Report No. 53241-MR Mauritania: Restarting the Reform Program Sector Policy Notes May 2010 AFTP4 Africa Region World Bank Report Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Report No. 53241-MR

Mauritania: Restarting the Reform Program

Sector Policy Notes

May 2010

AFTP4 Africa Region

World Bank Report

Pub

lic D

iscl

osur

e A

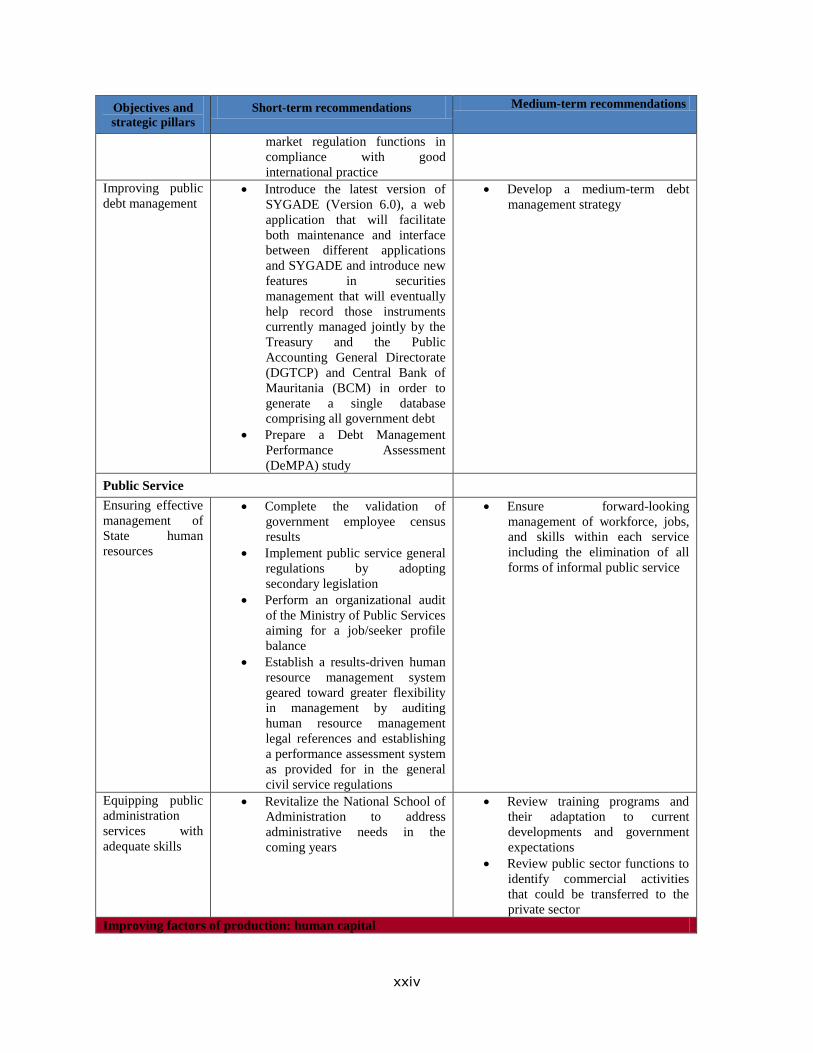

utho

rized

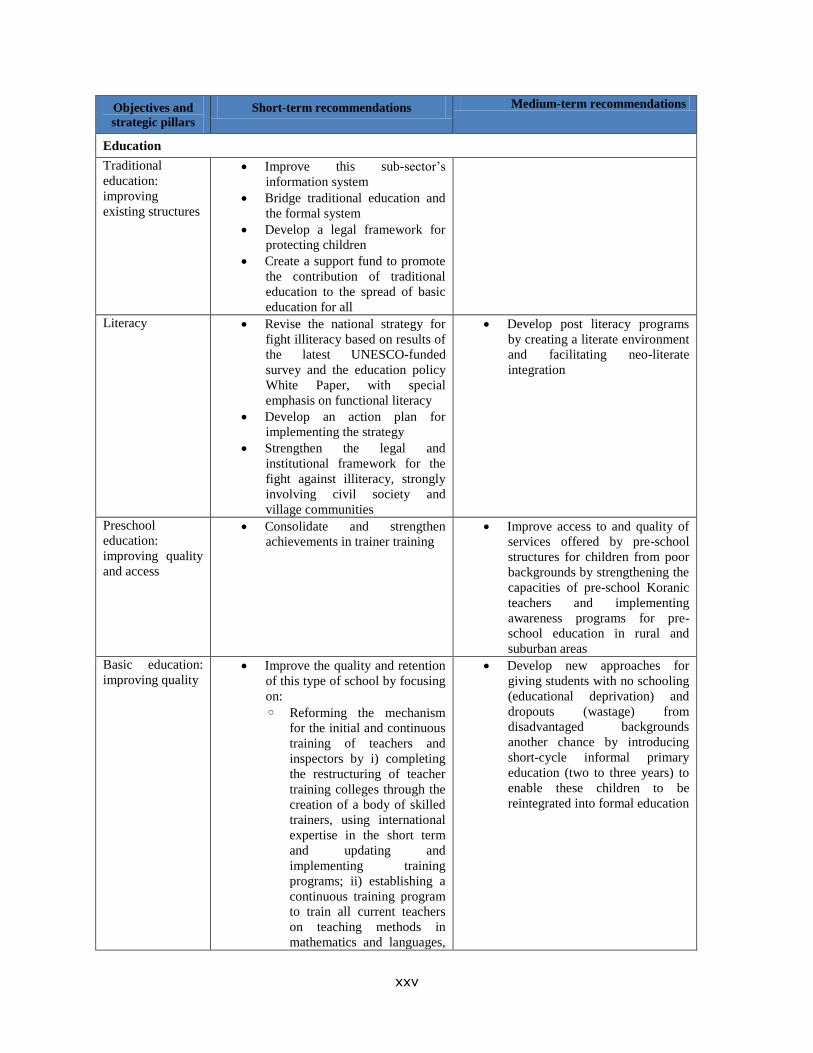

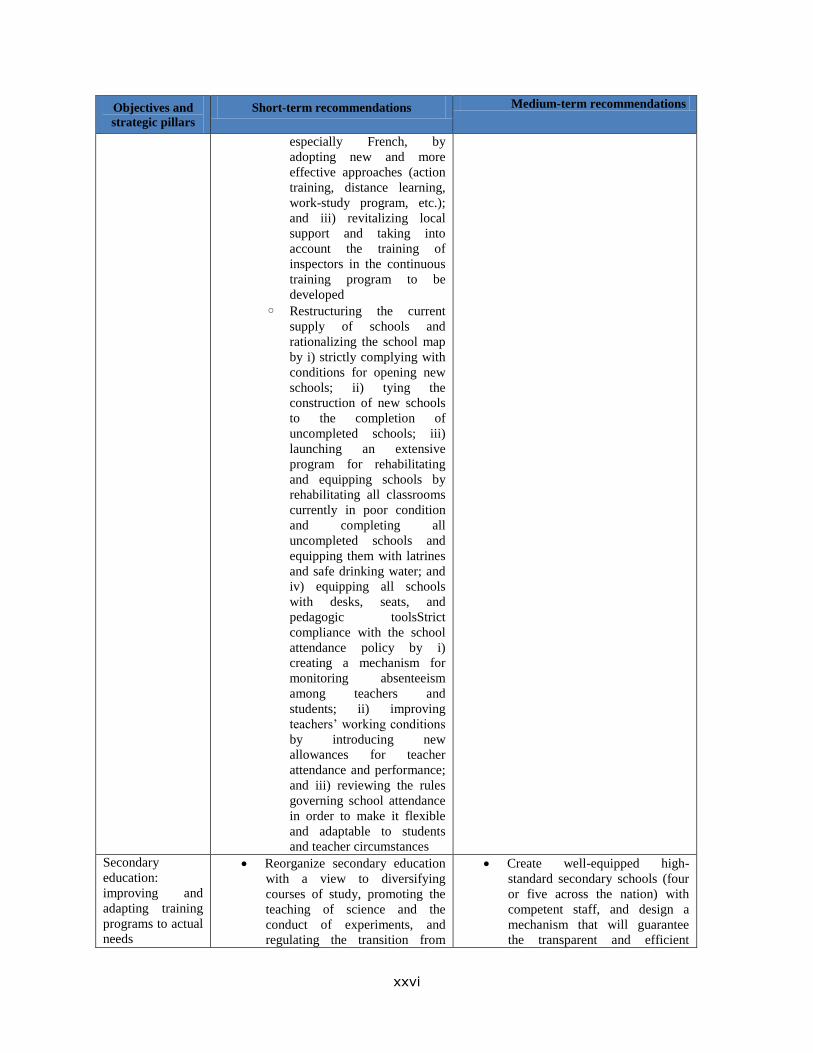

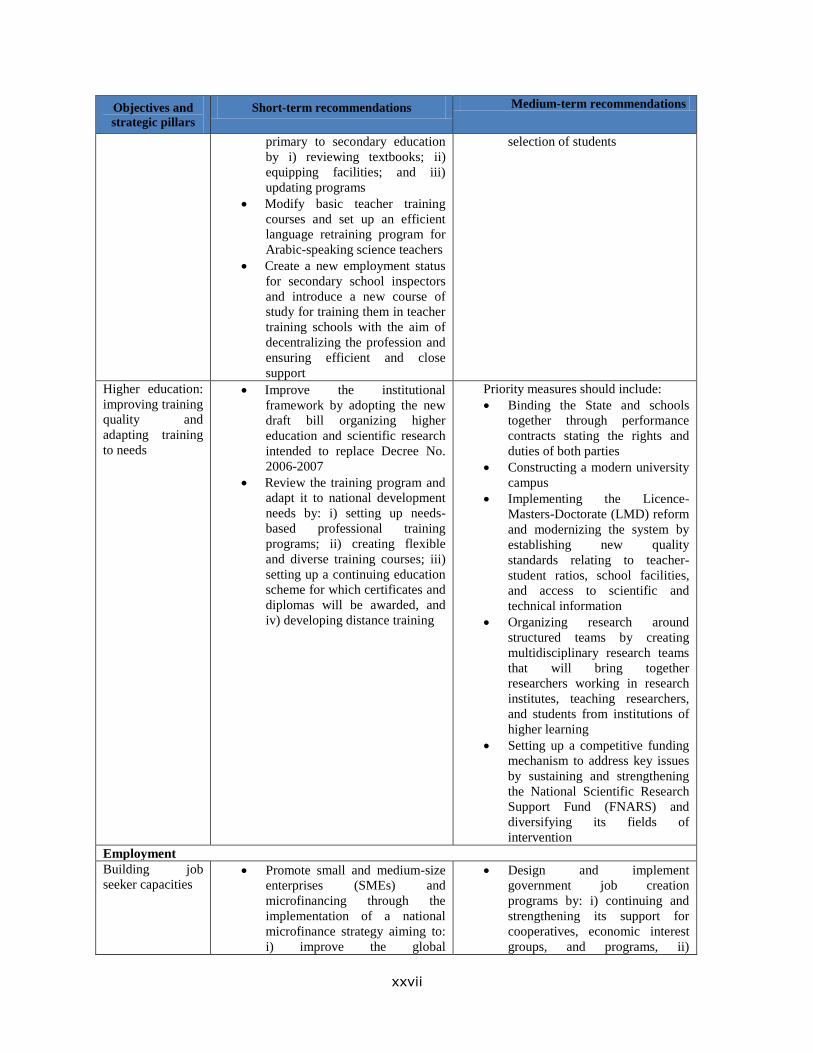

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

i

EXCHANGE RATES

(as of April 16, 2010)

United States Dollar = Mauritanian Ouguiya

USD 1 = MRO 261

FINANCIAL YEAR

January 1–December 31

TABLES OF ABBREVIATIONS AND ACRONYMS

AAAID Arab Authority Cooperation Accord for Agricultural Investment and Development

(Accord de Coopération avec l’Autorité Arabe pour les Investissements et le

Développement Agricoles)

ADER Rural Electrification Development Agency (Agence pour le Développement de

l'Electrification Rurale)

AEP Agricultural Economics Program

AFD French Development Agency (Agence Française de Développement)

AfDB African Development Bank

AFRITAC African Regional Technical Assistance Center

AIDS Auto-immune Deficiency Syndrome

AMEXTIPE Mauritanian Agency for the Implementation of Employment-related Public Works

(Agence Mauritanienne d'Exécution des Travaux d'Intérêt Public pour l'Emploi)

ANAPEJ National Agency for the Promotion of Youth Employment (Agence Nationale de

Promotion d’Emploi des Jeunes)

ANEPA National Safe Drinking Water and Sanitation Agency (Agence Nationale d’Eau Potable

et d’Assainissement)

AOP Annual Operational Plan

APAUS Agency for the Promotion of Universal Access to Basic Services (Agence pour la

Promotion de l’Accès Universel aux Services)

ARE Economic Regulation Authority (Agence de Régulation Economique)

ATPC African Trade Policy Center

BAC-T Technical Baccalauréat (Baccalauréat Technique)

BCM Central Bank of Mauritania (Banque Centrale de Mauritanie)

BEP Professional Studies Diploma (Brevet d'Etudes Professionnelles)

BNT National Transportation Unit (Bureau National de Transport)

BP Budget Program

BT Technical Diploma (Brevet de Technicien)

BTS Advanced Technical Diploma (Brevet de Technicien Supérieur)

CAMEC Medication, Medical Equipment, and Medical Consumables Central Purchasing Unit

(Centrale d'Achat des Médicaments, du Matériel, et du Consommable Médical)

CAP Professional Aptitude Certificate (Certificat d'Aptitudes Professionelles)

CBA Competence-based Approach

CBMT Medium-term Budgetary Framework (Cadre Budgétaire à Moyen Terme)

CCEG Conference of Heads of States and Governments of OMVS Countries (Conférence des

Chefs d’État et des Gouvernements de l’OMVS)

CCI Chamber of Commerce and Industry

CCM Central Commission for Markets (Commission Centrale des Marchés)

CDI Tax Office (Centre des Impôts)

ii

CDMF Common Data Management Facility

CDMT Medium Term Expenditure Framework (Cadre de Dépenses à Moyen Terme)

CDSS Social and Healthcare Development Council (Conseil de Développement Socio-sanitaire)

CE Spanish Development Aid (Cooperación Española)

CEM Country Economic Memorandum

CF French Development Aid (Coopération Française)

CFPP Professional and Technical Training Center (Centre de Formation Professionelle et

Technique)

CGA Certified Management Center (Centre de Gestion Agréé)

CIB Consolidated Investment Budget

CMAP Mauritanian Center for Political Analysis (Centre Mauritanien d'Analyse Politique)

CNEITI National Committee for the Extractive Industries Transparency Initiative (Comité

National EITI)

CNERV National Center for Livestock Breeding and Veterinary Research (Centre National

d'Elevage et de Recherches Vétérinaires)

CNME National Multisector Energy Committee (Comité National Multisectoriel Énergie)

CNRADA National Center for Agronomic Research and Agricultural Development (Centre National

de Recherches Agronomiques et de Développement)

CNRE National Center for Water Resources (Centre National des Ressources en Eau)

CNSS National Social Security Fund (Caisse Nationale de Sécurité Sociale)

CPI Investment Promotion Agency (Commissariat à la Promotion des Investissements)

CPN Community Postnatal Nursing

CPP Petroleum Allocation Contract (Contrat de Partage Pétrolier)

CRAER Center for Applied Research on Renewable Energy (Centre de Recherche Appliquée aux

Energies Renouvelables)

CSA Food Security Commission (Commissariat pour la Sécurité Alimentaire)

CSET Advanced Technical Training Center (Centre Supérieur de l'Enseignement Technique)

CSLP Strategic Framework for the Fight against Poverty (Cadre Stratégique de la Lutte contre

la Pauvreté)

CSM Market Monitoring Committee (Comité de Surveillance du Marché)

CVP Comprehensive Vaccination Program

DA Directorate for Sanitation (Direction de l'Assainissement)

DAF Directorate for Administration and Finance (Direction de l'Administration et des

Finances)

DAO Bidding Document (Dossier d'Appel d'Offre)

DAPBI Annual Budget Programming and Integration Document (Document Annuel de

Programmation Budgétaire Intégrée)

DCPCRF Directorate for Competition, Consumer Protection, and the Fight against Fraud (Direction

de la Concurrence, de la Protection des Consommateurs, et de la Répression des

Fraudes)

DDE Directorate for External Debt (Direction de la Dette Extérieure)

DDEE Water and Electricity Development Policy Statement (Déclaration de Politique pour le

Développement de l’Eau et de l’Electricité)

DeMPA Debt Management Performance Assessment

DGD Central Customs Directorate (Direction Générale des Douanes)

DGE Directorate for Large Enterprises (Direction des Grandes Entreprises)

DGI General Directorate for Taxes (Direction Générale des Impôts)

DGM General Directorate for Markets (Direction Générale des Marchés)

DGPIP General Directorate for the Promotion of Private Investment (Délégation Générale à la

Promotion des Investissements Privés)

DGTCP General Directorate for the Treasury and Public Accounting (Direction Générale du

iii

Trésor et de la Comptabilité Publique)

DH Directorate for Hydraulics (Direction de l'Hydraulique)

DHB Directorate for Hydrology and Dams (Direction de l’Hydrologie et des Barrages)

DMDR Rural Development Model Diversification (Diversification des Modèles de

Développement Rural)

DME Directorate for Medium-sized Enterprises (Direction des Moyennes Entreprises)

DMM Directorate for Merchant Marine (Direction de la Marine Marchande)

DOB Budget Orientation Debate (Débat d'Orientation Budgétaire)

DPAE Directorate for Forecasting and Economic Analysis (Direction de la Prévision et de

l'Analyse Economique)

DPCSE Directorate for Policy Setting, Cooperation, and Monitoring and Evaluation (Direction

des Politiques, de la Cooperation, et du Suivi et Evaluation)

DPM Directorate for the Policing of Mining (Direction de la Police Minière)

DPS Sector Policy Declaration (Déclaration de Politique Sectorielle)

DRI Request for Immediate Repayment (Demande de Règlement Immédiat)

DRS Regional Directorate for Health (Direction Régionale de la Santé)

DSA Social Dimension of Adjustement (Dimension Sociale de l'Ajustement)

DSPCM Directorate for Fisheries Monitoring and Maritime Control (Délégation à la Surveillance

des Pêches et au Contrôle en Mer)

EDSM Enhanced Data Support Methodology

EEA Exclusive Exploration Authorization

EEL Exclusive Exploration Permit

EEZ Exclusive Economic Zone

EFA Education for All

EFRP Economic and Financial Recovery Program

EIE Environmental Impact Evaluation

EITI Extractive Industries Transparency Initiative

ENA National School of Administration (Ecole Nationale d'Administration)

ENFVA National Institute for Agricultural Training and Dissemination (École Nationale de

Formation et de Vulgarisation Agricoles)

ENI Primary Teacher Training Institute (Ecole Normale d'Instituteurs)

ENR Energy and Natural Resources

ENS Advanced Primary Teacher Training Institute (Ecole Normale Supérieure)

EPA Public Administration Entity (Etablissement Public Administratif)

EPBR Port of Baie du Repos (Etablissement Portuaire de la Baie du Repos)

EU European Union

EUR Euro

FAO Food and Agriculture Organization

FCI Financial Commodity Investments

FDI Foreign Direct Investment

FNARS National Scientific Research Support Fund (Fonds National d’Appui à la Recherche

Scientifique)

FNRH National Oil Revenues Fund (Fonds National des Revenus des Hydrocarbures)

FNP National Fishing Federation (Fédération Nationale de Pêche)

FNT National Tourism Federation (Fédération Nationale du Tourisme)

FP Civil Service (Fonction Publique)

FR Road Fund (Fonds Routier)

FSAP Financial Sector Assessment Project

GDP Gross Development Product

GIE Economic Interest Group (Groupement d'Intérêt Economique)

GIS Geographic Information System

iv

GMM Mauritanian Granite and Marble (Granit et Marbres de Mauritanie)

GTZ German Technical Cooperation Organization (Deutsche Gesellschaft für Technische

Zusammenarbeit)

HIMO Workforce High Intensity (Haute Intensité de Main d'Oeuvre)

HIV Human Immuni-deficiency Virus

HLCS Longitudinal Survey of Living Conditions

IAEA International Atomic Energy Agency

ICA Investment Climate Assessment

ICI Industrial and Commercial Income

ICT Information and Communications Technology

IDP Infrastructure Development Plan

IGE General State Inspectorate (Inspectorat Général de l'Etat)

IGF General Financial Inspectorate (Inspectorat Général des Finances)

ILO International Labor Organization

IMF International Monetary Fund

IMROP Mauritanian Institute for Oceanographic Research and Fisheries (Institut Mauritanien de

Recherches Océanographiques et des Pêches)

IMS Information Management System

IRENA International Renewable Energy Agency

IsDB Islamic Development Bank

ISERI Institute for Advanced Islamic Studies and Research (Institut Supérieur d'Etudes et de

Recherches Islamiques)

ISET Institute for Advanced Technological Studies (Institut Supérieur d'Enseignement

Technologique)

LAOP Agro-pastoral Orientation Bill (Loi d’Orientation Agropastorale)

LDF Finance Bill (Loi de Finances)

LFTP Technical and Professional Training High School (Lycée de Formation Technique et

Professionnelle)

LIW Labor Intensive Work

LMD Licence-Masters-Doctorate

MAED Ministry of Public Finances and Development (Ministère des Finances Publiques et du

Développement)

MATEMA Mauritanian Maritime Technical Assistance Organization (Compagnie Mauritanienne

d'Assistance Technique Maritime)

MCM Mauritanian Copper Mines (Mines de Cuivre de Mauritanie)

MDR Ministry of Rural Development (Ministère du Développement Rural)

MEP Ministry of Energy and Oil (Ministère de l'Energie et du Pétrole)

MF Ministry of Finance (Ministère des Finances)

MFA Ministerial Financial Audit

MFP Multifunctional Platform

MHA Ministry of Hydraulics and Sanitation (Ministère de l’Hydraulique et de

l’Assainissement)

MICO Oasis Investment and Credit Union (Mutuelle d’Investissement et de Crédit Oasien)

MICS Multiple Indicator Cluster Survey

MOD Delegated Works Contractor (Maîtrise d’Ouvrage Déléguée)

MPEM Ministry of Fisheries and the Maritime Economy (Ministère des Pêches et de l'Economie

Maritime)

MRO Mauritanian Ouguiya

NGO Non-governmental Organization

NHP National Health Policy

OMRG Mauritanian Geological Research Office (Organisation Mauritanienne pour la Recherche

v

Géologique)

OMVS Senegal River Development Agency (Organisation pour la Mise en Valeur du Fleuve

Sénégal)

ONA National Sanitation Agency (Office National de l’Assainissement)

ONE National Electricity Agency (Office National de l'Electricité)

ONISPA National Health Monitoring Agency for Fisheries Products and Aquaculture (Office

National d'Inspection Sanitaire des Produits de la Pêche et de l'Aquaculture)

ONMT National Occupational Health Agency (Office National de la Médecine du Travail)

ONS National Statistical Office (Office National de la Statistique)

PACAE Economic Activity Climate Improvement Project (Projet d'Amélioration du Climat de

l'Activité Economique)

PAEPA Drinking Water Supply and Sanitation Project (Projet d'Approvisionnement en Eau

Potable et d'Assainissement)

PADEL Local Decentralization and Development Support Project (Projet d’Appui à la

Décentralisation et au Développement Local)

PADPAC Management and Development Plan for Artisanal and Coastal Fishing (Plan

d'Aménagement et de Développement des Pêches Artisanales et Côtières)

PAM Policy Analysis Matrix

PAN Autonomous Port of Nouadhibou (Port Autonome de Nouadhibou)

PANPA Autonomous Port of Nouakchott (Port Autonome de Nouakchott – Port de l'Amitié)

PASA Agricultural Sector Adjustment Program (Programme d’Ajustement du Secteur Agricole)

PCR Economic Consolidation and Growth Program (Programme de Consolidation et de

Relance)

PCS Permissible Catch Size

PDIAIM Integrated Program for the Development of Irrigated Agriculture in Mauritania

(Programme de Développement Intégré de l’Agriculture Irriguée en Mauritanie)

PDM Development and Modernization Program (Programme de Développement et de

Modernisation)

PDU Urban Development Program (Programme de Développement Urbain)

PED Potentially Epidemial Disease

PEFA Public Expenditure and Financial Assessment

PGT Treasury General Disbursement (Paierie Générale du Trésor)

PNAR National Program for Rural Sanitation (Programme National d'Assainissement Rural)

PNDSE National Program for the Development of the Education Sector (Programme National de

Développement du Secteur Educatif)

PNSAM National Food Security Policy (Politique Nationale de Sécurité Alimentaire)

PNSR National Program for Reproductive Health (Programme National pour la Santé

Reproductive)

PPIAF Public-private Infrastructure Advisory Facility

PPP Public-private Partnership

PRECASP Public Sector Capacity Reinforcement Project (Projet pour le Renforcement des

Capacités du Secteur Public)

PRISM Mining Sector Institutional Strengthening Project (Projet de Renforcement Institutionnel

du Secteur Minier)

PRSP Poverty Reduction Strategy Paper

PST Transportation Sector Plan (Plan Sectoriel de Transport)

RACHAD Expenditure Chain Automated System (Réseau Automatisé de la Chaîne des Dépenses)

RESEN State Report on the National Educational System (Rapport d'Etat sur le Système Educatif

National)

RGPH General Population and Habitat Census (Recensement Général de la Population et de

l'Habitat)

vi

SAE Environmental Affairs Department (Service des Affaires Environnementales)

SAMIA Arab Mining and Metallurgy Company (Société Arabe des Mines et des Industries

Metallurgies)

SAMMA Mauritanian Unloading and Handling Corporation (Société d’Anconage et de

Manutention en Mauritanie)

SDSR Rural Development Strategy (Stratégie de Développement du Secteur Rural)

SIGE Environmental and Geological Information Service (Service d'Information Géologique et

Environnementale)

SIGM Mining Information and Management Service (Service d'Information et de Gestion

Minière)

SMCP Mauritanian Fishing Commercialization Organization (Société Mauritanienne de

Commercialisation de la Pêche)

SME Small and Medium Enterprise

SMH Mauritanian Hydrocarbons Agency (Société Mauritanienne des Hydrocarbures)

SNAAT National Agriculture Planning and Works Agency (Société Nationale d'Aménagement

Agricole et des Travaux)

SNDE National Water Utility (Société Nationale de l'Eau)

SNFP National Drilling Company (Société nationale de forages et de puits)

SNIM National Industrial and Mining Company (Société Nationale des Industries Minières)

SNIS National Health Information System (Système National d’Information Sanitaire)

SOMELEC Mauritanian Electricity Company (Société Mauritanienne d'Electricité)

SOMIR Mauritanian Refining Company (Société Mauritanienne des Industries de Raffinage)

SONADER National Rural Development Agency (Société Nationale pour le Développement Rural)

SPO Socio-professional Organization

SRH Regional Water Services (Services Régionaux de l’Hydraulique)

STD Sexually Transmitted Disease

TFP Technical and Financial Partners

TIQ Transferrable Individual Quota

TML Tasiast Mauritanie Limited

TNS National Enrollment Rate (Taux National de Scolarisation)

TOR Terms of Reference

TPT Technical and Professional Training (Formation Technique et Professionelle)

UAE United Arab Emirates

UBS Union Bank of Switzerland

UNCACEM National Agricultural Credit Union Network (Union Nationale des Coopératives

Agricoles de Crédit et d'Epargne de Mauritanie)

UNCTAD United Nations Conference on Trade and Development

UNDP United Nations Development Program

UNESCO United Nations Educational, Scientific, and Cultural Organization

UNFPA United Nations Population Fund

UNICEF United Nations Children's Fund

UNIDO United Nations Industrial Development Organization

USD United States Dollar

USGS United States Geological Survey

WAEMU West African Economic and Monetary Union

WFP World Food Program

vii

Vice-President: Obiageli K. Ezekwesili (AFRVP)

Country Director: Madani Tall (AFCF1)

Sector Director: Sudhir Shetty (AFTPM)

Interim Sector Manager: Philip English (AFTP4)

Team Leaders: Manuela Francisco and Philip English (AFTP4)

viii

TABLE OF CONTENTS

PREFACE ............................................................................................................................................................... XI

EXECUTIVE SUMMARY: ........................................................................................................................................ XII

PART I: STRENGTHENING PUBLIC INSTITUTIONS .................................................................................................... 1

1. PUBLIC FINANCE MANAGEMENT ....................................................................................................................... 1

A. CONTEXT .................................................................................................................................................................. 1 B. MAJOR CONSTRAINTS .................................................................................................................................................. 3 C. RECOMMENDATIONS ................................................................................................................................................... 8 D. CHALLENGES TO IMPLEMENTATION .............................................................................................................................. 11 E. ANALYTICAL GAPS ..................................................................................................................................................... 12

2. CIVIL SERVICE ................................................................................................................................................... 13

A. CONTEXT ................................................................................................................................................................ 13 B. MAJOR CONSTRAINTS ................................................................................................................................................ 13 C. RECOMMENDATIONS ................................................................................................................................................. 15 D. CHALLENGES TO IMPLEMENTATION .............................................................................................................................. 16 E. ANALYTICAL GAPS ..................................................................................................................................................... 16

PART II: IMPROVING THE FACTORS OF PRODUCTION: HUMAN CAPITAL ............................................................. 18

3. EDUCATION...................................................................................................................................................... 18

A. CONTEXT ................................................................................................................................................................ 18 B. MAIN CONSTRAINTS .................................................................................................................................................. 20 C. RECOMMENDATIONS ................................................................................................................................................. 22 D. CHALLENGES TO IMPLEMENTATION .............................................................................................................................. 25 E. ANALYTICAL GAPS ..................................................................................................................................................... 25

2. EMPLOYMENT .................................................................................................................................................. 26

A. CONTEXT ................................................................................................................................................................ 26 B. MAJOR CONSTRAINTS ................................................................................................................................................ 27 C. RECOMMENDATIONS ................................................................................................................................................. 29 D. CHALLENGES TO IMPLEMENTATION .............................................................................................................................. 30 E. ANALYTICAL GAPS ..................................................................................................................................................... 30

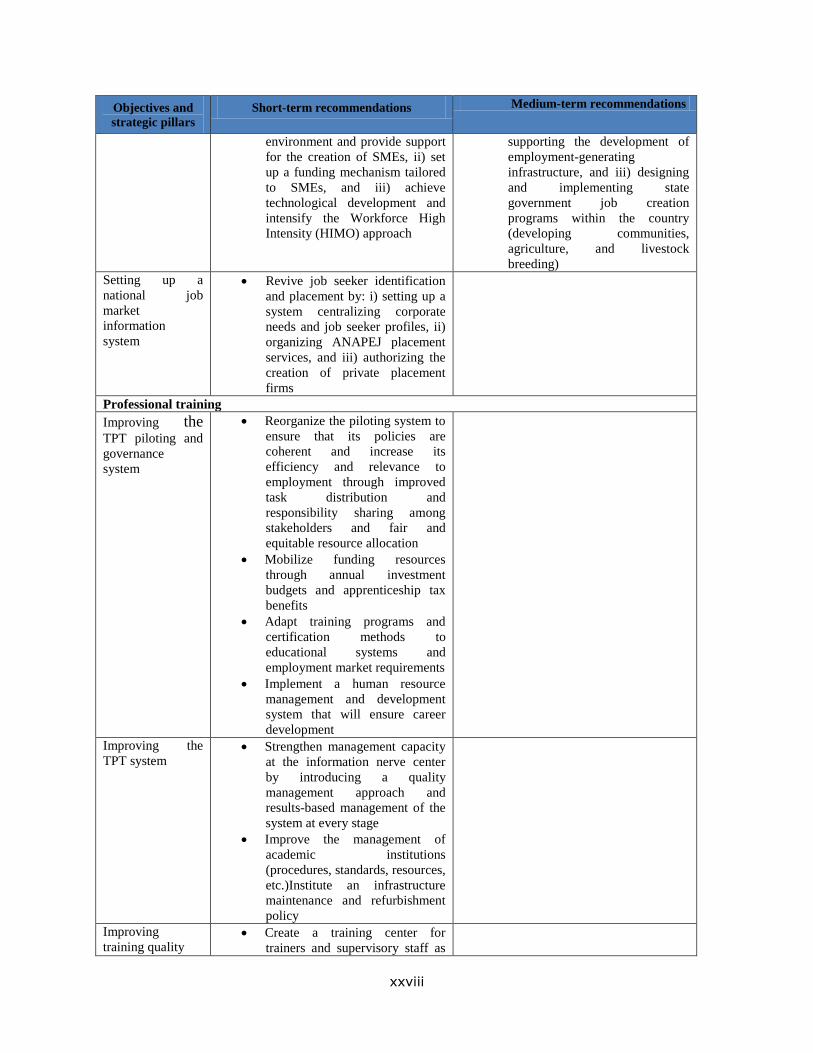

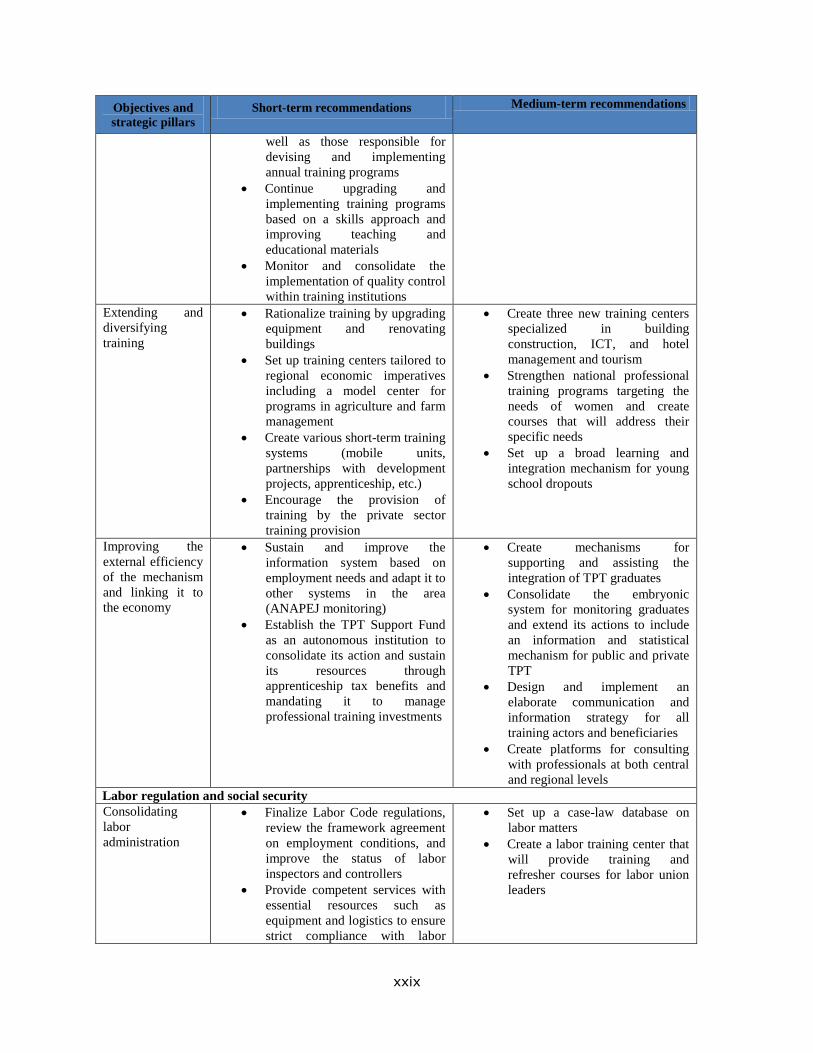

5. PROFESSIONAL TRAINING ................................................................................................................................ 31

A. CONTEXT ................................................................................................................................................................ 31 B. MAJOR CONSTRAINTS ................................................................................................................................................ 31 C. RECOMMENDATIONS ................................................................................................................................................. 33 F. CHALLENGES TO IMPLEMENTATION ............................................................................................................................... 35 G. ANALYTICAL GAPS ..................................................................................................................................................... 35

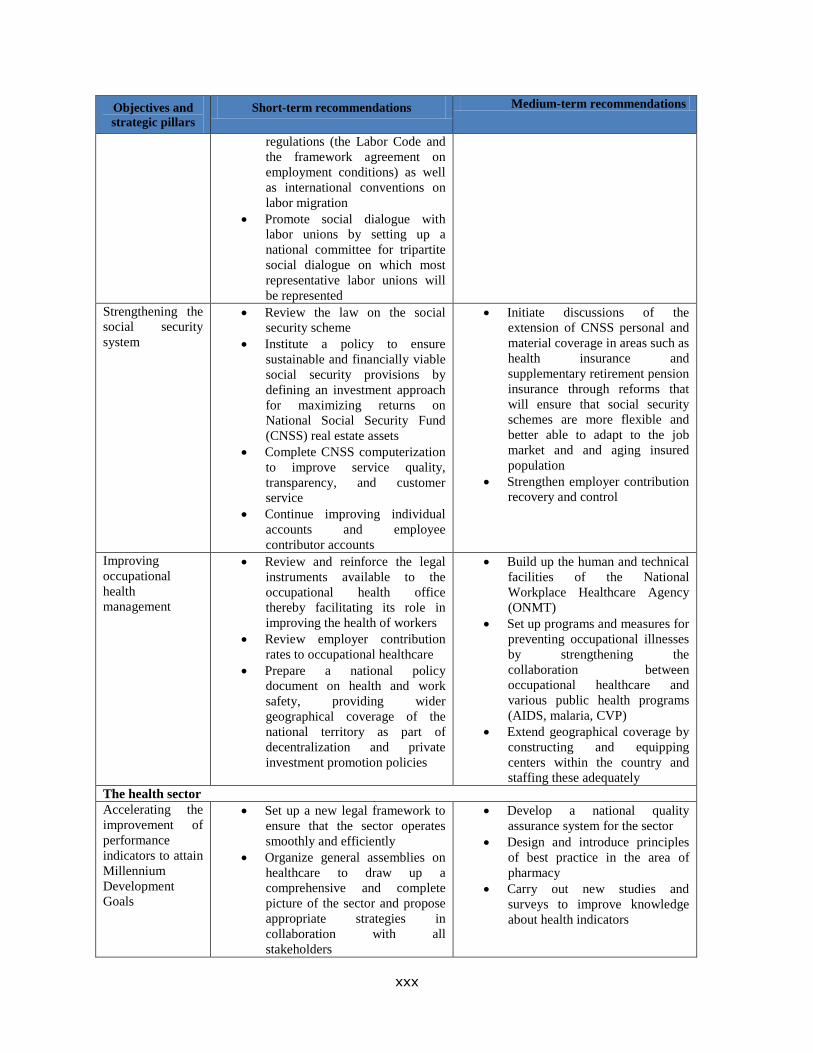

6. LABOR REGULATIONS AND SOCIAL WELFARE .................................................................................................. 37

A. CONTEXT ................................................................................................................................................................ 37 B. MAJOR CONSTRAINTS ................................................................................................................................................ 37 C. RECOMMENDATIONS ................................................................................................................................................. 38 D. CHALLENGES TO IMPLEMENTATION .............................................................................................................................. 39

ix

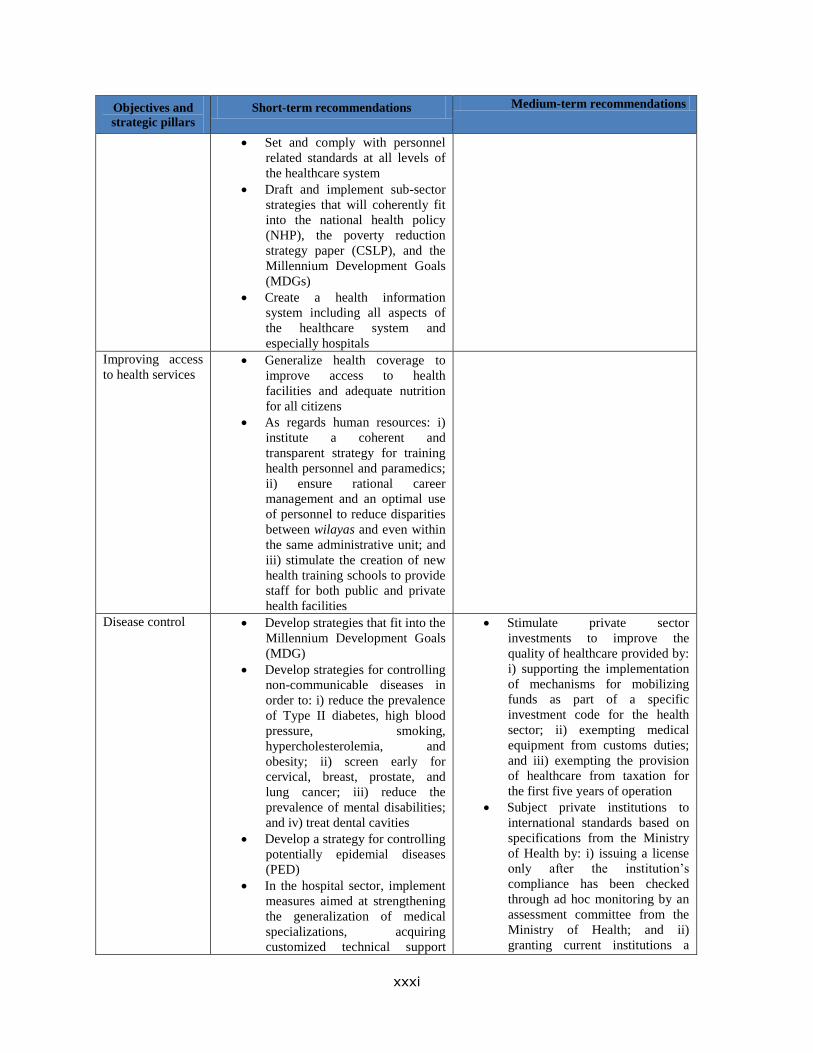

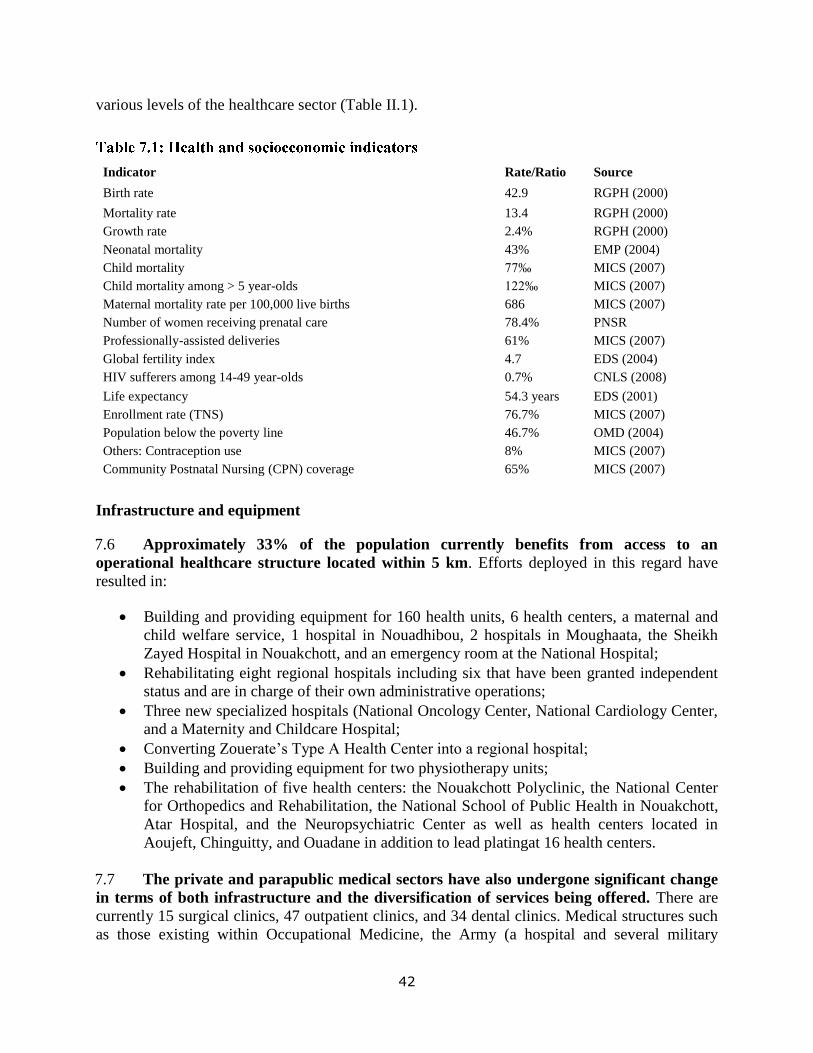

7. HEALTH ............................................................................................................................................................ 41

A. OVERVIEW .............................................................................................................................................................. 41 B. MAJOR CONSTRAINTS ................................................................................................................................................ 44 C. RECOMMENDATIONS ................................................................................................................................................. 47 D. CHALLENGES TO IMPLEMENTATION .............................................................................................................................. 50 E. ANALYTICAL GAPS ..................................................................................................................................................... 50

8. WATER AND SANITATION ................................................................................................................................ 51

A. OVERVIEW .............................................................................................................................................................. 51 B. CHALLENGES TO IMPLEMENTATION .............................................................................................................................. 62 C. RECOMMENDATIONS ................................................................................................................................................. 63 D. ANALYTICAL GAPS .................................................................................................................................................... 64

PART III: IMPROVING THE FACTORS OF PRODUCTION: INFRASTRUCTURE ........................................................... 65

9. ELECTRICITY ..................................................................................................................................................... 65

A. CONTEXT ................................................................................................................................................................ 65 B. MAJOR CONSTRAINTS ................................................................................................................................................ 66 C. RECOMMENDATIONS ................................................................................................................................................. 69 D. CHALLENGES TO IMPLEMENTATION .............................................................................................................................. 72 E. ANALYTICAL GAPS ..................................................................................................................................................... 72

10. ROAD AND MARITIME TRANSPORTATION ..................................................................................................... 75

A. CONTEXT ................................................................................................................................................................ 75 B. MAJOR CONSTRAINTS ................................................................................................................................................ 76 C. RECOMMENDATIONS ................................................................................................................................................. 78 D. CHALLENGES TO IMPLEMENTATION .............................................................................................................................. 79 E. ANALYTICAL GAPS ..................................................................................................................................................... 80

PART IV: DEVELOPMENT OF THE PRIVATE SECTOR AND GROWTH SECTORS ........................................................ 81

11. THE INVESTMENT CLIMATE ............................................................................................................................ 81

A. CONTEXT ................................................................................................................................................................ 81 B. MAJOR CONSTRAINTS ................................................................................................................................................ 82 C. RECOMMENDATIONS ................................................................................................................................................. 88 D. CHALLENGES TO IMPLEMENTATION .............................................................................................................................. 91 E. ANALYTICAL GAPS ..................................................................................................................................................... 91

12. RURAL DEVELOPMENT ................................................................................................................................... 93

A. CONTEXT ................................................................................................................................................................ 93 B. MAJOR CONSTRAINTS ................................................................................................................................................ 95 C. RECOMMENDATIONS ............................................................................................................................................... 100 D. CHALLENGES TO IMPLEMENTATION ............................................................................................................................ 103 E. ANALYTICAL GAPS ................................................................................................................................................... 105

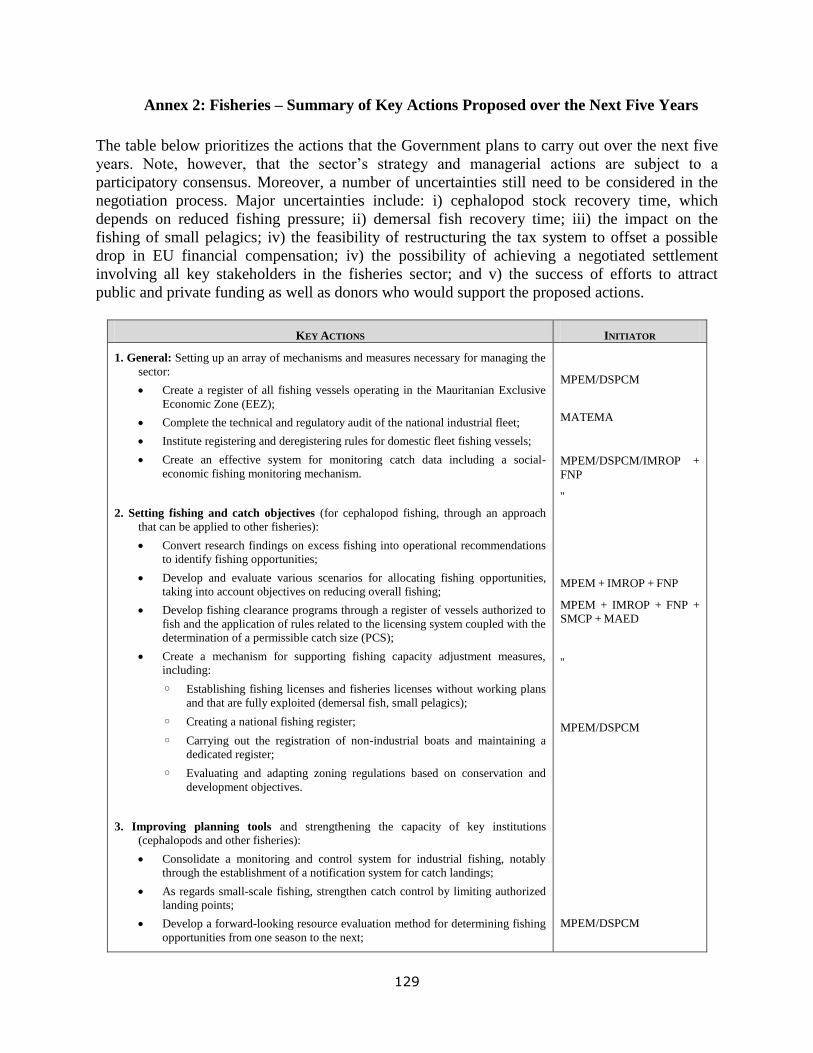

13. FISHERIES ..................................................................................................................................................... 107

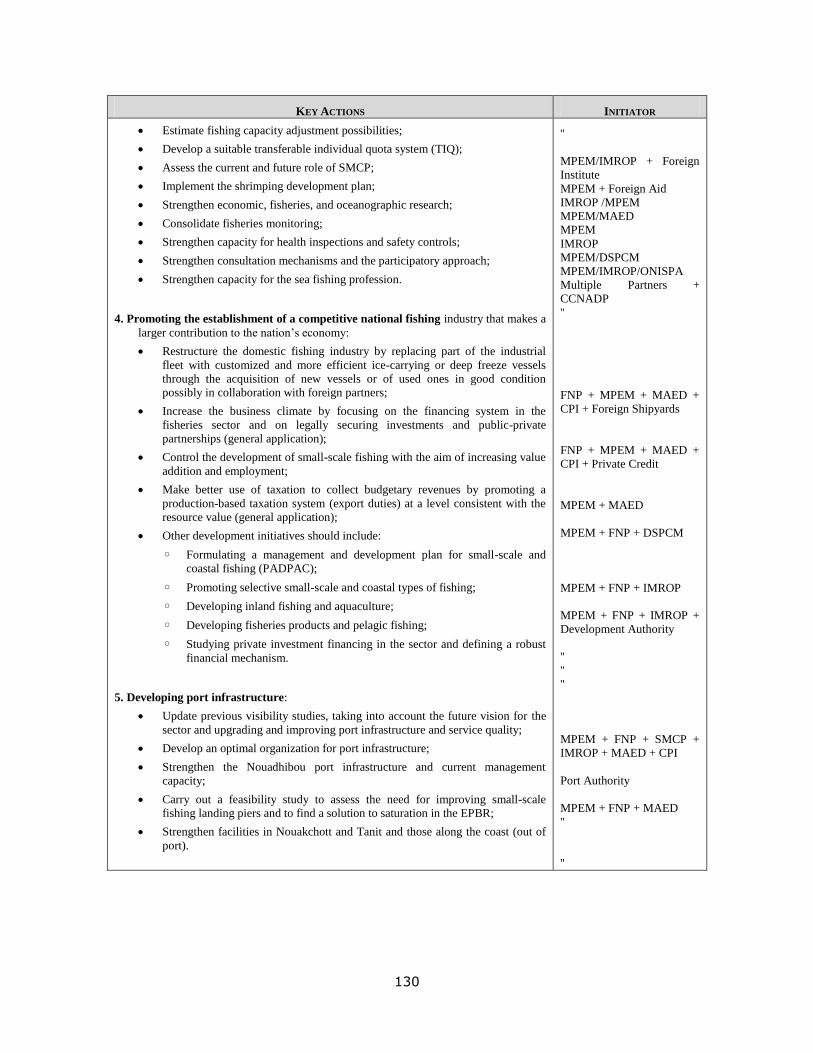

A. CONTEXT .............................................................................................................................................................. 107 B. MAJOR CONSTRAINTS .............................................................................................................................................. 108 C. RECOMMENDATIONS ............................................................................................................................................... 112 D. CHALLENGES TO IMPLEMENTATION ............................................................................................................................ 112 E. ANALYTICAL GAPS ................................................................................................................................................... 113

14. THE MINING SECTOR .................................................................................................................................... 114

x

A. CONTEXT .............................................................................................................................................................. 114 B. MAJOR CONSTRAINTS .............................................................................................................................................. 117 C. RECOMMENDATIONS ............................................................................................................................................... 118 D. CHALLENGES TO IMPLEMENTATION ............................................................................................................................ 119 E. ANALYTICAL GAPS ................................................................................................................................................... 120

15. OIL ............................................................................................................................................................... 121

A. OVERVIEW ............................................................................................................................................................. 121 B. MAJOR CONSTRAINTS .............................................................................................................................................. 123 C. RECOMMENDATIONS ............................................................................................................................................... 124 D. CHALLENGES TO IMPLEMENTATION ............................................................................................................................ 125 E. ANALYTICAL GAPS ................................................................................................................................................... 125

Tables

TABLE 2.1: COMPARISON BETWEEN PAYROLL AND PERSONNEL FILES ....................................................................... 14

TABLE 7.1: HEALTH AND SOCIOECONOMIC INDICATORS ............................................................................................ 42

Annexes

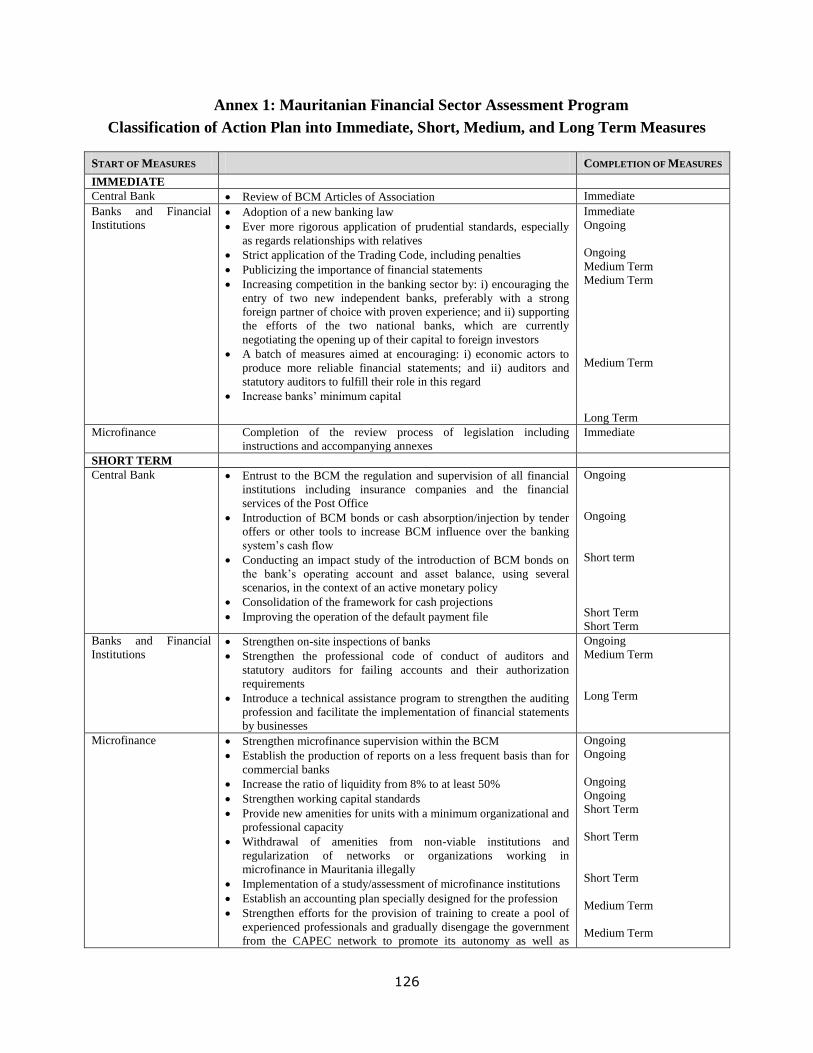

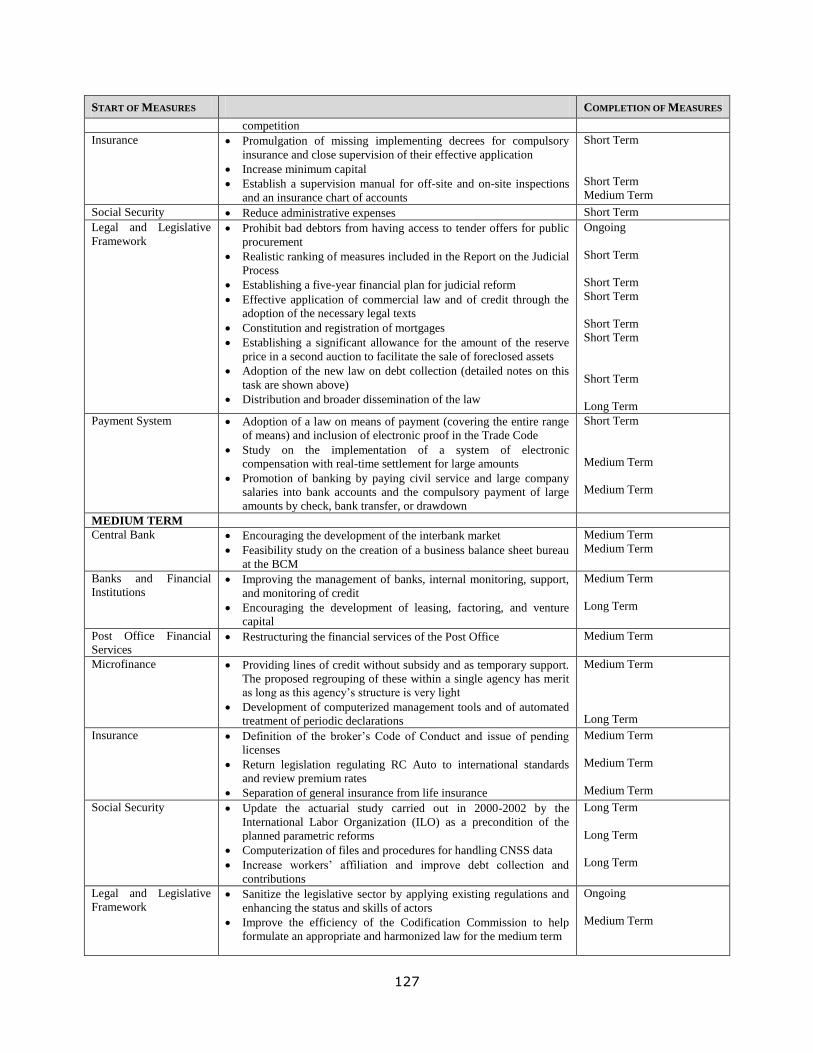

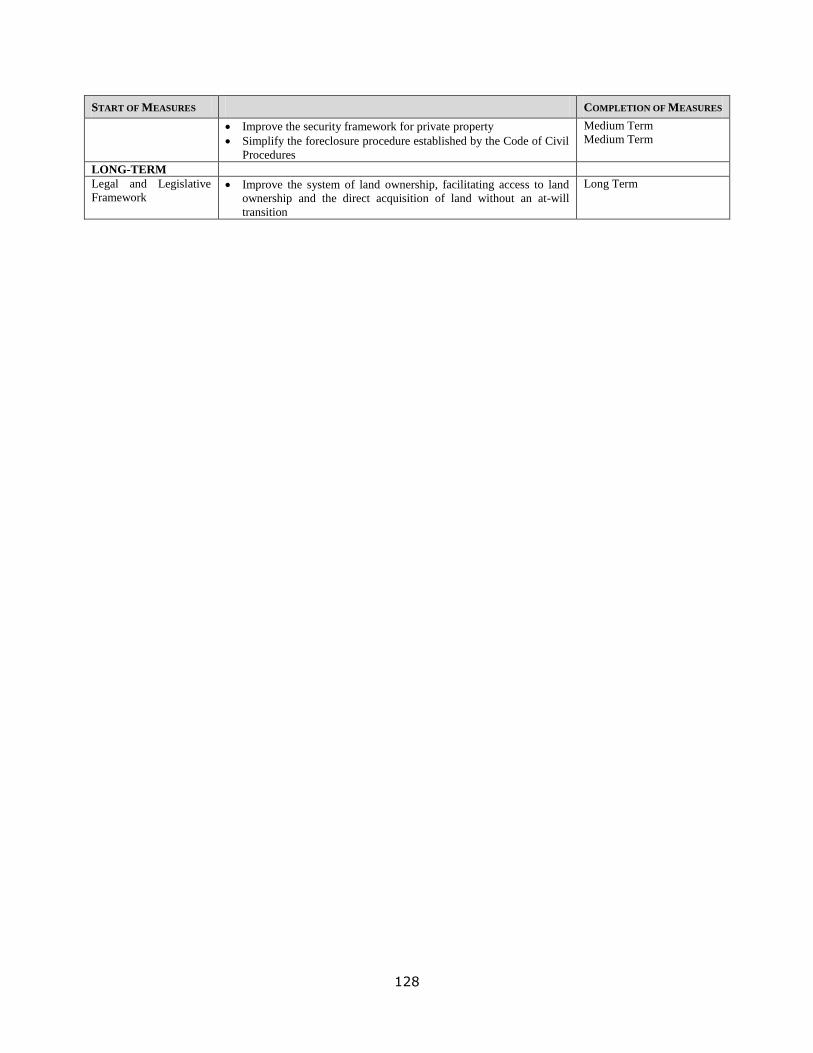

ANNEX 1: MAURITANIAN FINANCIAL SECTOR ASSESSMENT PROGRAM ................................................................... 126

ANNEX 2: FISHERIES – SUMMARY OF KEY ACTIONS PROPOSED OVER THE NEXT FIVE YEARS .................................. 129

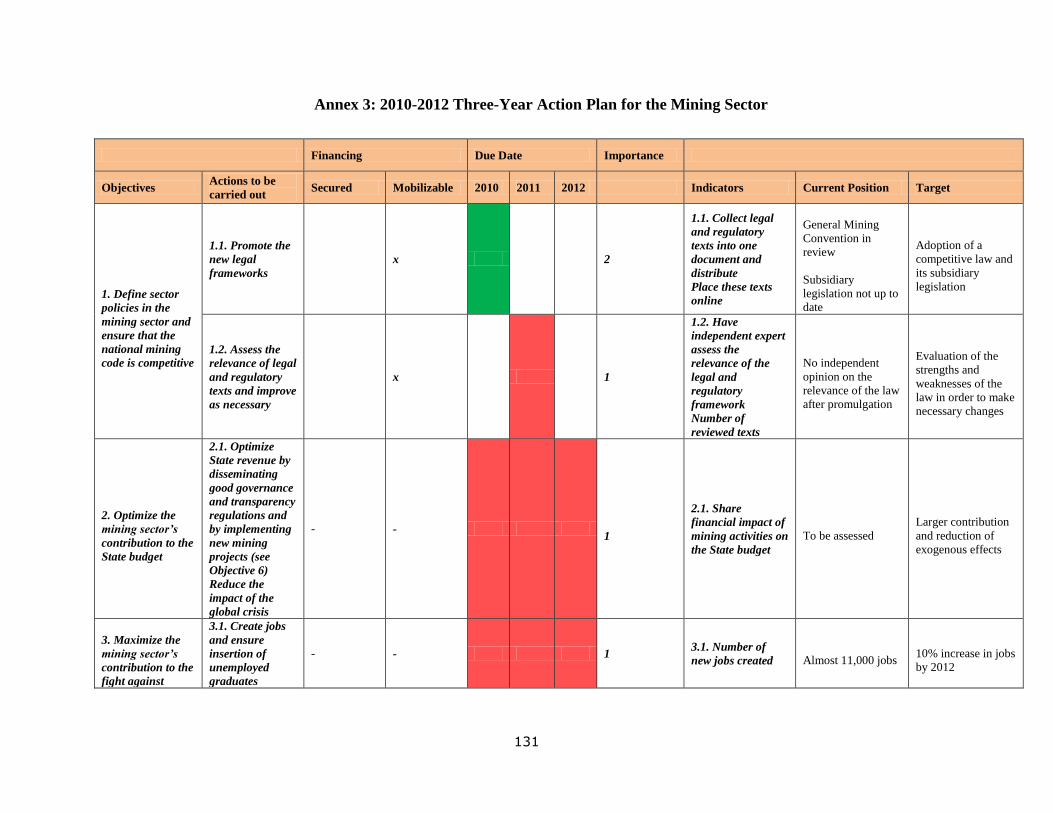

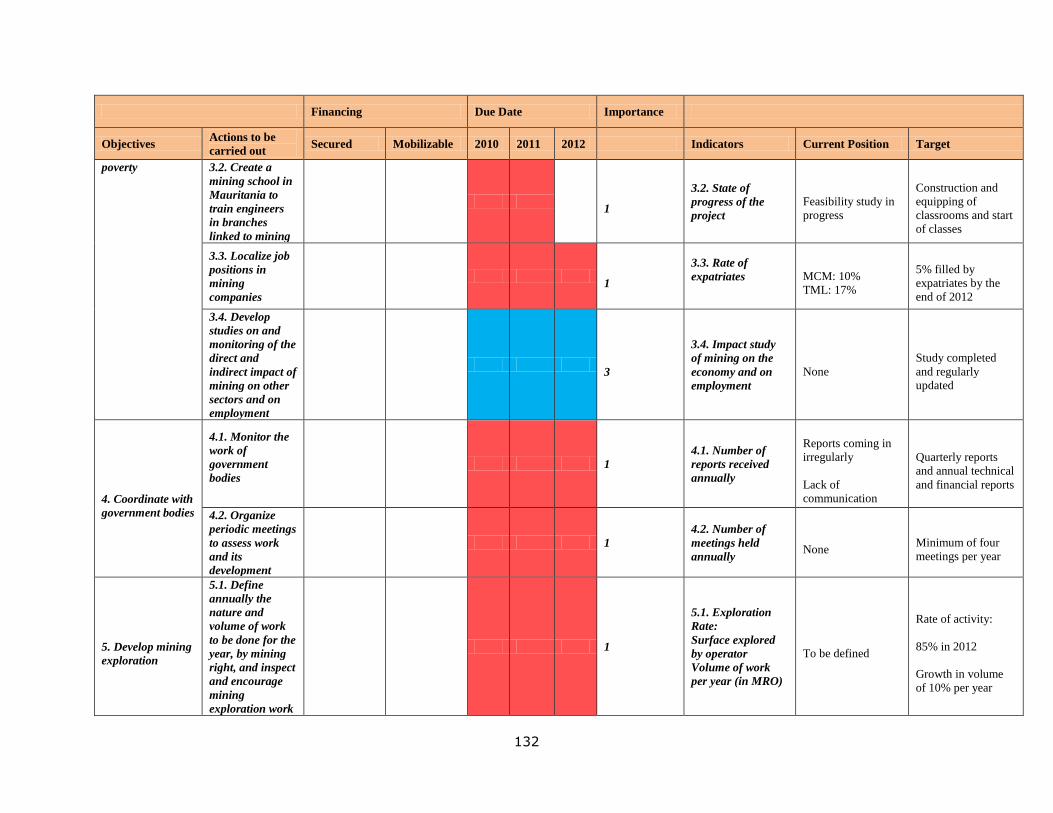

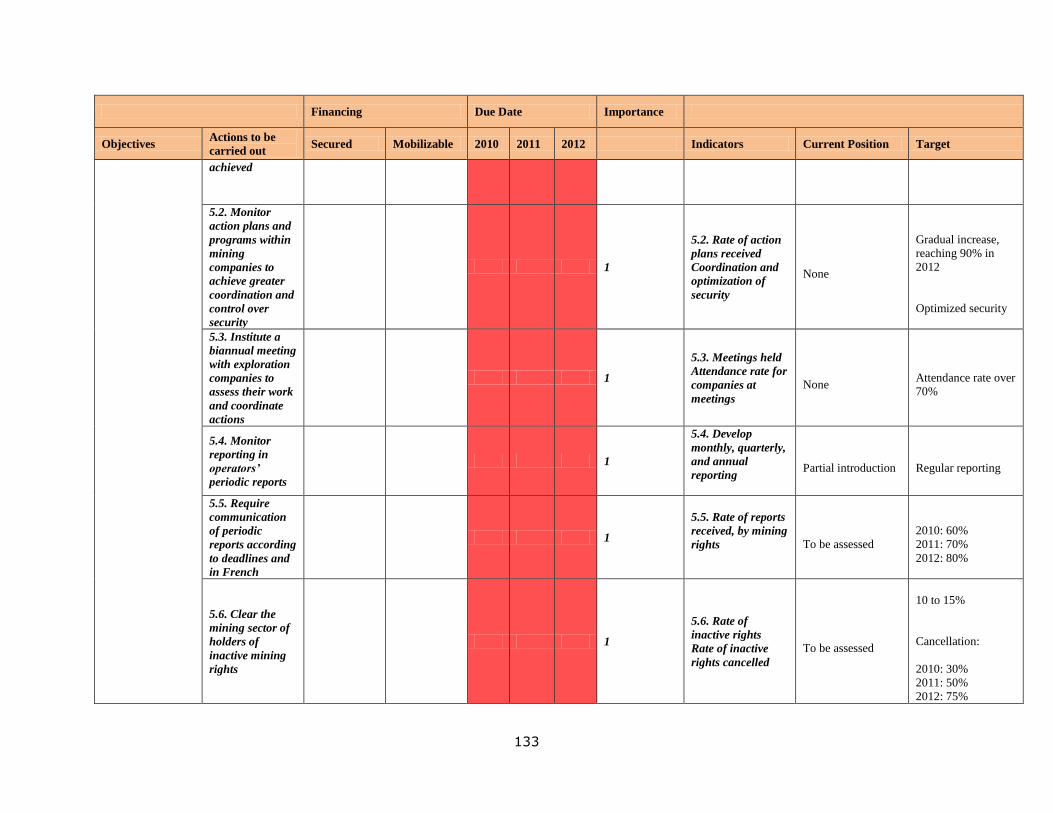

ANNEX 3: 2010-2012 THREE-YEAR ACTION PLAN FOR THE MINING SECTOR ........................................................... 131

This document has a restricted distribution and may be used by recipients only in the performance of

their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

xi

PREFACE

World Bank support to the preparation of these sector policy notes is part of the recommitment

process that followed the July 2009 presidential election. The Mauritanian authorities'

appreciation of the the World Bank's proposal led to its adoption and extension to other sectors.

Primarily as a result of ties that developed between the various technical committees during the

process that began under United Nations supervision, other technical and financial partners

quickly decided to participate in it. The number of notes thus increased from seven to 15,

including some for sectors in which the World Bank lacks extensive experience in Mauritania.

The preparation process for these policy notes has evolved over time. Drafts prepared by the

World Bank were taken up by the Mauritanian authorities and distributed to the ministries

concerned. While in some cases the substance of the sector notes was retained (with

modifications), in others the ministries concerned chose to redraft the documents. In some cases,

another partner conducted the drafting and writing process, particularly in the water and

sanitation sectors, to which the French Development Agency (AFD) contributed. An iterative

process has now been launched to find a consensus between the Mauritanian authorities, the

World Bank, and the country's technical and financial partners.

This collaboration has resulted in a more extensive and more appropriate report being made

available to the authorities. Prior to its being finalized and validated, it became apparent that the

policies of the Mauritanian government were already being influenced by this document.

Obviously, we are delighted. Furthermore, the recommendations contained in this report are

more numerous and less focused than initially planned, with only a few important issues not

being fully addressed. While the recommendations contained in the report form an excellent

basis for dialogue between the Mauritanian authorities and the country's partners, they will no

doubt be refined in the course of a validation workshop, the preparation of the new poverty

reduction strategy, and the subsequent process of program and project definition.

We would like to thank the Minister for Economic Affairs and Development, Mr. Sidi Ould Tah

and his Director of Policies and Strategies, Mr. Mohamed Ould Djié for the orientations they

gave to this reflection process and for the quality of their collaboration with the World Bank. We

would also like to thank all the members of the Mauritanian public administration services who

contributed to writing these notes for the quality of their work and for their commitment. Support

from development partners also made a significant contribution to the success of the process.

These include the UNDP and other United Nations agencies based in Nouakchott, the European

Commission, the IMF, and the French, Italian, German, and Spanish development aid agencies.

Finally, the authors would also like to thank all their World Bank colleagues in Mauritania for

their tremendous teamwork.

xii

EXECUTIVE SUMMARY:

Principal challenges to economic growth in Mauritania

1. Even though Mauritania’s real GDP recorded an average growth rate of 4%

between 2005 and 2009, the country’s economic growth remains unstable and vulnerable to

external shocks. At the same time, the distribution of profits through benefit sharing

continues to be very unequal. Growth is dependent on a few raw materials (oil, ore, and fish)

and development assistance, with very limited processing activity. Due in part to the availability

of income or resource rent generated by the exploitation of these raw materials, other sectors

have been neglected, especially agriculture, cattle farming, and the urban private sector in

general. The impact of this resource rent on the exchange rate and the high cost of living also

contributes to making other sectors uncompetitive. Yet, these are the sectors in which most of the

population is trying to make a living. The country’s development is therefore distorted, with

persistent poverty, even though poverty has been reduced from 47% in 2004 to 42% in 2008,

representing an annual fall of about 1.2 percentage points.

2. Since Mauritania’s independence in November 28, 1960, it has experienced several

periods of political and institutional instability that have strongly hampered its economic

and social development. The country has had no fewer than seven military coups since the fall

of the first civilian Mauritanian President in July 1978. Between 2005 and 2007, an initial

transition period put an end to the 21-year rule of Maaouya Ould Sid Ahmed Taya and opened

the door to legislative and presidential elections, which resulted in Sidi Ould Cheikh Abdallahi

becoming the country's President. After a year and a half in power, he was ousted in August

2008 in a military coup. The High Council of State then appointed General Mohamed Ould

Abdel Aziz as Head of State. Following a one-year-long political crisis, General Mohamed Ould

Abdel Aziz won the July 18, 2009 presidential election, which followed consensus being reached

among the divergent political opinions that had agreed to sign the Dakar agreement.

3. The management of a rent-based economy creates huge challenges. The public

finances must be managed efficiently to promote diversification, share wealth more equitably,

and fight transparently against the corruption that often accompanies resource rent. In addition,

resources must be used to stimulate the rural sector, where the majority of poor people operate,

and invested in human resources in order to improve their competitiveness. At the same time, the

business climate must be sanitized and infrastructure improved to promote investment and thus

create employment. The strengthening of institutions thus becomes critical, especially in order to

control abuse.

4. The impact of the recent economic and financial crisis on global demand and

particularly on the price of iron and copper in addition to the reduction in oil production

highlight the urgent need to identify new income generating sectors other than the

traditional exploitation of natural resources. The direct impacts of the global crisis have been

limited in Mauritania because the country is barely integrated in the international financial

system. However, the low price of raw materials, political instability, the reduction in foreign

xiii

aid, and the fall in oil production1 were contributing factors in the decline in real GDP growth in

2009 (-1%, compared with 3.7% in 2008, 1% in 2007, and 11.4% in 2006). At the same time,

prospects for income from oil are not encouraging. It is anticipated that the export of gold will

overtake that of oil until 2012 (with an average share of GDP of 7.2% and 5.2%, respectively, for

the period 2010-2012). New mining projects2 could help strengthen the economy but these would

not be adequate on their own. The diversification of the economy should reduce vulnerability to

outside shocks, create a favorable environment for growth, reduce the impact of price volatility

for oil and iron ore, and create employment.

5. In general, the economic crisis and political instability have delayed critical reforms

crucial to the development of a strong productive environment. In particular, the

implementation of economic reforms in the financial sector and the business environment as well

as the strengthening of governance have been delayed. This has slowed improvements in the

competitiveness of the private sector and strengthened over-dependence on income from the

exploitation of natural resources. With a very small and fragmented market and a limited

manufacturing sector, the domination of a few large business groups has slowed the emergence

of small and medium enterprises (SMEs). This is why trade, transport, communications, and

other services are the only sectors – excluding mining and oil – that have contributed to growth

over the past twenty years (with an average of 10.7%, 4.9%, and 11% of GDP, respectively, over

the period 1991-2008). Meanwhile, agriculture (excluding cattle farming) has accounted for only

a modest part of GDP (3.7% on average for the period 1991-2008). Despite its significant

contribution to growth in the early 1990s, industrial fishing has fallen back because of the age of

the national fleet and increased competition from foreign fisheries. Meanwhile, manufacturing

has not yet managed to position itself as an engine of growth.

Options for Policies Aimed at Accelerating Economic Diversity

6. After the presidential elections of July 2009, the government of Mauritania

launched a program of reforms aimed at accelerating economic growth by improving the

institutional framework to reduce the constraints on private sector development. The

viability of growth in Mauritania remains strongly tied to the country’s competitiveness and to

the diversification of its industrial fabric, particularly through value-added activities. Even

though some progress has been achieved in social sectors such as education and health, only an

ambitious program of reforms aimed at improving public institutions, the yield of production

factors including human and financial capital and infrastructure, the investment climate, and

support programs for future development sectors will speed up economic growth, promote

employment, and improve social indicators.

7. With this in mind, the Government has prepared notes on sector policy in order to

promote a consensus over the priority actions to be undertaken in 15 critical areas.

Developed with the support of the World Bank and other technical and financial partners, these

1 Oil reserves have been estimated at 310 million barrels. It is anticipated that oil production will stabilize at about

75,000 barrels per day (b/d) and cease after 15 years. Unforeseen geological problems have reduced the volume

extracted from the oldest deposit to only 36,000 b/d in 2006 and to 10,700 b/d in 2009, far less than was previously

predicted. 2

For example, the Guelb II project aims to increase iron production to 11 million tons in 2009 and to 13.5 million

tons in 2013. The financing for this project is now in place.

xiv

notes set out the state of affairs in each area, identify the main challenges and constraints,

determine objectives and strategic directions, and identify short- and medium-term reforms. This

process will facilitate the preparation of a new Strategic Framework for Fighting Poverty (SFFP)

for the period 2011-2015 and the World Bank’s future Strategic Aid to Mauritania. The priority

reforms identified in these notes will also be part of the dialogue between the Mauritanian

Government and the World Bank, the IMF, and the country's other technical and financial

partners.

Crosscutting Issues

An examination of sector policy notes reveals a number of crosscutting issues that remain a

hindrance to many emerging sectors.

8. Progress is often not about identifying but rather about implementing what needs to

be done. Many recommendations in the sector notes in effect reflect proposals that have been

made for some time. In many cases, even though significant financial and technical assistance (in

the area of privatization, for example) was provided, project implementation was weak and did

not lead to expected results. This reflects the difficulties associated with current economic

policies, on the basis of which the unbridled pursuit of income-maximizing activities coupled

with the weight of economic interest groups constitutes a hindrance to deployed efforts. Future

efforts toward reform should therefore attend to the current economic policy context and

concentrate on sectors that offer reasonable chances that projects will be successfully

implemented by taking into account the interests of all and by building partnerships suitable for

these reforms.

9. In addition to economic policy constraints, many sector policy notes highlight the

lack of capacity as a severe constraint on reform implementation. In the policy note on the

public sector, for example, there are significant recommendations for capacity building in the

public service. Generally, however, it is important to focus future capacity building and technical

assistance efforts on areas where current economic policies are conducive to reform.

10. Given that the public sector is lacking in financial and human resources, it is

important that its scope of activities be reviewed and that areas in which it can play a role

be identified. For example, although the public sector currently manages commercial activities,

the private sector may be more efficient in playing that role. Similarly, the private sector could

be involved in providing infrastructure services, particularly in the energy sector. In many

countries, the private sector is already playing a crucial role in providing services in the

education, health, and water sectors. This ensures that the public sector intervenes only where its

role is clearly justified. Among the advantages offered by such an approach are improvements in

public service delivery, more room to maneuver in the financing of basic government activities,

and a positive impact on the development of Mauritania’s highly dynamic private sector.

11. Poor decentralization of public services constitutes a significant obstacle to their

effective operation. This is the case in social sectors as well as in infrastructure and local

investment. Bringing services closer to those concerned would allow for greater public service

accountability as well as increased adaptation. Meanwhile, it is obvious that any successful

decentralization process requires deep political commitment. Similarly, significant efforts will

xv

need to be made to ensure that adequate capacity and suitable accountability mechanisms are set

up locally.

12. As regards infrastructure, the lack of adequate financing for maintenance is a

serious handicap. This results in the rapid deterioration of equipment and increased costs for the

rehabilitation of infrastructure. In this respect priority should be given to maintenance costs

during budget planning and implementation by paying sufficient attention to the recurring costs

related to investments.

13. The obsolete nature of the legal and regulatory framework in Mauritania is a

catalyst for informal practices, corruption, and inefficiency. Better governance therefore

primarily depends on a fundamental revision of this framework.

14. Finally, many sector policy notes emphasize the need to give special attention to

issues relating gender and young people. As in many other countries in the region,

Mauritania’s long-term development and continued social stability clearly depend on education

and job creation for young people.

Strengthening Public Institutions

15. Improving public institutions requires better management of public finances and a

modernized and better organized civil service. In particular, the management of public

finances currently suffers from specific malfunctions requiring improvement in budget

preparation and execution, human resources management, and monitoring and auditing. Budget

preparation is carried out on a short term basis without a multi-annual approach and no

objectives assigned to specific government programs. Despite some efforts being made to

implement a medium term budget framework for the period 2008-2010, this was not carried out

for 2008-2009 because of a lack of capacity in the technical ministries involved. The redrafting

of legislative and regulatory texts, the training of personnel in institutions responsible for budget

preparation, and the improvement of human resources remain essential. Budget execution suffers

from too many derogations, which should remain strictly limited, and from inadequate

monitoring at the decentralized level. The devolution of purchasing procedures and financial

control should be accompanied by the strengthening of audits and inspections, including the

publication of reports. Procurement procedures should be reviewed in depth to increase

transparency and insure separation between bodies responsible for tendering and those

responsible for monitoring and regulation. Furthermore, good governance also requires an Audit

Office staffed with specialized personnel to ensure the regular publication of reports.

16. The civil service currently suffers from organizational dysfunction. Staffing levels

are quite high. Various problems weigh on personnel management, recruitment, staff

remuneration, training, career management, and working conditions. Despite efforts made over

recent years, the lack of a management planning policy for staff entails a lack of control over

staff and future requirements. Thus, while Mauritania has about the same number of civil

servants as Benin, the population of the latter is more than twice that of the former. The total

payroll/GDP ratio also confirms the excessive number of civil servants in Mauritania. Human

resources management, in particular, suffers from problems linked to the lack of knowledge on

the part of the public service regarding legislation and procedures governing State personnel,

mediocre staff management at the ministerial level, the lack of monitoring of attendance at work,

xvi

instability in personnel responsible for the management of human resources, and low salaries.

Other dysfunctions are linked to the general status of the civil service, whose function is

compromised by informal procedures and unclear responsibilities. Corruption in the civil service

is also an obstacle to fair access to public services. Priority actions should lie principally in: i)

completing a census of staff; ii) implementing a more flexible system for managing human

resources based on management focused on results; iii) promoting good governance and fighting

corruption; iv) revitalizing the National School of Public Administration; v) adapting training

programs to the needs of administrative services, and vi) management planning for staff.

Improving Production Factors: Human Capital and Infrastructure

Human Capital

17. Overall, the strengthening of human capital is fundamental to the sustainability of a

qualified workforce. However, the Mauritanian educational system continues to perform

poorly in terms of retention, quality, and efficiency. The situation arises from a series of

internal structural problems at the level of pre-school, basic education, general secondary

education, and technical and vocational training as well as from external factors. Despite an

improvement in quantitative indicators such as the enrollment rate in schools over the past

decade, qualitative indicators for education remain poor. The student retention rate and the

knowledge acquisition rate in primary education are both low. Teacher training is inadequate,

teacher motivation is poor, and the distribution of teachers across regions is uneven. In addition,

there is almost no bilingual staff, and infrastructure is inadequate. There is also a lack of teachers

capable of meeting requirements at the basic, secondary, and higher education levels.

Accordingly, to remedy these constraints, it is necessary to target the strengthening of human

resources (quality and motivation of teachers, quality of training, strict compliance with school

hours) and infrastructure (refurbishment of schools, completion of unfinished schools, provision

of teaching materials). However, training must also be better adapted to needs. At the pre-school

level and in basic education, improving access to education and the quality of that education as

well as the restructuring of the provision of education should also be prioritized. Finally, the

restructuring of secondary education should diversify its syllabus and strengthen the teaching of

science.

18. Employment and vocational training are closely linked in that recent economic

growth has not generated enough jobs while the inadequacy of professional training

relative to the requirements of the national market has increased the number of

unemployed. The employment situation is very worrying, with a high unemployment rate

(31.2%)3 that particularly affects women and the young, as shown by the 2008 survey on

household standard of living (EPCV). Since the capacity of the Mauritanian economy to create

jobs is not sufficient to absorb increased demand, a significant portion of the population works in

the notoriously precarious informal sector. In addition, the level of training and professional

qualification of the active population remains low. In general, public policy has long ignored

employment as a priority development objective, which explains, among other things, the

absence of structured public dialogue, the low level of financing for employment programs, and

the lack of an information system on employment. The main strands of a policy promoting

3 Slightly lower than estimated in 2004 (32.5%).

xvii

employment should consist of: i) the implementation of public programs for creating

employment; ii) the revitalization of assistance for job seekers and for placing job seekers in

employment; and iii) the promotion of SMEs through microfinance.

19. At the technical and vocational training level, the challenges are enormous

especially in view of the number of young people who leave the education system every year

and could be candidates for vocational training. Responding to this situation requires: i)

improving careers advice, better governance of vocational training, and strengthening

management capabilities to achieve results; ii) mobilizing financing resources; iii) improving the

quality of training including creating a structure for training trainers; and iv) extending and

diversifying training opportunities by creating new institutions providing short-term training

adapted to local realities in unrepresented sectors and in the regions.

20. The employment and social welfare sector is an important element, particularly as

regards the definition of objectives assigned to public employment services as well as their

expertise and responsibilities in the strengthening of social dialogue and support for

reforms in this area. The migration of workers, which is a challenge in Mauritania, has forced

the administrative services in charge of employment to acquire expertise in the field of

employment law in order to ensure that implementation conforms to international conventions.

In addition, priority reforms should target: i) adapting the regulatory framework to the

socioeconomic context; ii) the renewal of trade union federations through elections; iii)

strengthening public employment services to enable regulations to be applied; iv) updating

legislation regulating social security and the National Agency for Occupational Health (Office

National de la Médecine du Travail); v) adapting the legal framework of the National Social

Security Fund (CNSS) to the country’s socio-economic context by analyzing the potential for

extending social cover to workers in the informal sector given that social security cover currently

extends to only about 7% of the active population.

21. The quality of human capital is also conditioned by the health of the population.

Current trends point to the risk that the Millennium Development Goals on child and maternal

mortality will not be reached. Nutritional imbalance also remains worrying, particularly for the

mother-child pair. The main problems in the health sector particularly involve the country’s

epidemiological profile, the state of the sanitation system, and the environment (hygiene, access

to drinking water, sanitation, food security, people’s level of education). Sanitation remains

inadequate in some areas and personnel (nurses, midwives, doctors) is often qualitatively and

quantitatively inadequate. In addition, some hospitals have become degraded, there is a lack of

some types of specialized care as well as poor coordination between the decentralized health

centers and regional hospitals, and the use of resources made available to the sector is inefficient.

Priority action must target, among other things: i) expanding health provision to give every

citizen local access to health and nutrition services; ii) strengthening medical and paramedical

staff training; iii) providing medical expertise nationwide; and iv) improving access to medical

equipment and financing.

22. The development of the drinking water and sanitation sector is also crucial to

human capital development and to the attainment of the Millennium Development Goals. Urban and semi-urban population growth limits progress in extending the coverage rate for

xviii

drinking water. The restructuring of this sector carried out between 2001 and 2008 has improved

the framework for intervention by creating specialized institutions. The water code has

established a framework for a partnership between the State, local communities, and private

operators. However, reform implementation remains incomplete either at the legislative level or

as regards accompanying measures. Weak civil service capacity remains a major constraint on

the sector. The sector strategy priorities outlined in the 2006-2010 Strategic Framework for the

Fight against Poverty (CSLP)4 must be strengthened through an annual program of hydraulic

infrastructure construction. Information on water resources must be improved, surface water

upgraded, sanitation measures in urban and rural areas reactivated, the public-private partnership

promoted, and stakeholder capacities strengthened at both central and local levels.

Infrastructure

23. To encourage the diversification of its production base, Mauritania must address a

lack of capacity in the electricity sector. Demand for electricity has greatly increased,

particularly in urban areas, and rural electrification remains limited. The situation in the sector is

worrying, given the precarious financial position of the sole operator, SOMELEC, whose

accumulated losses exceed its capital and reserves. Furthermore, the Economic Regulation

Authority (ARE) does not regulate SOMELEC’s activities, which means that questions

concerning incentives, how the operator is remunerated, and how the sector is performing remain

unexamined. There is an urgent need for change, particularly in the area of strengthening

SOMELEC’s management (collecting bills, fighting fraud, reducing technical loss, and

eliminating State-SOMELEC cross-debts), increasing its production capacity, and strengthening

rural electrification within the framework of a public-private partnership.

24. Another significant challenge for the country is upgrading transport infrastructure

to improve national competitiveness, including opening up agricultural production areas. The main constraints on transport development are linked to the country’s size, the poor

absorption capacity of public investment, high transport costs especially for marine freight, an

obsolete fleet of road transport vehicles, an inadequately maintained road network, the need to

upgrade infrastructure and port and airport equipment, the lack of staff training, difficulty in

applying legal and regulatory texts, and the absence of a framework for public-private

partnerships. As regards land transport, the road network is poorly developed and improved,

unpaved roads are rapidly becoming unusable. It is therefore necessary to strengthen the

management of the road fund, implement prioritized programs for road investment that will

promote the main axes of regional integration, build local tracks, and support road haulers in

modernizing their pool of vehicles. As regards port infrastructure, the two ports, Nouakchott and

Nouadhibou, are experiencing severe capacity constraints. Nouakchott's port is in urgent need of

an expansion program because it cannot handle a larger volume (two million tons per annum

compared to the predicted one million). Its costs are high (twice those of Dakar), as is the

waiting time for unloading onto docks. The structures of Nouadhibou's port do not meet security

requirements especially for the processing of oil cargoes, and do not allow for the development

of fishing to be stimulated. In Nouakchott, a public-private partnership should make possible the

construction of a new dock for container ships as well as of new docks for processing bulk cargo.

Similarly, Nouadhibou's port needs in-depth restructuring and rehabilitation so that it can better

contribute to the development of the fisheries sector and provide for the export of ore.

4 The Mauritanian authorities adopted the CSLP in October 2006.

xix

25. The development of the water supply and sanitation sector is also a priority for the

development of human capital and to attain the Millennium Development Goals. The

growth in the urban and semi-urban population has constrained progress in the coverage rate for

drinking water. The restructuring of the sector carried out between 2001 and 2008 has improved

the framework for intervention by creating specialized institutions. The water code has

established a framework for a partnership between the State, local communities, and private

operators. However, the implementation of reforms is not yet complete either at the legislative

level or in accompanying measures. The weakness of civil service capacity remains a major

constraint on the sector. The sector strategy outlined in the 2006-2010 SFFP priorities must be

strengthened by an annual program of hydraulic infrastructure construction. Information on

water resources must be improved, surface water upgraded, sanitation measures in urban and

rural areas reactivated, the public-private partnership promoted, and stakeholder capacities

strengthened at both central and local level.

Development of the Private Sector and Sectors with Future Potential

The Investment Climate

26. The investment climate is generally unfavorable to the development of the private

sector and therefore requires further sustained reform to stimulate the creation of jobs and

the diversification of the productive fabric. Despite reforms in various areas, these have not all

produced the results anticipated due to a lack of appropriate accompanying measures. The main

barriers5 to the development of the private sector are linked to the under-development of

financial markets, limited access to credit especially for SMEs, an overly burdensome tax

system, the anticompetitive practices of enterprises, the unreliability of the infrastructure, the

cumbersome nature of administrative procedures, customs and foreign trade regulations, the lack

of qualified workers, corruption, the poor operation of the legal system, and the lack of public-

private consultation and of a framework for a public-private partnership. In this context,

intervention should focus on: i) finalizing the Investment Code; ii) assessing the possibility of

creating a special economic area; iii) promoting financial intermediation and access to credit; iv)

simplifying tax procedures and lightening the tax burden for SMEs; v) promoting a policy of

competition; vi) easing procedures for creating and closing businesses and improving

information service in customs administration; vii) strengthening the legal system; and viii)

reforming the public market system and adopting a strategy for fighting corruption.

Development of Sectors with Future Potential

27. Despite its potential, the rural development sector is experiencing a profound crisis.

5

According to the 2007 Assessment of the Investment Climate (ECI), approximately 45% of businesses

believe that the main obstacles to carrying out their activities are the under-development of financial markets,

limited access to credit, and the high cost of financing for businesses working in the formal sector. In addition, about

37% of businesses blame taxation and the administration of fiscal policy, while 34% stress that they are negatively

affected mainly by the anticompetitive practices of businesses working in the informal sector. Among obstacles to

the development of the private sector, mention is also made of poor access to electricity (30%), customs and foreign

trade regulations (24%), the lack of qualified workers (22%), corruption (18%), and the unreliability of the

infrastructure (16%).

xx

The policy for the sector is incomplete and its organization is inefficient and marked by

improvisation in programming and the implementation of agricultural campaigns. Managers are

poorly motivated, the level of poverty of those dependent on agriculture and cattle farming is

high, technical capital remains insufficient, and the implementation of land regularization is

slow. The production of irrigated agriculture is on the whole inferior to anticipated results, rain-

fed agriculture lacks support, and cattle farming suffers from limited productivity and processing

activity. It is therefore urgent to update the 2001 strategy for rural development, the acceleration

of land regularization, and the implementation of the pastoral and cattle farming codes. Priority

measures should focus in particular on: i) increasing production in irrigated areas; ii) supporting

rain-fed agriculture more efficiently; iii) rationalizing production in oases; and iv) modernizing

the cattle farming sector. This requires a series of actions targeting, among other things, the

revitalization of marketing channels at every level, increasing crop intensity in irrigated areas,

diversifying production, increasing the quality of seeds, improving the environment for foreign

private investment, facilitating access to credit, and encouraging public-private partnerships.

Institutional reforms are necessary to strengthen the information system at the level of the

Ministry for Rural Development (MRD) and to focus the activities of research agencies.

28. The fisheries sector has reached a critical stage of development in that fish resources

have been heavily exploited while benefits to the national economy are largely generated by

foreign companies and a large part of the benefits generated by the fisheries sector is

exported. The main challenges in the sector are protecting over-fished demersal species and

increasing the country’s added value by creating upstream and downstream processing capacity

on Mauritanian territory and by increasing the value of unloaded catch through preservation,

processing, and the promotion of sanitation. The absence of a strategic vision for the sector is

also a significant issue. In view of its obsolescence, the national fleet must be modernized.

However, financing is inadequate. Short-term priority actions should focus on: i) fixing

objectives for fishing catch and effort (initially targeting cephalopod fishing within an approach

that can be later transferred to other types of fishing); ii) setting up management mechanisms and

measures (records of all fishing vessels, completion of technical and regulatory audits, rules

governing the entry and removal of records); iii) setting up a fishing authorization program; and

iv) creating conditions for locating catches and promoting the products in Mauritania in the best

way possible including the adaptation of current infrastructure.

29. The mining sector can increase its contribution to the national economy in a

framework of transparency and the good management of the environment while promoting

mining exploitation that generates added value and jobs. Some challenges are linked to the

inadequacy of the human and material resources available to the central government, which is

responsible for the promotion and framing of the sector, the lack of diversification in mining

production, weaknesses in current mining exploration, security issues affecting both people and

installations, and the lack of basic infrastructure. Key reforms should focus on: i) improving the

legal and regulatory framework; ii) strengthening and ensuring the sustainability of the structures

created; iii) promoting mining among foreign investors; iv) creating a mining school to train

engineers; v) strengthening coordination at the administrative level; and vi) preventing the

negative impacts of mining activity on the environment. Proceeding with the implementation of

the Extractive Industries Transparency Initiative (ITIE),6 which was delayed because of political

6

Mauritania is a candidate country for ITIE. The deadline for validation is March 9, 2010.

xxi

instability in 2008, is important for the good governance of resource rent.

30. Finally, although Mauritania is at the embryonic stage of its petroleum experience,

the sector remains strategic. The discovery of oil and gas deposits offshore and the operation of

the first oil field at Chinguetti in 2001 attracted oil companies, increasing revenues from the

2006 fiscal year. Although the industry has very high growth potential, it faces structural

constraints that, combined with the recent fall in oil production from the Chinguetti field and

rising servicing costs, led to a slow-down in exploration activities. Moreover, to date, there is no

strategy for promoting and exploiting oil blocks and the legal framework is unsuitable. In

addition, the Ministry of Energy and Petroleum does not have a competent operational

directorate, resulting in skill overlaps between the Ministry and the Mauritanian Hydrocarbons

Agency (SMH). Finally, since oil contracts are awarded without competition, oil exploration and

production are affected. Priority actions should focus on: i) adopting a hydrocarbon code and an

oil strategy and establishing a call for tenders mechanism for applicants to acquire oil blocks; ii)

improving the performance of the hydrocarbons department in the Ministry of Energy and

Petroleum; iii) reviving exploration activities, increasing production activities, and creating a

stable business and work environment; iv) starting production in the first gas pool; v) promoting

public-private partnerships; and (vi) closing audit records of recoverable oil costs on some

exclusive exploration licenses.

31. The matrix below presents a synopsis of recommendations for short- and medium-term

policies.

Recommendations Matrix

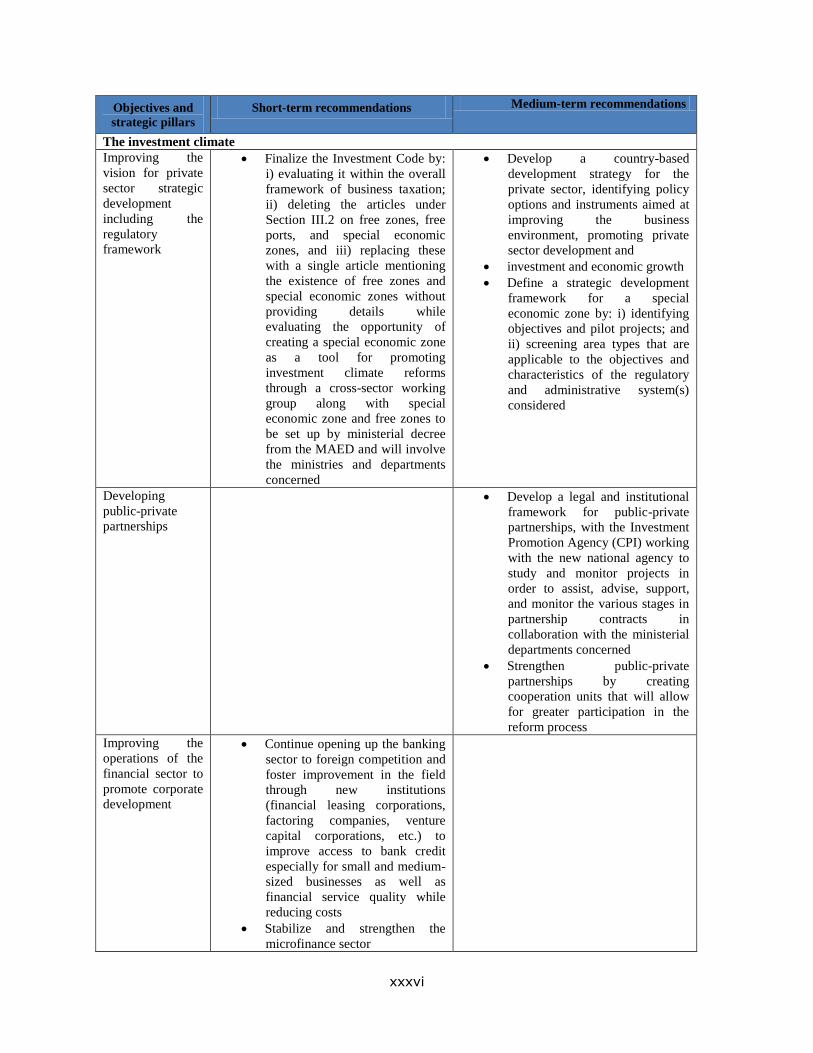

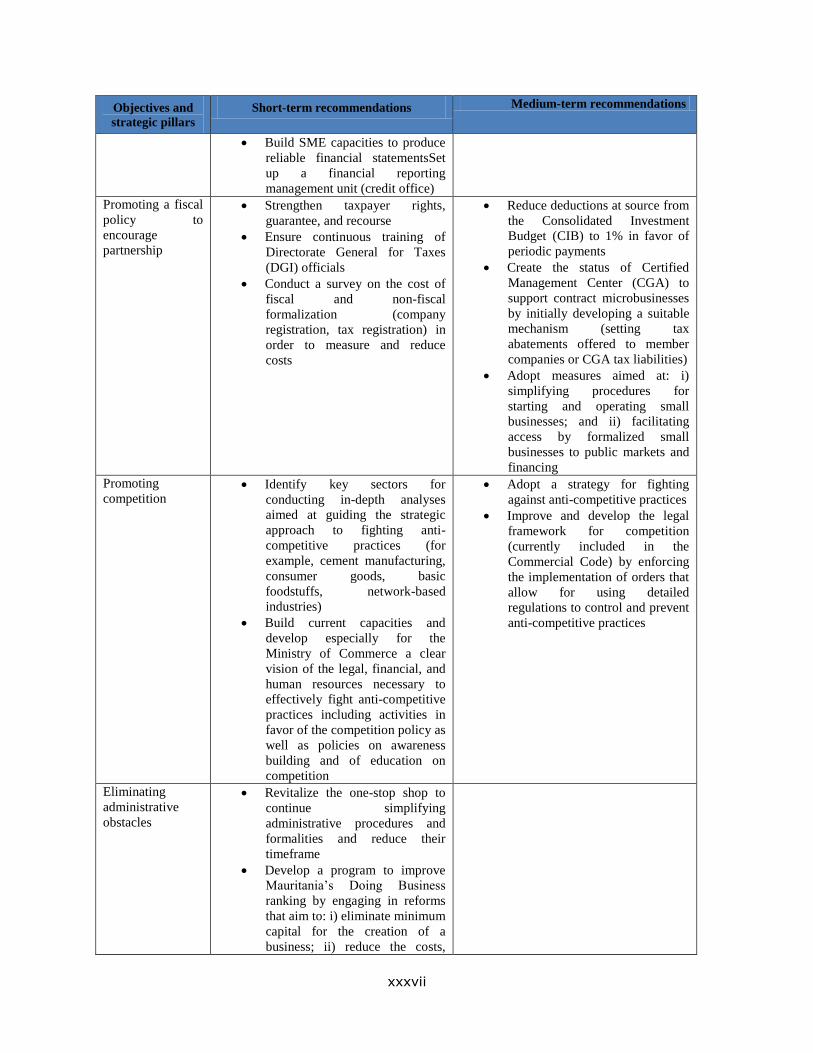

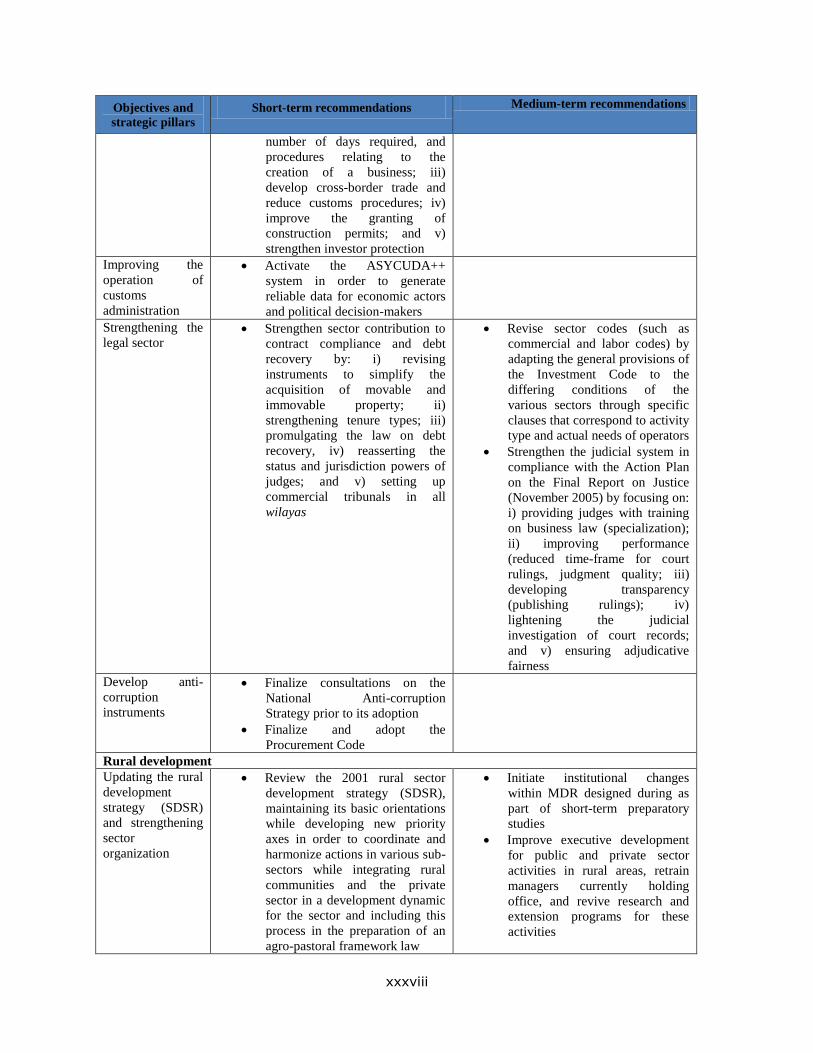

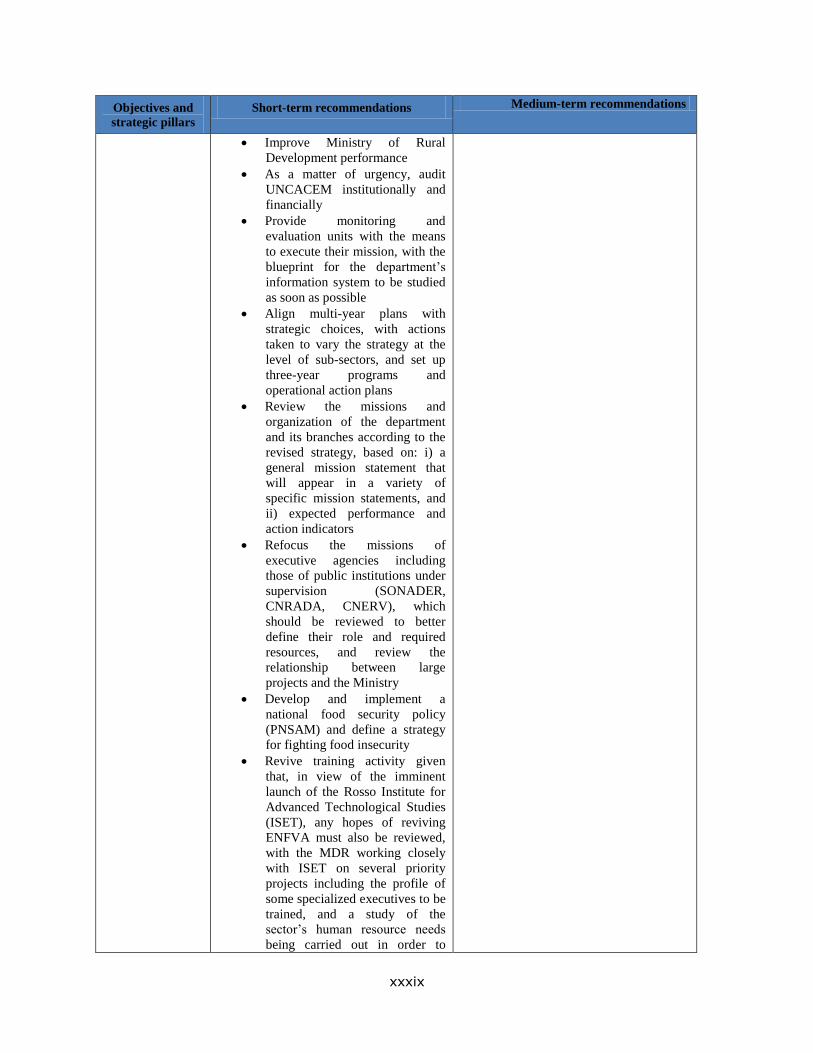

Objectives and

strategic pillars

Short-term recommendations Medium-term recommendations

Strengthening public institutions

Managing public funds

Establishing a

framework for

public finance

reform and

consolidating

reforms already

underway

Establish a public finance reform

framework with a TFP

monitoring committee

Establish performance indicators

to measure public finance

assessment via a PEFA

Ambitiously consolidate reforms

already underway (decentralizing

payment orders, strengthening

financial control and

administrative and financial

directorates, dialogue between

sector ministries and the

Directorate-General of the

Budget)

Improving budget

preparation,

focusing on

programs and

medium term

objectives

Submit the 2011 Finance Bill

(LDF) to the National Assembly

for consideration within a

reasonable timeframe to improve

the quality of parliamentary

monitoring

Introduce the 2011 budget bill

Strengthen the capacity of the

National Assembly Finance

Committee to examine the budget

and the Medium-term Budgetary

Framework (CBMT) and

strengthen the Ministry of

Finance’s technical capacities for

xxii

Objectives and

strategic pillars

Short-term recommendations Medium-term recommendations

including fiscal years 2012 and

2013 and including external

funding expenditure

Base budget planning on analyses

of region-based infrastructure

needs in close collaboration with

the CSLP and strengthen

strategic planning by better

aligning the CBMT with

priorities stated in the third CSLP

(2011-15) action plan

Establish performance contracts

between the State and public

enterprises in view of the results

of the audit to be conducted on

the State portfolio in order to

minimize budget overruns caused

by additional grants to these

public entities

Implement the timetable

established following the CBMT

workshop (CBMT, CDMF, and

the 2011-13 budget program for

pilot ministries)

Improve payroll supervision and

personnel management

Harmonize public service and

finance salary records and

implement the setting up of the

computerized personnel

management system

producing annual and multi-

annual budget estimates

Review major legislative and

statutory texts governing public

finance management (organic law

on LFDs, general regulations on

public accounting, framework

law on CSLP, budget