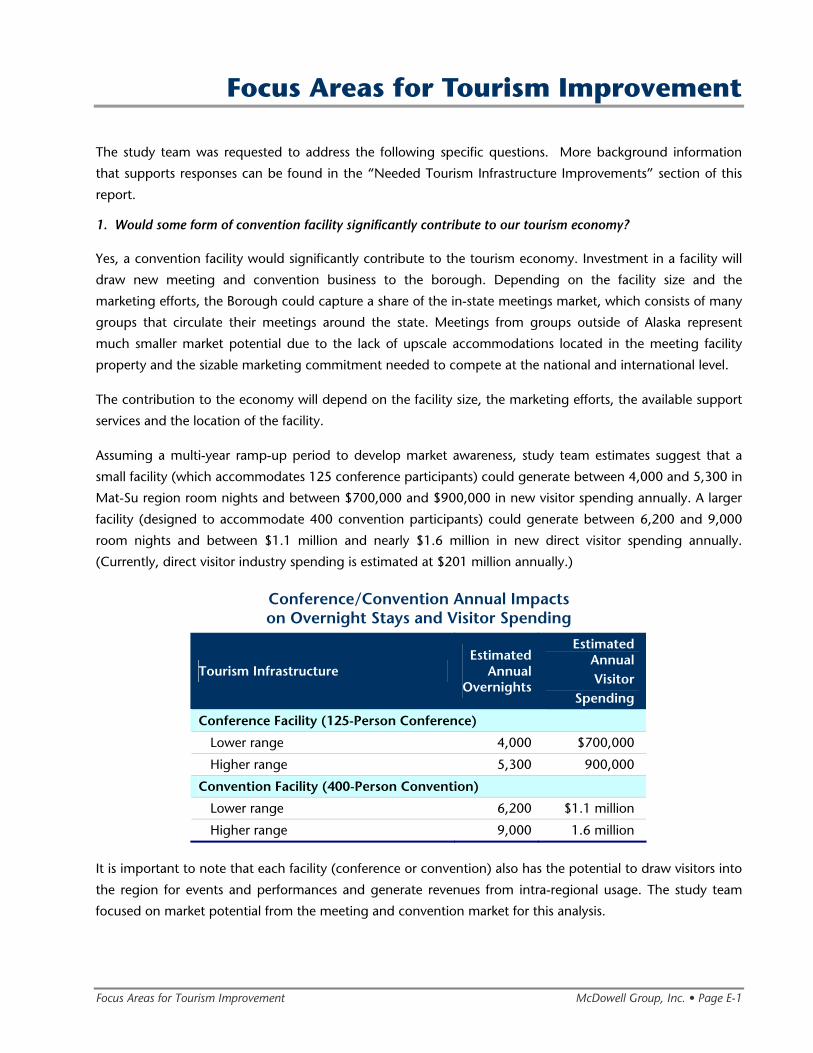

Matanuska-Susitna Borough Tourism Infrastructure Needs Study Prepared for: Matanuska-Susitna Borough June 2008

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Matanuska-Susitna Borough Tourism Infrastructure Needs Study

Prepared for:

Matanuska-Susitna Borough

June 2008

Matanuska-Susitna Borough Tourism Infrastructure Needs Study

Prepared for:

Matanuska-Susitna Borough

PREPARED BY:

Juneau Anchorage

In association with:

The Boutet Company Klugherz & Associates

MRV Architects

June 2008

Table of Contents

Executive Summary.........................................................................................................ES-1 Introduction and Methodology..................................................................................... IM-1 Geographic Overview ................................................................................................... GO-1

A: Base Case Tourism Infrastructure Description Introduction ..................................................................................................................... A-1 Accommodations ............................................................................................................. A-2 Meeting Facilities ............................................................................................................. A-6 Sports Facilities .............................................................................................................. A-13 Other Public Venues ...................................................................................................... A-16 Parks, Campgrounds, Boat Launches and Trails ........................................................... A-20 Transportation ............................................................................................................... A-25 Public Restroom Facilities .............................................................................................. A-29

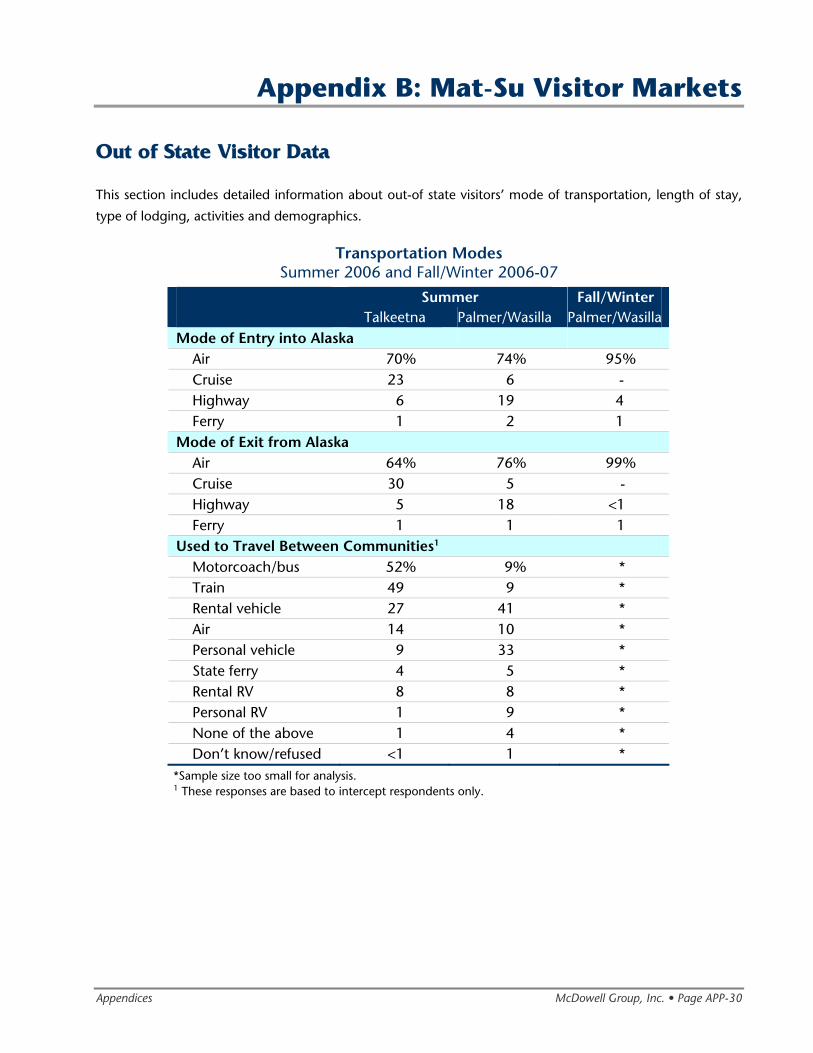

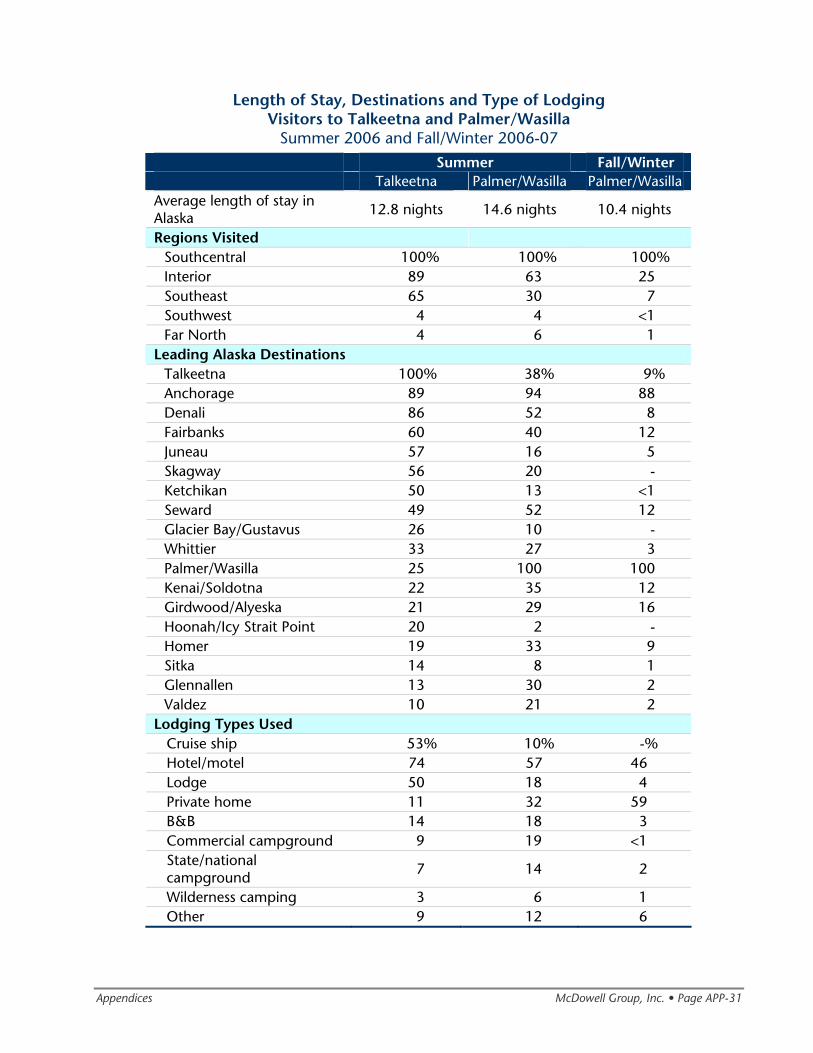

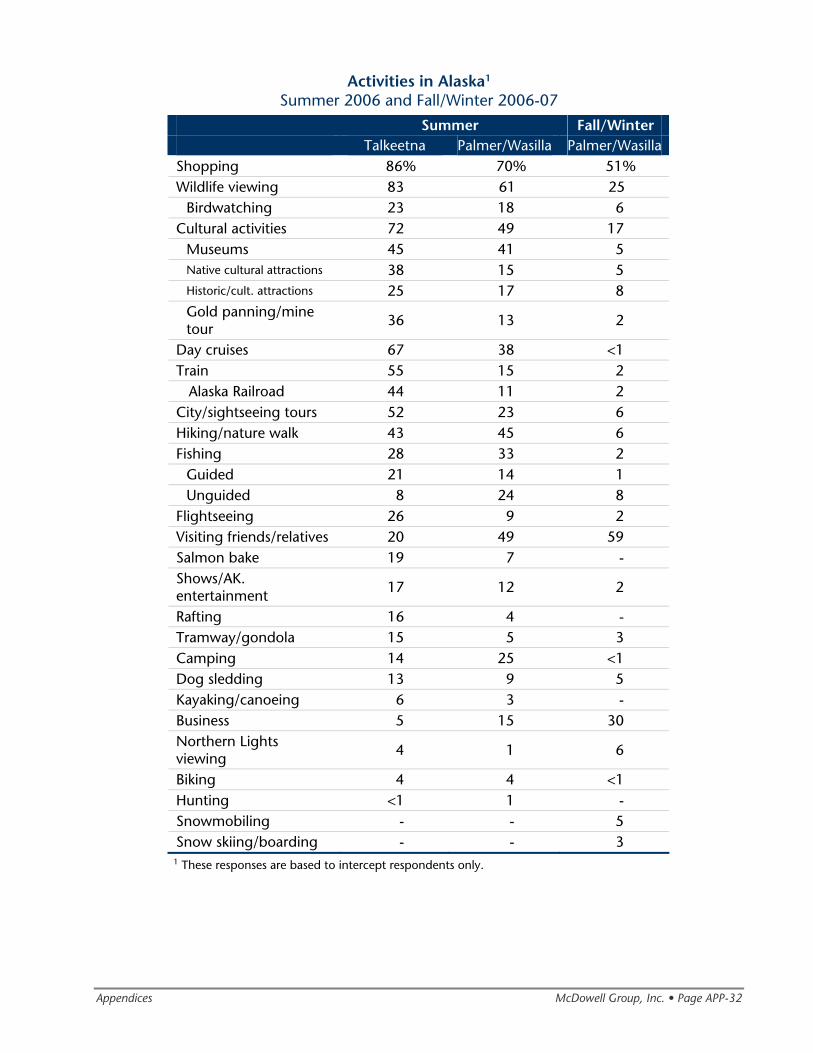

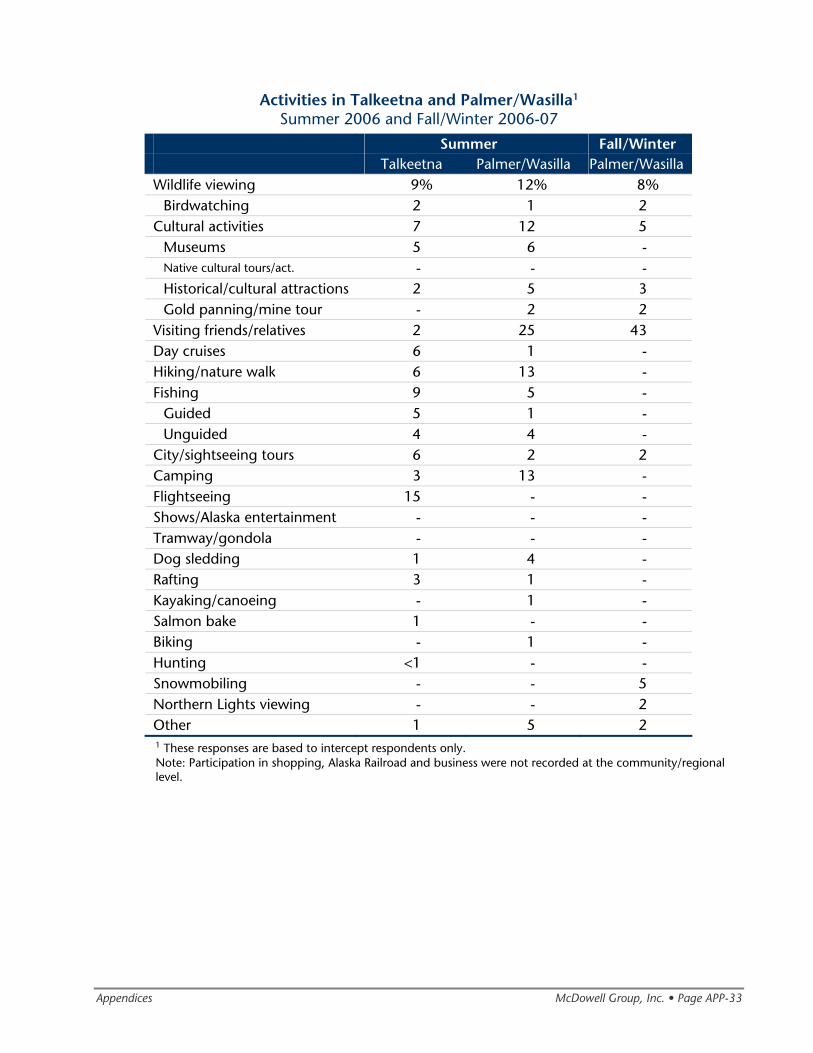

B: Mat-Su Visitor Markets Introduction ..................................................................................................................... B-1 Out-of-State Market Analysis........................................................................................... B-3 In-State Visitors.............................................................................................................. B-12 Market Outlook.............................................................................................................. B-14

C: Assessment of Tourism Industry Value Assessment of Tourism Industry Value ........................................................................... C-1

D: Needed Tourism Infrastructure Improvements Introduction .....................................................................................................................D-1 Meeting Facilities .............................................................................................................D-4 Road System Enhancements..........................................................................................D-11 Trail System Enhancements...........................................................................................D-17 Visitor Support Services.................................................................................................D-22 Determining Tourism Infrastructure Investment Priorities..........................................D-24 Potential Large Scale Destination and Attraction Developments................................D-31 Funding Approaches......................................................................................................D-36

E: Focus Areas for Tourism Improvement Focus Areas for Tourism Improvement ............................................................................E-1

F: Tourism Partnering Opportunities Introduction ......................................................................................................................F-1 Partnering Opportunities for Mat-Su Borough ...............................................................F-6

Appendices Appendix A: Tourism Infrastructure Description........................................................ APP-1 Appendix B: Mat-Su Visitor Markets ......................................................................... APP-30 Appendix C: Needed Tourism Infrastructure Improvements ................................... APP-52 Appendix D: Contacts and Information Sources ...................................................... APP-74 Appendix E: Montana Tourism Infrastructure Investment Program Guidelines................................................................................................................... APP-77

Executive Summary

Tourism Infrastructure Needs Study: Executive Summary McDowell Group, Inc. • Page ES-1

Introduction

The Matanuska-Susitna Borough is interested in understanding what tourism infrastructure investments are

needed to enhance visitors’ experience, increase overnight stays (thereby increasing bed tax revenue), and

maximize the overall economic return. The Borough contracted with McDowell Group, Inc. an Alaska

research and consulting firm with offices in Anchorage and Juneau, to take the lead role in the Tourism

Infrastructure Needs Study. Other members of the study team include The Boutet Company (an engineering

and planning firm based in Anchorage), Klugherz & Associates (a strategic planning and market development

firm based in Seattle), and MRV Architects (an architectural design firm based in Juneau).

The study includes six areas of analysis regarding borough tourism including: an inventory of existing tourism

infrastructure, an overview of visitor markets, the value of tourism to the borough, tourism infrastructure

needs, focus area questions and responses, and partnering opportunities.

• The study team compiled a detailed inventory of the Mat-Su Borough’s existing tourism

infrastructure, including accommodations, meeting facilities, sports facilities, parks, campgrounds,

boat launches, trails and other transportation infrastructure.

• The region’s current in-state and out-of-state visitor markets were analyzed, utilizing comprehensive

McDowell Group tourism research databases. The project also includes a discussion of the outlook for

several visitor markets and analyzes market implications for regional tourism infrastructure.

• The study team examined measures of tourism industry value, such as bed tax receipts and

employment. In addition, McDowell Group utilized modeling to estimate the direct, indirect and

induced economic benefits of the tourism sector in the Mat-Su region.

• The study team then examined how potential infrastructure improvements could enhance the

regional tourism industry and visitor experience. The team forecasted the increased number of

overnight stays likely to result and the overall economic return for four major categories of

infrastructure investment—meeting facilities, road system enhancements, trail system enhancements,

and visitor support services. Additionally, the study team examined development priorities, the

importance of large-scale destination and attraction development, and potential funding approaches.

• The study team responded to a series of questions specifically posed by the Borough at the beginning

of the study (entitled Focus Areas for Tourism Improvement).

• The project concluded with analysis of national trends in partnering that included ways in which

tourism entities, government, private land owners and others can work together to increase the

effectiveness of public dollars spent on tourism development. This section of the report includes

specific partnering recommendations for future tourism infrastructure developments in the region.

• Lastly, appendices provide detailed information supporting the assumptions and findings of the

study.

Key findings from the study are presented on the following pages.

Tourism Infrastructure Needs Study: Executive Summary McDowell Group, Inc. • Page ES-2

Base Case Tourism Infrastructure Assessment

The study provides a comprehensive look at the borough’s existing tourism infrastructure. The summary

below helps frame the current operating environment and potential for needed tourism infrastructure

developments.

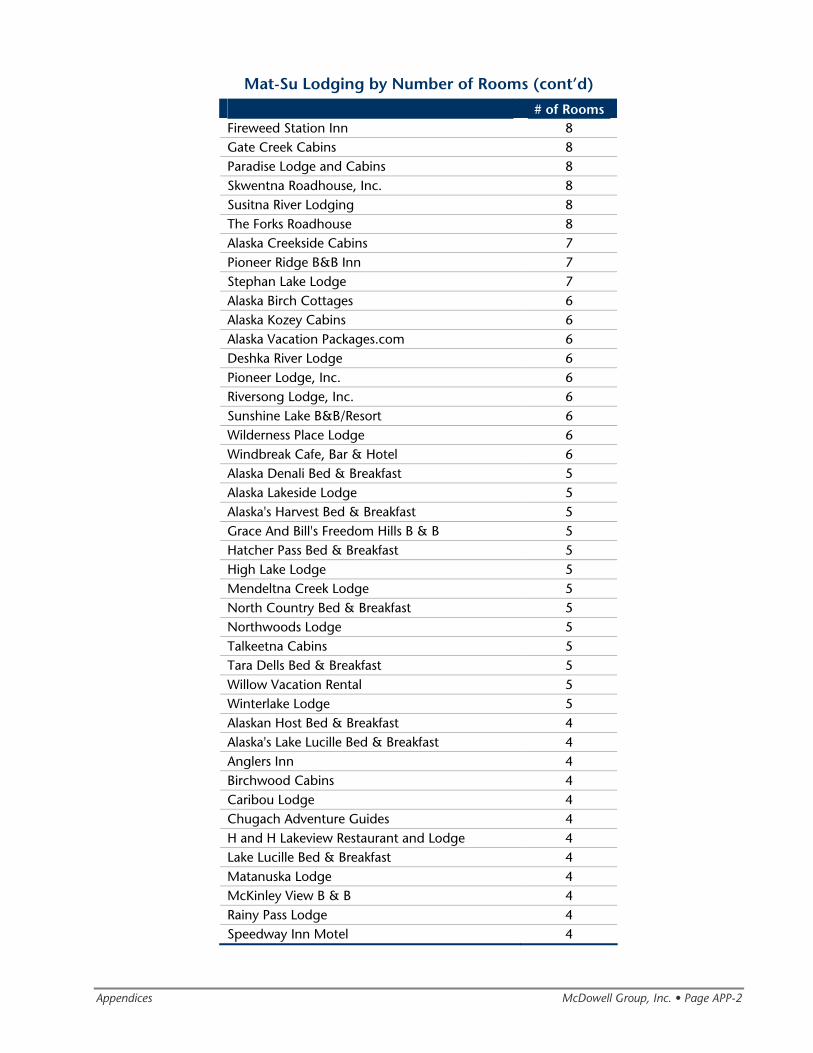

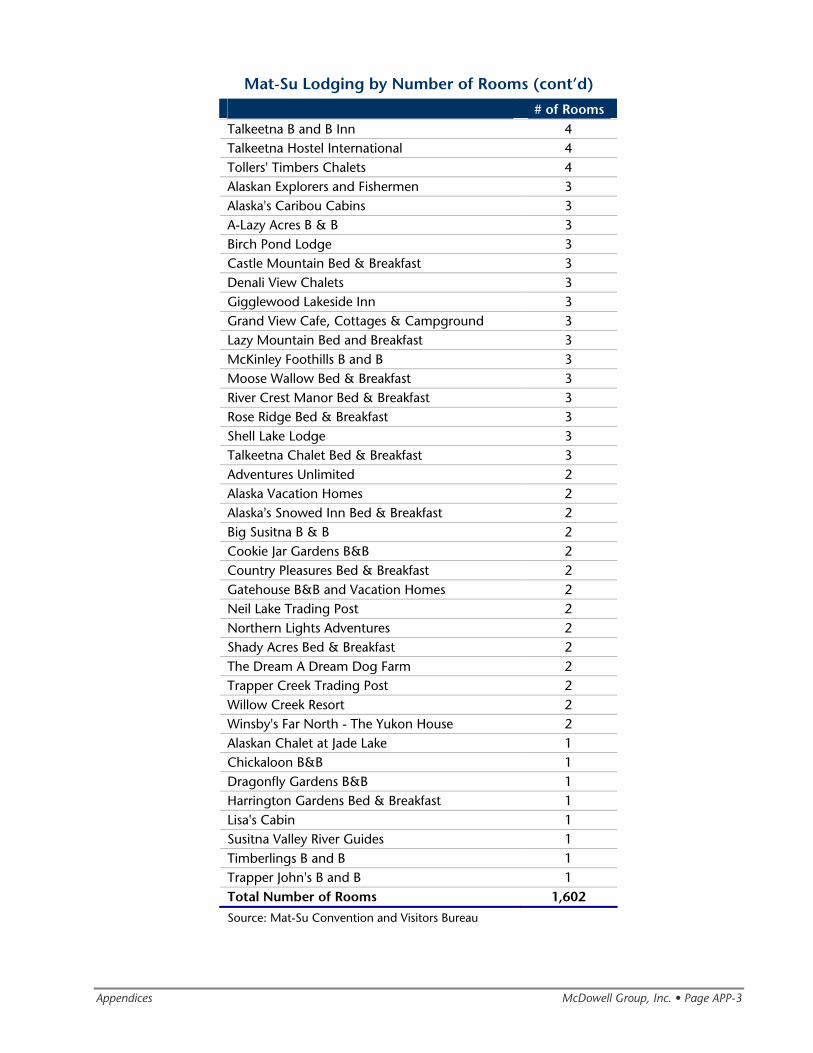

Accommodations • According to an inventory recently conducted by the Mat-Su Convention and Visitors Bureau, 118

different accommodations are available throughout the Mat-Su Borough with a total of 1,602 rooms.

The size of accommodations range from one-bedroom Bed & Breakfasts to a 460-room hotel.

• Fifty-eight percent of accommodations are concentrated in the Talkeetna/Denali State Park area,

including the two largest hotels (which account for 672 rooms).

• Small accommodations, consisting of one to nine rooms, make up the majority of individual facilities

in the borough and are found in all regions in the borough (90 properties or 76 percent). Twenty-

three properties make up the mid-sized accommodations (10 to 49 rooms). Just four properties have

50 rooms or more.

• The market for overnight accommodations is highly seasonal with the highest occupancy rates

occurring in the summer. Along with the two largest hotel properties, several other facilities also close

in the winter.

Meeting Facilities, Sports Facilities, and Other Public Venues • Ten large facilities are available to host a meetings, conferences and events ranging from 101 to 300

attendees. Most large facilities are located in the Wasilla/Palmer area; some additional facilities are

located in Willow and Talkeetna.

• Seven properties can accommodate groups between 51 and 100 participants. Locations vary.

• Twenty small meeting facilities are available throughout the Mat-Su Borough (capacity up to 50

attendees). The smaller, more remote properties are often used for staff or board retreats.

• Any meeting or event that requires a single facility with sleeping rooms, meeting rooms and dining

facilities is limited to approximately 100 attendees.

• While there are more than 400 guest rooms in the Wasilla/Palmer area, there is limited full-service

meeting capacity available to accommodate larger groups.

• While many of the existing sport facilities were developed to meet local residents’ needs, they are

important assets for attracting overnight visitors for tournaments and special events.

• Additional public venues that serve the visitor industry include the Alaska State Fairgrounds,

performance halls, museums, and several visitor centers.

Parks, Trails and Road System • The region includes parts of two national parks and 24 state park units.

• More than 20 public campgrounds offer 830 tent or RV sites. Additionally, 17 remote cabins are

available.

Tourism Infrastructure Needs Study: Executive Summary McDowell Group, Inc. • Page ES-3

• Over 60 boat launches provide access to waterways, including four prominent launches: Talkeetna

River Boat Launch, Susitna Landing, Deshka Landing, and the Little Susitna River Boat Launch.

• More than 2,000 miles of trails are located within the borough.

• Fewer parks and campgrounds are located along the Glenn Highway than the Parks Highway.

• The region includes 173 miles of the Parks Highway, 110 miles of the Glenn Highway, and

approximately 70 miles of the Denali Highway.

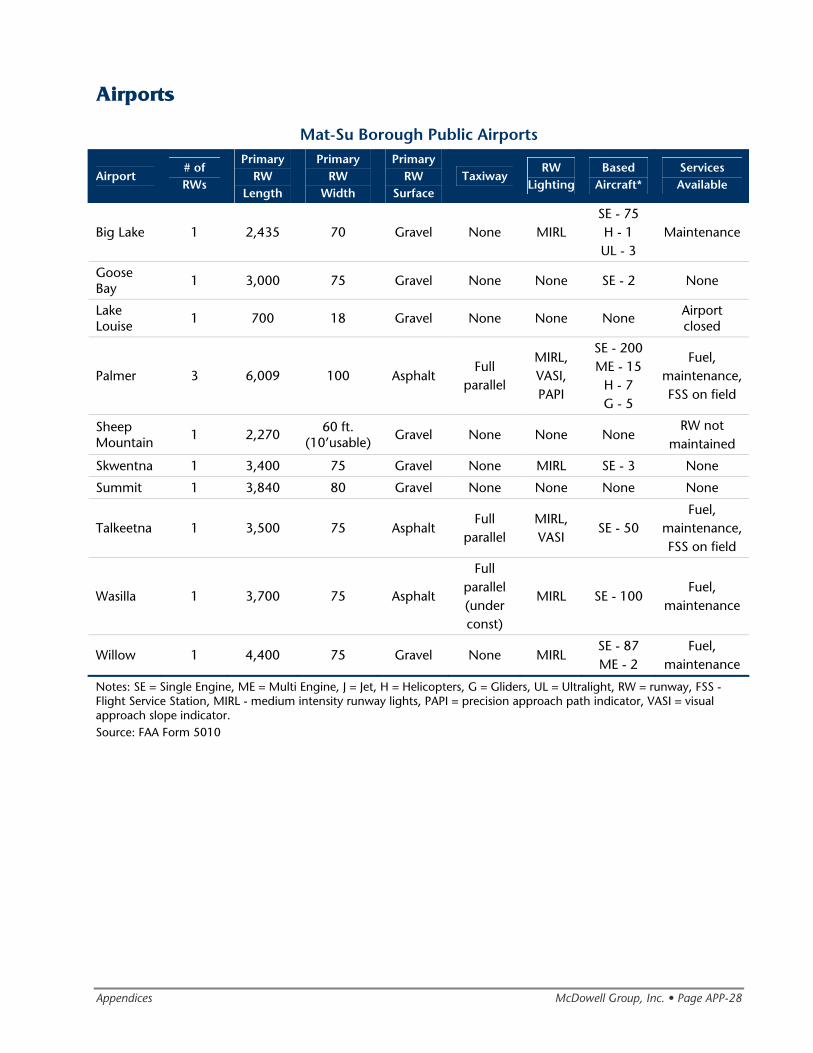

• Additional transportation infrastructure includes the Alaska Railroad, 10 public airports, and 200

private airports and air strips.

• The Parks and Glenn Highways have long stretches of roadway with no restroom facilities. Similarly,

the number of restrooms at trailheads, parks, and boat launches is insufficient.

Mat-Su Visitor Market Assessment

The study team examined both out-of-state and in-state visitor market to the Mat-Su Borough.

Visitor Volume • The approximate annual volume of all visitors to the Mat-Su Borough was estimated to be nearly

780,000 visitors in 2006/2007.

o An estimated 332,000 out-of-state visitors traveled to the Mat-Su Borough. Summer visitation

represented nearly 90 percent of the out-of-state visitor activity.

o The study team estimated that 446,000 Alaskans visited the Mat-Su Borough, with the largest

market being Anchorage residents. Summer visitors represented nearly 60 percent or

262,800 visitors; the number of fall/winter visitors totaled 183,400 Alaskans.

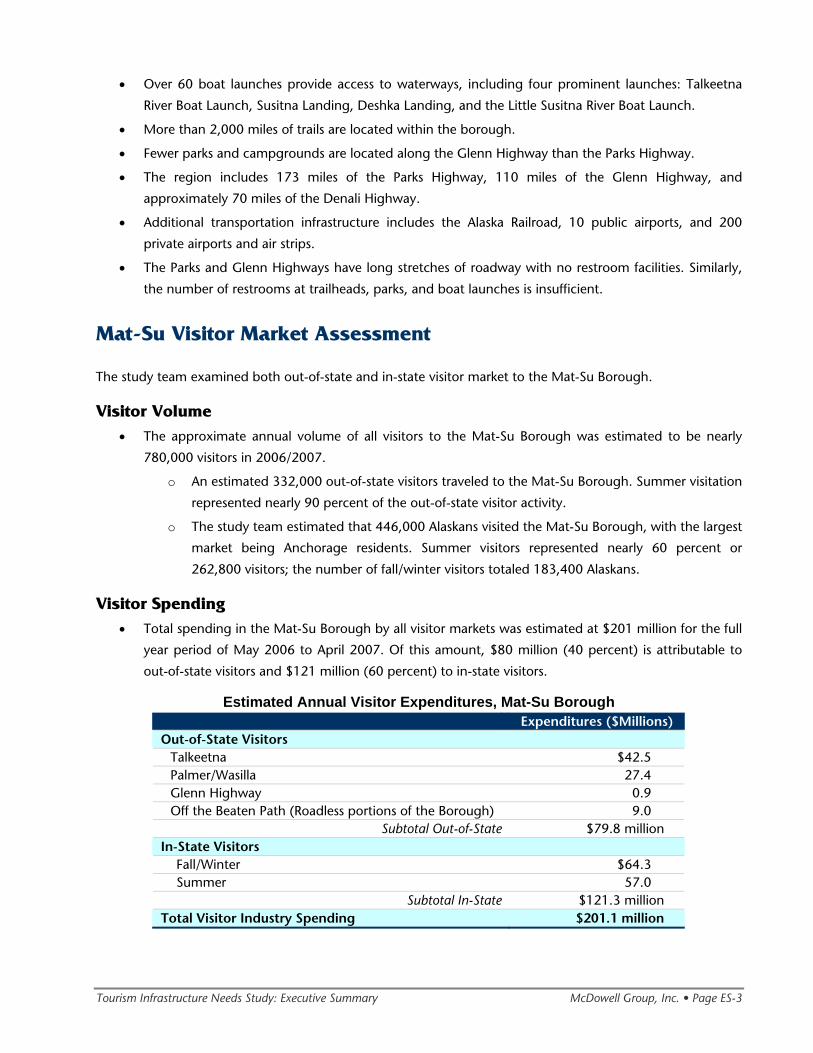

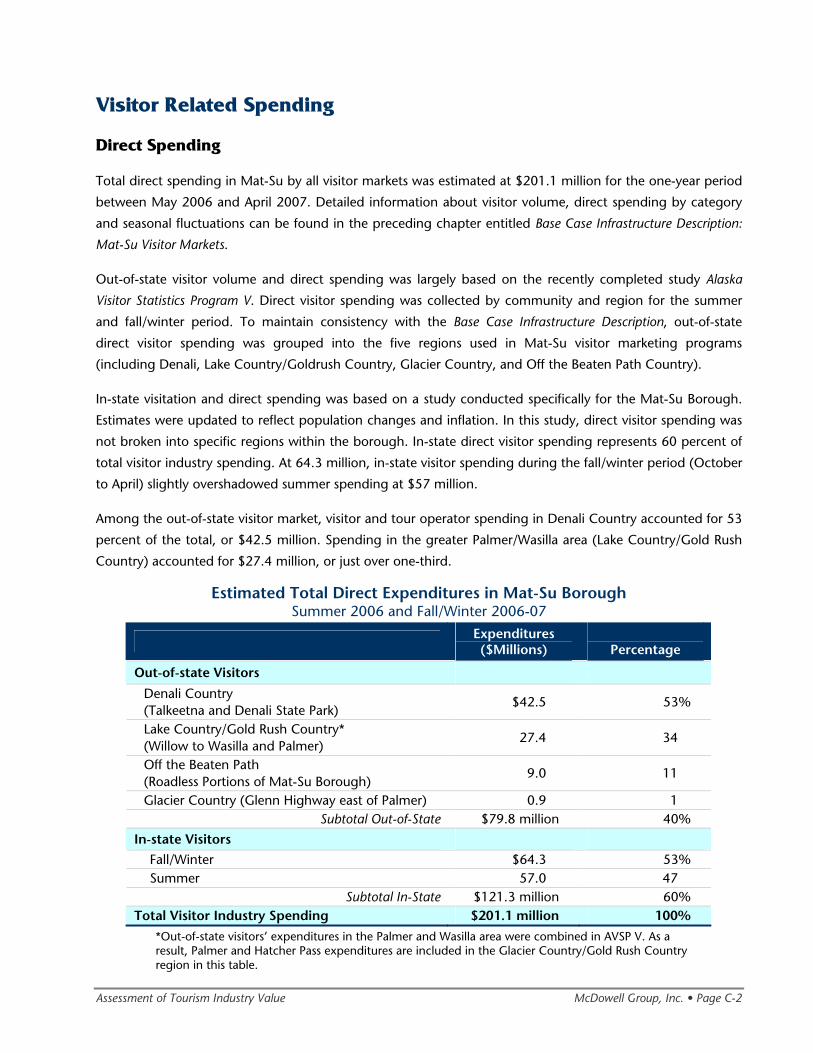

Visitor Spending • Total spending in the Mat-Su Borough by all visitor markets was estimated at $201 million for the full

year period of May 2006 to April 2007. Of this amount, $80 million (40 percent) is attributable to

out-of-state visitors and $121 million (60 percent) to in-state visitors.

Estimated Annual Visitor Expenditures, Mat-Su Borough Expenditures ($Millions)

Out-of-State Visitors Talkeetna $42.5 Palmer/Wasilla 27.4 Glenn Highway 0.9 Off the Beaten Path (Roadless portions of the Borough) 9.0

Subtotal Out-of-State $79.8 million In-State Visitors

Fall/Winter $64.3 Summer 57.0

Subtotal In-State $121.3 million Total Visitor Industry Spending $201.1 million

Tourism Infrastructure Needs Study: Executive Summary McDowell Group, Inc. • Page ES-4

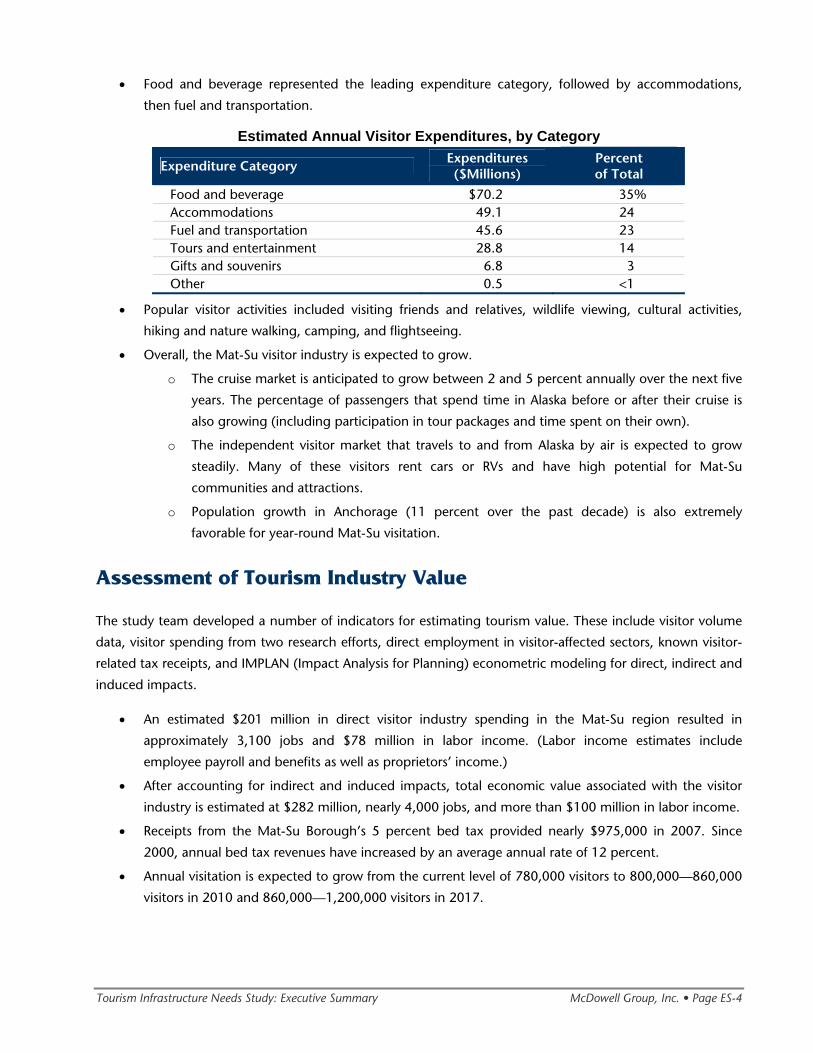

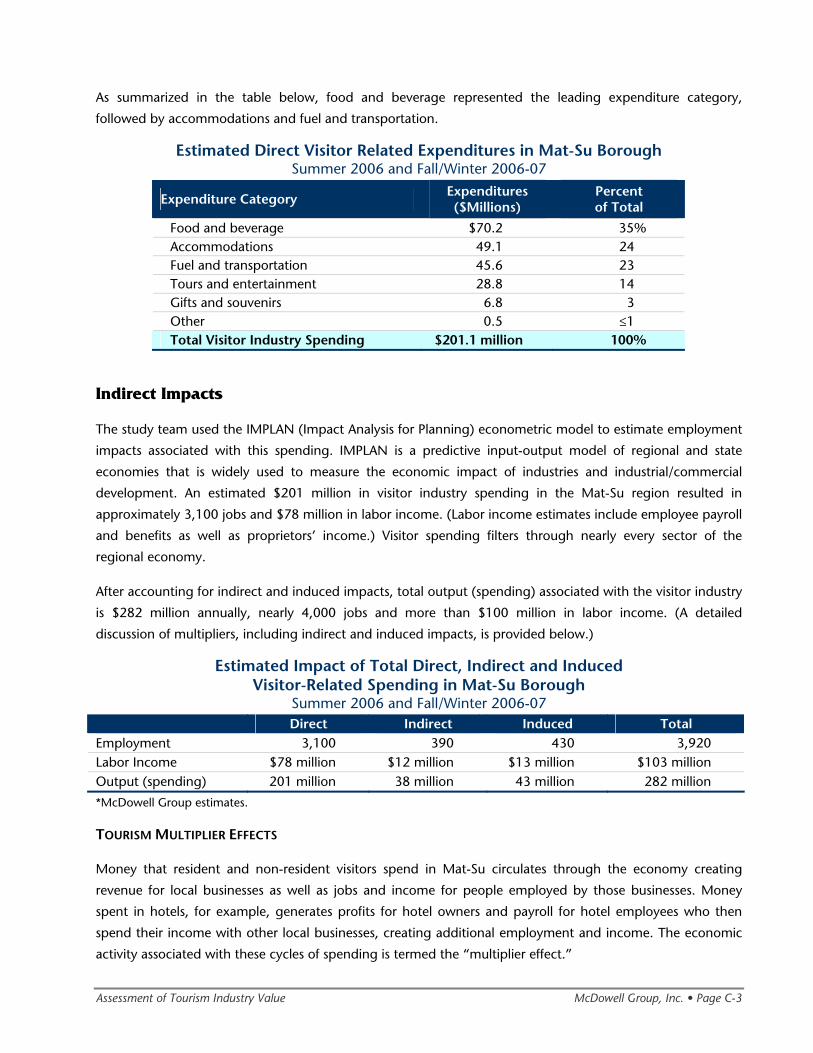

• Food and beverage represented the leading expenditure category, followed by accommodations,

then fuel and transportation.

Estimated Annual Visitor Expenditures, by Category

Expenditure Category Expenditures ($Millions)

Percent of Total

Food and beverage $70.2 35% Accommodations 49.1 24 Fuel and transportation 45.6 23 Tours and entertainment 28.8 14 Gifts and souvenirs 6.8 3 Other 0.5 <1

• Popular visitor activities included visiting friends and relatives, wildlife viewing, cultural activities,

hiking and nature walking, camping, and flightseeing.

• Overall, the Mat-Su visitor industry is expected to grow.

o The cruise market is anticipated to grow between 2 and 5 percent annually over the next five

years. The percentage of passengers that spend time in Alaska before or after their cruise is

also growing (including participation in tour packages and time spent on their own).

o The independent visitor market that travels to and from Alaska by air is expected to grow

steadily. Many of these visitors rent cars or RVs and have high potential for Mat-Su

communities and attractions.

o Population growth in Anchorage (11 percent over the past decade) is also extremely

favorable for year-round Mat-Su visitation.

Assessment of Tourism Industry Value

The study team developed a number of indicators for estimating tourism value. These include visitor volume

data, visitor spending from two research efforts, direct employment in visitor-affected sectors, known visitor-

related tax receipts, and IMPLAN (Impact Analysis for Planning) econometric modeling for direct, indirect and

induced impacts.

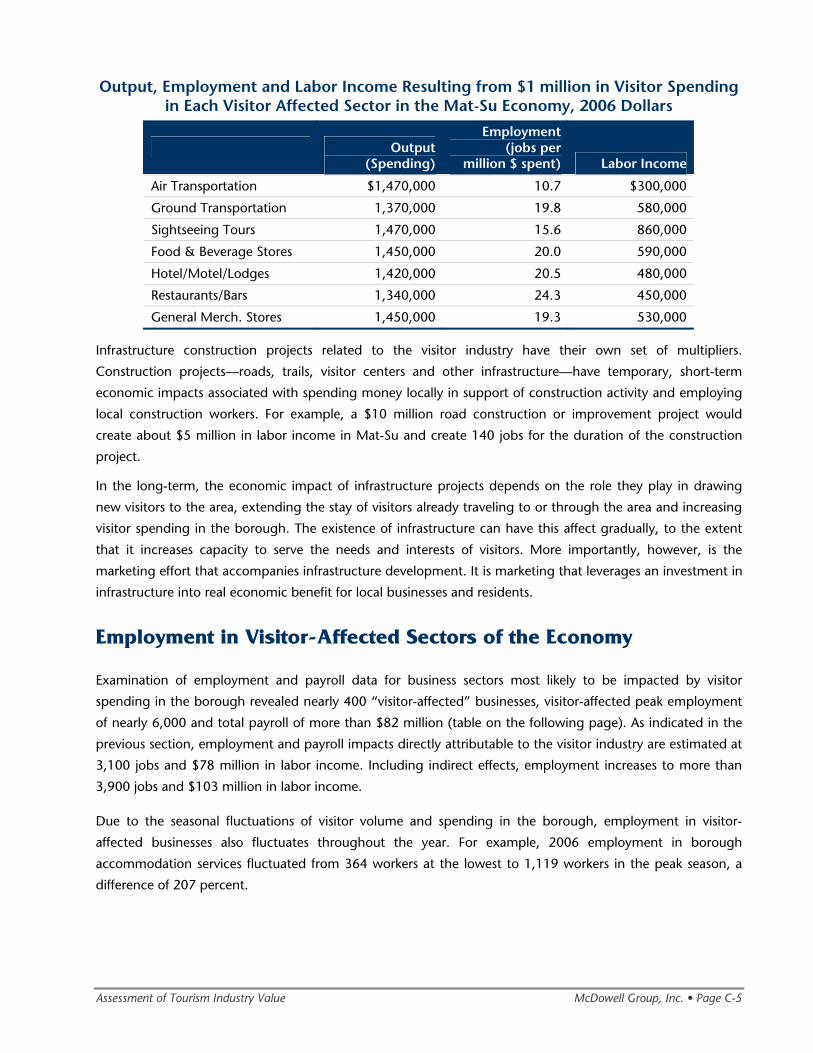

• An estimated $201 million in direct visitor industry spending in the Mat-Su region resulted in

approximately 3,100 jobs and $78 million in labor income. (Labor income estimates include

employee payroll and benefits as well as proprietors’ income.)

• After accounting for indirect and induced impacts, total economic value associated with the visitor

industry is estimated at $282 million, nearly 4,000 jobs, and more than $100 million in labor income.

• Receipts from the Mat-Su Borough’s 5 percent bed tax provided nearly $975,000 in 2007. Since

2000, annual bed tax revenues have increased by an average annual rate of 12 percent.

• Annual visitation is expected to grow from the current level of 780,000 visitors to 800,000—860,000

visitors in 2010 and 860,000—1,200,000 visitors in 2017.

Tourism Infrastructure Needs Study: Executive Summary McDowell Group, Inc. • Page ES-5

Needed Tourism Infrastructure Improvements

The study team identified four major categories of potential tourism infrastructure developments.

Development costs were estimated for each category as well as their potential effects on visitor volume,

overnight stays, and contribution to the regional economy. The likely impact of each category on the visitor

experience was also evaluated. A summary of findings for each of the recommended tourism infrastructure

development areas is provided below.

MEETING FACILITIES

The Mat-Su region is not competitive in the conference and convention market due to the lack of meeting

facilities that can accommodate meeting and banquet functions in the same building. Two proposed meeting

facility sizes were analyzed in this study.

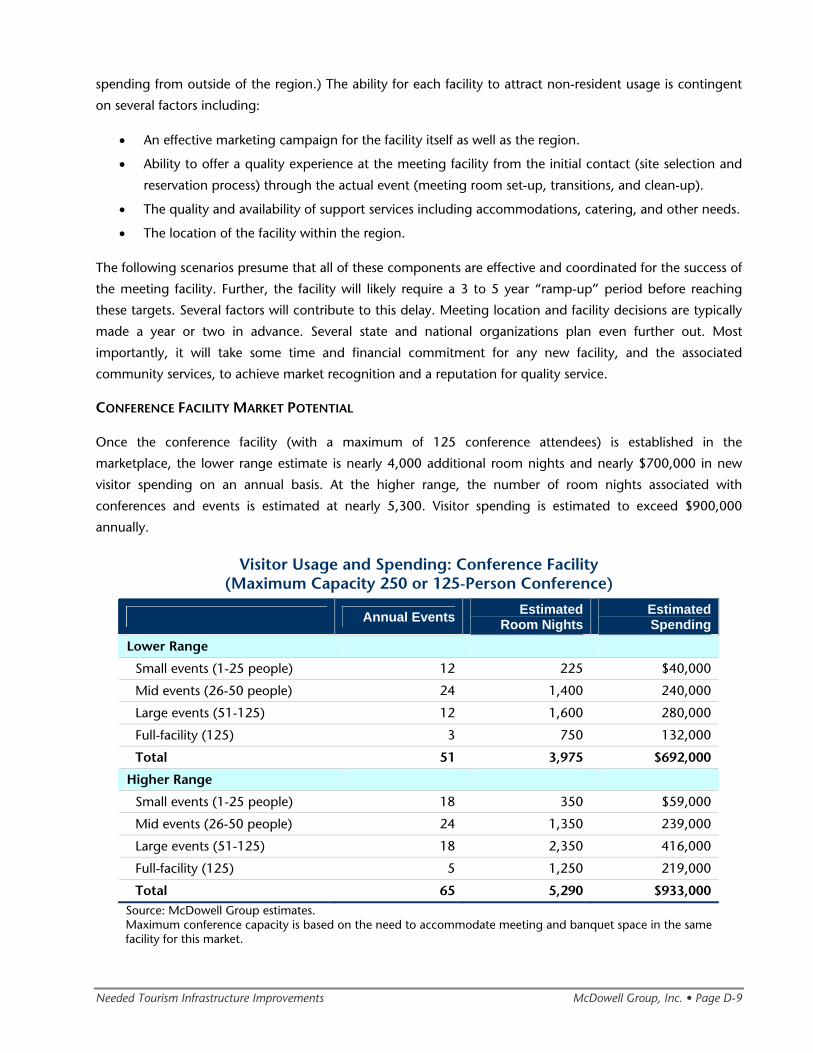

• Conference facility. At approximately 8,400 sq. ft., the facility could accommodate conferences of

125 attendees (or two concurrent events of 125 people.) Estimated construction costs would be $4.5

million. Based on comparable facilities, the financial gap between operating costs and revenues is

likely to be approximately $200,000. (This estimate includes routine operations and maintenance,

but does not include periodic capital costs or convention marketing.)

o Estimated annual meeting related market potential ranged from nearly 4,000 additional

room nights and $700,000 in new spending to nearly 5,300 room nights and $930,000 in

new spending.

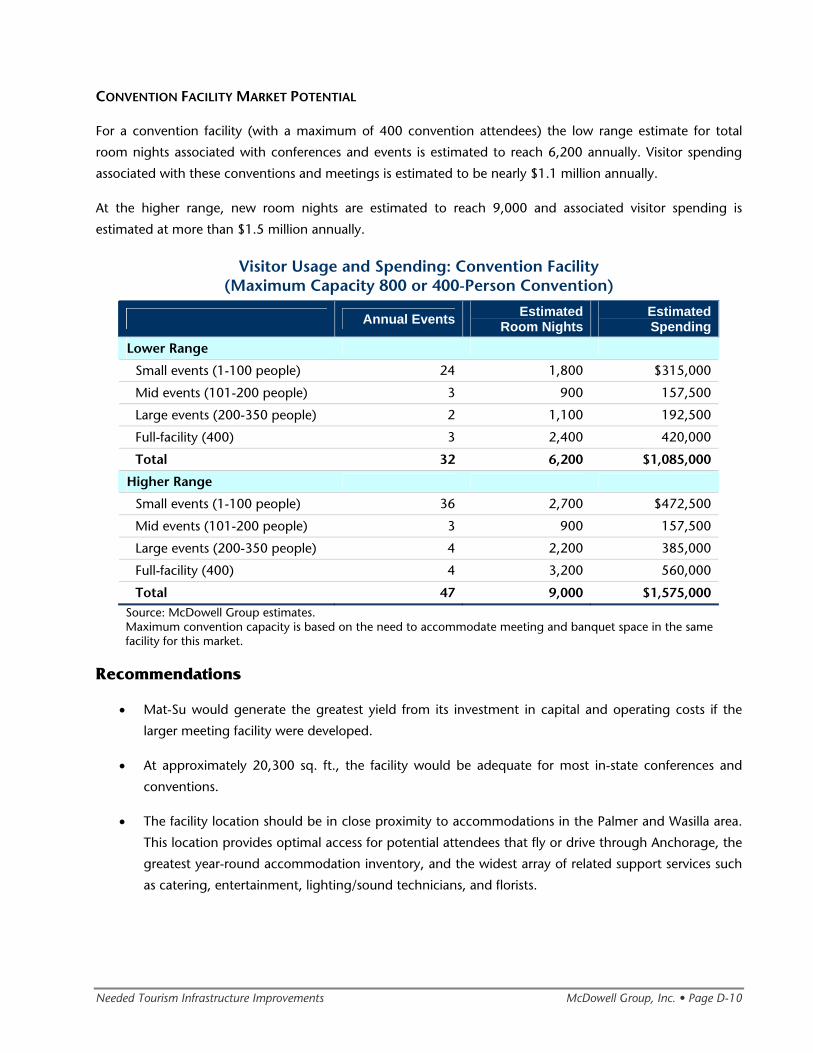

• Convention facility. At approximately 20,300 sq. ft., the larger facility is intended to accommodate

conventions of up to 400 attendees, including meetings, banquets, and three small conference

rooms that could be used for break-out sessions. Two concurrent events of 400 people could also

occur at the facility. Estimated construction cost is $10.8 million. The operating gap is estimated at

$300,000, based on comparable facilities. (This estimate does include routine operations and

maintenance, but does not include periodic capital costs or convention marketing.)

o Annual room nights associated with the convention and meeting market is estimated

between 6,200 and 9,000. New visitor spending associated with these conventions and

meetings is estimated between $1.1 and $1.5 million annually.

• While the initial capital costs are greater, Mat-Su would generate the largest return on investment

from annual operating costs from the larger convention facility.

• The optimal location for a new meeting facility is near Palmer and Wasilla, which offer the closest

proximity to Anchorage, year-round accommodations, and related services like catering,

entertainment, and lighting and sound technicians.

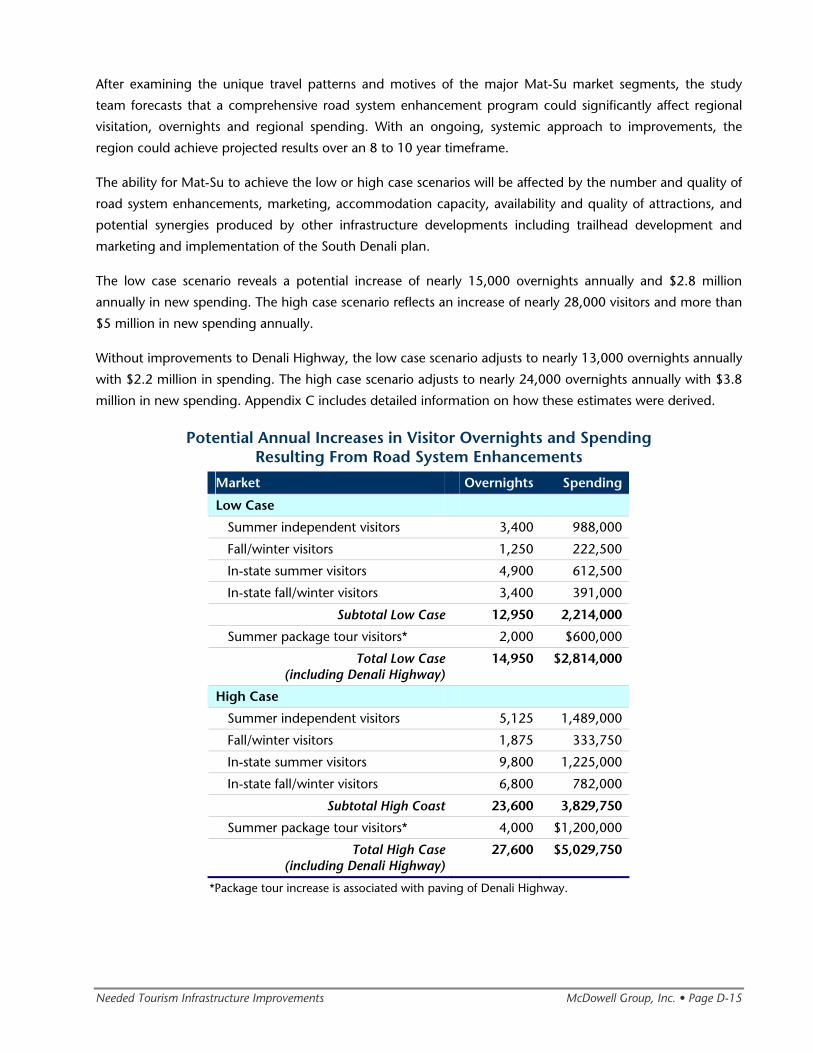

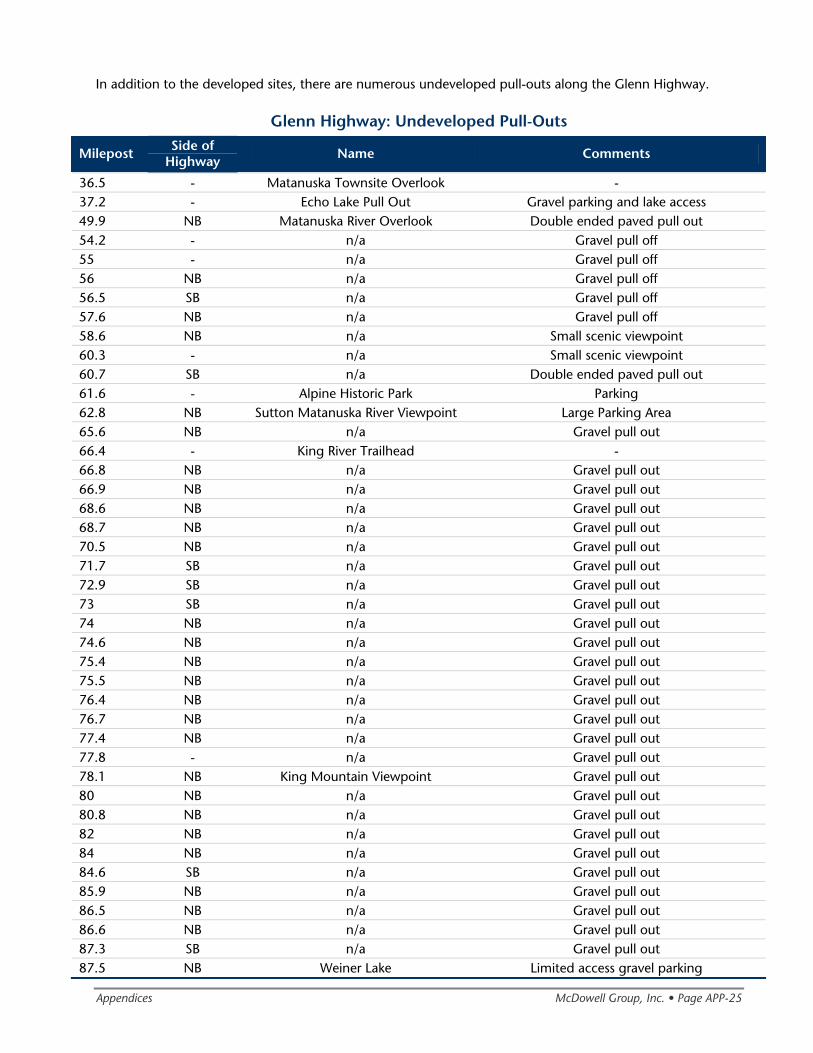

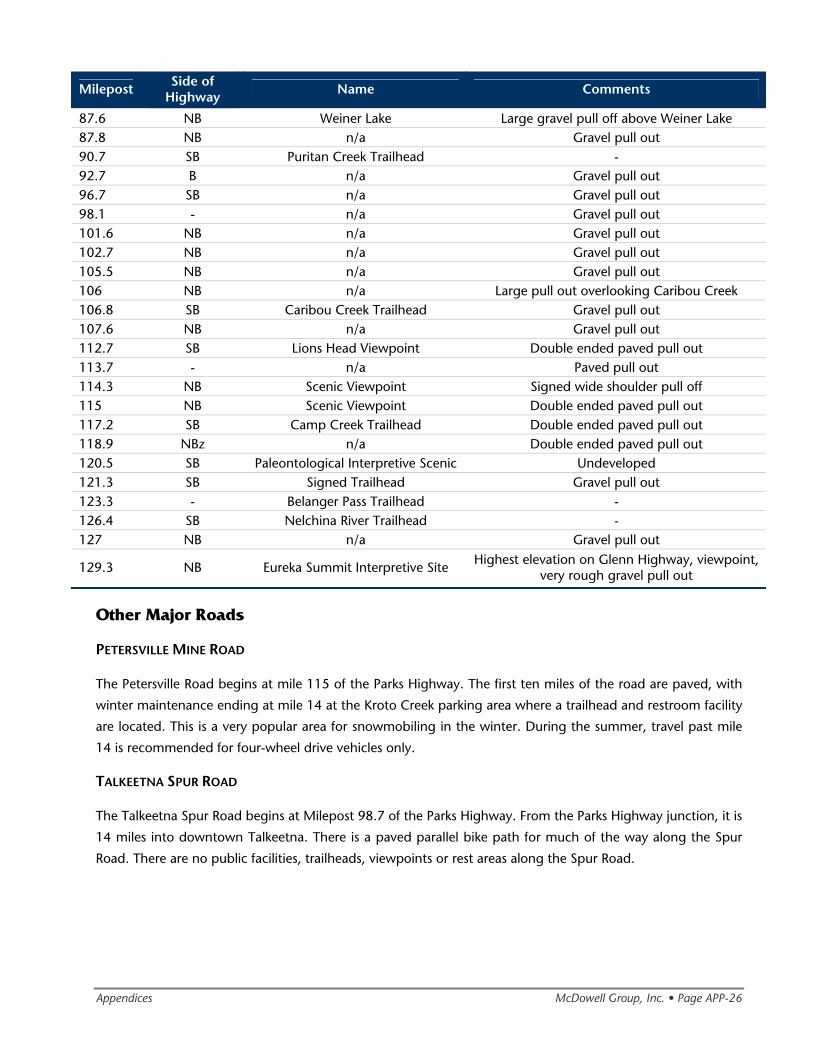

ROAD SYSTEM ENHANCEMENTS

The primary need in the region is restrooms, which are ideally placed every 40 to 50 miles along the road

system. The study also recommends improvements to a number of scenic viewpoints along the Glenn

Highway and upgrading the Denali Highway (which will promote a circular travel pattern and prolong visitor

stays in the region).

Tourism Infrastructure Needs Study: Executive Summary McDowell Group, Inc. • Page ES-6

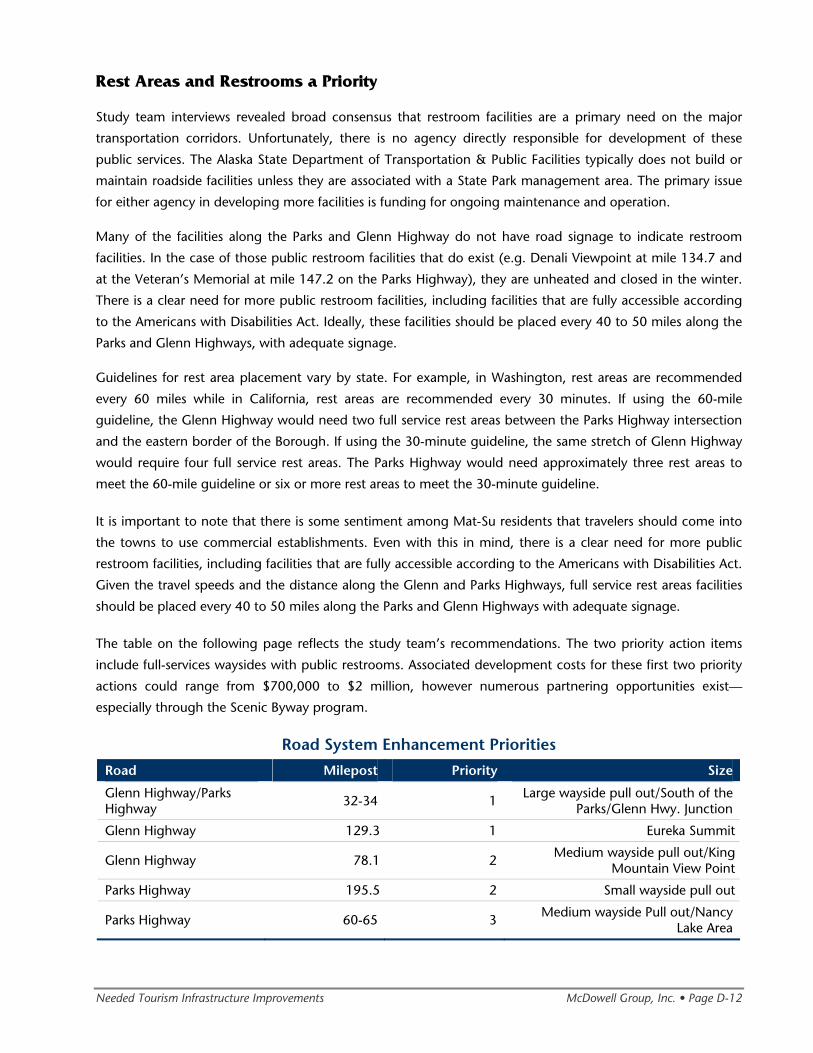

• Priority wayside and restroom areas include the following:

o Glenn Highway/Parks Highway intersection, mile 32-34

o Glenn Highway, mile 129.3

o Glenn Highway, mile 78.1

o Parks Highway, mile 195.5

o Parks Highway, mile 60-65.

• The study team estimated $500,000 to $1 million in annual investment, which could wholly fund

one or two waysides each year or support an accelerated program with partners.

o Development costs for individual wayside improvements, complete with restrooms and other

amenities can range from $350,000 to $1 million depending on the site, size, enhancements,

and current condition. Ongoing maintenance can be $30,000 to $75,000 per location.

o The amount invested by the Borough could be much more modest, depending on grants

and partners.

o Costs for the Denali Highway upgrade were not explored, as this longer-term consideration

would need to be explored with the State of Alaska, Denali Borough, and other parties.

• Assuming a systematic approach to road system enhancements, the region has potential for

considerable market growth.

o New annual room nights associated with road system enhancements are estimated between

13,000 and nearly 24,000. New visitor spending is estimated between $2.2 and $3.8 million

annually.

o Denali Highway improvements could result in another 2,000 to 4,000 overnights from tour

packages and $600,000 to $1.2 million annually.

TRAIL SYSTEM ENHANCEMENTS

While the region boasts a trail system of more than 2,000 miles and many outstanding attributes, the study

revealed a number of urgent needs. Priority areas included improved trailheads, restrooms, and signage.

• The following list is roughly prioritized, based on current condition and estimated usage:

o Point MacKenzie – Existing trailhead will eventually be consumed by port development.

Relocate trailhead/parking area approximately one mile north on Point MacKenzie Road and

install restrooms. Provides access to Figure Eight Lake, Flathorn Lake, Susitna River and

beyond.

o Ayrshire Road – Existing trailhead provides access to Figure Eight Lake, Flathorn Lake trail

system, Susitna River and beyond. Restrooms need to be installed.

o West Papoose Twins Road – Construct new trailhead during upgrade of road. Install

restrooms. Provides access to Crooked Lake Trail, Iron Dog Trail, Susitna River and beyond.

o North Crystal Lake Road – Expand existing trailhead. Install restrooms. Provides access to

Willow area trails.

o Willer Kash Road – Expand existing trailhead. Install restrooms. Provides access to Hatcher

Pass trail system, Kashwitna area trails.

Tourism Infrastructure Needs Study: Executive Summary McDowell Group, Inc. • Page ES-7

o Parks Highway MP 105 – Expand existing trailhead/parking area (possibly relocate short

distance to the north to get off the road). Install restrooms. Provides access to Trapper Lake-

Amber Lake trail system, Trapper Creek trail system.

o Petersville Road MP 4 – Construct new trailhead/parking area. Install restrooms. Provides

access to Petersville-Trapper Creek trail system, Denali State Park trails.

o Butte Pavilion Parking Area – Grade to level out. Install restrooms. Provides access to Jim

Creek, Knik River and Knik Glacier.

o Wendt Road – Expand existing parking area. Install restrooms. Provides access to Matanuska

Moose Range trail system.

o Sutton/Coyote Lake – Expand parking area. Replace damaged restroom. Provides access to

Sutton area trails.

o Kings River – Expand existing parking area. Install restrooms. Provides access to Kings River,

Young Creek and Red Mountain.

o Purinton Creek – Install restrooms. Provides access to Purinton Creek and Boulder Creek area

trails.

o France Road (CMT) – Develop future trailhead to coincide with trailhead move in case the

CMT unit is not moveable. Install single restroom.

o Matanuska Peak Trailhead – Install single restroom.

o Pioneer Ridge Trailhead – Replace outhouse with single restroom.

o Matanuska River Park – Install one restroom on back parking lot.

• The study also recommends an update to the trail plan to inventory and map all the trails in the

region and designate usage, design standards, and responsibility for maintenance. The planning

process will facilitate partnerships and potential funding.

• Continued trail system development is also important, as the region has untapped potential for new

or enhanced trail systems for hikers, equestrians, snow machine riders, and cross-country skiers.

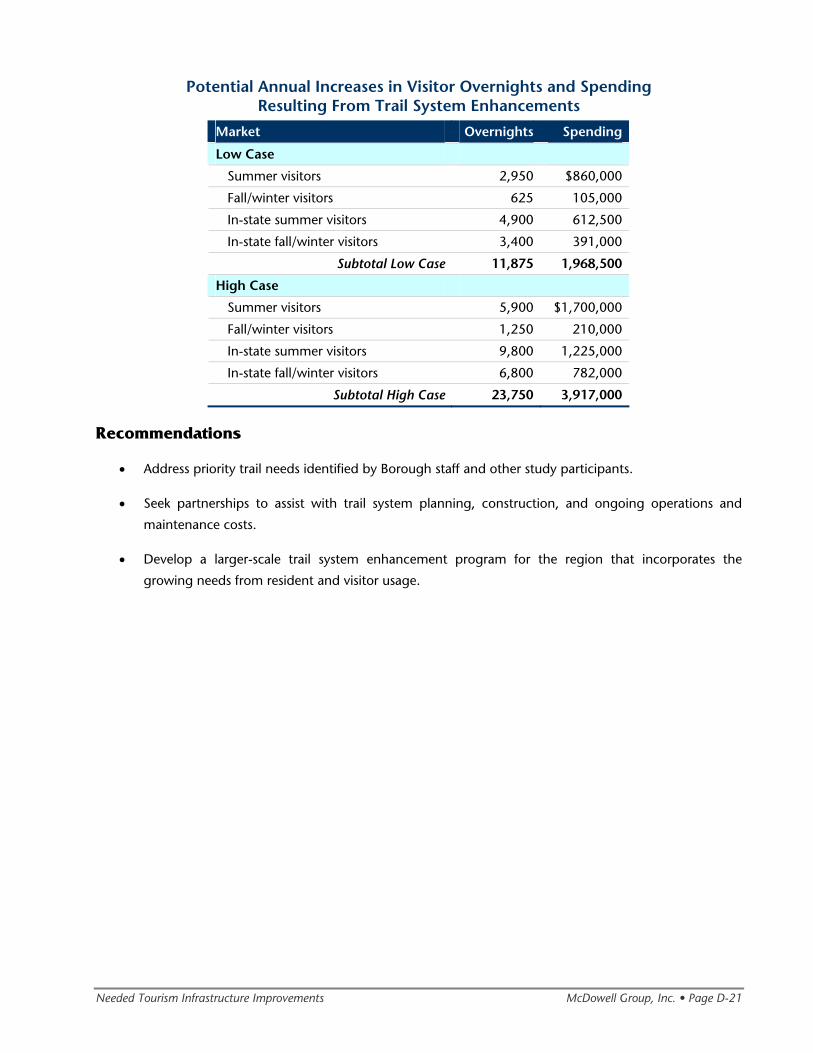

• The study team estimated $300,000 to $500,000 in annual investment, which could wholly fund one

to three trailheads each year or support an accelerated program with partners.

o Development costs for trailheads and related improvements, complete with restrooms and

other amenities, can range from $150,000 to $750,000 depending on the site, size,

enhancements, and current condition. Ongoing maintenance can be $10,000 to $50,000

per location.

o The trail plan update could range from $150,000 to $300,000, depending on the scope of

work and ability to partner.

o The Borough may wish to dedicate $50,000 to $150,000 for a grant program to support

planning, construction, and maintenance efforts that enhance the trail system.

• Considering the importance of outdoor recreation to in-state and out-of-state visitors, significant

market growth could result from an ongoing and systematic approach to the trail system.

o New room nights are estimated between 12,000 and nearly 24,000 annually. New visitor

spending is estimated between $2 and $3.9 million annually.

Tourism Infrastructure Needs Study: Executive Summary McDowell Group, Inc. • Page ES-8

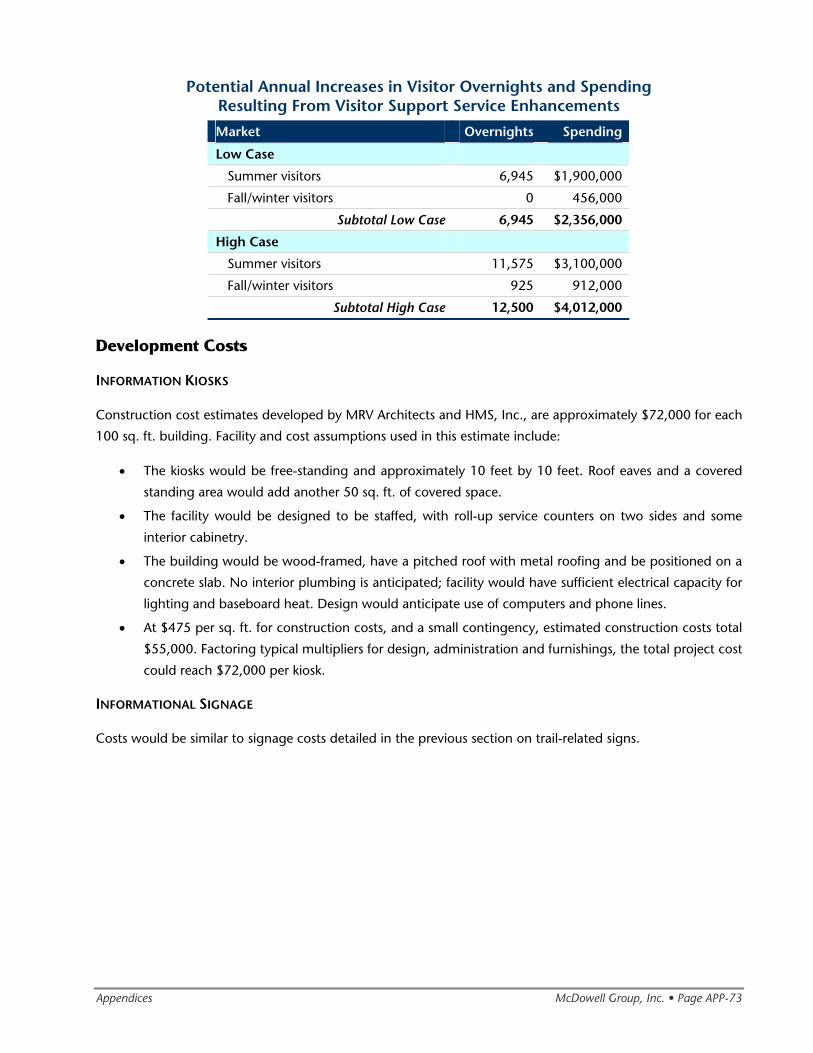

VISITOR SUPPORT SERVICES

Visitor center kiosks and signage should be found at major access points into the region. Past research shows

that this type of infrastructure can significantly enhance satisfaction. The study team also believes that length

of stay and spending can be influenced as well.

• Priority areas include the following:

o Glenn Highway is identified as the highest priority area and should be incorporated into any

new wayside development.

o Regional information should be made available at the new interpretive center and kiosks

developed through the South Denali Implementation Plan.

o Major airport and rail arrival points should be reviewed to ensure that information meets the

needs of the respective markets.

• A one-time expenditure of $75,000 to $180,000 should be sufficient to cover development of one or

two kiosks and signage upgrades.

• Increased visitor overnights are estimated between 7,000 and 12,500. New visitor spending estimates

range from $2.4 to $4 million annually.

Evaluation Criteria

The study team utilized eight evaluation criteria for recommending tourism infrastructure development

priorities. Ultimately, public policy makers may choose these or other criteria depending on the desired end

result of the borough’s tourism infrastructure investments.

1. Overall development costs

2. Potential economic returns on development costs

3. Distribution of economic benefits in the borough

4. Length of time to achieve market potential

5. Operating and maintenance costs

6. Impact on Mat-Su Borough revenues

7. Funding sources

8. Partnership opportunities

Tourism Infrastructure Priorities

Successful tourism growth is a synergistic result of a complex web of all the enhancements analyzed in this

report. For example, only focusing on trail system enhancements would not result in near the same benefits

as simultaneous development of road, trail and visitor support service enhancements. This makes forecasting

specific economic returns on each category very difficult. Even the relatively stand alone

conference/convention facility – provided it is centrally located and easily accessible – might have some long

term synergistic benefits by exposing meeting attendees to the more widely distributed road, trail and visitor

support services in the region.

Tourism Infrastructure Needs Study: Executive Summary McDowell Group, Inc. • Page ES-9

The Mat-Su Borough must first strategically decide the desired end result from their visitor industry

investment. Then investments can be chosen that yield those results. Fortunately, the substantial visitor base

that exists, the increased revenue from investments, and a potential increase in bed tax rates makes possible

investments in multiple priorities. The following are the study team’s recommendations based on the

apparent overall best interests of the Mat-Su Borough.

HIGHEST PRIORITY

The tourism investment priority that yields the highest positive return is visitor support services. The

investment required is relatively small and can be implemented quickly. Positive returns for the investment

should be realized in three to five years and the benefits from this investment will be spread throughout the

borough and throughout the year. Additionally, partnering opportunities exist with the Mat-Su Convention

and Visitors Bureau, private companies, and the State Department of Transportation & Public Facilities.

SECOND PRIORITIES

The second investment priorities are both road and trail system enhancements. As the immediate needs are

addressed, the study team recommends funding a more detailed enhancement plan for each program area. It

is assumed that enhancements can be implemented over a period of years allowing benefits to spread

throughout the borough and impact both summer and winter visitor seasons. There are good opportunities

to partner and leverage dollars with the National Scenic Byways Program, other federal and state programs,

as well as user groups and businesses.

THIRD PRIORITY

Development of a conference/convention center is considered a lower investment priority relative to the

positive investment returns on visitor support services, and road and trail system enhancements. Further,

most benefits will be localized around the center. However, a new meeting facility would provide new

spending in the non-summer months, and may provide increased room nights and spending earlier than

some other projects. Development of a conference/convention center offers some opportunities for

partnering.

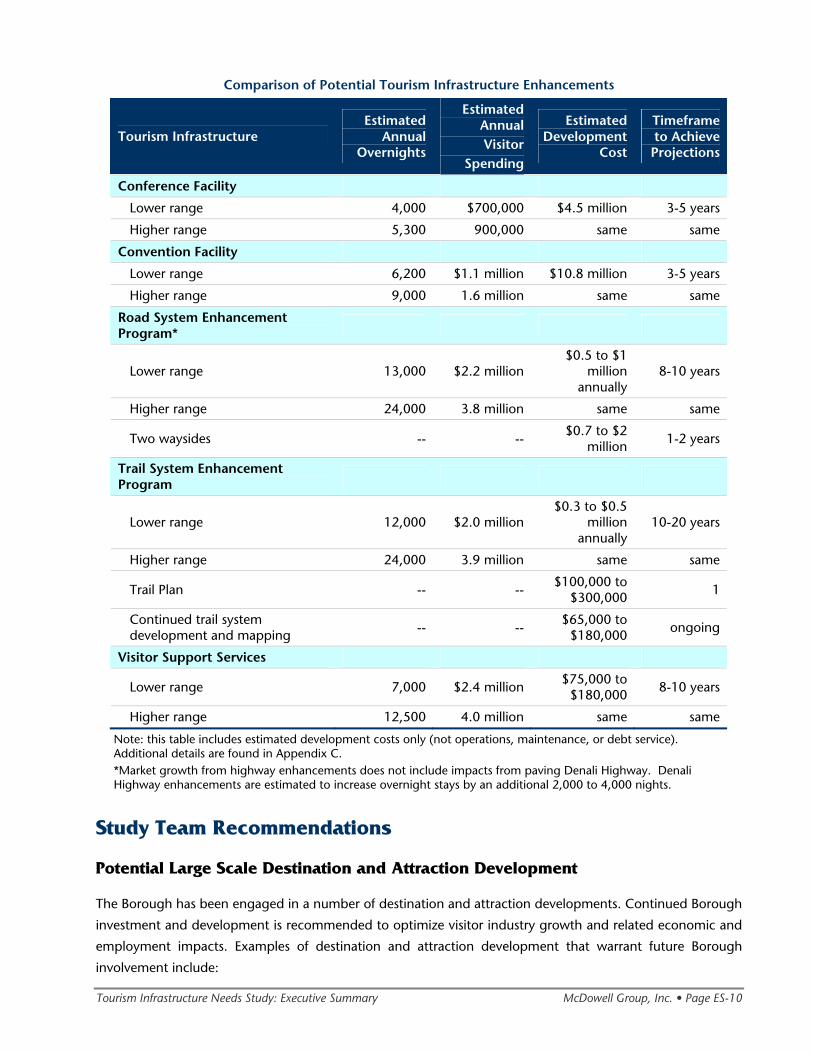

The comparison table on the following page provides a summary of estimated room nights, new visitor

spending, development costs, and timeframe needed to achieve projections. Operating and maintenance

costs are not expected to affect the outcome of this comparative analysis. They are minor when compared to

development costs and may be offset by grants and partnering.

Tourism Infrastructure Needs Study: Executive Summary McDowell Group, Inc. • Page ES-10

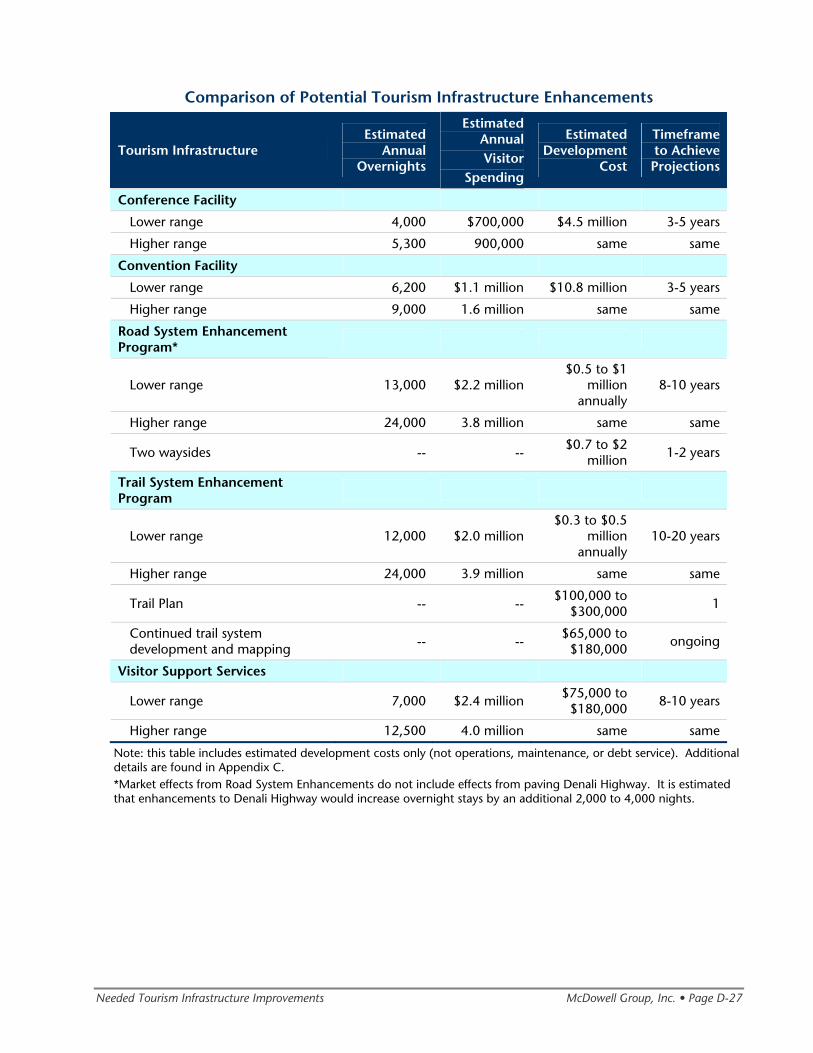

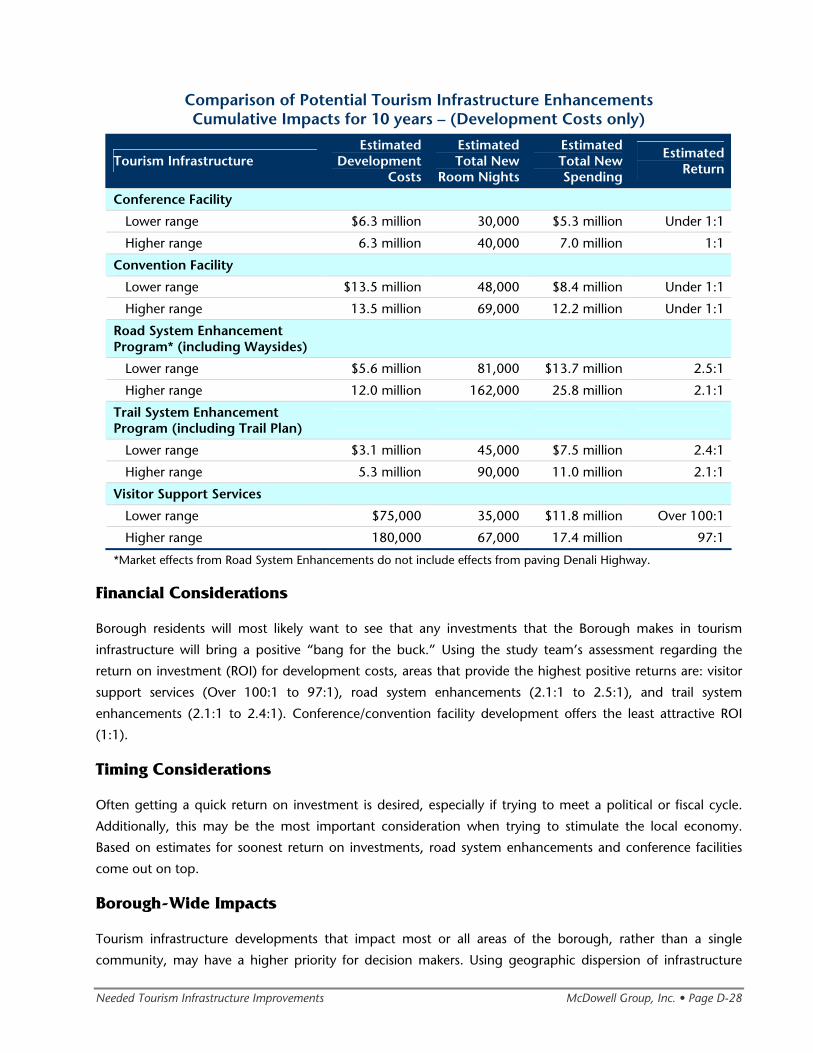

Comparison of Potential Tourism Infrastructure Enhancements

Tourism Infrastructure Estimated

AnnualOvernights

Estimated AnnualVisitor

Spending

Estimated Development

Cost

Timeframe to Achieve Projections

Conference Facility

Lower range 4,000 $700,000 $4.5 million 3-5 years

Higher range 5,300 900,000 same same

Convention Facility

Lower range 6,200 $1.1 million $10.8 million 3-5 years

Higher range 9,000 1.6 million same same

Road System Enhancement Program*

Lower range 13,000 $2.2 million$0.5 to $1

million annually

8-10 years

Higher range 24,000 3.8 million same same

Two waysides -- --$0.7 to $2

million 1-2 years

Trail System Enhancement Program

Lower range 12,000 $2.0 million$0.3 to $0.5

million annually

10-20 years

Higher range 24,000 3.9 million same same

Trail Plan -- --$100,000 to

$300,000 1

Continued trail system development and mapping -- --

$65,000 to $180,000 ongoing

Visitor Support Services

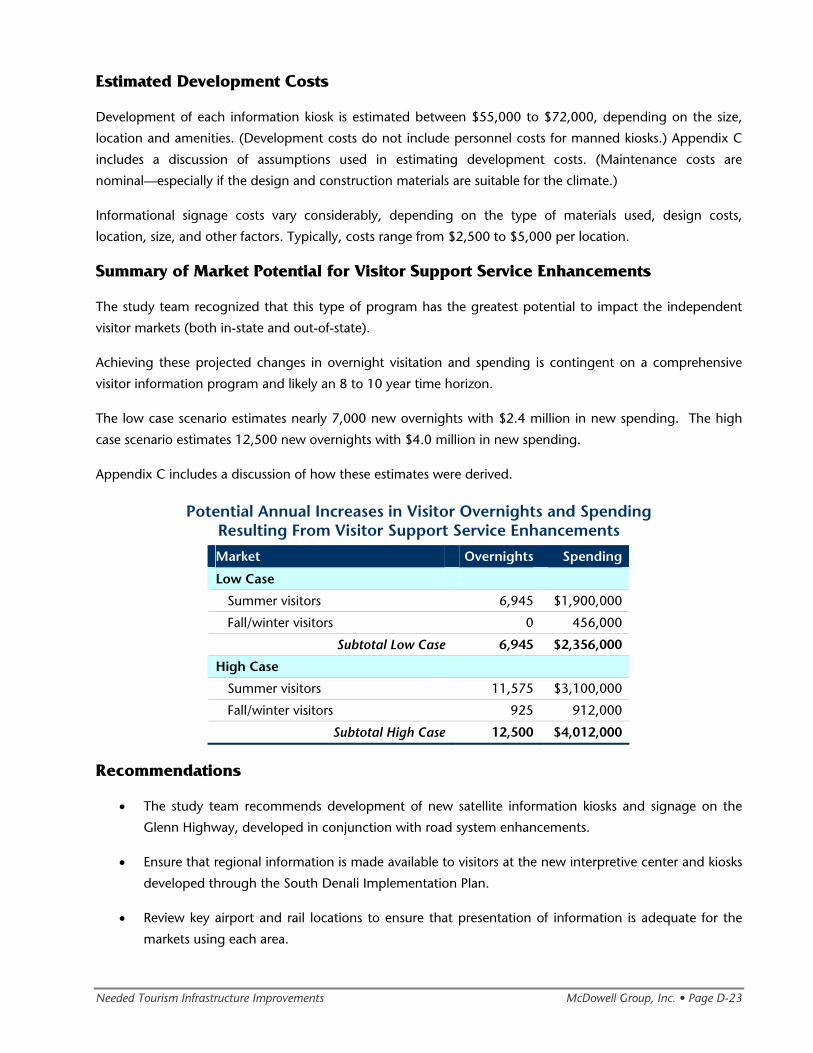

Lower range 7,000 $2.4 million$75,000 to

$180,000 8-10 years

Higher range 12,500 4.0 million same same

Note: this table includes estimated development costs only (not operations, maintenance, or debt service). Additional details are found in Appendix C. *Market growth from highway enhancements does not include impacts from paving Denali Highway. Denali Highway enhancements are estimated to increase overnight stays by an additional 2,000 to 4,000 nights.

Study Team Recommendations

Potential Large Scale Destination and Attraction Development

The Borough has been engaged in a number of destination and attraction developments. Continued Borough

investment and development is recommended to optimize visitor industry growth and related economic and

employment impacts. Examples of destination and attraction development that warrant future Borough

involvement include:

Tourism Infrastructure Needs Study: Executive Summary McDowell Group, Inc. • Page ES-11

• South Denali area. This area is expected to grow significantly as the South Denali Implementation Plan

unfolds. The Borough should remain involved in planning and infrastructure development.

• Hatcher Pass. The Borough should continue to develop this area as a visitor destination, as it has

significant long-term potential for virtually all visitor markets.

• Other examples include Independence Mine Tour, Glenn Highway Raptor Center, Palmer Hay Flats

Natural Science and Education/Community Center, and ongoing Trail Destination development.

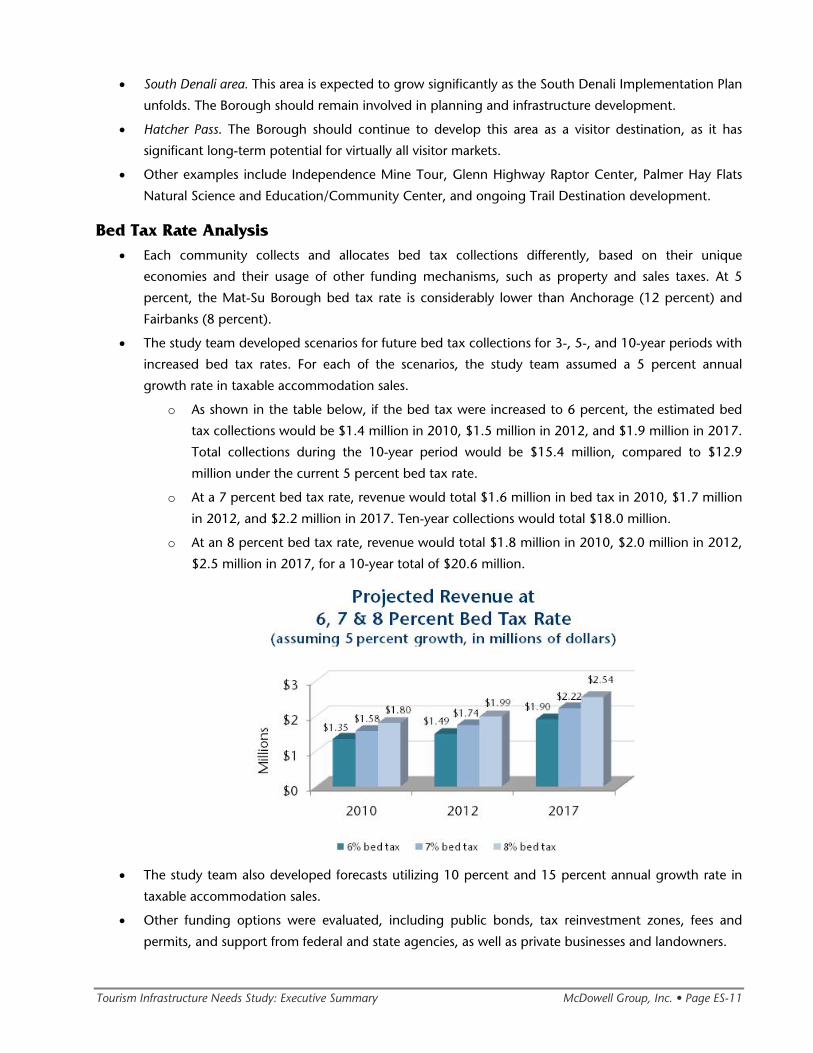

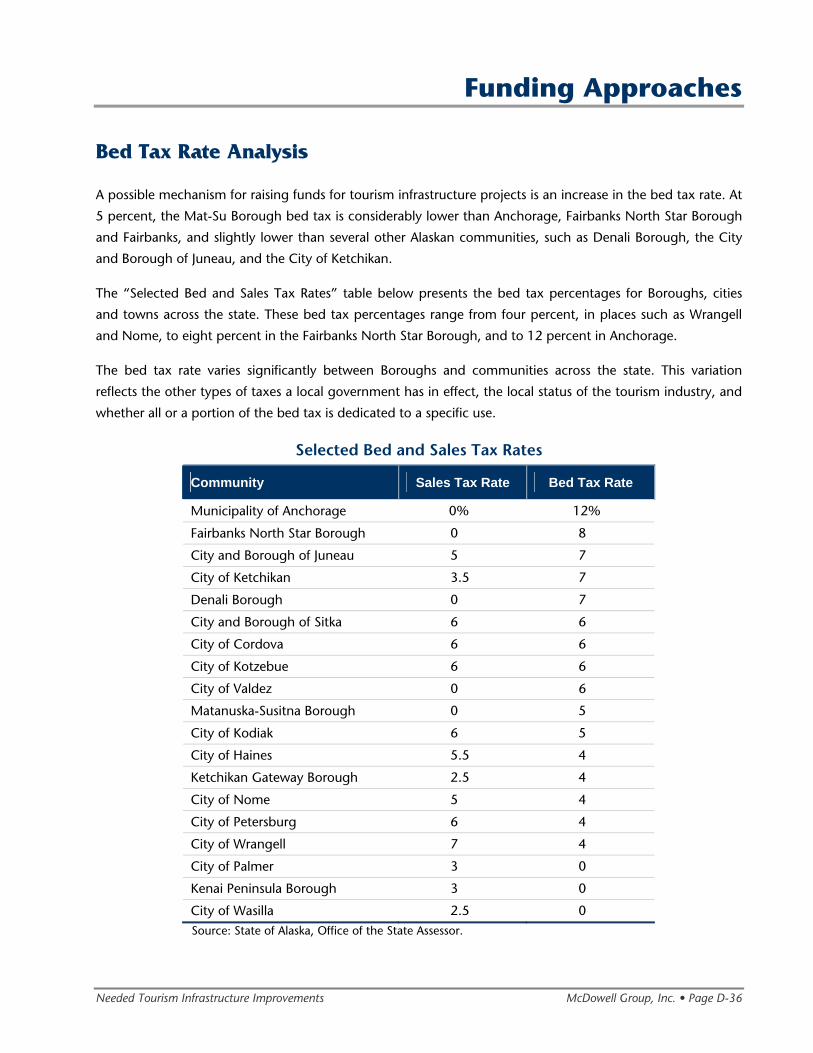

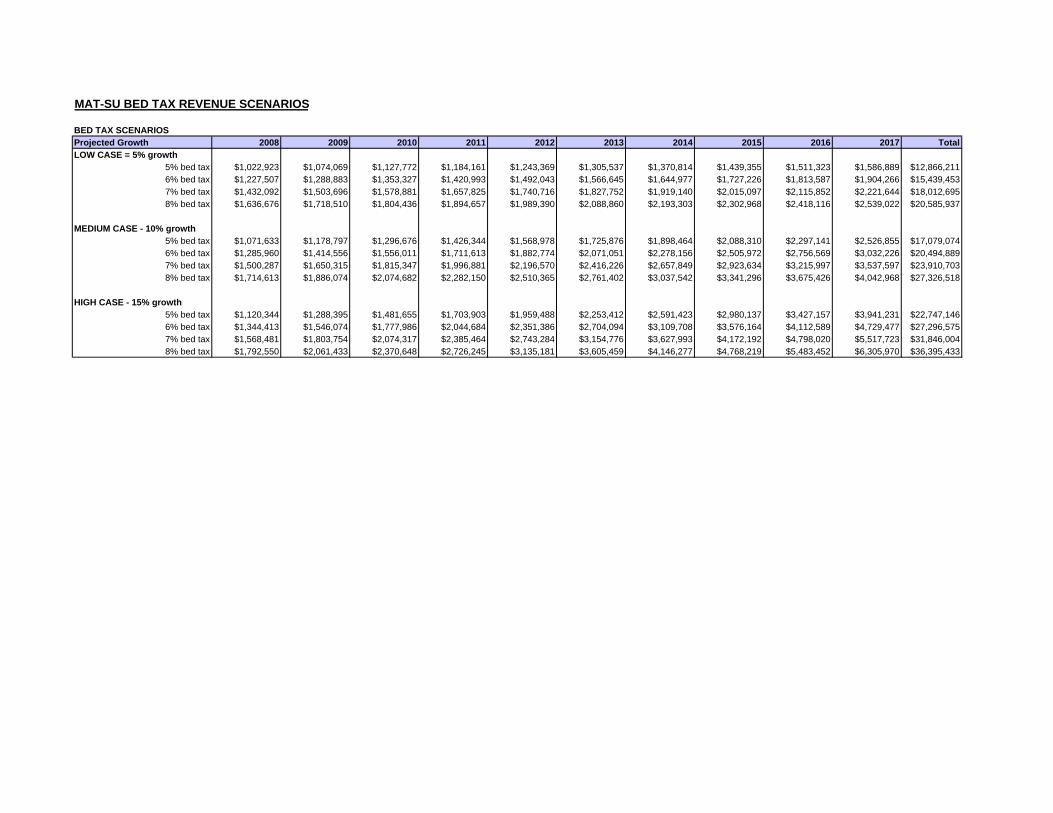

Bed Tax Rate Analysis • Each community collects and allocates bed tax collections differently, based on their unique

economies and their usage of other funding mechanisms, such as property and sales taxes. At 5

percent, the Mat-Su Borough bed tax rate is considerably lower than Anchorage (12 percent) and

Fairbanks (8 percent).

• The study team developed scenarios for future bed tax collections for 3-, 5-, and 10-year periods with

increased bed tax rates. For each of the scenarios, the study team assumed a 5 percent annual

growth rate in taxable accommodation sales.

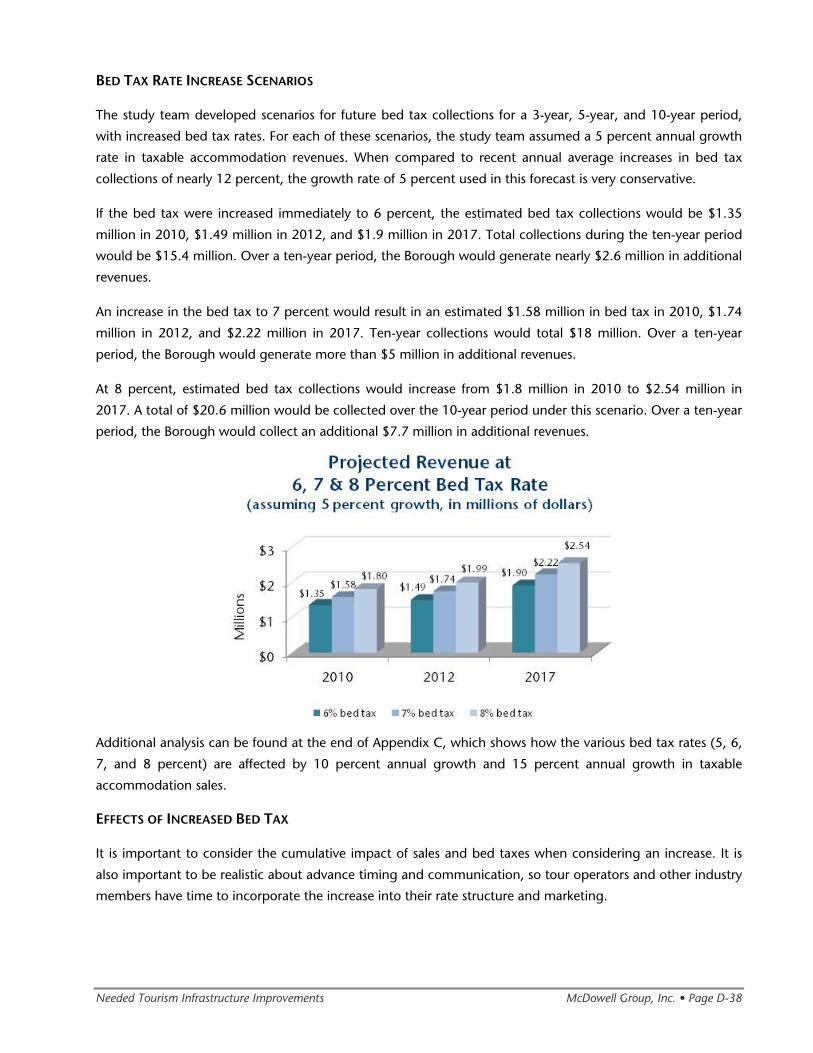

o As shown in the table below, if the bed tax were increased to 6 percent, the estimated bed

tax collections would be $1.4 million in 2010, $1.5 million in 2012, and $1.9 million in 2017.

Total collections during the 10-year period would be $15.4 million, compared to $12.9

million under the current 5 percent bed tax rate.

o At a 7 percent bed tax rate, revenue would total $1.6 million in bed tax in 2010, $1.7 million

in 2012, and $2.2 million in 2017. Ten-year collections would total $18.0 million.

o At an 8 percent bed tax rate, revenue would total $1.8 million in 2010, $2.0 million in 2012,

$2.5 million in 2017, for a 10-year total of $20.6 million.

• The study team also developed forecasts utilizing 10 percent and 15 percent annual growth rate in

taxable accommodation sales.

• Other funding options were evaluated, including public bonds, tax reinvestment zones, fees and

permits, and support from federal and state agencies, as well as private businesses and landowners.

Tourism Infrastructure Needs Study: Executive Summary McDowell Group, Inc. • Page ES-12

Focus Areas

Following is a summary of responses to the seven specific questions posed at the onset of the study.

• Yes, a convention center can contribute significantly to the economy, as it allows the region to attract

a market that it does not serve now. As summarized in the Needed Improvements section, a smaller

conference facility could attract between $700,000 and $900,000 annually in meeting-related

business. A larger convention facility could attract $1.1 to $1.6 million annually.

• The study team recommends construction of one larger facility rather than several small facilities if

this concept is pursued.

• Convention facilities will bring people to the valley for both overnight and day trips. The nature of

the meeting and number of attendees from outside the Anchorage area will influence travel patterns.

• All the tourism investment developments recommended in this study will contribute to overnight

stays. As shown in the Comparison of Tourism Investment table, road and trail system enhancements

have the greatest potential.

• It is economically better to locate a convention facility along the road system, as access to

accommodations, catering, and technical support are critical factors for success.

• Improved signage and restroom facilities greatly contribute to the tourism experience and economy.

• Compared to other areas, it makes sense to increase the bed tax. The study team believes that an

increase to 6 or 7 percent would be readily accepted by residents and the tourism industry. Is it

possible to increase the tax higher, but this should be approached with an educational campaign to

show what the additional funding will be designated for.

Tourism Partnering Opportunities • The study team provides a discussion of partnering trends as they relate to tourism infrastructure

development. Public/private partnerships and various incentive programs have emerged as

mechanisms to support the development of tourism infrastructure.

• There is no single model that works for public/private partnerships. Rather, partnerships are

structured in a variety of ways and can be as varied as the projects and organizations involved.

Usually these partnerships are created through contractual agreements between a public agency or

agencies, for-profit corporations and/or non-profit corporations or user groups. More often than not,

various investment incentives are included in the partnership, such as:

o Financial incentives in the form of government grants or loans from its own resources such as

special taxes, sale of revenue bonds, legislative appropriations (local, state or federal), etc.;

o Quasi-financial incentives in the form of loan guarantees, subsidies, or differential grants that

bridge the gap between official and commercial lending rates;

o Fiscal incentives, such as tax credits, enterprise zones, special districts, workforce incentive

programs, etc.; and

o Other incentives such as planning, management assistance, business development support,

or other technical assistance.

• The study team assessed each tourism infrastructure enhancement priority and then suggested

avenues for public and private partnering.

Tourism Infrastructure Needs Study: Executive Summary McDowell Group, Inc. • Page ES-13

Conclusions for Tourism Infrastructure Development

INVESTMENT DOLLARS

The Mat-Su Borough has significant opportunity, through increasing bed tax rates and market growth, to

generate substantial investment dollars for tourism infrastructure enhancements.

INFRASTRUCTURE SYNERGY

While visitor support service enhancements may have the best prospect for return on investment, the most

substantial tourism growth will occur through the synergistic effects of simultaneous development of visitor

support services, and highway and trail enhancements.

ECONOMIC ENHANCEMENT

Since a significant portion of Mat-Su’s visitor volume is short-stay through-traffic, infrastructure

enhancements should be successful in extending visitor’s time in the borough and creating economic benefits

as a result.

CAREFUL PLANNING

Conference and convention facilities rarely are profitable in their own right, so the location, sizing, and

operating efficiency of such facilities must be carefully planned.

PARTNERING LEVERAGE

Through partnering, the Mat-Su Borough’s investment dollars can be leveraged for much greater return.

A PROMISING FUTURE

Overall, the Mat-Su Borough has a promising future for tourism development, due to three major

contributing factors. First, the Mat-Su Borough has significant potential to increase its investment dollars.

Second, most infrastructure enhancements evaluated in this study will yield positive returns. Third, market

growth in both in-state and out-of-state markets has a positive outlook and the Mat-Su Borough is in a prime

position to capitalize.

Introduction and Methodology

Introduction and Methodology McDowell Group, Inc. • Page IM-1

Introduction and Methodology

The Matanuska-Susitna Borough contracted with the McDowell Group project team to develop an

independent study of the regional visitor industry. The primary purpose of the study was to identify

infrastructure development opportunities that would increase overnight stays in the Mat-Su region, enhance

economic and employment opportunities for residents, and improve the experience for in-state and out-of-

state visitors.

Study Team Overview

The study was led by McDowell Group, drawing on project management and staff support from the

company’s Anchorage and Juneau offices. Anchorage-based Boutet Company contributed to the Assessment

of Existing Infrastructure and final analysis and recommendations—particularly in the area of transportation

and trail system enhancements. Seattle-based Klugherz & Associates participated in the initial site visit and

identification of infrastructure needs at each stage of the study. Klugherz & Associates also led the project

team’s efforts in exploring partnering opportunities for each development recommendation. Juneau-based

MRV Architects supported the project team by developing estimates of construction and other capital cost for

the conference facilities.

Methodology

Shortly after the commencement of the project, the study team met with the Borough’s Economic

Development Director to refine the scope of the project and identify key contacts. Study team members from

McDowell Group and Klugherz & Associates also conducted a three-day site visit, which provided an

opportunity to personally experience key infrastructure in the borough, and conduct interviews with visitor

industry representatives, business owners, and other government officials.

Concurrently, the study team began compilation of information needed to develop an assessment of the

region’s existing tourism infrastructure. To supplement publicly available data and facility information, the

study team conducted interviews with industry experts, property and land managers, and Borough and

community government officials. (A list of project contacts, data sources, and other resources can be found in

the Appendix.) The team also reviewed available State, Borough and community comprehensive plans, land

use plans, transportation plans, and other documents referencing the need or goals to improve any

component that affects tourism infrastructure in the borough. Finally, the study team used its own industry

expertise to further assess the adequacy of current infrastructure.

Report Organization

GEOGRAPHIC OVERVIEW

This section provides a brief description of the geographic, scenic and recreational attributes in the region. It

also provides a short description of the five unique regions within the borough as defined by the Mat-Su

Convention and Visitors Bureau.

Introduction and Methodology McDowell Group, Inc. • Page IM-2

BASE CASE TOURISM INFRASTRUCTURE DESCRIPTION

This section includes detailed information regarding existing infrastructure and gaps including

accommodations, meeting facilities, sports facilities, other public venues, parks, campgrounds, boat launches,

trails and transportation.

MAT-SU VISITOR MARKETS

The study includes an analysis of the region’s current in-state and out-of-state visitor markets including visitor

volume, spending, locations visited, and activities within the borough. The section also includes a market

outlook discussion and implications for regional tourism infrastructure.

ASSESSMENT OF TOURISM INDUSTRY VALUE

The study team examined different measures of tourism industry value, such as bed tax receipts, state

employment income figures, number of tourism businesses, etc. This section also includes an estimate of

direct, indirect and induced economic benefits and a discussion of the intrinsic value of tourism.

NEEDED TOURISM INFRASTRUCTURE IMPROVEMENTS

This portion of the study examines how potential infrastructure improvements could enhance the regional

tourism industry by enhancing the visitor experience, increasing the number of overnight stays, and

contribute the most to overall economic return. This chapter also includes a discussion of large destination

and attraction projects in the region and funding approaches.

FOCUS AREAS FOR TOURISM IMPROVEMENT

This portion of the study addresses specific questions provided by the Borough related to infrastructure value

and need.

TOURISM PARTNERING OPPORTUNITIES

The study team provides a summary of national trends in partnering, including ways in which tourism

entities, government, private land owners and others can partner to increase the effectiveness of public

dollars spent on tourism development.

APPENDICES

There are four Appendix sections included at the back of the report.

APPENDIX A

Appendix A contains information that supports the Base Case Tourism Infrastructure Description section. This

appendix provides tables and text describing current tourism-related infrastructure in the borough.

Information on accommodations, sports facilities, Alaska State fairground facilities, museums, campgrounds,

parks, recreational areas, trails and transportation infrastructure in the region can be found in Appendix A.

Introduction and Methodology McDowell Group, Inc. • Page IM-3

APPENDIX B

Supplemental information from the Mat-Su Visitor Markets section of the report can be found in Appendix B.

This appendix includes more detailed information about special events and two significant attractions: the

Alaska State Fair and Hatcher Pass.

APPENDIX C

Appendix C includes details regarding size, construction cost, and other information that supports the

Needed Tourism Infrastructure Improvements section. For example, supplemental information is provided on

potential market increases from meeting facilities, road system enhancements and trail system enhancements,

as well as development costs.

APPENDIX D

Appendix D includes a list of project contacts and data and information sources. A number of individuals

were contacted and provided information that contributed to the development of the project. Additionally, a

number of sources were used to obtain visitor volume estimates, expenditure estimates and information

about visitors’ activities within the Mat-Su region.

APPENDIX E

Appendix E includes Montana Tourism Infrastructure Investment Program Guidelines 2007.

Geographic Overview

Tourism Infrastructure Needs Study: Geographic Overview McDowell Group, Inc. • Page GO-1

Geographic Overview

The Matanuska-Susitna Borough (commonly referred to as the Mat-Su Borough) is the fastest growing area of

Alaska and the nation’s third-fastest growing county/borough. It is bordered by Denali Borough to the north

and Anchorage to the south. The majority of the borough’s 80,000 residents live in (or near) the cities of

Palmer and Wasilla. The balance of the population is distributed within approximately 20 unincorporated

communities throughout the borough. The larger population centers of Houston, Big Lake, Willow, Sutton,

Trapper Creek and Talkeetna are located close to the state highways that transect the region.

Areas of the Mat-Su Borough can be reached by road, railway and air; this high level of accessibility is critical

to the success of the borough’s tourism industry. The George Parks Highway provides access to state and

national parks, and other destinations to the north. The Glenn Highway provides access to the southeastern

section of the borough, including the Matanuska Glacier and the Chugach Mountains. The Alaska Railroad

provides service between Anchorage and Fairbanks, with regularly scheduled stops in Wasilla and Talkeetna.

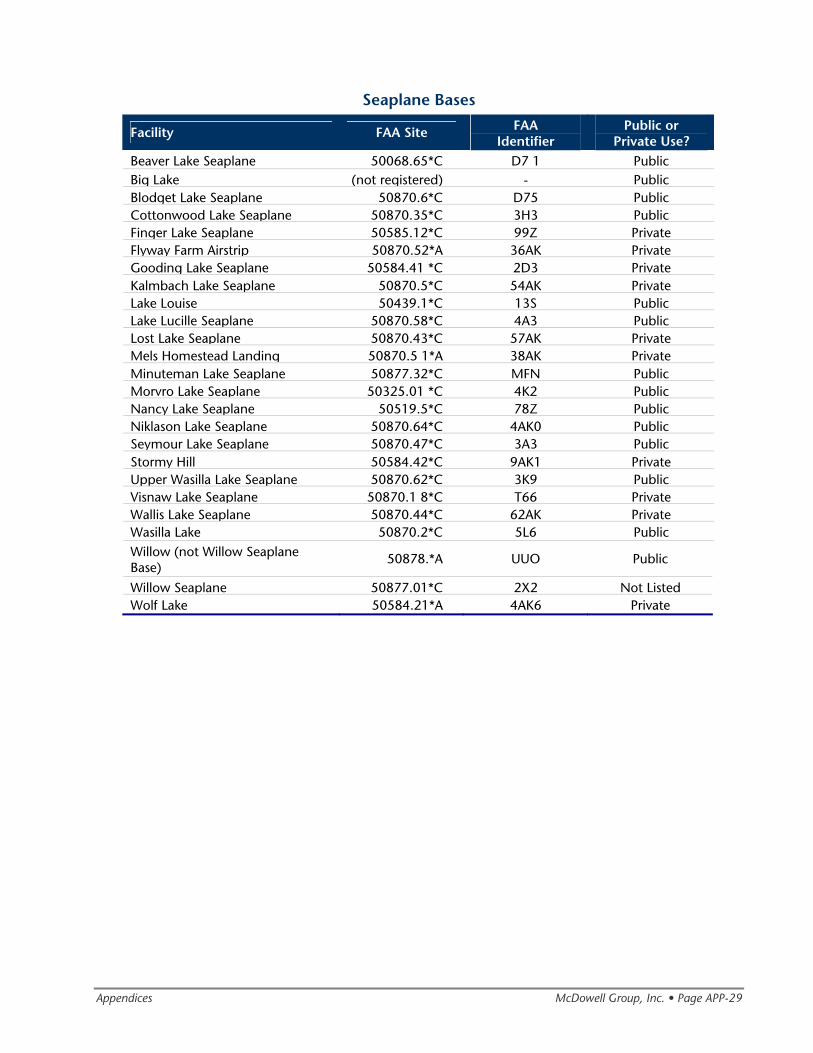

In addition to the airports in Palmer, Talkeetna and Wasilla, the region also offers several public and private

airfields and floatplane bases.

The Mat-Su Borough encompasses approximately 25,000 square miles of mountains, lakes, rivers, streams,

rolling lowlands and valleys. There are 24 state parks and recreation areas, including Independence Mine

State Historic Park at Hatcher Pass, which attracts visitors year-round. Denali State Park is located on the

borough's northern edge. Denali National Park, home to North America’s highest mountain, is one of Alaska’s

most popular attractions. The borough shares this National Park with the Denali Borough, with about 30

percent of the National Park located in the Mat-Su Borough. These parks provide a variety of year-round

recreational activities for local residents, in-state residents and out-of-state visitors.

Popular summer activities for local residents and visitors include salmon, trout and grayling fishing, hunting,

boating, golfing, mountain climbing, kayaking, rafting, flightseeing, gold panning and horseback riding.

During the winter, recreational activities include skiing, snowshoeing, skating, dog sledding, ice fishing and

snowmobiling. Denali National Park, Denali State Park, Independence Mine State Historical Park and the areas

around Matanuska and Knik Glaciers are especially popular areas for hiking, skiing and camping.

The borough hosts the Iron Dog Snow Machine Race and the Alaska State Fair. Additionally, the famous

Iditarod Trail Sled Dog Race winds through the Valley each March. Thousands of visitors attend these events

each year. There are a number of heritage sites and museums in the region, including the Iditarod Park,

Independence Mine State Historical Park, Dorothy Page Museum, Sutton Alpine Historical Park and many

others.

The Mat-Su Convention and Visitors Bureau promotes the region’s scenic, historic and recreational attributes

to Alaska residents and a wide array of non-resident visitors. Additional marketing and visitor information

support is provided by several local chambers of commerce.

Tourism Infrastructure Needs Study: Geographic Overview McDowell Group, Inc. • Page GO-2

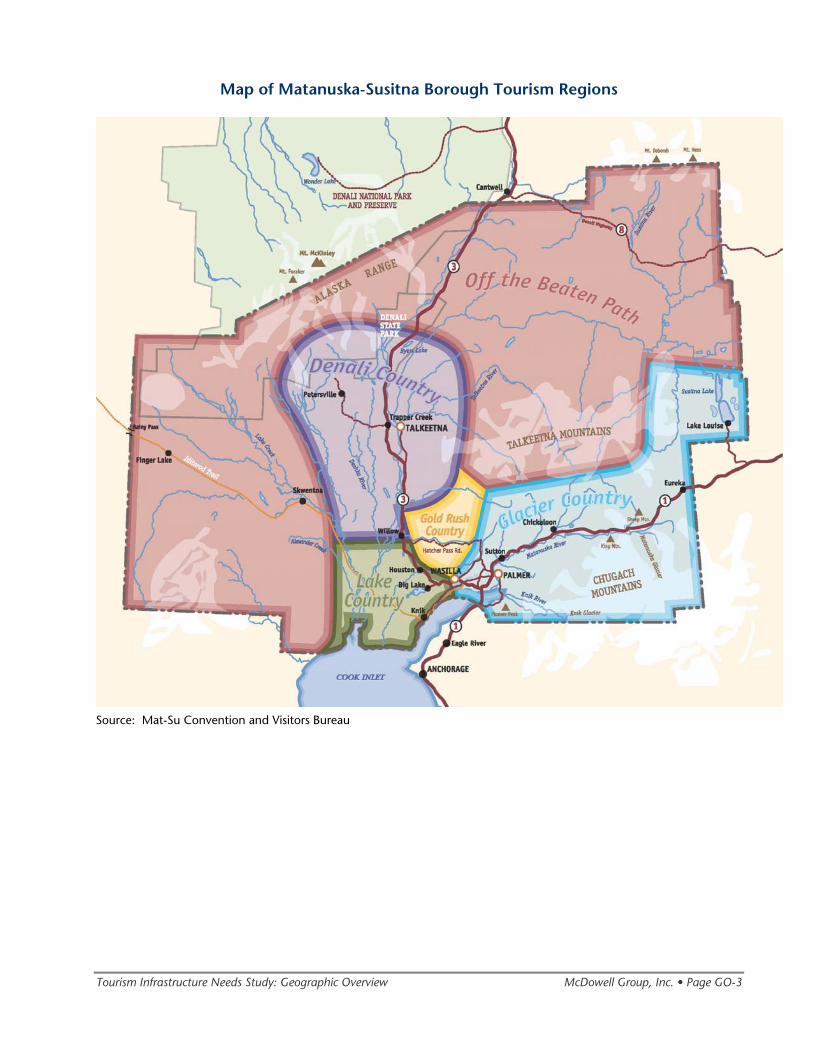

Visitor Regions To help visitors differentiate between the geographically diverse areas of the borough, the Mat-Su

Convention and Visitors Bureau developed five unique regions, which are briefly described below. These

regions are also used by the Bureau to define their accommodation and attraction locations.

• Glacier Country (Glenn Highway) -- the southeastern corner of the borough stretching northeast from

Wasilla to Lake Louise and Susitna Lake, including Wasilla, Palmer, Sutton, Chickaloon, Eureka and Lake

Louise. The Chugach Mountain Range borders to the south and the Talkeetna Range to the north. Many

glaciers can be seen from the Glenn Highway that runs along the Matanuska River.

• Gold Rush Country (Hatcher Pass) -- a southern section, including Independence Mine State Historic

Park at Hatcher Pass.

• Lake Country (Knik/Point MacKenzie, Big Lake) -- a small southern section along the Cook Inlet,

including many lakes and the communities of Knik, Big Lake and Houston. The Little and Big Susitna

Rivers, Yentna River and the Iditarod Trail winds through the area. The Parks Highway provides access to

the communities of Big Lake and Houston.

• Denali Country (Willow to Denali) -- in the middle of the borough, stretching north from Willow to

Denali State Park, including the communities of Willow, Talkeetna, Trapper Creek and Petersville. The

Parks Highway passes through Denali Country, providing access to these communities and the State Park.

• Off the Beaten Path (Roadless Portion of the Borough) -- the largest region of the borough,

encompassing a horseshoe-shaped swath of the southwest, north and northeast corner of the borough.

Thirty percent of Denali National Park is located in this region, as well as Denali State Park. The Parks

Highway provides access to these parks. The Denali Highway passes through the northeastern corner. The

Alaska Range stretches along the northern border and the Talkeetna Range stretches along the southeast

border.

(See map on the following page.)

Tourism Infrastructure Needs Study: Geographic Overview McDowell Group, Inc. • Page GO-3

Map of Matanuska-Susitna Borough Tourism Regions

Source: Mat-Su Convention and Visitors Bureau

Base Case Tourism Infrastructure

Description

Base Case Tourism Infrastructure Description McDowell Group, Inc. • Page A-1

Introduction

The Base-Case Tourism Infrastructure Description provides a description of the existing tourism

infrastructure in the Borough. For the purpose of this study, tourism infrastructure refers to developed

facilities that are used by visitors when they are traveling through and visiting the Mat-Su Borough.

The tourism infrastructure examined in this report is grouped into the following categories:

accommodations, meeting facilities used for conventions or conferences; sports facilities, such as ice

arenas, soccer or baseball fields; other public venues, such as the Alaska State Fair Grounds, performance

halls, museums, and visitor’s centers; parks campgrounds, boat launches and trails; transportation, such

as roads, railroads and airports; and public restroom facilities.

The following sections provide an analysis of each infrastructure category, assessing the types of facilities

available, quantity, condition, and challenges.

Base Case Tourism Infrastructure Description McDowell Group, Inc. • Page A-2

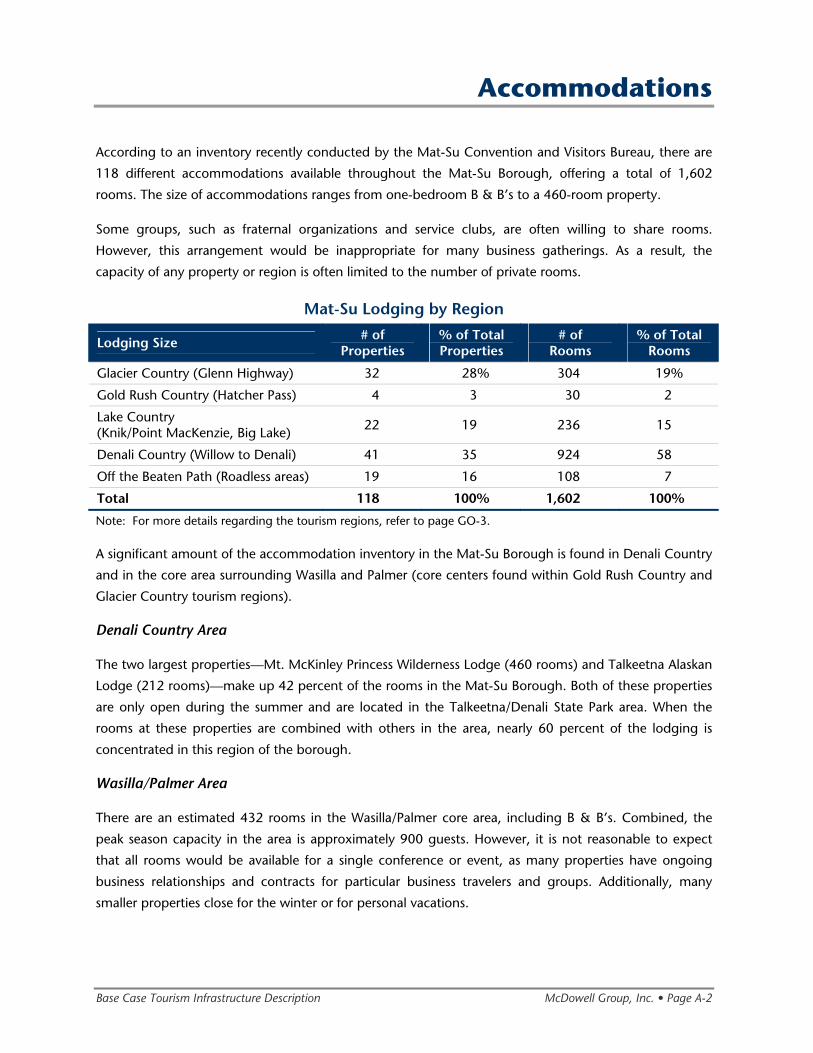

Accommodations

According to an inventory recently conducted by the Mat-Su Convention and Visitors Bureau, there are

118 different accommodations available throughout the Mat-Su Borough, offering a total of 1,602

rooms. The size of accommodations ranges from one-bedroom B & B’s to a 460-room property.

Some groups, such as fraternal organizations and service clubs, are often willing to share rooms.

However, this arrangement would be inappropriate for many business gatherings. As a result, the

capacity of any property or region is often limited to the number of private rooms.

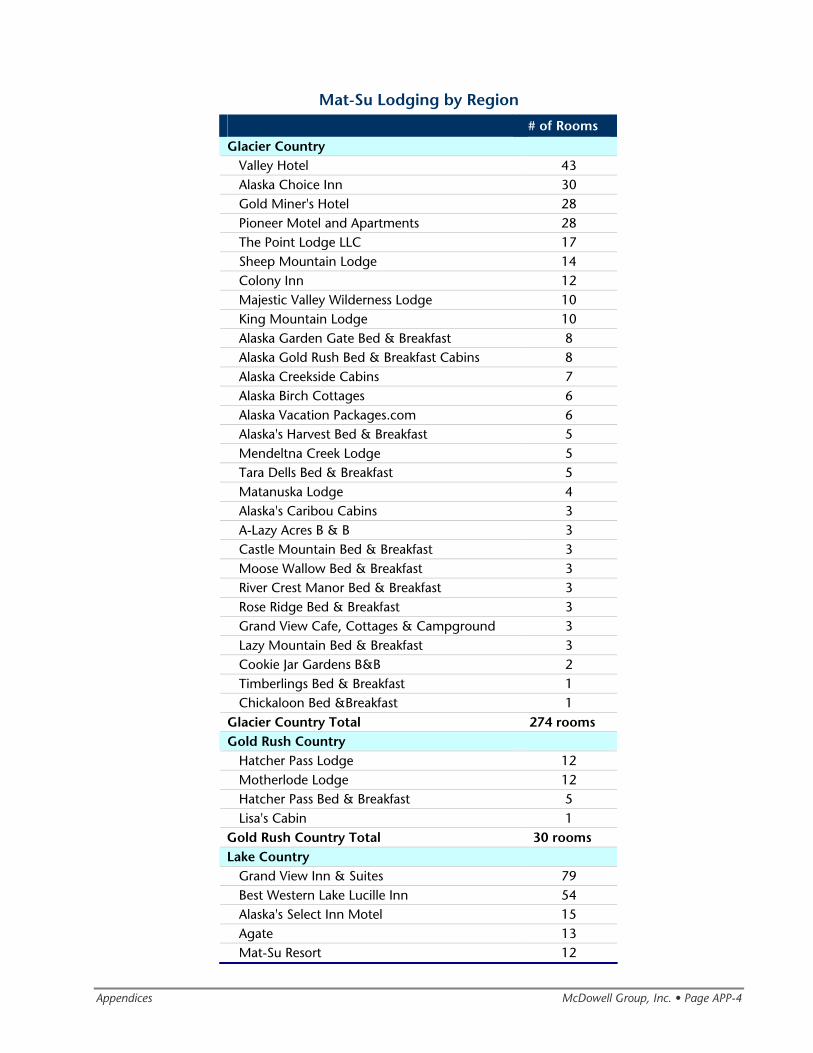

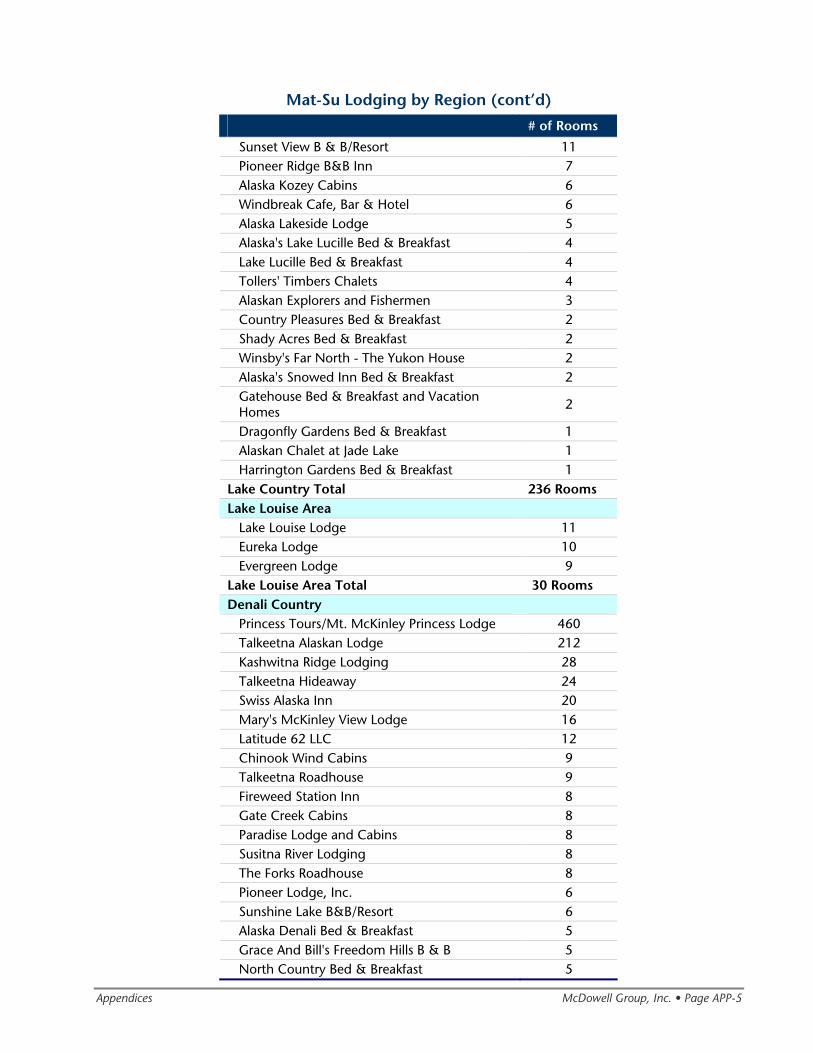

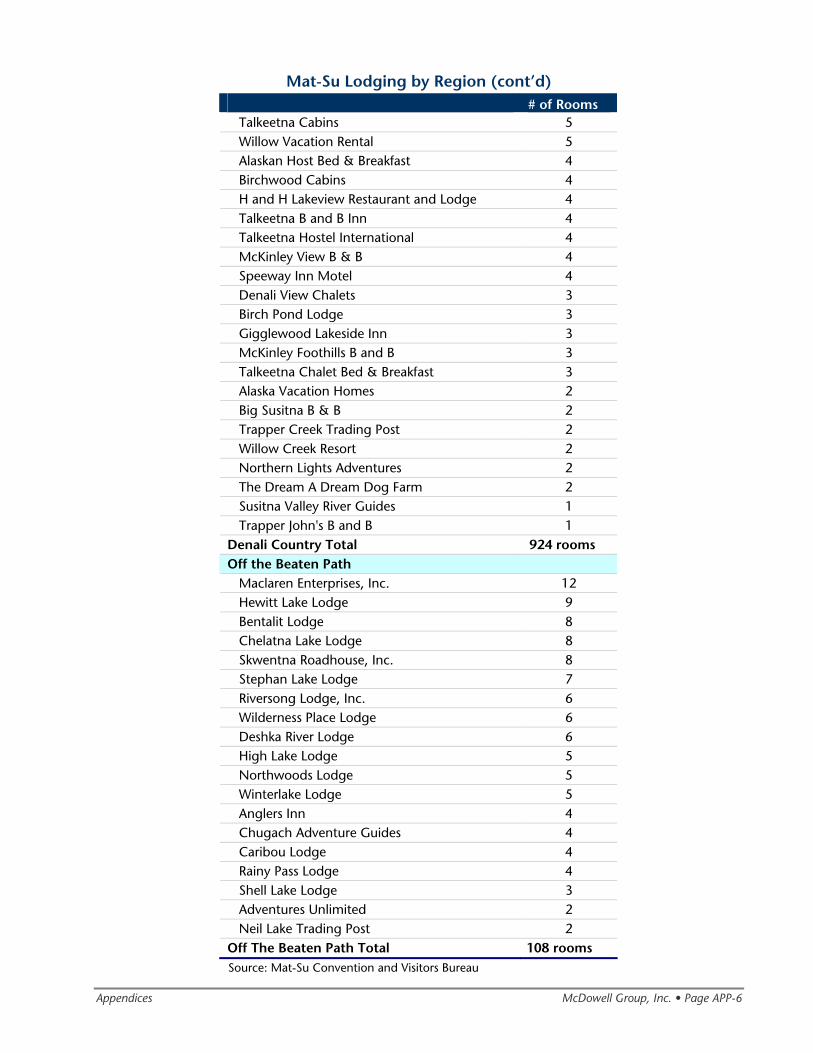

Mat-Su Lodging by Region

Lodging Size # of Properties

% of Total Properties

# of Rooms

% of Total Rooms

Glacier Country (Glenn Highway) 32 28% 304 19%

Gold Rush Country (Hatcher Pass) 4 3 30 2

Lake Country (Knik/Point MacKenzie, Big Lake) 22 19 236 15

Denali Country (Willow to Denali) 41 35 924 58

Off the Beaten Path (Roadless areas) 19 16 108 7

Total 118 100% 1,602 100%

Note: For more details regarding the tourism regions, refer to page GO-3.

A significant amount of the accommodation inventory in the Mat-Su Borough is found in Denali Country

and in the core area surrounding Wasilla and Palmer (core centers found within Gold Rush Country and

Glacier Country tourism regions).

Denali Country Area

The two largest properties—Mt. McKinley Princess Wilderness Lodge (460 rooms) and Talkeetna Alaskan

Lodge (212 rooms)—make up 42 percent of the rooms in the Mat-Su Borough. Both of these properties

are only open during the summer and are located in the Talkeetna/Denali State Park area. When the

rooms at these properties are combined with others in the area, nearly 60 percent of the lodging is

concentrated in this region of the borough.

Wasilla/Palmer Area

There are an estimated 432 rooms in the Wasilla/Palmer core area, including B & B’s. Combined, the

peak season capacity in the area is approximately 900 guests. However, it is not reasonable to expect

that all rooms would be available for a single conference or event, as many properties have ongoing

business relationships and contracts for particular business travelers and groups. Additionally, many

smaller properties close for the winter or for personal vacations.

Base Case Tourism Infrastructure Description McDowell Group, Inc. • Page A-3

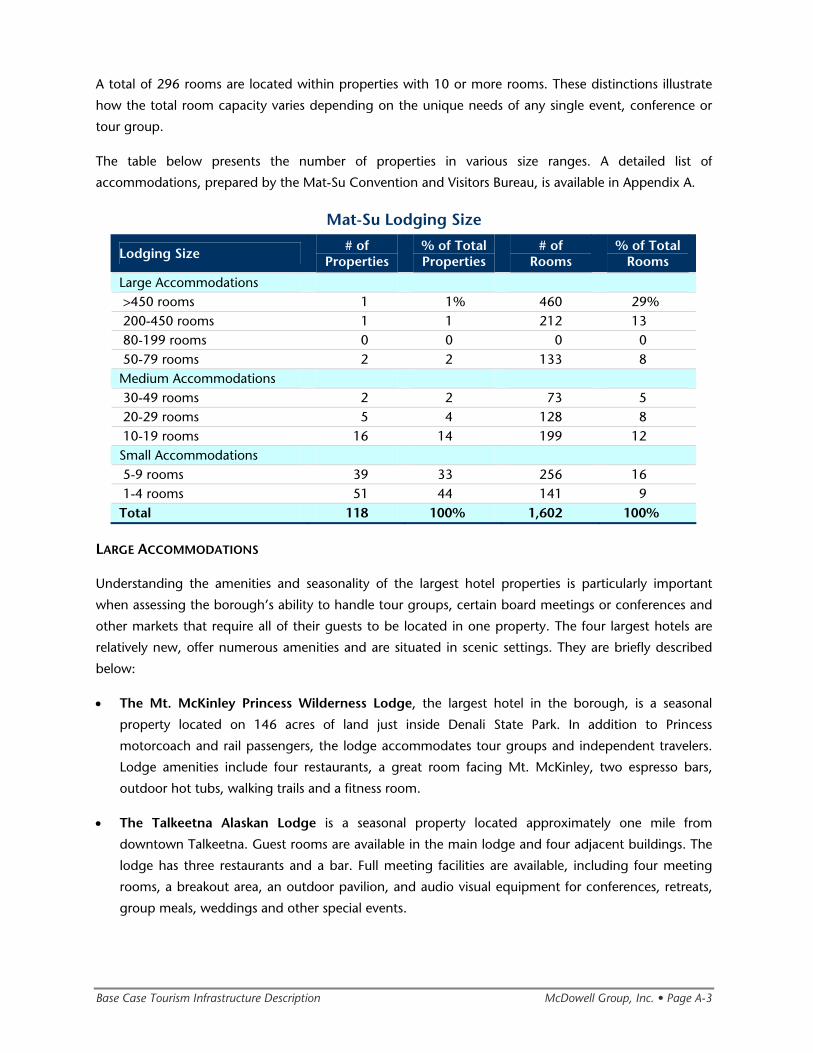

A total of 296 rooms are located within properties with 10 or more rooms. These distinctions illustrate

how the total room capacity varies depending on the unique needs of any single event, conference or

tour group.

The table below presents the number of properties in various size ranges. A detailed list of

accommodations, prepared by the Mat-Su Convention and Visitors Bureau, is available in Appendix A.

Mat-Su Lodging Size

Lodging Size # of Properties

% of Total Properties

# of Rooms

% of Total Rooms

Large Accommodations >450 rooms 1 1% 460 29% 200-450 rooms 1 1 212 13 80-199 rooms 0 0 0 0 50-79 rooms 2 2 133 8 Medium Accommodations 30-49 rooms 2 2 73 5 20-29 rooms 5 4 128 8 10-19 rooms 16 14 199 12 Small Accommodations 5-9 rooms 39 33 256 16 1-4 rooms 51 44 141 9 Total 118 100% 1,602 100%

LARGE ACCOMMODATIONS

Understanding the amenities and seasonality of the largest hotel properties is particularly important

when assessing the borough’s ability to handle tour groups, certain board meetings or conferences and

other markets that require all of their guests to be located in one property. The four largest hotels are

relatively new, offer numerous amenities and are situated in scenic settings. They are briefly described

below:

• The Mt. McKinley Princess Wilderness Lodge, the largest hotel in the borough, is a seasonal

property located on 146 acres of land just inside Denali State Park. In addition to Princess

motorcoach and rail passengers, the lodge accommodates tour groups and independent travelers.

Lodge amenities include four restaurants, a great room facing Mt. McKinley, two espresso bars,

outdoor hot tubs, walking trails and a fitness room.

• The Talkeetna Alaskan Lodge is a seasonal property located approximately one mile from

downtown Talkeetna. Guest rooms are available in the main lodge and four adjacent buildings. The

lodge has three restaurants and a bar. Full meeting facilities are available, including four meeting

rooms, a breakout area, an outdoor pavilion, and audio visual equipment for conferences, retreats,

group meals, weddings and other special events.

Base Case Tourism Infrastructure Description McDowell Group, Inc. • Page A-4

• Grand View Inn and Suites is located in Wasilla. Each unit has a kitchen equipped with full-sized

appliances. Hotel amenities include banquet and convention rooms, a restaurant and bar, a

swimming pool and fitness center.

• The Best Western Lake Lucille Inn is located in Wasilla. Hotel amenities include a restaurant,

lounge, lakeside gazebo, fitness club and meeting facilities. The onsite banquet facilities can

accommodate up to 350 people; however, the onsite banquet facilities have recently been closed.

MEDIUM ACCOMMODATIONS

Medium-size accommodations in the borough range from 10 to 50 rooms, and make up 20 percent of

total properties. On their own, each of the medium-sized properties can accommodate a small tour

group, meeting or retreat. The market for overnight accommodation in the borough is highly seasonal,

with the highest occupancy rates occurring in the summer. Several of the accommodations in this size

range close in the winter.

SMALL ACCOMMODATIONS

Small accommodations, ranging from one to nine rooms, make up the majority of properties in the

borough (76 percent). Many of the small accommodations in the borough are B & B’s, of which most

are spread along the Glenn and Parks Highways. These B & B’s range from high-end accommodations

with many amenities like jacuzzis, fireplaces, etc., to casual accommodations consisting of simple

bedrooms in family homes. Several smaller properties close for the winter. Those that remain open for

the winter attract visitors for skiing, snowmobiling and snowshoeing. For example, visitors to the Sheep

Mountain Lodge and the Matanuska Glacier Lodge along the Glenn Highway have access to groomed

cross country ski trails and opportunities to snowmobile and snowshoe in the Talkeetna mountain range.

Additionally, visitors to the Motherlode Lodge and Hatcher Pass Lodge in the Independence Mine State

Historic Park also have access to snowmobiling and cross country skiing.

Base Case Tourism Infrastructure Description McDowell Group, Inc. • Page A-5

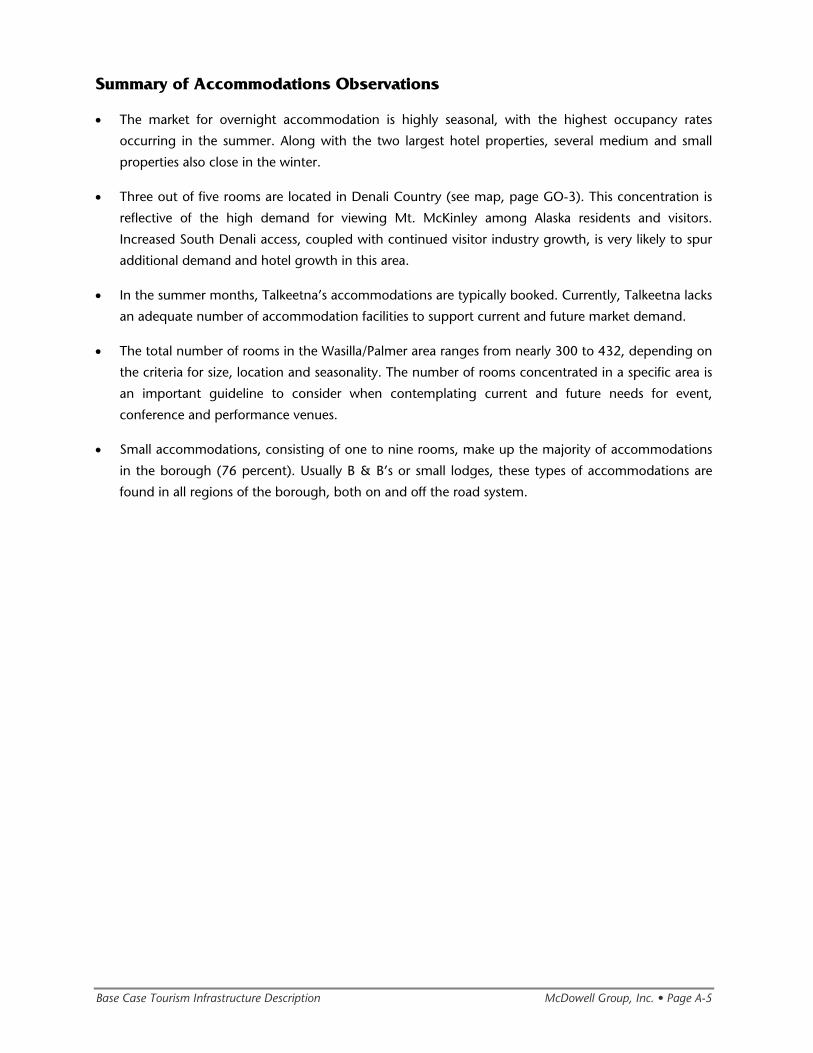

Summary of Accommodations Observations

• The market for overnight accommodation is highly seasonal, with the highest occupancy rates

occurring in the summer. Along with the two largest hotel properties, several medium and small

properties also close in the winter.

• Three out of five rooms are located in Denali Country (see map, page GO-3). This concentration is

reflective of the high demand for viewing Mt. McKinley among Alaska residents and visitors.

Increased South Denali access, coupled with continued visitor industry growth, is very likely to spur

additional demand and hotel growth in this area.

• In the summer months, Talkeetna’s accommodations are typically booked. Currently, Talkeetna lacks

an adequate number of accommodation facilities to support current and future market demand.

• The total number of rooms in the Wasilla/Palmer area ranges from nearly 300 to 432, depending on

the criteria for size, location and seasonality. The number of rooms concentrated in a specific area is

an important guideline to consider when contemplating current and future needs for event,

conference and performance venues.

• Small accommodations, consisting of one to nine rooms, make up the majority of accommodations

in the borough (76 percent). Usually B & B’s or small lodges, these types of accommodations are

found in all regions of the borough, both on and off the road system.

Base Case Tourism Infrastructure Description McDowell Group, Inc. • Page A-6

Meeting Facilities

Rapid business and population growth in the Wasilla/Palmer area has resulted in a higher profile for Mat-

Su and greater opportunities for conferences and events. The region’s inherent appeal as a destination is

enhanced by fairly quick access for meeting attendees making travel connections via Anchorage.

Small and mid-sized meeting facilities are available throughout the Mat-Su Borough. The smaller, more

remote properties are often used for staff or board retreats. The larger facilities host a variety of

meetings, conferences and events. However, there are a number of limitations that preclude the region

from competing on a larger scale for this market.

From a meeting planner perspective, ideal convention and conference facilities offer the flexibility to

reconfigure rooms as needed for trade shows and large meeting areas for plenary sessions, receptions,

breakout rooms and onsite dining. The facility should be large enough that a group can efficiently move

between meeting and banquet functions throughout the course of a day. Although in-state conferences

and conventions are typically more willing to meet in a facility that is separate from guest rooms, it is a

competitive disadvantage as the meeting planner has to factor in the added time and expense for

transferring meeting attendees between venues.

This section discusses the meeting facilities available in the Borough and provides details regarding their

capacity and availability of banquet facilities and lodging. The meeting facility section is divided into

“Trade Shows/Large Event Gathering Space,” “Large Meeting Spaces,“ “Medium Meeting Spaces” and

“Small Meeting Spaces.” There is also a short assessment of meeting facilities.

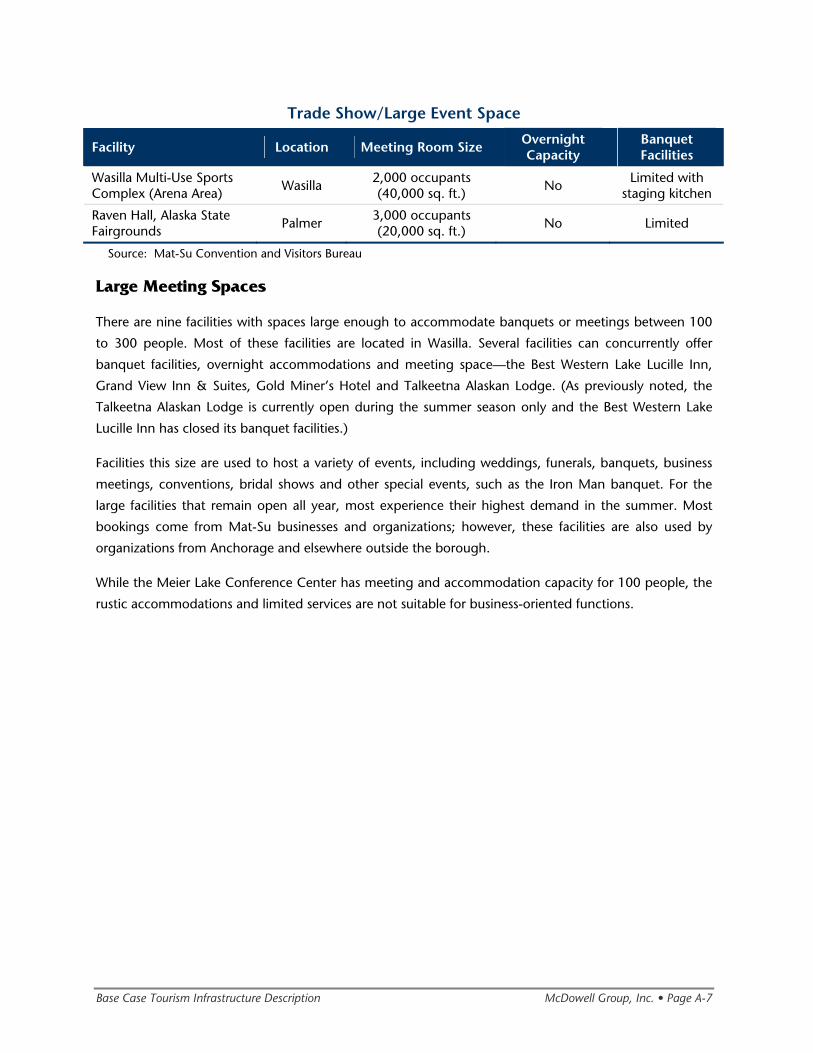

Trade Show/Large Event Gathering Space

Two facilities can accommodate large trade shows or indoor events, the Wasilla Multi-Use Sports

Complex and Raven Hall on the Alaska State Fairgrounds. While these facilities offer adequate size, they

lack the comprehensive services and flexibility needed to make them ideal conference or convention

locations. Both facilities are located in the core Wasilla/Palmer area.

The Wasilla Multi-Use Sports Complex offers meeting space that can be divided into three smaller rooms

or opened to seat up to 90 people. While it is possible to use the ice area and associated seating for

trade shows, concerts or other special events, the Complex has seasonal commitments for the ice rink

that preclude most non-skating events between fall and spring. While limited kitchen facilities will be

installed soon, lack of full-service banquet facilities further limits the type of events held at the Complex.

The 20,000 sq. ft. Raven Hall is the newest structure on the Alaska State Fairgrounds. The hall has

overhead doors, high ceilings, restrooms, a developing kitchen area, electrical power and phone lines.

The hall has been used for small conventions, trade/consumer shows, exhibitions, the Governor’s

Inaugural Ball and large meetings. The facility does not offer the ability to breakout into smaller meeting

spaces, banquet services or the other amenities required for multi-day events.

Base Case Tourism Infrastructure Description McDowell Group, Inc. • Page A-7

Trade Show/Large Event Space

Facility Location Meeting Room Size Overnight Capacity

Banquet Facilities

Wasilla Multi-Use Sports Complex (Arena Area) Wasilla

2,000 occupants (40,000 sq. ft.) No

Limited with staging kitchen

Raven Hall, Alaska State Fairgrounds Palmer

3,000 occupants (20,000 sq. ft.) No Limited

Source: Mat-Su Convention and Visitors Bureau

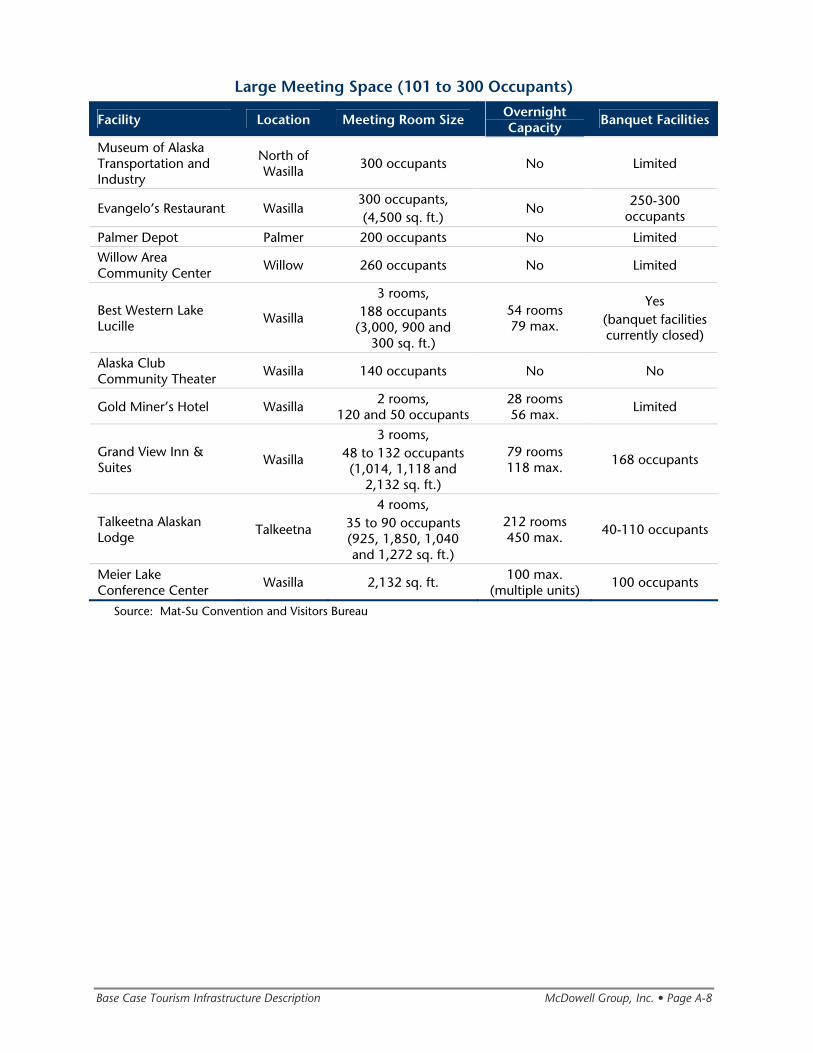

Large Meeting Spaces

There are nine facilities with spaces large enough to accommodate banquets or meetings between 100

to 300 people. Most of these facilities are located in Wasilla. Several facilities can concurrently offer

banquet facilities, overnight accommodations and meeting space—the Best Western Lake Lucille Inn,

Grand View Inn & Suites, Gold Miner’s Hotel and Talkeetna Alaskan Lodge. (As previously noted, the

Talkeetna Alaskan Lodge is currently open during the summer season only and the Best Western Lake

Lucille Inn has closed its banquet facilities.)

Facilities this size are used to host a variety of events, including weddings, funerals, banquets, business

meetings, conventions, bridal shows and other special events, such as the Iron Man banquet. For the

large facilities that remain open all year, most experience their highest demand in the summer. Most

bookings come from Mat-Su businesses and organizations; however, these facilities are also used by

organizations from Anchorage and elsewhere outside the borough.

While the Meier Lake Conference Center has meeting and accommodation capacity for 100 people, the

rustic accommodations and limited services are not suitable for business-oriented functions.

Base Case Tourism Infrastructure Description McDowell Group, Inc. • Page A-8

Large Meeting Space (101 to 300 Occupants)

Facility Location Meeting Room Size Overnight Capacity Banquet Facilities

Museum of Alaska Transportation and Industry

North of Wasilla 300 occupants No Limited

Evangelo’s Restaurant Wasilla 300 occupants, (4,500 sq. ft.)

No 250-300 occupants

Palmer Depot Palmer 200 occupants No Limited Willow Area Community Center

Willow 260 occupants No Limited

Best Western Lake Lucille

Wasilla

3 rooms, 188 occupants

(3,000, 900 and 300 sq. ft.)

54 rooms 79 max.

Yes (banquet facilities currently closed)

Alaska Club Community Theater

Wasilla 140 occupants No No

Gold Miner’s Hotel Wasilla 2 rooms, 120 and 50 occupants

28 rooms 56 max.

Limited

Grand View Inn & Suites

Wasilla

3 rooms, 48 to 132 occupants (1,014, 1,118 and

2,132 sq. ft.)

79 rooms 118 max.

168 occupants

Talkeetna Alaskan Lodge

Talkeetna

4 rooms, 35 to 90 occupants (925, 1,850, 1,040 and 1,272 sq. ft.)

212 rooms 450 max.

40-110 occupants

Meier Lake Conference Center

Wasilla 2,132 sq. ft. 100 max. (multiple units)

100 occupants

Source: Mat-Su Convention and Visitors Bureau

Base Case Tourism Infrastructure Description McDowell Group, Inc. • Page A-9

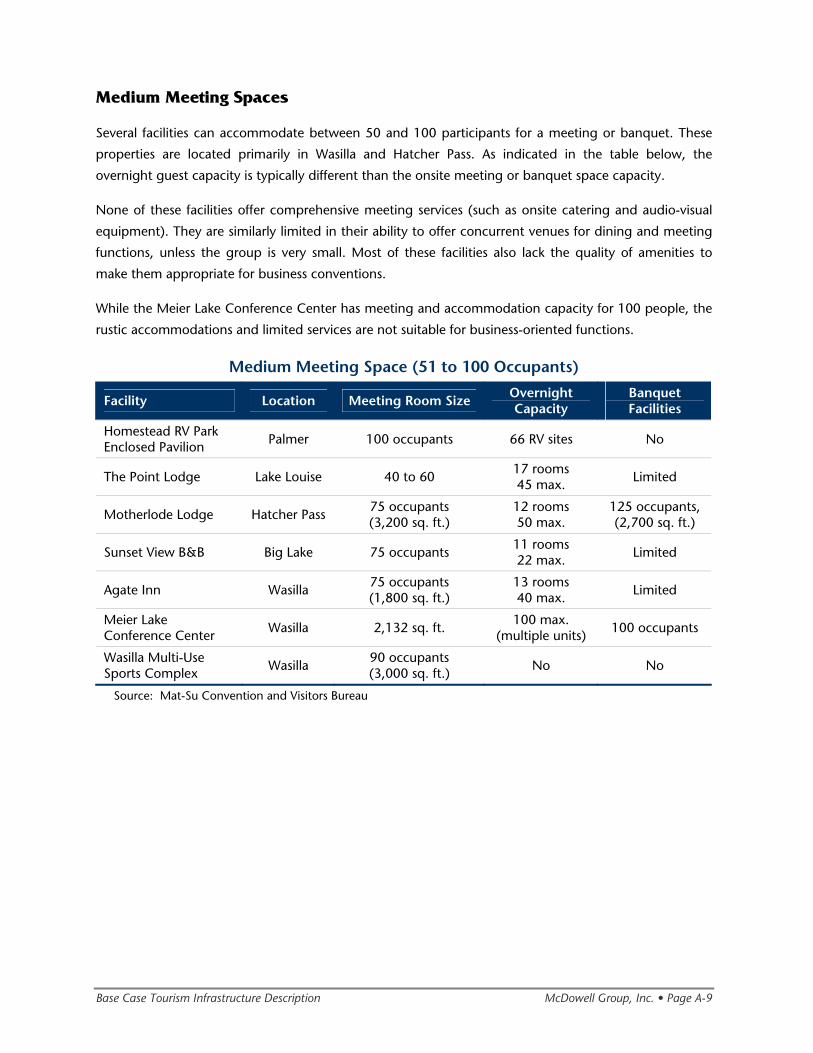

Medium Meeting Spaces

Several facilities can accommodate between 50 and 100 participants for a meeting or banquet. These

properties are located primarily in Wasilla and Hatcher Pass. As indicated in the table below, the

overnight guest capacity is typically different than the onsite meeting or banquet space capacity.

None of these facilities offer comprehensive meeting services (such as onsite catering and audio-visual

equipment). They are similarly limited in their ability to offer concurrent venues for dining and meeting

functions, unless the group is very small. Most of these facilities also lack the quality of amenities to

make them appropriate for business conventions.

While the Meier Lake Conference Center has meeting and accommodation capacity for 100 people, the

rustic accommodations and limited services are not suitable for business-oriented functions.

Medium Meeting Space (51 to 100 Occupants)

Facility Location Meeting Room Size Overnight Capacity

Banquet Facilities

Homestead RV Park Enclosed Pavilion Palmer 100 occupants 66 RV sites No

The Point Lodge Lake Louise 40 to 60 17 rooms 45 max. Limited

Motherlode Lodge Hatcher Pass 75 occupants (3,200 sq. ft.)

12 rooms 50 max.

125 occupants, (2,700 sq. ft.)

Sunset View B&B Big Lake 75 occupants 11 rooms 22 max. Limited

Agate Inn Wasilla 75 occupants (1,800 sq. ft.)

13 rooms 40 max. Limited

Meier Lake Conference Center Wasilla 2,132 sq. ft.

100 max. (multiple units) 100 occupants

Wasilla Multi-Use Sports Complex Wasilla

90 occupants (3,000 sq. ft.) No No

Source: Mat-Su Convention and Visitors Bureau

Base Case Tourism Infrastructure Description McDowell Group, Inc. • Page A-10

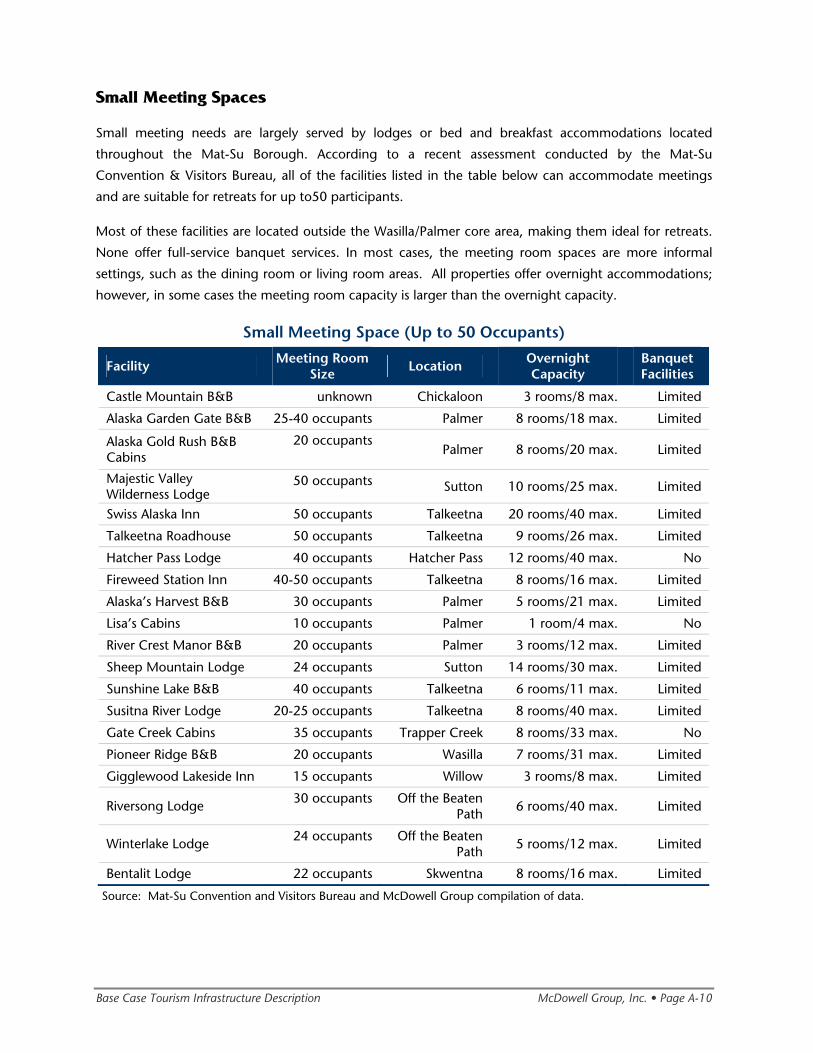

Small Meeting Spaces

Small meeting needs are largely served by lodges or bed and breakfast accommodations located

throughout the Mat-Su Borough. According to a recent assessment conducted by the Mat-Su

Convention & Visitors Bureau, all of the facilities listed in the table below can accommodate meetings

and are suitable for retreats for up to50 participants.

Most of these facilities are located outside the Wasilla/Palmer core area, making them ideal for retreats.

None offer full-service banquet services. In most cases, the meeting room spaces are more informal

settings, such as the dining room or living room areas. All properties offer overnight accommodations;

however, in some cases the meeting room capacity is larger than the overnight capacity.

Small Meeting Space (Up to 50 Occupants)

Facility Meeting Room Size Location Overnight

Capacity Banquet Facilities

Castle Mountain B&B unknown Chickaloon 3 rooms/8 max. Limited

Alaska Garden Gate B&B 25-40 occupants Palmer 8 rooms/18 max. Limited

Alaska Gold Rush B&B Cabins

20 occupants

Palmer 8 rooms/20 max. Limited

Majestic Valley Wilderness Lodge

50 occupants Sutton 10 rooms/25 max. Limited

Swiss Alaska Inn 50 occupants Talkeetna 20 rooms/40 max. Limited

Talkeetna Roadhouse 50 occupants Talkeetna 9 rooms/26 max. Limited

Hatcher Pass Lodge 40 occupants Hatcher Pass 12 rooms/40 max. No

Fireweed Station Inn 40-50 occupants Talkeetna 8 rooms/16 max. Limited

Alaska’s Harvest B&B 30 occupants Palmer 5 rooms/21 max. Limited

Lisa’s Cabins 10 occupants Palmer 1 room/4 max. No

River Crest Manor B&B 20 occupants Palmer 3 rooms/12 max. Limited

Sheep Mountain Lodge 24 occupants Sutton 14 rooms/30 max. Limited

Sunshine Lake B&B 40 occupants Talkeetna 6 rooms/11 max. Limited

Susitna River Lodge 20-25 occupants Talkeetna 8 rooms/40 max. Limited

Gate Creek Cabins 35 occupants Trapper Creek 8 rooms/33 max. No

Pioneer Ridge B&B 20 occupants Wasilla 7 rooms/31 max. Limited

Gigglewood Lakeside Inn 15 occupants Willow 3 rooms/8 max. Limited

Riversong Lodge 30 occupants Off the Beaten Path 6 rooms/40 max. Limited

Winterlake Lodge 24 occupants Off the Beaten Path 5 rooms/12 max. Limited

Bentalit Lodge 22 occupants Skwentna 8 rooms/16 max. Limited

Source: Mat-Su Convention and Visitors Bureau and McDowell Group compilation of data.

Base Case Tourism Infrastructure Description McDowell Group, Inc. • Page A-11

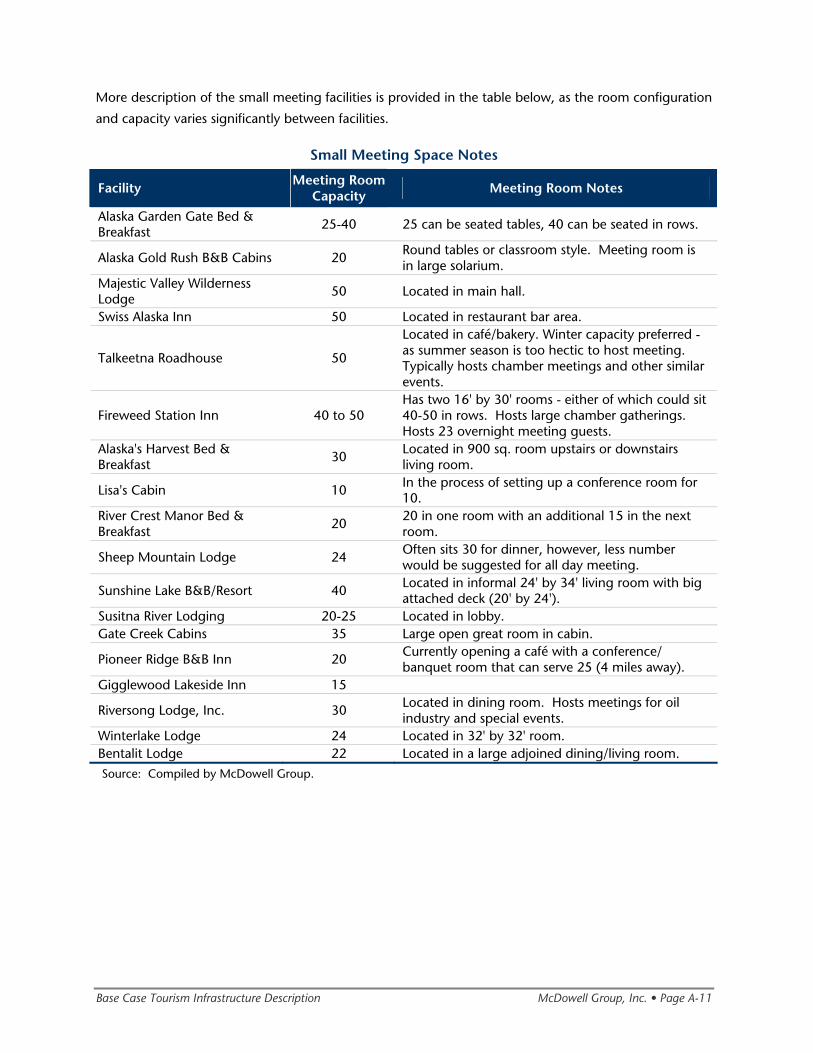

More description of the small meeting facilities is provided in the table below, as the room configuration

and capacity varies significantly between facilities.

Small Meeting Space Notes

Facility Meeting Room Capacity Meeting Room Notes

Alaska Garden Gate Bed & Breakfast 25-40 25 can be seated tables, 40 can be seated in rows.

Alaska Gold Rush B&B Cabins 20 Round tables or classroom style. Meeting room is in large solarium.

Majestic Valley Wilderness Lodge 50 Located in main hall.

Swiss Alaska Inn 50 Located in restaurant bar area.

Talkeetna Roadhouse 50

Located in café/bakery. Winter capacity preferred - as summer season is too hectic to host meeting. Typically hosts chamber meetings and other similar events.

Fireweed Station Inn 40 to 50 Has two 16' by 30' rooms - either of which could sit 40-50 in rows. Hosts large chamber gatherings. Hosts 23 overnight meeting guests.

Alaska's Harvest Bed & Breakfast 30 Located in 900 sq. room upstairs or downstairs

living room.

Lisa's Cabin 10 In the process of setting up a conference room for 10.

River Crest Manor Bed & Breakfast

20 20 in one room with an additional 15 in the next room.

Sheep Mountain Lodge 24 Often sits 30 for dinner, however, less number would be suggested for all day meeting.

Sunshine Lake B&B/Resort 40 Located in informal 24' by 34' living room with big attached deck (20' by 24').

Susitna River Lodging 20-25 Located in lobby. Gate Creek Cabins 35 Large open great room in cabin.

Pioneer Ridge B&B Inn 20 Currently opening a café with a conference/ banquet room that can serve 25 (4 miles away).

Gigglewood Lakeside Inn 15

Riversong Lodge, Inc. 30 Located in dining room. Hosts meetings for oil industry and special events.

Winterlake Lodge 24 Located in 32' by 32' room. Bentalit Lodge 22 Located in a large adjoined dining/living room. Source: Compiled by McDowell Group.

Base Case Tourism Infrastructure Description McDowell Group, Inc. • Page A-12

Summary of Meeting Facilities Observations

• The borough has a disadvantage as it competes with other destinations that have full-service

conference facilities with accommodations either located onsite or in close proximity.

• Any meeting or event that requires a single facility for sleeping rooms, meeting rooms and dining

facilities is limited to approximately 100 attendees. Because of ongoing commitments for guest

rooms and banquet rooms, the practical limit at any given time is likely between 50 and 80

attendees.

• The meeting facilities located within the Talkeetna Alaskan Lodge are an asset for attracting groups

and events—especially in the fall and spring. Other lodges and businesses in the surrounding area

are likely to benefit from increased marketing of this asset.

• While there are more than 400 guest rooms in the Wasilla/Palmer area, there is little full-service

meeting capacity available to accommodate groups that large.

Base Case Tourism Infrastructure Description McDowell Group, Inc. • Page A-13

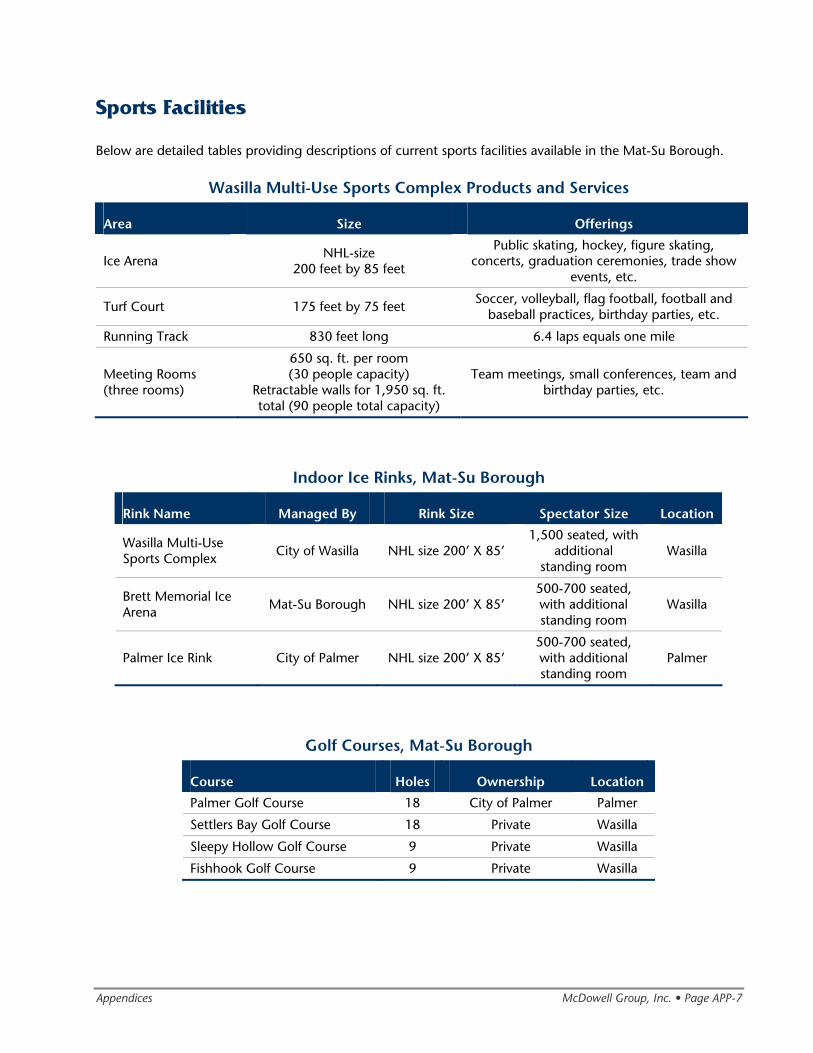

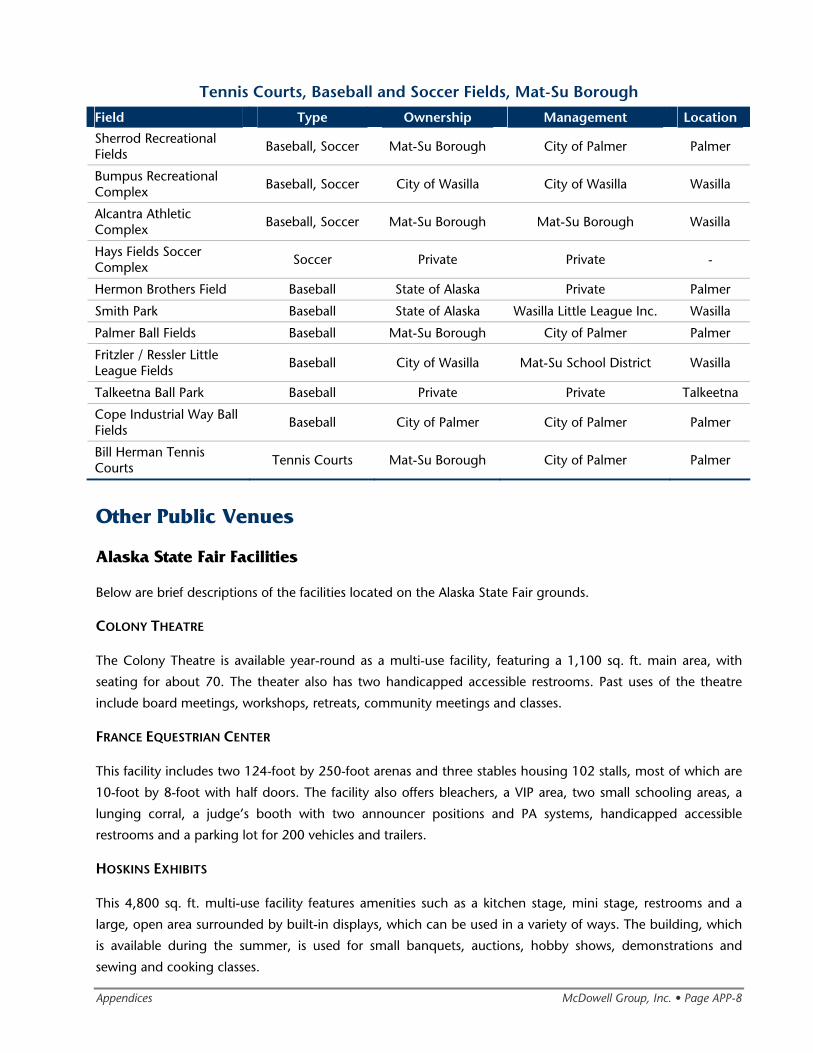

Sports Facilities

Currently, the sports facilities in the Mat-Su Borough are largely designed for local residents. However,

these facilities offer the potential to draw visitors from outside the borough who may stay overnight to

participate in hockey, ice skating, soccer, baseball or other sport tournaments or competitions. This

section provides an overview of sports facilities that draw visitors from outside the Borough. Detailed

tables showing current sports facilities available in the Mat-Su Borough can be found in Appendix A.

Wasilla Multi-Use Sports Complex

The Wasilla Multi-Use Sports Complex offers the highest quality and broadest sports usage in the Mat-Su

Borough. Opened in 2004, the 102,000 sq. ft. facility offers four primary activity areas: a National

Hockey League-size ice arena, an indoor artificial turf court, a running/walking track and three

community meeting rooms. These primary activities comprise the first phase elements of the 60-acre

master plan for the complex.

The running track is elevated above and encircles the bleachers in the ice arena. Large windows allow

natural lighting and an outdoor view for walkers, joggers and runners.

OTHER SERVICES

A new trailhead facility was constructed to provide access to nearby Iditarod and Tesoro Iron Dog trail

systems. A paved road and utility corridor linking to the Parks Highway was recently constructed. A new

bike trail also provides access to a new area of the city. By October 2008, the complex hopes to have a

staging kitchen completed. While the primary purpose of this kitchen is to provide support should the

complex need to be used as an emergency evacuation shelter, the kitchen can also be used to cater

events at the facility.

PLANNED PHASE II ADDITIONS