Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

RandeeAbramsonJaime AngaritaAlan CampbellBethany Carr

Lynn ClementsRichard Dotson

Lucinda GallagherWendy Johnson

Thomas LongmanJames LuffmanWilliam MaloneyRoger Michels

Christine MorenoMario Nowogrodzki

Pat PattersonRobert RankinRichard Shapiro

Poornima Srinivasan

Lynn H. Clements,DBA, CPA, CMA, CFM CFE, Cr.FAProfessor of AccountingFlorida Southern College Barnett School of Business & Economics

Odalys B. Lara, CPA, CVA, CFFA, CFD, CFFPartner/Perzel & Lara Forensic CPAs, PA

Fraud: It's Still a Big Problem

Lynn H. Clements, CPA, CMA, CFM, CFA, CFE

,

DBA, CPA, CMA, CFM, CFE, CrFAProfessor, Florida Southern College

Dr. Lynn H. Clements, Professor of Accounting at Florida Southern College, began as an adjunct instructor in 1984, and as a full-time instructor in 1990. After earning her Bachelor of Science degree at Florida Southern College, she practiced public accounting for 6 years, and then earned the Master of Business Administration degree at FSC. She has been certified as a Florida CPA since 1980, as a CMA (Certified Management Accountant) since 1992, as a CFM (Certified in Financial Management) since 1997, as a Cr.FA (Certified Forensic Accountant) since 2002, and as a CFE (Certified Fraud Examiner) since 2004. She is a member of the Florida Institute of Certified Public Accountants, American Institute of Certified Public Accountants, the Institute of Management Accountants (IMA), the American Accounting Association, and the Association of Certified Fraud Examiners. Lynn earned her Doctor of Business Administration degree from NovaSoutheastern University in March 2002. Her interests include family activities, reading, travel, and music.

Fraud: It’s Still a Big Problem!

Dr. Lynn H. ClementsCPA CMA CFM CFE Cr.FA

September 21, 2012

Objectives

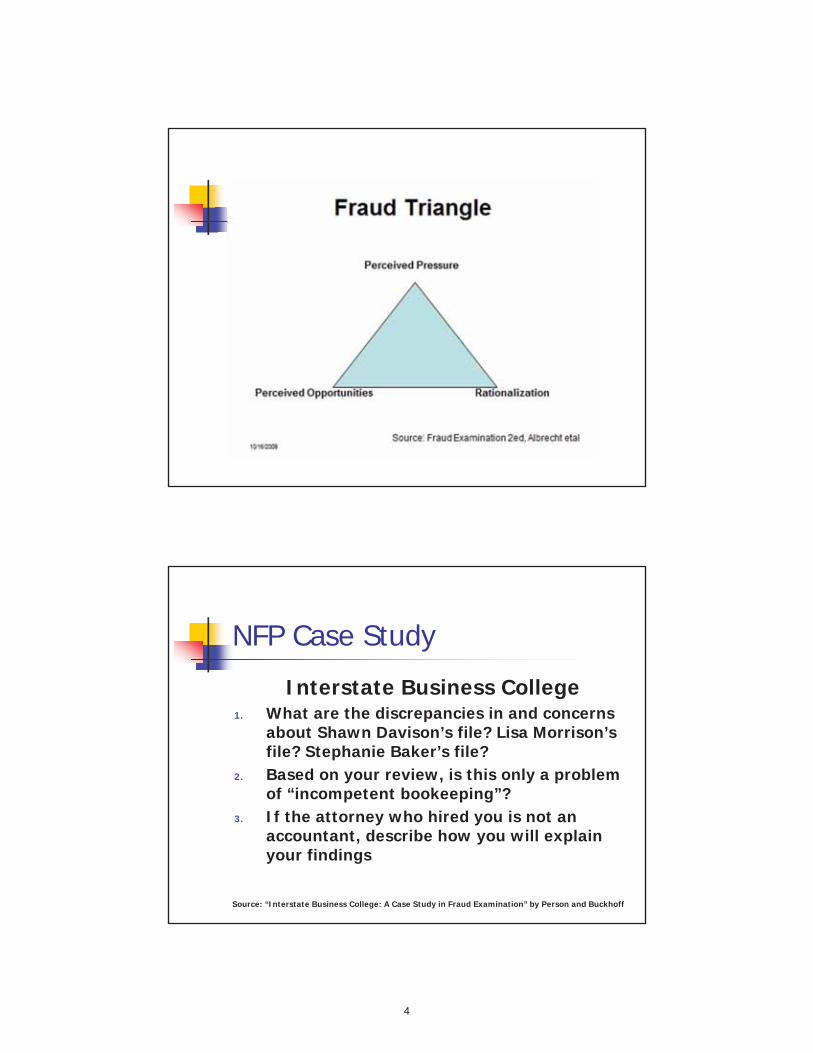

Fraud Triangle

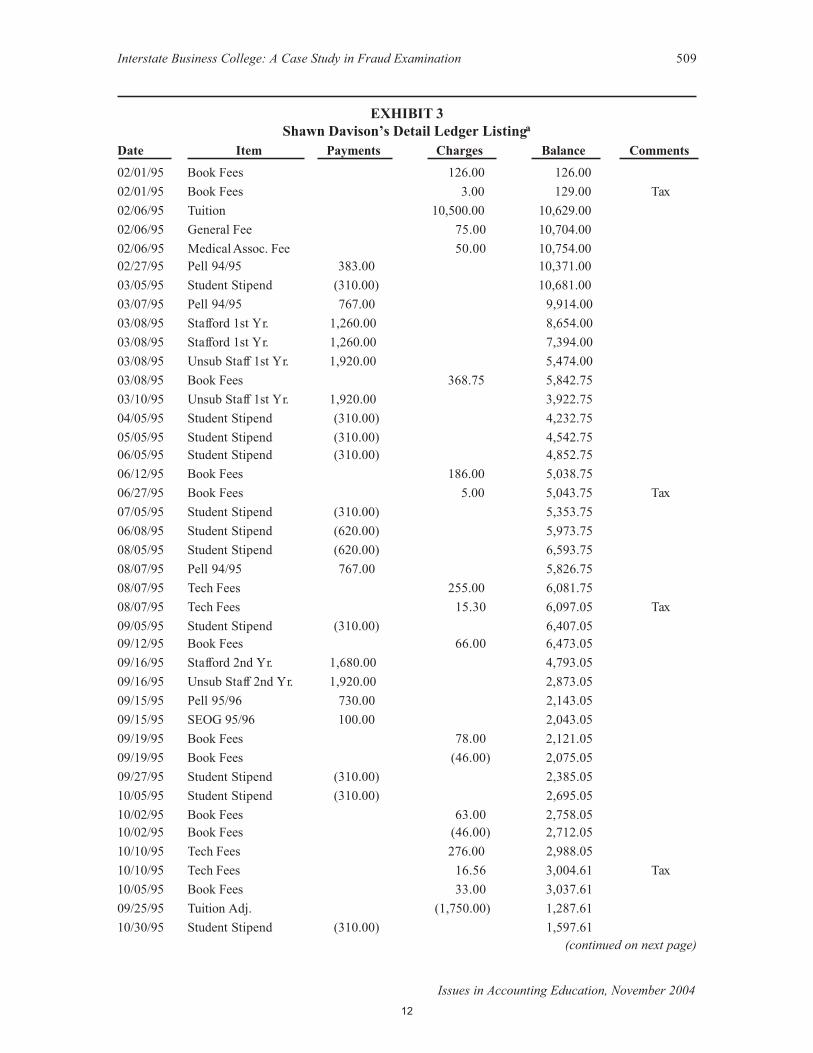

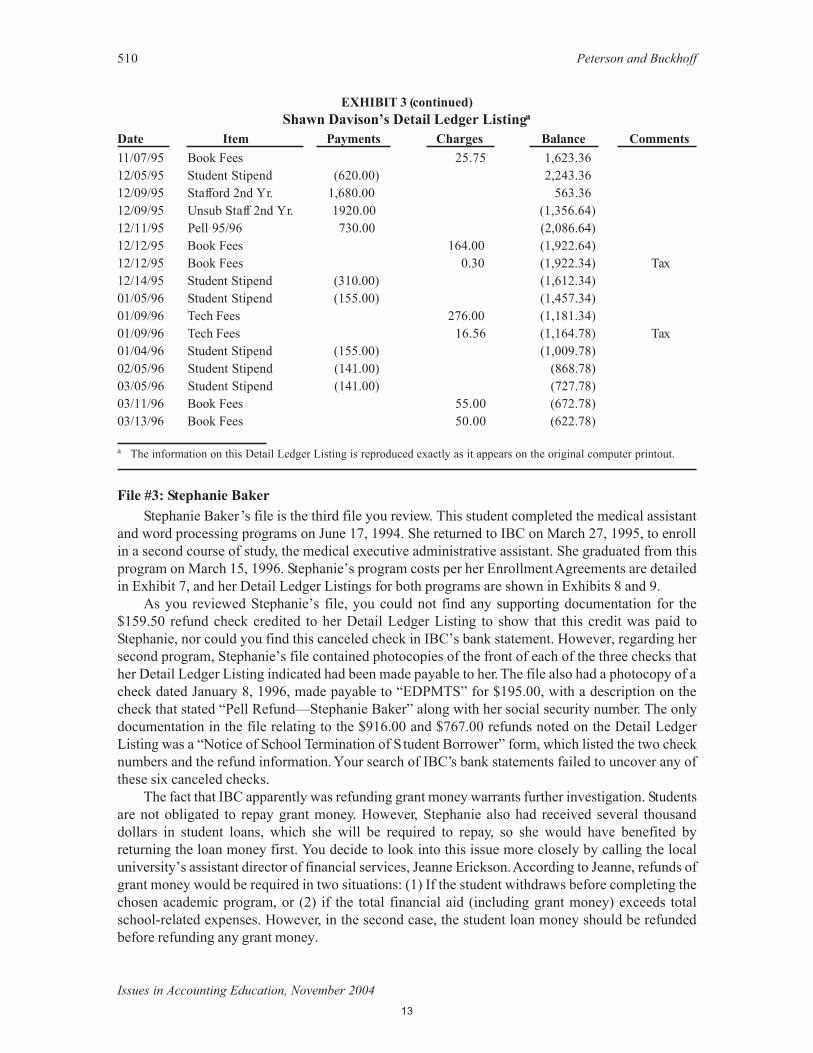

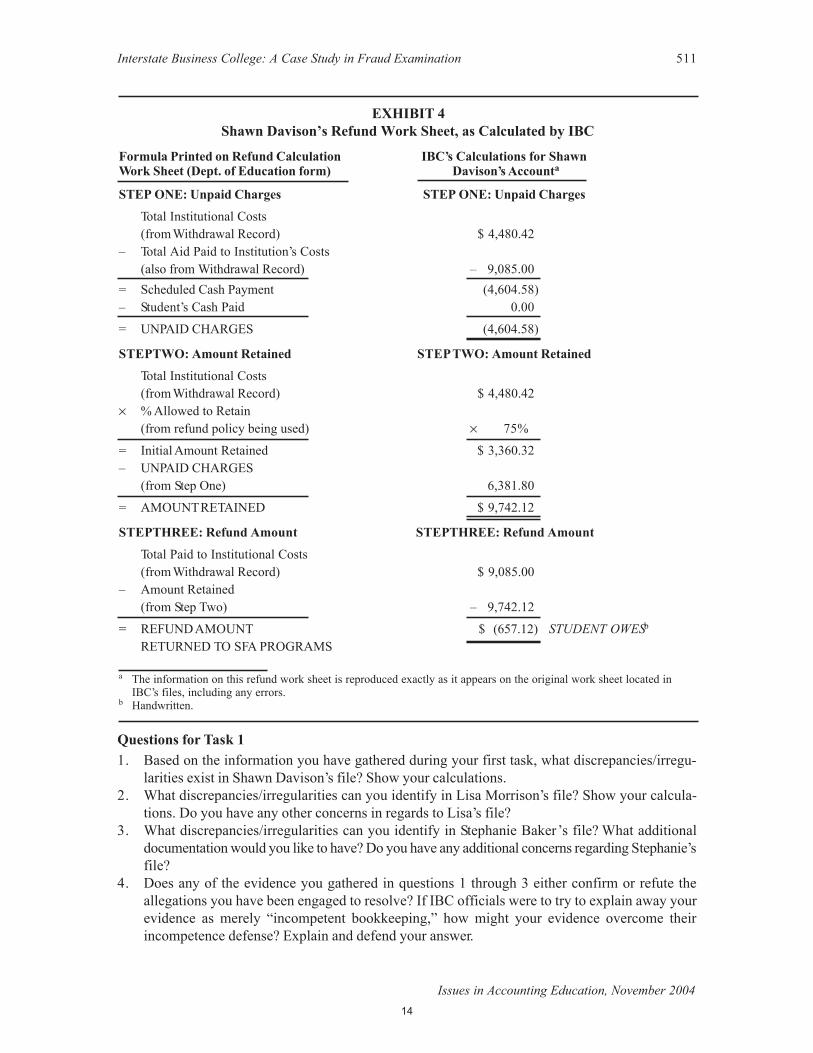

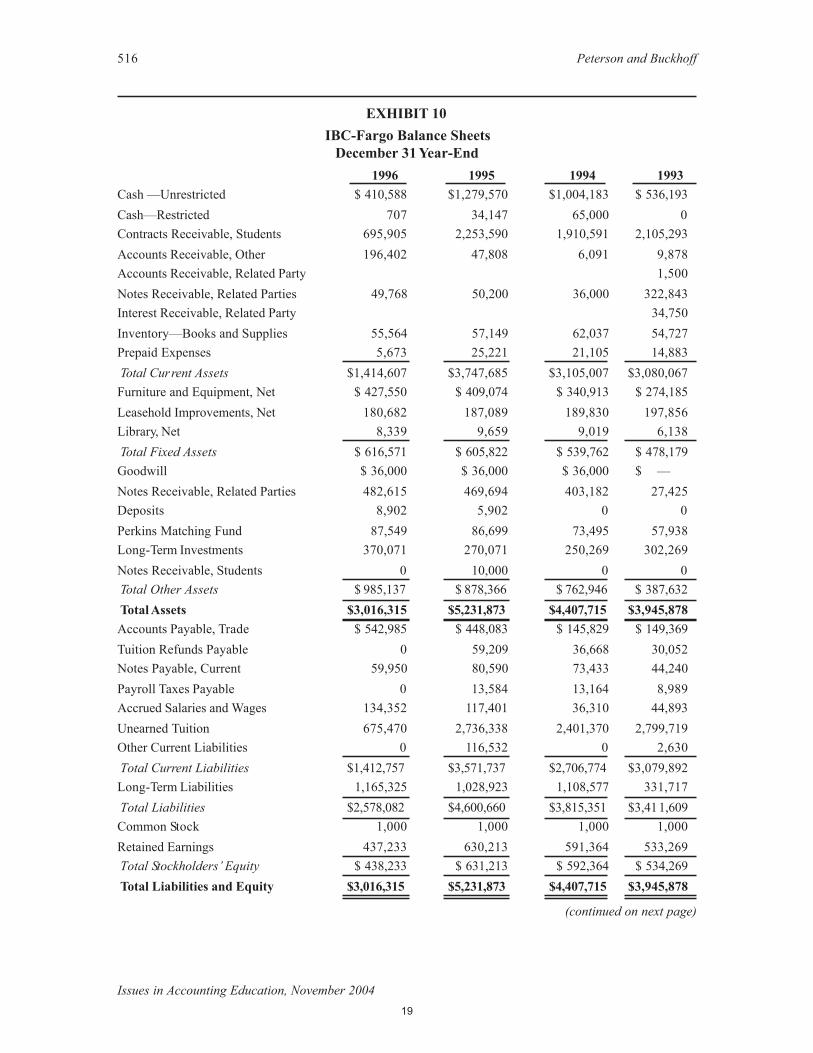

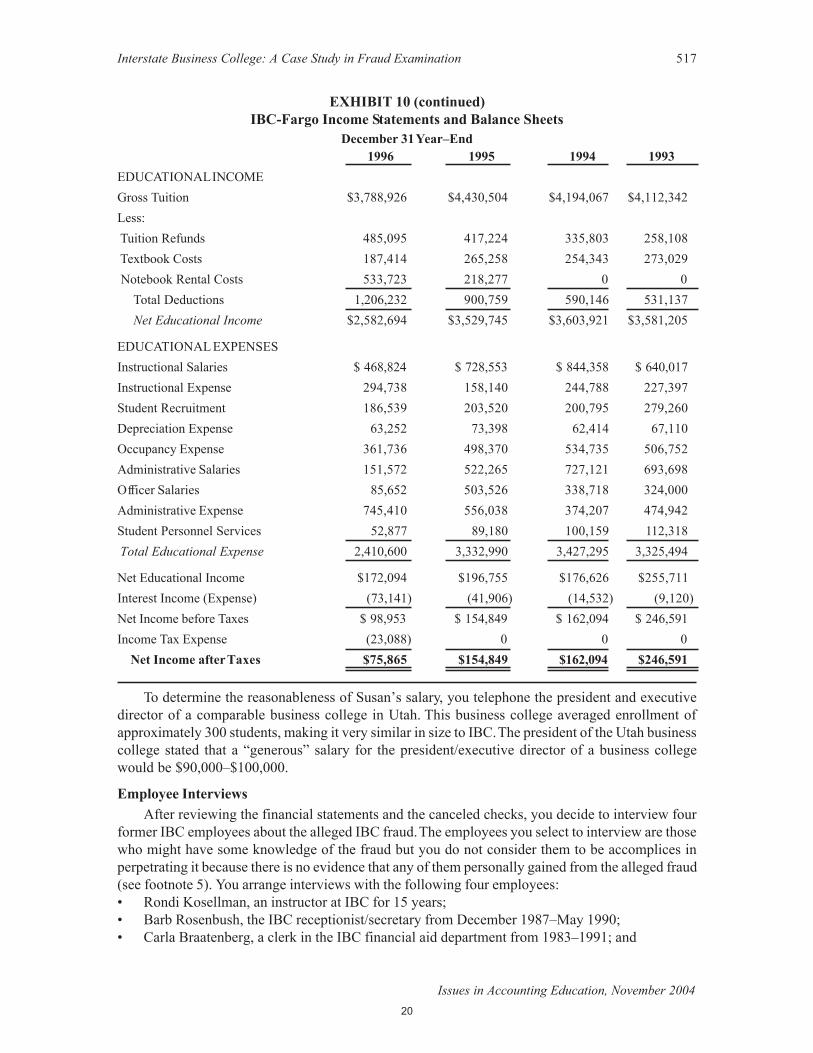

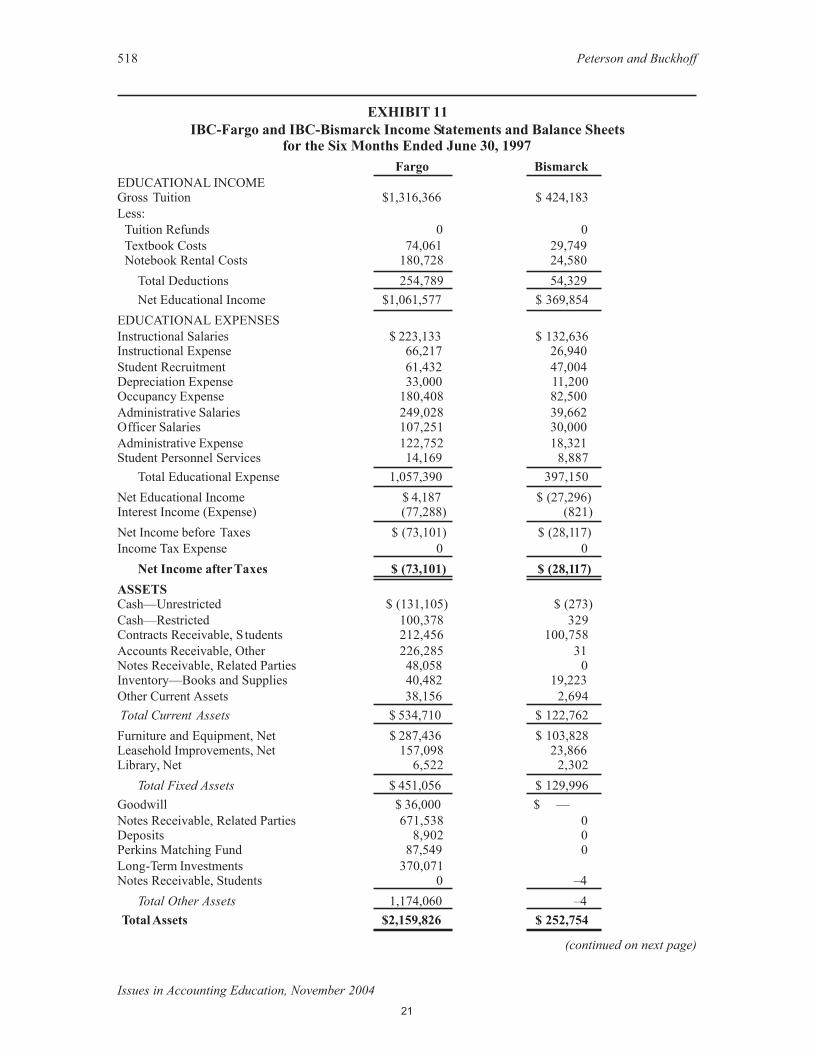

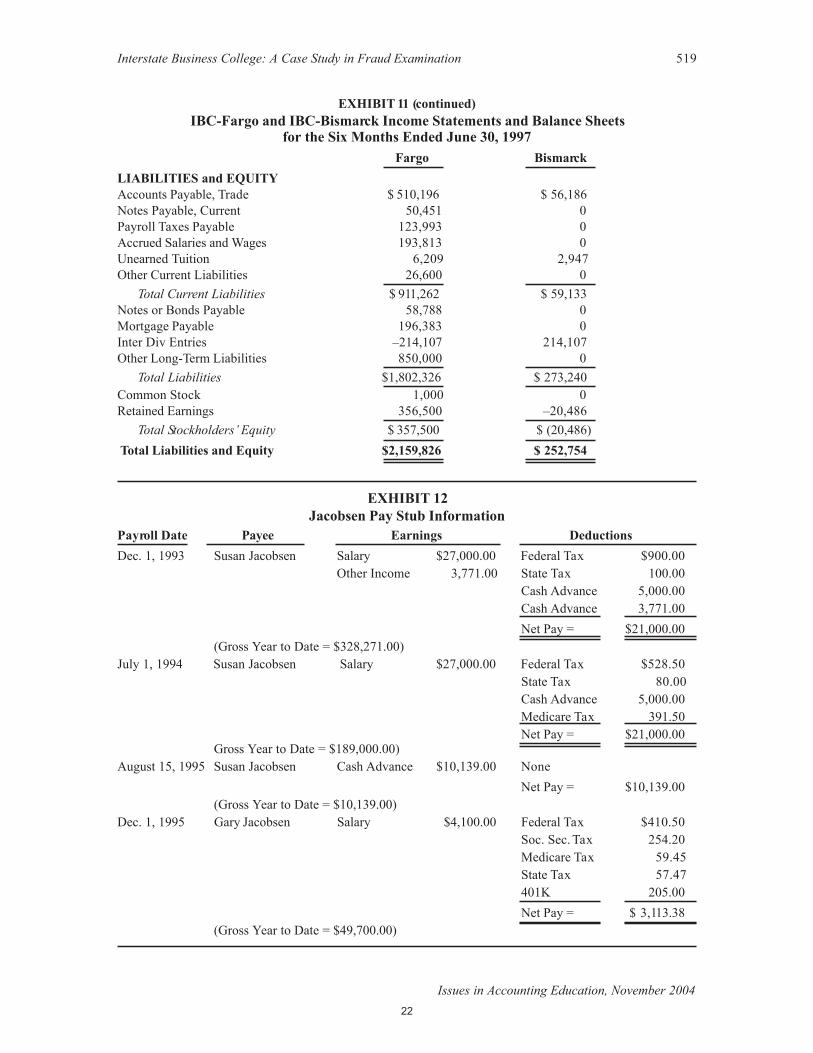

Interstate Business College: A Case Study in Fraud Examination, by Peterson and Buckhoff

NFP Case Study

Interstate Business College1. What are the discrepancies in and concerns

about Shawn Davison’s file? Lisa Morrison’s file? Stephanie Baker’s file?

2. Based on your review, is this only a problem of “incompetent bookeeping”?

3. If the attorney who hired you is not an accountant, describe how you will explain your findings

Source: “Interstate Business College: A Case Study in Fraud Examination” by Person and Buckhoff

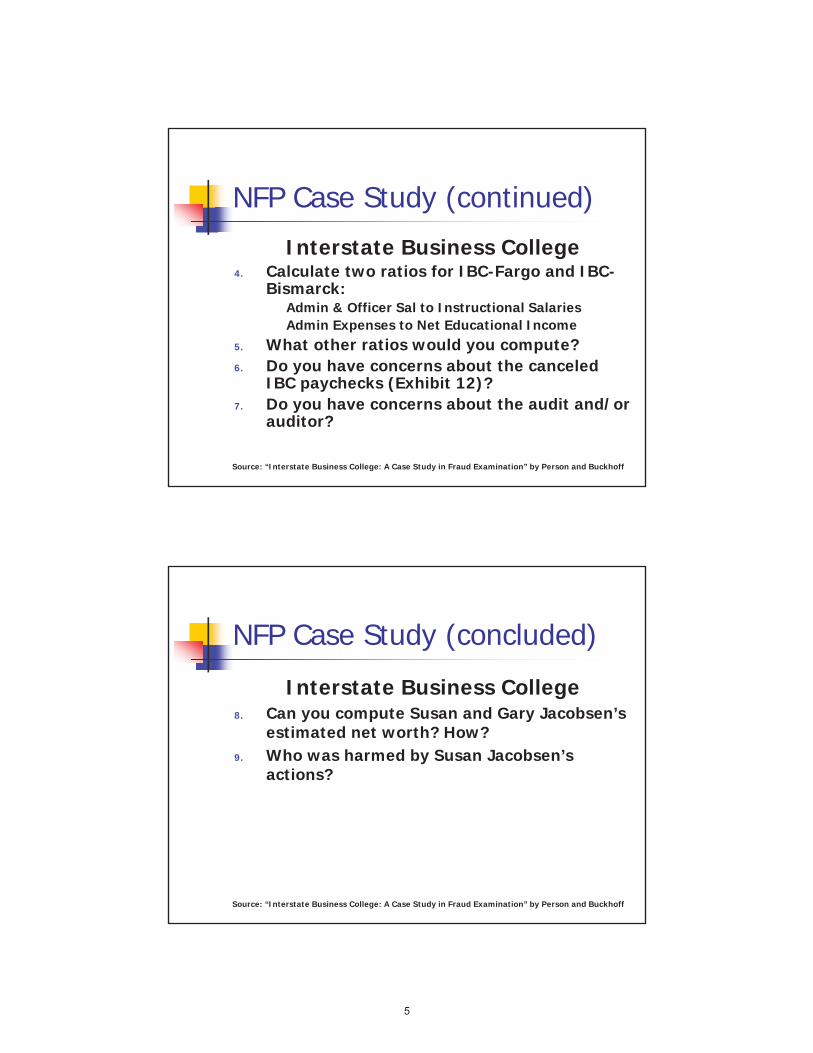

NFP Case Study (continued)

Interstate Business College4. Calculate two ratios for IBC-Fargo and IBC-

Bismarck:Admin & Officer Sal to Instructional SalariesAdmin Expenses to Net Educational Income

5. What other ratios would you compute?6. Do you have concerns about the canceled

IBC paychecks (Exhibit 12)?7. Do you have concerns about the audit and/or

auditor?

Source: “Interstate Business College: A Case Study in Fraud Examination” by Person and Buckhoff

NFP Case Study (concluded)

Interstate Business College8. Can you compute Susan and Gary Jacobsen’s

estimated net worth? How?9. Who was harmed by Susan Jacobsen’s

actions?

Source: “Interstate Business College: A Case Study in Fraud Examination” by Person and Buckhoff

Sources

Albrecht, Albrecht, & Albrecht (2005). Fraud Examination 2e. Southwestern.B.K. Peterson and T.A. Buckhoff, Interstate Business College: A Case Study in Fraud Examination, Issues in Accounting Education, 19(4), pp 505-527.

Questions?

Dr. Lynn H. ClementsCPA CMA CFM CFE Cr.FA

Dorotha C. Tanner Chair in Ethics in Business and EconomicsProfessor of AccountingFlorida Southern College

(863) [email protected]

×

×

Fraud: It's Still a Big Problem (continued)

Odalys Lara, CPA, CVA, CFFA, CFD,CFF

ODALYS Z. LARA, CPA, CVA, CFFA, CFFPRINCIPAL

Perzel & Lara Forensic CPA’s, P. A.

EXPERIENCE: Certified Public Accountant (CPA)Certified Valuation Analyst (CVA)Certified Forensic Financial Analyst (CFFA)Certified in Financial Forensics (CFF)

Odalys Z. Lara, CPA, CVA, CFFA, CFF is a principal of Perzel & Lara Forensic CPA’s, P.A. and co-chairs the firm’s litigation support department. Her extensive experience in providing a broad spectrum of professional services including forensic accounting, auditing, tax, pension and estate planning, provides the technical foundation required to excel as a certified business valuation analyst (CVA), Certified Forensic Financial Analyst (CFFA), and Certified in Financial Forensics (CFF).

Over twenty years as a certified public accountant, with a wide variety of experience in many different industries, with differing accounting practices and methods, as well as significant tax issues, has provided the technical background needed as a professional providing business valuations, forensic and fraud prevention services, expert witness, and litigation support services. Odalys Lara’s ability to communicate clearly as well as withstand cross-examination and other courtroom dynamics strengthen a case by adding an unparalleled level of credibility and expertise. Clients depend upon her business valuation recommendations in the areas of divorce, mergers and acquisitions, buy-sell agreements, partner and stockholder agreements, damage losses, and succession and estate planning.

Odalys has also earned the premier NACVA designation of Certified Forensic Financial Analyst in the areas of economic damages and fraud deterrence & detection (CFFA) and AICPA designation of Certified in Financial Forensics (CFF). She uses this additional training in forensic accounting to investigate and uncover financial fraud as well as construct fraud prevention programs.

Odalys’ experience includes valuation services for medical and professional practices, service businesses, construction, manufacturing, etc. Her varied background in working in many industries as well as her thirst for up-to-date technical information keeps her on the forefront of business valuation issues.

Odalys also teaches nationally for NACVA fraud prevention and detection training.

Slides by Perzel & Lara, Forensic CPA's

FRAUD CASES

Odalys Lara, CPA, CVA, CFFA, CFD, CFFPerzel & Lara Forensic CPA’s

2105 Drew StreetClearwater, Florida 33765

www.perzellara.com(727) 466-0777

Slides by Perzel & Lara, Forensic CPA's

Today’s Objective

• To review government fraud case• Warning Signs for Investments• Report to the Nation 2012

Slides by Perzel & Lara, Forensic CPA's

Case – Public School

• Government bidding and utilizing a lack of internal controls. Replacement of unnecessary parts. Billing employees at two different locations.

Case Background

• Plumbing contractor awarded bid for lowest bid

• Contract signed not shared with Accounts Payable Department

• Contractor submitted invoices with little or no documentation

Slides by Perzel & Lara, Forensic CPA's

Findings

• Billings utilizing incorrect hourly rate – not verified with contract

• Backflow for schools – comparison of – New Installation– Repair– Replace– Overlap of serial numbers among all three

categoriesSlides by Perzel & Lara, Forensic CPA's

Findings

• Employee categories incorrectly billed• Employee in two places at the same time

– Based on sign in sheets at different school locations

Slides by Perzel & Lara, Forensic CPA's

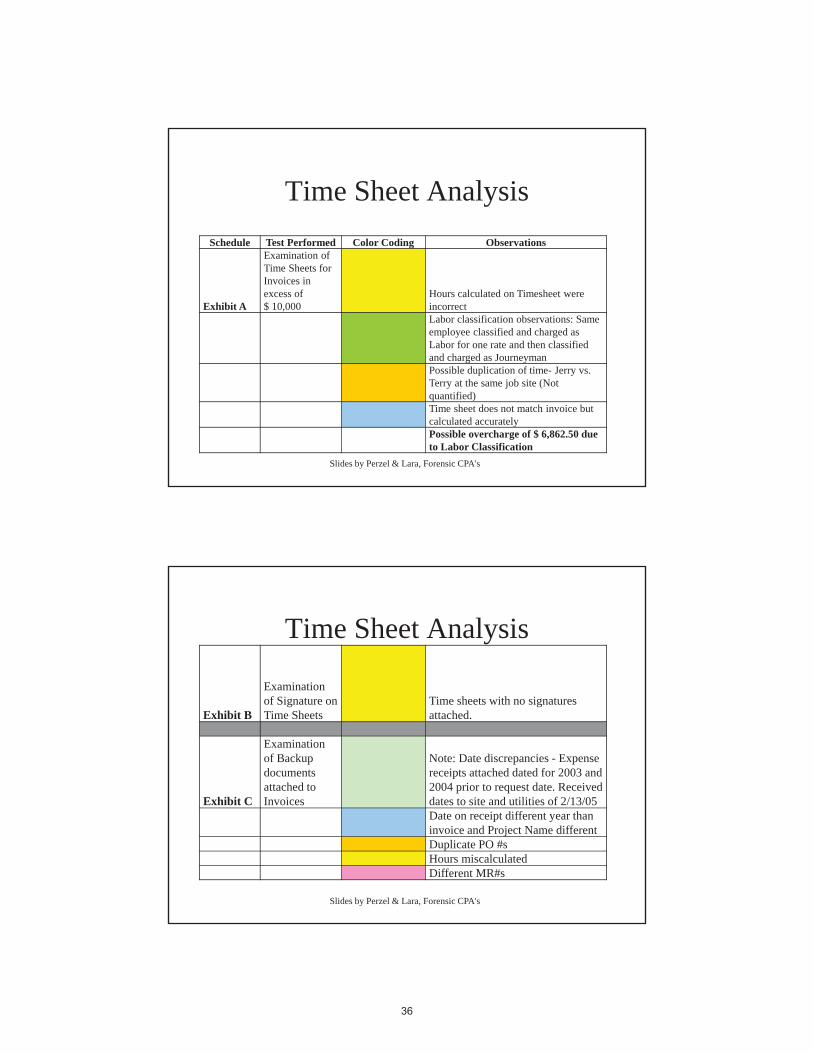

Time Sheet Analysis

Slides by Perzel & Lara, Forensic CPA's

Schedule Test Performed Color Coding Observations

Exhibit A

Examination of Time Sheets for Invoices in excess of $ 10,000

Hours calculated on Timesheet were incorrectLabor classification observations: Same employee classified and charged as Labor for one rate and then classified and charged as Journeyman Possible duplication of time- Jerry vs. Terry at the same job site (Not quantified)Time sheet does not match invoice but calculated accuratelyPossible overcharge of $ 6,862.50 due to Labor Classification

Time Sheet Analysis

Slides by Perzel & Lara, Forensic CPA's

Exhibit B

Examination of Signature on Time Sheets

Time sheets with no signatures attached.

Exhibit C

Examination of Backup documentsattached to Invoices

Note: Date discrepancies - Expense receipts attached dated for 2003 and 2004 prior to request date. Received dates to site and utilities of 2/13/05Date on receipt different year than invoice and Project Name differentDuplicate PO #sHours miscalculatedDifferent MR#s

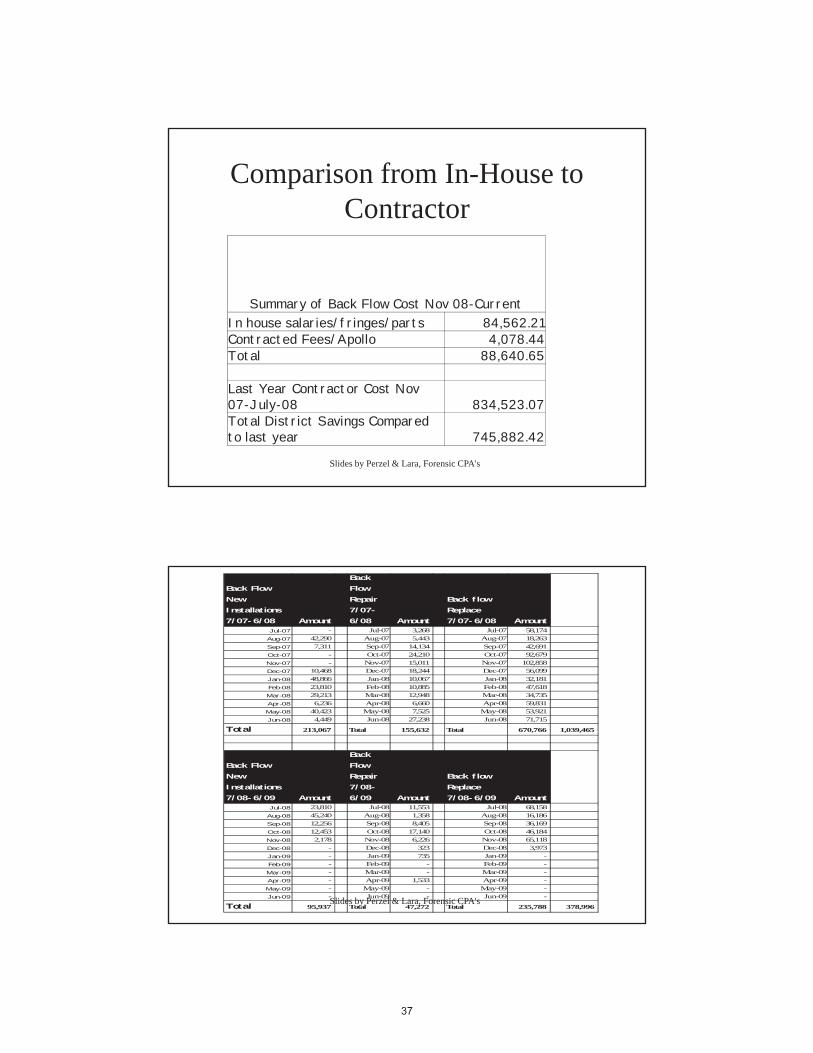

Comparison from In-House to Contractor

Slides by Perzel & Lara, Forensic CPA's

Summary of Back Flow Cost Nov 08-CurrentIn house salaries/fringes/parts 84,562.21Contracted Fees/Apollo 4,078.44Total 88,640.65

Last Year Contractor Cost Nov 07-July-08 834,523.07Total District Savings Compared to last year 745,882.42

Slides by Perzel & Lara, Forensic CPA's

Back Flow New Installations 7/07-6/08 Amount

Back Flow Repair 7/07-6/08 Amount

Back flow Replace 7/07-6/08 Amount

Jul-07 - Jul-07 3,268 Jul-07 58,174 Aug-07 42,290 Aug-07 5,443 Aug-07 18,263 Sep-07 7,311 Sep-07 14,134 Sep-07 42,691 Oct-07 - Oct-07 24,210 Oct-07 92,679 Nov-07 - Nov-07 15,011 Nov-07 102,858 Dec-07 10,468 Dec-07 18,244 Dec-07 56,099 Jan-08 48,866 Jan-08 10,067 Jan-08 32,181 Feb-08 23,810 Feb-08 10,885 Feb-08 47,618 Mar-08 29,213 Mar-08 12,948 Mar-08 34,735 Apr-08 6,236 Apr-08 6,660 Apr-08 59,831 May-08 40,423 May-08 7,525 May-08 53,921 Jun-08 4,449 Jun-08 27,238 Jun-08 71,715

Total 213,067 Total 155,632 Total 670,766 1,039,465

Back Flow New Installations 7/08-6/09 Amount

Back Flow Repair 7/08-6/09 Amount

Back flow Replace 7/08-6/09 Amount

Jul-08 23,810 Jul-08 11,553 Jul-08 68,158 Aug-08 45,240 Aug-08 1,358 Aug-08 16,186 Sep-08 12,256 Sep-08 8,405 Sep-08 36,169 Oct-08 12,453 Oct-08 17,140 Oct-08 46,184 Nov-08 2,178 Nov-08 6,226 Nov-08 65,118 Dec-08 - Dec-08 323 Dec-08 3,973 Jan-09 - Jan-09 735 Jan-09 - Feb-09 - Feb-09 - Feb-09 - Mar-09 - Mar-09 - Mar-09 - Apr-09 - Apr-09 1,533 Apr-09 - May-09 - May-09 - May-09 - Jun-09 - Jun-09 - Jun-09 -

Total 95,937 Total 47,272 Total 235,788 378,996

ONLINE SCAMS

• Craigslist• Beauty Products• Work at Home• Bank contacts• IRS• www.InternetScamsWatch.com

Slides by Perzel & Lara, Forensic CPA's

Identity Theft

• Subscribe to a credit monitoring service through one of the major credit bureaus.

• They provide daily monitoring• Experian• Equifax

Slides by Perzel & Lara, Forensic CPA's

As many as 9 million Americans have their identity stolen each year. Who's protecting your

identity?Product Overview

Slides by Perzel & Lara, Forensic CPA's

INVESTMENT PITFALLS

Slides by Perzel & Lara, Forensic CPA's

Slides by Perzel & Lara, Forensic CPA's

Forbes – 12 Warning Signs an Investment is a Scam

1. High returns are "guaranteed."• Run--don't just walk away from any pitch that uses

words like "guaranteed," "sure thing" or "no risk" while claiming a sustained return much in excess of what you can get with T-bills or a bank CD (admittedly, not much these days). Big returns come only with big risk.

Forbes – 12 Warning Signs an Investment is a Scam

2. A fellow Baptist is pitching you.• Or a fellow Lithuanian, African American, Mason,

Orthodox Jew, Rotarian or whatever. Beware any appeal that seeks to leverage a shared characteristic with you such as race, religion or social membership. That can be a tip-off to affinity fraud, premised on your letting down your guard because you’re with a spirit you think is kindred.

Slides by Perzel & Lara, Forensic CPA's

Forbes – 12 Warning Signs an Investment is a Scam

3. A stock went public in a reverse merger.• It's perfectly legal for a private company to

become public by merging with a dormant public company. The problem is this circumvents many protections of a traditional initial public offering, such as an underwriter on the hook if factual promotional statements should prove false. The current wave of collapsing Chinese stocks is being led by fallen reverse mergers.

Slides by Perzel & Lara, Forensic CPA's

Forbes – 12 Warning Signs an Investment is a Scam

4. There's a claim of "breakthrough technology."• Game-changing inventions do come along.

But they are not likely to emanate from that small, unknown company you are pondering. Look to see if that new technology is just licensed from another firm and still unproven.

Slides by Perzel & Lara, Forensic CPA's

Forbes – 12 Warning Signs an Investment is a Scam

5. Numbers are hard to come by.• A surprising number of supposedly public

companies don’t file extensive financial statements regularly with regulators. Many of them are listed on sketchy exchanges like the Pink Sheets. Are such companies really where you want to invest your retirement or college money?

Slides by Perzel & Lara, Forensic CPA's

Forbes – 12 Warning Signs an Investment is a Scam

6. Investment methodology makes no sense or is unexplained.• Ponzi-man Bernard Madoff fleeced investors of

billions after refusing to explain how he was able to generate excellent steady returns in both good and bad times. Don’t accept silence for an answer. This applies more to investments with money managers.

Slides by Perzel & Lara, Forensic CPA's

Forbes – 12 Warning Signs an Investment is a Scam

7. Who's that auditor?• Despite managing $65 billion (on paper),

Madoff was audited for years by a three-person accounting firm headquartered in a strip shopping mall. A big, well-known auditor is certainly no guarantee that an investment will work out, but it does reduce the chance of outright fraud.

Slides by Perzel & Lara, Forensic CPA's

Forbes – 12 Warning Signs an Investment is a Scam

8. A long-running offer isn't registered.• State and federal law permits sale of certain

securities that haven't been registered, or subject to extensive disclosures, so long as the number of investors is below a certain number. But that's probably not the case if the promoter has been running his campaign for years

Slides by Perzel & Lara, Forensic CPA's

Forbes – 12 Warning Signs an Investment is a Scam

9. A long-running offer isn't registered.• State and federal law permits sale of certain

securities that haven't been registered, or subject to extensive disclosures, so long as the number of investors is below a certain number. But that's probably not the case if the promoter has been running his campaign for years

Slides by Perzel & Lara, Forensic CPA's

Forbes – 12 Warning Signs an Investment is a Scam

10. Act now or else!• Beware any investment in which you are

pressured to hand over money immediately. It's often a ploy to keep you from doing research or consulting with others who may be knowledgeable. If you are looking at the long run, timing isn't that important.

Slides by Perzel & Lara, Forensic CPA's

Forbes – 12 Warning Signs an Investment is a Scam

11. Your money is going overseas.• Investing internationally makes a lot of

sense. But sending your cash to some foreign address you know nothing about does not. It's an added level of unneeded risk.

Slides by Perzel & Lara, Forensic CPA's

Forbes – 12 Warning Signs an Investment is a Scam

12. Your money is going overseas.• Investing internationally makes a lot of

sense. But sending your cash to some foreign address you know nothing about does not. It's an added level of unneeded risk.

Slides by Perzel & Lara, Forensic CPA's

Anti-Fraud Controls• Internal Controls• External Audit of Financial Statements• Code of Conduct• Internal Audit• Management Review• Independent Audit Committee• Hotline• Surprise Audits• Rewards for Whistleblowers

Slides by Perzel & Lara, Forensic CPA's

Internal Control Weaknesses• Duties are not segregated.• Physical safeguards are not present.• Independent checks are not made.• Proper authorization is not obtained

consistently.• Proper documents and records are missing.• Existing contents of documents can be

overridden.• Accounting systems are inadequate

Slides by Perzel & Lara, Forensic CPA's

Slides by Perzel & Lara, Forensic CPA's

Tips

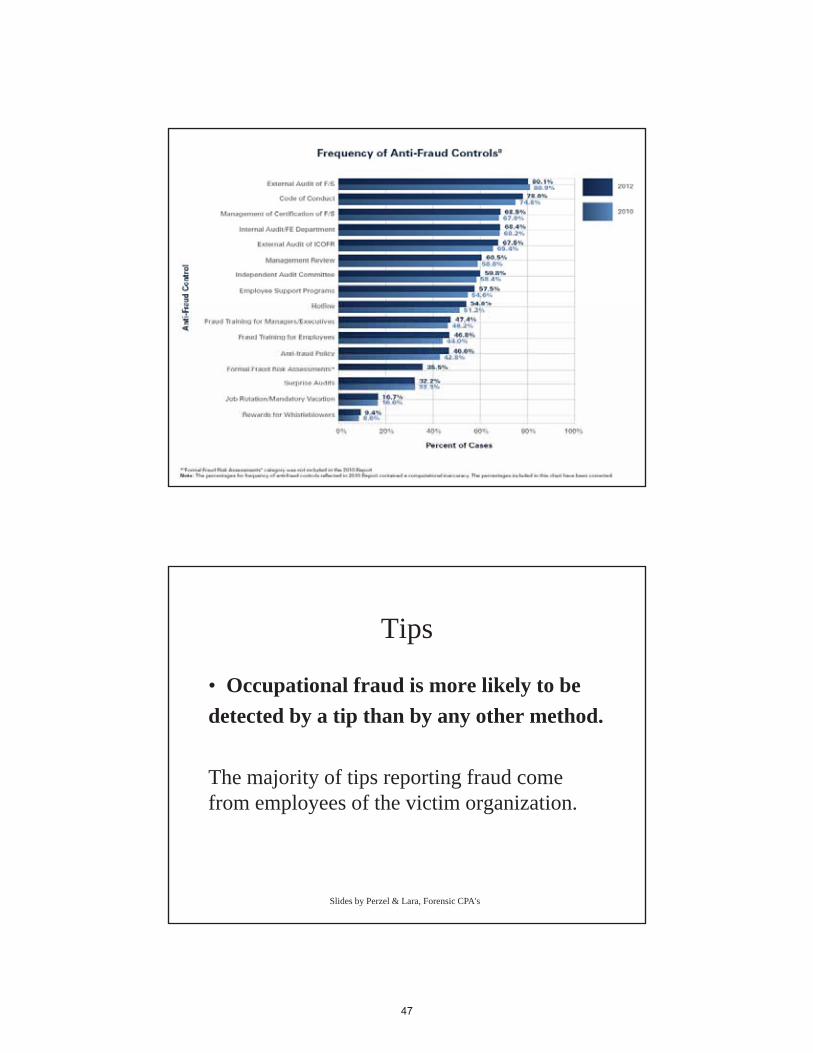

• Occupational fraud is more likely to bedetected by a tip than by any other method.

The majority of tips reporting fraud come from employees of the victim organization.

Slides by Perzel & Lara, Forensic CPA's

Slides by Perzel & Lara, Forensic CPA's

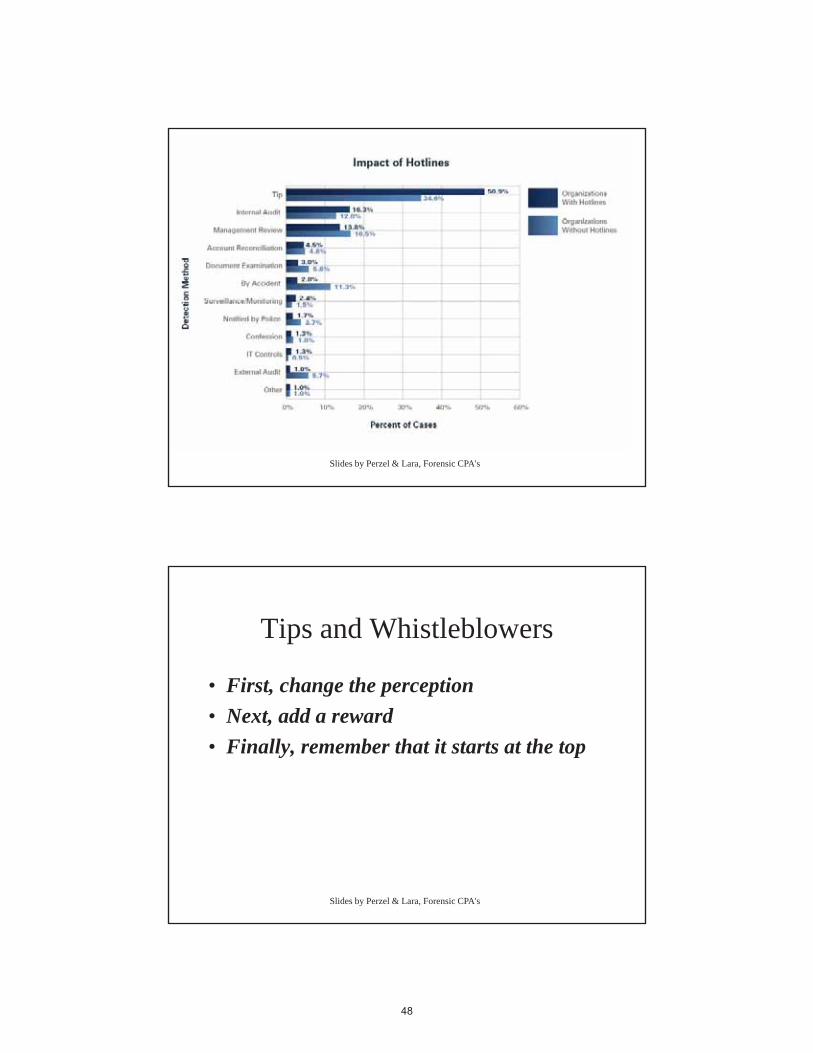

Tips and Whistleblowers

• First, change the perception• Next, add a reward• Finally, remember that it starts at the top

Slides by Perzel & Lara, Forensic CPA's

ACFE – Report to the Nation 2012 - Update

• Survey participants estimated that the typical organization loses 5% of its revenues to fraud each year.

• Applied to the 2011 Gross World Product, this figure translates to a potential projected annual fraud loss of more than $3.5 trillion.

Slides by Perzel & Lara, Forensic CPA's

ACFE – Report to the Nation 2012 - Update

• The frauds reported lasted a median of 18 months before being detected.

Slides by Perzel & Lara, Forensic CPA's

ACFE – Report to the Nation 2012 - Update

• The median loss caused by the occupational fraud cases in the study was $140,000.

• More than one-fifth of these cases caused losses of at least $1 million.

Slides by Perzel & Lara, Forensic CPA's

ACFE – Report to the Nation 2012 - Update

Asset misappropriation schemes were by far the most common type of occupational fraud, comprising 87% of the cases reported

they were also the least costly form of fraud, with a median loss of $120,000.

Slides by Perzel & Lara, Forensic CPA's

ACFE – Report to the Nation 2012 - Update

• Corruption and billing schemes pose the greatest risks to organizations throughout the world.

• For all geographic regions, these two scheme types comprised more than 50% of the frauds reported.

Slides by Perzel & Lara, Forensic CPA's

ACFE – Report to the Nation 2012 - Update

• In 81% of cases, the fraudster displayed one or more behavioral red flags that are often associated with fraudulent conduct.

Living beyond means (36% of cases), financial difficulties (27%), unusually close association with vendors or customers (19%) and excessive control issues (18%) were the most commonly observed behavioral warning signs.

Slides by Perzel & Lara, Forensic CPA's

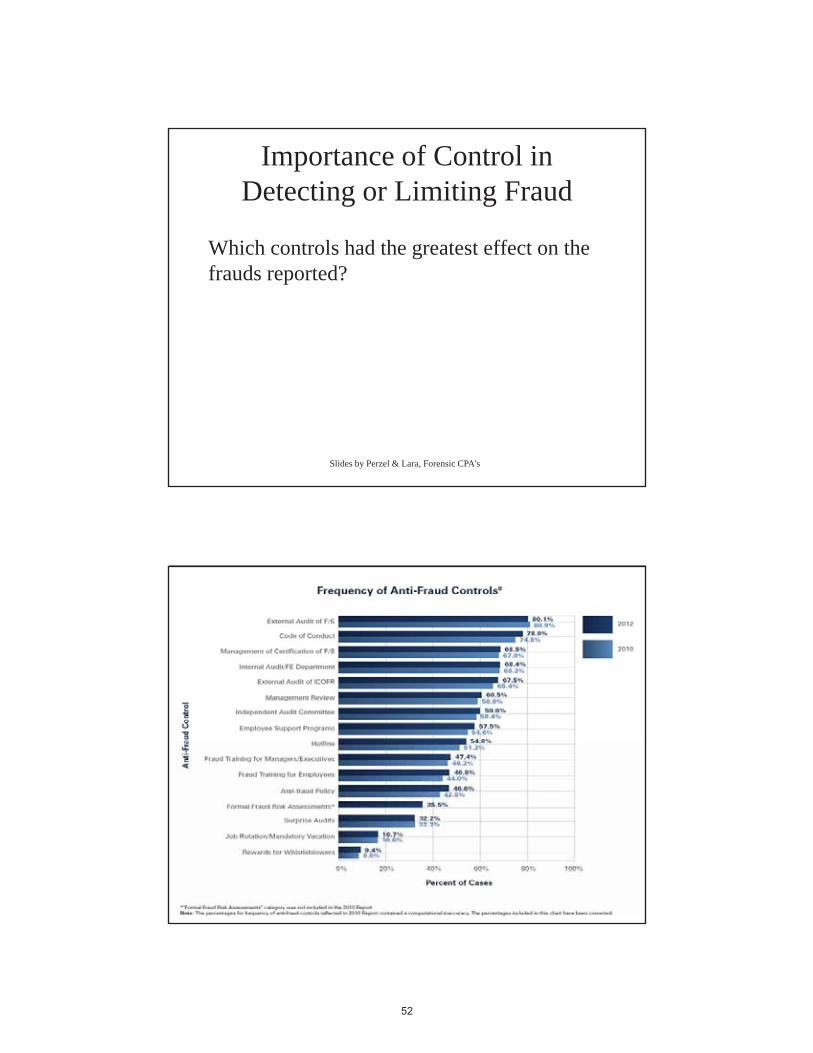

Importance of Control in Detecting or Limiting Fraud

Which controls had the greatest effect on the frauds reported?

Slides by Perzel & Lara, Forensic CPA's

Slides by Perzel & Lara, Forensic CPA's

Slides by Perzel & Lara, Forensic CPA's

Slides by Perzel & Lara, Forensic CPA's

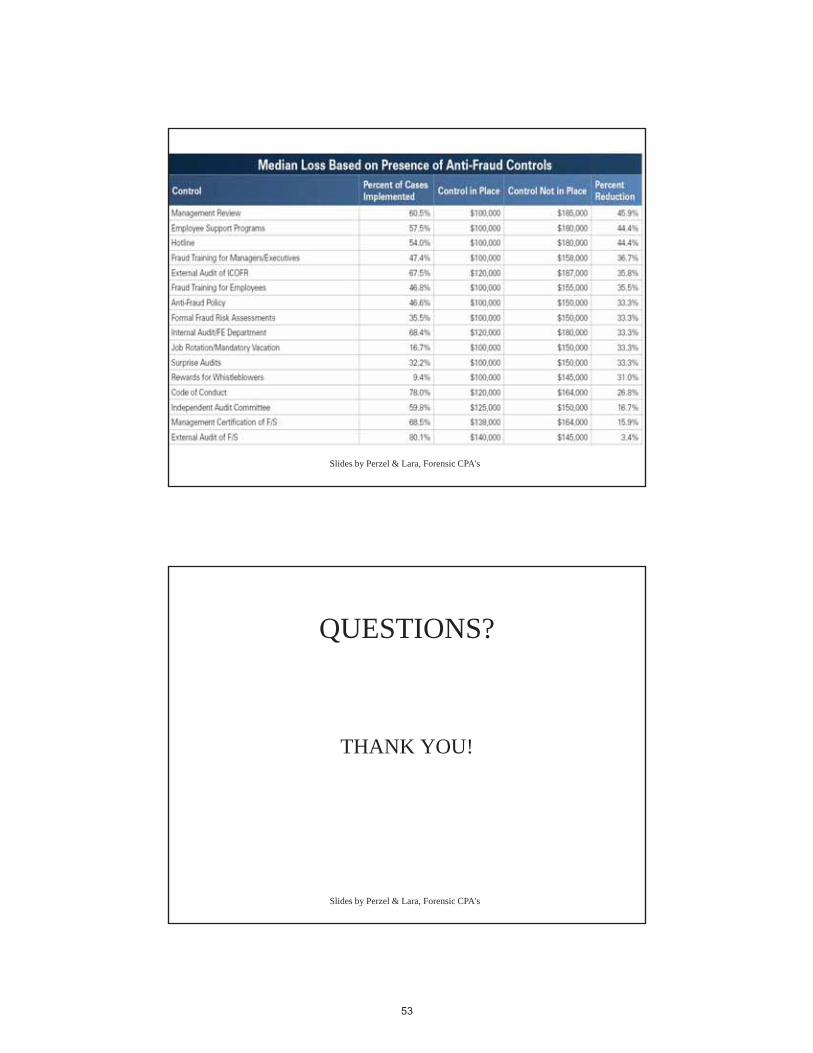

QUESTIONS?

THANK YOU!

Learn more about membership. | [email protected] | www.ficpa.org(800) 342-3197 (in Florida) | (850) 224-2727

“ I renew because of the invaluable networking opportunities that being a member of the F ICPA provides. From being involved with your local chapter to attending networking events, the F ICPA is an organization that is

known and respected across many industries.”

Monica Ospina, CPA, ABV, CFF Cherry, Bekaert & Holland, LLP

Coral Gables Member since 2007

“ I renew my F ICPA membership because of the signif icant access to education, current events, and the

networking it provides.”

Ray Monteleone, CPA President, Paladin Global Partners

Fort Lauderdale Member since 1979

“ Ibeced

“ I’m renewing my F ICPA membership because it keeps me professionally and socia lly connected to my fellow peers in the profession.”

David White, CPA Carr Riggs & Ingram LLC

Tallahassee Member since 2010

FICPA Membership: Connect, Learn and ThriveProud to be a Member

Keep Your Organization Moving Forward

For more information, please contact the FICPA at [email protected]

or call (800) 342-3197 (in Florida) or (850) 224-2727 extension 412.

The FICPA has partnered with the AICPA and other providers to address the changing needs of business professionals. This partnership now enables us to provide a wide range of courses, instructors, and educational solutions in a variety of formats, including on-site training, seminars, and webcasts.

Topic areas including: • Technical • Strategic and Business Management • Leadership Development • Communication skills • Ethics

Using FICPA on-site training benefits your staff by offering:• Team building opportunities while enhancing their skill set • Smaller class sizes and more interaction with the instructors • Professional development opportunities without the hassle of travel

Meanwhile, employers gain by:• Saving money by eliminating travel expenses • Saving time by scheduling training when it is convenient for you and your staff • Customized, flexible training designed to fit your company’s specific needs

Call or e-mail us today to find out how FICPA has the right training solutions for you!

Related Documents