ALTECH Environmental Consulting Ltd. Marbek Resource Consultlants 12 Banigan Drive, Toronto, M4H 1E9 300-222 Somerset St. W., Ottawa, ON K2P 2G3 Tel: (416) 467-5555 www.altech-group.com Tel: (613) 523-0784 www.marbek.ca Market Profile and Conservation Opportunity Assessment for Small and Medium-Sized Industry in Ontario Prepared for: Conservation Bureau (Ontario Power Authority) Prepared by: Altech Environmental Consulting In association with: Marbek Resource Consultants FINAL REPORT September 2006

Welcome message from author

This document is posted to help you gain knowledge. Please leave a comment to let me know what you think about it! Share it to your friends and learn new things together.

Transcript

ALTECH Environmental Consulting Ltd. Marbek Resource Consultlants 12 Banigan Drive, Toronto, M4H 1E9 300-222 Somerset St. W., Ottawa, ON K2P 2G3 Tel: (416) 467-5555 www.altech-group.com Tel: (613) 523-0784 www.marbek.ca

Market Profile and Conservation Opportunity Assessment

for Small and Medium-Sized Industry in Ontario

Prepared for: Conservation Bureau (Ontario Power Authority)

Prepared by: Altech Environmental Consulting

In association with:

Marbek Resource Consultants

FINAL REPORT

September 2006

TABLE OF CONTENTS

1. INTRODUCTION..............................................................................................................3 1.1 Study Context and Outcomes...................................................................................3 1.2 Report Presentation..................................................................................................3

2. STUDY SCOPE, APPROACH AND MODELLING PLATFORM .............................4 2.1 Study Scope .............................................................................................................4 2.2 Industrial Model Description ...................................................................................6

3. BASE YEAR PROFILE AND REFERENCE CASE.....................................................9 3.1 Basre Year Profile....................................................................................................9 3.2 Reference Case Forecast ........................................................................................13

4. ECONOMIC ASSESSMENT OF CDM MEASURES.................................................14 4.1 Methodology..........................................................................................................14 4.2 CDM Measures ......................................................................................................17 4.3 Results....................................................................................................................19

5. ECONOMIC POTENTIAL SCENARIO......................................................................21 5.1 Methodology..........................................................................................................21 5.2 Summary of Economic Potential Forecast – Energy Efficiency ...........................22 5.3 Sector Results.........................................................................................................25

6. ONTARIO SM INDUSTRY SITUATION ASSESSMENT AND PROGRAM CONCEPTS......................................................................................................................28 6.1 CDM Programming Targeted to the SM Industyr Sectors ....................................28

7. BEST PRACTICE CDM PROGRAMMING ...............................................................35 7.1 Underlying Strategic Elements ..............................................................................36 7.2 Keys to successful portfolio management .............................................................37 7.3 Other Programs ......................................................................................................38

8. AN ASSESSMENT OF BARRIERS IMPEDING CDM TAKE-UP...........................42 8.1 Some General Observations About Market Barriers .............................................42 8.2 LDC Managers Survey Results..............................................................................45

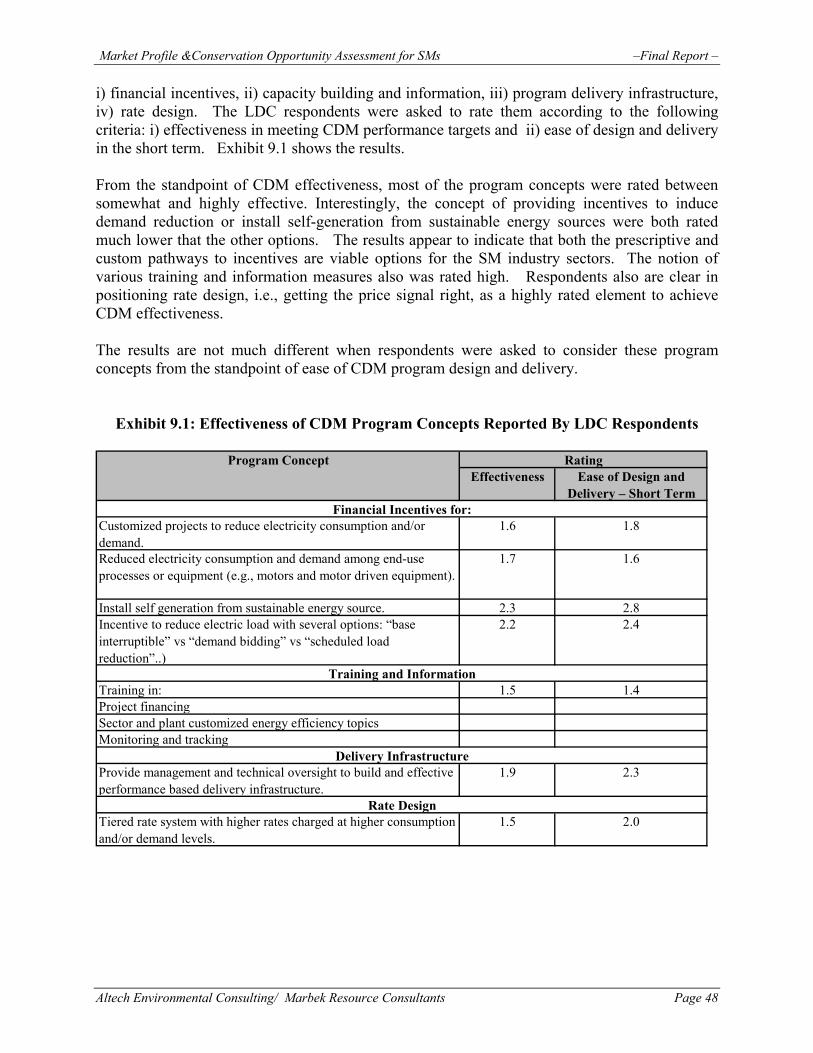

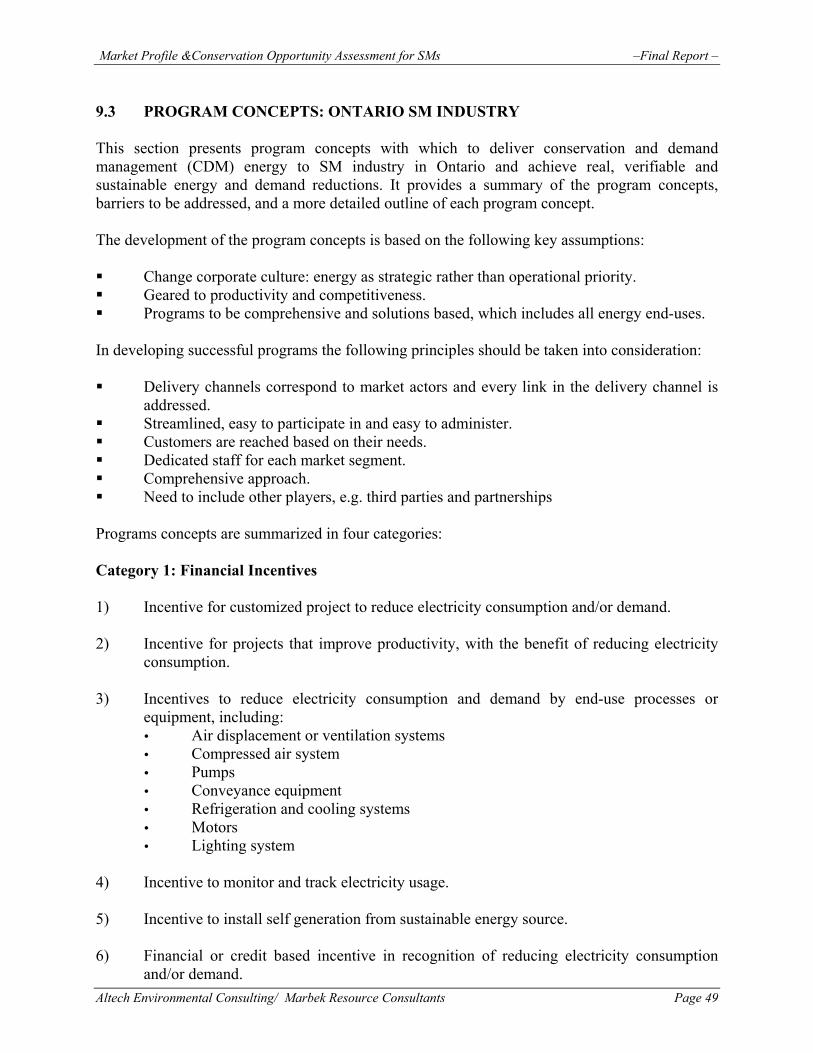

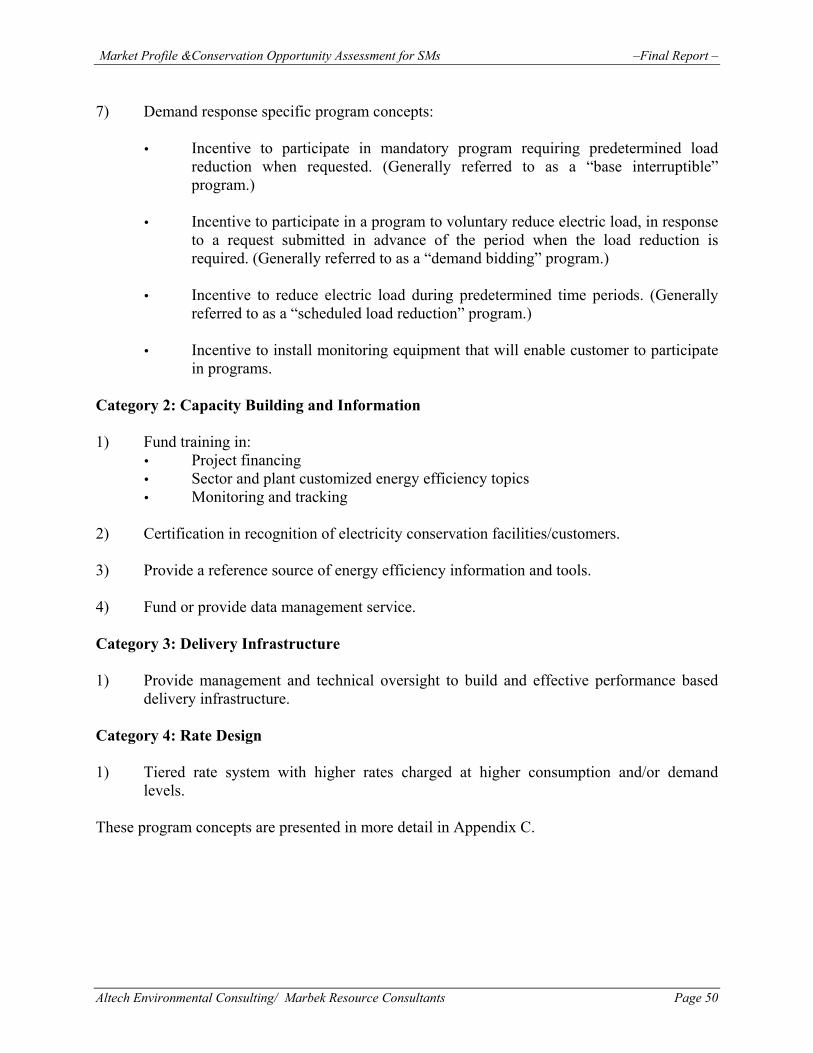

9. PROGRAM CONCEPTS................................................................................................47 9.1 Enabling Conditions for CDM in the SM Industry Markets..................................47 9.2 Program Concepts: LDC Survey ...........................................................................47 9.3 Program Concepts: Ontario SM Industry ..............................................................49

10. ACHIEVABLE POTENTIAL FORECAST .................................................................51 10.1 The Concept ...........................................................................................................51 10.2 The Achievable Potential Program Concepts ........................................................51 10.3 The Achievable Potential Assumptions .................................................................53 10.4 Results....................................................................................................................55 10.5 Observation, Uncertainties and Implications.........................................................62

APPENDIXES

APPENDIX A: ALLIANCES OF LOCAL DISTRIBUTION COMPANIES APPENDIX B: CALIFORNIA CDM PROGRAMS APPENDIX C: PROGRAM CONCEPTS FOR ONTARIO SM INDUSTRY

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 3

1. INTRODUCTION 1.1 STUDY CONTEXT AND OUTCOMES Ontario is facing a significant electrical supply challenge over the next several years. The OPA reports 25,000 MW of supply is going out of service by 2025 and needs upgrading. Such an investment will likely require an estimated $70 billion. Looking ahead, Conservation and Demand Management (CDM) will play an important role in the province’s electricity supply mix. It is important, therefore, for the OPA to have a clear picture of where and how electricity is being used in the various sectors of the economy, as well as where the CDM opportunities lie. Small and medium sized industry (hereafter referred to as SM industry) is a key target market for CDM in Ontario. Consequently, the OPA Conservation Bureau identified the need for a market scan of this sector to profile how electricity is used, where the CDM opportunities are and what types of program concepts might help overcome market barriers and achieve significant CDM performance. The key study outcomes are: A baseline profile of SM industry electricity consumption by sub-sector and energy end-

use. An analysis of the economic performance of CDM technical measures suitable to the SM

industry sectors. A profile of current CDM program activities directed to the SM industry sector.

An assessment of the barriers that impede take-up of cost-effective CDM measures in SM

industry. Characterization of CDM program concepts suitable to the SM industry sectors.

An estimate of the economic and achievable potential for CDM in SM industry.

1.2 REPORT PRESENTATION Section 1 of the report provides the context and background of the project, while Section 2 defines the scope, approach and modeling platform used in the study. A baseline profile and a reference case were developed for the SM industry and are presented in Section 3. The economic assessment of CDM measures and economic potential are respectively analyses in Sections 4 and 5. An assessment of CDM program concepts currently implemented by utilities, including best practices and barriers are discussed in Sections 6, 7 and 8. Program concepts applicable to the SM industry in Ontario and the achievable potential forecast are presented in Sections 9 and 10.

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 4

2. STUDY SCOPE, APPROACH AND MODELLING PLATFORM 2.1 STUDY SCOPE Study Period

The study covers the period from calendar year 2005 (base year) to 2025. The milestone years progress annually to 2010 with subsequent 5-year increments to 2025. Target Industry Sectors

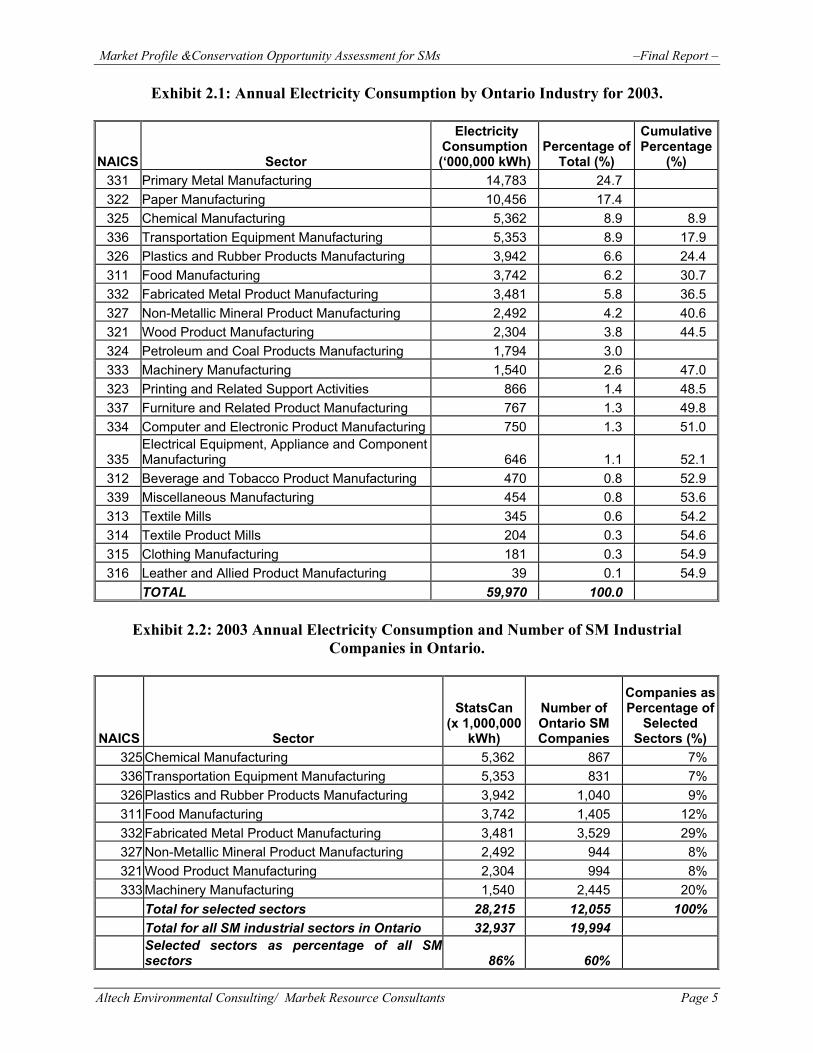

The target market for the study is all Ontario industry facilities with an average peak demand of < 1 MW. Given the budget and time constraints the OPA agreed to an approach whereby the analysis would focus on the SM industry sectors representing roughly 60% to 70% of the overall load in this market. Exhibit 2.1 below shows the break-down of all Ontario industry electricity sales based on Statistics Canada data for 2003, which was the latest data available at the time of the study. The SM portion of the following Ontario industrial sectors was considered to be minimal and these sectors were excluded from this study: Primary metal manufacturing Paper manufacturing Petroleum and coal products manufacturing.

When the SM portion is extracted from Exhibit 2.1, the results show that 55% of the total annual electricity is consumed by SM industry. Consequently, the study emphasizes the following sectors: Chemical manufacturing Transportation equipment manufacturing Plastics and rubber products Fabricated metal products Food manufacturing Wood products Machinery manufacturing Non-metalic minerals.

Exhibit 2.2 shows the 2003 annual electricity consumption for the selected industrial sectors. To profile the distribution of SM companies across the industrial sectors, Scott’s Canadian Business Directory and Database was used to determine the number of industrial companies in each sector. The results are provided in Exhibit 2.2 and indicate that the 8 selected industrial sectors accounts for 60% of all the SM facilities in Ontario. The geographic profile of annual electricity used by SM facilities in Ontario was developed with the aid of Scott’s Canadian Business Directory and Database. The number of facilities in each of the 8 industrial sectors was determined for each of the main Ontario census divisions, and was proportionally applied to the sectors’ total electricity consumption. The results are provided in Exhibit 2.3.

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 5

Exhibit 2.1: Annual Electricity Consumption by Ontario Industry for 2003.

NAICS Sector

Electricity Consumption (‘000,000 kWh)

Percentage of Total (%)

Cumulative Percentage

(%) 331 Primary Metal Manufacturing 14,783 24.7 322 Paper Manufacturing 10,456 17.4 325 Chemical Manufacturing 5,362 8.9 8.9 336 Transportation Equipment Manufacturing 5,353 8.9 17.9 326 Plastics and Rubber Products Manufacturing 3,942 6.6 24.4 311 Food Manufacturing 3,742 6.2 30.7 332 Fabricated Metal Product Manufacturing 3,481 5.8 36.5 327 Non-Metallic Mineral Product Manufacturing 2,492 4.2 40.6 321 Wood Product Manufacturing 2,304 3.8 44.5 324 Petroleum and Coal Products Manufacturing 1,794 3.0 333 Machinery Manufacturing 1,540 2.6 47.0 323 Printing and Related Support Activities 866 1.4 48.5 337 Furniture and Related Product Manufacturing 767 1.3 49.8 334 Computer and Electronic Product Manufacturing 750 1.3 51.0

335 Electrical Equipment, Appliance and Component Manufacturing 646 1.1 52.1

312 Beverage and Tobacco Product Manufacturing 470 0.8 52.9 339 Miscellaneous Manufacturing 454 0.8 53.6 313 Textile Mills 345 0.6 54.2 314 Textile Product Mills 204 0.3 54.6 315 Clothing Manufacturing 181 0.3 54.9 316 Leather and Allied Product Manufacturing 39 0.1 54.9

TOTAL 59,970 100.0

Exhibit 2.2: 2003 Annual Electricity Consumption and Number of SM Industrial Companies in Ontario.

NAICS Sector

StatsCan (x 1,000,000

kWh)

Number of Ontario SM Companies

Companies asPercentage of

Selected Sectors (%)

325 Chemical Manufacturing 5,362 867 7% 336 Transportation Equipment Manufacturing 5,353 831 7% 326 Plastics and Rubber Products Manufacturing 3,942 1,040 9% 311 Food Manufacturing 3,742 1,405 12% 332 Fabricated Metal Product Manufacturing 3,481 3,529 29% 327 Non-Metallic Mineral Product Manufacturing 2,492 944 8% 321 Wood Product Manufacturing 2,304 994 8% 333 Machinery Manufacturing 1,540 2,445 20%

Total for selected sectors 28,215 12,055 100% Total for all SM industrial sectors in Ontario 32,937 19,994

Selected sectors as percentage of all SM sectors 86% 60%

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 6

Exhibit 2.3: Geographic Profile of Annual Electricity Consumption SM Industrial

Companies in Ontario.

CDM Measures

The CDM measures assessed in the study refer to technical and operation and maintenance measures to improve energy efficiency and reduce peak demand for the major electricity end-uses in the SM industry sectors. CDM Program Concepts

The study examines the possible impacts of a suite of program concepts directed to the SM industry market. The program concepts are indicative only as the study scope does not include program design. 2.2 INDUSTRIAL MODEL DESCRIPTION Marbek’s customized spreadsheet model is the modelling platform for this study. The Industrial Energy Management Model (IEMM) enables clients to answer a wide variety of questions concerning the economic and market potentials for energy efficiency and fuel substitution in the industrial sector. The IEMM is capable of generating the following outputs: Economic and financial assessment of energy management measures, both operational

and capital, using various criteria: Total Resource Cost Test, simple and discounted

GTA58%

Central24%

East3%

Southwest13%

Northeast1%

Northwest1%

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 7

payback and IRR. Baseline profile of energy use and electricity demand by sub-sector and energy end-use.

Reference Case (Business as Usual) Forecast of energy use.

Technical and economic potentials for energy management (energy efficiency, peak load

management, fuel substitution and cogeneration). Market, or achievable potential, based on policy instruments and program concepts.

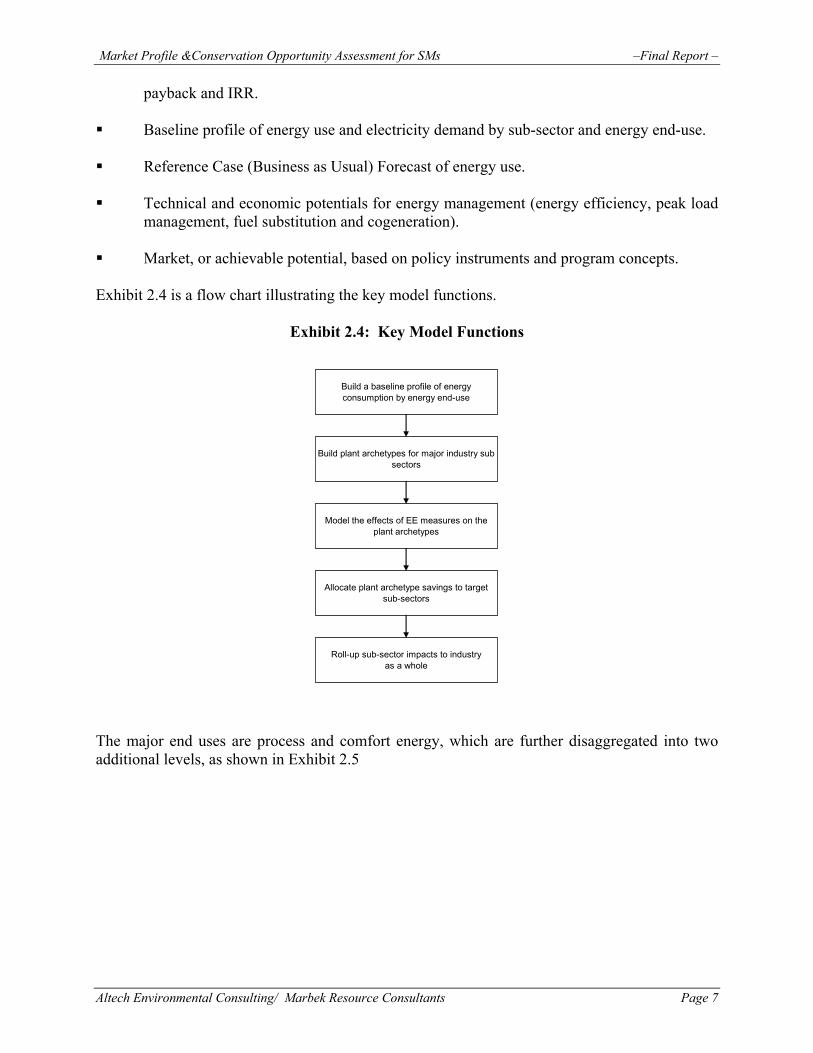

Exhibit 2.4 is a flow chart illustrating the key model functions.

Exhibit 2.4: Key Model Functions

Build a baseline profile of energy consumption by energy end-use

Build plant archetypes for major industry sub-sectors

Model the effects of EE measures on the plant archetypes

Allocate plant archetype savings to target sub-sectors

Roll-up sub-sector impacts to industry as a whole

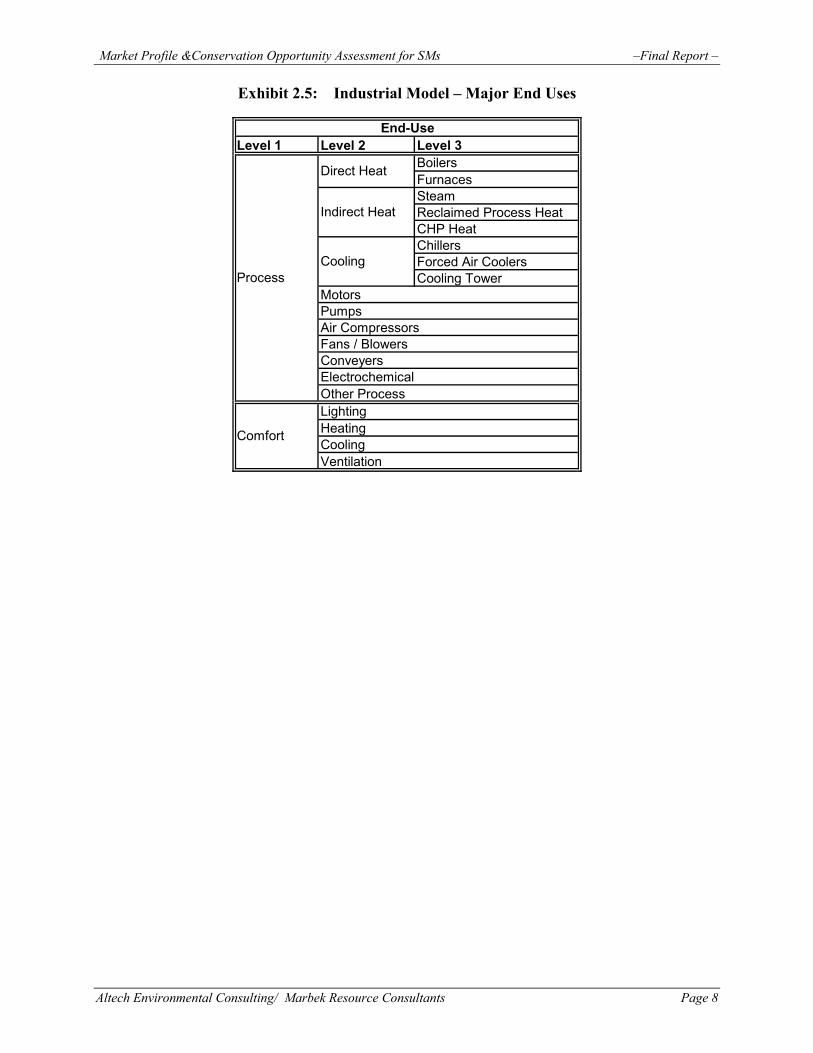

The major end uses are process and comfort energy, which are further disaggregated into two additional levels, as shown in Exhibit 2.5

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 8

Exhibit 2.5: Industrial Model – Major End Uses

Level 1 Level 2 Level 3BoilersFurnacesSteamReclaimed Process HeatCHP HeatChillersForced Air CoolersCooling Tower

MotorsPumpsAir CompressorsFans / BlowersConveyersElectrochemicalOther ProcessLightingHeatingCoolingVentilation

Comfort

End-Use

Process

Direct Heat

Indirect Heat

Cooling

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 9

3. BASE YEAR PROFILE AND REFERENCE CASE This section presents two main outputs: A profile of energy consumption in Ontario’s SM industrial sector in the base year of

2005. The Reference Case forecast of SM Industry electricity consumption to 2025.

3.1 BASE YEAR PROFILE The Base Year is the starting point for the analysis and, for this study, is calendar year 2005. The base year profile provides a detailed description of “where” and “how” energy is currently used in the Ontario SM industrial sector. The base year derivation comprises the following tasks. Build Plant Archetypes for EM Measure Application

In order to build a robust, defensible platform for the CDM potentials analysis it is necessary to establish a bottom-up, energy end-use profile of electricity use in the key SM industry sectors. The end-use profiles are established according to sector specific plant “archetypes”. The archetypical plant is a composite of energy use patterns, energy intensities and consumption levels within the particular target sub-sector (or a specific type of plant within a given sub-sector if there are substantial process differences).

Plant archetypes were developed for each of the 8 target sectors in SM industry. The archetypes were derived on the basis of two major information sources: i) consulting team in-house data and files and ii) secondary literature review. Compile actual base year utility data for electricity consumption

The energy end-use profile has to be calibrated to actual base year electricity consumption in the SM industry sectors. The preferred method is to obtain NAICS coded sales data from the utilities that can be sorted to the target SM industry sectors. A request for data structured in this way was sent to the Local Distribution Companies (LDCs). However, we learned that most of the LDCs do not have robust databases of this nature. In most cases they archive data according to rate class only. NAICS coding of customers is not frequently done, or when it is done, not maintained and updated. Consequently, the fall-back option used for the study was the Statistics Canada 2003 data. Allocate plant archetype end-use profiles to target sub-sectors

The plant archetype energy end-use profiles are allocated to the target sectors to which they pertain. We were able to establish a profile of the number of SM industry plants, by location, in Ontario. From this an average plant consumption was derived and the archetype end-use allocation was applied to the “average” plant size. This enabled a roll-up to the SM industry sector and then to all of the SM industry market as a whole.

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 10

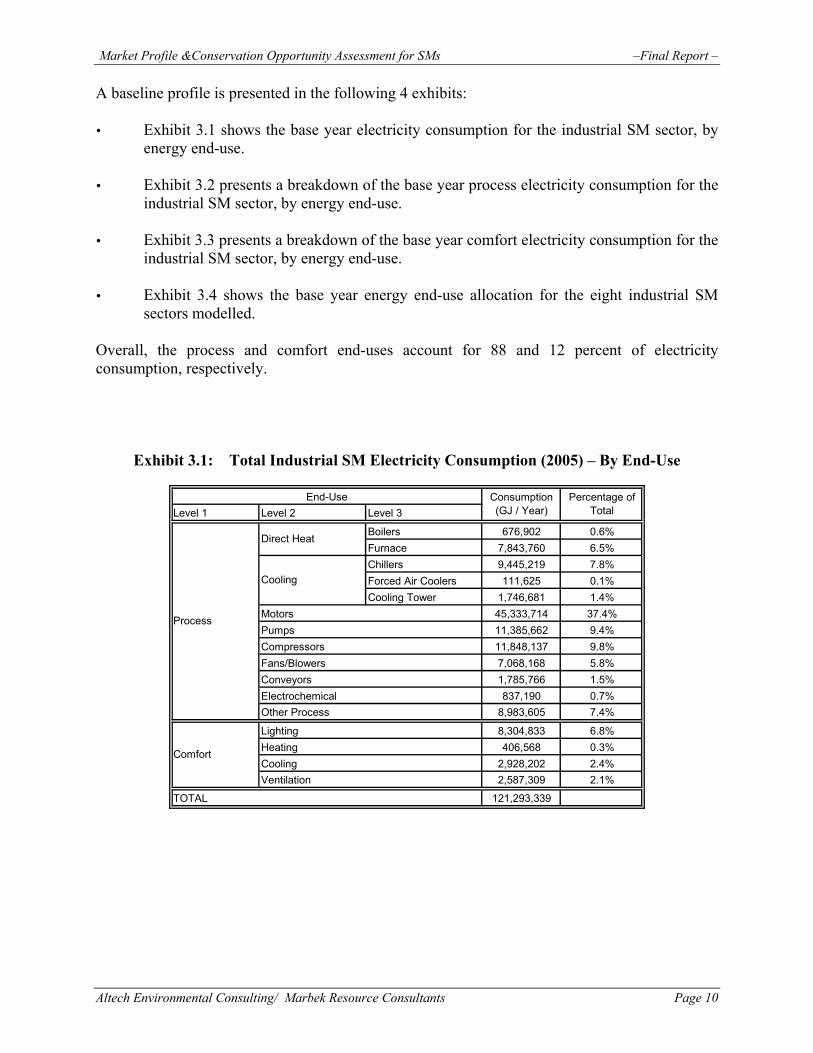

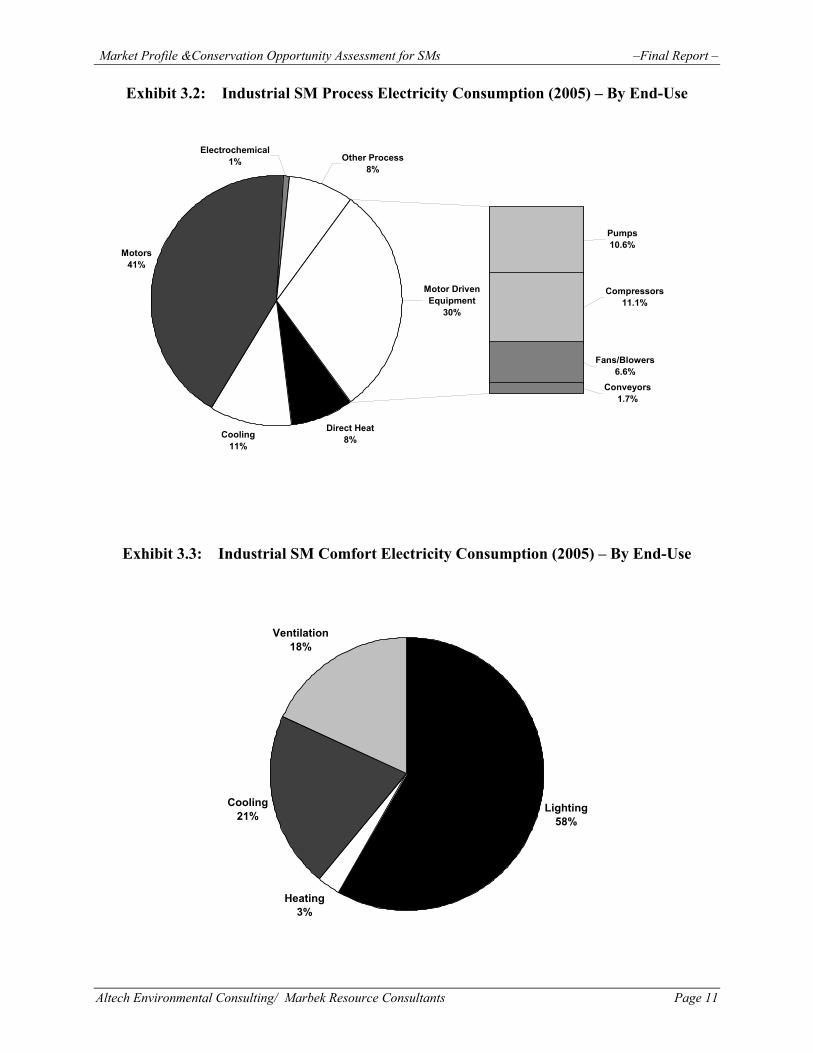

A baseline profile is presented in the following 4 exhibits: Exhibit 3.1 shows the base year electricity consumption for the industrial SM sector, by

energy end-use. Exhibit 3.2 presents a breakdown of the base year process electricity consumption for the

industrial SM sector, by energy end-use. Exhibit 3.3 presents a breakdown of the base year comfort electricity consumption for the

industrial SM sector, by energy end-use. Exhibit 3.4 shows the base year energy end-use allocation for the eight industrial SM

sectors modelled. Overall, the process and comfort end-uses account for 88 and 12 percent of electricity consumption, respectively.

Exhibit 3.1: Total Industrial SM Electricity Consumption (2005) – By End-Use

Level 1 Level 2 Level 3

Boilers 676,902 0.6%Furnace 7,843,760 6.5%Chillers 9,445,219 7.8%Forced Air Coolers 111,625 0.1%Cooling Tower 1,746,681 1.4%

Motors 45,333,714 37.4%Pumps 11,385,662 9.4%Compressors 11,848,137 9.8%Fans/Blowers 7,068,168 5.8%Conveyors 1,785,766 1.5%Electrochemical 837,190 0.7%Other Process 8,983,605 7.4%

Lighting 8,304,833 6.8%Heating 406,568 0.3%Cooling 2,928,202 2.4%Ventilation 2,587,309 2.1%

TOTAL 121,293,339

Cooling

Direct Heat

Process

Comfort

End-Use Consumption (GJ / Year)

Percentage of Total

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 11

Exhibit 3.2: Industrial SM Process Electricity Consumption (2005) – By End-Use

Direct Heat8%Cooling

11%

Motors41%

Pumps10.6%

Conveyors1.7%

Fans/Blowers6.6%

Compressors11.1%

Electrochemical1% Other Process

8%

Motor DrivenEquipment

30%

Exhibit 3.3: Industrial SM Comfort Electricity Consumption (2005) – By End-Use

Lighting58%

Heating3%

Cooling21%

Ventilation18%

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 12

Exhibit 3.4: Industrial SM Electricity Consumption (2005) – By Sector and End-Use

Level 1 Level 2 Level 3 Chemical Mfg.

Fabricated Metal Mfg.

Food Mfg.

Machinery Mfg.

Non-Metallic Mineral

Product Mfg.

Plastics & Rubber

Products Mfg.

Transportation Equipment Mfg.

Wood Product Mfg.

Boilers 0.5% 0.4% 0.6% 0.3% 0.5% 0.8% 0.5% 0.9%Furnace and Ovens 0.7% 4.5% 1.3% 3.5% 38.5% 6.0% 6.1% 0.0%Refrigeration / Chillers 0.2% 0.4% 41.7% 3.0% 2.1% 6.8% 4.5% 0.0%Cooling Tower 3.9% 0.9% 1.5% 0.5% 0.5% 0.8% 0.7% 0.9%

45.5% 40.5% 21.9% 34.0% 40.7% 61.2% 27.4% 20.1%27.4% 1.5% 5.4% 3.9% 0.9% 0.8% 10.3% 11.3%4.8% 9.6% 11.7% 14.6% 4.6% 6.2% 16.3% 11.7%3.9% 2.4% 2.0% 3.2% 2.1% 1.6% 7.1% 31.7%1.0% 0.2% 0.6% 0.3% 0.9% 0.8% 0.6% 10.5%3.6% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%2.9% 14.4% 7.0% 21.4% 1.6% 4.8% 9.9% 3.5%2.9% 19.0% 3.3% 9.1% 4.3% 4.8% 8.4% 4.6%0.0% 0.0% 0.2% 0.5% 0.0% 0.0% 1.5% 0.0%1.0% 4.1% 0.3% 2.6% 1.1% 4.0% 2.7% 4.7%1.2% 2.2% 2.5% 3.1% 2.1% 1.2% 4.0% 0.1%

CoolingVentilation

Comfort

MotorsPumpsAir CompressorsFans/BlowersConveyorsElectrochemicalOther ProcessLightingHeating

Electricity Consumption Profile (%)

Process

Direct Heat

Cooling

Electricity End-Use

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 13

3.2 REFERENCE CASE FORECAST The reference case is a forecast of the expected level of electricity consumption that would occur over the study period in the absence of new or incremental CDM market interventions by utilities and government in the SM industry sectors. The reference case is the point of comparison for the subsequent calculation of “economic” and “achievable” savings potentials in the industrial market.

The reference case forecast assumes that some level of “natural conservation” will occur over the study period. The scope and rate of natural conservation is driven by such factors as industrial plant growth and productivity improvements, energy prices and the availability and performance of energy management measures. Unfortunately, there is insufficient evidence to determine how each of these factors come into play in Ontario industry.

Utility and government forecasts generally assume some degree of a natural conservation effect in their forecasts. Consequently, it was decided to use the IESO forecast, specifically, the Medium growth rate scenario, which assumes some accountability of the natural conservation phenomenon. The Ontario SM industrial reference case is tuned to the IESO forecast.

In the absence of specific data on future industry output levels and type, it was further assumed that future output levels increased in approximate proportion to the increased levels of energy demand. Where data permitted, known future plant closures were taken into account. Hence, the base year market shares for each technology and fuel type within the model were, in effect, frozen for the study period.

Exhibit 3.5: Reference Case Forecast

REFERENCE CASE

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

2000 2005 2010 2015 2020 2025 2030

Year

Ener

gy C

onsu

mpt

ion

(GJ)

Reference Case

Average Growth Rate = 1% per annum

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 14

4. ECONOMIC ASSESSMENT OF CDM MEASURES This section presents the findings of the CDM measure economic performance for the Ontario SM industrial sector. In total, 52 CDM measures were assessed as a set of 17 CDM measure bundles, targeted to 9 electricity end-uses in each of 8 industrial sectors. 4.1 METHODOLOGY The method employed comprises the following steps: Identify Candidate Energy Efficiency Measures

An initial set of candidate measures were identified for inclusion in the study based on an extensive literature search, the consultants’ in-house database, and the experience of the project team.

Select Priority Measures by Energy End-Use

Given the large number of CDM measure options possible, only technologies applicable to energy end-uses with high potential for energy reductions were selected. The priority end-uses were selected with the aid of the following criteria:

Energy usage: How frequent, for what duration and in what quantity is energy used?

This consideration was based on the actual energy end-use allocation from plant data.

Potential for Efficiency Improvement: Does the currently installed technology represent a strong potential for improvement? For example, if a given end-use in the sector is largely represented by older stock, the opportunity may be greater than one in which newer technologies may already be in place.

Technology development: How active is the development of new technology for this end-use leading to energy performance improvements?

Profile the Technical Performance of Measures

In this step, the technical performance of the final candidate set of energy efficiency measures was established. The modelling construct used to analyse the measures established embodies four key dimensions: Differentiate According to Baseline and State-of-the-Art Technologies

Baseline Technology (BT): The baseline technology represents the baseline performance against which the CDM measure performance is calculated. The BT refers to the most common choice for equipment replacement. In other words, it is the predominant standard efficiency option in the marketplace.

State of the Art (SA): This category refers to the CDM measures that are more energy efficient than BT, are currently commercially available, but have low market penetration.

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 15

Differentiate According to End-of-Life and Retrofit Applications

The CDM measures are further categorized according to application at the time of normal stock turn-over, referred to as End-of-Life (EOL) or as a candidate for immediate replacement, referred to as “Retrofit Now”. The EOL CDM measures are costed on the basis of incremental costs (i.e., the difference between the installed costs of the BT and SA CSM measures). The retrofit-now CDM measures are costed at full cost.

Differentiate According to End-Use vs System Wide Applications

The energy efficiency measures were defined as either end-use level measures (such as motor replacements), or system-wide measures (such as plant balancing). This categorization determines whether or not the measure savings are applied to only the end-use energy allocation, or the energy consumption of the entire generic plant.

Establish Measure Bundles

The combination of a long measure list coupled with the range of industry sub-sectors means that there are lots of permutations to the CDM measure applications. To simplify the analysis, it was decided to create measure bundles comprising a logical grouping in terms of end-use and application. It is the measure bundles to which the TRC test is applied. It is assumed that the individual energy efficiency measures within a bundle would be applied in a logical sequence to account for how investment decisions are made and to reflect the technical performance interaction among measures. The sequencing was applied as follows: load management (right sizing), then control applications (on, off, variable frequency etc.), and finally, end-use equipment upgrades. Each subsequent measure within a bundle therefore acts on the residual energy after the implementation of the previous measure. The modelled roll-up of savings assumes no interaction of savings among measure bundles directed at one end-use. The savings for a given bundle is applied to the appropriate portion of the consumption of the generic plant.

Calculate the Demand Reduction Impact

The demand reduction impact of the energy efficiency measures was assessed using the average on-peak demand methodology employed in the TRC Guide. The reductions in electricity consumption during the winter and summer peak periods were divided by the number of hours in each period. As electricity consumption was allocated at close to 100 percent for both periods, the difference in average on-peak demand is negligible between summer and winter. As such, no differentiation is made and a single average on-peak demand reduction is reported. Average on-peak demand savings are first determined at the measure and measure bundle levels and appropriate cost savings for the summer peak period are included in the calculation of the TRC for each measure bundle. A composite demand reduction factor

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 16

that translates the consumption savings, equipment operating hours, and coincidence factor into the average on-peak demand savings is developed for each bundle. These factors are weighted and combined at the end-use level to derive the average on-peak demand savings by energy end-use. As with the consumption savings, the modelled roll-up of savings assumes no interaction of savings among measure bundles directed at one end-use.

Estimate Capital and Operating Cost of Measures The consulting team in-house data, supported by secondary research, was used to estimate the cost of implementing each CDM measure bundle. All cost information is in constant (2004) dollars.

Calculate the Total Resource Cost (TRC)

The key economic performance metric generated in the technology profiles is the Total Resource Cost (TRC). The Total Resource Cost is the net present value of the total of savings and costs accrued over the life of the energy management measure. An energy management measure passes the economic test and becomes a candidate for the economic potential scenario when the NPV is positive. The TRC method as described in the OEB Guide was used, with the following specific assumptions:

Discount rate is 6% real; The useful life of the measure bundle and all its component measures is assumed to

be the useful life of the longest-lived component measure; If a measure bundle passes the TRC test at full cost, it is implemented as an

immediate retrofit; and, Distribution and transmission losses are not accounted for in the savings component

of the TRC calculation as per the TRC Guide.

The analysis also generates two additional metrics, the Cost of Conserved Energy (CCE) and the simple payback. The CCE for an energy efficiency upgrade is defined as the annualized incremental cost of the upgrade measure divided by the annual energy savings achieved, excluding any administrative or program costs required to achieve full use of the technology or measure. The CCE is expressed as $/kWh or $/GJ saved and is compared against the long-run marginal cost of new energy supply. The simple payback is generated to show the measure from the customer’s financial perspective. Simple payback is “a measure of the length of time required for the cumulative savings from a project to recover its initial investment cost and other accrued costs, without taking into account the time value of money. The simple payback period is usually measured from the service date of the project.” 1 The cost of the measure (incremental or full, as appropriate) is divided by the expected annual savings that will result. The answer is usually given in years.

1 Sieglinde K. Fuller and Stephen R. Petersen. (1996). “Life Cycle Costing Manual for the Federal Energy Management Program”. National Institute of Standards and Technology Handbook 135, 1995 Edition, Washington, DC.

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 17

The following equation illustrates how this calculation is done, for a situation where an upgrade has a higher upfront cost than the baseline technology, but lower ongoing operating costs:

SPB = (CostUpgr – CostBase)/(AnnBase – AnnUpgr)

where: SPB = simple payback period of choosing the upgrade (years) CostUpgr = initial capital cost of the upgrade ($) CostBase = initial capital cost of the baseline technology ($) AnnUpgr = ongoing operating cost of the upgrade ($/year) AnnUpgr = ongoing operating cost of the upgrade ($/year)

4.2 CDM MEASURES Two sets of CDM bundles were included in this study: end-use measures, and system level measures. An overview of each set is presented below. 4.2.1 End-Use Measure Bundles

End-use measure bundles are measure applied directly to a given energy end-use such as motors, pumps, compressed air systems, etc. Note that although common measure bundles were defined (as presented below), each measure bundle was modified as appropriate in term of savings, operating times, implementation costs etc. to suite the generic plant type to which it was applied. The following end-use measure bundles were developed for this study: Motor Upgrade, Small, Medium & Large, both End-of-Life and Retrofit Now –

Depending on size, this measure bundle typically contains:

− Optimized premium efficient motor sizing − Synchronous belts − Variable speed drives

Pump Upgrade, Small, Medium & Large, both End-of-Life and Retrofit Now –

Depending on size, this measure bundle typically contains:

− Optimized, high efficient pump sizing − Synchronous belts − Variable speed drives

Fan/Blower Upgrade, Small, Medium & Large, both End-of-Life and Retrofit

Now – Depending on size, this measure bundle typically contains:

− Optimized, high efficient fan/blower sizing − Synchronous belts − Variable speed drives

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 18

Conveyor Upgrade, both End-of-Life and Retrofit Now – Depending on size, this

measure bundle typically contains:

− Optimized premium efficient motor sizing − Synchronous belts

Air Compressor Upgrade, both End-of-Life and Retrofit Now – Depending on size, this measure bundle typically contains: − Optimally sized, high efficient compressor − Air leaks and condensate traps repaired − Optimally sized and designed systems, including air receiver tanks − Variable speed drives

Refrigeration/Cooling Upgrade, both End-of-Life and Retrofit Now – Depending on size, this measure bundle typically contains: − Optimally sized, high efficient refrigeration/chiller systems − Lowering condensing temperature − Heat recovery − Optimized defrost cycle − Energy demand and supply balance

Furnace/oven Upgrade, both End-of-Life and Retrofit Now – Depending on size, this measure bundle typically contains: − Insulation − Heat recovery

Lighting System Upgrade, Retrofit Now – This measure bundle typically contains: − High efficiency lighting system with optimum lumens − Occupancy sensors and/or timed control system

HVAC System Upgrade, Retrofit Now – This measure bundle typically contains: − Optimally designed, high efficiency HVAC system

4.2.2 System Level Measure Bundles

System-level measure bundles are efficiency upgrade options that span several energy end-uses, and are therefore applied against the entire generic plant’s energy consumption. Each measure bundle was modified as appropriate in term of savings, operating times, implementation costs etc. to suite the generic plant type to which it was applied. Indeed, process improvement upgrades were defined specifically for the generic plant in question. The following system-level measure bundles were included in this study.

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 19

Control System Upgrade – Control system upgrades include digital controllers aimed at informing energy management and providing real-time demand management. They include:

− Sub-metering and interval metering − DMS system upgrades − Artificial intelligent based control

Energy and Mass Balancing – This bundle aims to apply advanced modelling and

analysis methods to improve productivity and throughput. This bundle typically includes:

− Vibration analysis of motors − Energy and mass balance modeling of process flows. − Process integration and/or Pinch analysis

Maintenance and Operating Improvements – Operating and maintenance

improvements were developed for each generic plant type in the study. These measure bundles includes training and strategies to create a corporate culture of energy conservation.

4.3 RESULTS The TRC and CCE tests are highly sensitive to several of the key assumptions in the analysis. In some cases, marginal measures might change from passing the TRC test to failing (or vice versa) based on a slight change in one of the assumptions. Sensitivity analysis was conducted to test the sensitivity of the analysis against key variables. In order to ensure that such marginal measures were identified, the following assumptions were varied: Avoided cost of electricity (5% lower, 5% higher, and 10% higher) Implementation cost of the measures (10% lower, 25% lower) Measure life (years).

Avoided cost and implementation cost were varied by the percentages specified above. CCE provided a useful guide to which measures required sensitivity testing: changes were observed only when the measure’s initial CCE was relatively close to the avoided cost of electricity. The results are shown in Exhibit 4.1.

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 20

Exhibit 4.1: TRC Summary

Level 1 Level 2 Level 3 Full Cost Incremental

CostTRC Net Benefit

TRC Pass / Fail Avoided Cost Discount Rate

Furnace/Oven Upgrade (Now) Chemical, Nonmetallic 140,000$ 679,361$ Pass Pass Pass 2.4 8$

Furnace/Oven Upgrade (Now) Fabricated, Machinery, Plastics, Transportation 100,000$ 194,559$ Pass Pass Pass 3.5 13$

Refrigeration/Cooling Upgrade (Now)Chemical, Fabricated, Machinery, Nonmetallic, Plastics, Transportation

79,000$ 108,323$ Pass Pass Pass 5.1 19$

Refrigeration/Cooling Upgrade (Now) Food 260,000$ 84,325$ Pass Pass Pass 9.9 20$ Small Motor Upgrade (Now) All sectors 2,733$ 2,509$ Pass Pass Pass 6.1 23$ Medium Motor Upgrade (Now) All sectors 24,150$ 246,903$ Pass Pass Pass 1.3 3$ Large Motor Upgrade (Now) All sectors 71,000$ 716,953$ Pass Pass Pass 1.4 4$ Small Pump Upgrade 1 (Now) All sectors 1,000$ 155-$ Fail Pass Fail 6.2 38$ Small Pump Upgrade 2 (Now) All sectors 400$ 671$ Pass Pass Pass 3.6 22$ Small Pump Upgrade (EOL) All sectors 1,200$ 3,686$ Pass Pass Pass 3.7 9$ Medium Pump Upgrade 1 (Now) All sectors 20,200$ 227,400$ Pass Pass Pass 1.2 3$ Medium Pump Upgrade 2 (Now) All sectors 23,500$ 244,996$ Pass Pass Pass 1.3 4$ Compressor Upgrade 1 (Now) All sectors 35,000$ 2,245$ Pass Pass Fail 9.9 34$ Compressor Upgrade 2 (Now) All sectors 12,000$ 14,259-$ Fail Fail Fail 24.9 105$ Small Fan/Blower Upgrade 1 (Now) All sectors 1,650$ 212$ Pass Pass Pass 10.0 33$ Small Fan/Blower Upgrade 2 (Now) All sectors 800$ 1,357-$ Fail Fail Fail 12.4 85$ Medium Fan/Blower Upgrade 1 (Now) All sectors 13,700$ 234,540$ Pass Pass Pass 0.8 2$ Medium Fan/Blower Upgrade 2 (Now) All sectors 17,000$ 252,774$ Pass Pass Pass 0.9 3$ Large Fan/Blower Upgrade (Now) All sectors 66,000$ 710,891$ Pass Pass Pass 1.3 4$ Conveyor Upgrade (Now) All sectors 1,300$ 654$ Pass Pass Pass 10.1 24$ Lighting Upgrades (Now) All sectors 120$ 11$ Pass Pass Pass 8.7 27$ HVAC (Now) All sectors 52,000$ 39,438-$ Fail Fail Fail 42.2 121$ HVAC (Now) All sectors 52,000$ 39,438-$ Fail Fail Fail 42.2 121$

ComfortLighting

Process

Furnaces

Chillers

Motors

Cooling

Pumps

Air Compressors

End-Use

Conveyers

Fans / Blowers

Direct Heat

Cooling Ventilation

CCE ($/GJ)Measure Bundle

TRC Sensitivity (Pass / Fail) Simple Payback (Years)

Core AnalysisApplicationSector Applicability

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 21

5. ECONOMIC POTENTIAL SCENARIO This section presents the economic potential forecast for the Ontario SM industrial sector over the study period (2005-2025). The economic potential forecast is the level of energy consumption that would occur if all industrial processes, equipment and buildings were upgraded with energy management measures that pass the TRC test. In other words, this is a scenario which reflects circumstances where a “rational” economic decision-maker is making energy management investments unimpeded by market barriers. Given the preponderance of market barriers, the boundary established by the economic potential forecast is an upset level that helps to frame the discussion on achievable potential. The discussion in this section is organized according to the following subsections: Methodology Summary of results Interpretation of results.

5.1 METHODOLOGY To develop the economic potential scenario, the following steps were undertaken:

The CDM measure TRC results for each of the energy management measures presented

previously were reviewed. Measures that had positive TRC results were selected for inclusion in the economic potential scenario, either on a “full cost” or “incremental” basis.

CDM measures passing the TRC test on a “full cost” basis were implemented in the first

forecast year. Those upgrades that only passed the TRC test on an “incremental” basis were introduced as the existing stock approached the end of its useful life (EOL).

Calculate energy consumption for the study milestone years when the efficiency

measures are employed. Compare the economic potential energy consumption levels with the reference case consumption levels and calculate the energy savings.

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 22

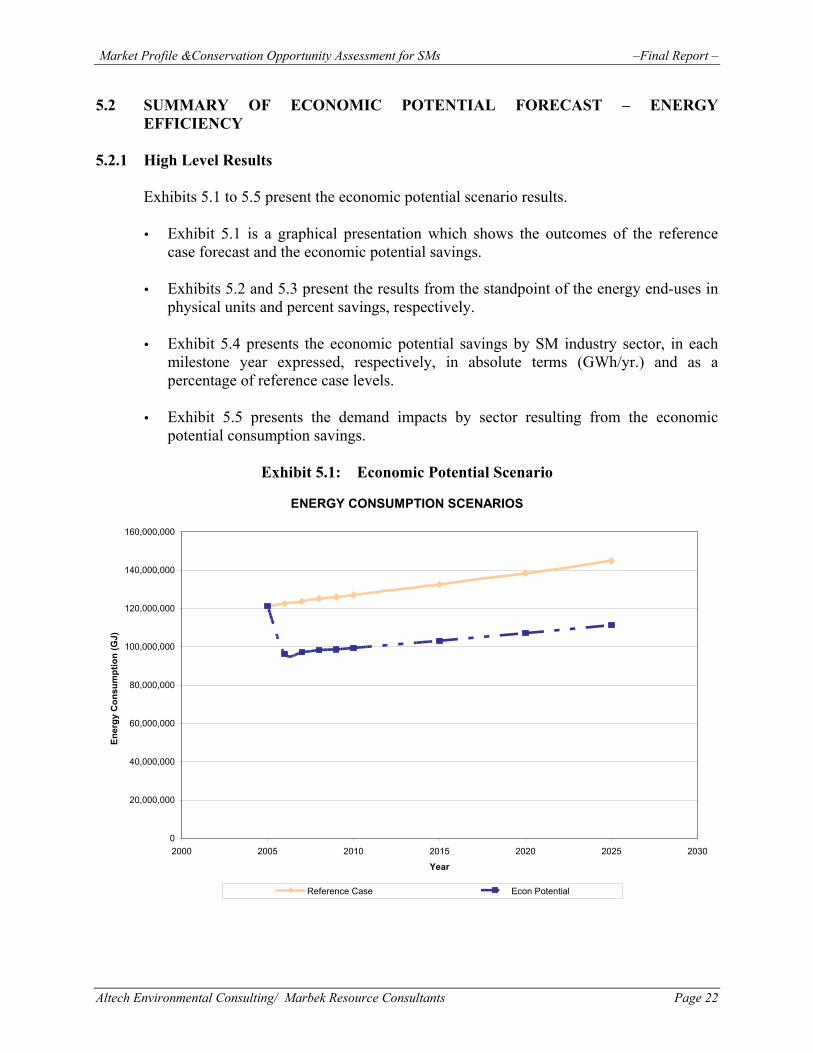

5.2 SUMMARY OF ECONOMIC POTENTIAL FORECAST – ENERGY EFFICIENCY

5.2.1 High Level Results

Exhibits 5.1 to 5.5 present the economic potential scenario results.

Exhibit 5.1 is a graphical presentation which shows the outcomes of the reference case forecast and the economic potential savings.

Exhibits 5.2 and 5.3 present the results from the standpoint of the energy end-uses in

physical units and percent savings, respectively.

Exhibit 5.4 presents the economic potential savings by SM industry sector, in each milestone year expressed, respectively, in absolute terms (GWh/yr.) and as a percentage of reference case levels.

Exhibit 5.5 presents the demand impacts by sector resulting from the economic

potential consumption savings.

Exhibit 5.1: Economic Potential Scenario

ENERGY CONSUMPTION SCENARIOS

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

2000 2005 2010 2015 2020 2025 2030

Year

Ener

gy C

onsu

mpt

ion

(GJ)

Reference Case Econ Potential

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 23

Exhibit 5.2: Economic Potential Savings by End-Use (GWh)

Level 1 Level 2 Level 3 2005 2006 2007 2008 2009 2010 2015 2020 2025Boilers 0 26 26 26 26 27 28 29 30Furnaces 0 525 530 537 540 545 568 594 621Chillers 0 692 698 707 711 717 748 782 817Forced Air Coolers 0 4 4 4 4 4 5 5 5Cooling Tower 0 66 67 68 68 69 72 75 78

0 2,464 2,505 2,554 2,585 2,625 2,831 3,053 3,2900 447 466 487 504 524 626 737 8560 1,165 1,177 1,191 1,198 1,209 1,261 1,318 1,3770 439 443 448 451 455 475 496 5180 130 131 133 134 135 141 148 1550 32 32 32 33 33 34 36 370 340 344 348 350 353 368 385 4020 717 724 733 737 743 776 811 8470 15 16 16 16 16 17 17 18

Cooling 0 111 112 113 114 115 120 125 1310 98 99 100 101 102 106 111 1160 7,271 7,373 7,498 7,572 7,671 8,176 8,722 9,300

ConveyersElectrochemicalOther Process

Comfort

TOTAL:

LightingHeating

Ventilation

End-Use Annual Energy Savings by Milestone Year (GWh)

Process

Direct Heat

Cooling

MotorsPumpsCompressorsFans/Blowers

Exhibit 5.3: Economic Potential Savings by End-Use (%)

Level 1 Level 2 Level 3 2005 2006 2007 2008 2009 2010 2015 2020 2025Boilers - 0.4% 0.4% 0.3% 0.3% 0.3% 0.3% 0.3% 0.3%Furnaces - 7% 7% 7% 7% 7% 7% 7% 7%Chillers - 10% 9% 9% 9% 9% 9% 9% 9%Forced Air Coolers - 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1% 0.1%Cooling Tower - 1% 1% 1% 1% 1% 1% 1% 1%

- 34% 34% 34% 34% 34% 35% 35% 35%- 6% 6% 6% 7% 7% 8% 8% 9%- 16% 16% 16% 16% 16% 15% 15% 15%- 6% 6% 6% 6% 6% 6% 6% 6%- 2% 2% 2% 2% 2% 2% 2% 2%- 0.4% 0.4% 0.4% 0.4% 0.4% 0.4% 0.4% 0.4%- 5% 5% 5% 5% 5% 5% 4% 4%- 10% 10% 10% 10% 10% 9% 9% 9%- 0.2% 0.2% 0.2% 0.2% 0.2% 0.2% 0.2% 0.2%- 2% 2% 2% 2% 1% 1% 1% 1%- 1% 1% 1% 1% 1% 1% 1% 1%

100% 100% 100% 100% 100% 100% 100% 100%

CompressorsFans/Blowers

Comfort

VentilationTOTAL:

Other ProcessLightingHeatingCooling

MotorsProcess

Direct Heat

Cooling

Pumps

End-Use

ConveyersElectrochemical

Percentage Annual Energy Savings by End-Use

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 24

Exhibit 5.4: Economic Potential Savings (GWh)

Year Base Year Consumption (GWh)

Reference Case Consumption (GWh)

Economic Potential Scenario Consumption (GWh) Savings (GWh) Savings as Percentage

of Reference Case

2005 33,693 33,693 33,693 0 0%2006 34,040 26,769 7,271 21%2007 34,366 26,993 7,373 21%2008 34,800 27,302 7,498 22%2009 34,995 27,423 7,572 22%2010 35,299 27,628 7,671 22%2015 36,840 28,664 8,176 22%2020 38,498 29,776 8,722 23%2025 40,231 30,930 9,300 23%

Exhibit 5.5: Demand Impacts of Economic Potential Savings (MW)

On-Peak Demand Savings by 2025 (MW)

0

500

1000

1500

2000

2500

Chemical Mfg. FabricatedMetal Mfg.

Food Mfg. MachineryMfg.

Non-MetallicMineral Prod.

Mfg.

Plastics &Rubber Mfg.

TransportationEquipment

Mfg.

Wood ProductMfg.

Total

Sectors

On-

Peak

Dem

and

(MW

The results show that, under the economic potential scenario, electricity consumption in 2025 would decline by about 23% relative to the Reference Case forecast. In absolute terms, this is a reduction in 2025 from 40,231 GWh to 30,930 GWH and a reduction of 2,084 MW. As shown, the savings are relatively flat from 2007 to the end of the study period. This is because most of the energy efficiency measures passed the TRC test at full cost and, consequently, were modelled to achieve full market penetration early in the forecast

The results also show which energy end-uses have the largest potential for savings.

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 25

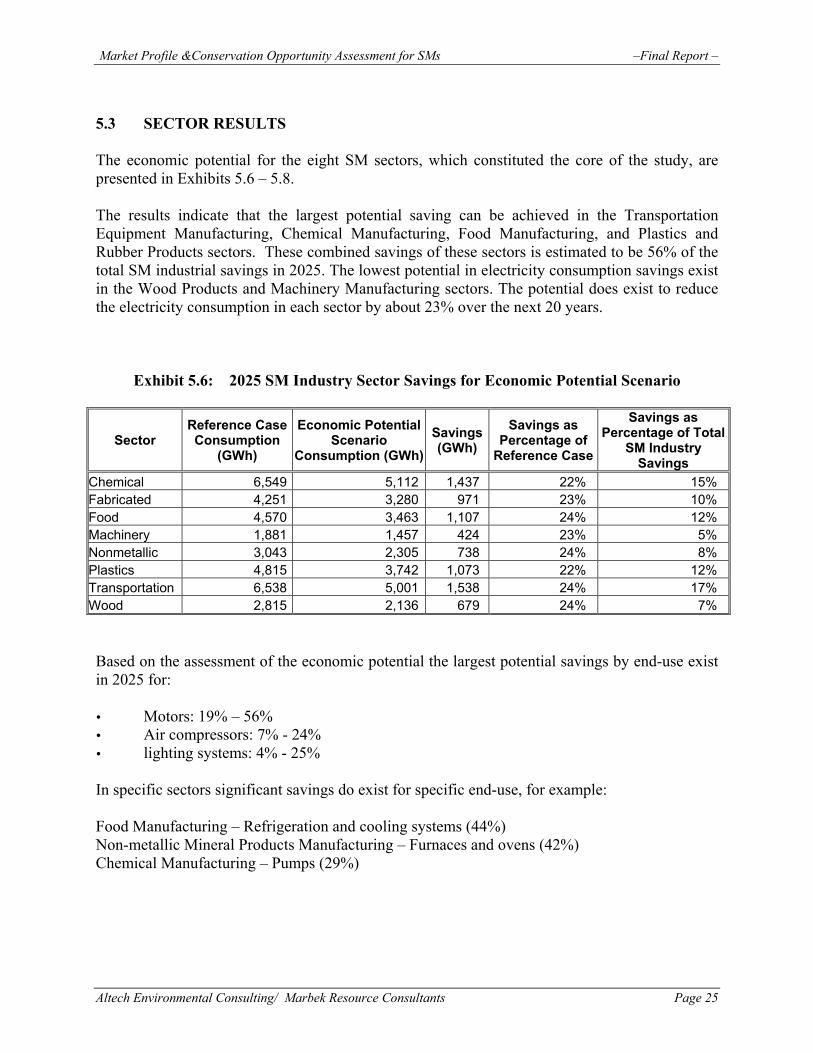

5.3 SECTOR RESULTS The economic potential for the eight SM sectors, which constituted the core of the study, are presented in Exhibits 5.6 – 5.8. The results indicate that the largest potential saving can be achieved in the Transportation Equipment Manufacturing, Chemical Manufacturing, Food Manufacturing, and Plastics and Rubber Products sectors. These combined savings of these sectors is estimated to be 56% of the total SM industrial savings in 2025. The lowest potential in electricity consumption savings exist in the Wood Products and Machinery Manufacturing sectors. The potential does exist to reduce the electricity consumption in each sector by about 23% over the next 20 years.

Exhibit 5.6: 2025 SM Industry Sector Savings for Economic Potential Scenario

Sector Reference Case Consumption

(GWh)

Economic Potential Scenario

Consumption (GWh)Savings (GWh)

Savings as Percentage of

Reference Case

Savings as Percentage of Total

SM Industry Savings

Chemical 6,549 5,112 1,437 22% 15% Fabricated 4,251 3,280 971 23% 10% Food 4,570 3,463 1,107 24% 12% Machinery 1,881 1,457 424 23% 5% Nonmetallic 3,043 2,305 738 24% 8% Plastics 4,815 3,742 1,073 22% 12% Transportation 6,538 5,001 1,538 24% 17% Wood 2,815 2,136 679 24% 7% Based on the assessment of the economic potential the largest potential savings by end-use exist in 2025 for: Motors: 19% – 56% Air compressors: 7% - 24% lighting systems: 4% - 25%

In specific sectors significant savings do exist for specific end-use, for example: Food Manufacturing – Refrigeration and cooling systems (44%) Non-metallic Mineral Products Manufacturing – Furnaces and ovens (42%) Chemical Manufacturing – Pumps (29%)

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 26

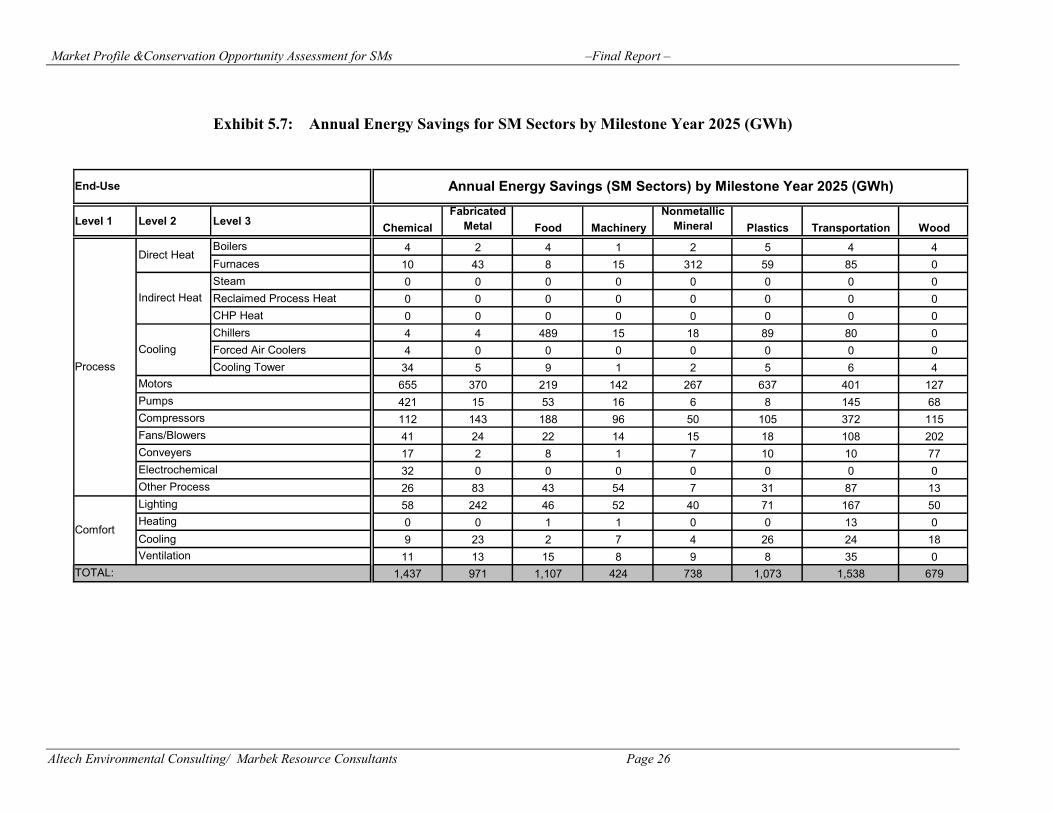

Exhibit 5.7: Annual Energy Savings for SM Sectors by Milestone Year 2025 (GWh)

Level 1 Level 2 Level 3 ChemicalFabricated

Metal Food MachineryNonmetallic

Mineral Plastics Transportation WoodBoilers 4 2 4 1 2 5 4 4Furnaces 10 43 8 15 312 59 85 0Steam 0 0 0 0 0 0 0 0Reclaimed Process Heat 0 0 0 0 0 0 0 0CHP Heat 0 0 0 0 0 0 0 0Chillers 4 4 489 15 18 89 80 0Forced Air Coolers 4 0 0 0 0 0 0 0Cooling Tower 34 5 9 1 2 5 6 4

655 370 219 142 267 637 401 127421 15 53 16 6 8 145 68112 143 188 96 50 105 372 11541 24 22 14 15 18 108 20217 2 8 1 7 10 10 7732 0 0 0 0 0 0 026 83 43 54 7 31 87 1358 242 46 52 40 71 167 500 0 1 1 0 0 13 0

Cooling 9 23 2 7 4 26 24 1811 13 15 8 9 8 35 0

1,437 971 1,107 424 738 1,073 1,538 679TOTAL:

ConveyersElectrochemicalOther Process

Comfort

LightingHeating

Ventilation

End-Use Annual Energy Savings (SM Sectors) by Milestone Year 2025 (GWh)

Process

Direct Heat

Indirect Heat

Cooling

MotorsPumpsCompressorsFans/Blowers

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 27

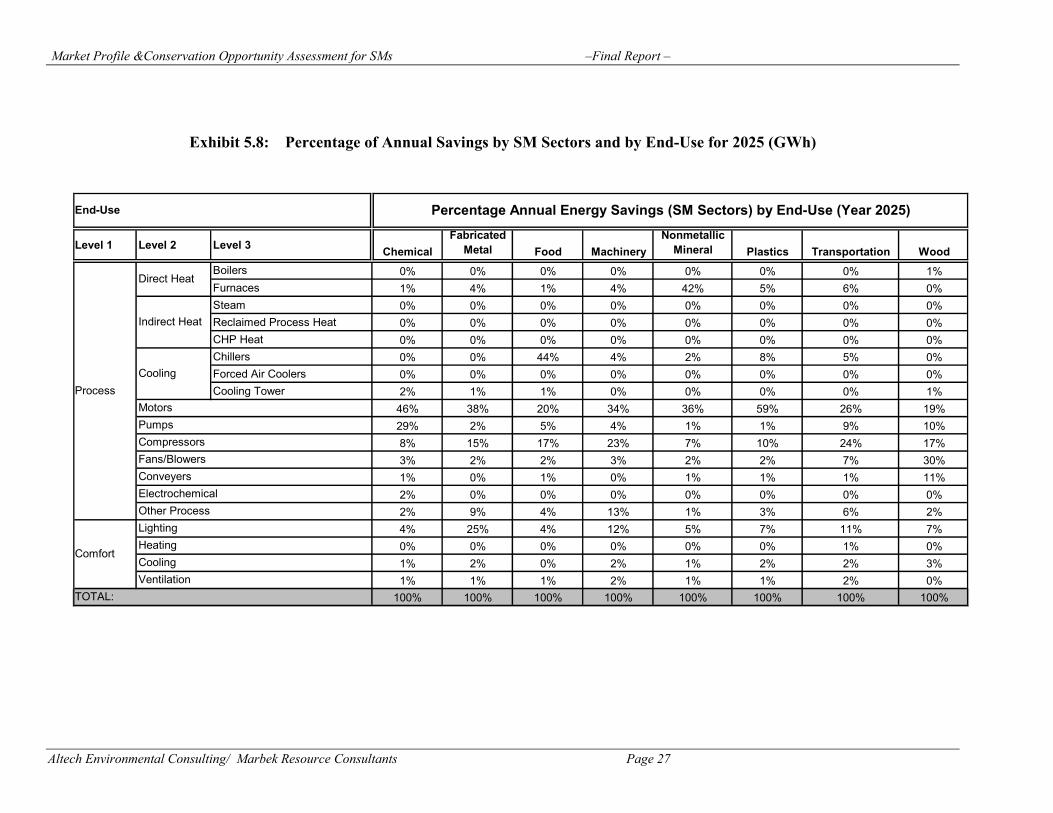

Exhibit 5.8: Percentage of Annual Savings by SM Sectors and by End-Use for 2025 (GWh)

Level 1 Level 2 Level 3 ChemicalFabricated

Metal Food MachineryNonmetallic

Mineral Plastics Transportation WoodBoilers 0% 0% 0% 0% 0% 0% 0% 1%Furnaces 1% 4% 1% 4% 42% 5% 6% 0%Steam 0% 0% 0% 0% 0% 0% 0% 0%Reclaimed Process Heat 0% 0% 0% 0% 0% 0% 0% 0%CHP Heat 0% 0% 0% 0% 0% 0% 0% 0%Chillers 0% 0% 44% 4% 2% 8% 5% 0%Forced Air Coolers 0% 0% 0% 0% 0% 0% 0% 0%Cooling Tower 2% 1% 1% 0% 0% 0% 0% 1%

46% 38% 20% 34% 36% 59% 26% 19%29% 2% 5% 4% 1% 1% 9% 10%8% 15% 17% 23% 7% 10% 24% 17%3% 2% 2% 3% 2% 2% 7% 30%1% 0% 1% 0% 1% 1% 1% 11%2% 0% 0% 0% 0% 0% 0% 0%2% 9% 4% 13% 1% 3% 6% 2%4% 25% 4% 12% 5% 7% 11% 7%0% 0% 0% 0% 0% 0% 1% 0%1% 2% 0% 2% 1% 2% 2% 3%1% 1% 1% 2% 1% 1% 2% 0%

100% 100% 100% 100% 100% 100% 100% 100%TOTAL:

Comfort

LightingHeatingCoolingVentilation

Fans/BlowersConveyersElectrochemicalOther Process

End-Use Percentage Annual Energy Savings (SM Sectors) by End-Use (Year 2025)

Process

Direct Heat

Indirect Heat

Cooling

MotorsPumpsCompressors

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 28

6. ONTARIO SM INDUSTRY SITUATION ASSESSMENT AND

PROGRAM CONCEPTS This section presents the results of the Ontario SM Industry Situation Assessment and also presents a preliminary suite of program concepts for consideration to achieve CDM take-up in this market. The method employed to generate these outputs comprised the following elements: Literature review LDC interviews California Utility Interviews

6.1 CDM PROGAMMING TARGETED TO THE SM INDUSTRY SECTORS This sub-section summarizes the current CDM programming targeted to the Ontario SM Industry sectors. The profile focuses primarily on the activities of the Local Distribution Companies (LDCs) that supply power in Ontario, supplemented by some information on activities by the provincial and federal governments. The LDC program review is based on their CDM plans and reports submitted to the OEB, as well as the interviews conducted for this assignment. The current LDC program suites are operating under the auspices of approval from the OEB to invest $ 163 million in CDM initiatives over a three-year period from March 1, 2005 to September 2007. The key findings are organized under the following topics: Overview of current LDC programming Program types Program development Program delivery Assessment and funding of programs Program deployment

6.1.1 Overview of Current LDC programming

At the present time, it’s evident that LDC programming is largely targeted to the residential and commercial sectors, and far less directed to industry. To understand this situation, it’s important to consider how the LDCs are segmented as far as SM industry reach as well as how some of the LDCs have coalesced under various alliances. There are 87 LDCs in Ontario, including Hydro One. However, a total of 37 LDCs service 97% of the SM industry market, making this group the focus for planned and potential programming. Moreover, 31 LDCs have come together under the auspices of three coalitions to design and deliver some CDM programs on a collaborative basis: the Coalition of Large Distributors, Cornerstone Hydro Electric Concepts, and Niagara Erie Public Power Alliance.

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 29

Exhibit 6.1 provides a summary of the planned and active CDM program activities under the auspices of the largest LDC alliances and LDCs servicing a significant portion of SM industrial sector. The first year of activity, 2005, was mainly used to develop and deploy programs, and consequently, CDM impact in SM industry in 2005 will not yield significant energy or demand savings.

Exhibit 6.1: LDC Conservation and Demand Management Programming 2005 – 2007

Program Description LDC Financial Incentives

Voluntary demand response Burlington Hydro CHED

Incentive to reduce peak demand CLD Load displacement (promotes alternative/renewable energy) CLD

CHED GHWED NEPPA

Load control program CLD GHWED Hydro One

Energy audits and projects CHED NEPPA

Co-generation pilot programs GHWED Training and Information

Energy efficiency showcase Burlington Hydro Education, outreach and promotions Burlington Hydro

CLD CHED GHWED Hydro One

Interval metering CLD CHED Hydro One NEPPA

Building design advisory program CLD Support – e.g. conference, website, newsletter, staff training. CLD

CHED Billing practice CHED Customer survey and market research CHED Technology and program research and demonstration GHWED

Hydro One Delivery Infrastructure

Leveraging energy conservation and/or load management programs delivered by government or gas utilities

CLD CHED NEPPA

On-the-bill financing (pilot program) CLD Rate Design

Time-of-use rate (pilot program) Hydro One CLD: Coalition of Large Distributors CHEC: Cornerstone Hydro Electric Concepts GHWED: Guelph Hydro and Wellington Electric Distribution Hydro One: Hydro One Networks and Hydro One Brampton NEPPA: Niagara Erie Public Power Alliance

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 30

See Appendix A for a list of LDCs in each alliance/coalition Based on the program reviews and the LDC interviews, the following observations emerge: 6.1.2 Program Types:

Incentive Based Prescriptive and Custom Based Programs With a few exceptions, the business model exemplified by the “powerWISE Business Incentives Program (PBIP), is currently the most common suite of incentive based programming targeted to SM industry. PBIP has two streams: prescriptive and performance. The prescriptive stream offers incentives for specific end-use products, most commonly: High and Premium Efficiency Fluorescent T8 Lighting Fixtures and ENERGY

STAR® LED Exit Signs 3-phase Premium Efficiency Motors up to 200 hp ENERGY STAR® compliant 3-phase Transformers ENERGY STAR® compliant Unitary Air-Conditioning up to 20 tons in size

The custom stream offers an incentive for a given unit of energy saving (kWh) or demand reduction (kW reduction). Most incentive based activities in Ontario are structured on this basis. Given the energy use and economic potential profile for the SM industry sectors, the targeting of 3-phase premium efficiency motors is a good fit. The other products are more suited to the comfort, non-process end-uses in SM industry, particularly, lighting and air conditioning. The custom incentive stream allows for process based CDM measures but apparently, there has been little take-up among SM industry of these types of investments. Information and Training

Within the category of information and training, there are 8 program types in action at the moment and the 3 most widely used are discussed below. Energy audits as a platform for inducing customer CDM investments Some of the other LDCs have funded energy audits, on an ad hoc basis, if a particular situation arises where they will help to induce CDM investments. On the other hand, Hydro ONE has piloted an energy audit program using the Envinta “ONE-TO-FIVE” concept. Although the pilot is targeted to customers with load of 2 MW and up, the concept, in one form or another, could be designed for smaller industry customers. The difference between the Hydro ONE and powerWISE model is that it is more focused to market transformation, inducing corporate culture changes in a step-wise approach. Hence, to date Hydro ONE has completed 1 initial audits and 3 of the 11 customers are moving forward to the next stage of energy management planning and project development.

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 31

On-Line Information Services Utilities are offering diverse data management services to SM industry customers online to which typically fall into the following categories: Access to consumption data: A number of standard reporting templates are

available, for cost management enabling comparisons of energy consumption at individual or multiple sites. The data can be supplied at different intervals.

Advisory services: utilities offer automated advisory services or have technical

staff available to help customers optimize their energy usage and manage the costs more effectively. The service offerings vary and can include: i) troubleshooting, referred to as “exception and performance” reports that help identify and manage any potential energy management issues, ii) solutions, whereby energy reports are interpreted at varying levels of sophistication leading to proposed O&M and capital improvements.

Toronto Hydro Energy Services offers an Energy Profiling service which, among other things, enables staff to access utility data and reports to identify costly consumption trends or problems with equipment and project utility costs. The service offers “Energy and Cost” alarms to alert the customer when energy consumption, demand or the next hour's electricity price is projected to go above a set threshold so that steps can be taken to contain costs. Interval Metering The Coalition of Large Distributors are supporting the Minister of Energy’s commitment to increase the installation of SMART meters in the province by 2007 by supporting the installation of interval metering in commercial, institutional and industrial facilities. Support mechanisms include the mandatory installation of interval meters for all customers with a peak demand of greater than 200kW (e.g., Veridian), pilot installations of interval meters (e.g., PowerStream, Toronto Hydro, Hamilton Utilities) and testing of various SMART metering communication technologies (e.g., Hydro Ottawa). The SMART meters provide customers with the option of tracking load profiles and consumption to better manage energy usage and demand. Coalition members plan to facilitate wider penetration of interval metering in all sectors, including industry, and to move beyond the pilot phase in the near future.

6.1.3 Program Delivery – Delivery Channels, Roles and Responsibilities

Partnerships and alliances play and important role in developing and deploying programs. Although multi-party programs are viewed as highly desirable they are also much more complex and time consuming in terms of legal issues, administration and verification of results. There are a number of partnerships and alliances that can be beneficial:

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 32

Alliances between LDCs are deemed invaluable. Especially smaller LDCs lack resources to develop and implement CDM programs. These LDCs have to balance the cost of developing skills internally versus contracting outside sources, and managing time of human resources to provide operational services versus developing and implementing CDM programs. The main advantages of LDC alliances are reported to be sharing of knowledge and resources, efficiency, cost effectiveness and leveraging market reach and market penetration.

Partnerships with organization, contractors, manufacturers and retailers that

have experience with targeted technologies and/or targeted customers incorporate existing skills, knowledge and delivery channels.

Using expertise in the energy field, e.g. universities and consultants, can help

to develop specific initiatives and assessment tools that provide a basis for sound decisions.

To ensure program delivery is efficient, readily available and understood by all

customers it is important that the there is coordination amongst the many organizations in the energy industry. The main goal should be a rapid program deployment through the LDCs’ direct channel to the market. Most customers do not understand the relationship amongst the various organizations in the hydro industry, and an attempt to deliver programs to the end customer by different groups confuses customers and creates the impression of an uncoordinated energy industry. It would be beneficial to clearly define the roles of the LDCs, Conservation Bureau (OPA), IESO, EDA, etc.

Government and the OPA should address the areas that utilities cannot address,

for example codes, standards and broader policies. In defining the role of the Conservation Bureau (CB) and the LDCs, programs with direct interaction with customers should be the role of LDCs and the CB (OPA) should not duplicate the efforts of the LDCs, which is currently the case in the residential sector with, for example, the coupon program.

LDCs believe they are well positioned to deliver programs to the communities

they represent and have resources and expertise in conservation and demand management measures. However, typical concerns by LDCs include efficacy of measures, consistency of conservation message, communication, value for investment and economies of scale. Many utilities have not increased internal resources to address the CDM portfolio. Recognition of the impact of continued CDM programming has on resources is required in both the funding and reporting requirements.

6.1.4 Program Development

CDM program development and capacity building takes time. To ensure long-term sustainable conservation success it is necessary to thoroughly address legal and environmental issues up front. Developing programs too fast and in an uncoordinated fashion may jeopardize the success of the programs.

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 33

It is recommended to give greater priority to programs designed to reduce both

base load and peak load consumption, and programs that improve the load shape, i.e. programs that flatten the load shape and improve the load factor. These programs are capable of delivering energy reduction and demand reduction benefits year round and not necessarily in a season, and provide system operators with enhanced operational flexibility.

To enhance the efficiency of programs it is recommended that administrative

reporting efforts should be streamlined where possible. If, for example, certain conservation programs have already proven to be effective, then the verification efforts required to substantiate these programs at their conclusions should be minimized.

Many customers do not consider electricity a significant factor input cost, and

industrial customer timelines for conservation projects are often longer and appear to have a lower sense of urgency then what the LDCs expected. To encourage and speed up conservation projects incentives have to be very meaningful and demonstrate a reasonably short payback period arising from a program that does not conflict with or disrupt their core business.

Some utilities reported that incentives for energy audits and feasibility studies

created an opportunity for customers to recognize the potential energy savings and advance plans for implementing solutions or measures. Other utilities reported a low success rate with energy audits and feasibility studies due to no measurable kW/kWh savings, and plan to discontinue the programs.

6.1.5 Assessment and Funding of Programs

The TRC model is seen to encourage “quick return” programs and does not provide any measure of foundation or education programs, which are critical in developing a “conservation culture”. Without savings results recognized for these activities it effectively penalizes utilities for participating in these initiatives. Recommendations made by LDCs relevant to the TRC model include:

The TRC tool needs to be expanded to take into account education and

foundation type programs. For education programs mechanisms for obtaining feedback from customers is required.

For cost effective evaluations the OEB needs to continue to refine and add to

the list of assumptions, and reflect new and emerging technologies.

Measures of programs need to be understood and clearly defined at the program design stage.

Environmental benefits, like reduction in greenhouse gas emissions, should be

added to the model.

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 34

LDCs require additional clarifications on the topics of LDC cost recovery, lost revenues and criteria for assessing prudence of CDM spending. These clarifications will lead to more aggressive applications for second generation funding.

Measuring the effectiveness of a program is challenging. It requires follow up

with the client to ensure implementation, and in most instances monitoring and tracking capabilities are not in place.

A clearly defined, practical funding framework needs to be developed and

implemented, to ensure the progress in developing and implementing CDM programs are sustained past 2007. The framework should be simplistic with minimal administrative and regulatory burdens.

6.1.6 Program Deployment

Conservation opportunities exist with small industrial customers, but the marketing channel faces many challenges. These customers lack the appropriate tools or models to accurately assess their options to implement solutions, and are overwhelmed by market information.

With the emergence of new technologies and many new service providers it is

important to offer industrial customers access to information through convenient forums such as trade shows or workshops. There is a need for customers to understand the new technologies, and the impact and value these technologies can have on their specific operations. A better understanding will potentially increase participation and adoption of new energy efficient technologies.

Pilot programs or staged rollouts of new and emerging technologies, or new and

high risk applications in the marketplace, are an important step in deploying programs.

To allow the implementation of commercial programs across jurisdictions and

beyond individual stores, the needs of customers, manufacturers and retailers must be address at the corporate, municipal, provincial and national level. Effective and efficient coordination is required to allow corporations to make programs available at all store locations regardless of location by city. Large areas with low population density are a difficult and less attractive market for retailers, suppliers and other partners.

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 35

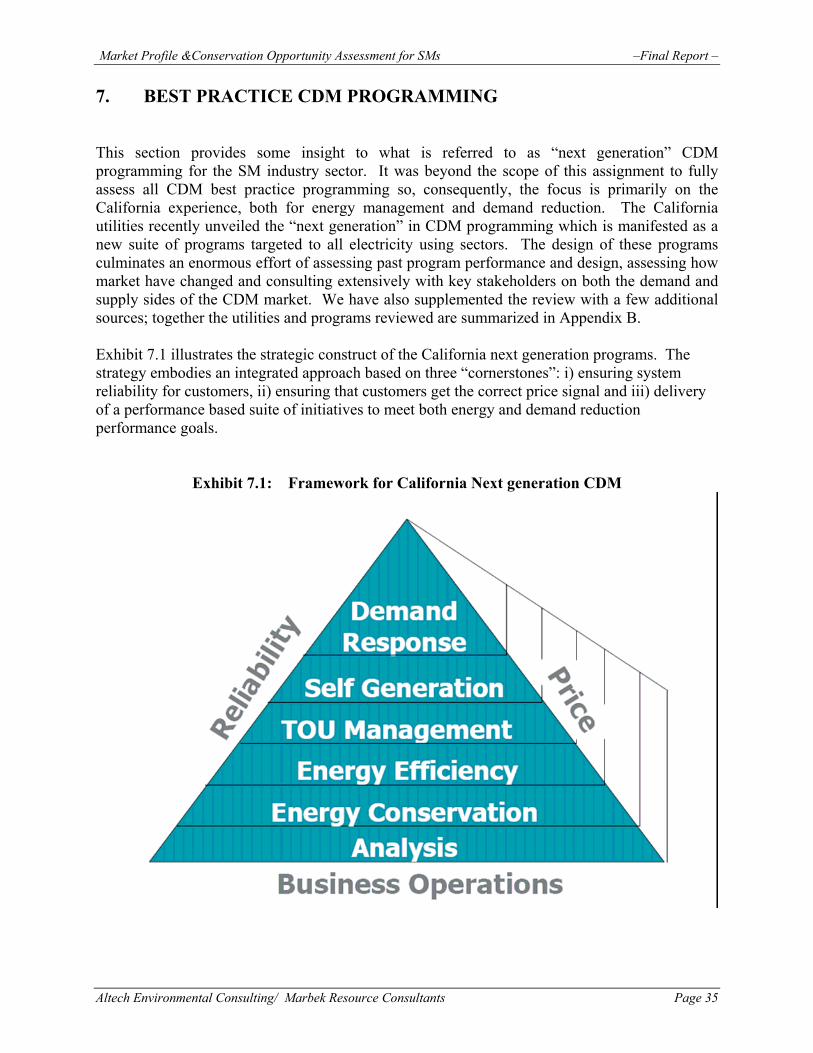

7. BEST PRACTICE CDM PROGRAMMING This section provides some insight to what is referred to as “next generation” CDM programming for the SM industry sector. It was beyond the scope of this assignment to fully assess all CDM best practice programming so, consequently, the focus is primarily on the California experience, both for energy management and demand reduction. The California utilities recently unveiled the “next generation” in CDM programming which is manifested as a new suite of programs targeted to all electricity using sectors. The design of these programs culminates an enormous effort of assessing past program performance and design, assessing how market have changed and consulting extensively with key stakeholders on both the demand and supply sides of the CDM market. We have also supplemented the review with a few additional sources; together the utilities and programs reviewed are summarized in Appendix B. Exhibit 7.1 illustrates the strategic construct of the California next generation programs. The strategy embodies an integrated approach based on three “cornerstones”: i) ensuring system reliability for customers, ii) ensuring that customers get the correct price signal and iii) delivery of a performance based suite of initiatives to meet both energy and demand reduction performance goals.

Exhibit 7.1: Framework for California Next generation CDM

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 36

SM industry managers in some of the leading California utilities were asked to discuss the strategic thinking behind the formulation of the new portfolios for the SM Industry sectors and to comment on how previous program experience had led them to the program suite being offered at the present time. The key findings are summarized below. 7.1 UNDERLYING STRATEGIC ELEMENTS The key strategic approaches noted by the Californian utilities which are currently being used are summarized below. These approaches are largely based on the lessons learned from past programs, as well as the energy reduction goals imposed on the utilities by the Californian Public Utilities Commission. As elaborated below, the strategies being considered are not radical in comparison to the past CDM experience, but rather, represent further refinements and tuning of approaches that, to date, have achieved considerable success. Focus on selling the high level concept – This a philosophical adjustment from previous approaches, in that the primary emphasis is placed on selling the concept of energy efficiency to the customer first, i.e., making the business case for CDM investment. Upon this platform, the various program rebates/incentives are made available to suit the target markets and products. A focus on selling the idea that customers can help California in minimizing power outages by committing to being more energy efficient has resulted in a better reception and participation in programs from industry, than simply selling the rebate. This is akin to the efforts in Ontario to foster the “Conservation Culture”. Shift to upstream/midstream players – In the past, a strong focus was placed primarily on paying rebates and incentives to downstream customers. While the current suite of programs still contains some incentives based initiatives for customers, so-called upstream and midstream players (manufacturer and distributor) have also been included in the mix. A strategic shift to provide incentives to the upstream/midstream market is aimed at a change in the equipment stocking situation, where higher efficiency equipment will be more readily available for customers “off the shelf”. Previously, this equipment would have been a “specialty” order, creating a barrier to the uptake of more efficient equipment. This strategic shift has already been initiated with the result, in some cases, that some distributors now only carry 100% premium efficiency equipment. In addition, by providing the incentives to the distributor/contractor, the utility is able to capture the planned equipment upgrades as well as the emergency situation upgrades. Previously, if there was an emergency equipment replacement needed, a customer would typically only have access to standard equipment available off the shelf. It was noted that the shift to upstream/midstream players can result in some customer complaints because the subsidy might not be passed on to the customer. This situation could be alleviated either through a mandated requirement or as competition increases and other distributors provide rebates and customers start to shop around for competitive pricing. Third-party implementers – The use of third-party specialists who can “talk the talk” of specific industrial sectors, is strategically used to achieve credibility with industrial customers. This allows the utility to offer a more customized benefit to customers, rather than relying solely on internal utility account executives who may not have the in-depth knowledge of a particular industry. Through a Request for Proposal process, specialists are screened by the utility to ensure they have the necessary industry specific expertise and understanding of energy

Market Profile &Conservation Opportunity Assessment for SMs –Final Report –

Altech Environmental Consulting/ Marbek Resource Consultants Page 37