Material Weakness in Internal Control and Stock Price Crash Risk: Evidence from SOX Section 404 Disclosure Jeong-Bon Kim Department of Accountancy City University of Hong Kong [email protected] Ira Yeung Kellogg School of Management Northwestern University [email protected] Jie Zhou NUS Business School National University of Singapore [email protected] Current Version May 2013 We have received useful comments from Jong-Hag Choi, Yuyan Guan, Jay Lee, Zhenbin Liu, Jacky So, Liandong Zhang, and participants of research workshops/seminars at City University of Hong Kong, Fudan University, University of Macao, and National University of Singapore. Kim acknowledges partial financial support for this project from the GRF grant of the Hong Kong SAR government (Project No. 144511). All errors are, of course, ours.

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Material Weakness in Internal Control and Stock Price Crash Risk:

Evidence from SOX Section 404 Disclosure

Jeong-Bon Kim

Department of Accountancy City University of Hong Kong

Ira Yeung

Kellogg School of Management Northwestern University

Jie Zhou

NUS Business School National University of Singapore

Current Version

May 2013

We have received useful comments from Jong-Hag Choi, Yuyan Guan, Jay Lee, Zhenbin Liu, Jacky So, Liandong Zhang, and participants of research workshops/seminars at City University of Hong Kong, Fudan University, University of Macao, and National University of Singapore. Kim acknowledges partial financial support for this project from the GRF grant of the Hong Kong SAR government (Project No. 144511). All errors are, of course, ours.

1

Material Weakness in Internal Control and Stock Price Crash Risk:

Evidence from SOX Section 404 Disclosure

Abstract: This study investigates the hitherto unexplored questions of whether and how the presence of undisclosed material weakness in internal control over financial reporting (ICW) and its initial disclosure differentially influence the occurrence of extreme negative outliers in firm-specific return distributions, which we refer to as stock price crash risk. We predict and find that firms with ICW problems are more crash-prone than firms with no such problem. We also predict and find that stock price crash risk is even greater for fraud-related ICWs. We provide strong evidence that the impact of ICW on increasing crash risk is observed at least two years prior to the initial disclosure of the adverse opinion on internal control quality, but gradually decreases over the two-year period subsequent to the initial disclosure and essentially disappears once publicly disclosed ICW problems are remediated. The above results hold even after controlling for various firm-specific determinants of crash risk and ICWs. Overall, our results suggest that the presence of undisclosed ICWs tends to exacerbate managers’ bad news hoarding until the ICW problems are disclosed to the public, which increases crash risk. On the other hand, public disclosure of ICWs constrains managerial incentive and ability to withhold bad news from outside investors, thereby mitigating crash risk.

Keywords: Internal weakness, crash risk, Sarbanes-Oxley Act (SOA)

JEL Classification Codes: G12, M41, K22

2

1. Introduction

The past two decades have witnessed a series of large-scale corporate debacles and

accounting and auditing failures around the world, including the cases of Enron, Tyco and

Worldcom. These scandals, which cost investors billions of dollars when the share prices of the

affected companies collapsed, dramatically shook public confidence in the capital markets in

general and the quality and reliability of accounting disclosure in particular. In an effort to

restore shredded investor confidence, the U.S. Congress passed the Sarbanes-Oxley Act (SOX)

in 2002. Section 404 of SOX (hereafter SOX 404) requires the management of a public company

to evaluate the effectiveness of the company’s internal control over financial reporting and report

its conclusion in the company’s annual reports. Also, SOX 404 requires a firm’s auditor to attest

to the management’s internal control evaluation and report the auditor’s own conclusion

regarding internal control effectiveness.1

Prior research shows that material weaknesses in internal control over financial

reporting—or simply internal control weaknesses (ICWs)—are associated with negative stock

returns and relatively high cost of (both equity and debt) capitals.

2

1 In this study, we focus on SOX 404 disclosures because compared to unaudited SOX 302 disclosures, auditor-attested SOX 404 disclosures are more reliable indicators of a firm’s financial reporting system quality.

This line of research has

typically analyzed the impact of ICWs on actual realized return or implied cost of capital (which

is conveniently referred to as the first moment effect of ICWs). The ICW disclosure

requirements under SOX 404 were in response to the abrupt, large-scale decline in stock price

and the associated loss of investor confidence in the quality and reliability of financial reporting.

Nevertheless, previous literature has paid little attention to the effect of ICW on negative tail risk

2 See, for example, Hammersley, Meyers and Shakespeare, 2008; Ogneva, Subramanyan, and Raghunandan, 2007; Kim, Song and Zhang, 2011; Costello and Wittenberg-Moerman, 2012; Ashbaugh-Skaife, Collins, Kinney and LaFond, 2009; Beneish, Billings and Hodder, 2008; and Dahliwal, Hogan, Trezevant and Wilkins, 2011.

3

or the likelihood of observing extreme negative outliers in firm-specific return distribution

(which is conveniently referred to the third moment effect of ICWs).3

To better understand the role of internal control quality in stock price formation process,

our study first investigates whether the presence of (not-yet-disclosed) ICW prior to the initial

ICW disclosure is positively associated with the likelihood of observing extreme negative returns

or stock price crash risk. In so doing, we attempt to isolate the presence effect (the effect

associated with the presence of undisclosed ICW problems prior to the initial public disclosure of

ICW) from the disclosure effect (the effect associated with the initial public disclosure of ICW

under SOX 404). Second, we predict that the public disclosure of ICW itself is likely to improve

firm-level transparency, and thus, mitigate a firm’s crash risk. To test this prediction, we further

examine whether the public disclosure of ICW under SOX 404 in fact decreases stock price

crash risk from the pre- to the post-ICW-disclosure period. Finally, we also examine whether and

how the remediation of publicly disclosed ICW problems impacts crash risk in the post-ICW-

disclosure period.

As a result, little is known

about whether and how ICW is associated with the occurrences of extreme negative returns or

stock price crashes.

We are motivated to examine the above research questions for the following reasons:

First, as noted in SEC (2003), internal control is a much broader concept that encompasses not

only the financial reporting process but also the overall information environment of a firm. Kim

et al. (2011) provide evidence that internal control quality captures the overall quality of a firm’s

3 This third moment effect enables researchers to better capture the accumulated effect of an information-related event such as the initial disclosure of ICWs (Kim and Zhang, 2012).

4

information production system.4

Second, SOX 404 requires managers of all public firms to assess the effectiveness of

internal controls over financial reporting and to provide periodic auditor-attested evaluations of

internal control effectiveness. In comparison with SOX 302 disclosures of ICW, Section 404

disclosures is thus viewed as a more comprehensive, objective, and unambiguous indicator for

the quality of a firm’s information production system.

Further, Hutton, Marcus and Tehranian (2009, hereafter HMT)

document a positive association between information opaqueness (captured by the three-year

moving sum of absolute abnormal accruals) and future crash risk. Given the above evidence, our

study examines whether the impact of internal control deficiencies on stock price crash risk goes

beyond and above the effect of HMT’s information opaqueness on crash risk. In other words, we

are interested in examining whether the lack of internal control quality, as reflected in ICW, is

incrementally important over and beyond the lack of earnings quality in determining crash risk.

5

Lastly and more importantly, our research setting allows us to: (i) differentiate the ICW

presence effect on crash risk from the ICW disclosure effect; and (ii) to evaluate whether and

how the initial disclosure of ICWs and its subsequent remediation affect stock price crash risk.

Given that prior research that examines the economic consequences of ICW disclosures fails to

differentiate the presence effect from the disclosure effect, our study allows us to make cleaner

Therefore, establishing the link between

internal control quality under SOX 404 and stock price crash risk can provide useful insights into

whether and how the reliability and quality of a firm’s overall information production system,

not a specific attribute per se, are incorporated into stock price formation process, particularly

negative tail risk or the third moment of firm-specific return distribution.

4 Kim et al. (2012) provide strong evidence that ICW is significantly associated with a higher cost of private debt, as reflected in unfavorable loan contracting terms (e.g., higher loan spread and more restrictive covenants) even after controlling for financial reporting quality. 5 See Feng, Li and McVay (2009) and Cheng, Dhaliwal and Zhang (2012).

5

interferences on whether the ICW disclosure requirement under SOX 404 indeed accomplishes

its intended policy objectives. In short, the results of our investigation have much potential to

provide new insights into the ongoing debate about the cost and benefit sides of SOX 404

disclosure and compliance.

Briefly, our results, using a large sample of firms with auditor-attested ICW disclosures

during the post-SOX period of 2004-2011, reveal the following. First, we find that, in the years

prior to the initial disclosure of ICW, firms with ICW problems are more prone to experience

stock price crashes relative to firms with no such problem. Our results are robust to different

measures of crash risk and alternative research designs and econometric methods. The above

findings support the view that effective internal controls mitigate stock price crash risk, and thus,

help to maintain stability in the stock market. Second, to provide additional insights into the

impact of internal control quality on crash risk, we examine whether stock price crash risk is

associated with the severity or seriousness of ICWs. We find that firms with more severe fraud-

related ICWs face higher crash risk than those with less severe ICWs. This finding suggests that

fraud-related material weaknesses point to more fundamental problems, such as maintaining an

ethical culture in the workplace (Kizirian, Mayhew and Sneathen, 2005). Finally, the results of

our over-time analyses show that the crash risk of ICW firms declines in the years subsequent to

the initial disclosure of ICWs, and disappears, in large part, after their publicly disclosed ICW

problems are remediated. The finding suggests that the ICW disclosure under SOX 404

contributes to constraining bad news hoarding by corporate insiders and mitigating crash risk,

and thus, facilitates stability in the equity market.

Our study adds to the extant literature in the following ways. First, to the best of our

knowledge, this is the first study to examine the third moment effect of ICW, that is, the effect of

6

ICWs on negative tail risk. Second, to our knowledge, our study is the first that explicitly

separate the consequences associated with the presence of undisclosed ICW problems from those

associated with the initial disclosure of ICW. Third, our study provides new evidence on the

benefit sides of SOX 404 compliance: the disclosure of ICW discourages corporate insiders to

engage in bad news hoarding, and thus, improves firm-level transparency, which in turn

mitigates future crash risk. This crash risk-reducing effect of ICW disclosure has not been

documented in prior research. Fourth, our research provides strong and reliable evidence that

internal control quality is an incrementally significant determinant of stock price crash risk above

and beyond earnings quality and other known determinants of crash risk. This finding is

particularly relevant given the evidence that investors are increasingly concerned about tail risk

or the probability of extreme outcomes (Pan, 2002; Yan, 2011). Finally, the results of our study

provide an important policy implication to accounting and security market regulators: internal

control deficiencies are a significant factor driving stock price crashes, and internal control

quality thus plays an important role in controlling future crash risk and/or maintaining stability in

the equity market.

The paper proceeds as follows. Section 2 provides a brief review of prior literature and

develops research hypotheses. Section 3 describes the sample, data, and variable measurement.

Section 4 discusses our empirical results. Section 5 presents the results of further analyses and

robustness checks. The final section concludes.

2. Literature Review and Hypotheses Development

Our study is related to two strands of prior research, that is: (1) one that examines the

relation between financial reporting quality and stock price crash risk; and (2) the other that

7

investigates the determinants and consequences of SOX 404 disclosure. In what follows, we

offer a brief review of prior research in each strand, and then develop our research hypotheses.

2.1 Prior research on firm-specific determinants of stock price crash risk

Stock price crash risk at the firm level refers to the likelihood of observing extreme

negative outliers in the distribution of firm-specific returns, that is, observed returns after netting

out a portion of returns that co-move with common factors (Jin and Myers, 2006; HMT; Kim et

al., 2011a; 2011b). Research on stock price crash risk has received considerable attention from

the investment community and security regulators, since a series of corporate debacles and high-

profile accounting scandals associated therewith occurred in the early 2000s. The recent financial

crisis that started in 2008 has further magnified interests in negative tail risk or stock price crash

risk from the investing public, regulators, and academic researchers.

Relying on a model where outsiders have limited information, Jin and Myers (2006)

examine whether information asymmetry between corporate insiders and outsiders could be

related to stock price crash risk.6

6 Other analytical studies include Bleck and Liu (2006), and Benmelech, Kandel and Veronesi (2010).

Specifically, their model predicts that opaque stocks are more

likely to deliver large negative returns. Since then, much effort has been dedicated to empirically

test this prediction. Notably, Hutton et al. (2009) use the three-year moving sum of absolute

abnormal accruals as a proxy for information opaqueness and document a positive association

between information opaqueness and stock price crash risk. Their study concludes that

transparency in financial reporting is crucially important for maintaining stability in the capital

markets.

8

Building on earlier theoretical and empirical works, more recent research has focused on

how other factors associated with financial reporting influence stock price crash risk. Similar in

spirit to HMT, Kim et al. (2011b) hypothesize that complex tax shelters and tax planning allow

managers to manage earnings via restructuring real transactions, which provides a useful means

for hiding negative information. Consistent with their hypothesis, they find that corporate tax

avoidance is positively associated with stock price crash risk. In another study, Kim et al.

(2011a) find that when a firm’s managers—particularly, the chief financial officers (CFOs)—are

given option-based compensation contracts, they tend to hide bad news within the firm to

maximize their incentive compensation, which in turn engenders relatively high crash risk.

DeFond et al. (2011) examine whether and how the mandatory IFRS adoption in 2005 by

European Union countries affects stock price crash risk. They provide evidence suggesting that

mandatory IFRS adoption decreases crash risk for industrial firms by increasing transparency or

decreasing information opaqueness, while it increases crash risk for financial firms by

magnifying stock return volatility for these firms. In another related study, Kim and Zhang

(2012) posit that conservatism curbs managerial incentives to delay the release of bad news, and

thus constrains managerial ability to withhold bad news. Consistent with this view, they find that

the degree of conditional conservatism is negatively associated with future crash risk.

While the aforementioned studies provide evidence that bad news hoarding is the key

factor that leads to stock price crash in the future, they are largely silent on the precise nature of

the process in which information problems increase crash risk. Recognizing the importance of

management guidance in shaping a firm’s information environment (Beyer, Cohen, Lys and

Walther, 2010), Hamm, Li and Ng (2012) extend prior research that focuses mainly on

mandatory reporting and examine how management earnings guidance, an important voluntary

9

disclosure channel, is related to future crash risk. They find that the positive association between

opacity in reported earnings and crash risk, as documented in HMT, is stronger when opacity

interacts with more frequent earnings guidance. The finding suggests that managers rely on both

mandatory financial reporting and voluntary disclosure to manage or guide earnings expectations

by outside investors. To our knowledge, however, no prior research has investigated the impact

of internal control weakness on stock price crash risk.

2.2. Prior research on economic determinants and consequences of SOX 404 disclosure

Earlier studies on SOX 404 disclosures are of descriptive nature. For example, Doyle, Ge

and McVay (2007b), among others, find that firms with weak internal controls tend to be

smaller, younger, less profitable, more complex, or undergoing restructuring changes.7

To our knowledge, however, no prior research has investigated the impact of internal

control deficiencies on the likelihood of observing extreme negative outliers in stock return

distribution. Our study therefore focuses on the third moment effect of ICW, that is, the

More

recent studies examine the economic consequences of SOX 404 disclosure, particularly, the

impact of ICW on cost of equity (e.g., Ogneva et al., 2007; Ashbaugh-Skaife et al., 2009), cost of

public debt (Dhaliwal et al., 2011), and cost of private debt (Kim et al., 2011). Overall, this line

of research focuses its attention on the first moment effect of ICW, namely the effect of initial

public disclosures of ICWs under SOX 404 on ex post realized stock returns and/or ex ante

implied costs of capital. The main findings from this line of research are that initial ICW

disclosure has a negative impact on the market, as manifested in negative stock returns and/or

higher cost of capital.

7 See also Ashbaugh-Skaife, Collins and Kinney, 2007; Ge and McVay, 2005.

10

likelihood of observing extreme negative outliers in firm-specific return distribution. Prior

research on the economic consequences of ICW disclosures under SOX 404 fails to isolate the

ICW presence effect (the consequence associated with the presence of undisclosed ICWs) from

the ICW disclosure effect (the consequences associated with initial ICW disclosures under SOX

404). As will be further explained below, however, it is important to separate the ICW presence

effect from the ICW disclosure effect, when examining the impact of ICWs on stock price crash

risk.

2.3 Hypotheses development

2.3.1. The effect of the presence of undisclosed ICW on crash risk

Effectiveness of internal control over financial reporting is an important factor that

determines the quality and reliability of a firm’s information production system. The quality of

internal controls can affect not only the quality of public information disclosed via external

financial reports but also the quality of (undisclosed) private information idiosyncratic to

corporate insiders. For example, Doyle et al. (2007a) find that ICWs are generally associated

with poorly estimated accruals that are not realized as cash flows. Feng et al. (2009) find that

management forecasts are less accurate among firms with ICW problems. Their results suggest

that internal control quality not only influences earnings reports, but also has an economically

significant effect on voluntary disclosure that relies on internal management reports (e.g.,

management earnings guidance).

11

The presence of (undisclosed) ICW entails procedural and estimation errors as well as

opportunistic earnings management,8 thereby deteriorating corporate transparency. Prior research

provides evidence that lack of transparency in financial reports enables managers to

opportunistically withhold bad news or unfavorable information (Jin and Myers, 2006; HMT;

Kim et al., 2011a; Kim and Zhang, 2012), thereby increasing future crash risk.9

Given the scarcity of evidence on the issue, it is interesting and important to test whether

the quality and reliability of a firm’s information production system, as reflected in ICW, go

above and beyond HMT’s information opaqueness measure in predicting future crash risk. To

provide systematic evidence on this unexplored issue, we test the following hypothesis in

alternative form:

However, there

is a limit to the amount of unfavorable information that managers can absorb or successfully hide

from outside investors. This is because, once the total amount of hidden negative information

reaches a certain threshold, it becomes too costly or impossible to continue to withhold it. When

the total amount of the hidden negative information that has accumulated over time reaches a

tipping point, it will come out abruptly, leading to a large negative, extreme return on the

individual stocks concerned, i.e., a stock price crash (Jin and Myers, 2006; HMT; Kim and

Zhang, 2012). One can therefore expect that ceteris paribus, firms with (undisclosed) ICW

problems are more prone to experience stock price crashes than firms with no such problem.

8 A material ICW is defined as “[a] deficiency, or a combination of deficiencies, in internal controls over financial reporting such that there is a reasonable possibility that a material misstatement of the registrant’s annual or interim financial statements will not be prevented or detected on a timely basis by the company’s internal controls” (www.sec.gov). 9 Prior research shows that firms with ICWs tend to disseminate less transparent or more opaque financial reports than those with no ICWs. (Doyle, Ge and McVay, 2007a; Ashbaugh-Skaife, Collins and Kinney, 2007; Feng, Li and McVay, 2009).

12

H1: All else being equal, the presence of material weaknesses in internal control over financial reporting, or simply material internal control weaknesses (ICWs), prior to its initial disclosure is positively associated with the likelihood of stock price crashes.

2.3.2. Does the severity of undisclosed ICW problems matter?

Admittedly, however, there are also other reasons why our prediction may not hold

empirically. First, prior research suggests that ICWs are attributed primarily to a firm’s

complexity and insufficient resources (Doyle, Ge and McVay, 2007b). The disclosure of ICWs

simply implies that the firm’s internal controls are not sufficient to prevent or detect potential

accounting misstatement. Therefore, ICWs do not necessarily suggest the existence of

accounting misstatement. One way to further substantiate our prediction in H1 is to see if stock

price crash risk differs when firms are faced with different types of ICWs and with different

levels of severity. For this purpose, we aim to provide systematic evidence on whether the

association between ICW and crash risk is stronger for firms with more severe ICW problems.

Specifically, we interpret ICWs related to unethical issues or potential restatements

(fraud-related ICWs) as a signal for an environment in which the probability of managerial rent

extraction is at its highest. Prior research suggests that restatements are often linked to aggressive

accounting and management culpability (Efendi, Srivastava and Swanson, 2007; DeFond and

Jiambalvo, 1994). 10

10 For example, Efendi et al. (2007), among others, find that managers’ compensation incentives are associated with restatements. In a similar vein, DeFond et al. (1994) suggest that capital market pressure is one motivating factor leading to restatements.

Skaife, Veenman and Wangerin (2012) also find that managers whom

external auditors identified as lacking integrity tend to engage in more profitable insider trading.

We expect that fraud-related ICW problems are more fundamental and severe in nature, and thus,

are more closely associated with managerial opportunism in financial reporting, such as bad

news hoarding. We therefore predict that the association between ICW and crash risk is stronger

13

for fraud-related ICWs than for other types of ICWs. To provide empirical evidence on the above

prediction, we test the following hypothesis in alternative form:

H2: All else being equal, stock price crash risk prior to the initial disclosure of ICW is positively associated with fraud-related ICWs, to a greater extent, than it is with other non-fraud-related ICWs.

2.3.3. The effect of initial public disclosure of ICW on crash risk

In comparison with previous ICW-related research, our study uses the relatively long

(post-SOX) sample period of 2004-2011. This, along with our unique research setting, provides

us with an opportunity to evaluate the changes in crash risk around the first-time disclosure of

ICWs as required by SOX 404. Ex ante, it is not clear how the disclosure of ICWs will impact

crash risk. On the one hand, one can expect the disclosure of ICWs to have a negative impact on

the market. To the extent that the presence of ICW problems allows corporate insiders to

withhold bad news within the company and accumulate the hidden unfavorable information over

time, initial public disclosures of ICWs may enable outside investors to evaluate the

consequences of hidden unfavorable information, namely the likelihood of stock price crashes. In

such a case, the initial ICW disclosure is likely to exacerbate crash risk underlying a firm’s stock.

On the other hand, the disclosures of ICWs are expected to cause a dramatic change in a

firm’s information environment. First, while the presence of undisclosed ICW increases

information opacity and thus increases future crash risk, public disclosure of ICW per se can

improve corporate transparency almost immediately, and thus mitigate future crash risk: Upon

the initial public disclosures, investors become aware of ICW problems inherent in these firms,

and are more likely to exercise a heightened degree of scrutiny over these firms. Second, upon

the ICW disclosures, boards of directors may impose additional monitoring mechanisms in an

effort to discipline managers. Third, facing the adverse consequences from the public disclosures

14

of ICWs,11

Given the two opposing predictions above, the directional effect of initial ICW disclosure

on stock rice crash risk is basically an empirical question. To provide systematic evidence on this

unexplored question, we test the following hypothesis in alternative form:

managers are likely to have strong incentives to exert greater effort to remediate

publicly disclosed ICW problems: For example, managers are likely to become more

forthcoming with respect to bad news disclosure. In such cases, the disclosures of ICWs mitigate

stock price crash risk.

H3: The initial public disclosure of ICWs and the subsequent remediation of publicly disclosed ICWs lead to a decrease in stock price crash risk, all else being equal.

3. Sample selection and variable measurement

3.1 Data and sample selection

As reported in Panel A of Table 1, the initial sample for this study includes all firm-year

observations that are jointly included in the three databases, Compustat, Center for Research in

Security Prices (CRSP), and Audit Analytics. This initial sample consists of 34,565 firm-years

for our post-SOX sample period of 2004-2011. The sample period begins in 2004 as accelerated

filers were required to comply with SOX 404 starting from the fiscal year ending on November

15, 2004. We merge CRSP weekly stock return data with Compustat financial statement data and

Audit Analytics SOX 404 audit report data. In so doing, we eliminate 338 firm-years with fewer

than 26 weeks of stock-return data. We also drop 2,940 low-priced stocks with their average

price for the year less than $2.50. Finally, we eliminate 11,890 firm-years with insufficient

11 These adverse consequences may include lower compensation and higher forced turnover (Johnstone, Li and Rupley, 2010; Wang, 2010).

15

financial data to calculate control variables. The final sample consists of 19,397 firm-year

observations for the sample period of 2004-2011.

Out of 19,397 firm-years in our final sample, 1,397 (7.2%) report ICW problems. In our

regression analyses, we create an indicator variable, denoted by MW, that equals one if the firm

reports ICW problems in a sample year and zero otherwise. Panel B of Table 1 reports the

number of sample firms in each sample year and the percentage of firms with ICW problems in

each sample year. As shown in Panel B, we clearly observe a declining pattern in the percentage

of firms with ICW disclosures over our sample period. The percentage of ICW disclosures

gradually declines from a high of 17.2% in 2004 to 3.0% in 2011. This declining pattern is

consistent with the finding of some recent related studies (e.g., Cheffers, Whalen and Thrun,

2010; Kinney and Shepardson, 2011).

3.2 Measuring firm-level crash risk

Following prior literature, we employ three measures of crash risk.12

where 𝑟𝑗,𝑡 is the return on stock 𝑗 in week 𝑡, and 𝑟𝑚,𝑡 is the return on the CRSP value-weighted

market index in week 𝑡. We include the lead and lag terms for the market index to allow for

nonsynchronous trading (Scholes and Williams, 1972). The residual from Eq. (1), i.e., εjt,

captures firm-specific weekly return. Since these residuals are highly skewed, we transform them

In so doing, we first

estimate the following augmented market model to calculate firm-specific weekly returns for

each firm in each year:

𝑟𝑗,𝑡 = 𝛼𝑗 + 𝛽1𝑗𝑟𝑚,𝑡−2 + 𝛽2𝑗𝑟𝑚,𝑡−1 + 𝛽3𝑗𝑟𝑚,𝑡 + 𝛽4𝑗𝑟𝑚,𝑡+1 + 𝛽5𝑗𝑟𝑚,𝑡+2 + 𝜀𝑗𝑡 (1)

12 For space limitation, we report results using two measures of crash risk, CRASH and NCSKEW. We conduct robustness analysis using the third measure, DUVOL, but do not tabulate the results.

16

by obtaining a log-transformed form of firm-specific weekly return, Wjt, that is the natural log of

one plus the residual return from Eq. (1); Wjt = ln (1+εjt).

The first measure of crash risk for each firm in each year, denoted by CRASH, is an

indicator variable that equals one for a firm-year that experiences one or more firm-specific

weekly returns (i.e., Wjt) falling 3.2 standard deviations below the mean firm-specific weekly

returns for that fiscal year. This measure captures the likelihood of observing extreme negative

outliers in firm-specific weekly return distribution.

The second measure of crash risk is the negative conditional return skewness, denoted by

NCSKEW. We calculate NCSKEW by taking the negative of the third moment of daily returns,

and dividing it by the standard deviation of daily returns raised to the third power. Therefore, for

any stock 𝑗 in year 𝑡, we obtain:

𝑁𝐶𝑆𝐾𝐸𝑊𝑗𝑡 = −[𝑛(𝑛 − 1)3/2�𝑊𝑗𝜏3]/[(𝑛 − 1)(𝑛 − 2)(�𝑊𝑗𝜏

2)3/2

]

where 𝑛 is the number of weakly return observations in the period.

Our third measure of crash risk is the down-to-up volatility ratio measure that was first

used by Chen, Hong and Stein (2001). For any stock 𝑗 over year 𝑡, we separate all the weeks

with returns below the period mean (“down” weeks) from those with returns above the period

mean (“up” weeks), and compute the standard deviation for each of these sub-samples

separately. Then, for any stock 𝑗 over year 𝑡, we calculate DUVOL as follows:

𝐷𝑈𝑉𝑂𝐿𝑗𝑡 = log [(𝑛𝑢 − 1)Σ𝑑𝑜𝑤𝑛𝑊𝑗𝜏2/(𝑛𝑑 − 1)Σ𝑢𝑝𝑊𝑗𝜏

2]

where 𝑛𝑢and 𝑛𝑑 are the number of up and down weeks in the period, respectively.

17

Panel C of Table 1 reports the incidence of stock price crashes, measured by CRASH, for

each sample year. As shown in Panel C, on average, 19.8% of firms in our sample experience at

least one crash event during a given year. Not surprisingly, crash incidence is the highest in 2008

(the year of U.S. stock market crash) at 22.8%. It is also interesting to observe that the likelihood

of observing firm-level stock price crashes is greater during the pre-crisis period of 2004-2007

than during the post-crisis period of 2009-2011.

4. Empirical results

4.1 Descriptive statistics

Table 2 presents descriptive statistics on the main variables used in this study, as well as

additional variables that are used as controls in our multivariate analysis. Detailed definitions of

all variables are provided in Appendix A. The mean value of 𝐶𝑅𝐴𝑆𝐻 is 0.198 for the full sample,

suggesting that, on average, 19.8% of firm-years experience one or more extreme, negative

return outliers that fall at least 3.2 standard deviations below the annual mean of the log-

transformed firm-specific weekly returns, i.e., Wjt. Here, the mean 𝐶𝑅𝐴𝑆𝐻 is higher than that

reported by Kim et al. (2011b) and Kim and Zhang (2012).13

13 For example, Kim et al. (2011b) reports an average crash probability of 0.161 based on the sample period from 1995-2008.

It should be noted, however, that

our sample period is more recent and covers the financial crisis of 2008. We find that mean crash

likelihood is significantly higher for the ICW sample (26.0%) than for the non-ICW sample

(19.3%), which is consistent with the prediction in H1. The mean value of 𝑁𝐶𝑆𝐾𝐸𝑊 is also

much larger than that reported by Kim et al. (2011b) and Kim and Zhang (2012), suggesting that

firms in our study are, on average, more crash-prone than those in these two studies. We also

find that both mean and median of 𝑁𝐶𝑆𝐾𝐸𝑊 are significantly greater for the ICW sample (0.178)

18

than for the non-ICW sample (0.059), which is again consistent with the prediction in H1. As is

the case for CRASH and NCSKEW, we also find that, on average, the down-to-up volatility ratio

(DUVOL) is significantly higher for the ICW sample (0.115) than for the non-ICW sample

(0.031), which is, anew, in line with prediction in H1.

We find that the mean value of 𝑀𝑊 is 7.2%, which is lower than those reported by Feng

et al. (2009) and Kim, Song and Zhang (2011). This finding is not surprising, because our sample

period covers more recent years up to 2011, and the percentage of firms with ICWs under SOX

404 disclosure has been steadily declining over the recent years.14

With respect to our control variables, the following are apparent. We find that firms with

ICW problems are smaller, less levered, less profitable, more opaque in financial reporting, less

dependent on foreign sales, more likely to incur a loss, have restructuring activities, appoint non-

Big 4 auditors, and experience auditor changes, compared with firms without ICW problems.

These differences in firm characteristic between ICW and non-ICW firms are, in general,

consistent with those reported in prior research on cross-sectional determinants of ICWs (e.g.,

Doyle et al., 2007a).

Table 3 presents the correlation matrix for the main variables used in our regression

analysis. Our three measures of crash risk, 𝐶𝑅𝐴𝑆𝐻, 𝑁𝐶𝑆𝐾𝐸𝑊, and 𝐷𝑈𝑉𝑂𝐿, are all significantly

positively correlated with each other, suggesting that they capture the same underlying construct.

We find that the correlation between the ICW indicator, i.e., 𝑀𝑊, and the three measures for

crash risk are all positive and significant at less than the 1% level. Though only suggestive of the

underlying relation, this finding is consistent with the prediction in H1 that the presence of ICW

14 See Table 1 Panel C for the incidence of ICW by each year.

19

is positively associated with stock price crash risk. It should be noted, however, that it is

premature to draw any conclusion from the univariate analysis, because other confounding

factors can potentially drive the positive ICW-crash risk association. In the next section we

therefore perform multivariate regression analyses to test our hypotheses.

4.2 Are ICWs positively associated with stock price crash risk?

4.2.1 Test of H1

Hypothesis H1 is concerned with whether stock price crash risk is higher for firms with

undisclosed ICW problems (i.e., ICW firms) than for firms with no such problem (i.e., non-ICW

firms). To test H1, we estimate the following regression of crash risk on the presence of ICW

and control variables (firm subscripts are subsumed for brevity):

𝐶𝑟𝑎𝑠ℎ𝑅𝑖𝑠𝑘𝑡 = 𝛼 + 𝛽1𝑀𝑊𝑡 + 𝐶𝑟𝑎𝑠ℎ 𝑅𝑖𝑠𝑘 𝐷𝑒𝑡𝑒𝑟𝑚𝑖𝑛𝑎𝑛𝑡𝑠𝑡−1

+ 𝐼𝐶𝑊 𝐷𝑒𝑡𝑒𝑟𝑚𝑖𝑛𝑎𝑛𝑡𝑠𝑡−1 + 𝜀 𝑡−1 (2)

In the above equation, CrashRisk refers to one of our two proxies for stock price crash risk,

CRASH and NCSKEW.15

15 As mentioned earlier, we also use DUVOL as an additional proxy for crash risk. Untabulated results are explained in section 5.3.

𝐶𝑅𝐴𝑆𝐻 is an indicator variable representing the ex-ante likelihood of

crash occurrence, and is ex post coded one if a firm experiences one or more crash events in each

sample year, and zero otherwise; NCSKEW represents the negative conditional skewness of

weekly firm-specific return distribution, as defined earlier and used by prior research (Chen et al.

2001; Kim et al. 2011a, 2011b; Kim and Zhang 2012); and 𝑀𝑊 is an indicator variable that

equals one if the firm reports ICW for the first time under the SOX 404 requirement, and zero

otherwise.

20

To isolate the presence effect (the effect of the presence of ICW on crash risk) from the

disclosure effect (the effect of the initial public disclosure of ICW on crash risk), we take the

following approach. As illustrated in Figure 1, suppose that a firm initially discloses its ICW

problem in year t+1, i.e. interval (t, t+1) in Figure 1. For each year t, i.e., interval (t-1, t), we

construct a treatment sample of ICW firms (MW = 1) and a control sample of non-ICW firms

(MW = 0). Implicit here is the assumption that a firm that discloses its ICW problem in year t+1

should have had the same problem in year t, though the problem is not yet disclosed to the public

(Doyle et al. 2007a; Schrand and Zachman 2012). The above approach allows us to effectively

exclude the disclosure year (year t+1) from our sample period so that the observed difference in

crash risk between the two samples captures the presence effect that is not confounded by the

initial disclosure effect. Note here that, for the purpose of testing H1, both the presence of ICW

itself and crash risk are measured in the same year t in which ICW problems have existed but

have not been disclosed yet. Note also that, as illustrated in Figure 1, our control variables are

measured in year t-1. Hypothesis H1 translates into a significantly positive coefficient on MW,

i.e., 𝛽1 > 0, which suggests that crash risk is significantly higher for ICW firms than for non-

ICW firms.

We control for seven firm-specific crash risk characteristics that are known to determine

firm-level crash risk. Chen et al. (2001) predict that stock price crashes are more likely to occur

when there are large differences of opinion among investors. Following their study, we control

for the detrended average monthly trading turnover, denoted by DTURN, which proxies for

differences of opinion among investors or investor heterogeneity. In addition, Chen et al. (2001)

also document several other variables that predict crash risk. Specifically, they find that firms

with high return skewness in the prior year, measured as lagged 𝑁𝐶𝑆𝐾𝐸𝑊, are likely to have

21

high return skewness in current year as well. Meanwhile, they also document a positive

association between prior stock return volatility, denoted by lagged 𝑆𝐼𝐺𝑀𝐴, and crash risk, and

that stocks with high past returns are more crash-prone in current year. Therefore, we control for

return (𝑅𝐸𝑇) in prior period. Finally, both Chen et al. (2001) and HMT find that crash risk is

associated with firm size (𝑆𝐼𝑍𝐸), market to book ratio (𝑀𝑇𝐵), return on asset (𝑅𝑂𝐴), and

leverage (𝐿𝐸𝑉). We therefore include these variables as controls in our regression model.

HMT (2009) use a three-year moving sum of absolute abnormal accruals, denoted by

𝑂𝑃𝐴𝑄𝑈𝐸 , to proxy for information opaqueness. They find that 𝑂𝑃𝐴𝑄𝑈𝐸 and crash risk are

positively related. We argue that our measure of internal control quality is a more comprehensive

measure of the quality of a firm’s information production system. We therefore include

𝑂𝑃𝐴𝑄𝑈𝐸 in our regression model for two purposes. First, we would like to validate the effects

of information opaqueness on crash risk as documented in HMT (2009) and Jin and Myers (2006)

using our sample with more recent observations. 16

Previous research has identified firm-specific characteristics that determine the presence

of ICW. For example, both Ge et al. (2005) and Doyle et al. (2007a) show that ICW firms are

smaller, younger, financially weaker and more complex. To alleviate possible problems of

omitted correlated variables and potential endogeneity concerns associated therewith, we include

in regression (2) a set of control variables that are associated with ICWs. We control for a firm’s

financial performance by including a variable capturing recent losses, 𝐿𝑂𝑆𝑆, which is defined as

Second, we want to ensure that our test

variable, 𝑀𝑊, captures some aspects of financial reporting quality that are incremental over and

beyond HMT’s information opaqueness.

16 In particular, HMT suggest that the effect of information opaqueness, measured as a three-year moving sum of absolute discretionary accruals, on crash risk has diminished after the passage of SOX.

22

the percentage of the most recent three years in which the firm reports a loss. We include a

foreign sales indicator (𝐹𝑆𝐴𝐿𝐸) and the natural log of one plus the number of business segment

(𝑆𝐸𝐺𝑀𝐸𝑁𝑇𝑆) to control for business complexity. We also include three additional indicator

variables representing restructuring activities (𝑅𝐸𝑆𝑇𝑅𝑈𝐶𝑇𝑈𝑅𝐸), Big 4 auditors (𝐵𝐼𝐺4), and

auditor changes during each sample year (𝐴𝑈𝐷𝐶𝐻𝐴𝑁𝐺) to isolate the effect of these variables

from the effect of MW on crash risk. To address potential cross-sectional and serial dependence

in the data, we report z-statistics (two tailed) that are based on robust standard errors corrected

for double (firm and year) clustering (Peterson, 2009; Gow Ormazabal and Taylor, 2010).

Throughout the paper, all regressions include year and industry indicators to control for year and

industry fixed effects, respectively.

Panel A Table 4 reports the results of logistic regressions using CRASH as the dependent

variable. The baseline model presents the estimated results for Eq. (2) after excluding a set of

ICW determinants. The regression results for the baseline model show that the coefficient on our

key variable of interest, 𝑀𝑊, is highly significant with an expected positive sign and z-statistic

of 4.84 (𝑝 < 0.01). To assess the economic significance of our test results, we compute the

marginal effect of 𝑀𝑊 that captures the change in 𝐶𝑅𝐴𝑆𝐻 associated with a change of 𝑀𝑊

from 0 to 1, holding all other independent variables at their mean values. The marginal effect of

𝑀𝑊 is about 0.05, suggesting that crash risk is higher for ICW firms by about five percentage

points, compared with firms with no ICW problem. This is economically significant, given that

the average unconditional probability of crash occurrence is 19.8% in our sample.

Throughout our study, seven crash risk determinants, which are used as our control

variables, are all measured with a one year lag (i.e., measured in the year prior to the year when

CRASH is measured) so that current-year return distribution fully reflects the impact of these

23

control variables, if any. With respect to the estimated coefficients on our seven control variables,

the following are noteworthy. We find that the coefficients on known determinants of crash risk

are in line with the findings of prior research: Crash risk is positively and significantly associated

with lagged detrended trading volume (𝐷𝑇𝑈𝑅𝑁), lagged stock return (𝑅𝐸𝑇), lagged firm size

(𝑆𝐼𝑍𝐸), and lagged market-to-book ratio (𝑀𝑇𝐵). The coefficient on lagged opaqueness

( 𝑂𝑃𝐴𝑄𝑈𝐸) is positive but insignificant. This result, along with a significantly positive

coefficient on MW, indicates that the effect of ICW on increasing crash risk is incremental above

and beyond prior-period accounting opaqueness.17

One may argue that our test variable, MW, may suffer from potential endogeneity bias,

because MW is, to a large extent, subject to managers’ self selection. In an effort to alleviate

potential endogeneity concerns associated with this self-selection bias, we also estimate Eq. (2)

after including well-known determinants of ICW as additional controls. As shown in the second

section of Panel A, we find that the coefficient on MW remains highly significant with an

expected positive sign. This suggests that ICW is incrementally significant in explaining crash

risk even after controlling simultaneously for all known determinants of both crash risk and ICW.

We also find the sign and significance of estimated coefficients on seven crash risk determinants

are, overall, similar to those obtained for the base model.

The coefficient on lagged return on assets

(𝑅𝑂𝐴) is both significant with a predicted negative sign.

18

17 We find that the coefficient of 𝑂𝑃𝐴𝑄𝑈𝐸is insignificant when we exclude our main test variable, 𝑀𝑊 . One possible reason is that after SOX, the relation between 𝑂𝑃𝐴𝑄𝑈𝐸and crash risk has significantly diminished, as documented by Hutton et al. (2009).

Interestingly, we find that crash risk

is higher for firms with foreign sales (FSALE) and restructuring charges (RESTRUCTURE),

while it is lower for firms with more frequent losses (LOSS) and more business segments

(SEGMENTS).

18 One notable difference is that the coefficient on 𝑂𝑃𝐴𝑄𝑈𝐸 becomes significant in the augmented model.

24

Panel B of Table 4 reports the results of ordinary least squares (OLS) regressions for Eq.

(2), using 𝑁𝐶𝑆𝐾𝐸𝑊 as the dependent variable. As shown in Panel B of Table 4, the coefficient

of 𝑀𝑊 is significantly positive in both the base model and the augmented model, which strongly

supports the prediction in H1. This result is economically significant as well: Taking the baseline

model as an example, the coefficient of 𝑀𝑊 is 0.126, suggesting that ineffective internal control

is associated with an approximate 85% increase (0.126/0.068-1) in 𝑁𝐶𝑆𝐾𝐸𝑊.

Overall, the results reported in both Panels A and B of Table 4 are similar to each other

and generally consistent with the prediction in H1 that the presence of (undisclosed) ICW prior

to its initial disclosure increases stock price crash risk. This finding is robust to different

measures of crash risk, and holds even after controlling for Chen et al.’s (2001) investor

heterogeneity, HMT’s information opaqueness, and other firm-specific determinants of crash risk.

Our results hold, irrespective of whether or not we control for firm-specific characteristics that

are known to determine ICW. In short, our findings are consistent with the view that effective

internal control plays a significant role in limiting managerial incentive, ability, and opportunity

to withhold or delay the disclosure of bad news, which in turn significantly lowers the likelihood

of bad news being stockpiled within a firm, and thus, stock price crash risk.

4.2.2 Test of H2

Hypothesis H2 is concerned with the impact of the severity or seriousness of ICW on

crash risk. To test whether (more serious) fraud-related ICWs have a stronger association with

crash risk than (less serious) other ICWs, we estimate the following regression in which ICWs

are decomposed into fraud-related and other (non-fraud related) ones:

𝐶𝑟𝑎𝑠ℎ𝑅𝑖𝑠𝑘𝑡 = 𝛼 + 𝛽1𝑀𝑊_𝑓𝑟𝑎𝑢𝑑𝑡 + 𝛽2𝑀𝑊_𝑜𝑡ℎ𝑒𝑟𝑡 + 𝐶𝑟𝑎𝑠ℎ 𝑅𝑖𝑠𝑘 𝐷𝑒𝑡𝑒𝑟𝑚𝑖𝑛𝑎𝑛𝑡𝑠𝑡−1

25

+ 𝐼𝐶𝑊 𝐷𝑒𝑡𝑒𝑟𝑚𝑖𝑛𝑎𝑛𝑡𝑠𝑡−1 + ɛ𝑡−1 (3)

In Eq. (3) above, as discussed earlier, CrashRisk refers to either CRASH or NCSKEW.

𝑀𝑊_𝐹𝑟𝑎𝑢𝑑 is an indicator variable that differentiates fraud-related ICWs from other ICWs.

Fraud-related internal control problems are based on the reason key fields in Audit Analytics that

describe the nature of the material weaknesses contributing to ineffective internal control.

Specifically, 𝑀𝑊_𝐹𝑟𝑎𝑢𝑑 is coded one if Audit Analytics classifies a material weakness as

related to “restatement or non-reliance of company filings” (reason key #5) or “ethical or

compliance issues with personnel” (reason key #21), and zero otherwise. Similarly, 𝑀𝑊_𝑂𝑡ℎ𝑒𝑟

is coded one if a firm has non-fraud related ICWs and zero otherwise. Based on this

classification, we identify 573 firm-year observations as having fraud-related weaknesses

(2.95%).19

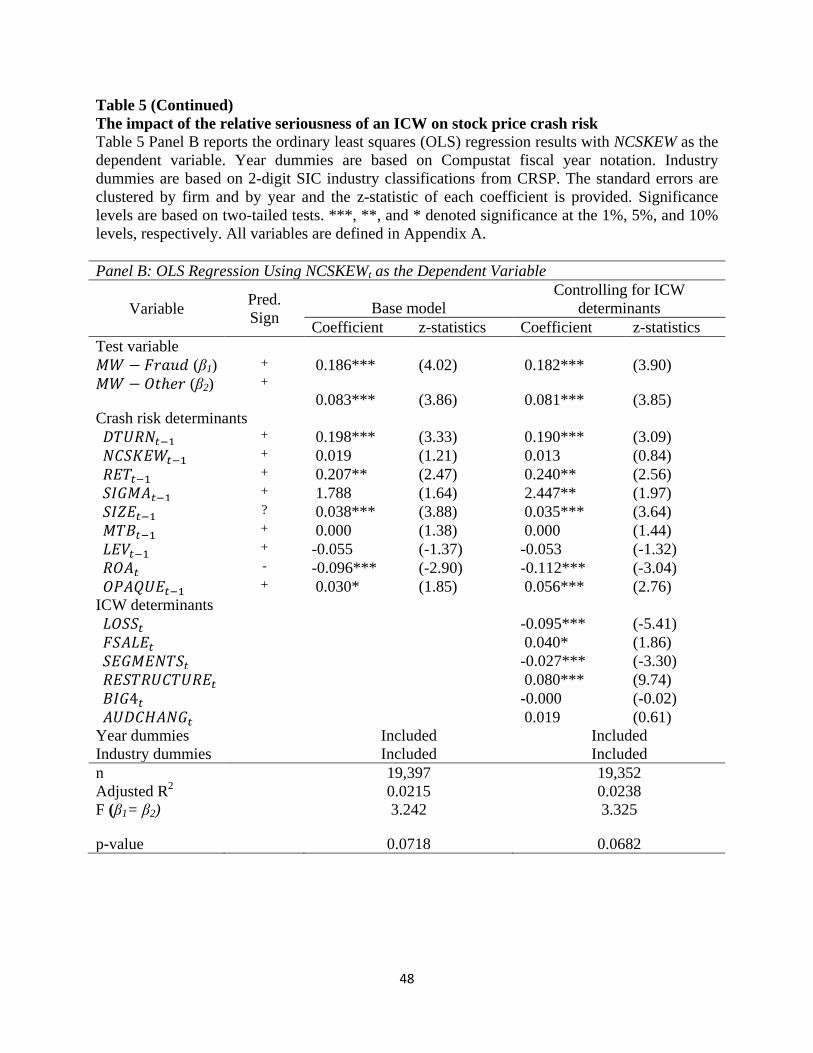

Panels A and B of Table 5 present the regression results for Eq. (3), using CRASH and

NCSKEW, respectively, as the dependent variable. We find that the coefficients on both

MW_Fraud and MW_Other are positive and highly significant at the less than 1% level,

irrespective of whether the base model or the full model is used. We also find that the coefficient

on MW_Fraud is larger in magnitude and more significant than the coefficient on MW_Other. As

indicated in the bottom part of the table in Panel A, the results of Chi-square tests for the

difference in magnitude between the two estimated coefficients indicate that the difference is

The difference between the coefficients of 𝑀𝑊_𝐹𝑟𝑎𝑢𝑑 and 𝑀𝑊_𝑂𝑡ℎ𝑒𝑟 captures the

incremental crash risk for firms that have been identified by their auditors as not in compliance

with regulation and standards and having a higher probability of misstatement, relative to firms

with other types of internal control problems.

19 551 firm-year observations are identified as having problems with “restatement or nonreliance of company filings,” 74 firm-year observations are identified as having problems with “ethical or compliance issues with personnel,” and 52 firm-year observations are identified as having both types of problems.

26

statistically significant (at about the 5% level in two-tailed tests) for the base model as well as for

the full model. This suggests that firms with fraud-related ICWs are more likely to experience

extreme negative outliers in their weekly firm-specific return distribution than firms with other

types of ICWs.

As shown in Panel B of Table 5, when 𝑁𝐶𝑆𝐾𝐸𝑊 is used as the dependent variable, we

also find that the coefficients on 𝑀𝑊_𝐹𝑟𝑎𝑢𝑑 and 𝑀𝑊_𝑂𝑡ℎ𝑒𝑟 are both significantly positive,

and the former is larger in magnitude and more significant than the latter. As shown in the

bottom part of the table, the results of an F test for the difference in magnitude between the two

coefficients, MW_Fraud and MW_Other, indicate that the difference is statistically significant at

less than the 5% level at two-tailed tests). Overall the results in Panel B are qualitatively

identical with those in Panel A.

In short, our results reported in both panels of Table 5 are consistent with H2, suggesting

that (a) firms with fraud-related ICWs and those with other types of ICWs are likely to have

higher crash risk than firms with no such problems and (b) fraud-related ICW problems are more

serious than other ICW problems in terms of their impacts on increasing crash risk.

4.3 Does the disclosure of ICW reduce stock price crash risk?---Difference-in-difference tests

Recall that hypothesis H1 is concerned with cross-sectional differences in crash risk

between ICW firms and non-ICW firms prior to the ICW disclosure under SOX 404. This is

based on Doyle et al.’s (2007a) conjecture that ICW problems may have actually existed in years

prior to the ICW disclosures under SOX 404. 20

20 In a similar spirit, Schrand and Zachman (2012) report a “slippery slope” to financial misreporting for firms that are subject to AAERs.

In contrast, hypothesis H3 is interested in

27

whether and how the ICW disclosures bring about an over-time change in crash risk from the

pre-disclosure period to the post-disclosure period.

To test H3, we pool pre-SOX observations in years prior to the initial ICW disclosure and

post-SOX observations in years subsequent to the initial ICW disclosure. If ICWs facilitate bad

news hoarding by corporate insiders, then the increased crash risk associated with the presence

of undisclosed ICW (that existed in years prior to the initial ICW disclosure) should diminish

once firms reveal their ICW problems to the public: This is because the ICW disclosure itself

improves corporate reporting transparency and crash risk is inversely associated with

transparency (Jin and Myers, 2006). Specifically, one can expect that in the years after ICW

firms publicly disclose their ICW problems, there should be no significant difference in crash

risk between firms with no ICW problem and such firms that report ICWs. Stated another way,

ICW firms have now become transparent as they publicly disclosed their ICW problems, and

thus, in the post-disclosure period, the difference in crash risk should not be significant between

transparent ICW firms with public disclosures of their ICW problems and firms with no ICW

(and thus no disclosure of ICW).

Since it is unclear how long it will take ICW firms to remediate their publicly disclosed

ICW problems, we construct an expanded sample of 22,421 firm-years that covers two years

prior to and two years subsequent to the year of the ICW disclosure under SOX 404. To test H3,

we stack the four-year observations together, and then, estimate the following regression model:

𝐶𝑟𝑎𝑠ℎ𝑅𝑖𝑠𝑘 = 𝛼 + 𝛽1𝑃𝑅𝐸2 + 𝛽2𝑃𝑅𝐸1 + 𝛽3𝑃𝑂𝑆𝑇1 + 𝛽4𝑃𝑂𝑆𝑇2

+𝐶𝑟𝑎𝑠ℎ 𝑅𝑖𝑠𝑘 𝐷𝑒𝑡𝑒𝑟𝑚𝑖𝑛𝑎𝑛𝑡𝑠 + 𝐼𝐶𝑊 𝑑𝑒𝑡𝑒𝑟𝑚𝑖𝑛𝑎𝑛𝑡𝑠 + 𝜀 (5)

28

In the above equation, CrashRisk refers to either CRASH or NCSKEW. 𝑃𝑅𝐸1 (𝑃𝑅𝐸2) is an

indicator variable that equals one if the observation is within the 1-year (2-year) period before

the year of the adverse internal control opinion under SOX 404 disclosure and zero otherwise. To

the extent that publicly disclosed ICW problems existed in years prior to the public disclosure,

we expect that the coefficient on 𝑃𝑅𝐸1 (𝑃𝑅𝐸2) to be significantly positive. 𝑃𝑂𝑆𝑇1 (𝑃𝑂𝑆𝑇2) is

an indicator variable that equals to one if the observation is within the 1-year (2-year) period

after the ICW disclosure under SOX 404 and zero otherwise.21

Panel A of Table 6 reports the results of the logistic regression in Eq. (5) using CRASH as

the dependent variable. This regression allows us to assess the temporal variation in stock price

crash surrounding the initial public disclosure of ICW. As shown in Panel A, for both base and

full models, we find that the coefficients on 𝑃𝑅𝐸1 and 𝑃𝑅𝐸2 are both significantly positive. This

is consistent with the prediction in H1, suggesting that crash risk is higher for ICW firms than

non-ICW firms in up to two years prior to the initial ICW disclosure of an adverse SOX 404

audit opinion.

Our hypothesis H3 translates into

β2 > 0,β3 − β2 < 0.

On the other hand, the coefficient on 𝑃𝑂𝑆𝑇1 is significantly positive for both models. As

shown in the bottom part of Panel A of Table 6, the results of Chi-square test for the difference

in magnitude between the two regression coefficients suggests that the difference, β3 − β2, is

significantly negative. This is consistent with our hypothesis H3 that stock price crash risk

declines significantly from the pre-ICW-disclosure period to the post-ICW-disclosure period,

once ICWs are publicly disclosed. Interestingly, the coefficient on 𝑃𝑂𝑆𝑇2 is not statistically

21 For example, 𝑃𝑅𝐸1is equal to one for fiscal year 2003 if the firm discloses a material weakness for fiscal year 2004. 𝑃𝑂𝑆𝑇1 is equal to one for fiscal year 2005 if the initial disclosure of a material weakness occurs in fiscal year 2004. 𝑃𝑅𝐸2 and 𝑃𝑂𝑆𝑇2 are defined similarly.

29

different from zero, suggesting that crash risk differentials between ICW firms and non-ICW

firms disappear, in large part, in the second year of the post-disclosure period following the

initial disclosure. Stated another way, it takes about two years for the crash risk differentials to

dissipate in the post-disclosure period.

Panel B of Table 6 reports the results of OLS regressions for Eq. (5) using 𝑁𝐶𝑆𝐾𝐸𝑊 as

the dependent variable. The results in Panel B are qualitatively identical to those in Panel A,

except that the coefficient on 𝑃𝑂𝑆𝑇2, which is insignificant in Panel A, becomes significant at

the 5% level in the full-model specification.22

In short, the results in Panels A and B are, overall, consistent with our hypothesis H3 that

the disclosure of ICWs leads to a significant decline in stock price crash risk during the post-

disclosure period. Stated another way, our results in Table 6 can be interpreted broadly in such a

way that the public disclosure of ICW improves corporate reporting transparency, particularly,

bad news hoarding, thereby leading to a decline in crash risk in the post-disclosure period.

The F-statistics in the bottom part of Panel B

indicates that the decline of crash risk from the PRE1 period to the POST1 period is highly

significant.

5. Further Analysis and Robustness Check

5.1 Post-remediation analysis

In our main analyses, we provide evidence that the presence of ICW is positively

associated with stock price crash risk. We also provide evidence suggesting that upon the initial

ICW disclosure, managers of ICW firms tend to exert extra effort to improve internal control

22 An F-test indicates that the difference between pre and post coefficients, our main variable of interest, is negatively significant.

30

quality as manifested in a reduced crash risk in the post-ICW-disclosure period. For

completeness of our story, we further analyze whether the difference in crash risk, if any,

between ICW and non-ICW firms in the post-disclosure period disappears after firms with

adverse internal control opinions under SOX 404 remediate publicly disclosed ICW problems.

To address this issue, we estimate the following model:

𝐶𝑅𝐴𝑆𝐻 = 𝛼 + 𝛽1𝑃𝑜𝑠𝑡_𝑅𝑒𝑚_1 + 𝛽2𝑃𝑜𝑠𝑡_𝑅𝑒𝑚_2

+𝐶𝑟𝑎𝑠ℎ 𝑅𝑖𝑠𝑘 𝐷𝑒𝑡𝑒𝑟𝑚𝑖𝑛𝑎𝑛𝑡𝑠 + 𝐼𝐶𝑊 𝑑𝑒𝑡𝑒𝑟𝑚𝑖𝑛𝑎𝑛𝑡𝑠 + 𝜀 (6)

where 𝑃𝑜𝑠𝑡_𝑅𝑒𝑚_1 (𝑃𝑜𝑠𝑡_𝑅𝑒𝑚_2) is an indicator variable that equals one if the observation is

within the 1-year (2-year) period after previously disclosed ICW problems are remediated and

zero otherwise.23

Panels A and B of Table 7 reports the regression results, using CRASH and NCSKEW,

respectively, as the dependent variable. In Panel A, we find that the coefficients on 𝑃𝑜𝑠𝑡_𝑅𝑒𝑚_1

and 𝑃𝑜𝑠𝑡_𝑅𝑒𝑚_2 are both insignificant at any conventional level. This is consistent with the

view that the remediation of ICW problems constrains managerial opportunism in financial

reporting, including bad news hoarding by corporate insiders. As shown in Panel B, the results

using 𝑁𝐶𝑆𝐾𝐸𝑊 as the dependent variable are, overall, qualitatively similar to those in Panel A,

Once firms with adverse internal control opinions successfully remediate their

ICW problems and subsequently receive clean internal control opinions, stock price crash risk

for such firms should not differ significantly from crash risk for firms with no ICW problem. In

other words, we predict that the coefficient on 𝑃𝑜𝑠𝑡_𝑅𝑒𝑚_1 (𝑃𝑜𝑠𝑡_𝑅𝑒𝑚_2) is insignificant.

Under this prediction, no differential crash risk exists between ICW firms and firms that

remediate previously disclosed ICW problems, and thus, subsequently receive clean opinions.

23 For example, 𝑃𝑜𝑠𝑡_𝑅𝑒𝑚_1 is equal to one for fiscal year 2006 if the firm discloses a material weakness for fiscal year 2004 and a clean opinion for fiscal year 2005.

31

except that we find the coefficient on 𝑃𝑜𝑠𝑡_𝑅𝑒𝑚_1 is significant, but becomes insignificant once

we extend the post-remediation period up to two years. In short, the results of our post-

remediation analyses reinforce our main inference that the crash risk differential between ICW

and non-ICW firms decreases or largely disappears, once previously disclosed ICW problems are

ex post remediated.

5.2 The Cox hazard model approach

Jin and Myers (2006) point out that time can enter investors’ assessment of crash

probabilities in the sense that the probability of crash occurrence in current period depends on

the occurrence of a crash in the previous period. In a related vein, Kim and Zhang (2012) argue

that a proportional hazard approach is more appropriate for the purpose of examining firm-

specific determinants of crash risk, because this approach controls for the past history of crashes

when predicting future crash likelihood. However, one drawback of this approach is that it

necessarily leads to a substantial reduction in sample size, because it requires that a firm be

included into the sample only when such a firm experienced at least one crash event during the

sample period.

Similar to Kim et al. (2012), in an attempt to check the robustness of our main results, we

estimate the Cox proportional hazard model as specified below:

𝑙𝑛ℎ𝑗𝑘(𝑡) = µ�𝑡 − 𝑡𝑗(𝑘−1)� + 𝛽1𝑀𝑊𝑗𝑘

+𝐶𝑟𝑎𝑠ℎ 𝑅𝑖𝑠𝑘 𝑑𝑒𝑡𝑒𝑟𝑚𝑖𝑛𝑎𝑛𝑡𝑠 + 𝐼𝐶𝑊 𝐷𝑒𝑡𝑒𝑟𝑚𝑖𝑛𝑎𝑛𝑡𝑠 + 𝜀𝑗𝑘 (7)

32

where ℎ𝑗𝑘(𝑡) is the “hazard” or instantaneous likelihood of crash occurrence, for firm 𝑗 at time 𝑡,

conditional on 𝑘 crashes having occurred in firm 𝑗 by time 𝑡;24

To estimate the hazard model in Eq. (7), we identify a sample of firms with at least one

crash event during the sample period. For each crash event of a firm, we calculate the crash

interval, which is the length of time (in weeks) from the current crash event to the next. If no

further crash event is observed, the interval is the length of time from the current event until the

firm’s delisting date or the ending date of the sample period, whichever occurs first. The control

variables are the same as in Eq. (2) and year dummies are included. The model is estimated using

partial likelihoods developed by Cox (1975). The partial likelihood estimation makes it possible

to estimate all coefficients without specifying a particular functional form of 𝜇(. ). Industry-level

stratification allows different industries to have different baseline hazard functions, while

constraining the coefficients to be the same across industries (Allison, 2005).

𝑡𝑗(𝑘−1) is the time of the (𝑘 − 1)th

event; and 𝜇(. ) is an unspecified function that captures the baseline hazard. Hypothesis H1

predicts that 𝛽1 > 0 , which can be interpreted as the extent to which the hazard of crash

occurrences increases with the lack of internal control quality given the past crash history.

Table 8 reports the estimated results for the hazard model in Eq. (7). As shown in Table 8,

we find that the coefficients on 𝑀𝑊 are significantly positive in both models. This is in line with

our earlier finding in Table 4, suggesting that the instantaneous crash likelihood of firms with

ineffective internal control at time 𝑡 is higher than that of firms with no ICW, even after

24 The hazard function is defined as follows:

ℎ𝑗(𝑡) = 𝑙𝑖𝑚∆𝑡→0𝑃𝑟 [𝑁𝑗(𝑡 + ∆𝑡) − 𝑁𝑗(𝑡)]

∆𝑡

where 𝑁𝑗(𝑡) is the number of events that have occurred to firm 𝑗 by time 𝑡.

33

controlling for past crash history. This lends further support to our main finding that the presence

of ICW is positively associated with stock price crash risk.

5.3 Alternative measures of crash risk

As our third proxy for crash risk, we use 𝐷𝑈𝑉𝑂𝐿 as the dependent variable25

6. Conclusion

and re-

estimate all the regressions reported in Table 4 through Table 7. Though not tabulated for brevity,

the results using this alternative measure of crash risk are qualitatively similar to those reported

in the paper.

We examine whether and how the presence of ICW and its initial disclosure and

subsequent remediation are associated with stock price crash risk. Consistent with our prediction,

we find that the presence of (undisclosed) ICW is positively associated with crash risk, and this

positive association exists up to two years prior to the initial ICW disclosure. Moreover, we find

that the impact of initial ICW disclosure on crash risk gradually declines in the post-disclosure

period up to two years subsequent to the initial disclosure, and largely disappears after

remediation of previously disclosed ICW problems. In addition, we find that firms with fraud-

related ICWs are more crash-prone than other ICWs. The above results are incrementally

significant even after controlling for Hutton et al’s (2009) information opaqueness, Chen et al.’s

(2001) investor heterogeneity, other firm-specific factors that prior research identified to be

associated with stock price crash risk, and firm-specific determinants of ICW identified by prior

research on internal control quality. Our results are robust to the use of alternative proxies for

crash risk and different econometric designs.

25 See section 3 and Appendix A for an empirical definition of 𝐷𝑈𝑉𝑂𝐿.

34

Collectively, our findings support the view that the quality of a firm’s internal controls

plays an important role in constraining stock price crash risk and maintaining the stability of

stock markets. More importantly, our results highlight the importance of the disclosure of

material weaknesses in internal controls over financial reporting: ICW disclosure induces a

heighted degree of scrutiny and external monitoring by outside investors, and thus, encourage

corporate insiders to be more forthcoming with respect to bad news disclosure. This contributes

to lowering stock price crash risk. Our study provides new evidence on the market consequences

of ineffective internal controls and the potential benefits associated with SOX 404 disclosure.

35

References

Allison, P.D., 2005. Fixed effects regression methods for longitudinal data using SAS. Cary, NC: SAS Institute.

Altamuro, J., Beatty, A., 2010. How does internal control regulation affect financial reporting? Journal of Accounting and Economics 49: 58-74.

Ashbaugh-Skaife, H., Collins, D., Kinney, W., 2007. The discovery and reporting of internal control deficiencies prior to SOX-mandated audits. Journal of Accounting and Economics 44, 166-192.

Ashbaugh-Skaife, H., Collins, D., Kinney, W., LaFond, R., 2009. The effect of SOX internal control deficiencies and their remediation on accrual quality. The Accounting Review 83, 217-250.

Ball, R., 2001. Infrastructure requirements for an economically efficient system of public financial reporting and disclosure. Brookings-Wharton papers on Financial Services 2, 127-169.

Ball, R., 2009. Market and political/regulatory perspectives on the recent accounting scandals. Journal of Accounting Research 47, 277-323.

Beneish, M.D., Billings, M.B., Hodder, L.D., 2008. Internal control weakness and information uncertainty. The Accounting Review 83, 665-703.

Benmelech, E., Kandel, E., Veronesi, P., 2010. Stock-based compensation and CEO (dis)incentives. The Quarterly Journal of Economics, 1769-1820.

Berger, P., Li, F., Wong, F., 2005. The impact of Sarbanes-Oxley on cross-listed companies. Working paper, University of Chicago.

Beyer, A., Cohen, D.A., Lys, T.Z., Walther, B.R., 2010. The financial reporting environment: review of the recent literature. Journal of Accounting and Economics 50, 296-343.

Bleck, A., Liu, X., 2007. Market transparency and the accounting regime. Journal of Accounting Research 45, 229-256.

Charles River Associates, 2005. Sarbanes Oxley Section 404 costs and remediation of deficiencies: Estimates from a sample of Fortune 1000 companies.

Cheffers, M., Whalen, D., and Thrun, M., 2010. SOX 404 Dashboard, Year 6 Update. AuditAnalytics.com.

Chen, J., Hong, H., Stein, J.C., 2001. Forecasting crashes: trading volume, past returns, and conditional skewness in stock prices. Journal of Financial Economics 61, 345-381.

Cheng, M., Dhaliwal, D., Zhang, Y., 2012. Disclosure of internal control over financial reporting effectiveness and empire building. Working paper.

36

Costello, A.M., Wittenberg-Moerman, R., 2011. The impact of financial reporting quality on debt contracting: Evidence from internal control weakness reports. Journal of Accounting Research 49, 97-136.

Cox, D.R., 1975. Partial likelihood. Biometrika 62, 269-272.

Dhaliwal, D., Hogan, C., Trezevant, R., Wilkins, M., 2011. Internal control disclosures, monitoring, and the cost of debt. The Accounting Review 86, 1131-1156.

DeFond, M., Hung, M., Li, S., Li, Y., 2012. Does mandatory IFRS adoption affect crash risk? Working Paper.

DeFond, M., Jiambalvo, J., 1994. Debt covenant violation and manipulation of accruals. Journal of Accounting and Economics 17, 145-176.

Doss, M., Jonas, G., 2004. Section 404 reports on internal control: Impact on ratings will depend on nature of material weakness reported. Moody’s Investors Service, Global Credit Research. October.

Doyle, J., Ge, W., McVay, S., 2007a. Accruals quality and internal control over financial reporting. The Accounting Review 82, 1141-1170.

Doyle, J., Ge, W., McVay, S., 2007b. Determinants of weakness in internal control over financial reporting. Journal of Accounting and Economics 44, 193-223.

Efendi, J., Srivastava, A., Swanson, E., 2007. Why do corporate managers misstate financial statements? The role of option compensation and other factors. Journal of Financial Economics 85, 667-708.

Fairfield, P., Sweeney, R., Yohn, T., 1996. Accounting classification and the predictive content of earnings. The Accounting Review 71, 337-355.

Feng, M., Li, C., McVay, S., 2009. Internal control and management guidance. Journal of Accounting and Economics 48, 190-209.

Ge, W., McVay, S., 2005. The disclosure of material weakness in internal control after the Sarbanes-Oxle Act. Accounting Horizons 19, 13-158.

Gow, I.D., Ormazabal, G., Taylor, D., 2010. Correcting for cross-sectional and time-series dependence in accounting research. The Accounting Review 85, 483-512.

Hamm, S., Li, X., Ng, J., 2012. Management earnings guidance and stock price crash risk. Working paper.

Hammersley, J.S., Myers, L.A., Shakespeare, C., 2008. Market reactions to the disclosure of internal control weakness and to the characteristics of those weaknesses under Section 302 of the Sarbanes-Oxley Act of 2002. Review of Accounting Studies 13, 141-165.

Harvey, C.R., Siddique, A., 2000. Conditional skewness in asset pricing tests. The Journal of Finance 55, 1263-1295.

37

Hogan, C., Wilkins, M., 2008. Evidence on the audit risk model: do auditors increase audit fees in the presence of internal control deficiencies? Contemporary Accounting Research 25, 219-242.

Hong, H. A., Kim, J.-B., Welker, M. Divergence of cash flow and voting rights, Opacity, and stock price crash risk: International evidence. Working Paper (University of Memphis, Citry University of Hong Kong and Queens’ University)

Hong, H., Stein, J., 2003. Differences of opinion, short-sales constraints, and market crashes. Review of Financial Studies 16, 487-525.

Hutton, A.P., Marcus, A.J., Tehranian, H., 2009. Opaque financial reports, R2, and crash risk. Journal of Financial Economics 94, 67-86.

Jin, L., Myers, S.C., 2006. R2 around the world: new theory and new tests. Journal of Financial Economics 79, 257-292.

Johnstone, K., Li, C., Rupley, K., 2010. Changes in corporate governance associated with the revelation of internal control material weakness and their subsequent remediation. Contemporary Accounting Research 27: 1-53.

Jones, J., 1991. Earnings management during import relief investigations. Journal of Accounting Research 29, 193-228.

Kim, J.-B., Li, Y., Zhang, L., 2011a. CFOs versus CEOs: equity incentives and crashes. Journal of Financial Economics 101, 713-730.

Kim, J.-B., Li, Y., Zhang, L., 2011b. Corporate tax avoidance and stock price crash risk: firm-level analysis. Journal of Financial Economics 100, 639-662.

Kim, J.-B., Song, B.Y., Zhang, L., 2011. Internal control weakness and bank loan contracting: Evidence from SOX section 404 disclosures. The Accounting Review 86, 1157-1188.

Kim, J.-B., Zhang, L., 2012. Accounting conservatism and stock price crash risk: Firm-level evidence. (2012 Contemporary Accounting Research Conference paper).

Kim, J.-B., Zhang, L., 2013. Financial Reporting Opacity and Expected Crash Risk: Evidence from Implied Volatility Smirks. Contemporary Accounting Research (forthcoming).

Kinney, W.R., and Shepardson, M.L., 2011. Do control effectiveness disclosures require SOX 404(b) internal control audits? A natural experiment with small U.S. public companies. Journal of Accounting Research 49, 413-448.

Kizirian, T.G., Mayhew, B.W., Sneathen, J. 2005. The impact of management integrity on audit planning and evidence. Auditing: A Journal of Practice & Theory 24, 49-67.

Kothari, S.P., Shu, S., Wysocki, P., 2007. Do managers withhold bad news? Journal of Accounting Research 47, 241-276.

Lunndholm, R., Sloan, R., 2006. Equity valuation and analysis. McGraw-Hill, New York.

38

Ogneva, M., Subramanyam, K.R., Raghunandan, K., 2007. Internal control weaknesses and cost of equity: Evidence from SOX Section 404 disclosure. The Accounting Review 82, 1255-1297.

Pan, J., 2002. The jump-risk premia implicit in options: Evidence from an integrated time-series study. Journal of Financial Economics 63, 3-50.

Petersen, M.A., 2009. Estimating standard errors in finance panel data sets: Comparing approaches. Review of Financial Studies 22, 435-480.

Schipper, K., Vincent, L., 2003. Earnings quality. Accounting Horizons 17: 97-110.

Scholes, M., Williams, J., 1977. Estimating beta from nonsynchronous data. Journal of Financial Economics 5, 309-327.

Schrand, C., Zechman, S., 2012. Executive overconfidence and the slippery slope to financial misreporting. Journal of Accounting and Economics 53, 311-329.

Securities and Exchange Commission (SEC), 2003. Management’s report on internal control over financial reporting and certification of disclosure in exchange act periodic reports. http://www.sec.gov/rules/final/33-8238.htm. Release Nos. 33-8238.

Skaife, H., Veenman, D., Wangerin, D., 2012. Internal control over financial reporting and managerial rent extraction: Evidence from the profitability of insider trading. Journal of Accounting and Economics, forthcoming.