into a wealth of consumer data through its Discovery Vitality program – an incentive plan initially set up to promote better claims experience for the company’s health business

It uses innovative techniques to obtain consumer data through online health assessments and wristbands that record real-time fitness levels

This wealth of data and advanced analytics enables them to take advantage of robust underwriting and pricing techniques which has given them a competitive advantage in S.Africa

The access to real-time data enables DL to be responsive to emerging trends

Analytics Engagement & Retention Membership

17

DIRECT MARKETING INNOVATIONS IN THE NEW WORLD

TELEMATIC

Insurance providers can now fit a telematics device into your car that measures how well you drive

This enables the consumer to prove how safely he drives

Premiums are then based on how safe and conscientious they are instead of paying for an average across all drivers.

18

DIRECT MARKETING INNOVATIONS IN THE NEW WORLD

TUNE INSURANCE

Tune Group, which is owned in part by the low-cost airline AirAsia, launched an online insurer to leverage the airline’s extensive digital infrastructure (namely the significant customer database of its online ticketing and reservations system). It offers travel insurance to customers when they book

Tune Insurance sold 6m policies in 2012, and has sold 3.65m policies in 1H 2013 across 13 countries including Malaysia, Indonesia, Thailand, Singapore and China.

The insurer has added 1,000 agents and 15 branches across Malaysia and a wider range of non-life products.

Their goal is to be recognized as ASEAN’S leading regional digital insurance franchise by 2015

Cross & Upsell Leverages existing digital

assets Channel integration

19

DIRECT MARKETING INNOVATIONS IN THE NEW WORLD

KROODLE

Kroodle uses the most innovative technology & facebook integration to enable people to access an insurance that is completely digital and mobile

It is completely digital eg. Submitting an insurance claim is done via facebook thus consumers have full transparency of what they are getting and what others are getting

Purchasing insurance is done on facebook – you start on the Kroodle homepage but the purchase process is then integrated with facebook pulling all of your personal information to complete the transaction

No signature required, no paperwork

Leveraging social media to create consumer communities

Channel Integration

Related Documents