Page 1 of 6 A comprehensive range of market research reports by award-winning economists and analysts are exclusively available for download from w w w .rhbinvest.com Local Market Leads: ♦ Lifted by a rally across the regional markets amid signs of strengthening economic recovery in major Asian countries, the local market staged an early rally on Thursday. ♦ China’s manufacturing activity rose more than expected to 57 in Mar from 55.8 in Feb. Meanwhile, the Bank of Japan’s quarterly tankan survey of business sentiment showed confidence among the nation’s biggest manufacturers improved significantly to -14 in Mar, against -25 in Dec. ♦ These lifted the negative impact from the overnight US markets’ retreat amid an unexpected drop in US private sector employment. ♦ Back home, the FBM KLCI ended up 9.27 pts or 0.70% to 1,329.84, led by strong gains in MISC (+33sen), CIMB (+32sen) and IOICorp (+5sen). ♦ However, turnover dropped further to 807m shares, from 961m shares on Wednesday. Market breadth turned positive with 423 counters up against 316 counters down. Technical Interpretations: ♦ From an intraday low of 1,319.76 (-0.81-pt), the FBM KLCI staged a strong run-up on the back of strong buying momentum in the early session, before traded rangebound for the rest of the day. ♦ By chalking up a huge bullish candle following a successful penetration of Tuesday’s high at 1,323.83, the index indicates a potential retest of Mar’s high of 1,334.34 soon. ♦ If the index manages to overtake 1,334.34, the momentum will accelerate, hence lifting the daily trading volume and lead the FBM KLCI further to our medium-term target at 1,390. ♦ For now, strong support is near the 10-day SMA of 1,312 and the important resistance-turned-support level at 1,300. Chart 1: KLCI Daily Chart 2: KLCI Intraday Technical Research Daily Trading Strategy Market Technical Reading Low Volume The Main Dampener To Short-term Trading Sentiment... M a l a s i a M A R K E T D A T E L I N E P P 7 7 6 7 / 0 9 / 2 0 1 0 ( 0 2 5 3 5 4 ) Please read important disclosures at the end of this report. 2 April 2010 RHB Research Institute Sdn Bhd A member of the RHB Banking Group Company No: 233327 -M

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

8/9/2019 Market Technical Reading : Low Volume The Main Dampener To Short-term Trading - 02/04/2010

http://slidepdf.com/reader/full/market-technical-reading-low-volume-the-main-dampener-to-short-term-trading 1/6

Page 1 of 6A comprehensive range of market research reports by award-winning economists and analysts are exclusively

available for download from w w w . r h b i n v e s t . c o m

Local Market Leads:

♦ Lifted by a rally across the regional markets amid signs of strengthening economic recovery in major Asian

countries, the local market staged an early rally on Thursday.

♦ China’s manufacturing activity rose more than expected to 57 in Mar from 55.8 in Feb. Meanwhile, the Bank of

Japan’s quarterly tankan survey of business sentiment showed confidence among the nation’s biggest

manufacturers improved significantly to -14 in Mar, against -25 in Dec.

♦ These lifted the negative impact from the overnight US markets’ retreat amid an unexpected drop in US private

sector employment.

♦ Back home, the FBM KLCI ended up 9.27 pts or 0.70% to 1,329.84, led by strong gains in MISC (+33sen), CIMB

(+32sen) and IOICorp (+5sen).

♦ However, turnover dropped further to 807m shares, from 961m shares on Wednesday. Market breadth turned

positive with 423 counters up against 316 counters down.

Technical Interpretations:

♦ From an intraday low of 1,319.76 (-0.81-pt), the FBM KLCI staged a strong run-up on the back of strong buying

momentum in the early session, before traded rangebound for the rest of the day.

♦ By chalking up a huge bullish candle following a successful penetration of Tuesday’s high at 1,323.83, the index

indicates a potential retest of Mar’s high of 1,334.34 soon.

♦ If the index manages to overtake 1,334.34, the momentum will accelerate, hence lifting the daily trading volume

and lead the FBM KLCI further to our medium-term target at 1,390.

♦ For now, strong support is near the 10-day SMA of 1,312 and the important resistance-turned-support level at

1,300.

Chart 1: KLCI Daily Chart 2: KLCI Intraday

Techn ica l Research

D a i l y T r a d i ng S t r a t egy

Market Technical ReadingLow Volume The Main Dampener To Short-term TradingSentiment...

M a l a s i a

M A R K

E T

D A T E L I N E

P P

7 7 6 7 / 0 9 / 2 0 1 0 ( 0 2 5 3 5 4 )

Please read important disclosures at the end of this report.

2 April 2010

RHB ResearchInstitute Sdn BhdA member of theRHB Banking GroupCompany No: 233327 -M

8/9/2019 Market Technical Reading : Low Volume The Main Dampener To Short-term Trading - 02/04/2010

http://slidepdf.com/reader/full/market-technical-reading-low-volume-the-main-dampener-to-short-term-trading 2/6

2 April 2010

Page 2 of 6A comprehensive range of market research reports by award-winning economists and analysts are exclusively

available for download from w w w . r h b i n v e s t . c o m

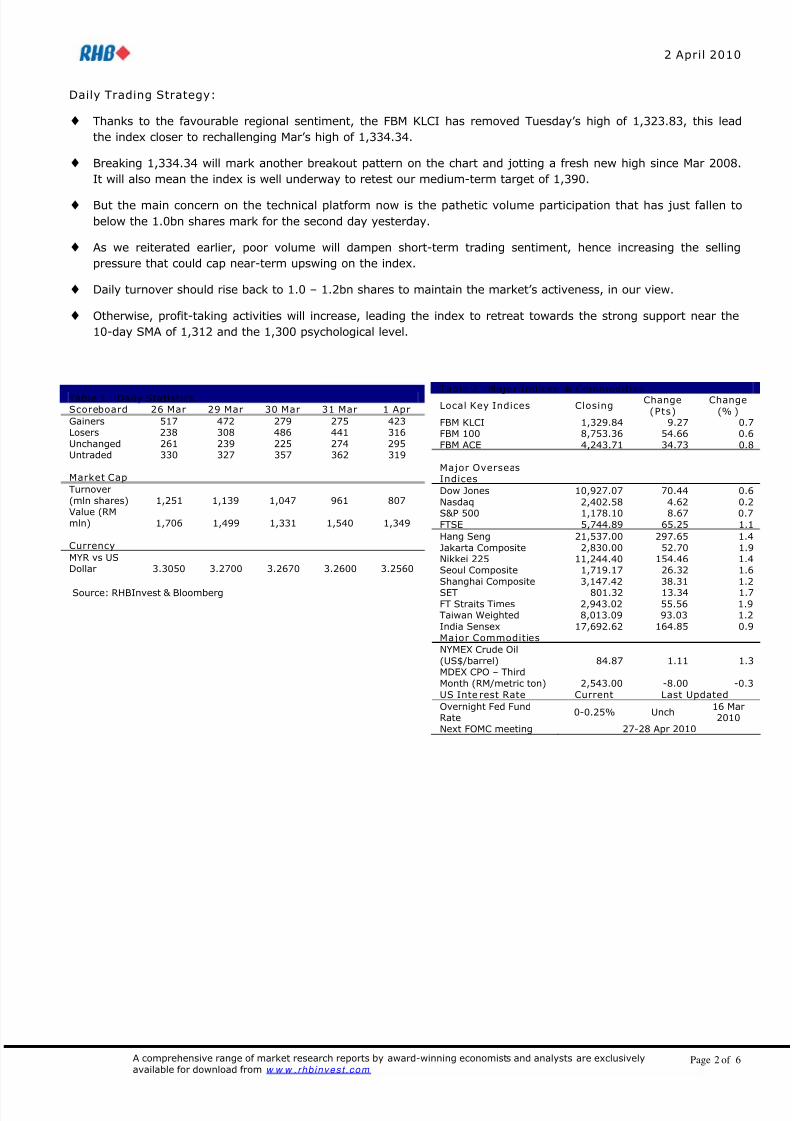

Daily Trading Strategy:

♦ Thanks to the favourable regional sentiment, the FBM KLCI has removed Tuesday’s high of 1,323.83, this lead

the index closer to rechallenging Mar’s high of 1,334.34.

♦ Breaking 1,334.34 will mark another breakout pattern on the chart and jotting a fresh new high since Mar 2008.

It will also mean the index is well underway to retest our medium-term target of 1,390.

♦ But the main concern on the technical platform now is the pathetic volume participation that has just fallen to

below the 1.0bn shares mark for the second day yesterday.

♦ As we reiterated earlier, poor volume will dampen short-term trading sentiment, hence increasing the selling

pressure that could cap near-term upswing on the index.

♦ Daily turnover should rise back to 1.0 – 1.2bn shares to maintain the market’s activeness, in our view.

♦ Otherwise, profit-taking activities will increase, leading the index to retreat towards the strong support near the

10-day SMA of 1,312 and the 1,300 psychological level.

Source: RHBInvest & Bloomberg

Table 2 : Major Indices & CommoditiesLocal Key Indices Closing

Change

(Pts)

Change

(% )FBM KLCI 1,329.84 9.27 0.7FBM 100 8,753.36 54.66 0.6

FBM ACE 4,243.71 34.73 0.8

Major OverseasIndices

Dow Jones 10,927.07 70.44 0.6

Nasdaq 2,402.58 4.62 0.2S&P 500 1,178.10 8.67 0.7

FTSE 5,744.89 65.25 1.1

Hang Seng 21,537.00 297.65 1.4

Jakarta Composite 2,830.00 52.70 1.9Nikkei 225 11,244.40 154.46 1.4Seoul Composite 1,719.17 26.32 1.6

Shanghai Composite 3,147.42 38.31 1.2

SET 801.32 13.34 1.7FT Straits Times 2,943.02 55.56 1.9Taiwan Weighted 8,013.09 93.03 1.2

India Sensex 17,692.62 164.85 0.9

Major Commodities

NYMEX Crude Oil

(US$/barrel) 84.87 1.11 1.3MDEX CPO – Third

Month (RM/metric ton) 2,543.00 -8.00 -0.3

US Inte rest Rate Current Last Updated

Overnight Fed FundRate

0-0.25% Unch16 Mar2010

Next FOMC meeting 27-28 Apr 2010

Table 1 : Daily StatisticsScoreboard 26 Mar 29 Mar 30 Mar 31 Mar 1 Apr

Gainers 517 472 279 275 423Losers 238 308 486 441 316

Unchanged 261 239 225 274 295Untraded 330 327 357 362 319

Market Cap

Turnover

(mln shares) 1,251 1,139 1,047 961 807Value (RM

mln) 1,706 1,499 1,331 1,540 1,349

Currency

MYR vs USDollar 3.3050 3.2700 3.2670 3.2600 3.2560

8/9/2019 Market Technical Reading : Low Volume The Main Dampener To Short-term Trading - 02/04/2010

http://slidepdf.com/reader/full/market-technical-reading-low-volume-the-main-dampener-to-short-term-trading 3/6

2 April 2010

Page 3 of 6A comprehensive range of market research reports by award-winning economists and analysts are exclusively

available for download from w w w . r h b i n v e s t . c o m

Technical Interpretations:

♦ Taking cues from the bullish sentiment in Asian regional markets amid renewed optimism on global economic

recovery, the local futures index regained its bullish momentum, closing at its highest level since Feb 2008.

♦ The FKLI for Apr contract surged 11.50 pts or 0.87% to 1,338.00, after forming a huge technical gap at 1,320.50

- 1,327.50 on the chart. The FKLI Mar contract settled at 1,317 upon expiry on Wednesday.

♦ Technically, the bullish candle and the mild improvement on the short-term momentum indicators suggest a likely

reversal on the recent selling momentum.

♦ More importantly, the futures index ended marginally above Mar’s high of 1,337 yesterday, marking a potential

chart breakout if it sustains at above the high today.

♦ As such, the FKLI has a strong chance to expand yesterday’s rally towards the next medium-term target at 1,390

amid stronger follow-through buying momentum in the near term.

♦ Prior to that, it is expected to fill up a huge technical gap from 1,314 to 1,348 formed since Feb 2008.

♦ For the support, we expect the 10-day SMA near 1,315 and the 1,300 psychological level to provide strong buffer

to any short-term selling pressure.

Daily Trading Strategy:

♦ Yesterday’s strong closing suggests a likely resumption of the buying momentum.

♦ Therefore, traders should prepare to go “long” again upon confirmation of the removal of 1,337 today, i.e. the

registering of another positive candle on the chart.

♦ The trading range for the FKLI is likely to be between 1,333 and 1,348 today.

Table 3: FKLI ClosingsFKLI (Month)

Contracts Open High Low Close Chg (Pts) Settle Volume Open Interest

Apr 10 1328.50 1338.50 1327.50 1338.00 11.50 1338.00 6547 18826

May 10 1327.50 1338.00 1327.00 1338.00 - 1338.00 393 0

Jun 10 1326.00 1336.00 1324.00 1336.00 11.00 1336.50 301 455Sep 10 1323.00 1336.00 1321.00 1336.00 14.00 1336.50 74 157

Source: Bursa Malaysia

Chart 3: FKLI Da ily Chart 4: FKLI Intraday

8/9/2019 Market Technical Reading : Low Volume The Main Dampener To Short-term Trading - 02/04/2010

http://slidepdf.com/reader/full/market-technical-reading-low-volume-the-main-dampener-to-short-term-trading 4/6

2 April 2010

Page 4 of 6A comprehensive range of market research reports by award-winning economists and analysts are exclusively

available for download from w w w . r h b i n v e s t . c o m

US Market Leads:

♦ Buoyed by the upbeat readings on manufacturing and weekly jobless claims data, the Wall Street started the

second quarter on a bullish tone by kicking off a strong comeback on Thursday.

♦ The Institute for Supply Management (ISM)’s manufacturing activity index expanded for an eighth month in a row

by rising to 59.6 in Mar, in line with strong manufacturing data in overseas, such as China. Also, the weekly

jobless claims fell by 6,000 to 439,000 last week.

♦ This encouraged investors to scoop up stocks, even as ahead of the crucial Mar non-farm employment reports on

Friday and that the US markets and most of the European markets will be closed on Friday for Good Friday

holiday.

♦ Backed by strong US economic data that pointed to a sustainable economic recovery, the US light sweet crude oil

futures for May delivery advanced US$1.11 or 1.3% to US$84.87/barrel, its highest closing since Oct 2008.

Technical Interpretations:

Dow Jones Industrial Average (DJIA)

♦ Instead of extending its profit-taking activities, the US DJIA staged a surprise rebound by gaining 70.44 pts or

0.65% to 10,927.07 on Thursday.

♦ By bouncing from the 10,850 technical level with a bullish candle, this indicates a good chance of renewing a

fresh upswing leg soon.

♦ And a further clearance of yesterday’s intraday high of 10,956.39 will help it to trigger a new rally towards the

next upside target at 11,250. Solid support is now seen at 10,850, added with the 21-day SMA of 10,727.

Nasdaq Composite (Nasdaq)

♦ After fluctuating between a wide range of 2,383.77 low and 2,423.43 high, the Nasdaq Composite Index settled

at 2,402.58 with a 4.62 pts or 0.19% gain.

♦ Chart wise, the formation of a “star-like” candle points to a possible weakness ahead.

♦ But with the mild uptick in both the short-term momentum indicators, we believe it is likely to extend the current

rangebound consolidation at between the 21-day SMA of 2,376 and Mar’s high of 2,432.25.

♦ And for it to kick off a new rally towards 2,470, it has to take out Mar’s high of 2,432.25.

Chart 5: US Dow Jones I ndustrial Average (DJI A) Daily Chart 6: US Nasdaq Composite DailyChart 5: US Dow Jones I ndustrial Average (DJI A) Daily Chart 6: US Nasdaq Composite Daily

8/9/2019 Market Technical Reading : Low Volume The Main Dampener To Short-term Trading - 02/04/2010

http://slidepdf.com/reader/full/market-technical-reading-low-volume-the-main-dampener-to-short-term-trading 5/6

Page 5 of 6A comprehensive range of market research reports by award-winning economists and analysts are exclusively

available for download from w w w . r h b i n v e s t . c o m

Daily Technical Watch:

Tanjong Public Limited Company (2267)

The target for the “triangle breakout” pattern points to RM19.50…

♦ After hitting its lowest level since Oct 2003 at RM9.00 in Oct 2008, the share price of Tanjong turned around and

launched an impressive uptrend.

♦ By end-Jul 2009, the stock received another boost when it finally removed the key barrier of RM14.30.

♦ The uptrend continued until it reached the RM18.00 resistance level in early Jan 2010.

♦ Thereafter, the stock began its consolidation phase, congesting at below the RM18.00 hurdle to form an

“Ascending Triangle” pattern on the chart.

♦ After a nearly three months of consolidation, it finally broke out of the triangle with a huge bullish candle

yesterday, indicating a bullish rally ahead.

♦ The stock jumped 46sen at the close to RM18.40, following a test of a fresh all-time high at RM18.56.

♦ Backed by the breakout point support of RM18.00, the “triangle breakout” pattern is pointing at a one-to-one

target at RM19.50.

♦ If the buying interest increases today due to the triangle breakout momentum, the stock could accelerate towards

the RM19.50 region, before meeting its first line of profit-taking momentum, in our view.

Technical Readings:

♦ 10-day SMA: RM17.954

♦ 40-day SMA: RM17.739

♦ Support: IS = RM18.00 S1 = RM16.70 S2 = RM15.40

♦ Resistance: IR = RM19.50

Chart 7: Tanjong Daily Chart 8: Tanjong I ntraday

8/9/2019 Market Technical Reading : Low Volume The Main Dampener To Short-term Trading - 02/04/2010

http://slidepdf.com/reader/full/market-technical-reading-low-volume-the-main-dampener-to-short-term-trading 6/6

Page 6 of 6A comprehensive range of market research reports by award-winning economists and analysts are exclusively

available for download from w w w . r h b i n v e s t . c o m

IMP ORTANT DI SCLOSURES

This report has been prepared by RHB Research Institute Sdn Bhd (RHBRI) and is for private circulation only to clients of RHBRI and RHB Investment Bank Berhad(previously known as RHB Sakura Merchant Bankers Berhad). It is for distribution only under such circumstances as may be permitted by applicable law. Theopinions and information contained herein are based on generally available data believed to be reliable and are subject to change without notice, and may differ orbe contrary to opinions expressed by other business units within the RHB Group as a result of using different assumptions and criteria. This report is not to beconstrued as an offer, invitation or solicitation to buy or sell the securities covered herein. RHBRI does not warrant the accuracy of anything stated herein in anymanner whatsoever and no reliance upon such statement by anyone shall give rise to any claim whatsoever against RHBRI. RHBRI and/or its associated personsmay from time to time have an interest in the securities mentioned by this report.

This report does not provide individually tailored investment advice. It has been prepared without regard to the individual financial circumstances and objectivesof persons who receive it. The securities discussed in this report may not be suitable for all investors. RHBRI recommends that investors independently evaluateparticular investments and strategies, and encourages investors to seek the advice of a financial adviser. The appropriateness of a particular investment orstrategy will depend on an investor’s individual circumstances and objectives. Neither RHBRI, RHB Group nor any of its affiliates, employees or agents acceptsany liability for any loss or damage arising out of the use of all or any part of this report.

RHBRI and the Connected Persons (the “RHB Group”) are engaged in securities trading, securities brokerage, banking and financing activities as well as providinginvestment banking and financial advisory services. In the ordinary course of its trading, brokerage, banking and financing activities, any member of the RHBGroup may at any time hold positions, and may trade or otherwise effect transactions, for its own account or the accounts of customers, in debt or equitysecurities or loans of any company that may be involved in this transaction.

“Connected Persons” means any holding company of RHBRI, the subsidiaries and subsidiary undertaking of such a holding company and the respective directors,officers, employees and agents of each of them. Investors should assume that the “Connected Persons” are seeking or will seek investment banking or otherservices from the companies in which the securities have been discussed/covered by RHBRI in this report or in RHBRI’s previous reports.

This report has been prepared by the research personnel of RHBRI. Facts and views presented in this report have not been reviewed by, and may not reflectinformation known to, professionals in other business areas of the “Connected Persons,” including investment banking personnel.

The research analysts, economists or research associates principally responsible for the preparation of this research report have received compensation based

upon various factors, including quality of research, investor client feedback, stock picking, competitive factors and firm revenues.

Technical recommendation framework for stocks and sectors are as follows: -

Technical Recommendation:Trading Buy = Short-term positive opportunity spotted. It is an aggressive trading recommendation with a book to sellers’ price for short-term technical upside.Bargain Buy = Short-term positive but technical signals have yet to trigger a rally. Traders can park and queue for their desired entry level within a small range.Buy on Weakness = Short- to Medium-term positiveness anticipated, but technical readings are still negative. Traders can pick-up the stock for future rally.Sell on Strength = Short-term momentum still positive, Traders are advice to lock in profit base on current strength.Take Profit = Short-term target achieved. Traders are advice to exit before the technical readings turn bearish.Avoid = Risky situation in the short-term and high volatility expected on the share price. Traders’ best strategy is staying away until it stabilises.

Technical Time Frame:Immediate-term = short time frame within a contra period.Short-term = moderate time frame within two to three contra periods. For tracking purposes, we refer to 10 trading days.Medium-term = medium time frame usually refers to two to three weeks period. For tracking purposes, we refer to 20 trading days.

Technical recommendations are generally short-term in nature and may differ from RHBRI’s equity fundamental view and recommendation on the same company.

RHBRI is a participant of the CMDF-Bursa Research Scheme and will receive compensation for the participation. Additional information on recommendedsecurities, subject to the duties of confidentiality, will be made available upon request.

This report may not be reproduced or redistributed, in whole or in part, without the written permission of RHBRI and RHBRI accepts no liability whatsoever for theactions of third parties in this respect.

Related Documents