Market size and tax competition Gianmarco I.P. Ottaviano, Tanguy van Ypersele

Market size and tax competition Gianmarco I.P. Ottaviano, Tanguy van Ypersele.

Dec 18, 2015

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

Market size and tax competition

Gianmarco I.P. Ottaviano,

Tanguy van Ypersele

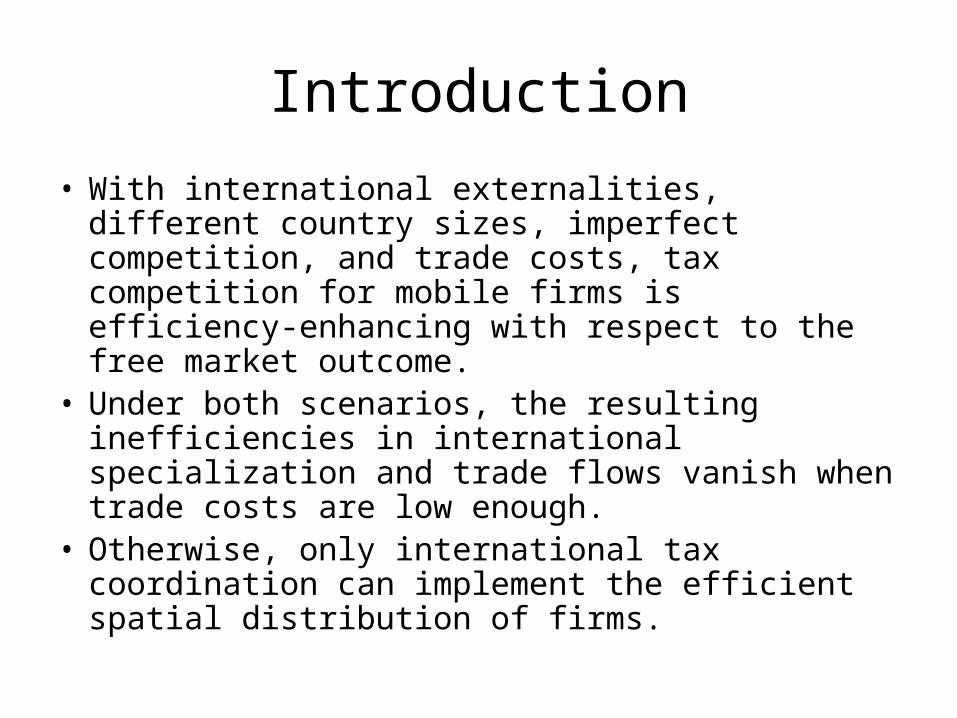

Introduction

• With international externalities, different country sizes, imperfect competition, and trade costs, tax competition for mobile firms is efficiency-enhancing with respect to the free market outcome.

• Under both scenarios, the resulting inefficiencies in international specialization and trade flows vanish when trade costs are low enough.

• Otherwise, only international tax coordination can implement the efficient spatial distribution of firms.

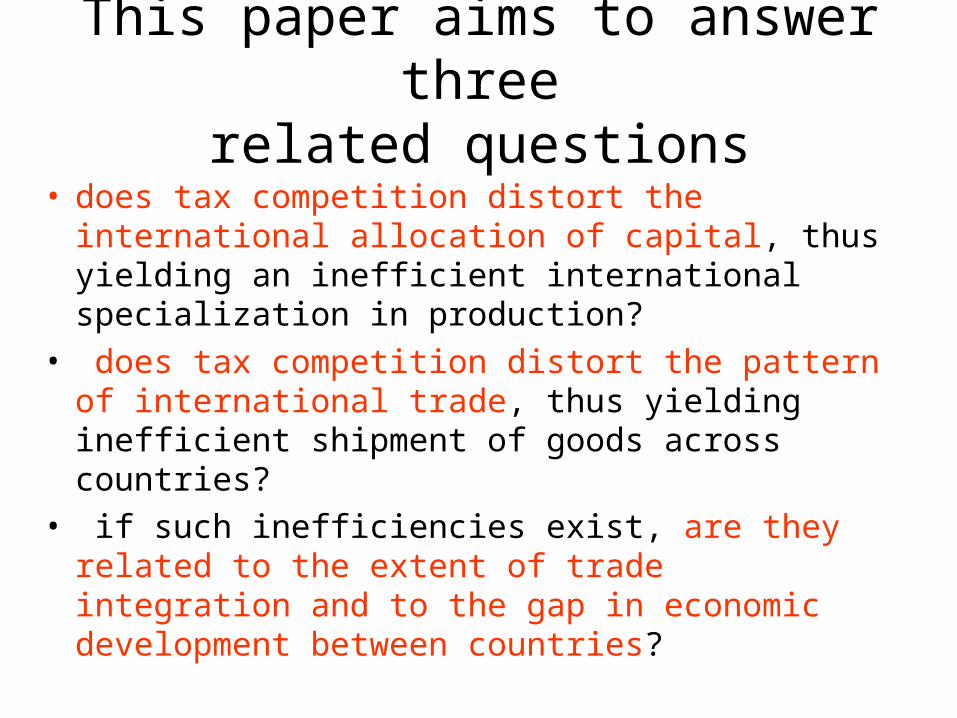

This paper aims to answer threerelated questions

• does tax competition distort the international allocation of capital, thus yielding an inefficient international specialization in production?

• does tax competition distort the pattern of international trade, thus yielding inefficient shipment of goods across countries?

• if such inefficiencies exist, are they related to the extent of trade integration and to the gap in economic development between countries?

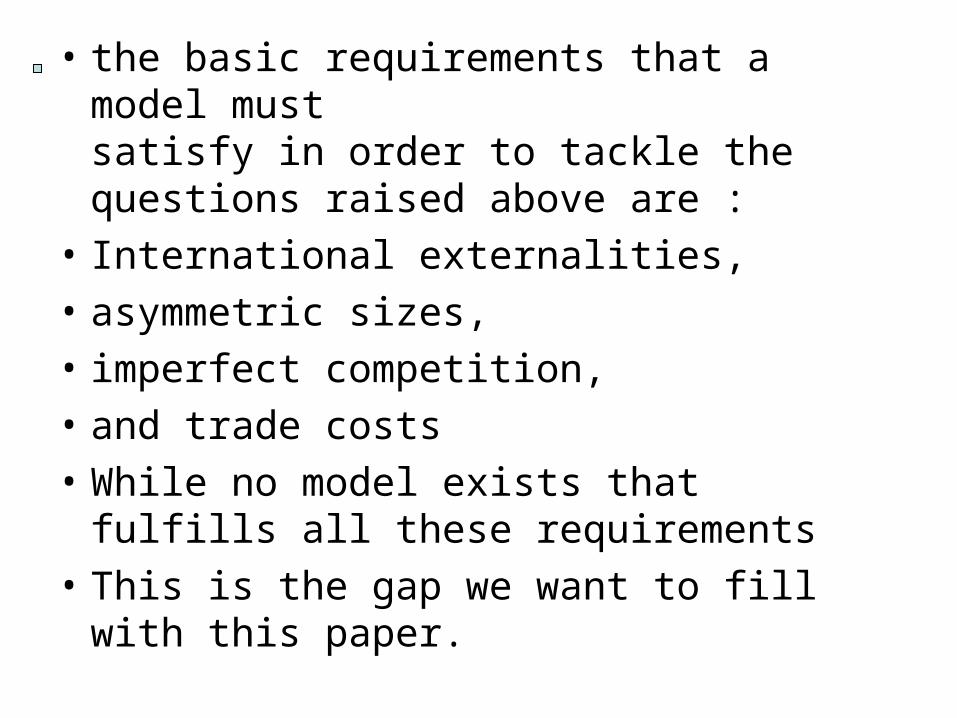

• the basic requirements that a model mustsatisfy in order to tackle the questions raised above are :

• International externalities,

• asymmetric sizes,

• imperfect competition,

• and trade costs

• While no model exists that fulfills all these requirements

• This is the gap we want to fill with this paper.

• The first develops a general equilibrium model in which two countries compete for monopolistically competitive firms.

• The second section characterizes the free market outcome.

• In the third section, this outcome is shown to be inefficient, unless trade costs are low enough.

• The fourth section characterizes the tax competitive outcome.

• The fifth section shows that, unless firms are all clustered in one country, tax competition is efficiency-enhancing with respect to the free market.

• The sixth section concludes.

The model

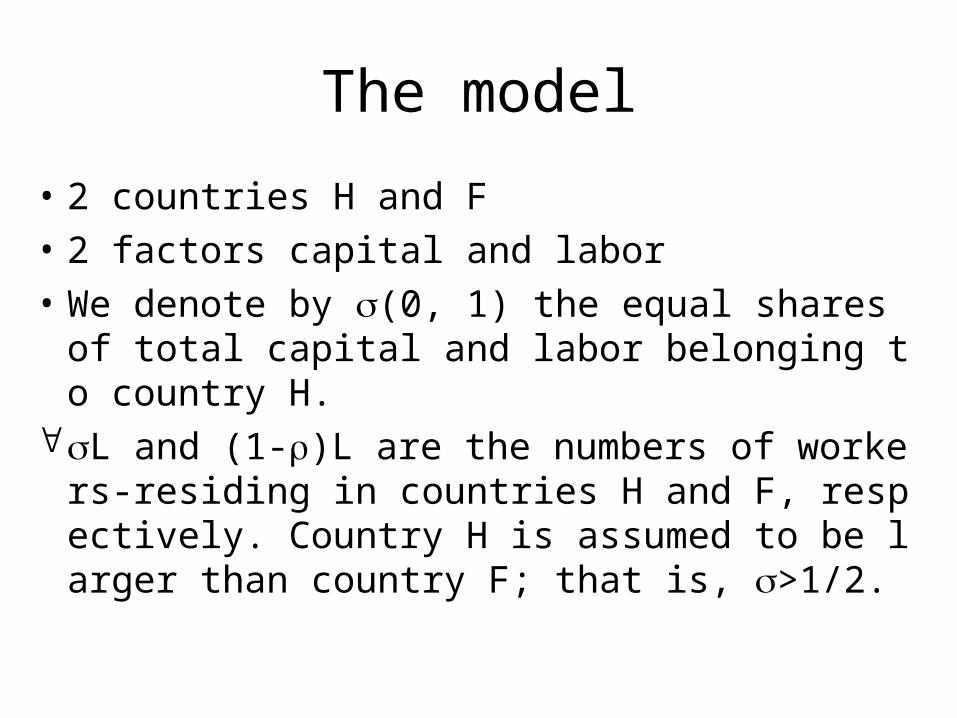

• 2 countries H and F

• 2 factors capital and labor

• We denote by (0, 1) the equal shares of total capital and labor belonging to country H.

L and (1-)L are the numbers of workers-residing in countries H and F, respectively. Country H is assumed to be larger than country F; that is, >1/2.

Preferences

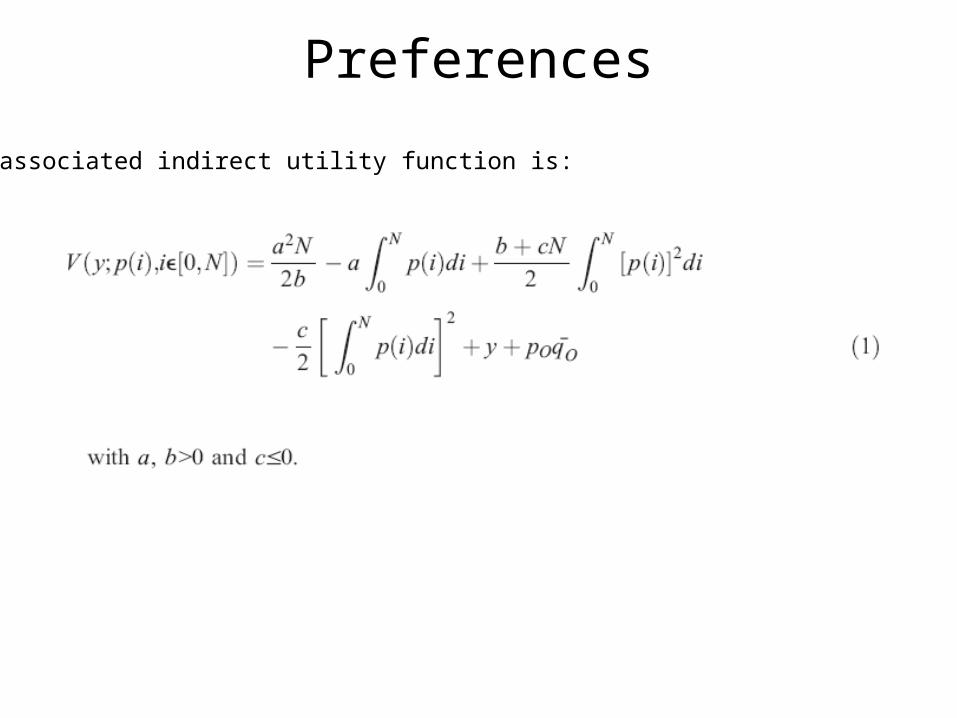

The associated indirect utility function is:

Technology

• The differentiated varieties and the homogeneous good are supplied by two different sectors, modern and traditional.

• The modern sector under increasing returns to scale and monopolistic competition.

• The traditional sector produces its homogeneous good under constant returns to scale and perfect competition.

International mobility

• While the traditional good is assumed to be freely traded, the modern good faces trade costs.

• Workers are immobile and supply labor only to their countries of residence. They can, however, invest their capital freely wherever they want.

Free market equilibrium

• workers maximize utility given their budget constraints

• firms maximize profits given their technological constraints

• all markets clear

• we choose the freely traded homogenous good as nume´raire.

• international wage is unity.

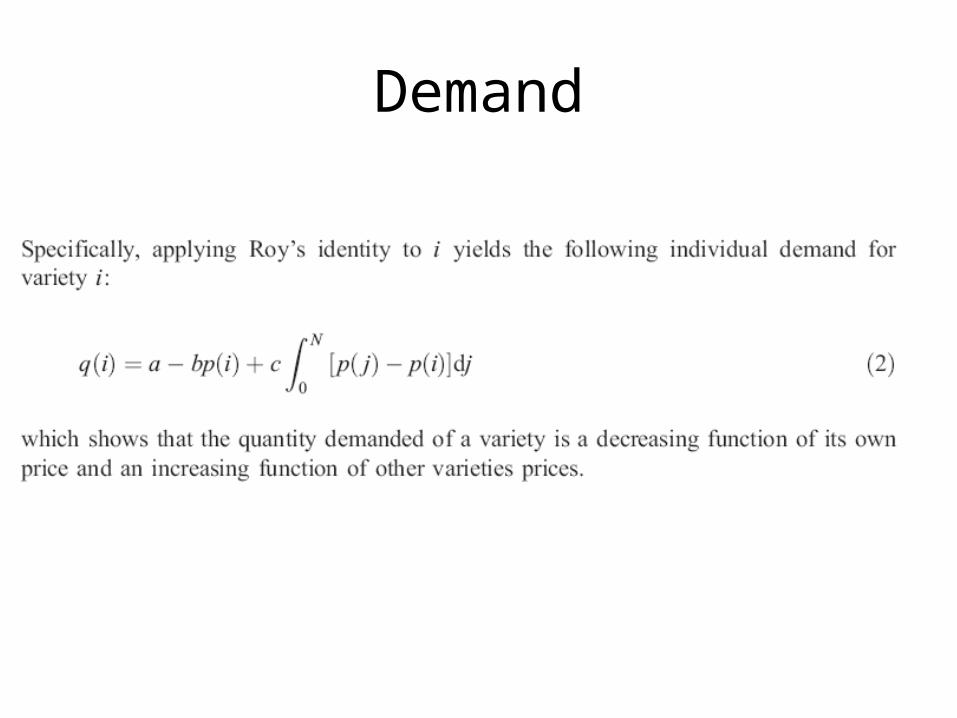

Demand

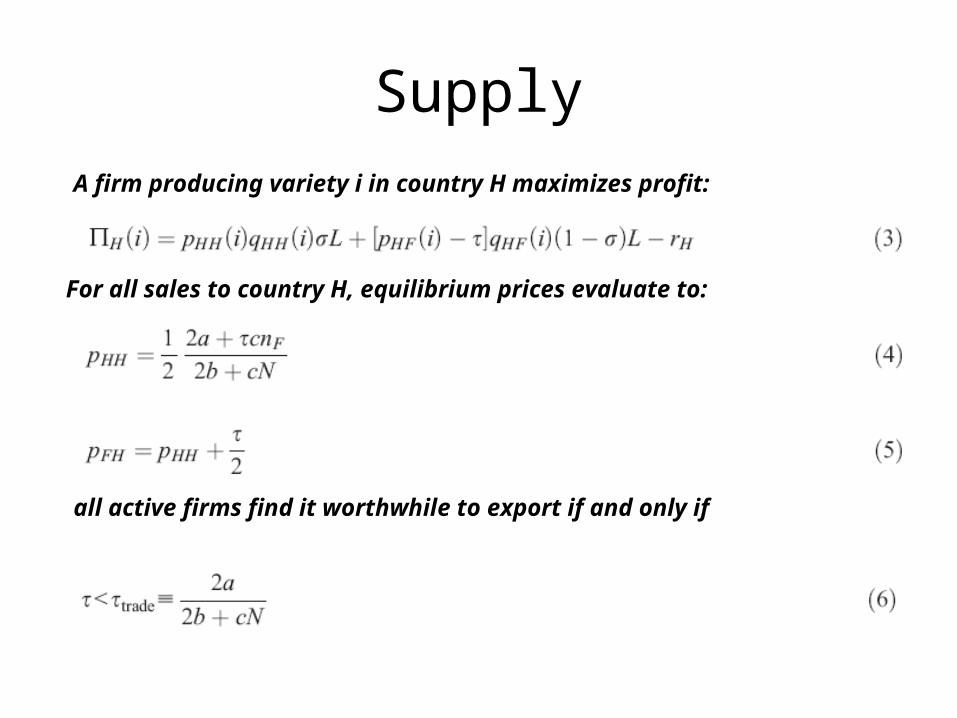

SupplyA firm producing variety i in country H maximizes profit:

For all sales to country H, equilibrium prices evaluate to:

all active firms find it worthwhile to export if and only if

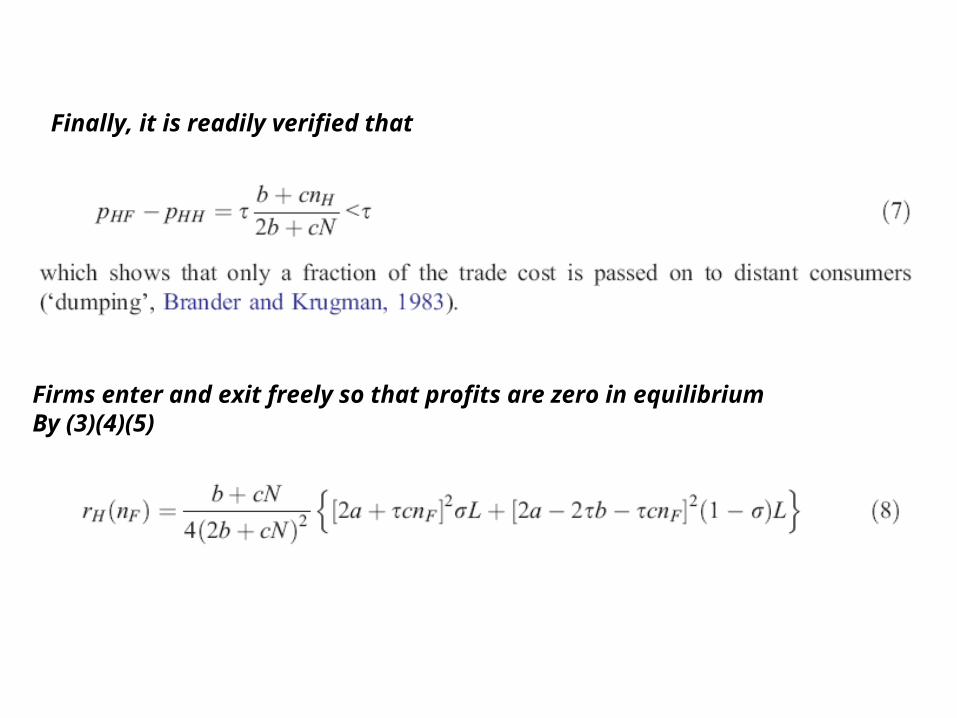

Finally, it is readily verified that

Firms enter and exit freely so that profits are zero in equilibriumBy (3)(4)(5)

Market clearing

• There are four markets: for the modern and the traditional goods, for capital and labor.

• In the modern sector, market clearing is ensured by the profit maximizing choices of firms facing downward sloping demand curves.

• In the traditional sector, market clearing is granted by the fact that, as discussed above, given quasi-linear utility, traditional consumption absorbs any supply not used as trade cost.

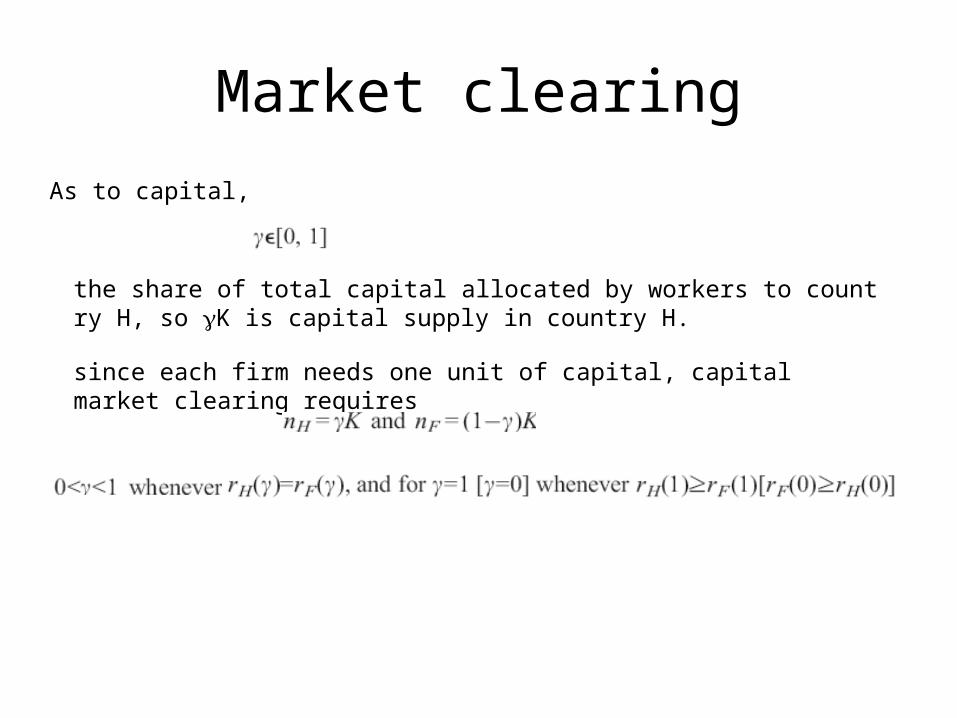

Market clearing

As to capital,

the share of total capital allocated by workers to country H, so K is capital supply in country H.

since each firm needs one unit of capital, capital market clearing requires

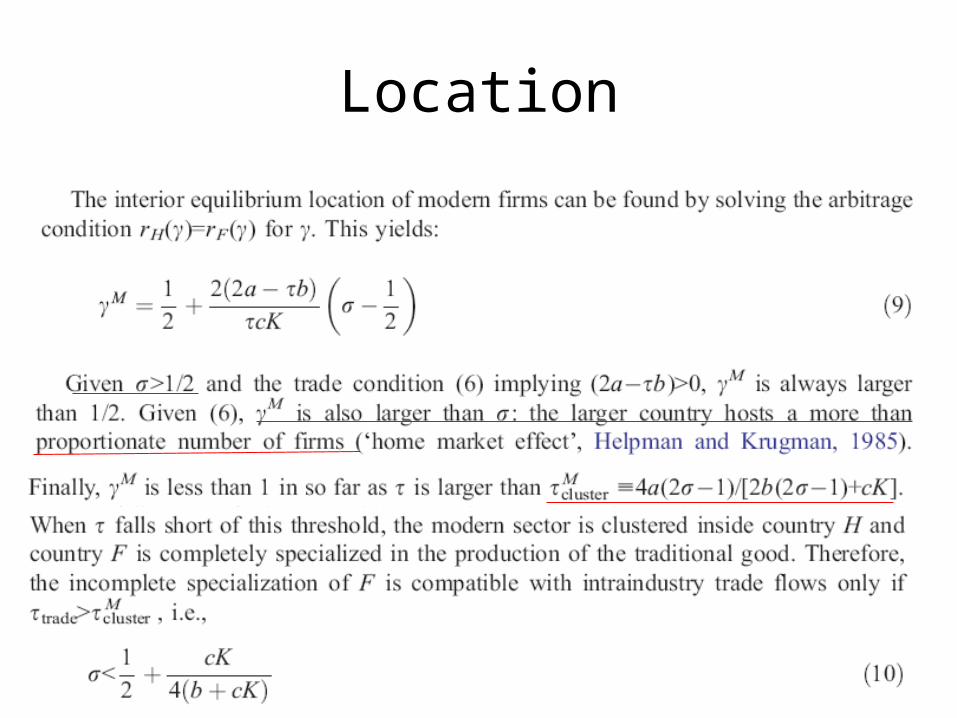

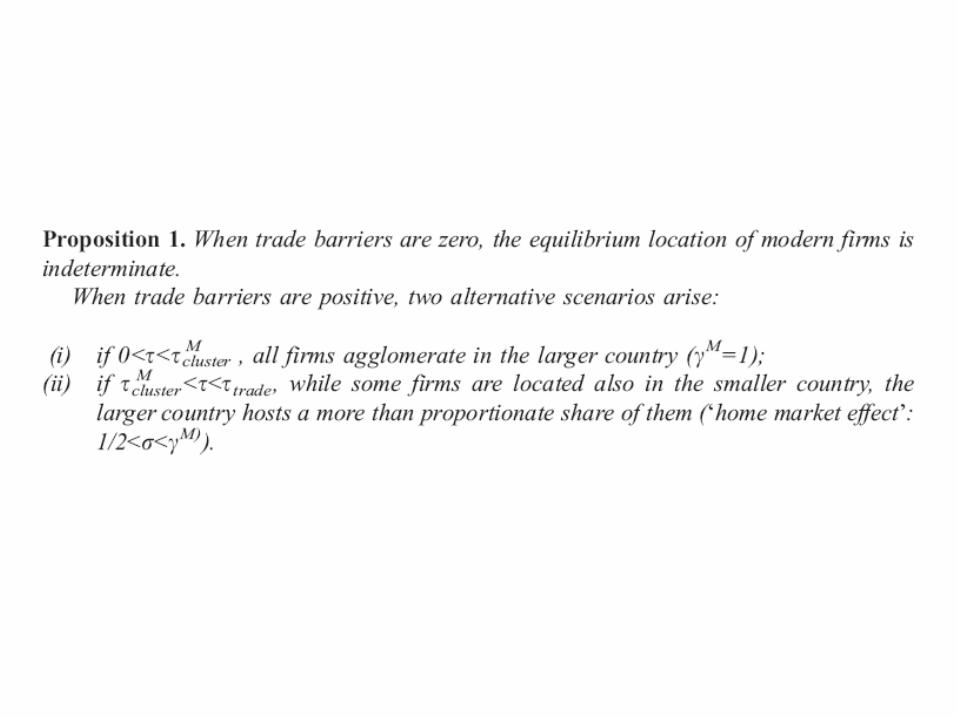

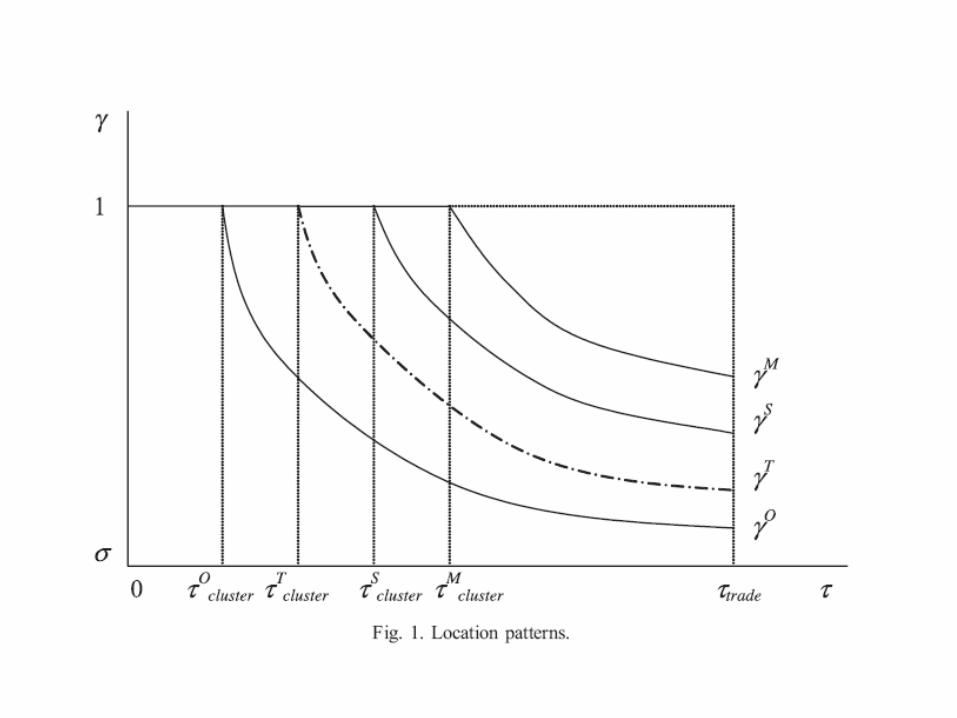

Location

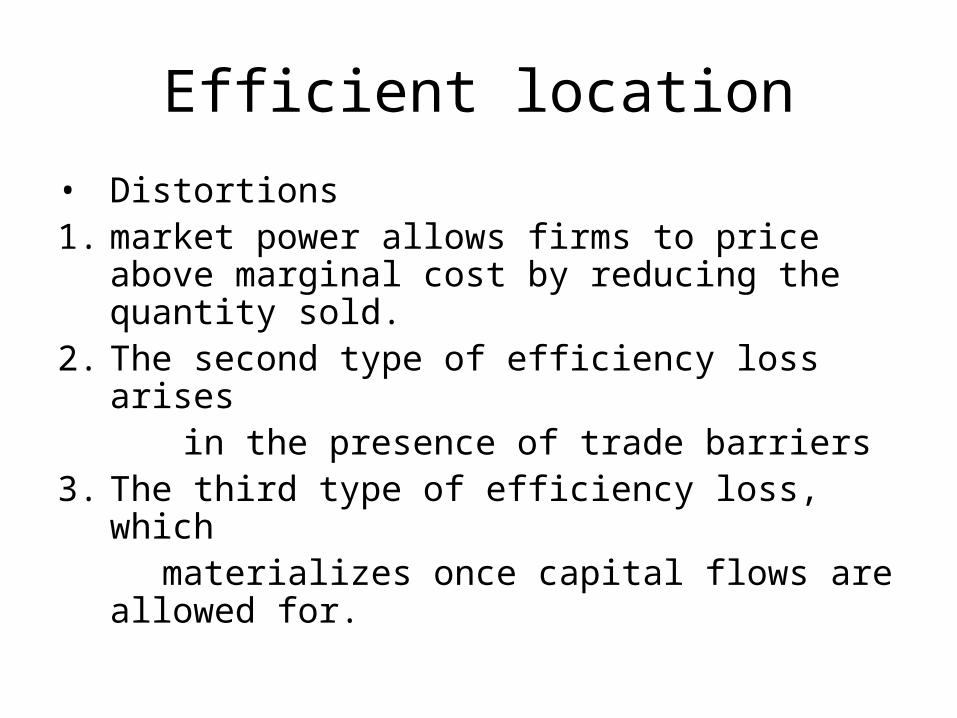

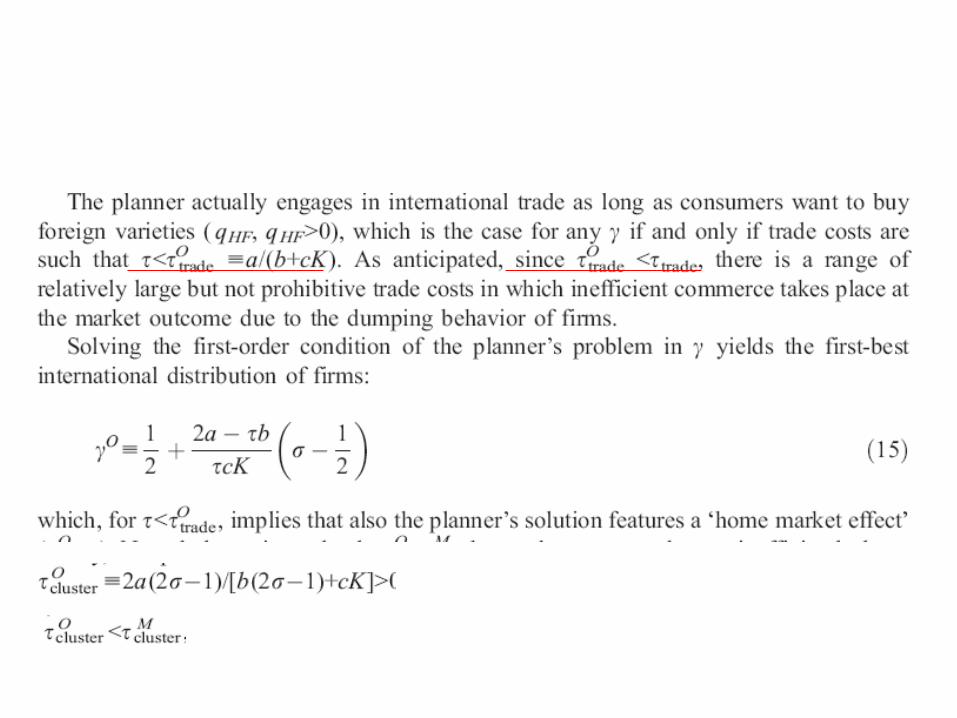

Efficient location

• Distortions1. market power allows firms to price above

marginal cost by reducing the quantity sold.

2. The second type of efficiency loss arises in the presence of trade barriers3. The third type of efficiency loss, which materializes once capital flows are

allowed for.

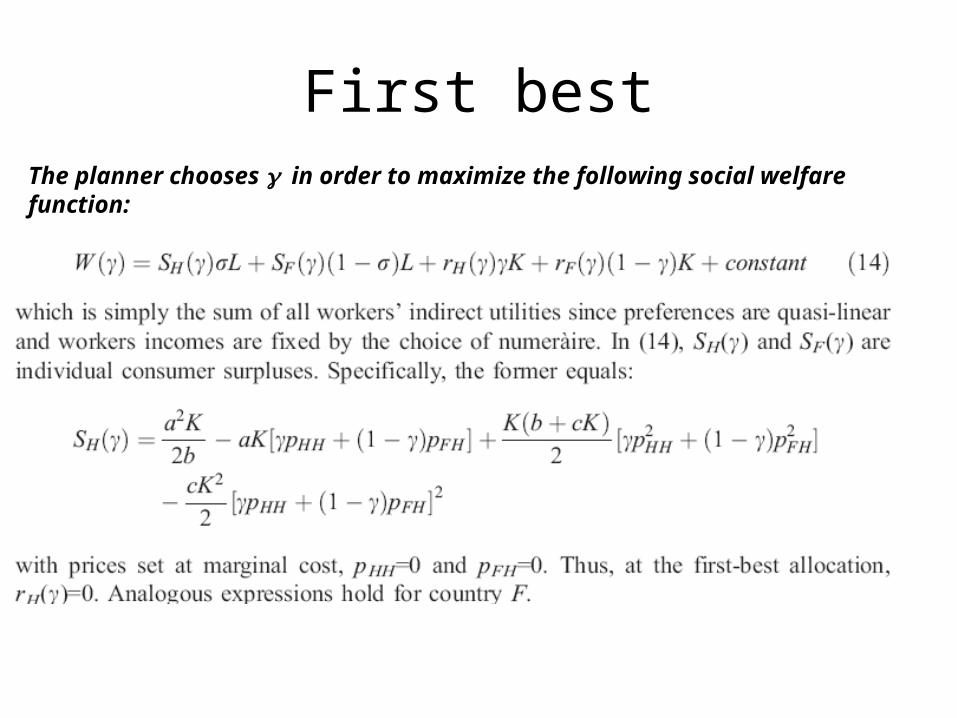

First bestThe planner chooses in order to maximize the following social welfare function:

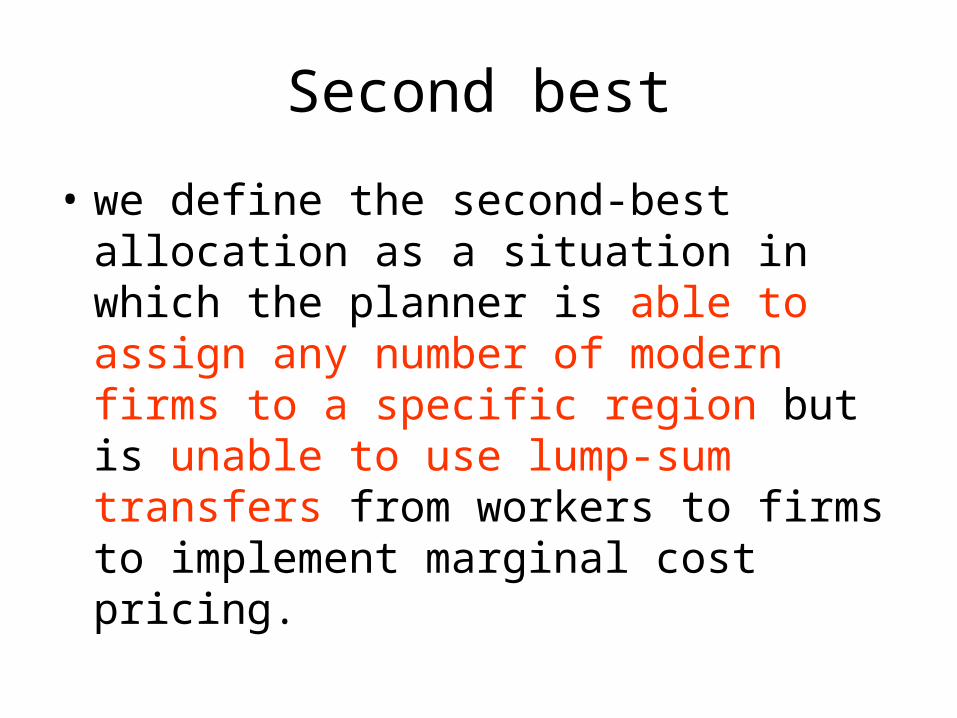

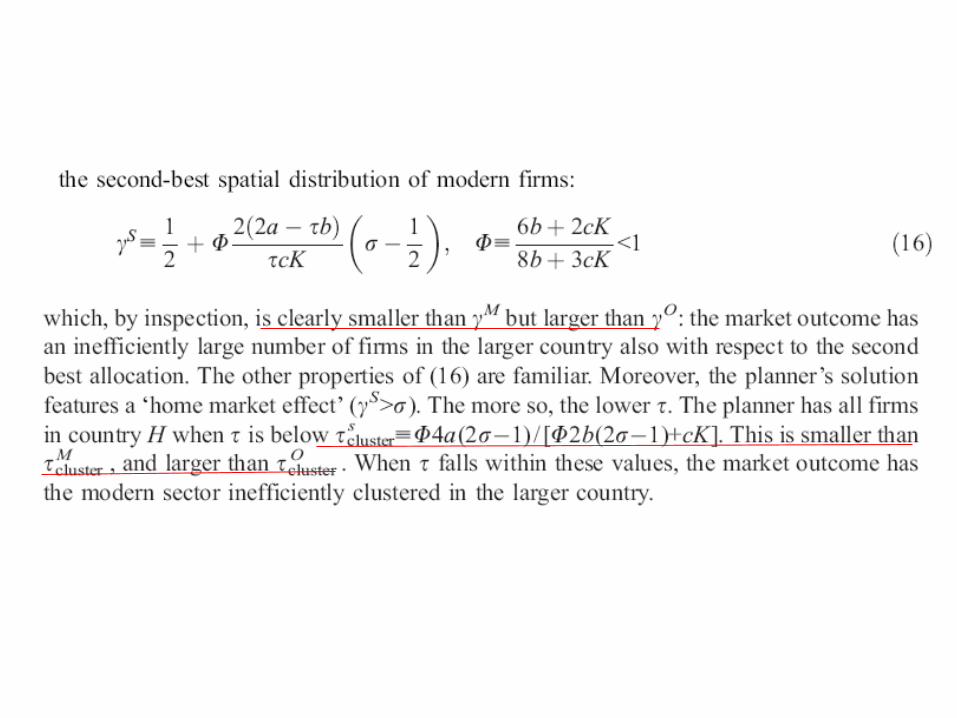

Second best

• we define the second-best allocation as a situation in which the planner is able to assign any number of modern firms to a specific region but is unable to use lump-sum transfers from workers to firms to implement marginal cost pricing.

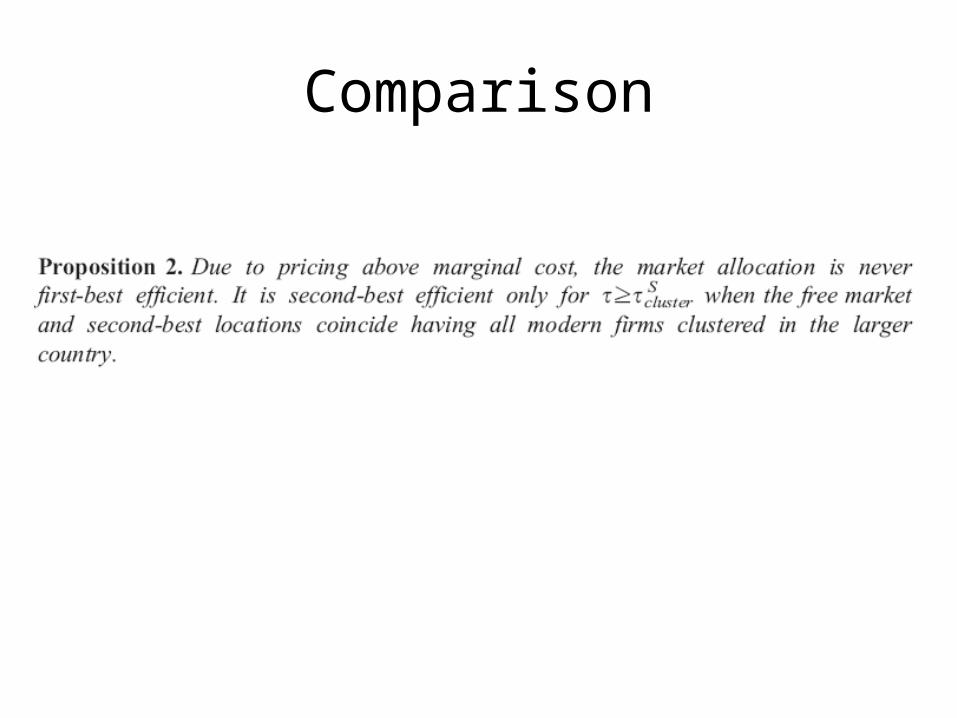

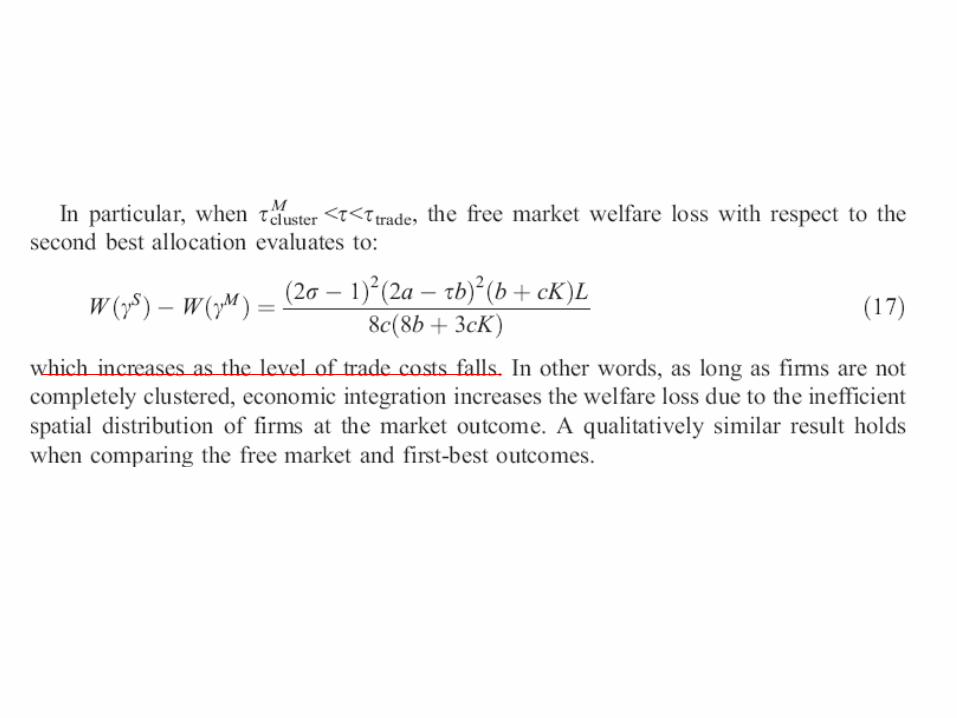

Comparison

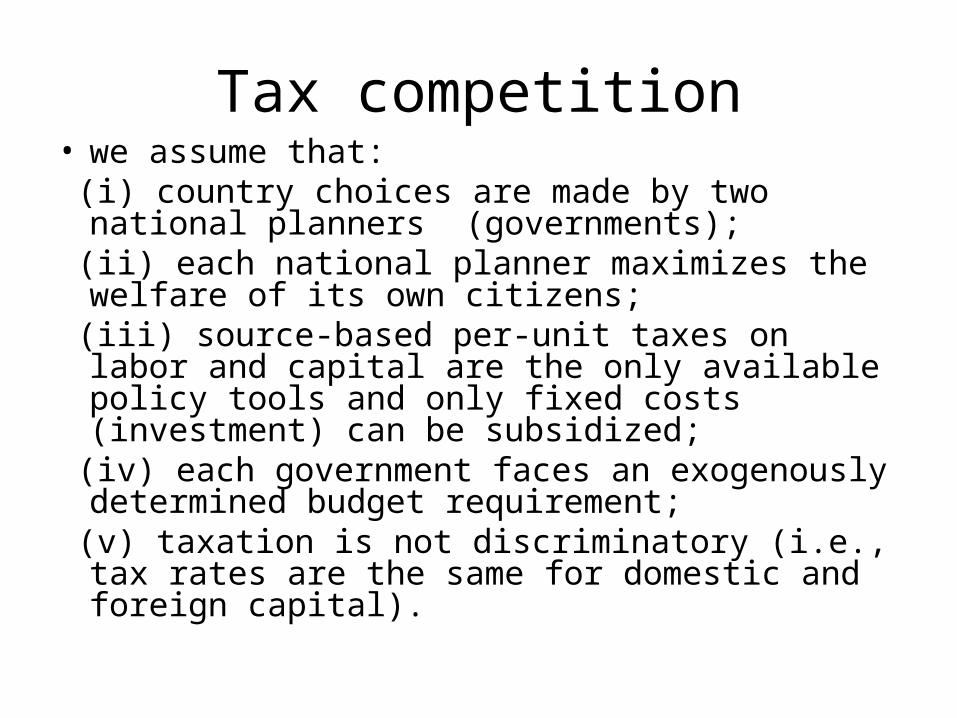

Tax competition• we assume that: (i) country choices are made by two national

planners (governments); (ii) each national planner maximizes the welfare of

its own citizens; (iii) source-based per-unit taxes on labor and

capital are the only available policy tools and only fixed costs (investment) can be subsidized;

(iv) each government faces an exogenously determined budget requirement;

(v) taxation is not discriminatory (i.e., tax rates are the same for domestic and foreign capital).

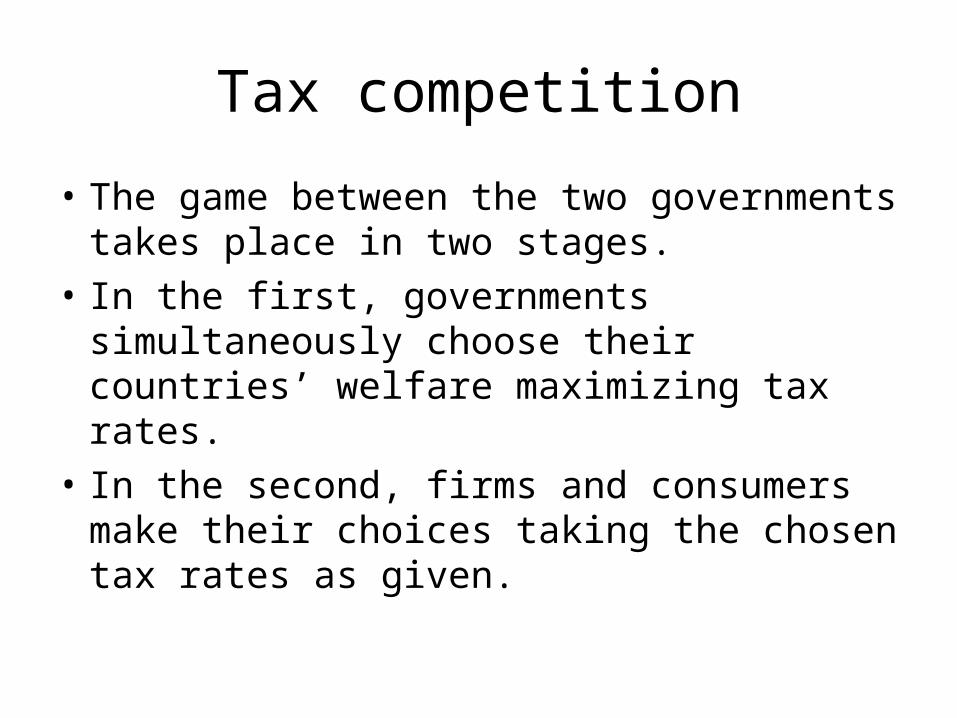

Tax competition

• The game between the two governments takes place in two stages.

• In the first, governments simultaneously choose their countries’ welfare maximizing tax rates.

• In the second, firms and consumers make their choices taking the chosen tax rates as given.

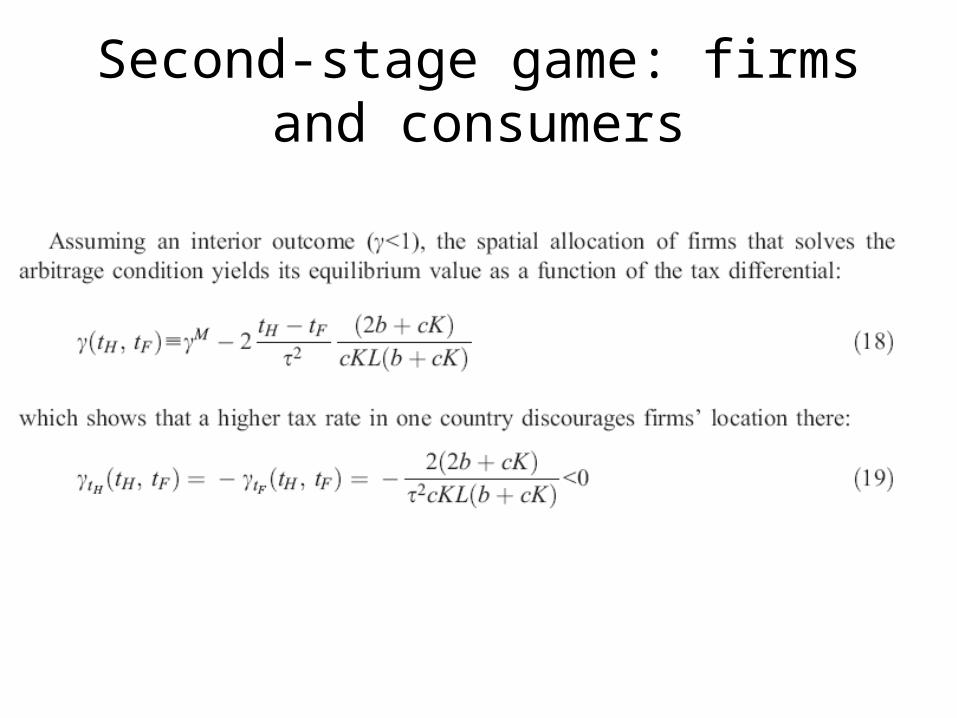

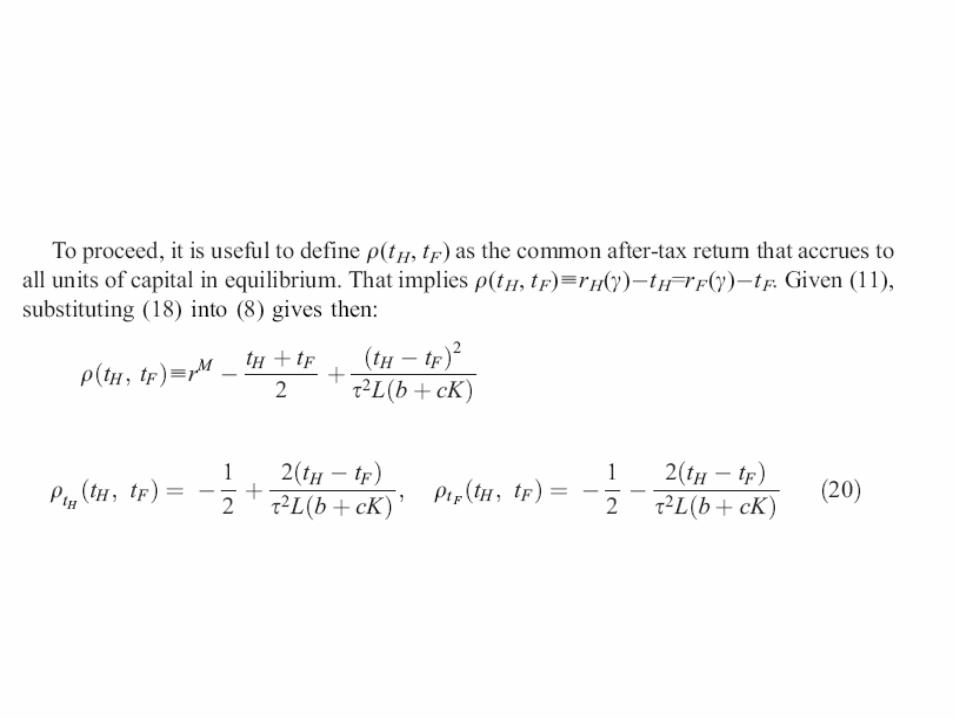

Second-stage game: firms and consumers

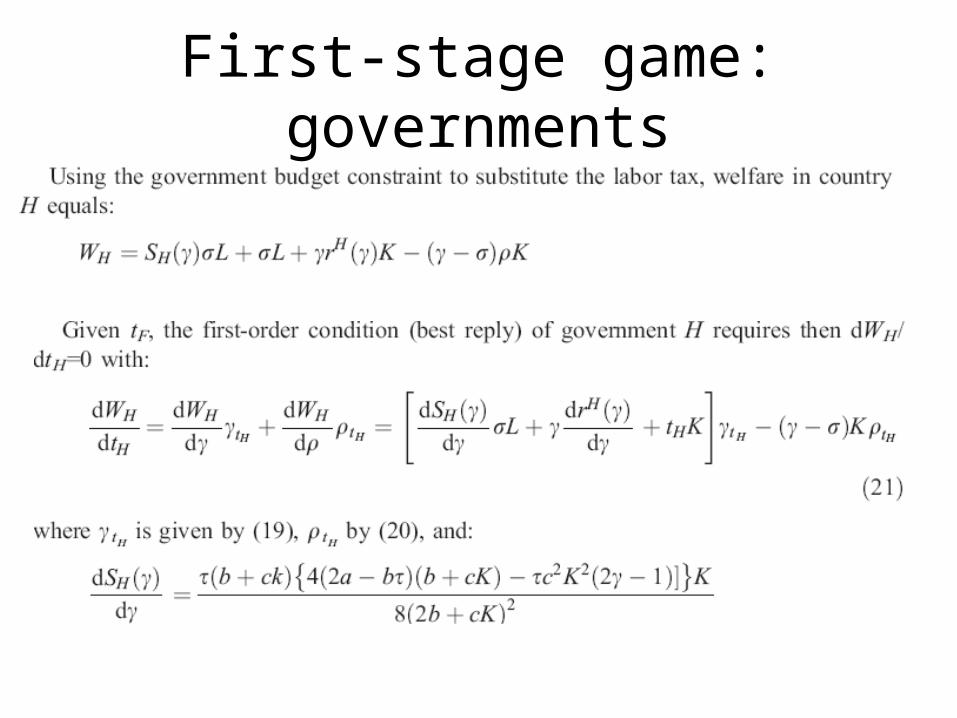

First-stage game: governments

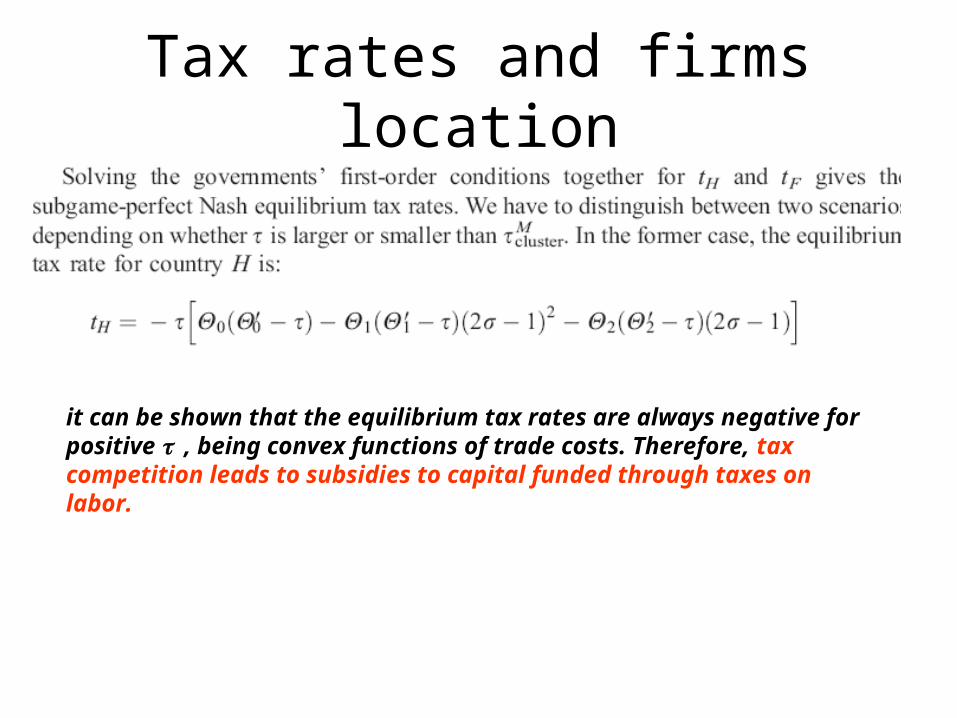

Tax rates and firms location

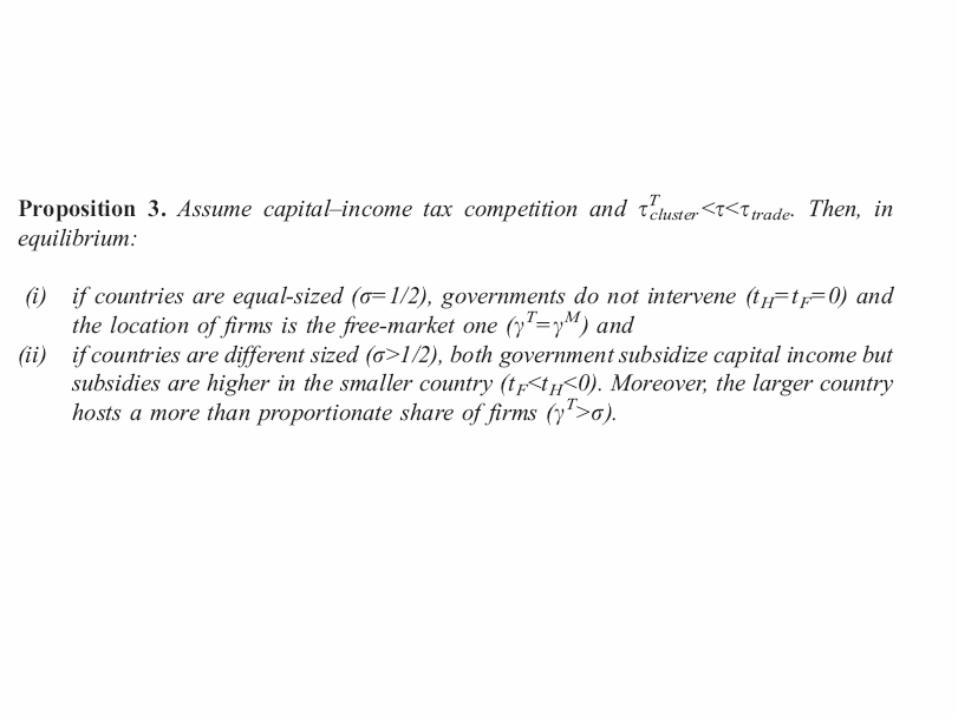

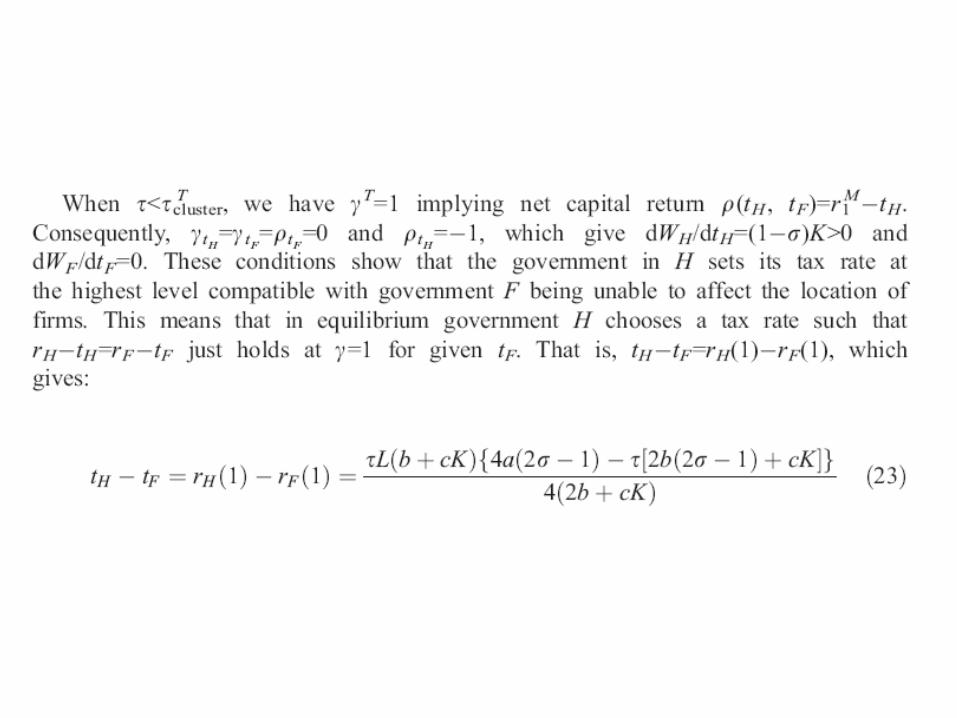

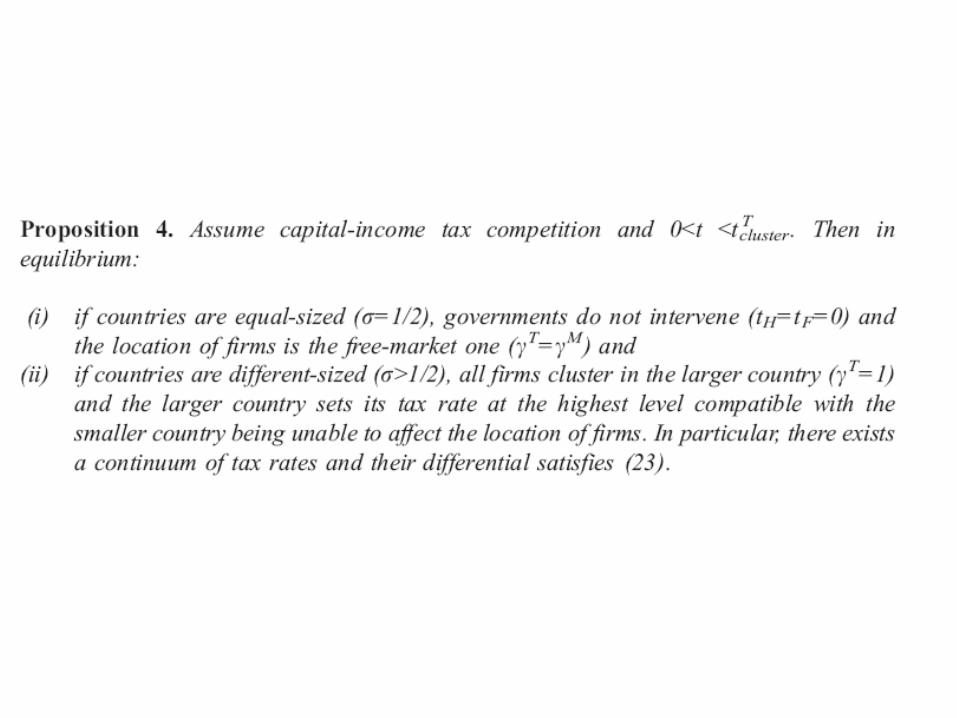

it can be shown that the equilibrium tax rates are always negative for positive , being convex functions of trade costs. Therefore, tax competition leads to subsidies to capital funded through taxes on labor.

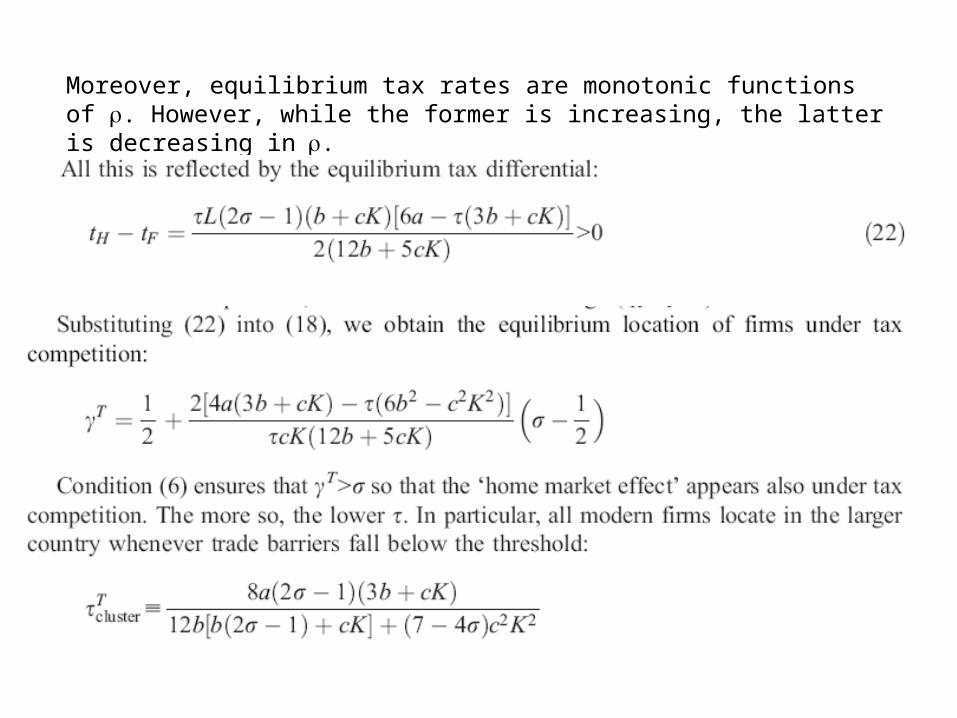

Moreover, equilibrium tax rates are monotonic functions of . However, while the former is increasing, the latter is decreasing in.

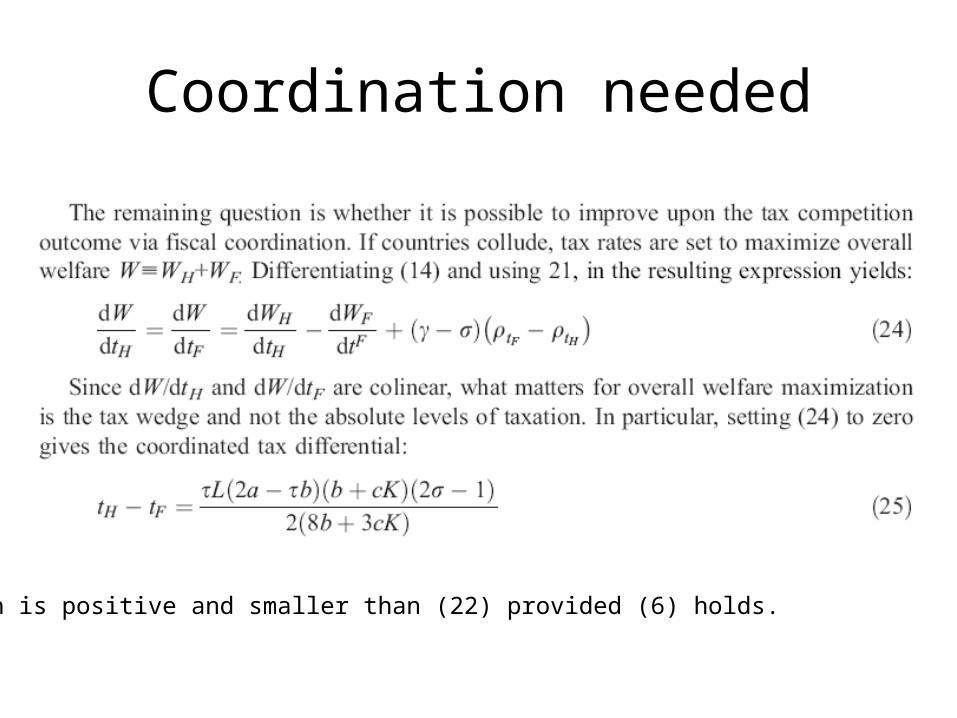

Coordination needed

which is positive and smaller than (22) provided (6) holds.

• Coordination improves overall welfare, a natural question to ask is whether it improves the welfare of both countries.

• Since the coordinated outcome is a tax wedge, there is a degree of freedom left. Increasing the level of capital taxation while keeping the tax differential at (25) allows governments to transfer resources from the capital exporting country to the capital-importing one. In other words, the choice of the level of capital taxation can be used as an indirect side payment mechanism in order to make coordination not only efficient but also Pareto-improving

• under tax competition the tax rate is inefficiently high in the larger home country and inefficiently low in the smaller foreign one. The reason is the presence of a fiscal externality.

Conclusion

• the policy attitude towards tax competition should depend on the degree of trade integration.

• at the initial stages of an integration process, forbidding tax competition without agreeing on tax coordination is a bad idea.

Related Documents